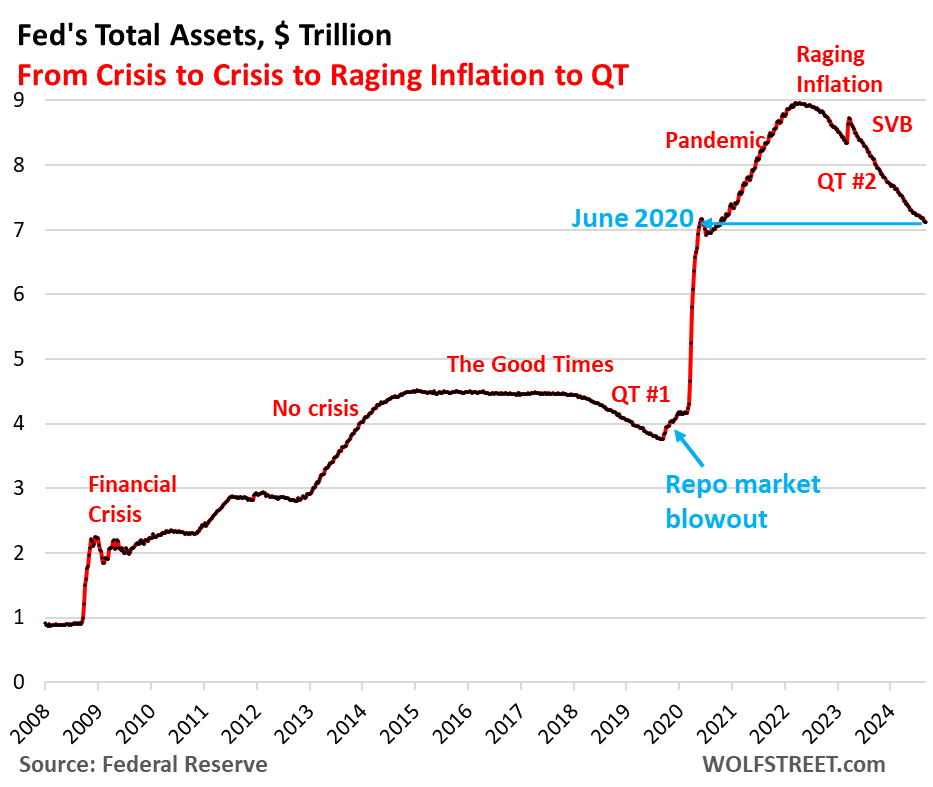

Quantitative Tightening has shed so far 38% of the assets that pandemic QE had added.

By Wolf Richter for WOLF STREET.

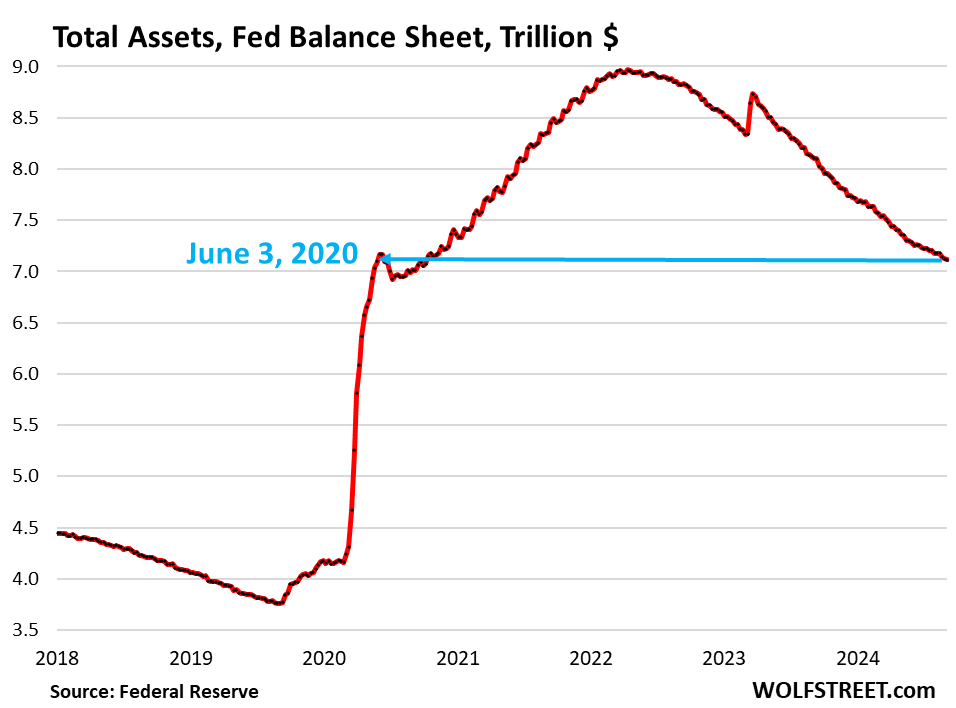

Total assets on the Fed’s balance sheet dropped by $66 billion in August, to $7.11 trillion, according to the Fed’s weekly balance sheet today.

The balance sheet first reached this level on June 3, 2020 (blue arrow in the chart), as the Fed was wrapping up three months of super-mega QE. This is another QT milestone of sorts:

Since the end of QE in April 2022, the Fed has shed $1.85 trillion, or 38% of the assets that it had added during pandemic QE.

August was the third month at the new pace of QT, announced in May, that reduces the cap for the Treasury runoff to $25 billion a month, but removes the cap for the MBS runoff, and whatever MBS come off, will just come off; any amount over $35 billion will be reinvested in Treasury securities.

The idea of the slowdown is to get the balance sheet down as far as possible without blowing anything up – to avoid a fiasco, such as the repo market blowout in September 2019 after QT-1 that the Fed dealt with by undoing a big part of QT-1.

QT by category.

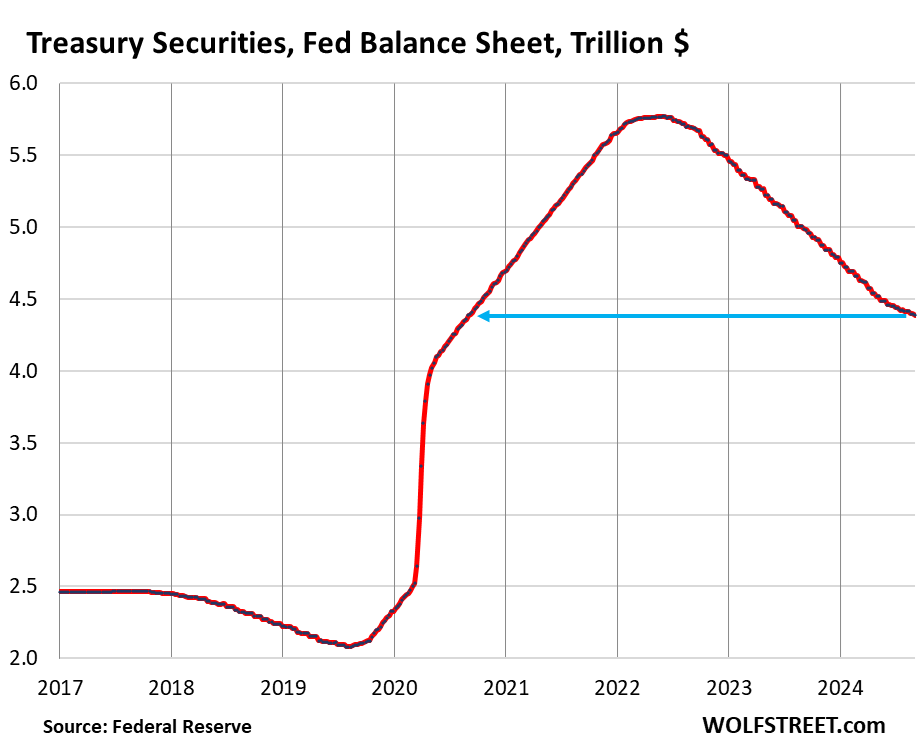

Treasury securities: -$25 billion in August, -$1.38 trillion from peak in June 2022, to $4.39 trillion, the lowest since September 2020.

The Fed has now shed 42% of the $3.27 trillion in Treasury securities that it had added during pandemic QE.

Treasury notes (2- to 10-year) and Treasury bonds (20- & 30-year) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. The roll-off is now capped at $25 billion per month, and about that much rolled off in August, minus a small amount of inflation protection the Fed earns on Treasury Inflation Protected Securities (TIPS) which was added to the principal of the TIPS.

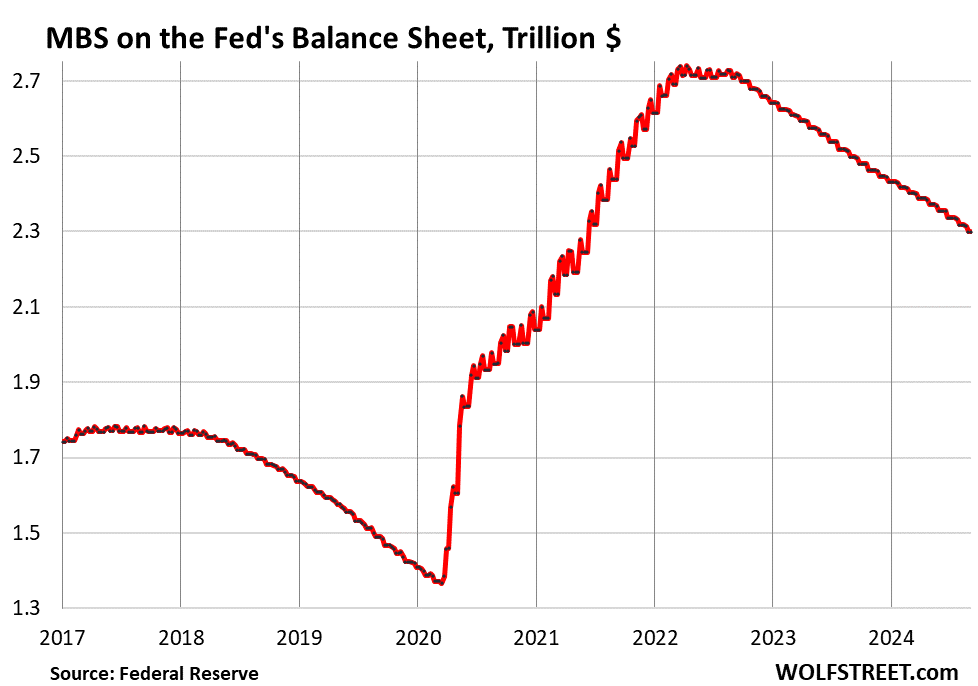

Mortgage-Backed Securities (MBS): -$18 billion in August, -$440 billion from the peak, to $2.30 trillion, the lowest since June 2021. The Fed has shed 32% of the MBS it had added during pandemic QE.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made. But sales of existing homes have plunged, and mortgage refinancing has collapsed, and so fewer mortgages got paid off, and passthrough principal payments to MBS holders, such as the Fed, have been reduced to a trickle. As a result, MBS have come off the balance sheet at a pace that has been below $20 billion in most months.

In recent weeks, applications for refinance mortgages have begun to rise and are up sharply from the very low levels late last year and earlier this year. There is a long lag between a refi mortgage application and – if that mortgage actually closes – when the Fed finally gets the passthrough principal payments from the old mortgage that was paid off. Some of it has started to show up: MBS QT has accelerated from an average of $14 billion a month early this year to $18 billion per month currently.

Bank liquidity facilities.

Only two bank liquidity facilities currently show a balance: The Discount Window and the Bank Term Funding Program (BTFP). The other bank liquidity facilities — Central Bank Liquidity Swaps, Repos, and Loans to the FDIC — are either at zero or near zero.

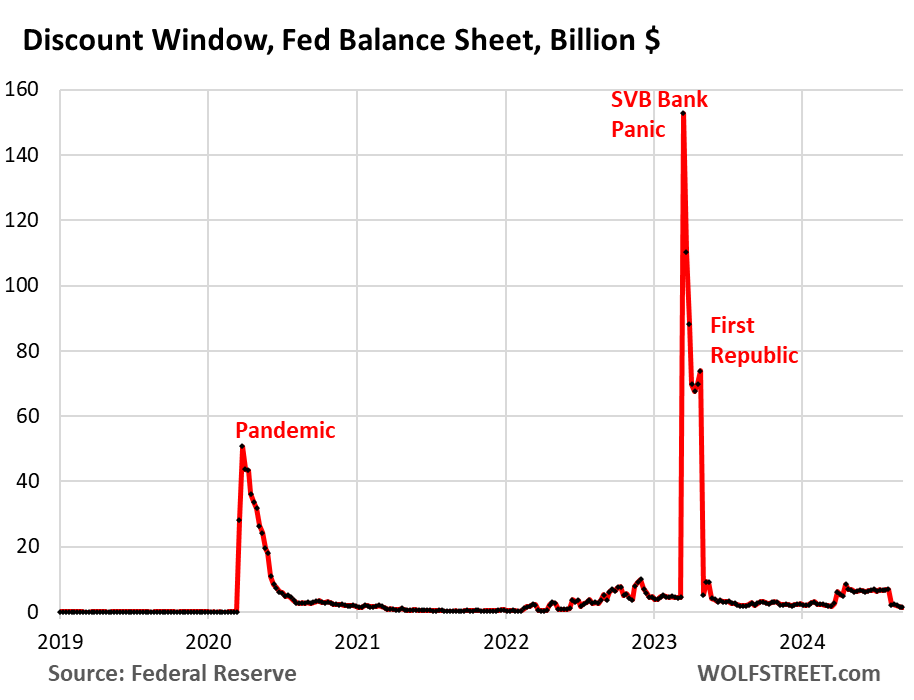

Discount Window: -$5.4 billion in August, to $1.5 billion. During the bank panic in March 2023, loans had spiked to $153 billion.

The Discount Window is the Fed’s classic liquidity supply to banks. The Fed currently charges banks 5.5% in interest on these loans – one of its five policy rates – and demands collateral at market value, which is expensive money for banks. In addition to the cost, there’s a stigma attached to borrowing at the Discount Window. So banks don’t use this facility unless they need to.

The Fed has been exhorting them to make more regular use of it, or at least figure out how to use it – apparently SVB hadn’t. Powell said the system was “clunky” and that banks should practice using it with small-value exercise transactions and that they should preposition collateral so that they can use it when they need to.

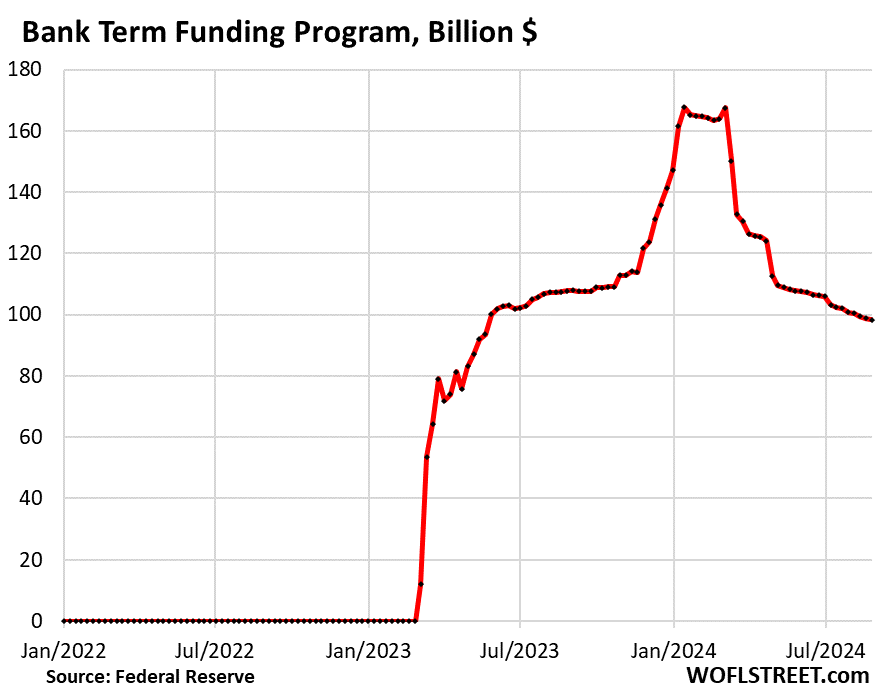

Bank Term Funding Program (BTFP): -$3.7 billion in August, to $98 billion.

The BTFP had a fatal flaw when it was cobbled together over a panicky weekend in March 2023 after SVB had failed: Its rate was based on a market rate. When Rate-Cut Mania kicked off in November 2023, market rates plunged even as the Fed held its policy rates steady, including the 5.4% it pays banks on reserves. Some banks then used the BTFP for arbitrage profits, borrowing at the BTFP at a lower market rate and then leaving the cash in their reserve account at the Fed to earn 5.4%. This arbitrage caused the BTFP balances to spike to $168 billion.

The Fed shut down the arbitrage in January by changing the rate. It also decided to let the BTFP expire on March 11, 2024. Loans that were taken out before that date can still be carried for a year from when they were taken out.

So no later than March 11, 2025, roughly in six months, the BTFP will be zero, removing another $98 billion by then from the Fed’s balance sheet, on top of regular QT.

What else caused total assets on the balance sheet to drop?

The balance sheet declined in total by $66 billion in August. Above, we accounted for $52 billion:

- $25 billion Treasury securities

- $18 billion MBS

- $5.4 billion Discount Window

- $3.7 billion BTFP

Here are $13.4 billion of the $14 billion we left out above that also reduced the balance sheet:

$10.6 billion of “other assets,” mostly accrued interest on its bond holdings that the Fed had set up as a receivable, and that it got paid in August. When it gets paid interest, it destroys the money (instead of having a “cash” account, like companies do, that it could put cash into or take cash out of, the Fed creates money when it needs to pay for something and destroys money when it gets paid.

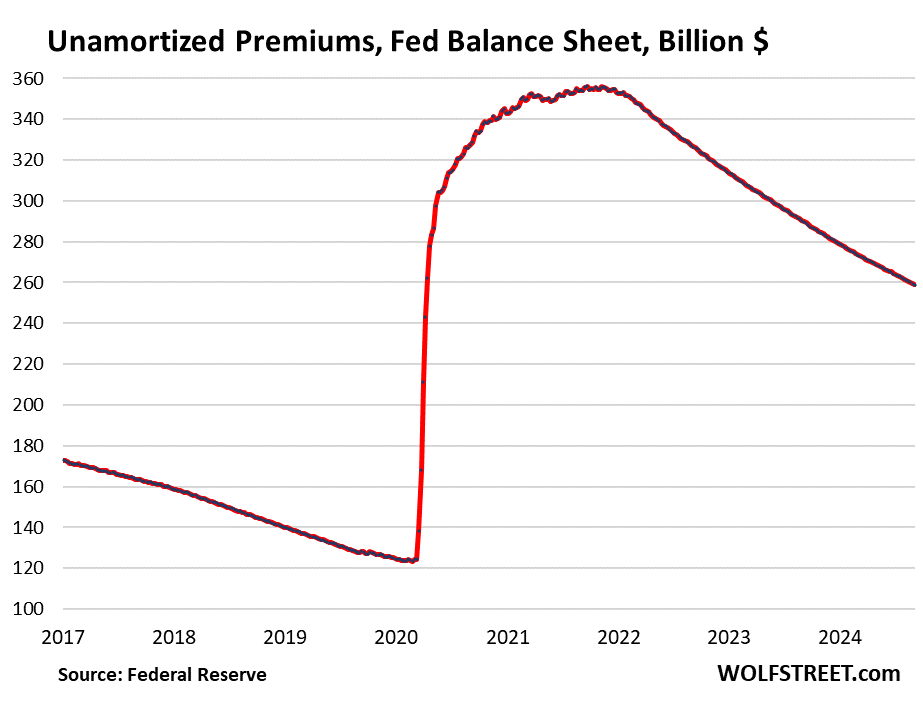

$2.8 billion “unamortized premiums”: the amount the Fed writes off every month to account for the premium over face value it had to pay for bonds during QE that had been issued with higher coupon interest rates and that had gained value as yields dropped. Institutional bondholders, such as the Fed, amortize that premium over the life of the bond. The remaining balance of unamortized premiums is now down to $259 billion, from $356 billion at the peak in November 2021. And there’s a chart for that:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

And no, the Fed’s balance sheet cannot go back to “2008” to $800 billion. The Fed’s balance sheet has always risen at least in parallel with “currency in circulation,” the “Federal Reserve Notes,” or paper dollars, that the Fed issues to the banks in exchange for collateral, such as Treasury securities. Currency is demand-driven; the banks must have enough on hand to meet demand; and much of it stashed somewhere overseas.

Currency in circulation is a liability for the Fed (money it owes the holder of the paper dollars). And a balance sheet must always, well, balance, with assets = liability + capital. So when the liabilities rise, such as currency in circulation because there is demand for them, assets must rise in equal measure.

Respectfully for your work Mr. Wolf, but to this engineer the graph of the Federal balance sheet matching the “currency in circulation” of 2008 to present looks nothing like the shape of the graph in this comment of 2003 to 2008. What it does look like is an unstable system with a positive feedback (like microphone feedback) that was just barely stopped at a new normal point, but still likely unstable with a new input (financial situation). When disasters happen with say something doubling, the catastrophe isn’t at the start when the problem goes from 1/4 to 1/2 and then 1/2 to 1 (100%).

Another point of mis-undertanding for me is the apparent mislabeling on the first graph that assigns the duration of the 75% increase in the Fed’s balance sheet. I thought that the covid expansion began a year at least before that. And is actually the vertical portion of the curve.

Thanks Wolf.

There is nothing mislabeled in the first chart. The text is correct too. Maybe read it again?

I appreciate your description of what post 2008 currency in circulation vs. total assets would look like, but can anyone courteously post a more recent 2008-2024 currency overlay added to the commonly seen total asset graph? In similar format to Wolf’s 2003-2008 graph?

It’s hard for me to visualize a chart appearance just using an ‘unstable system with positive feedback’.

My thanks to anyone who can do this.

The structure of the Fed’s balance sheet on the liability side has changed a lot, including through the inclusion of the TGA (government checking account), RRPs, and reserves.

Read all about the liabilities, including currency in circulation here.

https://wolfstreet.com/2024/06/13/fed-liabilities-under-qt-1-71-trillion-from-peak-to-7-22-trillion-update-on-reserves-on-rrps-currency-the-tga-and-foreign-official-rrps/

I’m no math genius, but I’m pretty sure 7.11T/8.9T = 79.88% or a reduction of 20.12%, not the “38%” stated in the article….

Your problem isn’t math (you’re doing fine there), it’s reading.

This is what I said:

“Since the end of QE in April 2022, the Fed has shed $1.85 trillion, or 38% of the assets that it had added during pandemic QE.”

Not total assets.

Pandemic QE amounted to 4.807 trillion. It has shed $1.853 trillion = 38.5% of Pandemic QE.

What a bunch of bs this was? It is so simple and yet they have created lots of problems for all of us. You have one Fed and Twelve Central Banks throughout the US and printing machines to churn out free cash at your disposal. What a joker!

You are wrong. I strongly suggest you re-read and look at the charts again. Perhaps an Economics College Course might, just might benefit you.

Maybe RS didn’t RTGDFA. Maybe RS just glanced at the picture I posted into my comment at the top of the balance sheet from 2003-2008 that goes straight up, not seeing that it was from 20 years ago. That’s the comment RS replied to.

The next 2 months will be an exciting ride. If the fed cuts, the mortgage refi’s will really pick up pace reducing the fed balance sheet more (at least the MBS portion). I heard that history says the 3 months after the first fed rate cut are not positive for the S&P500. And with more liquidity draining, fewer job openings and a sticky inflation report on Sep 11th, it will be interesting… Keep the informative articles coming Wolf. Thank you!

WR mentions that 6 cuts are already baked into mortgage rates. So unless the market bakes in more cuts, there’s no reason refis will jump more than they already have.

Most refis now are cash-out refis by homeowners who want access to their money buried in the house. That’s what we’re seeing. Non-cash-out refis are still dead, and that makes sense.

I don’t like the “rate cuts are priced in’ for durations greater than 1 year. Shirt term policy rates certainly influence things, but they’re not in th driver’s seat. Mortgages also hav credit risk. The spread between the 30y mortgage and the 2-10 ust spread is still historically high which means investors remain cautious. About what? I’d argue collateral values. Buyers aren’t the only ones on strike, it’s also lenders.

Certainly, a lot of food for thought. Thanks.

In my version, the Fed rate cut is an emergency palliative in response to the night after sun, shining in our collective, foggy presence. Not the immediate cause but certainly the master mind of the wobbly economic predicament that we find ourselves in.

Asset prices are at all time highs. Only people of means can afford them. I think we are worrying about a collapse of three affiliated bubbles, that, like a hot air balloon , are dependent on increasing monetary supply to remain inflated.

Potentially, the overvaluation grain of sand, will be the one that initiates the collapse of the sand pile.

“Asset prices are at all time highs. ”

You need to look at stock prices before you write this stuff. Mag 7 down 15% from all-time high, semiconductor index down 24% from all time high, Nasdaq down 10.5% from all-time high, S&P 500 down 4.6% from all-time high. They’re NOT at all-time highs. Other asset prices have plunged from all-time highs, including cryptos.

This is just silly Wolf. So markets are off a few percent. Close enough to all time highs. The Fed still has tons of dollars sloshing around and a very inverted curve out to 2s then it starts to steepen. That is very much a giant angry warning sign. He who eases here might unleash a torrent. Labor markets are still tight and factories are still being built as we re onshore. Powell would be well advised to leave the sleeping giant alone.

Dividing index values by gold price (for the same time points), we are also not close to market highs.

SPX/gold ~ 2.160 today, Sep 9.

spx/gold ~ 2.65. Jan 1, 2022.

So down close to 18.5% in gold terms.

From late Feb ’24, spx/gold ~ 2.5, now down ~13.6%.

The dollar prices are useful in a short term comparison since we use the dollar everyday, and that is what we are taxed on, but in a world of competing investments for me a realistic comparison needs to be made, such as gold price.

The nominal index values or portions like mag 7 nominal don’t convey reality. Some kind of inflation adjustment should be used. Measures of competing investments. If you don’t like gold you can use CPI or something else.

Inflation is stealing the jam out of the nominal market prices.

How about pricing the SPX not in gold but in Nvidia shares? How about pricing it in US natural gas or in milk or in EV battery costs per kWh? Lets have some fun here.

OK:

$spx in $natgas peaked in Q1, over 3000, now ~2500.

$spx in nvda, very low, bottoming out, bouncing, now ~50 after long long slide. 5 years ago, was over 700.

$spx in $wtic is local high, up trend, but below highs late 2020.

There is some non-sense in the $wtic because oil prices went to zero or near zero in the covid crash.

The classic laugh is prices in bananas, but I can’t get that in stockcharts.

To do a ratio or comparison in stockcharts, put colon : between symbols. eg, $SPX:$SILVER

I’m not a subscriber, so limited to 5 yr. They adjust past prices when dividends. For index or commodities, no adjustments.

(They have bitcoin at least as GBTC that looks in pattern like bitcoin price action, but it is scaled?)

I’m not a stockcharts expert.

Huge loss in SPX vs bitcoin (GBTC) since Jan ’23, local highs.

From over 500 Jan ’23 to current ~120.

🤣❤️ Thanks TR! You actually did it! Awesome!

Are you suggesting and insinuating that the US will be a lot messier after the first rate cut by the Fed? And are you getting excited when most Americans are standing at the cliff of point of no return and you’re happy about the situations?

It appears there is currently around $2.5T in circulation. Keeping the same ratio as pre-QE suggests the fed could reduce its balance sheet to around $4T. Does that seem realistic over time or would it cause too much damage to the economy?

I think the answers are above.

Is the Fed looking for a number, or will they keep the balance sheet at a high enough level to avoid asset price drops, write offs, and job losses. Who knows what level that is, but it surely will be a lot higher than before due to recent asset and price inflation.

In a debt ridden economy, you can have inflation, and excess inflation, but never deflation.

Bob,

$4 trillion would be tough.

The balance sheet has changed structurally: Since the Financial Crisis, it also has the TGA (government checking account) on the liability side. Before then, the government’s checking accounts used to be with JPMorgan and other banks. That account has between $50 billion (at the end of the debt ceiling charade) and over $1 trillion (during a crisis) in it, and it must be balanced on the asset side. Currently, it shas $771 billion in it. It fluctuates widely, but it keeps growing.

ON RRPs will go close to zero, but “foreign official” RRPs with central banks, where they deposit their dollar cash, is getting bigger, currently $400 billion and growing. That’s a liability and it must be balanced with assets.

TGA and RRPs combined might average $1.5 trillion in a couple of years. So you’re already over $4 trillion.

Reserves are also needed. They’re currently $3.2 trillion, but they don’t need to be that huge. If they can be brought down to $1.8 trillion, the balance sheet would be just under $6 trillion.

How do you interpret the effects of these different aspects of the Balance Sheet on the global economy? What for example is the significance of the growth of the “foreign official” RRPs? Or the growth of currency in circulation, etc?

They’re both demand-based. They’re a result of people wanting to hold US paper dollars and a result of foreign central banks wanting to deposit their dollar-cash at the Fed where it’s instantly available if they need it. They could also buy T-bills, but they would have to sell the T-bills to get the cash.

The only significance of people wanting to hold paper-dollars is that they’re giving their money to the Fed for free, and the Fed buys Treasuries with it an earns interest on it. That principle of seigniorage is how the Fed has always funded itself. All central banks do that.

In terms of the foreign official RRPs, it’s a service the Fed offers to other central banks. Other central banks, such as the ECB, offer similar services.

Personally, I think Wolf has that one dialed in.

Can’t recall the exact number of Wolf’s estimate of the minimum Fed balance sheet which seemed reasonable. I know that it is far less than the current Fed balance sheet. If I recall, it was like 50% less than the current, grossly obese Fed balance sheet.

The remnant of a monetary experiment, gone awry. Perhaps.

With possible rate cuts coming, there may be one small silver lining.

If (I know that’s BIG IF) FED cuts rate by75 BP by end of Dec 2024, FED will only pay may be 4.5/4.6 to Banks. The BTFP arbitrage will go away as when Banks took the money it was around 4.8%. Thats not going to be profitable for Banks and they will be kind of forced to pay off that money to FED.

We may not have to wait for March 2025 for them to disappear from FED’s balance sheet. That $98 billion amount may not be Huge number in Absolute but its like 2 months of QT.

There’s no mor arbitrage with the BTFP. It was cancelled in March. No one can take out new loans. Its current balance consists of old loans, and when they reach their one-year term, they have to be paid off. All of them will be paid off no later than March 11, 2025.

Wolf,

I understand the loophole was closed later and there is no more BTFP. I was referring to existing loans taken by Banks. But Banks who already took the money, they continue to hold it right?

In Nov-Dec 2023 time, Banks who used arbitrage and took the money got it at around 4.8% and they are earning 5.3% today isn’t it?

So IF FED drops the rates by 75 BP then those Banks will no longer earn 5.3 but they would rather earn 4.5 type.

So if they dont return the money soon and keep waiting till March 2025, they will be paying the difference. ( assuming they took the money just for arbitrage).

In nutshell, I am thinking BTFP balance will become lower much sooner than March 2025.

“Its current balance consists of old loans”.

When FED closed arbitrage, it also forced those Banks to return the money?

Sorry, I missed this point then.

Seems you got it right.

The arbitrage banks did return the money. You can see that in the shape of the curve. I’m not sure to what extent that was “forced.”

The arbitrage started in early November when market rates began to drop. Until then, the banks that borrowed at this facility really needed the liquidity, and that amount ran along about $100 billion. Those banks are now also paying off the loans as they can borrow elsewhere for less.

Wolf,

I may be misunderstanding your comment, but it is not clear to me from the graph/curve that the arbitrage money was returned. The visible drop may be similar in magnitude to the Nov/Dec surge, but it appears to be in March which suggests it was a portion of the initial one-year borrowing dutifully being repaid. Interestingly this drop is much smaller than the initial surge which suggests, that while many of the banks really needed the money in March, those same banks saw the arbitrage opportunity later in the year and decided to extend/reset their loans to milk it for as long as possible.

I think we are all in agreement that this borrowing will likely be returned long before next March, probably in Nov/Dev when the arbitrage money will both reach the one year mark and/or rates dropping will have eliminated the arbitrage.

Even the FOMC is not dumb enough to cut rates by 75 bpts. I’m hopeful they won’t be dumb enough to cut by 50 bpts.

The wailing by the wealthy about the market value of their assets, morally, should not be the basis of their decision. 25 bpts.

From 1 trillion pre financial crisis to 7 trillion as of today. The country never recovered from the financial crisis, it was only propped back up with the financial trickery of the fed.

There will also inevitably be more financial crises. The Fed being the Fed, and having set the precedent, will continue printing 💰money in response to the next one. Bill Fleckenstein argues that the Fed is the primary creator of bubbles. I think he’s right.

LOL!!! Ya think?

A financial crisis — a financial panic — when allowed to run, can destroy the banking system, and the broader financial system, and everything that depends on it, which destroys the economy for years, see the Great Depression.

The banking system is the money-equivalent of the electrical grid. If you allow the electrical grid to blow itself up (it could do that, which is why it is so heavily regulated), the economy shuts down, and all your cryptos vanish, and your cellphone doesn’t work anymore, and you cannot comment here anymore because everything electric and electronic is dead. Similar with the banking system.

A financial crisis is nothing to be trifled with.

There have always been, and there will always be financial crises, just like parts, big parts, of the grid go down occasionally. The question is: how do you stop it before it spreads too far.

DO NOT conflate a “crisis” with FRAUD.

Prosecute the fucking FRAUD, bankrupt and JAIL the preps and you will have fewer actual crises.

Come one Wolf, stop being so disingenuous.

Funny that you mention the great depression, yes, now why don’t you remind us all about the regulation that was actually implemented after the depression? Then we can talk about how all that regulation has in FACT now been UNDONE.

there’s nothing wrong with stopping the banking system from wholesale failing, assuming that you don’t also bail out tons of people who made bad decisions.

The bailouts of bank investors (stockholders and bondholders) and of bank executives, and assuring that instead of being indicted, they got record bonusses was a massive fiasco and should have never happened, I totally agree with that.

It’s a system designed wih intended purpose. It’s not the system to be blamed, it’s the people who are controlling and monitoring to be blamed. Do you blame the car or the driver? The FED must revived its organization without question.

Lacey Hunt-

U.S. Treasury is also complicit — the two have wrecked the price-signaling nature of the treasury securities market and that of the shape of the yield curve. They broke the thermometer.

Wonder if the signal-squelching interference will be temporary or permanent…

Not surprising considering the revolving door between The Fed, Wall Street, the treasury, and the regulatory agencies.

CONgress has also been fully captured (bought via K-street)

We all know this to be true, but as far as I can tell, so long as we can profit from it, life goes on…

Interesting times.

WB

Thanks for amending the list.

Long as we’re being inclusive, let’s not exclude the halls of Academia.

Cheers

Rising unemployment is due to inflation ravaged Americans rejoining the labor market to survive. Someone has to serve benefactors of the Fed Put.

Yes but I would point out that love is the only deadly sin that can explain how we survived. A hairless, prey in a world of predators.

If the Fed cuts rates, then they need to accelerate the rate of MBS dumping. Allowing the Fed to purchase MBS in the first place was bullshit. Lowering rates in the current housing market will only worsen the affordability issue.

What ? Someone had to buy the dreck of the AAA rated bond tranche unless every bank were in danger of insolvency if the securities they were holding were to be marked to market.

A rule was discarded which suspended the FASB requirement of mark to market in favor of a mark to internal estimate of the value of worthless securities.

It bears pointing out that the BTFP allowed arbitrage not just because it was based on market rates, but because it was specifically based on the market rates for one-year loans. Once the market started pricing in a lot of rate cuts in early 2024, the one-year market rate dipped below the overnight rates set by the Federal Reserve, allowing the arbitrage. Nevertheless, I imagine there would have been oddities from BTFP regardless because the Fed was ultimately handing out one-year loans with the expectation that they would fund reserves earning an overnight rate.

Arbitrage, taking advantage of market mispricing, is a miserable fate awaiting the traders who remind me of a nervous cat , always on alert hoping to take advantage of some mope trying his hand betting in the free market.

Taking advantage of mopes never feels good, emotionally.

Good morning Wolf,

What are the chances you could give us an article explaining “the ins and outs” of the BOC simultaneously participating in QT and overnight repo operations (while cutting interest rates)? Seems the BOC is the commercial banks’ lender of choice and suppresses the overnight rate.

Posted mortgage rates (at big commercial banks) for more highly leveraged borrowers (amortization 25+, less than 20% down payment) is less than those being offered to borrowers with a lower debt load (possible CMHC influence?). Seems backwards – shouldn’t higher debt and higher risk be reflected in the interest rate. Anyways, seems like the BOC is in a hurry to reignite business and consumer credit expansion while hoping inflation doesn’t get carried away. Judging by existing home sales taking a dip in 2019 when the BOC increased rates above 1% I have my doubts that sales volumes will have a substantial increase based on current prices; perhaps an increased amortization is forthcoming?

Repos are demand based. If there is demand, the BOC provides them. The BOC has always provided day-to-day liquidity to the banking system via repos.

But after QE, there was no demand for repos for a while, and balances went to zero, because there was so much liquidity in the system.

The BOC has now drained much of that QE liquidity, and so banks make use of the repo facility again. There are currently $16 billion in repos outstanding, which is a little more than the average balance in 2019. Compared to the overall balance sheet of $289 billion, it’s a pretty small component, and proportionately a smaller component than it was in 2019.

The BOC has said that as QT ends this year, it will start shifting its assets from longer-term GOC bonds to short-term T-bills and very short-term repos (most of them overnight). So this shift to short-term will slowly happen over the next few years.

It’s interesting though, and the BOC has explained this: there is now demand for this liquidity to fund bets on long-term bonds due to massive rate-cut expectations, as bond prices go up when yields go down. So this is to fund speculative activity on rate cuts.

A $25 billion bond issue rolls off the balance sheet this month. When it is reflected on the weekly balance sheet which comes out on Fridays (maybe today, maybe later in Sept), I will cover that. And then I will also discuss the repos.

Wolf, I’m not quite getting the unamortized premium bit. How is that an asset for the Fed?

I get that having paid over part for the bond, the Fed created liquidity. But how/why is that bond different than one the Fed bought at face value, from the bal sht perspective?

It’s OK not getting this. Bond accounting is not intuitive. If you’re an institutional bond holder, you will do it the same way. That’s just how bonds work and how they have to be accounted for.

But note: During QE, the Fed bought bonds in the market at market price, not at auction at face value. For example, in 2020, it bought 30-year bonds that were issued 10 years earlier with 4% coupon interest that had 20 years left to run, so they traded like 20-year bonds in 2020. But in 2020, market yield for 20-year maturities might have been 1.5%, and the Fed had to pay a huge premium to get that 4% coupon interest so that the yield would turn into 1.5% market yield. That’s how bond trading works. So it didn’t pay face value for them. It’s those bonds that it bought in the market at market prices (premium over face value) that it then set up on an amortization schedule.

Bonds that it buys are auction at face value are not set up on an amortization schedule. But their market-price changes show up in the unrealized gains and losses that the Fed reports in its quarterly financial statement.

Oh I think I get it… the unamorized premium is the unrealized loss from buying above par but only getting par back at maturity.

CB’s don’t actually lose money, so that unrealized loss is becoming ‘realized’ via reduced bal sheet.

Man central bank accounting is weird.

LOL, no you don’t get it. And forget the Fed for a moment. ALL institutional bond investors account for bonds they bought in the market the same way. This is NOT Fed-specific. This is standard bond accounting 101.

That bond with 20 years left to run that the Fed bought at a premium pays a 4% coupon interest rate, while market yields for this maturity were 1.5% when the Fed bought it. So the Fed is receiving a coupon interest payment of 4% for the next 20 years, which was 2.5 percentage points higher than market yields when it bought it. So it paid a premium to get the premium coupon interest payments for the remaining life of the bond.

Due to the premium, the Fed receives a yield to maturity of 1.5%, which is equal to the market yield because that’s how the bond was priced. There is no loss involved. The Fed bought a 20-year maturity at a price that equaled a 1.5% yield to maturity.

But accounting for this transaction requires that the Fed books the bond at cost (face value plus premium), takes in the 4% coupon interest as income, and amortizes the premium against this extra interest income over the life of the bond. When the bond reaches maturity, the Fed gets face value which is by then its book value.

ALL INSTITUTIONAL INVESTORS, including bond funds, account for bonds the same way. I don’t because I’m not an institutional investor.

Somebody and/or a group of somebodies made a killing selling those 30-year bonds in 2020 to the Fed considering the bond sellers could have re-invested the huge premium received at over 4% just 2-3 years later, anyway.

I think that’s why it’s so hard to wrap one’s head around the Fed never taking a real loss. Somebody took the loss somewhere…amorphously?

Thanks for these charts Wolf. Had been wondering about the pace and details of the Fed’s balance sheet past few months and this really shine a light on it and what’s going on behind the scenes.

Does anyone know if the rate of Fed MBS run off affects mortgage rates themselves? I.e. will mortgage rates have upward pressure (to an extent) from the fed as folks get new mortgages/refi? I would think if they were letting them run off it would at least not support MBS yields, but I’m not sure if this remotely affects mortgage rates compared to Fed funds rates expectations/10-year yields. Thank you!

When the Fed reduces its portfolio of MBS while overall issuance of MBS continues, it means that the market must pick up all the new issues. The Fed was a huge player in the MBS market, so with it pulling out, it would put upward pressure on the spread between mortgage rates and the 10-year yield. And the spread widened a lot since QT started:

You explain the mechanics in a very helpful way.

Thanks for your patience and commitment to your readers, Wolf!

IMHO, all these discussions and debates about the economy are no different than an argument over a bar tab on the Titanic.

Then why are you even still commenting if we’re all going to hell on our Titanic? 🤣

The Fed is in a predicament of their own making. If they were truly apolitical, they would allow the cost of money to more accurately reflect the risk in the market. This would apply greater pressure to the political class to do the only job they really have, which is to balance the budget and be fiscally responsible. Issuing more currency (credit) after people behave badly, only encourages more bad behavior. The more unsettling problem to me is that The Fed is not the only central bank that has been doing this. It’s a global economy, and has been for a long time.

“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.” – Mises

It was true then, and is just as true now.

Interesting times.

Credit expansion has been going on forever, and we’re still waiting for the collapse.

If you look at the long-term long bond chart, it looks to me like it ran up from about 1980-2020. It has crossed my mind that we have several decades of downhill in store.

I expect a temporary upward blip caused by selling of (bubble) stocks the next few months.

Yes, you said the dirty word allowed, forgotten as an input into any financial calculation is an estimate of risk.

Risk is what happens as we plan the future. If you have never had someone in your family get sick. You are not special. You are lucky.

Hmm….. if the whole world is behaving different than you think it should, maybe it isn’t their problem. Maybe it is your expectations are incorrect.

There are two components to debt. A borrower but a lender as well. A lender who treats the loan as an asset that makes money in interst on the loan.

Don’t you think it is kind of odd that you using quotes about the horrors of debt expansion from someone who is long dead, yet debt expansion has continued long past their deaths?

Your mistake is not changing your premises after all of the evidence shows they are not true.

waller came out saying he thinks a bunch of rate cuts will be appropriate. these people can’t help themselves. a few down days in the stock market and they have to jump in to reassure everyone that asset price deflation will not be tolerated. bobber was and is right.

Hot off the press:

“The Fed Has Room to Cut, Rates Are High Relative to Inflation, and Job Growth Could Use some Juicing Up”

Job growth bounces back some, hourly earnings jump, unemployment dips, but job growth is too slow to absorb the massive influx of immigrants.

https://wolfstreet.com/2024/09/06/the-fed-has-room-to-cut-rates-are-high-relative-to-inflation-and-job-growth-could-use-some-juicing-up-to-maintain-momentum/

censorship doesn’t make it not true ;)

Your comments seem to be dropping off bro, wonder why.

As long as you see this, i’m happy ;)

Quit posting BS, and your comments might make it. This is not a repository for BS. Go spread BS somewhere else.

I’ve culled commenters in recent months because I was wasting way too much time shooting down their BS. Life is too short. Internet BS is toxic. If it’s BS, it gets deleted, not wasting my time on BS anymore. BS spreaders get blocked. I’ve had BS overload.

It looks like your knowledge of the definition of the word “censorship” is as faulty as your understanding of economics.

A private entity not allowing you to take a dump in their living room is not censorship.

Could the Fed at this point lower rates while accelerating lessening it’s balance sheet to a target of let’s say 5 trillion? (The currency in circulation to assets graph only shows up to 2008). This way it helps ease the frozen housing market while not risking blowing up the banking sector since lower lending rates and better yields on existing bonds should avoid liquidity problems. Or is there something I’m missing here?

The BTFP numbers are the ones that I am watching. It only dropped by $3.7 billion this month? Wow! So the average drop needed to close those out has gone from about $11 billion a month to over $16 billion a month since the Fed in May lowered the amount of “regular” QT it wants to do. I would have thought it would be a faster drop but the banks are hanging onto their good deal it seems.

That said, obviously the Fed has called these guys and mapped out when they are all likely to close out this arbitrage. Still… if it doesn’t start happening soon it is going to have to happen “bigly” in the end.

Interesting, M2 has been going up lately. Not much, but a little. I would assume that QT is being offset by banks making more loans. Is this the only way M2 can go up during QT, or are there other possibilities?

M-2 is a flawed measure, which is why only bloggers still look at it. For example, when you move $200k from one CD to two $100k CDs, M-2 rises by $200k.