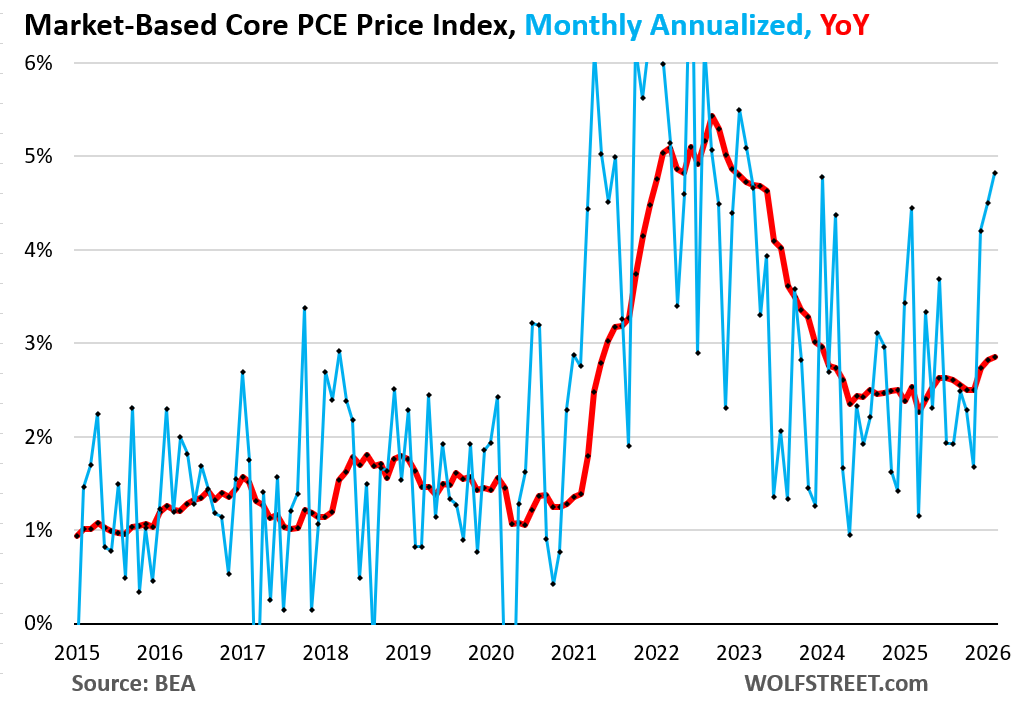

“Market-Based Core PCE price index,” which excludes the imputed housing components, spiked by the most since February 2023.

By Wolf Richter for WOLF STREET.

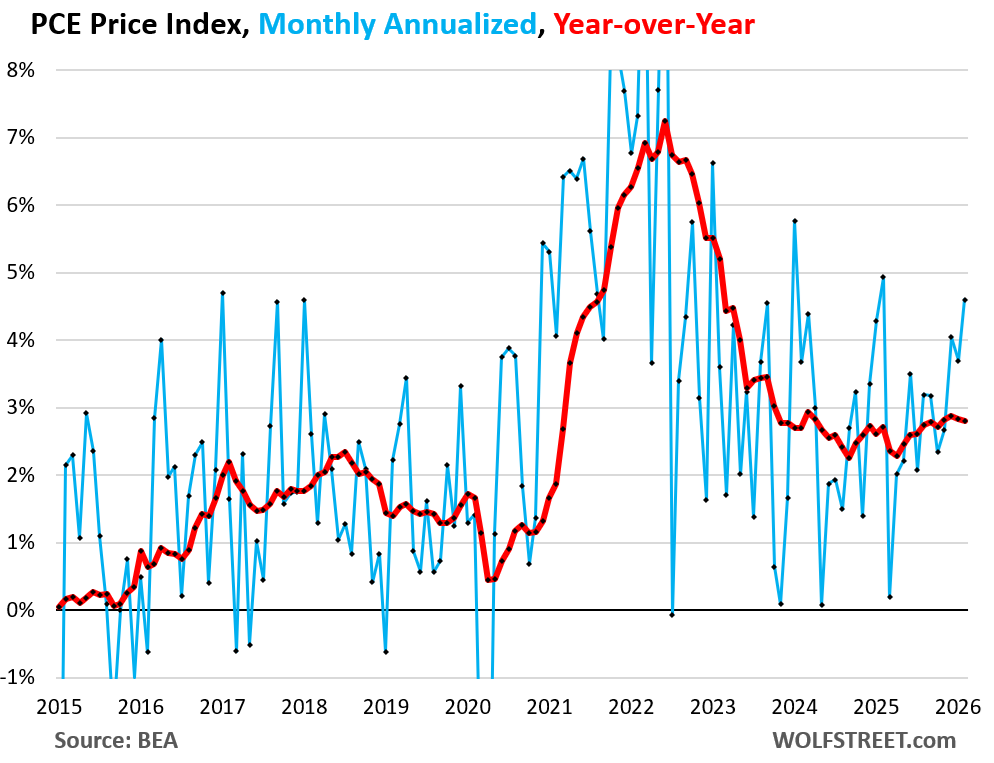

The Fed-favored inflation measure, the PCE price index, which includes food and energy, jumped by 0.38% in February from January (+4.6% annualized), the biggest jump in a year, though the energy price spikes from the Iran war hadn’t started yet (blue line).

Year-over-year, the PCE price index rose by 2.8%, roughly the same increase as in the prior three months, and all of them were the biggest increases since the spring of 2024 (red line).

The Fed’s target for the year-over-year measure is 2.0%.

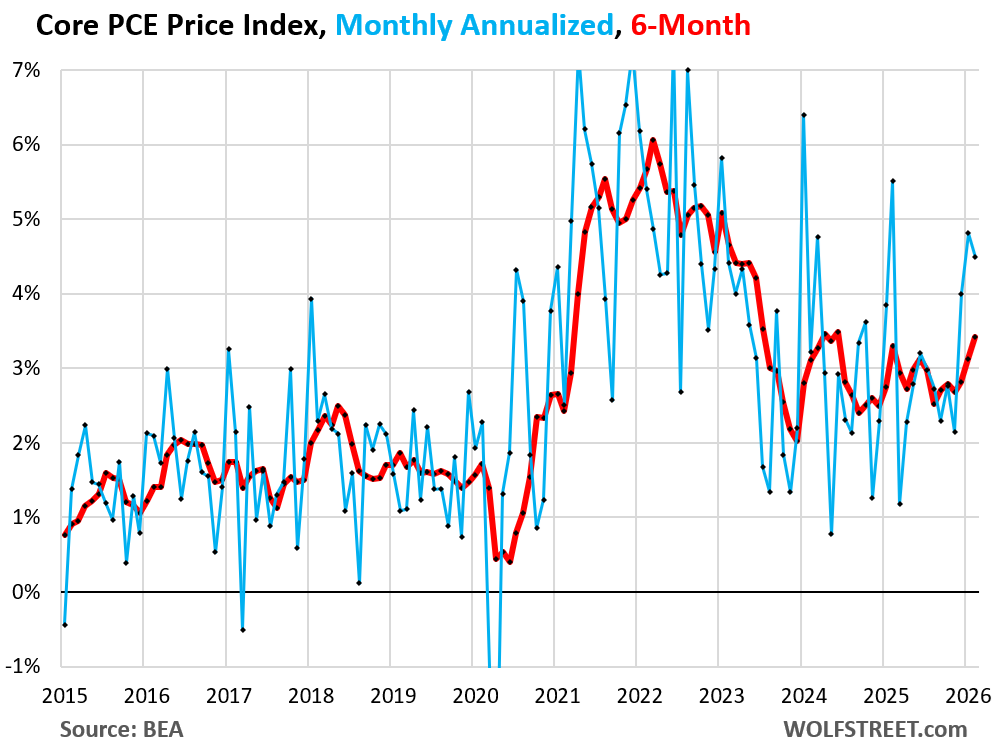

The core PCE price index jumped by 0.37% in February from January, or +4.5% annualized, the third month in a row in the 4%+ annualized range.

This pushed up the 6-month core PCE price index to +3.4% annualized, the worst since June 2024. The six-month index shows the recent trend, and that trend has been going in the wrong direction (red line):

The year-over-year core PCE price index (not shown in the chart) rose by 3.0%, a slight deceleration of the prior month (+3.1%). The Fed’s target for this measure is 2.0%.

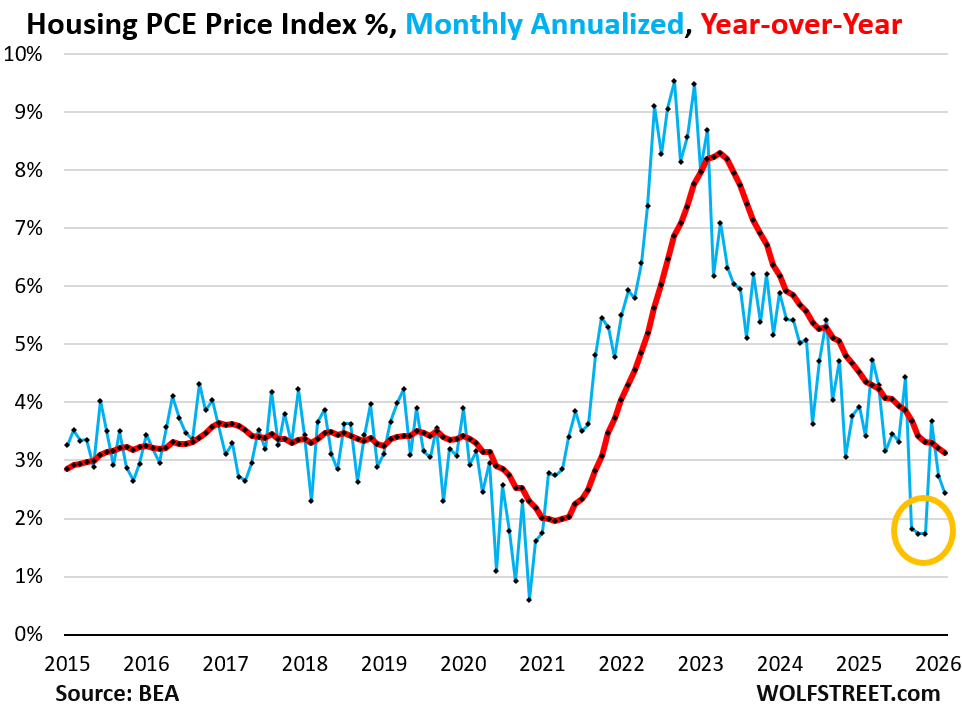

The housing index, including the imputed housing components, continue to hold down the overall PCE price index, the core PCE price index, and the core services PCE price index.

In February, the housing PCE price index rose by only 0.20% (+2.45% annualized, blue in the chart below). Year-over-year, it rose by 3.1% (red).

A major component in the index is “imputed,” so not based on price data but on what homeowners think their homes would rent for.

The declining imputed components take the place of actual inflation that homeowners face with surging homeowner’s insurance, property taxes, HOA fees, and repairs and maintenance.

The imputed data is from the BLS, what in CPI is called “Owner’s equivalent of rent,” which was heavily doctored last fall (explained in detail here), and is visible in the chart below in the outlier three months circled in yellow.

Those three months will continue to push down the year-over-year comparisons until they begin to fall out of the 12-month time frame in September.

But the “Market-based core PCE price index,” which excludes all imputed components, spiked by the most since February 2023, by 0.39% (+4.8% annualized).

Year-over-year, it rose by 2.9%, the worst since January 2024:

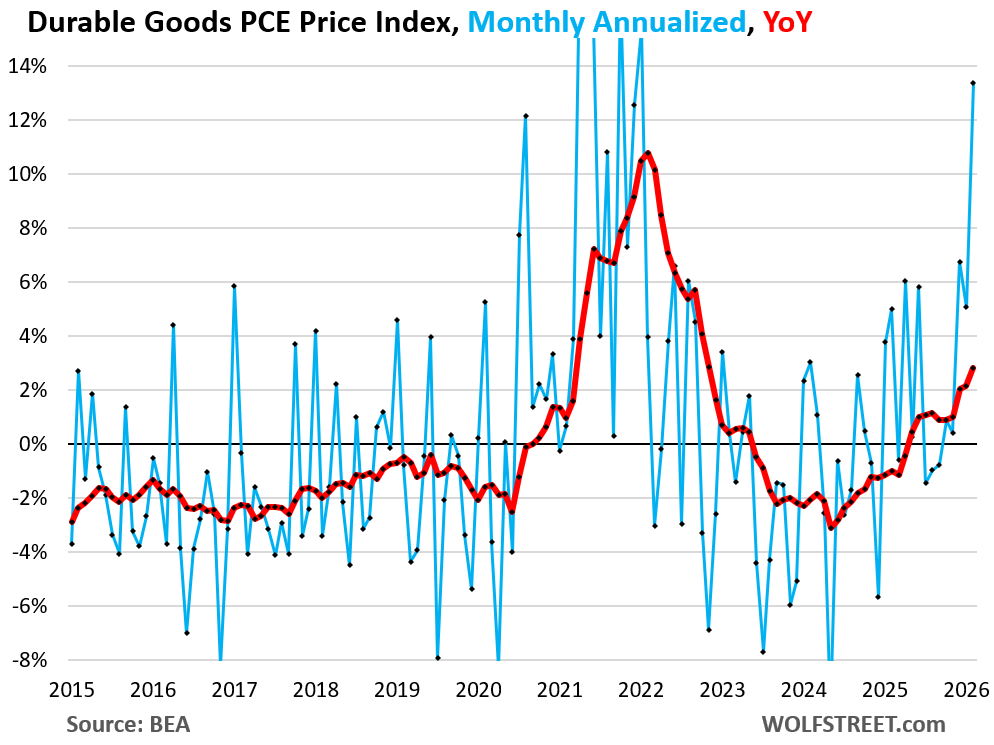

Durable goods prices spiked month to month by 1.0% (+13.4% annualized), but not because of motor vehicles, the biggest component, where prices where unchanged month-to-month and nearly unchanged year-over-year; and not because of furnishings and durable household equipment and appliances, which ticked up by 0.3% for the month; but because of huge massive month-to-month spikes related to gold, guns & ammo, and computer software (and I’ll explain how computer software ends up in durable goods):

- “Jewelry”: +7.0% month to month (+125% annualized), +10.8% year-over-year, as part of the surge of gold prices through January that made it into jewelry retail prices with a lag;

- “Sporting equipment, supplies, guns, and ammunition”: +1.7% month-to-month (+22% annualized), second big month-to-month spike in a row, which flipped the year-over-year decline through December to an increase of +3.7% year-over-year. This category does not include bicycles, etc., which are in a different category, “sports and recreational vehicles,” where prices dipped in February.

- “Computer software and accessories”: +6.5% month-to-month (+113% annualized), third big month-to-month increase in a row; +8.0% year-over-year. Software is not tariffed. It’s under durable goods because it’s part of “information processing equipment,” which includes “personal computers & tablets,” which are tariffed, but were unchanged month-to-month (+0%) and barely up year-over-year (+0.9%).

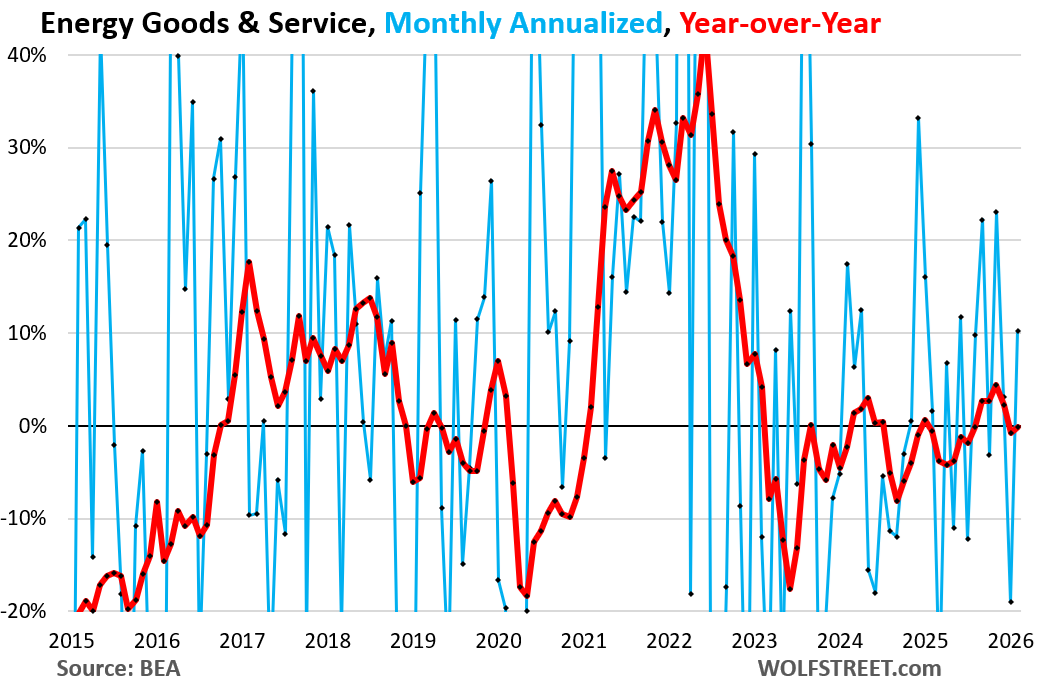

Energy prices jumped in February, before the Iran war, by 0.81% from January (+10.2% annualized), but were still unchanged from a year ago.

The energy price spike in March will add to the inflation data for March.

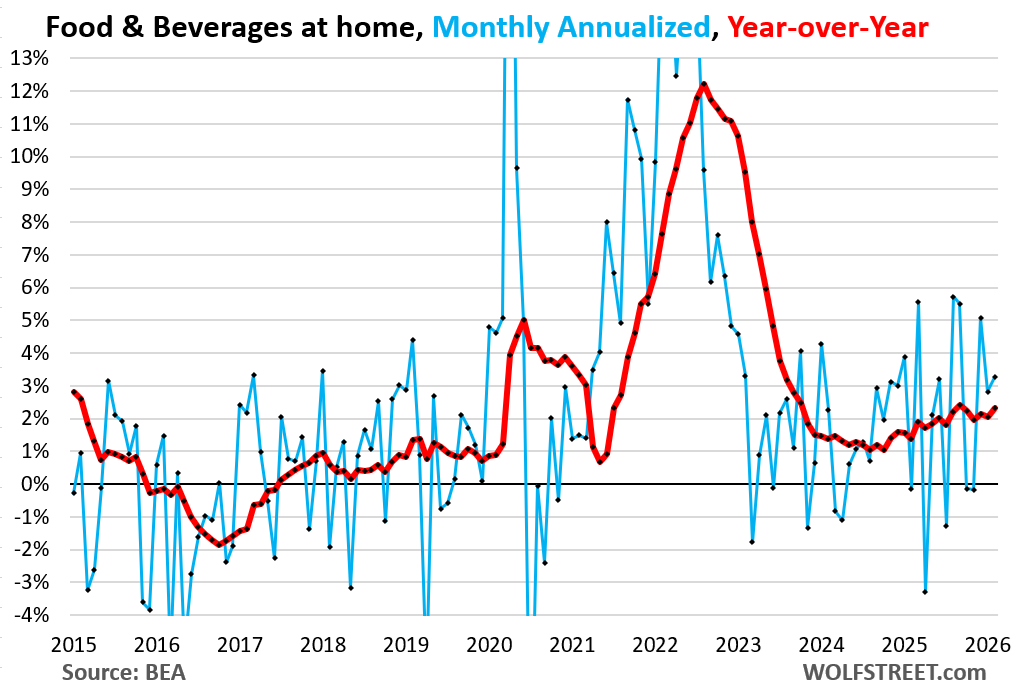

Food prices rose by 0.27% in February from January (+3.3% annualized, blue line). Year-over-year, they rose by 2.3%. The trend has been accelerating since mid-2024.

Part of it has been driven by the four-year-long huge price increases of beef and veal (+14% over the latest 12 months) and coffee (+12% over the latest 12 months). Some other food prices, such as eggs, have fallen from their prior spikes but remain much higher than before.

Inflation isn’t going away, on the contrary. There is a lot of stimulus in the economy: Government deficit spending, tax cuts for companies and individuals, bigger tax refunds to consumers starting in March, massive corporate investments in anything related to AI, too-low interest rates, and still too narrow spreads. Inflation feeds on these conditions.

The housing index and especially the declining imputed measures that replace the soaring actual inflation homeowners face are covering up the extent of the inflationary pressures in the economy.

The Fed needs to pay attention to inflation, and it has been to some extent, and it keeps mentioning it as a risk to the upside, and it has put rate cuts on hold because of it.

And in case you missed it: New inflation pressures suddenly building up in the pipeline are concerning – Used Vehicle Wholesale Prices Jumped. That’s How it Started in 2020 when Broad Inflation Took Off

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hey tarriffs I am looking at you…….

Good lordy. So do the impossible and try to read the article. It tells you where this came from, including this section here, quoted verbatim from the article:

Durable goods prices spiked month to month by 1.0% (+13.4% annualized), but not because of motor vehicles, the biggest component, where prices where unchanged month-to-month and nearly unchanged year-over-year; and not because of furnishings and durable household equipment and appliances, which ticked up by 0.3% for the month; but because of huge massive month-to-month spikes related to gold, guns & ammo, and computer software (and I’ll explain how computer software ends up in durable goods):

The FED needs to step back and let the bond market take the lead. If it does not step up, then the FED needs to react.

Not if they want to keep their jobs.

just think if GOVT would actually try to eliminated/greatly reduce the FRAUD taking place in plain sight

the deficit could be nearly eliminated – ie balanced budget

but there doesn’t seem to be any will to do so

Please expand, what fraud? By whom? When? What sector?

Well I suggest that it is the Fed who is actually responsible for the relentless bid in both the stock and bond public markets.

The QE equilibrium where asset prices are not allowed to fall.

Meanwhile . Tomorrow they are likely to be replaced

Could the software inflation be due to an annual increase in “per seat” license costs by Mag 7 players (MS, Google, Amazon) and the longer term trend of basically renting software (AWS, MS 365, etc.) among corporations rather than owning it.

If that is the case, perhaps the spike would be a once-a-year event (every January, the Mag 7 sticks it to you for/from the Cloud) and therefore not appropriate to annualize.

On a much, much (much) smaller scale, I know I was recently irritated by MS hiking its annual subscription fees for its individual cloud services (I was somewhat, but so far insufficiently, motivated to buy increasingly rare physical versions of MS Office to avoid just this sort of auto-inflation.

Here’s what you need, and it’s free:

https://www.libreoffice.org/

I never paid a dollar for MS Office. I am using it now for free (mostly Word and Excel) from their cloud. Again, never paid a dollar in subsriptions or anything. I created two free Outlook accounts and have two clouds (for different purposes) with free MS Office. What are people paying for? What am I missing?

Global RAM issues predating attacking Iran etc.

This was a classic supply/demand thing (AI), post a hormuz settlement who knows.

The Federal Reserve restarted Reserve Management Purchases (RMPs) in December 2025, it has purchased about $93 billion in securities through early March 2026.

Reserve balances with Federal Reserve Banks are: 3,026,708 up

+ 32,753 from the prior week. The FED is validating the increase in oil prices. Otherwise, core PCE would be lower as oil is largely inelastic in price.

Reserve balances are roughly flat from year end. And they will drop in the second half of April around Tax Day when liquidity drains from reserves into the TGA (government checking account at the Fed) as companies and individuals pay their taxes due for 2025, and pay their estimated quarterly taxes for Q1. I just paid mine GRRR.

These oil price increases have zero to do with reserves and everything to do with the war in Iran.

If oil prices rise P, and M*Vt stays the same, then T falls. But since oil is rather inelastic, core falls if the FED remains tight.

This is Exhibit A of why people, rightfully, ridicule basic economic formulas. they’re just silly. I went through that stuff in grad school and thought it was silly. And since then, it was confirmed over and over again that this stuff is silly. Reactions and relationships in the economy don’t work that way.

Wolf,

Like always, excellent article.

Based on spike in energy prices where do you think March PPI will land?

I just have a feeling that Potus and his buddies will find 10 different ways to keep energy out of CPI and PPI just like they did with OER (you have covered it in many articles over last few months) and keep inflation numbers artificially down. May be something like, war is an exception and its not our fault that one country has caused the disruption of more than 20% crude oil traffic so we are not going to count energy in PPI and CPI until supply is back to normal.

I hope I am wrong and energy will be included but I have to see it to believe it.

Don’t worry. Energy will be included, and it will be hot. It will push up all of the overall inflation measures: CPI (tomorrow), PPI (Tuesday), and PCE price index for March (Apr 30).

But CPI, PPI, and PCE also offer “core” versions, which exclude the costs of food and energy precisely because food and energy are so volatile, they plunge and spike. These “core” indices will eventually reflect higher energy costs as they push up prices of goods and services (for example, airline fares).

Typically, the current macroeconomic model is in flux which makes microeconomic projections statistically unreliable.

3% inflation is the new target. Be lucky to achieve that!

Agreed.

Can anyone come up with any argument or evidence to refute the following?

“The FOMC’s stated inflation target of 2% is irrelevant. Their actual inflation target is 3%.”

What was the Core Services PCE Price Index for February, both MoM and YoY?

+0.22% month-to-month (+2.6% annualized); +3.2% yoy

It got pushed down by the housing components, including the imputed OER, and also by a month-to-month plunge in recreation services: Recreation services dropped by -0.5% (-6.0% annualized) in March, after the big increases in the prior two months.

The FED is paying close attention. They’re planning a rate cut even now.

It says a lot about our society when nearly everyone(NOT ME) wants interest rates to be as low as possible,

It’s as if everyone was in hock up to their tits already and die’n to spend even more.

There was a time when people aspired to financial prudence.

Anecdotally, talked to a banker recently (single mom, not pretty at all, rather cranky) who said that she was hoping for interest rate to be dropped to zero. I’m amazed at how many bankers are almost all ignorant of economics and finance.

I guess that’s where they get central bankers from.

Watch the Big Short it’s very enlightening.

I love that movie! Sad ending though as taxpayers got handed a bag of $#!+ . The real ending should have been about bank CEOs and fund managers gutting their accounts and liquidating all assets to pay back what was never theirs to sell. A loan should never be able to transfer more than one degree from the originating underwriter. I wonder what level of leverage private creditors are at right now, especially the ones holding commercial real estate?Can’t wait for the real meltdown in private credit! Maybe that movie will become my new favorite.

No. The Federal Reserve is not planning any sort of ‘rate cut’ at all.

Any predictions for March through April once it’s released over the next couple of months? Monthly annualized PCE Price Index above 6%?

I agree. The Fed really needs to pay attention.

“How could you let this happen? You were supposed to be the night watchman”.

“I was watching. I saw the whole thing. First it started falling over… and then it fell over”.

I don’t think the Fed is serious about achieving its 2 percent inflation target, and I have doubts about whether they even care.

Stock market bubble update:

S&P 500 market cap now $61.843 Trillion, just a bit lower than the peak a few months ago. The top eight tech stocks still account for more than 35% of the index, at $21.93 Trillion.

They don’t care as long as investors still buy treasury bills. The bond market is what they care about most

I agree with you, I don’t think they’re concerned in the least if inflation doesn’t attract undo attention

So final Q4 GDP came in at .5% after another down revision and Atlanta fed now estimate is down to 1.3% from over 3%… Are we willing to accept stagflation yet?

If so what will the bond markets tell the Fed to prioritize growth or inflation?

Spending by the federal government COLLAPSED in Q4 in a historic manner due to the shutdown. That hugely pushed down GDP. But that spending was just delayed. It’s now flowing out in Q1 and will boost Q1 GDP. People will be surprised.

Mr Wolf writes: “The Fed Needs to Pay Attention[.]”

Article: Federal Reserve Bank of Minneapolis entitled: “Tariffs can’t explain rising goods inflation.” April 8, 2026. Authors: Neil Mehrotra and Michael E. Waugh.

Conclusion: “In short, accounting-based estimates of the contribution of tariffs to core PCE inflation may be overstating the impact of tariffs on core goods inflation. The underlying pattern of inflation within core goods is inconsistent with the predicted pattern of price increases from tariffs.”

Great report as usual. This is the only place to get an honest look at the various inflation reports.

“too-low interest rates”

yes.. the public must be re-educated – and soon – as well as Congress. If Jerome Powell and the FED were really working for “the american public” then he wouldn’t say “it’s not my job not to” when asked why he has enabled this mess. In senior leadership positions, where is it acceptable to say “it’s not my job”? honest question.

Voters reward empty promises and punish any vestiges of self-accountability. I challenge anyone to refute this statement.

What we’re seeing is a breakdown in the theory of democracy – the idea that voters will choose the best leaders. We are the failure point. The founding fathers never could have imagined people consuming 4-8 hours of media drivel each day, and being manipulated into voting against their own interests and the interests of their country. Yet here we are, living in the stupidest of times.

“Computer software and accessories”

Could this be mostly computer RAM? You mentioned software, but I couldn’t tell if you saw an actual line item separating software from the rest of the category.

No because see my line about “laptops and tablets” … their prices didn’t budge: “...information processing equipment, which includes “personal computers & tablets,” which are tariffed, but were unchanged month-to-month (+0%) and barely up year-over-year (+0.9%).“

If the FED was tight, there’d be movement in the interbank market.