Active listings explode in the metros of Tampa, Orlando, San Diego, Denver, Seattle, and others.

By Wolf Richter for WOLF STREET.

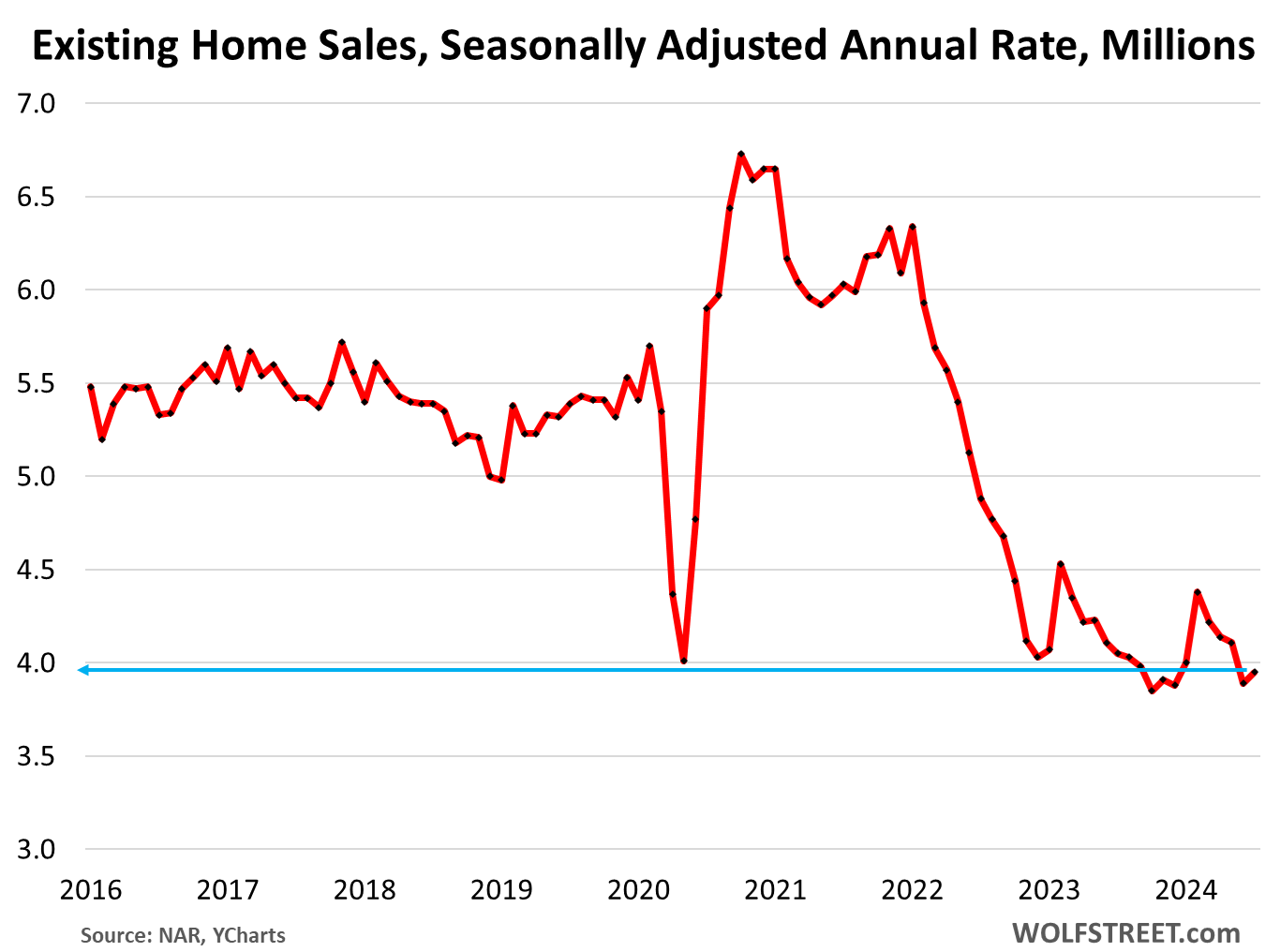

Despite the drop in mortgage rates – to 6.5% in the latest reporting week – and the surge in inventories as vacant homes for sale are coming out of the woodwork, sales of existing homes have been wobbling along the lowest levels since the depth of the Housing Bust in 2010 amid wilting demand in face of prices that are still way too high.

Sales of existing homes of all types – single-family houses, townhomes, condos, and co-ops – in July inched up 1.3% from June, to a seasonally adjusted annual rate of 3.95 million, below the low point in May 2020, the fourth-lowest since the depth of the Housing Bust in 2010, behind only June 2024, and October and December 2023.

Sales in July were down from the Julys in prior years by (historic data via YCharts):

- 2023: -2.5%

- 2022: -19.1%

- 2021: -34.5%

- 2019: -26.7%

- 2018: -26.7%.

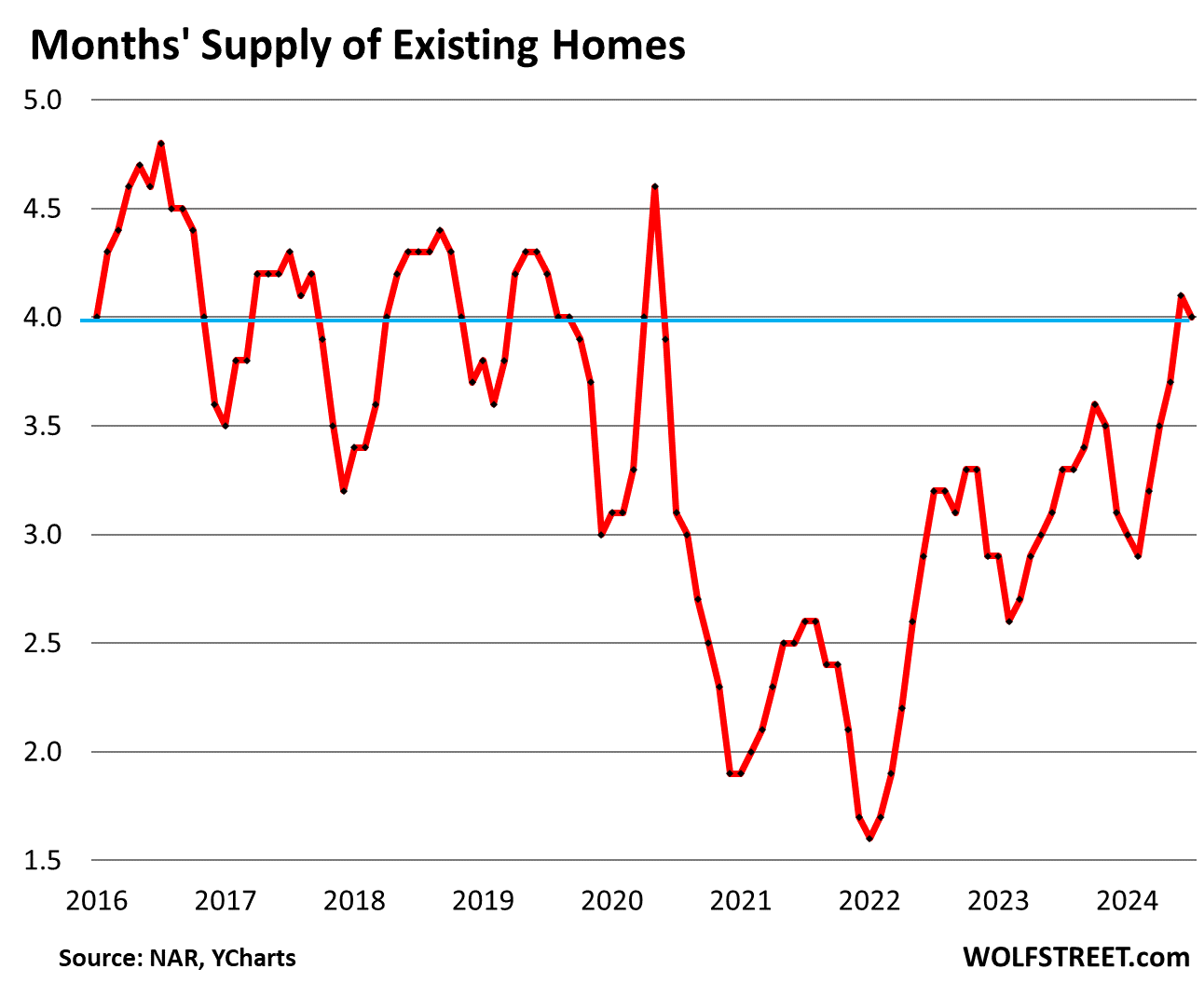

Inventory and supply have reached multi-year highs, as sales have sagged. Inventory rose to 1.33 million homes, the highest since October 2020, according to NAR data.

Supply, after spiking to 4.1 months in June at June’s rate of sales, dipped in July to 4.0 months, as sales ticked up. Both June and July were the highest since the spike in May 2020, and just a notch below the Julys in 2019 (4.2 months), 2018 (4.3 months), and 2017 (4.3 months). In July 2023, supply was 3.3 months.

That spike in supply in recent months is quite something – the result of dismal sales and the rise in inventories as the vacant homes are coming out of the woodwork that homeowners wanted to ride up the price spike with all the way to the top (historic data via YCharts):

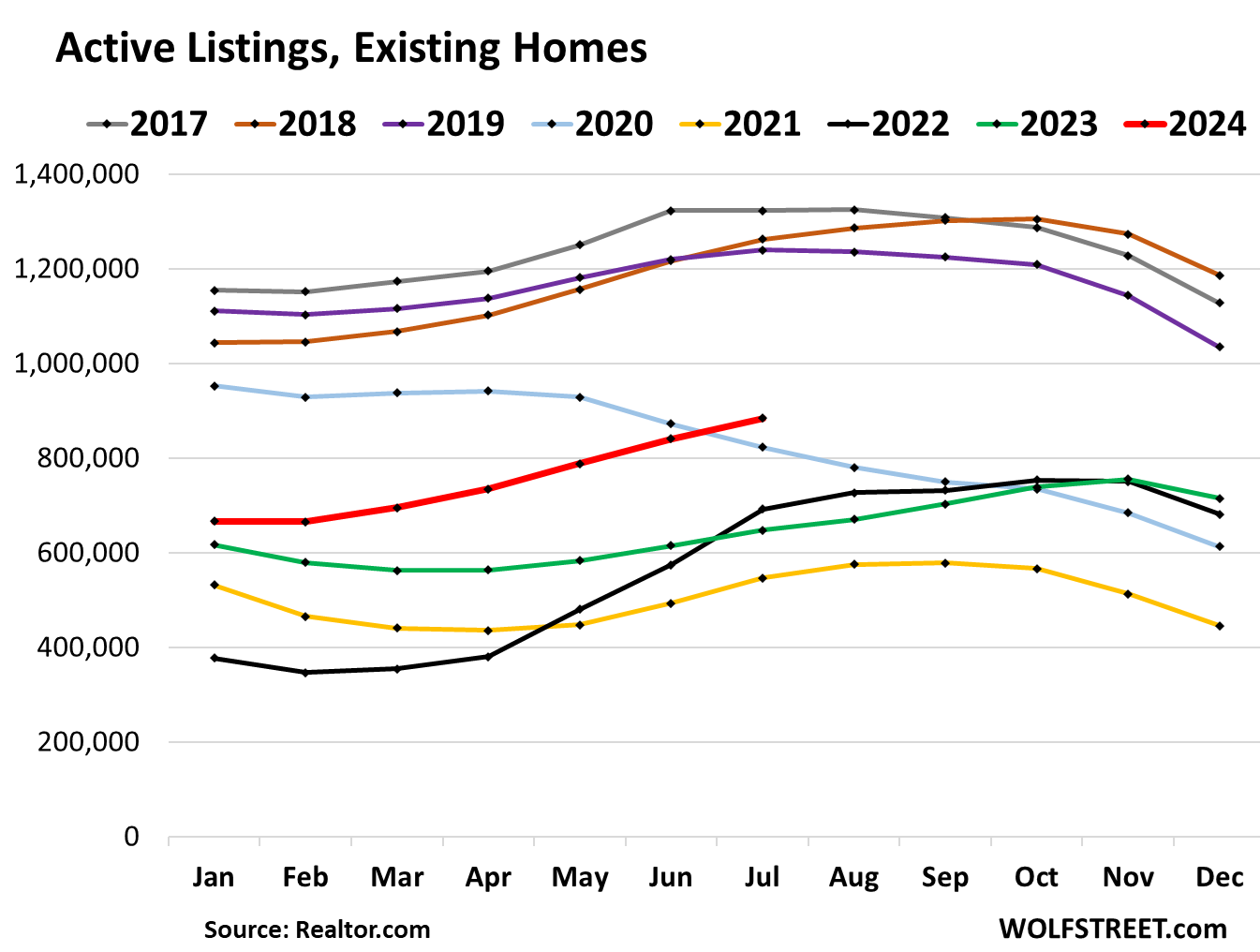

Active listings surged by 36.6% year-over-year to 884,273 in July, the highest since May 2020, according to data from Realtor.com.

Active listings exploded in some of the 50 biggest metros, with data from Realtor.com – note the housing-to-the-moon metros at the top of the list: Tampa, Orlando, San Diego, Denver, and Seattle, where active listings spiked between 95% and 74% year-over-year, while sales fell, and vacant homes came out of the woodwork.

| Metro Area, July 2024 | Active Listings YoY | New Listings YoY |

| Tampa-St. Petersburg-Clearwater, Fla. | 95% | 6% |

| Orlando-Kissimmee-Sanford, Fla. | 79% | 7% |

| San Diego-Chula Vista-Carlsbad, Calif. | 78% | 15% |

| Denver-Aurora-Lakewood, Colo. | 75% | 11% |

| Seattle-Tacoma-Bellevue, Wash. | 74% | 37% |

| Jacksonville, Fla. | 73% | 15% |

| Miami-Fort Lauderdale-Pompano Beach, Fla. | 72% | 5% |

| Phoenix-Mesa-Chandler, Ariz. | 61% | 2% |

| San Jose-Sunnyvale-Santa Clara, Calif. | 61% | 31% |

| Charlotte-Concord-Gastonia, N.C.-S.C. | 60% | 12% |

| Columbus, Ohio | 58% | 17% |

| Atlanta-Sandy Springs-Alpharetta, Ga. | 57% | 2% |

| Dallas-Fort Worth-Arlington, Texas | 52% | 3% |

| Raleigh-Cary, N.C. | 51% | 6% |

| Memphis, Tenn.-Miss.-Ark. | 49% | -3% |

| Sacramento-Roseville-Folsom, Calif. | 48% | 0% |

| San Antonio-New Braunfels, Texas | 45% | 1% |

| Los Angeles-Long Beach-Anaheim, Calif. | 43% | 8% |

| Riverside-San Bernardino-Ontario, Calif. | 41% | -1% |

| Richmond, Va. | 39% | 10% |

| San Francisco-Oakland-Berkeley, Calif. | 37% | 5% |

| Oklahoma City, Okla. | 36% | 16% |

| Houston-The Woodlands-Sugar Land, Texas | 35% | -13% |

| Cincinnati, Ohio-Ky.-Ind. | 35% | 10% |

| Birmingham-Hoover, Ala. | 35% | -10% |

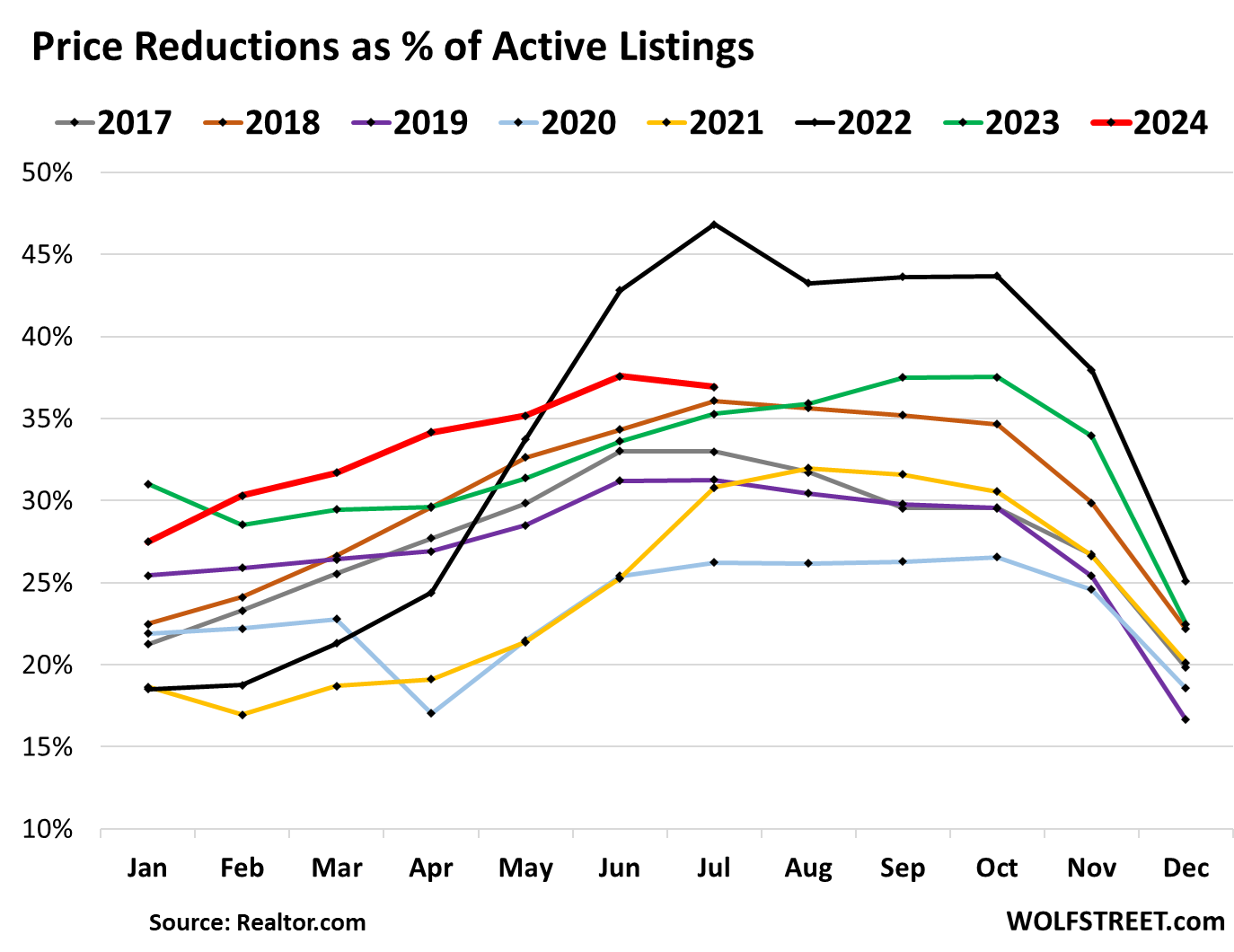

Price reductions as a percent of active listings, at 37.6%, were the second highest for any July in Realtor.com’s data going back to 2016, behind only July 2022:

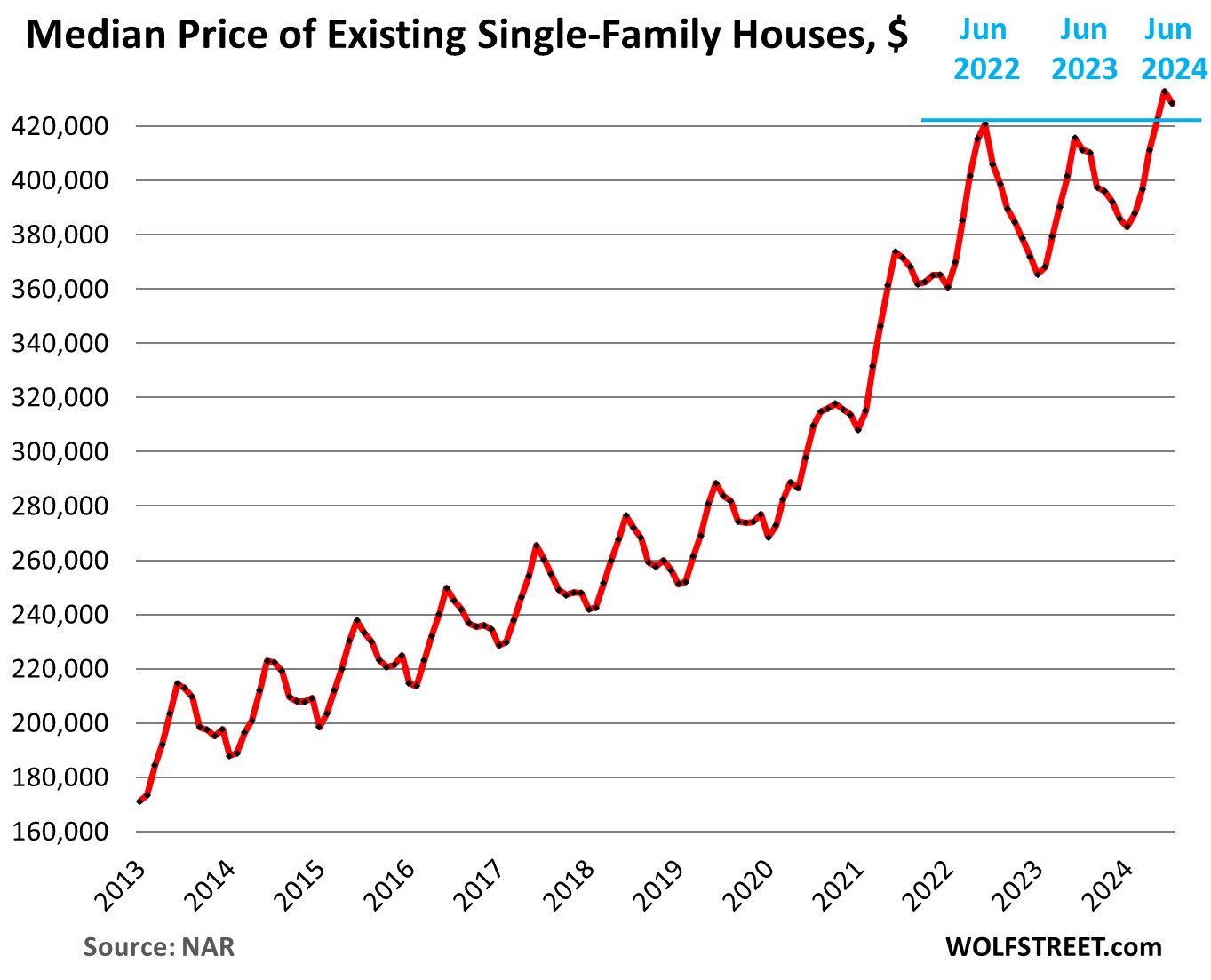

The median price of single-family houses dipped to $428,500 in July from the seasonal peak in June, and was up 4.2% year-over-year.

Since we track the progress from the prior peak in June 2022 – the blue line in the chart below – the median price was up 1.8%. For seasonal reasons, the median price will fall for the rest of the year into early 2025. Junes mark the high points.

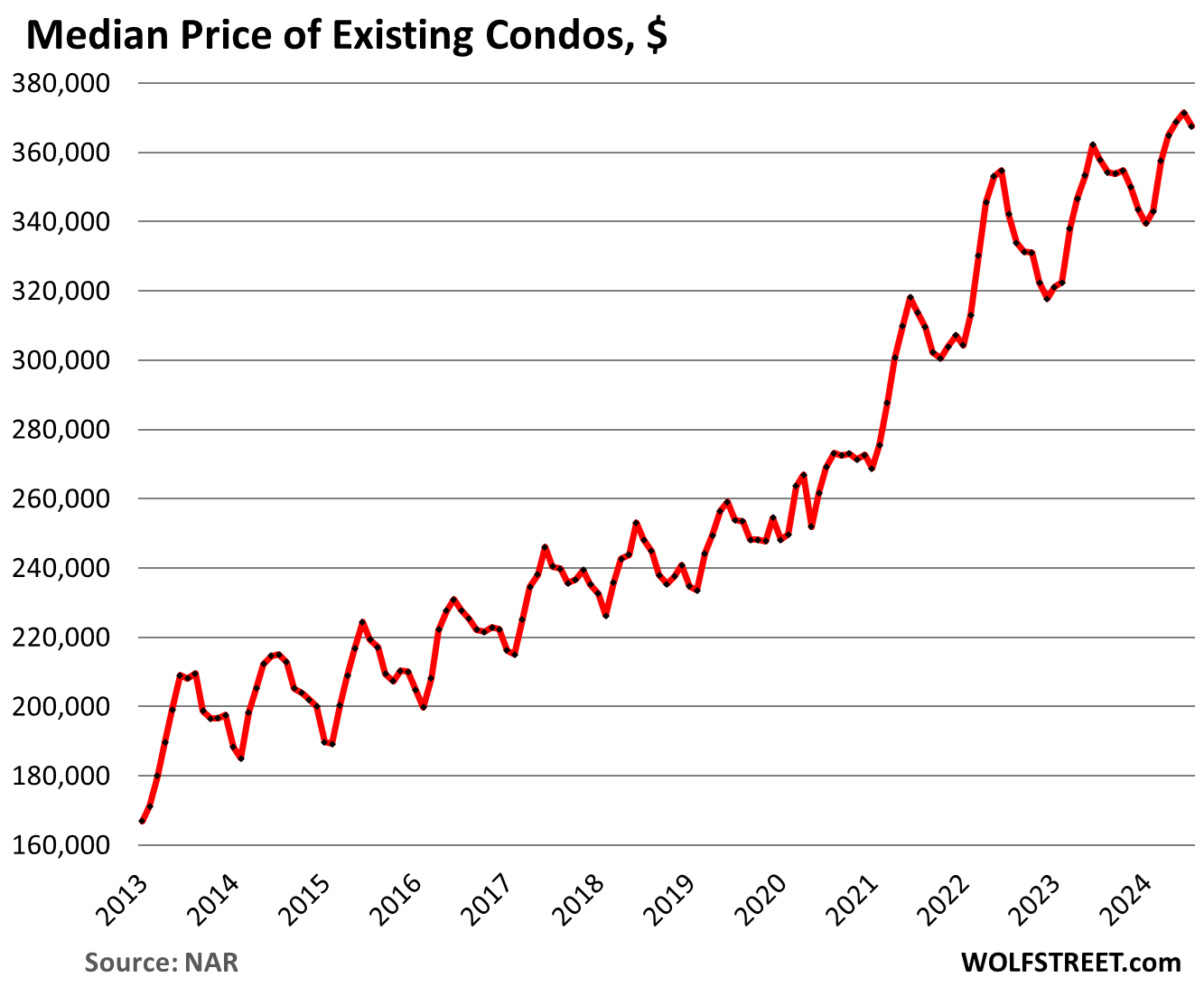

The median price of condos and co-ops fell to $367,500 in July, and was up 2.7% year-over-year. The year-over-year increases have been getting smaller from the 8%-plus range late last year. Unlike single-family house prices, condo prices didn’t book any year-over-year declines in mid-2023. But now they’re running out of steam.

“The condominium market is underperforming compared to the single-family market. Rising maintenance and insurance costs have lessened the appeal for condominiums,” NAR said.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Next steps: prices implode, then housing bulls heads explode. Lots of ‘plosions on the menu. I watch lucky Lopez youtube videos out of Vegas about the car market and according to him he’s getting serious GFC vibes.

I’m noticing more for sale signs around where I live but the listings aren’t searchable online, or even on the listing company’s website. There’s always been a lot of shady pocket listings here but usually they never had signs out.

Car sales are doing OK and are running at the highest pace since 2019, but there is a lot of overpriced inventory sitting around. Automakers and dealers need to cut their prices, after they jacked consumers around during the pandemic. The used-vehicle price spike has already unwound by over half, now the new-vehicle price spike needs to do the same.

How is the collector car market holding up? I read that the art market is in a tailspin – any correlation with the collector car market?

The collector car market is booming more than ever and a 1955 Mercedes-Benz 300 SL Gullwing went for $1,825,000 today on BAT (Bring A Trailer)!

Hagerty, which insures collectors cars, on Aug 20:

“The classic car market continues to cool, as the mixed results from the Monterey Car Week auctions come to a close. The Hagerty Market Rating dropped 0.12 points this month to 63.38, continuing its slide to its lowest value since Spring 2021. In the past two years, the Market Rating has only seen a month-over-month increase twice.”

https://www.hagerty.com/media/market-trends/hagerty-insider/another-month-another-drop-for-the-hagerty-market-rating/

The MB 300 Gull Wing is too rare to be used as a trend indicator of the general collector market, which for its main stream depends on more plentiful and therefore accessible cars.

I was working with a nonprofit group who wanted insurance coverage to drive the classic cars in the Monterey car show as needed in and out of the auction areas – not sure if they found coverage or not but sounds like the show wrapped up.

I just finished watching a report by a cox automotive economist and was utterly shocked to see how high the average interest rates are for both new and used car loans @ 14% for used cars and 10% for new cars. What are people doing, buying cars on their credit cards?

Unlike mortgages which seem to be following the bond market yields down, auto loans apparently have a mind of their own.

Shocking how auto rates reflect the reality of the consumer’s financial risk when they aren’t backstopped and guaranteed by the government like mortgages. Who would’ve guessed.

At least with new cars if you pay cash they don’t charge you extra money like they do if you pay cash for a used car.

Okay, but who’s got that much cash lying around?

BTW, I’m picking up that used car tomorrow. Half down, half financed, even though I have cash for the whole. This dealer absolutely insisted on charging me 1500 for a cash sale, even though I can pay off the loan the next day and he’ll get nothing in terms of a kickback. And at these interest rates, I’m not up for paying one cent more for having to play games with financing, credit agencies, and insurance companies.

I just bought a 2025 Honda Hybrid CRV and they financed it at 4.8% for 4 years. For the ICE version of the same vehicle they were offering 2.9%!

Same here in Paradise Valley and Scottsdale, some houses live with for sale sign and nothing on the website. Every day, I look at listings and cand price reductions are increasing. If a new listing is priced reasonably, it goes pending. Often the properties come back on the market after due diligence. Very few homes have closed and most have price cuts, some significant, off last price. That’s after looking back at a series of price adjustments. I also see a bunch of short term rental type products on the market which most residents avoid. However, we own a 2nd home in Sedona where non HOA properties sell at a premium due to income potential. In high end Paradise Valley, new and whole house remodels are priced over $1000 a foot including a spec house last week which went pending at $1800 a foot. Older properties on acre lots are closing in mid $400s/foot indicating any buyer contemplates a whole house remodel. The other thing here is that people want dirt, so larger lots with homes are sold to scrape or remodel, but condos are selling at steep discounts or lingering for months or being taken off the market. Arizona is still a magnet for snowbirds and high tax state refugees. I don’t have water issues living here but the summer heat is confining and the densification of the metro is contributing to increasing urban heat island.

I spend a lot of time in Phoenix. Already planning to head back soon, mid October this year. The urban infill is actually removing some of the heat island elements. Old asphalt strip malls are replaced with modern condos with green spaces, etc. I’ve heard that between Phoenix, Scottsdale and Tempe they estimate housing for another 509-750k people through infill. Along the rail lines and so on.

You’re right about “dirt”. In ten years Phoenix went from an easy place to have a house and 8000+ sqft yard to basically Southern California. If your home doesn’t share walls with the neighbors you’re considered rich now. Even south Scottsdale where the homeless OD at the bus stops sfhs are $600k.

Fascinating how people think they can determine what is overpriced or not by ‘looking at listings online’. The only thing I have been able to determine online is if a property is even worth a site visit or not.

I lived in AZ for sometime and just couldn’t withstanding the summer and heat.

One can’t even pay me to live there..

I think some context is important here. Median price still very high. The rapid increase in inventory only brings it to pre-pandemic levels when things were good. Interest rates are currently looking like they are not going up for now. There just aren’t the market forces right now for prices to “implode”.

It will take a much higher level of inventory, higher interest rates, and/or a recession to get what you are hoping for.

Median SP is at an ATH. Inventory’s rate of change is what you need to watch and it was taking off, but will slow as fall arrives and unrealistic sellers pull their homes. It’s the spring into next summer when we’ll see the glut come on in an increasing number of markets. Many are already at or near 2019 levels, and my local market hit 2014 to levels last month. YOY, MOM and QOQ are all declining, 6, 4 & 3% Rates will abate a bit more but it won’t help. Unemployment is ticking up and buyer demand will continue to swindle. We are starting to see real signs of what people like myself and Wolf gave been calling for for years.

“my local market hit 2014 to levels last month”

Where are you?

Considering that nationally, we’re still (apparently) far short of 2019 “for sale” inventory levels, I’m curious where those levels are back to 2014 numbers.

I disagree. I live near Tampa. prices are down well over 25% from peak and inventory is still growing. this means the price drops still aren’t big enough to create more demand. it’s starting to look like the entire covid bubble might pop for this region. it was never a demand spike as the realtors claimed, but a supply shortage here… and that’s over.

I disagree. I just looked up the numbers from Tampa on RedFin’s data center. Prices in Tampa are flat. Most definitely not “down 25% from peak”.

@MaxPower

its not an opinion about price declines, its a fact. prices in SWFL are down 15-35% off peak pricing which occurred in 2022. depending upon what you are purchasing and which neighborhood also influences the size of the decline off the pwak…. sfh vs condo vs townhome/villa and what price point 250k 500k 1mm 2mm+.

keep in mind,, prices also jumped up 60-120% from 2019 through 2022. so prices are still elevated after this decline.

@Central Bankster

I am looking at data RedFin collects from the MLSs. Shows no sort of price decline. You can look it up yourself.

As for SW Florida (i.e., Ponte Gordy/Ft. Myers) … parts of it are some of the few markets in Florida that show declines, but that is probably more due to weather/hurricane issues.

Median price is distorted by sales mix changes as well as and over-averaging across too many location-location-location specific markets.

Also, sales process has gotten faster as a result of the various COVID adaptations. The current market has found stable prices at inventory and months-of-supply levels lower than pre-pandemic. So “return to pre-pandemic levels” may indicate a transition to buyers’ market already, especially in local markets with trends running in buyers’ favor.

The “2008” bust saw prices peak in 2005 in some local markets (maybe even 2004 in a few), but prices did not top out until 1-3 years later in other regions.

This time will be different in details and any bust may not be as extreme due to ongoing supply-demand mismatch… but when people start reporting that their local market has topped out, I think that’s meaningful early-warning info.

If you look up median sales price per square foot, which cancels out much of the effect of sales mix changes, you’ll see that prices are anywhere between unchanged to up, even for the markets with giant inventory increases.

So, while the inventory increases are indeed impressive, their effect on prices has so far been negligible.

Note that I am not discounting the possibility that an effect will emerge at some point, it’s just that it hasn’t happened yet. It will be very interesting to see where we will be home price-wise one year from now.

exactly right. prices have already peaked in jacksonville, Orlando, Nashville and Phoenix as well. sunbelt has declining prices and rising inventory, as a general rule of thumb. but some sunbelt markets are lagging because they don’t have the same inventory overhang so its possible this is a slow motion decline instead of sharp drops like 08-09. less forced sellers, less deep recession.

Important context, indeed. Texas, Idaho, Florida and Tennessee are the only 4 states in the country with more inventory compared to July 2019. The northeast, for example, is down roughly 70% compared to 5 years ago. For even more fun context, in those 4 states with increased inventory, population growth has risen at a rate faster than said increase in inventory. Interesting times.

Some news out of US auto makers: GM is axing 1000 salaried jobs. I suspect this will be much more expensive than the Stellantis layoffs because of the severance packages. Also, this downsizing is likely permanent, unlike layoffs that could be recalled. Second and a bit of a shocker, Ford apparently is giving up on all electric in favor of hybrid autos, like Toyota as the news item said. I’m sure I’ve seen an ad for the electric F150 in the last few days, with caption ‘The only EV that’s an F150’

Don’t know if that is a hybrid. If not it would be unusual to be advertising a product you are retiring.

Ford has cancelled some upcoming all-electric models but they are most definitely not “giving up on all-electric”. Not yet anyway. They claim to be working on a reduced-cost electric platform that will allow them to be cost-competitive with Chinese brands.

The Big 3 plan to be competitive with Chinese brands is to beg Congress/President to levy 100% tariffs on Chinese imports. It’s been a successful plan in the US. In China, the market for Western autos is shrinking.

Worked for trucks!

Ford canceled 1 (one) EV model, the high-priced big three-row SUV. Big expensive ICE vehicles, such as high-end pickups and SUVs are now piling up in inventory. They’re not selling. Ford miscalculated some years ago when it got into EVs, thinking that it could charge a premium price, and that EVs would run at $70k-plus. But then Tesla started cutting prices, and the Chinese EVs are threatening, and the sweet spot today is lower prices, and Ford doesn’t have any EVs that it can sell profitably at lower prices, and it doesn’t even have any ICE vehicles that it can sell at lower prices because it canceled its lower-priced ICE sedans. Ford also is now trying to redo its battery supply chain, which today is critically dependent on China. So it’s going to bring manufacturing of batteries into the US with non-Chinese suppliers.

But the announced moves here to lower-cost EVs and battery production in the US are the things Ford should have done years ago. But Ford went upscale on its ICE vehicles, and lost a big chunk of its sales, and it thought it could enter the EV market at the top of the scale. And that was wrong.

Ford executives can never manage their way out of a paper bag. They keep screwing up because they kowtow to Wall Street more than anything.

https://wolfstreet.com/2024/01/04/ugly-charts-of-auto-sales-by-gm-toyota-ford-stellantis-oh-my-got-crushed-by-hyundai-kias-record-sales-tesla-has-arrived/

The total subsidy for battery plants in Canada is up 17 % to 45 billion C or 35 billion US $. For context that would be like 350 billion for the US economy/ budget.

The magic word justifying this is of course: JOBS!

But at what cost per job? For a billion you can give one thousand job seekers one million dollars each.

I guess the hope is that ‘good guy’ Canada’s batteries will supply the US after China’s kicked out. Surely they wouldn’t be subject to US tariffs, just cuz they’ve had 45 billion in subsidies?

Mercury Marine just had huge layoffs & supposedly have miles of unsold inventory around. Big boy toys are slowing also.

Wait, my Realtor® told me home prices always just magically go up.

Surely anyone with a registered trademark symbol after their title wouldn’t lie!

So far this cycle, they’re right. The massive increase in inventory has not yet translated to falling prices, although that might be coming at some point.

Correct. They would never lie. Nor would they exaggerate. They simply wouldn’t.

The long and short of it is: this is still far from being a buyer’s market. Prices are not good – they are only less bad. Buyers at current prices still run a substantial risk of going underwater on their mortgage loan. No thanks.

P.T. Barnum would enjoy this situation. Further evidence of his famous statement.

Hopefully this will be a start to a long trend to bring price back to sanity level in the near future and not some BTFD moment like the stock market…

Personally getting really sick of seeing any crazy crapshack all asking for a million and above in SoCal

haha, I’m sick of crazy crapshacks asking for a million in Scottsdale!

Mahana was ugly, she lived in a tree. But after care, she came down and became a very beautiful woman.

Even if you are a crapshack and in disrepair, you will be found. Some people will never accept you, but know if theirs money to be had, creative craftsman on the cheap can “make over” mahana and reep.

And only morons can’t see through that lipstick on a pig. They deserve the money pit they stupidly buy.

Johnny Lingo would approve

Never in a million years would I have expected to see a Johnny Lingo reference on wolfstreet. Reality is bending.

I agree. 500k 1980s pieces of garbage with only a carport in bad areas along north I17. This country is a clusterfck.

The real tragedy is that the insane pandemic price hikes (50%+ in 3 years, *after* 1 million+ get killed – the real, real tragedy) somehow isn’t yielding *insanely* fast levels of new supply (I know supply is increasing…but apparently not enough to offset those 50% psycho price hikes).

It all depressingly reminds of the perverse results of 20 years of ZIRP – soaring prices due to existing home speculation (followed by implosion) and, yet, fairly damn meh increases in actual *new* home supply/homebuilding employment (otherwise there would not have been Bubble 1.0).

It is very strange how slow/resistant *new* home supply is to price signals over the last 20 years. Meanwhile, speculator orgies lead to boom/busts in the existing home market.

Those dynamics have turned housing (by far people’s biggest expense) into a crapshoot casino for 20 years.

CAS: there aren’t a ton of workers for builders to scale their operation. I define a builder as a licensed contractor who performs at least some or all of the work. So Lennar and DR Horton don’t count. A lot of builders that could potentially run 10 crews and build 30 to 40 homes/yr end up running small operations with 1 crew and it’s just as profitable.

Prices are coming down a bit in my neighborhood but still overpriced. Not sure if it will ever implode. Too many people moving to AZ. It is the next CA.

Remember when Alan Greenspan reduced interest rates? We’re paying for it now…

The “Greenspan put” was a monetary policy strategy popular during the 1990s and 2000s under Greenspan. Throughout his reign, he attempted to help support the U.S. economy by actively using the federal funds rate to aggressively lower interest rates to fight the deflation of asset price bubbles.

Source: https://www.investopedia.com/terms/a/alangreenspan.asp

Under Greenspan, the Nasdaq collapsed by 78% and the S&P 500 by 50%. It took many years and lots of money-printing under Bernanke to bring them back up.

Agreed. Greenspan was worshipped during his reign, despite his many failures. More people need to understand just how poorly Greenspan’s policies worked in practice.

Greenspan also bears the blame for exploding real estate prices. People buy the house they can afford, based on monthly payments. Lower interest rates dramatically, people start buying. Demand increases while supply stays relatively constant- and prices rise dramatically. Jack interest rates back up, and real estate becomes increasingly unaffordable. Homeowners can’t afford a bigger house, or are underwater, so can’t sell. The median income doesn’t qualify for a loan to buy the median priced home, so they can’t buy.

2000 was dot-com bubble bursting was it Greenspan’s fault? 2008 was supposed to be financial Armageddon Bernanke’s response wasn’t about markets but saving the system I think. Not that I like any central gangster Wolf.

The dotcom bust wasn’t his fault. But the dotcom bubble was in part. He tried a little to reign it in with his “irrational exuberance” remark in late 1996, which caused a big selloff, and so he back-tracked. But he didn’t have to backtrack. And then, in 1998, with the bubble in full swing, he cut rates, and the bubble boomed through 1999. By late 1999, stuff was already blowing up. But the Nasdaq overall continued to rise until March 2000. And then it imploded under its own weight.

“And then, in 1998, with the bubble in full swing, he cut rates, and the bubble boomed through 1999.”

I trust Powell has studied history and won’t repeat this error.

Just finished appraising a condo in the center of DC in a relatively good neighborhood which a private owner was holding on to try to make all of his initial investment + improvements. It was in pretty good shape and unoccupied. After three years of trying to get top dollar he dumped the property for a $30K loss. This could be the new trend as the economy slips into a recession.

Man — I just don’t see signs of a recession. Not saying I think the gooey filling isn’t mostly sugary garbage, but I see no signs of it running dry.

There seems to be a kind of econo-dysphoria beseeching much of the public mindset. It’s perpetual springtime; a blue bird on every window sill singing in A major.

There is no recession yet, despite the BS, and there likely won’t be one for years if the Fed starts its cutting cycle in September. The Fed is cutting just in time to enact a “Fed put” on overextended lifestyles. Party on!

I see on Zillow for my Chicago NW suburb a home listed at $650k selling for $700k. Not the only such instance. I strongly suspect existing-home sellers are doing deals with buyers to buy down mortgage rate in exchange for a higher sale price. This will come back to bite the buyers if prices eventually start to fall to restore affordability, and they are forced to sell; if the market price for the home falls to, say, $600k they are upside down by $100k instead of just $50k if they hadn’t bought down the rate.

jm,

I see the same thing for Condos in a Chicago Western suburb.

County Tax Man must be be in cahoots with the banks to buy up houses at stupid high prices to justify much higher property value reassessments in the near future. Not only do these foolios get the privilege of overpower for a roof over their head in typical american suburban hell-style land, they will be rewarded with paying annual property taxes that amount to about a third of total year income of the average commoner. All these people who are pat themselves on the back for not being a renting sucker must not like to admit to themselves that it’s possible to rent a decent places for the same monthly cost as the property taxes alone break down to be. That doesn’t include maintenance like a new roof, furnace, water heater, landscaping, air conditioner, sewer bill, etc…… People are being had, trading their lives for vinyl siding, chipboard subflooring, sheets of drywall, and being completely dependent on the government to eat and interact with other humans since it’s not possible to walk or ride a bike to anything you need or anyone you want to see. That condo downtown sounds nice though. Could pretend your living in an episode of sex in the city with the wind at your face and the cold shriveling your genitals.

It’s odd that so many people don’t understand how property taxes work. When property values go up the rate required to fund the counties budget goes down. Last year my valuation went up but my taxes went down slightly. Landlords also pay property taxes, they are not going to rent their properties for less than the taxes, that’s absurd. I have a 1.2M house, the taxes are $5400/year the house across the street from me rents for $5,000/month. My house originally cost me $475k Who has the better deal?

Residential property owners in the Chicago are being reassessed at many people are being hit with hug tax increases. Property taxes are generally going up all over the country, regardless of the formulation for assessing and taxing the property owners. I understand the sort of property tax assessment you are talking about, but it does not mean that those places are still not asking for overall more money to fund more pet projects. Specifically, Illinois and more so, the Chicago metro area, have some of the highest property taxes in the country. Look at property taxes in Lake County, Il for example. A not so great house in a not so nice suburb will easily get you a $10,000 a year property tax bill……..that’s for a house that is less than $300,000, which these days is not that high considering average house prices across the country. Imagine the taxes on a $700,000 house. $20,000 a year in property taxes is reality for a wannabe McMansion. Check DeKalb County as well for houses in that price range, which there should be a lot of. See Republican states like Texas. See a pseudo-Republican state like Utah as well, where taxes are going up, despite having the type of property tax evaluation formulation and budgeting like you are referring too. The other part you are talking about………that’s why if you rent, you don’t rent a whole house. Rent an apartment. The utilities can be multiples cheaper for an apartment than for an entire poorly built house. Shared walls with people who have similar unit temperatures internally, better exterior construction, a single roof to maintain for many people, little landscape and snow removal spread over many tenants, one sewer line and water line for the landlord to pay the bill for, etc…. It’s called efficiency. Thermodynamics. Science. Cost per unit. Newer apartment buildings are built like complete sh— and are advertised as luxury apartments. Older smaller apartment buildings can be relatively well built, much better than homes. Most homes built in the last 30 years sound like a speaker bass box when anyone is moving around. The same for newer apartments. Good landlords with a smaller older style well built building who manage it themselves is what matters here. Those are humans who are worth paying rent to. Not the lazy money grubbing rent seeking class of morons who think they should be handed cash for asking a bank to hand them money. Taxes goes up on an entire house they are renting, you can’t always charge tenets more. Why do you think a landlord can always pass on their cost increases but business can’t and risk losing customers to other businesses. Competition. They take the risk, they can take a loss. They can sell their house. They can suffer more loss by letting it sit vacant for trying to get the peasants to cover their lifestyle and poor investment decisions. A lot of places have overbuilt out apartment capacity in the last few years. People can move out of a greedy landlords house if the landlord thinks they are god’s gift to humanity.

In my county in California the property tax rate has not gone down in over 20 years, in fact it has gone up, despite valuations doubling or tripling.

Government is always hungry for more.

Only a dedicated anti-tax voter base protects property owners from higher tax rates.

In Illinois the property tax scheme is quite convoluted as you stated. Many were complaining during the last housing bust: “but, the value of my house went down but why didn’t my property taxes?” Because the county/township still needs the same amount (or more) cash to operate regardless of the value of your house!

@Cupcake,

Utah is a Republican state, but has a relatively high overall state and local tax burden, although income taxes are declining. Property taxes in Utah are quite reasonable though, at least in the areas I’m familiar with. It is not a low tax state like WY or NV though.

It’s not 1.2 million until you sell it.

South Lake Tahoe will be voting to tax “vacant” homes defined as homes that are empty for half the year (183 days or more). I’m wondering how Wolf defines “vacant” homes. Our cabin is empty for more than 200 days a year but is rarely empty for 14 days in a row and I would not call it “vacant” (fortunatly for us we are on the North Shore and don’t have to worry about the “vacant homes tax” passing).

What method of enforcing this are they going to use? Flock cameras? Police monitoring?

If it’s not owner-occupied, I imagine you’d have to show the taxman proof of a tennant or vacation-rental clients having signed leases to occupy the premises for at least 183 days.

ApartmentInvestor

These are vacant homes on the market for sale. No one lives in them when they go on the market. Owners bought another house some time ago and moved, but kept the old house because they didn’t want to sell when prices soared. They wanted to max out their gains. This is why there was such a shortage of houses a few years ago, because buyers didn’t sell their old house, but kept it. Now those houses are coming on the market. So you see inventory shoot up, reversing the decline when those homeowners didn’t want to sell.

You’re talking about stuff that is NOT for sale. That’s totally irrelevant here. Apples and oranges.

However, a vacant-home tax on vacation homes in South Lake Tahoe could put some of those vacation homes on the market. But they will still be a vacation homes because of the location they’re in.

Sounds like they are doing it at least partly for show while leaving loop holes big enough that the average rich white collar criminal can drive a semi truck load of furniture through those loop holes. People will just lie and say they are occupied even if they aren’t. They will say that they are there more than they are. They’ll say that their extended family member is staying there while recovering from a spending addiction. If they really wanted to do what is right, they would tax non-primary residences at a higher tax rate. If someone can rent the place as an airbust-n-balls to qualify as occupied then that just contributes to the investment pattern that helps to create a housing shortage for local residents. I’m all for freedom and success and choices, but people don’t need to have so many homes and use them as investments when people are trying to have a first home. It’s a waste of material and human resources on a planet of finite availability. It would be like, before the internet, me going and checking out every dictionary that the library has and keeping them for a month just because one isn’t good enough. All the other people, f-em.

People won’t be able to just lie and say they were there more than they really were or that they had renters when they did not. It will be up to the owner of the home to prove that they were there. The government doesn’t have to prove anything. The burden of proof is on the taxpayer.

This is how people get into trouble and end up in prison for tax fraud.

A local city government is very different than the IRS. It’s not that hard to lie and trick police, and a lot of times police don’t want to dig too deep anyway. Considering the type of people local and county governments employ are not real go-getters, I’m pretty sure some dishonest answers on paperwork or a phony rental contract is not that hard to show. If they want to see rental contracts, are they going to look through all the airbnb listings for the year with a fine toothed comb for the calendar year and see if it’s just over the required minimum days of occupancy or not. People lie all the time. They lie about past work experience to get jobs. They like to their spouse. They lie to get PPP and EIDL loans. Again, this isn’t the IRS they are lying to, and people do that as well. City employees want to do the least amount of work to get through their day. If you lie to them and tell them you meet their requirements, it makes their job easier and it makes them happier with you. Anyone can print up a rental contract they get off the internet and put a signature on it and claim it’s a renter. Are they going to start demanding copies of driver’s licenses of the tenets and all the rental payment checks from the year, with the risk of liability for handling such documentation and risk of making false accusations against someone who really did occupy the property. They won’t do anything. If they wanted to, they would tax non-primary residences at a much higher property tax rate and if they won’t do that, they won’t do s—. Fake it till you make it is the new way in america, don’t cha know.

@Lucca

Sounds dystopian.

Im all for winding down the housing investment craze but i think it should be done the good old fashioned way. Let the market contract from higher interest rates, cut out any and all MBS nonsense and let everyone get cleared out that isnt financially responsible enough to weather a few years problems. Maybe some welfare for the poorest of the poor with legitimate income issues so we dont end up with a flood of homelessness.

Im not a fan on all these band aid solutions that let the rich get away with murder while the middle class gets the old yeller treatment and the poor stay trapped.

Im also sick of working a 6-7 day, 70 hour week, a 2+ hour daily commute, and being at the nearly highest paid company in my area stacking back 110k/yr and still not being able to buy a “starter home” in this area.

@Lucca,

Simple to show proof of occupancy — put a lot of lights in the house on randomized timers, and same with the sprinkler sysrem. Hand over daily graphs of your utility usage to the government, and threaten to sue them if they question you. This is the problem with unenforcable laws — there are always loopholes and workarounds. Sort of like insider trading.

It’s too bad that there isn’t an initiative to raze all homes over 4,000 square feet. Let’s make Tahoe great again.

Reminds me of a recent walk through Venice Beach. Tons of available street parking. So quiet you could hear a pin drop. Then it dawned on me. Probably half the housing units are empty 10 months of the year. But tax credits for first time buyers will surely do the trick

Wealthy people will buy yet another home, but do it in the name of their young adult children with the child signing the paperwork and the parent sitting there and overseeing the process and writing the checks. The child will get to live in the house for free for a few years and then the child, on paper at least, will be selling the home to their rich parent who originally paid for it. The house will not be sold until the minimum time period has passed to avoid paying a higher capital gains tax on what the profit between difference in sales prices is. The alternative is for the child to sell the property to the parent (the parent to buy the house back from their self really) and contribute to potentially lowering the assessed value for property tax purposes for the long term holding, or play funnier games through tax writes based on tax loss harvesting like what seems to have been the case in the years following the last recession with many odd transaction prices occurring at strange time periods. The time most people spend at work is the time that a lot of wealthy people have to try to figure out how to avoid paying taxes and formulating their next grift.

I think it was implied based on the previous comment but I meant to specifically address the potential first time home buying government handout of $25,000 gossip that is going around and would not be surprising if it happened. I’ve already seen almost exactly the same government handout happen legislated and passed at the state level of a specific state ran buy a cult that is only exceeding in wealth holdings by the Vatican. The government lawmakers are in on the property grift, big time. It’s not just the stock market. Mr. T himself made his money on real estate and his first presidency helped to fast-track the pounce onto the last remaining component of the United States to be fully capitalized and financialized and overtaken at the higher levels of wealth stratification. Natural resources plundered. Check. Human plundered check. American businesses plundered. Check. Banks plundered. Check. Stock market plundered. Check. Real estate plundered. Check.

@Cupcake

Sure, there may be some of that. But most will not be, I’m willing to wager.

I received a $10,000 total tax credit when buying my first home in the SF Bay Area in the 1990s. It was either a state or county program IIRC, and I had to live in the house for at least 8 years before selling in order to use this credit. The paper work was specific and demanding in terms of my providing proof of situation. There may have been an upper limit on my salary in order to qualify too, but it’s long ago enough now that I don’t remember for sure.

I imagine a determined well off family like you mentioned could pull such a grift, depending on how they’d set it up. Doubt it would be all that many doing it though.

This program was quite helpful, as I was young, did not have much savings, but had just gotten my first decent paying job out of grad school and needed whatever help I could get at the time to afford that starter house. It was very useful in getting started in home owning when I needed it most, and I would be pleased if a new program can help others that are in those “needing a starter home” shoes now, in a similar way.

I thought when they raised rates in 2022 and homes sales plummeted it would hit the economy/GDP more than it has. Realtors, lenders, home depot, furniture stores, escrow title, etc… all laying people off.

2023: -2.5%

2022: -19.1%

2021: -34.5%

2019: -26.7%

2018: -26.7%.

As Wolf’s numbers above show. The fact the sales are SO much slower than normal…. for 2-3 years in a row now…. I thought would have slowed the economy & GDP more. And I have been wrong.

I think if the 10 yr treasury stays above 4%, sales will stay sluggish indefinately. Either prices have to fall by 25% or rates need to come way down. Rates can’t come way down unless inflation comes way down.

If I were a betting man (and I am), I would speculate that longer term rates may continue to ease in the near term, but likely go a heck of a lot higher in the intermediate and longer term. That would likely crash both the bond and housing markets. After all, it’s simply too risky to be holding American long term debt for a pittance above inflation.

Sales of existing homes have almost no impact on GDP. The impact from housing on GDP comes during construction, when they enter the GDP formula under residential fixed investment.

Mortgage brokers and mortgage bankers started getting laid off massively in mid-2022. By mid-2023, the layoffs were done. Several thousand mortgage brokers were laid off. So that’s minuscule in the overall economy. And they quickly got other jobs in what was then a still hot labor market.

In terms of Realtors, I would suspect that quite a few of them are leaving or have already left the industry to work somewhere else.

Rates will not fall dramatically, ipso facto, unless we head into recession. Therefore, rates will either stay close to recent values, or fall due to economic circumstances that will push housing prices down.

Oh no, not our beloved San Diego on this list..I am sure as inventory starting to go up, we will get people still saying price continue to go up and houses are sold in matter of hours or days…

They might be right for now but if this trends continue for long I wonder…

Talking to a couple housing bulls I know in SD, they are very much in the “prices and sales are going to spring to life as the rate cuts come” mindset, and still looking for more “investment” properties to purchase, the currently horrendous cap rates be damned. I think they’re very mistaken, and have encouraged them to step back and stay out of this market, but it’s going to take quite a few more reports like these to shake the bullishness out of them.

nah, just enjoy the show…you can only lead a horse to water, but you can’t make him drink. So far they have been right and they don’t think this can ever go south and we will never have any significant correction in housing ever…

In the meantime, get out of their way, plus you don’t want to be blame if you talk them out of buying and the market does continue to go up indefinitely…we do live in some weird F up time…

I want to buy a house / condo in a nice part of San Diego. Both for investment and long-term purposes for the family. The cap rate after expenses work out to 2% on the cheapest of properties. I would rather just rent and use my capital to earn money. Home price appreciation seems like dead in the water over the next few years.

Realtors point to short supply and housing not available in California. But even the rarest of things need to have a reasonable price. A Van Gogh might be expensive, but could be a phenomenal investment. Unfortunately, housing in California is not among those

A Van Gogh doesn’t hit you with about 1.25% of its assessed value—which starts at the inflated purchase price you bought it for—in annual property tax, plus maintenance, either.

A nice part of SD (thinking OB, PB, Point Loma, La Jolla, even Bay Park) is going to set them back starting at about $2 million right now for what’s really a pretty mediocre 3-4 bdrm, 2000 to 2500 sqft home. Why so many people are eager to sign up for $25k in property tax alone (most of which is now non-deductible) for something like that “as an investment” is wild to me.

OB, PB, bay park are nice? Lol! Small areas are, rest is dicey. Mission hills is much better.

I just saw a video that the Costa Verde shopping center in the golden triangle was now abandoned. I lived a block from there over 30 years ago. If I was told back then that that area would collapse I would have figured world war 3 must have happened. Very nice part of San Diego. Just goes to show how far this country has fallen.

@NYguy the UTC “Golden Triangle” area has not “collapsed” it is just taking longer than expected for the guys that bough the “Costa Verde shopping center” for $125 million a few years ago to get going on the big redevelopment they have planed for the site.

“…it is just taking longer than expected for the guys that bough the “Costa Verde shopping center” for $125 million a few years ago to get going on the big redevelopment they have planed for the site.”

The next owners who buy it for $12 million will do better.

I used to visit UTC long back.

Last I visited was 7 years back.

I live pretty close to this place.

Let’s wait to see the effect of the new realtor scam that is designed to force buyers to pay a commission for showing a house or houses.

Praying for a buyer rebellion. +92% of homes are found by buyers on the internet without a realtors help. Forget using a realtor for contracts, use a lawyer.

Lawyers cannot get you access to a house to see in person that you find on the internet. Realtors can.

I never needed buyers agent to see a house unless things have changed recently.

I’d simply email listing agent for the showing.

The boomers approach eighty. Gen alpha (2010/2024) is the smallest generation in 100 years. They are 30/40 million smaller than the boomers.

There are not enough people to buy the boomer’s homes. Kamala Harris,

if elected , plans to build 3,000, 000 housing units in the flyover areas and in the suburbs.

Your numbers are wrong, and I would add that ongoing immigration hasn’t kicked in yet for the current youth generation, while it has swelled the ranks of the older generations for decades. There is no demographic crisis here, you should look at Asia and Europe first.

I’m always amazed at how some people put economics before citizenship. It’s as if they consider human beings to be moveable units of consumption that can be distributed about the globe without any thoughts of how that impacts culture, customs and traditions

Jon – …’twas ever thus…(…and time to re-read some Studs Terkel…).

may we all find a better day.

I can’t help feeling that the real estate market is going to go crazy if the Fed decides to lower the FFR by 25 basis points. Even at these painfully high prices! I definitely do think that more people will list their homes if that happens, which will add to inventory, which could put downward pressure on prices. It’s anyone’s best guess from here. Thanks for the great data as usual Wolf.

Inventory is still low. Equilibrium (depending on price point) is normally around 6 months supply. We’re at 4, which is only high compared to the crazy 1 week or 1 month supply during the pandemic.

There’s still a long way to go before prices drop a lot. It’s beginning to happen with price reductions, but if/when the fed drops rates, sales should pick up, even at higher prices.

“Equilibrium (depending on price point) is normally around 6 months supply.”

That was 20 years ago. It’s now completely out the window because technology has finally arrived in the RE industry. Back then a house went into inventory when the seller made a deal with a broker. Then the broker would prepare the weekly or monthly RE ad in the local paper or RE journal, and so the print version would begin to circulate. And that would start the process of potential buyers first seeing the ad. When a deal was finally made, getting a mortgage and closing took a very long time, everything done on paper being sent back and forth. And when the deal closed, the home was finally taken out of inventory. These processes combined could take two months or longer.

Now the day a house is listed, it shows up on the internet, and buyers can do video tours and buy, and getting a mortgage is very fast, and all the processes have shrunk to just days.

If you speed up the process between listing and closing by two months, the inventory shrinks by two months because homes on average spend two months less in inventory. So keep dreaming about your 6-month equilibrium, LOL, it’ll be a glut.

But if the Fed cuts by 25bps, maybe they’re about to do a whole cutting cycle… in which case these prospective buyers may think it’s worth waiting a few months or a year if rates (they think) are coming down even more.

Mortgage rates, which track 10-year Treasury yields, have already dropped a whole lot, pricing in a whole bunch of rate cuts. So that’s already priced in. If that’s how many rate cuts we get, then mortgage rates are going to stay about where they are. If we don’t get this “whole bunch of rate cuts,” mortgage rates will likely rise some.

Sadly even though this is the case, it’s also counter to every MSM / housing bulls talking points and beyond what a lot of people understand about mortgage rates. Everyone and their mother is counting on that rate cut to bring mortgage rates down to 3% in some fairy tale scenario…These are also the same people that drank the date the rate, marry the house koolaid. They all think their house will continue to rocket up and can simply refinance down to with that magic rate cut is right around the corner, so over leverage in buying a house they marginally can afford is just a short term hedge…

If house price falls by enough they won’t be able to refinance.

I don’t see 3% mortgages ever existing again in our lifetimes.

I’ve been trying to find the answer to this, but no luck so far.

What percentage of mortgages are closed or replaced (via sale of home or refi) before maturation? And before 10 years?

It was seven years before sale or refi. With the 3% mortgages amid these rates, it might stretch out a little further.

unlikely. short term rates are inverted to long rates. fed can drop and is expected to drop ffr by 1% year end. if economic and employment data don’t surprise to downside, mortgage rates will be flat into year end. however, I personally expect data to surprise to downside, so you may get some further easing in long rates… but then again, spreads could widen on mortgage rates vs treasuries, curtailing improvements there.

there seems to be a lot of confusion around this topic. ffr do not drive long term rates. rather, long term rates drive ffr decisions by the fed. perfect example recently, long rates spiked dramatically, THEN the fed raised ffr.

If the fed cuts (even 25 basis points) the power will shift from a buyers’ market to a sellers’ market again. These sellers are in no mood to sell lower. They will not budge. I wouldn’t be surprised that its they who are taking the cash-out refinance to keep up with the payments.

Seeing a ton of new for-sale signs in my hood… much needed inventory as sub-1500sqft starter homes are still in the $400-450k range

I’m going to buy up all the companies that make refrigerators and then jack the prices up on refrigerators to like $20,000 plus each. Some peasant family needs a basic Hot Point refrigerator for their little crap shack, that will be $20 grand, sorry, not sorry. You want a fridge, work harder like the old days ya bums. So……..a lot of people will start to accept not being able to own their own fridge. They won’t be able to keep much food at home under their own control and won’t be able to cook during the week. They will eat out more and go buy food daily more. Then, we can jack up all the prices in the restaurants and the perishable items at the grocery store. If they don’t like it, they can buy old Twinkies off of eBay, maybe invest in them to sell in their neighborhood to other peasants like them. You can die with a conscience and holes in your pockets or with a cold heart, a fat bank account, and see your kids go to the best schools where they learn how to copy and beg for extra credit points.

Too complicated and too much work in doing that…go big or go home, take a page out of Mad Max and control water supply, then you can really jack up the price..this is already kind of a thing for Central Cali farmers by the lovely Resnick family..

I’m an insanely wealthy amateur who lives in a storage unit. You’re talking about professional white collar criminals. Kind’a like the Pritzkers and their tubby son who moved from Coliformia and commandeered the state of illinois to his benefit where it’s less ostracized to be morbidly obese compared to the west coast. The criminals that run this nation are so boisterously arrogant and open about their ways at this point that the Prickster bragged at the DNC the other night about how he’s so much richer than Mr. T, the wanna be billionaire from NYC. Imaging, two daddy’s boys rich multi-generational wealth having spoiled old children standing on stages telling brainwashed commoners that they know what is best for them because they are rich and never had a real job in their life.

Looks like tin foil hats are cheap do better. You are just looking for an excuse to blame others for your failure.

So you’re saying I need to stop being a wimp and gain a lot of weight and inherit a lot of money, then so be it, that’s what I’ll do my man! Oh, and the hat isn’t tinfoil. Is high grade aluminum, from the Reynolds family of Lake Forest, Illinois.

greed causes blindness. blindness leads to insolvency.

That’s a great a line. Did you come up with it?

The wallstreetbets sub has entered the chat.

Lol

That is an absurd take on the current environment. Laughingly ridiculous.

Laugh all you want, until your fridge goes out or runs away and I’m selling you a new one for 20-G’s. I bet you used to laugh at all us wimps back in the days at school too. Now we’re all jacked on steroids, tatted up with full sleeve artwork, and arresting guys like you on domestic violence charges for grabbing your wife’s banana bread when she’s mad at you.

Crazy driving through Main Street in Windermere, FL (just outside of Orlando) this past weekend. Saw like 4 houses for sale in a row (FSBO for one) all canal front and on other side saw a sign for open house. LOL. Been a while since I saw that. Not much selling…prices are still stupid high for what they are. I believe one of the homes next to the for sale is still listed for rent, but no longer with sign in the yard. It was bought probably 2 years ago now and immediately put up for rent (canal front) and price cuts…never seen a car in that driveway or lights on. At least the house on the corner finished being built and wasn’t a flip…probably can’t flip in this market.

Football has two hearts, the offense and the defense. As a former offensive lineman, I tend too cringe at the mis-management of the offensive core which leads to losses.

etc; going back to the problem before us, the housing market which is an existential threat to our culture.

From the economic perspective, there are at least four active economic bubbles in housing, stocks, bonds, and inflation. I’ll get too my point after I set the stage for the severe contraction I see, dead ahead post election.

Beauty, often hides.

At some point, it just becomes a better deal to move out of the country if you have a nest egg. Things aren’t off the rails yet, but the caretakers of the track have given up on maintenance. It’s like the whole country is being run by BART management.

— It’s like the whole country is being run by BART management–

Oh my, now there’s a formula for success.

Not.

Especially in the pre-pandemic days when the workers could get in on the fun and threaten to clog up road traffic with a strike every 3-4 years.

I envision the people that I encounter as points under the normal distribution curve, the odd begin at +- 1 std deviation.

Einstein was + 1.96 std deviation from the mean expected response.

I had the opportunity to see an adventure that has always been there but I was blind. Until recently.

I’ve noticed when listings get delisted, the listing data gets scrubbed from websites, as if they were never listed to begin with. Previously had this issue with Redfin, but now seeing it happen with multiple listing sites, Zillow, Trulia, Coldwell, etc. This is obviously to the sellers benefit.

It still comes up in Google cache and some random website further down search results.

When I’m looking on Zillow, I still see “listing removed” with date and before then the entry for “listed for sale” with price, preceded by prior efforts to rent out with asking rent listed, and then rent listing removed, etc. It’s still all there. It never left.

You’re right. Properties that have been delisted in CA or HI have that data.

I am tracking house prices in Portland. I had favorited 36 houses in that area. Four of these houses have been delisted in the past few months. All 4 do not have the delisted info in the major websites. Putting the address here, hopefully not against the rules:

8411 SW 47th Ave, Portland, OR 97219

1775 SW Troy St, Portland, OR 97219

231 SW Gibbs St, Portland, OR 97239

8810 SW Spruce St, Tigard, OR 97223

evidence it was listed on moveto: https://www.movoto.com/tigard-or/8810-sw-spruce-st-tigard-or-97223-491_15576575/#propertyPriceHistoryPanel

The third one was delisted twice, once in 2020 and once in 2024, and none of them are on there. Maybe it’s an Oregon thing, maybe it’s a service thing, you pay extra and they don’t show the delisting history. But the fact that all four are missing this info is rather curious.

Wow. Some crazy prices for soggy ol’ Portland. Alright city 20 years ago.

Same as many southern states. Somehow, they get property history removed.

Correct . That’s my experience as well.

Zillow etc. holding a lot of inventory now?

Wes,

Zillow abandoned the house flipping business in late 2021 after booking huge losses, and then dumped all of its inventory in 2022:

https://wolfstreet.com/2021/11/02/zillow-comes-unglued-lost-1-4-billion-on-flipping-houses-since-2019-bails-out-lays-off-25-of-staff-stock-plunges-further/

I often wonder if there are games that RE agents or sellers can play on Zillow or Redfin to show pending or contingent but then get relisted again after a week or two. I am seeing more and more of that now. Perhaps it’s truly pending sales but buyers are falling through, either backing out or not qualifying for the loan…

It does look a bit sus, when it’s a tiny place in not that great neighborhood asking big money, showing pending/contingent, then all of a sudden it’s back on market. Meanwhile nicer and bigger house nearby are stuck on the market longer without the whole pending then back on the market deal..

reminds me of an auto auction I attend. The auctioneer bids up the price himself with no one bidding sometimes, hoping some fool will place a bid along the way and he sells it then. Then suddenly he restarts the bidding way back again acting like it was not him but somehow some bidder backed out or some miscomunication or similar not to expose himself. Fraudulent practice but common in a lot of business. It does work sometimes because too many people cant price things accurately.

I’ve seen it too. It doesn’t happen every time, but I have definitely seen it enough times. I have seen and posted about many other oddities much more concerning than the scrubbing of listing prices, previous sales prices, price reductions, listing removals and re-postings. You’re not seeing things. It is market manipulation through manipulation of data. The whole market can be skewed by these data brokers now, if they so choose. Yes, I understand that transaction information comes from counties and such as well as non-government sources. The states with non-disclosure laws really open the door to major manipulation of home seekers and they’re being had from what I’ve seen. Home buyers are operating in the dark and don’t really have much references to go by.

So…in 2022 sold my house in texas – tried working with local realtors and told them there are 4 words i never want to hear “Back on the Market” – they all got long faces.

eventually sold to OPENDOOR – got my price and no hassle closing in 1 day

In the sense that some dirt bag hawking junk, like now. Buy into an over priced market, bailing out the smart money taking advantage of inside information.

Should we care.

The idea that houses are in a bubble is hardly inside information…

Much of the housing problem is due to the dramatic increase of Airbnb and such short term rentals of single family properties. These properties seem unlikely to be at the ADA (American Disability Act) accessibility level of professional hotels. Further, the safety level of these widely varying unique properties seem unlikely to be at the level of a professional hotel. Since there is little media reporting of ADA or Tort lawsuits against short term rentals, it appears that such potential plaintiffs are undeserved. Such attention to potential plaintiffs would both increase the quality level of short term rentals, while eliminating the conversion & removal of housing stock that was never designed or zoned for commercial purposes.

There are lawyers who make a living bringing these ADA suits against commercial establishments. Another form of ambulance chasers in a way.

But maybe they could become more useful by doing this and freeing up supply as airbnb owners get wary.

$428,500? So, what’s that, like 8x the average wage? Sounds sustainable…. LOL!

It’s not sustainable at normal interest rates. Which is why volume has collapsed.

or the current PRICES. And guess what Powell is signaling a cut, gee, I wonder what will happen to prices now?

It really is criminal at this point.

no “emergency cut,” not 50-basis-point cut, just a 25-basis-point cut. A couple of weeks ago, the argument was over either an emergency cut right now or a 50-basis-point cut in September.

our consumer-driven economy cannot run as hot as they’d like without artificially low interest rates.

So, Jerome Powell will be Arther Burns, on steroids. Lovely.

The economy does seem sound.

Last month or 2 without the cut it’s basically been treading water. Which is a good sign that a cut would propel it upward.

Inventory increases so far have been very impressive but with hardly any effect on price… yet. Based on Wolf’s third chart, we’re still sitting at nearly 25% less inventory than what was seasonally normal prepandemic.

It may take a recession to get affordability back down to within reasonable levels. Otherwise, the only other avenue would be a very long stretch of time where home prices increase at less than the overall rate of inflation.

Its regional though. There are regions where inventory levels are at 2019 levels or exceeding 2019 inventory levels. Sunbelt areas mostly. You have to realize that demand is much lower than 2019 levels in these areas as well. So we have some staggering Month of Supply levels for certain types of listings. Condos 2mm+ I see areas all over SWFL where MOS is 10-15months. These markets are likely to crash. Whereas SFH, 300k, MOS is 2-4, unlikely to crash, but might soften a bit.

The sawtooth “median price” chart has a pretty clear post GFC trend, that appears likely to be crossed again sometime around 2028 to 2030. So home prices may chop at today’s levels for another several years until everything is back in balance.

The question becomes then – buy now at an obviously overpriced level, or rent for 4-6 years at $30k a year and wait? There’s no free lunch (or free roof over your head).

Powells speech…..

cut cut cut

Labor markets are softening……..where?

What a crook.

Labor markets are definitely softening, “Sahm rule” has been triggered. More info on this search for the youtube channel “EuroDollar University”. His recent videos are highly educational about how the Fed is behind the curve on employment data and he predicts (correctly or not) that unemployment data is about to get seriously worse.

Another significant video regarding this is how when you put consumer sentiment on a 12 month lead, we get an R-squared of 0.7. Consumer sentiment under this light also predicting serious unemployment en route.

Sahm rule has become as irrelevant as the “inverted yield curve” rule. These two are retrospectives — in how things used to work.

The inverted yield curve rule was killed by QE. It already failed in 2019. And it has failed for the past two years.

The Sahm rule got killed by the huge influx of illegal immigrants into the labor force in 2022 and 2023 — meaning a higher unemployment rate as many of the 6+ million illegal immigrants look for jobs, thereby driving up the unemployment rate, while employment is still rising. That’s a new scenario that we haven’t had before, and the Sahm rule is based on what we had before.

Claudia Sahm herself pointed out that this influx of immigrants is “making the current reading of the Sahm rule look overly ominous.”

A recession means that the unemployment rate rises due to layoffs and falling employment, along with a decline in GDP (not slower growth). We’ve had neither one of them.

thanks for the reasoned reply.

Im not sure I agree about the 2019 failed signal on inverted yield curve but I’m open to reconsidering my viewpoint. I don’t have time right now to give a full explanation, but I will try to circle back sometime soon in another article.

as far as sahm rule goes, I had heard she said she wasn’t confident about her signal anymore and appreciate your explanation. I will try to dig further and see what I can find.

I am picking nits, I will fully admit. That said…..

Most of the immigration overload in 2022 and 2023 was NOT illegal. It was people claiming refugee status. It might not have been people coming to America from the normal, acceptable channels (i.e work visas), but it wasn’t illegal.

Labor markets aren’t strong. Most of the jobs we’ve been creating have been part-time ones. And the monotonic rise in continuing unemployment claims is telling.

If you’re referring to JOLTS data – that data is a joke. It’s based on a survey with a pitiful response rate.

I’m currently contracting for a tech company that deliberately posts fake jobs for the purpose of feeling-out “wage discovery” – i.e. determining whether they can cut the wages of their existing employees. This is becoming standard operating procedure in the industry.

Manufacturing has been in a recession for more or less two years and we’ve been shedding jobs in tech more more than 18 months.

Outside of construction – the worker shortage is a great big lie as far as I can tell.

New weekly unemployment claims have risen from around 215K to around 230K. This is still way below recessionary levels. The percentage of of workers who are part time is around what it was precovid. The labor market has definitely loosened but it certainly isn’t signaling we’re in a recession like some folks are claiming.

@Max Power,

Manufacturers have been afraid to cut positions until very recently because it was so hard to fill them after the lockdowns ended.

But that’s changing. You can see the employment portions of the PMIs lying down now.

Business services has been hemorrhaging jobs – mostly due to offshoring (Thanks, WFH!). Some of this is due to the recent decision of the AICPA allowing offshore auditors to earn US certifications. We’ve seen about 700 Big Four auditor jobs vanish in Boston in just the last 6 months alone from that.

Boston’s Tech Boom peaked in the summer of 2022. Outside of lab-based biotech and DraftKings – the rest is rolling over. And this looks secular – not cyclical.

BigAl – appreciate the observation on the fake-job posting phenomenon…

May we all find a better day.

4 of my friends in Bay Area working in Hi Tech were laid off last May-2-23.

They are still looking for jobs.

Jobs at the lower spectrum of wages e.g. construction workers,, waiters,, health care aide etc are plenty but high paying jobs were rare.

My friend were getting total $300K, you can’t expect them to take a job paying $20 right away.. it is sad situation.

Maybe they were overpaid at $300k? They had a good run. So now, maybe they should be happy with $150k? or $200K? If they’re holding out for $300k, well, good luck. Which is probably why they haven’t found a job yet.

Just part of the sloughing off of excess in the ongoing price discovery for working talent. Incidentally, they were getting paid more than a lot of neurosurgeons in the country.

There’s always Only Fans

My parents taught me there’s no shame in working at the local gas station if you’re in between higher-paying jobs. Income is income.

Yeah they prob were being overpaid and thought that they were rocket scientist necessary. Well guess what? Their education level and training prob didn’t correlate with those large salaries.

A seasoned doctor or lawyer make that much at the apex of their careers. Not people with software degrees from university of Phoenix online.

Man, I wish the shortage in engineers wasn’t real. But then again I wouldn’t have gotten a 40% pay bump for recently switching jobs if it was a hoax…

Glad you excepted construction BA, as the local general contractor managers I have spoken with over the last year or so have complained endlessly regarding how slow the sub contractors are because of shortage of workers…

Certainly appears that way as new, replacement type, houses are taking a long long time, with frequent lapses of several weeks between subs.

Perhaps you should actually listen to Powell’s words rather than get some distorted summary from a source that takes advantage of your ignorance. You will do better.

FedReserve clearly indicating rate cuts are incoming at Jackson Hole. Keep in mind FFR are ultra short term rates, and this does not guarantee mortgage rates will fall, or fall in proportion to the the ultra short term rates. This is particularly true because current yield curves are inverted (short term rates are higher than long term rates), so this leaves room for short term rates to fall substantially without an in kind reaction from long term (and mortgage rates).

However, a significant change in economic outlook, could bring down treasury rates lower than anticipated at this time. The question would remain however, would the spread that lenders require over 10 year treasuries, grow during a recession? I would anticipate yes, but its hard to know how much? So might the spread widening, severely impede mortgage rates falling as far as 10 year treasuries in the next 12 months?

There is zero acknowledgement from the FED that the level of federal debt and spending and QE and ZIRP had anything to do with inflation.

Of course not. Central Bankers are never honest about the origins of inflation (money printing via unfunded deficits). They are also dishonest about short term interest rates impacting long term sources of inflation. The Feds primary unspoken missions: 1) is to keep treasury markets liquid and stable (bond prices tanking too quickly is bad) 2) keep member banks solvent (a few can go under, but never allow systemic failures). Everything else is Fedspeak. Dual mandate on employment/inflation is cover for their actual 2 most pressing missions described above.

They raise rates, and enact QT, which reverse QE and ZIRP – to combat inflation.

But won’t admit that QE and ZIRP were the cause of the inflation. Point at supply chain shocks – as if services had a supply chain shock lol – as the culprit.

Looking ahead -based on past episodes- there should be a rug pull not too long after the cuts start coming.

All this while home sales just increased 10% due to just 50 basis points decrease in mortgage rates.

Something gotta give.

The 10% increase was sales of NEW houses by homebuilders, adding massive supply to the market, and it will help push down prices of existing houses.

This is is what we’re talking about — in terms of adding massive supply to the market:

https://wolfstreet.com/2024/08/23/inventory-of-new-completed-houses-surges-to-highest-since-2009-triple-from-2-years-ago-exactly-whats-needed-to-bring-down-prices-across-the-housing-market/

By comparison, the median price (three-month-average) of new houses, red in the chart below, is roughly $10,000 lower than the median price of existing single-family houses. For seasonal reasons, the median price of existing houses will drop for the rest of the year (blue):

That crook, Jay Pow, just pivoted according to the media. This country is a cesspool. I do not agree with anyone that rates should be cut at this point. I don’t care about the fake economy of this country.

Consumer behavior proved to be utterly-insensitive to rate hikes.

The sickness no longer responds to the medicine. It’s immune.

yes, feels like.

I think that the JP knows more than you and me. Let’s relax a bit.

It’s ironic that the topic of the Jackson Hole symposium is

“Reassessing the Effectiveness and Transmission of Monetary Policy.”

I have heard a rumour that Kamala will appoint Wolf as the new Fed guy. That would be good if true :)

Or I just said that and heard myself back.

If she wins. Otherwise it’s RFK.

I hope you are right and that it’s just more media and wall street hype. There is no hope for that wall street shill, Goolsbee, though.

one thing is for sure. neither major u.s. presidential candidate cares about the lower to middle classes. harris is espousing idiotic solutions to make housing more affordable which really just transfers more wealth to existing homeowners. trump measures economic performance by the stock market, which is a casino for the rich.

no wonder people are so unhappy.

I agree, rates should actually go up. PRICES need to come down further.

If the growth rates are true, then there is no need to cut rates. Someone is lying.

Not sure that would help. I was definitely on “Team Rate Hike” until last year. Now I’m not so sure.

The higher rates are discouraging investment in the “real economy” and companies seem to just be interested in purchasing distressed assets.

The growth rates are propped up by debt-fueled consumer spending. They are fake.

In other words your mind is made up regardless of the data. Burying your head in the sand is not a great way to make investment decisions.

We are trying to buy a home in a midwest metro and have been on the market for six months. We have been seeing more inventory and moderate price cuts the past few weeks. Viewing 4 houses tomorrow.

I am hoping we can seal the deal on something before the fed rocks the boat too much!

Unless you really really need to buy right now, I wouldn’t touch it.

But good luck!

So, in other words, there’s going to be a big wave of layoffs and people are going to go bottom up on their mortgages leading up to deflated housing prices?

Geez, guess the Fed better cut then, eh? Get ahead of things?

Or prices are just going to go down because you say they should go down?

Good luck Matt!

Nobody has a crystal ball.

However, homes are historically unaffordable. Prices were peaking in ’22 due to near free mortgage money. Speculation was rampant. Sales volume has completely collapsed in an epic fashion. Inventory is rising pretty fast. Big jobs revisions to the downside. Unemployment is still low but has begun to noticeably increase. If you have waited this long, now is NOT the time to capitulate as a homebuyer. Unless you think prices are going UP UP UP from here – which sounds like Realtor speak to me.

Midwest Ralph,

Do you understand that it is YOU buyers who are driving up the prices? It’s not the sellers. it’s you people trying to buy. Don’t complain about high prices while contributing to driving up prices.

Prices come down when you people stop looking for homes to buy.

If you buy now, you’re just making the sellers a bunch of money.

“No single raindrop believes it is to blame for the flood”

Nice try Wolf but you’re wasting your time trying to get this group of folks to understand they are the problem….

This group just look at people who don’t believe in buying a well-over-inflated asset and are on a long buyer strike as doomers. This is also why I think this bubble will drag out for much longer to my dismay. We need other external forces to continue or increase pressure to keep this group of people from buying, only then we will have true price discovery. I also believe most of the buyer strikes we are seeing now are due to affordability rather than intentionally abstaining from buying. In other words, I truly question how many people with say $500k to $1M that can be used as a downpayment are truly staying on the sideline because they are protesting the fundamental value. Sure there are some like myself, but if I have to take a guess, probably the minority is in this camp and probably even less so in SoCal unfortunately.

Yes — sober, numerate and shrewd = permabear, doomer, crybaby, etc.

They are not the problem. Your expectations are the problem. They are seeing a price they find reasonable and are buying. Why do you assume you know better about their finances than them?

JimL — you’re a contrarian stirrer. Take that turd outta your pocket. It’s olde.

I dunno,

I’m sorta with Ralph, if you’ve been renting 8-10 years waiting for a drop and your job looks stable, I think I’d buy now too.

How long can one person wait? Their entire life?