Lennar’s average sales price drops to lowest since Q2 2020, gives up entire 2020-2022 price explosion. Homeowners wanting to sell have no idea what they’re up against.

By Wolf Richter for WOLF STREET.

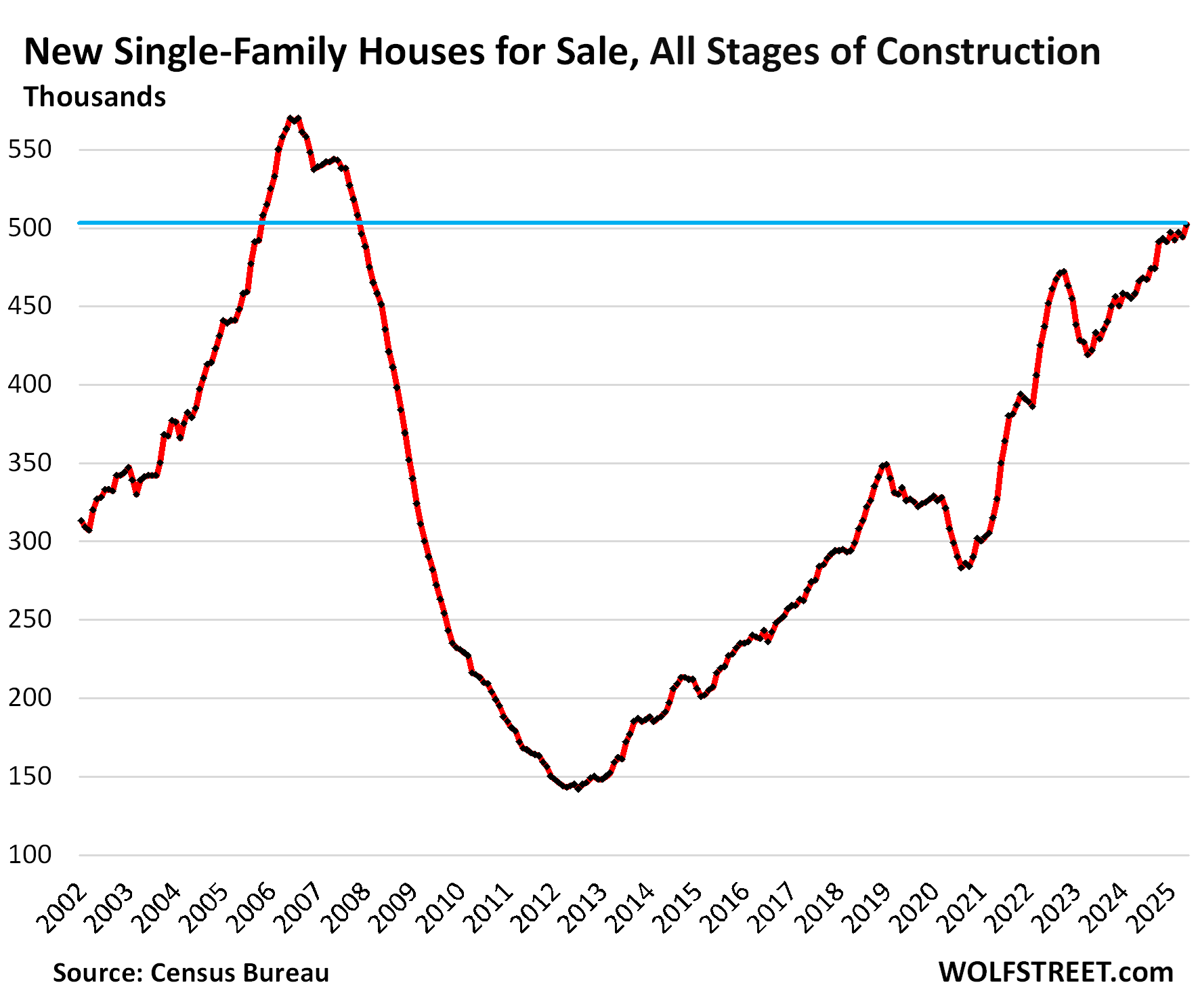

New single-family homes for sale at all stages of construction rose to 502,000 homes in May, the highest since November 2007, when inventory was on the way down during the Housing Bust. Inventory has been above 490,000 for the seventh month in a row, all seven months the highest since November 2007, according to data from the Census Bureau today.

During the housing bust, inventories first reached this level on the way up in October 2005. Over the following three years, oversupply and lack of demand wreaked havoc among the homebuilders.

But now there is still somewhat decent demand for new homes, as homebuilders are cutting prices and offering massive incentives – especially costly mortgage-rate buydowns – to take sales away from homeowners trying to sell at illusory prices, while demand for these existing homes at these prices has collapsed.

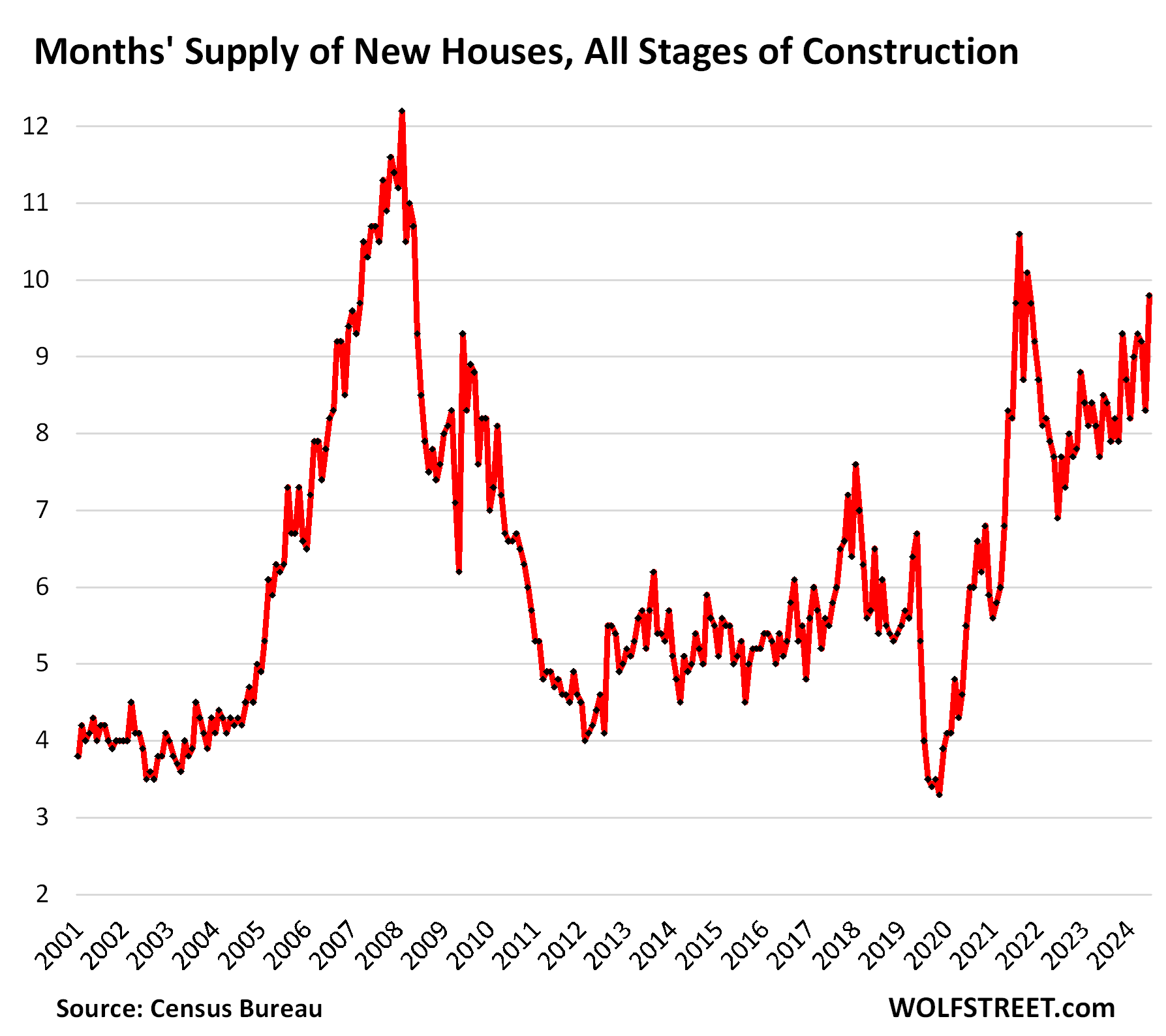

Supply of new homes spiked to 9.8 months in May at the current rate of sales. A glut of new houses on the market is exactly what this overpriced housing market needs.

In their earnings calls, homebuilders are talking about bringing their costs down to be able to sell profitably where demand is, and they’ve been sacrificing gross profit margins for the past two years because they have not been able to get costs down quickly enough. But gross margins had fattened to extraordinary levels during the home-price explosion in 2020 to 2022, and homebuilders have lots of room left to give up – we’ll look at Lennar’s gross margin in a moment.

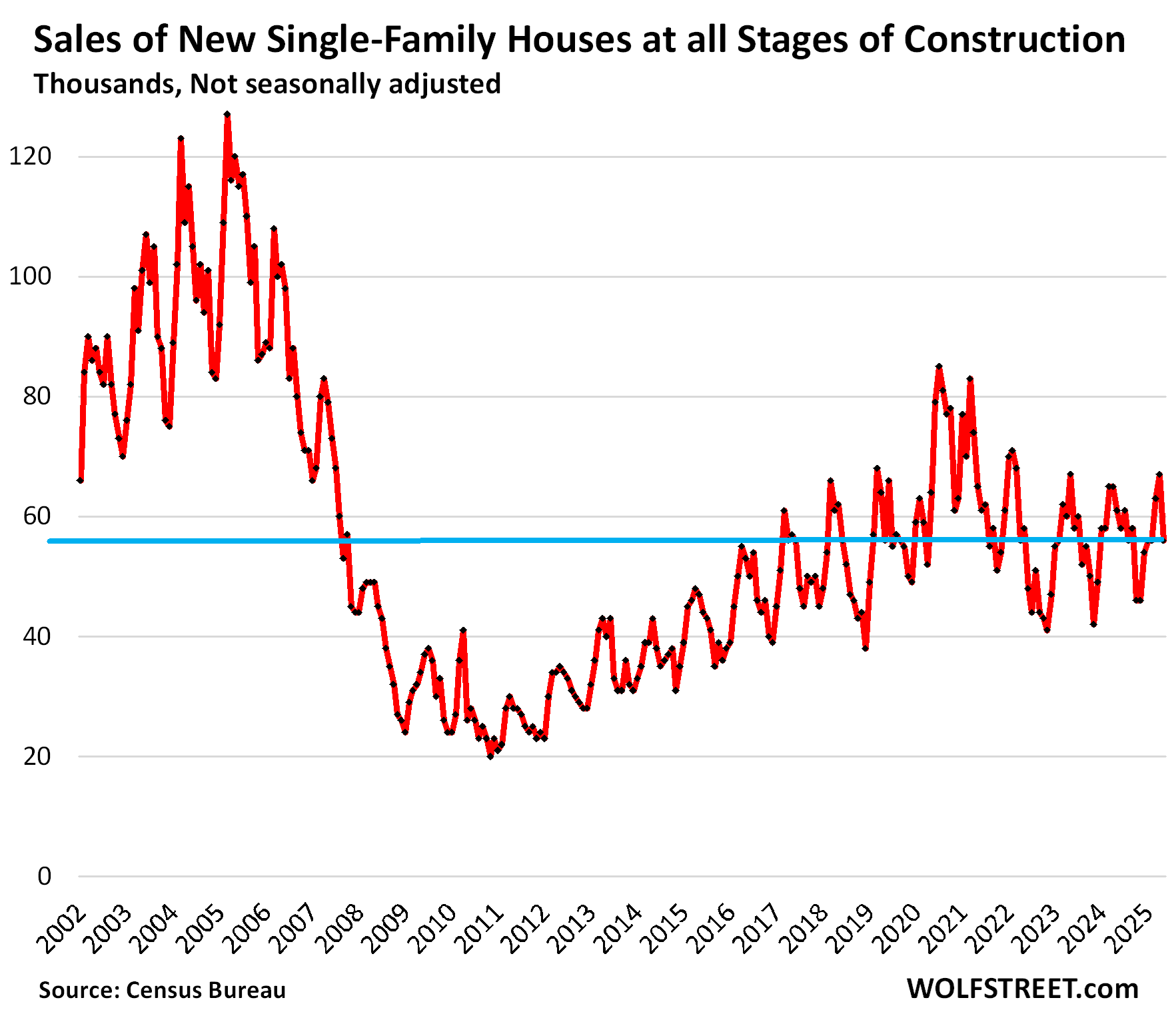

Sales of new homes, at 56,000 contracts signed in May, were down by 8.2% from a year ago and down by 12.5% from May 2019.

These sales are tracked by signed contracts, not closed sales. Some of these deals will fall through before closing. As such, they compare to “pending sales” of existing homes, which are also based on signed contracts, not closed sales. April pending sales were down by 32% from 2019, the pre-pandemic normal, reflecting the ongoing collapse in demand for existing homes.

So compared to existing homes, sales of new homes are in far better shape. Homebuilders face a tough market, but they cannot just not sell and wait for better days – unlike homeowners. It’s their business, and they have to build homes and sell homes, no matter what the market is, and they have to find the price points at which they can do so.

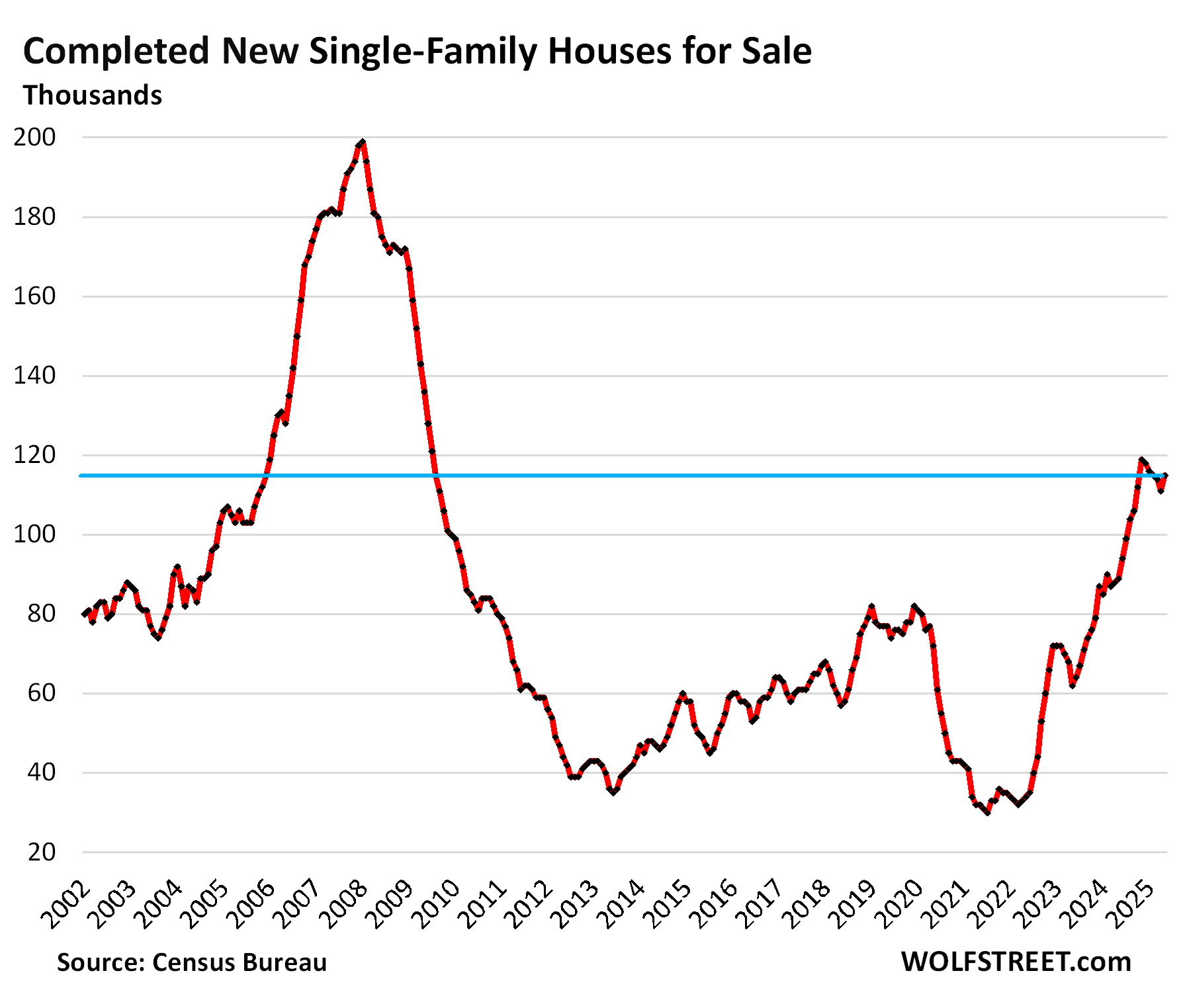

Inventories of completed new single-family houses for sale rose to 115,000 in May, up by 29% year-over-year, and up by 49% from May 2019. Inventories have been at this about level or higher for the seventh month in a row.

Homebuilders are motivated to sell them quickly because they’ve sunk a lot of capital into them.

And they’re selling them at a good clip. Sales of completed homes, at 30,000, were unchanged from a year ago, and up by 36% from May 2019. This is where the action is. Supply was about four months at this rate of sales, roughly normal for normal times, but double of where it had been in 2021 and 2022.

The publicly traded homebuilders have been shedding some light on their strategies in this market as their shares have sunk from their highs in mid-October: DR Horton [DHI] -34%, Lennar [LEN] -39%, KB Home [KBH] -37%, PulteGroup [PHM] -30%, etc.

Lennar has been disclosing more details about its incentive spending than some of the other homebuilders, and it has done so for years in the same format, so we’ll use it here as an example.

Incentive spending jumped to 13.3% of revenues, “primarily” due to mortgage-rate buydowns, said Lennar Co-CEO Stuart Miller in the earnings call earlier in June for Lennar’s Q2 ended May 31.

This 13.3% was the highest incentive spending rate since 2009, and up from 8.4% in Q2 2023 and up from 1.5% in Q2 2022.

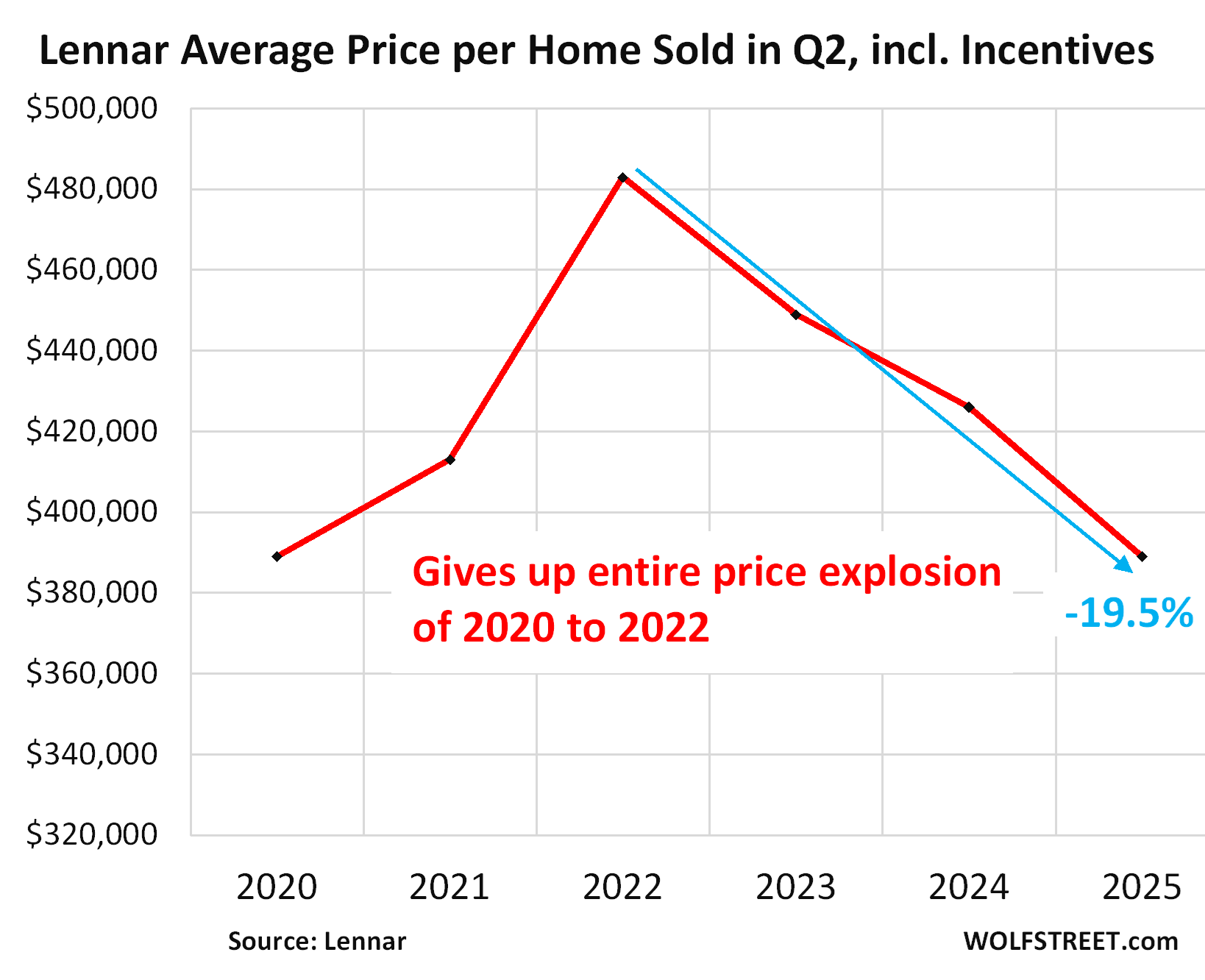

The average sales price per delivered home, which includes all incentives, dropped by 8.7% year-over-year, to $389,000 in Q2. Compared to Q2 2022 ($483,000), it dropped by 19.5%. It’s back where it had been in Q2 2020, having given up the entire price explosion of 2020 to 2022.

Homeowners wanting to sell have no idea what they’re up against:

Gross profit margin on home sales dropped to 17.8%, down from the fat profit margin in Q2 2023 of 22.5% and from the obese profit margins in Q2 2022 of 29.5% when FOMO-addled homebuyers lined up to pay whatever, and homebuilders were happy to let them pay whatever.

So price reductions have largely come out of the obese profit margins. But Lennar talked a lot about bringing its costs down over time to hit the “affordability” targets while still remaining profitable.

In the earnings call, Co-CEO Stuart Miller said among other things (transcript via Seeking Alpha):

“As mortgage interest rates moved higher for longer and consumer confidence declined, we continue to drive volume with our starts, while we incentivize sales to enable affordability.

“As a result, during the second quarter, sales incentives rose again to 13.3% reducing our gross margin to 18%, excluding purchase accounting, as expected, on a lower-than-expected average sales price.

“We expect our average sales price [in Q3] to be between $380,000 and $385,000 as we expect to continue to see pricing pressure on homes that will be sold during the quarter.”

“The markets that experienced more challenging conditions during the quarter were:

- the Pacific Northwest markets of Seattle and Portland

- the Northern California markets of the Bay area in Sacramento

- the Southwestern market of Phoenix, Las Vegas and Colorado

- and some Eastern markets such as Raleigh, Atlanta and Jacksonville.

“These markets experienced sensitivity to higher home prices and/or the macro impact on the technology workforce.

“We expected that the new normal of higher interest rates for longer would mean lower margins for longer as we drove affordability.

“We knew that we and the industry, we’re initially going to have to bring down the price of homes we build through incentives and mortgage buydowns to meet affordability and normalize the supply and demand balance.

“We are building what will become a stronger margin driving platform by using volume to enable us to drive costs down across our platform. We know this takes time, but we also know it will help build a healthier housing market and position Lennar for bottom-line growth even as the market remains soft.

“This trend has started with reducing margins and using incentives to enable affordability. But looking ahead, it is much more about transitioning to lower cost structures.”

But incentives are not included in the median price by the Census Bureau.

The Census Bureau tracks sales prices of new houses by the prices in purchase contracts that buyers signed. These prices that are in the contracts do not include the costs of mortgage-rate buydowns and some other incentives, and thereby overstate the effective sales prices. But homebuilders disclose the effective sales prices net of all incentives – what Lennar calls the “average sales price” – in their financial statements.

So Lennar’s average sales price fell by 19.5% in Q2 2025 from three years ago in Q2 2022, giving up the entire pandemic price spike.

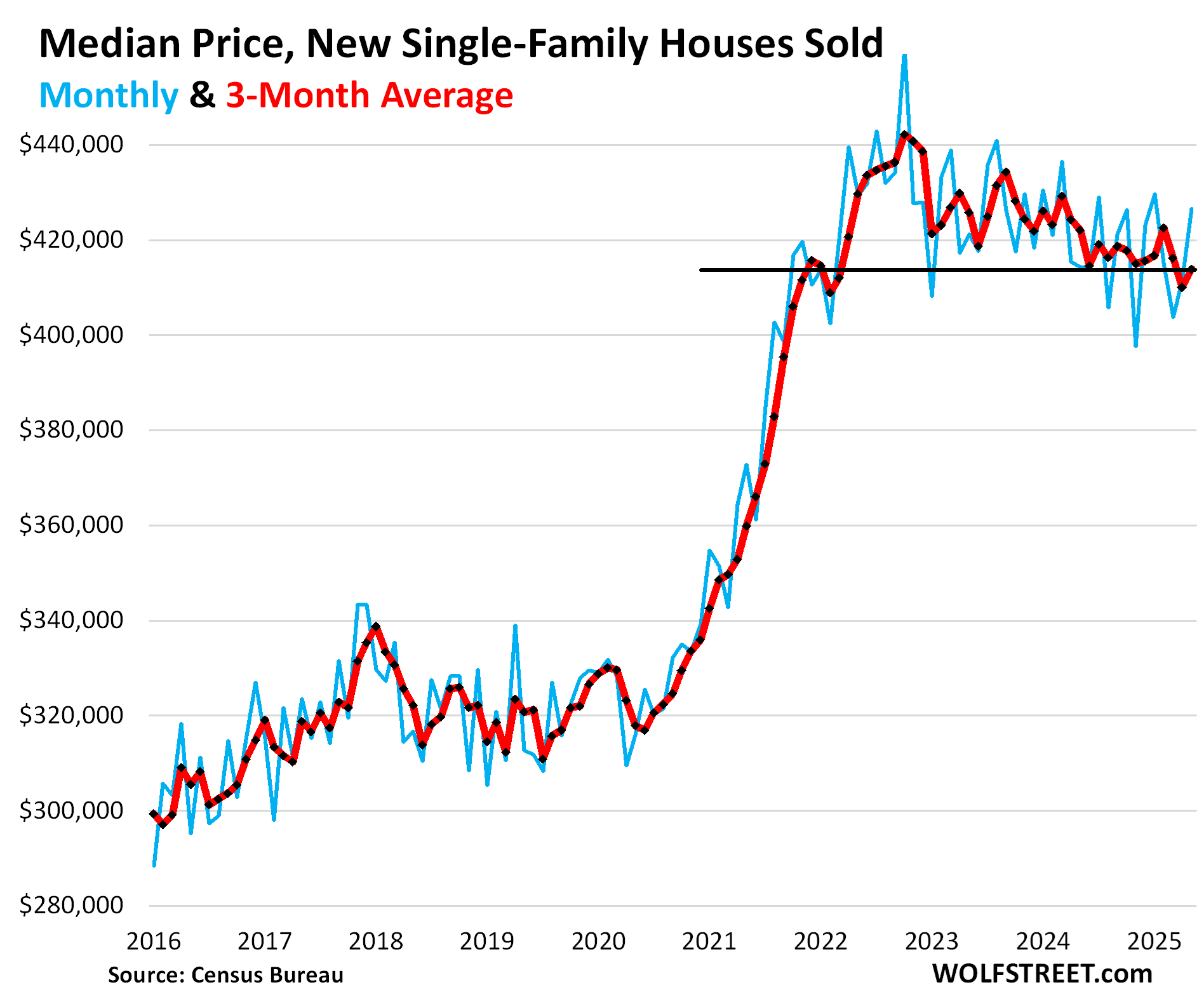

The median contract price, as reported by the Census Bureau, has also zigzagged lower, but only barely, because the rising costs of the mortgage-rate buydowns and other incentives – that have soared to 13.3% of revenues at Lennar – are not included.

In May, the median contract price rose to $426,600 (blue in the chart below). The three-month average, which irons out some of the month-to-month squiggles rose to $413,900 (red). This was down by only 1.9% year-over-year and by 6.4% from the peak in 2022.

Inventory for sale by region.

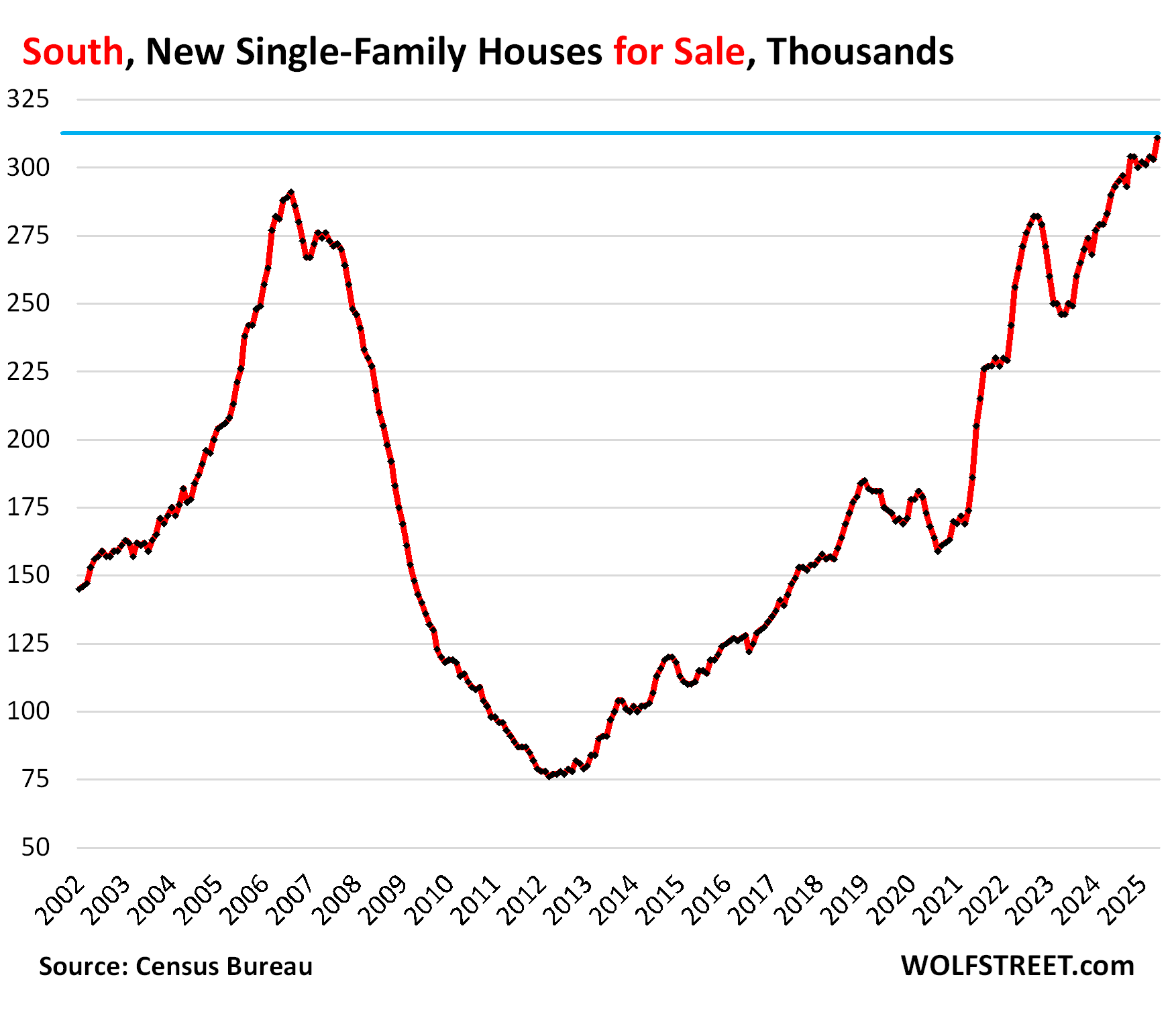

In the South, inventories of new houses for sale at all stages of construction jumped to a record of 311,000 in May, well above the peak levels during the Housing Bust, and up by 71% from May 2019! Inventory for sale has been above the Housing Bust peak for an entire year.

The huge Census region, dominated by Texas and Florida, typically with the most vibrant population growth, is by far the largest market for new houses in the US, accounting for 62% of total US inventory for sale, and for 55% of total US sales in May (a map of the four Census regions is below the article at the top of the comments).

Sales plunged by 16% year-over-year in May to just 31,000 new homes. Compared to May 2019, sales were down by 11%. Given the surge in inventory, and the drop in sales, supply jumped to 10 months.

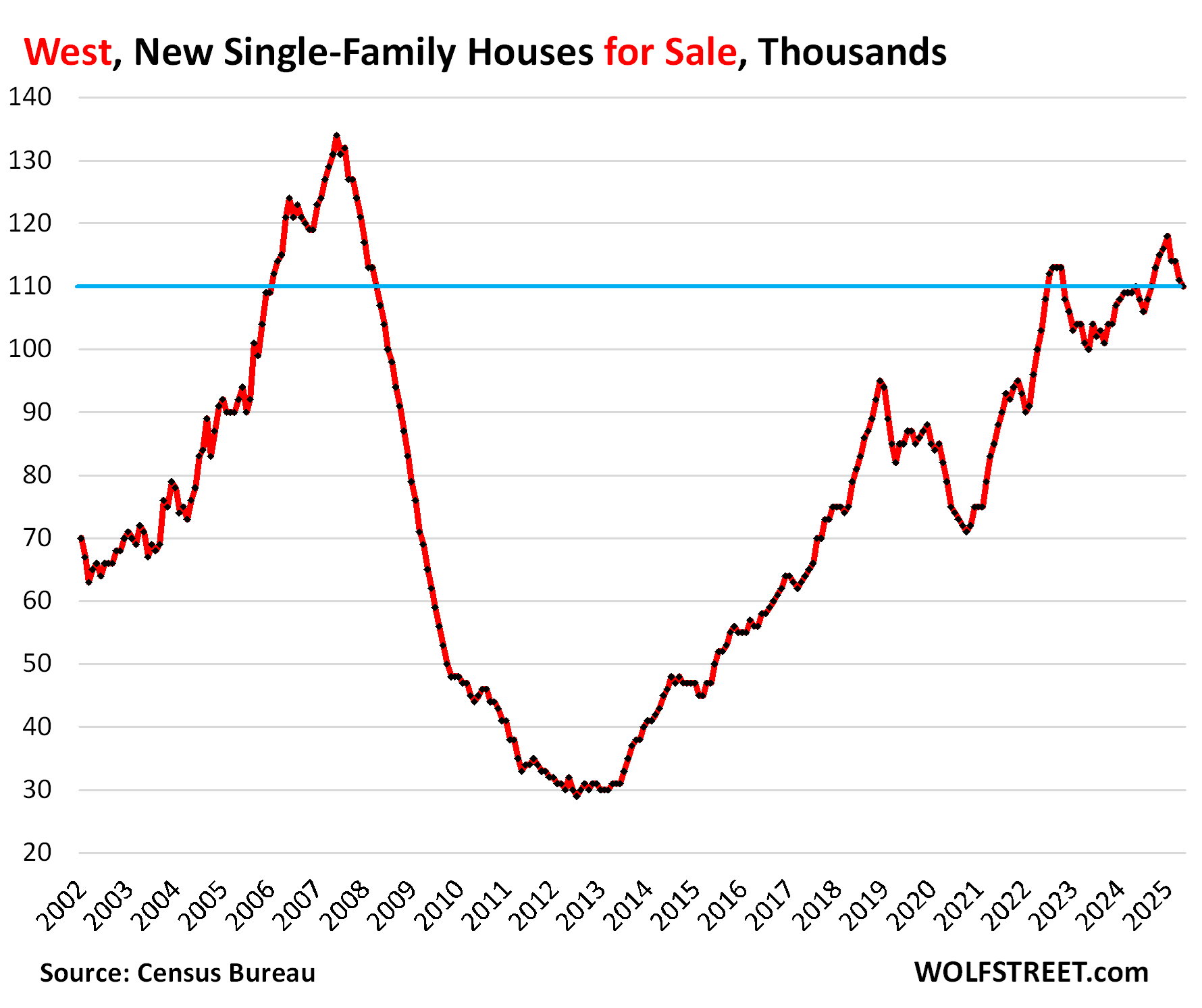

In the West, inventories dipped to 110,000, unchanged year-over-year, and up by 29% from May 2019.

The West accounted for 22% of the total US inventory and for 27% of total US sales in May.

Sales in the West remained at 15,000 new homes, up by 7% year-over-year and up by 25% from May 2019.

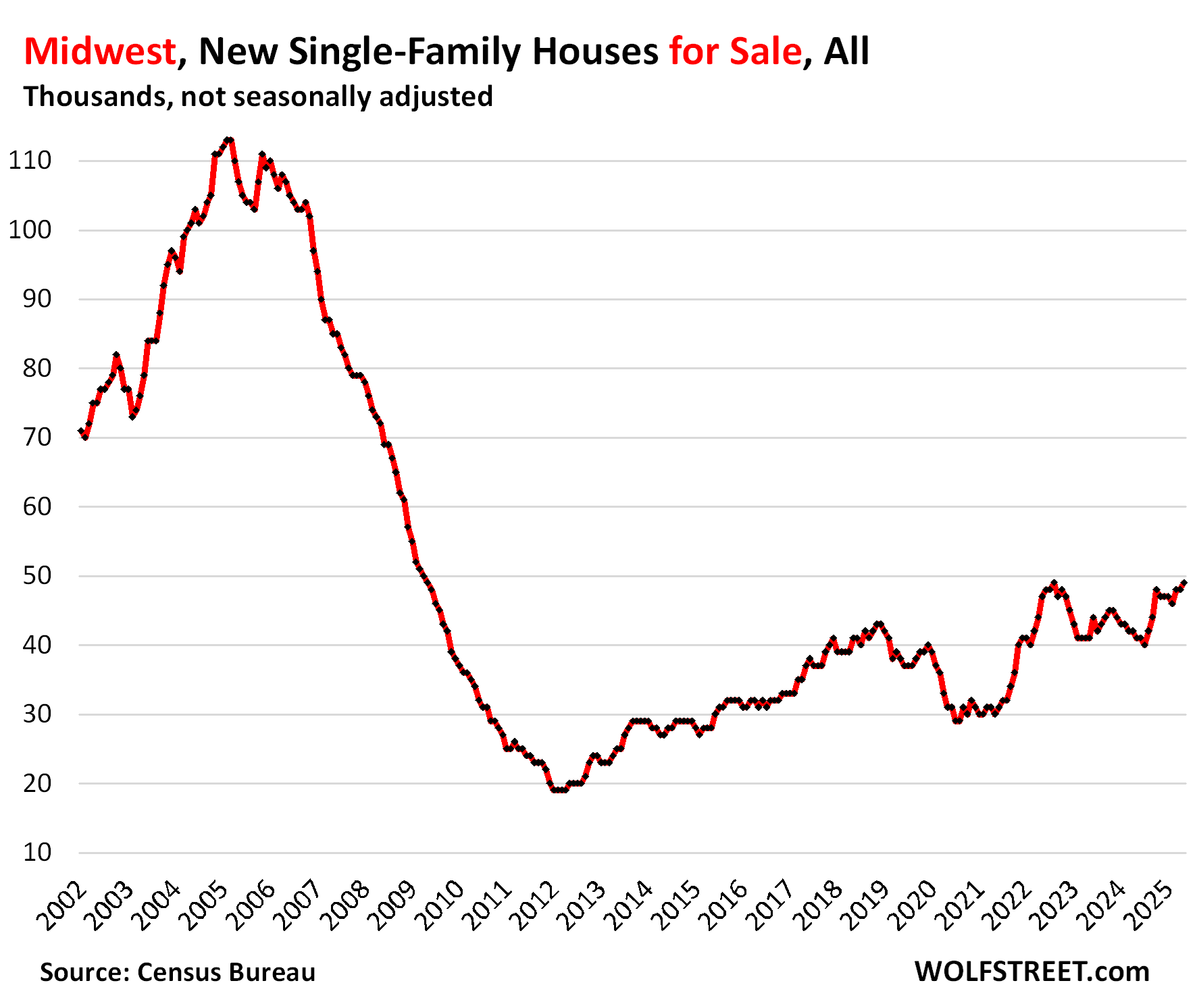

In the Midwest, inventory rose to 49,000, up by 19% year-over-year and up by 29% from May 2019.

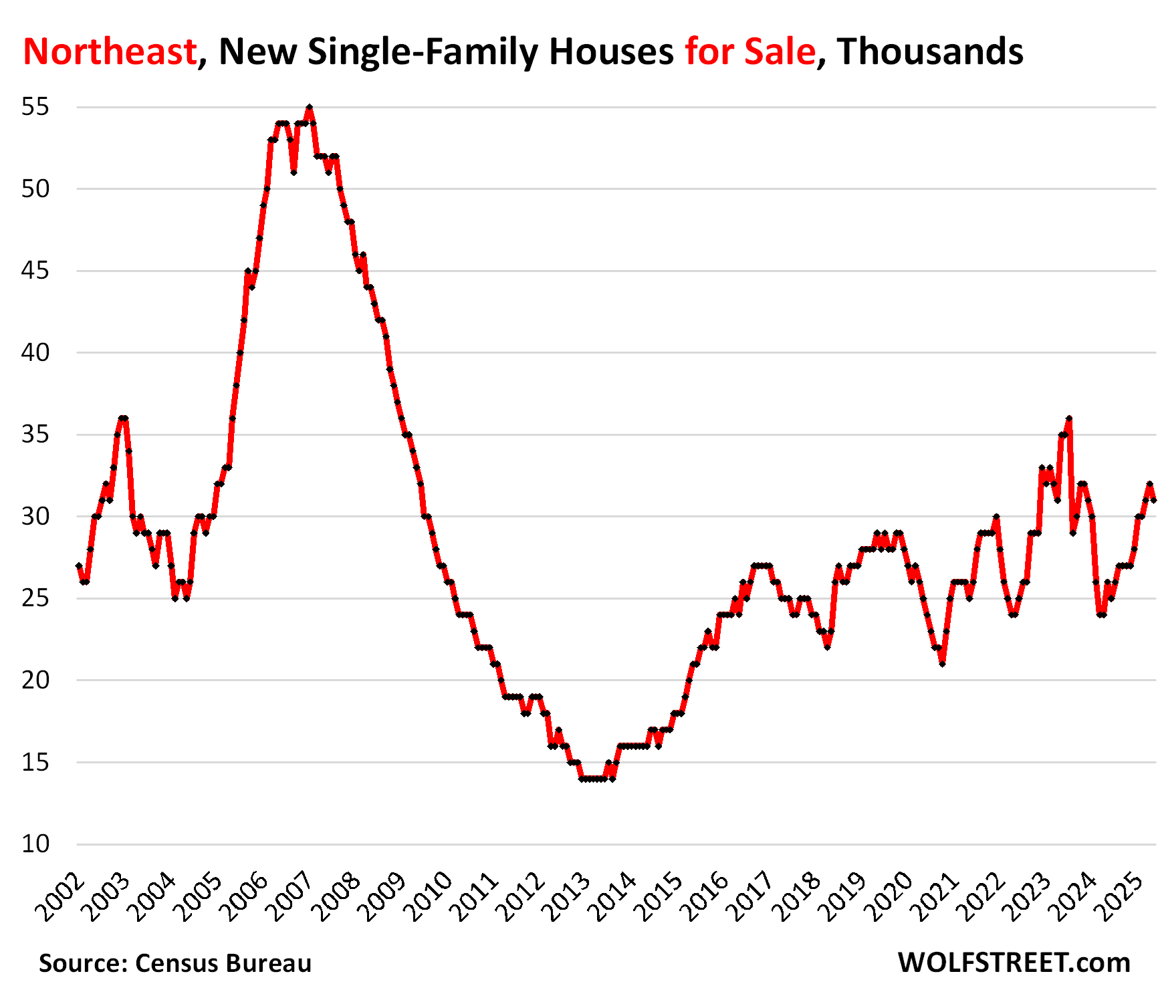

In the Northeast, inventory dipped to 31,000, up by 19% year-over-year and by 7% from May 2019.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The promised map of the four Census regions of the US:

Are these homebuilders trying to take a page out of Stellantis playbook when it comes to inventory? Well, not quite there yet in comparisons but still….sure is rising faster than they probably forecasted or anything within their imagination, especially if the signal to build was based on forecast model from back in 2021-22 market dynamics.

Too bad there isn’t as many Lennar new build in desirable part of SoCal, sure would be nice to have this kind of new home price decline/inventory pressure to “motivate” existing home sellers. Also, one has to wonder, with these new inventory spiking, must be harder for MSM and RE to continue to spin the we don’t have enough houses narrative.

In my town in the NE, there are lots of new developments going in all over the place. And it is amazing the (list) price that they sell for (not showing incentives) compared to what existing homes in the best neighborhoods go for. To me, I’d pay just about any premium to live close to downtown on a big lot in the original suburbs, versus one of these God-awful new developments. I’m amazed they sell at all, but I guess there will always be demand for used houses from people like me, (and also because I like a masonry build from before the 1930s).

“…and also because I like a masonry build from before the 1930s”

Plaster walls are nice, but eventually come apart in places, and the plaster needs to be replaced, or partially replaced, that stuff doesn’t last forever. And if it’s more than just a repair job, if you have to re-plaster the walls, that is VERY expensive. Unless you have lots of cash lying around, you’ll end up putting sheetrock over the plaster walls instead, and then it’s adios plaster walls. Old houses are a money-pit. That’s why they get torn down and replaced.

I live in a almost 100 year old home with plaster walls and last time we had a repair is was not only as Wolf says “VERY” expensive the guy (an Italian American that I guess was pushing 80) who did the work asked if we had any other plaster in the house that needed repair and said that even though people like me living in expensive Bay Area homes pay top dollar for repairs and he has paid the people that worked for him in the past top dollar he can’t find any young people that want to do plaster work to work for him to give the business to when he soon retires.

I like my new efficient build with a $43/month energy bill too much to go back to an old house.

Building anything in socal or any-coastal-cal is like shutting yourself in the foot.

Powell is a bufoon

For past errors, especially the pandemic panic? Probably, yes.

Currently, not as much.

“Sorry we ruined the economy and your ability to provide shelter and feed your family. But, we are trying to fix it”

Powell deserves the hate.

He hasn’t ruined the economy. That implies he’d ruined it for everyone. The economy is doing great for the rich who are the people that matter.

Is he a buffoon in your view because he hasnt lower rates ?

Is it possible that the 5 years of 3% mrtg rates is the reason why house prices are so unrealistic now ? Lowering rates would support current prices, is that what is needed ?

6 or 7% 30 year fixed rates seem about right to me. Many people will be hurt because they bought to high, In my little town, the town has become unviable in the long run because the prices are so high that only people bringing outside money can buy. A regular family will find it very difficult. We can see it in the demographics. It’s growing older. Enrollments in the elementary school are down 20%. The people working in the grocery store are temps imported from Serbia or other places living in company, barracks like housing.

It’s going to take a decade of rates at these levels to bring the economy back into balance. Of course that will never happen. Politics will eventually force rates down – at least those rates the FED can control/influence. And surprise, that will make the imbalances worse not better….

He’s a buffoon for his actions in 2021, in my opinion.

Declining population is going to be the norm in a lot of places. Anecdotally, I’ve got several kids but half of my siblings don’t and are unlikely to at this point. Cost has been a major factor for several of them (large, expensive metro areas).

In 2020 the US Census Bureau reported

18.4 million under 5, 20.1 million 5-9, vs

22.3 million between 25-29 and ~21.3 million for 60-64 year olds.

~17% drop in twenty five years, that’s a chunk.

I know colleges talked for years about the coming enrollment cliff once Millenials all filtered through. Rural areas and small cities seem to be getting the brunt of it right now, and it’s not going to be pretty.

He’s job isn’t to make houses affordable. That’s congress, senate, and president.

Ask the party in power why housing is more expensive under their rule.

When you create the problem, it sure is your job to fix it.

Why in the world would it be, and even more so, why in any rationalization, would anyone want, the federal government to be responsible for housing prices?

Who has dealings with the government and thinks, “Yeah, I need more of that!”?

The government is in part responsible for the home price inflation with policies that subsidize mortgages, such as taxpayer guarantees on most mortgages now via Fannie Mae, Freddie Mac, the VA, Ginnie Mae, etc. It includes forbearance programs for homeowners that don’t make payments, etc. Pull these subsidies of the mortgages, and mortgage rates will rise, and home prices will fall.

Not sure how much margin the builders have to work with. A lot of it comes down to the raw land cost. If inflated (priced assuming million dollar mini mansions on each 1/4 acre), bad news. Land valuations are based on their potential use, and priced accordingly. I am sure a lot of highly priced land was sold during the past few years ( along with the inflated housing).

“Not sure how much margin the builders have to work with.”

The article tells you about Lennar’s margin. Where it was in mid-2022 (29%) and where it’s now (18%).

Powell lowering rates 50 basis points before an election was his mistake when the data suggested otherwise. Look at these markets with sky high valuations, fart coin over a billion dollars, cryptos at 3.5 trillion, meta 1.8 trillion (a company that pins neighbor against neighbor), etc. He needs to pop the funny money markets as it is changing the behavior of the workforce (prime aged males) and how they view the necessity of work. He needed to do a Greenspan with a suprise rate hike and talk the wealth effect. Pop the markets irrational behavior leaving a lasting bad taste in their mouth. Then rates could be lowered without a doubt and have a reset. This country has enormous challenges especially regarding rare earths that will require enormous capital to fix. Yet even the institutions now chase momentum misallocating capital chasing fart coin.

Market is up 300 points at open when the commerce department just reported the economy shrank in Q1. Trump’s tariff pause is coming to an end. Global chaos and country’s were just lobbing missiles at each other.

And somehow everything just keeps going up and to the right like the party will never end.

“Powell lowering rates 50 basis points before an election was his mistake when the data suggested otherwise.”

That’s revisionist. The data at the time before the FOMC meeting showed a tanking labor market, and I wrote about it. The thing is, the tanking labor market data was revised substantially higher in October after the FOMC meeting, and the problem went away, so when we look at the revised data today, it doesn’t look that bad, but it DID look bad at the time they made their decision.

Here is the nonfarm payrolls data as of Sep 6, 2024 through August payrolls, just before the meeting. This is what they saw:

https://wolfstreet.com/2024/09/06/the-fed-has-room-to-cut-rates-are-high-relative-to-inflation-and-job-growth-could-use-some-juicing-up-to-maintain-momentum/

And then in October — AFTER the FOMC meeting — came the upward revision, and it came with a bunch of other upward revisions, and I wrote this article:

https://wolfstreet.com/2024/10/04/ok-forget-it-false-alarm-labor-market-is-fine-bad-stuff-last-month-was-revised-away-wages-jumped-no-more-rate-cuts-needed/

With this chart to show the original data (red) and the revised data plus September (blue):

Do they have their own mortgage arm so they can buy it down still borrowing short and going long on mortgage and contributing to earnings? I would guess if including WIP backlog the numbers could be higher depending on states of completion…

“Do they have their own mortgage arm so they can buy it down…”

Yes, they all have their own mortgage origination divisions. They don’t disclose exactly how they do and hedge the buydowns. That’s considered a trade secret. But when DR Horton’s buydown hedges blew up in late 2023, it had to disclose the damage (a big write-off), and so it had to disclose a little bit about how it was doing that with forward contracts.

The rest of your comment appears to be tangled-up nonsense.

Where can I read about this 2023 Dr Horton hedging stuff ? Sounds like fun .

https://wolfstreet.com/2024/01/24/d-r-horton-sheds-some-light-on-the-massive-costs-of-mortgage-rate-buydowns-as-a-hedge-went-awry-stock-tanks/

Yes, all stages of completion includes WIP…

Talking to the supt in charge of a new house on the lot across the street recently, in saintly part of TPA bay area, I was told the house cost approx. $200/SF to build, (2.700SF) The lot cost $300K including demo of old stuff. House sold day it was listed, day after Milton, $1.3MM. Not in flooded area.

Supt. also said they had 60 houses under construction, most sold before started…

Nicely built top to bottom BTW.

Custom homes are still selling in the exurbs of Minnesota as well. It’s been a few years since I’ve set foot in a Lennar/Pulte/DRH development, but those guys charge a lot for what you get. I can’t say I feel to sorry for their decreasing profit margins. They’re simply approaching their actual value.

Warning: rough estimates ahead.

South Census region had about 111 million resident population in 2007, when there were about 290,000 new homes for sale (eyeballed estimates from the line plot).

That’s about 0.0026 new houses for sale per resident.

2024 population estimate was about 133 million, with 311,000 new houses currently for sale.

That’s about 0.0023 new houses for sale per resident.

Wow, I didn’t realize we’re already this close on a per-capita basis to the catastrophic inventory blowup at the peak (2007) of the Housing Bust in the South. I thought we had a little more leeway on a per-capita basis.

Will be interesting to see how far Texas and Florida fall, and how much the contagion spreads to other states in the South region.

Household size in the south has likely decreased during that period which offsets the seemingly high number of homes per capita compared to historical averages

Rent now or be priced in forever

Buy now or be even worse off?

Midwest graph looks right.

Out here in my little slice of flyover, we are

still back logged with work. Large % of the

work is new construction.

I would say it feels more like a “normal” year.

The existing home work is noticeably down.

tom,

Pretty much the same here in the western suburbs of Chicago.

IIRC prices out here did NOT zoom up to the stratosphere. So – anecdotally – they seem to be holding.

Not really sure if that is actually correct or not. Obviously … YMMV

Sellers with sub 3% mortgage are probably doing ok in cities with good jobs. They can wait for the FED to manipulate 10Y rates to near zero, which they will likely do in 1-3 years. Then, they’ll sell for the 2022 price or even more.

Even if the sellers lose their job, they have renters to work hard for them & pay mortgage. Nothing short of catastrophic job losses can fix the housing market.

Meanwhile, the rest of us can work harder, earn raises only to find it meant nothing because of the latest round of (inevitable) QE.

I think the fed is going to have a hard time selling another round of QE without potentially raising inflation expectations. It could backfire.

“…because of the latest round of (inevitable) QE.”

I’ve had QE mongers here day-in and day-out ever since the Fed ended QE over three years ago. These manipulative BS comments get really old if you have to look at them every day, but you don’t have to since I delete them now, much like I delete other manipulative BS.

Still drunken real estate sailors in my Seattle hood. There’s a house boat for sale for them. It’s about 1800 sq ft and only 5 mil🤣

It’s not what they want for it, it’s what they get for it, that matters. If they can even sell it. Only goofballs get excited about asking prices seen on the internet.

Friends listed too late, boulder home asking price 3.1M, sold for 2.35M.

Asking price is always a useless metric.

“Only goofballs get excited about asking prices seen on the internet.”

I love this website. Thanks Wolf

I wonder if my QE comments qualify. I don’t think that it should happen – I didn’t even think the last two rounds should have happened despite my benefitting from it. But I think it will happen.

MussSyke

I replied to your comment that started out with “Delete this comment (maybe read it first)…”, which you posted yesterday, addressed to me, under the Fed article of June 18. My long reply explains this to you. And it explains a lot of other things that you brought up.

Many people have never put away their QE hats — and many of the same people are always comfortable wearing recession hats — regardless of which way the wind blows.

It was pretty clear that the Biden admin didn’t want a recession on their watch, so we e fed up with fairly dramatic fiscal and monetary stimulus.

Those policy efforts created an awkward equilibrium that basically held together, if you ignored the deficit.

Although the new admin admonished prior policies, they are fully embracing Bidenomics, and adding to the deficit — but also, laying clear groundwork for QE-like stimulus, in terms of wanting to implement a lower Fed fund rate.

Apparently, cutting taxes is stealth QE?

Within that framework, it’s easy to wear QE and Recession hats and wear sunglasses:

“ Reports indicated that President Trump is considering announcing his nominee for the next Fed Chair as early as September or October, positioning a “shadow” chairperson who is likely to be more accommodative to the looser financial conditions that Trump advocates”

Don’t Jinx it Wolf. We are always just one bank failure away and the CRE market is still mess…

Manipulative BS. The Fed continued QT just fine at a pace of $90 billion a month when the banks blew up in March-April 2023. All it did was provide temporary liquidity to the FDIC to bail out depositors, and to the banks that were struggling with mini-runs. That liquidity was then quickly drained back out. Throughout, QT continued at $90 billion a month.

That’s the new model, which is the same as the old pre-QE model: provide short-term liquidity to banks when they need it. The Fed has revived its Standing Repo Facility to support this effort. QE (= rapidly increasing securities holdings) is likely dead.

This is why I delete this revisionist manipulative BS and block commenters that abuse my site to spread it.

Manipulative BS is what I would call the valuations of CRE currently on the books at many banks.

I appreciate your cut and dry articles. I sometimes have trouble wrapping my mind around some of the concepts of policy, QT/QE, bond yield stuff, but that is a me problem.

I suppose that is why I do not comment on things of that nature.

I just attempt to over simplify your info so that I can understand it, and maybe it can assist me in making some halfway intelligent financial decisions in my life.

Either way, it has been helpful…..

just sayin’

re “Nothing short of catastrophic job losses can fix the housing market.”

Lending/investing by the DFIs (deposit taking, money creating institutions), expands both the volume and the velocity of new money. I.e., lending/investing by the DFIs is inflationary.

Lending/investing by the NBFIs (nonbanks) increases the turnover of existing deposits (a transfer of ownership), within the commercial banking system. I.e., lending/investing by the NBFIs is non-inflationary (other things equal).

The correct solution to stagflation is the 1966 Interest Rate Adjustment Act, i.e., drive the banks gradually out of the savings business as lowering Reg. Q ceilings for the commercial banks did (which doesn’t shrink the size of the payment’s system), lowering deposit rates, while draining bank reserves.

This action raises the real interest rate for saver-holders outside the payment’s system, by lowering inflation, while making the banking system as a whole more profitable.

Existing home sellers need to get the hint. Only slightly less delusional over here.

Great article. Thoroughly enjoyed it. Question Were the obese profit margins really in Q2 2024 or is the year a typo?

Typo, thanks, 2022.

” the obese profit margins”

Kinda curious about the evolution of true (non-GAAP) profit margins during the long night of ZIRP from 2002-2022.

Kinda hard to believe that builders could construct homes at a profit at $160k in 2002…but “had to” price ’em (net) at $380k in 2025 to turn a profit…given 25 years of technological advance and the insanely faster dissemination of knowledge (including construction knowledge).

I wonder if Lennar is going to build through ready lot inventory and projects, then pullback and “rightsize”. And the winners of 2007-8 bought huge tracts of land from the bankrupt. Last boomer turns 65 in 2029. That cliff is approaching as well.

But it’s going to be a slower, more normal crash than the last time. The delusion helped by the pandemic rates will allow immense extend and pretend by sellers in the private sector.

I have now watched some realtors in the area start getting listings for nice property in 10-15% under the pretender stale listings for quick sales. I do notice the 20% down monthly nut is still pretty high. All I can say is that problem property is going to be a lot cheaper than it has been with the flipping flop up on deck next.

“The delusion helped by the pandemic rates will allow immense extend and pretend by sellers in the private sector.”

IDK, there is a reason why loan contracts exist – and it ain’t so lenders can give away something for nothing.

I’ll admit that loan “amend and extend” is rampant, amazingly pushing back seemingly doom-laden maturity walls over and over…but I’m fairly sure that lenders extract their incremental pound of flesh at every loan workout session.

Buying in one of these communities is a big risk. If you have to sell for whatever reason, then you have to compete with builder incentives- good luck!

Also, if I were going to buy crappy new construction, might as well be actually new, and not five years old, coated in someone else’s dog hair and polluted by their scent.

This seems a lot like the discussion about tariffs in that- The company / exporter will pay the tariff (excluding illegal collusion practices) because some other company is either manufacturing in a tariff-free environment or is willing to pay the cost of the tariff to hold up sales… eating into whatever profit(s).

This seems much the same- eat some of those fat profits and lose whatever share value or don’t sell them. They can try and reduce quality costs but at some point, people go, ‘that’s walmart-level crap’ and walk and they still won’t get sold.

You know what is really Walmart level crap? All that wire shelving they put in “oversized” closets in new construction.

God, I hate that. Just give me a blank room and I’ll figure something out, even if I don’t have a table saw (which I do).

Depends on where it is locale-wise, MS. In the South and other areas of persistent high humidity the air-circulation in-over-around-and-about closet space is a noticeable factor to be considered. Even with AC.

walmart-level crap is them attempting to sell you a warranty at the checkout counter.

We need to create a sort of “bedraggled housing index”.

“Federal Reserve Governor Christopher Waller believes the central bank can lower interest rates as early as July1”

Waller, Williams, and Logan seem to be agreed. They “believe the Fed can keep unloading bonds even when officials cut interest rates at some future date.”

Waller dissented from the decision at the March meeting to slow the Treasury QT to $5 billion a month, from $25 billion a month. He wanted to maintain the $25 billion a month pace.

The rate cuts in 2024 have shown that there is unanimous agreement at the FOMC that rate cuts are separate from QT, and are unrelated to QT. Rate cuts are now considered classic monetary policy, and QT is to “normalize” the balance sheet and ret rid of the MBS.

MW: Trump takes aim at Powell — and sends the U.S. dollar tumbling to a 3-year low

Total reserves 2023-03-01 3258.4 are on par with total reserves 2025-05-01 3262.9. This figure is down from 2024-02-01 3567.7.

So far, the FED’s maintained a tight money policy.

Reserves will drop by several hundred billion dollars within a few months of the debt ceiling getting lifted, as the TGA will be replenished via lots of new T-bill issuance, and that will drain some of the reserves. And it will drain ON RRPs back down to low levels.

Howdy Youngins. Flounder said, ” Oh Boy is this great “. You bet it is Lone Wolf. Some of US saw what was coming in housing bust 1 and 2. Some of US prosper well in the RE business no matter what Govern ment does. Looks like buying RE in a few years will be a good investment. AGAIN

Sell at the right time and buy at the right time…..

RE money is always made during the bad times. Still have a condo in our portfolio if sold today is a 9x, got it for 30K in the last bad vegas market.

I’m still laughing at the buyers of two of our properties one in SF and in Colorado where they overpaid so badly with zero contingencies. Like the perfect storm of fools with $ and zero sense.

Howdy Kracow. Saw lots of good RE companies bite the dust during Housing bust 1…Also saw lots of good RE companies make $$$$ too.

Just have to know what you are doing. The RE flippers that bought and just refliped without adding any value to a property, lost big time…..

Is there any data on if builders are changing their product mix to sell at cheaper prices and keep costs down?

The mass-market builders are building smaller homes on smaller lots to meet the price points where demand is. They’re talking about it, and you can see it in their financial statements.

But note that these smaller homes are still MUCH larger than the 1,000-1,200 SF homes commonly built the 1940s and 1950s, many of which have been torn down and replaced by larger homes by now.

On a related note, the s&p 500 is four standard deviations above its long-term trend. This is mind-bogglingly overvalued historically. Let’s assume that both stocks and real estate will return to their long-term trend as is often the case otherwise it wouldn’t be a long-term trend. Would this be a major blow to the economy or could the government paper over it?

Do your calculations take into account the value of the dollar going down due to inflation? Gold is over $3000 an oz now….

They can compile a list of every home for sale in a given month. That list can be cross-matched against the debt owed on each listed property to gauge how much equity is in each home. That will yield a percentage amount that a seller individually (and then sellers in the aggregate) can afford to discount off the asking price. And it will reveal how much flexibility exists in the market over all, on a relative basis. Burgeoning inventory with no room to negotiate would be a worse signal than sellers swimming in equity.