In the San Jose metro (Silicon Valley), active listings hit at least a 10-year record for March. But Orange County lags behind.

By Wolf Richter for WOLF STREET.

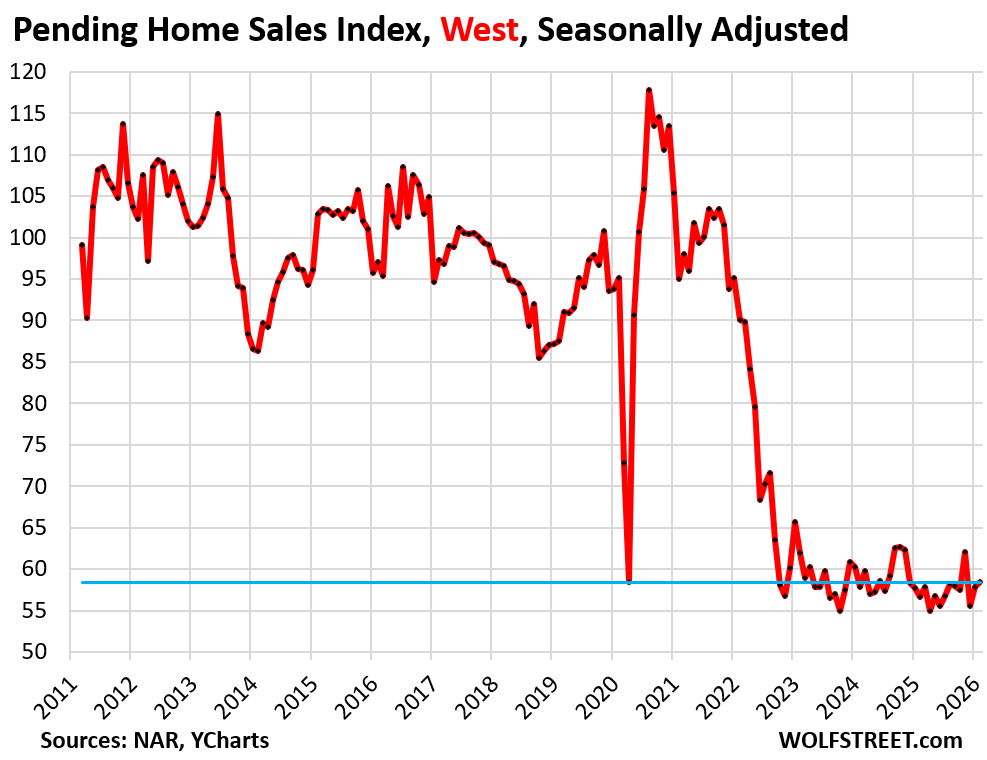

The average 30-year fixed mortgage rate is back in the 6.4% range, after the surge in March, which has pulled the rug out from already weak demand for existing homes in March. Even before mortgage rates began to re-surge, in February, pending sales of existing homes in the West were still down by 33% from 2019, hobbling along at very low levels (see chart at the bottom of this article). And March was even tougher, as shown by the drop in mortgage applications to purchase a home.

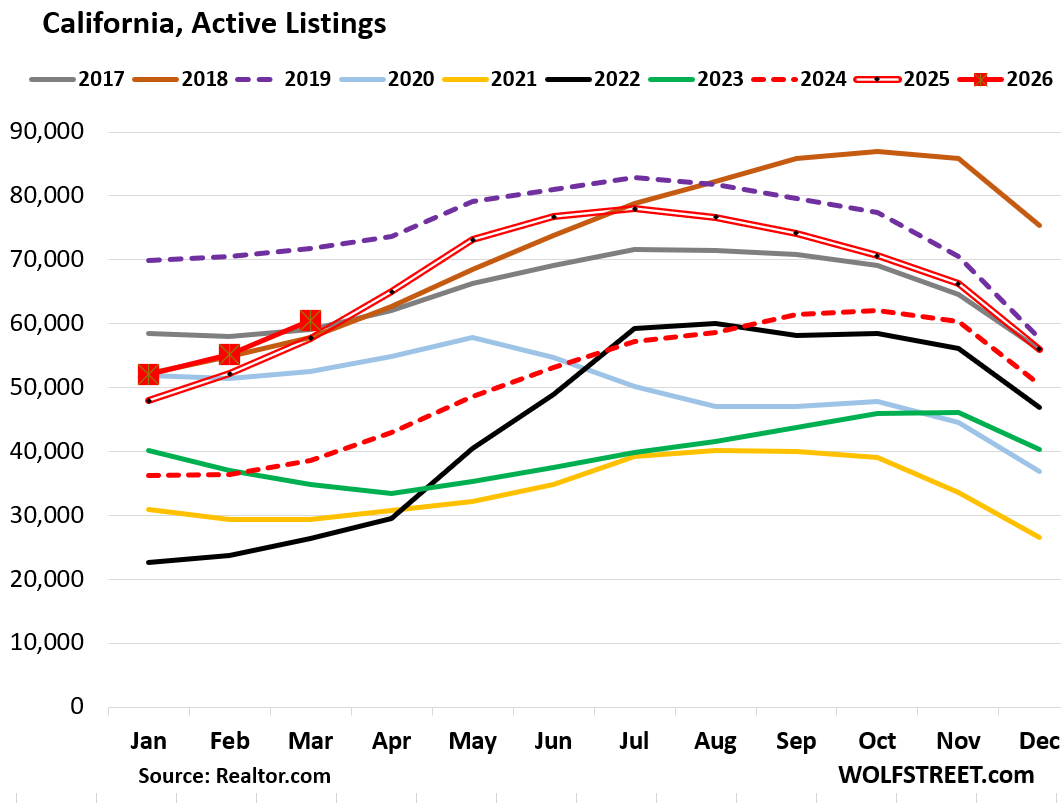

But active listings continued to rise in California and in March reached 60,521 homes for sale, the second-highest for any March over the past 10 years, behind only March 2019 (purple dotted line), but ahead of 2017, 2018, and all the others.

Compared to March 2025 (double red line), active listings were up by 5%; compared to March 2024 (dotted red line) by 57%; and compared to March 2021 by 105%, according to the data from Realtor.com, which goes back to mid-2016.

The dynamics in 2018 and 2019: In 2018 (brown line in the chart above) and through July 2019 (dotted purple), inventories were piling up amid the Fed’s hiking cycle when the average 30-year fixed mortgage rate rose and briefly hit 5% by November 2018. Mortgage rates then began declining as the Fed indicated a pivot at its December 2018 meeting, when it hiked for the last time in that cycle. In July 2019, with inflation below target, the Fed cut its policy rates. And mortgage rates had already dropped, and home sales were picking up, and active listings began to ease.

The reason active listings are now piling up isn’t a flood of new listings – there isn’t – but a plunge in demand of roughly 25% to 35% compared to pre-pandemic levels, and what is on the market is slow in selling. Delistings have also run high, which have kept the inventory from surging further.

The plunge in demand is a result of home prices having exploded during the pandemic’s below-3% mortgage rates to levels that are beyond where they make any kind of sense.

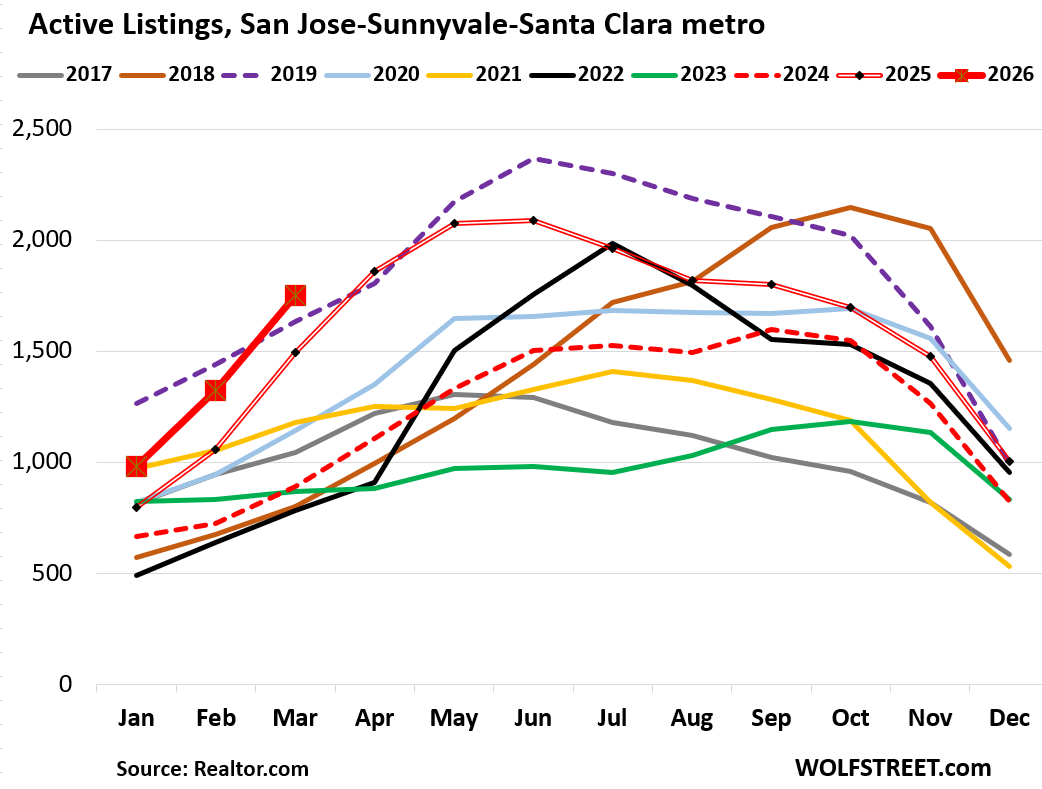

In the San Jose-Sunnyvale-Santa Clara metro, the southern portion of Silicon Valley, active listings rose by 17% from March 2025 (double red line), and by 97% from March 2024 (dotted red line), to 1,753 homes for sale, the most for any March in at least these 10 years of available data from Realtor.com.

This is quite an amazing turn of events.

The metropolitan statistical area (MSA) includes Santa Clara County and San Benito County, which extends south into rural areas.

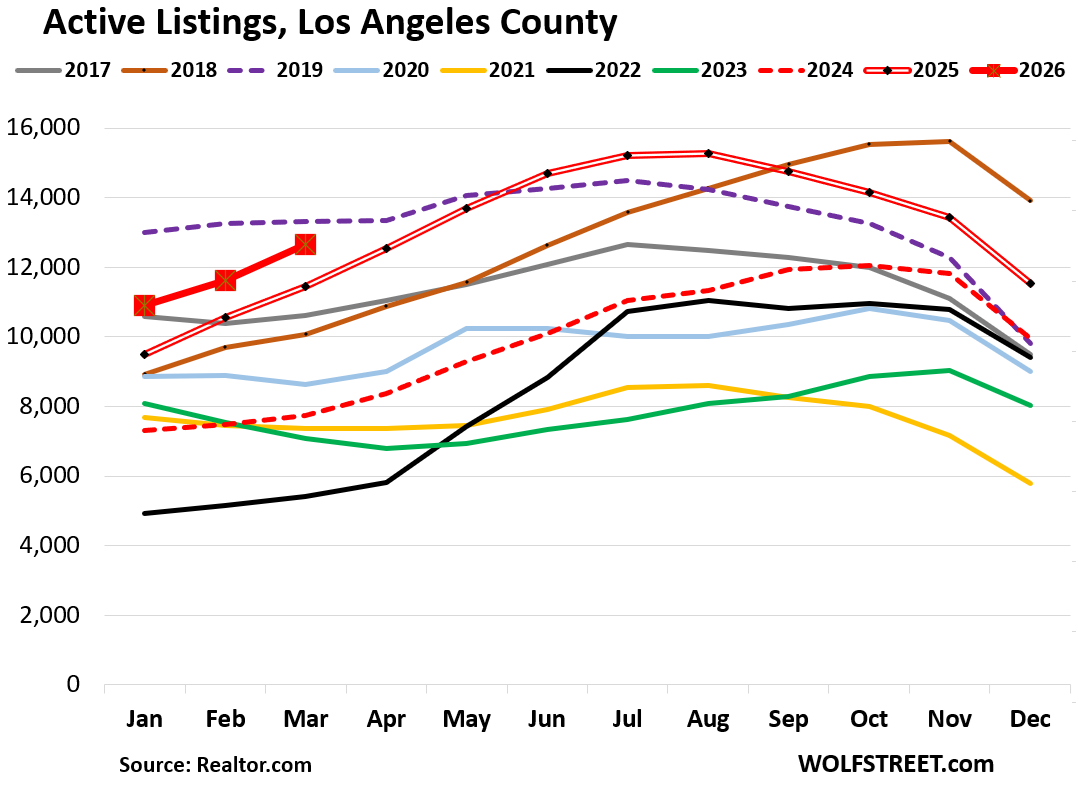

In Los Angeles County, active listings jumped by 10% year-over-year, and by 63% from March 2024, to 12,647 homes for sale, the second-most for any March over those 10 years, behind March 2019, in the data from Realtor.com going back to mid-2016.

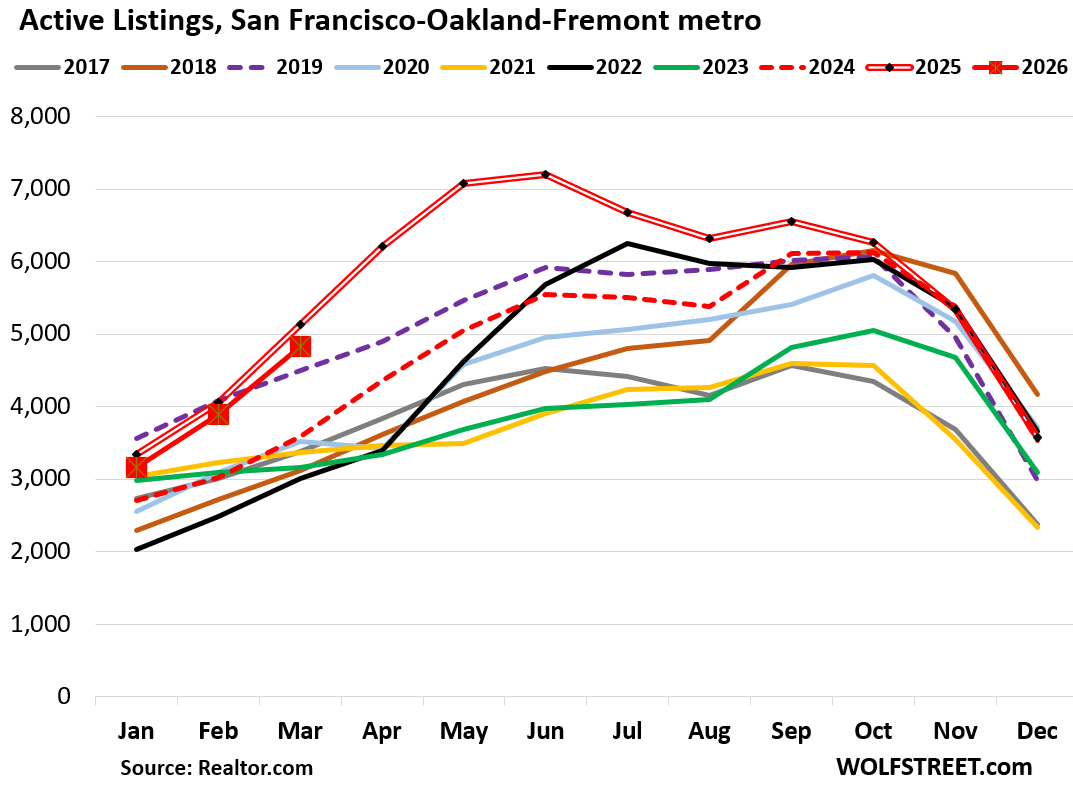

In the San Francisco-Oakland-Fremont metro, active listings were 6% below March 2024, which had been the highest for any March in those 10 years.

Compared to March 2024, listings were up by 35%. Compared to March 2019, listings were up by 7%; compared to March 2018, listings were up by 55%.

The MSA includes the city of San Francisco, the county of San Mateo (northern portion of Silicon Valley), part of the East Bay including Oakland, and part of the North Bay.

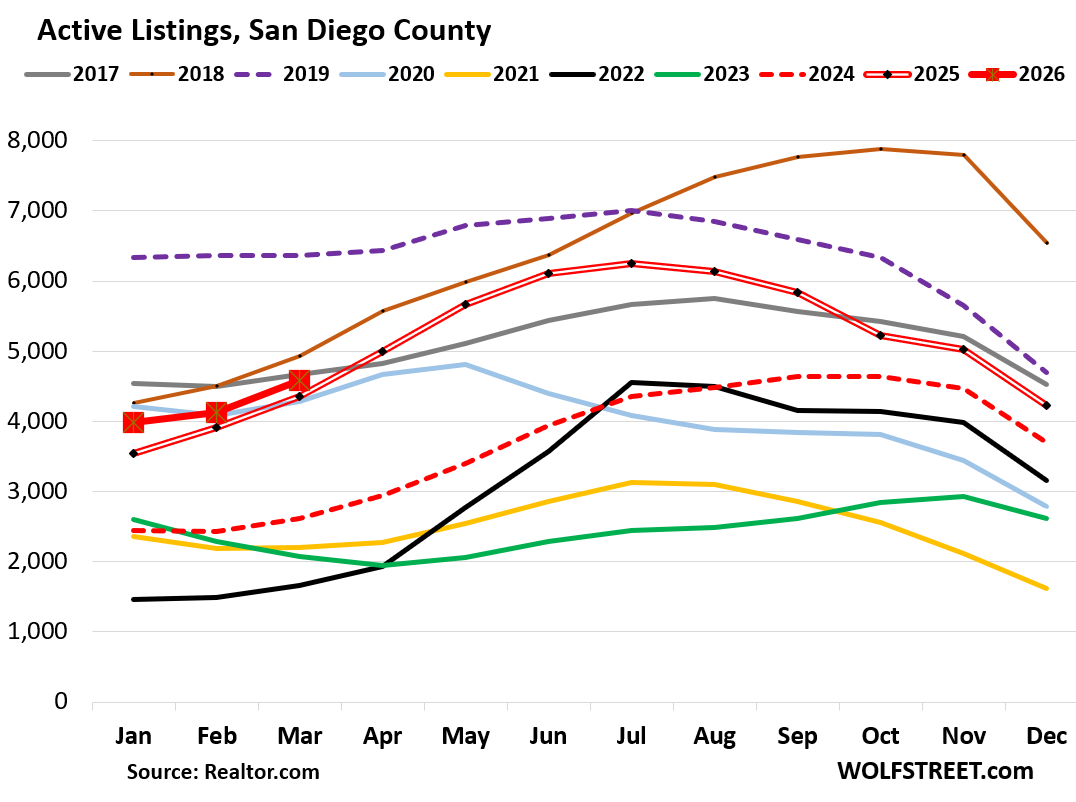

In San Diego County, active listings rose by 5% year-over-year and by 76% in two years, to 4,586 homes for sale, almost even with March 2017, and behind 2018 (brown line), and 2019 (purple dotted line).

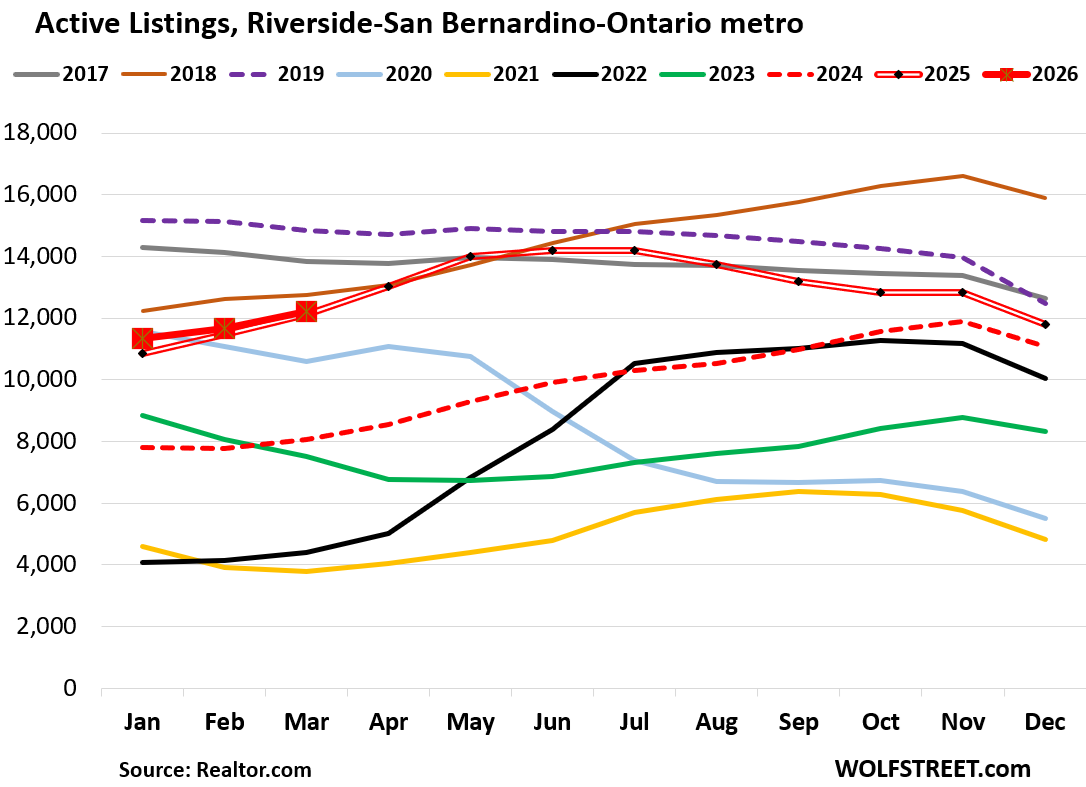

In the Riverside-San Bernardino-Ontario metro, active listings rose by 1% year-over-year, and by 51% from two years ago, to 12,232 homes, still below 2018-2019.

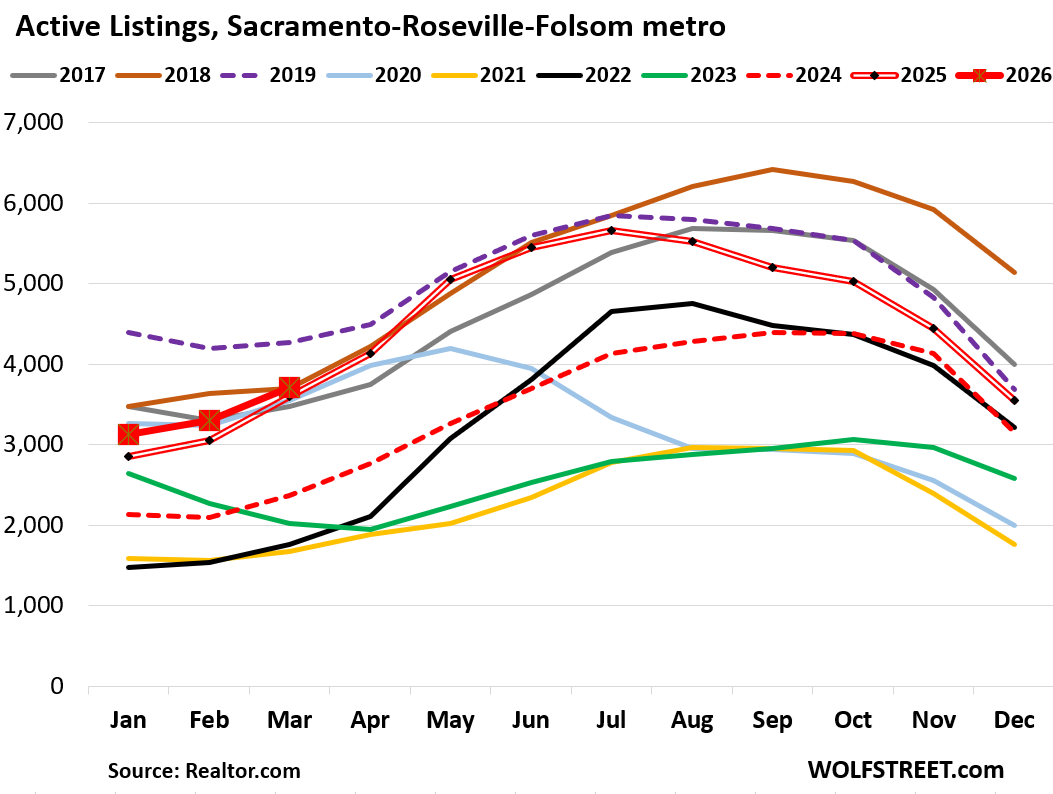

In the Sacramento-Roseville-Folsom metro, active listings rose by 3% year-over-year, and by 57% from two years ago, to 3,715 homes for sale, the second-highest March in those 10 years, behind only March 2019.

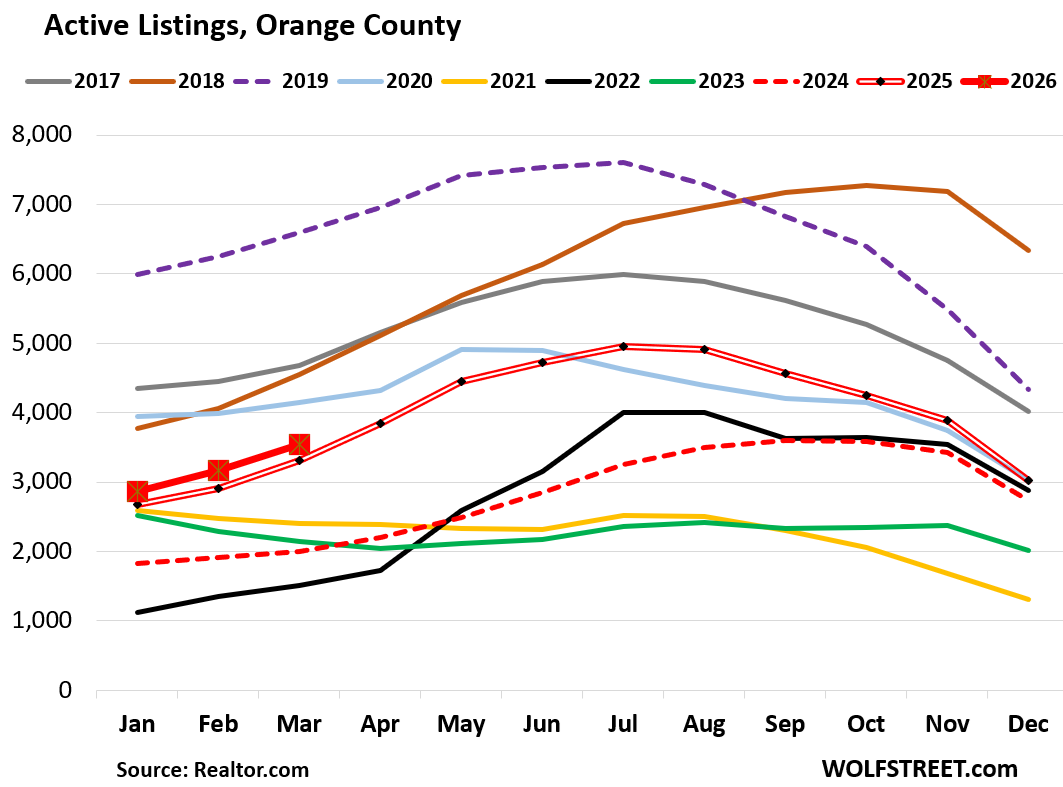

Orange County: Active listings rose by 7% year-over-year, and by 78% from March 2024, to 3,544 homes.

Inventory in Orange County got a late start taking off, but spiked from those very low levels starting in 2024. It still has some catching up to do.

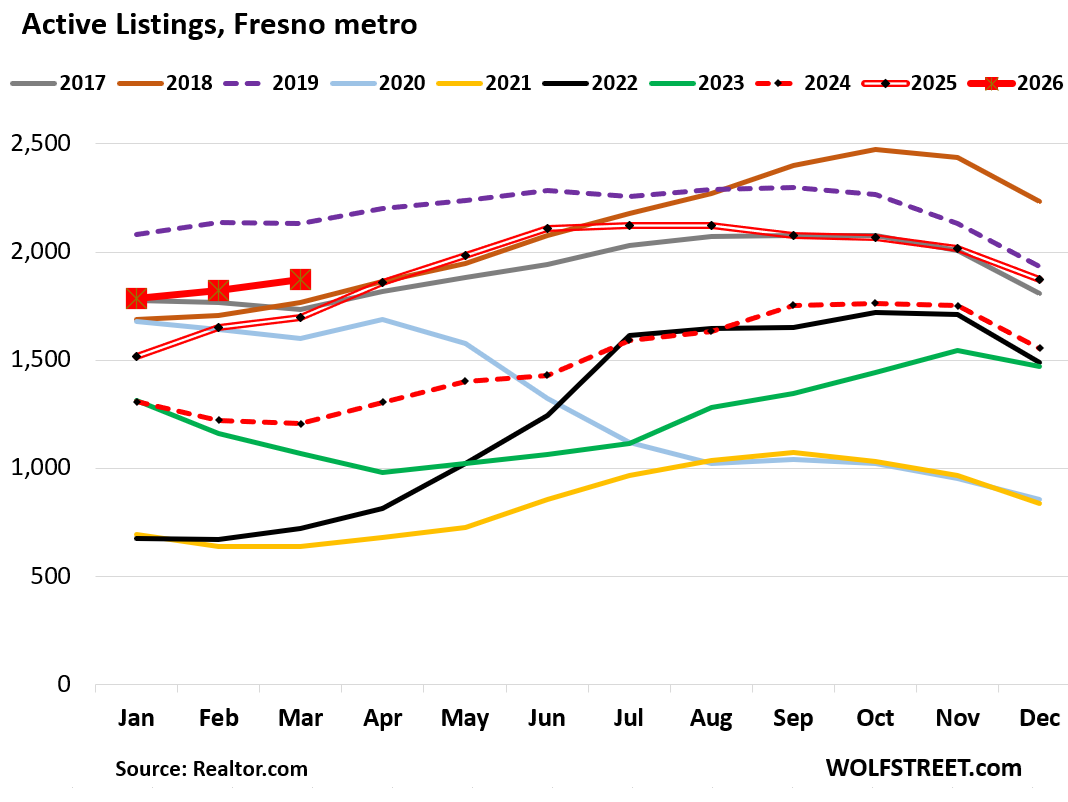

Fresno metro: Active listings rose by 10% year-over-year, and by 55% from two years ago, to 1,872 homes for sale, the second-highest March in those 10 years, behind only March 2019.

It’s a buyers’ market, but the buyers left.

Pending sales of existing homes in the West inched up by 0.9% in February from January, seasonally adjusted, and by 3% from a year ago, wobbling along at rock-bottom, down by 33% from February 2019, according to data from the National Association of Realtors (more here).

Pending sales track contracts that were signed but haven’t closed yet. A portion of them get canceled for various reasons, including difficulties in getting affordable homeowners’ insurance.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Looks like this Mexican standoff is not ending anytime soon… Price still nuts for the lost part, demand is in the gutter but that stubbornness of pulling off the market and hoping for a better day mindset is still rampant..

Maybe we do need the global event in the middle east to play out that might trigger a forced downturn to “motivate” some of these boomer sellers with extra houses to sell, if their retirement portfolio tank fast and hard, it might give them less room to wait out the market. Until then Mexican standoff continues especially in SoCal

While I would be happy to see home prices fall am not willing to have it happen due to our folks in the service getting into a hamburger grinder for another countries ambitions/evil.

1911….

I was going to say the same thing…..

Send our troops to war in a land far far away, so that our homes might become more affordable??

There are other ways to achieve more affordable housing besides exporting violence and war.

Agree with you both, it’s completely insane to think this would be any kind of designed solution to bring housing prices down. Merely pointing out this might be where we are headed regardless, I guess we will continue to see 2-3 weeks, narrative and action seems to change day to day anyway

FU re ‘boomer seller’ comment. You don’t know that. You’re just showing ridiculous age discrimination. High prices happen for many reasons. Sellers aren’t trying to screw you because of their age.

High prices happen because buyers are paying them. They were outbidding each other to grab a property and went nuts and prices exploded. Sellers had nothing to do with this nuttiness. They just watched in awe as their asking prices got bid up into the sky. Younger homebuyers, buying homes sight-unseen, were a big driver behind this price explosion in 2020-2022.

When it finally ends with reasonable prices I may be able to finally contemplate a home, or a shack of some sorts, in SoCal. As a canuck I love the area but only get to visit from time to time. Well, unless our economy implodes to the point where we even lose our Gov. contracts, that’s the nightmare scenario up here in the 51st (or 52nd?) state

The cure for High prices is….

High Prices!!!!

“Slowly at first, and then all at once….”

YMMV….

You also need to understand migration as it relates to this issue. i.e. supply and demand

With really high housing costs, it matters who leaves and who comes into the state.

“From 2010 through 2024 (the year of the latest data), almost 10 million people moved from California to other states, while just over 7 million people moved to California from other parts of the country, according to the American Community Survey. In fact, according to the Department of Finance estimates, the state has lost residents to other states every year since 2001”.

You didn’t mention the international in-migration to California, which as in the other big coastal states (esp. Texas and Florida) was a massive force. And California’s population continued to grow until Covid. International in-migration is still happening, but during Covid and since the crackdown on illegal immigration at a much slower rate, so the normal domestic negative net-migration is no longer or is only barely being compensated for with international in-migration. So with international migration included, it looks different. I did this for you and everyone else a couple of months ago, and even tied it to housing:

https://wolfstreet.com/2026/01/29/californias-population-declines-again-200000-since-2020-relief-for-housing-shortage-as-new-supply-keeps-getting-built/

5:48 AM 4/2/2026

DJIA F 46,169 -637 -1.36%

S&P F 6,518.25 -99.50 -1.50%

NASDAQ F 23,735.25 -459.50 -1.90%

Gold 4,649.20 -163.90 -3.41%

Silver 70.715 -5.363 -7.05%

Crude Oil 111.16 +11.04 11.03%

Basically all losses recovered. There are still too many investors out there who see any dip as a “sale,” and are convinced that the government won’t let their stocks drop.

As long as investors believe that, whether it’s true or not, we’re never going to have any real correction.

Essentially 20 years of ZIRP policies turned housing into a playground for interest-rate speculation – causing all sorts of pathologies for those of us who just want reasonably priced, semi-stable housing.

But the Fed’s endless attempts to “fine tune” or “optimize” the US economy via interest rate manipulation (via money printing) in order to manipulate the “housing channel” wealth effect (soon to be poverty effect) has, in the end, accomplished very little other than dramatically increase latent instabilities – making the macro-economy worse off.

It is a multi decade tragedy of hubris and the utter inability of our “commanding heights” “elite institutions” to course correct in the face of empirical reality.

Exactly. For all the mainstream media coverage about “housing in-affordability,” there’s been little mention of the primary villain: the Fed.

It is all the Fed’s fault, and the oligarch government’s fault. First give tax breaks to the top 10-20%. Then “pay” for the tax breaks by printing $2T new govt mone against USG debt. USG spends the money once, then the money lands on Wall St amd drives speculation. Then compound the mistake by printing some $1.8T against mortgage debt (bonds). The top 10% go wild with housing and stock speculation, based on the double effect of more income (remember: tax breaks) AND low interest rates (which was part of the money printing process). Net result: Rampant housing and stock inflation since 2008 and counting, and finally consumer inflation once we could no longer import our way out of domestic costs spiraling due to the overpriced rent and housing and health insurance. Eventually the inflation spreads into energy and even food. Then the calamitous idiocy in 2020-2022 of printing $4.4T, justified by the self-imposed Covid panic. Come 2022-2026 the playbook is to start wars against Russia, Venezuela and Iran of steal their resources, to cover up decades of US financial mismanagement, among other specious motivations.

Narmageddon….

As far as the portion of your comment on Covid times…

I think it is easy to forget that 80-90 percent of society was stressed or in full panic over the Covid and bought off on, or agreed to alot of things.

Right, wrong, or indifferent, society, gov, etc, did alot of things that they are now conveniently forgetting.

But the consequences… good or bad are still with us.

100% @Narmageddon

It’s a fantasy of mine that a debate moderator would force our politicians to explain how they’ll help make housing simultaneously both affordable and an investment.

Yep, I think it’s called continuation bias. It all comes down to the fact that you can’t create something from nothing. The government can’t create wealth, in the end. It can make it easier or harder for individuals or companies to create wealth, but all government does when it tries to “fine tune” the economy is shift wealth and income from one person to another. It’s that simple.

The time frame of the Keynesian economists that have dominated the FED since the early 60s is 24 hours rather than 24 months.

The imbalances will correct. Every month, a greater percentage of homeowners have 6%+ rate mortgages. They are leveraging out to buy at today’s prices. Things will be very tight for them in a slow growth economy. They will sell at reduced prices. Problem is, they will probably try to do this around the same time.

Many buyers today are on unsure footing, taking a big risk.

“The imbalances will correct.”

Sure…but the historical record of the last 25 years is that favored/privileged sectors that blow themselves up (using Fed supplied leverage in the name of macro “optimization”) get bailed out because they are “too crucial to fail”.

And the only tool the Fed has to bail them out is *more* money printing.

Basically, in the name of trying to re-animate the US economy since 2000 (with nobody having to reform *anything* – corporate productivity, political spending, any goddamn thing), the Fed has basically done little more than create a shambling macro corpse whose limbs periodically fall off – necessitating ever more pathological forms of macro-economic necromancy to keep the illusion of economic health “alive”.

A debt-fueled zombie economy that looks alive but is mostly dead – because the underlying economic fundamentals have been allowed to rot away, papered over with printed money.

I just want to say that I much appreciate the comments by cas127 over the years. Since wolfstreet does not have up/down/like/dislike, you may not get much feedback, but know that your effort is noted. Thanks. Of course, Wolf may not get the accolades he deserves, either, moving mountains every day. But I guess maybe the engagement he sees is his positive feedback :). The data extraction and scraping skills it takes to create this website is something to behold. I wish I knew how he does it. I also wish Wolf would not pre-moderate me, but I guess it is because I disagree with him about some very few but important points.

Having lived in Orange County (Corona Del Mar) I can tell you from experience that people are just different there. Not quite as privileged as Laguna Beach, but pretty damn close. LOL.

Don’t think that’s exclusive to Corona Del Mar, seem to be a general OC thing and the more south you go, the worse it gets, probably starting from Costa Mesa down. You want exclusionary, NIMBYism and privileged to the max, try Ladera Ranch or Rancho so Mission Viejo, they certainly take the cake. So privileged in fact, people in Ladera ranch are so entitled, you can often find near new and perfect second hand items in their trash dump simply because they are too lazy and entitled to donate or try selling it on marketplace

Lot of great things about the CA coast.

One thing I do not miss about the CA Coast is amount of self entitlement, and blatant rudeness that coincides. It has seemingly become more common in recent times.

Unfortunate.

The basic premise that people should expect (or are somehow owed) a “reasonably priced” or “affordable” house is wrong. There’s no room for nostalgia – Housing’s a business. Government’s ZIRP simultaneously made “homes” less affordable and “investments” more attractive. Like it or not, it’s math and people’s demands and expectations aren’t part of the equation.

Housing has gotten so expensive that big landlords have been selling the homes they’d bought in 2012-2013 and are not buying more of them. they’re building their own now because that’s cheaper than buying them from homeowners. Because high prices make these investments “un-attractive.” Not “more attractive.”

Yes. I saw a house around here that someone paid $1.9 million for and then promptly turned around to rent for $7,500/month. Subtract from that probably $2,500/month in taxes, $500/month in HOA fees, and $1,000/month in insurance.

Are these people insane?

Yes

“Are these people insane?”

The institutions lending them 80%-95% of that $1.9 million are the truly insane – they’ve barely survived through multiple rounds of this coked-up goat rodeo and yet their incinerated fingers simply cannot resist wombling back to the fire.

And they are supposed to be “professionals”

Often, a rental owner will do a 1031 exchange from a rental property, into a home that they might wish live in but first need to show two tax years as a rental. This saves capital gain taxes on the rental sold and despite seeming insane, actually saves a lot of money.

Just one of several non-insane strategies.

cas127, I think these are cash purchases. I don’t think traditional mortgage lenders will issue a loan like this to an investor.

I think these are small time investors who have some cash and think it’s a good way to “put their money to work.”

Dougpent, I hear you, but I don’t think it’s the case here, as the buyers were 68 and 66, and it was a 5 bedroom, 4,400 square foot house.

The pitch reflects what I have learned about T Bills here Wolf:

Why would you buy any real estate as an investment it it doesn’t beat 3.7% risk free return, net exclusive of Fed taxes? As these elevated prices most property looks stupid as an investment. Cap gains look more like a myth than a sure thing.

Buffet is STILL cash heavy.

But that’s true for stocks too. The mantra you see online is “buy and hold,” “dollar cost average,” “stay invested.” Nobody thinks there’s any real risk with equities.

There is an incentive for society to be able to provide at least a basic level affordable housing unit. If you don’t, what do people have to live for?

Where will the people who cook your meals, haul your trash, and guard you at night live? Have you not seen Fight Club?

The Market provides housing. Not society. Just as it does cooks, trash haulers and guards. Mostly it’s when government involves itself does housing supply / demand become imbalanced. A headwind for buyers / renters. An opportunity for investors. Econ 101

I spent January and February in Orange County and Los Angeles. Prices are way too high. Condos and townhomes are lower, but HOA dues are a killer. Then there are the homes in fire zones that are uninsurable. Sellers are unwilling to drop prices low enough to beat comparable rents. Prices of multifamily units are also dropping, but are elevated especially with rent control. Until people are forced to realize losses, the market will remain frozen.