US Government sold $651 billion of Treasury securities this week into these rising yields.

By Wolf Richter for WOLF STREET.

It was a rough week in the Treasury market and the mortgage market. Inflation fears spread amid surging gasoline prices and some lousy inflation data that don’t even yet include those surging gasoline prices: The Fed-favored core PCE Price Index for January rose to 3.1%, worst in nearly two years, when the Fed’s target for it is 2%. And worries cropped up about the deficit as the financial costs of the war in Iran would have to be borrowed, and reluctant new buyers would have to be enticed by higher yields to buy that debt.

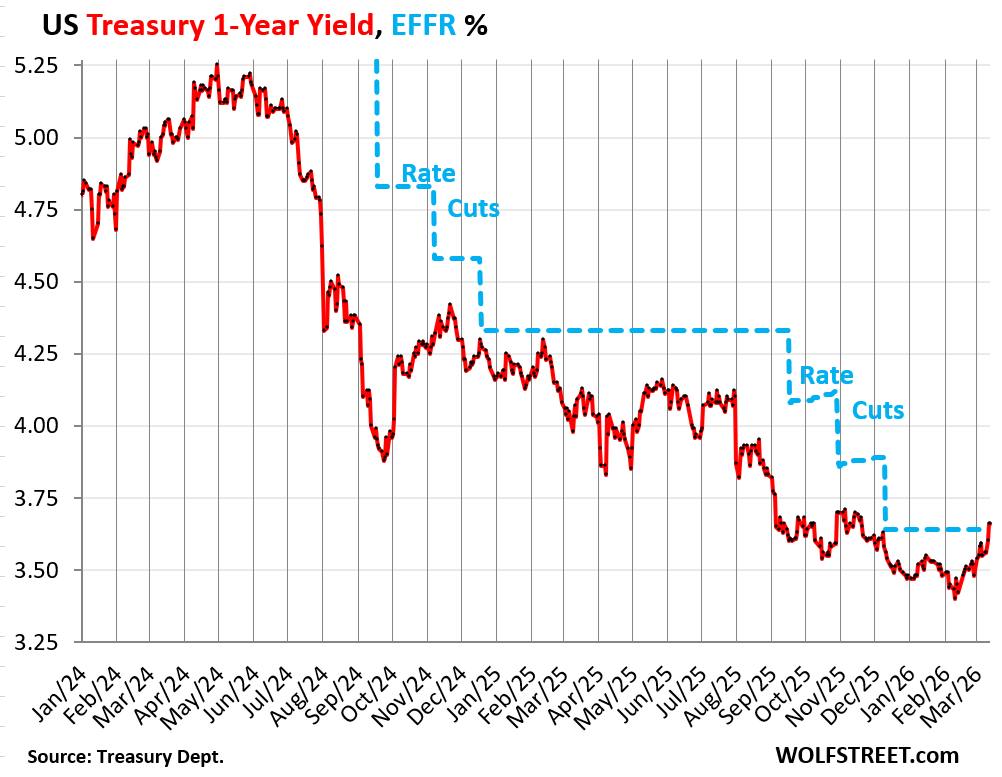

The 1-year Treasury yield squeaked over the Effective Federal Funds Rate (EFFR, blue in the chart) on Friday for the first time since November 2023, which had been nearly a year before the Fed even cut its policy rates. The EFFR is the overnight rate the Fed targets with its policy rates; and with the 1-year yield now at it, the bond market has moved rate cut expectations off the table for this year.

All Treasury yields across the yield curve, including all short-term maturities, are now at or above the EFFR, indicating that, for the bond market, rate cuts are essentially not in the scenario anymore.

The US government sold $651 billion of Treasury securities this week, spread over nine auctions, including 10-year Treasury notes and 30-year Treasury bonds.

Of these auction sales, $532 billion were Treasury bills, with maturities from 4 weeks to 26 weeks, most of them to replace maturing T-bills.

| Type | Auction date | Billion $ | Auction yield |

| Bills 4-week | Mar-12 | 101 | 3.640% |

| Bills 6-week | Mar-10 | 95 | 3.635% |

| Bills 8-week | Mar-12 | 91 | 3.625% |

| Bills 13-week | Mar-09 | 94 | 3.605% |

| Bills 17-week | Mar-11 | 70 | 3.600% |

| Bills 26-week | Mar-09 | 81 | 3.535% |

| Bills | 532 |

And $119 billion of Treasury notes and bonds were sold this week.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| Notes 3-year | Mar-10 | 58 | 3.579% |

| Notes 10-year | Mar-11 | 39 | 4.217% |

| Bonds 30-year | Mar-12 | 22 | 4.871% |

| Notes & bonds | 119 |

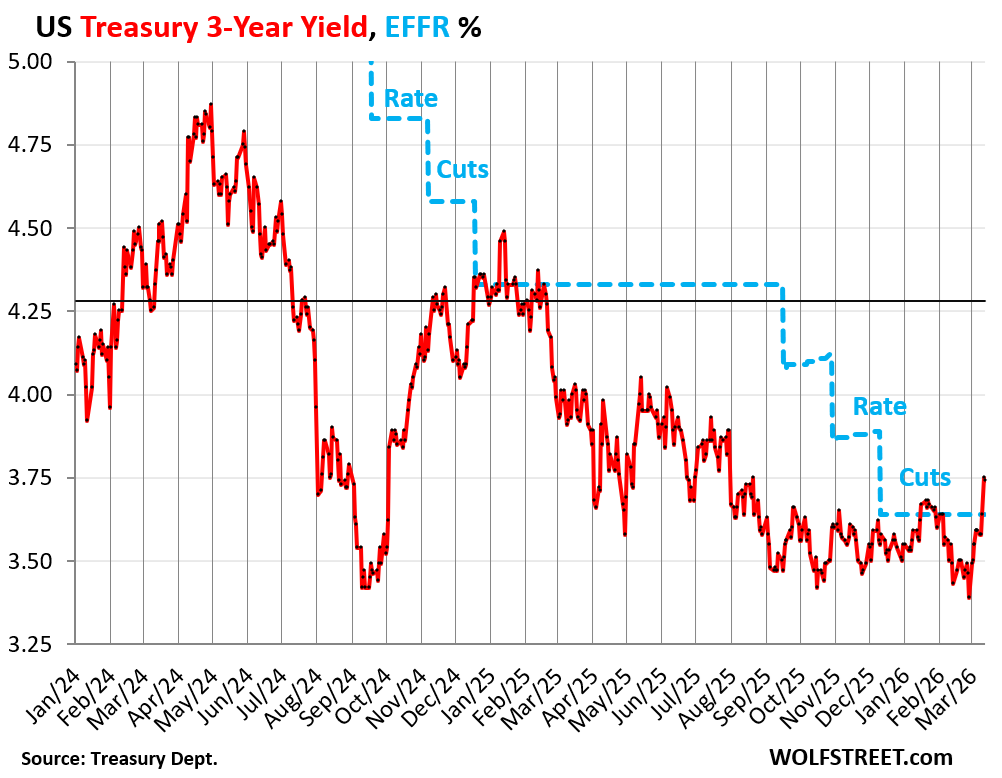

The 3-year Treasury notes sold at auction Tuesday morning at a yield of 3.58%. In the secondary market, the 3-year yield continued to rise for the rest of the week and by Friday closed at 3.74%, having jumped by 16 basis points since the auction. And it brought the yield spike over the past two weeks to 36 basis points. That’s a lot.

The issue with the 3-year maturities in the secondary market was in January and February, when they rallied ferociously (prices rose, yields fell) amid deafening Wall Street propaganda that the 3-year maturities were the sweet spot for whatever reason and that everyone needed to pile into them, and they did, and by February 27, the yield had dropped to an inexplicably low 3.38%. But then the propaganda died, the 3-year maturities sold off, and the yield spiked by 36 basis points in two weeks, the most of any Treasuries in that two-week period.

The three-year yield is kind of a bad deal for yield investors, though it can be a good deal for leveraged price speculators, if they can get out quick enough, which is maybe why it got hyped by Wall Street. The 3-year yield lagged the rate hikes in 2022 and 2023 (prices didn’t drop as much), and then it front-ran the rate cuts (prices fell faster sooner). But then at the end of February, it flipped and the yield spiked as these leveraged speculators tried to get out.

And from another point of view: The spike of the 3-year yield above the EFFR suggests that the possibility of rate hikes next year might be starting to worm its way into the scenario.

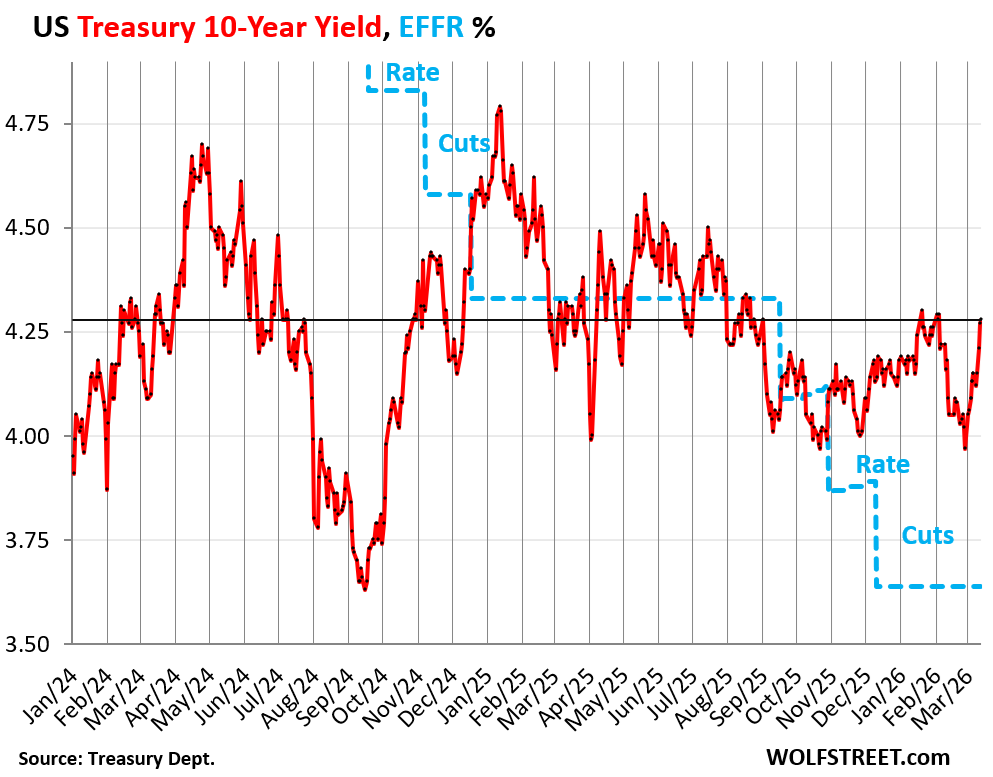

The 10-year Treasury yield rose to 4.28% by the close on Friday, the highest since early February, having risen by 13 basis points during the week.

A week ago on Friday, it had closed at 4.15%. At the 10-year Treasury note auction on Wednesday, they priced at 4.22%. There was nothing panicky about this, just a grind of higher yields and lower prices.

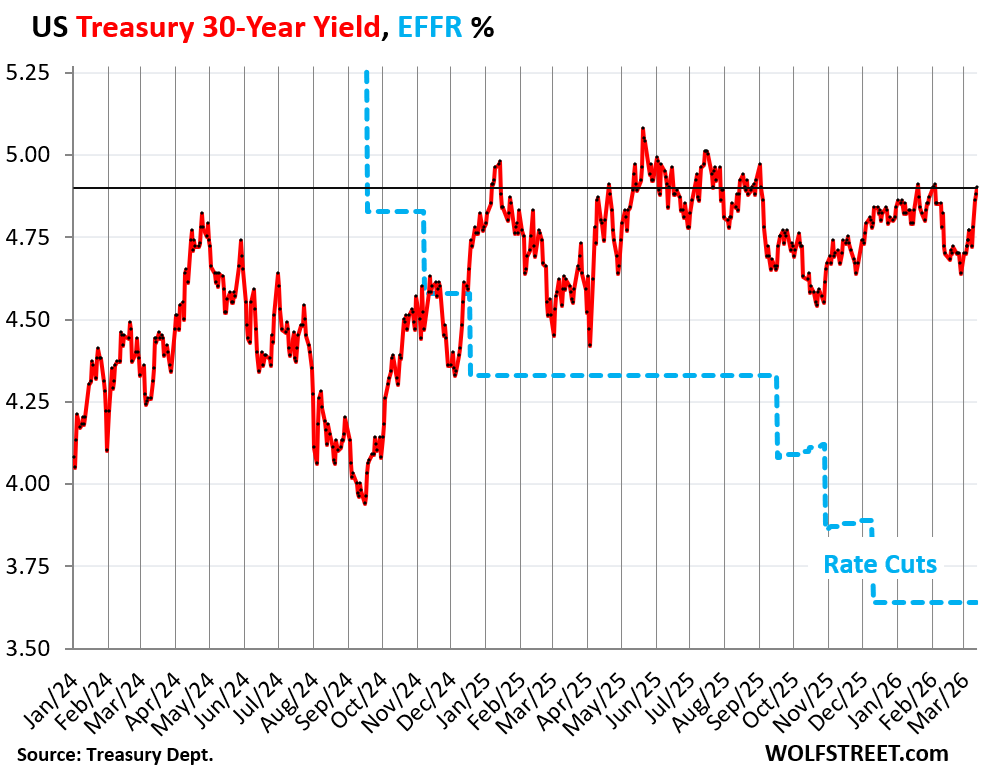

The 30-year Treasury yield rose to 4.90%, the highest since, well, one day in January, and one day in February, and before those two days, the highest since September, three rate cuts ago.

Buyers of the long bond aren’t focused on overnight policy rates. They’re worried about the next 30 years, about inflation during those years that would eat the purchasing power of their investment whose interest payments could be too low to compensate them for it; and they’re worried about even higher long-term interest rates in the future that would tank the market price of their long bonds if they try to sell them before they mature. Three decades is a long time for things to go wrong. And they want to be paid for taking that risk.

At the 30-year bond auction on Thursday, they priced at 4.87%, and in the secondary market, the 30-year yield continued to rise to 4.90% on Friday.

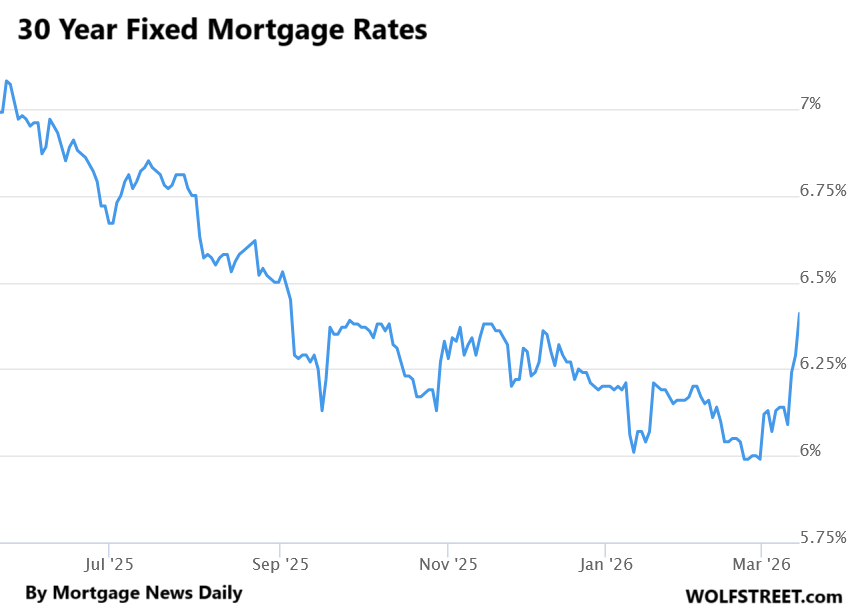

And mortgage rates spiked to 6.41%. The daily measure of the average 30-year fixed mortgage rate by Mortgage News Daily spiked by 27 basis points this week to 6.41% on Friday, the highest since early September, after having jumped by 14 basis points in the prior week.

Over the past two weeks, the daily measure of mortgage rates has spiked by 42 basis points, from 5.99% to 6.41%. The ballyhooed adventure below the 6% line was brief and shallow, and the snapback vicious.

Mortgage rates key off the long-term Treasury market, not the overnight rates targeted by the Fed’s policy rates. They roughly track the 10-year Treasury yield but are higher, and that spread between them varies.

The announced buybacks of MBS by Fannie Mae and Freddie Mac are supposed to shrink that spread, and thereby bring down mortgage rates, and they did that to some extent for a little while. But they cannot do anything about the bond market, and might increase the worries in the bond market as the two GSEs have to shed their Treasury holdings to get the cash to buy the MBS.

In case you missed it – and it’s going to get harder with mortgage rates back at 6.4%: What it Takes to Sell Homes in this Market: Lennar Cuts Average Selling Price to 2017 Level

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The way things are going now, the 10-year US Treasuries and mortgage interest rates will just continue to soar upwards with no end in sight.

MW: It was ‘unthinkable’ a couple of weeks ago, but could the next move by the Fed be a rate hike?

It should be, but NFW does this Fed have the balls, no matter how sick of Trump they may be.

FR will do something. And if past predicts present – it will be time late and the wrong action.

FR NIRP/ZIRP/QE and support for excessive gov’t debt is a prime mover in all the economic trauma that has evolved into the present.

It probably depends on when Trump wraps up the major hostilities with Iran, how well we’re able to secure transit through the Strait of Hormuz, and what the next couple of inflation & jobs numbers look like. But I certainly won’t bet against it, if employment holds up. Warsh will get a trial by fire as soon as he’s sworn in.

Probably close to CEP.

From my own pov, shedding the Earth of Iranian terrorists is worth some short-run economic pain.

I can’t wait for it to be “great again”.

Most PhD economists around the world can be replaced by Wolf Street. Thank you for doing what you do.

Wolf street all on its own is more valuable than WSJ, CNBC, FT & BLOOMBERG combined. Think about that. One blog site is better than all of MSM. MSM has betrayed us all a long time ago.

People like Wolf, Lacy Hunt, Michael pento, John Rubino, & Quoth the Ravin Chris Irons are the financial news now. People want the truth, not lies.

Karma is coming for the stock market. NIRP-ZIRP has twisted everyone views on bonds.

Honestly… I cant help but to feel anger .

I’ve been buying T bills , I BONDS, 30 YR & 20YR. Drunkmiller is shorting this stuff. Something about that man I don’t like. I cant put my finger on it… maybe it’s because he is a soros man.

Let’s be clear. You are investing in the independence, skill, transparency, and morality of the Federal Reserve.

Is that a low risk investment? I wouldn’t put all my eggs there.

Morality? Whose morals? Yours?

Picking up metaphorical nickels in front of an out of control steamroller bearing down on you, is what you’re doing.

Mohamed El-Arian is very good. It’s worth paying attention to everything he says (just like Wolf!) 😊

People watched what happened to TLT when the fed raised rates and think that long term government bonds is still a good investment. I won’t touch them! The only way out of this is the gubmint inflating the debt AKA your investments

Has everyone extolling Wolf kicked in some money? I did a few months ago. 50. Please contribute, and compensate Wolf for his work, that you benefit from in spades.

“Most PhD economists around the world can be replaced by Wolf Street.”

I’d vote for that!

While we’re at it, how about he replaces the gang on the Board of Governors too.

Agree, Wolf gives His honest unvarnished educated opinion so there for He would not be eccepted by the crooks pushing the buttons and pulling the levers in Our modern day corrupt government.

;-0)

Financial news isn’t what PhD economists do.

The 1981 peak of 15.82% occurred during a period of intense Federal Reserve efforts to contain high inflation.

Are we there yet? I will take 10% right now in my MMA’s. The great reset is just around the corner. AI won’t solve this problem, quietly quitting the market running for a safe haven. When will the all you can eat buffet on Wall Street be over? Does the Fed really want to eradicate inflation?

I remember getting 21% interest in1981. In a Merrill Lynch Cash Management Account (CMA

We had a truthful CPI at that time.

“We had a truthful CPI at that time.”

That CPI maxed out at 14.6% in April 1980. Are you living in a fantasy world, thinking it went to 21%? That was your money market account, not CPI.

In this cycle, CPI maxed out at 9.0% in June 2022. Back in 1980, inflation was massive, much worse than in 2022. I lived through both periods as an adult.

But what we DID have in 1980 and what you referenced were more “truthful” interest rates, as the Fed didn’t have the kind of huge balance sheet it has now, and as Volcker was going nuts with rate hikes to devastate the economy and cause 10% unemployment, including me coming out of grad school.

Cry us a river Wolf. MANY of us experienced that. We did fine because we understood that anything of real value requires real work. You know what else will result in massive unemployment (and worse)? Hyperstagflation.

I got a 10 yr CD at a Bank in KC that was 14.45% compounded daily which translated to 16.82 % ( I kept it as a memento ) ; it was an IRA ( only $2,000 invested ). The banker told me that rates would continue to rise so don’t lock it in for 10 yrs – I told him that if that was the case it wasn’t going to be worth anything anyway. Franklin Savings out of Lenexa KS ( it went under shortly thereafter but, the Bank that took over the accounts honored the CD. I think that was about the time that several banks went under in the mid-80s. I believe I got the CD in ’83 or thereabouts. Wish it would have been a larger investment but, I was only 34 at the time and in the Army so didn’t have a lot of extra income.

I don’t think Mark said that CPI was 21%. Reread his post, take a breathe.

I didn’t say he did, but there isn’t that much difference between 9% and 14.6%, for him to post this goofball comment, but there is between 21% and 9%. Re-read my comment.

Volcker’s implementation of reserve requirements against NOW accounts halted the rise.

I wonder where the buyers find $651 billion to purchase these Treasurys. Is it cash sitting in their bank accounts ? Or do they sell other securities to raise the cash?

And what is to stop the Fed from purchasing substantial amounts of them, or enabling other central banks to do so via swap lines?

Like the Bank of Japan does for JP govt bonds, the latter purchases reportedly having reached an all time high of 27789 bil yen in February 2026.

There is a fundamental thing you need to understand: Bonds are not stocks; with bonds you get your money back when they mature on the maturity date. With stocks, you have to sell them to get cash out.

Only the additional debt that is sold and that makes the total pile of debt grow will have to find new cash, and that’s about $2.2 trillion a year currently, or about $45 billion a week on average. So on average, the market needs to come up with $45 billion a week in new cash.

The rest of those auction sales replace maturing securities. So if you hold T-bills on automatic rollover in your brokerage account, each time your old T-bills mature, your broker buys at auction new T-bills with the cash from your matured old T-bills, plus you get the cash interest paid from the old T-bills. So people and funds, including money market funds and bond funds, that maintain a securities portfolio and want to keep it level have to replace what is maturing, and they don’t have to come up with any new cash to do that.

The rest of your comment is nonsense. The Bank of Japan has been shedding securities since it started QT at the beginning of 2024:

https://wolfstreet.com/2026/01/06/bank-of-japans-qt-cuts-502-billion-from-balance-sheet-jgb-yields-surge-as-boj-steps-away-from-bond-market/

Economic reality can be avoided (for a while)

BUT the effects of economic reality can not be avoided

Controlling the narrative, calling for cuts, making water run up hill works only so long.

Shock: I am in your camp and have been wondering about these same questions for a few years now. And yet, going back over some of Wolf’s earlier pieces relating to the issues, I keep coming back to a couple of themes, the first being the enormous demand we’ve been seeing for treasury issues (at least up to this point), and the second that there may be some key differences between the current environment versus what drove extraordinary measures under Volcker’s Fed back in the early 1980s. (And like Wolf, I graduated college around that time and it painfully limited my early career prospects.) A guaranteed 10% on my money would be awesome, assuming it’s not accompanied by persistent hyper inflation, but over the past few years we keep seeing these treasury yields retreat almost as soon as they hit the 5% mark. Still, I’m holding back some liquid funds and keeping that powder dry in the event long-term treasuries do spike the way you’ve implied they might. I’m waiting to see how this plays out.

I can’t imagine Volcker being good at anything but trout fishing.

volcker had bigger cajones than powell or yellen or bernake

Dr. Richard Anderson didn’t take into account the money multiplier when he spliced the legal reserves from the nonmember banks.

https://fraser.stlouisfed.org/title/review-federal-reserve-bank-st-louis-820/june-july-1983-24470?page=16

The realtors must be so depressed. Just when they thought the rates were heading below 6. And for this to happen just before the Spring selling season.

There will be NO spring selling season for Realtors. The only sales will be bank sales, distress sales and foreclosures. NO Realtors will be involved. Marland had 3,000 Realtors hangin it up last year. This year it will be 5,000.

Cassandra: Your “waiting to see how this plays out” doesn’t make sense to me. What are you waiting to see? If longer-term yields spike, you’ll still have the issue of inflation, which is unpredictable and capable of rapid change. Doesn’t it make more sense just to maturity-ladder the amount you want to allocate to Treasuries and their equivalents?

Could this be the start of a repeat of the 70’s. Too much money sloshing around. Nixon tries price controls, which they say made inflation worse, got embedded, expected and took off until Volcker squeezed the sloshing dollars out of the economy.

War drags on, more stimulus, Warsh lowers interest rates and we’re off to the races.

LOL! What did the national debt and deficits look like in the 70’s? Yeah go ahead, raise the federal funds rate to 15%, I triple dog dare you!!

This is NOT the 70’s.

Hedge accordingly.

The exploding national debt is not a reason to keep rates low.

Low rates have encouraged the continual deficit spending and resultant borrowing by the government.

Rates must rise to a point that it deters deficit spending.

Even Keynes said deficit spending is to be removed once the economy reaches a certain normality or recovery. The “new” Fed since 2009 at least, decided to turn the punch bowl into Buckingham Fountain.

Notice corporate America is floating debt and buying their own stock….rather than issuing stock. This points to the attractive level of interest rates….ie too low. IMO.

“The exploding national debt is not a reason to keep rates low.”

No shit sherlock. My first mortgage was at 18%, so work on your reading comprehension skills, because you completely missed the point.

The price of money/credit must be high enough to compensate for the RISK and PREVENT capital mis-allocation and mal-investment (bubbles). DUH.

The Fed raised the FFR about 5.25%, and it has caused the interest expense to explode to the point where we’re spending $1 out of every $5 we take in one servicing the debt.

Sure, the Fed might be able to raise interest rates back up to 5%, but there’s a good chance that will cause a recession & will add at least $200B more to interest expense, if not more.

The main problem with Congress is they don’t want to go after waste & fraud. And the problem there is that going after at least $500B will again cause a recession.

In theory, your point is valid, but the national debt renders that theory extremely hard to implement.

WB

this is Sherlock and I was responding to the notion, floated by other posters, that because the debt was so large and higher interest rates would cause the debt service to be a larger issue that it already is, that thus that a reason not to raise rates.

I disagreed.

@BenW lol, congress isn’t going after the waste and fraud because it was engineered as paybacks for campaign support. That’s the way the game works, you can see it out in the open now as the Trump children rack up investments in war supplies.

The FOMC watches real rates of interest to judge whether policy is actually restrictive or stimulative, even if the effective federal funds rate hasn’t changed. Inflation expectations are unanchored.

Seems the administration is walking a fine line between wanting in increase affordability for those that don’t own a home but want to along with those paying high rents, and those that will feel poor and spend less money supporting the economy if their real estate holdings decrease in value by another 30%

Many years ago (10-15), I read a comment by a financial fund manager on the deficits. His concern was that if the government did not get them under control, it would lose the ability to lower interests during a recession as a stimulus measure, and hence any recession would be more severe and last longer than previous ones.

From your charts, it does like the effects of federal reserve interest cuts are becoming less effective.

I’ll take this one for Wolf.

They found a new trick. It’s called QE.

That’s an old trick. They already did that during WW2, which, after the war led to 17% inflation, and they undid it.

That old word stagflation pops up now and again in some financial articles that I come across these days. As in, are we going there again?

Those weren’t good times. I remember them.

I just read an interesting report in the NYT about the Commerce Department effort to cheat at the margins to try to shave downward the reported inflation rate. Apparently, when issuing the January PCE, rather than using the customary legal services data, the Commerce Department switched data sources to capitalize on a likely bogus 2% January increase in legal service costs rather than a 11% increase that the usual data suggested. Of course, the legal service portion likely should go up more than 2% in January 2026 since that is when the law firms adjust their rates for the new year and try to outrun inflation. Whether 11% is accurate should just be subject to correction later.

It is hard to have confidence in the numbers anymore. They are making unannounced changes on the fly all meant to under report inflation and induce the Federal Reserve to cut rates. As Wolf has reported, the Trump Administration is especially likely cheating on the housing numbers, both owners and renters. Since that is a large % of the CPI, it has a much larger effect than the cheating going on with the legal services costs. But if they are cheating multiple times which we know of, what else are they fiddling with?

The one investment most affected by this is TIPS (inflation indexed treasury bonds) which under compensate for inflation, while losing value as market rates climb, making them a terrible investment. That basically impairs the one obvious method of trying to protect yourself from inflation.

The 10- year below 5% seems low to me. Maybe I’m just old…

I’m just itching to leave the first comment on your next housing article about how cheaply built new homes are nowadays.

Ok, calm down. My name is Bozo, after all.

I would like to see my MMA between 4-5%.