Services inflation was on the ECB’s worry-list when it kept rates unchanged for the third meeting in a row.

By Wolf Richter for WOLF STREET.

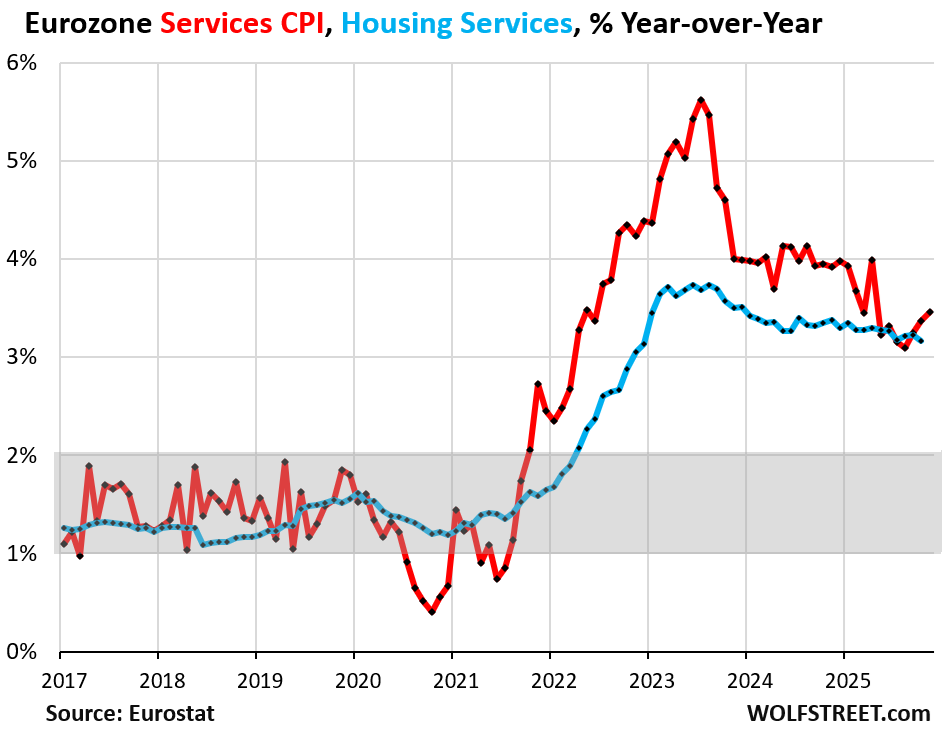

Services inflation in the 20 countries that use the euro accelerated for the third month in a row on a year-over-year basis, to 3.5% in November, the highest since April, and far above the prepandemic range between 1% and 2%, according to Eurostat’s preliminary inflation data released today (red line in the chart). The recent low point that it bounced off was in August at 3.1%. The drivers of this recent acceleration were non-housing services.

By contrast, housing services (blue line) have increased at a steady though high rate of about 3.2% year-over-year for the four months through October after decelerating in prior months (November is not available in the preliminary release today).

The shaded area indicates the pre-pandemic range. The services components of inflation remain far hotter than before the pandemic. Housing-related services include actual rents paid by tenants; services for the maintenance and repair of dwellings; insurance connected with the dwelling; refuse and sewage; repairs of household goods; and domestic and household services.

For the ECB, worries about this recalcitrant services inflation have colored its rate-decision announcements and Q&A, including at the most recent policy announcement on October 30, when it kept its policy rates unchanged for the third meeting in a row (deposit facility rate at 2.0%), with some members suggesting that no additional rate cuts may be needed.

What had caused overall CPI for the Eurozone to cool substantially between mid-2022 and October 2024, were the plunge in energy prices off the huge spike, the drop in durable goods prices that had surged during the pandemic, and the return to prepandemic rates of inflation in food prices.

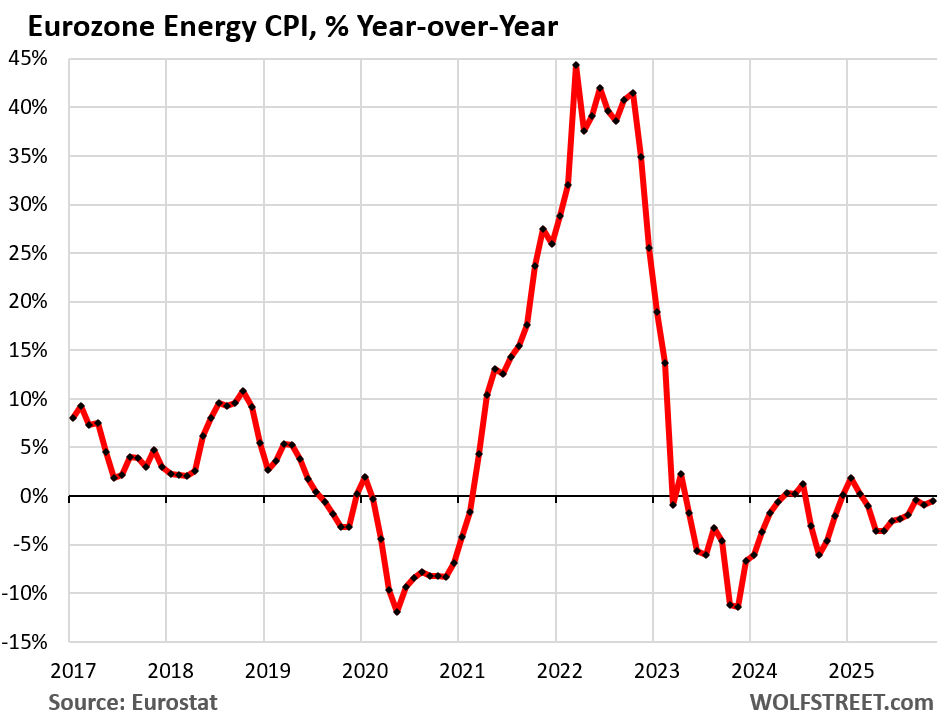

Energy inflation was again negative, with prices dropping 0.5% year-over-year.

The CPI for energy – which tracks prices for gasoline, diesel, natural gas, electricity, heating oil, etc. – had spiked by 70% from December 2020 to October 2022, and then started giving up part of the spike and is now down 15% from the top. Energy prices remain very high compared to prepandemic times.

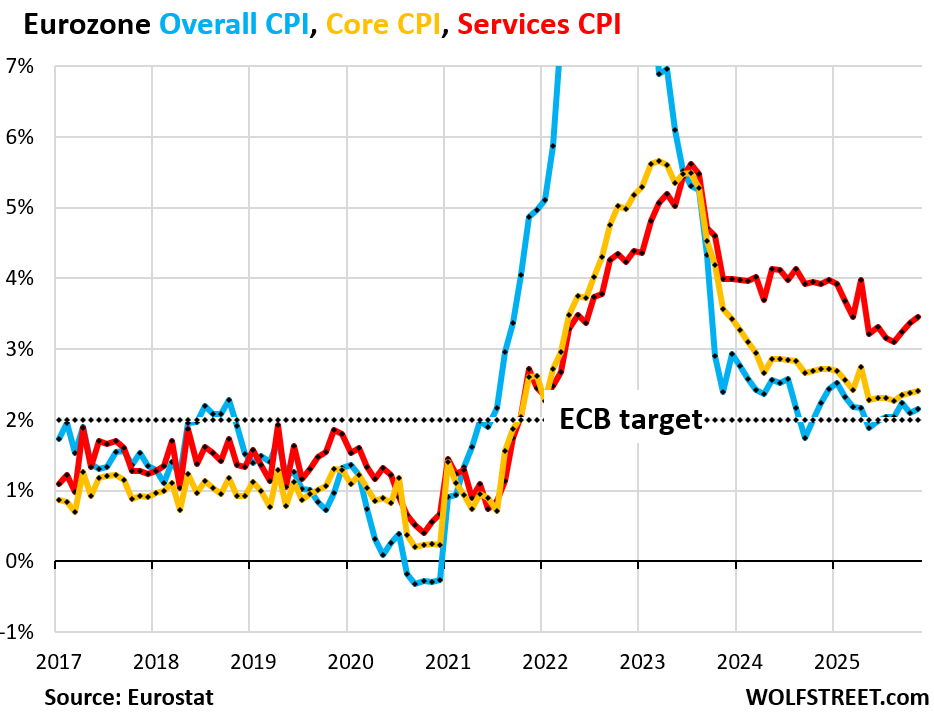

Overall CPI accelerated to 2.2% year-over-year, driven by services, even as the continued year-over-year decline in energy prices, essentially flat durable goods prices, and slower-rising food price pushed the other way (blue in the chart below).

Spiking energy prices and food prices in 2021 and 2022 had been big factors in the Euro Area overall inflation spike at the time, powering the overall CPI to a 10.5% year-over-year increase by late 2022.

Now, with energy inflation negative, durable goods inflation close to zero, and food inflation low, overall CPI is close to the ECB’s target of 2%. The worrisome aspect is the persistence of services inflation, as energy prices aren’t going to drop forever, which could pull CPI further away from the ECB’s 2% target.

Core CPI – which excludes food, energy, tobacco, and alcohol products – rose by 2.41% in November, the biggest year-over-year increase since April, edging past the October increase of 2.37%. Core CPI is dominated by services.

The chart shows overall CPI (blue), core CPI (gold), and services CPI (red), along with the ECB’s target (black dotted line).

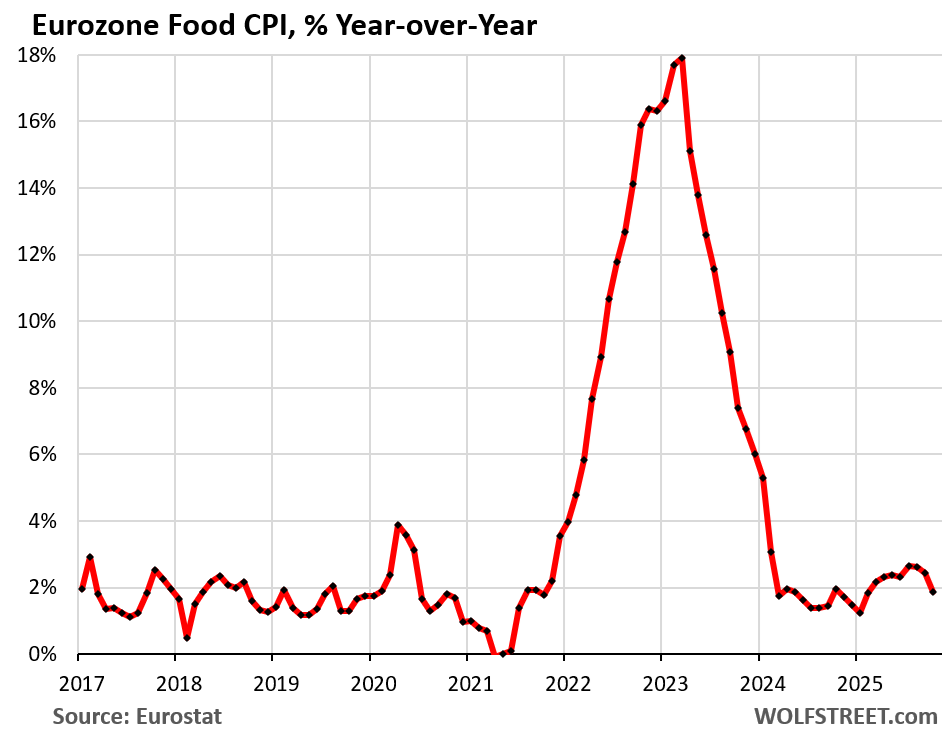

Food inflation rose by 1.9% year-over-year in October (November not available in the preliminary release). Price increases have slowed substantially after the 18% year-over-year spike into early 2023. Since March 2024, food prices have been rising from these very high levels at the prepandemic rate.

This cooling of food inflation off the massive spike in 2022 and early 2023 has contributed to the cooling of overall CPI.

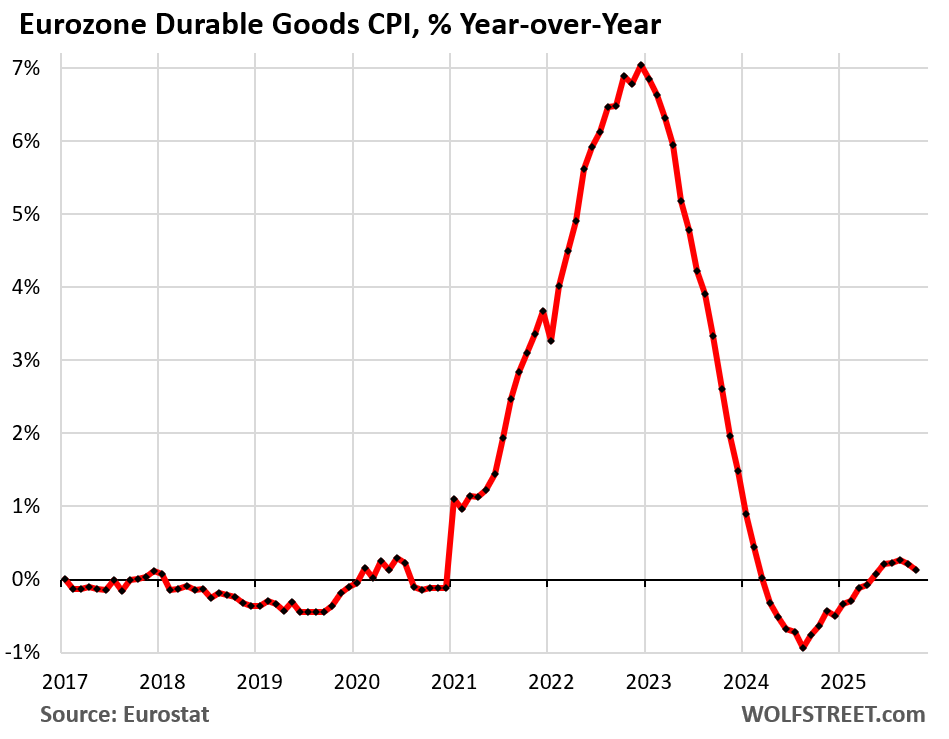

Durable goods CPI rose by 0.1% year-over-year, so nearly unchanged in October (November not available in the preliminary release). After the 13% price spike from December 2020 through April 2023, prices have remained essentially unchanged to slightly down since then, remaining at very high levels.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Weird, UUP(bullish $usd) is set up to pop for a longer term run higher. the US dollar closed at an inflection point today it looked like the Euro was rolling over, but if euro inflation goes higher the euro should follow inflation if the ECB is doing their job, When US AI stocks are liquated, the world will be forced to buy US dollars during the liquidation process. My eyes are on Googl (post blow off top?) for the tell with the bubble direction. I am excited to see our inflation data next week. Service inflation continues to heat up? Everything should get really exciting soon.

Well it is not as if we were not joined at the hip. The world’s largest economy always gets my attention.

So, you’re watching China then…

That means you are not aware of which is the largest economy? .

Yes. Anyone that is bullish on the Federal Reserve Note (technically the dollar is long dead) is relying on old cycles when there was no alternative during uncertain times. Precious metals and cryptos are now being recognized as an alternative along with mbridge. While the FRN isn’t disappearing anytime soon, the demographics of the planet will ultimately win. In a nutshell what percentage of the world’s population are responsible for paying that 36 trillion in American debt? How productive are they. Yes, the same can be asked of the Chinese debt, Russian debt, etc., but the point is, the age of 300 million people dictating economic terms to 4+ billion people is ending.

“cryptos are now being recognized as an alternative” to going to Las Vegas and playing the slots.

Yes, but stupid is as stupid does. So what? Doesn’t chage the facts. It is what it is.

Yeah if I wanted to gamble, I’d much rather play cards. It’s a lot more fun.

If you ask crypto afficionados, nothing is more fun than trading cryptos, or just watching them implode overnight. Keeps them entertained all night long.

“If you ask crypto afficionados, nothing is more fun than trading cryptos, or just watching them implode overnight. Keeps them entertained all night long.”

Perhaps, but many have made a lot of money as well. Again, is what it is. As others, much smarter than I have said, “there’s a sucker born every minute”.

Just be sure to pay your capital gains tax!

When you don’t do that, then the real trouble starts! LOL!

Craptos are now being recognized as the worthless Ponzi scheme they are and have always been.

Saylor from MSTR said~ Bitcoin moved from about $55,000 to $94,000 over a 14-month span! Bitcoin just completed its counter trend rally from the low 80s to 94k yesterday. I thought it was weird that he used 94k and 55k, technically I did t see it as technically important. But those numbers ar! Elevator drop to 55k before the real money buys the dip to try and prevent the crypto exodus and BTC to 12k. 14weeks instead of 14months? 191k unemployment claims has to provide fuel for the Fed to stay put. This secular bull market will quickly turn into a secular bear. Bearish engulfing in Googl by close? That will start it!

Looking forward to seeing the U.S. data soon. The “good” news is that once things become unaffordable, any additional inflation is largely irrelevant…

I stand by my original hypothesis that that first peak is simply the first wave of three.

Hedge accordingly.

Is it true the Fed ended QT on December 1st? I have looked at several sources and seems to be consistent. Could be they have just rolled off enough but not sure what, if anything to make of it, and trust very little of what I read out there, let alone any analysis of it.

Jesus!! Do you ever read any articles here at all???? (you’ve been commenting here for a long time).

The Fed ANNOUNCED at the last FOMC meeting that they would end QT on Dec 1. Read my article about it:

https://wolfstreet.com/2025/10/29/fed-cuts-by-25-basis-points-with-2-dissents-in-opposite-directions-qt-to-end-but-mbs-to-continue-rolling-off-to-be-replaced-by-t-bills/

I have posted numerous articles here about WHY the Fed will end QT when the balance sheet drops to certain levels (I started those articles in about 2022). And the balance sheet has now dropped to levels where liquidity becomes tighter. See my articles here about the repo market and the Fed’s balance sheet. They’re all here.

https://wolfstreet.com/category/all/federal-reserve/

As to affordability, Donald John Trump said yesterday ‘Affordability doesn’t matter to anyone or anything.’ The day before he said that he is ‘always right abut everything.’

Wolfman – I feel sorry for our European friends but I’m more worried about inflation on this side of the pond. 🤔🤓

So the Eurozone has an underlying inflation problem in the areas of housing and services. Yet, unlike the U.S. they did not:

-print and distribute helicopter money during the pandemic

-cut their own tax collection agencies

-cut taxes (more stimulus)

-tariff everything from outside the Eurozone

-increase debt/GDP across the whole Eurozone to 125% (so far) like the US did

-increase money supply at the level the US did

What they DID do is cut their overnight deposit rate to below the rate of inflation. This is stimulative and inflationary. The US applied all the inflationary fiscal and monetary policies listed above and yet was only facing 3.0% CPI inflation as of September. Yes that’s worse than the Eurozone, but still!

The difference: The U.S. only cut its FFR from 5.5% to 4% (upper bounds). The Eurozone cut their overnight deposit rate from 4.5% to 2%. So the change in the U.S. was only 1.5% and the FFR remains above the rate of inflation, whereas the Eurozone cut 2.5% and brought their rate below inflation.

So I think the reason the US isn’t seeing 5% to 7% inflation is because we DIDN’T keep cutting rates all the way to 2% in 2025. We paused. The Eurozone just kept cutting.

The US pause offset the US’s highly inflationary fiscal policies, while the Eurozone’s cuts offset their slightly better fiscal responsibility.

So the US would be wise to hold right here rather than daring inflation to hit 10% again, like we apparently are tempted to do.

Another outcome: Eurozone wages are increasing at around 2.5% per year. US wages are rising at 3.8%, and were recently rising closer to 4% per year. Thus, I think the high services inflation in the Euro countries is “a monetary problem” due to rates being too low. In the US it is a wage-price spiral.

So yea, Steven Miran, let’s cut rates into a wage-price spiral and see what happens for the LOLz.

Long OILK.

The Short-TLT trade is getting crowded at over 25% short interest, and might possibly push down long term rates as an effect of a short squeeze. The currency would be the victim if that happened, so consider UDN or puts on UUP.

“Yet, unlike the U.S. they did not: -print and distribute helicopter money during the pandemic”

You gotta be kidding. I discussed this here most recently in October: note the hump in 2020 through 2022 of mega-money-printing, and note the €3.5 trillion in QT… that’s €1 trillion more than the Fed’s QT.

https://wolfstreet.com/2025/10/08/ecbs-qt-has-knocked-e3-28-trillion-off-its-balance-sheet-far-more-than-the-feds-qt-and-accelerated-qt-further-this-year/

and here (assets as a percent of GDP):

https://wolfstreet.com/2025/11/27/amazing-how-central-bank-money-printing-reversed-around-the-world-after-the-inflation-shock/

This chart is of just their QE assets, not total assets:

The recent inflation period looks to me like previous periods of high inflation a political maneuver to reprice wages to be cheaper in real terms, my usual arguments:

* There has been zero or negative cost-of-living inflation in China, where all the manufactured stuff we buy is made and that sources the same foodstuff and other raw materials from the same global markets “the west” does.

* In the cases where wholesale global cost-of-living prices went up and then down local prices in “the west” did not fall back to the previous level, prices just remained constant.

* Booming asset (both property and stocks) prices are a policy goal in much of “the west” as they are the critical factor for buying the support of the middle class for lower wages and pensions.