Oakland, Austin, New Orleans, Cape Coral, San Francisco, Birmingham, Washington DC, Fort Myers, Denver, Portland, Phoenix, and Sarasota.

By Wolf Richter for WOLF STREET.

Each housing market moves to its own drummer. In some cities, prices of single-family homes have continued to rise, but in others they started to tank in mid-2022 or more recently, and that list of cities with dropping prices has been getting longer, and the list of cities with price drops of 10% or more has been getting longer too.

And there are a bunch of cities that are not included here because prices have dropped a little less than 10% so far, but each monthly decline gets them closer to the double-digit zone.

In 12 bigger cities, prices of mid-tier single-family homes have already dropped by 10% or more from their peaks through July, seasonally adjusted. In two of them, prices have dropped by 23% so far.

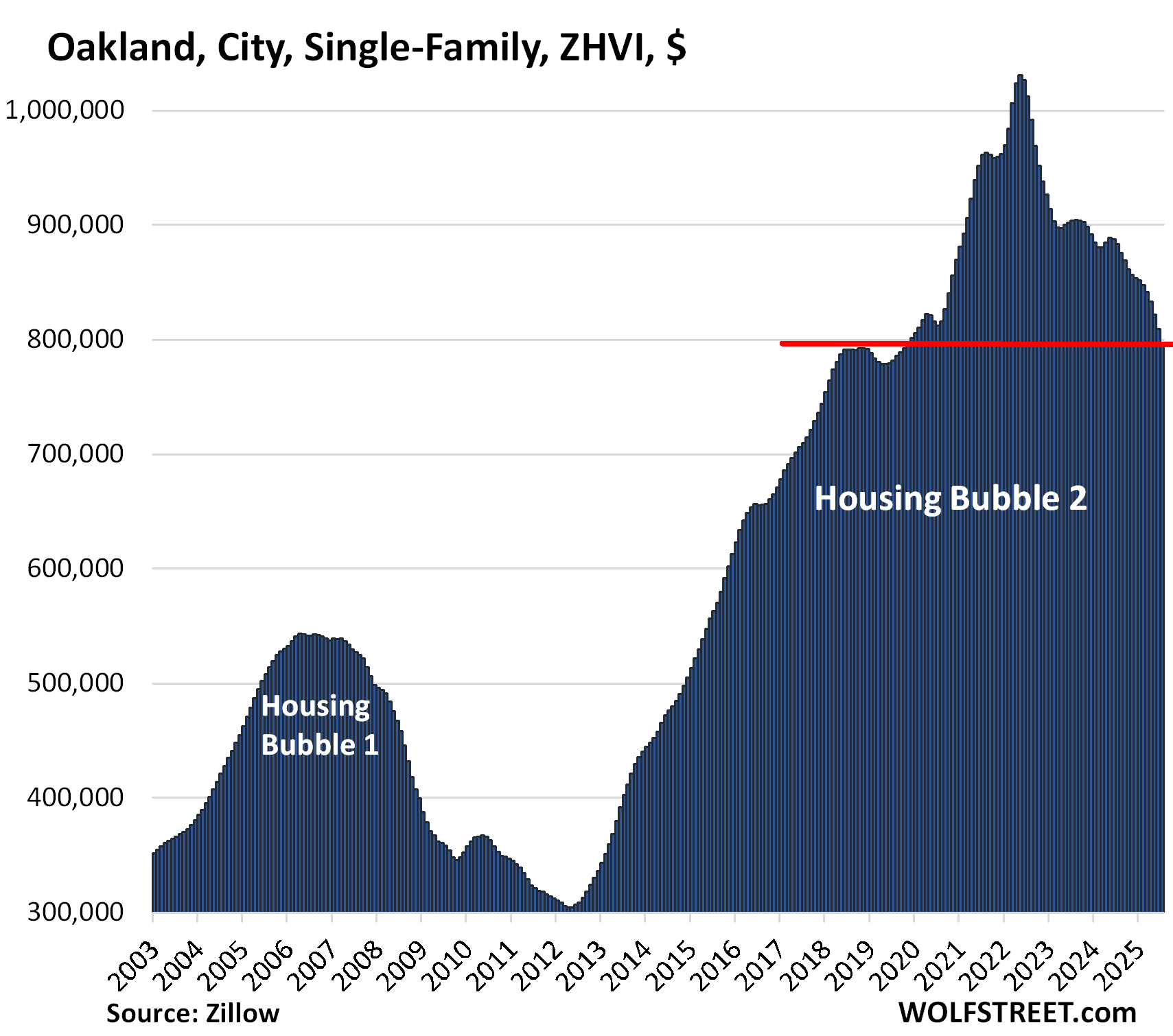

- Oakland, CA: -23%

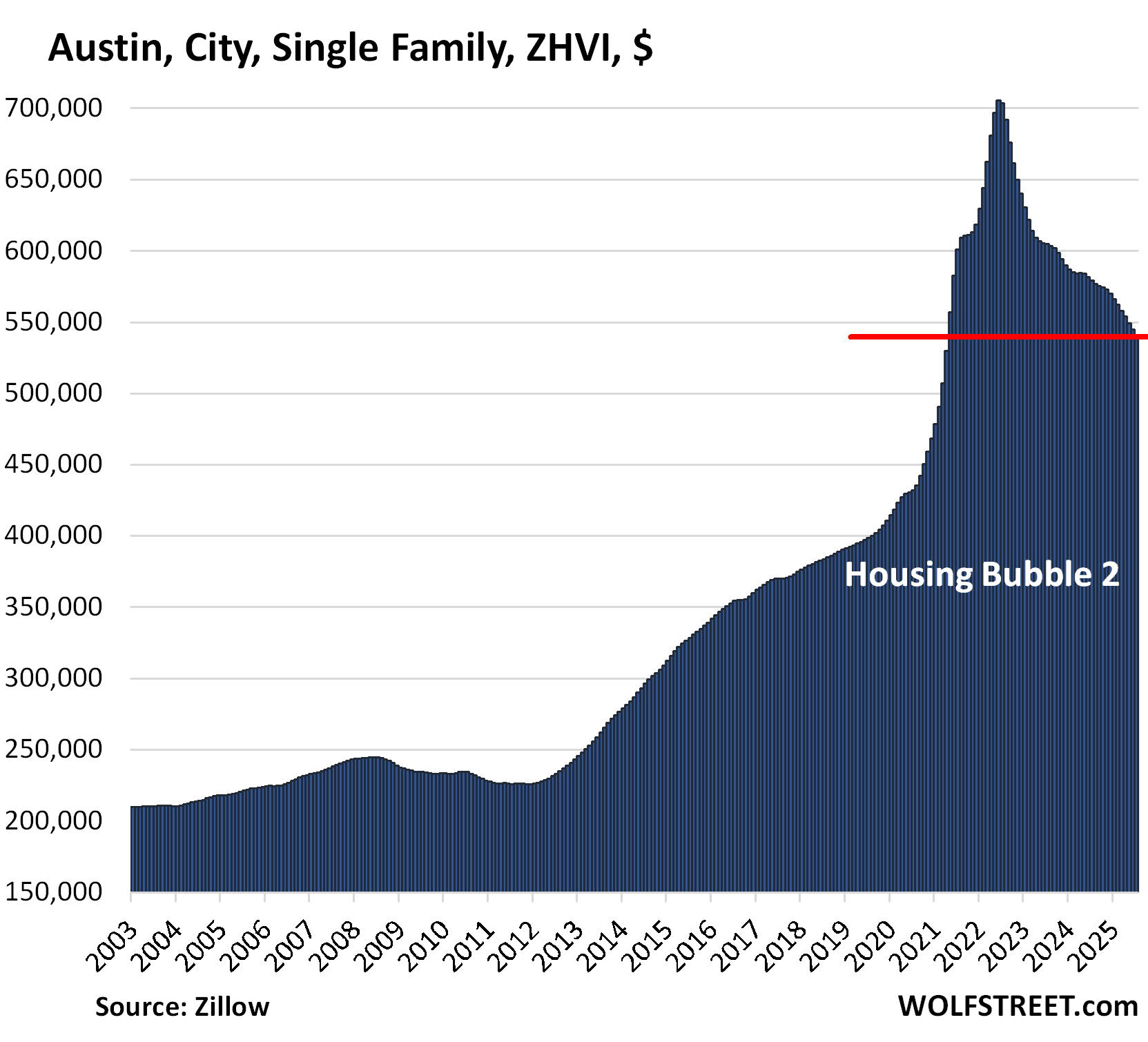

- Austin, TX: -23%

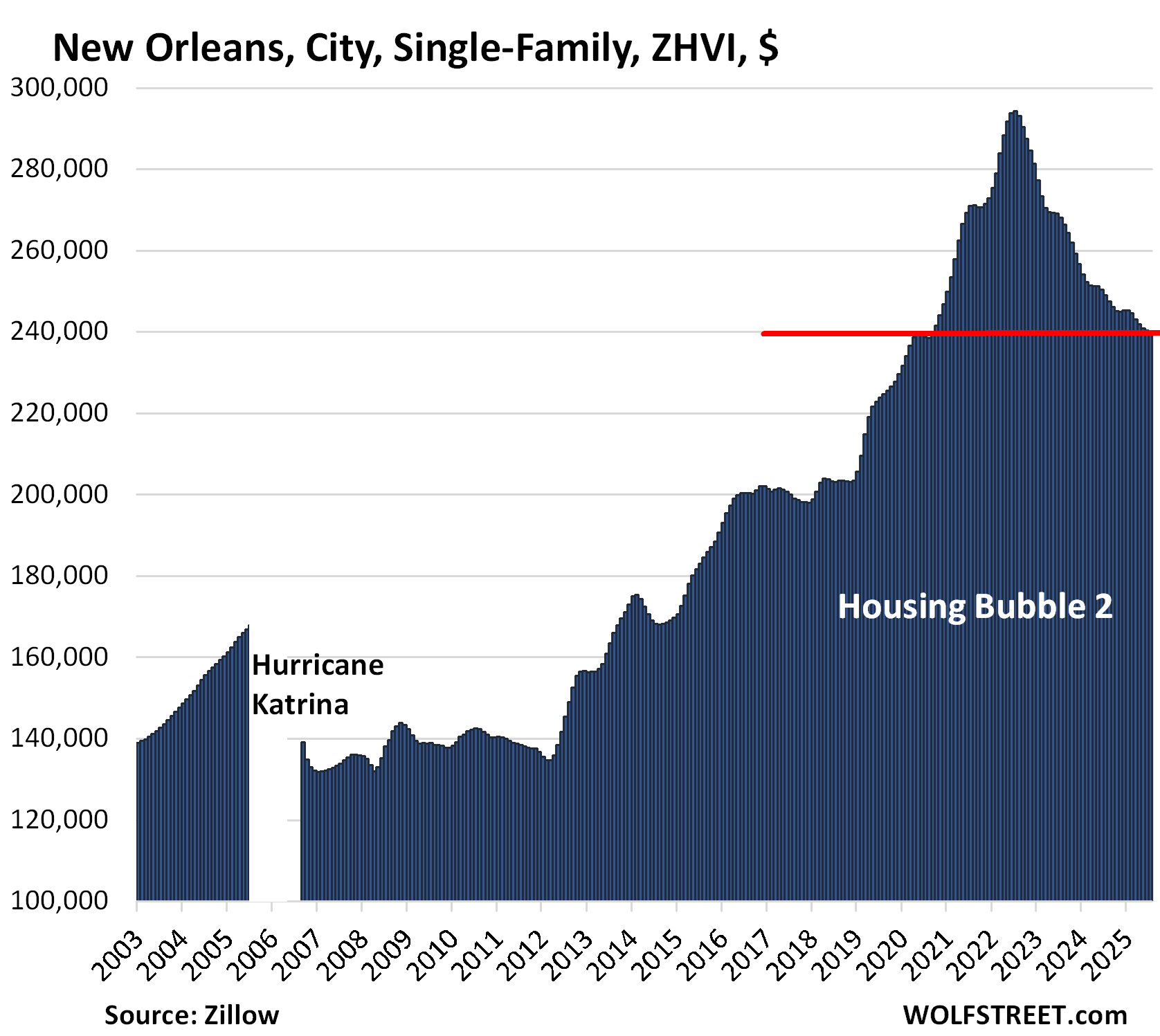

- New Orleans, LA: -18%

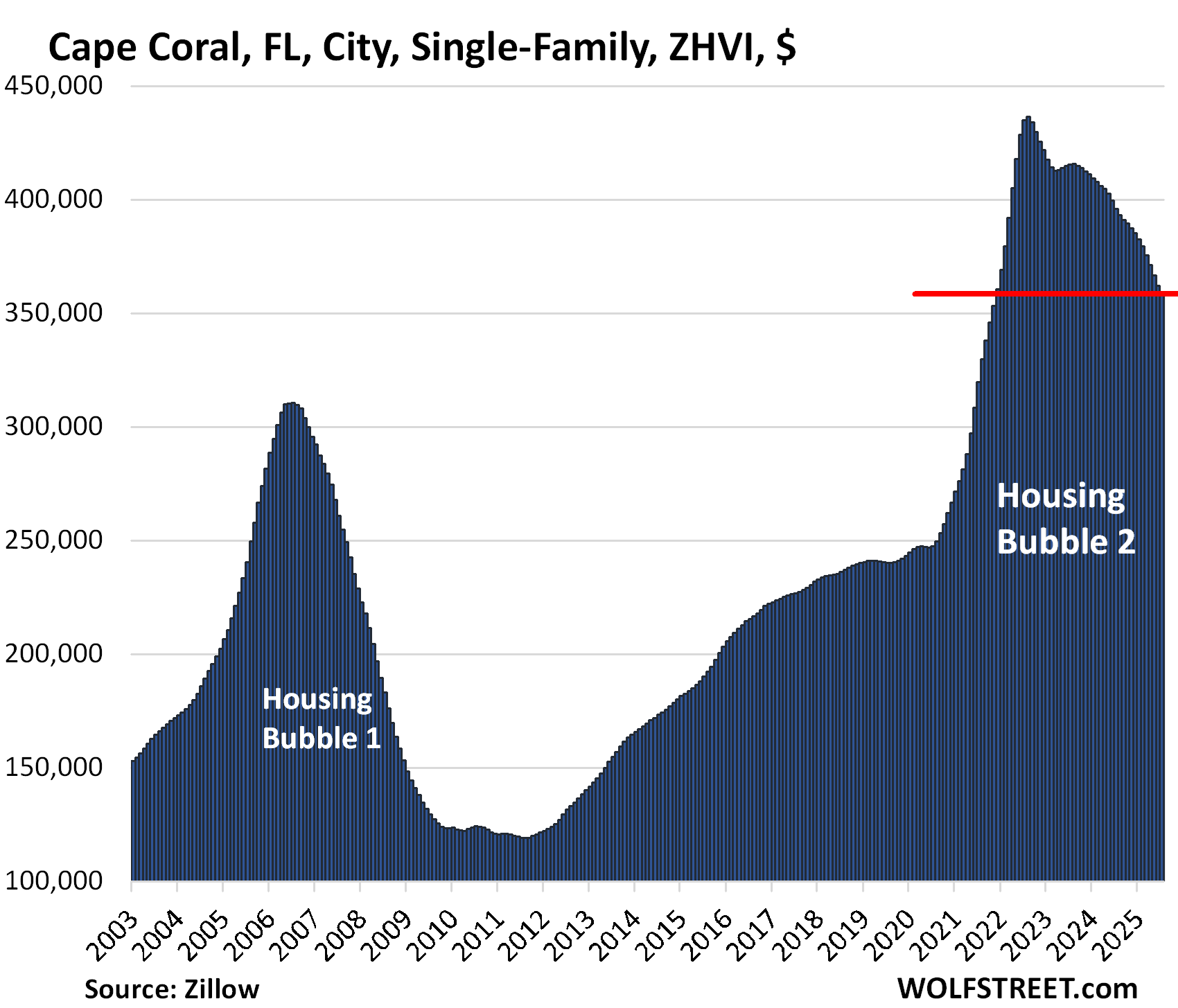

- Cape Coral, FL: -18%

- San Francisco, CA: -16%

- Birmingham, AL: -15%

- Washington, DC: -12%

- Fort Myers, FL: -12%

- Denver, CO: -10%

- Portland, OR: -10%

- Phoenix, AZ: -10%

- Sarasota, FL: -10%

In four of the 12 cities, the price drops of mid-tier single-family homes have wiped out the entire or nearly the entire or more than the entire pandemic-era price spike. But in these four cities, the pandemic-era price spike didn’t measure up to the price explosion in some of the other cities.

In San Francisco, prices were already sky-high at the beginning of the pandemic – $1.47 million for a single-family mid-tier home – and had already hit a ceiling, and with some of the highly paid tech talent leaving during the pandemic, price increases were much smaller than in other cities where the Free Money era did its magic:

- San Francisco

- Oakland

- Washington, DC

- New Orleans.

Month-over-month, single-family home prices declined in all of the 12 cities in July, topped off by:

- Oakland: -1.5%

- Myers: -1.3%

- Sarasota: -1.2%

- Cape Coral: -1.2%

- Austin: -0.8%

Year-over-year, prices also declined in all 12 cities in July, topped off by:

- Oakland: -9.8%

- Fort Myers: -9.8%

- Cape Coral: -9.6%

- Sarasota: -8.4%

- Austin: -6.7%

Condo prices have skidded downhill faster than prices of single-family homes: Condo Prices Already Dropped by 12%-26% in 21 Bigger Cities through July. Condo Bust Takes Shape

Methodology and data: These prices are seasonally adjusted three-month averages of single-family mid-tier homes in “cities” (not in Metropolitan Statistical Areas, which are much larger). All data here are from the Zillow Home Value Index (ZHVI), which is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals. These are not median prices.

The 12 Cities with the biggest price declines:

The metrics in each table from left to right: price decline from the peak, month-over-month change (MoM), year-over-year change (YoY), and increase since January 2000 (or 2022 as indicated).

| Oakland, City, Single-Family Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -23% | -1.5% | -9.8% | 285% |

The month-to-month plunges are adding up: -1.5% in July, -1.6% in June, -1.4% in May (seasonally adjusted). This was fast!

Prices are back to late 2019, and nearly back to late 2018, having wiped out 100% of the pandemic-era price spike plus some.

In the decade between mid-2012 and the peak in May 2022, prices had exploded by 236%.

| Austin, City, Single-Family Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -23% | -0.8% | -6.7% | 168% |

Prices of single-family mid-tier homes exploded by 64% in two years between mid-2020 and mid-2022. They’re now back where they’d first been in May 2021, having wiped out 60% of the pandemic-era price explosion.

| New Orleans, City, Single-Family Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2007 |

| -18% | -0.1% | -3.6% | 108% |

Back to September 2020, having undone nearly 100% of the pandemic-era price spike.

| Cape Coral, City, Single-Family Home Prices | |||

| From Aug 2022 peak | MoM | YoY | Since 2000 |

| -18% | -1.2% | -9.6% | 220% |

Note the 9.6% year-over-year drop. This is going fast.

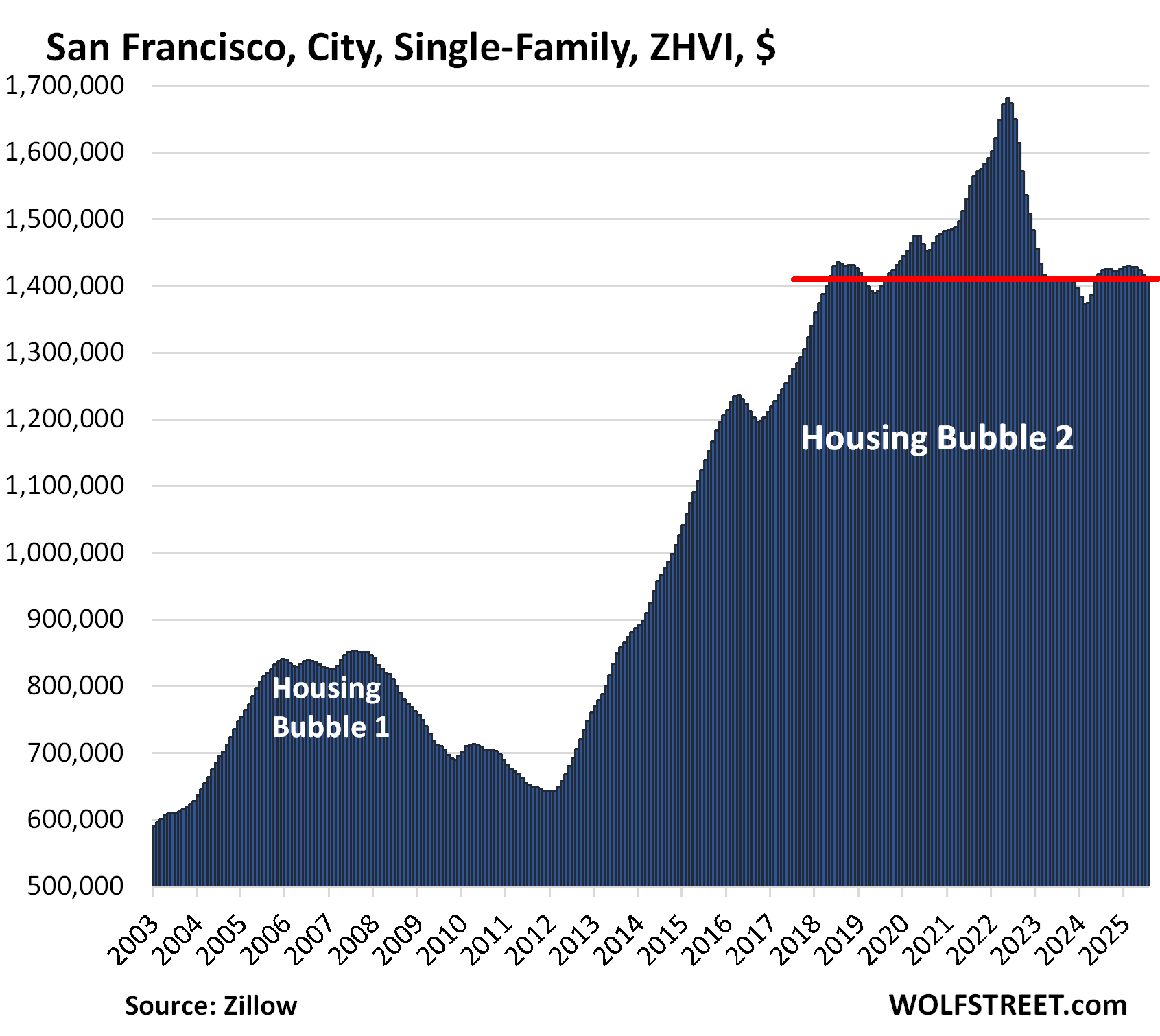

| San Francisco, City, Single-Family Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -16% | -0.4% | -1.0% | 233% |

Prices of single-family mid-tier homes are back to where they’d first been in May 2018. The entire pandemic-era price spike plus some have been undone.

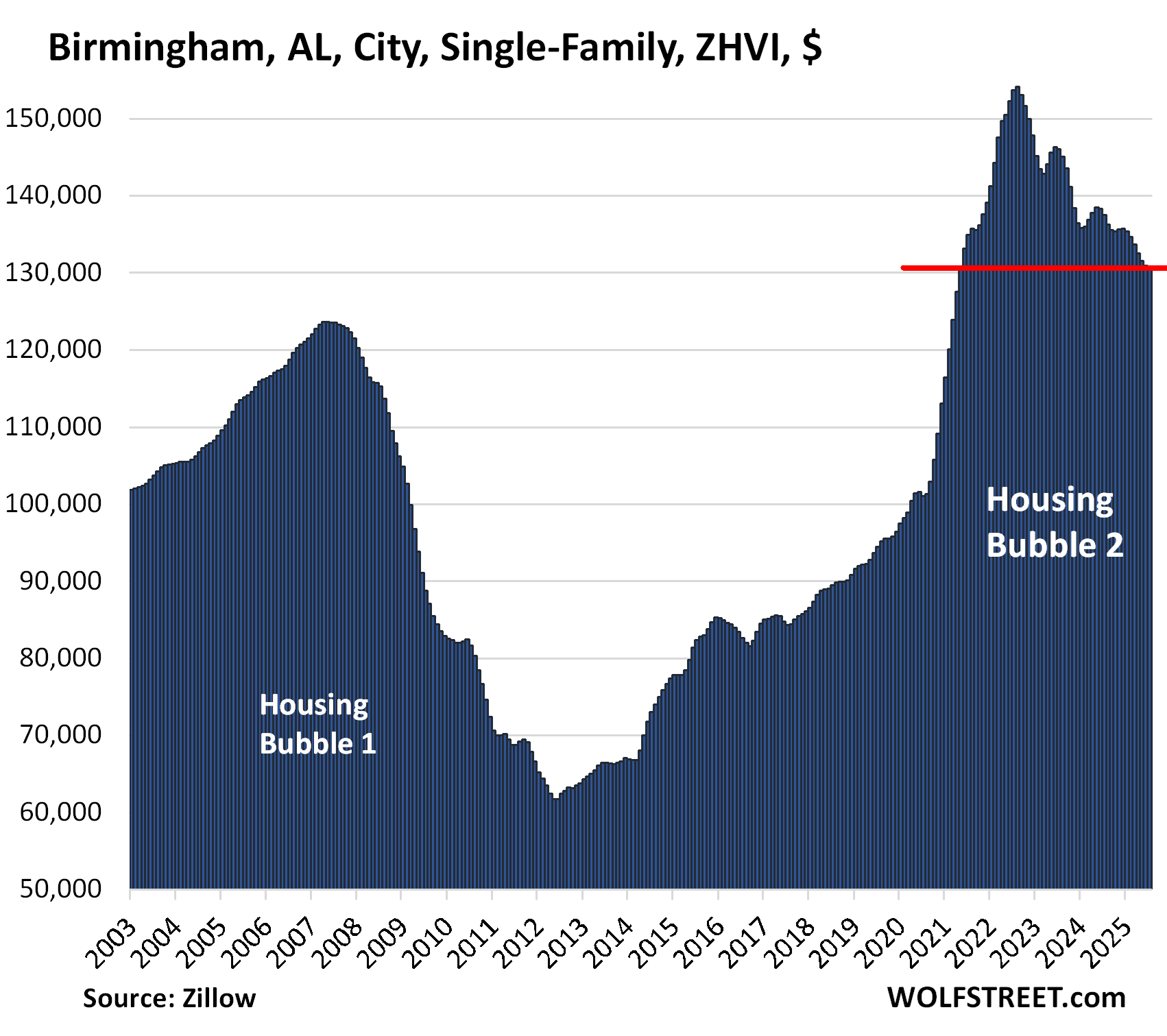

| Birmingham, AL, City, Single-Family Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2002 |

| -15% | -0.1% | -4.8% | 32% |

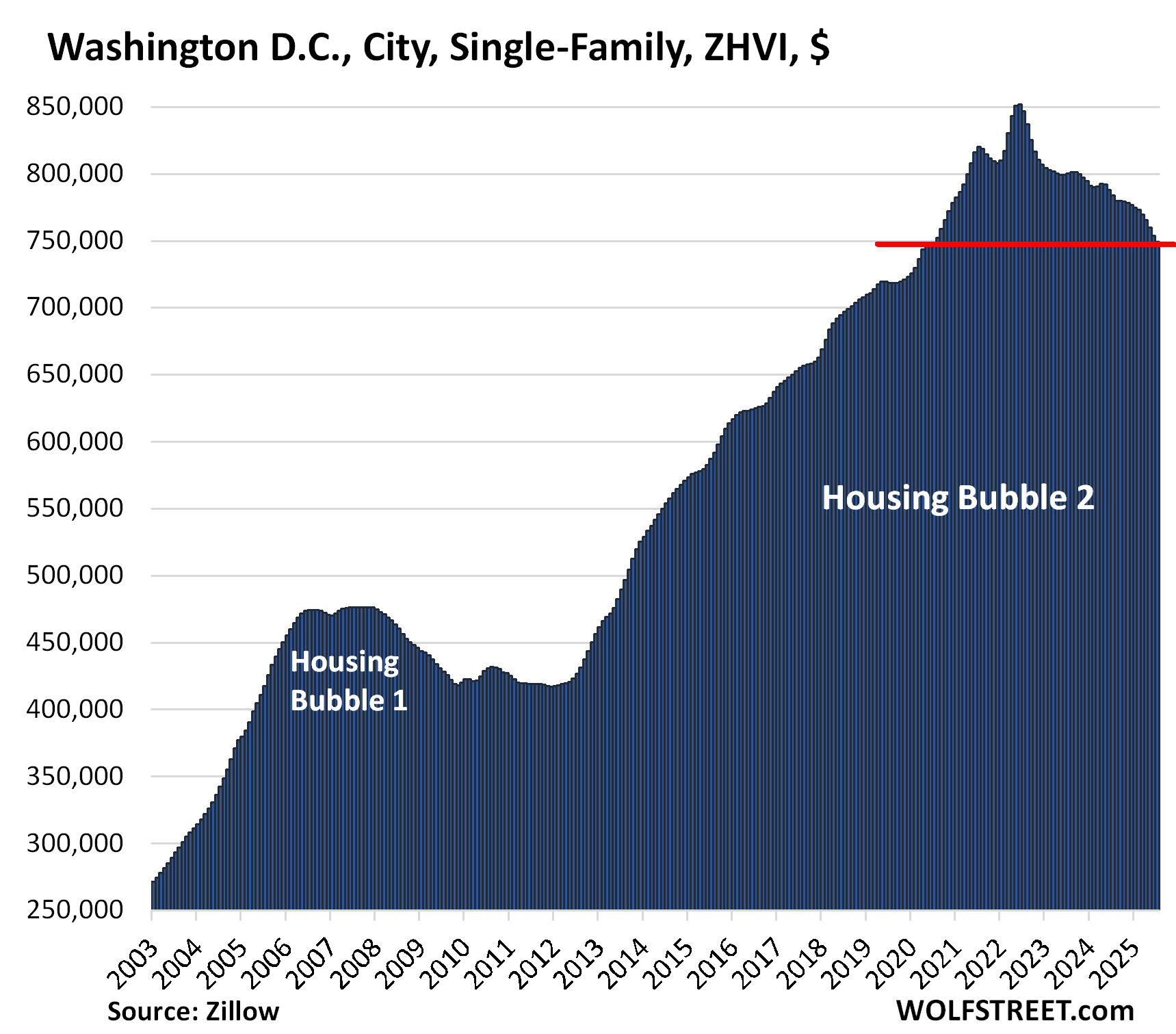

| Washington D.C., Single-Family Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -12% | -0.6% | -4.4% | 274% |

Lowest since mid- 2020, having undone the entire pandemic-era price spike.

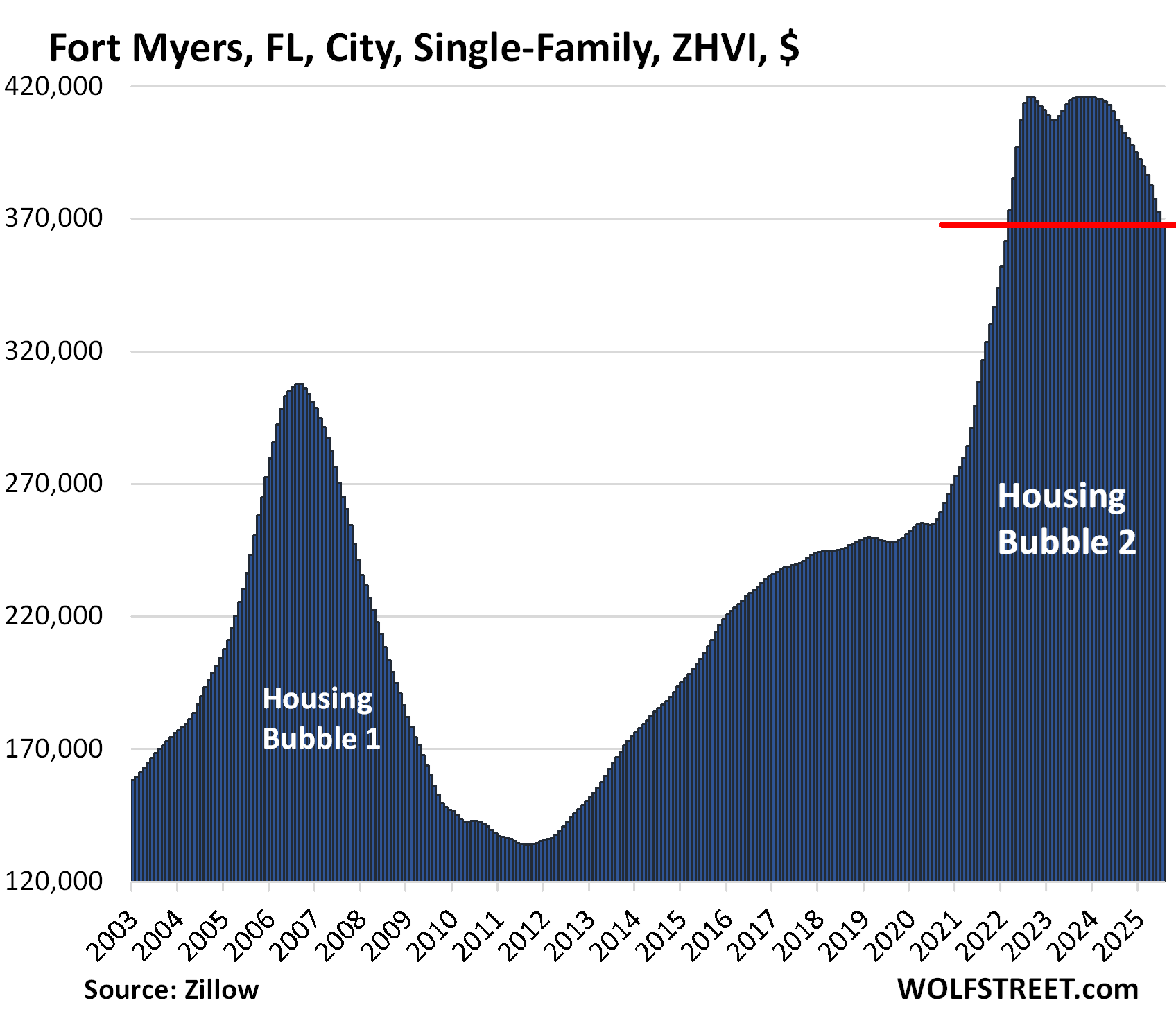

| Fort Myers, City, Single-Family Home Prices | |||

| From Aug 2022 peak | MoM | YoY | Since 2000 |

| -12% | -1.3% | -9.8% | 195% |

Note the 9.8% year-over-year drop.

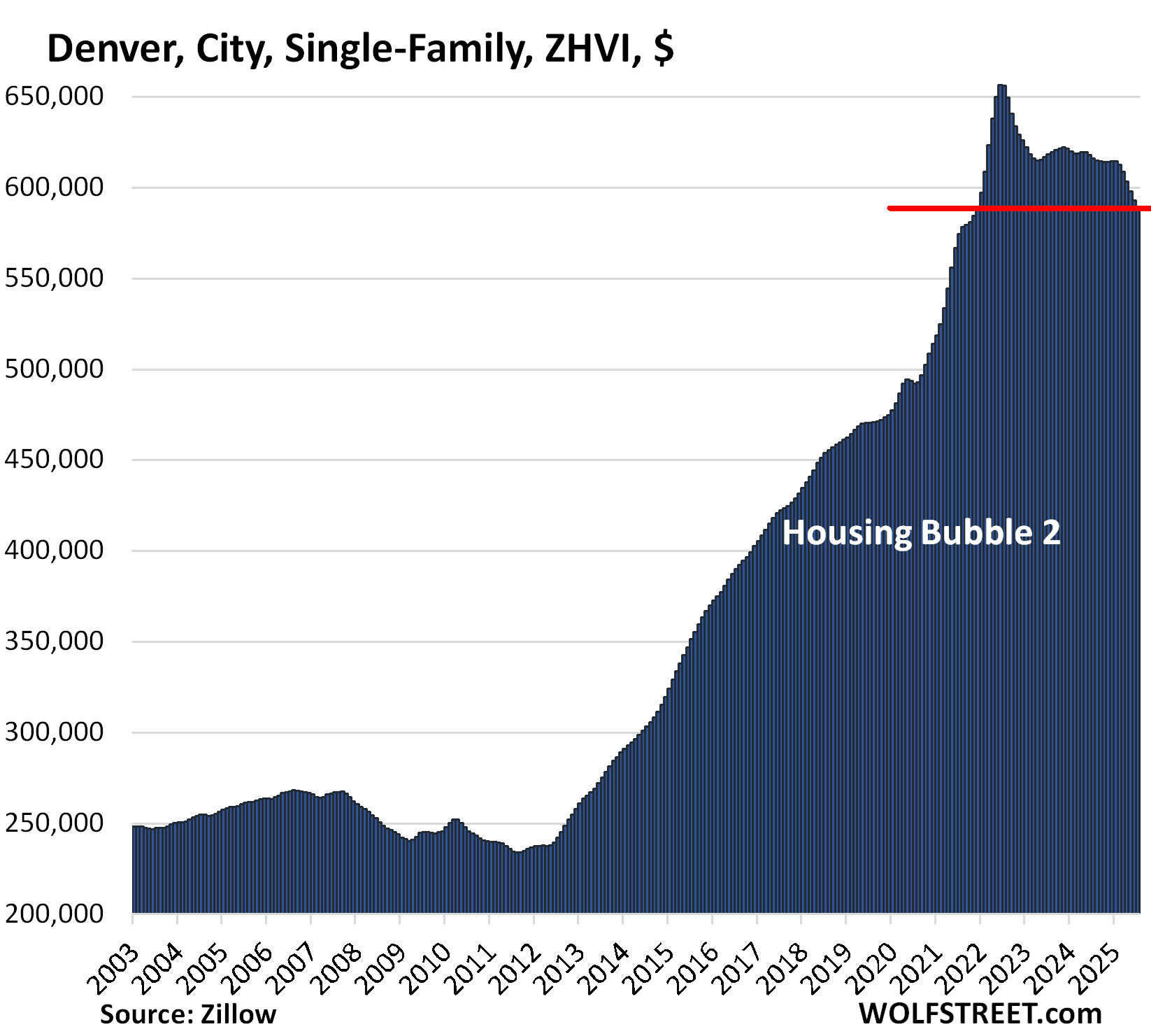

| Denver, City, Single-Family Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.6% | -4.4% | 213% |

Back to November 2021. From mid-2012 through mid-2022, prices had spiked by 174%.

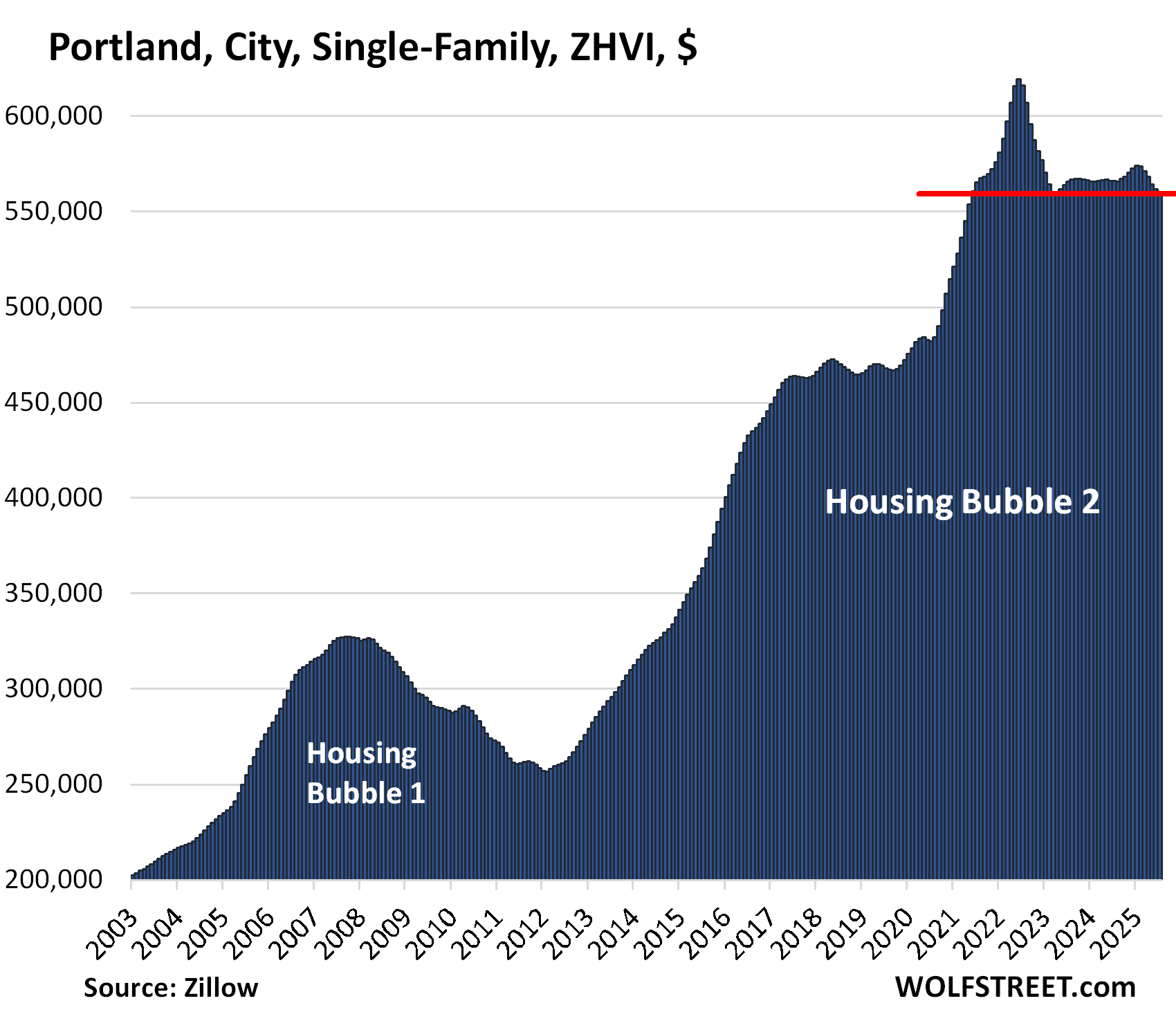

| Portland, City, Single-Family Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.2% | -1.0% | 222% |

Back to June 2021

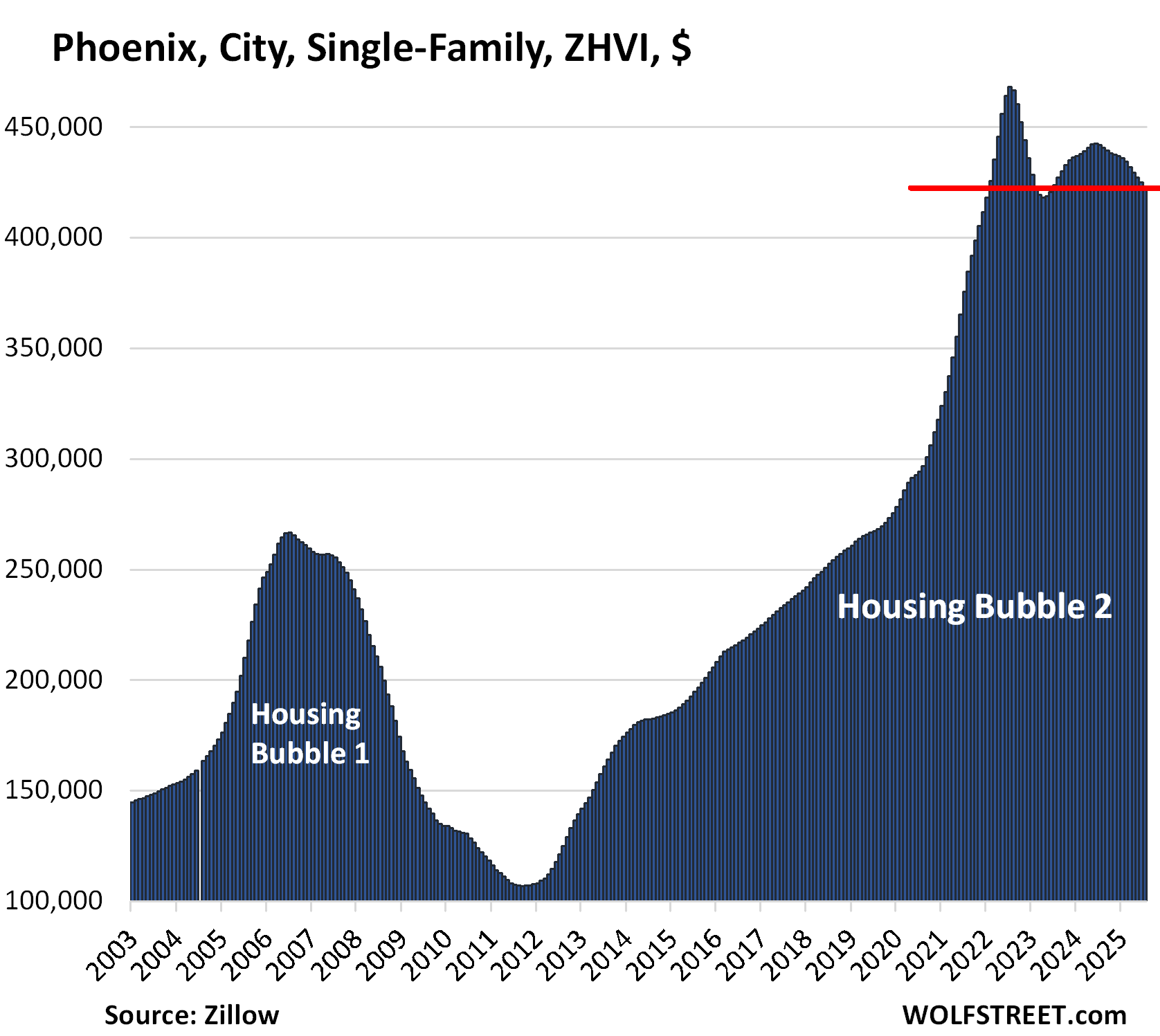

| Phoenix, City, Single-Family Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -10% | -0.5% | -4.4% | 250% |

From mid-2012 through mid-2022, prices had spiked by 339%, over half of it from April 2020 through July 2022, which was completely nuts.

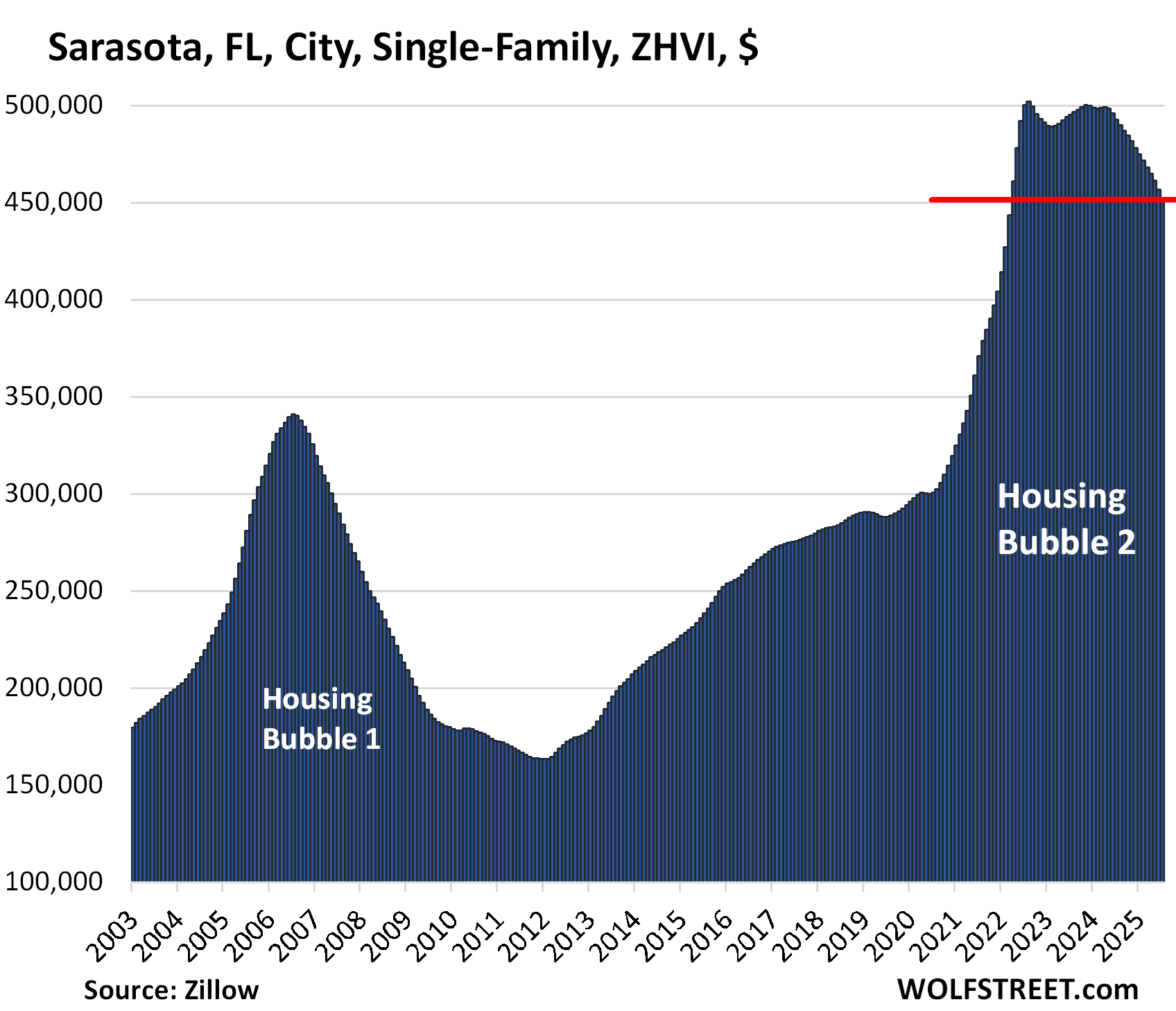

| Sarasota, FL, City, Single-Family Home Prices | |||

| From Aug 2022 peak | MoM | YoY | Since 2000 |

| -10% | -1.2% | -8.4% | 234% |

And in case you missed it:

Condo Prices Already Dropped by 12%-26% in 21 Bigger Cities through July. Condo Bust Takes Shape

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, I know back in 2008 Great Recession, there was a chart about how much the adjustable mortgages would be reset in subsequent years.

Given the hey day of housing since 2020, and rising rates since 2023, I wonder if there is a similar chart out there ?

Thanks

Newly issued adjustable-rate mortgages are now about 9% of total new mortgage issuance (Mortgage Bankers Association). So that’s up from where it was during the 3% mortgage era, but it’s still pretty low.

ARMs are only a problem when interest rates shoot higher. But that phase has already happened. When interest rates decline, AMRs adjust downward.

During the 3% mortgage era, AMRs were a minuscule portion, and when interest rates shot higher starting in 2022, these folks had some struggles after the reset, and those already on floating rates, but the number was small, and the issue is now largely behind the market since rates have been high for several years.

“But that phase has already happened.”…

I’ll take the other side of that trade. Interest are going up, is 1973 again, this time with a vastly different debt:GDP…

Interesting times.

The problem with adjustable mortgages is that if rates go up a lot, your new payments will cost you an ARM and a leg.

TS….,I saw what you did there!

Even with this the numbers still do not in my opinion make any sense for buying at the moment,still on strike.

Yes. Timing is everything. I bought a house in 1983 for $65,000 when interest rates were 16%. Nobody was buying property, the house was on the market for more than a year. I regretted that decision every day until I resold it for $850,000 in 2018.

History doesn’t repeat itself — it only rhymes.

This time the bubble is the investment is GPU hardware.

The return will be lower than people hoped and then comes the crash.

I agree. In a truly “free market” all that power (watts, calories, joules, whatever) would not be keeping processors warm and instead would find much more productive pursuits (i.e. growing food, building houses, building fusion reactors, fuck, building anything…)

We had machine learning (AI) in the 70’s, and the input data was much better, now we have much faster processors but the input data is an exponentially larger pile of crap..

Interesting times.

On a upbeat note:

A Mortgage is also known as a Death Pledge.

Enjoy your weekend!

☀️

Meaning simply that the debt survives the death of the holder, a requirement for a mortgage market.

chatGPT

Pose the query:

“The 12 Bigger Cities with the Biggest Price Declines of Single-Family Homes”

Even AI bows the knee to Wolf

(Artic) Wolf – picture a 747 jumbo jet full of people traveling at 500 mph at a 90 degree angle to the ground, at an altitude of 300 feet. Such is this current housing market. We all know the end result (‘we’ includes you). It’s too late to right the plane. There is no fix or solution. A 90 degree landing isn’t going to be pretty. Quite the opposite. Buckle up, ladies and gents!

A 45-degree landing is enough to make a mess.

Definitely. Standard instrument approach slope is 3-degrees.

I like that analogy, given each market moves at different speed and dynamic, since most SoCal areas are not yet on this list, I guess they are equivalent to being the back part of the plane instead of the front like Austin which already hit the ground?

Hey, that’s where I live (SoCal) and its NOT going to happen in my neighborhood…..HAHA.

Phoenix – I have been following the market in San Diego and more specifically N. County San Diego very closely. One of my neighbors put his house up a few months ago (Carlsbad) at the prices sellers were getting a couple of years ago. He wasn’t getting many buyers, so every few weeks he dropped the price by $25 – $50k and it just went into pending at ~$400K less than what he initially started at.

Will be interesting to see where all this stands in the next year but I presume there will be continual price drops – at least for the sellers that need to sell.

I have a friend just listed 5000 sq ft in the eastern foothills of San Diego in golf course community

Home listed for 2.6mm

2.5 acres with guest home .

Maybe 20 years old but has not been updated.

As Wolf says price and buyer can be matched up just a matter of willingness of the two parties

haha yup, the prevailing mentality in SoCal is not only this time is different but also WE are different….the wheel can be falling off the wagon everywhere else but here, no way! The hubris around here have that SoCal uniqueness to it so to speak..

Good example though, will be interesting to see where they end up selling at. On the contrary, it amazes me how many are still buying at current rates and insane price. Case in point, know two couples, one bought in San Ramon for $1.3M and the other in Placentia for $1.2M just couple of months ago, both at 6.2- 6.5% range 30 year and both have $1M mortgage taken out. That’s some strong faith in the market will continue to print money and value to the moon because 20% adjustment and they will be upside down immediate and at the same time giant albatross of $1.M ($7k-$8K a month) for 30 years…kind of give me a new perspective and context when someone else told me they just bought a house in SoCal recently…

@Phoenix_Ikki,

There are roughly 600,000 single family residences in orange county, california and roughly eight billion people in the world that would find the weather, landscape, low crime rates, and local amenities extremely attractive. There’s also a sucker born every minute and they are all willing to fight each other over scraps. That’s why Orange County is different.

@BS ini “Eastern foothills of San Diego”. Around here we call that “fire country”.

@Phoenix_Ikki If someone asked me if thought they should buy or rent in San Ramon (Zillow just lists one home for sale under $1mm an had 3br homes renting from ~$4K to $11K) I would tell them to rent since prices are still going down, but if they want to buy and can afford the payment I would not worry about it. A MD friend has always leased Hondas and he asked me if he should buy out his lease a and keep his Accord (with ~40K that he garages every night) rather than lease a new one. I told him to buy out the lease and drive it until at least 120K, but he leased a new one since he can afford it and that is what makes him happy. $8K/month is a big mortgage payment but for someone who had had $500/month increases for the past few years locking in a payment often seems like a good idea.

Old aviation motto: A good landing is any landing you walk away from.

Sarasota, Fort Myers, Cape Coral show that the peaks occurred in 2024, that may be in error. Looking at the price graphs think all the peaks occurred in 2022.

yes, thanks.

Man, I’ve just come to the conclusion I’ll be a renter forever, given I have 30 years till I’m dead (hopefully sooner), and I can’t take a house with me.

I live in a poor area, and the houses are pretty much starting at 270k to 315k. Reached out to the mortgage broker for the low end, and he told me if I want my monthly payment to be around $2,200 a month I would have to put down about 80k.

Only thought I had was how in the hell I would come up with 80k. The crazy thing is when I was a kid these same houses were going for low 100k. In the late 90’s early 2000’s my parents were renting a house in the same area for $500 a month.

$2,200 is over the 25 to 30% mark of my monthly income, so I definitely won’t be stupid and purchase anything. It doesn’t fit my lifestyle being in construction, and the possibility of a layoff at any random time.

I have a friend who sells commercial real estate in NY, and he told me to keep renting, because a house is a giant liability with rising insurance, taxes and maintenance costs.

I know a lot of younger guys that are paying half their monthly income on the mortgage, and I couldn’t fathom that type of slavery.

When that layoff comes up the games over.

I guess my issue is I’m right around six figures, but with the rising costs of everything else (groceries, electricity, rent payment, student loans, debt to the state, gas, etc.) I’m essentially check to check as it is. Plus I’m single, and don’t have any family with any resources that may be able to help me.

I don’t even attempt to save anymore. Just live day by day. My only goal is to reach my destiny with the grim reaper lol.

Hey Buddy- I know it’s easy to feel that way.

You might consider house hacking. Look for a decent 2-4 unit prop, that yields 2k month for 200k, 3k for 300k etc. if you’re in construction you have a great opportunity to improve the units and get better rents and tenants. They just introduced 5% down Fannie loans for owner occupied 2-4 units to solve the crazy numbers you described. You might achieve some cash flow with time and improvements, there’s mortgage pay down, and appreciation (usually 3% year) and tax breaks. 4 ways to win. Treat your tenants like clients and you will have little competition.

Especially for somebody in construction. I’d be looking into something like that if I wasn’t right at the bottom of the bell curve for physical skill, or even knew people I could trust to do it competently and at a fair price. However, I am, and I don’t. So a renter I’ll remain.

The housing market is a financial asset whose value changes in response to the contract interest rate which impacts and ultimately determines the price that that the average working stiff can afford.

@It’s over when you say “I have 30 years till I’m dead” I’m guessing you are at least 50 (since over half the guys make it to 80 today). If you have been in constuction for years you probably have the skills to fix stuff at rental property (part time on nights and weekends) and since few “kids today” know how you can make some decent extra cash (my “lowest” paid – lowest skilled handyman/cleaner makes $45/hr) to put in a money market that will grow until you need it. For any young people reading this If you commit to spending less than you make EVERY month for decades and investing the difference you will be a lot better off than most of youe friends at 50.

Do we see similar numbers or analysis for commercial real estate?

Commercial real estate has very few but huge transactions. So if you go by city, you might have zero transactions over a three-month period, then 2 transactions in one month worth hundreds of millions or even a billion $ each. So constructing a by-city monthly index is meaningless.

But we have looked at some of the individual transactions. In the office sector, prices of these transactions were down by 40% to 80% from the last sale years earlier, and sometimes more. You can find them here:

https://wolfstreet.com/category/all/commercial-property/

For ALL buyers AND sellers,,,

Wolf does a really great job of reporting the in and outs of ALL the RE and other ”financial” news far damn shore…

While I can see and understand completely based on his reporting, I can testify that in ”former crashes” , in FL especially, RE prices have gone down 75% in many cases that I have personally watched the last 50 years.

Some took a short time to recover, especially those really well built gulf front,,, others took longer…

seems very likely we will see similar sooner and later

Can Floridians still get homeowners insurance ?

If you couldn’t get basic insurance which is fire…you couldn’t get a mortgage anywhere.

Yes. I even got a new company to insure my Miami Beach house.

It seems to be the general consensus that the housing industry must inevitably bear the major impact of a tight money policy.

See: New Privately-Owned Housing Units Under Construction: Total Units (UNDCONTNSA)

Units under construction fell from 2022-09-01 1721.1 to 2025-07-01 1371.8.

Will be interesting to see if these price declines spread to Midwest and northeast. South and West are cooked, and we are just getting started.

Impatiently waiting here. I wonder what is the case for/against this?

I see nothing special about midwest and northeast. They would follow surely, may be bit late.

Still hoping Seattle will follow suit like these other cities. ZHVI for Seattle is down 1.4% YoY, or 7.9% from the peak if I did my math correctly. Hoping for more.

One thing I’ve noticed here is that town homes are sitting on the market significantly longer than single family homes. We’ve seen these sellers or new-build companies do everything in the sun except lower prices. Rate buy downs, incentives, etc. My wife and I are thinking of throwing some low-ball offer at this town home in a neighborhood we love that has 7 units left, all sitting on the market for a year. I don’t fully like the idea of a town home but in some neighborhoods it’s the only “affordable” choice.

There is still a lot of pent-up money here in Seattle from tech employees with their years of MAG7 RSUs unwinding.

As always thank you for your analysis, wolf, we’re going to buy you a beer.

Seeing the same here with townhomes and I’m in a midwest market that’s still pretty hot. Probably below pre pandemic pricing in real terms on average. If this keeps up the lowballs are going to start going out.

Each housing market moves to its own drummer

Each graph demonstrating the 20 pctish decline in home prices.

The mountain of debt contrived by the QE era upon which the price declines rests,

contrasts the absurdity of ignoring the likely outcome when the obvious house price bubble collapses. Of course, I have usually been wrong which I attribute too the morality of my education

Denver 10% reduction should be just the tip of the iceberg, the thriving metropolis which still leads the nation in car theft. The multiple shootings continue to take place downtown, the homeless are given free rein to set up camp anywhere. We will be the twin city of Austin, TX with more professional sports teams. 5 years out of the pandemic, lots of folks are finally figuring out the juice is not worth the squeeze. 80% of the water is west of the continental divide, while 80% of the population lives east of the continental divide.

I drive around downtown Indy neighborhoods where prices have doubled/tripled in the last ten years and a lot of them are actually worse than they were in 2013-2015 when you could not give away a house here.

Denver certainly has had a bad 5 years, but crime is rapidly turning a corner for the better, the homicide rate year to date in 2025 is the 3rd lowest in the last 20 years, much lower than prepandemic, and very close to the lowest levels this century recorded in 2010 and 2014. In fact, the drop year to date is the largest drop of any large US city. Car theft has also dropped drastically, 46% less than the previous year. The peak year for the crime explosion 2022, and it will take a few more years of improvement to really sink in, but things are actually moving in the right direction after the utter stupidity of public policy toward policing during the pandemic.