And they’re big. That assumes their hedges don’t blow up, but that’s precisely what hit D.R. Horton.

By Wolf Richter for WOLF STREET.

When mortgage rates rose to 6% and then 7%, sales of existing homes plunged by close to 40% from 2021 and by over 30% from 2019 because sellers refused to cut their prices enough to make 7% mortgages work, and buyers lost interest. Commercial real estate has been repricing properties, and the haircuts are massive. But home sellers are not in the mood. They’re going to wait this out or whatever. So sales have plunged even as active listings and supply have risen to the highest in years.

Homebuilders, however, have to build and sell houses regardless of how high mortgage rates are, that’s their business, they cannot wait out anything. So they have gone on an aggressive program of buying down mortgage rates, even for the entire term of the mortgage (“permanent”), and of throwing in other incentives, such as free upgrades and closing-cost pickups. And sales have held up.

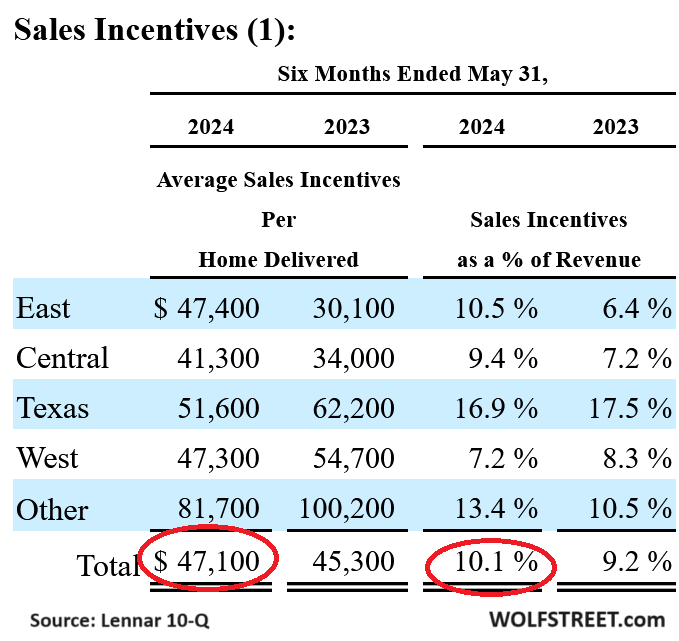

But it’s expensive: $47,100 per house on average: Lennar

Lennar, one of the largest homebuilders in the US, filed its 10-Q for its second quarter with the SEC last Friday. And it disclosed what these incentives cost:

In the first half of 2024, the average incentive costs, including the costs of mortgage-rate buydowns, rose to $47,100 per house sold, or to 10.1% of the average sales price, up from 9.2% a year ago.

The costs of those incentives vary by market. In Texas, they reached 16.9% or $51,600 per house. In “Other” regions, which include Florida, they amounted to 13.4%, or $81,700 per house (table from the 10-Q filing):

Lennar has also reduced prices:

“Revenues were higher [by 9%] primarily due to

-

- a 15% increase in the number of home deliveries,

- partially offset by a 5% decrease in the average sales price of homes delivered.”

The average sales price of homes delivered fell to $426,000 in Q2 from $449,000 a year earlier. The 5.1% drop, it said, “was primarily due to pricing to market through an increased use of incentives and product mix.”

And it said:

“With our ready access to capital, we have been able to adjust and capture demand by using incentives to reduce the affordability constraint.”

In its first-quarter 10-Q filing three months ago, it said:

“Homebuilders have been uniquely able to capture demand by using incentives, including interest rate buy-downs, closing cost pickups and price reductions, to unlock affordability restraints and enable purchasers to buy homes.”

On their financial statements, publicly traded homebuilders add the costs of mortgage-rate buydowns and incentives to their costs of goods sold, and therefore deduct it from their gross profit, so investors see the impact of the costs. And the GSEs (Fannie Mae et al.), when they acquire the mortgage from the builder’s mortgage company, obviously also understand the math of the buydown. So it’s not that there is anything hidden here.

But the costs suddenly spiked for D.R. Horton when its hedges blew up.

Homebuilders use complex hedges of various types in an attempt to control the risks of mortgage-rate buydowns. But last fall, during the Rate-Cut Mania, when mortgage rates plunged, D.R. Horton’s hedges blew up and needed to be restructured, triggering a $65 million charge to cost of goods sold and thereby to gross margin, which came on top of the costs of mortgage-rate buydowns and other incentives, it disclosed in January.

So the jury is still out on future incidents like this where mortgage-rate buydowns exercise their unexpected costs on income.

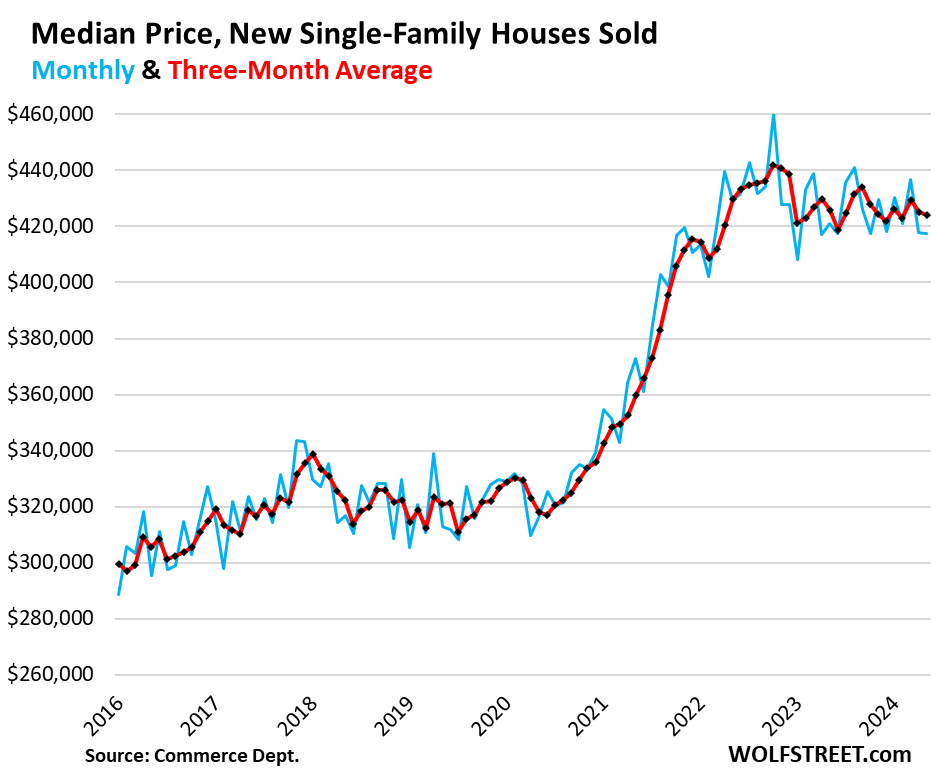

But these costs are not reflected in contract prices.

The Census Bureau, when it reports on new residential sales, relies on contract prices — the amount in the purchase agreement with the buyer — to come up with its median prices, and those contract prices don’t reflect the costs of mortgage-rate buydowns and incentives.

Those contract prices were down 4% in the period of Lennar’s Q2, from the peak in the fall of 2022 and are back where they’d been in Q2 2022.

This is the latest revised data through May. Did you miss Revision Chaos a month ago? Census Bureau Revises Away 25% of Pandemic-Era Price Spike of New Single-Family Houses

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s not like the majority of potential home sellers can do this forever. Death, divorce, job transfer, upsize for a growing family, down scale for empty nesters, job loss, no need of a vacation house anymore, etc.

Eventually, the “wait” of feeding the monthly houding alligator becomes a rush to sell when prices keep declining or become stagnant.

“But home sellers are not in the mood. They’re going to wait this out or whatever. So sales have plunged even as active listings and supply have risen to the highest in years.”

Overall I’d agree. However, I wonder what percentage of the “potential home sellers” have covid-era low interest rate mortgage loans. Those loan terms are a powerful incentive to stay put, even if the property is no longer ideally suited to their needs.

Some of that group have probably resigned themselves to the fact that a new mortgage loan will have less favorable terms. But with the (supposed) upcoming Fed interest rate cuts, some will wait a while longer before placing their current property on the market. How long? That varies from person to person.

The elephant in the room for the residential RE market is an honest-to-goodness recession. Once again several investing and economic forecasters are stating that is a real possibility. But those are just predictions. Which are usually wrong.

As a friend of mine says, “the economic forecasters are often wrong but never in doubt.”

Essentially the fed put of always coming to the rescue with lower rates and QE is costing millions of potential homebuyers hundreds of thousands of dollars (for the ones that can’t wait and go ahead and buy now), or time wasted that could’ve gone into moving a family into a home (bc they refuse to pay these nonsensical, outrageous prices on top of the high rates).

I wish more people realized how seriously awful this past decade+ has been for so many people, particularly younger folks and renters; anyone on the wrong side of the wealth inequality divide.

Funny how these homebuilders are throwing so much money to desperate keep the mirage going that home price will only go up, at least on the surface.

“But home sellers are not in the mood. They’re going to wait this out or whatever”

Unfortunately, this has also embolden existing home sellers think this is the way things will be forever and in markets like SoCal where there’s less new build in general compare to other states, this will just make this mexican standoff go on longer and longer…and honestly with this FED, I probably wouldn’t be surprise they will be able to end up holding out long enough for rates to come down and market back to the moon again.

They cannot lower prices or else they will get sued by the former buyers. Simple as that.

Welcome to the US of A, the land of the free.

Anyone can sue anyone in the US. All it takes for someone to sue someone else is to file the paper work and pay a filing fee, and that’s about it. The success of a lawsuit is a different story. If the lawsuit is considered “frivolous,” it could backfire on the plaintiff and their lawyer. So there’s that.

So someone can sure sue a homebuilder for whatever reason — file the paperwork and pay the filing fee. Prevailing in a lawsuit like you describe is a different story, and may be considered frivolous, with blowback to the plaintiff and their lawyer.

Homebuilders cut prices when they need to, and they did during the housing bust massively, and they’re doing it now and have forever when they have trouble selling homes in a particular development, no problem.

All this is the furthest thing from legal advice ever.

Back when I was starting a business, we looked for a lawyer. One explained that if we were successful, we would be sued. I looked at him with a ‘say what?’ glance. He said, “I can sue you for stealing my boat, and I don’t even have to own a boat.” Caught my attention for sure.

So absolutely, anyone can sue anyone…

When you buy from DR Horton or Lennar, you sign away your rights to sue and instead must go to arbitration.

In my region, home prices deflated. After 2 years, home prices are still 6% estimated below June 2022 highs. With he fed most recent statement (inflation target of 2 percent hopefully q4 25 q1 26), we should not hold out. Cuts ain’t happening until 2026. It helps to note that my state is building properties at a good rate.

In my little slice of southern Socal, within the past month we have seen all-time highs on a couple of houses sold, and now others have been put on the market and are still sitting there weeks later. Might have been the top or maybe just a pause. I think it is mainly all cash deals where financing rate doesn’t matter.

Does anyone else think the term “Mexican standoff” has changed from what it meant everywhere I lived in CA since ’54? Don’t know when, how or in or by what groups it changed, but even wiki is wrong by my experience (and that is including a LOT of other people).

I won’t even give my understood meaning so as not to bias any answers…..should I get them…..

This is where bad-mouthing most everyone here (and posting several articles behind) works against me.

Will post my understanding and ask what THAT situation is called in a few days.

Actually was too young to use term in ’54……say 5-6-7th grade or so..HS for sure….from beginning of puberty (girls become “sorta more interesting” in gradual degrees ending with total obsession) and awareness of many other things in this world are added, too.

See post below for situation description.

A small builder near me in Texas is offering a low buy down mortgage rate to clear out the remaining new, unsold houses (about 5 in this phase). Houses are 1,200 to 2,300+ and are priced at about $175.00/sq. ft.

On his sign: “Buydown rates starting from 3.99% {6.4846% APR}. On select homes, with preferred lender only, must close by 8.12.24.”

Lennar is building a mile away and is offering about the same buy down.

I sold my last spec homes in Texas last year by buying down mortgages and/or giving buyers credit towards closing costs. It works great. I get my proprties sold and buyers get a lower house payment or have to come up with less cash to close.

That’s certainly the theme around here now.

So many factors involved and especially for this election cycle. I’ve listed my 2005 home after putting about 30k into it — to make it look nice. We shall see. I definitely want to get into $ powder, but for now, I’ve given no desperate indication to the market or my realtor;-)

It’s not just the home builders offering incentives. We just closed on a house we purchased from a mega landlord, in a community where they had built a large percentage for rentals. They offered a lower price point than the builder in the community and other sellers. They also offered an incentive, which we used for closing cost.

We are happy with our purchase, but prices are dropping as we speak. Our decision was based on locking in a long term rent because our landlord priced himself out of the market. Our new mortgage is slightly more than our rent was, and it is mostly capped, and we can always refinance to a lower rate.

No, you can’t always refinance to a lower rate.

I am so full of myself to make such a bold and simple and direct statement aren’t I, but I can prove it with another simple and direct statement.

Go and refinance to a lower rate right now, or next week, or later this month, or next season, or next year. I’d put real money on it that it ain’t happening regardless of the pleasure talk. I’ve had a few bankers tell me over the last two years that rates are coming down soon. I sat across the desk from them and told them that rates are going to stay high for some years and this economic cycle will not have reset until about 2030. One banker told me about his new certificate and that he was doing well, “Look at my new suit.” I laughed at him and walked out in my jeans. Fruit cake couldn’t even open a money market account like other banks, even though he was the one calling me to see what they “could do for me.” Waste of time. It’s amazing how much people believe others when they are told exactly what they want to hear. Rates aren’t coming down in the next few years, except, at best, a small head fake of one time lowering it and then saying oops, we shouldn’t have done that due to the data that follows so we will briefly hold and then raise the rate again. The Fed is smarter than you think, they are smarter than the average, and they know that people believe what they hear without complex analysis. These are the same people that told you that pretend like they didn’t know inflation would happen, then that inflation was transitory…………they knew, even though they told you something different in conjunction with their media co-conspirators.

Nobody knows when and by how much rates are going to change, down OR up, including cupcake, his/her bankers, or anyone else.

Yogi Berra – “It is difficult to make predictions, especially about the future”.

…if we accept that a ‘generation’ still spans prox. twenty years, we might consider ‘generational memory’ at work, i.e.- the inner belief created over one’s earlier years that an insanely-low (as viewed by my aged eyes) cost of money always was, and thus should always be, the ‘norm’ (much like my old memories that 4% bank savings accounts, $0.04 First Class postage stamps and $0.49/half-gallon milk would be signs of ‘normalcy’, although that insanely-cheap money has been demonstrated as, perhaps, the headiest memory of all…).

may we all find a better day.

You might have answered the question I posted above…2 days before I asked it.

Also….maybe I better lay off watching this Twilight Zone Marathon every night. Not too good for my senility prospects.

NBay – I often think I see the spectre of Mr. Serling just vanishing around the corner when I arrive anywhere, these days. The doc tells me it’s probably an effect of the PD, but I dunno…best.

may we all find a better day.

So the meaning of “Mexican standoff” has always been the same everywhere and I just have had a 50+/- year brain fart with nobody bothering to correct me?

Then WHAT is it called when you gesture “you go” / “no you go”, at, say an intersection, then both go, both stop, gesture again, go…….rinse and repeat until someone is REAL insistent and breaks the standoff? Happens in other crossing paths situations, too, like the nice “old” (tip-off to me) lady who is holding up traffic to let you cross street or main “street” in a parking lot? I usually just turn and walk away to end it. Or even just walking it can happen.

What is THAT kind of standoff called if not Mexican, which I always thought?

There is a medical term for catching things moving quickly when nothing did. But I think I have more silverfish, so it’s not always my aged brain.

Hope that PD is mild. If doc told you to to do PT that probably means it is.

Later.

NBay – my understanding of that cultural phenomenon is that it’s root lies in the uniquely French “…oh, no, after YOU, Alphonse…” running gag of decades past-a situation portrayed as two men attempting to pass through a doorway at once that comically decays from that of one accepting a minor common courtesy into one of: ‘who is more polite, and therefore genteely/socially superior’. (…I must admit, though, that I’m one to definitely pause and emphatically direct traffic to proceed before me, if necessary, at unlighted intersections when on a motorbike-have had too-many close calls and friends subject to ‘…but I didn’t see him, officer!…’ left-turn impacts from auto drivers…).

My understanding of ‘Mexican Standoff’ (and no disrespect intended or implied) has always been one of a situation that most likely would result in what might be known as the later Cold War term of ‘Mutually-Assured Destruction’…

(PT AND the carbo-levo are doing a good job of stalling the decline, so far, thanks. Hope the back is giving you less hell.). Best!

may we all find a better day.

NBay – (hoping Wolf continues to indulge us, here) thinking a bit more about ‘standoff’, I can certainly see a potential for a ‘Mexican Standoff-‘MAD’ incident at an intersection where two right-angle drivers wave each other on, both take off, and then collide. Mendo-speak being a differently-filtered term for the same thing, then! Best.

may we all find a better day.

Thanks!…..that French root explains how it could go either way….wish I could remember exactly where and the people I was with when I formed my belief of that meaning…could be parents?

Back is little bit worse standing/walking, but better sitting driving…..but for my age and life experiences I’m still damn lucky so no whining here. Life’s good……enough for me.

Later.

Cupcake,

I generally don’t care about the consensus on interest rates because I have been around a long time and know they will do what they have to to save the system. If things keep sliding downhill for bank profits, they will cut in 2025 -> 2026. I expect to see 5.5 during this period.

Here’s a new twist I had never heard before too, the mortgage broker we used offered us a “free” refi if we use them to refi later on. I believe it will be on their fees only. This is how you know things are really bad out there, they need the volume.

What you are saying seems to reinforce what I am saying but you seem to think it also reinforces what you are saying. If they promised you a free refinance rate and rates don’t drop, they never really even have to act on their promise so it’s not a real promise if the promising party knows that they will never be challenged to fulfill it. But it would make the justification for the pricing easier to swallow now if there is partly based on some theoretical future circumstances that don’t need to be fulfilled.

Typically, after bank and other refinancing fees, it doesn’t make sense to refinance a loan unless you can get a couple of points less. Even then, you may just break even. We may not ever see those 3% rates again!

Just keep in mind your city/town will likely re-asses you based on your purchase price, and your prop taxes will go up from the number you were shown when applying for your mortgage.

MM,

Actually, the opposite is true in our case. The mega landlord was not homesteaded so their taxes were high. We will be homesteaded and our purchase price was below the current tax assessment. Our taxes will be lower than theirs.

Our house was not attractive as a listing because the current taxes were higher than average from other listings. But we knew why. Most buyers overlook whether the listing is an investment property or owner occupied, it matters for affordability.

It’s a shame that builders don’t just cut the price by $47k instead of offering that as incentives. But I guess its important to maintain the illusion that houses ought to be worth $426k. There must be an awful lot of margin there to so casually offer 10% off on a house.

@Kent –

Which, as a buyer would make me nervous, thinking about what corners are being cut to maintain margins…

DR Horton anecdote: The house I stay in for work has to have it’s second floor re-leveled. It was bought in early 2023, with a buydown. That, plus the warranty repairs makes me doubt they made much money on it if any. There’s a bunch of people in South Carolina who have major issues with DR Horton homes too, if you want to do some googling.

A friend of mine bought a DR Horton home new about 10 years ago. Inspector noticed that the roof vents were installed in the shingles, but no holes were cut in the roof sheeting. Not a quality build. At least when you buy DR Horton you know every corner than can be cut, and gotten away with, is.

Around here, all the subcontractors do not speak English. I doubt any of them are citizens or have any formal training in their skill. My new house (bought mid 2023) had to have some walls refloated and repainted due to poor taping and floating. In addition, the makeup air duct for the additional outside are was never wired up (motorized damper). There were also many cosmetic issues and some interior plumbing issues with drains that needed to be corrected. The secondary drain pan for the A/C coil in the attic was stolen by someone, probably for another new house in the area.

I delayed the closing due to all this crap and the builder was not happy, but I was not going to buy this place and try to have them fix this stuff after they had my money.

It is absolutely wise to hire a house inspector to go over the dwelling to find the stuff the builders try to leave behind since they don’t actively monitor the subcontractors work. This advice goes for low end and high end homes.

Plenty of clips on YT about the horrendous build quality and corner-cutting on houses from the big builders like Lennar and Horton.

There is a solid husiness reason to offer rate buydowns rather than price cuts. Since a buyer can only benefit from the buydown if he stays in the home, he won’t flip the house (which would compete with the builder^s future sales).

Kent,

Two reasons why they don’t cut the price, real estate commissions and real estate taxes. The people that collect these don’t like it.

I don’t know what the mega landlord we purchased from paid because they paid cash and bought many houses from the builder. However, here is the tax assessment history of my new house: 2022 – $405K,

2023 – $375K, 2024 – $345K. We know 2025 will be lower.

2025 will be whatever you paid for it.

Try seeing it from the perspective of the entire house of cards from the top down. If they give people incentives but the technical price of the house stays the same, on paper it’s easier to make the neighborhood of houses still look like their true value is as it was in the recent past. The city does not want property taxes to go down, but if prices are cut outright, it’s hard for them to pretend and not take into account such price reductions when doing assessments for taxes. They already have declining taxes in commercial real estate so it’s not like they are eager to get punched in the face two or three times in a row. They’ve got pensions too. The Inflation Acceleration act shored up municipalities, cities, and states teetering on bankruptcy and a lot of that money is still sloshing around at the government level but the house of cards constructors will need to do another hopium injection of mass moolah to keep the cards standing. Banks probably have quite a bit of incentive for their own books to have assets and loans in places where the controlling government entities are not teetering on bankruptcy. How many years is it going to take people to understand how rigged the game is. It’s truly a house of cards and they can make it up as they go and they explain away their actions after they’ve made their moves.

The “Thrill is Gone” take away QE and wolves teeth stop chumping at the bit. There is no doom or gloom, no loaded gun forcing folks the give up their once in a lifetime 2.5% mortgages. Most are priced out, others force their way in with incentives and creative financing, lots of help from mom and dad. I don’t hear the desperation in the neighbors voice to sell. The smart folks understand disposable income, car notes, day care, insurance, taxes, have also increased. Downsizing now days means paying more even if you are exiting the California market. Beating a dead horse, when there no demand.

They are going to wait this out..,…. Until…

One is made redundant, two, both are on short shifts, three, their incomes do not cover expenses and anyone knocking on the door might be a debt collector and the bills on the fridge get paid by what hits the floor first with the Positions Vacant pages in a scrunched up ball.

I have seen this movie before…It was painful for me but I sold the anchor and moved, at a loss. But ended up 15 years later in a debt free position and a passive income. I still work at 70 but wife needs me gone 12 hours

In my town of ~25k residents, there’s a grand total of 4 new construction homes currently for sale, ranging in price from 1.3 mil to 3.7 mil. And this is in southern NH, believe it or not. If I had to guess, I’d say mortgage rate buydowns in this price range are non-existent.

If you’re looking for “affordable” new construction, you’re better off avoiding the greater Boston area. Builders in this area are focusing exclusively on expensive, high margin sales.

Great work surfacing Lennar’s massive incentives, Wolf. Their incentives (as a % of revenue) are approaching what they offered in the lead-up to the GFC.

That said, I wonder whether the following paragraph in your write-up is correct:

“On their financial statements, publicly traded homebuilders add the costs of mortgage-rate buydowns and incentives to their costs of goods sold, and therefore deduct it from their gross profit, so investors see the impact of the costs.”

Based on that paragraph, I initially thought (like Kent, above) that Lennar’s average sales price LESS incentives was $379k (= $426k – $47k).

However, I looked at the accounting notes in several of Lennar’s SEC filings. They appear to me to suggest that Lennar deducts incentives directly from reported top-line revenue (and hence reported average prices) — rather than including incentives in COGS.

E.g., p. 51 of Lennar’s 2023 10k states: “Revenue Recognition… In order to promote sales of homes, the Company may offer sales incentives to homebuyers…. They include primarily price discounts on individual homes and financing incentives, all of which are reflected as a reduction of home sales revenues.” (Curiously, this note is absent from their Q2 2024 10Q — but is reflected in multiple other SEC filings.)

Of course, Lennar’s accounting treatment doesn’t affect your main point that contract prices do not reflect all incentives. But Lennar’s accounting treatment matters for folks who may be trying to back out Lennar’s prices less incentives.

Could you please weigh in to clear up my confusion? Thank you!

Interest rates are only “high” in the context of the last few years.

Go back further in time and will realize they are actually quite normal.

I’ve been a carpenter who worked during several long past collapses. This is what happens. Big new projects keep the signs up….”Coming Soon!, Luxury Development, Phase 1″, whatever they call it, but there is no action happening. The large developments have what looks like active home building sites, piles of sewer pipe and drain rock, maybe a locked up ‘display unit’, but no action and no building going on. Partially finished houses might get finished and might be sold, but the developments look like war zones; apartment/condo sites stop dead, just holes in the ground with partial foundations.

This is Canada, but on my way to town yesterday there are still two 700-800 housing sites supposedly to be finished end of 2022. Hah. Their website shows million dollar+ plus homes all nicely rendered and landscaped….the best lots on the cliffs above Seymour Narrows start at $750K (just for the lot), nothing going on beyond the first site prep, an excavator sits with bucket down and has done so for more than a year now. The cleared forest is starting to reseed and renew, and the cleared lot sites are covered with thistle and lupins. These developments were to bring in newcomers fleeing from cities like Vancouver and Toronto after selling up, because no local would buy such a thing and probably could not afford to do so.

Guess what, if people cannot sell up, or like in US are reluctant to leave a 3% mortgage locked in, then they stay put if possible where they currently live. The developments for newcomers stall.

Many new developments can stop for years. I’ve seen one other waterfront site ‘in development’ for 20 years now. Maybe happen one day, but hard to say? They do have a nice looking display suite though. There is always a hold up. Plus, behind the scenes there is also litigation going on; unpaid suppliers, etc etc.

The actual building contractors who run the crews try to find work for their people. The good ones are compassionate and they certainly do not want to lose good carpenters. They’ll find work to keep their key people going. The numbers development people seem to just disappear. I remember a past ‘major player’ once charged and convicted of fraud, back in the early 90s. Another big developer I worked for was busted with a load of dope in his float plane….this was back in the 70s and I had forgotten about it until just now. I worked for him for a year as a 3rd year apprentice, a good union job.

The workers go on UI, EI, the Dole,whatever it is called where you live, maybe work on their own places or do cashie jobs under the table. I once built a fish hatchery and the crew was made up of subsidised carpenters getting a UI top up. I had already left construction and aviation and remained the hatchery foreman, learned to raise salmon. Changed careers for awhile. This was in the high interest rate 1980s.

It all….all of it depends on interest rates and affordability. We live on trade of goods and services and require growth. If everyone hunkers down all the financing tricks in the world won’t make up for the downturn. My favourite past employer had his apartment properties foreclosed on. He sued the banks and after 10 years or so got a settlement. Meanwhile, he kept limping along keeping one or two long term people working with him, pounding nails as we say.

Mortgage buy backs? Maybe for a while. Not forever. It’s stop gap waiting for a change. The needed change requires people to be optimistic about their own future. Or as Clint said it best, “Feeling lucky, punk”?

All this.

My favorite “sign of the top” is the new 4- seasons Telluride.

I haven’t been up to look, but I picture a jobsite like the one you described coming (back) to a town near me.

Lennar is a good example to illustrate rate buy down as in my experience they don’t offer upgrades. We live in a Lennar house built in 2021 and they only offered the choice between “decor” packages A.B.or C which all cost the same. If you wanted to upgrade the countertops or something they send you to an outside contractor that is approved and you arrange and pay for that separately. Their model is just to keep production flowing by building the exact same thing that was designed with the exact same components they planned on. They figure the cost savings in efficiency outweighs the extra profit for a fancy countertop, or tile shower here and there.

So basically their real sale price has declined from around $405k to $375k in a year.

Perhaps the Commerce Dept. needs to revise their median price data to “median price less incentives” so we can see where everything is really at. Data is useless if the input is garbage. Over 10% in incentives is not some statistically insignificant number.

I’m assuming the new sales prices are weighed heavily by the bigger builders.

New home buydowns in the 80s were routine. 30-year one percent buydown from 10% to 9% cost eight percentage points – simple yield calculations were memorized. 8% to 7% cost more, 15% to 14% cost fewer points, duh. Routinely would buy from 16% (or greater) to 12%. New home builders spent huge on buydowns. Managed sales of thousands of new homes – essentially buyers bought the below-market mortgage, house came along with it. Sometime later, Feds capped buydowns. New home builders will always use multiple ways to move highly toxic standing inventory. Pack the house, rate buydowns, pay max closing, bump buyer broker fees – routinely paid BBs 5+%. TFS

I’m happy with my house being a cash cow, soon I will go to town with the cow and sell house for some magic beans.

I know how this story ends, I climb the bean stalk, sneek past the giant and steal the goose that lays the golden egg, then I live happy ever after with my 3 wife’s.

Fe- fi- fo- fum, I smell the blood of a stinking greedy American.

ha ha………..made me grin, good ol’ satire

DM: Nationwide discount retailer, Big Lots, with 1,400 stores sparks fears of mass closures as it mulls bankruptcy…

A nationwide discount homeware chain with almost 1,400 stores is the latest to warn of money problems.

Big Lots has told financial regulators it may not be able to continue as a ‘going concern’ – raising the risk of store closures and bankruptcy.

The Columbus, Ohio-based chain has seen its takings fall consistently for each of the past ten quarters. And it lost an eye-watering $132 million in the first three months of 2024.

Maybe, just maybe, even poor people are seeing the futility of buying cheap crap and/or now feel richer so are buying higher end?

Just playing Devil’s advocate. I’d never shop at Big Lots as an adult. Can’t believe there is demand for such places (oh, I guess there isn’t).

As to 3% mortgage holders who need more space but are unwilling to move because of mortgage rates …

if the home they bought has an unfinished basement or second floor it might make sense for them to UPGRADE those spaces.

I do realize that is NOT an option for many (most?) young homeowners.

Perhaps they can rely on “The Bank of Mom and Dad” for help 🤪

It what way does it make sense to ‘upgrade’ a basement? And what houses get built with unfinished second floors, unless you are referring to a ceiling being the floor of an attic on a one story house. Many people dump a lot of money into remodeling and never get that money back in the resale value of the house, and finish a basement can be a good example of that. I’d love to have an unfinished basement to use as storage so a finished basement would personally be something I would not care for and for other people, they may have different styles and uses in mind if they do want a finished basement. If you have to borrow money to remodel, don’t remodel. Do it on your own with spare cash or just live with what you bought.

Good answer. But, as with everything financial, it depends.

If you do not view your home as an “investment” but just as a shelter you don’t care if your upgrade increases your home price. Then it might make sense as it could add extra space for less than the cost of a move, along with a new mortgage, and moving your kids away from their friends …etc.

Here in Western DuPage county of Illinois you can buy a new home with an unfinished second floor. It costs less and the new owner can finish the way his wife wants it to look.

Basements as storage are great. Yet you can finish part of it and leave the other part open for storage.

As you say it is usually best to use your own money to remodel. But not everyone feels that way. YMMV

Wow, unfinished second floors? I’m a FIB, at least I was. I don’t know how they do it out there in DuPage county though. The metro area is too big to pretend I know every aspect of it. So these unfinished second floors, do they just leave them as bare studs without electrical outlets, lights, drywall, and only a subfloor and no bathroom upstairs? What kind of McMansions do they have the amigos building out there these days. I doubt there’s any bungalows, ranch houses, or true starter homes being built. Chicago suburbs are Truman Show -esque from all that I ever saw and I doubt that has changed. That’s really something if you can buy an unfinished upstairs considering upstairs usually means a handful of bedrooms that you can call a bedroom or office or ‘honey I’m sleeping in the other room’ because you p-ed me off and you snore room. When the whole upstairs of most suburban houses are nothing but drywalled studs with really cheap paint and cheap carpet and a basic bathroom or two, to do any less than that is really a reverse accomplishment. DuPage county though. I’m looking down my nose at you from Winnetka you poor member of the soiled masses out there in DuPage. Just joking, the north shore can get stroked for all I care, bunch’a white collar criminals. People in Illinois are cool compared to a lot of places. I’d go back if not for the weather and the state lawmakers wanting to keep digging deeper holes for the citizens to lay in, but I might if all things are relative. The western US is far more full of people with a lack of work ethic than the midwest and far more drugs (especially meth) compared to even what people would think Chicago is like.

Love my unfinished basement. Workshop, storage, easy utility access and upgrades. All kinds of cool stuff you can do down there.

And I’ve never been one to want to retreat to the basement at night to watch a movie or whatever. Certainly don’t want to be taxed for finished space in the basement: I feel like that is the biggest ripoff ever.

Unfinished attics in the old houses around here are often finished as well to make flex space or more bedrooms.

Seems like new construction is often maxed out square footage-wise, leaving very little to upgrade.

“Certainly don’t want to be taxed for finished space in the basement: I feel like that is the biggest ripoff ever.”

Same – this is why I will never actually finish my basement. I’ve just been putting carpet over the studs to make it feel more ‘cozy’ instead.

Works if you are on a slope and it’s a walk out basement. Finish that at it could add 30% to livable square footage.

Patch: CA Dominates World’s Most ‘Impossibly Unaffordable’ Places For Housing

Four of the world’s most unaffordable places are right here in the Golden State.

CALIFORNIA — Californians know that it’s expensive to live in California. But a few California cities are now so expensive they are considered “impossibly unaffordable,” according to a new report.

The annual Demographia International Housing Affordability report assessed housing affordability in 94 major markets across eight countries.

Four of the world’s most “impossibly unaffordable” cities are right here in the Golden State. San Jose, Los Angeles, San Francisco and San Diego all made the top 10.

Honolulu also made the list, which means five of the top 10 most unaffordable places are in the United States, according to the report, which has looked at housing costs for two decades.

In the 1990s I worked for a Las Vegas Bank that no longer exists. They were a joint venture partner and lender with the builder of Hidden Hills, Ca near LA. Now a very exclusive area. I was sent to do an audit. When I arrived, the development was similar to those described here: about half the houses finished, some holes in the ground and the rest vacant lots with utilities and roads. The market had been cold dead for months, no sales with a large land and infrastructure construction loan to pay interest on. I went over his books and could find nothing wrong. It was the economy. He had a note on his office door “God, please let there be another housing boom, and I promise not to screw it up again.” Needless to say, there have been some California housing booms since.

Those incentive numbers must include a lot more than rate buy downs. or perhaps I’m missing something.

We just closed a home purchase with conventional financing and bought down the rate by 1%. The cost was $6.5k, reducing the monthly payment by almost $200/month. We figured the cost of the buy down would pay for itself in about 3 years.

Of course the calculation blows up if you end up refinancing or selling/moving.

It would be interesting to see that new home price chart with another line for “net of incentives” to see when they started kicking in and to gauge how much they have really fallen.

I am still in awe of this real estate market.

In my hot southeastern housing market, housing inventory YoY is up 40 percent and is pretty close to the prepandemic average. Days of supply is up a lot also. You’d expect house prices to start to come down given this massive increase in supply but nope. Median sales price is up 3% and median sales price per square foot is up 2.5% YoY. This appears to defy the law of gravity yet there it is.

It should be starting to reverse right. But there are many levers to manipulate this puppet show and they have been pulling a lot of them in a varied sequence but the curtains will start to close after too many of the levers were pulled and special effects activated. The glitter and fog machines will need to be reloaded by the stage hands eventually, but that can’t be done while the show is still live unless during a long intermission (Fed / Treasury Intervention). We are starting to see things turn just as we did in later 2022………..but then the Fed stopped their rate hikes and then outright played people for fools by telling them what they wanted to hear to keep the show going into overtime. So by the looks of it, next year may finally be different than the last 6. When the banks own the referee (the Fed), they is always a chance of major manipulation though (bailouts, injections) and if they’ve done it before, repeatedly, in this cycle, I wouldn’t say for sure they won’t do it again, but they know the game and know when they are ready to let a recession happen when their buddies have their assets in order and shored up and their money parked.

Median sales price increasing may be telling a story more about sales mix than it is about home prices increasing. This has been happening throughout the country, and Wolf has written about it repeatedly.

That’s why I quoted both median price and median price per square foot (which helps cancel out sales mix effects). Both are up.

Everyone is waiting and hoping FED would cut rates.

All the signals are like this: We have made good progress on inflation and are itching to cut rates.

Inflation has indeed come down form 9% to 3% and made great progress.

Only if FED has more hawkish message.

Stocks and real estate ATHs..

As inventory grows while demand weakens, price cuts will have to continue — in addition to fewer building permits issued.

I assume new homes will also start to feel price pressure from existing home inventory increases — but the economy is booming with high paying fast food jobs, so we’ll probably see everything headed higher.

DM: The 30 US cities that have been ‘taken over’ by the upper classes

America’s upper classes are swelling despite record-high living costs, new research has found.

The proportion of US households considered upper class shot up from 14 percent to 21 percent between 1971 and 2021, according to figures from the Pew Research Center.

It means traditionally blue-collar cities are now being ‘taken over’ by affluent families earning $150,000 and above and/or those with net worth more than $1,000,000.

What I find hard to grasp, is the insatiable perpetual process of new developments and the thirst of builders to assume they have a nonstop goldmine with infinite profit.

We saw china implode because of that short sighted stupidity and obviously this is a global game, but nothing seems in perspective anymore except the certainty that casino mentality is like a cascading waterfall.

I think we’re watching the Chinese boondoggle playing out the same exact way in America.

It’s all about stuffing pipelines with leverage .

Example:

“ There’s no hard-and-fast tally of permitted units that are not under construction across dozens of Greater Boston communities. But officials in suburban towns talk about construction permits sitting on the shelf because developers can’t close on financing. In Boston, for example, researchers at the city’s planning and development agency last year estimated there were nearly 23,000 units stuck in the pipeline”

Where is there actual new construction in Boston???? There’s literally no room here.

See:

A 10,000-unit housing development at Suffolk Downs is on hold indefinitely. Here’s why.

In addition, land development loans are in somewhat of a crash, primarily because the cost to start a project doesn’t make sense – but, the backlog of projects in the pipeline is a tsunami everywhere. The imbalance of too much inventory supply everywhere is totally distorted, especially as demand continues to weaken. The pipeline is clogged by toxic waste.

Hubberts- a good observation, sounds very similar to the market-adaptation strategy of the Japanese automakers entering the American realm, back in the day. Post WWII, U.S. automakers slowly neglected Henry Ford’s ‘any color, as long as it’s black’ segment of the market (which Henry didn’t SWOT-analyze, enough, either, believing the success of the ‘T’-model could go on, forever) in favor of highly-profitable extensive optioning and a consumer willingness to wait for ‘their’ auto to be built and delivered-(with a concurrent decline in QA) thus leaving the gap for the end of the wedge-on the lot, no waiting, good-value/quality pieces of transport (…no foreign-built homes available in this analogy, but perhaps equivalent foreign VC? Looking at YOU, ‘California Forever’…).

may we all find a better day.

Dustoff,

The one of H Ford’s they REALLY neglected was, “If it ain’t there it can’t break”.

Always heard he said that.

Hope you check back on my Mexican Standoff dilemma…maybe it was just said in a part of Mendo Co. ?

Only took one small band of stone throwing chimps to make us evolve….upright walking and big brains, both.

And most all stash rocks for throwing, says Jane Goodall.

Not that it gets me off the hook for using term wrong for 50 years +.

NBay – wasn’t familiar with the Henry quote, doubtless was the germ of the later: ‘…if something works really well, it doesn’t have enough ‘features’, yet…’.

With respect to ‘standoff’, I’ve had similar experiences with different terms, having jarring, near cognitive-dissonant impacts in later years-but language being the constantly-mutable (and powerful) thing it is, it can become what locals believe it to be, then employ it as such-at least locally as you note, irrespective of ‘proper’ etymology (a macro-example might be Churchill’s: “…Great Britain and the United States, two great nations divided by a common language…”)-yet another of the many reasons for despair among those who lament the relentless ‘bastardization’ of a mother tongue (and for stashing and throwing rocks)…Best.

may we all find a better day.

Welp… two days late and don’t know if this comment will be read by many, but I see a number of smaller spec developers in my market dumping lots instead of building them out. That to me is the sign that they are getting ready to hunker down…

DR Horton and Lennar are big builders in my rural area, and though we are growing, we aren’t growing THAT fast. I just looked on Zillow and there are currently over 150 new homes listed for sale in my community of about 4000 people.

It is interesting to see the financial engineering required to keep prices up while doing all of these complex buy downs, incentives, and hedges to push the product to consumers. I can only speculate that is to keep the sales revenue target numbers as high as possible even at the expense of losses with buy downs. Perhaps that is due to complex corporate loan agreements tied to sales, leverages against future sales, making sure sales forecasts look as good as possible for Wall Street or fees associated with sales price. Although I don’t really understand it there must be some very strong financial pressures to attempt to hold those sales numbers as high as possible and not to reduce them. This also appears to be happening with MSRPs on new vehicles whereby the manufacturer is doing everything possible to hold the MSRPs up.