Inventory of completed houses jumps to highest since 2009. This pile-up of spec houses is exactly what the housing market needs.

By Wolf Richter for WOLF STREET.

Prices of new single-family houses at all stages of construction have been meandering lower since the peak in late 2022, as builders try to make deals by offering houses at lower price points – smaller, less fancy houses, and less fancy appliances and finishes – and they’re throwing in big incentives, including mortgage-rate buydowns, which are costly for builders (Lennar disclosed that they cost $47,100 per house on average).

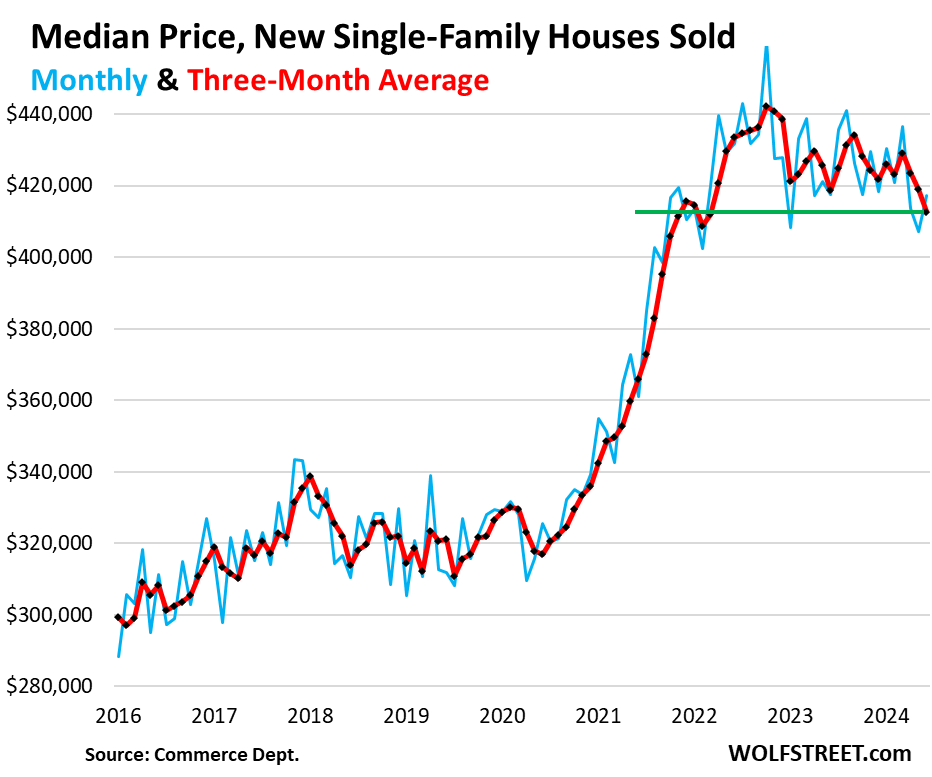

The median price of new houses (based on contract prices) is subject to heavy revisions every month, including a double-decker-whopper-revision two months ago, when the Census Bureau revised away 25% of the pandemic-era price spike in one fell swoop. So we focus on the three-month moving average of the median price, which includes all prior revisions, and irons out some of the monthly squiggles.

This three-month average of the median price of sales contracts declined to $412,667 in June, according to the Census Bureau data today, down a hair from a year ago, and down by 6.7% from the (slashed) peak in October 2022, and the lowest since March 2022. The contract price does not include the costs of the mortgage-rate buydowns.

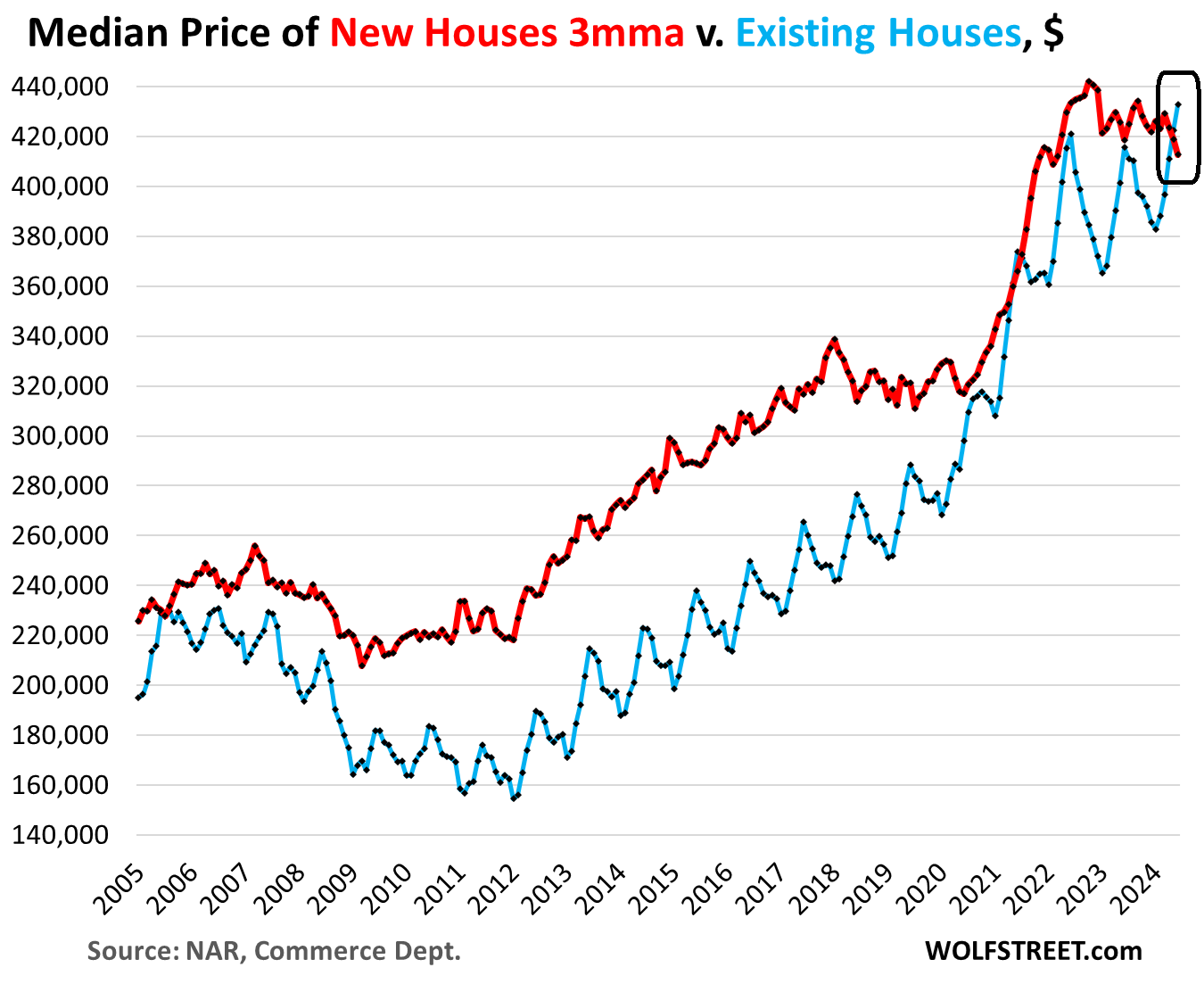

Prices of new houses fall below prices of existing houses.

At the same time, the median price of existing single-family houses rose to $432,700 in June, piercing its June 2022 high (blue in the chart below). It is now roughly $20,000 higher than the median price of new houses.

For seasonal reasons, the median price of existing houses will drop sharply for the rest of the year into early 2025, and June was the seasonal peak for the year. What we’re going to look for in the second half of this year: Will new house prices stay ahead on the way down, or fall behind, with the price of existing houses dropping once again below it?

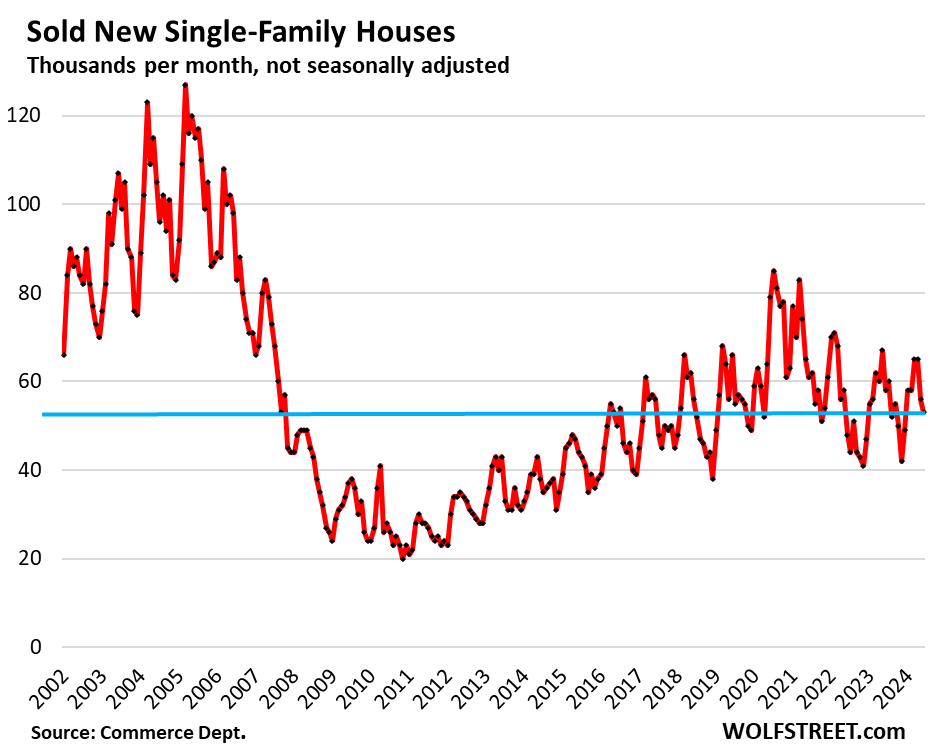

Builders have to deal with this market, and mortgage rates, and they cannot outwait this market, they have to build homes and make deals, and they’re doing it, and so sales have hobbled along below, but not far below, pre-pandemic levels, unlike sales of existing homes, which have plunged to historic lows.

Builders sold 53,000 houses in all stages of construction in June, not seasonally adjusted, down 8.6% year-over-year, and down by 3.6% from June 2019.

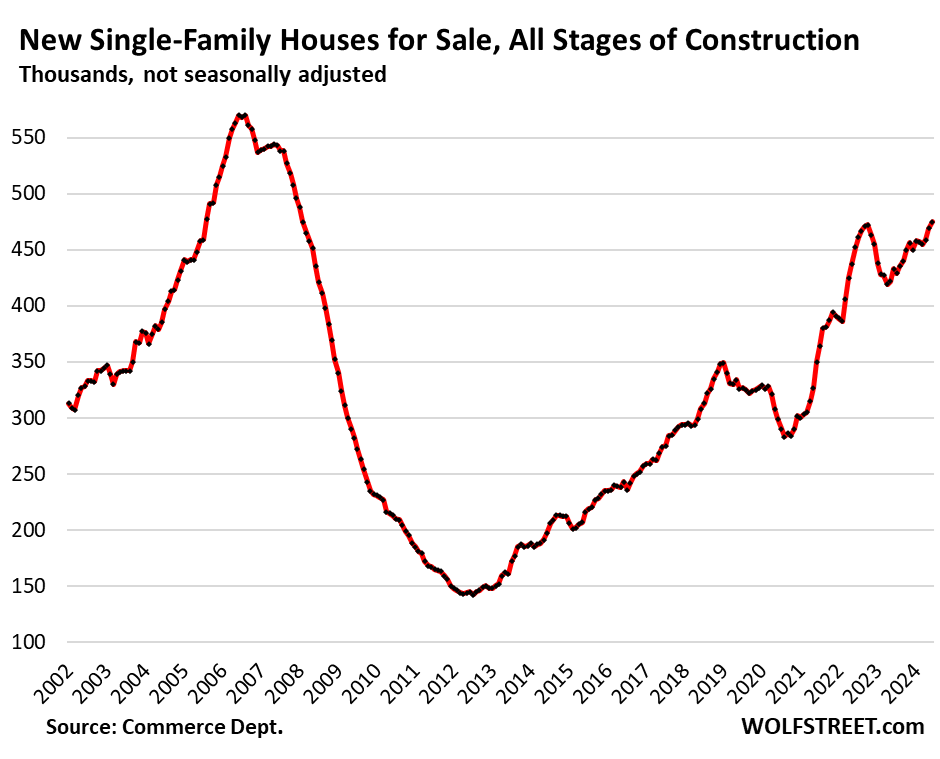

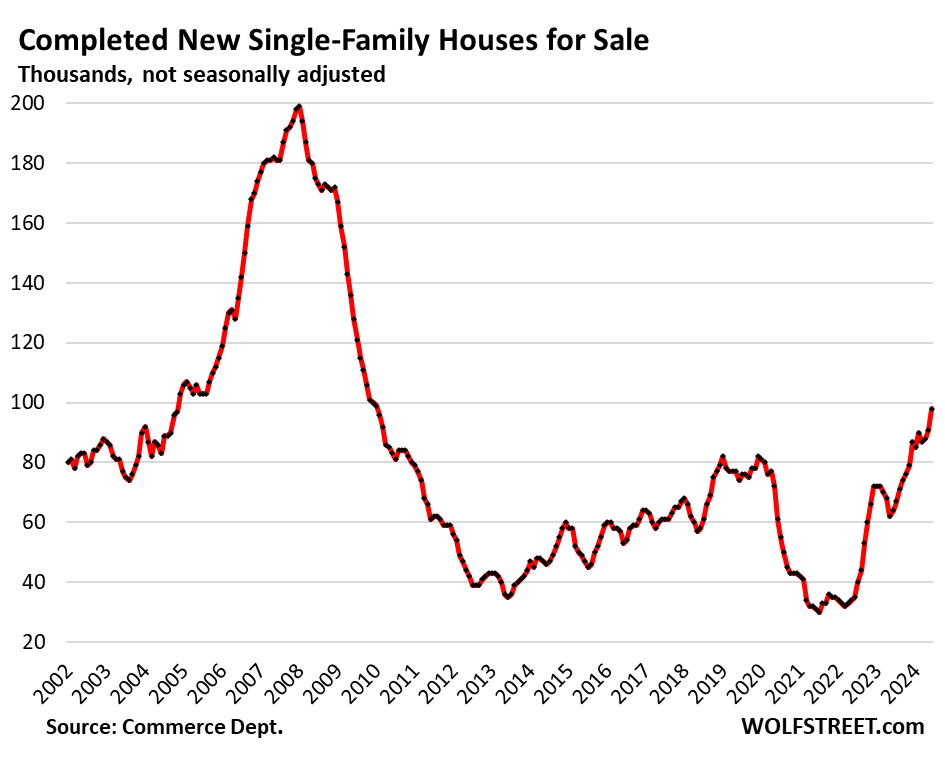

Inventory piles up. Exactly what the housing market needs.

Homebuilders’ inventories of houses in all stages of construction, including construction not yet started, rose to 475,000 houses in June, the highest since 2008. Supply jumped to 9 months.

So builders are aggressively adding supply to the market, no matter what the market does, and that’s good for the market, there’s nothing like lots of new supply to bring home prices back to reality, the more supply, the better. This supply of new houses ripples across the market for existing houses, as builders are competing with homeowners who want to sell.

Inventory of completed houses jumped to 98,000 houses in June, the highest since 2009. These speculative homes are essentially move-in ready, they have to be sold quickly, builders have tied up lots of money in them, and that inventory is encouraging builders to throw more incentives and mortgage rate buydowns into the fray.

This surge in spec houses, after the trough during the pandemic, is exactly what the housing market needs. People who are frustrated with trying to buy an existing house, can go out and make a deal for a move-in ready new house, at a lower-than-market mortgage rate, and come out with lower payments — and to heck with homeowners that sit on their vacant homes, hoping to run up the price spike all the way, or cling to 2022 prices. Homebuilders have to build and make deals no matter what the market is.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Howdy 3 % ers. You read it here first. YOU are a prisoner in your old home and could purchase a new home cheaper. They ZIRPed US to stupidity folks.

I’m a 2% er, does that mean I’m in super-max home prison?

If you don’t need, or want, to sell your house, it’s more like you are in one of those cushy white collar federal prisons where they sit around all day playing soccer and badminton and stuff like that.

Howdy Chs. Some people like prison too.

Howdy Nunya. Depends on YOU. Lots of ways to uncuff. Become a Squirrel, HELOC your way out of prison……More ways also…..

Not to get too sidetracked, but I’ve never really understood your comments where a 1st position mortgage is a prison and a HELOC is easy prison escape.

Howdy Chs. The Lone Wolf typed how MA and PA own the most second homes. HELOC the equity and invest in a second home is just one way. Business opportunities can be funded also. Takes guts and risk…..Just an old fools perspective…..

You can make the same arguments about not paying off your 1st mortgage, especially if you have a sub 3% prison sentence.

But I digress…. apologies

Debt-Free-Bubba, are you really Wolf?

Lucca,

That would be hilarious.

Only if you bought in the last 3 years. Then you are what they call a lifer.

Howdy Andy. The younger generation is getting a sense of Humor????? HEE HEE. Hope so…….

My well to do sister bought 10 years ago on 5 acres with barns, horses, the works. Her property backs to a large public park wooded area overlooking a reservoir. She refinanced at 2.8% and I don’t see her complaining other than her property taxes keep going up. But who doesn’t complain about that?

Howdy Gabriel Its Govern ment creating bubbles and picking winners and losers that has my ire…. So many were ZIRPed and do not even know it…. As long as you don t move and stay in one place is fine for most folks. Many live and die in the same state.

Bubba,

I always thought moving often (and selling and buying houses because of it) made very little financial sense. It costs a lot to sell, and a lot to move.

I just figure all the money I save (and invest) by staying put keeps me in my comfy home and leaves plenty for travel if that’s the point of all the moving.

I think this is just another way that younger people don’t save as much as their elders had, and they often don’t seem to realize how much money is being bled away each time they move (+ the new era of subscription-everything, etc.)

Many of those 3%ers are also retired, on fixed income, and watching their taxes rise with every years appraisal. They bought to live in those homes, not as an investment, and will, at some point, have to decide to move, not because they want to, but because the purchasing power of their pensions and investments has been degraded while the cost of living has gone up.

I don’t pay a mortgage (0%), so I must really be effed. Oh well, so long as I am my own warden!

New build house prices coming down will mean that the quality is also likely to come down too. Not that it was great to begin with.

Personally, I would never buy a new house. Not newer than the 1920s if I can help it.

Things keep getting “engineered” to new minimums and I can imagine all the nightmare stories of unskilled workers and never-finished houses are true and not exaggerated at all.

Having dealt with houses built in the 1940s and 50s, I am not convinced that quality was much better then than it is now. Lazy, unskilled workers are not a new phenomenon.

Instead, “survivor bias” accounts for a lot of our perception that quality was better then, workers more diligent, etc. The better houses are the only ones that are still around. The others have been torn down and replaced, or in some cases, abandoned.

Your second paragraph may be correct.

Note regarding your first paragraph: I said I would prefer not to buy post 1920s. ‘30s was when people were poorer or it was at least fashionable to pretend so. Around that time was when exterior walls were no longer masonry.

Around the war came modern manufacturing. Bad food and bad everything else.

I stand by my bias.

Yeah, I’ll counter this statement. Context: I live in a neighborhood where the majority of the housing stock was built from 1919-1945.

My house was built in the last 1920s and anytime I open up a wall to do some renovation work or maintenance I am horrified by the shortcuts and subpar work that I find: studs that are notched to within inches of being toothpicks, joists that have been drilled through with enough holes for pipes to be non-spec to code today, knob and tube that was run in places that then had metal lathe rubbing right up against it, or fasteners piercing the covering.

The materials may have been better, and in some cases the workmanship to a higher standard, but in the case of most mass-built homes in the ’20s…yeah, it ain’t much better. ;-)

Wolf is on fire with housing market reports..3 in a row. Loving it

Woke up setting Tesla down 10%… sure made my day a hell a better. Let’s see if their internal plunge protection team or BTFD cultist will bid it back to the moon by next week. For now though I’ll do a small victory lap and enjoy the moment

The Magnificent 7 are down another $1 Trillion today. But it’s the Monopoly money, so doesn”t matter.

so ridiculous. i’m counting on my mag7 stonks to finance my early retirement at 56 next year. after a few down days, that should be powell’s cue to reduce interest rates to 0 and print a few trillion by resuming qe. that’s really what his job is.

Nope. There will be no interest rate cuts at all ahead. What difference do you think they would even make anyway? Why?

The volume of short-term claims against the dollar implies that a decrease in interest rates will cause a flight from the dollar (higher inflation).

“What difference do you think they would even make anyway?”

That’s a very good point which macro analysts have been pointing out. Our debt laden economy is now like a diabetic with serious insulin resistance. You can give ever higher doses of insulin, but in the end it only results in worsening the insulin resistance.

It’s time for all that reckless congressional spending to go on a low carb diet. Or at least stop making things worse with yet another tax cut for those who need it the least. They’re fat enough already.

The fed FOLLOWS the market. They never LEAD on rates. Take a look at a chart of market rates with FED funds overlaid. Right now, markets are saying we’re staying put, which means the fed is staying put too.

After a few ups and downs and ups, we’re back at mid 2023 levels where fed funds peaked and stopped. When market rates move down substantially off 4.5% for an extended period, they’ll cut. They definitely won’t raise from here.

US debt went over the 1 trillion mark in 1981. Now a trillion lost in 1 day doesnt make people blink. The recent short squeeze was just another sign that scumbags run this market, mostly profitless tech jumped 20-40% in less than a week and a half.

Builder going at it on the lot down the street from me – 6 new townhomes. Paid a pretty penny for the land (probably @ 1m/acre) so selling price will need to be high to make a profit.

Microsoft should do well in 2026.

While I keep hearing the US needs between 2 and 5M more new homes, it seems like the average consumer can’t afford the prices. So, prices have to come down a bit. Unlike the GFC, each submarket will be different. My guess is the submarkets that have seen 100% price growth since 2020 will see larger decreases than a market that is only up 25% since 2020.

What economic growth since 2008 justifies housing or any asset at its current level?

2008 $10,025 68% Bank bailout and QE

2023 $34,001 122% Fed raises rates

I find it hard to understand that so few here understand debt. You’re just borrowing from the future. We front loaded all the growth so people in power wouldn’t lose power. When this all blows up, every cheerleader here will be so mad that nobody could this coming. And they knew all along that it was unsustainable. Cause ahhhh duh when the dah music is playing ya gotta keep dancing duhhhhhh.

Good summary Wolf, with one exception:

” Homebuilders have to build and make deals no matter what the market is.” is NOT true.

Builders can and do and certainly have just stop building.

Been there, done that as an employee as well as a builder.

I have seen many condo buildings stopped at lower levels than planned, etc., as well as subdivisions with many/most lots sitting empty, sometimes for decades.

“subdivisions with many/most lots sitting empty”

One of the reasons that existing homes can be more appealing. At least you know you won’t be living in some weird, partially built subdivision.

A small builder can. A big builder cannot. Big builders have huge businesses that they need to sustain. DR Horton, Lennar, etc. cannot stop building. They’re publicly traded, they have publicly traded debt, they have thousands of employees, payroll out the wazoo, interest expenses out the wazoo, and all sorts of fixed expenses. They MUST keep the revenues rolling in, or file for bankruptcy (some of the big ones got close to bankruptcy during the Financial Crisis). Home building is now dominated by the big companies.

Individual projects can stall temporarily for a variety of reasons, from permitting and funding to plan-changes. Big projects can get in trouble, see the Oceanwide projects in San Francisco (I have a series on it) and in Los Angeles. When that happens, the builder goes bankrupt, the contractors may go bankrupt, everyone is suing everyone, etc. Much of the money put into the project goes up in smoke. So no, a big builder cannot voluntarily stop building and expect to thrive. It’s over when they do.

If the big builders go bankrupt it would be a great thing, the small builders all buying lots in a subdivision like it used to be. The thousands of employees are probably just poor former entrepreneurs enslaved by Wall Street.

I like this idea a lot, but I can’t imagine a small company could build and sell as cheaply as the big companies, which seems like it would be a problem.

But all businesses getting concentrated under fewer bigger companies is sad/bad in so many ways…

Wolf, an excellent description of the national builders. The small builders never recovered from the 2008 crash.

The small guys, regardless how green the grass is in that new subd.,

make sure remodeling projects keep a roof over their heads.

It’s the risk inherent in developing land. Many builders float money so land devs know there is a risk of getting stuck holding the bag on a subdivision. Lennar develops a lot of their subs from the bottom up, but even they make prodigious use of groups like Hearthstone Investments to have the capital to do so.

I do wonder what narrative starts taking hold when the inevitable rate cuts start hitting soon and how it will affect home sales in the short term. We have an interesting situation of low sales, high median price, high stock market valuations and increasingly uncertain economic outlook. Stock market seems to be sending some different signals over the past couple of weeks.

The rotation in small caps is interesting. Market commentators declare this as “healthy market action” or “a true bull market now.” I’d have to go back and check actual data, but my recollection from the Dot Com Bubble was that small caps going crazy was part of the “last stage” of the bubble. I don’t count a few days of outsized small cap gains as “going crazy,” so it could have plenty further to go, but still, retail investors piling into the small caps feels alot like the “late stage” action of the late 1990s.

“inevitable rate cuts”

What makes you so sure?

When the first small rate cuts come, buyers on the sidelines with enough cash and credit will pile on again and prices will likely rise. When/if mortgage rates drop substantially further (1.5% or more) frozen inventory will start to come back on the market and price increases will slow or prices will fall.

High prices and interest rates have stopped buyers already. the anomaly no one expected, including the fed, was the seller strike due to low locked in mortgage rates and the differential between those and current rates. When that differential narrows enough, inventory will jump and prices will fall – fall, not crash… sorry.

“When the first small rate cuts come, buyers on the sidelines with enough cash and credit will pile on again…”

No they won’t, they’ll be waiting for more rate cuts. That’s what they’re doing right now, everyone is waiting for mortgage rates to go back below 5%. That’s why home sales have collapsed. But builders offering 4.99% buydown mortgages are making deals.

1:04 PM 7/24/2024

Dow 39,853.87 -504.22 -1.25%

S&P 500 5,427.13 -128.61 -2.31%

Nasdaq 17,342.41 -654.94 -3.64%

VIX 18.04 3.32 22.55%

Gold 2,398.50 -8.80 -0.37%

Oil 77.46 0.50 0.65%

Hi SoCalBeachDude

Let me know when all 3 indices above are down by 50% or higher.

Otherwise, we are still in the “everything bubble”.

ps: If 3 indices are 50% lower, they just get back to pre-pandemic level, which is STILL too high.

MW: S&P 500, Nasdaq have worst days since 2022 as disappointing Big Tech earnings drive selloff

By population new homes cost about fifty percent more than resale homes in the provinces of Ontario and British Columbia in Canada. The same is true of new townhouses but new apartments are about 20 to 25 percent more. In the other provinces about thirty to forty percent more. The lot the home sits on makes up about 75 percent of the overall sales price.

Seems like sales of ultra luxury homes > $10 Million is skewing the median prices. Is there a way to adjust for that?

You adjust for that by using the median instead of the mean. If there are truly enough >$10M sales to skew things, your metric *should* rise.

@Alex Pavchinski sales of $10mm + homes will have an impact on the “average” prices but not much of an impace on the “median” proces in any area with a decent volume of homes.

That’s totally wrong. It’s a high NUMBER of high-end sales that shift the median price up, especially if it comes with a low NUMBER of lower-end to mid-range sales. And that’s what is happening. The number of high-end sales has ballooned, while the number of low-end to mid-range sales has plunged.

@Wolf I agree with you that there is a big increase in the sale of high end homes that will move the median, but Alex was asking about $10mm + homes (there has never been a BIG increase in $10mm+ homes). I just looked and only 28 of the 1,611 homes listed for sale in SF are over $10mm (and one of the 28 was an island in the bay). In Truckee 10 out of 525 homes currently for sale are over$10mm. In any city with over 20,000 people I suspect that the sale of $10mm+ homes will not have a big percntage increase in “median” home price (just like the numbe of Billionaires in SF and Truckee don’t have much impact on the “median” net worth of the towns).

I’m curious if an informed person could explain what exactly incentivizes a mortgage rate buydown as opposed to a plain old price cut?

And why aren’t rate buydowns considered cheating for capital gains purposes – if the price of a house would be $400k at market interest rates but a buydown causes someone to buy it at $425k instead, isn’t that an illegitimate boost to the cost basis of the asset?

@Kyle K most people don’t buy on price they buy on payment. As an undergrad with a roomate that sold new cars in the early 80’s he made a fortune since he learned that most people were trading in cars with three year loans and were happy to buy a nicer new car with a five year loan since “the payment was lower”. P.S. The higher pruchase price also means higher property tax in most states (in CA that extra $25K would cost more than $2,700 in extra property taxes over the next ten years).

At an avg of $47,000 per home, depending on the sales price, that could be a significant percentage price reduction. The result is that it keeps new home prices artificially high. If nationally, new home prices are down by nearly 20% from the peak, if you factor in these rate buy downs it could be closer to 30%?

So long as the interest rate is above the IRS Applicable Federal Rate, there is no tax problem.

It’s better for the builder to keep price high as future sales will be based off that to a large degree. Another tactic is to offer rebates or free add ons. Anything but discounting the top line number.

We need another GI like bill to socialize housing. The private sector is never going to catch up.

May I dare to begin shorting XHB? It is up about 127% since the highs pre Covid.

I just have some doubts regarding the efficient markets, lol.

So supply is increasing to take advantage of high prices? The free market is actually working. How quaint.

Only a 6.7% drop in new US house prices since October-2022. We need to see at least a 27% drop just to get back to 2016 levels. We need to see at least a drop to $250,000 to see millions more Americans be able to afford it again. Interest rates much higher is the only real path to achieve this. We need 10% mortgage rates right away.

I retired as a lead real estate agent for 20 years and my other 14 years was in the local financing manager at a community bank and credit union and saw how the ridiculous low interest rates and lower credit quality borrowers getting cheap, easy money has done a real disaster to the American dream of owning a home.

What are people’s preferred method of judging the “affordability” of housing? When we look at the increase in average home prices nationwide what statistic do you compare that(combined with the average mortgage rate) with?

Generally, affordability is a measure of house prices, mortgage rates, property taxes, and insurance, v. household income.

House prices generally reflected employment rates and like you said income levels plus the type and quality of jobs available. Remember, location, location, location. Now it is mostly mortgage rates, interest rates manipulation and too much government intervention.

In SoCal and in large North East metros, the new homes are cheaper because they are located in distant locations that are not commutable to the jobs. So, they are not a factor.

But, in smaller cities, the new homes are close enough to the job centers, so the existing homes in those markets will take a hit.

Ever see the new commercial with a few women in their 20’s or 30’s going in together to buy a house?

That’s ‘cause modern day dudes are repulsive, with their man-buns and what-not.

Hahahaha

So, if the average price of a new home is currently $417,667 but builders are giving incentives of $47,100 according to Lennar, would it be safe to say that the “real” price of new homes is down to $370,567~ish?