And they fell in 21 of our 33 metros: Tampa, Austin, Miami, San Diego, Los Angeles, San Jose, San Francisco, San Antonio, Dallas, Phoenix, Orlando, Atlanta, Denver, Raleigh, Houston, Seattle… Others up YoY: Boston, Chicago, New York, Philadelphia… A few hit new highs.

By Wolf Richter for WOLF STREET.

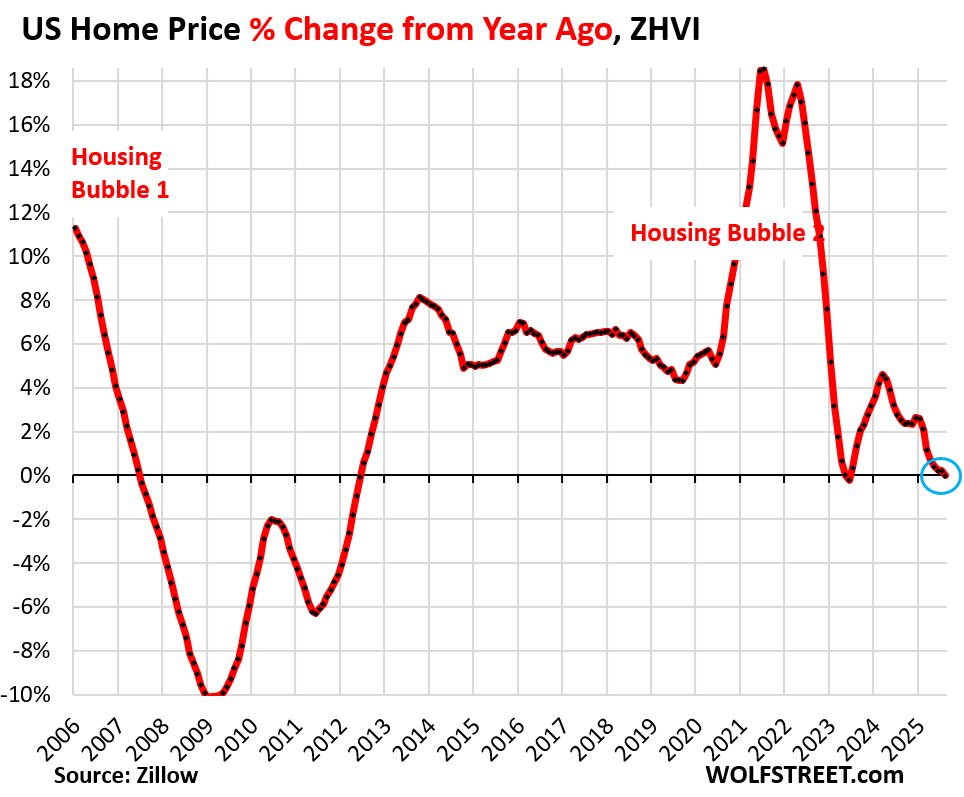

At the national level, prices of mid-tier single-family homes, condos, and co-ops declined year-over-year in August, the first decline since June 2023, and both were the first declines since the Housing Bust.

But prices moved in different directions among the 33 large and expensive metropolitan statistical areas (MSAs) that we track here: 21 had year-over-year (YoY) declines in July, up from 6 at the end of 2024. And in 23 of our 33 metros, prices were down from their peaks in prior years. But in a few others, prices inched up to new records.

The 21 metros of our 33 metros with year-over-year price declines:

The five metros with the biggest year-over-year declines among our 33 metros were in Florida and Texas.

Year-over-year declines in August:

- Tampa: -6.1%

- Austin: -5.8%

- Miami: -4.3%

- Orlando: -4.1%

- Dallas: -3.8%

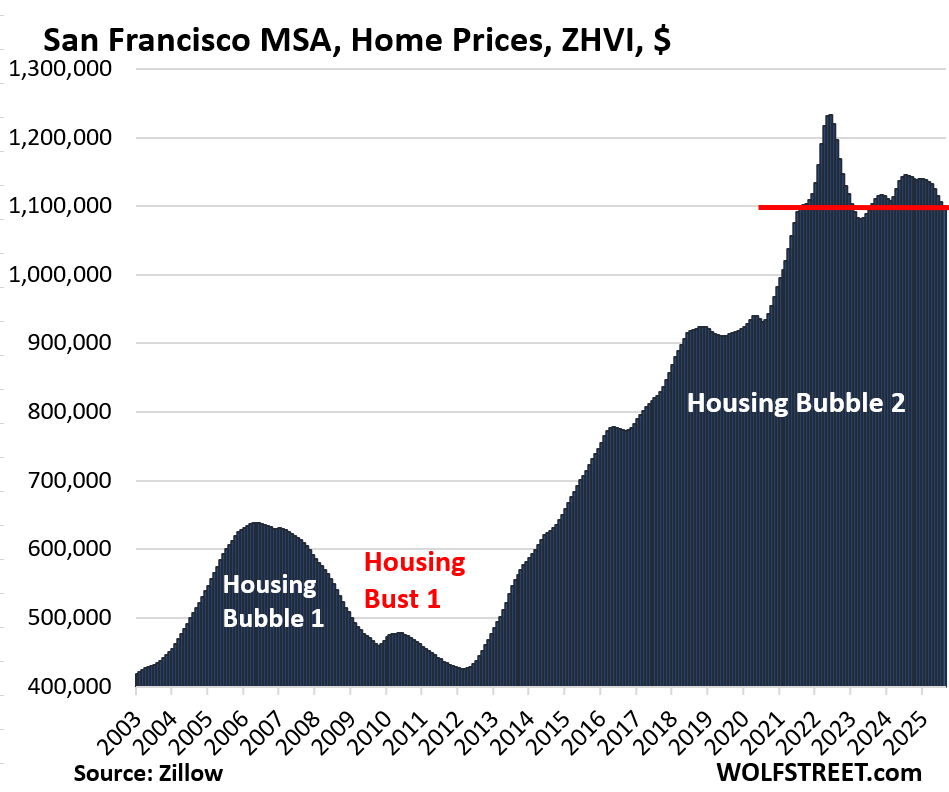

- San Francisco: -3.8%

- Phoenix: -3.6%

- San Antonio: -3.2%

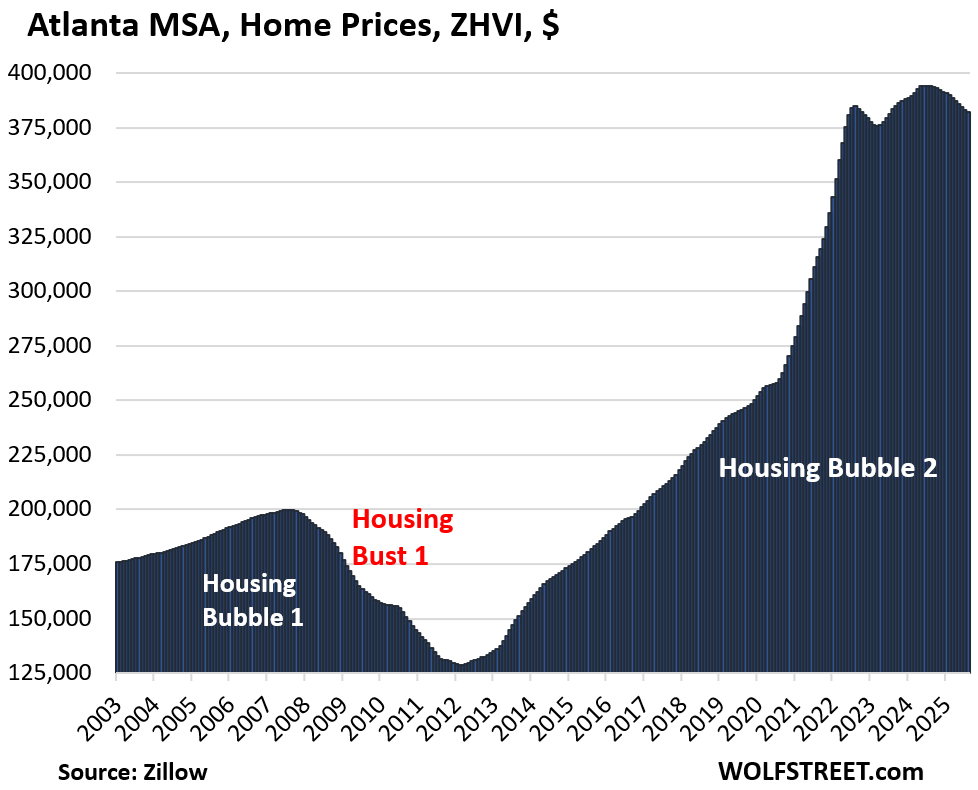

- Atlanta: -3.0%

- Denver: -2.8%

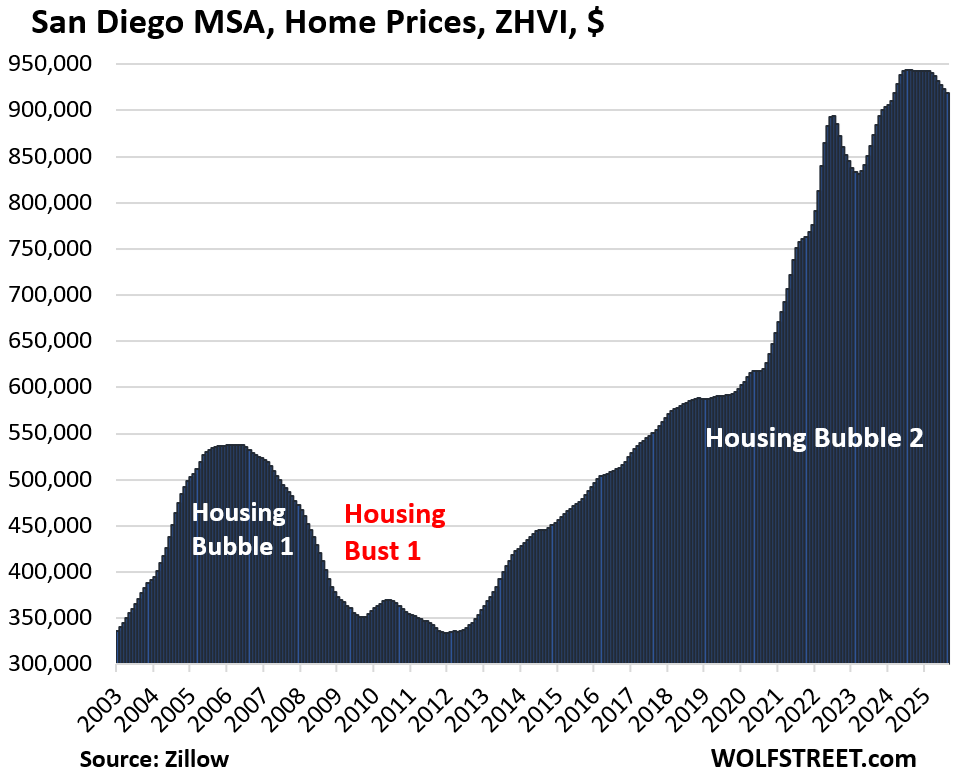

- San Diego: -2.5%

- Raleigh: -2.2%

- Sacramento: -2.0%

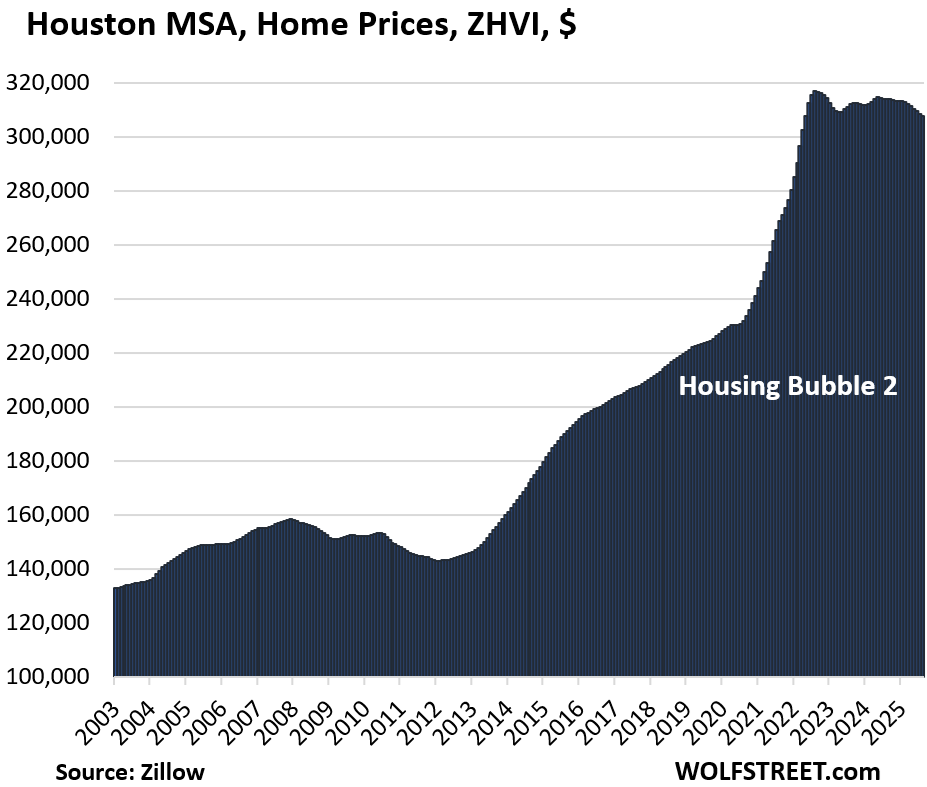

- Houston: -1.9%

- San Jose: -1.7%

- Honolulu: -1.7%

- Charlotte: -0.9%

- Portland: -0.7%

- Seattle: -0.6%

- Los Angeles: -0.4%

- Nashville: -0.1%

The 23 metros of our 33 whose prices are down from their highs in 2022 and 2024.

The peaks of 17 metros were in 2022; the peaks of the remaining 6 were in 2024 (Miami, San Diego, Atlanta, Charlotte, San Jose, Los Angeles).

Percentage declines from their respective highs in prior years:

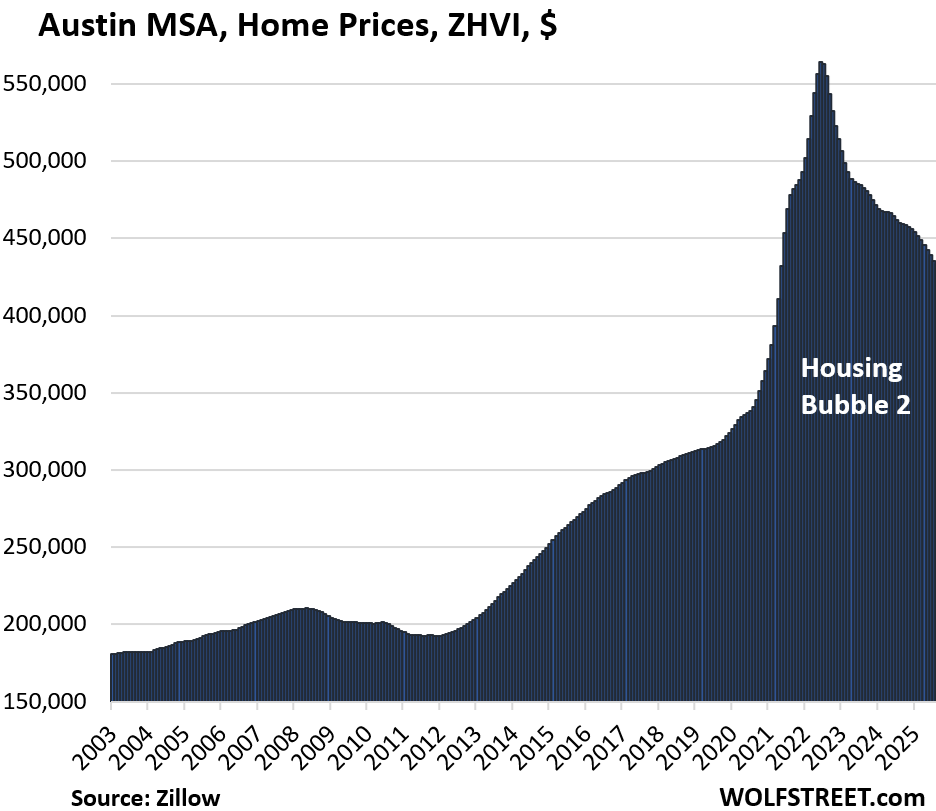

- Austin: -23.2%

- San Francisco: -10.7%

- Phoenix: -10.5%

- San Antonio: -8.4%

- Denver: -7.2%

- Sacramento: -7.1%

- Tampa: -6.7%

- Dallas: -6.5%

- Honolulu: -5.2%

- Portland: -4.8%

- San Jose: -4.8%

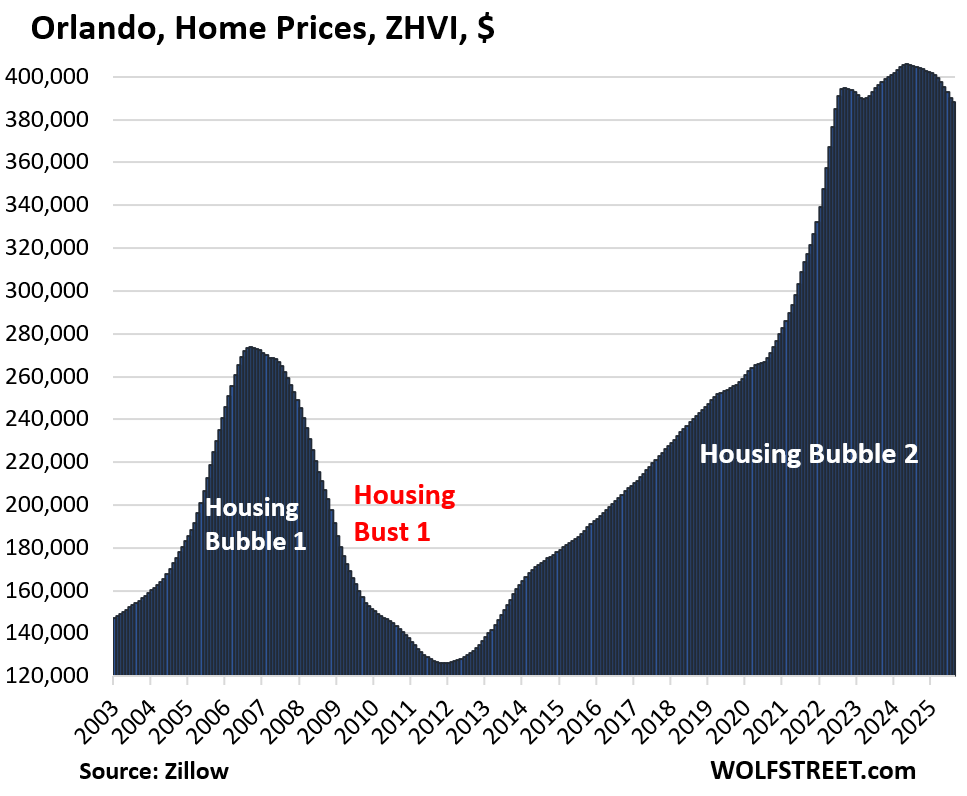

- Orlando: -4.4%

- Miami: -4.3%

- Seattle: -4.1%

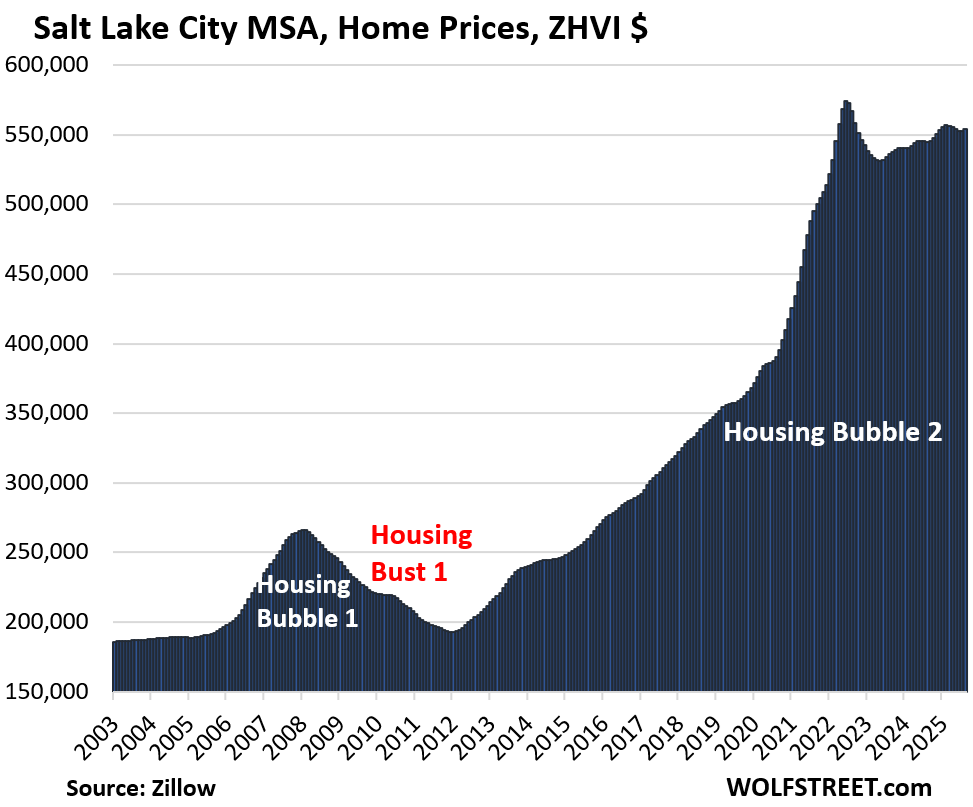

- Salt Lake City: -3.7%

- Raleigh: -3.5%

- Atlanta: -3.1%

- Houston: -2.8%

- San Diego: -2.6%

- Las Vegas: -2.5%

- Los Angeles: -2.5%

- Nashville: -1.7%

- Charlotte: -1.0%

Prices skidded in many markets because supply of existing homes has surged and demand has plunged. And homebuilders have been aggressively building inventory, and that inventory of new homes for sale reached the highest level since 2008, and in the South the highest level ever.

Methodology: All pricing data here for the 33 metropolitan statistical areas (MSA) is from the seasonally adjusted three-month-average mid-tier Zillow Home Value Index (ZHVI), released today. The ZHVI is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals. Zillow’s Database of All Homes also has sales-pairs data.

All data here about active listings is from Realtor.com.

To qualify for this list of 33 most splendid housing bubbles, the MSA must be one of the largest by population and must have had a ZHVI of at least $300,000 at some point. Some metros that are large enough don’t qualify for this list because their ZHVI has never reached $300,000, despite the blistering surge of home prices in recent years, such as the metros of New Orleans, Memphis, Oklahoma City, Tulsa, Cincinnati, and Pittsburgh.

The 33 Most Splendid Housing Bubbles.

In the little tables, MoM = month over month; YoY = year-over-year. In the column furthest to the right: the percentage increase “since 2000.”

| Austin MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -23.2% | -0.5% | -5.8% | 149% |

The lowest since May 2021.

From January 2020 through June 2022, prices in the Austin-Round Rock-San Marcos metro exploded by 73%. This price explosion documents the absurdity that the housing markets had become under the Fed’s reckless free-money monetary policy until 2022 – and when money is free, prices don’t matter.

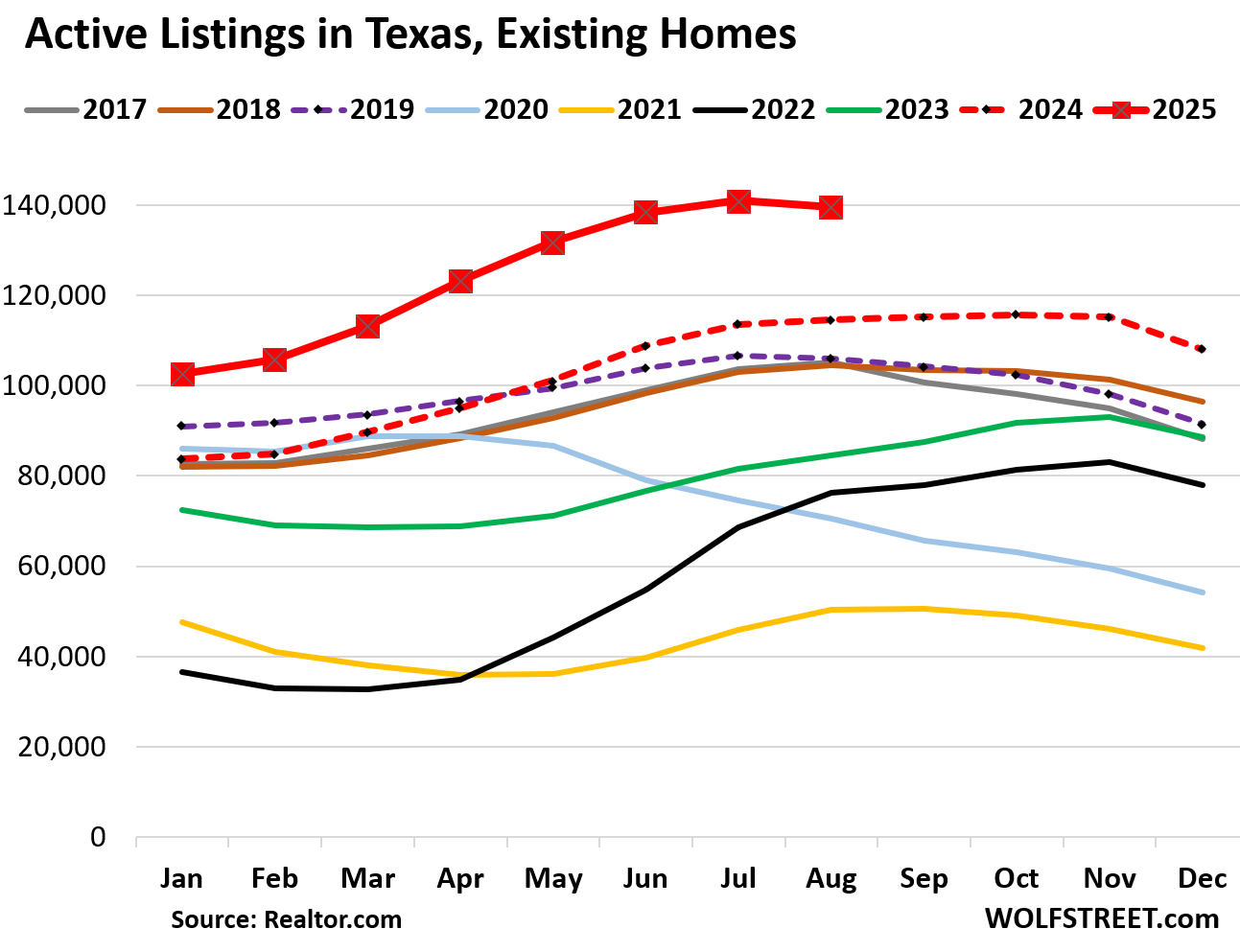

Here is what active listings in Texas look like:

| San Francisco MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -10.7% | -0.6% | -3.8% | 283% |

The San Francisco-Oakland-Fremont metro includes San Francisco, much of the East Bay (such as Oakland), much of the North Bay, and goes south on the Peninsula into Silicon Valley through San Mateo County. It does not include the San Jose metro, which covers the southern portion of the Bay Area (see below).

From January 2020 through June 2022, prices exploded by 33%.

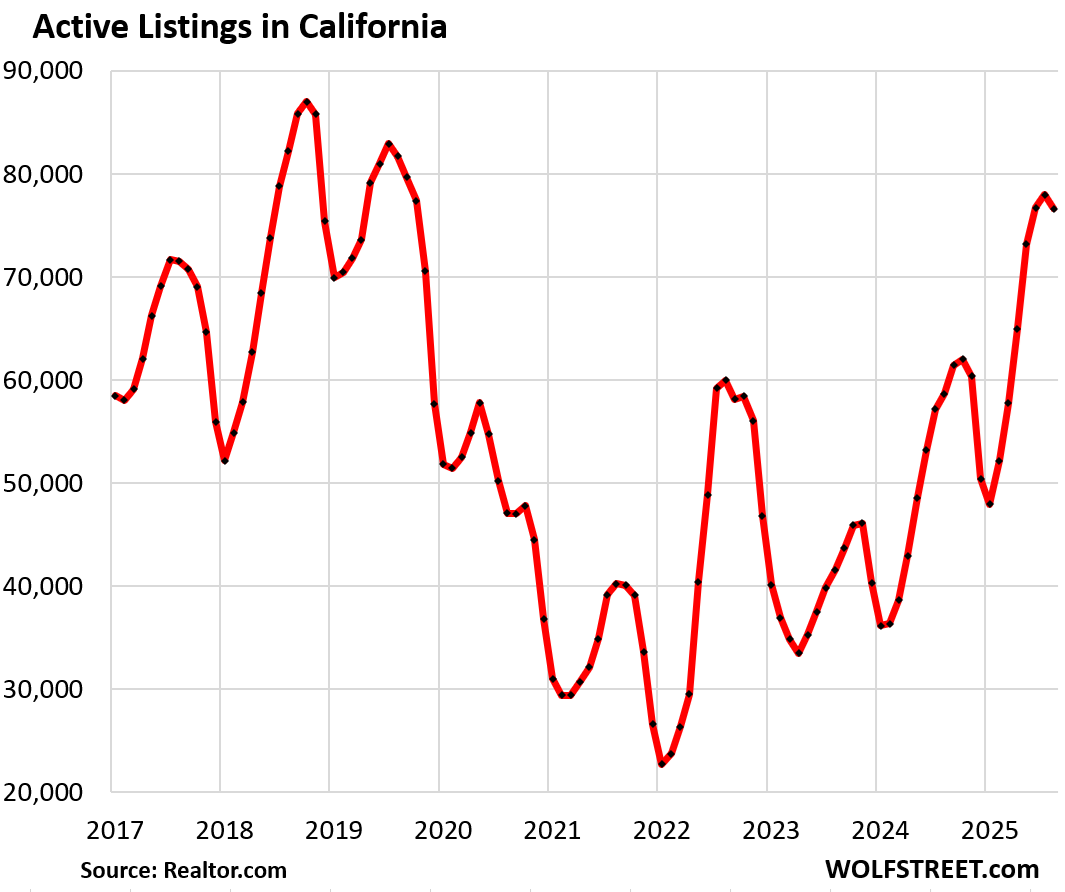

Inventory across California has been surging. And homes now spend more time on the market before they’re delisted or sold for this time of the year than in well over a decade.

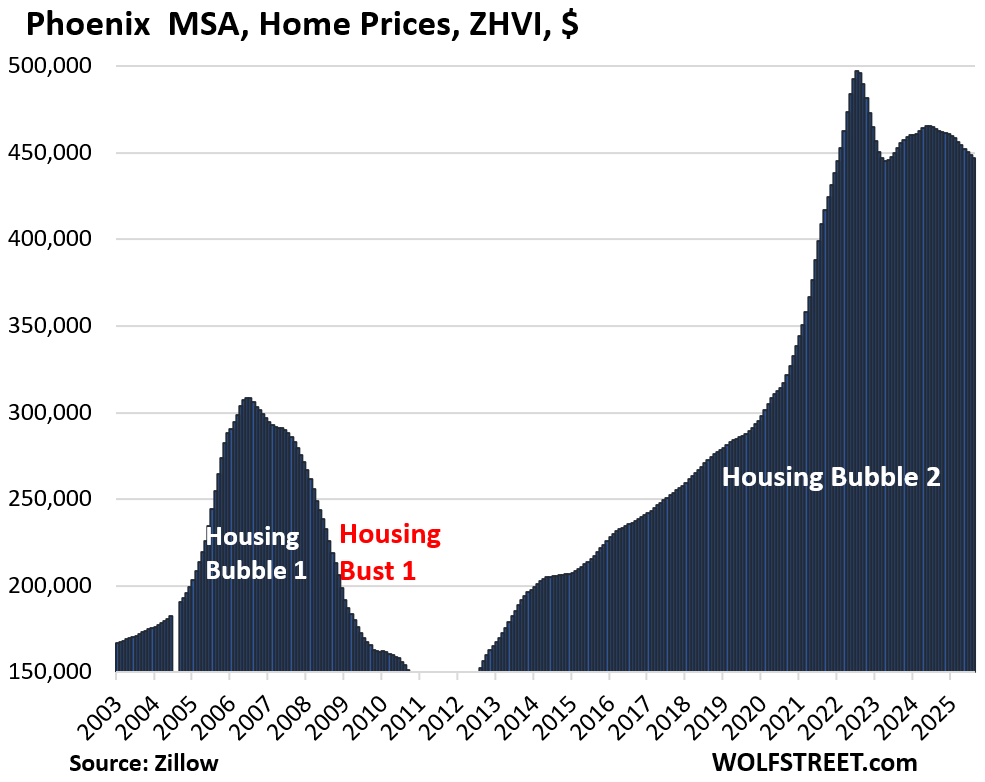

| Phoenix MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -10.1% | -0.4% | -3.6% | 212% |

Prices exploded by 65% from January 2020 through June 2022.

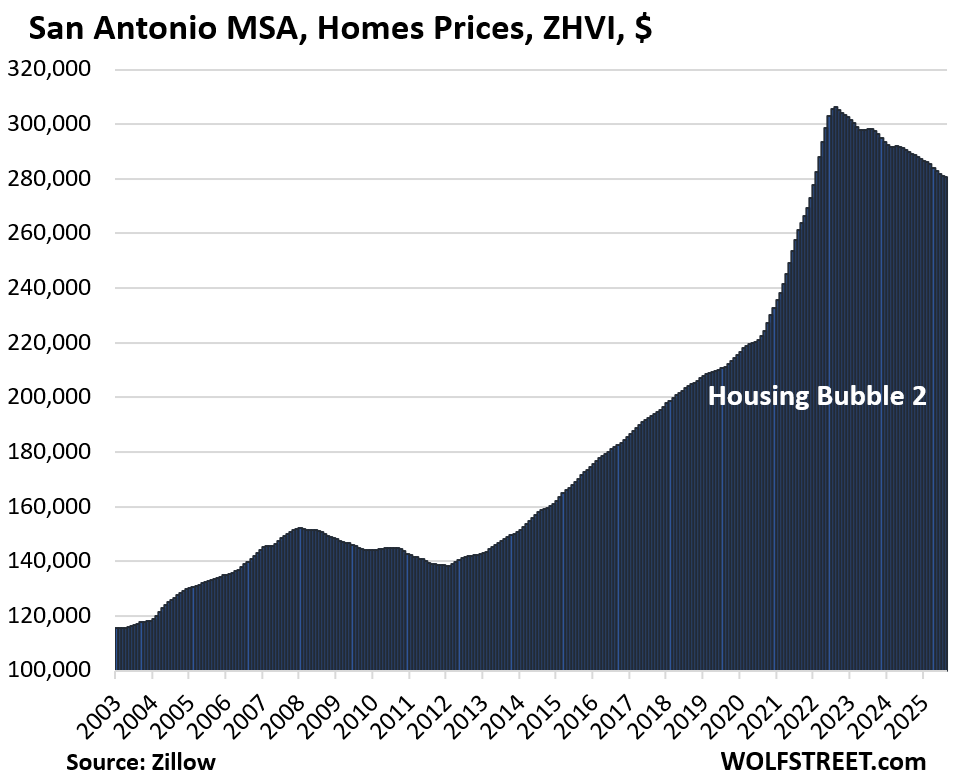

| San Antonio MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -8.4% | -0.2% | -3.2% | 144% |

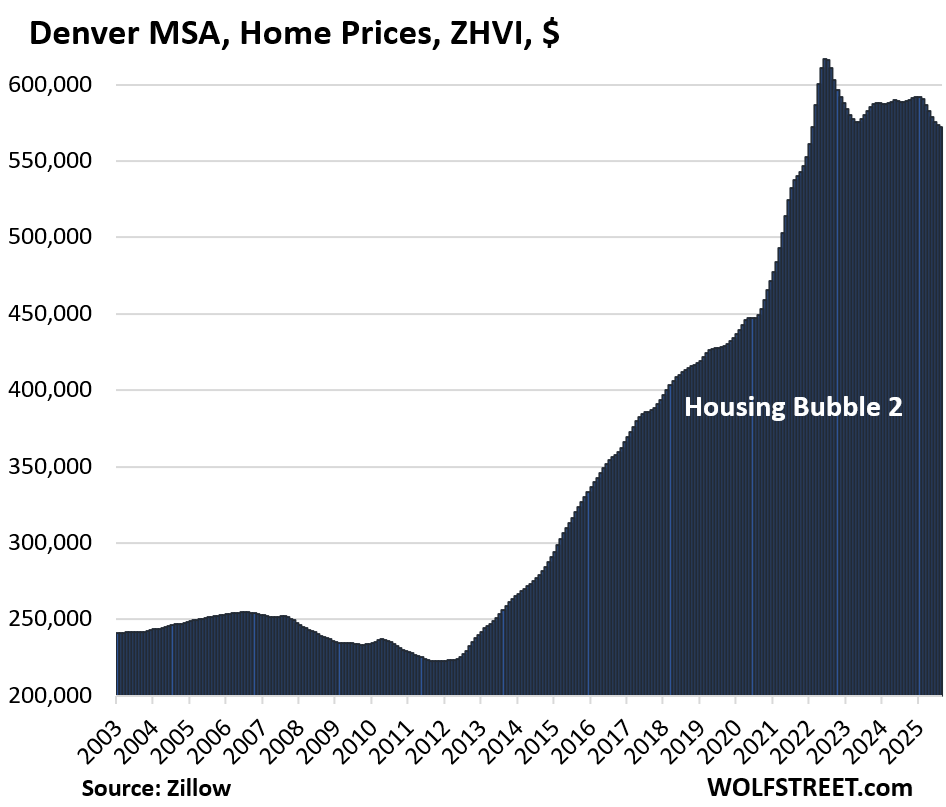

| Denver MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -7.2% | -0.2% | -2.8% | 203% |

And inventory in the Denver MSA:

| Sacramento MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -7.1% | -0.4% | -2.0% | 239.9% |

| Tampa MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -6.7% | -0.7% | -6.1% | 256% |

Prices exploded by 60% between January 2020 and June 2022.

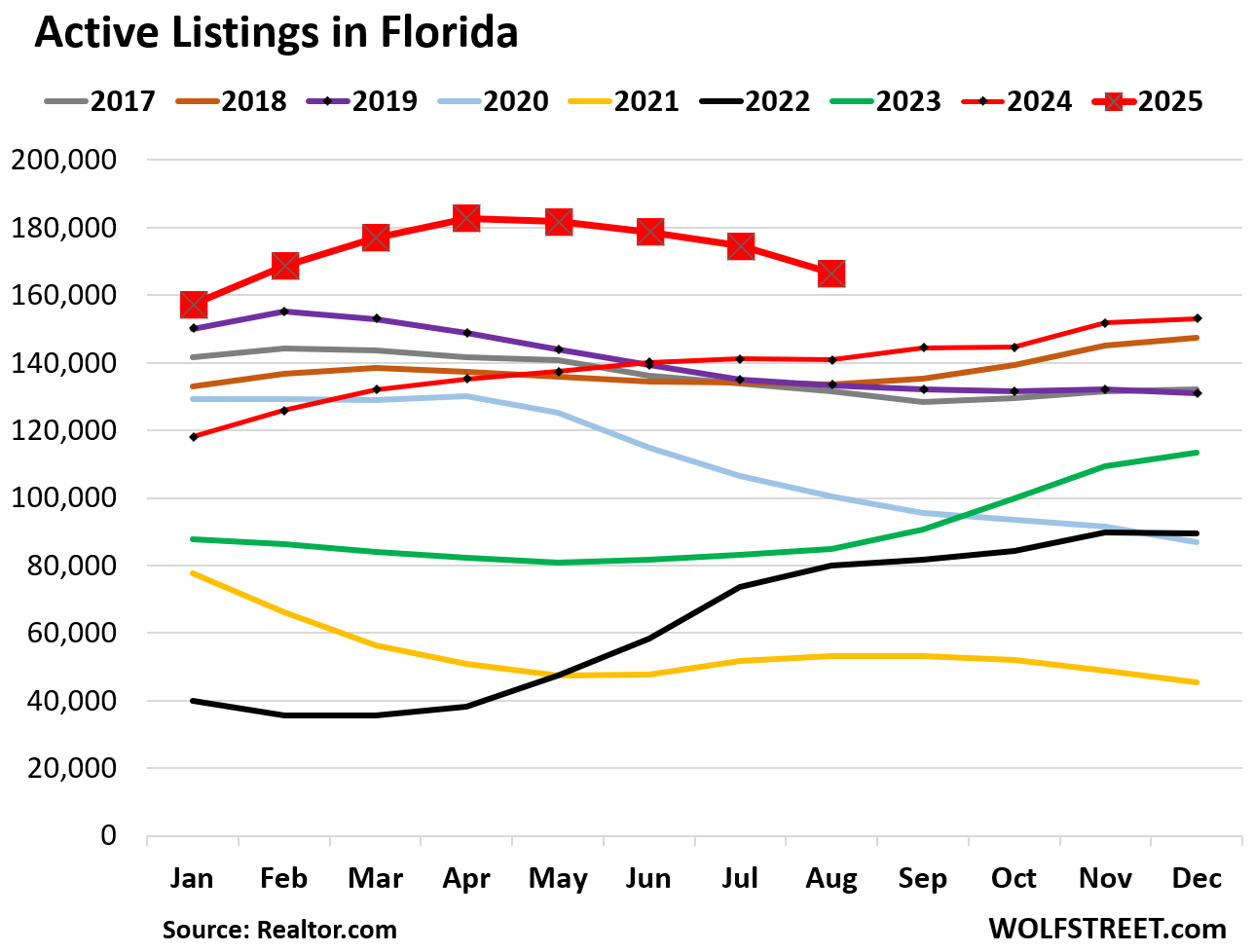

Active listings in Florida have been all year at the highest levels in well over 10 years:

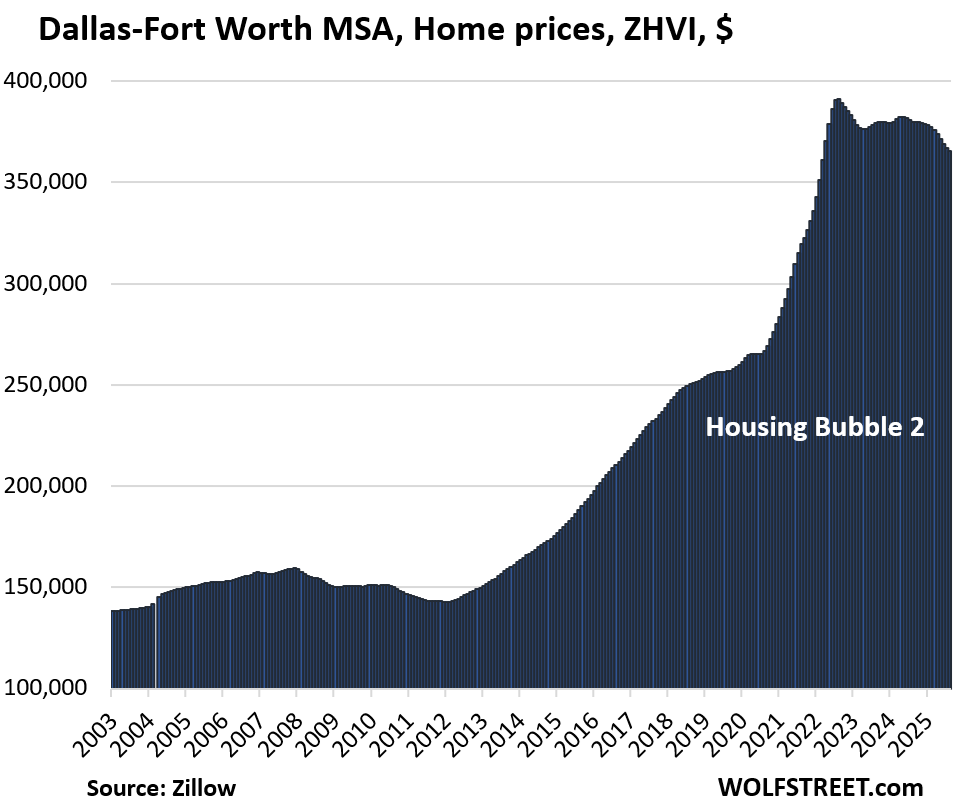

| Dallas-Fort Worth MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -6.5% | -0.4% | -3.8% | 184% |

Prices exploded by 48% between January 2020 and June 2022.

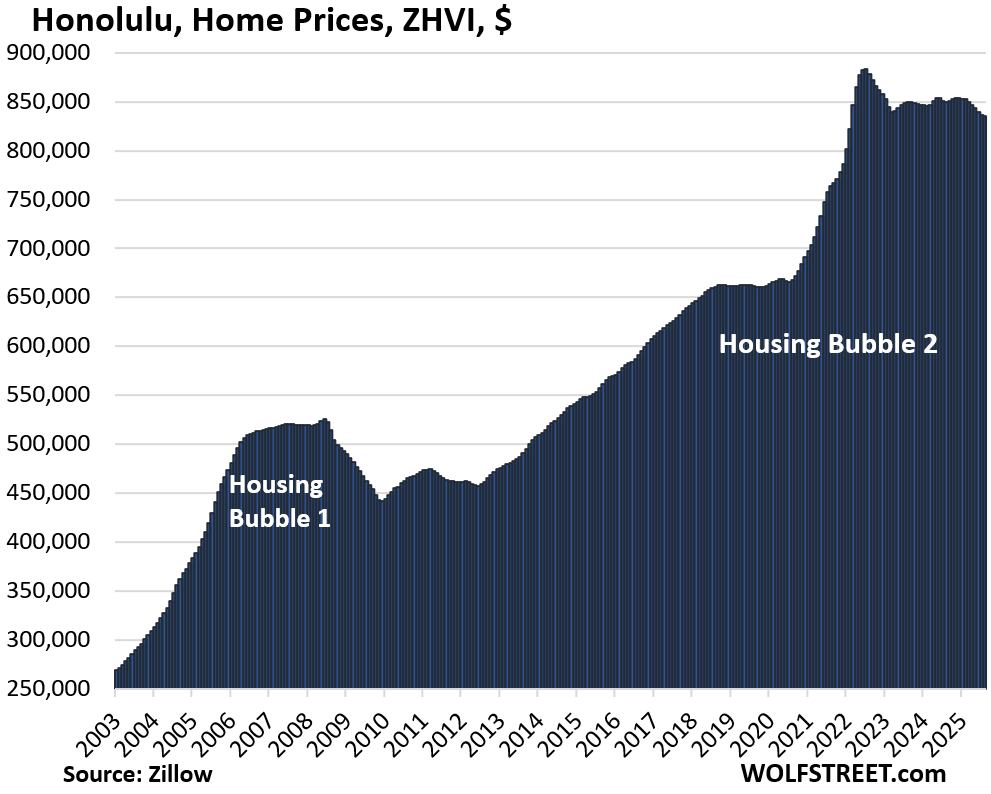

| Honolulu, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -5.4% | -0.2% | -1.7% | 275% |

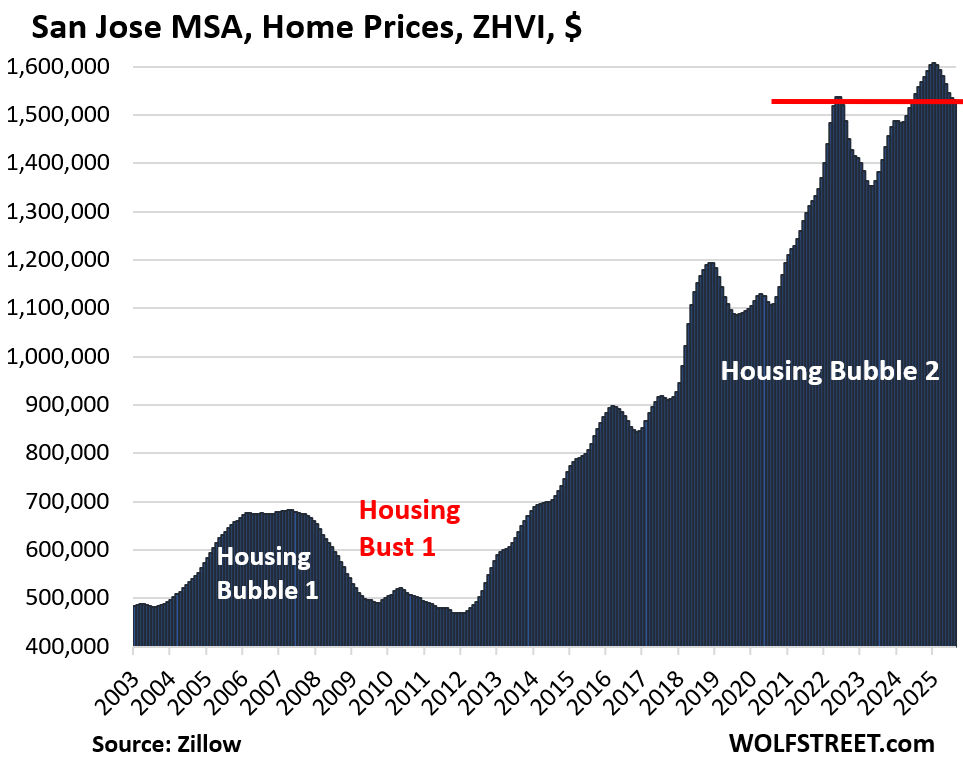

| San Jose MSA, Home Prices | |||

| Fr Dec 2024 high | MoM | YoY | Since 2000 |

| -4.8% | -0.2% | -1.7% | 326% |

Back to March 2022.

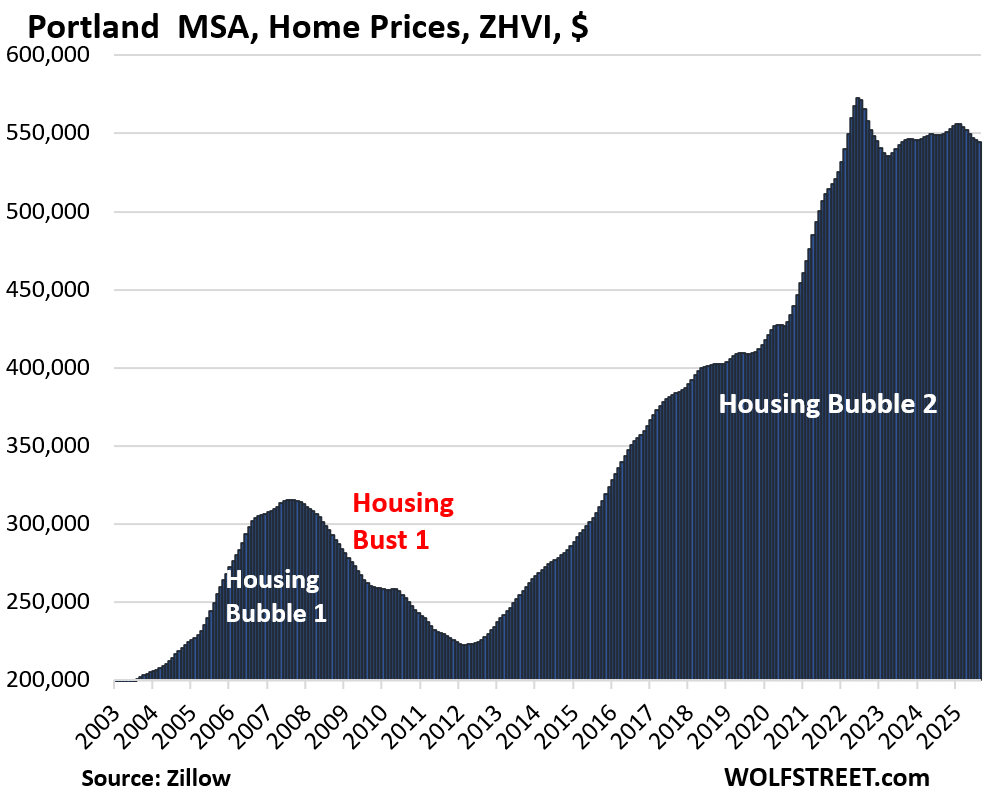

| Portland MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -4.8% | -0.2% | -0.7% | 212% |

| Orlando MSA, Home Prices | |||

| From June 2022 | MoM | YoY | Since 2000 |

| -4.4% | -0.6% | -4.1% | 226% |

Prices exploded by 48% between January 2020 and June 2022.

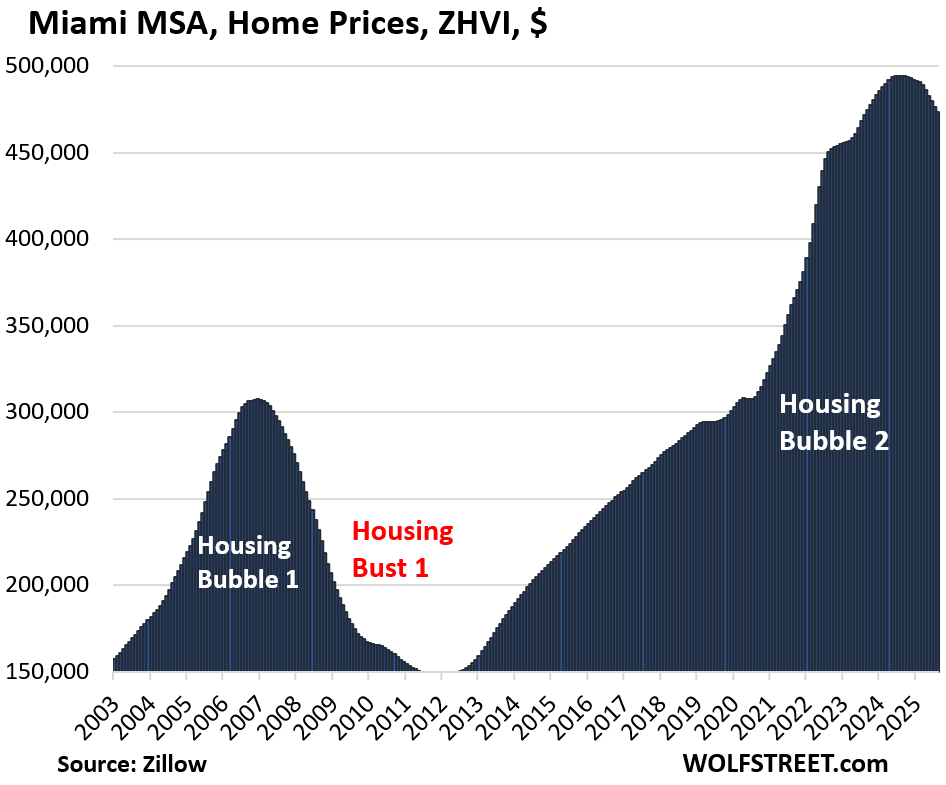

| Miami MSA, Home Prices | |||

| Fr Sep 2024 peak | MoM | YoY | Since 2000 |

| -4.3% | -0.6% | -4.3% | 315% |

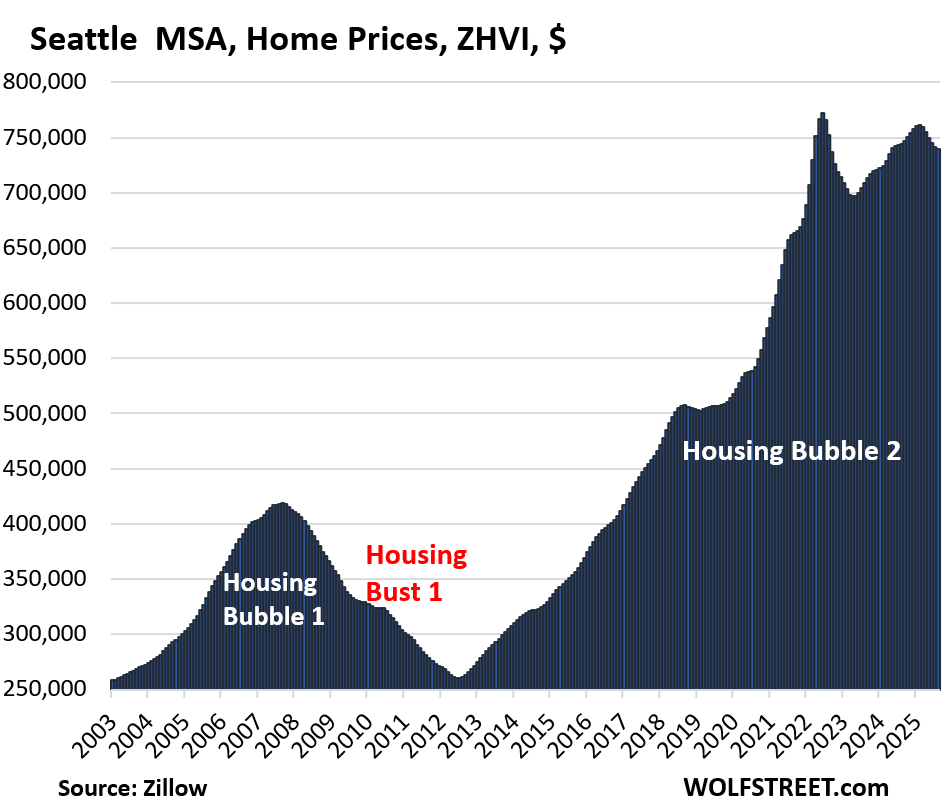

| Seattle MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -4.1% | -0.2% | -0.6% | 232% |

In the 2.5 years through June 2022, home prices had exploded by 49%.

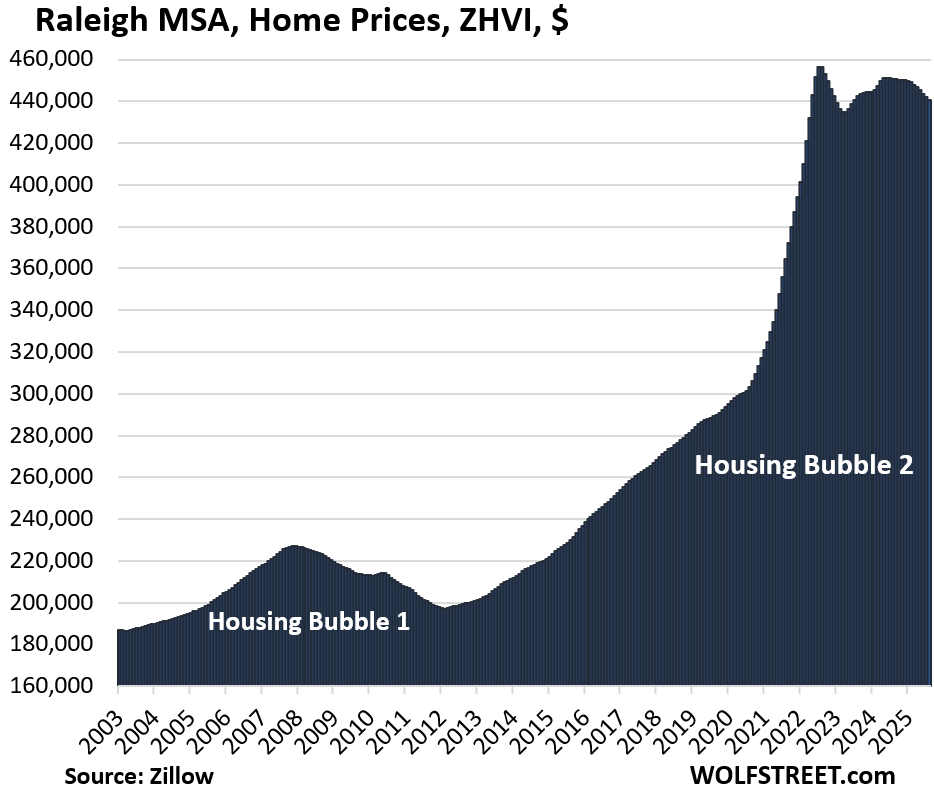

| Raleigh MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -3.5% | -0.3% | -2.2% | 153% |

| Salt Lake City MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -3.5% | 0.2% | 1.6% | 215% |

Prices exploded by 54% from January 2020 through June 2022.

| Atlanta MSA, Home Prices | |||

| From July 2022 | MoM | YoY | Since 2000 |

| -3.1% | -0.2% | -3.0% | 156% |

Prices exploded 51% between January 2020 and June 2022.

| Houston MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -2.8% | -0.2% | -1.9% | 147% |

| San Diego MSA, Home Prices | |||

| Fr Jul 2024 peak | MoM | YoY | Since 2000 |

| -2.6% | -0.4% | -2.5% | 328% |

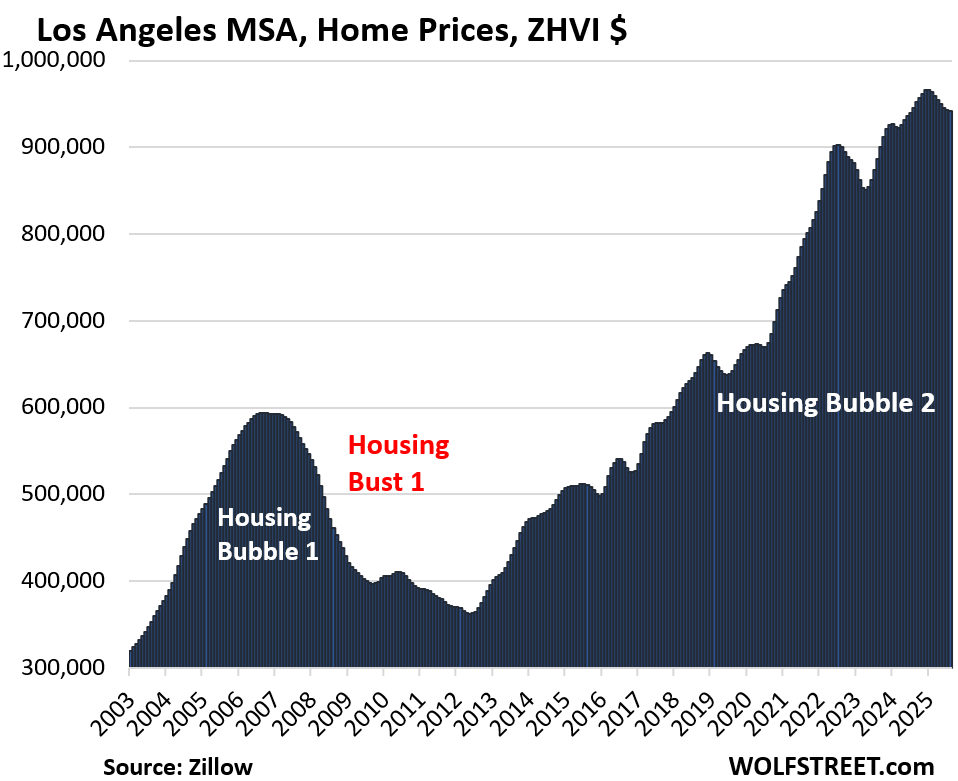

| Los Angeles MSA, Home Prices | |||

| Fr Dec 2024 high | MoM | YoY | Since 2000 |

| -2.5% | -0.1% | -0.4% | 324% |

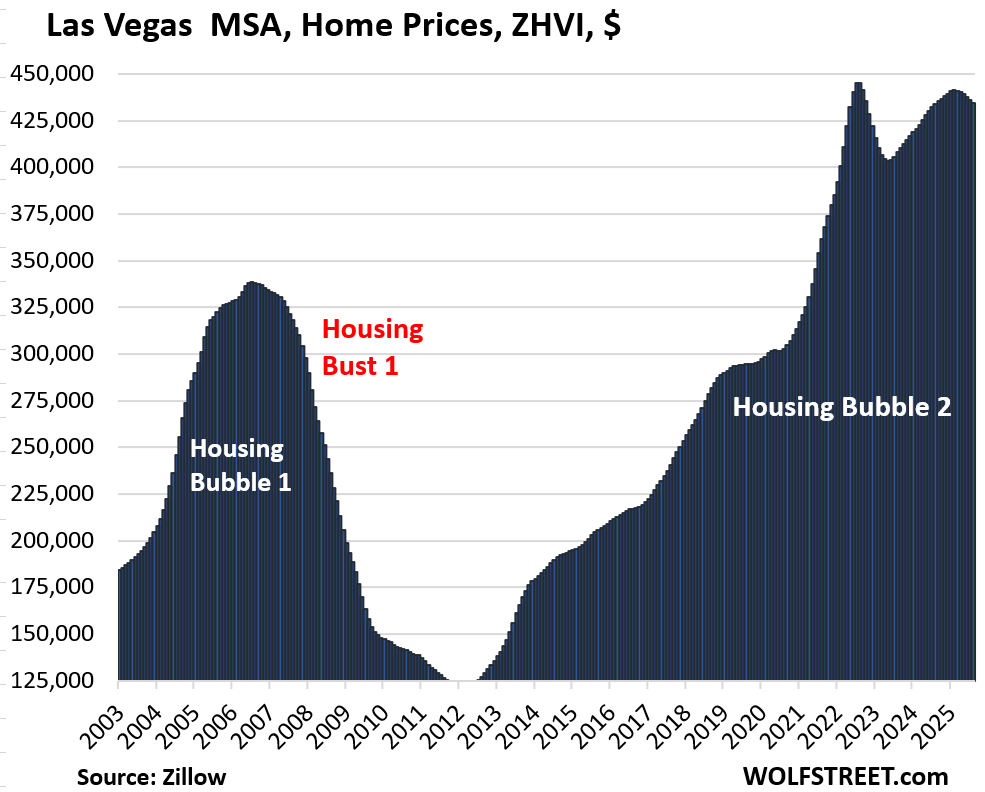

| Las Vegas MSA, Home Prices | |||

| From June 2022 peak | MoM | YoY | Since 2000 |

| -2.5% | -0.4% | 0.1% | 179% |

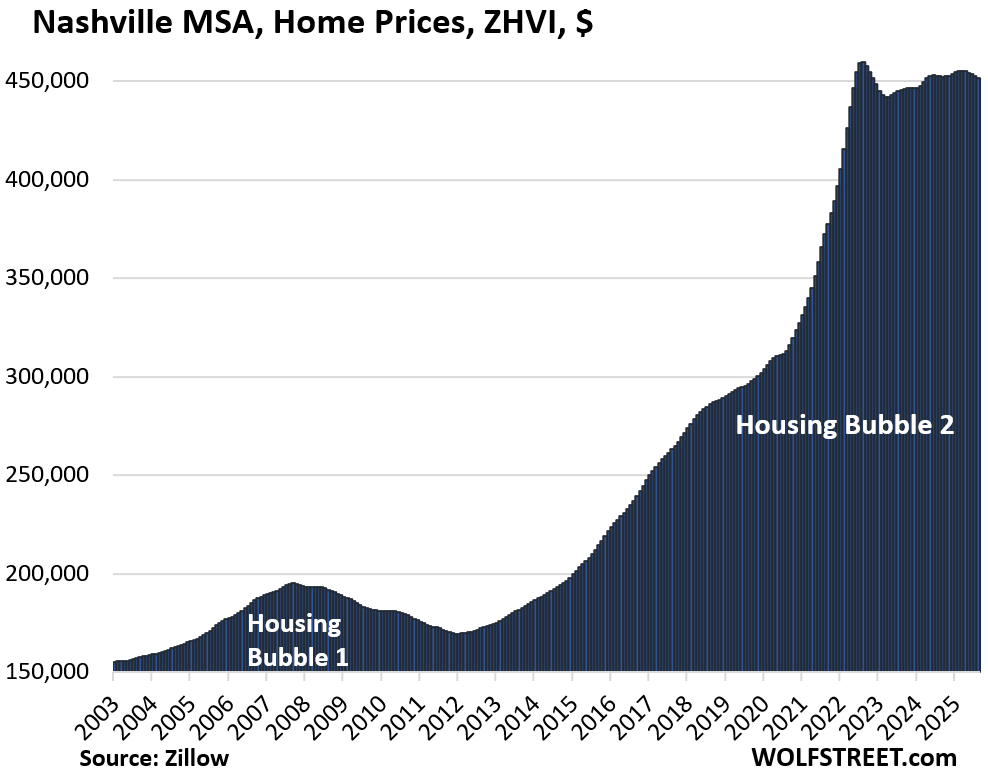

| Nashville MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -1.7% | -0.2% | -0.1% | 215% |

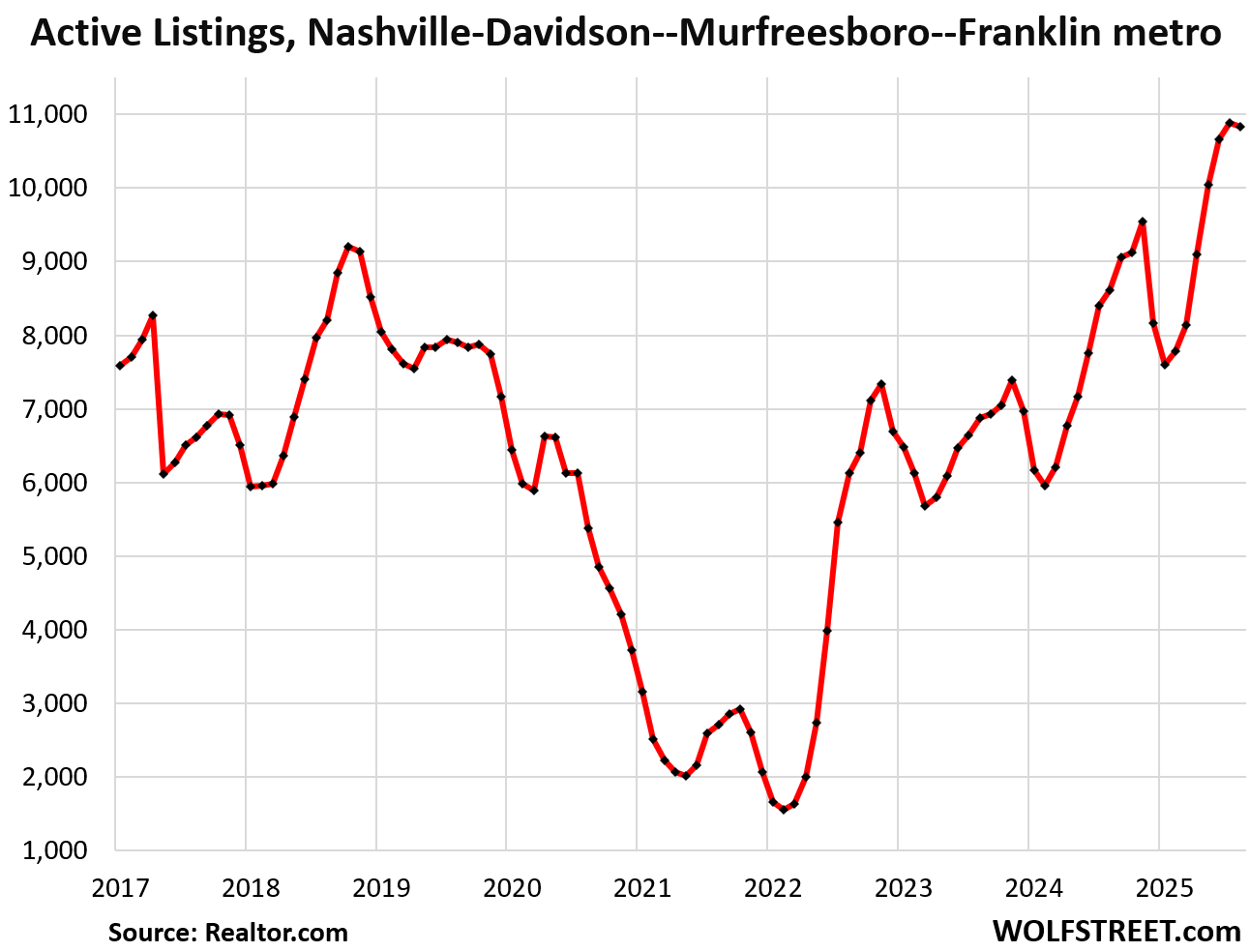

And inventory in the Nashville metro:

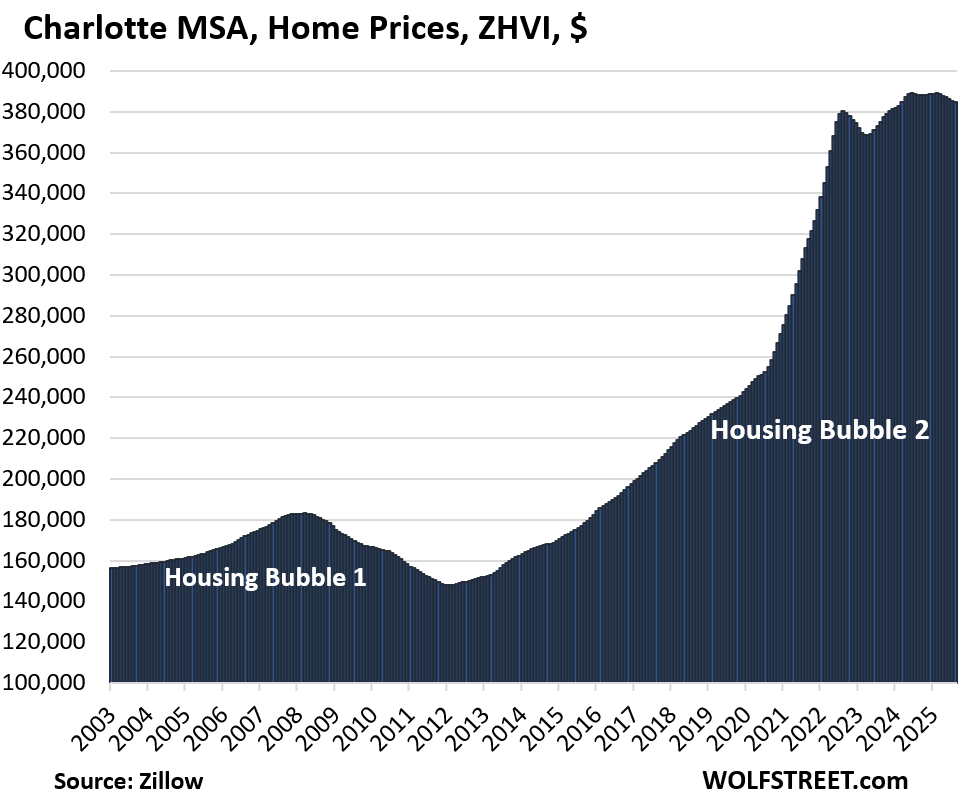

| Charlotte MSA, Home Prices | |||

| Fr May 2024 peak | MoM | YoY | Since 2000 |

| -1.0% | -0.1% | -0.9% | 166% |

Prices exploded by 54% between January 2020 and June 2022.

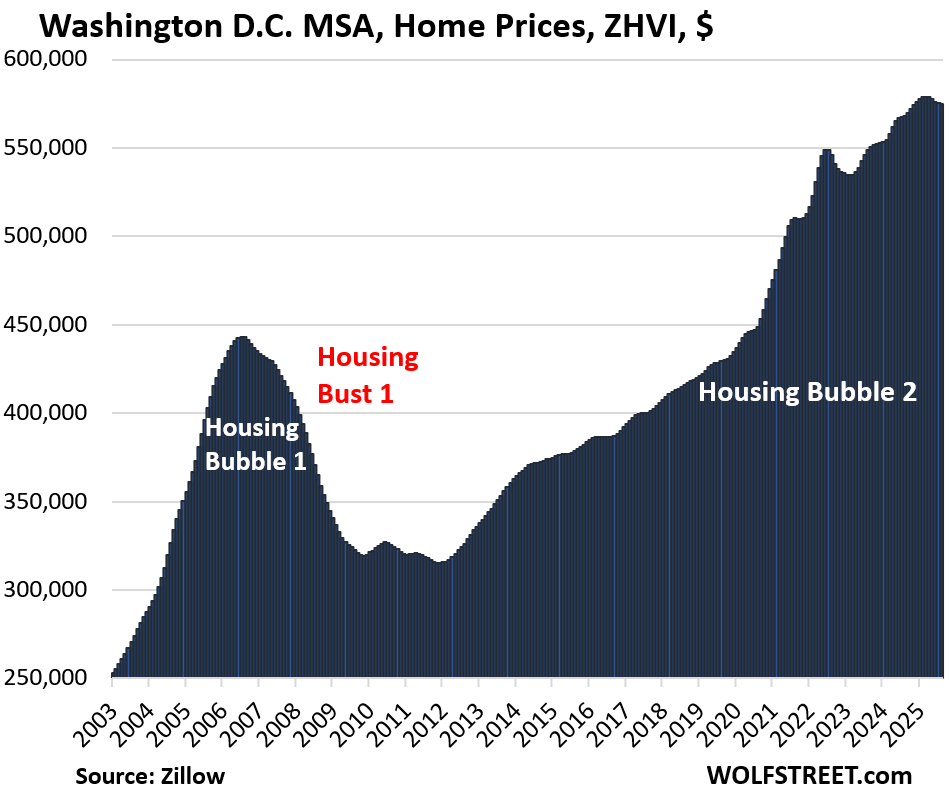

| Washington D.C. MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.1% | 1.1% | 216% |

The Washington-Arlington-Alexandria, which includes all of Washington, D.C., and parts of Maryland, Virginia, and West Virginia, is a huge diverse area. In Washington DC itself, prices have been skidding, with single-family home prices down 12% from their peak.

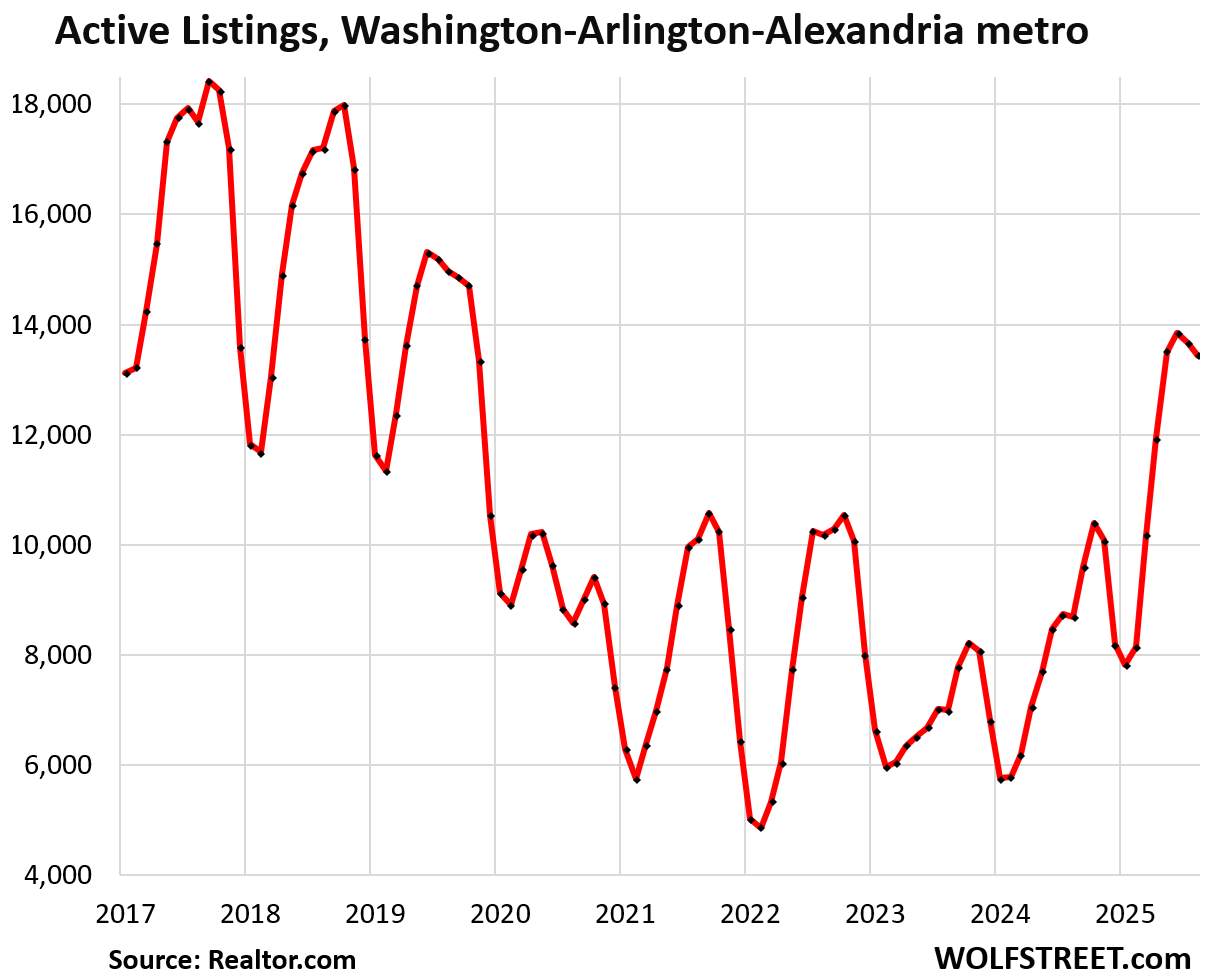

And inventory:

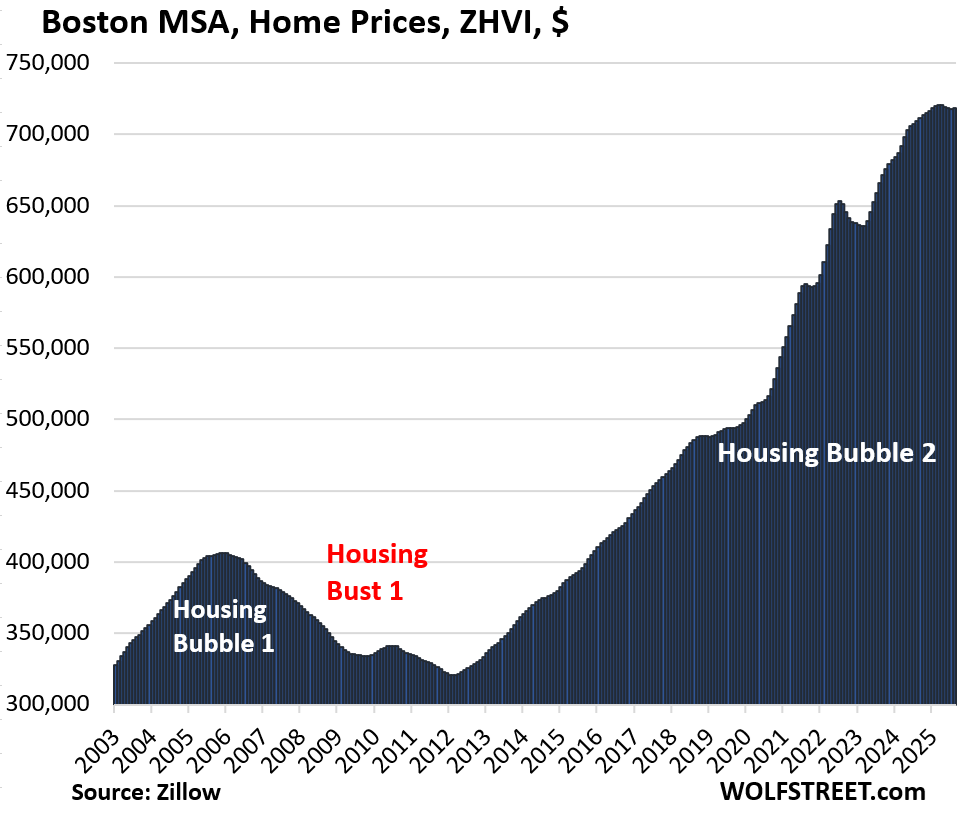

| Boston MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.0% | 1.2% | 225% |

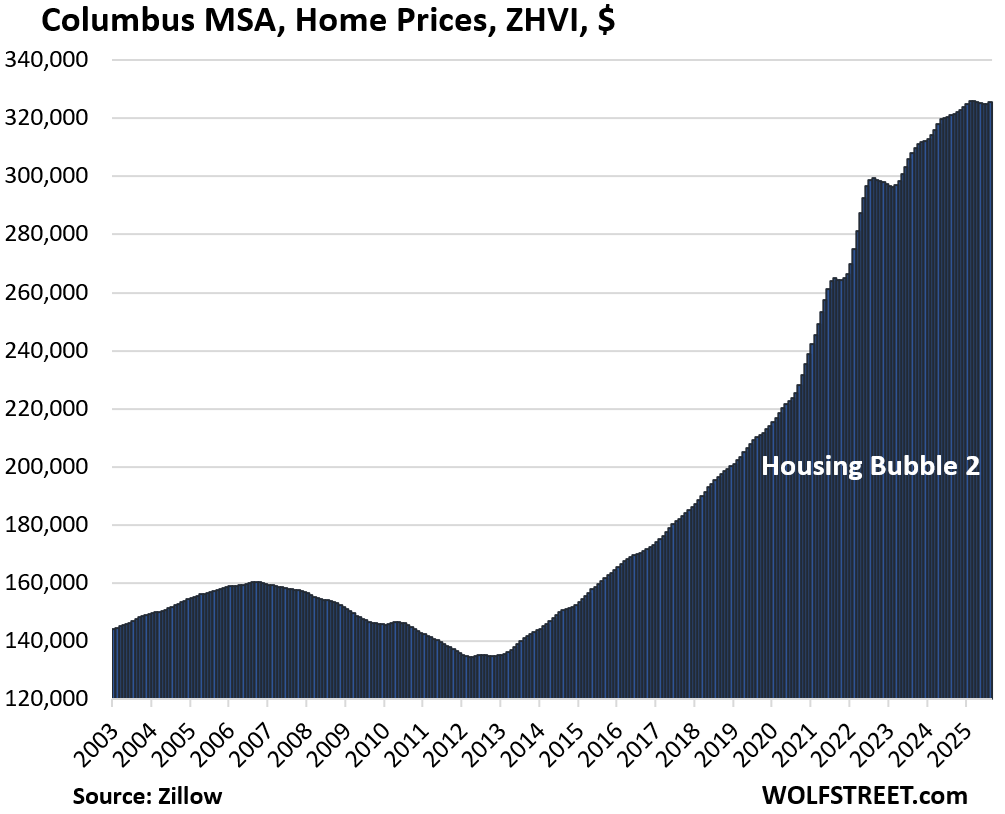

| Columbus MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.1% | 1.4% | 155% |

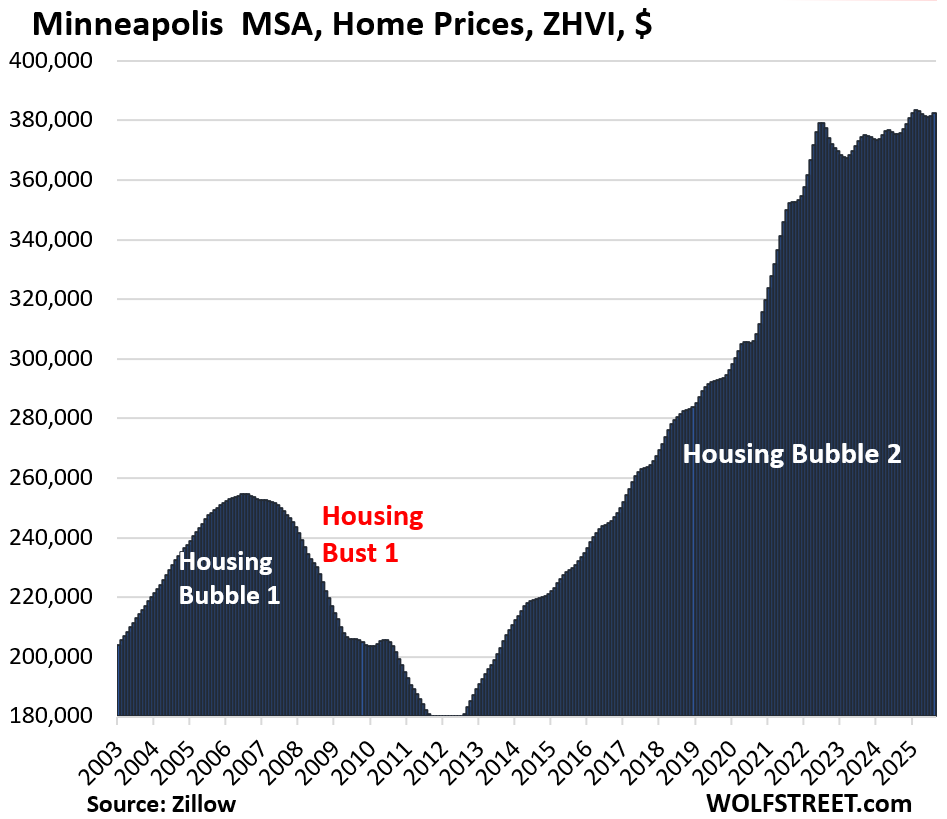

| Minneapolis MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.3% | 1.9% | 160% |

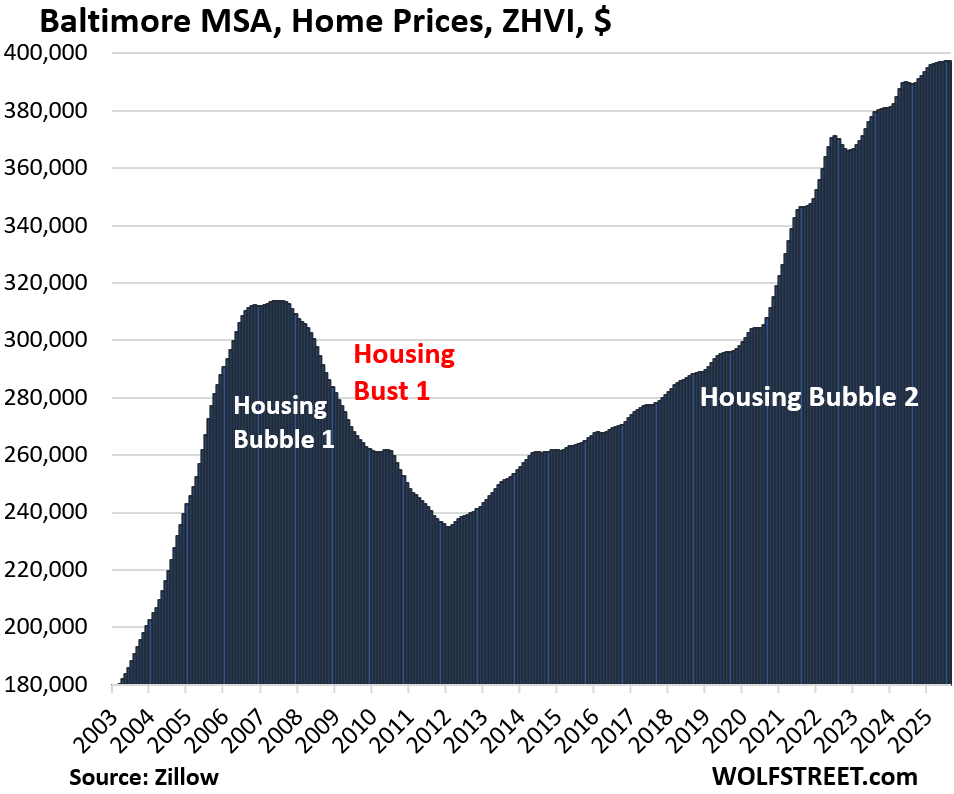

| Baltimore MSA, Home Prices | |||

| MoM | YoY | Since 2000 | |

| 0.1% | 2.1% | 177% | |

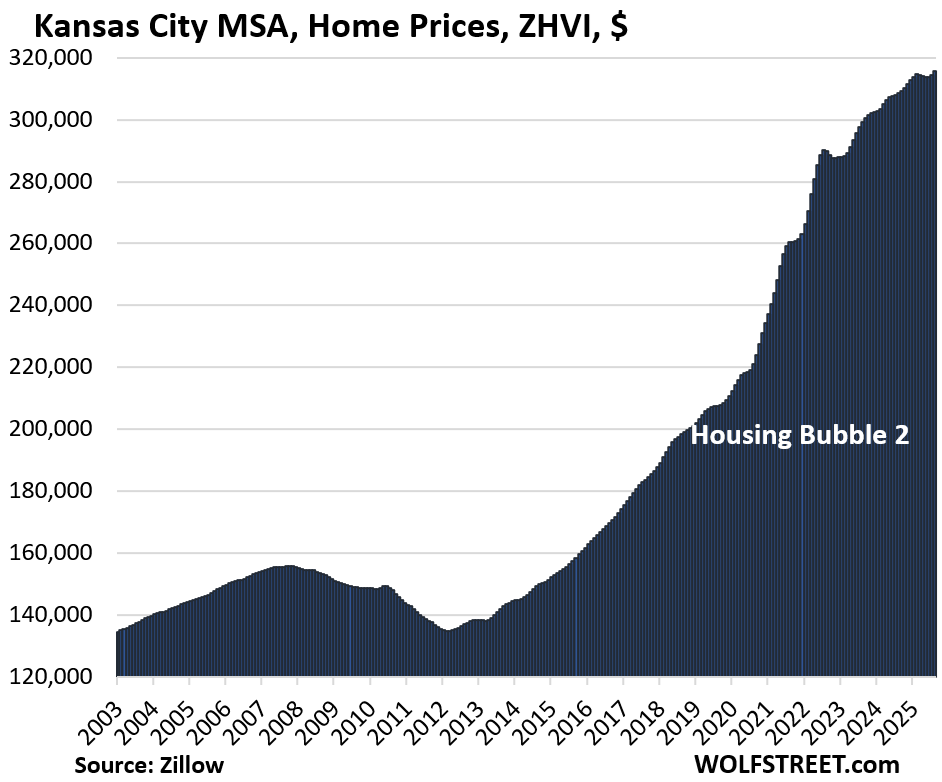

| Kansas City MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.4% | 2.3% | 178% |

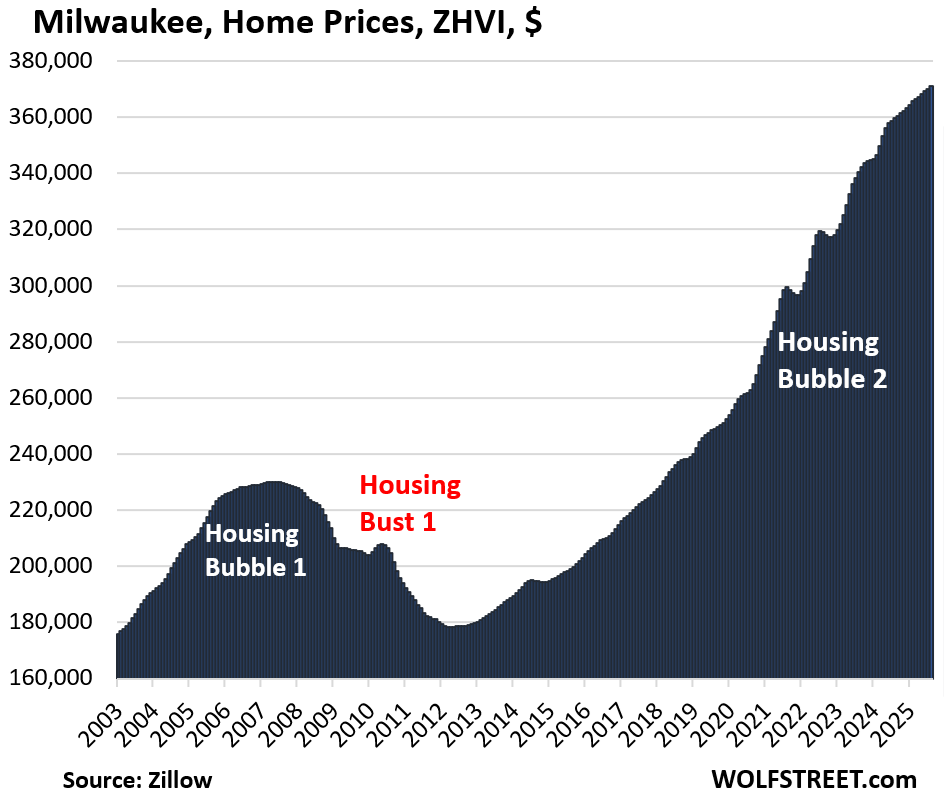

| Milwaukee MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.2% | 3.2% | 150.7% |

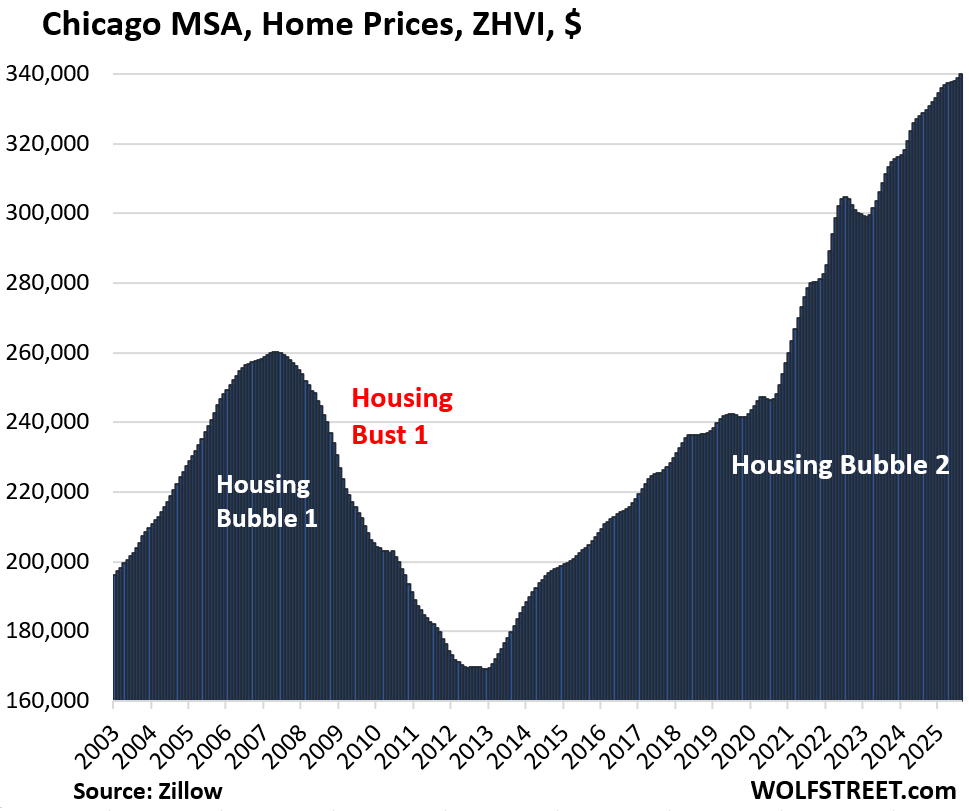

| Chicago MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.3% | 3.4% | 118% |

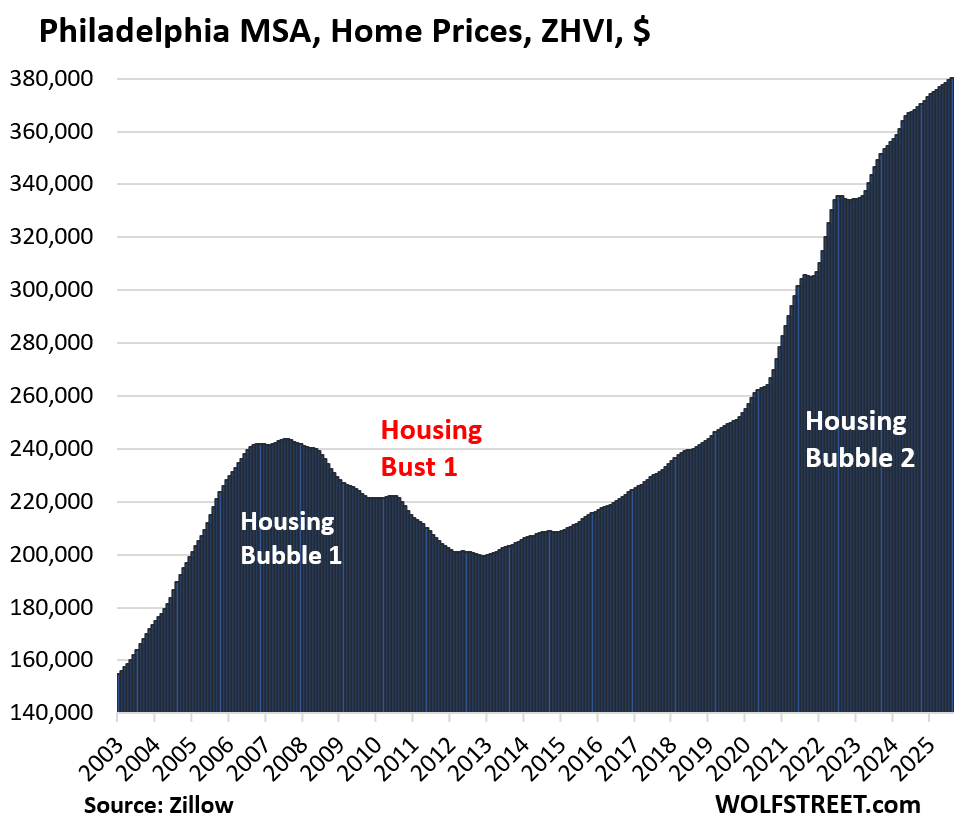

| Philadelphia MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.2% | 3.4% | 208% |

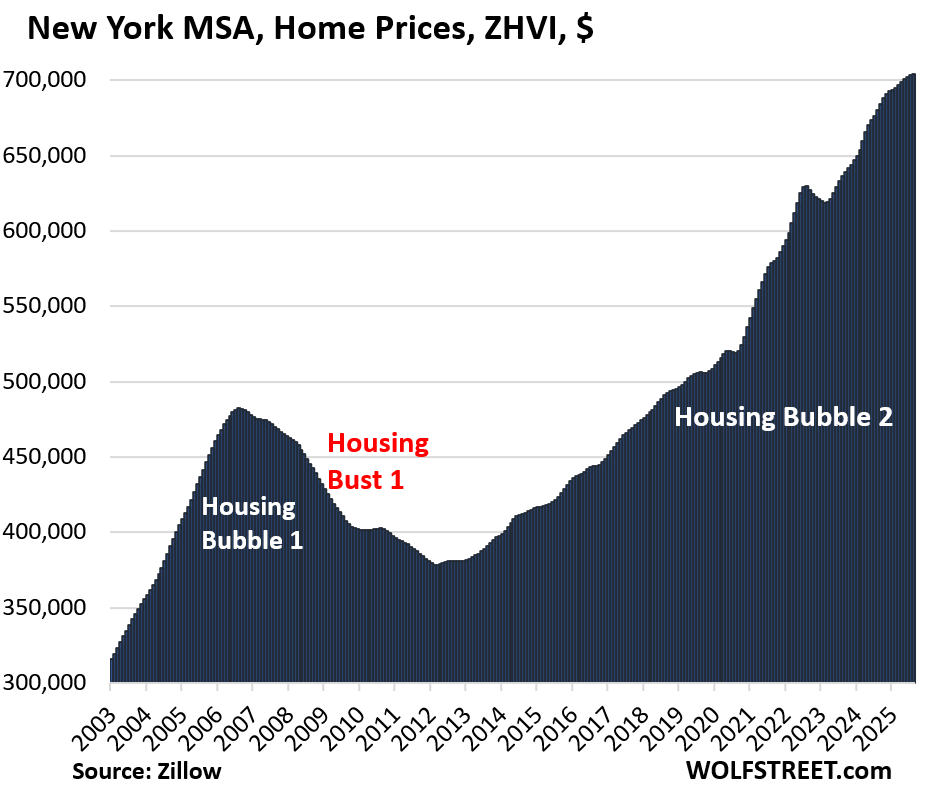

| New York MSA, Home Prices | ||

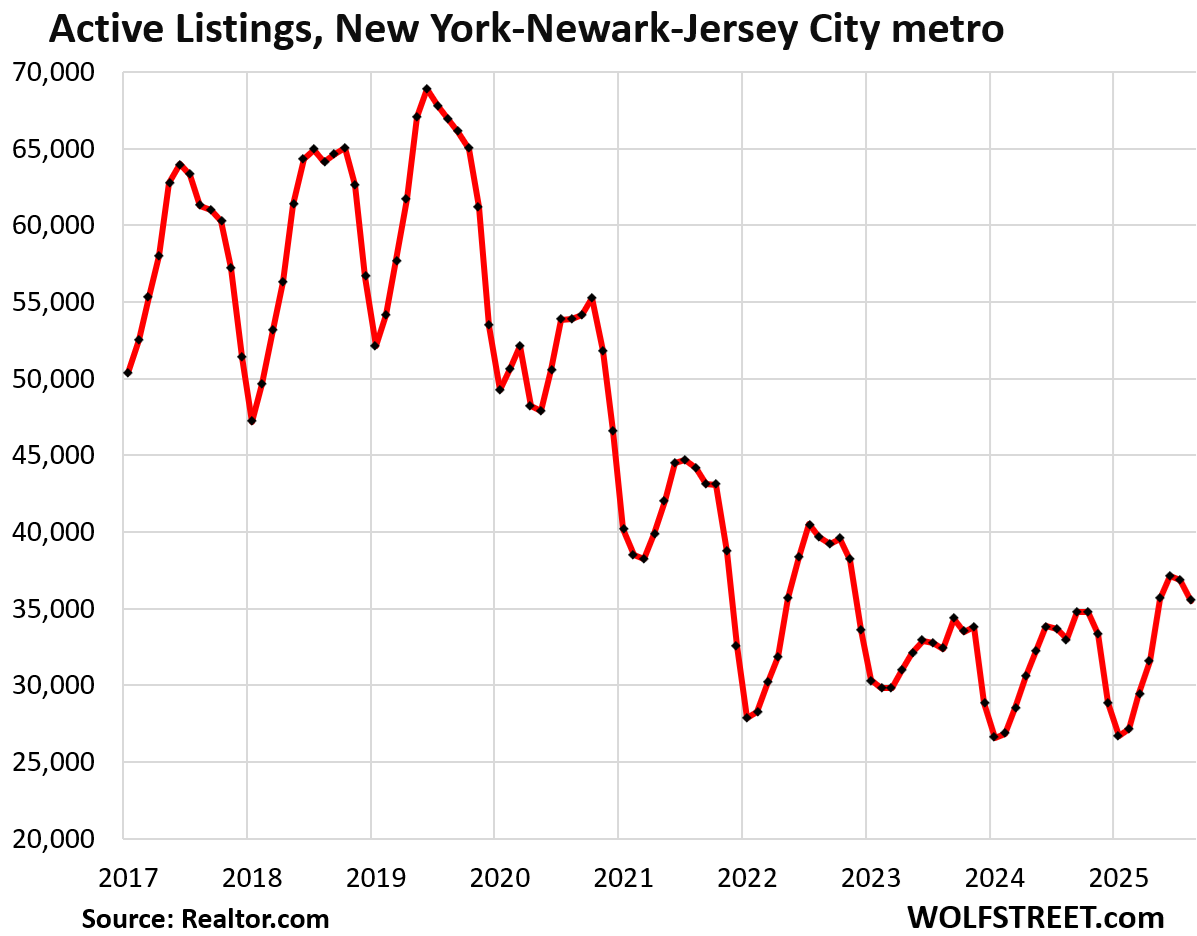

| MoM | YoY | Since 2000 |

| 0.1% | 3.6% | 219% |

And inventory:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

44 of biggest 50 metros flashing grave warning that house price crash next…

Totally not a click-bait headline.

/s

People love clickbait headlines and love to spread them, which is why they exist.

This is also why headlines for youtube streaming now look like the headlines on tabloids in the rack at the supermarket checkout line. This is what we have done with almost infinite computation and memory resources, and ultra-high speed communication. Sad.

Housing affordability is undoubtedly a big issue but I take issue with the presentation. Why? Let’s take NY. Approx. $315k starting median home price in 2003 to $705k 2025 price equals a sub 4% compounded annual growth rate. Big deal! Remember – these are nominal dollars! Tax law (capital gains exclusions) and 30 year mortgages (most countries don’t have these products) structurally inflate real estate.

“Approx. $315k starting median home price in 2003 to $705k 2025 price equals a sub 4% compounded annual growth rate. Big deal!

Compare to GDP growth, employment growth, or median income over same period…home price gains are well in excess of many other macro metrics – suggesting home prices were pumped up by little more than ZIRP empty air.

Median household income was $43k in 2003. It’s about $84k now.

Interesting, let’s see if this will continue to play out, MSM and plenty of RE agents and Redditors already hyping lower mortgage rates and the recent decline of 10yrs as the coming savior. Last I checked, my credit union is now doing 30yrs fixed at 5.25, lower than almost 7 just a month ago. For SoCal, maybe that’s enough to help tip the scale in bringing enough FOMO buyers back even though houses are still massively overpriced and crapshack still shamelessly asking and in some cases getting sold for over $1M…lower rates will certainly offer some incentives for certain groups of buyers that can afford and was on the sidelines to cross the rubicon.

Anyone who tries to play that game now is beyond mega-foolish. Sad.

Agree, Individuals who are easily manipulated by scam realtors deserve what they get.

It’s an investment of a lifetime, Do the homework.

Saw a clip yesterday, with a realtor saying SWF owners and builders are raising their prices in response to the lower mortgage rates. It really brings to mind the famous quote by John Kenneth Galbraith .

“People of privilege will always risk their complete destruction , rather than surrender any material portion of their advantage”

Why is anyone still paying attention what these manipulative real estate promoters say? They’re always saying the same thing: buy now before homes get even more expensive.

If you want to see what homebuilders are doing, pay attention to their financial statements and their average prices of homes sold. We just got Q2, and average prices fell.

We are suffering, yes suffering, the Great Housing Abomination.

One word is totally applicable – MANIPULATION.

Only by buyers bidding prices sky high. That is what markets always do.

That slide show of volcanos is fascinating — seems like massive amounts of lava left in the magma chambers – and likely we end up seeing eruptions all winter (and 2006). Those babies look ready to blow any second! I’m downwind…

Would be interesting to see the fixed and ARM rates overlaid on the housing bubble graphs and then ponder what might be next.

I would not advise any young person today to sign up for as much debt as it now takes to buy a “starter” home. All the math indicates they’d be better off renting and plowing the money they would have spent on a down payment, skyrocketing insurance, customization, and mortgage interest into paper assets instead. When you sign the line on a $500k mortgage (word bases mean “death lock”), you’ll never be free again.

Yes, a lot of stocks are so expensive they don’t make sense, but none of the affordability metrics make sense with houses at this level either. I can use options strategies and diversification to hedge stock and bond portfolios, but there’s nothing I can do to save your $400k “starter home” a hour outside Orlando with outrageous HOA dues from confronting the reality that most people can’t afford it.

And a huge chunk of inventory is owned by boomers who will either die within the next 5-10 years or will soon be shipped off to nursing facilities. Meanwhile, the US fertility rate has been below 2 since 2009, suggesting a falling population unless immigration makes up for it. And if anything botches the planned partial-privitization of Fannie and Freddy, so that 30y mortgages are not guaranteed to anyone with a job and a pulse anymore, then look out below.

Wolf, I’m looking at your earlier list of REITs and companies that have invested in SFH rentals. They seem like juicy short candidates. I can’t make the math work on SFH’s. Apartments maybe, but not SFH’s. So when I see INVH selling for a PE ratio of 33 like it’s a big tech company, I’m tempted to short it, or at least bet it won’t go up from here. I think the first recession blows up this industry.

Completely agree with you but do want to say among my friends, family members or co workers, saying this stuff feels like screaming into the void or throwing a paper kite into the wind…

Especially when speaking to people more bias in housing is never a losing proposition camp and with SoCal prices sell not seeing any noticable correction like Austin, it’s truly an exercise in futility

I have been following listing in Orange County CA. Still seeing homes bought & in few months even in 2 or 3 months, list @ a hefty price increase like $250k or even $350k. Flippers probably? When I add all cost of homeownership, it makes me wonder what is median household income in OC CA? $380k per year? #s just make no sense …

Yeah I am seeing plenty of that in OC and Long Beach, loony toon pricing IMHO and still selling, either some serious funny business or the FOMO and housing never lose narrative is next level in certain SoCal cities….

Or some people just don’t GAF about -10% or whatever lies down the road.

Phoenix_Ikki …

I am seeing the same strength in coastal Orange County. My opinion: the market is still reasonably strong because of the fires … many people have their insurance money and are looking for homes. Many of them are renting and waiting for better deals, but many are also buying. It is hard to say how long that will last.

Also, many are returning to keep their job. However, most of these people are renting because the prices are much higher than when they left. They are priced out.

“I am seeing the same strength in coastal Orange County.”

Orange County condos, seasonally adjusted, three-month average:

-0.2% in August from July

-2.0% from peak in Feb 2025,

flat YOY

Orange County SFH, seasonally adjusted, three-month average:

-0.3% in August from July

-1.8% from peak in Feb 2025,

+1.2% YOY

Coastal OC is doing better than the OC average. Just pull up Newport Beach and take a look. That is the insurance money from the Palisades fire. That is what realtors are saying.

Yes, not in my neighborhood. Common song here.

The math hasn’t work for at least the past 10 years and yet here we are. The Fed doesn’t care about math. It cares about doing their masters’ bidding, which is inflating asset values at all cost (the so-called wealth effect).

Or as Keynes famously noted, the markets can remain irrational longer than you can stay solvent.

I’m not necessarily saying your advice is bad, just that this hasn’t been a rational market for at least a decade, and unlike stocks, people need a home. Maybe you just had kids and need more space, or they’re approaching school age and you need to get into a good school district, or whatever, but housing is not entirely an economic choice.

People who divorce or die or get sick and move to nursing homes have no choice but to sell regardless of the market, but conversely some life events force you to buy regardless of the market. Depending on whether the market is up or down both groups of people can be massively screwed and yet don’t really have much choice but sign that “death lock”.

This has nothing to do with rational markets. Today it is much better to rent and invest the difference than own.

Good comment IMO Lune:

Summarizes a bunch of venues for both buyers and sellers, many of which WE, in this case the family WE have experienced over the last five or six decades.

Now at my ”end game” with no debt at all, but a spouse likely to persist for several decades, I would only hope that our lords and masters and ”the banksters” will actually realize that if they don’t provide SUFFICIENT ”safe” return on savings, all of us old and older folx will clearly become MORE burdensome on the entire economy,,, and these days, MORE likely to vote against the trend to reduce BIG GOVMINT, etc…

If you want a shelter then you can rent

There is absolutely no circumstances where one is forced to buy to live in a home barring very few exceptions.

I can understand the forced to sell part though.

I habe friends who got divorced had to sell

One of my old acquaintance foed.. had to sell.

My friend relocated..had to sell.

Hmm… I think some people here should look at the cost to build a home. Sure an 80lb bag of concrete is $3.50. But a concrete driveway costs about $20k in Minnesota. Look up how much plumbers and electricians are charging. Look up the price of cabinets and millwork and windows and doors, and compare that to installed prices.

If your house was written off as a total loss and your insurance paid you the market value of what your home was worth, and you hired a contractor to build you a new home here, there’s a chance you’d get less home with lower quality finishes than what you started with.

Is it that way in other parts of the country? I don’t know, but based on what I’m seeing in the industry here, I think the quantity of homes will become less abundant in the future.

All markets are certainly asset bubbles enabled by free money, but some are certainly going to hold up due to demographic shifts. I don’t think southeastern markets will see huge drops like in 2008 due to rapid in-migration

That in-migration has come to a crawl. There has already been a lot of soul-searching in Texas about it. Florida same thing. Other places too.

In Texas the extreme heat is expensive add that to high property taxes and high insurance rates it is not what it used to be. Florida is a disaster due to insurance and people asking if they want to hold their breath during hurricane season.

I wish that the half a million people that arrived here in the past two years would get up and leave.

Not yet in Tennessee. At present, the housing market seems in equilibrium. Buyers willing to up their bids to grease a sale but my guess prices are mostly sideways. A lot of Californians here, you meet them in Lowes, real estate business, plumbers, everywhere. New construction for homes and apartments everywhere, and renovations of older homes very common in fact thats the best way to keep low real estate taxes lower because tax is based on latest sale price transaction, but even then shockingly lower vs other states. Low real estate taxes no income tax sane pragmatic public office holders. MSM says Memphis is next up for Trump federalization of police enforcement. Memphis heavily minority. Locals consider Nashville overpriced. Knoxville is my sweet spot. People here say “God bless” not “have a nice day. “The retirement aspect and cost of living is attractive to baby boomers and the Silent Generation, the job market is attractive to Gen X and millennials, and the vibrant city life is attractive for Gen Z”.

Tennessee is one of the most hyped up market i watch closely and is due for big fall in prices

Its a matter of time.

Reason.. prices are out of reach .

Bless your heart!

Also, many of those Sunbelt cities have the highest rates of new home construction, so supply is matching demand much better than places like SF, LA, Boston, etc.

When net migration slows while housing still gets built that can cause big price adjustments. You have to look at both sides of the supply / demand equation

There is massive housing construction in Central Texas and a seemingly infinite supply of land within easy commute of good jobs. Expect Austin and San Antonio prices to continue their slide….

San Francisco has about 71,183 housing units in various stages of the pipeline as of Q2. There are vast areas (former naval base, former naval shipyard, former football stadium with huge parking lots, former port and warehouse areas, former coal powerplant, former industrial areas, a former reservoir, along some piers…) that are getting redeveloped. The problem isn’t space to be redeveloped; it’s the time it takes to get the permits, fight city politics, and clean up nuclear contamination on the former naval properties. And then, obviously, they’re not building single-family houses with big yards in a densely populated city. If you want a new house with a big yard, you need to look a good distance away from SF. Most of what they’re building here are multistory condo and higher-end apartment buildings, and a few townhouses. The areas are beautiful, nearly all of them near the waterfront, or directly by the waterfront, or surrounded by water (the old naval base on Treasure Island). The new buildings are surrounded by new parks along the water — some of those new parks just opened. They’re really spectacular.

I honestly don’t know what the Caribbean and Gulf coasts are going to do about Sargassum.

Mexico just started harvesting Sargassum for a variety of uses.

Is it a problem? Recent? What’s the cause?

Don’t know what it is but sounds like something that would make good kimchee,

The idea that real estate prices will come down fast enough seems unlikely in the short and medium term. To get the prices down it seems the only way this will happen is major recession no where in sight. Note the banks are not excited about losing high interest income along with solid asset values now headed downward. I cannot see any major adjustment only the slow moving destruction of people who have to sell especially the Baby Boomers now needing to exit big properties….

Agree, only a recession will break this bubble. So many homes pulled off the market indicates that the owners can afford to keep them. No urgency unlike in 08.

But in many hot markets, prices are down more than 22% from peaks despite hot job market and no recession.

Many? If Austin is many …

I read somewhere that the 2000s mortgage bubble was caused by activity in just 12 states. Look at the chart for Dallas, prices barely came down at all after the financial crisis while other cities like Vegas dropped 50%

1957 Baby boomer getting a new roof, refinish and upgrade pool, whole house generator, HVAC replacement , and some window replacements .

Total spend in 2025 is 140k on a 4000 sq ft home in East Texas prop tax rolls of 900k .

So guess I’m staying put for awhile longer . Eventually the overhead could force some baby boomers out of their homes.

In my neighborhood (100 homes all built 2005-2013) just had 2 Baby Boomer wives die in their early 70s and a male 68 get ALS and moving to small home . So 3 percent listing increase because of disease and death

“…don’t qualify for this list because their ZHVI has never reached $300,000, despite the blistering surge of home prices in recent years, such as the metros of New Orleans, Memphis, Oklahoma City, Tulsa, Cincinnati, and Pittsburgh.”

Interestingly, the above markets never even penetrated the lows, based on the charts, going back to 2003, of the following metros:

San Francisco

San Diego

San Jose

Los Angeles

Boston

New York

I think the housing market is going to stubbornly drag on with high prices…..

UNTIL, the PTB decide to pull the plug. 🔌

And then……CRASH, BOOM, WIPEOUT!

and buzz off to the guy who always yells ‘your comment is pure doom and gloom!” Face reality, ‘Frankie’.

PTB?

Sorry – TPTB – the powers that be.

What is a young professional to do these days? The best job opportunities are in the largest and coastal cities. Yet, affordability lies in the mid-sized and inland cities. Is it better to rent in larger cities and hope things improve or move across the country to a city where you might be able to afford a home and save. I’ve considered moving somewhere like Phoenix or Austin, but it’s a tough call to move away from family and community.

The total cost of owning a home is not going down. In all honesty if you can’t afford a home at todays prices, you can’t afford that home.

If you need a thirty year mortgage, you can’t afford that home.

Thinking costs will drop 50 percent for a place you would want to live is like playing Spin The Wheel And Choose My Ghetto!

What would any metro look like if its homes lost 50 percent of their current value?

All the talk of Boomers crocking is just wastful BS. Like watching the daily tide for sea level change!

What matters is location, location, and location, and a home you can afford!

A friend of mine who works as a paramedic left Houston earlier this year to work in Tillamook and now he makes roughly 50% more without an extremely toxic work environment. Cost of living barely shifted.

One strategy is to build the resume in the big city, while monitoring for that cherry job in a lower cost area. The excellent big city work experience will give you an edge.

If 30-year mortgage rates stabilize around 5.5 %, the Washington-DC housing market requires only a small 0–5 % nominal adjustment from today’s ZHVI levels, or a more noticeable 10–17 % decline from today’s median sale prices, to bring the typical household back to a sustainable 33 % PITI ratio within the next two years. Otherwise, simply letting inflation and income growth work for 24 months can produce an equivalent ~14 % real affordability improvement, even if nominal prices barely move.

The DMV is in a recession from the Federal government layoffs. We have a long way to go before we stabilize.

My crystal ball says the Fed cuts .25 today, then waits at least three months before any further action to see where inflation goes. This will likely drive the 4-week down to 3.75 or so. But if the ten year sticks around 4.0 then mortgages “should” eventually settle at ~5.5% given the historical spread. Flat or slowly declining prices combined with 5.5% will allow a slow, painful grind through this housing bubble as each individual buyer and seller comes to terms with this no-win market. Meanwhile hopefully MBS QT continues as the Fed unwinds its biggest policy mistake. It took them fifteen years to wreck the housing market – it could take ten or more years for it to heal.

I know we are looking in trends in general here, but I don’t get what specifically keeps Philly afloat.

I lived more than 10 years combined in NJ and in PA and after moving down south I can’t fathom going back. Almost every single Pennsylvanian I happen to know (yes, that’s a very limited sample, I admit) is unhappy and either dreaming of leaving or already posted stuff like “Moved to FL/SC/TX…” on his or her Facebook …

Yet Philly seems to be one of the few places with prices still going strong. How’s that even possible…

2024 report title, “Gen Z Flocks to Philadelphia, While Older Generations Move Out, New Report Finds”

“Over that period, Philadelphia recorded an inflow of 47,690 Gen Z residents and an outflow of 27,590. This puts the city’s Gen Z net migration at 20,100. In 2022, the city recorded an even higher Gen Z net migration of 22,405.”

My daughter lives on main line in Paoli/Malvern area and I believe is a paradise . Some of the most beautiful homes landscapes and neighborhoods I have seen. Prices have stabilized but no drops .

19396 Zip Codes (Radnor Hunt area)

Plenty of huge companies in Philly..Comcast, Amerisource. Lots of big financial services companies in the suburbs like Vanguard and Fiserv. Many prefer the slower pace vs. NYC.

We (Philly) also had an influx of New Yorkers move in, granted that was around COVID years of the early 20’s. They sold their higher priced ny property and bought lower priced home that was larger in Philly. I met one ny couple who said they were in health care and wanted a smaller city to raise their kids in. I myself moved in 2014 as millennial from l the burbs, burbs was way to expensive unless I wanted to rent. I bought back in 2014 luckily. We have not moved since everything is now very pricey but close to family and friends

Totally normal for home prices to triple in 10-15 years in world class cities like *checks notes* Phoenix Arizona. TOTALLY NORMAL.

There is the data, still a bit bubbly…

So why the hell are we lowering rates Jerome? My prediction is that the long end of the yield curve will steepen in a manner that is inversely proportional to the size of the rate cut.

CONgress refuses to “adult”, they are too busy stealing everything they can from the treasury and what’s left of the middle class.

As the saying goes; “Full Faith and Credit”

Interesting times.

Today’s news –

“Mortgage rates drop to 3-year low ahead of Fed meeting. The average rate on the 30-year fixed mortgage dropped 12 basis points from Monday to 6.13%, according to Mortgage News Daily. That is the lowest level since late 2022.“

This WILL DO NOTHING to fix the terminally ill

housing market. NOTHING.

Wondering if anyone has “boots on the ground” in the Philly market and can share insights. Thanks

I live in Philly, we have been holding our primary home since 2014, lots of infrastructure and public improvements no doubt spending our tax dollars hard. Not many homes for sale when I drive my normal route, the homes sub 500k sell pretty fast the homes 300k or less very fast. I only see the 500 to 1m homes sitting for awhile before they sell (6-10 months maybe) anecdotal of course but just what I see. Also, the cheap homes (less than 300k) get bought quickly by investors that rent to two or four adults and they can easily pay the rent amongst each other. I should mention my 1100 row home form 2014 (built 1949) was appraised at 112k when I bought it for 85k. They now regularly sell for 250-280!

I live in one of these ‘large expensive metros’ listed here and on the real estate sites I visit all I see is price cut, price cut, price cut. Sellers are gonna have to get creative because price cuts alone aren’t cutting it. How about if the sellers toss in the title to their 2019 Ford F-150 that they just finished paying off? Buy the house and the car comes with it, BOGO deals

Wolf,

Get the Fed press conference zapper ready! It should get a lot of use today!

Need a dedicated zapper for Nick Timiros and his “muh rate cuts” pleading every presser…

Who was the guy that used to say “The plane, boss, the plane!”? Well, I say, “The chart, boss, the chart!” after looking at your charts of Housing Bubble 2. There have been some minor retractions, but they still look like Mount Everest!

We have made a monster we cannot control.

Hey Wolf you should include Rio Rancho NM in your next one just for the amusement of the 2008 madness they did. If you look at the satellite imagery around the town it’s just mind boggling the fraud that went down there.

I wonder if.. given the large SFH holdings of the whole Landlord Corp group, at what point do they feel that prices have come down enough and want to keep prices up to avoid losing tenants while at the same time keep their balance sheets from looking bad, that they start buying en masse again?

They’ve become net sellers of the homes they bought in 2012-2014, and they’re building/buying their own build-to-rent developments with hundreds of brand-new purpose-built rental houses each, because these developments, with a central leasing/maintenance office and common amenities, are much cheaper to operate than hundreds of houses scattered all over the place.

I give you the number of sales of houses by the largest single-family landlords here. They’re done buying old houses. They’re into renting new build-for-rent houses for higher-end tenants because that’s where the profits are.

https://wolfstreet.com/2025/09/15/the-biggest-single-family-rental-landlords-and-multifamily-landlords-in-the-us-big-shifts-underway/