No longer the cleanest dirty shirt.

By Wolf Richter for WOLF STREET.

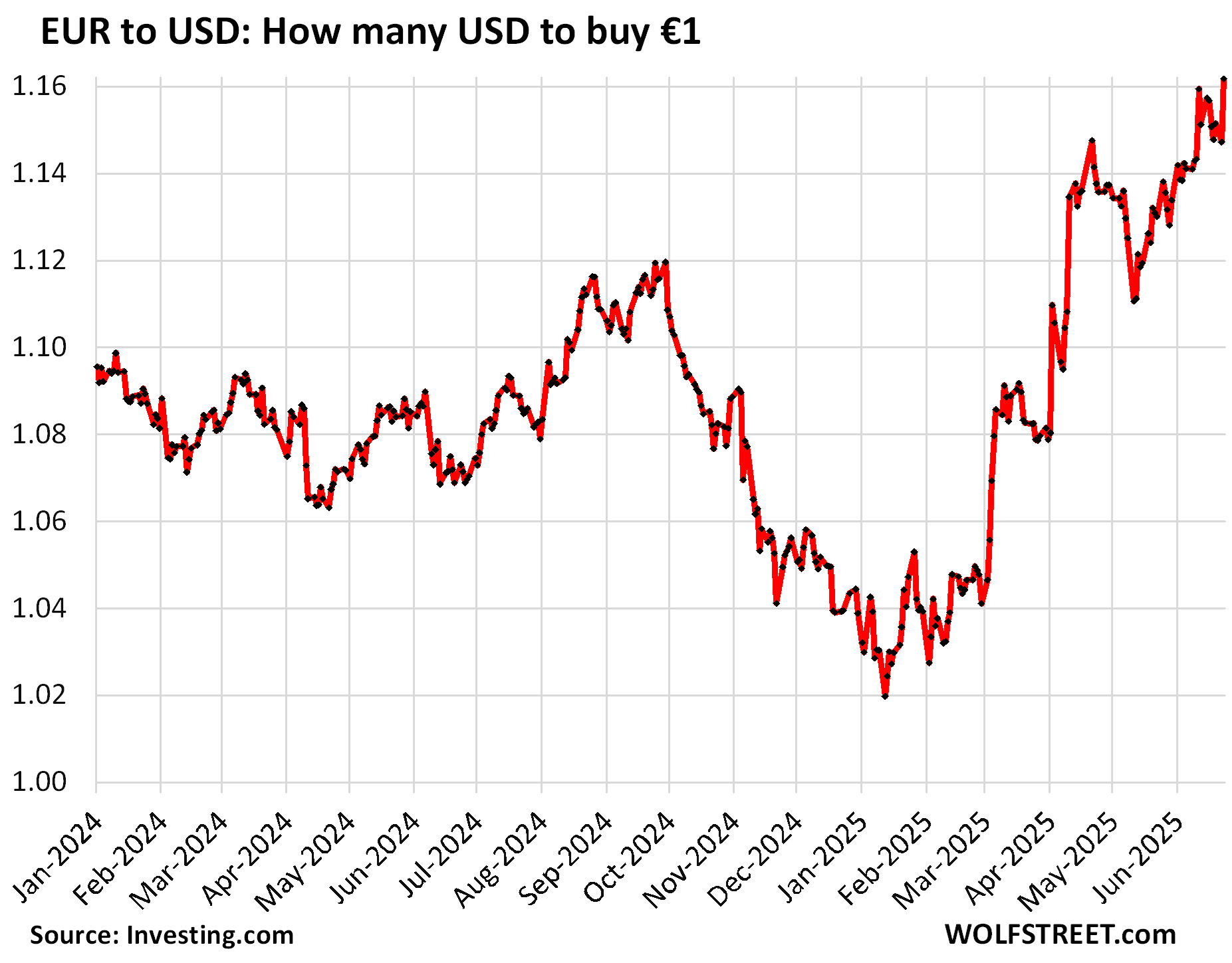

The somewhat bedraggled US dollar lost more ground against the euro today. It now takes 1.16 USD to buy 1.00 EUR, putting the dollar at the lowest level against the euro since November 2021.

In early January, after the euro had fallen against the USD for three months, there was talk that the euro would fall below parity with the dollar. That didn’t happen. After the euro dropped to $1.02, it bounced off and then began to soar.

Over the longer term, as we’ll see in a moment, the EUR/USD exchange rate just moved back into the middle of the long-term range. One thing the Euro Area is doing right: The ECB has accelerated its QT this year and has already shed €3 trillion in QE bonds and QE loans, even as the Fed has decelerated its QT this year after shedding only $2.3 trillion.

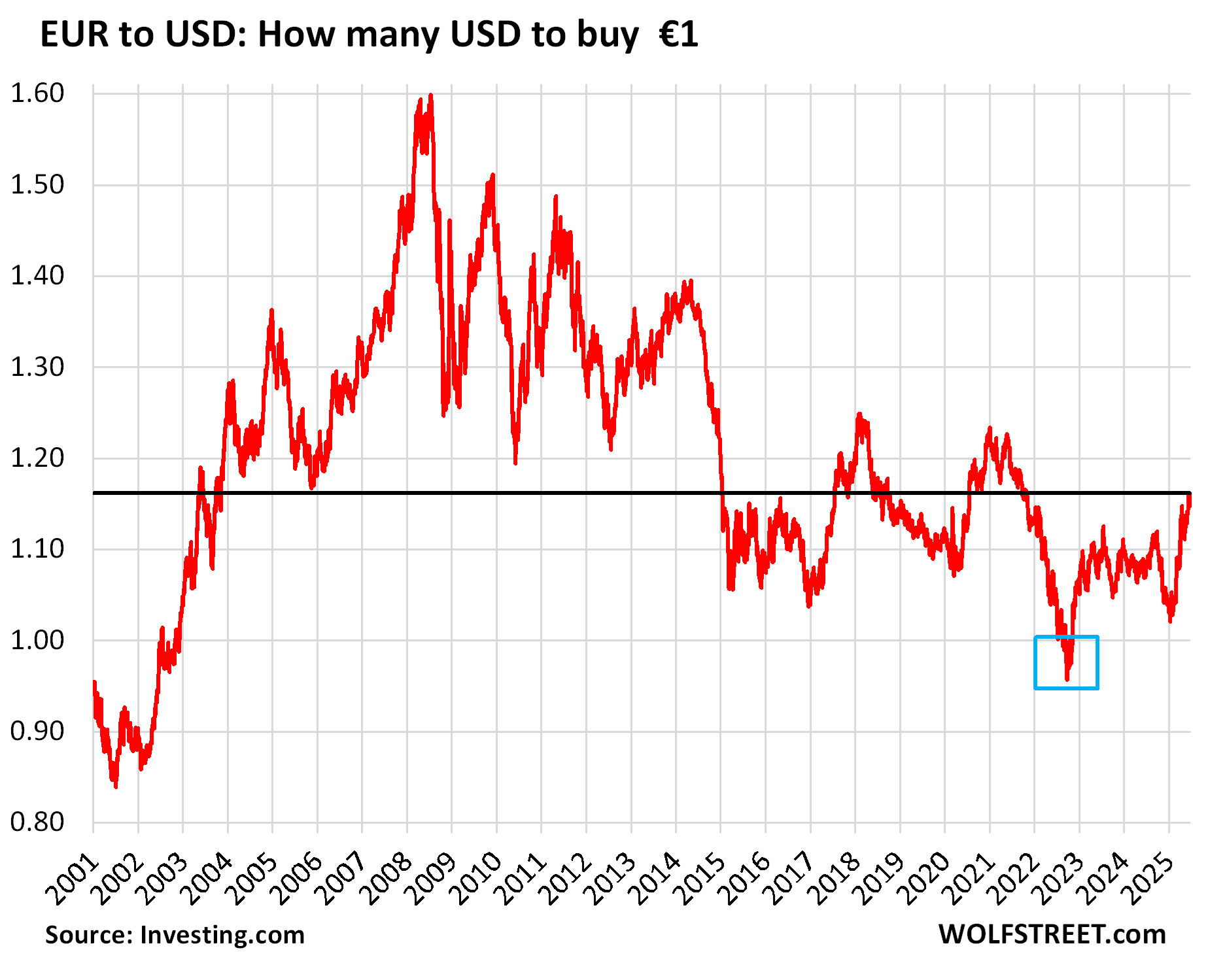

The dollar and euro have been a very volatile currency pair. When the euro was still young in the early 2000s, it had a very hard time. But then by 2005, the financial system in the US was starting to show cracks which opened into a full-blown Financial Crisis by 2008, which caused the USD to plunge against the euro.

But then the Euro Area went through the Euro Debt Crisis and, amid the central-bank shenanigans it took to resolve it, the euro plunged against the USD. So it’s one crisis or another, or no crisis, and currencies react in wild ways.

The time for Americans to go to the Euro Area and enjoy good deals was in late 2022, when the euro fell below parity (blue box in the chart below), and the USD bought lots of good deals.

Now not so much. That €1 item cost USians about $0.98 in October 2022. Now that €1 item costs $1.16. So over this period, the somewhat bedraggled USD has lost about 18% against the euro and is back where it had been in September 2021.

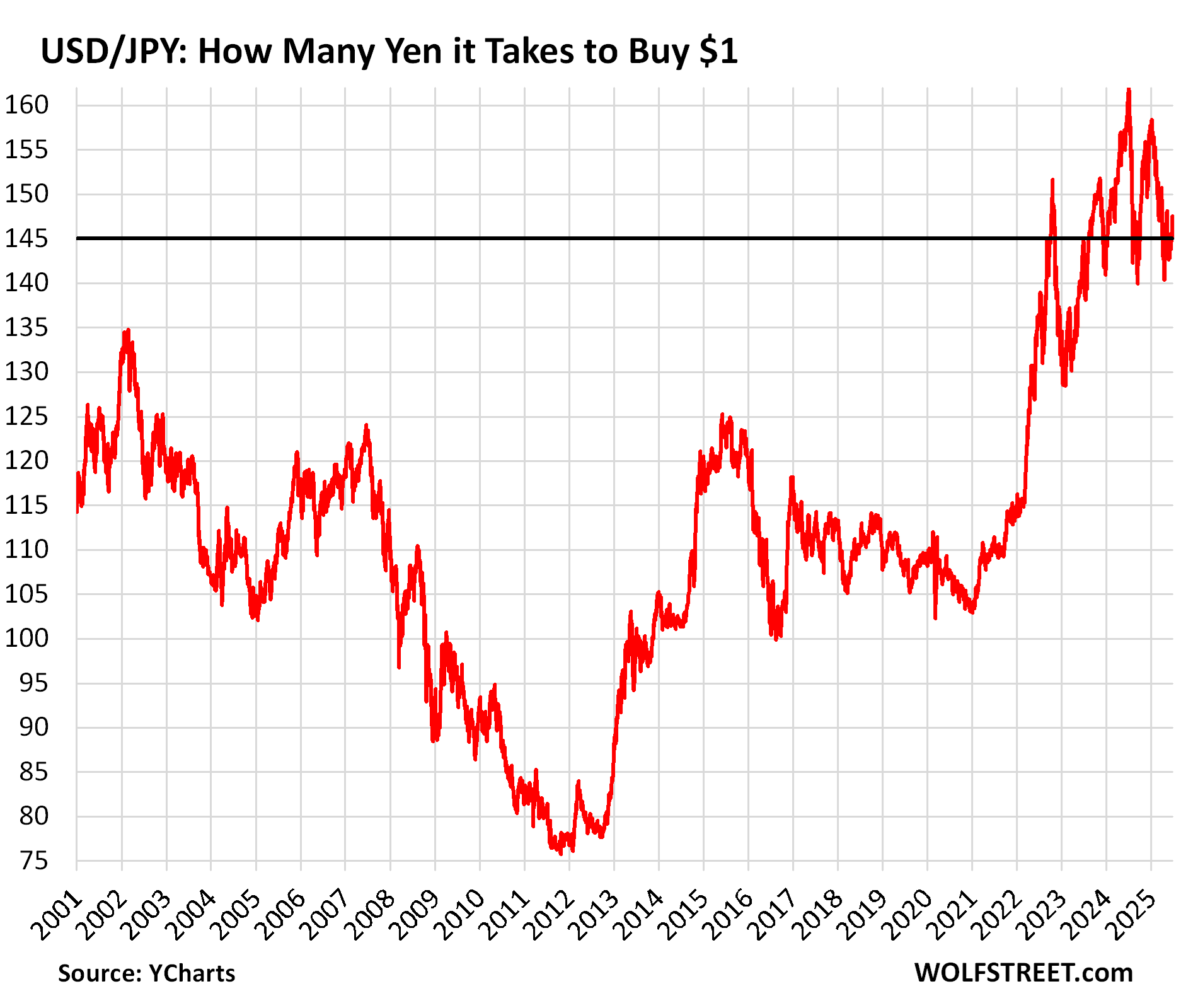

The Yen [JPY] had collapsed by roughly 50% against the USD between 2012 and mid-2024, some of it fast and furious, some of it in slow-motion, with lots of partial recoveries in between, falling from 80 yen to the dollar in 2012 – when it was exceptionally strong – to 160 yen to the dollar in July 2024.

The collapse of the yen halted and partially reversed after major interventions by Japan’s government in 2023 and 2024, plus some baby rate hikes by the Bank of Japan and the start of QT last year, which the BOJ has accelerated this year.

Currently the dollar trades at around 145 yen, which, prior to 2022, had been a multidecade low for the yen.

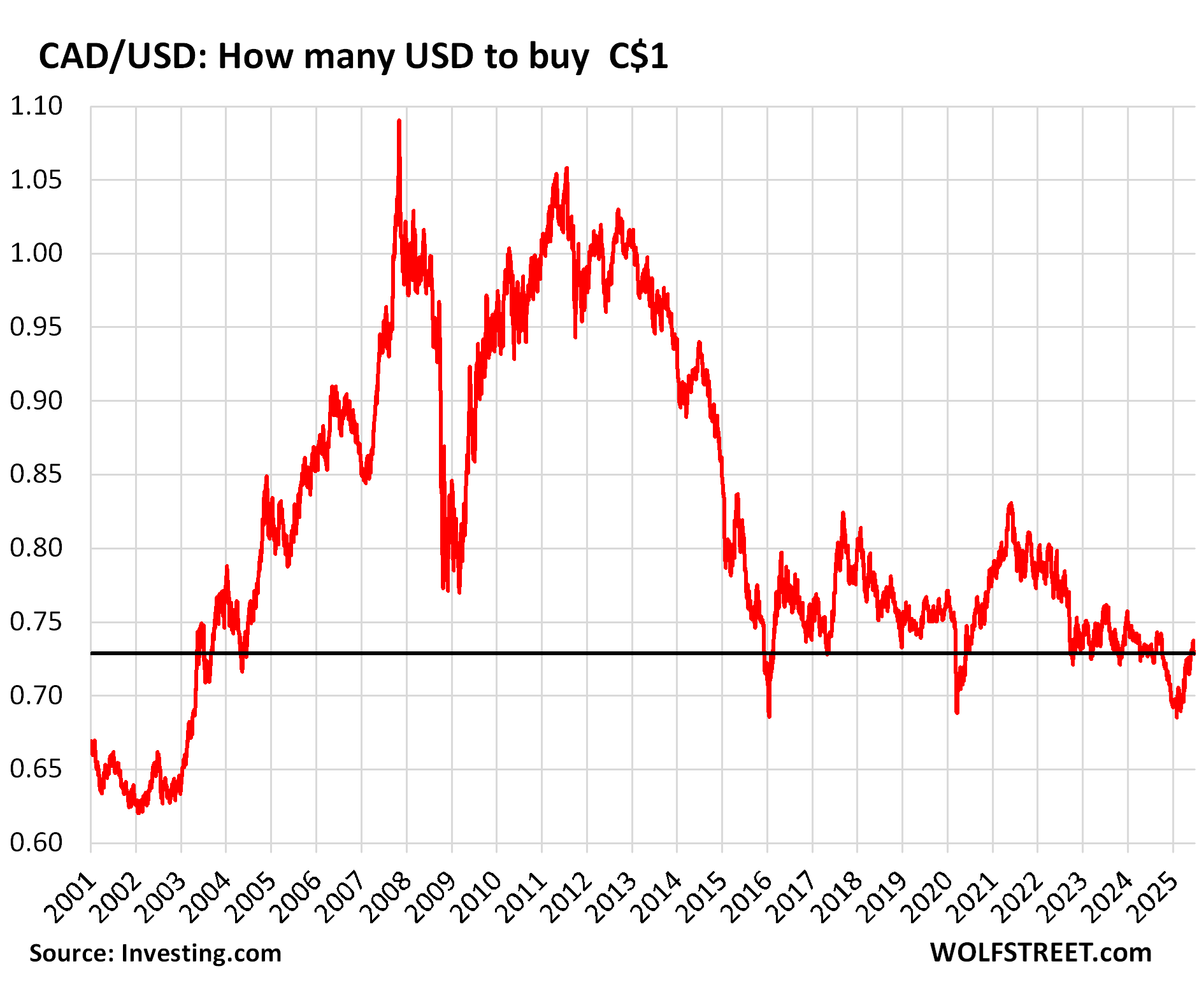

The Canadian dollar [CAD] staged a mini-recovery this year against the USD, after trading as low as 69 US cents in early January. But it is still wallowing around at low levels against the USD, which is obviously where Canadian authorities like it to be – at low levels against the USD – because it makes Canadian exports to the US more competitive with Mexican exports to the US.

Currently, it is trading at 72.8 US cents, so not exactly a big recovery against the USD.

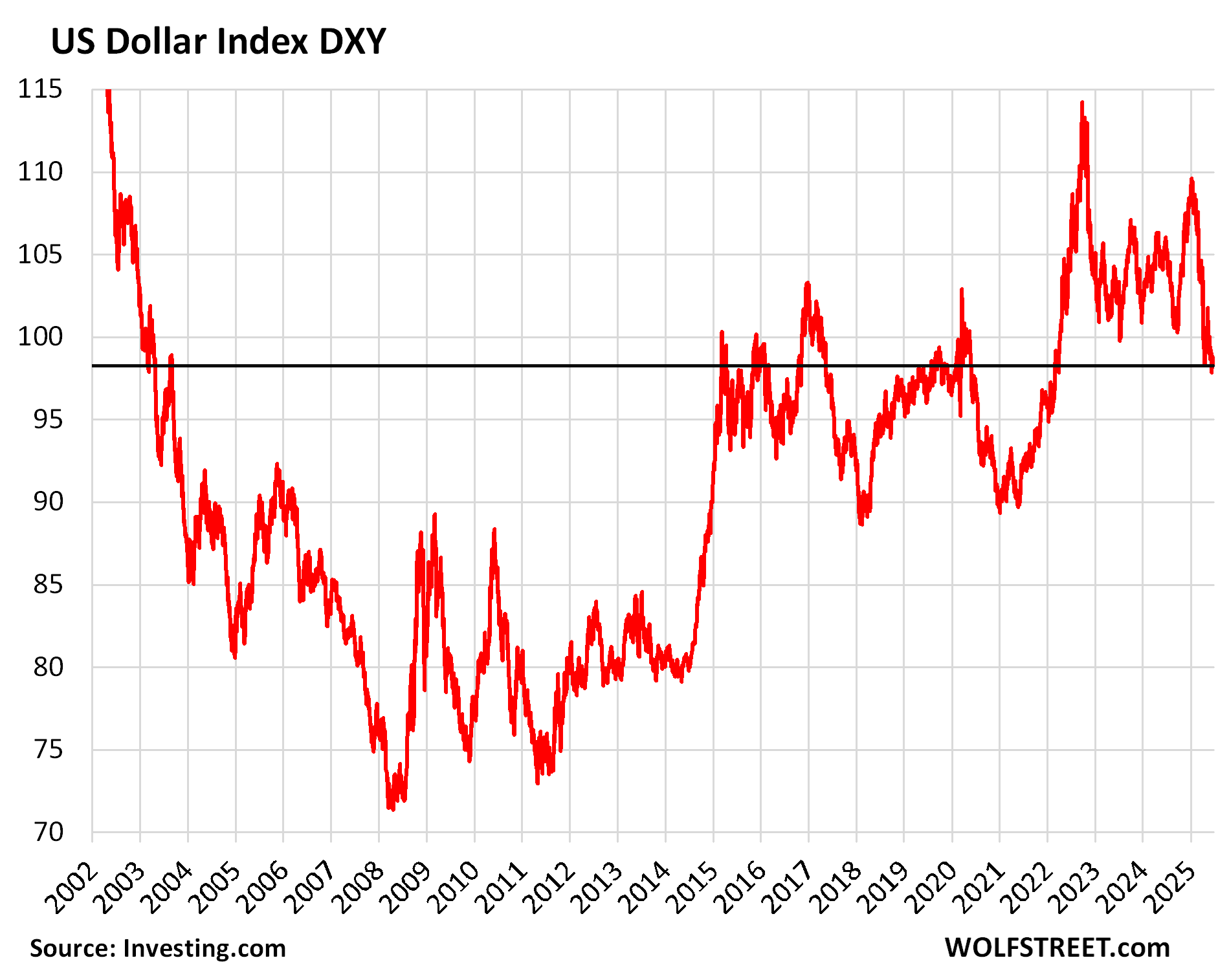

The DXY Dollar Index is dominated by the euro and the yen, but also includes in its basket four other currencies: British Pound Sterling, Canadian Dollar, Swedish Krona, and Swiss Franc. Canada is a big trading partner of the US, but the other three countries not so much. The currencies of countries that matter much more to US trade, such as China, Mexico, South Korea, Taiwan, etc., are not included in the DXY.

The DXY sits at 98.0 currently, after quite a drop from 110 in January 2025 and from 115 in October 2022. That 98-range is the lowest since April 2022. But it’s in the middle of the range over the past decade and far higher than in 2004 to 2014, when it had wallowed around in the mud sinking even below 75 for some periods during the Financial Crisis.

The DXY was set at 100 in 1973 when the data begins. So today’s reading is pretty close to 1973, but a lot has changed since then, including that several of the European currencies in the basket have been replaced by the euro, and that US imports shifted from Europe and Japan to China and Mexico, and that the relatively balanced trade in the 1970s deteriorated year after year and became what is now this mega-trade deficit in manufactured goods that the US has with the rest of the world.

When soft currencies are included in the basket…

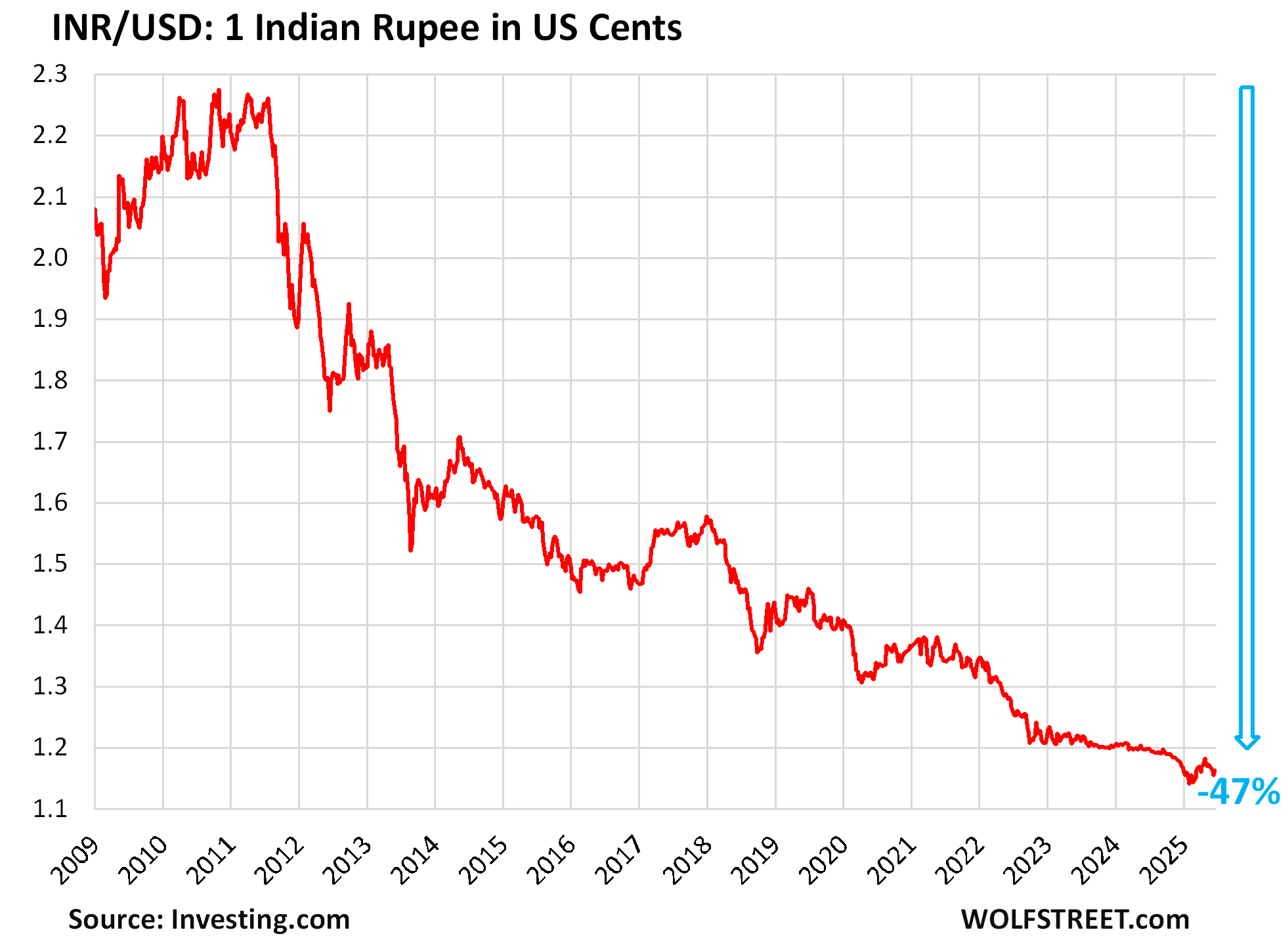

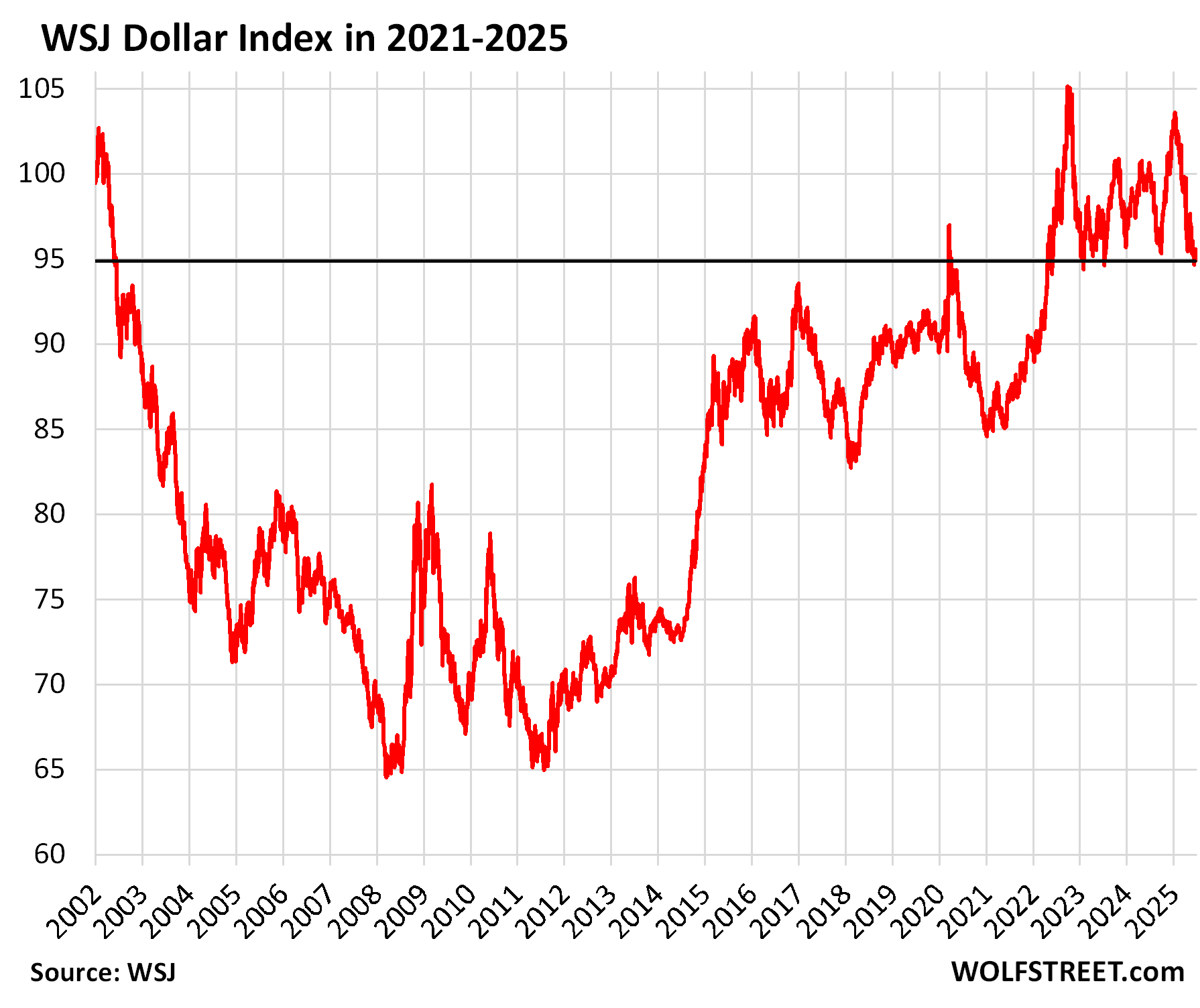

The WSJ Dollar Index is far broader. Its currency basket includes the six currencies of the DXY, plus, among many others, the Chinese RMB, Mexican peso, South Korean won, New Taiwan dollar, and Indian rupee. Each currency pair in the basket is weighted based on their share of the volume of global foreign exchange transactions. And some of those currencies keep skittering and sliding down that very slippery slope, such as the Indian rupee.

The Indian rupee [INR] has dropped to 1.16 US cents, down about 47% from the range in 2010. So this is in line with the collapse of the yen that had set the world atwitter, except for the rupee, it was just the normal progression of a currency of a developing economy, and it wasn’t a big deal.

The WSJ Dollar Index, due to its larger basket of currencies that include the soft currencies of large US trading partners – currencies that have careened lower over the years – has declined by only about 8% this year, from 103 in early January to 94.9 currently.

But that 103 was a lofty level. The WSJ Dollar Index was set at 100 for June 2001, when the data begins, and the periods when the index was above 100 were brief and few.

Since 2022, the WSJ Dollar Index has dropped to about 95 several times, before bouncing off again.

In the two decades before 2022, the index pierced 95 from underneath only once briefly in March 2020.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So back to long term basically. Doesn’t a weak dollar help with the trade deficit?

Promotes exports which in turn does help reduce the deficit.

Yes, and it’s tempting for countries to try to push down their currencies to boost exports of manufactured goods. But if that gets out of control, with countries slugging at each other by trying to push down their own currencies, it’s called a Currency War. And the winner is the loser.

‘Dollar slips on Fed’s credibility concerns as euro nears 4-year high’

CNBC headline June 26

Markets do what they do because they do it. Indicating WHY they do it is mostly just headline fantasy clickbait.

The weaker the US Dollar is the more expensive that foreign goods will be in the US and with the enormous trade deficit run by the US that will result in much high prices that consumers have to pay for goods and much higher interest rates that the US government will have to pay on Treasuries as investors lose confidence in the US as a ‘safe haven.’

Uhm the weaker the dollar, the more attractive our exports as well and the trade deficit closes. You are assuming the trade deficit remains the same. It won’t and hasn’t.

Shipments have propelled Ireland, a country of 5.4 million, to the second-largest goods-trade imbalance with the U.S., behind China.

Corporate America dodging US income taxes.

No. Ireland’s import/export sector is a gigantic Tax Scam.

I’ve often wondered about the exact function of other small trade entrepots (Hong Kong, Singapore, Netherlands/Switzerland to an extent) – I don’t know if those share Ireland’s tax avoidance bona fides, but I do suspect that their outsized macro stats have more to do with the jiggery-pokery of their huge neighbors (China for HK and Singapore, Germany for the Netherlands/Switzerland) rather than any straight-forward domestic production.

Perhaps somebody in the readership could provide clarity for what is really going on in one or more of these unusual countries economically.

I’m particularly curious about HK and Singapore, since I wonder if China’s macro stats might actually be *under-reported* due to pseudo-trade being routed from China via these much smaller countries.

I bet the major component of the deficit is branded drugs.

Wait a second.

Doesn’t Apple Pay the most us corporate tax of all?

🤔

In Ireland. At the 15% corporate income tax rate in Ireland.

The following confuses me: when the US talks about tariffs in the 10-20% area, panic breaks out. When the USD moves by 10-20%, the world moves on. I remember times about 15 years ago, when the steady decline of the USD had reached a low of about 1,60 against the Euro. Just about everybody in Europe predicted that we would soon see a 2:1 exchange rate. The opposite happened. If the world functioned quite well with a USD at 1,60 against the Euro, why could that not happen again? In fact, the old theory that trade deficits can only be corrected by large devaluations might prove correct.

Tariffs are expected to sustain across multiple years, currency exchange rates are more real-time?

It didn’t.

Yes, the tariff panic was BS ginned up in the media and social media, funded by companies and stockholders that hate corporate taxes, and that’s what tariffs are. There’s nothing to panic about. Companies either pay them and keep producing overseas, or dodge them by producing in the US.

“In fact, the old theory that trade deficits can only be corrected by large devaluations might prove correct.”

That “old theory” is BS, especially in the modern world with the modern US tax code that encourages companies to shift production overseas among other reasons to avoid US income taxes. Changing the tax scenario (tariffs) does wonders to shifting production to the US. Companies are very eager to dodge taxes, and when they can dodge taxes by shifting production to the US, they will — and they’re already doing it.

Can you foresee a scenario where the USD would return to the low levels of about 15 years ago, i. e. 1,60 against the Euro or even lower? If it worked then, should it not work now?

It’s really bedraggled against gold, down over 20 % as are all other fiats.

This ^

Imports 10% index move + 10+% tariffs + financing costs of tariffs more expensive. Exporters able to pay 10% more when competing for goods. That combination could be inflationary and constrain the fed for the next year.

Why does the forex quote “CAD/USD” mean 0.728 USD/1.00 CAD rather than 1.37 CAD/USD. In other words, why is the forex symbol the reciprocal of actual ratio of US Dollars to Canadian Dollars? It seems mathematically off. What am I missing?

The “/” is a relationship symbol not division symbol. The currency pair is also written as CADUSD or CAD-USD or CAD to USD.

USD is around 40% overvalued at least, given the trade deficit, a falling dollar will ultimately be good for the US and very bad for those parts of the world that are dependent on exports to the US.

It will also be bad for those who borrow lots of money to consume and not produce, like the federal government. Maybe the bond market will finally scare Congress?

Excellent article/insghts on the dollar and associated indexes.

Moving forward, it seems as though the existential threat to the US is if lots of countries move away from the dollar in both trade resolution and reserve holdings.

Is such a scenario even possible? Wouldn’t the US exact all sorts of punishment on countries attempting to do such?

It doesn’t make any difference to the US if two other countries trade with each other using their own currencies. European countries are not trading with each other in dollars, and a lot of their trade with the rest of the world is in euros. Oil might be priced in dollars, but European countries can pay in euros for a shipment, no problem, and this has no impact on the US. They yen is a big trading currency, and the Chinese RMB is slowly becoming one. Etc. Trading in currencies are than the dollar is very wide-spread and is no threat whatsoever to the US.

The US will feel some impact when foreigners don’t want to buy US assets, such as US real estate, stocks, Treasury securities, etc. But that impact may be positive, and not an “existential threat: it just means lower asset prices and higher yields, no biggie. Home buyers are looking forward to lower prices. Investors are looking forward to higher yields and lower asset prices… buying opportunities. Maybe higher yields will finally push Congress to get serious about the budget deficit. We can probably come up with a pretty good list of why slowing the influx of foreign capital flooding the US will be long-term good for the US (though maybe not Wall Street).

Exactly right. Foreigners driving up the prices of U.S. assets is good for the people who currently own assets, not people who would like to own them. But it’s the former that call the shots.

I personally would love to see the end of foreigners buying US land and real estate. Congress should pass legislation protecting Americans.

All it took to originally dethrone the US dollar, cease it to be convertible into gold, was a communist containment deficit, our far-flung military bases and troops. We have yet to learn the lessons of the past.

The defense budget as a % of GNP has been in decline for decades with a few blips. (Its postwar peak was under JFK.) The current proposed Trump fy 2026 BASELINE defense budget (not the temp. plus-up gimmick added in) is tens of billions less than the one Biden proposed on his way out, and comparable to what Obama planned on spending. The “Trillion Dollar” defense budget is an illusion. Communist containment worked until yesterday’s primary election for Mayor of New York City.

I tried some containing back in 67-8 and it didn’t work then. What is your time range for that claim you make?

More global debt will eventually impact currencies and treasury yields. The dirty shirts will drift around in the global washing machine, but the grease and stains will be intractable.

“GDP Deflator In the Euro Area increased to 118.69 points in the first quarter of 2025 from 118.06 points in the fourth quarter of 2024”

“When the dollar depreciates, it can lead to higher import prices, which may influence the GDP deflator by increasing overall price levels in the economy”

Resetting the global economy with inflation is utterly stupid, but here we are.

“NATO allies on Wednesday agreed to more than double their defense spending target from 2% of gross domestic product to 5% by 2035, in the most decisive move from the alliance in over a decade.”

Bullish for higher yields — yippy

Yes, don’t overthink any of this. The bottom line is that risk is being repriced globally. Full FAITH and credit…

..same as it ever was. The difference is we have an egotistical, self-serving clown/puppet in the white house. Uncertainty increases risk. TINA is done, one reason gold has risen.

“Bedraggled”, wow there is a descriptive word you don’t see very often. (I’m not certain if I have ever seen it before but it has promise and deserves more usage!)

(Engage Yosemite Sam’s voice – Sam’s dragon is sneezing) · Sam: “Ya crazy, idgit, bedraggled dragon! I warned ya about lettin’ your fire get low! Now ya caught cold!”

And so, back to the real Looney Toons, not the US Dollar!

It is easy to focus on goods, but let us not forget travel and tourism – which is close to 10% of the US economy. A stronger dollar increases the number of US tourists taking vacations overseas and spending their dollars there… and foreign tourists staying home, or vacationing locally.

Would the cleanest dirty undies we are wearing come from overseas?