The “war for space” before the pandemic unravels into the biggest office glut ever.

By Wolf Richter for WOLF STREET.

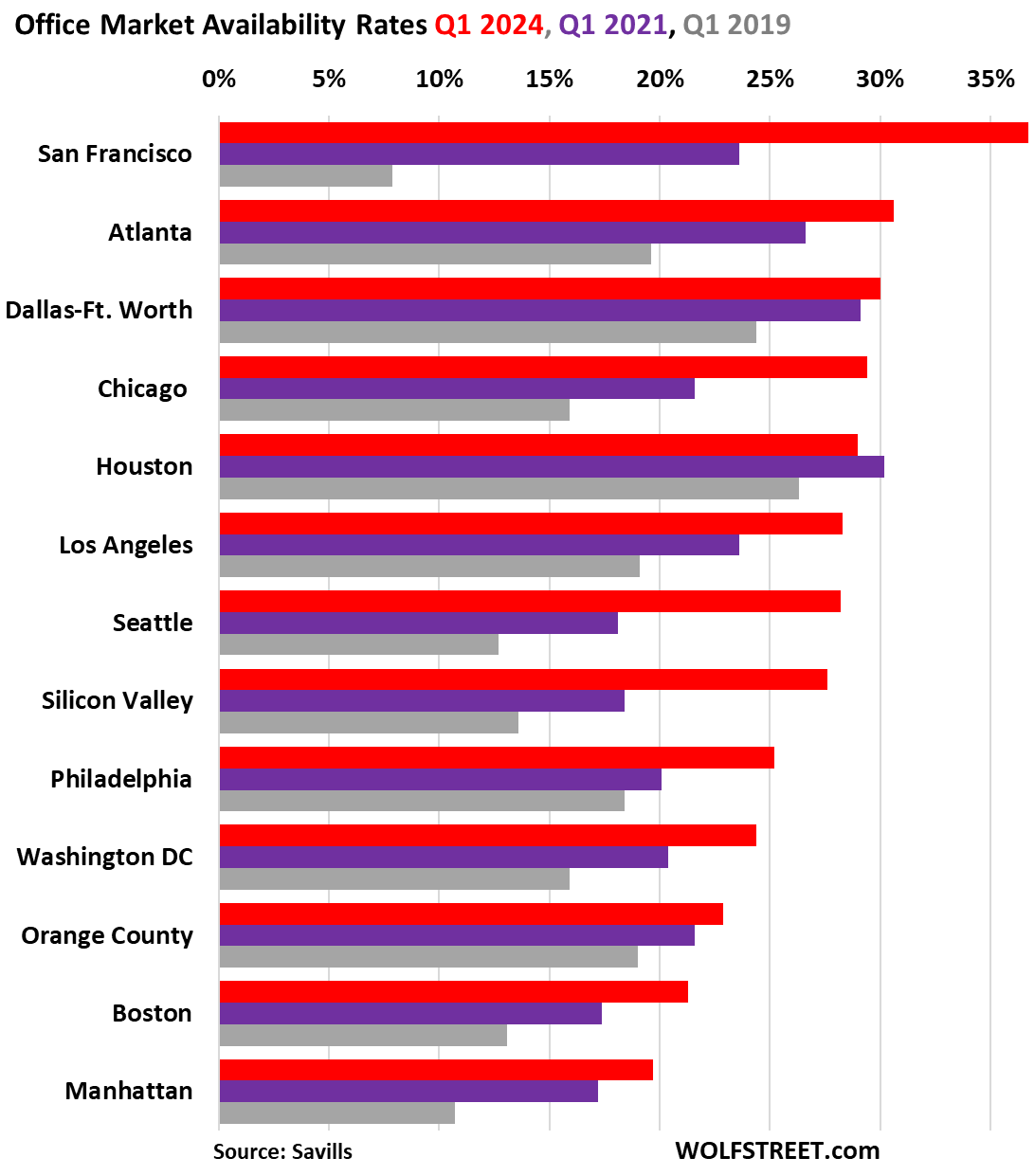

The glut of vacant offices on the market for lease, as depicted by availability rates, rose to new records in many major office markets in Q3, despite pronouncements by landlords that the office glut has bottomed out. The availability rate is the office space on the market for lease either by the landlord directly or by a tenant as a sublease, expressed as a percentage of the total office market.

Of the 15 office markets for which Savills released data today, these five had the biggest office gluts:

- San Francisco: 36.6%

- Atlanta: 30.6%

- Dallas-Ft. Worth: 30.0%

- Chicago: 29.4%

- Houston: 29.0%

Of the 15 markets, 6 hit new records, and 1 matched its prior record:

- San Francisco: 36.6%

- Atlanta: 30.6%

- Chicago: 29.4%

- Los Angeles: 28.3%

- Seattle: 28.2%

- Silicon Valley: 27.6% matched prior record

- Washington DC: 24.4%

Within a hair of their record were Dallas-Ft. Worth (30.0% v. 30.1% in Q1 and 29.8% in Q4 2023) and Philadelphia (25.2% in Q3 from 25.3% in Q1).

The chart shows the availability rates at three different points in time: red = Q3 2024; purple = Q1 2021; gray = Q1 2019.

The year 2019 (gray in the chart above) was when “office shortage” was still promoted by the CRE industry to bamboozle companies into leasing office space they didn’t need, and would never need, and they jumped on anything that came on the market, just so they could save it for later when they grow into it. This warehousing of office space propelled the office-shortage propaganda to the next level. But during the pandemic, CEOs embarked on a big rethink – and this vacant office space suddenly started showing up on the sublease market.

A lot of the leasing activity since then consisted of renewals, relocations, and downsizing – with no positive impact on availability rates. There is also a flight to quality, with the latest and greatest office buildings attracting tenants away from older buildings that are then doomed.

These older buildings then have huge vacancy rates, don’t collect enough rent to make their interest payments, and default. Those older office properties have sold for 50% to 70% off some prior price.

And in some of the deals where the building was split from the land, the land had value, and the building was essentially worthless, which happened among others, to this 925,000-square-foot office tower in Manhattan – land value being the ultimate value of older office towers.

San Francisco was the hottest office market in the US in 2019, sporting an availability rate of 7.9% amid deafening industry hype about the “office shortage,” triggering epidemic-scale office space hogging by companies such as Meta, Twitter, Google, and many others.

Back in Q1 2019, Savills’ quarterly office market report called it “the war for space”:

“New supply is limited with only a handful of projects underway, and all new product completing this year has already been pre-leased to-date. The technology, advertising, media and information (TAMI) and coworking sectors continue to dominate the war for space.

“Rapid rise of coworking offers flexible options WeWork, HQ by WeWork, and Knotel accounted for five of the ten largest leases in San Francisco during Q1. These leases alone added 260,000 sf to an already robust coworking inventory.”

Alas, Knotel filed for bankruptcy in January 2021, and WeWork finally filed for bankruptcy in November 2023.

In Q3, 2024, San Francisco’s office glut set a new record with an availability rate of 36.7%, despite all the AI hype. Savills:

“While there has been cautious optimism in 2024 that the office market might have bottomed out, with AI companies sustaining demand, corporate occupiers have continued to consolidate their office space, such as X Corp. announcing their intention to vacate both Market Square North and Market Square South this quarter.”

Leasing activity increased a tad to 1.7 million square feet (msf) in the quarter, with 315,000 square feet (sf) being leased by OpenAI, the largest deal in the quarter. A substantial portion of the remainder of the leasing activity was relocations and renewals with a net of zero impact on the market, unless they were downsizing, which would add to the glut.

Asking rents for class A space have dropped about 24% from 2019, but remain very high, at $68.22 per square foot (psf) per year, which is part of the problem.

And yet, San Francisco is one of the exceptions. In most other office market, asking rents continue to rise despite the epic office glut. Landlords are often locked in by their loan contracts, and by the reality that if they cut rents enough to fill the building, the lower rents won’t pay the interest on the loan, and they’ll default anyway.

Atlanta sports the second-worst office glut of these markets here, with an availability rate of 30.6%. Sublease space on the market remains at about 8.6 msf, including “notable blocks of large space from IBM, Elevance Health, and Cox Automotive,” Savills said in its report for the Atlanta office market.

Of the 10 largest leases signed during the quarter, 6 were renewals and relocations for a total of 438,000 sf, with no net impact on availability rates. Only four leases were for new locations, totaling 256,000 sf.

Despite the office glut, asking rents continue to increase, which is obviously part of the problem, and in Q3 rose 4% year-over-year to $32.57 per square foot per year, up from about $20 psf in 2019, which is nuts. Landlords are trying to overcome the high rents with big incentives, such as tenant improvements and rent abatements. And so the glut remains at record levels.

In Dallas-Ft. Worth, the third-worst office glut of these markets, availability rates have been around 30% for over two years.

There was quite a bit of leasing activity in Q4, with 4.2 msf in leases signed, roughly in line with 2019. But 8 of the largest 10 deals were renewals, and 1 was a relocation, with no impact on the office glut. Only the smallest of the 10 deals was a new location.

And yet, asking rents jumped 8.4% in Q3 year-over-year to $30.92 per square foot per year. But here too, landlords are trying to make up for it with incentives, such as tenant improvements and free rent, according to Savills.

Downtown Chicago set a new record for its availability rate at 29.4%. Here too, there is a flight to quality, with high-end spaces in great locations finding demand, and class A availability dipped to 24.2%.

But everything else sank deeper into trouble, with class B availability reaching new record highs, “while occupier demand waned and landlords found themselves at a crossroads, lacking sufficient capital to execute leases or to make monthly loan payments,” Savills said.

And the overall asking rents continue to rise, up 3.8% year-over-year, with class A asking rents up 6.0%.

Houston was for years the worst office glut in the US due to the American Oil Bust that started in late 2014, eventually pushing availability rates to over 30%, while San Francisco was still bathing in the aura of its office shortage. Houston was recovering from all this when the pandemic hit, and availability returned to 30%-plus by Q1 2021.

In Q3, 2024, Houston’s availability rate worsened to 29%, compared to 28.1% a year ago. Of the top 10 leases, the largest 8 were renewals and relocations. And yet asking rents – you guessed it – have been rising, including in Q3, by 1.8% year-over-year to $36.70.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So how does this affect the average diversified main street 401k?

Property REITs, bond funds that hold office CMBS and CLOs, commercial mortgage REITs, banks, insurance companies, etc. You might have some of them in your diversified 401k.

If you have a pension, you’re exposed indirectly because pension funds invested heavily in the office sector.

Just a quick note, then I’m back to lurking in the shadows. Equity REIT investors already sold off a lot of their office positions for obvious reasons. Office REITs are currently about 3.2% of VNQ (vanguard’s equity REIT index ETF). And risk isn’t distributed equally for all office reits. It’s not like 100% will fail.

I wouldn’t want to invest in anyone holding their mortgages though.

If there’s an easy way to convert all these gluts easily into residential housing at affordable prices. Sure would help take a dent out of this housing crisis we have…too bad it’s not as simple as that and instead we will all just get to sit back and watch empty good space go to waste…force people back in the office 5 days, that’ll fix the problem for you….

Funny how CRE promoted shortage to illicit FOMO and not gluts everywhere….would be lovely to see this same thing play out in the residential housing market, similar narrative of supply shortage…

Doomers News Network had someone on their show a month back talking about converting Office Buildings to Residential Buildings. The basic gist is that it’s not cheap, easy or quick. In most cases the conversion is so costly that you’re basically left at the land value of the building. It’s just cheaper to tear it down and start from scratch.

He mentioned stuff like structural integrity being all wrong for residential, plumbing and electrical being having to be reworked, tearing walls can cause the need for environmental hazard assessments for older outlawed building materials and more.

It was a bit of an eye-opener how difficult and slow any conversion would be.

“If there’s an easy way to convert all these gluts easily into residential housing at affordable prices.”

Not “easy” and “easily.” Only some office buildings can be converted into residential at all, and even then, it costs a lot of money, and takes a lot of time. But it has been done for decades. I’ve seen one of them from the inside in Manhattan’s financial district over 20 years ago. Looked OK.

Another option for smaller towers is conversion into a hotel. I stayed in one in Tulsa that used to be the city hall tower when I was still living there. It was kind of cute the way they left some of those 1960s office tower innovations in place, just for decoration, such as the brass mail chute. But the after-thought bathroom was weird, and you couldn’t open the windows, which is a no-no in a residential building.

Those people in that leaning tower of Pisa San Francisco building have the money to go over to some office building and sit there.

Back in June, I stayed in a San Diego hotel that had been a bank. Believe it or not, it was a Courtyard by Marriott, and I didn’t get the chain hotel vibe at all.

Here in Tucson, there’s an office tower hotel conversion called the Leo Kent. Haven’t been inside yet, but the exterior looks very attractive.

Just another comment; Nick Gerli also mentioned that there might actually be the starting of a glut of residential buildings in certain states (mostly Texas and Florida atm but could be others soon).

Most of the builders haven’t stopped building and units/houses are still showing up to the market. It’s actually forcing rents down in the Southeast right now. If you start to see a lot of landlords realizing that they can’t raise rents and the prices are sinking… well look out below!

People who suggest this have never looked at the architecture of office buildings. Just consider the plumbing; in an office enviroment it’s centralized, which means at best one or two locations per floor. How many apartments are going to want to share a communal bathroom? And how many office bathrooms could handle the increased flows from 24/7/365 use to include increased flow from families, showers, etc? Are the building connections to the city sewage up to the increased flow?

Replumbing a single story building is a chore, replumbing a multistory building not originally planned to accommodate such a change is a nightmare.

The office I used to work in struggled to handle the bathroom load after lunch!

Weird how there is a shortage of housing yet you see price reductions all over the country.

Well, that’s because there’s still a lot of delusional sellers out there, I know as this is especially true in SoCal. As long as there’s still buyer demand (albeit reduced compared to the crazy time) it will still give these sellers on trying…even if they lower their price, it’s still pathetic by comparison to pricing just 3-4 years ago…

Wake me up when the price is at least back down to 2019….I’ll put the probability of that happening to people landing on Mars in the next 2-3 years as someone promised…

Not just SoCal – the delusion is everywhere.

Case in point – one home I looked at online near Reno – sold in Jan 2017 for $790k; listed April 2024 for $2.3 million. Just under 4x the purchase price 7 years ago.

While that sale to asking is extreme, an asking of 50% over a purchase in 2021 or 2022 is typical.

Prices can’t come down. The banks can’t afford to take that kind of a loss. They have mortgages for the “value” of the property. If that value decreases those losses directly impact bank capitol.

Tthis is why China is having a problem. This is why there are tens of thousands of unfinished houses in places like Spain, or Turkey, that cannot be sold at a price where someone would buy them. They cannot afford to take the loss. Better to hang on and hope, and take the depreciation.

KGC,

“Prices can’t come down.”

LOL, delusional. (And everything you said about the banks is wrong. Banks hold very few residential mortgages. They sell them to the government which packages them into government guaranteed MBS and sells them to investors.)

For example:

@Fast Eddie I don’t follow the Reno, NV but over the past few years as the median home price in Truckee, Olympic Valley and Tahoe City all passed $1mm that many who work in the Tahoe Basin have started commuting from Reno five days a week. I clicked Zillow thinking that your $2.3mm home would have been one of the ten mst expensive homes and I was blown away that was abotu the 75th most exppensive home (and how many people were listing homes for $1mm more than they paid just a few years ago when interest rates were lower).

Sacramento is about 11% vacancy and the government has wanted to convert some to affordable housing but difficulties on all fronts have meant none. The only conversion was a motel as those are easier for obvious reasons. One of our largest buildings, 400 Capitol Mall, or better known as Wells Fargo Tower just sold for 40% less than last purchased. Doesn’t speak to vacancy but certainly to valuations.

Hopefully this artificial mortgage rate suppression, a big contributor to the high housing prices burdening our nation in far more ways than any supposed benefits, imo, continues going down, and all the way to zero.

a better tomorrow

You can link the article I published on Thursday about the Fed’s balance sheet, including its MBS holdings, and you can even link the chart:

https://wolfstreet.com/2024/10/03/fed-balance-sheet-qt-66-billion-in-sept-1-92-trillion-from-peak-to-7-05-trillion-back-to-may-2020-below-7-trillion-in-1-2-months/

Re: your quotes from Savill’s:

“Rapid rise of coworking offers flexible options WeWork, HQ by WeWork, and Knotel accounted for five of the ten largest leases in San Francisco…” [Q1 2019]

and

“…. corporate occupiers have continued to consolidate their office space, such as X Corp. announcing their intention to vacate both Market Square North and Market Square South this quarter.” [Q3 2024]

“WeWork” shifted toward “WeWalk” over half a decade. CRE (being a capital-intensive, long-lived, heavily regulated, and highly-levered endeavor) continues to evolve slowly, and for many, painfully.

Excellent article!

It seems like a good problem to have, there’s plenty of office space for all.

A lot of these buildings are probably in desirable locations so if the buildings fails then falls, plant some grass and trees for the birds, bees and transients.

A good glut is a terrible thing to waste, me being older, I have a glut of time that is being pondered.

If a CRE falls in the woods does anyone hear it? It seems all these CRE problems never effect the broader economy, stock market, etc…

Mark to fantasy practiced by pension funds will see the bill come due when its your time to retire and the funds are g-g–gone.

Who knew all the cities were over priced hell holes and given a chance businesses and residents would flee like its a sinking ship? Thanks covid! Guess the authorities should have mandated masks that cover peoples eyes as well, lol!

Houston is the only market listed that is better now than in 2021. At least they are treading water.

Houston’s worst period was in 2016-18 following the oil-and-gas bust and the retrenching of the oil-and-gas industry headquartered largely in Houston. Back then it had availability rates of over 30%. It was just recovering from this when Covid and the rethink about working from home hit, unleashing a new wave of problems.

We covered the foreclosure sales of a couple of those office towers in 2022 where lenders lost over 80%.

https://wolfstreet.com/2022/02/17/whats-a-vacant-office-tower-worth-foreclosure-sales-show-how-values-of-1980s-office-towers-in-houston-have-collapsed-dishing-out-huge-losses-for-cmbs/

NVDA mooning!!!

“In Q3, 2024, San Francisco’s office glut set a new record with an availability rate of 36.7%, despite all the AI hype”

Maybe I’ve misunderstood the entire premise/promise of AI but I thought the goal was to replace thousands or millions of mid level clerical or processing type workers with computers to reduce labor costs. Seems to me that once AI actually starts delivering that instead of helping to fill that 37% vacancy it will actually chip away at the remaining 63% occupancy as those jobs are replaced by severs in windowless suburban buildings scattered in anonymous suburbs near power plants. Why rent a tower with windows for people when you can run the computer 24/7 outside of Phoenix or Dallas? All this investment in AI isn’t to increase labor costs. People should think about what’s coming.

That’s AFTER AI starts delivering as promised.

Now we’re in the period where AI itself is getting worked on, and huge amounts of money are thrown at it to improve it and make it more functional and reliable. And there has been a hiring boom for AI-type jobs, even as other tech jobs might have declined. And so the biggest office lease signed in Q3 was by OpenAI for 315,000 square feet.

In regard to RTGDFA, google spits out:

At the 2024 MIT World Real Estate Forum in June, industry experts offered their perspectives on the sector’s opportunities and roadblocks

“A lot of our clients are telling us right now they have offices in the right cities but in the wrong neighborhoods,” said Breslau.”

“I think this is the office of the future,” Poleg said. “The story here is not about whether you’ll work from your bed or work in an office. The story is that work is getting distributed [and is] popping up in all sorts of places closer to people’s homes — in new types of towns, different parts of the city, and in different types of buildings.”

There was also an absurd quote about ai designing work space, because ai efficjency will help people be more creative — as they both hallucinate about the future: See the Eloi in The Time Machine — HGW 1895

Interesting how rents are rising but so are the incentives. Would be interesting to know the true new rental rates, rent less incentives. Netted out I suspect the new rents would be down. The banks must know about these financial games but don’t appear to care.

Has office tower construction advanced in the past few decades such that older (say 30 year old) towers face the same type of “functional obsolescence” experienced in many older single family homes?

@John H. What is the “functional obsolescence” you are talking about in SFHs? P.S. My home is almost 100 years old and still has the original toilets – one jus had the all brass top fill valve fail and it was a pain to find one, but we are now good for another 100 years,,,

Regarding the sale of older office buildings:

100 N Charles St in Baltimore 345,663 SF sold for $12/SF

201 N Charles St in Baltimore 268,645 SF sold for $12/SF

3551 Hamlin Rd Auburn Hills, MI 209,596 SF sold for $10/SF

150 Verona St Rochester, NY 403,113 SF sold for $3/SF

Land value. Or less. That’s the going rate.

Remember when oil spiked below zero in March 2020? I am thinking about RE values on lots that are costly to demolish on. Maybe not $0/SF, but big discounts. That might be compounded by the financial condition of their owners, and their urgency to liquidate, once the extend-and-pretend period runs out.

Usually I lurk but I felt this would help out:

https://www.gspublishing.com/content/research/en/reports/2024/02/26/b455f8f4-3b5d-4d85-8230-858fe2630cb9.html

Nice writeup on CRE conversion costs and feasibility. I have not read since it was published so don’t ask me about it.

-DD

Thanks DD. That was an informative read. Quite disheartening for those of us who would have liked to see some of these offices turned into residential. The article pretty much puts a kibosh on that.

Unfortunate really.

Does anyone know how is this CRE financed ?

Do the owners of that CRE have mortgages ? Or a line of credit ? Or a loan for say 5 years with one fixed rate and that then after the loan expires then they have to take out a new say 5 year loan with a new fixed (interest) rate ?

Or is the interest on that loan fixed for say 2 years and after that the rate become a floating rate ?

I have heard a few scary stories about CRE loans in 2022 and 2023 but they never told me why these loans were in trouble. I am curious how rising interest rates in 2022 and 2023 had an impact on these CRE loans. This information would give me a better clue how deep CRE is in trouble with the current interest rates.

Have you EVER read a single CRE article here? That was a rhetorical question. Here they are, and each one discusses the different aspects of how CRE is financed, and who holds this debt, and what happens to it when the landlord defaults, and who takes the losses, and which part of guaranteed by the government.

Yes, click on it and start reading, and spend the next two days informing yourself:

https://wolfstreet.com/category/all/commercial-property/

I am amused by the ongoing “return to office” back and forth in the press — meanwhile in the background office CRE just continues to slowly get crushed by the emerging reality that 2019 is never coming back, no matter how many corporate dinosaurs roar for its return. I look forward to Wolf’s ongoing coverage of this process much as he did the decades long “Mallpocalypse” which preceded it …

Why would I want to open an office in any downtown mega city? I could do that locally and support my own “little” city. Across the country, smaller exurbs and suburbs are creating small downtowns with restaurants and street life. And more to the point – these small downtowns do not have the social distinctly American in-human conditions that you see in this countries big cities. I suspect the type of vacancies you see aren’t going to come back, at least not as working locales. Society has moved on just as it did with the factory, many of which are residences today.

The price drops are shocking. I know this building in Minneapolis and it is pretty nice. The Forum buildings on the 900-block of 2nd Avenue sold last week for $6.5 million. That comes after selling for more than $73 million in 2019. The 634,000-square-foot Forum buildings were previously known as International Centre and Oracle Centre and are just across the street from the iconic Foshay Tower. My question is it the place is now that cheap why would anyone pay high rent. You are looking at ten dollar per square foot to buy space….a law firm of whatever that just wants space could save a ton of money just buying or renting at that rate. For a lot of businesses rent is a big deal. But nice office space for essentially nothing? It would seem everyone would move out of high rent places and enjoy the savings. Please someone enlighten me.

here is all the “doom and gloom” about Japan posted here. Clearly, you have never read a thing here:

https://wolfstreet.com/category/all/japan/