Because prices are way too high. Buyers’ Strike deepened even with mortgage rates at 2-year lows at the time of those sales. But rates have spiked since then.

By Wolf Richter for WOLF STREET.

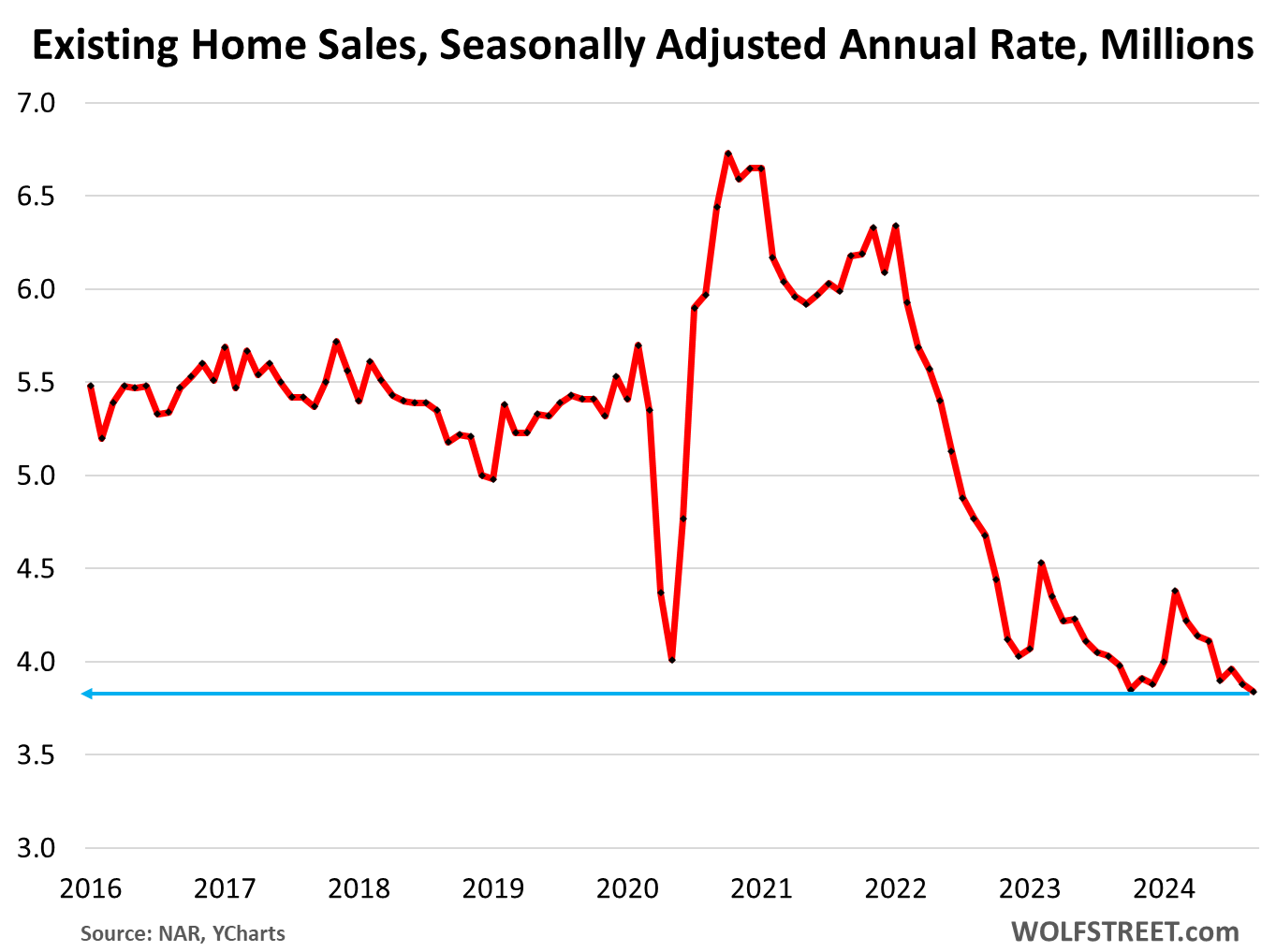

Demand for existing homes is wilting further, despite surging inventories and spiking supply and much lower mortgage rates – they hit a two-year low at the time these sales were made:

Sales of existing single-family houses, condos, and co-ops that closed in September dropped to a seasonally adjusted annual rate of 3.84 million, the lowest rate of sales since the worst three months of the Housing Bust, down by 3.5% from the crushed levels a year ago, down by 38% from September 2021, and down by 29% from September 2019, according to data from the National Association of Realtors (NAR) today.

But the impact of the recent spike in mortgage rates is still to come. These were sales that closed in September but were made in prior weeks and months when mortgage rates were much lower. Mortgage rates bottomed out in mid-September, then slowly ticked up after the Fed’s monster rate cut. They didn’t start spiking until the beginning of October, which will show up as a further hit to the closed-sales data in a month or two (historic data via YCharts):

Too-high prices cause demand destruction on an epic scale.

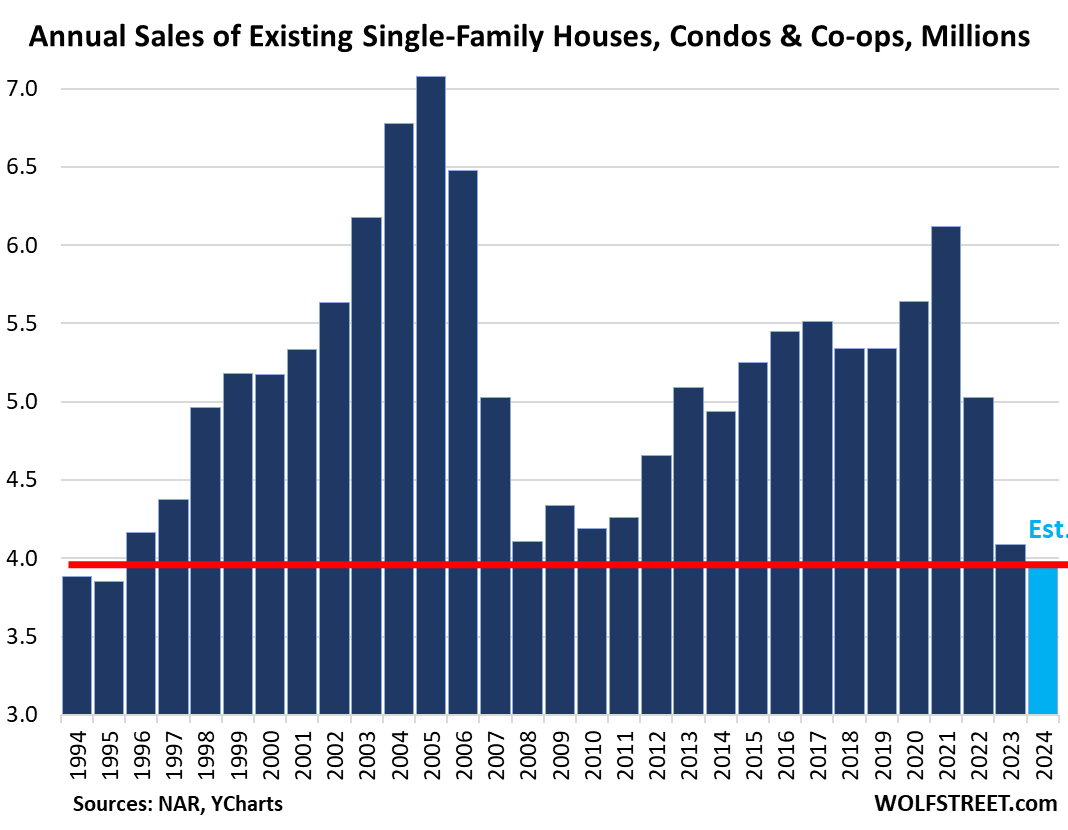

Actual home sales in September (not seasonally adjusted, not annual rate) dropped to 331,000 homes. For the first 9 months, actual sales fell by 2.8% from the already crushed levels of the first 9 months last year.

So we updated our estimate for whole-year sales in 2024, using the 9-month year-over-year decline as factor to estimate the remaining three months. Today’s sales figures push our estimate below the 4-million mark, to 3.97 million sales, the lowest since 1995.

This demand destruction, caused by the gigantic spike in prices – they’re now way too high – is even larger than during the Housing Bust.

But during the Housing Bust, demand destruction was caused by an economic and financial crisis, as millions of people lost their jobs and mortgages blew up after years of reckless mortgage lending.

Too high prices destroy demand, which is a fundamental economic principle that even home sellers cannot escape (light-blue column = our estimate for 2024, historical data from YCharts).

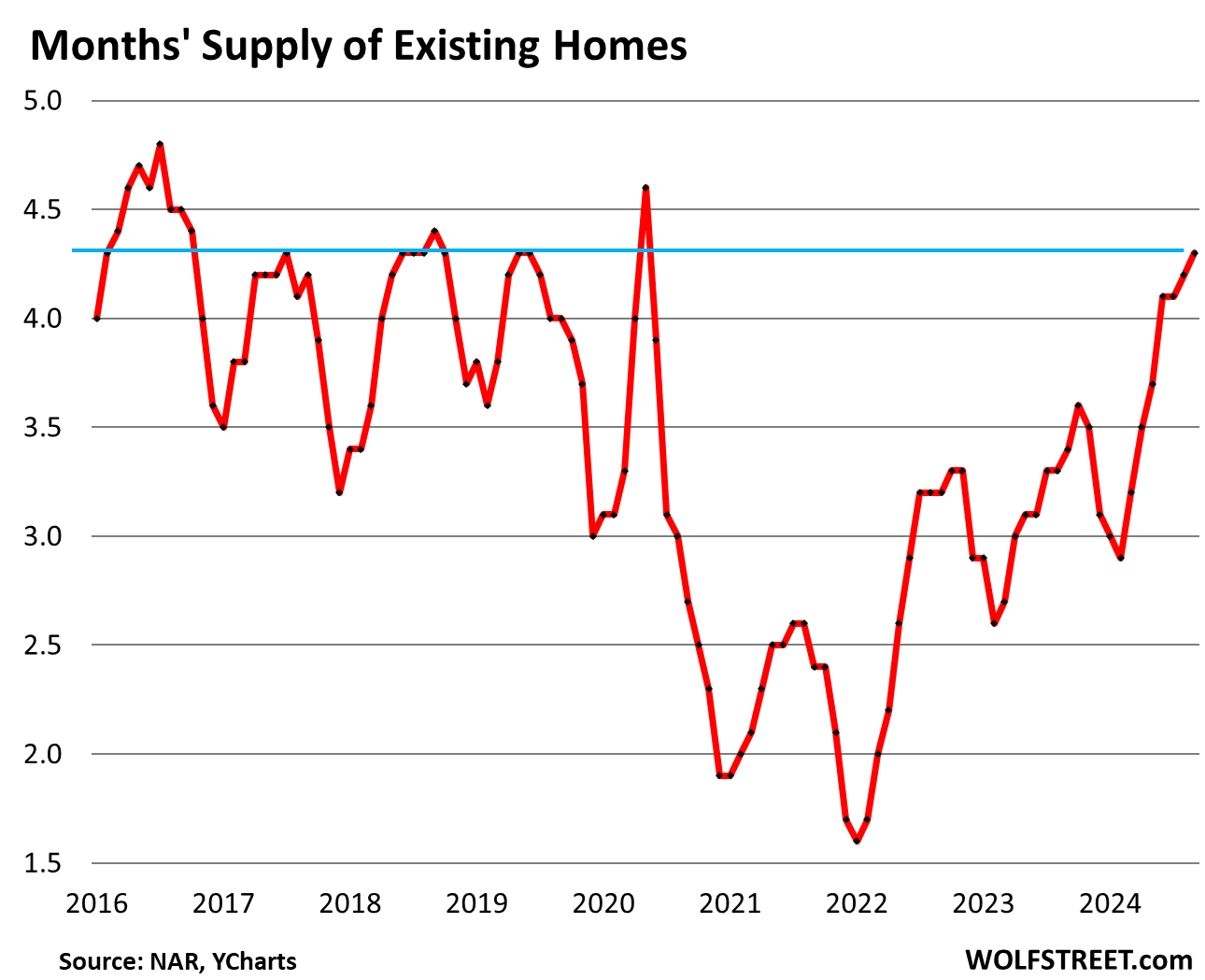

Inventory and Supply spike to multi-year highs.

Unsold inventory jumped to 1.39 million homes in September, the highest in four years, and up by 23% from a year ago, according to NAR data.

Importantly, inventory jumped in September, when it normally falls in September. Inventory normally peaks in June and then declines every month for the rest of the year with the low point in December.

But this year, every month since June, inventory has risen, instead of falling. Those are the vacant homes coming on the market even as demand has wilted.

Supply, given the wilting demand, jumped to 4.3 months at the current rate of sales, up by 27% from a year ago, and the highest for any September since 2018 (4.4 months), and higher than in the Septembers of 2019 and 2017 (historic data via YCharts):

What the much lower mortgage rates since November 2023 have done is bring out the sellers, and so inventory and supply have surged. But buyers have retrenched in their Buyers’ Strike because prices are way too high.

New listings jumped in September, when they normally decline in September, according to data from Realtor.com. These are the vacant homes that are now coming on the market that homeowners had moved out of, often years ago, but didn’t put on the market because they wanted to ride up the price spike all the way, and they already bought a new home back then, and so by not putting their homes on the market when they bought one, they contributed to the inventory shortage at the time. Now they’re trying to unload them, just as demand has collapsed.

Nearly anything will sell if the price is low enough. People in commercial real estate have figured this out, selling office towers 60% and 70% below their prior transaction prices.

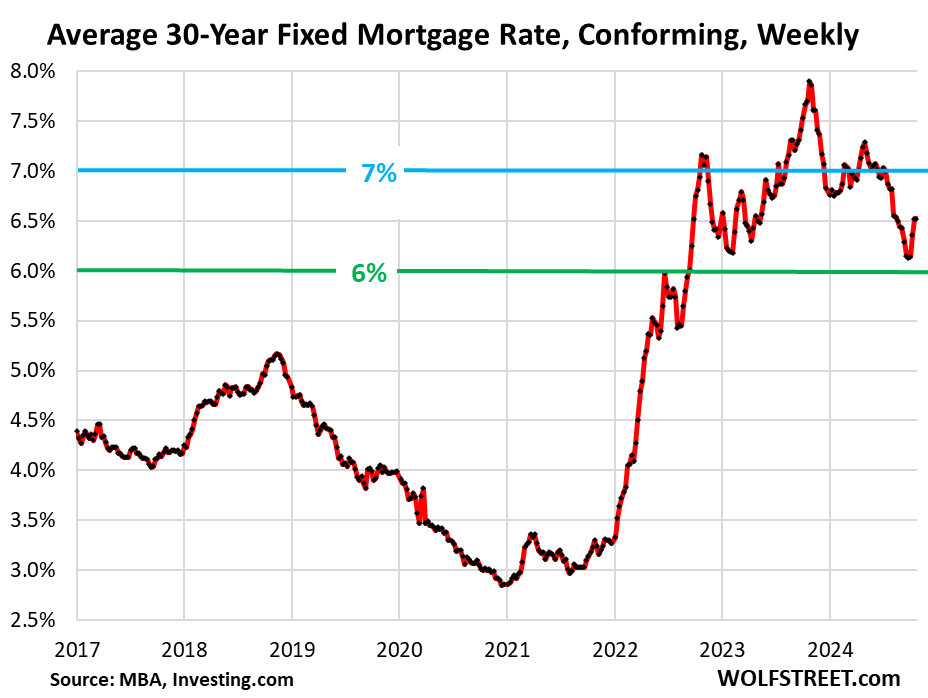

Surging mortgage rates in October will weigh on sales.

Mortgage rates have surged recently, but during the time these sales were made, they’d hit two-year lows. The average 30-year fixed mortgage rate started plunging in November 2023 from the 7.8% range and reached 6.14% at the end of September, the lowest since September 2022, according to data from the Mortgage Bankers Association (MBA). Then in October, it spiked to hit 6.52% a week ago, and remained there, according to the MBA today.

This weekly average hasn’t yet captured the moves over the past few days. But the daily measure of the average 30-year fixed mortgage rate by Mortgage News Daily jumped to 6.92% today. The impact of this jump in mortgage rates in October will show up in closed sales over the rest of the year.

The weekly average 30-year fixed rate via the MBA:

NAR blames everything except the problem: too-high prices.

The median price by the National Association of Realtors of existing homes has exploded by 50% since the beginning of the pandemic in early 2020, most of it in the first two-and-a-half years, fueled by the Fed’s interest rate repression and free money. It was the craziest 2.5-year frenzy ever in the housing market, and those now way-too-high prices have destroyed demand. Buyers are on strike, and they’re staying on strike.

But here comes the National Association of Realtors, trying to blame something other than the way-too-high prices: Last year, it had blamed the inventory for the collapse in demand, and then it blamed the surge in mortgage rates for the collapse in demand. But this year, inventories surged, and mortgage rates dropped. So both excuses are out the window.

So now it is blaming, you guessed it, the election:

“Perhaps, some consumers are hesitating about moving forward with a major expenditure like purchasing a home before the upcoming election,” the NAR said today.

The NAR has been blaming everything it can drag by its hairs except the actual problem: Prices are too high and have killed demand. Much lower prices would stimulate demand – and commissions for Realtors because they’d make more sales. Why is this so hard to come to grips with?

But instead, the NAR has started the long wait for wages to catch up with a 50% spike in home prices: “With wage growth now outpacing home price appreciation, housing affordability will improve,” it said.

Yes, but it will take a long while – years – before wages have risen enough to catch up with the 50% spike of home prices from already precariously high levels before the pandemic.

Commercial real estate has figured this out a while ago: Massive revaluation has caused sales to pick up. And the homebuilders have figured this out too: They’re offering homes at lower prices and with big incentives and costly mortgage-rate buydowns to sell the homes they built, and they’re running circles around sellers of existing homes.

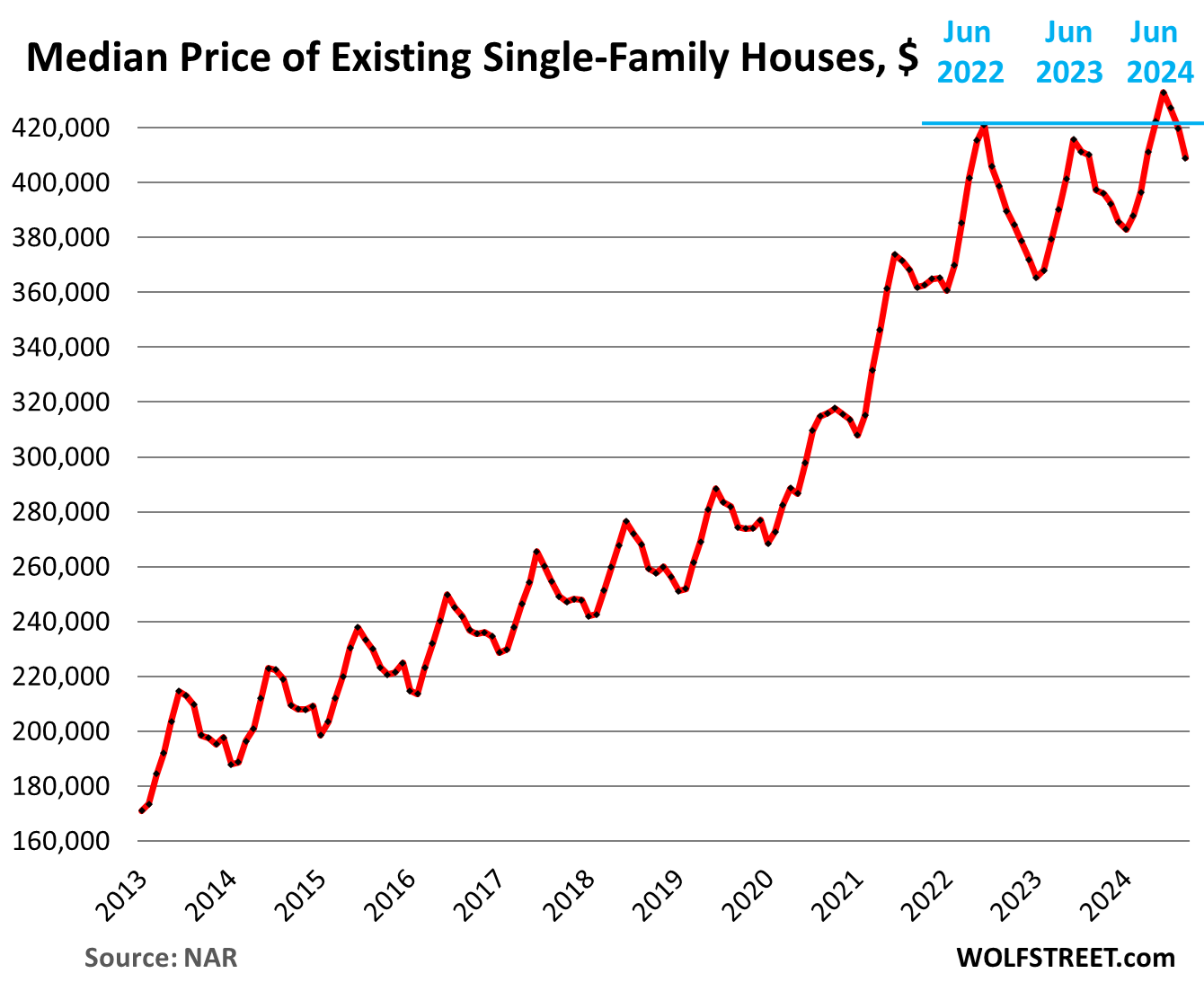

The median price of single-family houses fell to $409,000 in September, the third month of seasonal declines from the seasonal peak in June. Year-over-year, the price was up by 2.9%, down from year-over-year price increases of 3.9% in July, 4.1% in June, 5.2% in May, and 5.4% in April.

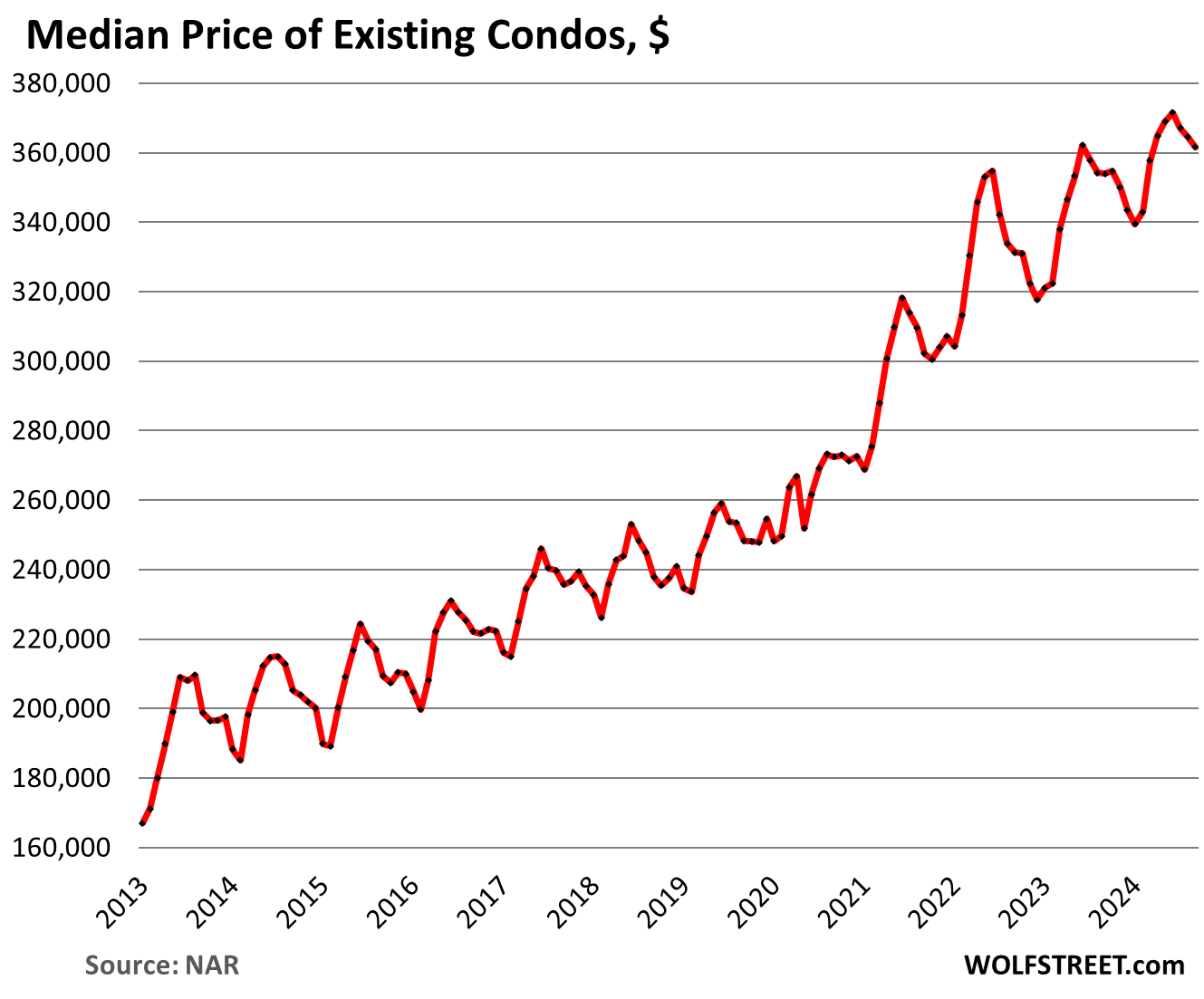

The median price of condos and co-ops fell to $361,600 in September, which whittled down the year-over-year gain to 2.2%, from year-over-year gains in the +4% to +9% range late last year and earlier this year.

Unlike single-family house prices, condo prices didn’t book any year-over-year declines in mid-2023.

Home prices by metro vary widely.

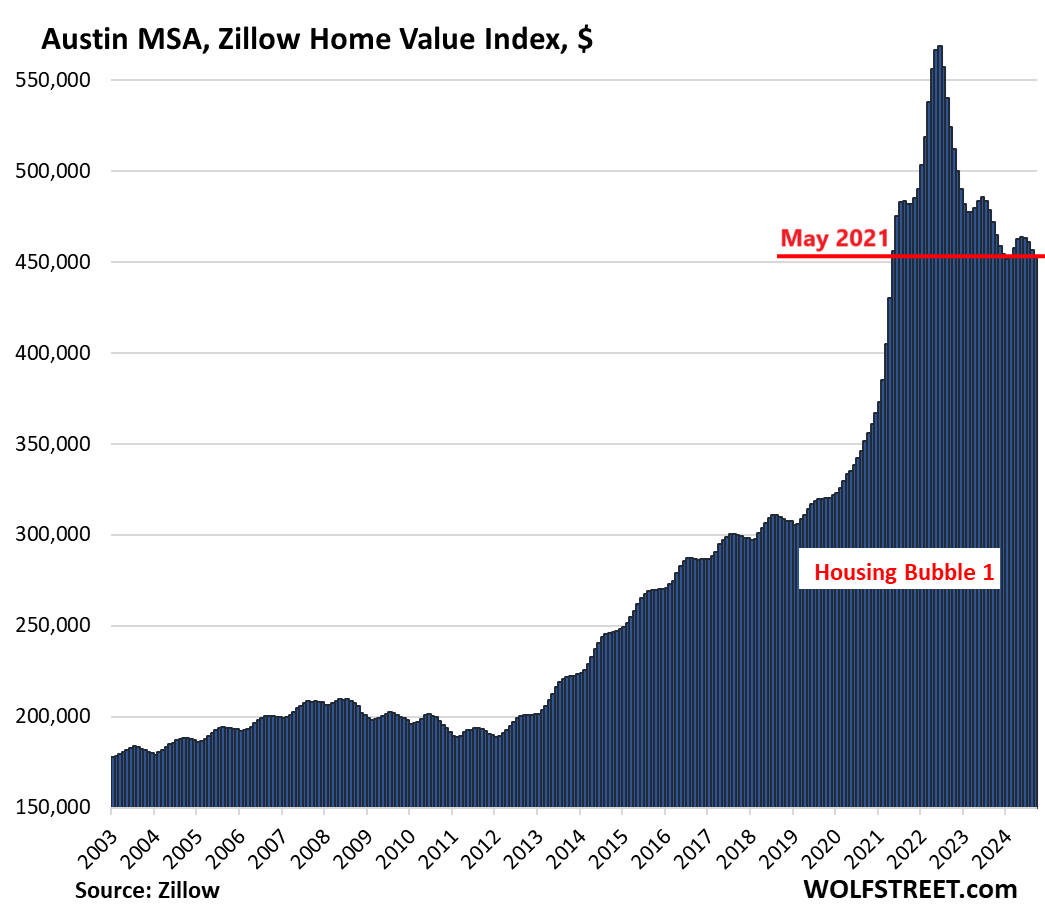

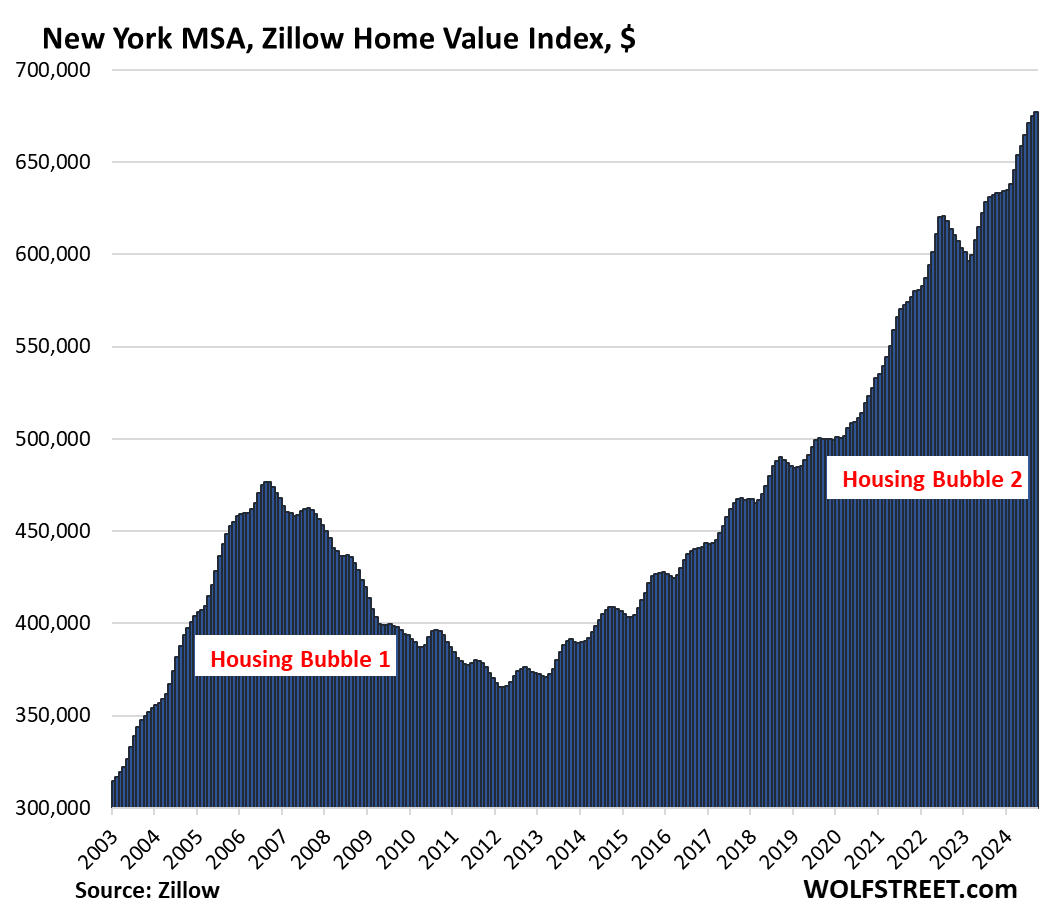

In some metros, prices have plunged, such as in the Austin metro (-20% from the peak), while in other metros, prices have risen to new highs, such as in the New York City metro. But in all metros they spiked insanely in the 2020-2022 period, which is now causing the demand destruction,

We discuss by-metro September prices here: The Most Splendid Housing Bubbles in America: September Update: Prices Drop in 26 of 28 Big Metros, even San Diego, Los Angeles, and these are two of the 28 charts:

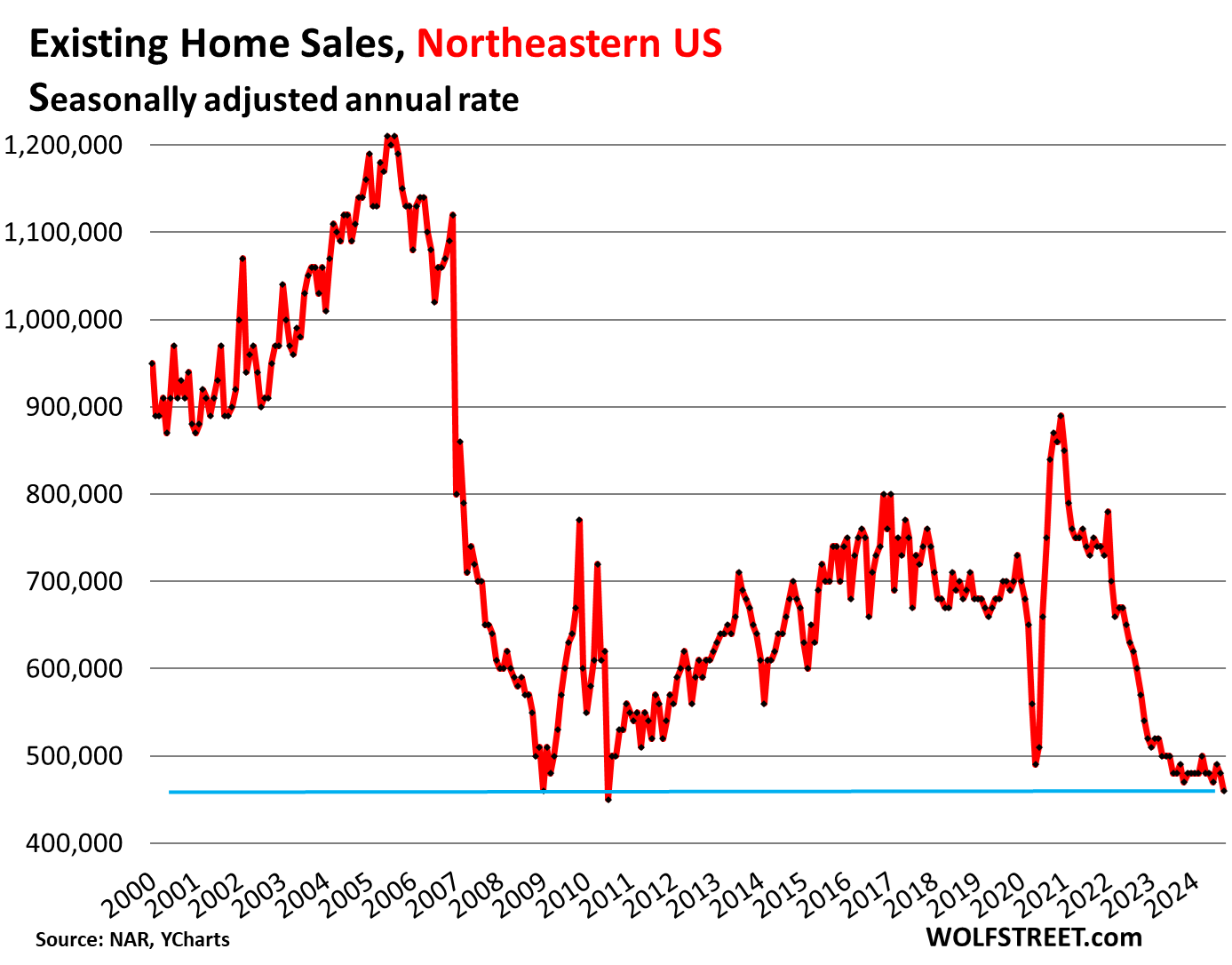

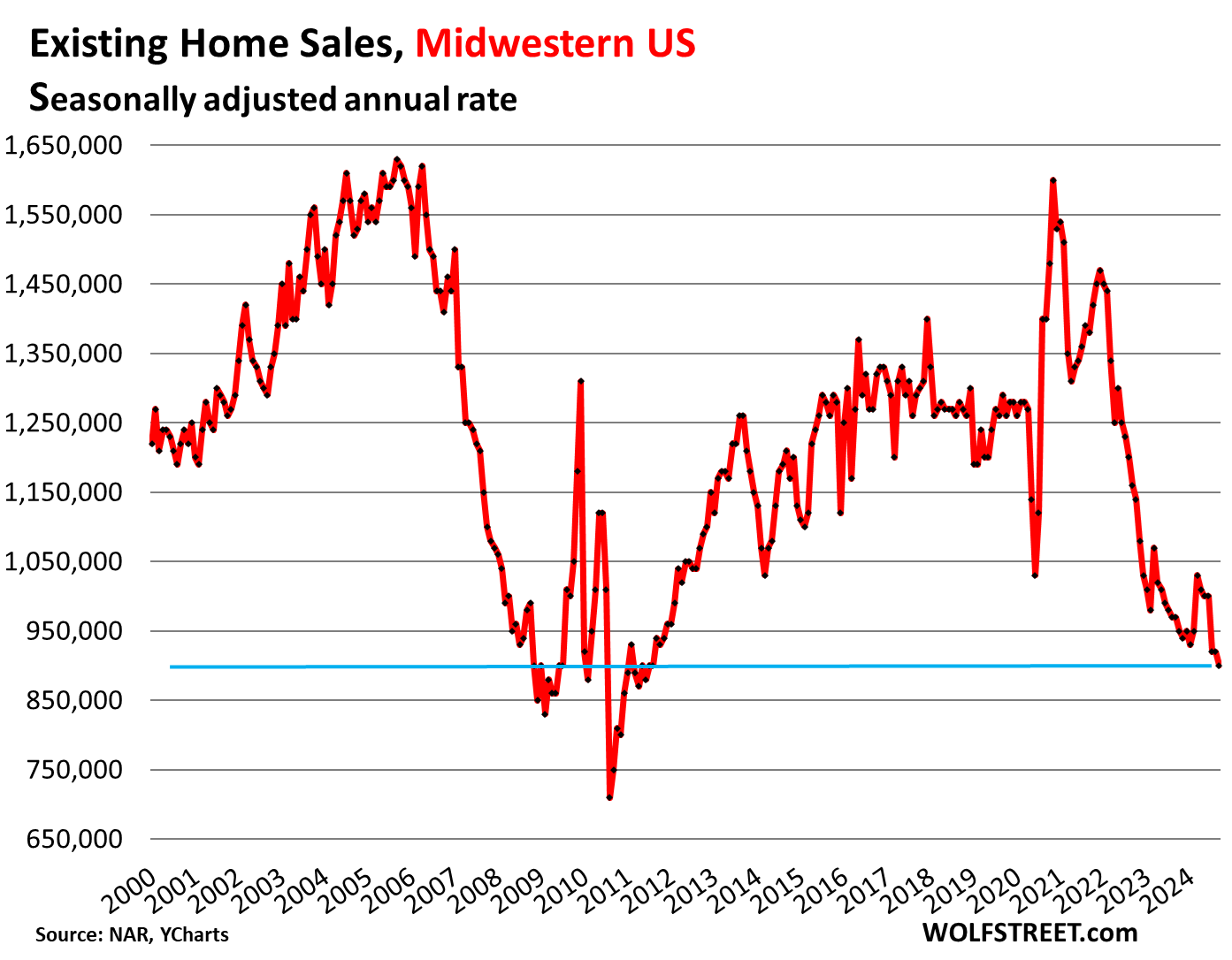

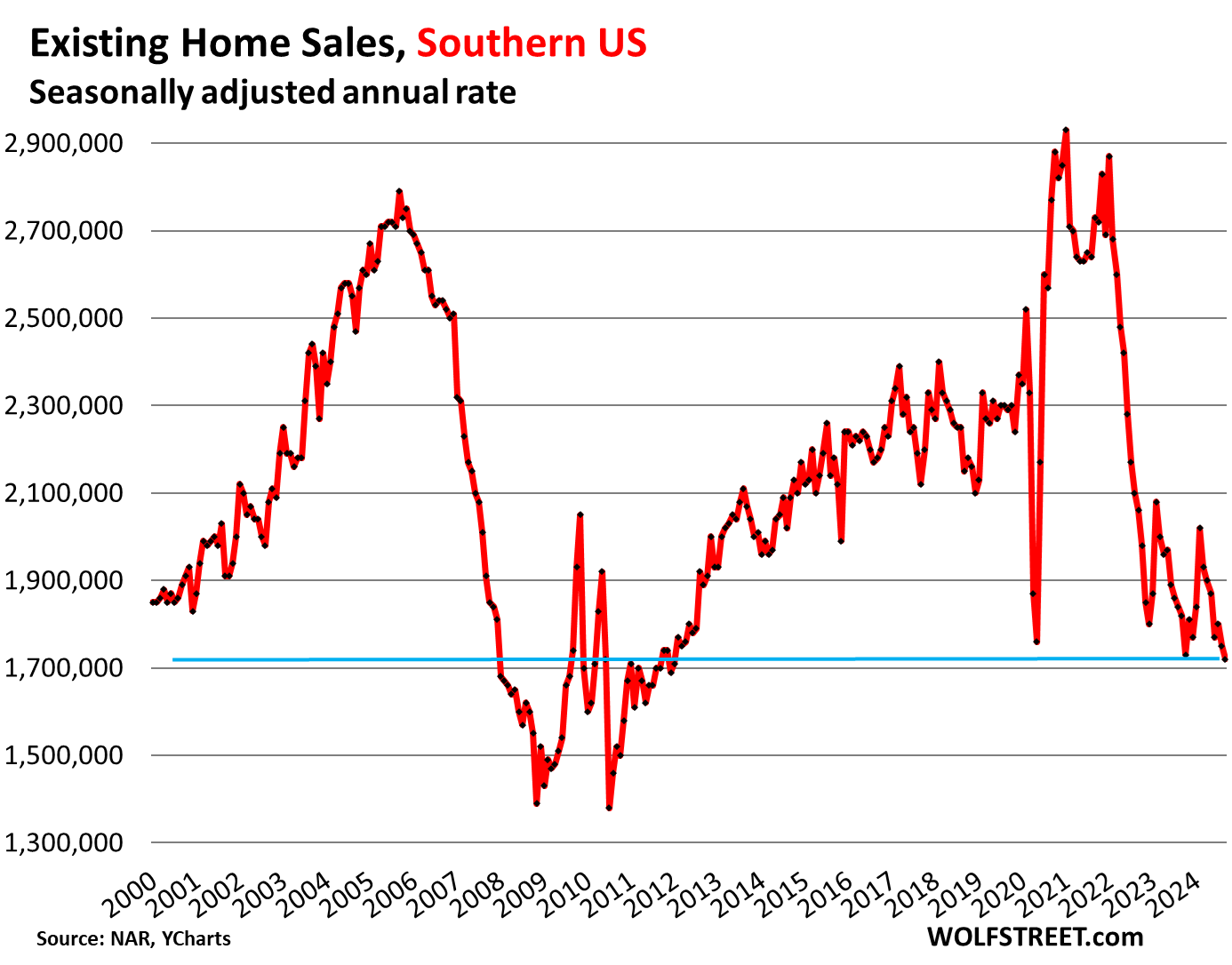

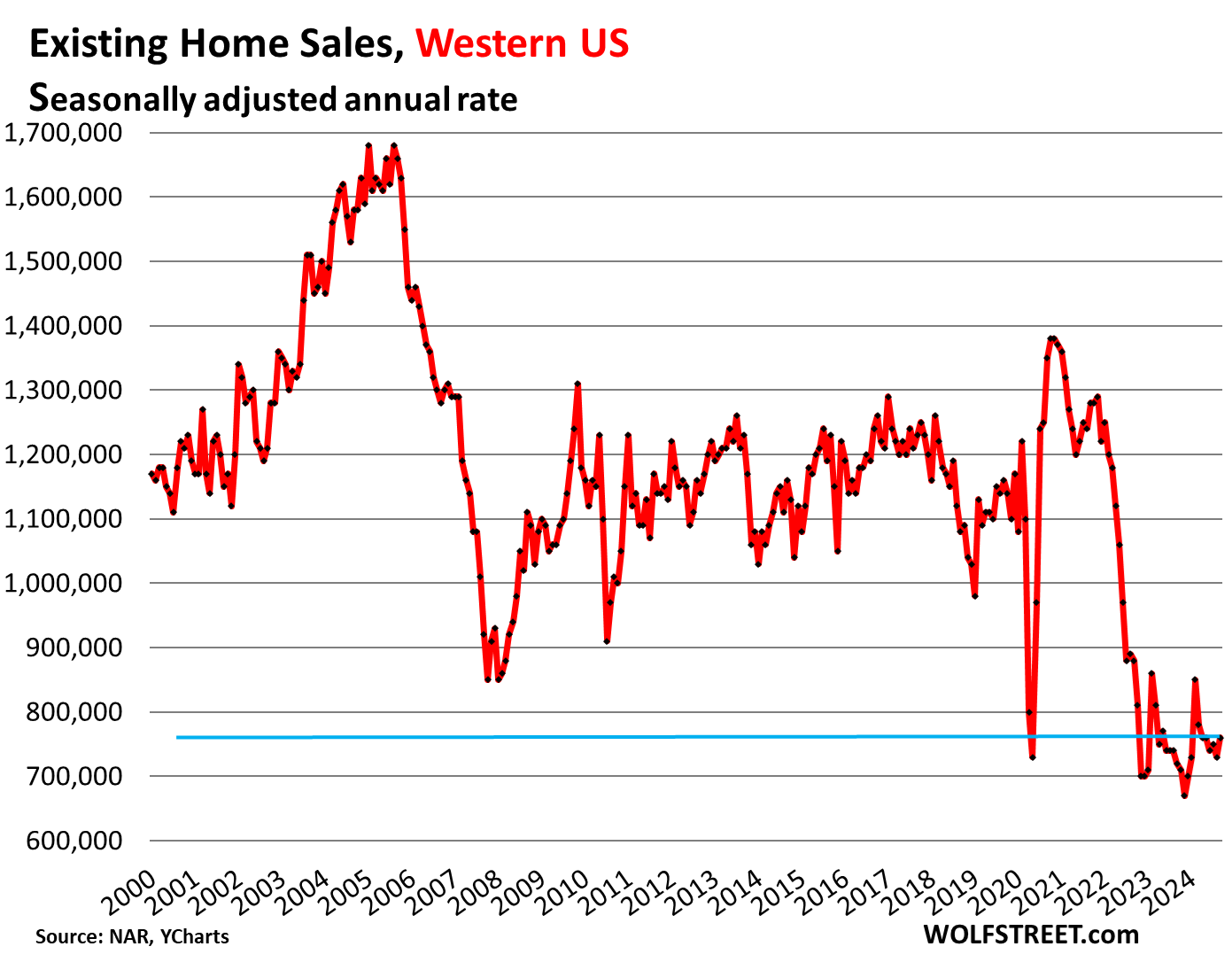

Demand destruction has occurred in all regions.

The charts below show the seasonally adjusted annual rate of sales, released by the NAR today, in the four Census Regions of the US. A map of the four regions is in the comments below the article.

Northeastern US: Sales fell to a seasonally adjusted annual rate of 460,000 homes, the second lowest since the 1990s, just a hair above July 2010.

Midwestern US: Sales fell to a seasonally adjusted annual rate of 900,000 homes, the lowest since the Housing Bust.

Southern US: sales fell to a seasonally adjusted annual rate of 1,720,000 homes, the lowest since the Housing Bust.

Western US: sales ticked up to a seasonally adjusted annual rate of 760,000, a little higher than some months in 2023 and 2024, but beyond that, the lowest since the 1990s:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As promised in the article, the map of the four regions:

While prices are higher, they are higher on everything. Wages are also higher in a lot of cases also. Not for everyone of course.

My real concern here is that this chart of home costs does not show a comparison to money value today vs years past.

I sold a home in 2020 for $131 per sqft. I am having a home built today around $150 per sqft that’s much nicer. When I run the cpi inflation calculator it shows $131 in 2020 has the same buying power as $160 today making my new home cheaper.

Our money has changed. It seems that we need to compare dollar value alongside these charts to help people understand. Am I wrong in my thinking?

NO, you are not exactly wrong AZ:

RE, as always is very very ”local specific” and that’s why the old meme, “Location Location Location” still continues to resonate.

While Wolf, correctly IMO, specifies averages, either median, mean, or mode, to describe RE,,, in fact,,,,

”Results differ widely” would be the best way for everyone to understand what might be happening ”’LOCALLY.”’

Our hood, a very small sample now that I am walking rather than biking, has gone from rentals at about $1/month/SF to almost and sometimes more than $4.

Sales very similar since we and others purchased at or less than $100/SF to now $400/SF for old houses, and many are bought to tear down and build new with much more SF and those for more $/SF, as they should be, with even well done rehabs going for $500/SF or more…

OTOH, a couple long time renters younger neighbors just purchased across the street for less than $200/SF, but had to assist to remove decades of ”stuff” stacked to ceilings,,,

Local still prevails IMO.

“I sold a home in 2020 for $131 per sqft. I am having a home built today around $150 per sqft that’s much nicer.”

——————————————————————————

When people complain about high existing house prices. I would think just go to a builder and build a new house and you will be getting market prices….not inflated existing prices which the median prices that are now probably over $200 sq ft? Wolf has shown existing house prices are too high.

The existing vs. New build cost per sf is probably the most important equation in real estate finance – since it is pretty hard to see why 85% of the market would ever want to pay *more* for an *older*/faster deteriorating/depreciating house (with perhaps 15% of buyers willing to suffer that in exchange for “better location”).

New builds add supply and limit/eliminate price hikes – they are absolutely key in eliminating the insanity that 20 years of Fed interest rate/money supply manipulation hath wrought.

So long as “existing psf costs” exceed “new build psf costs” new SFH will continue to be built and sold, adding to supply. That is the core engine of why free market supply and demand works to lower prices in *any* product mkt under capitalism.

It is only decades of Fed f*ckery-pokery with interest rates that deranged the housing mkt in the first place.

Most new builds are out in the exurbs. That means more commute time and more mileage

AZ,

The cost of your new home does not include its current taxing structure. Your old house may have paid a different tax rate. Your new one may pay a lot more because property taxes are another thing that is out of control. You don’t know how much cheaper or expensive that new house is yet.

Right now, property taxes are impacting house prices. The mega landlords are selling properties they bought at good prices, but can’t rent because of the taxation. The taxing authorities are borrowing and spending like crazy and the taxes are eroding the value of property.

This is happening at the same time income has hit a wall for many.

What I’m seeing is the unskilled labor wages have kept up with inflation. This who were making minimum wage to the lower teens are now making $13-20/hr. Those in the top 20% have more income due to the stock market and interest income. Those in the middle who do not have much to invest and did not see the big pay increases are the ones hurt the most. Most of the money sitting in MMF bel9ng to the top 20%. They are the majority of homebuyers and that’s why sales are so low.

You also left out much higher mortgage rates now vs 2021. I was quoted 2.75% in November 2021. It’s now 7.37%

A $500K loan at 2.75% is $2,041/mo

At 7.37% it’s $3,455.

I only scrolled through a couple of comments and I don’t understand why there is never any mention, much less discussion about the what has become the giant elephant sitting on top of my and most people’s homes.

Home owners insurance.

My insurance company is not only raising rates every year but is threatening to drop me this year because my roof is now over 10 years old.

In the world of insurance a 10 year old roof is now considered “high risk “.

And I live in the Midwest nowhere close to the coast.

And then there is the cost of that roof.

It seems to me that the financial cost of “living the American Dream” is on unsustainable path.

How much will my insurance go up next year with my 11 year old roof?

This gets discussed quite a bit here. But it’s different in every state. It’s a total fiasco in Florida and California. It’s not so bad in some other states.

The evaluation by appraiser and purchasing power calculations by banks is

Main problem.

Housing should not be seen as an investment that profit is to be paid by next buyer.

Fanny Mai and FHA should stop buying loans that are not priced to affordable valuations relative to income levels of the general population.

Valuations should be at the original

capital and labor costs and with return based on that number escalated by ppi.

The boomers are passing off their retirement the backs of next generations.

Travis from real estate mindset social platform said that the local CADS are committing fraud with the property taxes and that’s why everything is so overpriced in our economy.I think it’s because of this current administration economic policy.

Several developers in my neck of the woods have finally begun building out large properties that they have sat on since ~2010. Mostly duplexes. Talk about bad timing, but I am sure the hedge funds will snap them up after the bankruptcies… 2007/2008 redux.

… Have you considered that maybe local developers know more about local real estate conditions than you?

Have you considered how many local homebuilders went bankrupt during the last crash? I’m a CPA and saw the carnage. I’m not saying it will be exactly the same situation this time, but homebuilders either build or go out of business. Most of these guys live beyond their means and keep very poor financials. They have cash flow problems even during good times.

Greetings,

In reading Wolfstreet and opening my eyes a bit, the price of my recent home is EQUAL to the home I purchased in 2001. The value of money has dropped, my $200k mortgage, in 2001, is now only 20K more in todays money than the 200K one was in 2001.

$200,000 in 2001 is now worth 360,000 due to inflation.

Weird

It’s even more intense than that, the currency debasement that is. Wage levels have kept a restraint on the escalation of inflation over the past 20 years, on most items. Except Gold. In 2001 gold was $279 and my wage might be $7 an hour. But in 2024 gold is $2750 but my wage is only $14 an hour. Housing inflation is somewhat subdued compared to that, but the nominal gold price is revealing of very substantial dollar debasement.

Correct IMO S:

GOLD, while not of any practical use now or in the event of calamity when only community will be helpful, is still an indication of the degradation of the USD as managed by the FRB to protect the bankster class and their owners.

It depends on the level of calamity. Are you talking about Mad Max collapse or Argentina style currency collapse and hyperinflation?

I’d be interested in an article that charts yearly wage growth and yearly mortgage cost and predicts when the two will match and how far down in price houses need to come to match now.

There’s another finance site that regularly posts a ‘housing affordability index’ based on median income and median selling price at current rates.

Of course, the issue with this is that the change in sales mix has been skewing the median price up.

No your home is not worth 360, it is back on its way down to 200 again. Look at what happened to Japanese housing to understand the future trajectory of you home’s price. Consumable prices – food, energy, health care, services, taxes will still rise as your home price falls. Historically, consumer wealth was buried, tied up in homes and not available for investment. The US govt fretted about this fact since the 70’s. Recent years of high home price inflation in fact turned that housing wealth into housing debt as you will discover in time. The US home is no longer the piggy bank of the past. Today it is a source of investment capital for those who hold the debt.

I recently bought a house and am quickly losing the equity I put into it. Most of the equity is gone in just three months. I knew this would happen but needed to move, so I did.

The other issue with the decline in equity is home owners losing the ability to refinance once rates drop. Equity is currently dropping faster than rates. Lower rates may not come fast enough to make a difference.

Overall, I see lower prices for next year too.

US has a higher birth rate and much higher immigration. The demand for housing will be higher. While housing could crash if there’s a hard landing, it won’t be like Japan unless we have a similar demographic collapse

The US housing stocks is growing a good clip. Every year, homebuilders are adding about 900,000 new single family houses and about 450,000 apartments and condos to the US housing stock. That’s over 1.3 million housing units added per year. If each unit is occupied by an average of 2.2 people, that’s additional housing for 2.8 million people added per year.

We get the Realtors Magazine every month. I read it to see how people in the RE industry think. If you do exactly the opposite of what they say in their publication you are more likely to be doing the right thing. The magazine is a pile of self serving propaganda, nothing more.

Ha…it’s like an old paper form of echo chamber on Facebook..

Nearly all wealthy Americans own their home. That’s why you read that rag…

How about the 8 million home “owners” who saw their SFH down payments/equity zero’ed out by foreclosures in phony RE boom 1.0, circa 2008-12?

SFH “ownership” was a real winner for them.

What percentage of Americans are wealthy? Maybe 10% or so. They can’t prop up the entire RE market

Always amazed at how well presented your data is. Great work and much appreciated.

Wolf – how high or low is the 1.39M homes on offer for sale on a historical basis, not in terms of months’ supply?

The highest in 4 years. But that doesn’t really matter that much. What matters are these two things:

1. Inventory jumped in September, when it normally falls in September. Inventory normally peaks in June and then declines every month for the rest of the year with the low point in December. But this year, every month since June, inventory has risen, instead of falling. Those are the vacant homes coming on the market even as demand has wilted.

2. Inventory in relationship to demand: months’ supply, which spiked because inventory has surged even as demand has plunged.

This phenomina is similar to a bear that should go into hibernation, but to the surprise, is still out and about rummaging for food because its not stored enough fat yet.

If the bear stays out much longer we’ve got a problem.

Houses are still selling, 3.84 million sold, its a good snack but not good enough to fatten the bear.

Hi Wolf. When does this increase in inventory and destruction in demand impact the new housing starts and post that employment in the sector? Some thoughts based on your historical data insight.

Thanks

Article on new houses coming. They’re building a lot and they’re selling at a good clip. They’re doing it with lower prices and costly incentives and mortgage-rate buydowns. New houses are now less costly on a monthly basis than an equivalent existing house. And so demand for existing houses has shifted to new houses and rentals (including new build-to-rent). Selling homeowners are losing market share to the pros who are offering better deals. That’s what you’re seeing.

Wolf – in response I get #1. Asking what the historical level of homes for sale are — for instance compared to during the housing bubble in ’08 etc — because #2 will surge even if inventory stays flat but sales plunge further. So months’ supply is not just a function of supply but also demand.

Also curious if there’s any data that tells us how many vacant homes are on the sidelines and available, potentially, for sale ? Is it a 1M homes or much less?

I’m calling it right now: 2025 spring “selling” season will end up being one of the worst on record due to delusional sellers that refuse to come down to earth.

Let’s hope so..I would love to see this spring season being the first where sales and volume are lower than winter… that’ll be something

Split this answer into two categories existing home sales and new build construction.

New build construction will but rates down and entire consumers to their direction. These buy downs are more enticing than traditional methods.

Existing homes, I’d love to see a correction. It’s time the lipstick on a pig treatment stops.

I do standby still saying wages must increase. It is a very real situation here where mortgage rates could exceed 7% even 8%. The rate cut was the fed indirectly favoring inflation over all right deflation. We will see soon.

‘Bright’ Research commentary for October 2024 states that:

“Falling mortgage rates in July and August were expected to bring more buyers into the market, but some home shoppers may be holding out for rates to fall further. Others may be taking a wait-and-see approach in the lead up to the Presidential election. Year-to-date, overall home sales activity is tracking at about 2023 levels.”

Nope, no mention of home prices.

“What are the downside risks to the performance of the housing market in Q4? Affordability is still a real challenge. Even with lower mortgage rates, some prospective homebuyers are still going to be priced out.

If inflation takes a turn and mortgage rates do not come down, home sales could be lower. If the economy weakens significantly, there could also be a slowdown in homebuyer demand. However, neither of those prospects seems very likely. ”

Still no acknowledgment that sky-high home prices are the main culprit. I mean, *some* home buyers may be priced out right now, but apparently most are not.

/facepalm

And even with the buyers that aren’t priced out why would they buy right now? Rent is always an option and given competing places to put their money why would they?

I see some of this simply as people had mobility before, as they might have wanted to move and could without a huge impact. Now moving to a nearby town, up sizing or downsizing, moving to a new school district suddenly is more expensive. I was in the process of moving from Sacramento to Portland for not any particular good reason other than a change and stopped plans. People in Oregon probably don’t want another transplant so positive on that front!

Oregon is mostly California transplants. Portland is great for that… Bend unfortunately, is full. 😀

The adventure of Glen going nowhere…staring…Glen.

My conclusion is that some elected official will ride in to rescue the housing dansel in distress and get her killed in the process….they can’t help it.

Maybe cash for clunker houses to thin the herd.

Don’t joke about “cash for clunkers” in the housing market.

It is only a matter of time before some DC genius suggests destroying “inadequate housing” (lowering supply) in the name of “stimulus”.

It’s anecdotal, but a lot of homes cut prices a bit and are moving in my Chicagoland area. I don’t know if October will be as bad as this, even with the higher mortgage rates.

The truly impressive thing is that these low sales — which match 2024 levels with the equally low 1994 levels — have seen 30 years of frantic housing construction across North America (Canada & U.S.). There is an even greater supply of housing now than there was in 1994. That tells you something about how demand has fallen out of the floor of the marketplace …

Thanks WR for this report.

Home prices need to fall a lot for them to be remotely affordable.

In my neighborhood, home prices increased by 100% plus post covid which is just wild.

Coming Spring would be entertaining for sure.

Here’s what’s delusional! I’m 70 years old. Been in some form of professional Real Estate since I was 12 years old. Have seen every peak and valley in our U.S. markets since I was young and can tell everyone that the Marketplace is always driven by 4 things: a) Supply b) Demand c) Available Financing/Money Supply (Not so much rates) and d) the biggest Metric which drives everything

irrespective of rates is “LOCATION/POPULATION MOVEMENT/GEOGRAPHICAL DIRECTION”

Re: “With wage growth now outpacing home price appreciation, housing affordability will improve”

I guess that’s one way to say home prices are crashing.

Zooming out just a tad, wage growth spiked a bit for a year after the depth of the pandemic, but overall wage growth is anemic and normalizing to new levels that don’t support outrageous home prices.

The level of cheerleading by NAR is totally inline with Fed cheerleading and rate cutting — and of course, Wall Street would have you believe earnings growth is strong — even though S&P 500 Shiller Cyclically Adjusted Earnings Yield have crashed 15.4% YTD (according to ycharts).

In terms of wage growth as a metric, it’s probably something that doesn’t matter — this time is different!

there’s one main difference between stocks and houses. stocks are easy to own with no carrying costs, so the top 1% hoarding most of them and unwilling to drop their asking prices doesn’t really mean anything to the larger market, as long as someone is willing to buy.

whereas with housing, the top 1% can’t hoard too many houses, as it just costs too much to maintain them. so they might not be in a rush to sell, but eventually, they’ll start asking why they’re paying several thou a month in taxes, mortgage, insurance whatever and dropping prices. the drops tend to become an avalanche in a crash.

Agreed.

On a semi-related note, it is interesting just how much SFH speculation (via interest rate changes) is basically similar to plain ole bond speculation (via interest rate changes) – except home speculation has a ton more transaction costs.

Both home prices and bond prices have an inverse relationship with interest rate levels (prices up when rates go down, prices down when rates go up).

If only newbie speculators had realized this, a lot of macro harm would have been avoided.

It seems like sellers are in no rush to sell (keeping their asking prices too high), and buyers are in no rush to buy (not willing to pay crazy prices). At some point something has to give, and it will be the sellers, perhaps pushed along by a recession. But there is no sign of recession now, so the market will just be sort of stupid, as it has been the last couple of years. Some leaks have appeared in the dam (the dam being the damn sellers). I am waiting for the dam to burst. It should be glorious, for buyers.

Buyers can wait it out by renting and save money.

In my neighborhood for example one can buy as home and pay 11k per month for all expense of rent the same home for 6k.

Sellers may need to sell for many reasons death divorce relocation etc.

“So now it is blaming, you guessed it, the election:

“Perhaps, some consumers are hesitating about moving forward with a major expenditure like purchasing a home before the upcoming election,” the NAR said today”

These fxxking people, if there’s a gaslight of the century award, they would be right up there on the podium along with Tobacco and oil industries.. they are going to shill as long as they can but 50% up in last couple of years, under what universe is that normal?

Still long long long way for price to come down in expensive markets and let’s hope a pathetic 10% price doesn’t all of a sudden entice buyers to start biting..I say maybe 30 to 40% correction then you’ll see more fair value even at 6 to 7 mortgage rates

After the election they’ll move on to blame climate change, lol.

“They” are already blaming climate change indirectly. Article in the SF Chronicle is headlined “There’s a new deal-breaker in California real estate purchases.”

Miatadon,

They’re blaming a real problem: crazy increases in homeowner insurance premiums, and the difficulty of even finding homeowners’ insurance after big insurers have refused to renew many policies and pulled back from some areas. Similar thing is happening in Florida and other parts of the US. Insuring a home against disasters is getting increasingly expensive. And lots of deals are now falling through when the buyers find out they cannot get insurance or cannot afford the insurance they can get.

One of the big reasons for the insurance fiasco is that replacement costs of homes have spiked by 50% or more in just a few years. No one was prepared for that.

NAR National Association of Rodents ?

That would be a more fitting name IMHO but then it will be an insult to rodents

“but 50% up in last couple of years, under what universe is that normal?”

One in which the central bank printed a f”*ckload of money, maybe?

Look, no one hates realtors more than I do. But they don’t set prices, they don’t write checks to buy, etc., they only have a minor and EXTREMELY annoying influence, not much different than those ridiculous auctioneers at car or whatever auctions. BLAME THE BUYERS.

Oh trust me, I do blame the buyers and hate some of them just as much if not more, like the ones that bought over bidding everyone at above asking price during the last couple of years or the ones that come in here complain about high prices yet still put in an offer at ridiculous price and bitch about getting outbidded and wonder why price is so high…

Toxicity only thrive when there’s enough enablers to support it. This is true with this housing market, true for toxic relationship or narcisscists to get away without consequences.

If I hadn’t “overbid” on a property the day it went “coming soon” back in 2021, I would never have achieved my dream home in the perfect location; not only have prices risen dramatically, but every other house that’s turned over in the last few years has doubled or tripled in size. And I’ve lived in this town a long time; I didn’t want to be priced out of my own town.

I mean, we gotta do what’s best for ourselves, because other people will run you over.

Also, neighbors immediately told me I paid too much. They were wrong, obviously. And we don’t know if 2024 buyers are wrong or if we’re gonna get another blast of QE next year and devalue the dollar further.

Just want to add, had I missed that (last) opportunity, I’d be crying like a Millennial as well (quite seriously).

musssyke, they were wrong, now in retrospect, but if the housing market crashes in the next year or two and drops by 40-50%, will they be wrong then?

Franz,

Don’t know. Don’t care. I have the house I’ve been trying to get for years, and I bought it with free money. No debts for life.

Honestly not bragging. I know it’s not fair. And I do sympathize with people who legitimately got screwed.

free money? did you rob a bank or something?

@MussSyke yeah you are the kind I am talking about and the embodiment of Covid/Post Covid FOMO mentality…

Franz,

Well, I was BSing a little bit to irritate the Bird, or keep the conversation going.

I earned some extra doing special projects early on. It just quadrupled itself in regular index funds so easily…not nearly the hard work I was told making money would require. It feels free.

That said, lots of dudes where I work who didn’t do the extra, and if they did, bought rims for their cars or whatever.

You gotta wonder, if God himself told people their money would quadruple in a decade, would they manage not to squander it to get the big payout, or just go broke buying iphones and crap anyway (not that I don’t have a decent phone, but you get the drift)

Well, the real-estate industry had a hand in it. “Housing is your best investment”, blah blah, blah.

Call it what it is. houses are money pits. the only investment where you have to keep throwing money at to try to maintain its value.

Im a money pit as well, all that food I eat costs a good penny, hair cuts, health care, dentists, lice treatments. If you care and like something like yourself or your house, you spend money to maintain it, and it cares for you.

Exactly

Supply up 23%…so much for”housing shortage” that I constantly hear.

It’s a BS narrative that’s about as valid as why there’s solid fundamentals that 30-50% up in the last 2-3 years is the norm as they say….or how the last 08 crash was all because of foreclosure and nothing else. It was a catalyst for sure but prime borrowers back then were defaulting too and affordability was also an issue last cycle…but those points are always left out in RE talking points

Anyone hearing of homeowners/Sellers refinancing, taking the equity, then walking away… essentially selling the house back to the bank?

It’s clearly appearing that the current crop of homeowners who’ve listed their homes for sale are stuck in the old economic model that a home was a safe investment for making a huge windfall in a few short years. Does greed play a part?

The new model has fully emerged in that a home is no longer an investment, but a place to live. Thus the Buyer’s Strike.

In terms of your first sentence: if someone does that intentionally, as you indicate, it’s mortgage fraud.

Maybe if you are bouncing back to a foreign country that doesn’t have reciprocity for banks? There was some guys in my area that were wanted for other things that Heloc’ed their properties to the max before trying to go back to Pakistan. They were stopped at Dulles airport. If it wasn’t for other things and existing issues they probably would have made it.

Why did they get stopped at Dulles?

Why would anyone do that?

Most banks only lend 80% LTV.

Refinance and walk away from 20% equity?

Wall Street Journal has an article showing Home Equity is now 35 trillion. They said this comes to about $400k per homeowner. Not sure how they get that number.

Of course it depends where you live because my home is only worth $415k. and the median home is selling for around $400k.

Anyway, they think there is going to be a Home Renovation boom as people hit the home equity for renovations.

HD to $500 or more!

Yes, please.

Those renovations were done during the pandemic when people had time off and free money.

Everyone still has tons of free money, and now contractors *might* have some time. Multiple houses on every street being doubled or tripled in size. One big house is spending $600k and not even adding any space…

My friend who is a renovation contractor is very busy.

Anyone with boots on the ground knows how expensive it is in renovating anything.

Want a 12 x 14 elevated deck replaced. 4 bids were between $40k to $65k. (for a deck?)

Want to replace a standard window with a builder grade window. $600. double or triple this if you upgrade the window quality

Paint the exterior of your house. $10000 to $16,000 for a normal two story house.

My contractor said a house they are working on was hit by hail and the many windows needed replace. They were not standard size windows so all need to be custom built. Pella came back with a bid of $215k and this is for a 1600 sq ft house worth only about $800k .

I need a small basement window replaced that needs to be custom built. $830.

Boston housing will be one of the biggest price crashes the world has ever seen, eventually. City is sinking, younger people can’t get on the ladder and lots of big old houses no one will want or need. Also, too much traffic and shitty weather for much of year. Trust me, it’s a powder keg.

To the moon baby….I guess at $35T, you can see why people like to argue the FED or government cannot let the housing market adjust down or let alone fall…another too big to fail for you…at least that’s the argument that camp will use anyway,..

My oldest builders are back to doing remodeling.

They were able to let go of the occasional want to work guys.

Let the youngsters chase the new construction with the lowest bid.

50% Wolf? How about 100% and drop of 5% still leaves houses 95% overpriced, so you are damn right we are still on strike. The quantity and quality of the dog sh•t flips in my so cal beach town is appalling. Junk all day long for fantasy prices because a $13k monthly payment is totally normal. I love the people who have the house they paid $1m+ a year ago for $500k more because real estate only goes up right? Long way to go and nowhere to go but down.

New roof, new water heater, and the school taxes are going up, up, up.

School taxes go up and the kids are getting dumber

It isn’t that they are dumb. It’s they are not educated. It is we, the elders who are dumb for allowing this to happen.

Candyman – triple check, but YOLO-think (overt or covert) is a very strong countercurrent to a heretofore traditional ‘Murican paradigm…

may we all find a better day.

The housing market is not exactly liquid, however. As an illiquid asset (you have to live somewhere), a game of musical chairs gets played whereby each asset is sold and another one picked up again right away. It’s a zero-sum pie.

No, because prices are always set on the margins. The margins on the selling side are set by elderly and/or deceased people who must sell, and speculators who cannot afford to sit on a loss. The margins on the buying side are younger people – first time buyers, second-home buyers, and speculators.

The “trade this for that” owners you are thinking about net to zero in the accounting, but they aren’t the ones setting prices.

Holding a house the last 2 years got you crushed compared to dumping and getting the proceeds in the markets.

Yeah but having a roof over your head and a place to sleep is pretty nice.

Unless your broker lets you sleep in their lobby.

Main reason for this is from companies like Lennar over crediting buyers to buy their homes by offering rates existing home sellers legally can’t do! SOMETHING they can’t legally do either but they are hiding the credits and not showing them on the closing statement. Because of the greed of 1 all other track builders are following suite and making it hard to sell existing homes at much higher rates. CFPB DO YOUR FRICKEN JOB! IVE LEFT NUMEROUS MESSAGES!

Sure you can Brent. If it’s paid off, owner finance it at whatever rate you like.

I’ve done it many times. But, gotta say, the rate was never lower…

The down payments were 20k and rate was 10%.

In each and every case, I showed the people rent to own is a terrible idea. In each and every case, they didn’t care and did it anyway.

I learned years ago that I am not responsible for another’s poor decision nor am I required to pass over an opportunity.

Agree or disagree, I’ve made a lot of money with a clear conscious. 1/13 people actually end up keeping the home.

Pilotdoc,

Could you put some alphanumeric stuff in front of or behind the number in your email address? All your comments end up in moderation — and I think the reason is your email address.

Would the Fed purposely move the 10 year higher to keep the mortgage rates high in order to reduce these ridiculous prices? And what about the real estate tax rate tied to the EVA factoring.Home ownership sucks, at the current price points.

I’ll give it to you Wolf, always keeping us thinking!

The rates on 10 year US Treasuries are established by the free markets and the Federal Reserve has nothing directly to do with that at all. Those yields are what are most influential of mortgage rates plus about 3% and they will do whatever the markets so decide.

I think the key word is “directly” because their business model is to manipulate the “free markets”.

Not that there’s anything wrong with that!

“free markets”, as Wolf says there was interest rate suppression, reserves for T-Bills.

you’re right if they’re not printing money. if they are printing money and buying 10 year treasuries, then they obviously are affecting that market.

Not really the Treasury controls the amount of new supply issued at ten years.

They could spike the ten year yield by going heavy long at the 10 year point>

The Fed doesn’t control the 10yr yield, the market does. The Fed understands that overpriced homes and locked-out first time homebuyers is disastrous to the country over time (think declining birth rates, increasing populism, etc). The Fed will continue to lower rates as inflation is gradually abating, and accelerating job losses remains a real threat to their dreamy “soft/no landing”.

Remember, the Fed forced the 10-year rate down to less than 1% a few years back. Monetary authorities can influence long rates through open market operations and autocratic statements like “we’ll do what it takes”.

true but there was stupidity on the part of private actors too. the fed buying 10 year bills drove up the demand for them, increasing the price. but nobody forced other investors to go along. they could have said “sorry, but we’re not buying 10 year treasuries at under <1% yields if you wanna do that, you need to become like the bank of japan and buy all of them such that none actually move on the free market."

but they didn't. these idiots greedily gobbled them up, thinking they could flip them for a capital gain when rates became negative.

it was abject stupidity.

Re: “ The Fed will continue to lower rates as inflation is gradually abating”

I’m seeing several signs of very sticky inflation, like today, looked at Proshares Inflation Expectations Etf (RINF).

It’s a tiny barometer, but it tends to lead the 10 yr and it’s headed upward, as is the 10.

In general, the macro environment is inflationary and the total lack of concern from anything related to the election cycle — screams deficit and treasury issuance and future inflation — however, I think this episode of inflation is somewhat transitory and not a long term crisis, as in years ahead.

We’re at an inflection point where a lot of things are close to breaking and I suspect, this narrative of hesitant buyers is going to be a dominate theme for many months, as people look for safe harbors.

The Fed cutting is part of the trifecta that a lot of people are praying for — huge rate cuts, tax cuts and anything to keep the equity bubble in parabolic ascent.

The deficit can triple as long as people see their wealth rising. Who cares?

Really depends on the dollar/eurodollar flows, especially in light of the trade deals being established by the BRICs nations. For now, the is still plenty of demand internationally for the dollar, but there will be no saving us if all the dollars out there come rushing back to U.S. proper, especially if they are coming back in exchange for energy/chemical assets. Demographics, and TRADE matter, probably the only thing that really matters in the long run.

“a lot of things are close to breaking”

I’ve been hearing that since the Fed started hiking in ’22.

Short – …semantics. ‘break’ as in a total fracture, or more akin to multiplying leaks along a pipe?

may we all find a better day.

I’m imagining what the chart would look like as “existing home sales per capita”. About 30% more people in the US now than back in 95’

“per household,” I guess would be better. Yes, it would look even worse.

“Perhaps, some consumers are hesitating about moving forward with a major expenditure like purchasing a home before the upcoming election,” the NAR said today.

LMAO. Imagine actually believing this. Only an economist could come up something this ridiculous.

Are there any statistics on the percentage of all the housing stock that has turned over in the past 4 years and the implications for what would happen when that many homes are upside down with negative equity?

I’m not sure if this qualifies as irony, but…

John Rubino, in his latest substack, posted a number of “arguments” for why we’re about to enter a recession and the fed will be “forced to do QE” (I know, I’m sick of that phrase too).

In his last volley, and right above his concluding paragraph where he says blah blah blah QE, is a reference & link to… Wolf’s 1 Oct article on the epic office glut.

https://wolfstreet.com/2024/10/01/epic-office-glut-hits-records-in-san-francisco-atlanta-chicago-los-angeles-seattle-washington-dc-dallas-availability-rate-dips-to-30-houston-rises-to-29/

NB: I don’t usually read Rubino’s stuff, but the article was titled ‘Bonds Don’t Trust the Fed’ so I was intrigued; instead it was just a bunch of anxiety about higher rates and general QE-mongering.

All due respect to WS and various posters…. I don’t get the whole “unaffordable” thing, and how the market is frozen or whatever terms you want to use. Sales are down 20-25%, not 90%! PLENTY, as in MILLIONS of homes are still selling. Those buyers may be idiots, or who knows. But there are still plenty of them.

I figured our area was pretty dead. Then I looked at recent sales and pending. It’s pretty much within normal ranges, and this is a pop 100,000 area where the median is >$1m, with tons of sales $3m+.

If Apple’s revenues plunge by 30% from one year to the next, it’s not a nothingburger but a full-blown catastrophe-burger for the stock and for the S&P 500. I’d love to be on that earnings call.

So long as the stock markets are near all time highs and employment is at or below 4%, there won’t be a residential RE crash.

All that we are seeing now is a little air coming out of the bubble. This will likely continue for a few years unless something pops the bubble.

No one has a crystal ball. None of us can predict how this plays out.

In certain markets, e.g. Florida, residential RE has already crashed.

Really depends on IF the RE flooded or was old and wind damaged shorty,

Here in our high and dry hood it’s still going fast, and new replacements being built too…

LOCATION x 3,,, as always.

Look carefully at almost every beach scene and you will see NEW construction is OK even when all the old stuff nearby is gone.

Anything built before actual implementation of at least the 1994 codes MUST be considered a ”tearer downer,” and priced accordingly. Same for almost all mobile homes, though it IS possible to make them a ton more resistant to winds than is usually done.

All the older houses in this hood are just that, and the new ones have had no problems with any recent storms.

Yeah good luck with that….Tesla up 21% so far today…that animal spirit and people tie to stock market and Crypto wealth will be here to stay for a while sadly..

A 20-25% drop in sales in an illiquid market can still be considered substantial. People can trade one overpriced asset for another and I still wouldn’t consider the market “healthy”. What’s on the decline are first time buyers and investors. That the inventory is still rising shows prices are high compared to demand.

“Sales are down 20 to 25%”

Wolf says 20% of those missing sales could be from those not selling or buying (not putting house on the market). If that’s the case then the inventory of homes would also rise 20% as well but I’m now getting confused so…. sayonara.

fter the election they’ll move on to blame climate change,

Pricing should be falling significantly, yet here we are…. I think people still have the idea they can wait on the fed. We need some sort of event that instills panic in sellers.

Similarly the Denver metro had its biggest apartment building boom since the 70s, yet zero price drops despite net out population migration in the last year. Prices actually slightly increased. Lots of new buildings with super high vacancy rates as I drive around. They’d rather leave them vacant or offer 1 month free than cut rent because they feel they can wait this out…

I notice a lot of apartment towers in Boston with a significant % of apparently-vacant units, implied by all the dark windows at night…

I’ve wondered how these property managers are able to make money with such high vacancy rates. I think I heard once that they get tax breaks on the empty units but never looked into whether or not that’s true.

“I’ve wondered how these property managers are able to make money with such high vacancy rates.”

Um, they don’t? But have you considered the even more obvious? That maybe those units aren’t actually vacant?!

Being a landlord isn’t rocket science. You rent out as many units of your unit as possible. You adjust price until you fill the unit. If you can’t achieve enough in prices to pay the bank loan, you hand the building back to the bank.

Tax break on empty units… That’s like saying I get a tax break when I make an unprofitable trade!

I can’t believe the conspiracy mindset that prevails around real estate, landlords, and developers. It’s just business! Normal capitalist enterprise! Why all the counter-enlightenment sturm und drang?!

Just check Miami metro area, (weeks’ supply 44.2 from Redfin) , it could be the highest number in US, over 20% from last year, homes sold -26.5%

Miami is overdue for a correction. It’s a fairly poor city with few high income jobs but popular with tech bros and overseas buyers. Not exactly a solid foundation.

Well I think the problem here is not the regular buyers like you and me who offered below asking price to negotiate the price of the house one big problem is the realtors didn’t actually sell houses they auctioning the houses to the higher bidder trying to get more commission. In my opinion it should be a law to prevent this type of abuse to the regular buyer. Now big corporate have all this power and can hold the house we want and make the economy crash into they get they over price house money.

A law that if you offer you house for sale you have to accept the highest offer, no matter how low it is relative to your initial asking price?

What kind of “capitalism” would you call that? What kind of “freedom” would you call that? Sounds like “cap talisman” and “free dumb” to me.

I’ll add my own anecdotal experience here, based on what I’ve seen when I’m in the field examining new construction sites: builders around here seem to be throwing houses up at an astonishing rate, but *not* breaking new ground on lots they own and have slated for future construction. It’s almost like they want to get rid of existing inventory as fast as possible but aren’t committing to future construction…at least not as much as they were just a few years ago.

“Much lower prices would stimulate demand – and commissions for Realtors because they’d make more sales. Why is this so hard to come to grips with?”

Thanks for stating that truth Wolf. Part of the NAR’s hesitancy in discussing that issue is the myth they’ve helped to propagate that residential RE is a good investment. Many residential RE agents have been making that claim that for years. So, a formal statement from that group saying the solution to the current situation is to drop prices may appear hypocritical. What happened to my good investment?

As many financially astute posts on your site have previously noted, agents ALWAYS use nominal gains in their “good investment” claims. “He bought his house for $300,000 and sold it four years later for $375,000.” Ah, OK. But the real return on that investment would account for such items as inflation, selling expenses, maintenance, repair and improvement costs.

Take all those into account and residential RE is often (not always) a losing investment. The real return is far below the nominal – it may not even be a positive number. Even after accounting for the mortgage loan interest deduction.

Another item that may be affecting the current pricing is that sellers who paid “bubble prices” must now get a certain price or go underwater on their mortgage loan. And that certain price may be above what the market is willing to pay now. Many buyers are sensing the market is changing and will continue to take a “wait and see” approach to buying.

“Take all those into account and residential RE is often (not always) a losing investment”

————————————————

So true. One of my rental houses I have owned for 20 years has a P/L of -$22k over the 20 years because of a couple of bad tenants along the way which required a complete remodel. So when you only were collecting $650 a month in rent ($7800 year)) and after taxes / insurance and your profit is about $5k/year but the tenant ruins all the carpet, doors and kitchen counter doors and it takes $15k to $20k to remodel, that is 4 years of profits gone. Then have a couple of tenants do this. Plus, I basically kept rent at $650 from 2002 to 2020. The house value never went up for those 18 years. What hurt was renovation prices kept increasing YOY.

Luckily for me, this area is now hunting grounds for large investors who are buying up and renovating with granite counter tops and stainless steel appliances. I get mail and calls daily from investors wanting to buy this house. The house has doubled in appreciation 4 years. (from $58k purchase in 2002 to $130k to $140k value today). If I sold today, I would finally see a little profit on P/L from the house appreciation. Not much to brag about and not worth the headaches. I would not do it again.

My wife kept telling me to sell it but I said, it cannot stay at the same price forever. It will eventually go up. Hahahahaha. It only took 18 years.

So there is a lesson in this story somewhere. ;)

What were your house payments on that $300,000 home?

I really don’t understand why anyone would buy a house right now.

I rent my place in San Diego for $4500 per month. A purchase of a $1.5M home at 6.5% would result in a payment that is more than double my rent payment. And I have no maintenance costs or anything else. I call the property manager and they have to fix it.

Asking prices would have to dip at least 40% with the current mortgage rates to even make buying be appealing. I make more than enough to buy and am fully prepared to when the time comes. But there is just no reason to at the moment.

A lot of my coworkers did buy in the last two years because of rate cut mania. They told me rates will come down and homes prices would boom again. Not sure how they feel not but I think they way overpaid for their house.

And many employers have started the return to office policies. So many of the remote employees in my neighborhood are going to have to either quit of move states to stay with their employer.

There are lots of people that are now arbitraging, like you’re doing, the big cost difference between renting and buying, which is in part why demand for existing homes has plunged.

Doesn’t that support the idea that there’s a considerable floor to housing market? If lots of folks are sitting on the sidelines while renting, won’t they rush back into the market during a dip and keep the whole thing afloat?

So sure, a 10% or 15% decline in current prices might spook people, but there are plenty of folks out there with the cash and desire to own their own place. Just not at these prices obviously.

If prices drop far enough — by a whole bunch — to where buying is a better deal than renting, people who do that sort of math will switch to buying. So that would be an increase in demand.

I’d be more than happy to buy if it made sense. My last house that I bought resulted in a mortgage payment that was about $1500 more than renting. I could deal with that. But paying $5K more just to say you own while getting killed in interest and maintenance costs doesn’t make sense.

Agree and yup because math is hard for a lot of people, especially ones that let their emotions do the buying rather than some common sense math comparison. It’s the same way how car dealers always want you to talk about how much you can afford a month, rather than how much it is OTD, that’s how people get bend over happily over and over again..

One look at SD or LA, I can rent at $4500 or pay $600- $700K downpayment to buy a similar place and still pay that much if not more on a 30-year mortgage…..hmmm no brainers there but a lot of people don’t run on a rational MO, plus to them, who wants to be a poor peasant that’s not part of the homeowner American dream class? They don’t want that stigma of being a renter class…

I’m literally in the same exact position — and live in San Diego as well. I have plenty of money — a great secure job — could afford to purchase — but it simply doesn’t make sense — when it makes sense I will — but for now I’ll continue renting – I’m sure there are many like us — but I guess it will take a while for things to figure themselves out — I feel the people that bought in the last couple of years — with payments being $5k and above — and that’s minimum for a simple 2 bedroom condo — will have some issues with those payments —

Yes, there’s so much pent up demand like this that we’re facing an impending tidal wave of buyers that will come off the sidelines when prices dip even a smidge. That’s why yesterday Barbara Corcoran kindly informed us that it’s the “very best time” to buy a house, but we only have “1 month” to buy before the surge! 😂

Headline: “You Have One Month Left to Buy a House, According to Barbara Corcoran. Here’s Why.”

How many sqft and what kind of amenities are you getting for $4500/mo? If you don’t mind me asking.

I’m continuously blown away by how expensive Cali is. Even renting in overpriced Boston for 8 years, my rents were only between $1800 and $2500/mo. And I always had at least a couple roommates to split the cost with.

Personally I never paid more than $625/mo for rent, except the one year I rented a penthouse and paid $1300/mo. My first apartment in 2013 was a single room for $450/mo.

SD is probably similar but for not so nice part of Long Beach, $4500 doesn’t go a long way, maybe a 80s style condo, 2 or 3 bedrooms, nothing fancy to get excited about…once in a while, you’ll see kind of nice house for rent near the ocean for $10k and it will still be kind of a tiny house..

I rent a 2500 sqft house that is about 35 min from downtown San Diego. I live 20 miles east of the ocean so it is just a boring suburb where a bunch of other commuters live. The housing in the beach towns is significantly more expensive.

It’s not just San Diego. There are many other markets around the country where it is now way cheaper to rent than own (especially when you start considering things like maintenance and insurance). This is a complete shift from prepandemic where it was usually a bit cheaper to own than rent.

Plenty of people still insist on buying though, even though it’s not in their best financial sense to do so.

Is it “momentum”? Momentum of house prices going up for so many years (decades?) and just being “expected”. On the other side, the momentum of inflation and mortgage rates acting to reduce potential buyer’s resources. Both pulling sellers and buyers in the opposite direction.

At some point does the momentum acting on both fizzle out and the pricing and buyer resources begin to return to levels agreeable to sellers and buyers. Guess we’ll just have to wait and see.

I can’t help but see a metaphor between home price greed and the ongoing H5N1 flu contagion hitting industrial farms that create the perfect environments for pathogenic mutation — one might suggest that the mutation of greed in the housing market is like a pandemic — and thus, that disease will need to be managed, by culling the prices.

From NYT:

““They have weaker immune systems, because bless that fat little turkey’s heart, they are morbidly obese,” said Mr. Reese, 75, who pasture-raises rare heritage breeds. “It’s the equivalent of an 11-year-old child who weighs 400 pounds.””

What we have here, are morbidly obese housing prices!

yeah but look at how long Murica has been morbidly obese literally speaking, so this kind of stuff can go on forever and become the norm…plus there will be a lot more pain to get this housing market back to shape so to speak in comparison to our actual obesity crisis..do we have the tolerant for that kind of pain?

Long story short, there will be a lot of headwinds for the housing bears out there. Many more people are counting on the house of cards to go up forever than the number of people cheering for a crash or, heck, even just back to fundamental value.

The 10-year and 3 month are getting ready to Un-invert, so plan accordingly.

I am buying NVDA at these bargain basement prices

Healthy economy as per Mr Wolf, so no recession. Maybe a tickle more inflation. AI is a good investment. Do it for the environment!

You may want to see an ophthalmologist about seeing just a trickle of inflation.

CPI in uptrend, heading higher, dragging 10yt higher, confirmed by many barometers, including:

Quadratic Interest Rate Volatility and Inflation Hedge ETF IVOL

IVOL is not in the inflation trickling down mindset.

Treasury futures are pricing in higher for longer inflation and obviously, increasing deficit is trickling up substantially.

AI says:

“According to Google’s latest environmental report, its greenhouse gas emissions increased by 48% compared to 2019, with the primary cause attributed to increased energy consumption in their data centers”

Wow that fund has done poorly over the last couple years.

The Austin chart kind of looks like it’s giving us the middle finger 😆

This is the key statement in the NAR report.

NAR: “The inventory of distressed properties, which can often create deals for buyers, remains minimal because the mortgage delinquency rate remains very low.”

Not key, it’s what we’ve been saying on a quarterly basis for a few years: With home prices having shot up since 2020, trouble homeowners can sell a home, pay off the mortgage, and walk away with some cash before they fall too far behind, and it never even gets to a foreclosure. Where this no longer works is in markets that have seen home price declines since 2022, where the troubled homeowner bought near the peak in prices and then cannot make the mortgage payment due to loss of income. If they didn’t make a big down-payment, they’re in a negative equity situation. Subtract sales expenses, and they’re in a hole, and cannot sell and pay off their mortgage. But this is a very small number of homeowners at this point.

https://wolfstreet.com/2024/08/07/here-come-the-helocs-mortgages-the-burden-of-mortgage-debt-delinquencies-and-foreclosures-in-q2/

small number yes but probably a bigger percentage in some of the most bubbled markets.

whether that’s enough to make any real difference remains to be seen.

The labor market remains robust. No job losses = no forced selling.

I am still a cash buyer looking for home with a lot of land…..sigh,am still on buyers strike.

How much of a deterrent to home sales are capital gains taxes? The exemptions have not increased since 1997 when the taxation of home sales underwent a major change. In two cases in my California suburb, senior owners actually left their homes empty when they moved into nursing homes. Others brought in a full time caregiver or an adult child. When the owners die the homes passed to their heirs with no capital gains tax and probably no estate taxes. The capital gains tax is a big deterrent for me to downsize, as I would have to come up with a lot of cash to make the trade work.

couples get $500k in free capital gains on their primary residence, so the vast majority of homeowners don’t have this as an issue.

I see the housing market right now as something akin to one or two moves before checkmate – you can move, but you know in another move or two, you are totally screwed. TOTALLY SCREWED. So, here we are – buyers on strike. Sellers high on opium, reluctant to lower prices to reasonable levels. The Fed and the government know checkmate is around the corner….maybe around the election. 🗳️

Wolf,

With the Annual Sales of Existing homes in millions chart falling to values not seen since the 90’s, I’m curious how much worse that chart would look if it was relative to the total number of homes and the population, both of which are certainly much higher today than 30 years ago.

i.e. Sales of Existing homes as a percentage of Total Existing homes

Another commenter mentioned something similar.

Home sales as a % of households would make the housing market look even worse from the larger denominator.

I live where there is NO gravity. Physical laws repealed.

The record $2700/sf sale was (almost immediately?) outdone by a $3000/sf sale on our property.

Of course there’s a huge HOA on top of that. The new owners arrived yesterday for a visit and were ecstatic!!! Cash buyers of course (to the tune of $8-12.8 million on half dozen different transactions on the property).

I call it ridiculous and job security.

Year-over-year in my hot Southeastern market, months of supply is up a whopping 62% but median sales price is also up at 2%, and median sales price per square foot is unchanged.

So wake me up when all this supply starts affecting prices. At the end of the day it all comes down to the price of the asset and apparently when it comes to real estate the laws of supply and demand have stopped working.

I see the housing market right now as something akin to one or two moves before checkmate – you can move, but you know in another move or two, you are totally screwed. TOTALLY SCREWED.

So, here we are – buyers on strike.

Sellers high on opium, reluctant to lower prices to reasonable levels. The Fed and the government know checkmate is around the corner….maybe around the election.