Housing inflation was hot and accelerated in May, amid crazy whiplash-data in other services.

By Wolf Richter for WOLF STREET.

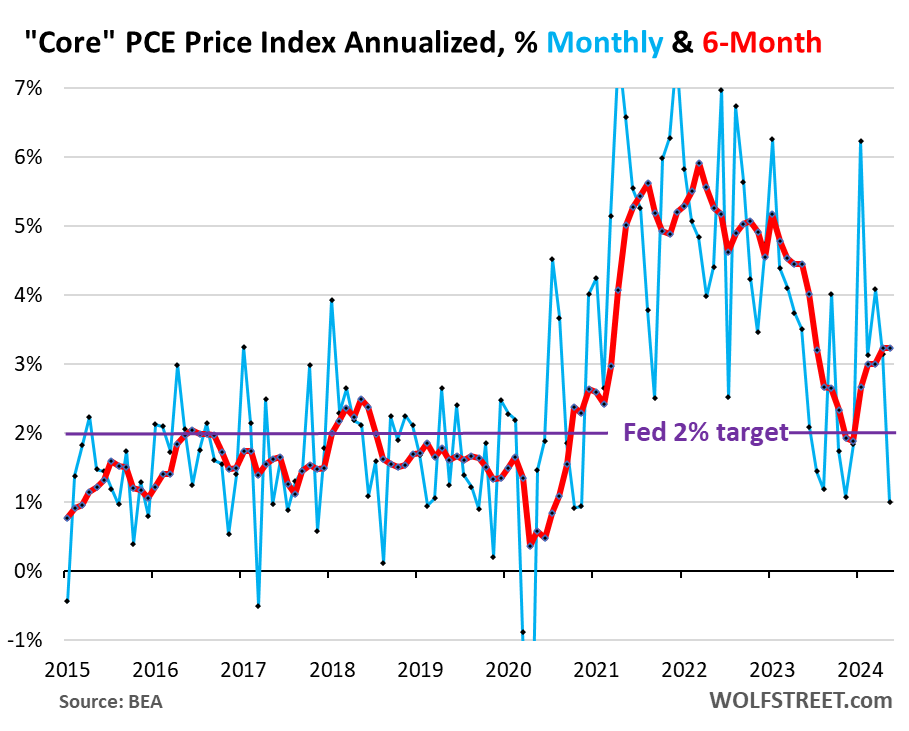

The Fed’s primary yardstick for its 2% inflation target, the “core” PCE price index, which excludes the volatile components of food and energy, rose by 1.0% annualized in May from April (not annualized, +0.08%), thereby below the Fed’s target, according to the Bureau of Economic Analysis today.

This was driven primarily by a plunge in the index for durable goods (-9.1% annualized, the biggest month-to-month plunge in over 23 years), and secondarily by a relatively small rise in the index for “core services” (+2.1% annualized; housing inflation and healthcare inflation accelerated, but some of the other super-volatile services components fell hard).

The six-month annualized core PCE price index, which irons out most of the monthly squiggles, and which Powell cites a lot, rose by 3.2%, same as in April. Both were the worst increases since July last year (red).

In summary, year-over-year:

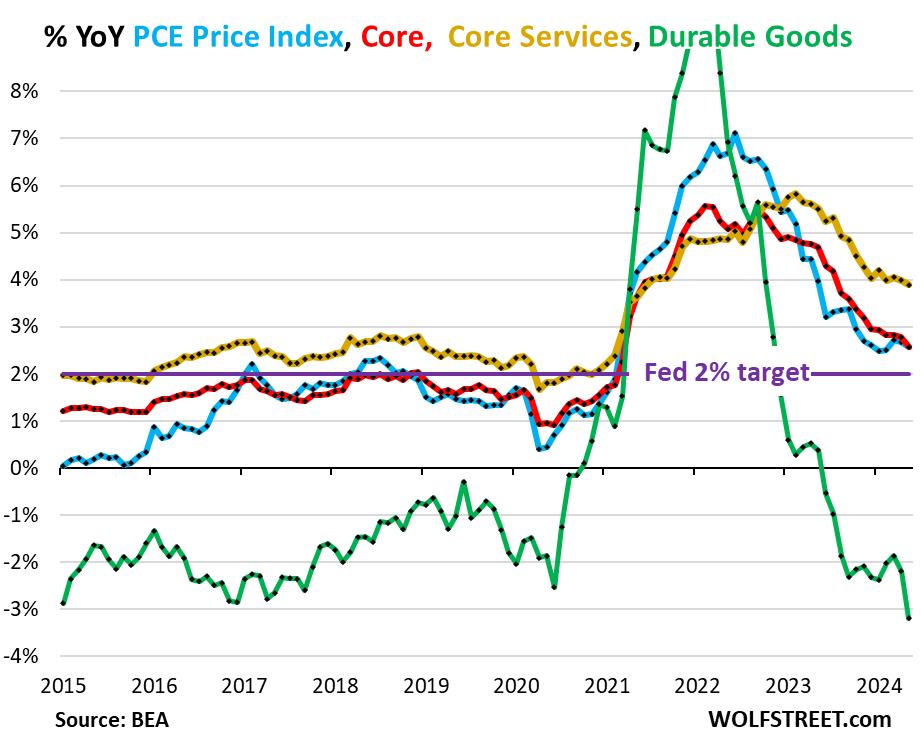

Overall PCE price index, which includes food and energy was unchanged in May from April, and rose by 2.6% year-over-year, a deceleration from the prior two months, but higher than in January and February (blue in the chart below).

Core PCE price index rose by 2.6% year-over-year, continuing the deceleration (red). The Fed’s target for this metric is 2% (purple).

“Core services” PCE price index rose by 3.9% in May, down just a hair from the prior months. It has been in that 4.0% proximity since December (yellow).

Durable goods PCE price index fell by 3.2% year-over-year, the biggest drop since 2004 (green):

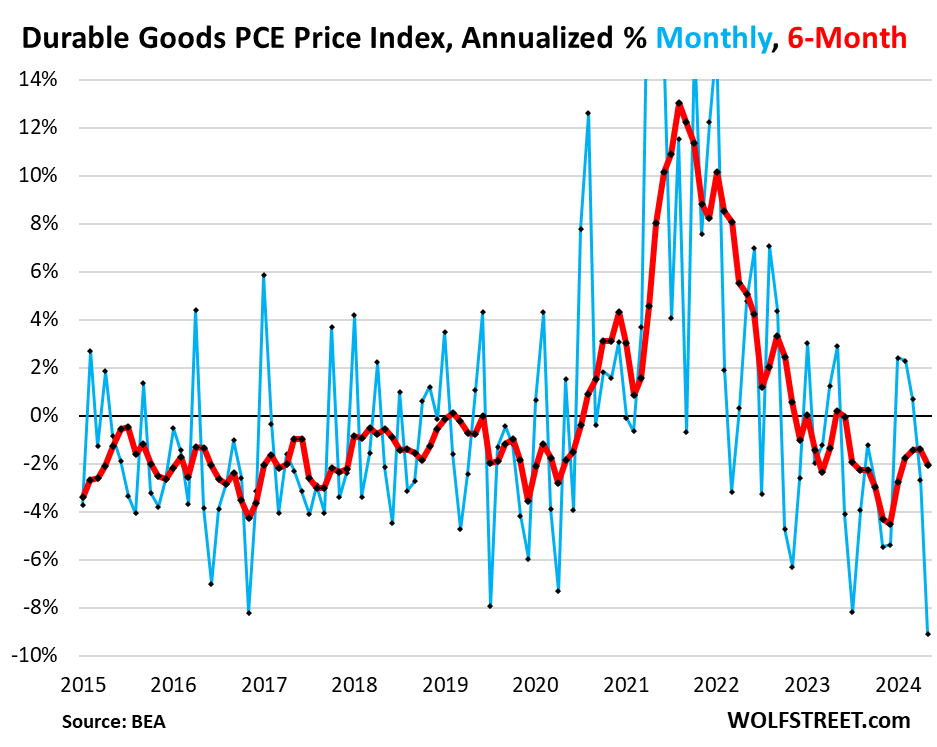

Durable goods deflated, after the huge spike. The PCE price index for durable goods fell by 9.1% annualized in May from April, the biggest drop since September 2001 (blue). Durable goods include motor vehicles, recreational goods and vehicles, appliances, electronics, furniture, etc.

The six-month index fell by 2.0%, the biggest drop since January (red). It tends to run in the slightly negative range during normal times amid manufacturing efficiencies and globalization.

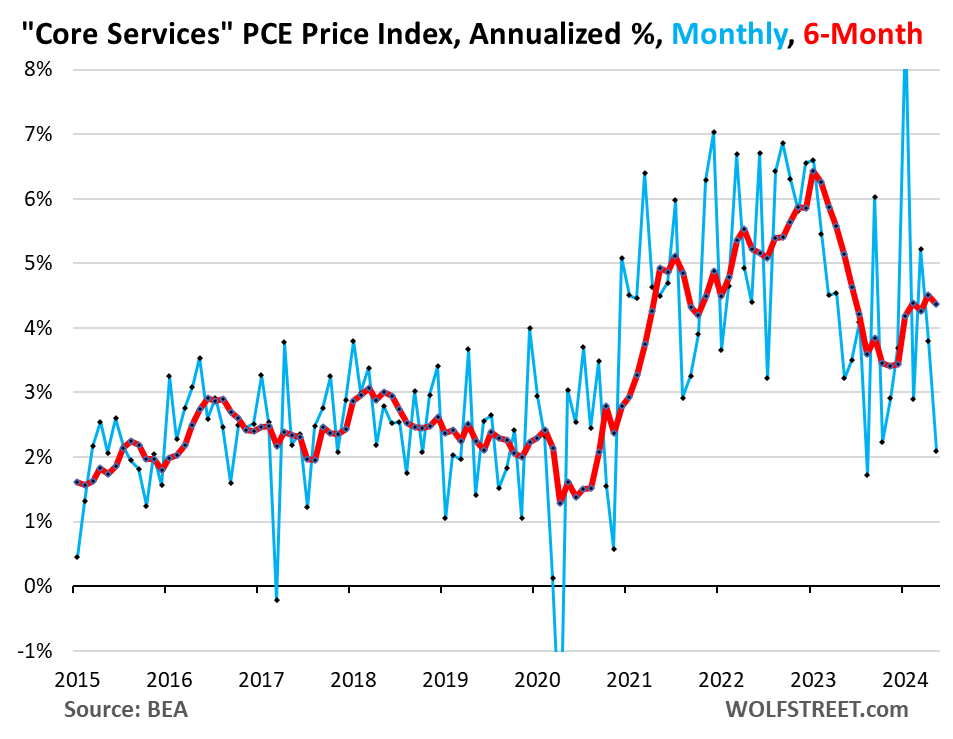

“Core Services” PCE price index, which excludes energy services, rose by 2.1% annualized in May from April, the smallest increase since August 2023 (blue in the chart below).

The six-month core services PCE index jumped by 4.4% annualized, right in the middle of the range of the prior four months (4.3% to 4.5%) and above the range in the second half last year.

Core services is where inflation has gotten entrenched, and it’s where the majority of consumer spending goes. It includes housing, healthcare, insurance, transportation services, communication services, entertainment, etc., with charts further below.

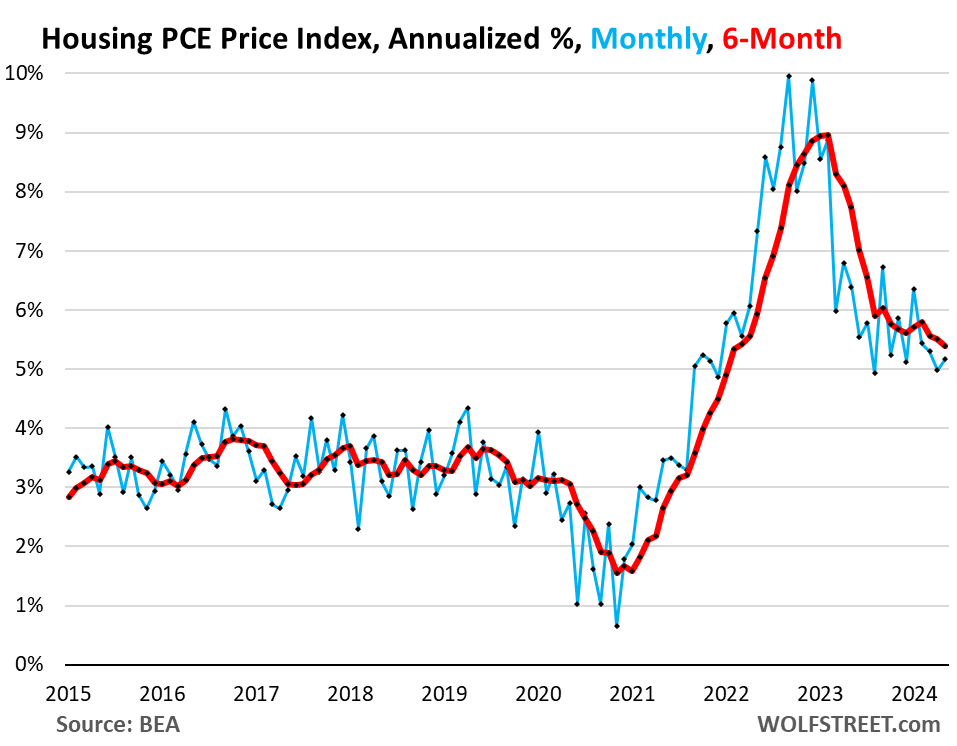

Fed speakers constantly point at the way-too-high core services inflation; and they have been hoping and predicting that housing would cool dramatically, and it did for a while, and then it didn’t. Since August last year, the month-to-month PCE price index for housing inflation has hovered in the 5.0% to 6.0% range.

The core services categories.

Housing PCE price index accelerated to 5.2% annualized in May from April, and was above where it had already been in December and August last year.

The six-month index jumped by 5.4% annualized, a slight deceleration from the prior month. It really hasn’t significantly changed since November and remains high.

The housing index is broad-based and includes factors for rent in tenant-occupied dwellings, imputed rent for owner-occupied housing, group housing, and rental value of farm dwellings.

The remaining core services components are super-volatile, with massive spikes and drops month-to-month that often shoot through or plunge off the charts. Clearly, with this kind of volatile month-to-month data, one month doesn’t make a trend. In fact, they’re so volatile month-to-month that even the six-month readings have big squiggles. Anyway, for your amusement:

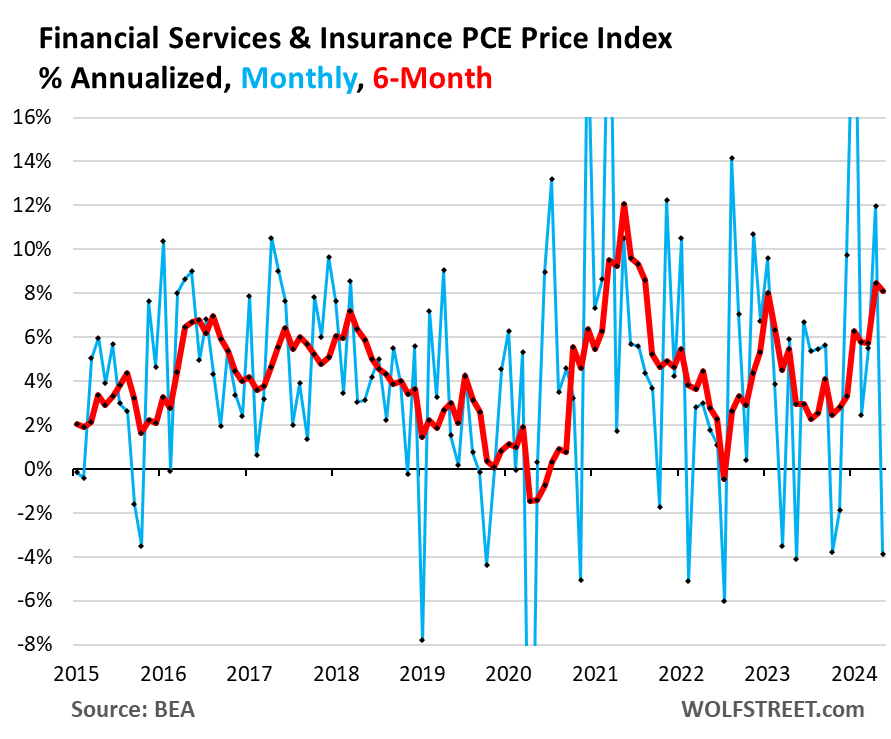

Financial services & insurance:

- Month-to-month annualized: -3.9%

- Six-month annualized: +8.1%

- Year-over-year: +5.4%

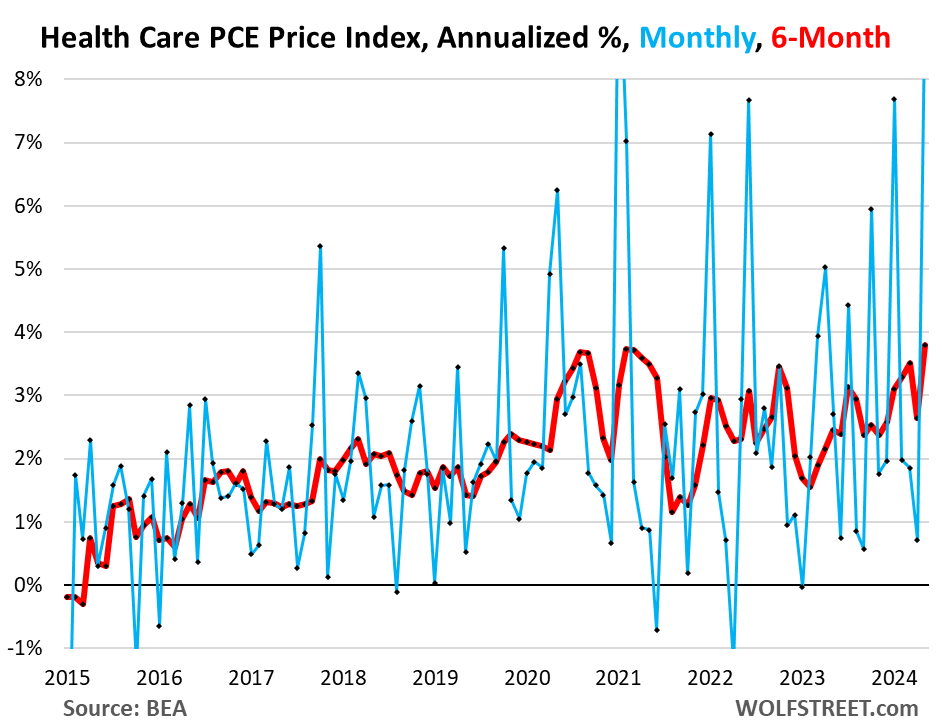

Healthcare PCE Price Index:

- Month-to-month annualized: +8.8%

- Six-month annualized: +3.8%

- Year-over-year: +3.1%

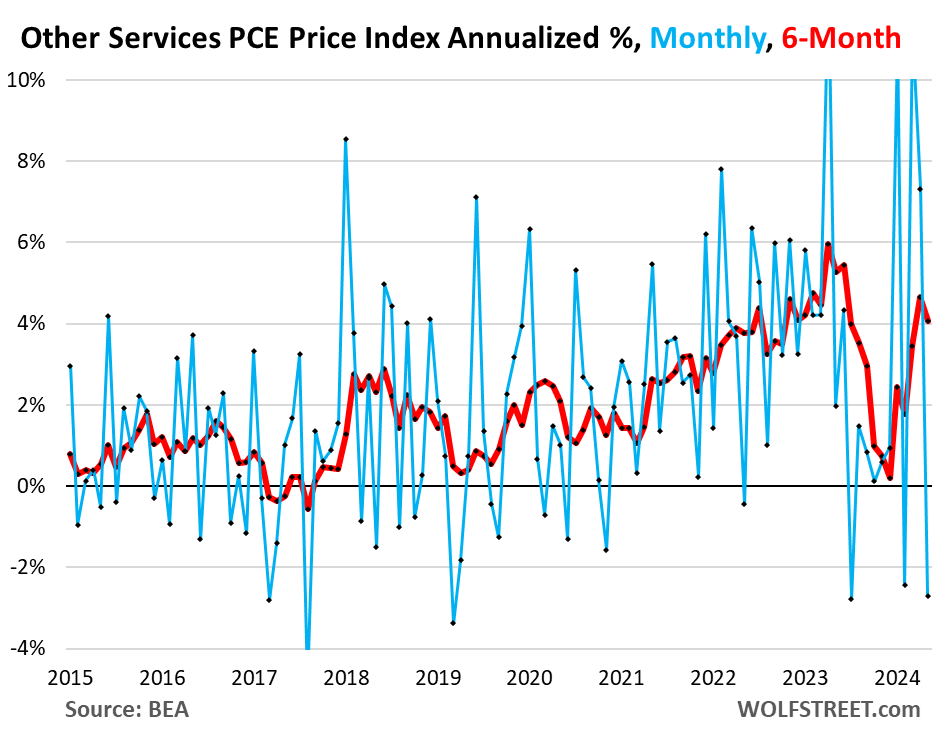

Other core services PCE price index (Broadband, cellphone, other communications; delivery; household maintenance and repair; moving and storage; education and training; legal, accounting, and tax services; dues; funeral and burial services; personal care and clothing services; social services such as homes for the elderly and rehab services, etc.):

- Month-to-month annualized: -2.7%

- Six-month annualized: +4.1%

- Year-over-year: +2.4%

Transportation services PCE price index (motor-vehicle maintenance and repair, car rentals, parking fees, tolls, airline fares, etc.):

- Month-to-month annualized: -7.5%

- Six-month annualized: -0.4%

- Year-over-year: +2.4%

![]()

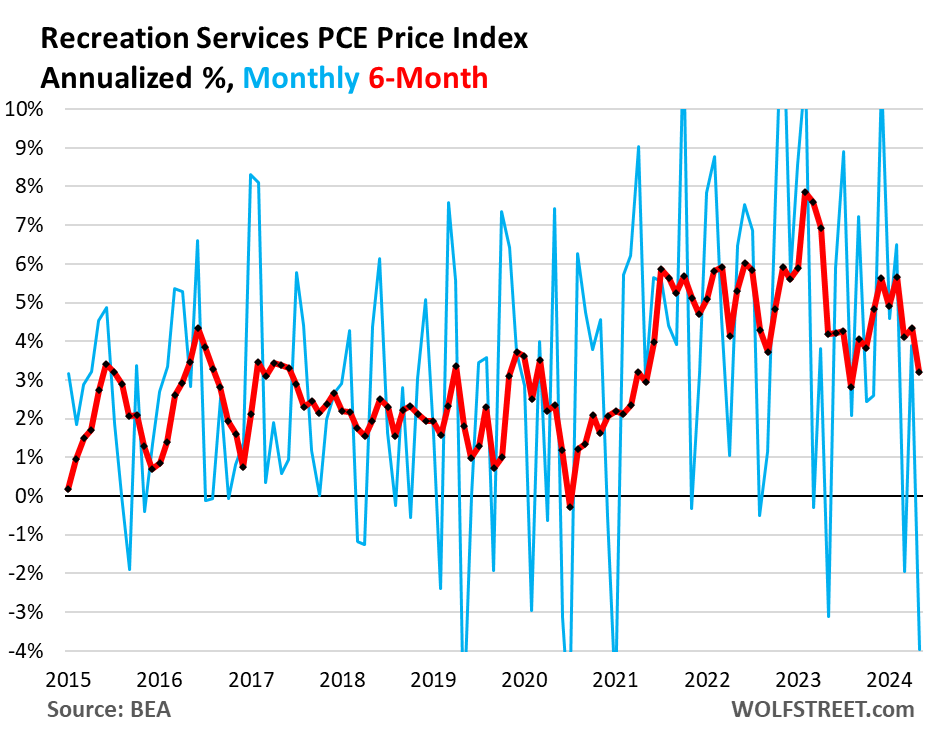

Recreation services PCE price index (cable, satellite TV & radio, streaming, concerts, sports, movies, gambling, vet services, package tours, maintenance and repair of recreational vehicles, etc.):

- Month-to-month annualized: -4.0%

- Six-month annualized: +3.2%

- Year-over-year: +4.0%

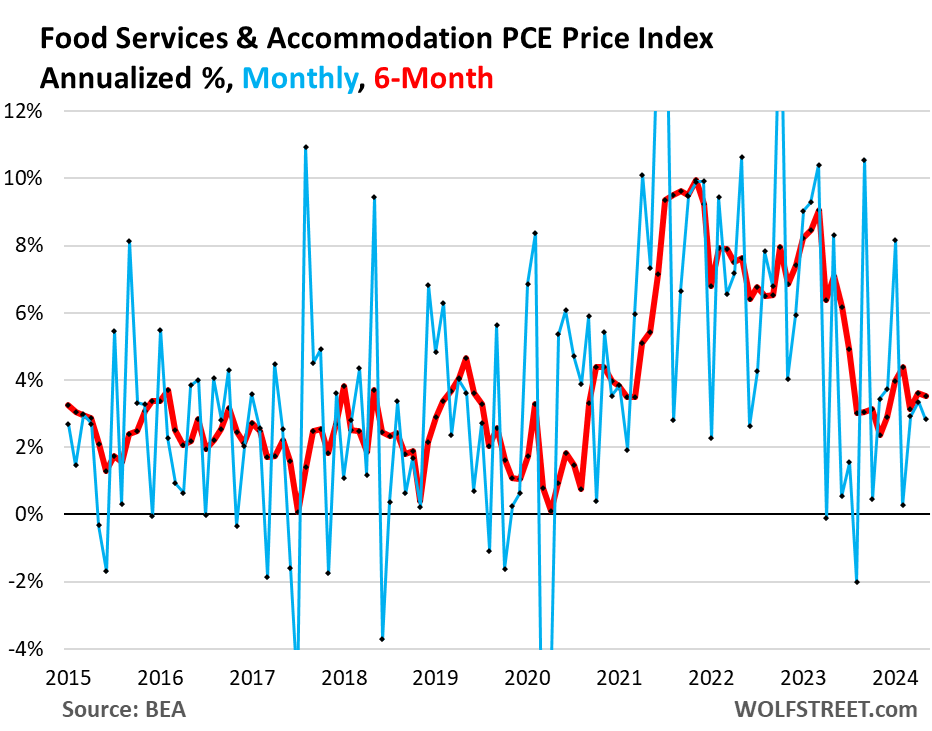

Food services & accommodation PCE price index (restaurants, hotels, motels, vacation rentals, cafeterias, cafes, delis, etc.):

- Month-to-month annualized: +2.8%

- Six-month annualized: +3.5%

- Year-over-year: +2.9%

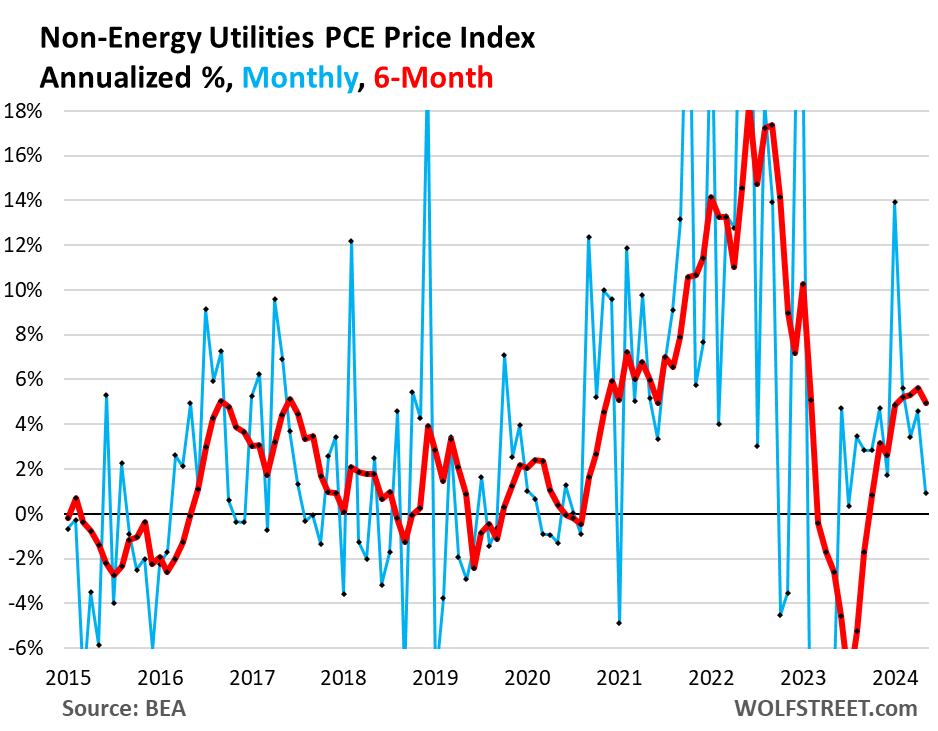

Non-energy utilities PCE price index (sewer, water supply and sanitation, trash collection):

- Month-to-month annualized: +1.0%

- Six-month annualized: +5.0%

- Year-over-year: +4.7%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf – in the 2nd chart, the FED 2% target line is placed on the 3% line.

Thanks as always for your tireless work.

Just anticipating the future 🤣

Thanks.

Hah! Good one. Thanks, Wolf.

Not often I’d say this, but I hope you’re wrong!! 🍻

I’m not sure it’s a joke. In my mind, the real inflation target, which Powell is willing to enforce over the next several years, is 3%.

Powell said he’s focused on bringing inflation down to 2%, but I haven’t seen any evidence of that the past six months. All I’ve seen is a tapering of QT and new highs in asset markets in the face of runaway deficit spending.

A few low-end trend followers no longer have the ability to afford the latest $120 Nike shoes or $8 Starbucks lattes, but asset holders continue to spend like there is no tomorrow. The Fed needs to spray out more gunfire.

Thanks for bringing out the obvious.

FED is totally fine with 3% implicitly but explicitly they are trumpeting commitment to 2%. But action speaks louder than words.

jon,

A 3% target means the base shifts to a 10-year yield of 5% and mortgage rates of 7%, and it goes up from there, for years or decades. Are you ready for home prices where mortgage rates of 7% are considered a great deal for years to come, and when much of the time they’ll be higher than that?

The only thing that keeps long-term yields and mortgages as low as they currently are right now is the belief that the Fed is committed to 2% and will get to 2%. When that shifts to 3%, long-term rates will rise to the next level as a base.

Right now, people are buying homes with 7% mortgages that they expect to refinance into 3% mortgages two years from now (good luck!). If the Fed shifts to a 3% target, those folks get to refinance those 7% mortgages into 8% mortgages LOL

There is a short-circuit in people’s brains about a higher Fed target. They think if the Fed raises the target, it will then cut its own rates.

But a higher Fed target means higher long-term yields/rates permanently. The cost of capital will go back where it had been in the 1980s and 1990s. And asset prices will adjust lower to produce those yields.

I’m good with permanently higher long-term yields, don’t get me wrong. But people need to understand the consequences of a higher Fed target.

Hi Bobber: As usual, I agree with you, but in an election year, more rate hikes ain’t gonna happen. It would be truly amazing to see another rate hike before the election. Besides, you have to consider the onerous cost of financing the massive govt debt, of which both the total debt and the servicing costs on that debt have spiked due to higher interest payments. The Fed is in a tough spot for sure. Damned if they do, and damned if they don’t.

Hey, here is a good one: According to analysts at JPMorgan, Berkshire Hathaway (BRK.B) controls 3% of the entire T-bill market. That’s $158 billion in total. What’s good enough for Warren Buffet is good enough for me! :-)

wolf, doesn’t that assume that the fed doesn’t resume qe? if it does, then they can control the long end rate curve and it doesn’t necessarily reset when the target changes.

Franz G,

Then you would have 20% inflation within a few months, 40% in a couple of years, the destruction of the currency, and an economic death spiral, such as in Argentina. Everyone knows that. No policy maker is stupid enough to even try this. You cannot do QE and 0% into surging inflation and expect the economy to survive intact. People put lots of braindead bullshit out there about QE to push their agenda.

Bobber:

Just saw an article calling this a “selective recession.” (Attributed to JPM)

We’re getting more creative about describing this growing wealth inequality. We’re also at peak justification of bad behavior.

I used to aspire to “create wealth.”

Now I aspire to hang on to a “middle class” status in a world that claims middle class is a household income of $125-$250k…+?

Wolf has explained in about 50 articles why QT is tapering and how that actually makes the 2% target more attainable.

Your comment makes as much sense as saying “I haven’t seen any evidence you’re driving to work, all I’ve seen for the past 6 minutes is you start tapping the brakes as the exit ramp approaches”

“Just anticipating the future”

Which would be a 50% increase in “allowable” inflation (3% target) ,

in “one fell swoop” – in American slang.

Now that’s a “pivot”

Mark,

See my comments above as to what happens if the Fed does that.

– I have been “on the fence” for a while whether or not the FED would hike or lower rates. I thought the FED would llet rates unchanged. But now I have come “off the fence”. It’s clear now the next move will be a rate cut.

Overall asset prices don’t really seem to be coming down. Feds first mandate of “assets go up” is still in tact. No cuts yet.

If they cut interest rates before asset prices come down, they are going to look very foolish. I believe deficit spending and the wealth effect are big drivers of inflation today. Higher rates are required to keep these forces in check.

☝️ truth

Funny how backwards these narrative are tho

Just like the idea of raising the inflation target being bullish we have the “rally that’s built on rates cut hopes” when in reality rate cuts are generally bearish.

They probably don’t cut until the markets are tanking and then they won’t be able to cut that much cause inflation is likely still going to be too high for comfort.

Does 25 bips calm down scared markets? I doubt it and that’ll be decision time but ultimately they can’t let inflation run wild and destroy the currency so they’ll have to sacrifice growth… Stormy clouds ahead

“It’s clear now the next move will be a rate cut.”

I disagree.

For the same reasons that Wolf outlines above, the Fed cutting short rates could “paradoxically” cause long rates to rise. Right now long rates are priced for an eventual return to 2% inflation, but if the bond market loses confidence in the Fed’s ability to get there, long rates could rise to reflect that.

Despite the Fed’s historical bias towards easing, I think Powell & co know what’s at stake right now.

The 2% target is intended to be an average. Do you happen to know the length of time the Fed uses?

For example, for much of the 2010s inflation ran below the 2% target. This doesn’t seem likely, but would there be a discussion along the lines of “Inflation averaged 1.8% in the decade of the 2010s, so I’m comfortable with an average of 2.2% during the roaring 20s?”

Along those lines, who do you nominate for this decade’s F.Scott & Zelda?

Median? Ur N. Anne,

The target used to be “2% or below” until 2020. It was a cap, essentially. In 2020, the Fed changed it to “symmetrical,” so it wants to hit 2% but will allow for small deviations below or above to average over time 2%.

Almost immediately after the Fed changed the target, inflation started to surge, and one of the reasons the Fed didn’t react to it right away was its new doctrine. And that then caused a huge problem in that inflation exploded, with rates at 0% and QE going at full blast. By now, even Powell admitted that the Fed reacted way too late. The Fed could have likely prevented much of the spike in inflation had it reacted instantly and forcefully. Changing to a target of “2% symmetrical” from “2% or below” is now considered by many to have been a mistake, given the outcome.

There has been some noise among the MMT crowd that the “2% arbitrary target” should be raised. I am still trying to figure out why inflation is a good thing in the first place. And the corollary that deflation is “bad”. Who came up with that? I guess it is more Keynesian mumbo-jumbo. I am so glad that I don’t understand their logic, even though I was an econ major in college. Too dumb, I guess.

Economists who advocate for raising the inflation target think that it’s better for the US economy to run with higher inflation rates at higher economic growth rates and higher interest rates. We had periods of that in the 1980s and 1990s. Remember the 10% mortgage? But during some of those years, economic growth was very strong, much stronger than over the past 15 years.

The people that I know who’re promoting this idea of a higher inflation target are not affiliated with MMT.

The Austrian School of Economics will agree with you. Why do we need inflation even at 2%? If 2$ is good would 4% not be doubly better? This is nonsense of course. No you are not too dumb.

Main issue I see with raising the inflation target is interest in debt would also be raising with long term rates going up so I don’t know the feasibility on that.

We need low interest rates to finance our politicians lol

Deflation is bad because it totally crushes economic activity.

Everyone hides cash under their bed and refuses to buy stuff or invest in new enterprises.

It’s not “mumbo-jumbo” it’s observed history. It is the reason there was relentlessly repeating depressions before central banking.

You should demand a refund from your college: their econ courses failed to teach you the most rudimentary concepts of economics. Hopefully they refused to give you a degree.

@Median?

I am not a fan of the Fed’s performance, but the fact is that real interest rates have been negative for a long time. This was a major mistake.

Equally important, I do not believe that inflation is 2% right now, and polls show that very few Americans disagree with me.

My expectation for inflation is 6%, over the next 2 years. If you agree with that, then you should expect long-term bond rates to increase substantially.

Right now, Powell et al. are playing catch-up, which is not a good place to be.

CPI inflation = 3.3% in May, not 2%.

2% is on the Fed’s wish list.

I think the FED is doing a pretty good job. The Government has been increase debt from 5% to 10% per year the last 6 or 8 years. That may be the case with almost all Government.

For the FED to get inflation down to 3% when the Government is gong to increase its debt this year by 10% is pretty good?

What happens when everyone have bought treasuries with all their savings, and there is nothing left to buy the next T-Bill?

What happens if there is such buying pressures on T-bills is that the yield will drop at auction, and so the 3-month bill might sell at a yield of 4.9%, which would then turn off a whole bunch of buyers, and demand falls, and then next month, there aren’t enough buyers at 4.9%, but there are enough buyers at 5.1%, and so the yield goes to 5.1%, and next month there might not be enough buyers at 5.1% and the yield goes back to 5.2% to reach enough buyers to sell all the T-bills. Yield and demand are in a dynamic interplay and regulate each other.

Bank credit is flat to slightly increasing. We are approaching the 5th seasonal inflection point on July 21st (typically a topping turning point).

The economy continues to increase but a a decreasing rate-of-change.

Howdy Folks. Yall better hope and pray the FED follows its own Dots….

I’m good with 0% inflation forever.

Which is why you will never be an overlord of the masses.

No hustle without the squeeze.

Capitalism died in the 70s when currency debasement became policy. It’s been a race to the bottom for the past 50 years.

It feels like the slope is getting slippery.

You’re “good” with an endless whipsaw of repeating depressions?

Most people prefer a stable, consistently growing economy. To each their own I suppose.

Another great article! Thanks Wolf! But, come on, guy. You need to ditch that headline. Nothing the Fed does makes sense. I heard that their new AI prediction model uses a sophisticated Monte Carlo simulation: Their supercomputer flips a million coins and sees if there are more heads than tails.

MW: US Treasury yields finish higher despite May’s PCE data, for two straight quarters of advances

10-year yield considerably higher.

10-2 jumped (still quite negative).

What was the comment about the “paradoxical” rise in the long end of the curve?

When it becomes clear that the near term growth is stalling and the next Fed move will be out of desperation: the curve will un-invert, and subsequently be given a catchy name (RE: Dot Com, GFC, Great Depression).

MW: Nike’s stock heads toward biggest drop ever as some analysts question company’s leadership

NKE -19.99%

MW: Stocks will fall 30% as the U.S. economy heads for a painful recession, strategist says

Retailers and wholesalers raised prices to preempt the hyperinflation.

Inventories of recycled and brand new cars are rising. Car dealers offer large discounts to move stuff.

The strong hands cannibalized the weak hands. Reshoring and tariffs benefit highly skilled workers. Low end workers compete with ten million illegal immigrants. Since the number of low end workers is much higher

than highly skilled workers and if the gov will trim its size ==> prices might deflate in the next few years.

You can drop a few (actually nine) zeros and look at the massive Federal Government as a small real estate investor that has $4,500 in gross rents but is spending $6,000 a year including his variable rate loan that was under $1K/year last year, but will probably be over $1K a year next year.

Despite what our elected leaders (aka “public” servants”) say they like inflation since it increases tax revenue more than it increases the interest on the national debt. I have no idea what will happen going forward but I would not be surprised if we are heading into a long period of higher than average (>3% inflation) .

Many people younger than me were not around to see the median price of a CA home go from ~$25K in 1970 to almost $100K (up 4x) in 1980, that then double (up 2x) going from ~$100K in 1980 to ~$200K in 1990. In 2004 median CA home prices were pushing $500K and it was over a decade later that they again got close to $500K. Looking back does not make the current “doubling in 20 years” “bubble” in CA RE prices seem that crazy.

With that said if anyone wanted to bet me a dinner that the CA median home price will be higher next year I would take the bet (and be pretty sure the guy would buy me dinner). I don’t think we are going to have 70’s inflation again anytime soon but I think we may get back to 80’s inflation where increasing incomes pushed rents and home prices up…

Howdy AInvester I will bet you 50 cents we are in a 70s 80s type inflation / election cycle. My old lava lamp shows it……. We shall see if we live long enough……

Your name checks out aptly 😀.

Btw.. I have few homes in San Diego .

The high home prices have totally destroyed the home buyer aspirations and future generations.

People working in lower spectrum of wages got big raise but still can’t afford a modest place to call home which cost a million dollar here

Something has to give in ..

I don’t know what but I am assured fed won’t break housing market at any cost

You’re exactly right. Something HAS to give. When the generations coming behind you have a lower standard of living and less $$$ to spend. The outcome seems pretty obvious. Major housing price crash OR wage inflation for many years. …If immigration is restricted by the government (a certain Orange man’s preferred approach), you’ll see wage inflation, which will in turn cause elevated inflation to eat into Boomer cash piles. …This might just be the ticket! 🤑 🤙💪

True. Even thought the FED is being a little restrictive it is not effecting Government borrowing. The US government is not having any issues in selling its debt at 5%. Plenty of people are buying it.

Home builders will start building starter homes again because there will be a big market for them. Starter homes are the 2 and 3 bedroom homes. 1000 to 1500 sq ft. That could drop the median home price down k to 80k to 150k

Currently, the median home sq ft listing price is $233. The median sq ft listing is about 1860 ( down from about 1960 sq ft prior to the last year.

So $233*1860 = $433k So if homebuilders reduce home sizes to 1200sq ft to 1500 sq ft. Then house prices could drop between 233 x 1200 = $279k to 233 x 1500 = $349k.

Did Boeing’s two straight months of zero orders for its MAX line of planes cause most of the plummet in the durable goods component?

Boeing has absolutely zero to do with it. The PCE (“Personal Consumption Expenditures”) price index for durable goods measures price changes in durable goods that consumers buy (cars, trucks, fridges, computers, tools, furniture). Consumers usually do not buy Boeings. I mean, as we know, Americans are maxed out on their credit cards, live from paycheck to paycheck, don’t have enough money for a $400 repair, and don’t have space left in their garage for a Boeing, and so they don’t buy many Boeings.

Right, you are. I better not give them any ideas.

@JeffD

Ah, right. Don’t give them any ideas. :-)

Durable goods plunge just looks like it is giving up some of that previous gain. Price competition finally working like its supposed to, but it will stabilize at some point.

Service inflation needs to come down much more and is surely running too hot to start cutting soon.

We have several revisions ahead, for both inflation data and employment, which obviously fuel those crazy squiggly volatile chart noises; it would be entertaining to break out a visual of how revisions influence this noise.

To wit, random upbeat commentary (worth nothing):

“… Olu Sonola, Fitch Ratings’ head of US economic research, said in commentary issued Friday. “Core inflation is now below the year-end median estimate that was penciled in at the last [Fed meeting]. If the trend we saw this month continues consistently for another two months, the Fed may finally have the confidence necessary for a rate cut in September.”

The May PCE data boosted investors’ optimism for a September rate cut. On Friday morning, the probability increased to 61.1% from Thursday’s 59.5% for the federal funds rate moving a quarter-point lower, according to the CME FedWatch tool.”

1. There won’t be any major revisions of the PCE Price index until early 2025. The last set of revisions was minor.

2. It’s kind of a silly hope by Fitch Ratings to hope that, with this brutally volatile data, we’re going to get the same low outlier reading three times in a row. If you look at the charts, you can see that it doesn’t happen. After one or two really low reading, you get some high readings. Which is what makes this data volatile. Check out the blue lines. I mean, tell Fitch to check out the blue lines.

And while at it, tell Fitch that May wasn’t a “trend,” but an outlier far outside of the trend.

Muh rate cuts!!

Thanks Wolf, more data showing that the Fed is doing their best to get CONgress to act responsibly. Allowing the target rate to creep up would be a disaster.

I take total, full, 100% of the responsibility for the May 2024 drop in PCE durable goods. Blame me. It is ALL my fault.

I bought NO PCE durable goods in May 2024. 🤪

Instead, I paid 50% of my yearly property tax assessment.

R* Limbo Dance and adjusting the bar

From Kashkashkari at fed:

“ Given that housing is a key channel through which monetary policy affects the economy, its resilience raises questions about whether policymakers and the market are misperceiving neutral, at least in the near term.”

Misperceiving data is ubiquitous these days

Inflation deniers keep hyping this one monthly datapoint as if it’s a trend.

Thanks, reminds me: We should make a list of the special terms we’ve coined here to express the spirit of our times. This is what I can recall at the moment off the top of my head:

Tapering deniers (late 2021)

rate-hike deniers (early 2022)

QT deniers (from mid-2022 through today)

pivot mongers (from mid-2022 through today)

rate-cut mongers (from mid-2022 through today)

inflation deniers

Do not forget: Drunken sailors

love that 5.25% on my T-Bills, Wolf…..Hope to live in the Brocklebank 1 fine day!

I see NO clear downtrends in these charts (looking at the red lines).

The transportation services chart is the closest… and shows a double bottom (possible reversal?)

Others are in uptrends and/or establishing a new higher range (compared to the 2015-2020 values).

The pain has diminished: Just what the sailors needed to feel emboldened. Americans are hard headed and resilient. We’ll just spend our way out!

Maybe the plunge in durable goods is due to the fact that consumers are maxed out and only spending for necessities? I haven’t bought a single durable goods item in the last 10 years, except a car which I had to buy as my previous vehicle was totaled in a hit & run accident. Not planning on any durable goods purchases for the next few years unless something breaks.

Durable goods are the smallest category of consumer spending, accounting for only 13% of consumer spending. Services are 65% of consumer spending. Nondurable goods (food, gasoline, supplies, etc.) are 22% of consumer spending. Younger households, when they start out, buy lots of durable goods to equip the home, get the cars, etc. Older people buy far fewer durable goods. That’s the nature of durable goods. Most people don’t buy a car every year. So it’s not a common every-day purchase. Same with laptops, appliances, etc. But during the pandemic, people when on a huge binge on durable goods because they couldn’t spend their money on many services, such as travelling, concerts, eating out, etc. And that’s now slowly reverting to trend.