10th liquefaction & export terminal shipped first cargo. List of LNG export terminals, operating and under construction, by in-service date.

By Wolf Richter for WOLF STREET.

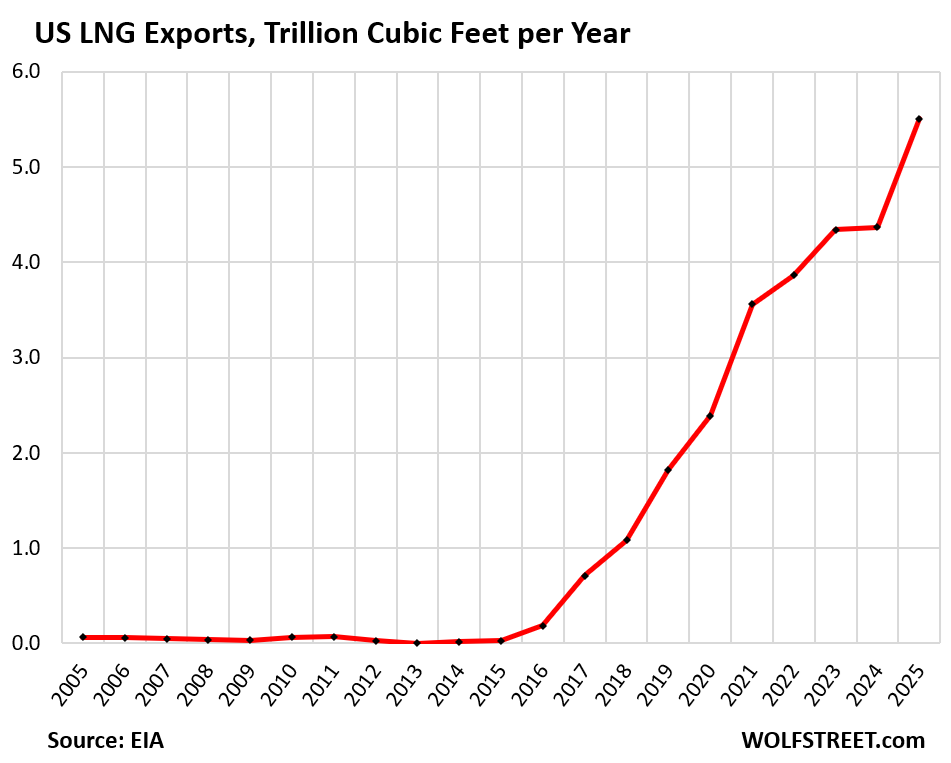

Exports of liquefied natural gas (LNG) took off when the first liquefaction train and export terminal in the lower 48 states, Cheniere Energy’s Sabine Pass in Louisiana, began operating in 2016.

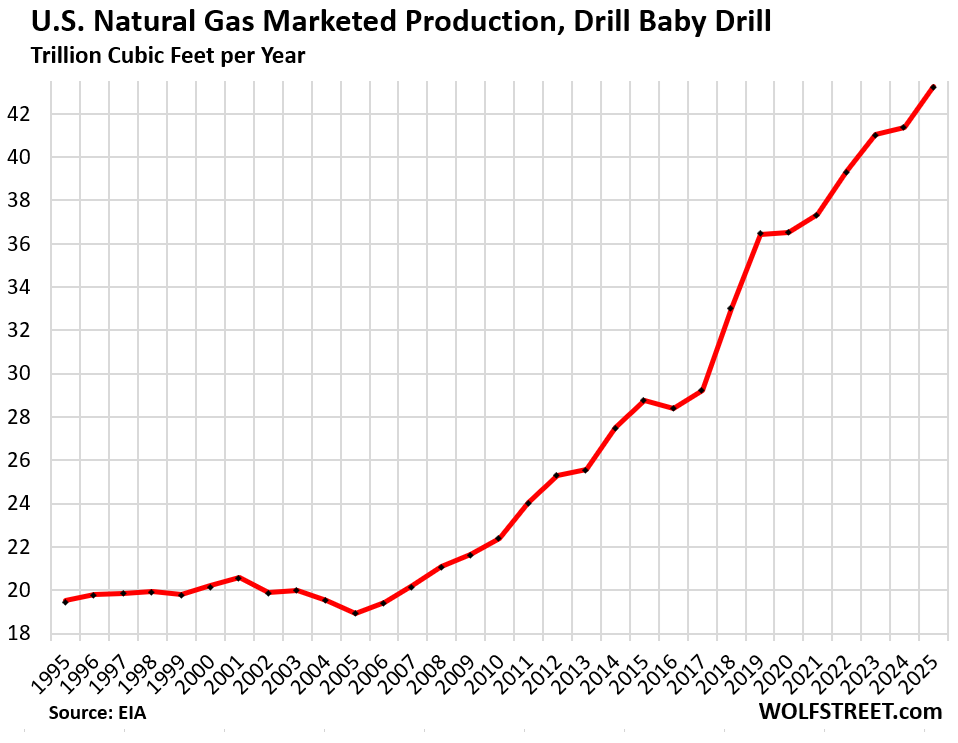

The ramp-up of fracking turned the US into the largest natural gas producer in the world by 2011, and generated a massive glut of natural gas in the US that no one knew how to throttle because a substantial portion of natural gas is a byproduct from fracked oil wells, and so with no exit for this production, other than by pipeline to Mexico, the price had collapsed, and hundreds of drillers went bankrupt in 2016.

LNG exports provided an outlet. LNG exports are limited only by the capacity of the export terminals, and this became a gigantic business, with new export terminals getting built for billions of dollars each in Louisiana, Texas, Georgia, and Maryland.

The newest and 10th LNG export terminal in the US, Golden Pass LNG in Texas, operated by Qatar Petroleum and ExxonMobil, shipped its first LNG cargo yesterday from liquefaction Train 1. Train 2 is scheduled to be completed later in 2026, and Train 3 in early 2027.

When all three trains are operational, they will have a combined nominal capacity of 16.6 million tonnes per annum (Mtpa) and a peak capacity of 18 Mtpa, according to EIA data. Export terminals normally run at over 100% of nominal capacity but less than peak capacity.

This brings the total operating capacity in the US to 121.8 Mtpa nominal and 147.8 Mtpa peak.

Numerous facilities are under construction, including Train 2 and Train 3 of Golden Pass, and they combined will add a nominal capacity of 100.9 Mtpa and a peak capacity of 118.6 Mtpa by 2031, over 40% of which is expected to start commercial operations in 2027. See table below.

It takes years to build a liquefaction and export facility. The investment decision for Golden Pass LNG was made in February 2019, and the first cargo was shipped in April 2026. But that project was delayed because the lead construction contractor, Zachry Holdings, filed for bankruptcy in 2024. This tangled the project up in court, and it took a while before a new lead contractor, Chiyoda International Corp, could take over.

When fully operational, Golden Pass (nominal capacity of 15.6 Mtpa) will be the third-largest facility in the US, behind Cheniere’s Sabine Pass (27.0 Mtpa) and Venture Global Inc.’s Plaquemines LNG (19.8 Mtpa).

The US became the largest LNG exporter in the world a few years ago, surpassing Qatar and Australia.

In 2023, no new export terminals came on line, and during the first 11 months of 2024, no export terminal came on line, which is why LNG exports in 2024 were flat.

But at the end of 2024, the huge Plaquemines LNG Phase 1 terminal (9.9 Mtpa) started operating, and in February 2025, the huge Corpus Christi Liquefaction Stage 3 (10 Mtpa) started operating, and exports of LNG shot up in 2025.

In terms of the Strait of Hormuz in billion cubic feet per day: The amount of LNG that was going through the Strait of Hormuz, but is now blocked, amounted to just over 10 Bcf/d, according to the EIA. Nominal US capacity has now reached 16.5 Bcf/d including the 0.68 Bcf/d from Train 1 of the Golden Pass terminal.

The US also exports large and growing amounts of natural gas via pipelines to Mexico; and it exports via pipeline to Canada, and imports from Canada (importing more than exporting), as a result of where producing and consuming regions, and pipeline connections, in both countries are.

Fracking has turned the US into such a prodigious natural gas producer in part because fracked oil wells produce a variety of liquid and gaseous hydrocarbons as byproducts, including natural gas. A substantial part of natural gas production being just a byproduct from oil wells changes the economic equation.

In the early days of fracking, those gases were flared because there was no takeaway infrastructure for gases. But pipelines caught up, and now there is massive production of natural gas whether anyone wants it or not (details here in my annual update on US natural gas production and exports).

| US Liquefaction Export Terminals, by in-service date | ||||||

| In-service date | Nominal capacity | Peak capacity | ||||

| Project name | Operator | Train | Mtpa | Mtpa | ||

| Sabine Pass | LA | Cheniere Energy | Train 1 | Feb/2016 | 4.5 | 5.8 |

| Sabine Pass | LA | Cheniere Energy | Train 2 | Aug/2016 | 4.5 | 5.8 |

| Sabine Pass | LA | Cheniere Energy | Train 3 | Jan/2017 | 4.5 | 5.8 |

| Sabine Pass | LA | Cheniere Energy | Train 4 | Aug/2017 | 4.5 | 5.8 |

| Cove Point | MD | Berkshire Hathaway BHE GT&S | Train 1 | Mar/2018 | 5.3 | 5.8 |

| Sabine Pass | LA | Cheniere Energy | Train 5 | Nov/2018 | 4.5 | 5.8 |

| Corpus Christi | TX | Cheniere Energy | Train 1 | Dec/2018 | 4.5 | 6.1 |

| Cameron | LA | Sempra LNG | Train 1 | May/2019 | 4.5 | 5.0 |

| Corpus Christi | TX | Cheniere Energy | Train 2 | Jul/2019 | 4.5 | 6.1 |

| Elba Island | GA | Kinder Morgan | Trains 1-5 | Sep/2019 | 1.3 | 1.4 |

| Freeport | TX | Freeport LNG Development | Train 1 | Sep/2019 | 5.0 | 6.0 |

| Cameron | LA | Sempra LNG | Train 2 | Dec/2019 | 4.5 | 5.0 |

| Freeport | TX | Freeport LNG Development | Train 2 | Dec/2019 | 5.0 | 6.0 |

| Freeport | TX | Freeport LNG Development | Train 3 | Mar/2020 | 5.0 | 6.0 |

| Elba Island | GA | Kinder Morgan | Trains 6-10 | May/2020 | 1.3 | 1.4 |

| Cameron | LA | Sempra LNG | Train 3 | Aug/2020 | 4.5 | 5.0 |

| Corpus Christi | TX | Cheniere Energy | Train 3 | Dec/2020 | 4.5 | 6.1 |

| Sabine Pass | LA | Cheniere Energy | Train 6 | Dec/2021 | 4.5 | 5.8 |

| Calcasieu Pass | LA | Venture Global LNG | Trains 1-9 | Mar/2022 | 5.0 | 6.0 |

| Calcasieu Pass | LA | Venture Global LNG | Trains 10-18 | Sep/2022 | 5.0 | 6.0 |

| Plaquemines LNG Phase 1 | LA | Venture Global LNG | Trains 1-18 | Dec/2024 | 9.9 | 12.0 |

| Corpus Christi Liquefaction Stage 3 | TX | Corpus Christi Liquefaction | Trains 1-7 | Feb/2025 | 10.0 | 11.5 |

| Plaquemines LNG Phase 2 | LA | Venture Global LNG | Trains 19-36 | Sep/2025 | 9.9 | 12.0 |

| Golden Pass | TX | Qatar Petroleum, ExxonMobil | Train 1 | Mar/2026 | 5.2 | 6.0 |

| Total operating | 122 | 148 | ||||

| Under construction: | ||||||

| Project name | Operator | Train | Mtpa | Mtpa | ||

| Golden Pass | TX | Qatar Petroleum, ExxonMobil | Train 3 | 2026 | 5.2 | 6.0 |

| Golden Pass | TX | Qatar Petroleum, ExxonMobil | Train 2D | 2027 | 5.2 | 6.0 |

| Port Arthur LNG Phase 1 | TX | Sempra Energy | Trains 1-2 | 2027 | 12.0 | 13.5 |

| Rio Grande LNG Phase 1 | TX | NextDecade Corporation | Train 1 | 2027 | 5.4 | 5.9 |

| Rio Grande LNG Phase 1 | TX | NextDecade Corporation | Train 2 | 2027 | 5.4 | 5.9 |

| Venture Global CP2 Phase 1 | LA | Venture Global LNG | Trains 1-26 | 2027 | 14.4 | 20.2 |

| Corpus Christi Liquefaction Midscale | TX | Corpus Christi Liquefaction | Trains 8-9 | 2028 | 3.0 | 3.6 |

| Rio Grande LNG Phase 1 | TX | NextDecade Corporation | Train 3 | 2028 | 5.4 | 5.9 |

| Woodside Louisiana LNG Phase 1 | LA | Woodside Energy | Trains 1-3 | 2029 | 16.6 | 17.7 |

| Venture Global CP2 Phase 2 | LA | Venture Global LNG | Trains 27-36 | 2029 | 5.6 | 8.8 |

| Rio Grande LNG Phase 2 | TX | NextDecade Corporation | Train 4 | 2030 | 5.4 | 5.9 |

| Port Arthur LNG Phase 2 | TX | Sempra Energy | Trains 3-4 | 2031 | 12.0 | 13.5 |

| Rio Grande LNG Phase 2 | TX | NextDecade Corporation | Train 5 | 2031 | 5.4 | 5.9 |

| Total under construction | 101 | 119 | ||||

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

LMG + Nuclear should be our foundation on which to build renewable energy sources (dependent on Geography constraints).

Nuclear is a dead end. The share of power generation will only shrink from here as aging power plants are decommissioned faster than the political and economic will exists to rebuild them. Modular reactors and GIV reactors are still unproven at scale, and by the time they’d be ready to go, the world will have moved on to much sounder investments.

Don’t get me wrong: There will be NP plants will be built for years and years, but the use cases will be for specific projects, and from the reactors being built now. The 2-300 reactors that go offline in the next 25-30 years will not be replaced by nuclear, and we will never, ever build the 1500 additional plants necessary to make a dent in fossil fuel emissions.

In conclusion, nuclear power is a dead end. Too expensive. Too risky. Too slow. The alternatives, including LNG, solar, wind, etc are simply better investments.

Palisades is historic because it’s the first U.S. commercial nuclear power plant ever brought back from decommissioning after shutting down. It sits on Lake Michigan in Covert Township and originally ran from 1971 until May 2022, when it was closed early due to economic and reliability concerns. [1][2]12

Michigan and the federal government later decided that losing 800 megawatts of carbon‑free baseload power was a bad idea—especially with rising electricity demand, grid reliability concerns, and climate goals. [1]

The Three Mile Island Unit 1 reactor in Pennsylvania (the one not involved in the 1979 accident) is being restarted under a major new deal tied to Microsoft

“Palisades is historic because it’s the first U.S. commercial nuclear power plant ever brought back from decommissioning after shutting down.”

Being first means it’s really an experiment. An experiment can end in success or end in failure, but we always learn from one. This experiment currently has about a $2.8 billion price tag attached to it, paid by Uncle Sam.

In the the early 90’s I lived close enough to Palisades that one of the technicians was in my social circle. He was ex-Navy, specifically subs, and said most of his coworkers were too. It seems there was a natural labor pipeline from running reactors on boomers and fast attack boats during the Cold War into the civilian reactor fleet after discharge. I notice now that the Silent Service has fewer than half the subs it had by the end of the Cold War. I wonder where the replacement for that lost skilled labor pool is going to come from.

I’ve got a bad feeling there’s a lot more we don’t know about restarting and extending the life of these things than we do know.

In addition to Poor’s arguments, nuclear has a massive waste issue. It’s not just waste from spent fuel rods. It’s also processing waste to get from ore to yellowcake – big pollution problems with other long-lived (1,000+ years) radioactive elements in the uranium decay chains like thorium and radium.

There’s also the problem that uranium production is restricted to a few number of players due to costs associated with mining U ore, processing it into high enough concentration of uranium, then refining further to concentrate U-235, converting into metallic fuel rods, constructing nuclear facilities, safely transporting radioactive materials, and operating nuclear facilities. Atomic bombs can be (and are) made with this stuff.

Solar doesn’t have any of these issues (aside from initial manufacturing which is currently dominated by Chine and SE Asia). Total costs are relatively small and distributed. For energy, I’d MUCH rather have that feature as a society.

gotta thank President Trump for helping out LNG/OIL companies thrive during these trying times

heck he eliminated like 50% capacity globally(thanks to IRAN drones)

I’m kinda with Steve here, but Poor has a point. The politics of nuclear are the biggest hurdle.

The track record is irrelevant, because the perception and spin are all that matters.

I’m not sure how the real world impacts of nuclear vs fossil fuels actually compare? The few nuclear incidents are hugely remembered, while massive explosions, leaks and contaminations from fossil fuels exploration/ extraction are just forgotten as “the cost of doing business.”

Nuclear technology has come a long way. It’s always been reliable and has no emissions. Small scale nuclear limits risks. There’s just no good way around the waste disposal issue, it’s not profitable and always a NIMBY.

Nuclear has good applications for certain use cases when mass is an issue (carriers, space, etc.), but are inefficient for power regeneration. Plus when things go bad…HOLY SHIT.

Solar, wind, and hydro are the cheapest ways to generate electricity. But they will differ on optimal approaches (rooftop solar is dumb if it’s on-grid IMHO), and each presents problems to adapt. Battery tech is helping smooth things out and pretty cheap.

Gas is also helpful in the energy mix as you can produce it all the time. Coal is pretty much becoming obsolete, except for energy security diversification. Oil is mostly just used for transportation, to leverage its energy density

It’s not really just an environmental issue, although carbon externalities should be taken into account. Climate change is expensive. Renewables are cheap, which is why they are taking almost all of the new power generation share as other approaches are often being phased out.

Nuclear has had quite a jump-restart recently. Quite a few projects (AI/Data Center) are seeking to use reactors to power their infrastructure. While their use-case might not be savory, hopefully their safe usage will trickle down to grid operation in the future.

Wolf had an article about this not too long ago.

X-Energy (EX) goes public today with an expected launch of $16-19. Amazon is their big investor, which suggests their SMR design should move to commercialization in a reasonable timeframe.

Looking forward to modular Thorium reactors!

And yet somehow they can’t produce or store enough helium (natural gas impurity) to fix the critical shortage faced by scientists.

Not all natural gas contains helium, helium comes from uranium decay and if there wasn’t much uranium scattered about in the era of plants and animals that decayed into the petrochemicals, or if the boundaries were permeable to helium, there’s no helium. Helium particles are small and can leak through things oil can’t

Petrochemicals do not originate from decaying animals and plants. That is a myth.

Ethane and Propane are the basic building blocks of petrochemicals. These light hydrocarbons are from decayed animal and plant matter.

There is no shortage of helium in the US. The US is the largest helium producer and exporter in the world, producing about 40% of global demand.

So price gouging, then? Or did it actually get 5X more expensive to produce helium in the last 15 years?

I’ve wondered about this. I tend to think it’s price gouging, akin to when microbrew went up a couple dollars a six-pack during the late 2000s hop shortage, then prices never came back down when the shortage was resolved.

If there were really an ongoing shortage, would people still be using it for balloons? Wouldn’t the government restrict it, and if not, wouldn’t companies be more careful about who they sold it to?

I don’t know if you were affected by the 2009-10 acetonitrile shortage, but we’d open a case we ordered and there would only be one bottle in it. We couldn’t get what we needed and had to ration it internally. People were switching LC methods over to methanol, which is not a trivial thing.

I guess some folks are switching their GC methods to hydrogen (what could go wrong?) We aren’t even considering it due to the safety hazard. But if it were a true shortage, like the acetonitrile shortage, I think we would be.

numbers,

Yes. Same with gasoline. Prices spiked the moment the Iran war began over the weekend even on the cheap gasoline still in the underground tanks at the gas station. I pointed this out at the time. In addition, the US is a huge producer and exporter of gasoline, and there won’t be a shortage in the US.

Companies will always charge the maximum price they think they can get away with. And during times like this, they can get away with a lot. Some people call that price gouging.

But the price increases are longer term than Iran. There was a show and steady doubling from 2006-2018, and then a tripling since then, with big spikes in 2019 and 2022.

Deciding to shut down the strategic helium reserve looks like a bad idea in retrospect.

There’s a large helium field in central Kansas near my home town.

I know what you meant, but couldn’t help picture a farm with plants bearing large fruits or gourds that are floating. You pick one and cut it open and take a deep inhale and start talking like a chipmunk.

Behold my helium crop.

What are the plans for when it runs out and fracking operations become stranded assets?

Just like refineries the plants with no feedstock will be removed . For sure not in my lifetime I’m 68

I always like to say, only partially tongue-in-cheek: We’re going to run out of clean air to breathe long before we run out of hydrocarbons to burn.

Remember when someone could hook up a generator to burn the gas instead of flaring it, and run a bitcoin mining rig with the power, all self contained in a shipping container? Such simple times

As you say, there is a lot of gas being produced and increasing amounts of infrastructure to move the gas to markets.

What is interesting to me is where the price of this gas for domestic consumers is going. There is increasing demand from electrified transportation, export and data centers And solar, wind and maybe nuclear will increase on the supply side. Solar seems destined to get cheaper to produce. That’s not as clear with gas.

And, as usual, we will wake up to a domestic natural gas shortage one day because both developed and developable reserves will be depleted. And then what will utilities, industry, homes, etc. use for power as they bear the brunt of shortages and increased costs?

The American way, full throtle without planning as usual. Our house of straw continues unabated. Strip the forests, use the water and other valuable resources without giving a thought to future needs.

But lets kill solar and wind.

“We” probably won’t wake up to it; “we” will probably be dead before that happens. Someone else might wake up to it. I’m more worried about the air “we” breathe and the land “we” farm.

They have just finished clear cutting a square mile of woods north of our town.

Heavy equipment will arrive to do site work and final grading.

Then they will install….a solar field.

The irony! It reminds me of an interaction with a mechanical engineer some years back, on the topic of carbon capture and sequestration (CCS).

His hope was around a plastic producing algae, while I was talking about reforestation to balance carbon cycles. (The “trillion tree” initiative was recently proposed at the time. Sadly it’s only 13.5 billion trees in).

He said that could never work. I said “I believe in trees.”

The dustbowl was a couple generations ago, and despite our knowledge of nutrient and mineral cycles greatly increased in this time span: policy and procedures are driven by politics and profitability.

I have always said that we need to find ways to make sustainability profitable, or it will not happen. In a globally competitive economy: nevagunnahappen.

LNG is a tremendous success for the US, going from gas import dependency to global export leader. A lot of talk about the technology sector but this is a truly unique strategic asset which is almost impossible to replicate elsewhere.

An equivalent for Europe would have been a continuation of the Nuclear build out program where we had several global leaders (ASEA Atom, Framatome, Siemens). We would then be completely energy independent rather than being fully exposed as we are today. What a missed opportunity.

Chenier terminals are Groninger 1959. The 1929/32 collapse was

caused by a Dutch Disease. Investors from all over the world

poured in, bought dollars to speculate in stocks, but import, especially import from Germany, was blocked. When businesses could pay their workers the Great Depression started. If the Gulf states and China cancel their orders and renege on unrealized promises Boeing will layoff its expensive workers. The chip industry and AI cannibalized each other. High tech companies are laying off expensive workers. When the strait of Hormuz will be opened LNG terminals will cannibalize each other.

Wolf: great article !!

How will this export ability effect local prices? Will nat gas power plants be looking to increase prices? Will this be inflationary for US citizens? I am an investor in Exxon, maybe I should use the profits from that to put up solar panels to cover my home electrical costs.

Australia has a case of that. But US production of NG is so huge because part of it is just a byproduct of crude oil production. So they produce it in overabundance, and the price continues to hobble along the bottom, currently around $2.60 per MMBtu at the Henry Hub, about where it had been in the 1990s, despite decades of inflation.

And what happens when there’s no longer enough water for fracking operations in severely drought-stricken areas of the country (e.g., the Denver-Julesberg Basin in Colorado)?

Hush, we don’t talk about that.

Since I was a kid growing up in Minnesota, there’s been talk of a pipeline: taking water from the Great Lakes across the Rockies.

It’s feasible, but politically undesirable. That is, until it becomes a “national security threat” to fall out of global energy leadership!

Struggler, to pump 1 cubic meter of water (264 gallons) from Lake Michigan to Colorado, it would cost approximately 10 to 15 kWh of energy. It’s theoretically feasible, but mind bogglingly cost prohibitive and impractical. Plus we have our neighbor to the north to contend with. Check out the “Great Lakes Compact.”

So, by the 15kw number that’s about 18.5 MW/ acre foot.

Did I say “fracking”? I meant to pronounce it as “data center.”

Now that 100MW data center that needs 10 ac/ ft of water daily is a 300MW center… SO we need more fracking… for the onsite gas fired power plant!!!

Don’t worry, the 52nd state: Canada (after Greenland), won’t mind us using a few of them.

At that rate, we just start taking the water from the west side of the Rockies too!

Remember: Security!

Not quite. It’s 10-15 kWh: kilowatt hours. Important distinction.

He said kWh. Doesn’t matter. It ain’t gonna happen.

Conventional oil in the US about depleted and maybe fracking has 50 years or so?

The stupidity of this administration to kill renewables is mind boggling.

They cannot kill renewables. But they can get in the way and slow it down. And they’re doing that.

Sounds like the same time given in the late 1970’s.

There’s always this: economic numbers are based on “proven reserves.”

It’s difficult and expensive to prove.

Unproven reserve estimates are pretty huge.

There’s probably not even close to 50 years of oil production left to frack out of the Permian. Regardless of whether or not there are even that many oil molecules down there, the problem is the produced water. They’re running out of places to hide it. And the locals are getting cross about dealing with new earthquakes from injection wells and toxic saltwater blowouts pushed up through holes in their land.

Texas regulatory bodies have a deer-in-the-headlights vibe, unable to cope. Does not compute.

🤣 NO ONE can predict what will happen in 10 years, much less in 50 years. 25 years ago, EVERYONE was wrong about the US energy supply in 2025, and NO ONE predicted that by 2025, the US would be the largest producer of crude oil, petroleum products, and natural gas in the world, the largest LNG exporter in the world, a large exporter of crude oil and petroleum products (gasoline, diesel, jet fuel, many others), the largest helium producer and exporter in the world, etc. etc.

Even in 2014, when the US was already the largest natural gas producer in the world, NO ONE predicted that in 10 years the US would become the largest LNG exporter in the world.

Here is one thing you need to take in: Technology improves ALL THE TIME, especially in oil & gas drilling where there are huge payoffs from improved tech.

I agree with everything you wrote. But I’m not talking about a technology problem. I’m talking about a VOLUME problem. They’re running out of places to dump the huge and growing proportion of produced water coming out of these wells. A lot of the new ones are really water wells that happen to have some oil and gas in the outflow. The oil and gas obviously gets burned; the water doesn’t. For now they’re just dumping it all back underground. That’s starting to cause some big problems.

I suppose you could put it in ponds to evaporate and then truck the toxic “tailings” to some Superfund site. That would solve the volume problem. But they apparently haven’t yet and that tells me a lot about how safe and practical that would be. (Actually, the way things work in Texas they’d probably just leave the tailings in the pond: “IBGYBG: I’ll Be Gone, You’ll Be Gone.”)

Yes, the state of Texas is going to try to use technology on the problem. They just signed legislation to research treating the stuff so it can be used to irrigate cotton and the food supply. Read that again: the FOOD supply. Sounds like desperation to me. Maybe the cotton will be okay but I know that when I read this stuff is actually being spread on Texas agricultural land I’ll have eaten my last Ruby Red grapefruit and Poteet strawberries.

I put a link in the reply box if I’ve piqued any interest. Reputable source, Texas A&M University.

Success in the oil and gas industry is difficult for smaller players due to the time to come online. If a project starts while prices are high, there’s no guarantee prices won’t drop before completion. This list of bankruptcies continues to grow while the smarter companies wait for distressed assets.

Wolf, why do you decline to post my comments regarding destruction of Nord Stream and the price of natural gas vs the price of LNG? Those are facts, not opinion!

RTGDFA. There was zero in it about the price of LNG. The entire article was about capacity of export terminals being built in the US, which started in 2016. The latest terminal that came online a few days ago, a topic in this article, was decided on in 2019. ALL of the terminals now operating were started YEARS before Nordstream got blown up in 2022. RTGDFA. You’re just trying to spread Putin effing propaganda here.