March was a lousy beginning of spring selling season. But mortgage rates ticked up only modestly.

By Wolf Richter for WOLF STREET.

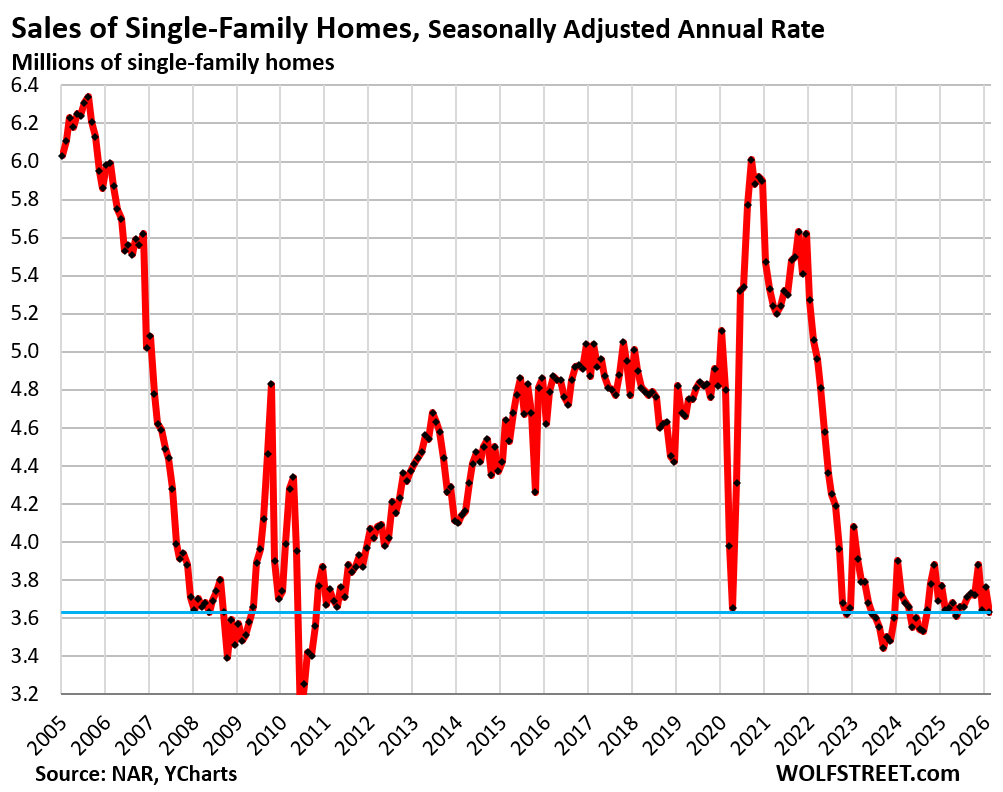

Sales of existing single-family homes that closed in March fell seasonally adjusted by 3.5% from February, to an annual rate of 3.63 million sales, the lowest since June 2025, and before then since September 2024, according to data by the National Association of Realtors today. It was four years ago, in March 2022 as mortgage rates began rising from suppressed levels, that home sales began to plunge and a few months later ended up in the deepfreeze, where they’re still today.

Compared to March in (historical data from YCharts):

- 2025: -0.3% (year-over-year)

- 2024: -2.4%

- 2023: -7.2%

- 2022: -28.3%

- 2021: -31.9%

- 2019: -22.4%

- 2015: -21.8%

- 1996: -4.7%

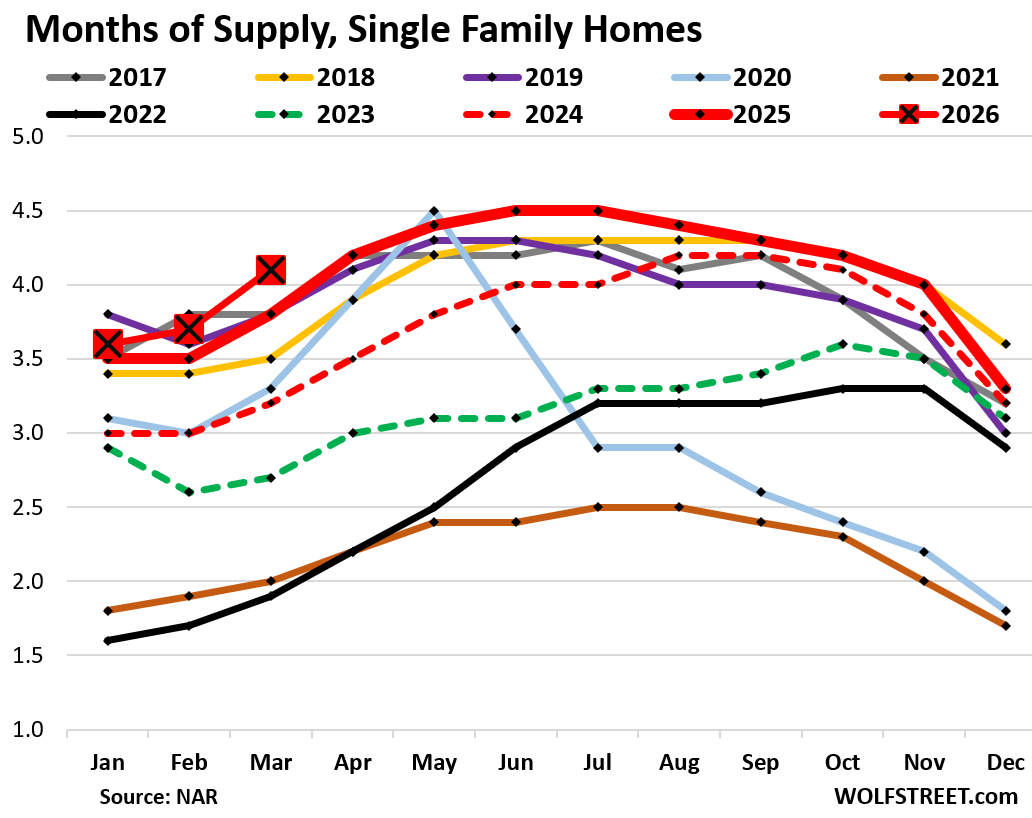

Supply of single-family homes jumped to 4.1 months in March (red line with big red squares in the chart below), the highest supply for March since 2015.

Supply is a function of sales (demand) and inventory. Inventory in a vacuum doesn’t matter that much; what matters is how much inventory there is in relationship to sales, and sales have plunged, which drives up the ratio of months’ supply.

Supply in 2025 had marked the high end for supply in the time range going back through 2016. And in 2026 so far, supply is even higher (historical data from YCharts).

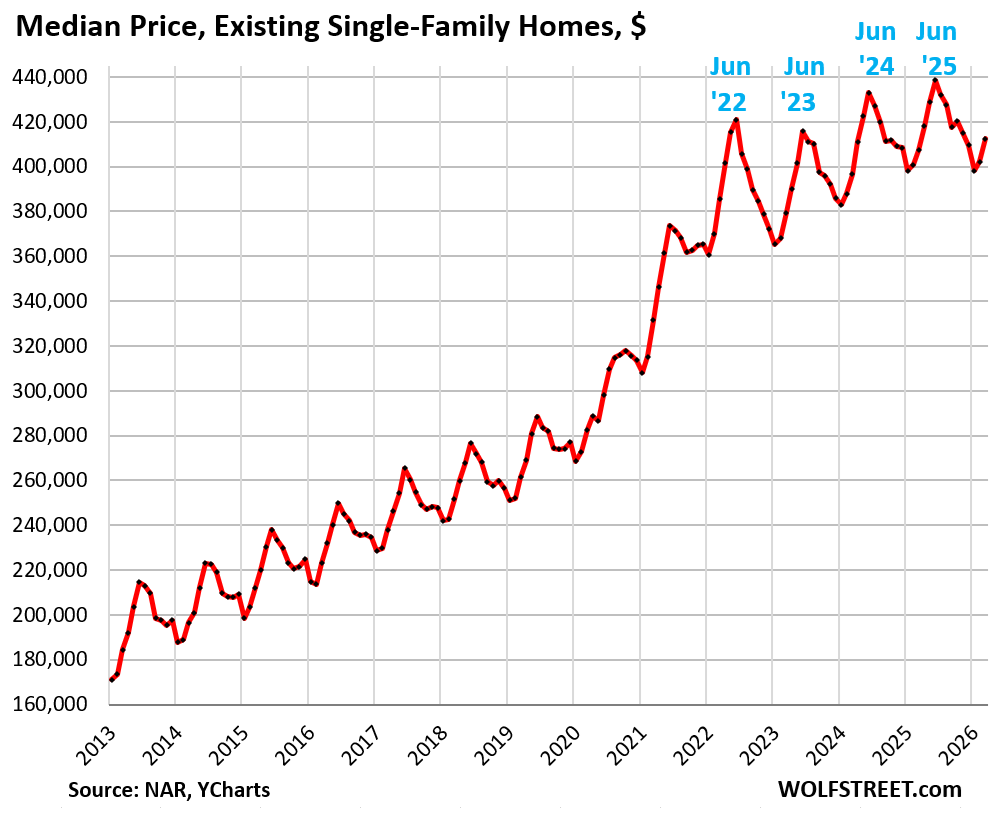

The national median price of single-family homes inched up year-over-year by 1.2% not seasonally adjusted.

The median price had exploded by 41% from June 2020 through June 2022, from already high prices. Those too-high prices (the core of the “affordability issues”) are one reason home sales have been in the deepfreeze since then.

The national median price is irrelevant for local markets. Since mid-2022, prices have dropped in some cities (for example by -25% in Austin and Oakland) and have continued to rise in others (for example year-over-year in Chicago by +2.5% and in New York City by +4.0%). For more, see my city-by-city analysis of home prices in 33 big cities.

The median price is very seasonal, rising and falling with the shift in inventories and sales, as a larger portion of expensive homes comes on the market and sells in the spring, thereby changing the mix of what sold, and shifting the median price up through June. In the second half of the year, the mix reverts, and the median price drops and bottoms out in January.

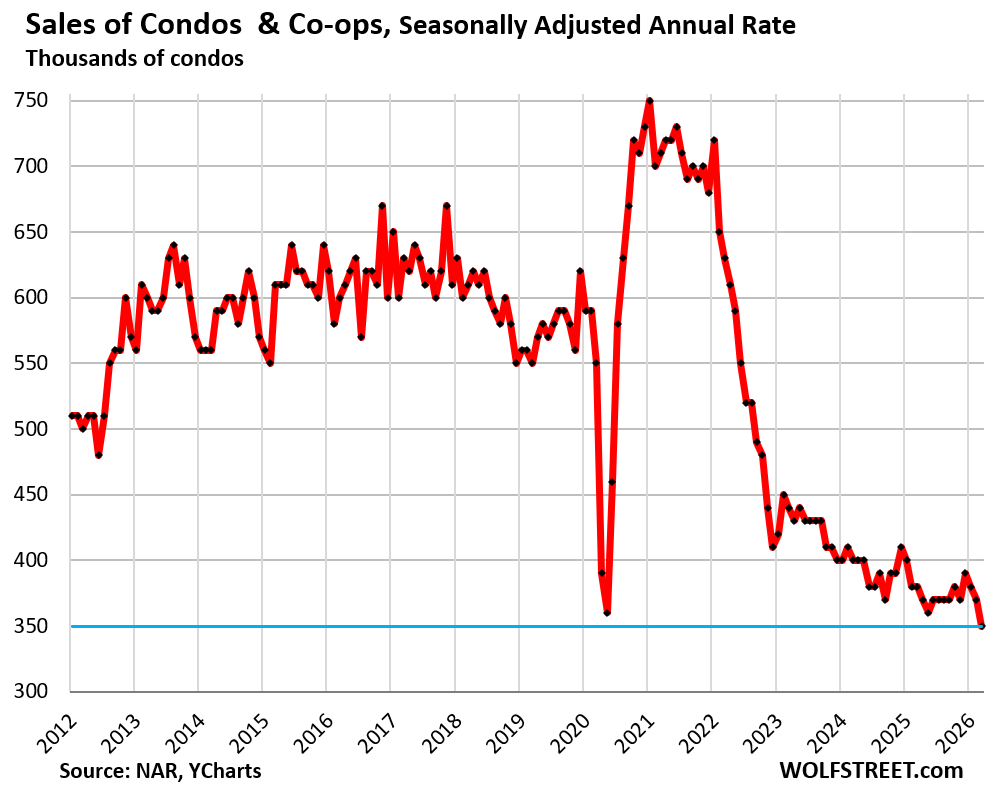

Sales of condos and co-ops plunged seasonally adjusted by 5.4% in March from February to an annual rate of 350,000, the lowest in NAR’s data on condos and co-ops, which go back only to late 2011; March 2012 was the first March in the data; note the 30% plunge since then:

Compared to March in:

- 2025: -7.9% (year-over-year)

- 2021: -50.7%

- 2019: -36.4%

- 2012: -30.0%

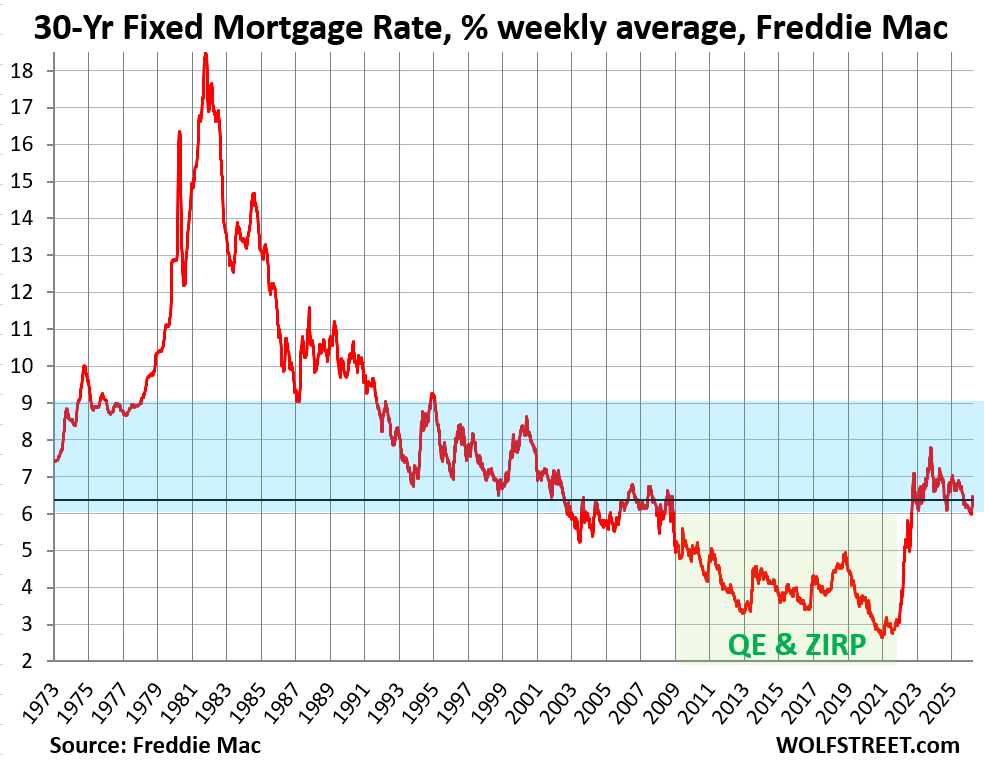

Mortgage rates ticked back up into the 6%-plus range in March, after dipping barely below 6% for just one week in late February.

The average 30-year fixed mortgage rate rose to 6.46% at the end of March, from 5.98% at the end of February, according to Freddie Mac’s weekly measure of mortgage rates. In the latest week, the average rate dipped to 6.37%. These moves are modest and are barely visible on a long-term chart.

Mortgage rates roughly track the movements of the 10-year Treasury yield, but are higher, and the spread between them varies. The 10-year Treasury yield moved back into the 4%-plus range, on accelerating inflation, which had already been accelerating for several months through February, before the war in Iran; and it is now leaping on the spike in energy prices.

These current mortgage rates are historically at the low end of the range in the decades before the era of the Fed’s QE – when the Fed bought trillions of dollars of mortgage-backed securities and Treasury securities with the purpose of pushing down mortgage rates deeply below the rate of inflation, which had caused home prices to explode, triggered the affordability problem, and helped trigger the worst inflation in 40 years.

Sales by region.

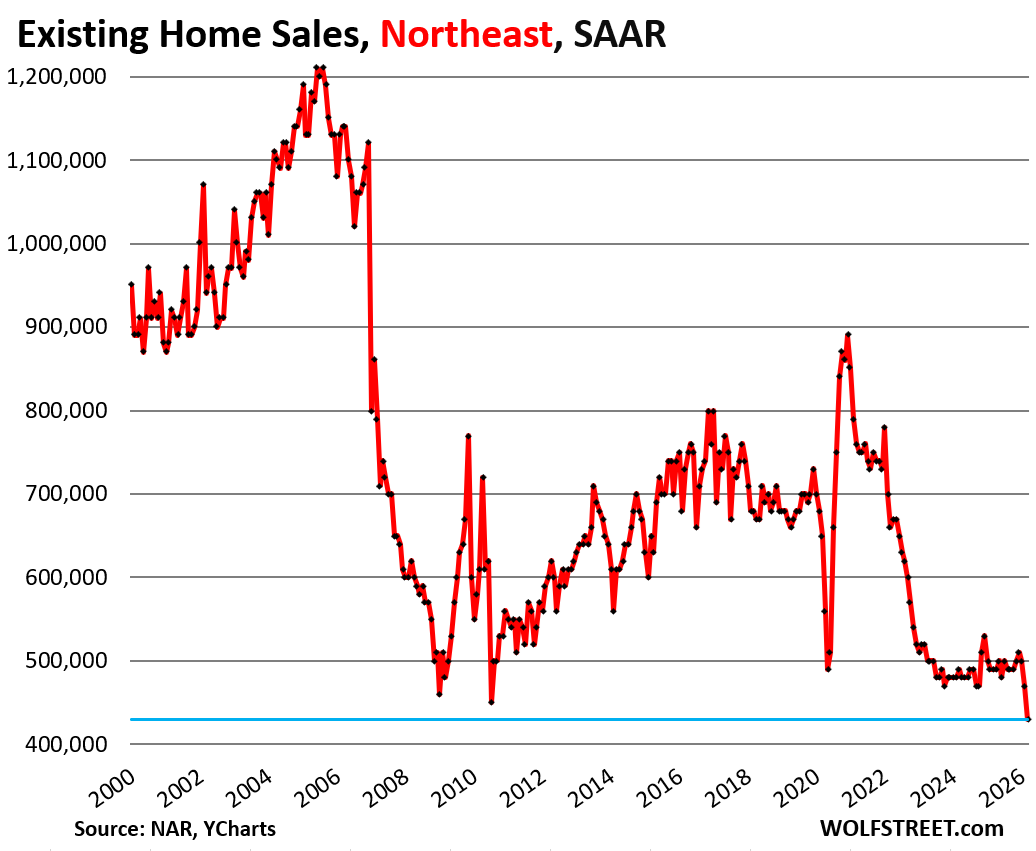

Home sales dropped in all regions in March from February, seasonally adjusted, but plunged the most in the Northeast.

The charts below show the seasonally adjusted annual rate of sales (SAAR) in the four Census Regions of the US. A map of the four regions is below the article at the top of the comments.

In the Northeast, the seasonally adjusted annual rate of sales plunged by 8.5% in March from February, after having already plunged by 6.0% in February from January, to 430,000 homes, the record low in NAR’s data, which goes back to 1999.

Compared to March in:

- 2025: -12.2% (year-over-year)

- 2024: -12.2%

- 2023: -17.3%

- 2022: -34.8%

- 2019: -35.8%

- 2018: -36.8%

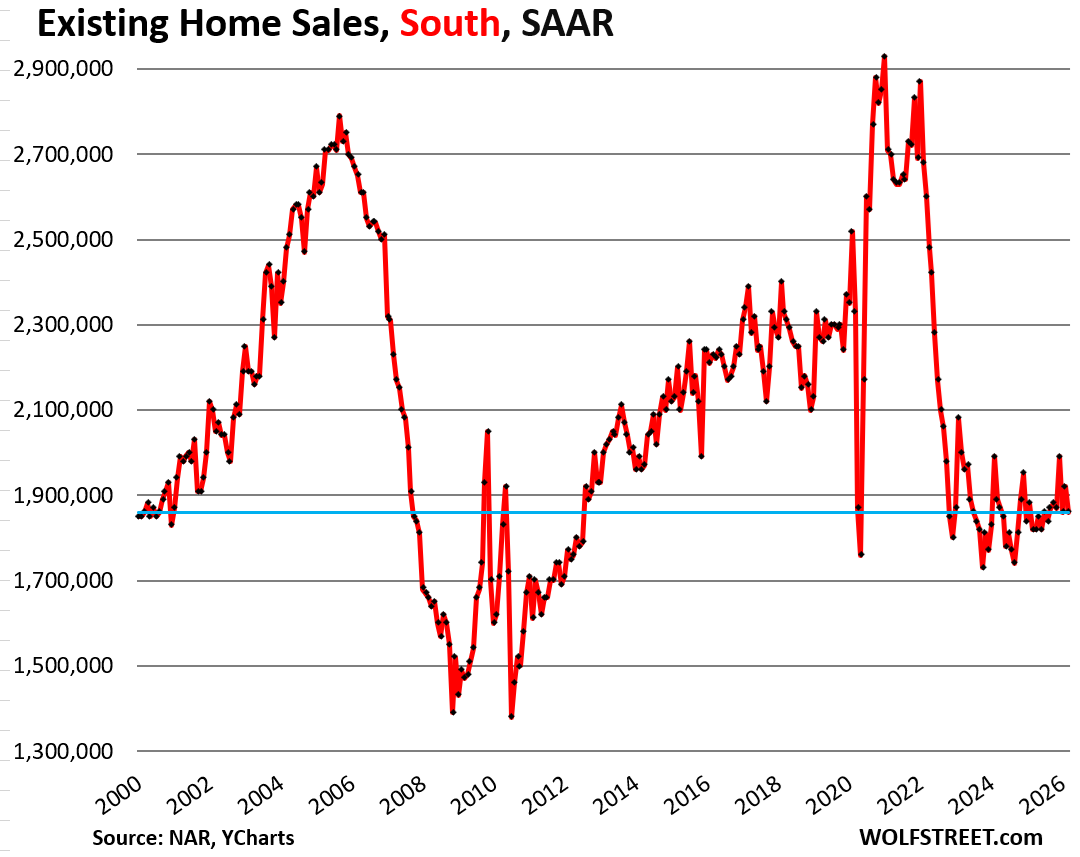

In the South, the seasonally adjusted annual rate of sales fell by 3.1% in March from February, to 1.86 million homes.

Compared to March in:

- 2025: +2.2% (year-over-year)

- 2024: -1.6%

- 2023: -7.0%

- 2022: -28.5%

- 2019: -18.1%

- 2018: -20.2%

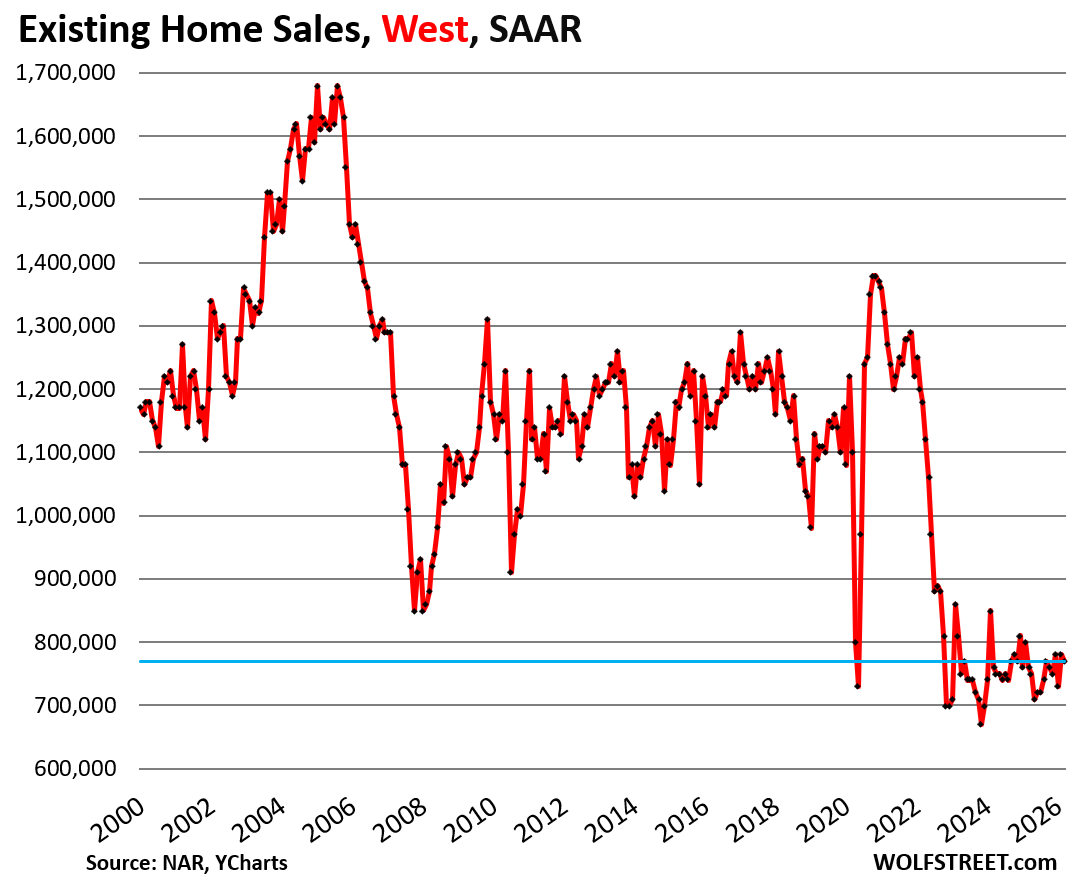

In the West, the seasonally adjusted annual rate of sales fell by 1.3% in March from February, to 770,000 homes.

Compared to March in:

- 2025: +1.3% (year-over-year)

- 2024: +1.3%

- 2023: -4.9%

- 2022: -34.7%

- 2019: -29.4%

- 2018: -36.9%

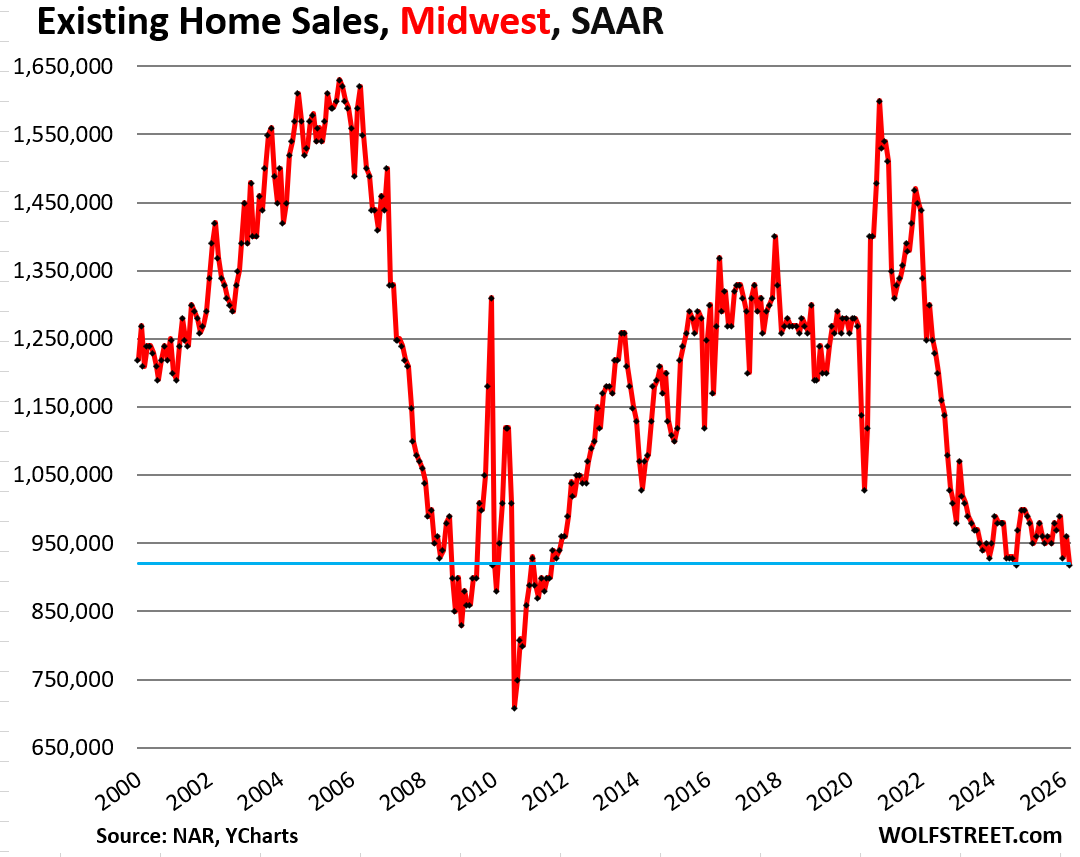

In the Midwest, the seasonally adjusted annual rate of sales fell by 4.2% in March from February, to 920,000 homes.

Compared to February in:

- 2025: -3.2% (year-over-year)

- 2024: -6.1%

- 2023: -9.8%

- 2022: -26.4%

- 2019: -25.8%

- 2018: -27.6%

In case you missed it: Update on the “Lock-in Effect” in the Housing Market: Below-3% & 4% Mortgages Fade Very Slowly

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Here is a map of the four Census regions of the US:

The cost of home ownership is out of control. I just received my insurance policy quote for 2026. A whopping 20% increase following big increases since 2023. I bought in 2019 before the pandemic price gains, but the cost of construction has jumped so much that maintaining a policy that can rebuild at today’s prices is ridiculous especially a fire zone. I can’t imagine how many home owners are underinsured.

That completely varies based on the company who is your insurer.

Allstate. I’m in New Mexico, and fortunately it’s better than my experience in a fire zone in Northern California where a policy jumped 700%. I had to do a property clean up to keep coverage in 2024. A friend with a condo told me that the HOA are struggling to keep coverage of complex. I’m sure if I dropped my policy back to the price I paid, the cost would drop significantly.

We also have a shortage of construction labor much like Northern California after the fires in Mendocino County, Paradise, Redding, etc destroyed entire communities. Contractors love to take advantage of people especially when there aren’t enough workers.

Anyhow, I raised my deductible by $5K and saved $750…

One factor that I don’t see in any of the discussion on housing volume is WFH, work from home.

A lot of people just don’t need to move for work anymore.

I’ve seen the headlines about companies recalling the WFH people, but no one that I know who is WFH has been called back to the office.

It might turn out to be a great for many people who already own homes, because in previous generations, many people got to be 60 years old and had almost no home equity because of corporate relocations.

MS that number has dropped as post-Covid RTO has negated some gains made on WFH. It has balanced out although, leading to a high degree of WFH compared to pre-Covid. Wolf has posted about this a couple of times I believe.

As well as where you live.

My renewal in March is the first time in five years that my rate held steady with virtually no increase, after years of 12 – 17% increases.

In the Great Lakes region – one of the ‘safest’ in terms of natural disasters.

I have park model in mountains

$1200 year + another $1k for taxes

insured value after $1k ded – $61k

add to above comment

I pay $1100 for $350k rental down in valley

The US suburban way of life is not economically viable. You’ll go broke trying to live that way. The future looks like European/Asian style concrete apartment / condo blocks. We’d see the change happening already if building anything but SFH’s wasn’t basically illegal in the US.

That change was pushed by Realtors. A good recap of the history is “A Nation of Realtors”. It’s only slightly less infuriating than the history of water in the West.

Sandy –

Yet one more example of the government “helping” people when convinced of the need by a PAC only looking out for themselves.

Likely not happening in any large scale. The US is too big with a third of the population, and also has way more buildable land. Europe’s history also led to that style of housing. Americans are mostly used to not living on top of and side by side people. What I think more likely happens is a reset like what happened after the great depression.

The problem isn’t a lack of buildable land, it will be that people lack enough income to maintain SFH’s, to heat and cool them, and to drive vast distances between them and everything else. The amount of resources we consume is only possible so long as foreigners are willing to work very hard to provide the raw materials and manufactured goods that make it possible. When that changes, so does our lifestyle, like it or not.

We would only have a concrete block apartment housing stock if government forced it Soviet style. SFH is what most folks want. Survey after survey shows it. Ditto suburbs. A little piece of land and autonomy. Stacking people in heat islands and being dependent on a landlord or a condo board is a choice for many but not the American first choice.

We don’t get a choice when the money runs out, or when the dollars become worthless. The physics of heating/cooling a rapidly deteriorating box made from OSB and plastic and then driving 50-100 miles a day only ever made sense in a world where hundreds of millions of foreigners were willing to work very, very hard for US dollars.

Already, SFH’s are unaffordable to people in the younger generation. I cannot recommend they buy.

Also, lots of people are already choosing to live in high rise condos in US cities, in exchange for low maintenance lifestyles and six figure salaries.

The same for commercial properties being developed to new setback, parking and landscaping standards. A city now collects taxes on a single business taking an entire city block and has to maintain all public utilities and infrastructure around that block. Back in the day a city could collect taxes on 6-8 businesses all on a single block. Maybe even some residential units on top to boot!

Your comment is so far off base it’s hard to know where to begin. SFH exists largely because there is a lot of demand. As for apartments being illegal, I don’t know what you are smoking – they are by far the majority of what is being built in cities today. And they aren’t uncommon in the suburbs either.

Chris B,

I’m amazed by how many replies to your comment completely missed your point.

We seem to be at a crossroads with costs having outdone consumers. I think we’re at the beginning of this cycle because local communities are running out of Covid funding and beginning to realign their tax bases just as insurance companies are continually reassessing risk- even to the point of leaving specific high-risk markets.

The longer people hold out the better because it will force the major lever that is stuck: Selling Price.

Up here in Canada, condo HOA fees are soaring due to insurance costs, esp. in multi-level buildings. Flood damage from upper floor units damaging multiple lower floor units seems to be the primary reason. I would never own in a multi-level building for that reason (and a few other reasons :)).

Housing is an industry that is exposed to the declensions of the rare competitive market. The consumer even when the magical leverage of the financial industry is applied cannot afford the asking price of the asset.

Bernanke’s legacy of a world economy running on the adrenaline of printing enough currency to make it worthless, zero interest rates.

Same story, the market is locked up because few are forced to sell. Despite the doom and gloom, the economy is good, unemployment low. We’re stuck here until a recession hits. Many argue for new construction, but this only helps in some areas but not for the many, urban, in-demand areas. Can’t build a substantial number of close-in housing. One might think that remote work would have alleviated this problem but only provided slight relief.

I don’t think you can say “the economy is good.” For a lot of people, it’s good, but for a lot of people, it’s bad.

By any objective measure the economy is currently mostly good.

People fear (for many good reasons) that it might get worse rather soon. Many people wish it were better for them personally, as they always have and always will.

But as far as historical economies go, this is a pretty good one. Employment is high, and incomes are higher than ever before. Housing is the one big negative, for those who rent or bought a long time ago.

“By any objective measure the economy is currently mostly good.”

Hmm – for one, not by the number of home sales transactions…the point of the entire post.

Consider how many people in their 70’s and 80’s in the Midwest and Northeast (containing some of the highest median age states with lowest sales volumes) who are in serious danger of having to terminally age in (frozen) place – because the economics of retirement relocation really don’t work in their favor anymore.

Even as younger potential home buyers are insanely priced out of the few markets where jobs have grown in the last 18 months-2 years.

There is a huge amount of distance between 3.6 million annual SFH sales (now) and 6.2 million (boom times) and even 4.8 million (last semi-stable period during last 25 years…one wholly propped up by ZIRP).

yeah, its all great, but then why are so many “in power” screaming for rate cuts?

They’re always screaming for rate cuts. All these people want free money. Everyone does. And no one wants to pay the price of free money.

I don’t agree. I consider being able to afford assets at reasonable entry points and essential services like child care as integral components of a “good economy.”

No one owes anyone the ability to buy assets. What we owe people is the ability to have access to basic amenities and the opportunity to things with your life.

Even child care is complicated because, yes, we absolutely want people to have help raising children, but the current model just simply can’t work mathematically: you can’t have child care be both affordable and reasonably well compensated unless it’s government assisted, which means more taxes.

I gotta admit, of all the people and situations in today’s economy I worry about, the inability of aging boomers to retire to a golf course in Arizona or Florida is not super high on my list.

We have a sclerotic society. People who are ‘in’ seem to almost be locked in, if they don’t screw up too much.

People who are ‘out’ are locked out, and can’t get in without lying or cheating.

There is a video on youtube by a former HR rep from google that said liars get the jobs.

And of course white guys can’t even lie themselves into a job.

A totally corrupt society.

I would think that China could topple us like the barbarian toppled Rome, but China is possibly even more corrupt.

Things will get to the boiling point when we get a critical % of our nation that has nothing to lose.

Numbers, I didn’t say anyone was “owed” anything. But without the ability to buy assets, it’s not a good economy.

And this is different from any other year….how, precisely?

I remember the late 90s. The economy was good in general, and not K-shaped

TSonder305 –

I think the K-shaped economy is a media and politically contrived term. The upper class has been benefitting from low interest rates and government intervention since the beginning of time. It is no different the past two years than what we have been seeing ad-infinitum. They just started pointing it out to drive their objectives.

For the top 20 percent who hold almost most assets economy is good

You want to argue about the “wealth disparity.” OK, argue about “wealth disparity.” It’s Huge.

But DO NOT CONFUSE “wealth disparity” with “wealth.” Even in the middle, Americans have massive wealth (assets minus debts), but there is a huge disparity with what Musk has.

Your phrase, “the top 20% hold most assets” is bullshit and makes it sound like everyone else is poor. The bottom 50-90% hold $57 trillion in wealth (assets minus debts). The bottom 50-90% = 53.9 million households who have a combined $57 trillion in wealth. That’s the middle class and upper middle class.

Even the bottom 20-50% hold about $4 trillion in assets; that’s 40 million households that hold a combined $4 trillion in assets. That’s the lower middle-class.

Households = addresses. A single person living alone is a household. It includes those singles who are just starting out and haven’t accumulated assets yet. There are quite a few of them.

The bottom 20% are poor and don’t have much of anything. Not the bottom 80%, you goofball.

The WSJ published an article a few days ago about how millions and millions of Americans have moved up into the upper middle class over the decades. And how the share of the middle and lower middle class has shrunk.

I normally delete comments that confuse “wealth disparity” with “everyone below the top 10% is poor” because life is too short to be wasting it on that bullshit.

Which is the paradox of what is wealth without the ocean so to speak, ie, the everyday society that are responsible for enforcing the Constitution of the United States of America

Freedom is a universal aspiration. America is not unique. It is just as strange, certainly, as Europe for instance.

Of course having grown up in a Rocky Mountain hick town that fundamental scholarship was a way to while away the long winter.

Frank,

I would say the unemployment and economic indicators are more nuanced than “good.”. Recessions seems to be a retrospective determination well after the fact when it started but not hard to see multiple headwinds right now, even without the American and Israeli war against Iran.

They are indeed determined after the fact by the NBER, but none of the major recession indicators or predictors are currently showing any signs of recession.

Could change in a month, of course.

yes, nothing is predicting recession.

so why are rate cuts being demanded, especially with high inflation?

with the rate cut panic and irresponsible fed policy, the bulls have avoided 37 of the last 0 recessions, but now we have this little inflation problem.

and you don’t mention inflation; so all is good, inflation be damned, right?

Recession – Hmmmm? One day….

“A hurricane is right out there down the road coming our way.” — Jamie Dimon, JPMorgan (2022)

Jamie Dimon (JPMorgan, 2023): “I think a mild recession is still on the table.”

“The probability of a U.S. recession is rising as the Fed tightens aggressively.” — Goldman Sachs economists (2022)

“We are heading toward a recession in the first half of 2023.” — Michael Hartnett, Bank of America (2022)

“The risk of recession is uncomfortably high.” — Mark Zandi, Moody’s Analytics (2022)

Mohamed El-Erian (2024 commentary): “The risk of recession remains elevated.”

Inflation is moderate. People are worried because it could be the beginning of an acceleration, but if inflation just stays at 3% forever, no one will be hurt. Even 4% would not be the end of the world. It’s when it accelerates further and begins the wage/price spiral that it becomes a problem.

So a bunch of business leaders predicted recessions that never happened? Or is that the point? Hard to tell from context here.

Mr./Mrs. numbers,

If you think that nobody gets hurt at 3%, or 4% inflation, then why this?

“According to The Wall Street Journal, the primary challenges facing the U.S. include a persistent affordability crisis, and declining economic mobility, which are fueling a widespread loss of faith in the American dream.”

Do you believe that people are NOT hurting? That they just like to complain? It’s mind numbing.

In any case, I think that politicians of all persuasions will be hurt by those high price levels, a product of your beloved benign inflation.

@numbers. The problem with 3-4% inflation is bond investors want a positive return on their investments after inflation. So 4% inflation probably means a 10 yr yield above 5% which impacts mortgages, corporate debt, and also interest rates the US can issue new debt at to find its deficits

One moron’s take beyond the land of graphs-

From 2015–2019 (pre-COVID), home sales were basically just flat. Some years were up a little, some were down a little, nothing big either way. One year (2019) popped up more, but overall it was just a steady, sideways market before all the COVID-era swings and the post-2022 drop.

Why – Gen Z and younger millennials just aren’t chasing the white picket fence anymore. Doesn’t matter if prices fall and rates are 0%.

Burned by the 200k college scam paying off mega-loans.

Marriage/Dating is dead – births tanking.

Heads-down doom scrolling in the matrix.

Uber everything — food-booze -chips

No rainy day funds.

Disposable digital gypsies – new-age hippies.

No family, no lawn to mow, no pool to clean, no interest in settling down with a mortgage.

We in the US absolutely worship “rugged individualism” right up until it conflicts with our cultural values of single family homes with white picket fences. The younger people have realized that the world their parents grew up in is out of their reach. If they own a home, it won’t be until they are in their 40s. They have 24/7 streaming entertainment, why would they want kids?

The economy has set itself up for maxium extraction of wealth from the public, so dual-income is a must, day care is horrendously expensive. Mom and Dad have moved to a retirement village in a sunbelt state, so they can’t provide child care. Pets take the place of children and the concept of family now includes fur.

You can pine for the way it used to be or accept the way it is. People would rather stare at their phones than engage with actual other people face to face. That’s just the way it is.

What it means in the big picture that relying on the young to fund the old is DOA. A new system needs to be designed and implemented really damn quick because the handwriting is very clearly on the wall.

Yes and more generally, younger people are realizing that they don’t have to just do things the old way, plus they’re realizing that they’re comfortable enough not to have to and it doesn’t look all that much fun anyway.

Everyone is a self-absorbed independent unit who never has to learn anything and never has to admit they’re wrong about anything because they can always find someone online who will tell them everything they ever wanted to hear: it’s all everyone else’s fault, compromise and cooperation are for suckers, there’s no reason to ever have to be even a little bit uncomfortable or inconvenienced, every thought or emotion that you ever had is always worth obeying.

They aren’t chasing it because they can’t. If the Federal government funded a new Levittown like development for young first time home buyers (without the pesky racist language that funded the original), you bet they would chase it. Housing prices are just too high to make it feasible.

Exactly

The price of housing is 50 pct overpriced. It needs to fall so that the segment of the population under the spell of the nesting instinct can afford to buy it.

“These damn kids these days” syndrome is repeating it’s perpetual cycle, lol! I’m with you on pricing pressure versus blaming their supposed anti-social, garbage work ethic, digitally addicted, no dating, lack of fun sponges (kids), latte buying, family hating tendencies.

My kids (and those in their social circles) ARE in fact chasing it…living life! They’re in the trades, in professions where college degrees in fact pay off student debt, public servants, etc…yet they are living meaningfully, each in their own way, outside their occupations. But because they’re doing it differently in many aspects, somehow that makes it wrong because, well, “that’s not how I did it”.

In terms of pricing…my parents built a home in 1973 when the US home price/income ratio was around 3.6. One of my kids just bought that home (well, not exactly but similar and built in 1974) and that same ratio is now 7.15’ish.

This is not their grandparents housing market, transportation market (vehicle prices/insurance), or any other market for that matter. They don’t want a white picket fence or a pool…they cost too much and there’s better things in life to enjoy.

No sex, no drugs, no wine, no women

No fun, no sin, no you, no wonder it’s dark…

Old age ain’t fun for many of us that mourn for the old days when I was young and sin was point of living.

If we really want to get property sales turnover and eventually lower prices and more affordability, all states should remove property tax caps and assessments caps and inflation levies.

Doesn’t make sense that people that have lived in their homes for 30 years get to pay 1/3rd the property tax of the home as a new buyer (uncapping) and it discourages older owners to sell and downsize.

From a progressive standpoint. Senior citizenship had the longest time to accumulate wealth and shouldnt get a senior property tax exemption or any discounts.

Amen. California prop 13 was one of the biggest wealth transfers from young to old in history.

How about anyone without kids over 50 then getting exempted from all school fees in those prop taxes? There are some areas in the NY area that do that for 55″ communities. Cuts taxes about it half. Sounds like a fair trade to consider vs Prop 13.

BTW, to you and Lazy above, why should anyone’s prop taxes be raised a couple years later because some idiots along the street overpaid for their houses when mort rates tanked? P13 creates distortions, but they’re better than the alternative.

P13 is fine. The only part that needs to go away is the inheritance part.

There is absolutely zero reason why property taxes should carry over to one’s kids.

And yes I know the original argument about poor widows. That generation is long gone.

If you sell a home and do not buy another, where are you going to invest the cash? The stock market is awfully high, the Treasury and bond markets are dangerous because of the government debt problem and possible interest rate hikes.

So just rent the home out or stay put.

We just bought a house in Central Valley of CA and will put our SoCal house on the market next month. When it does sell (and it will, it’s a great house and turnkey) we will put the profits into 4 different FDIC protected high yield savings accounts so we’re protected in case everything goes cattywampus. We’ll buy the final house when things stabilize a bit more and we see how things play out with AI. No way I’d put money into the stock market right now, I’d look to Tbills, CDs, high yield savings.

Respect for working “cattywampus” into the chat. I love seeing that word used in the right context.

“So just rent the home out or stay put.”

Which is a big part of why rental yields are tanking across the US–lots of “accidental landlords” who are increasingly unable to be cash flow positive on the property. These folks will become forced sellers into a weak market once there is a legit recession with labor market churn.

Wolf,

Is there a median price chart to go with the condo sales volume chart?

SFH transactions look to be off about 25% from last semi-stable period – but condo volumes are off 40-45% – wondering if that differential has resulted in condo price softening to a greater extent than in SFH.

At some point, transaction volumes fall so low, that smaller and smaller negative shocks can overwhelm what the mkts can currently absorb and prices (finally) have to go lower.

Just wonderin’ if 45% off is enough to unlock price declines of any appreciable amount.

Yes, but the NAR’s condo data (supply and prices) have gone whacko when they’re initially released, and then the next month they’re super-massively revised. You thought the BLS was bad about that! It started a few months ago, especially with supply of condos. The charts look ridiculous, and then the next month, the huge revisions bring them back into line. But then the old charts make me look like a goofball. So the condo data no longer meet my minimum requirements for publication, the minimum requirement being, don’t make me look like a goofball a month later. When they get this stuff straightened out, I’ll use the condo data again.

Tough time to be a realtor or mortgage broker.

I will get the violin out of the closet …LOL

Yeah, I remember all of the listings back in 2001-2003 that said “cash only buyers”. The listing agents never cried for us.

We are paying for the years of free money combined with the ridiculous pandemic work stoppages and the supply chain interruption. However, the economy is still chugging along in spite of all the complaints. But who isn’t going to complain when the free money stops?

Hi Wolf,

Maybe this is dumb, but would it be possible to do a slope from the 2013-2019 nation median existing single family home, like a linear regression to extrapolate what it would be in 2026 if the pattern had stay consistent to precovid (i.e no inflation/free money printer)

Tried this myself and took Jan 2013 – December 2019 w/ linear regression data from same source as Wolf, got $360,500 for Apr 2026.

$340k-$360k…just use a piece of paper or your hand catching all the peaks or troughs.

Current price is about 20% over that arbitrary amount.

Even that period post gfc was anomaly with multiple rounds of qe, the fed for the first time intervening in the mortgage market directly, and zirp. We can’t go back to that unless you just want to set the stage for the next bubble

It’s been a while since price discovery in many things

Federal student loan payments were paused for over 3.5 years (March 2020 to October 2023), while COVID-19 mortgage forbearance, which started in March 2020, generally allowed for extensions that lasted until April 2023 or later for many borrowers. (Oh how soon we forget, Federal Government took advantage and went into the Never Waste a good crisis Mode. Everybody got chance to pile on the huddle, free money for all, even PPP loans for Congress and professional scammers. $FOMO to $YOLO orchestrated by the full faith and credit of United States. The everything bubble fix is still in. Elons Space Ex IPO will be the Star Trek finally and the beginning of the new frontier. No one should be crying over the free money that has been given out to get US to this point. “Kid You Pigged Out” is so appropriate.

In the West, the seasonally adjusted annual rate of sales fell by 1.3% in March from February, to 770,000 homes.

Compared to March in:

2025: +1.3% (year-over-year)

Is there a Typo of + instead of -?

2025: -1.3% (year-over-year)

For once, it’s not a typo.

March 2026: 770,000

Febr. 2026 780,000

March 2025: 760,000

March 2024: 760,000

so the three “1.3” in a row — one with a minus and two with pluses — look kind of funny, but the NAR releases these sales figures rounded to the nearest 10,000. The percentages of the unrounded numbers would not be the same like this.

Wolf, you KNOW that this is the MOST screwed (dysfunctional, irrational) the housing market has ever been. Someone or something is operating behind ‘that curtain’.

What’s operating behind the curtains are too-high prices; the remaining 3% mortgages; the huge equity many homeowners have as a result of the price explosion in 2020-2022; a fairly strong economy and labor market that doesn’t force people to sell; and WFH which doesn’t force people to sell when they get a new job. Lots of things come together.

One other factor is property taxes. Appraised values have skyrocketed in many parts of the state. Texas caps the annual increase in property values at 10% for residential homesteads. However, if you sell your house and buy another, you pay the full appraised value of your new property.

For many homeowners, this would result in a property tax increase that is even higher than the amounts they would pay moving from a 3-4% mortgage to current rates. This factor does not get the same publicity as mortgage rate increases, but is just as important for locking homeowners in place.

10%!!!! Wow, leave it TX to be the exact opposite of CA.

Supply: up

Sales (demand): down

Prices: go UP?

That makes no sense.

Economic laws like “supply and demand” are natural laws and will be obeyed… eventually.

I have been saying this for the last 2 years. I keep telling people that prices should be coming down since nobody is buying and inventories are increasing but nothing. At least not where I live, Las Vegas.

I think its a combination of things. Listings that don’t sell get removed. Sellers may lower the price by $5K or $10K but eventually they pull it. So supply isn’t as big as it could be.

And I think there are a lot of new homes being built with enticing incentives.

I still think prices need to come down some. Apartment rents came down for sure.

@Andy – Las Vegas

Las Vegas actually had a strong spring.

Prices held steady even with a 41% jump in single-family inventory from February to March.

Sales were up 34%, with luxury really strong—And six penthouses cleared $1M+, including one at Waldorf Astoria Las Vegas that went for $10.1M.

“Sales were up 34%”

From near zero, and just a little higher than zero, LOL. Same BS over and over again. HOW FAR ARE SALES DOWN FROM 2022? FROM 2019?

Still waiting for March figures. But in February, sales were down 12% YOY and by 40% from 2021 (Redfin)

Prices are set at the margin, and the marginal house being sold is priced higher than the average house. Folks who can afford these more expensive properties can afford to pay more. All markets are different, and economics is far more complex than a simple supply/demand curve.

The market stopped responding to fundamentals awhile ago. Nowadays the market seems more driven by psychology and propaganda. So if the propaganda is buy now before rates drop and housing runs another 20% people keep buying. If the news was like that was a bubble, no appreciation for years, possibly depreciation – homeownership is not currently a good investment you’d start seeing a shift.

Also probably doesn’t help that everyone can see their Zillow historical price estimate chart. A lot of people are very attached to those numbers.

Personally I think we need something that creates a mild panic (not large panic though or the govt intervenes)

Another natural law, though not as strong, is that “prices are sticky-downwards.”

We can invert the supply & demand law to be:

Prices are up therefore:

Supply goes up,

Demand goes down.

That works, and describes what we’re seeing, but it’s much harder for one variable to influence two that the normal two-influencing-one; it won’t last.

But then: Markets can stay irrational longer than you can stay solvent. :-)

Hey Brian,

I like your take.

Wouldn’t one argue since prices are up we are all rich on paper?

Zillow has two types of sellers at the moment: those who don’t need to sell immediately and those who do. The ones that do set prices reasonably. Unfortunately, the number of those who don’t need to sell quickly out number those that do.

The people selling quickly today are the FOMO folks who bought quickly the past few years. There’s lots of seller pressure in that segment. They over levered. Rising home costs and falling prices are taking a toll.

Perhaps like Canada in 1990’s a slow prolonged return to normal as incomes rise, interest rates my moderate and house prices slowly bottom and then central bank + government do their inflation magic.

Well this starts to solve the unaffordable housing crisis that Kamala babbled about in her campaign!

This is purely anecdotal based on our driving trips in the FAR WEST suburbs of Chicago …

Very little NEW building activity. Very few homes have ‘For Sale’ signs in front of them.

The Fed is totally responsible for the current situation. End the Fed. We bought our home in 2004. 100K. In 2008, nobody called us except the mortgage company because we were a few days late with the payment. Now, we get calls and letters weekly from people that want to buy our house. In our town things are booming and apartment buildings have gone up everywhere.

All things considered, home prices are…………

Exactly where they should be!

I caught AI trying to sell me how things were great in the housing market, I then told it it was wrong and reffernced Wolfstreet.com. You can’t trust AI. I asked it to compare the answers it given me as a logic test and here was the output:

Why the “Wolf Street” Version is DifferentWolf Richter’s analysis typically strips away the optimism found in real estate trade group reports. In the context of 2026, the key differences are:

The “Shortage” Myth: Standard reports often say there are “no houses to buy.” Wolf Street uses data to show that inventory is actually jumping (especially in places like San Francisco and Silicon Valley), but homes are sitting because the “price-discovery” process is broken.

Volume vs. Price: A standard answer says the market is “strong” because prices are high. Wolf Street argues the market is “poor” because nobody is buying. If people can’t move, the market isn’t functioning.

Local Reality: While statewide median prices look stable, Wolf Street highlights the “losers” of the market—condos and specific cities like Oakland—where the correction is already visible and significant.

In short: The first answer sees a valuable market; the Wolf Street answer sees a frozen one.