The Bureau of Labor Statistics finally corrected part of the CPI distortions in September, October, and November.

By Wolf Richter for WOLF STREET.

The gasoline price spike hit CPI inflation for the second month, but electricity prices also spiked, core services inflation spiked – it’s the biggie, accounting for over 60% of CPI – and food prices jumped. So it’s a mess – and even if the Fed wants to “look through” the impact of the gasoline price spike, it’s going to smack into surging core services inflation, accelerating food inflation, and surging electricity inflation driven by the AI bubble.

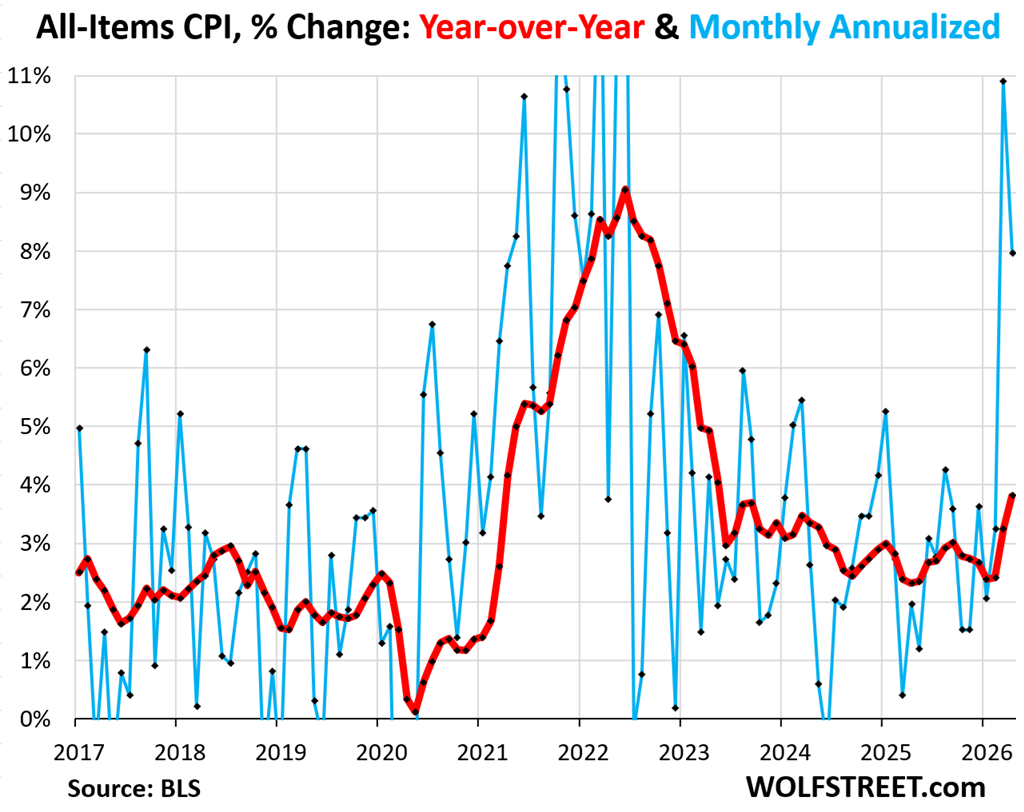

The all-items CPI spiked seasonally adjusted by 0.64% in April from March or by 8.0% annualized, on top of the majestic spike in the prior month (blue line in the chart). Not seasonally adjusted, it was even worse: +0.85% (+10.7% annualized).

Year-over-year, the all-items CPI jumped by 3.81%, the worst inflation reading since April 2023, according to data from the Bureau of Labor Statistics today (red in the chart).

Negative “real” rates: The year-over-year CPI, rising by 3.8%, has now blown by the Federal Reserve’s policy interest rates of 3.5% to 3.75%, thereby turning the Fed’s policy rates negative in “real” terms (adjusted for CPI). This situation of short-term borrowing costs below the rate of inflation is stimulative of inflation and of the economy. The bond market should freak out if the Fed sits on its hands and watches it play out.

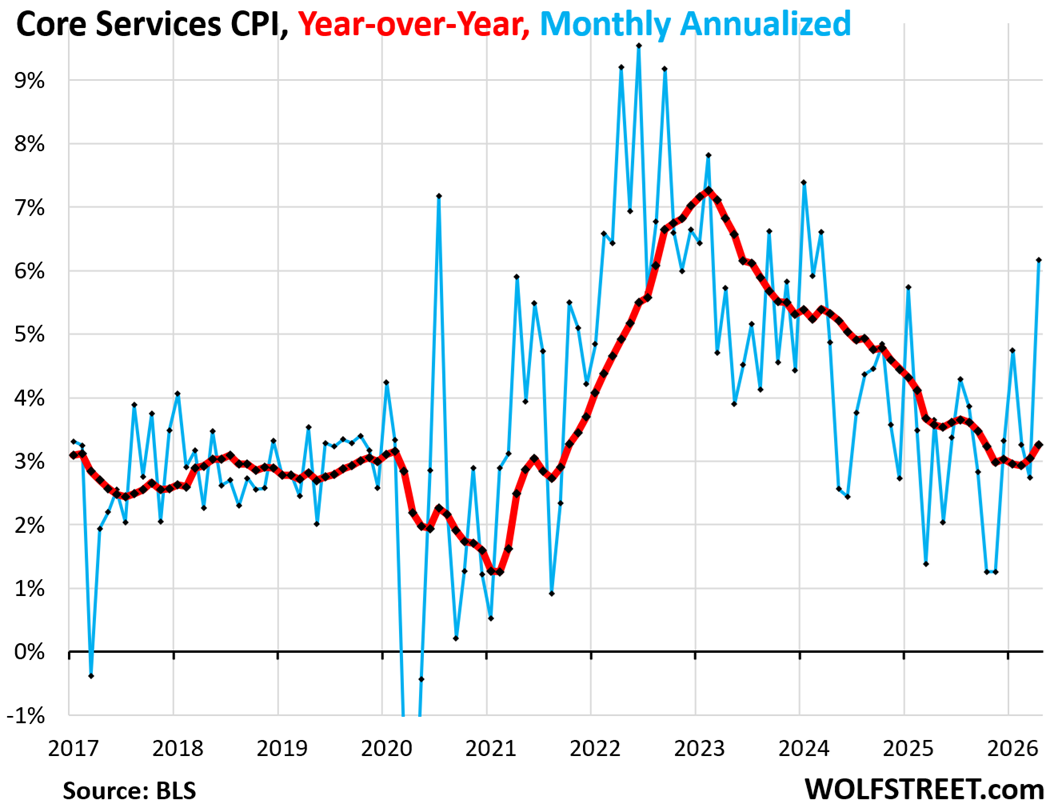

The CPI for core services, which excludes energy utilities such as electricity, jumped by 0.50% (+6.2% annualized) in April from March, the worst spike since March 2024 (blue in the chart below).

It was driven by hot inflation in housing (Rent and Owners Equivalent of Rent, see below), lodging away from home including hotels and motels, and airline fares. It weighs over 60% in the all-items CPI.

Year-over-year, it accelerated to +3.3% (red line).

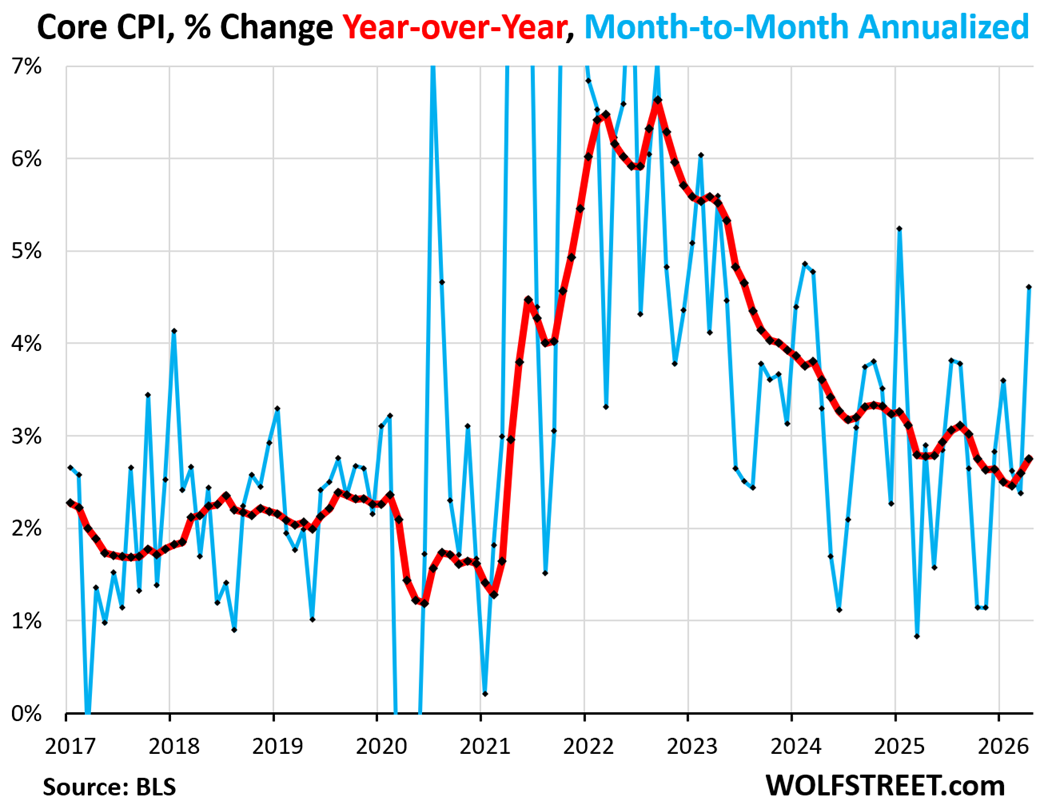

The “core CPI,” which excludes the spike in energy prices and food prices, jumped by 0.38% in April from March (+4.6% annualized), the worst increase since January 2025.

Year-over-year, it accelerated to +2.8%, the second month in a row of acceleration and the worst reading since September (red line).

The core CPI is dominated by the core services CPI, but also includes all goods except food and energy goods.

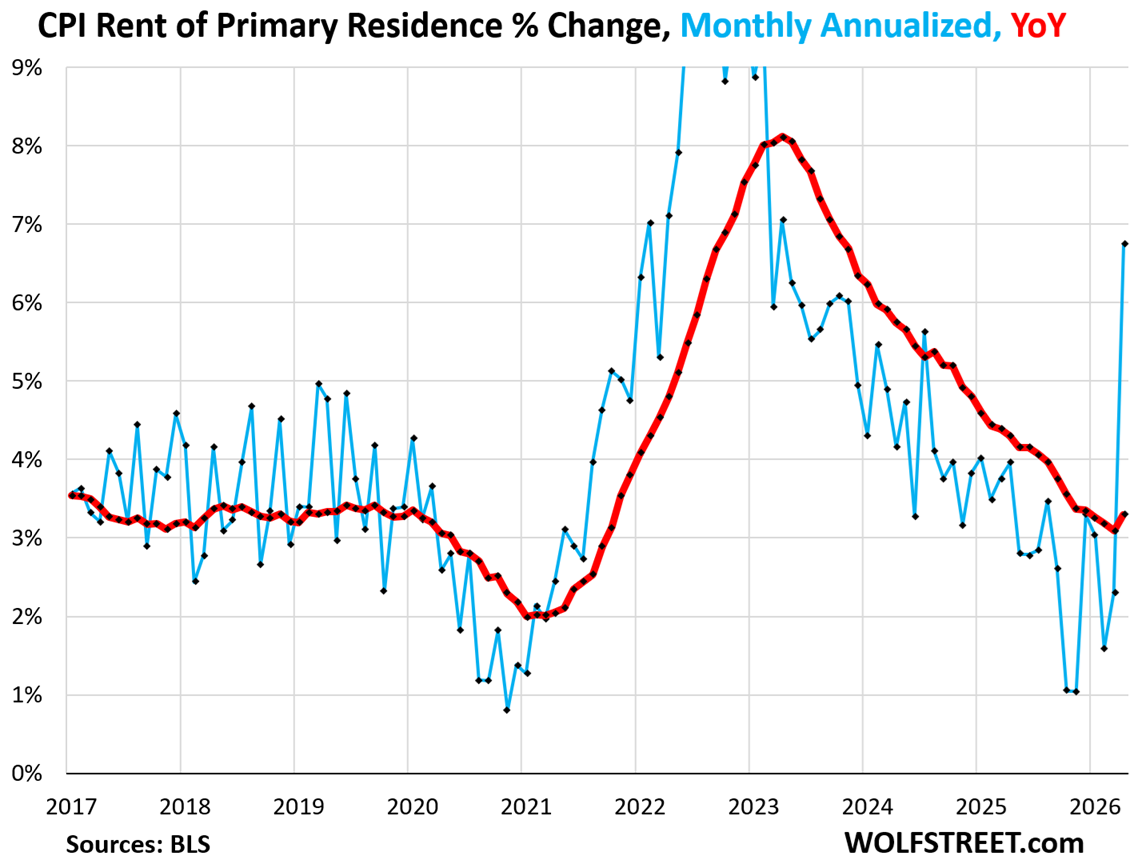

The CPI for rent of primary residence spiked by 0.54% in April from March (+6.7% annualized). The spike corrected for part of the distortions in September, October, and November last year that I lambasted month after month.

So this month-to-month spike in April does not reflect a spike in actual rents but a methodical correction of the distortions in September, October, and November. Actual rent inflation has calmed down quite a bit, with a widening gap between multifamily rentals and single-family rentals (my analysis on the widening gap between them in 14 of the biggest markets).

Year-over-year, the CPI for rent rose by 3.3%, the biggest increase since December.

The CPI for rent of primary residence weighs 7.7% in the all-items CPI.

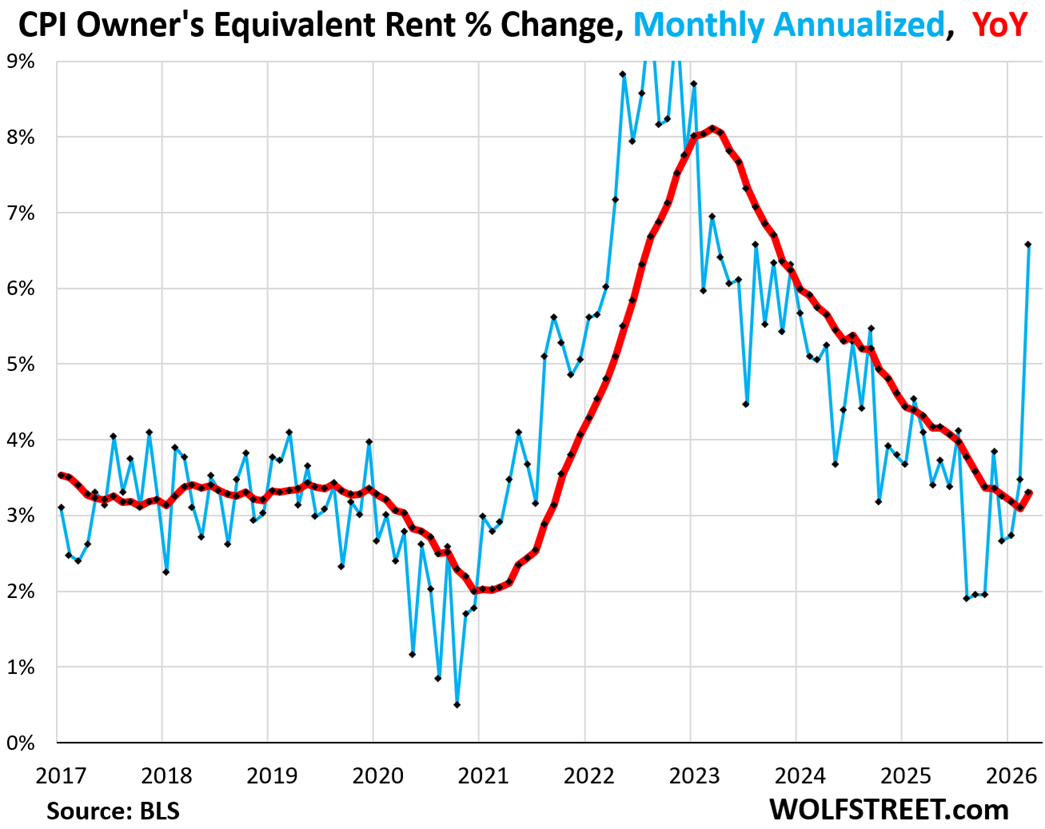

The CPI for Owners’ equivalent of rent (OER) spike by 0.53% (+6.6% annualized) in April after the same type of catch-up correction as the BLS had done to the rent CPI.

Year-over-year, it accelerated to 3.3% (red line).

The CPI for OER weighs 25.9% in the all-items CPI. Combined, rent and OER weigh 33.6% of the all-items CPI.

OER tracks what a large panel of homeowners think their home would rent for; it’s a lazy stand-in for costs that homeowners actually face, such as homeowner’s insurance, property taxes, HOA fees, repairs and maintenance, which are not included in CPI, and which are much harder to track accurately (but other countries, such as Canada, do it). It is a fundamentally flawed metric in the CPI and should be replaced by the actual costs homeowners face.

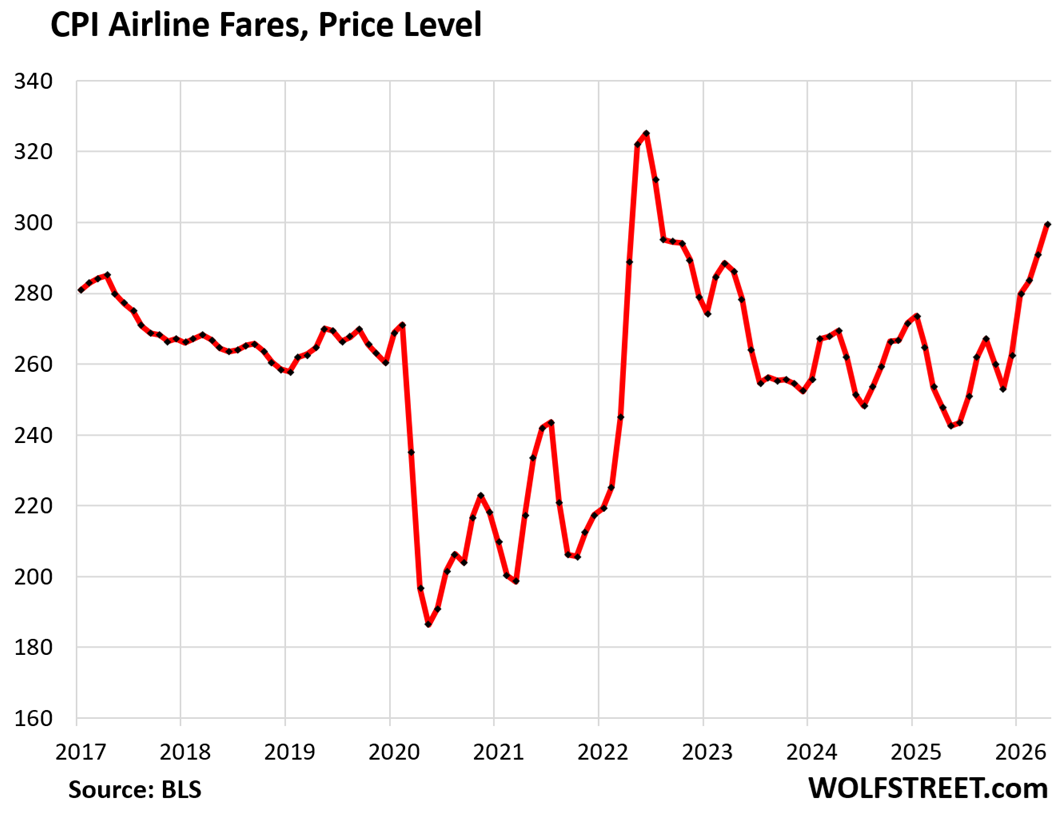

The CPI for airline fares spiked by 2.8% in April from March (not annualized), the second spike like this in a row.

Year-over-year, it spiked by 20.7%. Fuel prices are one driver; another driver is the collapse of Spirit Airlines, whose low fares had kept a lid on price increases of competing routes.

This chart shows the price level of airline fares, not the percentage changes. The price surge began in December. But prices haven’t yet reached the peaks of mid-2022.

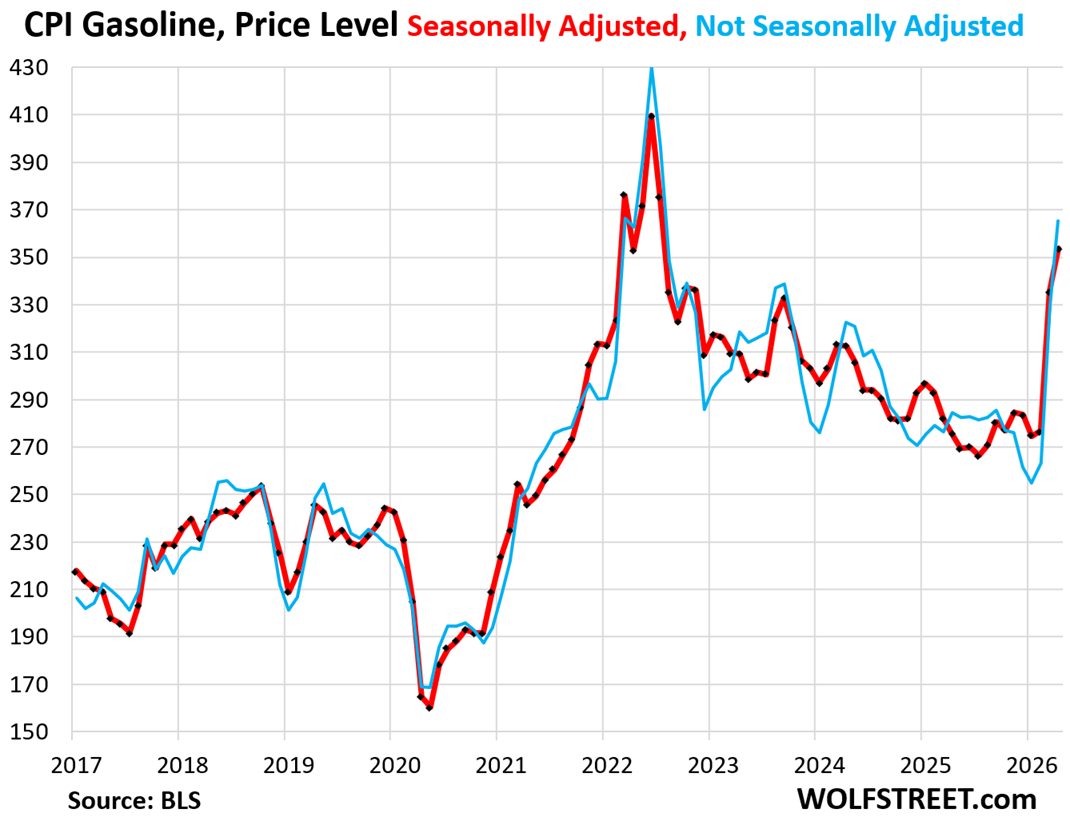

Energy inflation boils down to gasoline and electricity.

Gasoline prices, after a huge spike, tend to fall back at least partially. But electricity, provided by utilities to consumers, is a regulated service, and it just marches higher and higher, though more steadily than gasoline.

The CPI for gasoline spiked by 5.4% in April from March, seasonally adjusted, and by 11% not seasonally adjusted.

Year-over-year, it spiked by 28%.

In terms of the price level, which the chart shows, prices are now approaching the peak of the prior bout of inflation in mid-2022.

The Fed is going to “look through” this spike, expecting that it will subside eventually, but it cannot look through the non-gasoline parts of inflation.

The CPI for gasoline of all types weighs 3.6% of the all-items CPI.

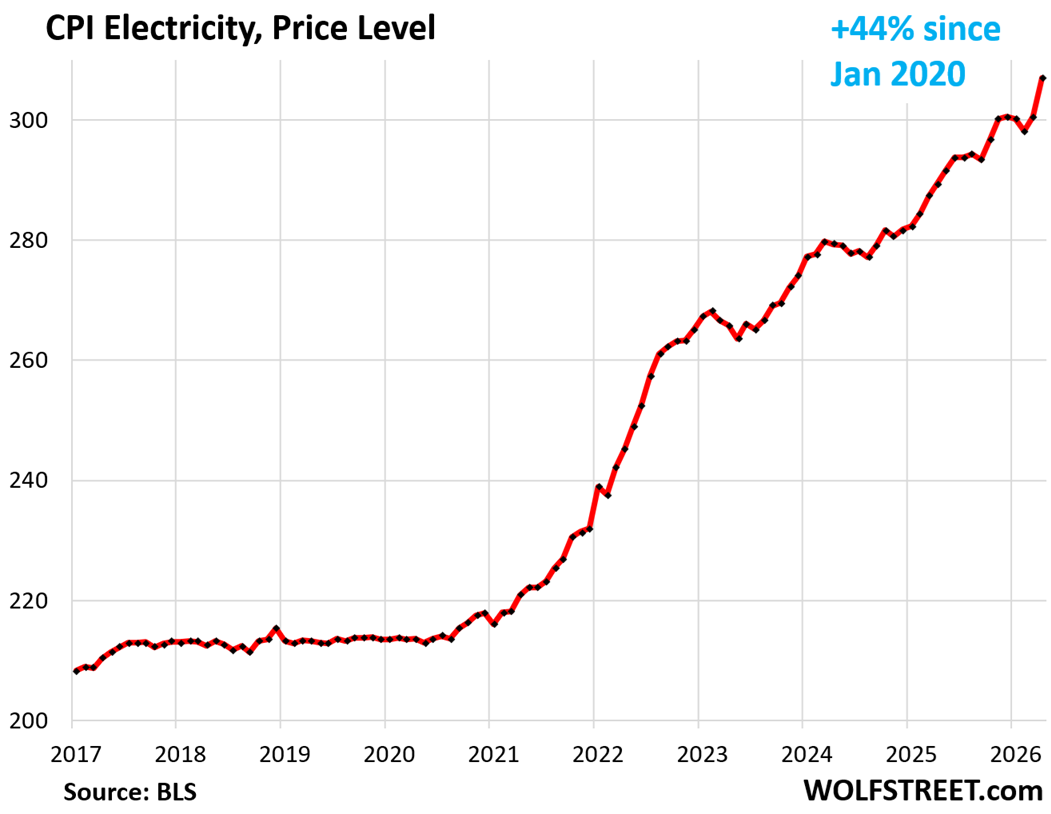

The CPI for electricity spiked by 2.1% in April from March, after the 0.82% jump in March from February.

Year-over-year, it jumped by 6.1%. Since January 2020, the index has soared by 44%.

The price that households pay for electricity on their monthly bills – the fixed fees and charges and the price per kWh used – is largely set by utilities that are monopolies. Some of the utilities are owned by public entities, such as a municipality; some are owned by their ratepayers, such as co-ops; others are investor-owned regulated monopolies, and investors come first. The only competition these electric utilities face is rooftop and plug-in solar.

Data centers are rapidly increasing the demand for electricity (see chart and data), but it takes a long time to build power plants. And regulator-approved price surges are the consequence. Electricity prices generally don’t fall back, and price increases are permanent, to be followed by more price increases.

The Fed cannot look through that type of AI-caused energy inflation. The CPI for electricity weighs 2.5% in the all-items CPI.

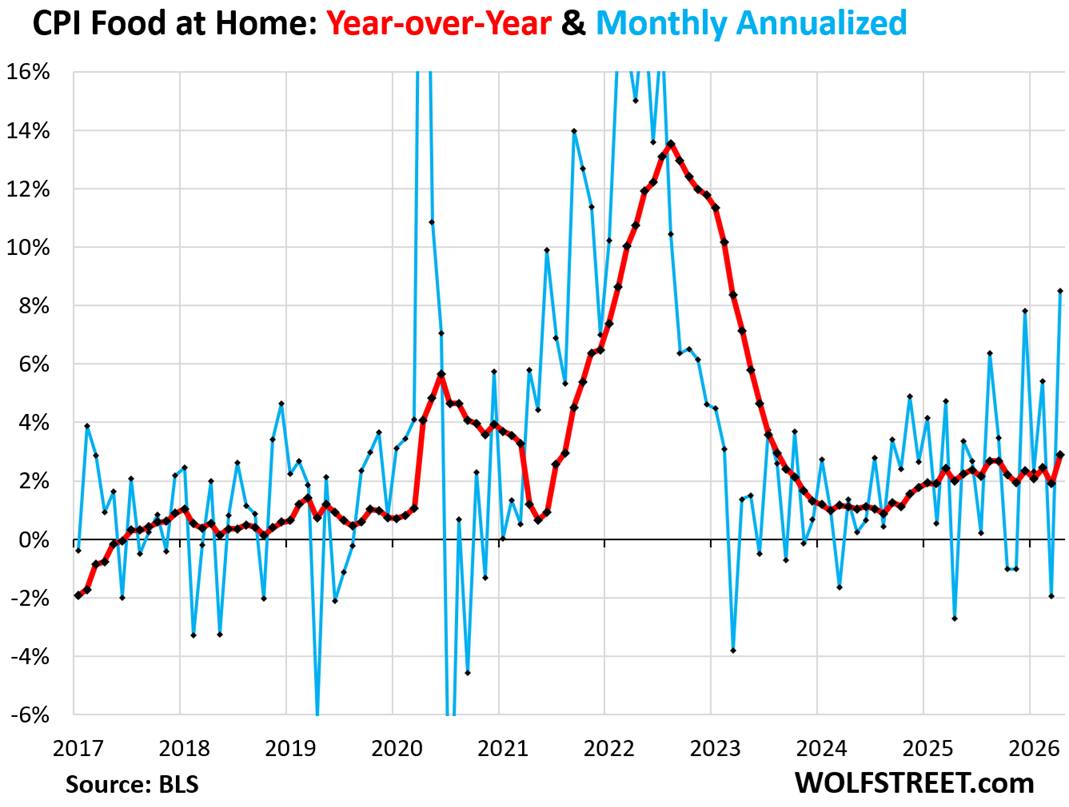

The CPI for food at home jumped by 0.68% in April from March (+8.5% annualized), the biggest month-to-month increase since August 2023, after a small dip in the prior month.

Year-over-year, food inflation rose by 2.9%, also the worst increase since August 2023. Note the acceleration over the past two years (red line).

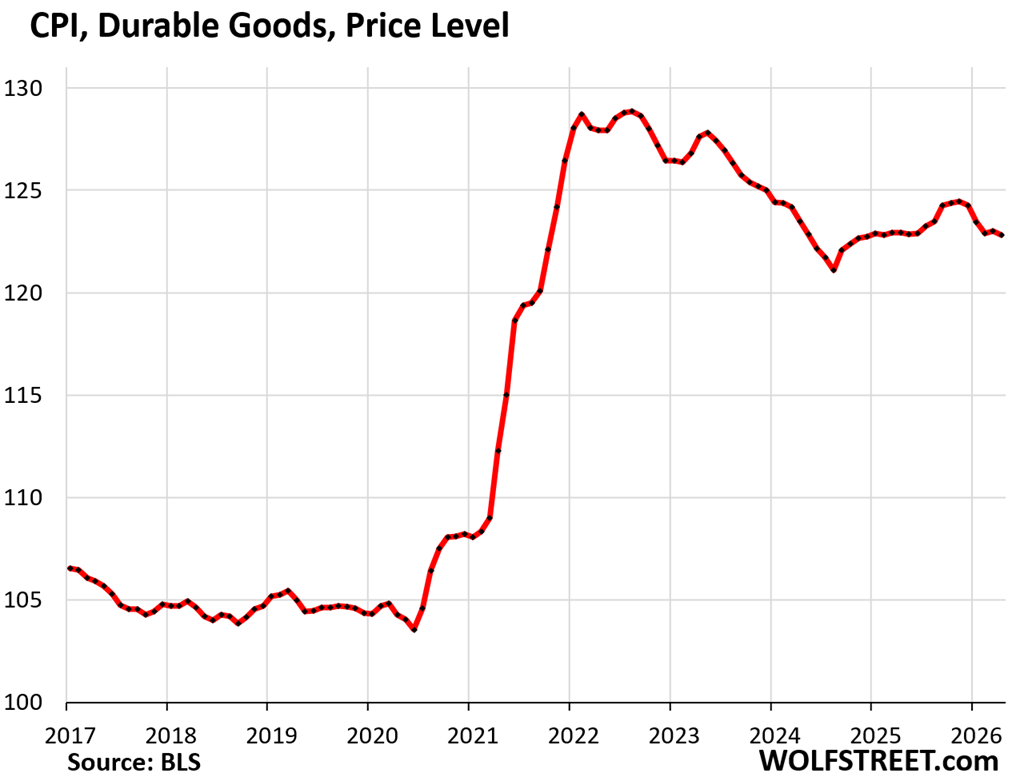

The CPI for durable goods dipped in March and was unchanged year-over-year. The chart shows the price level of durable goods CPI. Durable goods prices have come down from the peak in mid-2022, but not by much.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

– And no, the FED won’t raise rates. I consider it to be more likely that the FED will leave rates at the current level and perhaps even lower rates.

I work in manufacturing sector and we just received 30% price hike for our raw materials. Even during Covid we did not see 30% hike in one single transaction. We have passed it to our customers and who will be doing the same to their customers and we will be paying for it in coming months. If this war continues, this CPI is a good news compared to what is about to come. What most baffling is – Market is barely down since CPI release. Its like Market is living in alternate dimension these days.

in the long run, high inflation in the CPI will cause the stock market and real estate to go up.

This is one of the worst times to go into cash.

It doesn’t matter if you are diversified in cash, stocks, RE, bonds, metals, etc., and have hedges in place where needed.

Investments are not all-or-nothing propositions.

This is only true if we don’t get stagflation.

We’re not seeing inflation in wages so real estate won’t go up. Real estate is limited by purchasing power.

Isn’t everything limit by purchasing power?

If my homeowner’s insurance keeps going up and CPI doesn’t effectively capture this, over the next 5 years or so, it’s going to be a major issue for people’s ability to afford insurance.

This can be said about all sorts of things like food & car insurance, for example. Nowadays, these are necessities just like housing.

I dunno, one advisor I follow says cash is ok.

Especially if the bubble pops in tech.

In 2000 the index valuations got so weighted that it was a real problem, fund managers were arguing that the weights were going to kill their funds when the stocks dropped. And a lot were battered badly.

Problem is the indexes are setup to put weight to the most valuable stocks. But then they suck up all the demand.

So the indexer thinks he/she is safe, but then Nvidia, AMD etc etc all drop 50% (albeit slowly), then there goes 10-20% or more of the index’s value.

Then we have a lost decade and your losses fester for 10 years. If you hang on, you’re 20 years older when the recovery happens.

Real fun stuff 😬

Manufacturing and same here, seeing some pretty big jumps in raw materials (prior to the war even), that kind of came out of no where. Expecting more to come, so this inflation cycle is probably just warming up.

I am curious to see where tariff refunds are being put now that companies are getting them back. Seems potentially inflationary as well.

This calls for a rate cut, no?

Howdy Lone Wolf. Great honest article… All the Govern ment Bean Counters need to do , like most do ???? Use the term. ” As Expected “.

Party on Sailors. I plan too..

Shit show

If you are a borrower, it’s a great show.

The 30 year is above 5% today. 10 year is pushing close to 4.5%. I dislike politics in economics discussions, but the services and electricity prints were already coming in hot and the escapade in the desert is just making things messier not to mention the extra borrowing required to fund the military and potential gas tax suspension. Rates are going to spike with US debt interest payments becoming even costlier. Sometimes it’s best to cut your losses while you can.

Also, it’s time to actually deal with taxes and overspending. It’s going to require a mixture of budget cuts and taxes to stave off the looming debt spiral. We need a reset.

This isn’t what folks voted for, that’s for sure.

“We’ll just spend our way thru this inflation” seems to be the operating philosophy.

How is it possible that inflation is elevated well beyond Fed comfort and housing is stalled (to put it lightly) and no inclination of a recession? GDP is growing and yet inflation and housing are major obstacles?

October 22, 1979 the Volcker shock was delivered. A single rate increase of 250 basis points. We might need that again.

🤣❤️ that would be a hoot

Certainly a 250 shot is not likely, but what happens in July when the Fed has to decide again if inflation is “transitory”?

Personally, I’m looking forward to a rate increase. I’d like to see how the markets react.

If we can’t have a recession, then I’d certainly want the annual 15-20% drop to by the dip.

Ah sorry, inflation of and in itself is not harmful. Only unexpected inflation is bad because business managers can’t necessarily adjust to the unexpected.

Deflation is absolutely the worst.

Ah, yes, okay. Let me check with the starving masses. According to Mr. Google,

“As of May 2026, high food inflation is driving a global hunger crisis, with 52 million people projected to face acute food insecurity”

Seems pretty harmless to you, eh?

These charts just reinforce the incompetence of our federal government.

Its clear to me the world would be a better place today without the massive covid intervention.

Bernanke started in with QE.

Just sayin.

The only question left is will the 20/30 year bonds hold 5+% this time. If so, and TNX gets to 5 then we’ll see 30 year fixed mortgages at 7% as business as usual and the summer home buying season will be Gone with the Wind. 7.5-8% is conceivable by EOY. I thought last year but Powell had other ideas. Lucky for Powell, his revenge is having Trump and gang left on stage to answer stupid questions instead of him.

What a mess. A serious Fed would dispense the medicine now, instead of waiting for the data to get even worse. But like the other commenters, I see next to zero chance of that happening.

Americans have been told that they are energy independent but what most fail to understand is that energy prices are set at the margin by international markets! Big difference that is lost on most people.

Looks like the Strait will be closed for an extended period of time. Iran is in total control considering, among other things, they are the largest drone maker in the world. Inflation in the US is just getting started unfortunately…

So you said that the BLS finally corrected for part of the CPI distortions in September, October, and November. Approximately what percent of the distortions from that period would you say were corrected, and approximately what percent remain?

The Fed has a 2% inflation target, therefore inflation will average 2% over time. The Fed is telling us this, so it must be true.

FOMC should have raised at the last meeting to front-run some of this shit show. What did they have to lose? Powell is already on the way out and the others aren’t getting the chairman’s seat.

The average homeless man on the street knows how much a 7-Eleven hotdog is costing him now, but an institution with as many resources as the Fed doesn’t see this coming after 2-months of warfare? … And this is just the beginning.

What even is the point anymore?

This inflationary episode seemed extra predictable.

Anyways, I don’t see Warsh and the rest pissing off trump at his first meeting as chair by raising. So we’ll have another Fed is late because reasons and let inflation get out of hand a couple of quarters.

Gasoline inflation is baked in because of the air gap. Electricity inflation is baked in from the AI capex spend / contracts. Food inflation is baked in because of the fertilizer increases. The strait could open tomorrow and not much changes.

But the real chaos starts after inventories run out and it’s a free for all for bidding for demand destruction. We will see how bad that gets.

The Electricity CPI graph looked awfully stable up until the dawn of the data center age.

So if AI doesn’t take us out as fast as some fear, the high cost of running all of these servers in data centers certainly will.