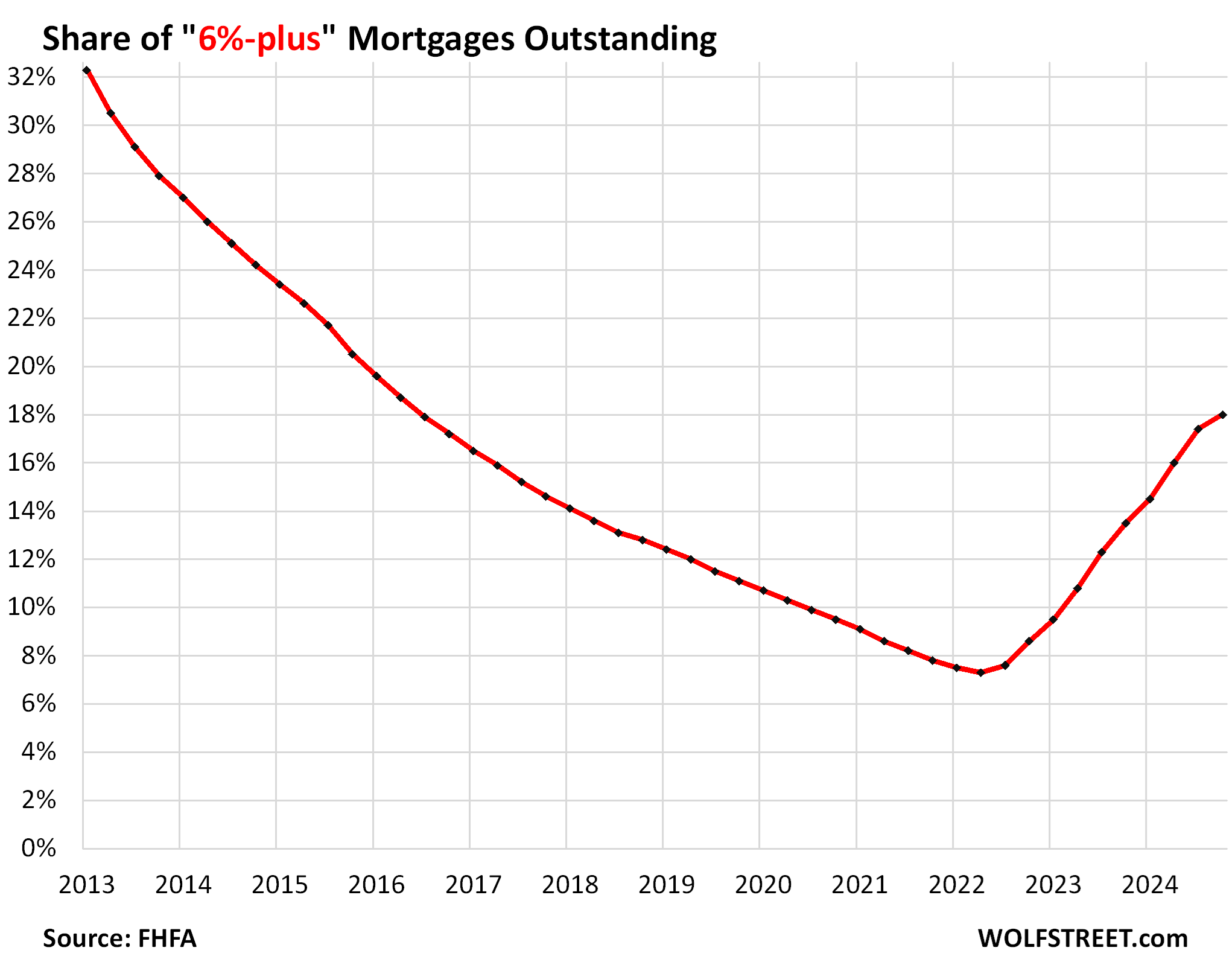

Conversely, the share of 6%-plus mortgages outstanding surges to the highest since 2016.

By Wolf Richter for WOLF STREET.

The 30-year mortgage with a fixed rate of 3% for the duration of 30 years was as close to free money in an inflationary world as regular folks can get, and it would make sense to hang on to it and never move and never refinance the mortgage and never do anything that would jeopardize this mortgage. But then life happens.

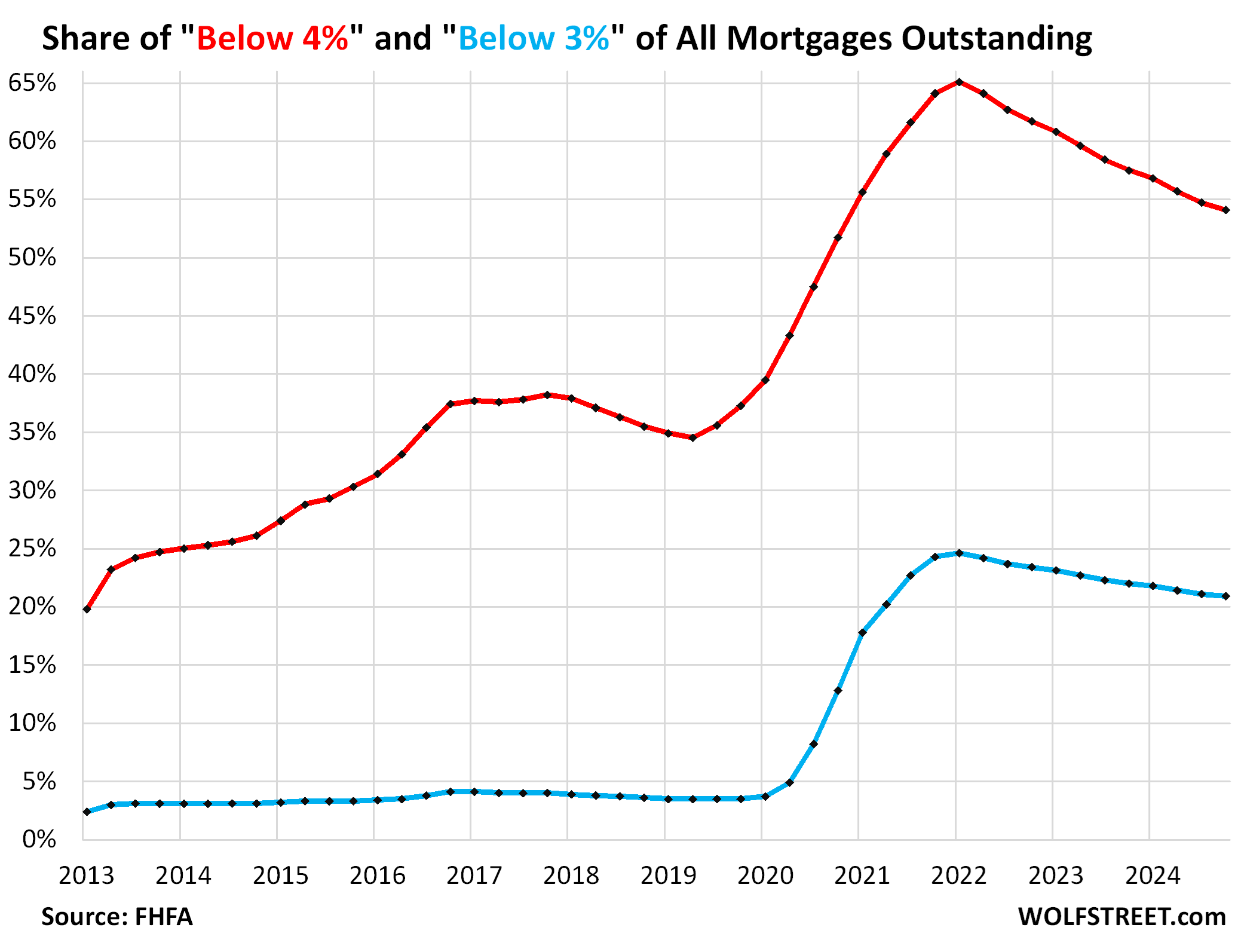

The number of mortgages outstanding with rates below 4% has been declining steadily as more and more of these mortgages get paid off. In Q4, the share dropped to 54.1% of all mortgages outstanding, the lowest since Q4 2020, and down from the high of 65.1% in Q1 2022 (red).

The share of mortgages outstanding with rates below 3% declined to 20.9% of all mortgages outstanding, the lowest since Q1 2021, and down from the peak in Q1 2022 of 24.6%, according to the Federal Housing Finance Authority’s National Mortgage Data Base on March 31 (blue in the chart below).

These mortgages include adjustable-rate mortgages, whose interest rates adjust based on some short-term benchmark interest rate, such as the six-month SOFR. Before there was SOFR, there was LIBOR. An ARM might be priced at 6-month SOFR plus a spread of 2 or 3 percentage points. During the years of ZIRP when the six-month SOFR/LIBOR was close to 0%, ARMs had very low rates, which explains the blue line before 2020.

But those homeowners experienced a payment shock when the Fed started hiking rates in 2022, and in July 2023, SOFR went over 5%, plus 2 or percentage points made for AMRs of 7% or 8%, up from 2%. That delivered a massive payment shock. Thankfully, not a lot of homeowners had ARMs.

Conversely, the share of 6%-plus mortgages outstanding rose 18.0% at the end of Q4 2024, the highest since Q2 2016, from a share of 7.3% at the low point in Q2 2022. It reflects purchase mortgages and refinance mortgages with rates of 6% or higher.

The fact that the share has more than doubled from 7.3% to 18% in a little over two years shows that “locked-in” ends when life happens: A change in jobs that requires a move, the need for a larger or smaller home, the urge to relocate closer to the kids. Death, divorce, marriage, natural disaster… are all reasons for 3% mortgages to get paid off. Other homeowners decide to sell the home to “lock in” their huge gains, pay off the mortgage, and walk away with piles of cash to invest, while paying rent instead of the costs of homeownership.

By historical measures, this share of 18.0% is still very low, as 30-year fixed rate mortgages were typically well above 6% in the decades prior to 2004.

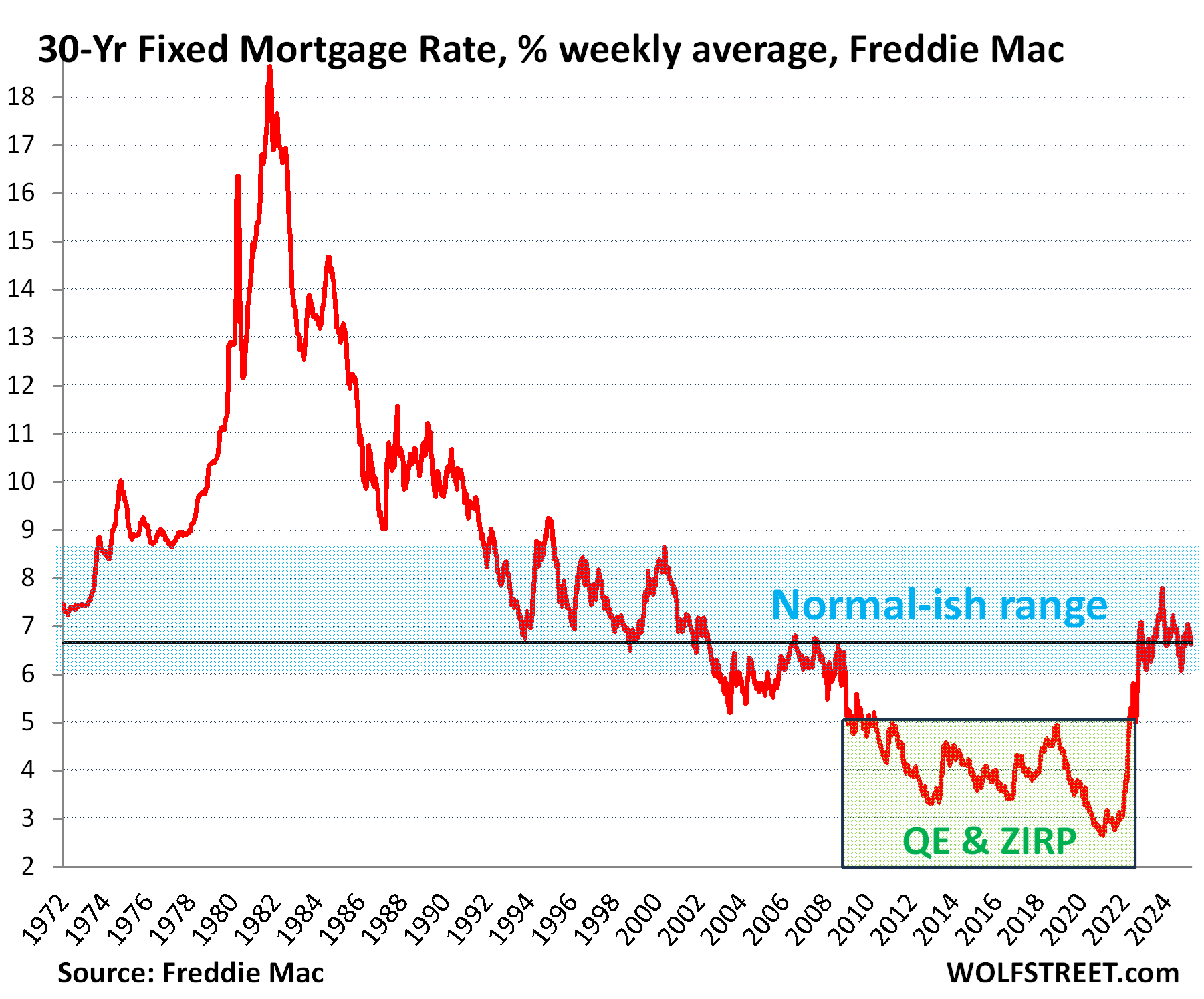

The average 30-year fixed mortgage rate has been above 6% since September 2022, according to Freddie Mac data.

The below-3% average 30-year fixed-rate mortgage occurred in a brief period from mid-2020 to late 2021, triggering the historic refinancing boom that by Q1 2022 caused nearly a quarter of all outstanding mortgages to have rates of less than 3%.

Below-4% mortgage rates occurred periodically starting in 2012.

Those super-low mortgage rates were a result of the Fed’s QE when the Fed bought bonds, including large volumes of mortgage-backed securities (MBS) specifically to repress mortgage rates, and those repressed mortgage rates caused home prices to explode, which is now the biggest problem that the housing market has to deal with.

The “locked-in effect” describes a situation where homeowners with super-low mortgage rates try to hang on to that mortgage for as long as possible by not moving, thereby staying off the housing market entirely, both as seller and as buyer. It ultimately doesn’t change inventory because they’re neither buying nor not selling a house, thereby not taking one off the market and not putting one on the market. But it depresses home sales, which are down by 20% to 25% from 2018 and 2019.

The brokerage industry – which makes money coming and going when a homeowner changes homes – and the mortgage-lending industry are very upset about this locked-in effect on sales because it’s eating their lunch, and not just their lunch, but their jobs.

But turns out, these below-4% mortgages are not so locked in as homeowners find themselves confronted with a situation where they want to, or have to, pay off the low-interest-rate mortgage and take out a new mortgage at a much higher rate. And so homeowner by homeowner, the locked-in effect fades.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

> normal-ish 30y mr

It was normal-ish when market was not sk[r]ewed and median house price was (I’m guessing) below 200k-ish range and you had to borrow ~150k. When you have to borrow jumbo — it is not normal-ish, but rather robber-ish.

Let’s get back to 1980-1981 interest rates, and PRICES!

Life is happening, they can’t hold on forever!

In case it wasn’t noticed, the 31 March article has been put up on Kitco News.

Since we’re not looking at anything like the Subprime Mortgage Crisis this time around and the Fed won’t be raising interest rates unless there’s a black swan event, that only leaves mass unemployment as the possible cause of a housing price collapse. Now, how could that happen?

No one is talking about a “collapse.”

Yet.

But seriously, house prices will have to be the last market to fall after the stock market is in a bear market and there is an official recession. An official recession (rather than the two-quarters thing) has to have rising unemployment. It all follows from falling corporate profits.

US corp. profits hit an all-time high in 24Q4. The problem with record profits is that they make it difficult to increase profits in the following quarter and the year-later comparisons. Anyway, this is all months in the future.

You need underwater home owners for a 2008 style collapse. Back then many homes were purchased with no or negative equity, the owners had nothing to lose by letting them go in a short sale. That’s not the case today.

In Canada a buyer can assume the seller’s mortgage rate. I think I saw that on this site. I read for the US, “USDA, FHA, and VA loans are assumable when certain criteria are met.” I wonder what would happen to the US housing market if ALL houses in the US could be sold with assumable mortgages.

Assumable mortgages aren’t always so easy to assume — at least in my VA loan case. There a many ways a mortgage company can make it difficult, through red-tape and whatnot, as they aren’t incentivized to do the deal. In my recent sale, the buyer would have had to come to closing with all the equity in cash. Thus, they ended up deciding to go fixed/conventional.

Mortgage rates would be higher at origination due to the lender assuming more risk.

Correct me if I’m wrong but in Canada I believe most mortgages are 5 year balloon loans (ie after 5 years you need to rollover the remaining principle into a new loan). So being to assume a loan that might only have a few years left on it isn’t that big a deal.

Re: the US it already takes massive government subsidies to make 30 year mortgages not destroy either the buyer or the lender (see previous article about how much money the government throws at the GSEs) and that’s with an average term of 7-10 years (that’s the average time a homeowner actually keeps a 30 year loan before either moving or refinancing).

If the average term of a 30 year loan actually went to anywhere close to 30 years (due to people assuming previous loans when they buy a house) it will likely require either much higher interest rates or a massive increase in government subsidies and protections to keep such loans from blowing up house owners or the banks.

Yes, 5 years is the most common mortgage duration in Canada, but you can also get 2, 3, 4, 6 or 7 year terms.

Thanks, fascinating data. Is there data available to see how many homes are mortgage free. Or at least the mortgage is so small as to not be a huge financial issue.

Latest I saw somewhere is that nearly 40% of all homes are free and clear, record territory. It used to be around one-third.

Wolf,

Anecdotally, for me at least, the number of our friends who are mortgage free is increasing.

Then, again, we’re all in our late 60’s-early 70’s and retired.

Thanks for another interesting post!

lots of homes were bought 2009~2011 in cash at cost lower than many SUVs nowadays.

So what are potential home buyers supposed to do, especially when their wages have not kept up with the inflated housing cost ?

Sellers in some big cities still price their homes as if interest rate is 3% or less. They might give an unrealistic discoint of 1-2% just to attract people. How does a buyer pay 7% on that pandemic price ?

How do you know that they are being paid off instead of being sold? It doesn’t make sense for someone to pay it while rates on T-Bills is higher than the mortgage rate?

Their not paying it off, they are selling it and therefore it gets paid off. This in turn ends the loan that’s sub 3% interest. Then they get to party….

Paid off and sold mean the same thing in this context (I.e., some mortgages are paid off upon selling the home). It’s not clear what % are being paid off due to home sale vs. not but I’d guess majority are due to home sale.

It’s the same thing for the purposes of this discussion. The old cheap mortgage is no longer.

Even if it’s logical to arbitrage the debt, some people can’t bear the shame attached to being in debt.

A few years ago, when TBIlls went above 4.5%, it made sense to not pay off the mortgage. While working, I’m in the 24% federal tax bracket so the effective TBill rate was a higher than 3%. My mortgage was 3%.

With a 4.2% TBIll rate, the after tax rate is 3%.

If TBIll rates fall below 4%, then it may make financial sense to pay off a 3% mortgage. If long term bond rates bump up higher (above 5%), then it would make sense to buy 10 or 30 year bonds rather than pay off the house.

With a 3% mortgage, it is hard to overcome the 29K standard deduction for SALT and interest/charity so there is not a tax deduction with owning a house. That is not a benefit. It is a benefit with a 7% mortgage to itemize deductions since the interest for 500K is 35K alone per year.

I’m watching TBIll and TBond rates to determine when it makes sense to pay off the house.

I don’t understand why anyone would take out a 30 year mortgage given the likelihood of life events discussed by Wolf. The first five years of payments are mostly interest.

societal pressure is a powerful force

You think homebuyers would foresee life events like death, divorce, losing a job, or natural disaster?

Not everyone who buys a house uses rational thinking. They are buying a monthly mortgage payment.

If buying housing, you are “buying” a monthly payment with upside or downside exposure of whatever kind. Rents could continue to rise, and leave you with no asset at the end.

Some now have fully paid-off mortgages in now otherwise unaffordable areas. I could not afford rent in the worst unit in the complex where I now own the best unit, free and clear. It is possible. I credit it most to my dogged unimaginative paying off of my mortgage, and making any sacrifices needed to do so. This is a matter of sorting one’s priorities over the long haul. Also, I have a physical asset as a hedge in a world of things like AI employment disruption. Long-term inflation has been a thing for many decades now, and there is an argument this will continue.

Eh, cash flow. Why aren’t mortgages only 5 year loans? Because the mortgage payments would be so high, not many people could afford them.

If you take out a 30 year mortgage, nothing prevents you from paying it off earlier.

What do you propose as the alternative for most people?

How much of the first five years of rent to a landlord do you get to keep? And how about the next 25 years after that?

My 30-year mortgage will be paid off in 2030 and at that point my monthly “rent” will be property tax and insurance, totaling maybe $600/month. In my area, a similar house rents for $3500/month or so. With a little luck I might live another 30 years after paying off the house… that would save me more than a million dollars in rents over that period assuming the spread stays the same (not that I assume it will.) But certainly it will save me more money than what I paid in interest.

When there was free money, I locked in 30 year mortgages on my rental properties at an average cost of 3.05%. That’s why you’d do a 30 year.

Because housing prices always go up 20% per year? Sarcasm

I would buy a house if:

1) I truly plan on living there for 10-15 years.

I realize sh*t happens but I also know time flies when you are working and raising kids. Most people don’t move when the kids are 10. Also, the 7-10 year itch happens with jobs and marriages so that gets you most of the way.

2) You have the cash for 20% down. Avoid the mortgage insurance. You are throwing your money away like rent.

3) You should be somewhat handy to repair and improve the small stuff. You should own and be able to use a paintbrush, screwdriver, wrench, hammer, and plunger. Plumbers around here charge $200/hour. Don’t call them to plunge your toilet or pour Drano for 1K.

4) Finally, look at going rents for the same house. My son is renting at half the cost of the PMI for buying the same house. If rent goes up and/or mortgages go down, be prepared. Half the cost for renting is severely unbalanced. Something will change soon. Just wait.

It’s a cost of capital consideration. 6%-7% Return on Asset vs. Cost of borrowing. I refinanced cash out sub 3% SOLELY because the cost of capital was so low and it is mathematically illogical to NOT do it. A waste of an opportunity.

Howdy Folks. Even with the decline, thats still a bigly amount of Prisoners.

ZIRPing USA.

Agree that most of these mortgages are being paid off for reasons explained. Want to add that some people just pay off their house due to economic fears or the feeling of freedom, even if it doesn’t make sense. Had this conversation with my wife recently.

With 3.125% mortgage, I figure I can arbitrage $50/$250k/yr. on 4.375% treasuries, assuming Fed tax rates stay the same. Seems wrong to pay off the mortgage, because the only way to get rich is to think like a rich person, but human nature urges to sell.

You’ll have to pay federal income taxes on that Tbill so it’s about a wash…

with my 2.5% mortgage on payment No. 28 it tilted to more principal being paid off than interest

Even after Fed taxes on 28 day t bills the Fed is paying off my principal at more than 50% of each payment/month

David,

If you can deduct the interest on the

mortgage, does that not make the taxes

a wash? Or maybe even a win, when

considering state taxes?

With a sub3% mortgage, most people don’t overcome the 29K std deduction. The 10K SALT cap makes it more difficult.

My idea of fairness would be able to deduct interest paid from interest earned before itemizing. Also, property taxes keep going up but people can’t deduct them due to the SALT cap. Greedily, this would benefit me.

With a 29K std deduction there are some great tax benefits being a renter.

Depends on what’s incremental above the standard deduction.

The reason I got a 30-year mortgage (in 2016) was for reasons stated above:

I have locked in my housing payment at a low- end rate (for the time). The rent prices were substantially higher than the mortgage payment and have risen substantially since then.

The 1/3 of the payment I that went to principal was 1/3 more than the similar rent payment I had already been paying.

I still have a sub-4% rate, as I was not in the position to refinance for less. The principal I accrue is only increasing, and it’s the most stable/ valuable “asset” I have ever owned.

Not to mention? I have enjoyed raising my family indoors.

I’m in a HCOL area. My mortgage payment is less than the national median rent.

Moving from my current location (paradise for some) to a crummy suburb would probably pay less and cost similarly.

Why are people paying off sub 4% mortgages?

I’m guessing a large number of them are cashing out the home price increases of 2020 to 2024. They may have 3-4% mortgages, but they realize the only way to capture the economic benefit of the mortgage is to hold the mortgage over time (while assuming the high risk of home price drops) or sell the home while prices are near peak. Lots of them are electing to sell.

Lemmings are on the move!