The effects of Tax Day. The 10-Year Treasury yield rose to 4.31%, 30-Year Treasury yield to 4.91%.

By Wolf Richter for WOLF STREET.

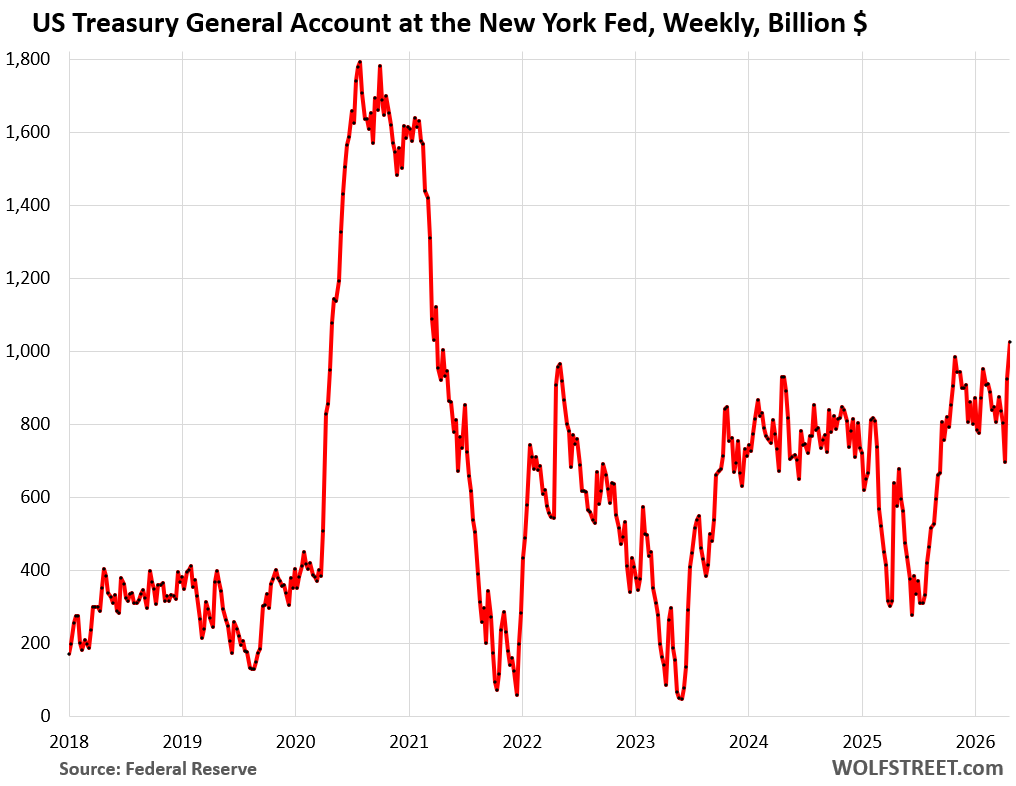

Around Tax Day, large amounts of cash from estimated quarterly taxes, capital gains taxes, and underpaid income taxes from businesses and individuals flow into the government’s coffers, and the balance of the government’s checking account, the Treasury General Account (TGA), has swollen to over $1 trillion, the highest since April 2021.

In response to this seasonal influx of cash, the Treasury Department has trimmed back the issuance of Treasury bills (terms of 4-52 weeks) in recent weeks, including this week. Trimming back the issuance of T-bills has caused the overall debt to dip below $39 trillion again, even though the outstanding balance of Treasury notes (2-10 years) and bonds (20 and 30 years) continued to grow. When this cash influx slows in May, the Treasury Department will increase the issuance of T-bills again.

The Treasury Department has increased the “desired level” of the TGA to $900 billion this spring, from $800 billion a year ago, to comfortably accommodate the huge amounts of cash flowing through that account on a daily basis, including the amounts needed to pay off the maturing debt of over $500 billion a week.

The US government sold $524 billion of Treasury securities this week, in eight auctions. Of these auction sales, $480 billion were Treasury bills, with maturities from 4 weeks to 26 weeks, most or all of them to replace maturing T-bills.

Amid this seasonal influx of cash, the Treasury Department reduced the size of three T-bill auctions (4-week, 6-week, 8-week) this week by a total of $35 billion compared to the same week in March.

| Type | Auction date | Billion $ | High Rate | Investment Rate |

| Bills 4-week | Apr-23 | 81 | 3.60% | 3.66% |

| Bills 6-week | Apr-21 | 75 | 3.61% | 3.68% |

| Bills 8-week | Apr-23 | 76 | 3.61% | 3.68% |

| Bills 13-week | Apr-20 | 95 | 3.61% | 3.69% |

| Bills 17-week | Apr-22 | 70 | 3.61% | 3.70% |

| Bills 26-week | Apr-20 | 83 | 3.59% | 3.71% |

| Bills | 480 |

“High rate” v. “Investment Rate”: The Treasury Department provides two different calculations of the yield at which T-bills were sold at auction.

T-bills are sold at a discount to face value, and at maturity, the holder gets paid face value; the difference is the interest. There are no coupon interest payments, unlike with notes and bonds. The “high rate” reflects the yield of that process.

But the fact that T-bills have no coupon interest payments makes the “high rate” calculation not comparable to Treasury notes and bonds where holders are paid interest every six months. So the Treasury Department also provides a conversion calculation of this discount yield into a yield that is equivalent to the yields of coupon securities, so that these yields can be compared, and it calls this yield the “investment rate.” Both the “high rate” and the “investment rate” are published in the auction results of T-bills.

This investment rate is higher than the “high rate” and matches fairly closely the “constant maturity yield” published for trading in the secondary market around the time of the auction.

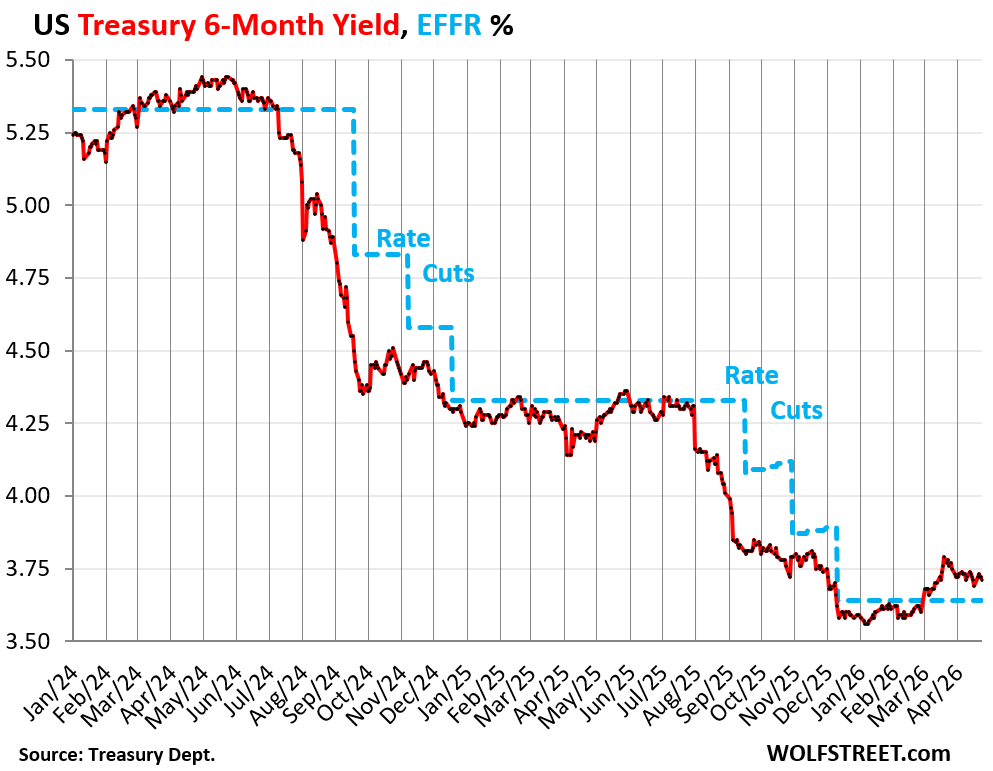

6-month T-bills, for example, sold at a “high yield” of 3.59% on April 20. But when recalculated as a coupon-equivalent “investment rate,” it was 3.71%. The auction took place in the morning of April 20. In the secondary market at the same time, the 6-month constant maturity yield was also around 3.71%.

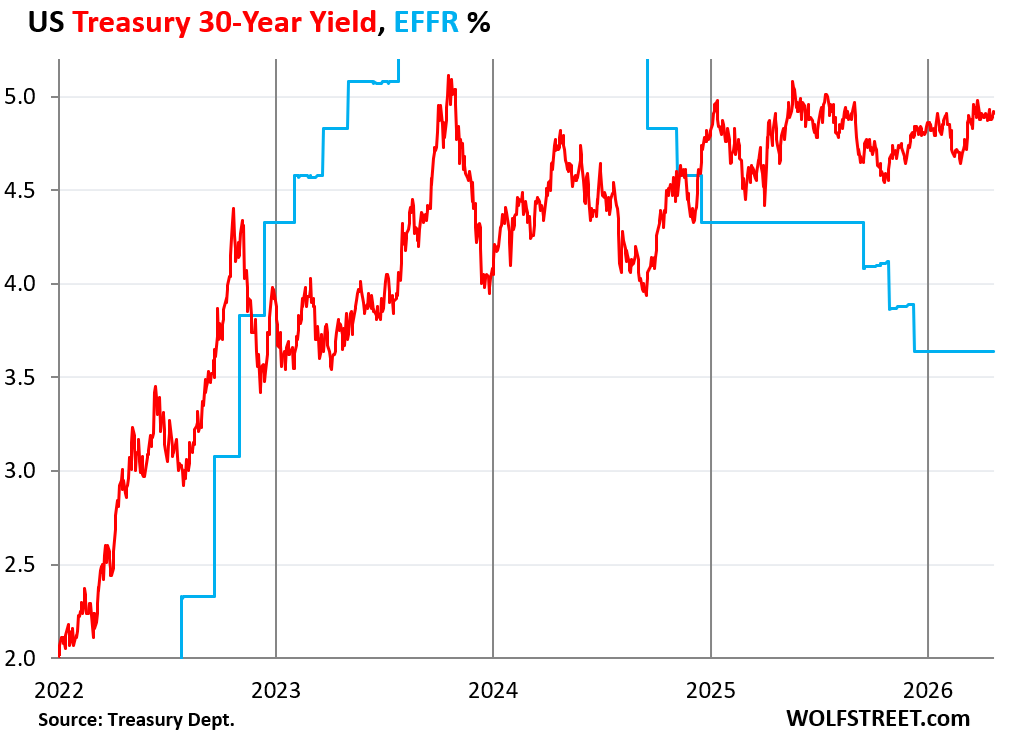

The 6-month yield, which closed on Friday at 3.71%, is currently above the Effective Federal Funds Rate (EFFR) of 3.64%, which the Fed targets with its policy rates. This shows that the bond market sees no rate cut in the six-month window, but maybe a slight chance of a rate hike.

But inflation rates are on track to surpass T-bill yields, or already surpassed T-bill yields, depending on the inflation measure. But T-bills are bracketed by the Fed’s five policy rates and react to those policy rates and the expected policy rates – they don’t react to inflation fears.

The PCE price index, which the Fed favors for tracking consumer price inflation, has moved close to 3.0% year-over-year through February, not yet including the energy price spike in March.

But the last three month-to-month readings through February were all near or above 4% annualized. The March readings, to be released next week, will spike from there due to the fuel price spike. These readings are already above T-bill yields.

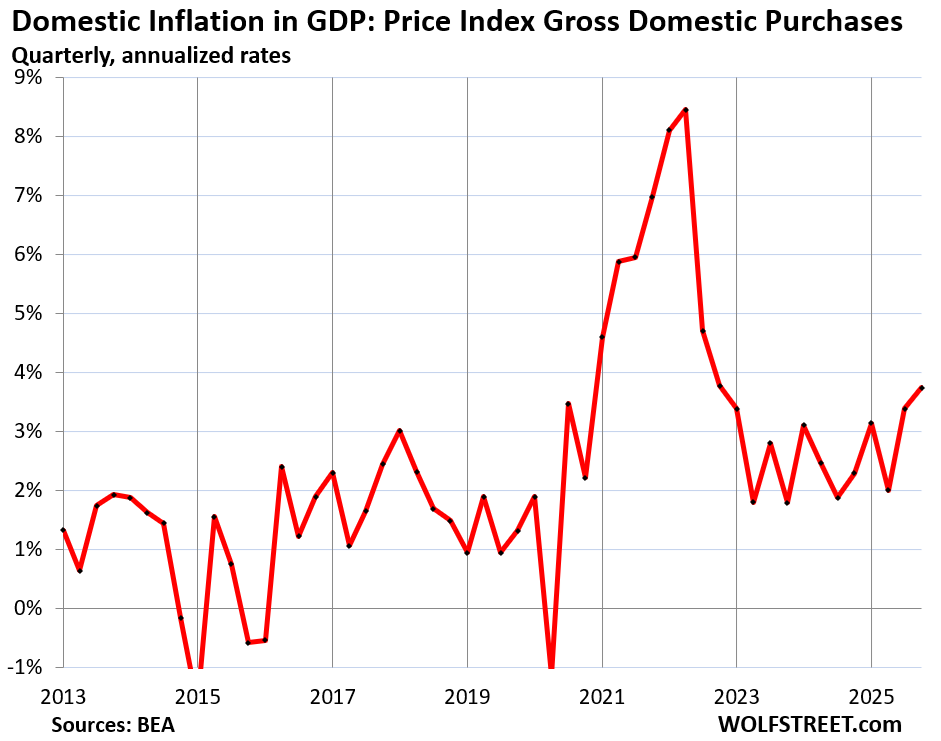

The Price Index for Gross Domestic Purchases, an inflation index for the broad domestic economy that tracks inflation facing consumers, businesses, and governments and reflects inflation in GDP, accelerated to 3.1% year-over-year in Q4, not including the energy price spike in Q1.

But it accelerated in Q4 from Q3 to 3.75% annualized, so already above T-bill yields.

The Q1 measure of this inflation index will be released next week, and it will contain the fuel price spike across the economy in March, which will likely push that inflation rate further above T-bill yields.

The US government also sold $44 billion of Treasury notes and bonds this week, spread over two auctions: 5-Year Treasury Inflation Protected Securities (TIPS) and 20-year Treasury bonds.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| TIPS 5-year | Apr-23 | 29 | *1.37% |

| Bonds 20-year | Apr-22 | 15 | 4.88% |

| Notes & bonds | 44 |

*TIPS yield is paid on top of the inflation protection that TIPS holders receive. This inflation protection is based on CPI and is added to the principal, and so the principal of the TIPS grows over time with CPI. The interest rate (the percentage is fixed for the term of the TIPS) is applied to the entire principal, including the inflation protection. As the principal grows over time with CPI, the interest payments increase, though the interest rate remains fixed.

In a year when CPI averages 5.0%, these 5-year TIPS sold at auction on April 23 with a yield of 1.37% will earn 6.37% combined. The 5.0% of inflation protection will be added to the principal, and the 1.37% interest will be paid on the total of the original principal plus the accumulated inflation protection.

TIPS have nasty tax consequences though: the inflation protection counts as taxable income. Each year, the portion of inflation protection that was added that year will show up on the 1099-INT for that year — so TIPS trigger a tax liability every year on the inflation protection that won’t actually be paid until maturity. Keeping TIPS in a tax-deferred account, such as an IRA, avoids that issue.

Brutal bond math: The $15 billion of 20-year bonds, with a coupon interest of 4.625%, were sold on Wednesday at 96.74 cents on the dollar to get to a yield of 4.88%, which is where the yield in the secondary market was running at the time. On Friday, the 20-year yield in the secondary market also closed at 4.88%.

But there won’t be any 20-year bonds maturing until 2040 because the Treasury Department halted the issuance of 20-year bonds in 1986 and restarted issuance in 2020, and the entire $15 billion of 20-year Treasury bonds sold this week add to the overall debt as no 20-year bonds matured.

This is how the long-term debt grows. 20-year bonds are new, and every single issue adds the entire amount to the long-term debt.

Similarly, with longer-term notes and 30-year bonds when they’re sold at auction: The maturing issues are much smaller than the current auction sales, and the difference adds to the long-term debt. Even if the government doesn’t further increase the size of the note and bond auctions, the outstanding balance of notes and bonds will continue to grow as much bigger new issues replace the maturing issues.

In recent months, for example, 10-year notes were sold in issues of $45-$50 billion at the monthly auctions, replacing maturing notes issued 10 years ago, of $20-$25 billion. So at each 10-year Treasury auction, the outstanding balance of 10-year Treasuries increased by about $20 billion.

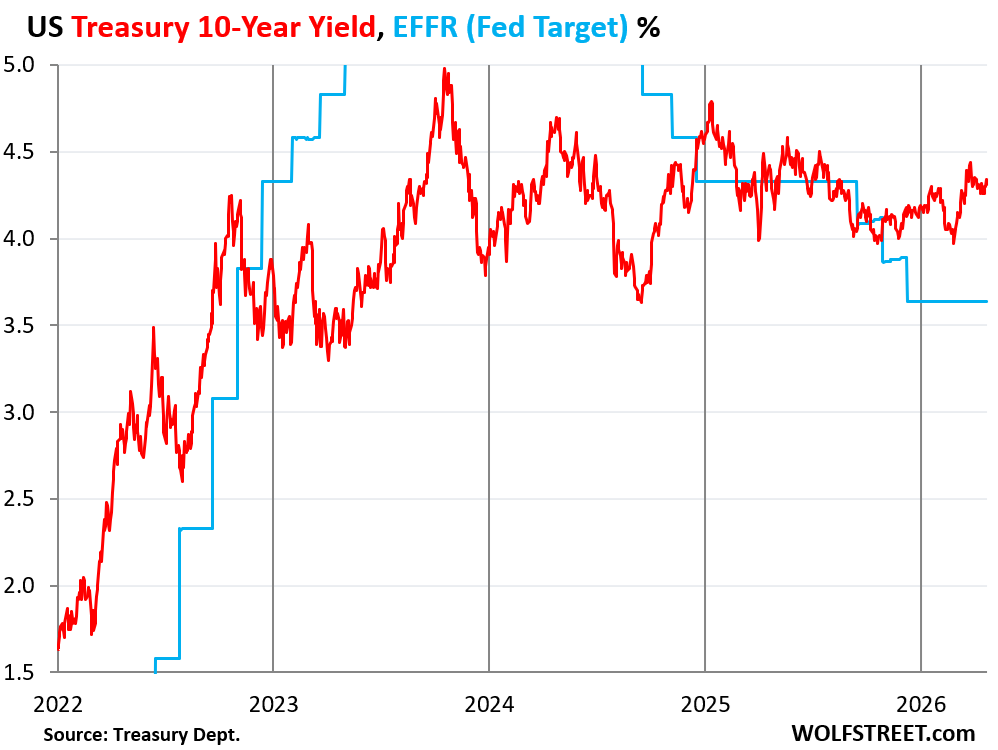

The 10-year Treasury yield rose by 5 basis points during the week to 4.31% on Friday, back to where it had been two weeks ago.

Higher bond yields in the market mean lower bond prices for existing holders, and vice-versa.

That longer end of the bond market doesn’t dance to the drumbeat of the Fed’s policy rates, but to fears and hopes about the future, especially the imagined path of inflation and the expected supply of Treasuries to fund the ballooning deficits that may require higher yields to attract ever more investors.

The 30-year Treasury yield edged up to 4.91% on Friday, up by 3 basis points from a week ago, and up 1 basis point from two weeks ago – so minimally changed over the past two weeks.

It has been hovering near 5% since mid-March. Over the past three years, it exceeded 5% several times briefly.

Obviously, the very long end of the Treasury market completely blew off the Fed’s rate cuts. What we can see is how the end of QE at the beginning of 2022 and the start of QT in the second half of 2022 allowed those long yields to rise:

In case you missed it: The Largest Foreign Holders of US Treasury Securities and the “Basis Trade”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yields still seem low given the current environment. But what do I know!?

Agreed but I think it might be good relative to what might be coming. Unlikely rates will increase and not out of the question short term sees some small cuts over next 18 months.

Why do you think short term rates would see some small cuts? The last six or so times the Fed did that resulted in the market pushing long term rates higher. Each cut, same result. It seems likely we’d be looking at sustained seven-handle mortgage rates going down that path. I sure wouldn’t want to have to answer for causing that, especially if I just started a new job at the Fed.

The 10-year Treasury was yielding 0.5% right before inflation exploded up to 9%. Yet they tell us the bond market knows what is coming.

No. That was the effect of QE, when the Fed was buying every 10-year in sight. I explained that in the article. That’s what QE does and is supposed to do. And you know that.

Thank you for explaining these auctions in such detail.

“including the amounts needed to pay off the maturing debt of over $500 billion a week”

Insane

The current situation isn’t too far from ZIRP on a real basis.

3.6% interest less 3.6% inflation = 0%

“A billion here, a billion there, and pretty soon you’re talking real money”…. update that to “A Trillion here….”