After getting whacked by inflation, incomes have now outrun inflation for the 17th month in a row.

By Wolf Richter for WOLF STREET.

Fueled by incomes that outgrew inflation, our Drunken Sailors, as we’ve lovingly and facetiously called them for well over a year, continued to increase their spending in May, and they did so at a solid pace, roughly in line with the Good Times just before the pandemic, and they saved the rest, our Drunken Sailors, and the savings rate ticked up too.

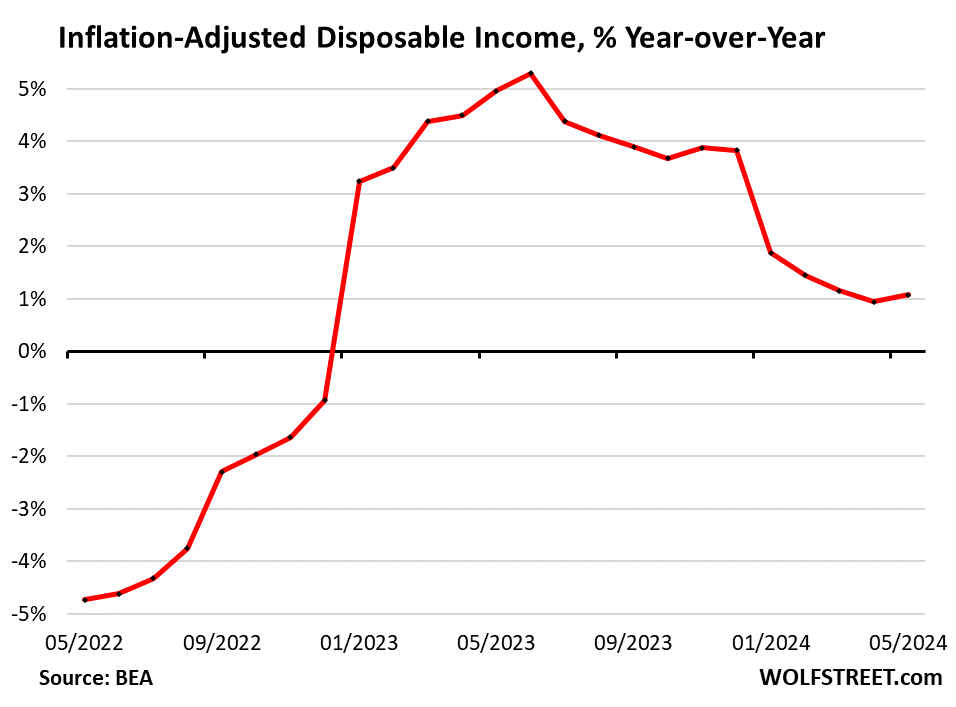

Disposable income, adjusted for inflation, jumped by 0.5% in May from April, the biggest increase since January 2023, according to the Bureau of Economic Analysis today. By contrast, in April, disposable income had barely kept up with inflation.

Compared to a year ago, inflation-adjusted disposable income rose by 1.1%. This marks the 17th month in a row when disposable income outran inflation on a year-over-year basis, after having taken a massive hit in 2021 and through mid-2022, when the explosion of inflation far outran the lagging wage increases. But this growth rate of “real” incomes has slowed dramatically from the 4% year-over-year range in 2023 to about 1%. Nevertheless, they’re out-earning inflation, and that’s what matters.

Disposable income is income from all sources after income taxes and social insurance payments. It includes income from wages and salaries, transfer payments from the government (mostly Social Security benefits, but also VA benefits, unemployment benefits, welfare benefits, etc.), income from interest, dividends, rentals, farms, personal businesses, etc. But it excludes capital gains. Disposable income is what consumers have left to spend on goods and services and to save. And they spent a lot and saved some too.

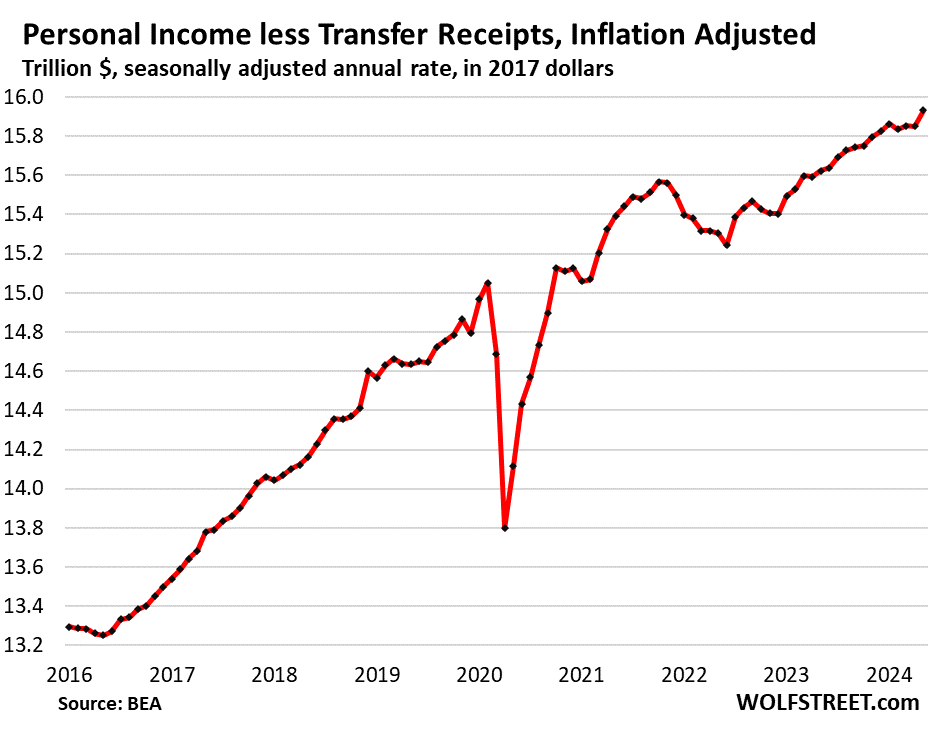

Personal income without transfer receipts, adjusted for inflation, rose by 0.5% in May from April, or by an annual rate of $81 billion, and by 2.0% year-over-year. It means our Drunken Sailors have out-earned inflation by a fairly wide margin, after having taken a beating in 2021 through mid-2022.

This is income from wages, interest, dividends, rental properties, farm income, small-business income, etc.

This income growth is a function of employment growth, rising wages, higher dividend and interest incomes, higher rental incomes, etc. About 11 million single-family rental houses are owned by mom-and-pop landlords with 1-9 rentals, and for them, rental income matters.

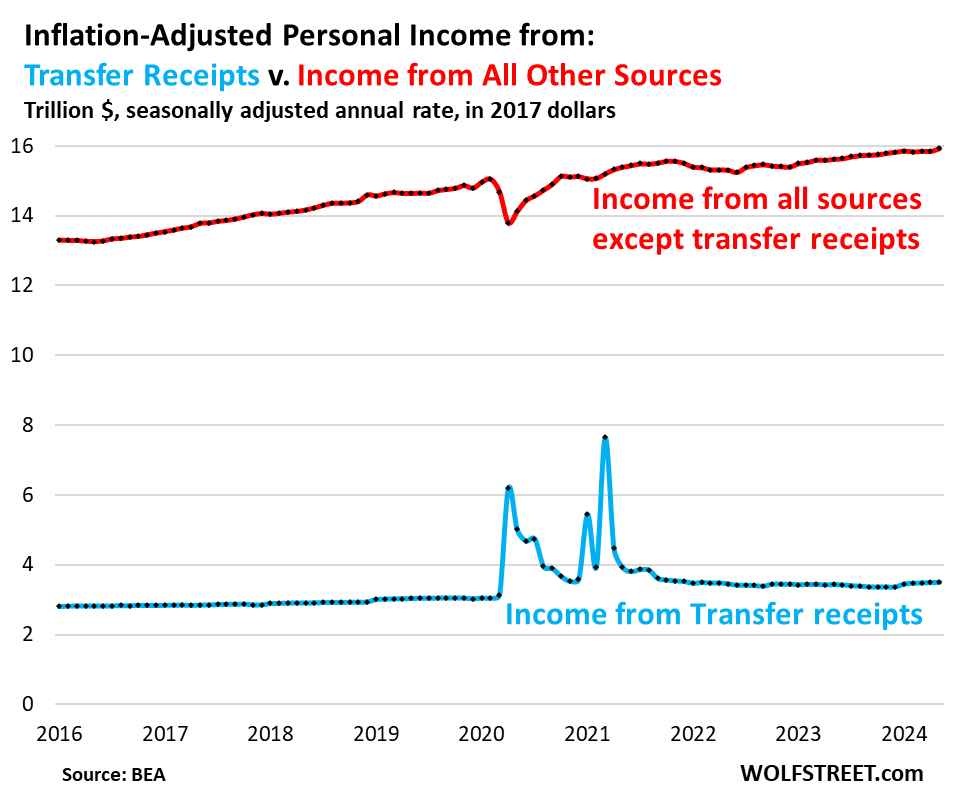

Transfer receipts, adjusted for inflation, rose by 0.3% in May from April, or by an annual rate of $12 billion, and by 1.9% year-over-year.

Transfer receipts are currently dominated by Social Security benefits that grow with more people receiving them, and rising benefits. They also include VA benefits, unemployment benefits, welfare benefits, etc. But during the pandemic, they were dominated by stimulus checks, unemployment benefits, extra unemployment benefits, and other pandemic payments made to consumers (blue in the chart below).

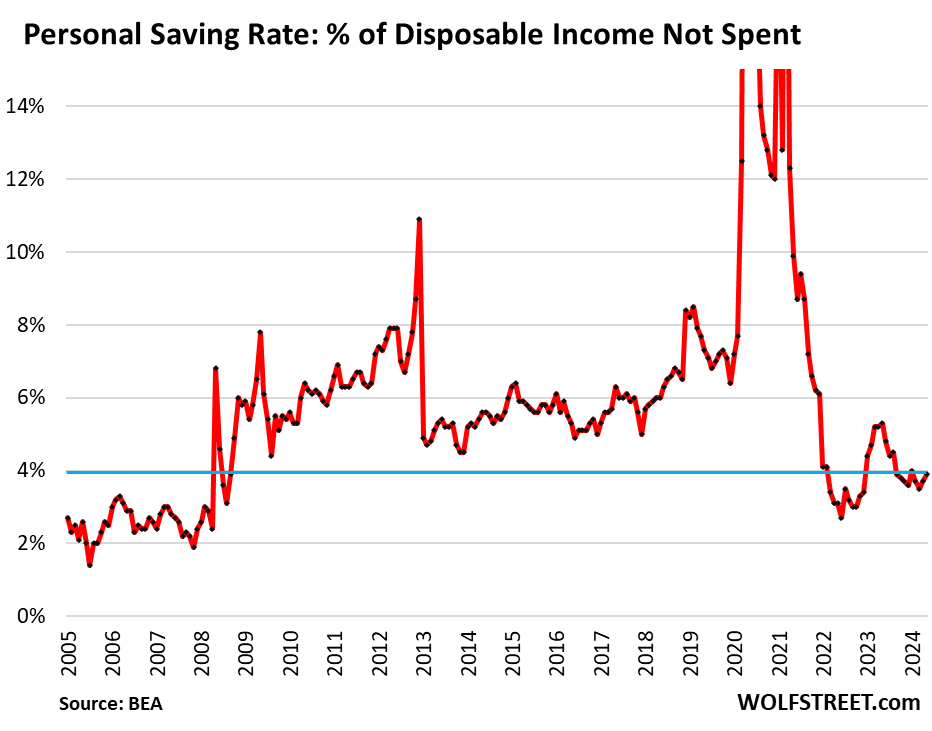

The personal saving rate rose to 3.9%. That’s the portion of disposable income that consumers didn’t spend. It doesn’t mean that they put it into savings accounts. They might have bought stocks with it, or left it in their checking account, or used it to pay down credit cards, or bought shares of a money market fund with it, or whatever.

Americans are not big savers, never have been. Money is there to be spent. But some gets saved anyway. The current rate is lower than in the decade before the pandemic, but higher than in the years before the Financial Crisis.

How our Drunken Sailors disposed of their disposable income:

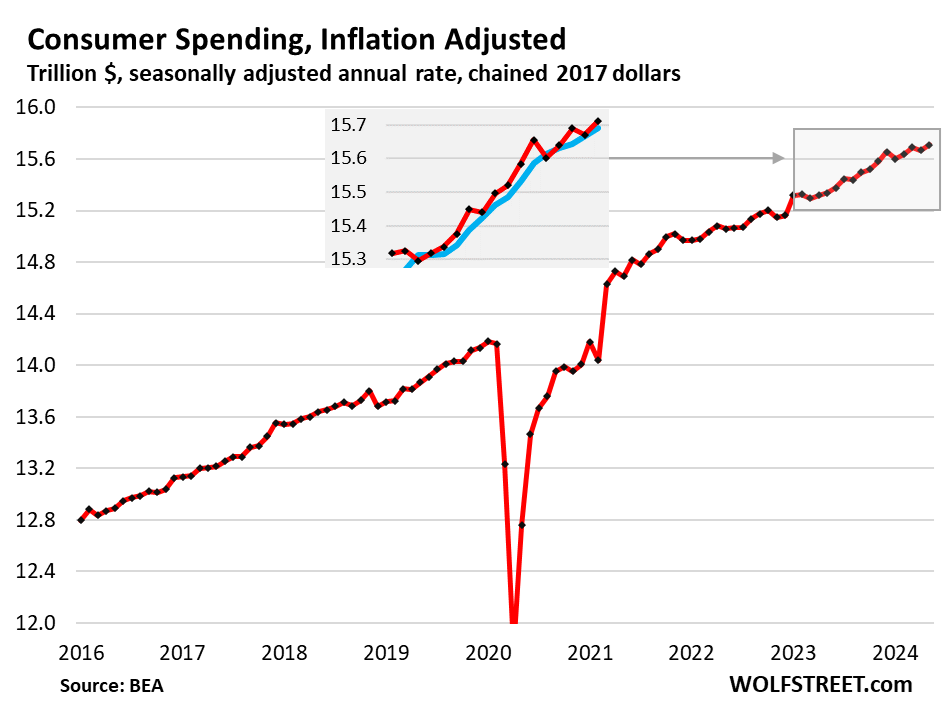

Consumer spending, adjusted for inflation, rose by 0.3% in May from April, and by 2.4% from a year ago. They were outspending inflation at a prepandemic clip: This “real” growth rate of 2.4% year-over-year is right in the range of the Good Times in the years before the pandemic, not exciting, but pretty decent for the US economy.

To see beyond the monthly squiggles, we also look at the three-month average (blue in the insert), which has been rising at a pace of 2.2% to 2.7% year-over-year for the past 12 months, right in line with a normal US economy.

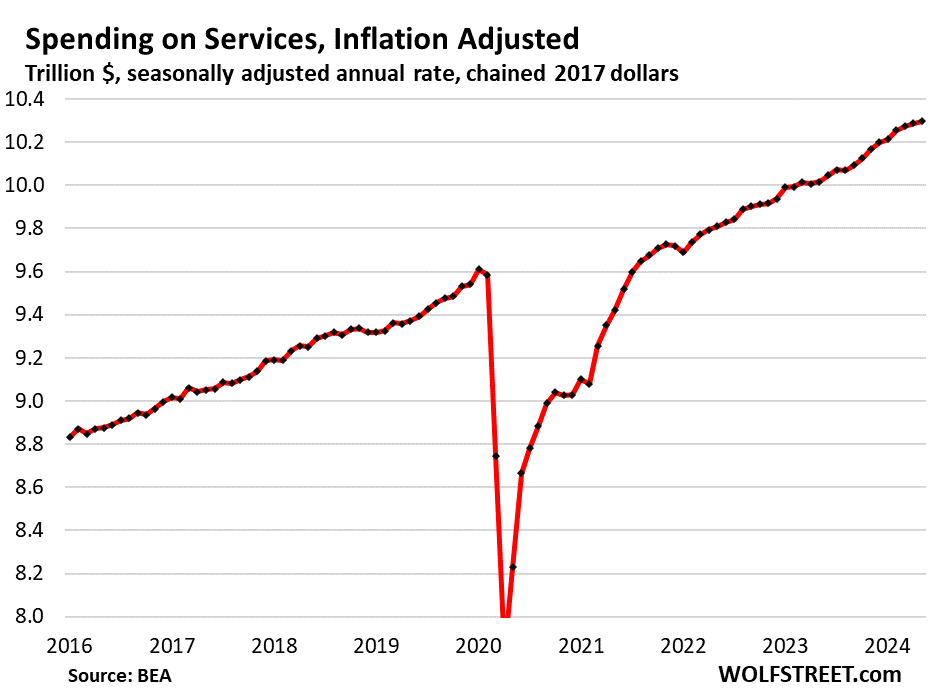

Spending on services, adjusted for inflation, rose by 0.1% for the month and by 2.8% year-over-year.

Inflation in services is high, and it’s difficult to dodge because many services are essential, and consumers are griping and moaning about services inflation, but they still outspent it, but barely.

Spending on services accounts for 65.5% of total consumer spending. It includes rents, utilities, insurance, streaming, broadband, cellphone services, entertainment, healthcare, airfares, lodging, rental cars, memberships, etc.

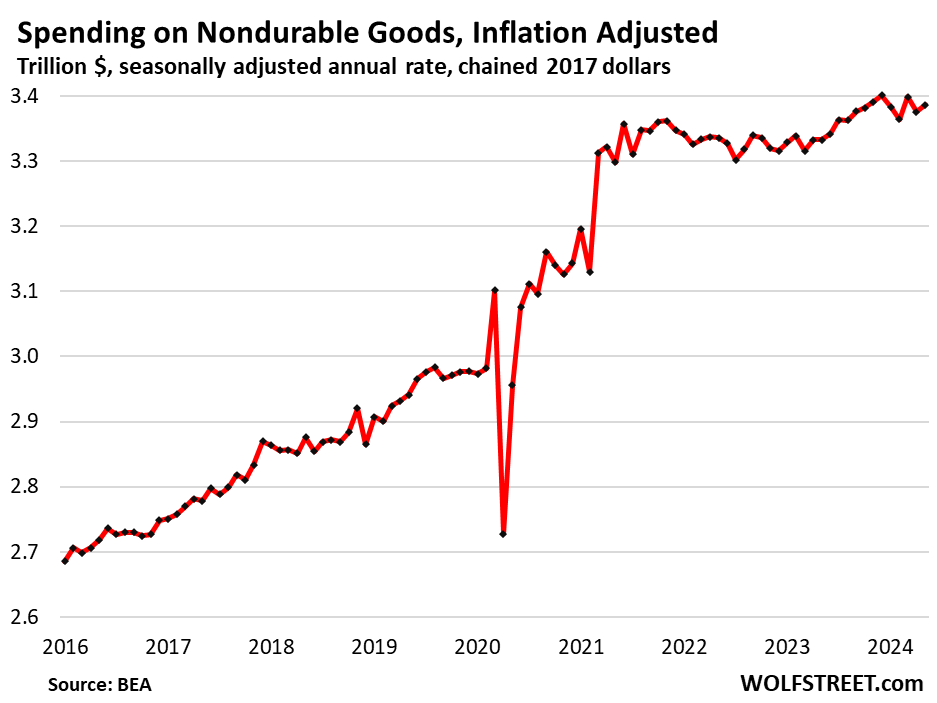

Spending on nondurable goods, adjusted for inflation, rose by 0.3% in May from April, and by 1.6% year-over-year. Nondurable goods are dominated by food, gasoline, apparel, footwear, household supplies, etc.:

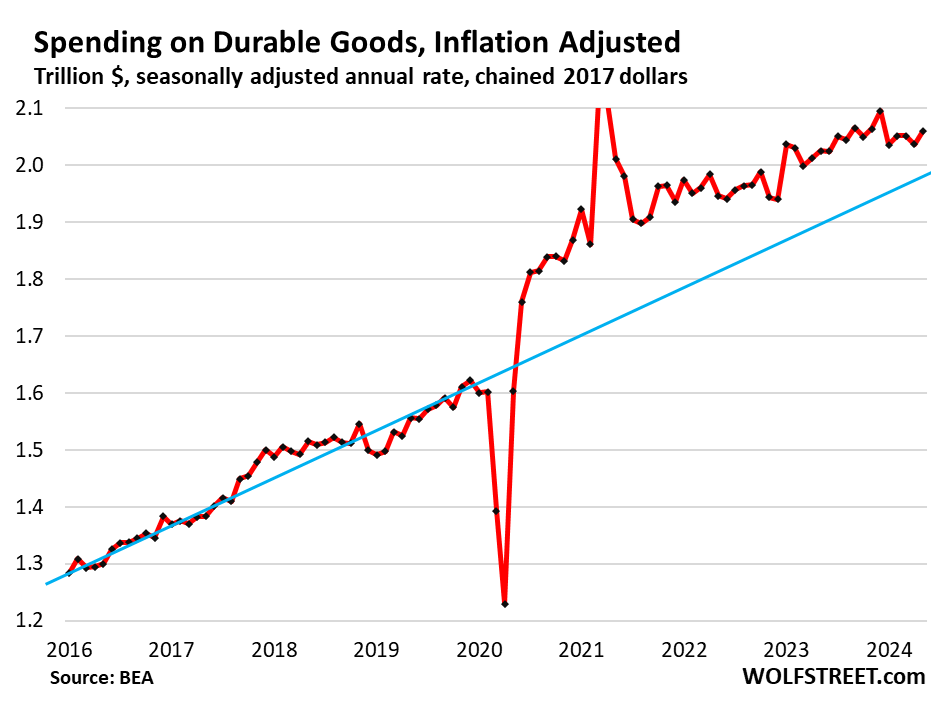

Spending on durable goods, adjusted for inflation, jumped by 1.1% for the month, after having declined the month before. So, the three-month average irons out some of those squiggles, and it rose by 0.13% month-to-month and by 1.9% year-over-year. It seems the pandemic has permanently shifted higher Americans’ inflation-adjusted purchase volume of durable goods. The trend never went back to normal, amazing:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Tha drunk sailors dog “swabbie” is also getting special treatment. Juicy bones for “swabbie”.

“What shall we do with a drunken sailor,

Shave his belly with a rusty razor”

NAH Ht:

” Throw him in the scuppers with a hose pipe on him” was the first and foremost and almost always adequate remedy” for many centuries for the drunken sailor..

Having been there and experienced/done that — clearly NOT when in US Navy, but previously when a deckhand on the largest staysail schooner in the world at the time, I can testify to the efficacy of that ”treatment.”

Time and enough for the application of such, or at least ”such like” for the obviously drunken folx now occupying the seats of the USA Congress,,, eh

Congress apparently is not subject to the feedback mechanisms you refer to. Part of it, alas, is the sailors who apparently like the setup. But as was more often recited circa 2008, risk doesn’t go away, it just pools in new (and not so new) places.

The family man spends hi money on his family. The more money the family makes the more money they spend, which seems like an obvious conclusion, which it really isn’t, because of the Central Limit Theorem certification.

I’ve sailed my entire life…I encourage everyone to get out there, sail off shore, and face their fears….

As in facing down the fear that someone else might have a bigger boat than you do?….and then learn NEVER to be a quitter and work towards a bigger one?

Went to a few Thursday Nite bonfire beach parties at Corona Del Mar……with a rich EX-friend and his mostly richer friends……and fearlessly faced down the yachts coming into Richport with the best of them……everyone there fearlessly faced yachts of ALL sizes although the drunker ones even said stuff like, “That’s my next boat at pretty expensive stuff”. But that’s just drunken courage, nor real courage. Forgot it next day, even denied it,

Hearty souls, all…….as I’m sure you are.

Oh…forgot to ask…..are you more fearless now?

Just amazing I would think most of this income is the higher for longer Fed rate and the fed gov deficit spending selling bonds to whomever paying 5.5 percent !!

Noticed the jump in the 10 year to 4.4 percent today maybe headed to 5? Higher for longer is a welcomed change

If it goes to 5% you can expect to hear a lot of speeches from the Fed. The Fed becomes a simpering coward when rates rise. With the demand for 10-year where it is this is unlikely in the near future. In the 4-4.5% range the Fed is a roaring lion. The meddlers should have left capitalism to sort out its problems instead of pandering to the markets since the Greenspan days.

I would expect QT to get zeroed on that 10yr yield as well

It is not amazing when one considers that the Fed controls the rate curve.

The whale burbed, so what.

Price is the only thing capitalist business really ever considers as important.

Business has had their way, dismantling the American manufacturing sector, pitting American workers against the Chinese peasants ordered to work by the CCP.

Is there any reason to(or not to) include capital gains as well? Since disposable income has outgrown inflation this year and that excludes capital gains, wouldn’t that end up being even more ridiculous? Ie. even my meager portfolio is up over 30% for the year and I’m feeling excited about the extra money. If many people are seeing large capital gains as well, that almost seems like it would just make matters better, would it not? Or at least reinforce the consumers ability and willingness to pay for stuff?

The wealthy and super wealthy make most of their money from capital gains (this includes stock-based compensation). Excluding capital gains (including stock-based compensation) effectively excludes the bulk of the income of the wealthy, which minimizes how the wealthy would skew the income data.

Saw a chart the other day showing 39% of the 2023 aggregate US consumption comes from the top quintile. (@SoberLook)

39% of the consumption comes from the top 20%? Sounds about right. The big spenders matter. We want them to spend big. A homeless person is never going to move the economic needle, but the big spenders do.

9,13,17 & 23% from bottom up for the other quintiles. Don’t expect the bottom 60% have much choice in the excess consumption department.

Will have to see how fickle the big spenders get if the market cools off significantly and the wealth effect mojo reverses. I suspect the horns pulling in could be rapid.

“Will have to see how fickle the big spenders get if the market cools off significantly and the wealth effect mojo reverses. ”

Agreed.

Think of it as the “California Model” – both CA citizens (via their home “values”) and their government (via capital gains taxation) “budget” (ahem) as though paper gains are perpetually guaranteed…as opposed the boom-bust cycles that empirical reality has repeatedly demonstrated.

Then phrases like “complete surprise” and “nobody could have predicted” are retailed as part of (equally predictable) lobbying campaigns in DC.

perhaps the ‘party’ is still ongoing.. but it is winding down.

today nike got absolutely hammered: down 20% on the day with the highest trading volume in history, nearly 130 million shares traded.

yesterday, levi’s was similarly blasted, down 15% on the day on very heavy volume.

these are 2 of america’s most well-known apparel brands.. both of these companies reported earnings in these 2 events and were very cautionary on forward outlook.

nike shoes and levi’s jeans are bona fide examples of ‘discretionary spending’, and consumers are pulling back. i believe these are 2 examples of a ‘canary in a coal mine’ moment, certainly for that sector.. but spilling over into other economic sectors as well.

and i really have to wonder about this whole ‘income outgrowing inflation’ thing.. this is not true across the board. for example, back in 2008, i took a job as a sales manager trainee for $37,000 a year in the dallas area. a similar role today in the oklahoma city area is being offered at 38-42,000$ a year, 16 years later.

once upon a time in the early 2000s i had a job in a call center that paid about $15.50 an hour. i browse through job postings on a frequent basis, and the same type of job now today pays nearly the same, ranging from 14-19$ per hour. nearly 2 decades later.

the minimum wage hasnt increased since 2009 on the federal level. there are still so many jobs out there which are only nominally above that, while inflation and costs are several multiples higher nowadays..

obviously, some wages have ‘kept pace’, but that is not true across the board. its madness to see that the same job i was doing nearly 20 years ago, pays virtually the same today.

Don’t extrapolate from a company’s own missteps and screwups and ineptitude to overall consumers. Amazon and Walmart — both have much bigger sales in the US than Nike — don’t have problems with US consumers.

But isn’t this because Amazon and Walmart are the most competitive on price.

I’m seeing a larger percentage of consumers as becoming more price sensitive.

While we don’t have a weak consumer there certainly is some cracks developing.

With it costing so much money to literally do anything these days it makes sense the consumer would not want to buy Nikes or Levi’s for retail prices

Yeah people are FINALLY waking up to absurd overpricing and responding accordingly!

Some people have stopped buying Nike products for a variety of reasons that have nothing to do with being price sensitive. I have personally found that their quality is outmatched by competitors and then on top of that the sweatshop allegations certainly aren’t a positive.

“I’m seeing a larger percentage of consumers as becoming more price sensitive.”

That should have happened in 2021 and 2022, and we wouldn’t have gotten this huge bout of inflation.

When we go to the store, we’re not constrained by a budget. But we HATE price increases, it’s infuriating, especially to me. Trader Joes took their OJ from 64 ounces to 52 ounces the other day, same price. So that’s a huge price increase. And it pissed me off. So we try to change where we buy things and what we buy, and we change what we eat, etc., to punish retailers and their suppliers for those price increases. We do our part in forcing down inflation. If everyone does this, inflation ends. Price increases are odious. And it’s up to consumers to lash out to force companies to end this BS – like they used to do before the pandemic. This has nothing to do with consumers being “weak” or there being “cracks” in the consumer or whatever, but with consumers being pissed off about these odious price increases. And every consumer survey shows the same thing: Consumers are pissed off, and largely because of the price increases (but they’re not pissed off about their wage increases).

To fight inflation, the first step should be to eliminate some of the most inflated products, which also happen to be some of the most unhealthy products – chips, soft drinks, ice cream, and other unhealthy snacks. These have been some of the worst inflation offenders.

I can live peacefully with inflation, but when she starts crowding the bed and snapping for no reason, that’s when I take notice and make a counter plan. Right now I sleep on the floor while I devise my plan.

A rude awakening for the person starting out in life. I’ve come to expect a rude awakening, so I set the alarm for a few minutes before it happens. Then I create my own rude awakening, one I control.

Sounds like the reverse of getting high. What to you do, sip bleach?

Heard that it WAS most likely a good cure for flu, though, based on the very solid evidence presented.

Forgot…the killing of flu bugs rate was based on various surfaces…table tops, etc, etc. All very true….and embarrassingly obvious, although it was done very quantitatively and logically.

Just the presentation embarrassed me, but the comment and that sycophant Doctor lady’s squirming reaction to it were priceless.

uhh.. wolf

amazon and walmart are very different retailers than nike and levi’s…

they are giants, they sell nearly everything, and its virtually impossible to avoid either of them in everyday life.. of course they dont have problems with US consumers.. almost everybody buys something from one or both of them on a regular basis.

“dont extrapolate .. missteps and screwups”

i can see this as being valid if i just cited ONE company as an example. but two of them? suffering the same ‘screwups’? thats unlikely..

i said: “nike shoes and levi’s jeans are bona fide examples of ‘discretionary spending’, and consumers are pulling back.”

not sure how you can find fault with this statement, or compare it to/with amazon/walmart..

Well, as much as they would like too have a monopoly with the government providing security free of charge, courtesy of the great unwashed diaspora.

All the shoe manufacturers have embraced of selling uncomfortable shoes because they look cool.

Nike is a blurb on the risk scale that is about to exceed it’s calibrated limits. The potential that the excessive price of most physical assets will suddenly be re-priced like the 30 year bond as the Fed jacked interest rates from zero to 5 pct. A 50 pct loss on the risk free security.

Here is a huge long collection of fatal screwups by retailers, going back to 2017, and nothing to do with “weak” consumer:

https://wolfstreet.com/tag/brick-and-mortar-meltdown/

You have to look at the split between wages and investment income. Income from investments is a much greater percentage of the GDP than it used to be.

The other factor is the changing incomes of various professions. There are many highly-paid professions today that didn’t exist 14 years ago.

Since we’re dealing with totals here, we can assume people working in ordinary jobs without investment portfolios are falling behind.

Try not to overthink this. If inflation rose faster than wages, we would all be living in tents within a few years. In the aggregate, of course. Some people do above or below average.

You can easily find data showing the dollar losing a lot of value over time. Wages (in all forms) must have risen faster. It’s quite obvious.

Do you follow fashion at all? Nike shoes air forces ones were the it shoe from about 2021 to 2023, first the white ones, then colors, and then some other Nike shoes became popular. They’re no longer cool now. This might be partially related to consumer spending but also might just be part of a fashion cycle. Same thing happened with Vans at VF Brands a few years ago. Similarly Levi’s jeans were the it jean for high waisted mom jeans and 90s straight leg jeans – but the trend is now wide leg jeans which Levi’s doesn’t do well and things are slowly transitioning to flares which Levi’s also doesn’t do well. Prior to 2020 and the rise of the mom jean I don’t know any woman in the 15-35yr old range who was buying Levi’s.

Wide leg and flares? Didn’t that trend end 10-15 years ago, or am I now way behind wearing the close leg pants?

Everything comes back eventually, we’re currently reliving the late 90s fashion wise. Easiest way to see this is with high school and college kids. If you live in a large metro you’ll also see this with 20-40 yr olds. Rural areas not as much because time tends to stand still post college.

“retro-styles” birthed from what cool-but-impecunious kids discover on thrift-store racks, perhaps?

may we all find a better day.

I haven’t been able too buy a comfortable running shoe for twenty years. Saving money on materials is a strangle your brand strategy.

When I was 45 (over 30 years ago), bones in my feet started breaking when I ran. Before this, I ran every day for 15 years. Trying to find a bright side to this, at least it has saved me money on running shoes.

dang – what happens when boardrooms and c-suites are overwhelmingly occupied by those who never spent a day working on their manufacturing or engineering floors, holding plenty of affection for the dollars generated by, but not much for, the products that brought the firm to the dance…

may we all find a better day.

It’s articles like this that make me regret some of my life choices. I got comfortable in my job and the next thing I know 20 years have passed and I realized that I haven’t gotten a raise higher than the rate of inflation for all those years. Last year was a pay cut. This year a whopping 2%. Wheee.

Yippee! We’re saving 4%! Everyone will be eating caviar and chugging champagne at retirement!!! Glad I’m old enough not to be around to deal with the sh*t show that this country is headed for!

I am in the same boat.

Same job for last 20 years which pays me good but could have done much better if I switched during covid times.

But I don’t regret as quality of life matters more for me than making few more bucks and I can’t take my money with me when I die .

And my lifestyle is very minimalist generally

It could be worse, you could have been a miner since the seventies when I was producing yellow cake in Wyoming. Then producing nickel, copper, cobalt, and ruthenium. Then I threw off a steady job producing copper and molybdenum for the chance to learn how to reduce gold and silver to their elemental state.

A mining technocrat like myself, was out of work for 30 pct of my career.

Now is not how it used to be.

The build in the reverse repo is sort of guaranteeing inflation in the near term, isn’t it? Or is it indicating exactly the opposite, as people try to squeeze blood from a turnip?

It’s the end of the quarter; ON RRPs always increase at the end of the quarter. Next week, they’ll plunge, probably to a new cycle-low. It’s the same thing every quarter. The overall trend for ON RRPs is toward zero.

Wolf,

Do you see any positive correlation of the recent spike of the reverse repos (see attached link) by about $300 billion, with the sticky inflation that is here to stay. At least indicates that the financial markets are well overbought and investors have started again to park money in high yielding money market accounts.

What do you think?

Thanks

Reverse repo spiked because of quarter-end rebalancing. It will come back down shortly.

Ciprian,

It’s the end of the quarter; ON RRPs always increase at the end of the quarter. Next week, they’ll plunge, probably to a new cycle-low. It’s the same thing every quarter. The overall trend for ON RRPs is toward zero.

I can see the party winding down in my world. I live on a big lake in NE GA and boat traffic is way down this summer. People partying on docks at rental houses is almost nonexistent. The vehicle traffic in town this summer is way off and you can see 20 cars before you see a Florida tag.

As a manufacturer, my distributors are doing great but since the beginning of Q2, my direct to the consumer DIYer business dropped off.

I’m not an economist but I think part of this sudden drop in consumer spending that I can see and other business owners are seeing is related to the big increase in auto, boat, commercial, and home insurance rates. If the average family is only paying an extra $250 a month in insurance increases, that’s a week long vacation or few long weekends out of town they taking or it’s a half cart of groceries they aren’t buying.

Floridians are hurting. Homeowner’s insurance is high enough to make a meaningful impact on discretionary spending. The monied classes live along the coast and they’re hit the hardest, inlanders not so much, but they don’t make as much money. Not to mention that the party houses along that beautiful lake are all AirBnBs and prices for such are through the roof. Funny to see the houses rent for $180 a night but a 4 night stay is $1200 because of “fees”. On the other hand, I’m sure folks who work for the insurance companies are making money hand over fist.

The current status of Florida housing foundations is not good. The probability that any given home will disintegrate in the next storm is high. The insurance companies are losing money insuring Florida properties.

Not happening here, LOL. Everything’s packed. People are travelling like never before. Record numbers going through airports. Leisure travel is huge. This goes into services spending. Here, they’re spending like there is no tomorrow, including in restaurants. Went to Costco last Saturday, total mayhem, despite the high prices. Streets congested even on weekends. There is no “sudden drop” in consumer demand here. Maybe instead of driving to the lake in Florida, they’re flying to San Francisco to spend their bonuses more efficiently?

Same perpetual party scene here in Austin: Everyone swanning around being fabulous, lighting cigars with hundred dollar bills. Even the homeless appear more as scrappy bon vivants, glamping in the middle of the action. Wine bars full; salons & parlors booked solid; downtown choc-a-bloc with shopaholics and their designer breed dogs, pushing through throngs of other shopaholics, vying for the next more fatuous money-pit to go spelunking in with their fat juicy raises/dividends.

Grocery store shelves are bereft of all the upscale fizzy water, fancy snacks and sundry other articles of decadence. Guy in queue ahead of me at liquor store where I buy my Everclear (for cleaning mechanical parts, thank you) bought a 6 pack carrier of wine that rang out to just shy of a $800…

No slo-down

Austin used to be fun.

Fun stopped being fun decades ago.

Anyone who goes to Costco on Saturday enjoys mayhem.

That’s the only time I get the car. The boss takes it to work during the week.

That Costco is an unusually high volume, though, for any Costco store. But I agree with the statement – most of my higher-earning employed friends have been gallivanting in Europe, Asia, and Beyond. Even if the unemployed friends have been traveling, you think if you were unemployed, you’d save your money and look for a job. While at home, I’m keeping everything I can for a first-time home buyer down payment.

Hartwell or Lanier?

I’m in the area and see the same lake traffic issues.

CO Tourism is appearing to be slowing down as well. The ski towns had a small decrease in visits this past winter. What I’ve heard from Airbnb owners out there was that a lot more booking were last minute and rates weren’t as great as the winter before. I’m very curious to see where Vail and Alterra’s season pass ticket sales are for next year in their next earnings release. For summer tourism I live in a tourist destination and last summer it took forever to drive across town – hoards of tourists everywhere just randomly walking into the street so you have to drive 5 mph. This year it’s not an issue. Also usually the trail along the river is just a line of tourists – this year I can still bike it, sure there’s still some tourists walking and taking pictures but it’s not one continuous line of them. I’m not saying there’s a crash but just that maybe things are finally going back to their normal 2019 levels which most of us locals would welcome. Oh and I can actually get red rocks tickets last minute at or below face value for most concerts – that hasn’t happened in years. But bars and restaurants are still full so people are def still spending and good luck getting dinner anywhere without a reservation.

Maybe they’re all going to Japan. Kyoto is apparently overwhelmed with tourists this year.

Americans are also massively going to Europe this year.

That’s every year.

We went to Kyoto just before COVID. Probably more of the history of Japan there than any other city, because it was not bombed in WWII. We will be spending another vacation there in the next year.

I see the opposite here in the Hamptons. Very busy “trade parade” every morning and afternoon with every conceivable heavy equipment truck and thousands of laborers in trucks/cars coming to work on homes and businesses. The main road cannot handle the volume and their are accidents all the time as people are frustrated with their long commutes.

I wonder how much of this increase in personal income is interest. Individuals earning 5% FEEL wealthy. They have extra cash flow but the real value of their principal is being destroyed faster than the income growth(using street inflation). They essentially are in slow liquidation mode.

These are “annual rates,” meaning if the May income continues for 12 months, it would be like this. So you can divide by 12 to get a rough per-month figure:

Interest income: $1.82 trillion

Dividend income: $1.89 trillion

Both have gone up only a little over the past 8 months (less than 1%). The bigger increases in interest income came earlier when rates were hiked.

Millions of immigrants expands the underground economy.

Expands consumption, the labor pool, and incomes.

Spencer must be referring to agriculture, because cutting up chickens on bandsaws in definitely above ground.

1) Transfer receipts : those two pulses in 2020/2021, during the war against the virus, in nominal terms, caused inflation.

2) Personal savings : those two pulses, in nominal terms, when the econ was comatose, were used to “sell short” people bank accounts to create a tsunami of money. The drunken US gov cont to pile debt, before the Nov election.

3) In 1920, when WWI was over, inflation was the highest ever. Income tax was 70%. The Fed raised rates from 4% to 7%. The value of US dollar and Liberty Bonds were falling.

4) Andrew Mellon in the treasury and Edgar Hoover in the commerce dept had to deal with plunging commodities, surplus war goods and industrial capacity and war veterans unemployment. They trimmed the gov and cut income tax as much as they could instead of kicking the can down.

5) In 1921 the Fed was BK. Their biggest asset, the Liberty Bonds, became worthless. Despite the early boom of WWI the DJI and the DJT dropped in 1921 to 1881 level, trading at 70% discount. 1921 was a great entry. In 1929 the DJI have risen x5 times during the greatest bull market in the stock market history.

6) On Mar 2009 SPX was 667. Today : 5,500. The Dow [1M] might flop

in July/Aug, either for a stopping action or for a recession.

It seems there is not an accounting for the increase in disposable income that occurred with the massive re-financing of home mortgages that occurred over the last three years or so. My kids, for example had their mortgage payments reduced by over $1000/month with this process. Millions did this and it doesn’t seem to show up in your charts anywhere. That’s over a grand a month, every month in their checking accounts and they received nice pay raises along the way as well.

Not to mention all the cash they pulled out when they did.

Mortgage payments don’t figure into disposable income. Disposable income = total income minus (income taxes + SS contributions). Disposable income is what’s left over after taxes, and is USED to make mortgage payments.

There’s an accounting for it alright — higher prices. Also, lanlords pulled the same trick, then increased rents by 30%+ on top of it. At least the rent increases get accounted for, if that makes you feel any better.

I can only speak for the industry I am in but swimming pool construction is way off in the Southeast. Now repair and maintenance of the ridiculous number of pools built during Covid is keeping us afloat.

That strikes me as an item that has a steady long term average. You only build the pool once. Covid will have had some spike effect (people built a pool who never would have otherwise), but the fall off in construction now is likely just the fallout from people accelerating a construction they would otherwise have deferred for a few years.

S.C. Heel,

All home improvement and remodeling is way off since the spike during the pandemic. It went through a huge spike, and then it just fell off. This was totally expected. You can see that here — we’ve covered this every month here under retail sales:

https://wolfstreet.com/2024/06/18/our-drunken-sailors-bought-lots-of-stuff-at-retailers-including-vehicles-but-at-prices-that-fell-from-the-pandemic-spike/

Yes Wolf but please explain that to our new owners who are expecting 2020-21-22 sales numbers to continue. Old owners made out bigly on that sale.

I’m surprised 3 year old pools need much repair? Maintenance, I can understand since they are chemically dependent and need cleaning.

In a few areas of TX, there’s this thing called concrete cancer…. and the pools are failing.

Probably just cheap-o matrixes or a cowboy job. Gunite should last 80-100 years, easy.

Allegedly, a lack of fly-ash in the mix.

I have several good friends with pools here in Texas and no one is experiencing concrete failures. Maybe that issue is not in the greater Houston area?

Could it be that this failure issue is related to newer pools put in by inexperienced contractors?

In N. Central CT there is a similar problem with foundations. There is a rare kind of sand that contains minerals that cause the concrete to degrade. There are at least 50 houses jacked up on cribbing getting new foundations. They might make testing of the sand used in concrete mandatory. It would save a lot of grief 40 years down the road.

Beach sand. NG.

If you saw some of the builders and subs that jumped into the business to make a quick buck during those crazy times, you would understand why those pools need repairs.

Like the guys who magically appear to repair roofs after every hurricane in Florida.

I work for a pool equipment manufacturer (Automation Controls, Pumps, Heaters, Filters, Lights, Sanitizers, Valves, Valve Actuators). It was nuts during Covid. We had a lot of problems with supply chain issues, now not so much.

Harvey we sold out everything to the bare walls and everything that came in was pre-sold and went right back out the door. It was like nothing I have ever seen in our industry. Buuuuut I would rather have that than the sales uncertainty we are facing now.

Agreed.

Howdy Folks. All US squirrels wanted was to earn some interest on our nuts…… This sober sailor will continue spending now and into the future….. Carter / Reagan Part 2 will be fun this time around………….

Interesting to see personal income and personal savings rate falling below the long term trendline. In fact, it looks like % of disposable income not spent is in a holding pattern near 4% when pre-covid it was closer to 6%. So in fact less overall cash is being saved at the end of the day, likely due to a higher appetite for spending by Americans. It looks like this phenomenon was also occurring in the mid 2000’s in the period preceding the Great Recession. Could this be the windfall of capital gains from a strong stock market that has people willing to spend more since their investments continue to go up?

It’s quite shocking that in a blockbuster economy like we have now, only 4% of disposable income is actually being saved. Sounds like a lot of Americans will be working past the retirement age of 65.

“Sounds like a lot of Americans will be working past the retirement age of 65.”

After they take a share of your savings, courtesy of monetary policy, these people might be looking at a bright early retirement.

Long term interest rates of 4.5% are clearly repressed by monetary policy, and I’m guessing that will continue as successive rounds of self-made “crisis” lead to future stimulus events. 2000, 2008, 2020, XXXX, XXXX,………….

I’m working past my “retirement age,” and I have a blast. Look at our politicians and billionaires, they’re working decades past their retirement age, and they’re having a total blast, and they’re not giving it up until they get kicked out or kick the bucket. Why should only the little people sit in rocking chairs and watch the world go by?

Because most little people do jobs they hate.

Good point (hate may be a strong word though, for “most” little people).

“Because most little people do jobs they hate.”

I don’t know that it’s necessarily the job they hate. In my case, it was the ingrained corporate political BS and those that were the “leaders” instructing you on what to do without any actual knowledge of what you did… and the impact that those decisions would have on the enterprise. Their lack of knowledge was either because they lacked the intelligence to comprehend it or the will to take the more difficult path, vs political expedience, to do what was right.

I worked well past my retirement age because I had my own business (Sub S Corp) and loved what I did. I am still very healthy and now enjoying retirement.

Several of my current friends are dead or almost dead due to poor life choices (lack of exercise, poor diet, etc). Several of these friends were corporate types that sat on their a$$ all day long.

Speaking for the little people, I find you “large people’s” complaints alternately sick and humorous….or both. Never had a desk…..big workbench count? I’m at a folding 6 footer right now….fits my decor well.

Most of the battles at work that I didn’t stir up just for my own or other’s fun, revolve around time clocks. But even they could be fun.

Had a boss who liked to line them up all to the left side several times a night. (11pm to 7;30 am)…..so I dumped a couple handfuls of really tiny set screws in all the slots..maybe 50 slots, for his “people” (as they said) plus mostly others. He was there with a step ladder picking them out with tweezers for hours.

I’m working past retirement age and still paying into SS. Not exactly what I planned in retirement but it has pluses and minuses. Went into a marginal, high crime, neighborhood Sat to do an appraisal and it was worse than it was the last time I went there. The only good thing were the prices. The buyer dude’s condo was selling for $185K using a VA loan. It was a real nice property inside and out. So, the takeaway is just what I said before, you can still get a good deal on property purchases if you are willing to tough it out in some fringe areas of the city. These are areas that not many people want to go live in.

People who have manual labor jobs end up wearing out their bodies faster. At age 65, they can’t even stay on their feet all day. Not true with a desk job. I have a sister with a lot of physical ailments, but she is still working in the insurance industry at age 73.

People like coal miners and oilfield roughnecks end up broken earlier and sit on the porch gobbling Oxycontin like TicTacs.

What you do is not “work.” You produce nothing.

You have zero understanding of what “production” is. You have zero understanding what “work” is. You have zero understanding what an economy is. Do you even know where your head is? 🤣

Wolf, as always, I love your reporting on the economy and its indicators. There’s something funky about this metric, real disposable income, on a per capita basis. The federal reserve chart. It’s pretty much been a straight line increase since 1960, with the exception of the pandemic years, which had high amounts of transfer payments. Here’s me thinking that the current day $50,000 per capita disposable income (in 2017 dollars), isn’t actually 4x higher than the 1960 $12,500 amount (also in 2017 dollars). A 1% year over year change sounds nice, until you need to pay rent, renew your insurance, buy a home or purchase a new car. I’d welcome your insight. Thanks

Since you “welcome” my insight, let me start with this: Everything in your calculus is wrong.

1. Do NOT use the monthly “inflation-adjusted ANNUAL RATES” and then apply another layer of inflation rates to it (your 1%).

— A. They’re already inflation-adjusted. And you’re trying to adjust them again.

— B. And they’re “annual rates” instead of “annual totals.”

2. Go back to the unadjusted annual totals.

3. So use actual ANNUAL disposable income, in current dollars, not inflation adjusted. You can get that here: https://fred.stlouisfed.org/series/A229RC0A052NBEA

4. Then compare the growth of this non-adjusted per-capita disposable income to inflation rates.

5. So ANNUAL nominal (not adjusted for inflation) per-capita disposable income rose from $2,080 in 1960 to $60,276 in 2023. That’s an increase of 2,797%.

6. Then look at CPI, which increased from 30.01 in 1960 to 308.7 at the end of 2023. That’s an increase of 928% (where did you come up with that 1% per year figure?).

7. This comparison shows that over those seven decades, disposable per-capita annual income (+2,797%) by far outran inflation (+928%).

8. Obviously, there are not very many people that worked for 73 years, from 1960 through 2023, though there are some, such as Buffett. So for most people, that’s not a personal-experience time span.

Personally, I can tell you from my shorter income experience (from only 1976) that my disposable income has by far outrun inflation over the ca. 50 years that I have worked, and that our standard of living has increased hugely, from (what today would be considered) abject poverty in 1976 to being quite comfortable and financially secure now. Obviously, lots of younger people today were born with a silver spoon in their mouth, and their standard of living was already up in the sky when they were kids (big house, vacation homes, big cars, expensive schools, expensive clothes, fancy vacations, cool electronics, etc.), and their standard of living may not get any higher unless their career is vertiginously successful.

Thank you for documenting what was obvious to me — that incomes MUST have risen faster than inflation, otherwise it would have been one continuous great depression.

One correction — 1960 to 2023 it 63 years, not 73. I was born in 60 and I know my age :)

Howdy Youngins. Seems to me some of you blame sober and drunk sailors, as though we caused the inflation in the first place….. Some of US will continue living the way we want…..

“Swabbie” could be heading your way. I believe you and the dog are getting the blame for this inflation. “Swabbie” is the drunk sailors dog.

The “youngins” gang is also in town looking for for the culprits.

Just ran the numbers on YoY% change on FRED’s Full Employment (household survey) since 1968 and correlated previous recessions dates.

According to that they start recessions a couple months before it goes negative and end them around the time the change reverses slope mol. I’m sure there are other inputs there too but seems pretty consistent.

According to that, we’ve been in a recession since last December already. That’ll be the bottom 60% I assume vs our big spending stock market asset owners…. they may officially float the boat for a while yet. All this fiat spending seems to have made this time different, go figure.

But the full effects of the big interest rate jump take about 18 months to kick in apparently (refs available ;-) ), and that’s not for a couple months yet. All I gotta say is watch out after July or so…

Homemade extra-fancy fantasy BS.

READ THIS:

https://wolfstreet.com/2024/04/03/how-the-huge-wave-of-immigrants-into-the-us-in-2022-and-2023-impacts-the-employment-data-of-the-bls-household-survey/

And this:

https://wolfstreet.com/2024/05/09/our-favorite-recession-indicator-next-recession-keeps-moving-further-out/

Yeah was inspired by ur favorite recession indicator unemployment rates. Another chart by R.I.A. crew shows that increases of 0.6% from trough on your fav has kicked in recessions before. U can see that on the chart up post. We r lower than the usual obviously but the rate of change was interesting so backtracked it thru the employment data. BS maybe but hey, economics, lol.

I’ll be interested to see what happens if the AI bubble pops but employment w the plebes has apparently turned the corner already.

Correct. The term is selective recession. Danielle DeMartino Booth(who used to work at the Fed) articulates we’ve been in a (selective)recession since q423. inflation is wealth transfer. wealth transfer is a selective process starting with the poorest and industries relating to them, and moves up the wealth chain until the aggregate shows official recession. the financial situation from inflation of the bottom 50% is much more dire than we know(see). next few quarters starting to look bleak from this reality coming to its fruition. once the stock market enters its bear market officially, all the background despair gets clearly exposed as focuses will then turn to the trillions of losses on stocks and real estate by the paper wealthy.

Even during the best of times, 1.7 million people lose their jobs every month (involuntary discharges). Some of those people are instantly in a “selective depression” (cutting back their spending by a lot) until the find another job.

You see, there is no such thing as a “selective recession,” it’s a figment of the imagination of the recession mongers who prayed for and predicted recessions for the past two years, and then didn’t get one, and so now they have to save face by saying this is a “selective recession?” The flow of bullshit by the recession-mongers never ends.

A recession is defined as a “broad-based” economic downturn that includes declines in GDP and employment. We have none of that. What we’ve had are some downturns in specific industries, such as CRE. But a recession is for the US overall, not just for a slice of it.

*Full Time Employment…

Caught a story about income generation, but I’m sure all the charts have priced this in — in addition to the downward September jobs revisions?

“ Walgreens announcing it was closing upwards of 2,100 stores, roughly one-quarter of its locations. CEO Tim Wentworth was quick to offer reassurances on relocating employees: “We don’t see this as an employee reduction, we see this as a footprint reduction.” Nonetheless, most closures will be within close proximity to another store. With 240,000 employees, this amounted to the biggest effective layoff announcement of the year.”

“story about income generation,”

Bullshit. Walgreens is part of what I have called Brick-and-Mortar Meltdown since 2017, which is chockfull with retailers that went bust. Don’t you ever read anything on this site and just come to post BS in the comments?

One of my favorite ophthalmology companies, NIDEK, produces innovative outstanding products has this philosophy…

Our long-term vision is to be a company that promotes wellness and longevity. It is said that life expectancy in Japan will be over 100 in the near future. By that time, social structure should have changed, and people in the age of 85 have a job and support their seniors in the age of 100. Having the business domain of “Eye and Health Care”, I am positive that NIDEK would be of assistance to people in their everyday life.

Hideo Ozawa, Founder

Motoki Ozawa, Current CEO

I, for sure, will be working at 85 if I am still alive. It will take decades for the younger medical staff to get the clinical experience we possess. We just had a member of our medical staff finally quit working at 96. He died. He was sharp (and had a quick wit).

Harry, did the 96 year old die at his desk or on the golf course?

That’s where I want to go, on the golf course after hitting a 300 yard drive at age 91.

Saying “income outpaced inflation” is a misleading statement. We all know that averages are grossly misleading as they do not in any way, shape, or form represent the median condition of the average person. The mass bulk of all rising income comes from upper tier income groups, and the amount of their rising income skews the statistics if you are using averages. A CEO that gets a 5 million dollar increase in income does not represent the Amazon worker who gets $.50 an hour increase, and is struggling to pay $300 to purchase a weeks groceries. For the average American, inflation is crushing their standard of living and pushing them into an ever declining lifestyle.

1. These are NOT averages or medians, but TOTALS.

2. Capital gains are NOT included here. But capital gains are how the rich make most of their money. Stock-based compensation is not included, trading profits are not included, capital gains from real estate and other assets are not included. So the well-to-do skew the averages a lot less than you think.

3. I know, all Americans are dead-broke, except the 1%, LOL, which is the biggest fiction that gets trafficked endlessly because it suits people’s narrative.

4. The lower 20% of the income spectrum have a truly hard time, and they always have a hard time, and inflation makes it worse. But they have also gotten the biggest pay increases. By the time you get to the middle line, the 50% marker, Americans are doing pretty well. 65% of the households are homeowners, and they’re sitting on massive gains; 16 million people will buy a new vehicle this year whose average transaction price is around $45k. Airports are reporting record traffic as people are flying all over the place for vacation, including overseas, etc. etc. But no one can afford it, LOL

Wolf a little off topic here.

I just made a round trip, St Louis to New Orleans and fuel cost both ways was $282. A week before a flight was quoted as $300 round trip. So cost was about the same.

On the way down traffic was below normal on a Sunday. Always stopover about halfway and traffic was the same on Monday. Coming back traffic was the same in being below normal for this time of year. Truck traffic was also somewhat lower.

SWAG for tourism in the Midwest is much lower now than in previous years. Simple thoughts for us old folks but the economy sure seems to be slowing.

Higher for longer seems to be working.

People are flying again. Airports are reporting mega-records.

In terms of truck traffic, sure, we’ve posted dozens of articles here discussing a slowdown in some goods categories (reversion to mean after the pandemic spike), as services have boomed, and services are the biggest part of the economy, including airline travel, we’ve also discussed employment in the transportation sector. Here’s an example — but make sure you click on the link to see employment in all the other categories to get a feel:

https://wolfstreet.com/2024/06/08/longer-term-trends-of-employment-by-industry-category/

Read this article shortly after it posted.

The chart about oil jobsite workers gives me faith in Joe Biden’s urge increasing oil prices. Especially after PJT’s oil glut where 3 drillers went belly up. Joe will now return some of my loss for not paying attention.

This weekend I contributed to drunken sailor-ness, but did not spend any money.

After the boat docks the crew stays for a couple drinks, but this is beer purchased wholesale for sale at the bar, which is then written off for our consumption.