These are aspects the Fed is considering in setting its monetary policy; that type of discussion is part of its meeting minutes.

By Wolf Richter for WOLF STREET.

Despite the turmoil in the stock market that has been zigzagging down from dizzying and mindboggling all-time highs as all kinds of stuff is getting repriced, broad financial conditions in the credit markets remain in la-la land, or are just barely exiting la-la-land.

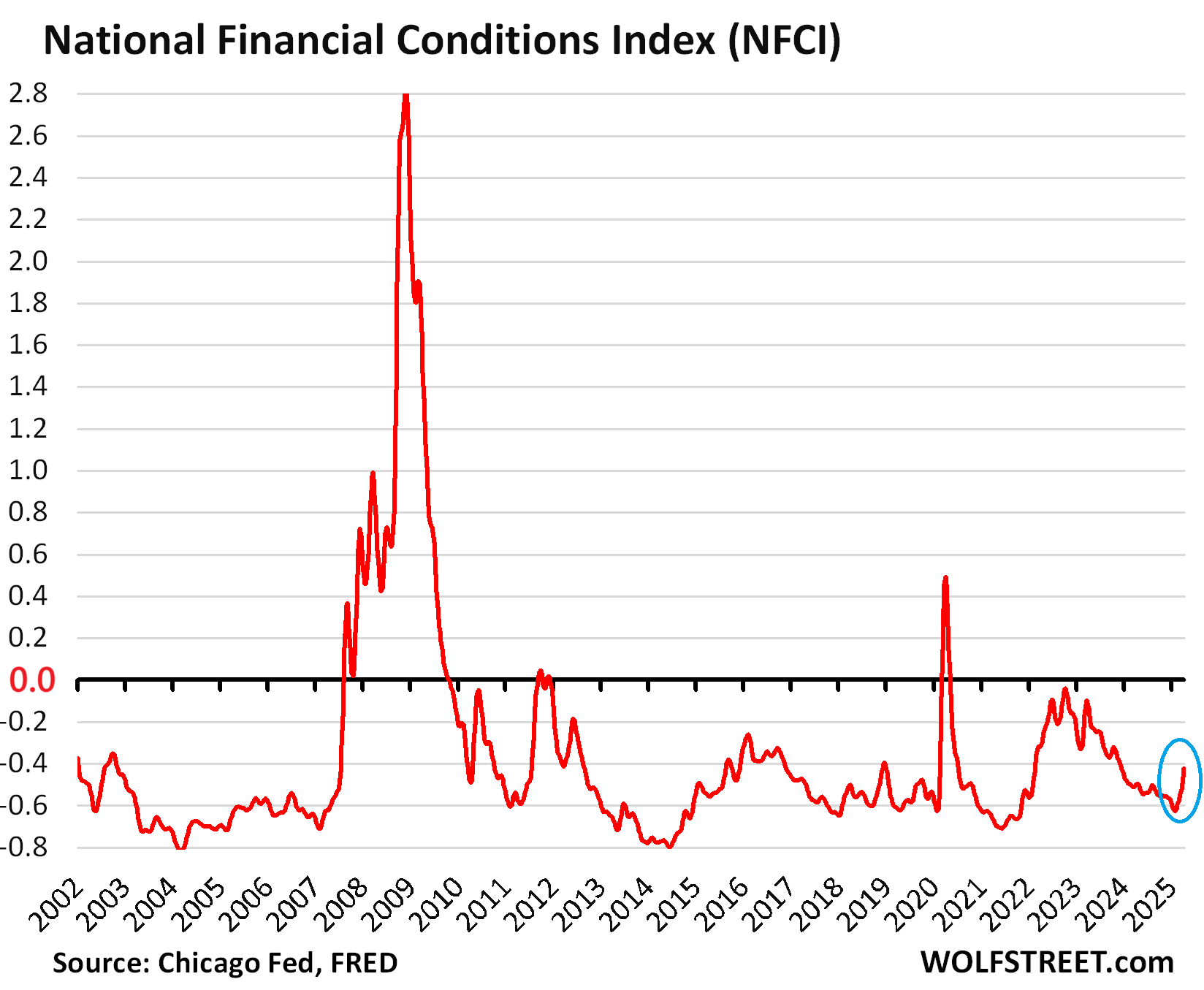

The NFCI is still in la-la-land but looking for the exit. Overall financial conditions in money markets, debt markets, and equity markets, according to the Chicago Fed’s National Financial Conditions Index which tracks over 100 data points, have tightened from ultra-loose at the end of January, to still very loose in the most recent week, when the NFCI rose to -0.42.

The average value going back to 1971 is zero, and negative values indicate looser-than-average financial conditions. The NFCI of -0.42 shows that financial conditions are still far looser than average, and looser than in the period from March 2022 through December 2023. But the looseness during the era of QE and interest-rate repression, and the looseness that ironically prevailed during much of the Fed’s tightening, is slowly fading.

The purpose of the Fed’s “tightening” – including $2.24 trillion in QT so far and higher policy rates – is tighter financial conditions that would put a damper on demand and thereby on inflation.

But the Fed’s tightening has been belittled and laughed off by many people as financial conditions loosened further, despite its tightening, after the depositor-bailouts of three regional banks that collapsed in the spring of 2023. And by November 2023, I mused: “Could it Be the Fed’s Mega-QE Created so Much Liquidity that Tightening Doesn’t Work until this Excess Gets Burned Up?”

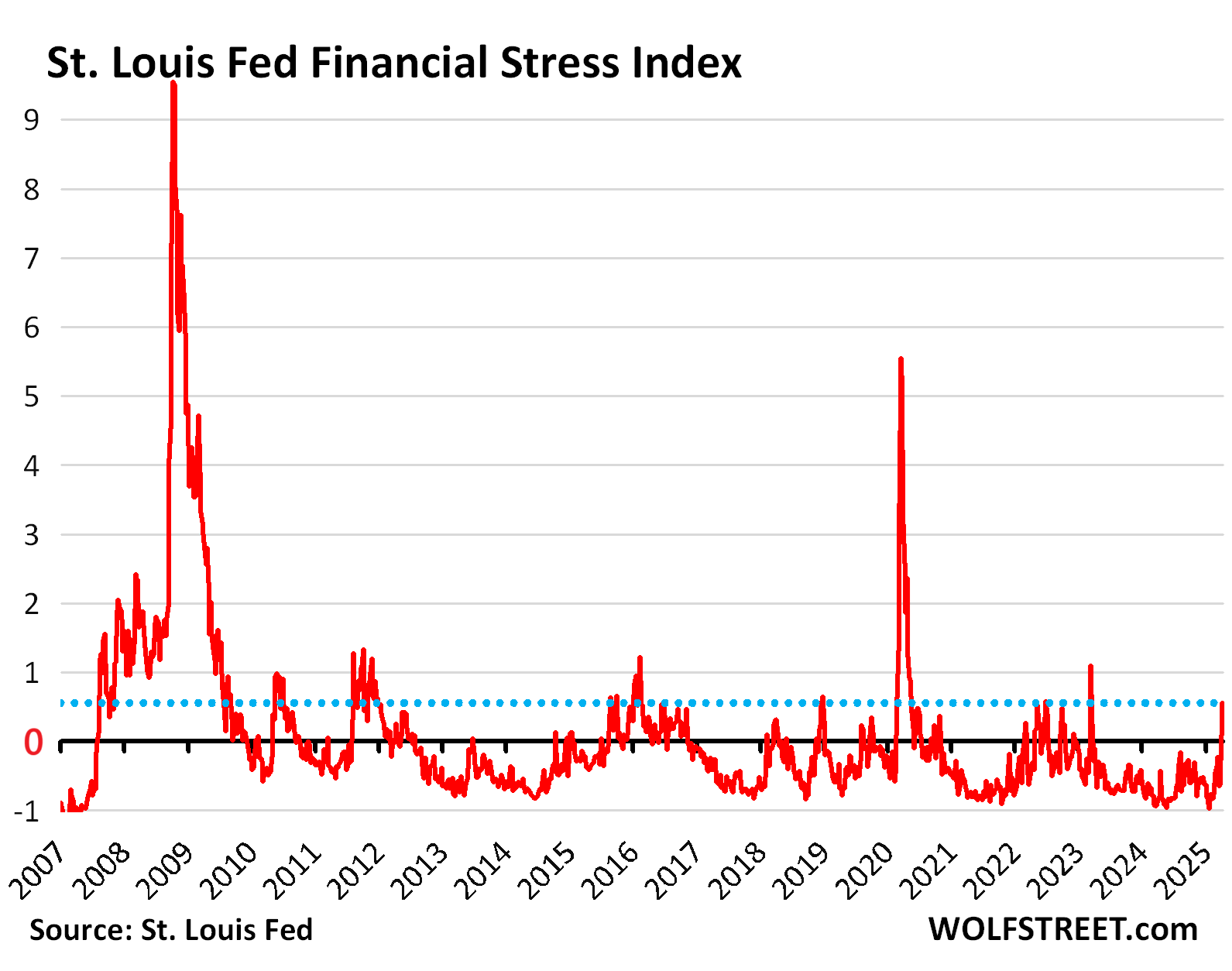

St. Louis Fed Financial Stress Index gets a little nervous. The index measures financial stress based on 18 data series from the credit markets, including seven different interest rates, six yield spreads, the Market Volatility Index (VIX), bond market indices, the S&P 500 financials index, and the TIPS-based 10-year breakeven inflation rate.

Periods of financial stress have “historically been characterized by increased volatility of asset prices, reduced market liquidity conditions, or the narrowing or widening of key interest rate spreads,” the St. Louis Fed says in describing this index.

The zero line denotes average financial stress. Negative values denote less than average financial stress. The index goes back to 1994. Over the past two weeks, the index moved into the positive for the first time since March 2023.

In the most recent week, the index rose to +0.55, about where it had been in mid-2022 and below March 2023, and far below any periods of real financial stress – March 2020 (+5.55) and October 2008 after Lehman Brothers filed for bankruptcy (+9.5).

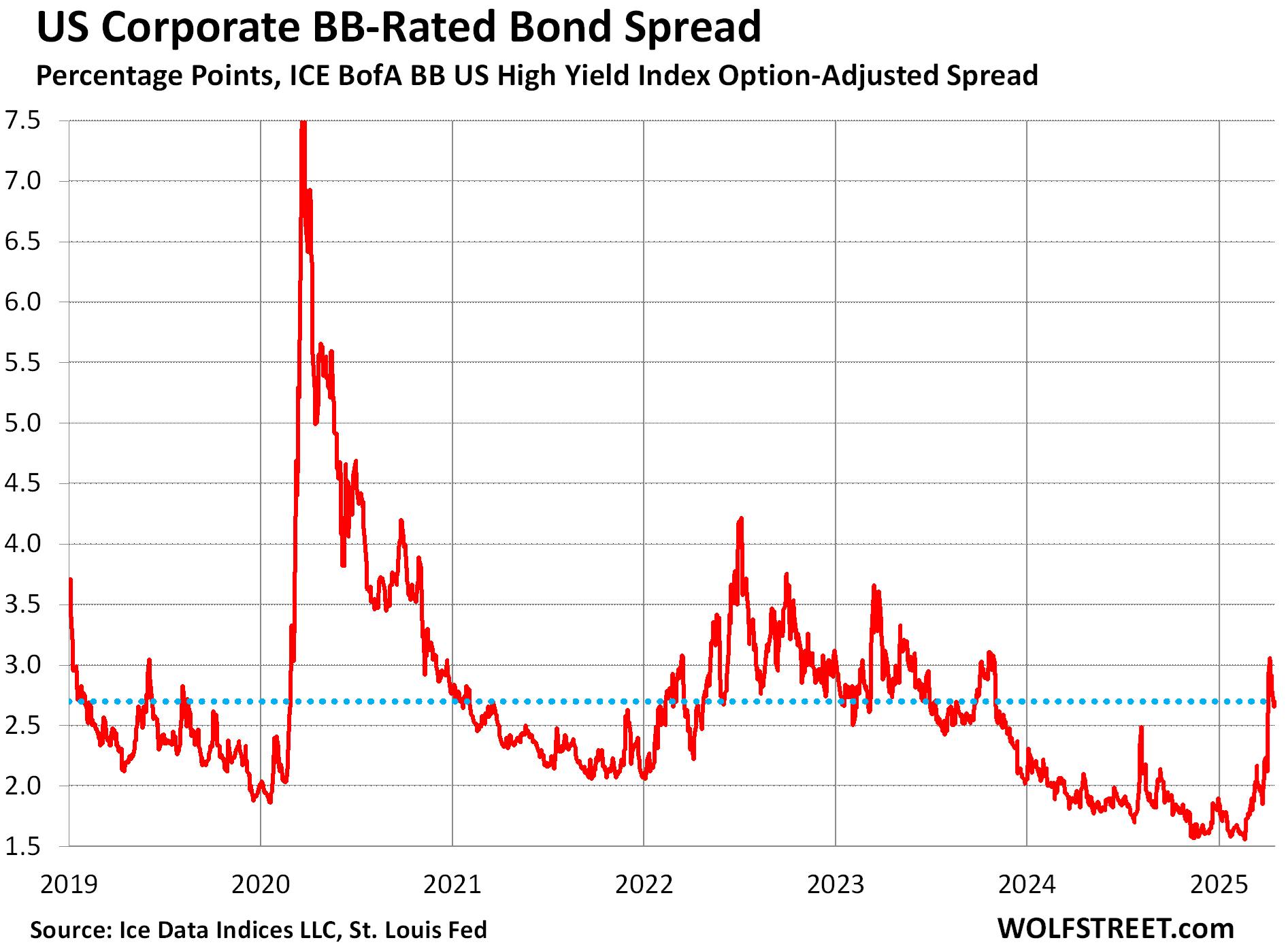

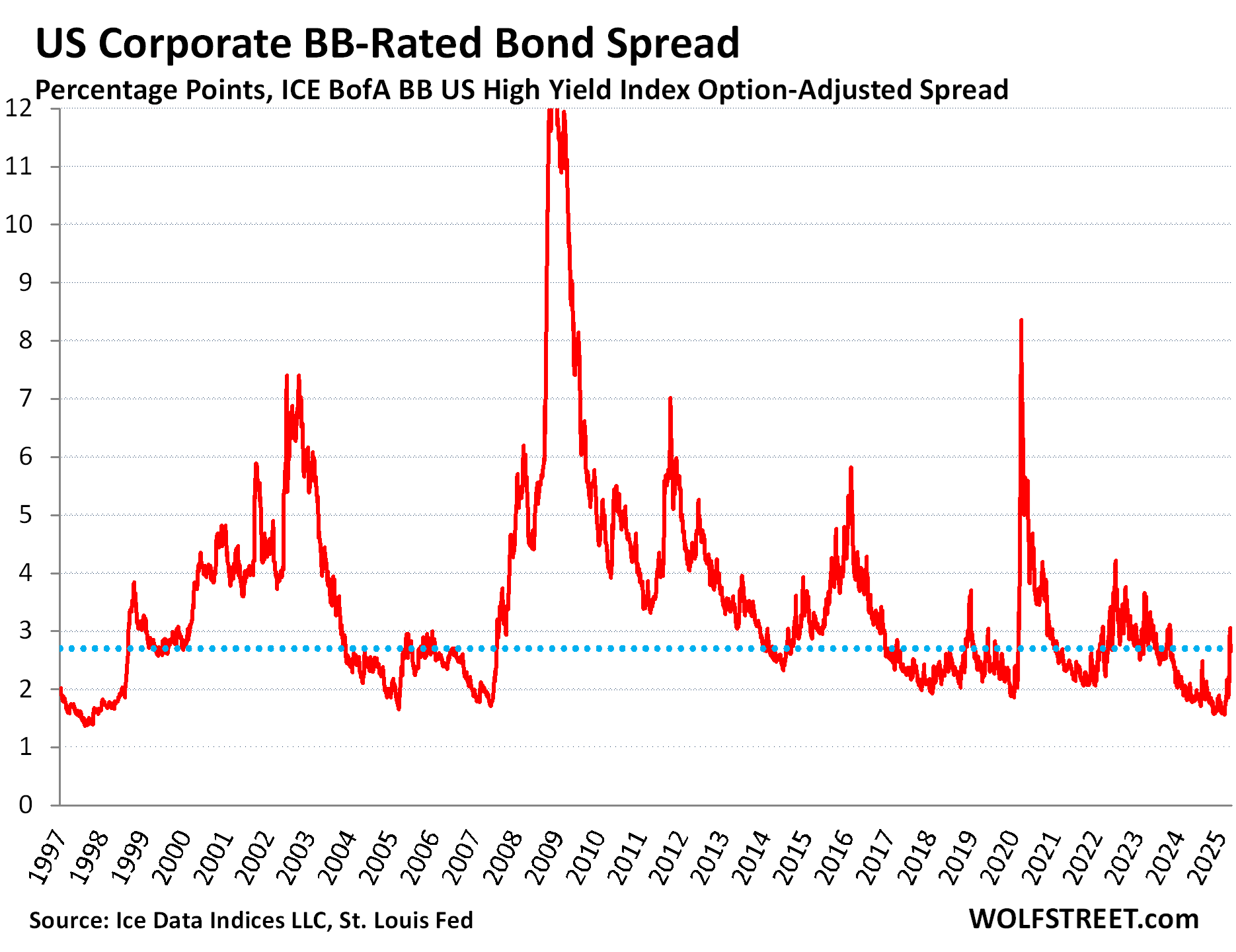

Junk bonds barely emerged from la-la-land and in recent days have tried to return to la-la-land. It’s just hard to keep the yield-chasers down.

BB-rated bonds make up the upper range of the high-yield spectrum. Companies that are rated BB have a higher theoretical risk of default than companies in the investment-grade spectrum (my cheat sheet for corporate credit ratings by ratings agency). They face greater cash-flow problems to service their debts when the economy spirals down, and they face greater difficulties refinancing maturing debts when financial conditions tighten.

The spread between BB-rated bonds and Treasury securities indicates how much more investors demand to be paid in interest to take on the additional credit risks that come with BB-rated bonds compared to Treasury securities.

The ICE BofA BB US High Yield Index Option-Adjusted Spread had widened to 3.06 percentage points by April 7, up from record lows in January, but has since then narrowed to 2.70 percentage points.

While the extra interest demanded is no longer at record lows as it was in January, it’s not even back to the range that prevailed over the majority of the time over the past 28 years.

These are fairly risky bonds, and the spread should be higher under normal conditions, that’s what this chart is telling us:

Various aspects of financial stress and financial conditions are something to watch. When financial stress gets very high, and financial conditions get very tight, more high-risk corporate borrowers lose access to the credit markets, or can borrow only at a very high cost, which increases their risk of default. For individual companies, this happens all the time as one or the other individual company gets in trouble. But when it happens across the spectrum, it can spiral into a bigger problem and exacerbate an economic downturn and unemployment.

So financial conditions are among the aspects the Fed is considering in setting its monetary policy, and that type of discussion is part of its meeting minutes. But so far, not much has happened, it has been rather uneventful, despite the turmoil in the stock market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

1:04 PM 4/21/2025

Dow 38,170.41 -971.82 -2.48%

S&P 500 5,158.20 -124.50 -2.36%

Nasdaq 15,870.90 -415.55 -2.55%

VIX 33.50 +3.85 12.98%

Gold 3,432.40 +104.00 3.12%

Oil 63.46 -1.22 -1.89%

A little wild out there today!

If equities have been overvalued by 100% for years on end (PEs at 30 and above), I’ll start to care after they’ve fallen by 50% (PEs at 15…the historical norm).

Right now, what is going on is a typically satanic marriage between the Death-to-Trump MSM (for whom any context-less half-truth is now standard operating procedure) and the Kill-the-Currency-to-Empower-the-Fed-Put Wall Street equities crowd (for whom essentially 20 years of ZIRP isn’t enough…for whom, *nothing* is ever enough).

So you get this moron-based, MSNBC-CNBC axis of liars.

(Personally I think Trump gives plenty of indications of being a lazy, half-knowing nitwit. But the 50 years of preceding political pathologies that *yielded* Trump, have to be addressed in one fashion or the other. And the two incumbent political mafias didn’t do jack for those 50 years…except feed the cancer.)

This is actually where I’m at. There is a ton of blame to go around.

Both parties sold out the American people over the past 3+ decades, all to enrich the top one-percenters who got wealthier than they could have ever even dreamed of. They (the FED and .gov) blew fantastic asset bubbles under the guise of a “wealth effect,” and once those wobbled they doubled, tripled and quadrupled down on the same failed polices – failed insofar as the majority of peoples’ financial lives are concerned, but wildly successful for the one-percenters.

And now here we are. Inflation has absolutely ravaged the working classes and the poor, and the new administration is publicly insulting the FED chair to try to force him to lower rates in the face of a resurgent inflation. This looks like it is going to end very, very badly for the country. I don’t honestly see a good way out, but I’d like to see the people finally get their pound of flesh out of the billionaire class. These people need to be humbled in the worst possible way. I’d like to see their assets seized, personally.

Amen

Yeah, Jay seems like such a nice guy.

“In 1993, Powell began working as a managing director for Bankers Trust. He left in 1995 after the bank suffered reputational damage when some complex derivative transactions caused large losses for major corporate clients.[30][31] He then went back to work for Dillon, Read & Co.[27] From 1997 to 2005, Powell was a partner at The Carlyle Group, where he founded and led the Industrial Group within the Carlyle U.S. Buyout Fund.[26][32] After leaving Carlyle, Powell founded Severn Capital Partners, a private investment firm focused on specialty finance and opportunistic investments in the industrial sector.[33] “

We need to stop repeating the same mistakes. We’re always promised the swamp will be drained, but it never happens. That swamp is Congress—the place of rulemaking and legislation, yet it’s overrun with NGOs, grift, and career politicians. It’s mind-boggling how people have grumbled about these problems for decades, only to fall back on their party for solutions. It’s never been the President’s role to drain the swamp, nor has it ever been realistic to expect Congress to reform itself. We need to vote them all out. Drain that swamp. Keep voting out incumbents until they legislate the reforms we need.

“Yeah, Jay seems like such a nice guy.”

No, Jay is a dirt bag. Nobody said he’s a nice guy. His “transitory” lie financially crippled millions. The public humiliation couldn’t happen to a more deserving guy. But that’s besides the point.

Cutting rates right now is grossly irresponsible. The President is hammering him because he cut rates for the last administration in an attempt to swing the election.

Powell is a Davos/WEF/globalist insider, the enemy of the current regime.

Great comment!

Dang I thoroughly agree with everyone here! This tells me there’s hope for everyone else to finally see through all the convoluted BS as well.

Maybe the market is in la la land because they think it’s a fool’s errand to react with any conventional wisdom of thinking or predicting, when things in a month or two might be completely different beyond one’s wildest imagination…

I mean after all, threats of getting rid of the “loser” in charge of setting monetary policy has only gotten louder….will be a good to show with some serious firework very soon….that stock and bonds PPT is going to have to work some serious OT very soon..

The simple fact is that Trump cannot “fire” Powell, unless they can dig up some dirt on him. Maybe a picture of Powell smoking a joint at a Grateful Dead concert or something. Photoshopping is always possible. While I agree with many of Trump’s edicts, saying he will fire Powell seems stupid, unless he is setting up the Fed as a scapegoat if the economy goes into recession. Powell will be chair until May 2026, when Trump will install his flunkie. That’s when the markets will really tank.

It is also just dumb. Powell can’t lower the rates himself.

Fact? Close to no cigar with the current climate. Are we still playing by conventional rules nowadays? Below sums it up well, I am sure this kind of guard rail will stop him /s. Only hope is that, someone in his inner circle can get it through his head that, forcing a lower rate on the short term might actually achieve greater damage than leaving things alone and possibly plunge the market into more chaos…

“Although Trump acts as if he has the power to remove the Fed chair, this comes as a direct challenge to a nearly 100-year-old precedent from a Supreme Court case in which the court held that President Franklin Roosevelt could not remove the heads of an independent agency without a good reason such as neglect or wrongdoing.”

Federal Reserve Act on length of offices:

10.2 “…unless sooner removed for cause by the President.”

The question turns on the definition of “for cause”. Here is a definition of “for cause”:

“for cause means any of the following actions by the Executive that result in an adverse effect on the Bank: (1) gross negligence or gross neglect; (2) the commission of a felony or gross misdemeanor involving moral turpitude, fraud, or dishonesty; (3) the willful violation of any law, rule, or regulation (other than a traffic violation or similar offense); (4) an intentional failure to perform stated duties; or (5) a breach of fiduciary duty involving personal profit. ”

Trump might argue (1) or (4) or both, but this would probably have to go to the Supreme Court. In any case, markets would definitely be roiled. I doubt Trump wants to roil the markets that much. But anything is possible.

So who is the fed accountable to? Surely not the people if the elected chief exec of the country can’t boot him out. I dont like all the power a president is given, but everyone in government has to be accountable to the voters, no exceptions.

Fed chair is only accountable to the elites ,who have siphoned off 37 trillion

BB only +2.70? No thanks, not in my portfolio.

That’s what I’m thinking. I already don’t want 10-year Treasury notes at less than 5%, given where inflation is and might be going. The average BB yield was 6.65% at the end of last week. I mean, what are these people thinking???

Agree 10, 20 and 30yr still kind of crappy consider the number of wildcard risks out there and duration. Agency bonds are not that bad though, and some you still get the benefit of state tax exemption.

Major downside is callable timing and plus it’s not unresonable to think maybe there’s are other unthinkable risks for these agencies, one that the market likely never considered before…like will some of these agency will still even be around or allow to default or miss coupon payment..

100%. Especially as the strategy has been kind of laid out by the gov: Supress yields, ‘refinance’, and then just inflate the debt away… If the plan is out, why would anyone play along?

Wolf,

Any chance of getting a fair-sized roll-call of BB (or worse) companies?

Sporadically over the years, I’ve tried Googling for such lists and (semi-surprisingly) I’ve not had a lotta luck.

I’m sure that S&P/Moody’s/etc. have all sorts of threatening legal language about subscribers widely/freely publishing such lists, but in the Internet age, I’m a bit surprised that the collective response isn’t a bit more along the lines of “Nuts-to-you S&P/Moody’s/etc.”

There are thousands of companies on that list, some have publicly traded shares, others are closely held. All PE-firm portfolio companies are on that list, essentially by definition. Anything involving leveraged loans is on that list too. Lots of companies with private-credit funding are on that list. It’s a vaster-than-ever universe.

I fully expect junk yields to blow out to 1000 bps over the underlying before this is over, it’s just a matter of time.

Drexel junk-bonds middleman, where are you when we need you?

Seriously, we need a new dealer of junk bonds out there. Someone who can generate a market by merely saying “Drexel believes this to be a good deal, and solid.”

Not every junk bond is a bad deal. In this world, you trade risk for reward. It’s like that in our personal lives, and it’s like that in the financial sector. I personally like the symmetry of it all.

If you fully expect junk yields to blow out to 1000 bps over Trsys you should buy deep out-of-the-money Put options on HYG, a large liquid junkbond ETF.

To add fuel to your fire, you should Sell in-the-money Calls on HYG & then use the sale proceeds to pay for your HYG Puts.

Then just sit back and wait for the world to eventually realize the wisdom of your prescient bets.

Twenty year treasuries now yield 4.94%. Nonetheless, I will need at lot more than .6% above three month treasuries to get interested. Maybe if those #%$& foreigners would quit piling into our bonds we could get an attractive rate. Or maybe Powell should yield to Trump and drop the FFR 50 bp and then see bonds jump to 6%. That would get real interest.

In terms of actually buying 20-year bonds at the auction (the 20-year yield is a calculated figure), they were sold at the auction last week at a yield of 4.81%.

The next 20-year auction is on May 21.

At Schwab, click on Trade, Bonds, US Treasuries, 20 Yr and you will see 912810RK6, YTM 5.014%. The only catch is the minimum is $200,000, which is typical for bonds in the secondary market. I can do it, but I am going to need a lot higher yield.

So that CUSIP number you cited (912810RK6) is not a 20-year bond; it’s a 30-year bond that was issued in February 2015, so that was a little over 10 years ago, and the bond has a little less than 20 years to run, so it came up as a 20-year maturity.

https://treasurydirect.gov/instit/annceresult/press/preanre/2015/A_20150204_1.pdf

Liquidity is low in these “off-the-run” bonds, and they sell at a discount (higher yield). If you wanted to buy it, you could put in a bid at a higher yield (not sure if Schwab online will let you, you might have to call the bond desk — and see if the order fills.

By “typical” I mean to say “typical to get the highest YTM”. The smallest minimum I saw was only $5000.

At the start of 2020, I went short junk bonds. It was my best investment idea, I thought. I couldn’t lose. Inflation was coming, and then the if we had a recession, credit risks would elevate. Interest rates, meanwhile, were at a 500 year low. I was convinced I was right. It was a high conviction investment. What could go wrong?

What went wrong is that for system stability reasons, the Federal Reserve decided to buy junk and mortgage securities. They were federally backstopped. I lost money on my short junk bond inverse ETF (symbol: SJB).

As they say, don’t fight the FED. My lesson learned was you can be right but still get screwed. I did much better on my inverse treasury bond speculation.

The stock market was vastly overpriced last fall at 5400 and it went up another 750 points from there as rate cut and AI mania ran wild. In my opinion it’s still 2000+ points too high. So many people in the market today have never seen a grinding bear market and think this minor drop is the end of the world. I think Trump and Powell have reached a standoff and I wouldn’t be surprised if rates don’t move at all for the rest of JP’s term.

Warren Buffet is heavy on cash. I read he has enough cash right now to buy 474 of the 500 companies in the SP500.

Yes, but not all at the same time, LOL. He can only buy one of the most expensive ones on the list. His cash holdings — T-bill and chill, as we call it here — amounted to $334 billion in Q1

Gold is the “canary”. It’s price action is screaming crisis.

You mean buyers of gold are the canary, and they are screaming crisis.

Your point being?

Just that gold isn’t some kind of thermostat. It’s just the price where buyers and sellers meet, an ever-changing set of people who are no more reliable about anything than anything else. Even less meaningful than the vaunted 2/10s inversion indicating recession.

Maybe you’ve covered this in the past, but I wonder what your thoughts are on the Financial Stability Board’s 2022 report, “Assessment of Risks to Financial Stability from Crypto-assets.”

Our economic time series don’t include this new asset class.

There’s also a 2024 report, “The Financial Stability Implications of Digital Assets.”

I invested almost everything in NFTs as think that market is barely tapped.

Glen, you are kidding, right?

Got a Bored Ape, if interested. Will give good price😃

Would you care to purchase a Hunter Biden original? If you say no, it’s going up for auction so don’t coming crying later.

You need 2-3 dollars of assets, like land or gold, for every dollar of cash in the bank just to best inflation. Interest just will not hack it anymore.

People have a lot more personal control over what they spend, than how their investments perform (especially what-the-hell management or the markets do).

Chasing yield as a panicky response to inflation has ruined a lot of people over the decades, around the world.

Taking residential real estate as an example – with prices still near all time highs (but trade volumes off 30%), does RRE really look like a good risk hedge?

It will be interesting to see what the new I Bond rate is a week from Thursday. (The rate is adjusted the first day every May and November.)

If it isn’t higher than where it was set in November (3.11%) I won’t friggin believe it.

It’s already been mostly determined. The inflation part (variable rate) will be 2.86% for 6 months. The permanent part (fixed) isn’t known, but will probably be about 1.1% for a combined 3.96% for 6 months. The fixed could be a tenth or so higher or lower.

The semi-annual inflation rate won’t be anywhere near that high.

It’s not figured like that anyway. This is the formula they use:

Composite rate formula: [Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

It’s exactly 2.86% – that’s annualized (as all interest rates are quoted). The 6 months data points going in are 0.12 – 0.05 + 0.04 + 0.65 + 0.44 + 0.22 = 1.43%; annualized = 2.86%.

And simply adding the fixed and (annualized) composite rates together is accurate to 1 or 2 basis points, much smaller than the rounding they do to the fixed rate (nearest 10 basis points).

Bottom line: Expect 3.9-4.1% with 3.98% most likely – though surprises to the fixed rate are possible.

Junk bonds are the worst investment anyone can make especially today with these low spreads. I learned the hard way. I lost money every time I ventured in this market to get more yield. Never again. These investments are for suckers.

Wolf, or anyone in the know,

Is it possible to link Schwab Roth IRA account to Treasury Direct (similar to linking a bank account to TD) ?

I can’t find this info anywhere. Will this be considered a withdrawal? I can’t find any 4-week t-bills at Schwab. Many thanks in advance.

Edit: Need to park my huge winnings from shorting this market (away from temptation). Still shorting it though after bear market rally plays out. Keeping core position of Jan/March puts thru the rally.

I don’t think you can “link” treasury direct to a Roth IRA.

You could contact your financial institution that holds your IRA to see if you can purchase treasuries through that account, like you could theoretically with any tradeable security. There may be brokerage fees. Or you could buy bond mutual funds/ETFs.

Just purchase BIL/SGOV. Simplicity and liquidity are valuable things

When the Treasury refills its cash account after the debt ceiling is lifted, there will likely be more than ONE TRILLION of federal debt offered to willing buyers. I expect that 3-6 month period will confirm that 10 year Treasuries should be at 5% plus. For now the Treasury is offering very little if any new debt, as it is constrained by the debt ceiling.

If the ten year goes to 5% and the mortgage spread settles down to a more normal 1.5-2%, then the rules will be clear for everyone to see for a while. 7% mortgages, “just starting to get painful” rates on massive government deficits, and stocks reprocess to this reality. The Fed might even be able to very carefully walk the short end down a tad to 3-3.5 (and buy a heck of a lot of those Tbills themselves) and maybe the boat won’t sink after all. Some of us remember life before ZIRP and QE – everyone is going to live in the world after. Money was never meant to be free and easy, or else what’s the point?

And then there is the bull in the china shop: T’s threats to fire Powell.

BTW: did T promise in the Inaugural Oath to respect the Fed’s independence?

Bitcoin is going up!!! My dirty ex wife WILL NOT get any in the divorce I have buried hard drives in the local public park.

You know what a good hedge is??? My Magic Computer Money!! EVEN the Current lady I am seeing thinks so. She thinks I am smart AND we make love. Unlike my Ex WIFE!

THANK you Wolf for being a source of steadfast grimoire in my turbulent life.

Now the Education Department’s going to start collecting on the 5+ million defaulted student loan borrowers (have not paid in 9 months). Another 4 million are 91-180 days late on payments. I wonder how many of those (defaulted and delinquent) student loan holders took out other loans that won’t be able to be repaid after Uncle Sam starts garnishing wages, and how much this change may contribute to financial stress (if at all)?

It just means those naughty delinquent student loan holders will have to get second jobs!

Well thank God they are. It is a slap in the face to those of us who took out loans and worked our asses off

Junk bond to Fed rate risk spreads are one of the most reliable signs of when the doo-doo is hitting the fan. And, as Wolf points out in this excellent article, the spread is still narrow. It is perhaps instructive to distinguish between exogenous factors and endogenous ones. So far, I only see exogenous factors slamming the market due to The Donald’s erratic financial comments and behavior. True market capitulation occurs when endogenous factors dominate. In other words, if profits get hit hard, and people give up on the tech bubble AI mania stocks because they no longer buy into their ‘Magical Poop Machine” story, that is when the bottom may finally be reached. At this point, it feels like we could have a long way downard to go. But, then again, market predictions are a fool’s game, so I will shut up now…

Who needs stocks? Who needs bonds? Gold is up 16% in 9 days(!!!)

I think that calls for a big WTF??!!

I guess it’s the new momo play since Tesla and Nvidia don’t go up anymore!!!

Every thesis about the future has an end game.. a point at which a fundamental adjustment is logically required. Rational thought is not religion, e.g. gospel. The behaviour of the gold price is looking like one of these moments.