The free-money hangover is getting worked off.

By Wolf Richter for WOLF STREET.

During the Free-Money era, credit card delinquency rates had dropped to record super-low levels. But when the free money ended, delinquency rates rose out of that trough, and overshot a little but still remained relatively moderate within the 25-year context of the data. And then, two years ago, the free-money hangover started to get worked off, and delinquency rates started declining again, and the trend has continued.

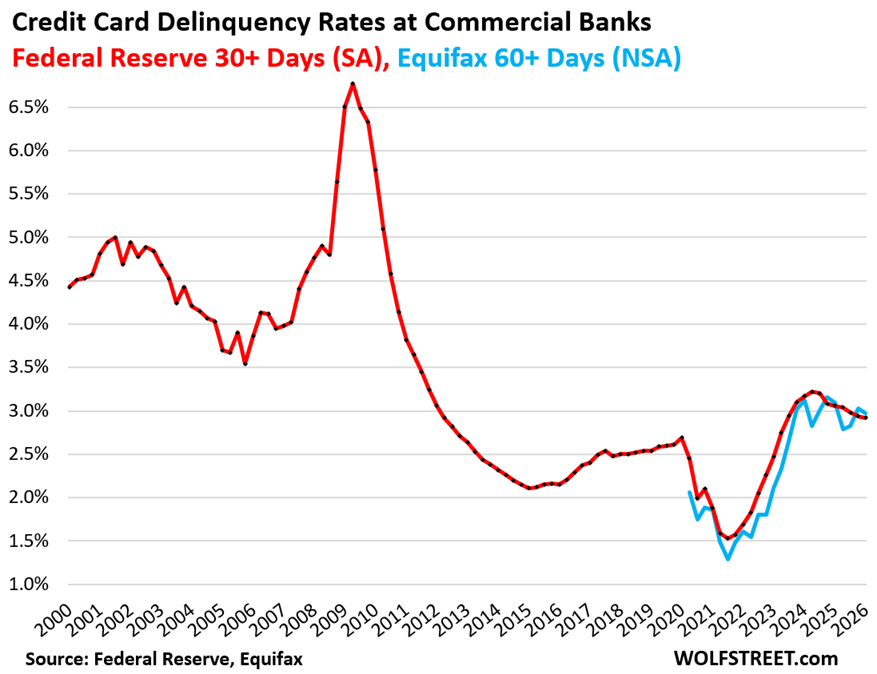

The 30-plus days delinquency rate on credit cards issued by all commercial banks declined to 2.92% in Q1, seasonally adjusted (SA, red in the chart), the lowest since Q2 2023, and down from 3.06% a year ago, and from 3.17% two years ago, according to the Federal Reserve, based on regulatory reports filed by all commercial banks. This includes credit cards by subprime-rated cardholders.

The 60-plus days delinquency rate by all credit cards, including private label credit cards (such as store cards), and subprime credit cards, declined to 2.97%, not seasonally adjusted, at the end of Q1, down from 3.09% a year ago, and down from 3.12% two years ago, according to Equifax whose data only goes back to June 2020 (NSA, blue line).

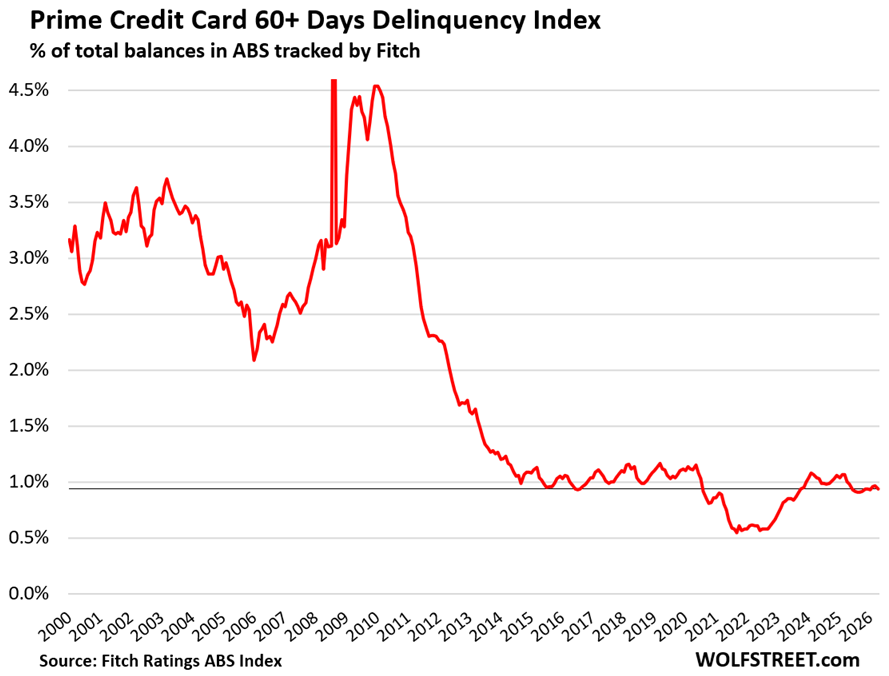

For prime-rated cardholders, the 60-plus days delinquency rate dipped to 0.94%, according to data from Fitch Ratings, which tracks the performance of Asset Backed Securities (ABS) backed by prime credit card balances.

The rate is below the low points before the pandemic and has been in this range for about a year, after coming down from the free-money hangover in the two years before, when it had gone as high as 1.07%, which was still lower than the highs in the Good Times years of 2017-2019.

Credit card balances: a measure of spending, not of borrowing.

Credit card balances are statement balances before payments are made. They’re a measure of spending, not a measure of borrowing. Most of these charges get paid off every month by due date and never accrue interest.

Over $5 trillion get paid for via credit cards every year. Credit cards are the dominant consumer payments method, largely replacing checks and cash. Debit cards are the second most popular payment method. Watchers of the economy keep an eye on credit card balances as an indication of consumer spending growth.

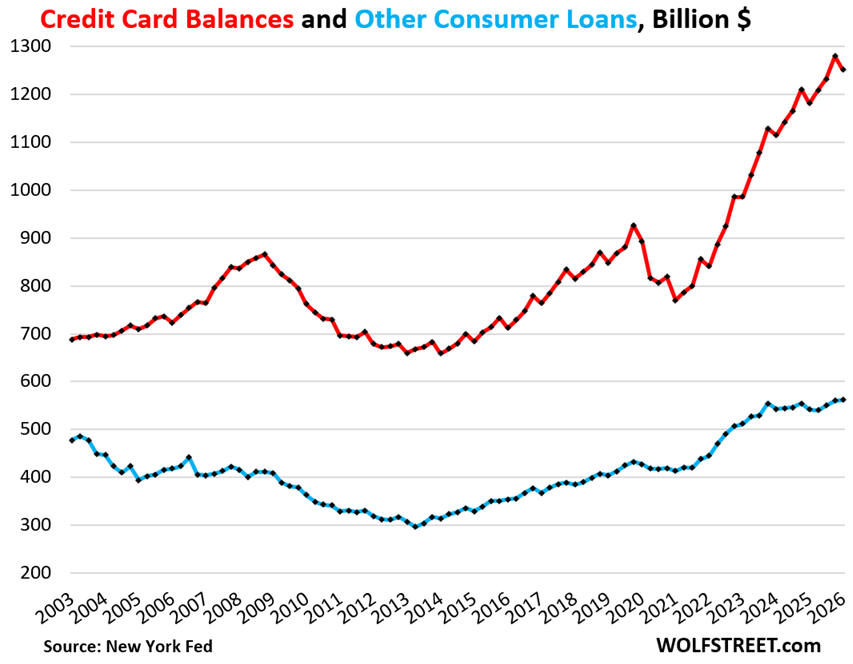

Credit card balances (red line in the chart below) dipped by $28 billion (-2.2%) in Q1 from Q4 – along seasonal trends after the holiday spending spree in Q4 – to $1.25 trillion, according to data from the New York Fed’s Household Debt and Credit report based on Equifax data.

Year-over-year, credit card balances rose by $70 billion, or by 5.9%, on growth in consumer spending and price increases. The data confirms that spending growth was solid but not spectacular.

“Other” consumer loans including BNPL (blue line) was essentially unchanged in Q1 from Q4 and rose by 3.7% year-over-year, roughly in line with inflation, to $562 billion.

This category includes personal loans, Buy-Now-Pay-Later (BNPL) loans, payday loans, etc., and many of these balances, except current BNPL balances, accrue interest.

What’s astonishing is that these other consumer loans have barely risen over the past 23 years, despite population growth, income growth, spending growth, 83% CPI inflation, and the arrival of BNPL loans.

The revolving-credit-to-income ratio.

Credit card balances (red in the chart above) and “other” consumer debt (blue above) combined – so total revolving consumer credit – dipped in Q1 from Q4 by 26 billion to $1.81 trillion. The dip was in line with seasonal patterns. Year-over-year, revolving consumer credit rose by 5.2%.

The debt-to-income ratio is a classic way of evaluating the burden of a debt. With households, we can use the debt-to-disposable-income ratio.

Disposable income (Bureau of Economic Analysis) consists of after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.

But it excludes capital gains, which is where the wealthy make most of their money. Excluded are thereby income from stock-based compensation plans and capital appreciation where billionaires make their billions.

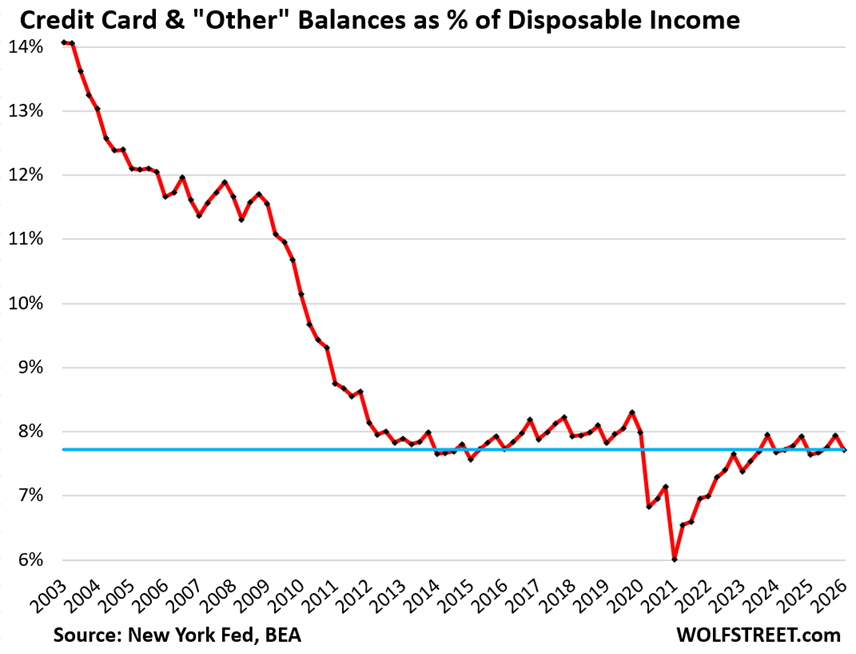

The ratio of revolving credit balances to disposable income in Q1 dipped to 7.72%, below where it had been during the Good Times before the pandemic.

During the pandemic, the ratio plunged as credit card balances dropped because travel, eating out, drinking out, and other activities were curtailed, and people couldn’t use their credit cards for them, while disposable income shot up amid an absurd flow of government payments directly to consumers.

The ratio emerged from that trough in 2022 but has remained below where it had been in the years before the pandemic and is very low in a 23-year context.

Before the Financial Crisis, Americans really did have a lot of credit card debt in relationship to their incomes, which caused some havoc during the unemployment crisis that followed. But that’s not the case now.

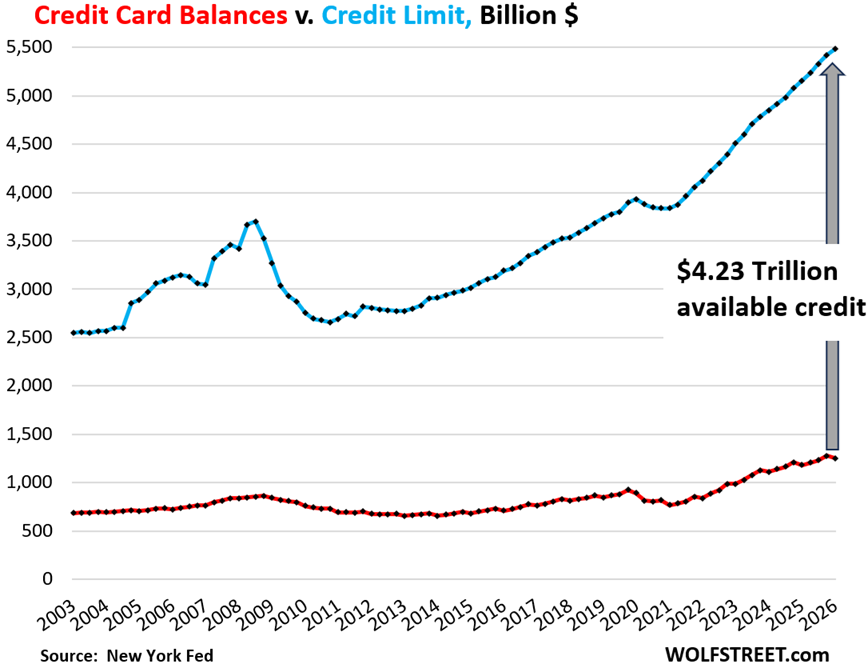

Unused credit rises to a record.

Banks make money on the swipe fees they earn every time a customer uses their credit card to pay. The merchant pays the swipe fees. So banks and their affiliate partners, such as airlines, are trying aggressively to get people to set up new credit card accounts, and they offer kickbacks to their customers to use the card, such as 1% or 2% cash-back or miles or whatever.

In addition, banks make large amounts of money on the annual fees they charge for some of their credit cards, and some of these fixed fees can be hundreds of dollars per year.

And it works, as Americans keep opening new accounts including for premium cards with high annual fees.

In addition, banks increased credit limits on some existing cards to encourage more spending and more swipe fees.

And it shows: The aggregate credit limit rose by $60 billion in Q1 from Q4, to a record $5.5 trillion (blue in the chart below), outgrowing balances which dipped by $28 billion over the same period (red).

And the available unused credit — the difference between the two — has soared from record to record, and in Q1 reached $4.23 trillion (gray arrow). So Americans are “maxed out on their credit cards?”

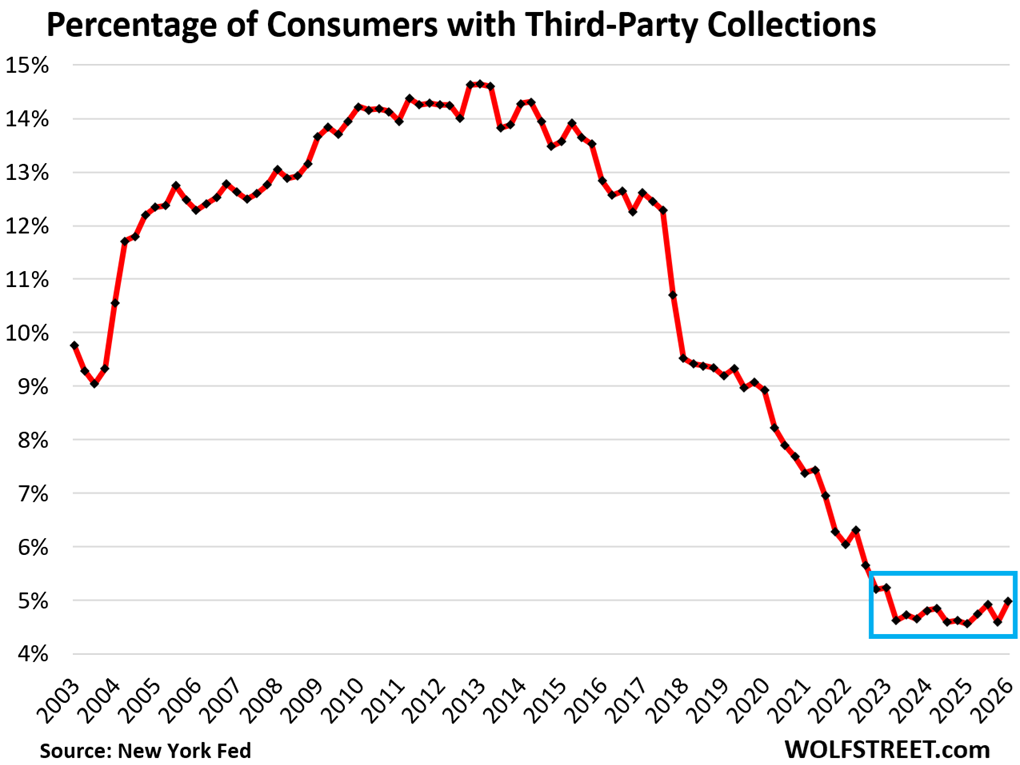

Third-party collections wobble along at record lows.

A third-party collection entry is made into a consumer’s credit history when the lender reports to the credit bureaus, such as Equifax, that it sold the delinquent loan, such as credit card debt, to a collection agency for cents on the dollar. At that point, the bank washes its hands off it. The New York Fed obtained this third-party collections data through its partnership with Equifax.

The percentage of consumers with third-party collection entries on their credit reports has been creeping along rock bottom for over three years, in the 5% range, down from 14% after the employment crisis that came with the Great Recession. Large-scale job losses eventually lead to large waves of hopelessly delinquent credit card debt getting sent to collection agencies.

In case you missed it, this rounds off my four-part quarterly analysis of consumer debt and credit:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()