Sales in the mid- and lower range swoon as many people who need a mortgage seem to be waiting for lower rates.

By Wolf Richter for WOLF STREET.

Still dogged by mortgage rates milling around in the 7% neighborhood, and by people’s urge to wait for lower mortgage rates before buying, sales of existing homes of all types – single-family houses, townhomes, condos, and coops – fell further in May from April on a seasonally adjusted basis, to an annual rate of 4.11 million homes, just a notch above the low points in late 2023 which had been the lowest since the depth of the Housing Bust in 2010, according to the National Association of Realtors today.

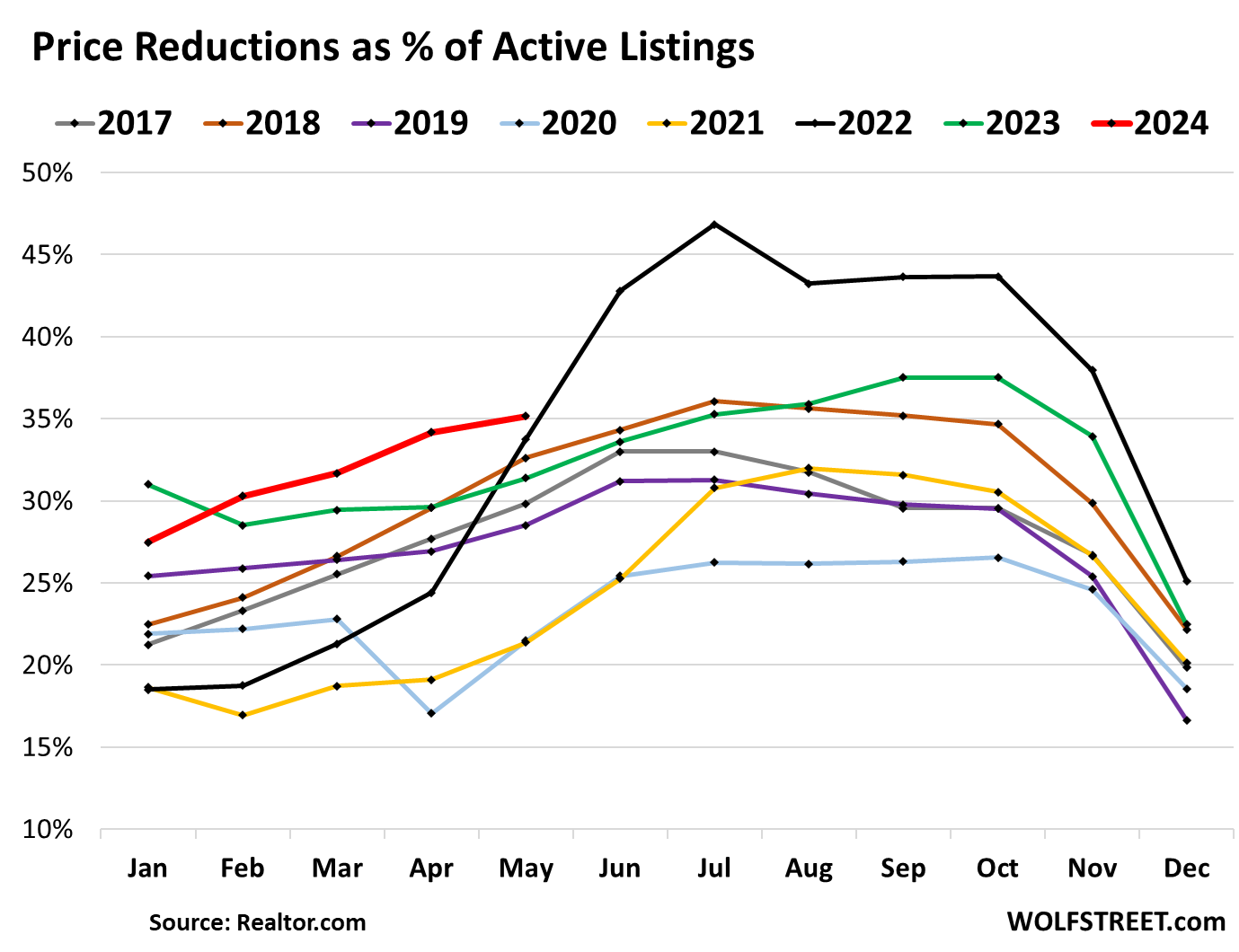

The drop in sales came even as supply and active listings jumped to multiyear highs, and as price reductions to active listings were the highest for any May in the data by Realtor.com going back to 2017. (historic data via YCharts):

But sales shifted massively to the higher end, while middle to lower end sales swooned, as the NAR pointed out, a change in mix that skewed the median price and pushed it higher (more in a moment).

Sales in May were down from the Mays in prior years:

- May 2023: -2.8%

- May 2022: -23.9%

- May 2021: -30.6%

- May 2019: -22.9%

- May 2018: -23.9%.

The 3% mortgage rates of yore are having the effect that these homeowners don’t want to buy another home, and they stay put. Because they don’t buy, sales are down. And because they therefore don’t put their current home on the market, inventory is down in equal measure. According to our estimates, the entire housing market may therefore have shrunk by about 20% because a large portion of homeowners with 3% mortgages are neither buying nor selling, and have vanished as demand, and have vanished in equal number as supply.

The average 30-year fixed mortgage rate has been between 6.5% and 7.5% since late 2022, reaching 7% in October 2022, according to the measure by Freddie Mac. In the latest week, mortgage rates averaged 6.87%. While that seems high after 14 years of interest-rate repression through 0% policy rates and QE that caused home prices to spike, those rates would have seemed like a pretty good deal during more normal times

Price reductions rose to 35% of active listings, the highest for any May in the data released by Realtor.com going back through 2017:

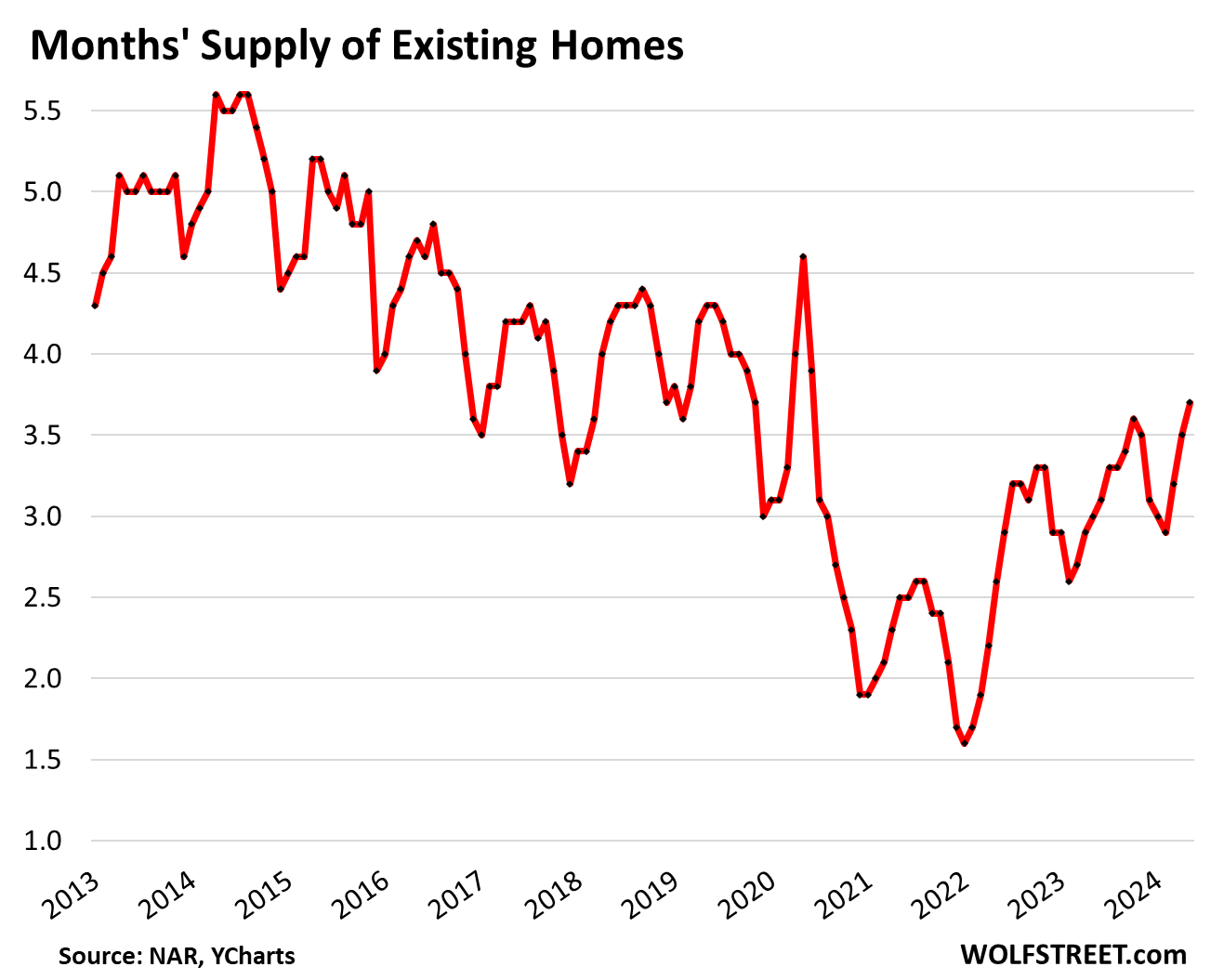

Supply jumped to 3.7 months, the highest since June 2020, as inventory for sale jumped by 18.5% year-over-year, to 1.28 million homes, according to NAR data, while sales were down 2.8% from a year ago, and by 20% to 30% from the Mays in earlier years.

Active listings surged to 788,000 homes, the highest since July 2020, and up by 35% from a year ago, according to data from Realtor.com, as more new listings came on the market amid very slow sales. Compared to May in prior years:

- May 2023: +35.2% (green)

- May 2022: +64.3% (black)

- May 2021: +76.0% (yellow)

- May 2019: -33.3% (purple)

- May 2018: -31.9% (brown)

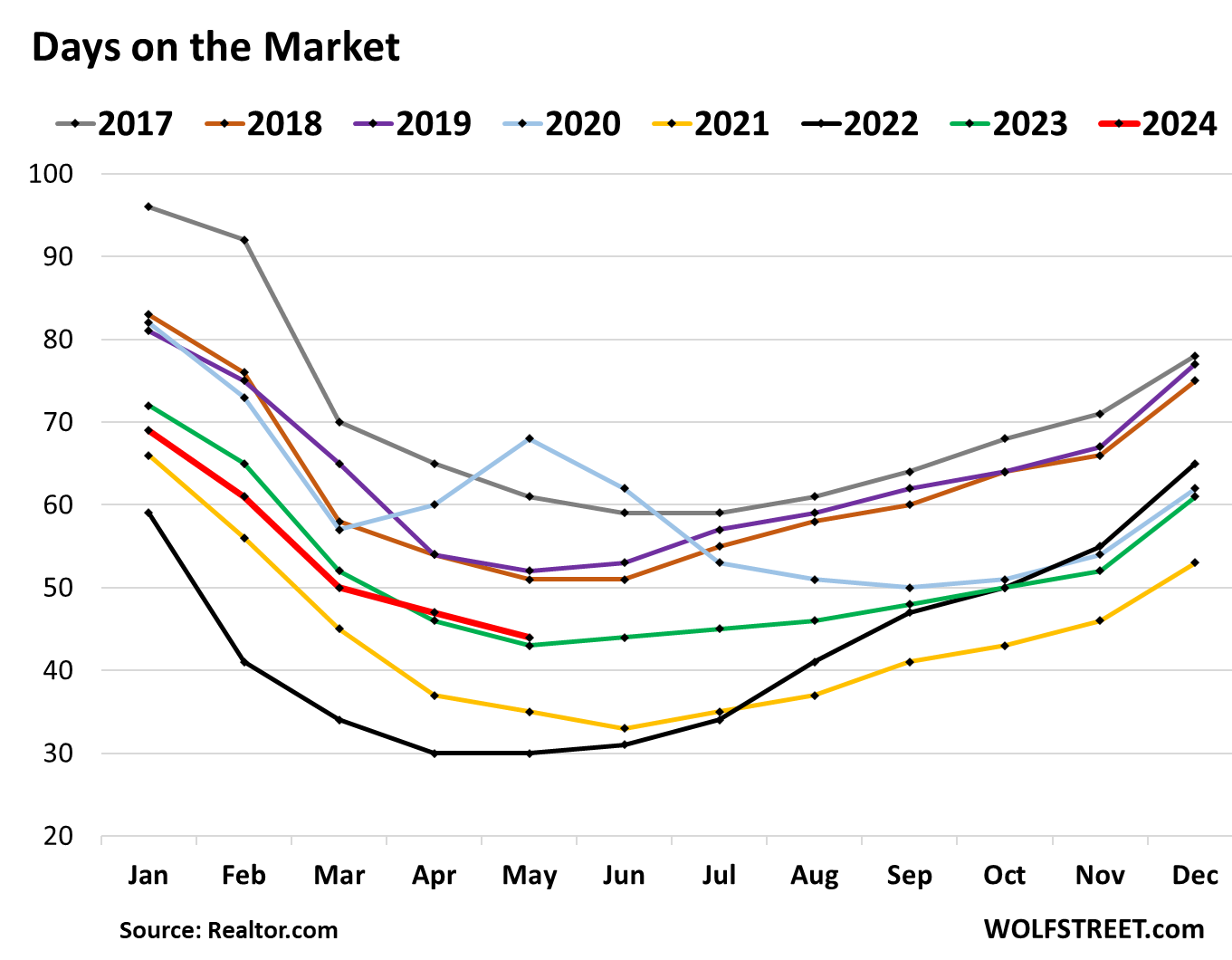

Days on the market – until the home is either sold or pulled off the market – at 44 days, was the highest for any May since 2020.

This metric is a function of two factors: How quickly a home sells, and how quickly it gets pulled off the market if it doesn’t sell (data via Realtor.com):

The median price was skewed by a surge in sales of higher-end homes.

According to the NAR, despite the overall decline in sales, the high end was hot:

- Sales of homes of over $1,000,000: +22.6% YoY

- Sales of homes of $750,000 to $1,000,000: +12.9% YoY

- Sales of homes of $500,000 to 750,000: +6.9%

- Sales of homes $250,000 to 500,000: +1.0%

- Everything below fell.

So the mix of homes that sold changed toward the higher end, with relatively fewer sales in the mid-range to lower-end homes.

The median price is the price in the middle. And this shift in mix of what sells toward the higher end pushes up the middle of the prices that sold, and thereby the median price. This is an infamous shortcoming of the median price. We discussed the mechanics, including a chart, of how median home prices are skewed by changes in the mix here.

The median price of single-family houses jumped to $424,500, amid that surge in sales of high-end homes that skewed the median price and shifted it higher (see our detailed discussion of how that works here). It eked out a new all-time high, up by 0.9% from the prior high in June 2022:

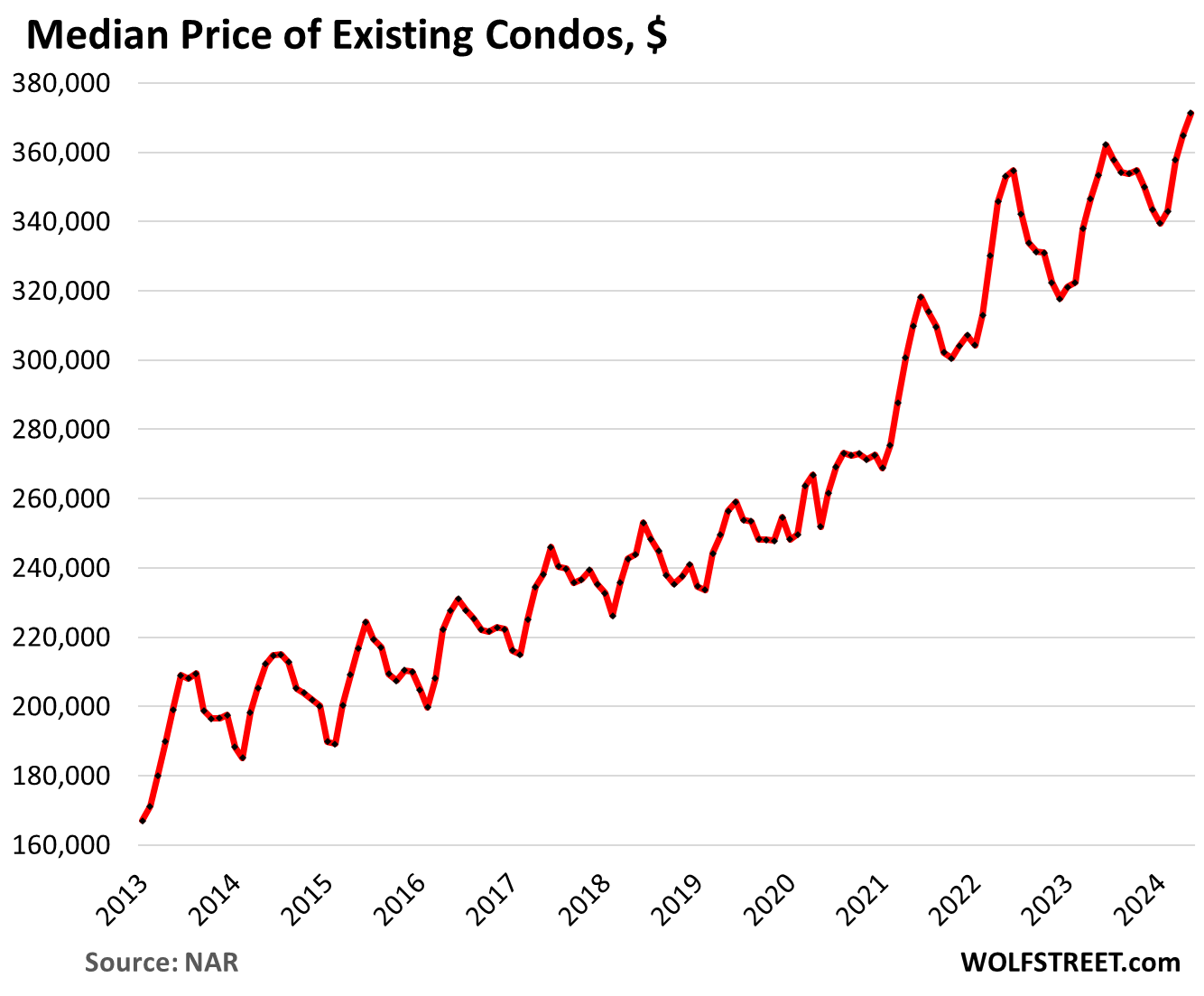

The median price of condos and coops rose to $371,300, a new record, amid similar shifts in sales to the higher end of condos:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Seeing a bunch of new listings in the last 2 weeks. Seems like each one is more overpriced than the last. Something got to give…

What we see a lot is that they put the property on the market at an aspirational price, and instead of cutting the price when it doesn’t sell, they’ll pull it off the market after a few weeks. And a few months later, they put it back on the market at a lower price; and if that doesn’t work, they try to rent it out or turn it into a short-term rental. Aspirational prices are very sticky. In their minds, people already have this money in their pocket, and they don’t want to give it up. That’s why it takes years to work through this. Housing Bust 1 took five years after it started.

Mr. Wolf’s comment: “That’s why it takes years to work through this. Housing Bust 1 took five years after it started.”

Perhaps this Federal Reserve strategy to avoid a correction at all costs will build up strain in the system to the point it ruptures like a major earthquake fault with nothing to hold back the financial mega tsunami. The poorer the country gets, within reason, the richer the average citizen becomes as they will have the same subsistence level finances, but the rich overlords will have less money to compete and drive up prices for the serfs.

2 houses sold in our neighborhood (SoCal) recently. 1st house bought in 2019 for ~0.7M. Sold for over a 1M. Sat on the market for 7 months. Price reduction 70k. 2nd house bought for 1.2M in 2022 and sold for 1.2M in 2024. (Lost money due to transaction cost). Btw., we just lost our home owners insurance dur to fire risk score and we couldn’t get new insurance other than the fair plan which costs 3-4times more. WTF.

just took contract on lower end home

there are a few buyers

they put in $10k in buy down of mortgage rates

The Federal Reserve has no such strategy of avoiding a housing correction at all costs. Your scenario is built on a faulty premise.

This FED is trying to achieve a soft landing in inflation while not driving the economy into recession, but that doesn’t imply anything about housing and other asset prices.

Wolf is right. It will take five years. Be patient. Save up any money you can, and when repos start showing up, slap your money down. They will start showing up to the point that they will be like confetti. It will happen.

My father bought a 1450 sq ft house in Titusville, Florida for $45,000 in 2008 and gave it to my sister. The house was built in the ’60’s and my sister did the basic remodeling of the kitchen, bathrooms, new carpet, etc… In 2021, she sold it for $315,000.

I’ll collect rent – but really don’t want to sell

rather have income

Housing bust 1 only took 2 years for the price to reach top to bottom. That’s not 5 years. The median price home over the last three years has effectively plateaued. Outside of new home, which had tons of built in profit margins, home prices are not falling. What’s going on these days doesn’t look anything like HB1. As you very well know, it will take a recession to do that which is nowhere on the horizon.

GuessWhat,

Case-Shiller 20-City Index:

Top: August 2006

Bottom: March 2012:

Duration: 5 Years and 8 months

I read all the doom and gloom about housing but a house in my neighborhood just sold in one week for 19% over listing price. I always check the price per square foot and this house went for $669 per foot. Which is more than double what I paid for my house in Nov 2019.

This is not unusual.

Don’t ask me to explain it. Soon I won’t be able to afford the property taxes and insurance.

The bad money drives out the good money.

I’m seeing indications of existing-home sales supported by interest-rate buydowns, e.g., a home listed at $650k closing at $700k — looks like deal bundling $50k of mortgage interest rate buydown rolled into the closing price.

Not happening like that in AZ. I’m seeing price cuts galore.

The price cuts I’m seeing in our little slice of desert heaven are primarily on properties that have non-correctable defects. Busy roads. Corner lots. Adjacent to stinky waste processing plants and commercial areas with 5:00 AM deliveries.

Might be a coincidence, but two homes listed on a street that has nearly zero traffic combined with killer views sold before they hit the listing service at full sticker. In May. Similar houses on busy (or busier) streets are languishing. Townhomes/condos are in the dead zone.

The higher end homes are selling, those talked about in this article. Lower end (and I don’t mean low end) are the ones sitting longer. That’s what I’m seeing.

That’s called position, position, position

Which area? Phoenix? They are still building left and right in phoenix. Prices are still very elevated it seems. Significantly below the peak but still beyond affordability. At least rents are coming down.

I’m seeing price cuts all over the state. I’m in Scottsdale and seeing good houses sitting on the market for a long time. I sold my Desert Ridge house two years ago and seeing price cuts there too. I’m seeing most of them on my Redfin feed. Huge price cuts up in Yavapai County, Prescott/Prescott Valley area especially. Yes, prices still elevated in parts of Phoenix metro but seeing many more signs of desperation creeping in compared to last year with many more price cuts. It’s happening. Need to be patient.

According to Phx Agent magazine, inventory increased almost 50% in Maricopa County in April and is still increasing.

Same here in bullhead city, AZ. zillow has a constant stream of price cuts, even new builds are cutting prices. More and more houses available for sale. My realtors not sure what to think but houses aren’t moving and he’s not happy. Says, high interest rate is a killer.

Should have this fixerupurrrr up soon, see what happens RAT

Wow keyboard warriors came out today. Real estate is all about location, location, location. There is only so much beach front real estate, and everyone wants it.

Areas where regulation seem to be stronger and areas with limited building space (SoCal and New York) seem to be holding up better than areas like Texas and Florida which are building like crazy and in areas like Texas, they can keep building in any direction.

I just bought a home 3 weeks ago, short sale but multiple offers on the home because it was below the median for the area. People were fighting for the home because of the location, and school district. Just started remodeling too, and I’m hearing from multiple JC ‘s that retirees are remodeling because they are choosing to retire in place other than a nursing home. So good luck everyone in So Cal, homes are building up here, but mainly overpriced homes or luxury.

Totally great point. NY & SoCal have less useable land, so land is more valuable and property has higher demand. Texas you can build anywhere, so land is cheaper. On Zillow I see almost no homes over $5 million in Texas solid recently, but 1,000s of $5 million+ homes have sold in Florida, NY & California.

Superb analysis as usual.

Where I live near Denver CO, there are mark downs on almost all properties except in the most desirable high demand areas. At all price points. And homes are taking longer to sell.

The wealth gap continues to get wider and wider.

Wasteful non sequitur of a comment.

I don’t think it’s a non-sequitur at all. The fact is that wealthy people are trading homes like baseball cards as the overall number of home sales continues to drop. Relative to history, the ratio of sales vs traffic is extremely high, despite the low number of listings. Why is that? Pocket listings that never make it to the MLS. The majority of first time home buyers in California are 49 years old or older. In 1980 that number was 32 years old. There is something to be said about what David brings up — monied older generations are doing the vast majority of the buying, not as actively through the MLS as it used to be in a healthier economy.

As was yours.

Muss,

Yes, I noted the irony as I was typing that.

Probably the best “noter” of irony here. None better, even if he only picks up on it while typing it…..an insignificant fault, to be sure.

I still haven’t picked up on it…..but that’s nothing new.

“Wasteful non sequitur of a comment.”

Narcissist much?

Nothing goes to waist in the wolf sphere, even a wasteful non sequester of a comment gets consumed and tossed about.

jeffd, you are right. it’s not just homes being traded like baseball cards, but stocks too. does anyone actually think the top 1-10% trading stocks back and forth at higher and higher valuations is actually increasing the country’s wealth?

Jeff D:

1980 was a different world from 2024. At that point in time, there were more traditional households being established vs. today. Today, marriages are occurring later, if at all. Singles find it tough to accumulate enough savings to plunk down on a home.

https://www.census.gov/content/dam/Census/library/visualizations/time-series/demo/families-and-households/ms-2.pdf

“Nothing goes to waist in the wolf sphere”

I disagree. The beer I’m drinking from Wolf’s mug is certainly going to my waist.

MM – consumed and sequestered, there…

may we all find a better day.

I no longer live in Colorado but I’ve been still keeping an eye on it. The price cuts I see are basically a joke. 5k reduction on a 600k home. All that is, is comedy.

We are visiting Colorado right now, for about a month long stay, and have been watching some area housing prices for several years. To state the obvious, housing prices are nuts. We see these small price reductions and keep moving — we are waiting for about a third these prices or less. Probably that day will not come until people realize the air quality issues will make for misery later in life. It’s hot, feels like the desert, where we are (Fort Collins). I think this trip between the heat and ozone warnings, has convinced me that we would rather stick to the catskills in NY for our summer home. Or our RV so that we can easily move to higher elevations when needed. Our primary residence is Florida. I swear it feels hotter and is definitely much dryer, not in a good way.

Unfortunately the brown cloud really took over the Front Range there in the early 90s. Coincided with the beginnings of the huge real estate boom too – shoulda been buying instead of bailing for air quality… oh well. ;-) Locals tell me it’s better now but I have my doubts w all the expansion…

Your RV will not save you, Tina.

Maybe nothing will give and prices will go up forever. What evidence is there that wealth inequality might ease in the future?

Isn’t it more likely that as the national debt grows out of control that current capital owners will simply use their nominal gains from existing capital to buy more real estate assets, further driving the prices of homes and rents up? Interest rates won’t change this. I’m not telling, but genuinely asking as a young man born with low capital. What is the alternative to the 1% eventually losing their heads?

The rich asset holders will sell to debt-strapped middle-class folks right before asset prices collapse…

I actually think the rich are equally enept at understanding when assets are about to crash as everyone else…. however they just lose a bunch of paper money while poor people die during a recession.

Hyperbole?

Wealth stratification is a legitimate concern—let’s not blow it out of proportion.

DDTM – what’s not out of proportion? U mean when 50% of the population barely has a pot to piss in and is working paycheck to paycheck?

Don’t get me started on the other 75% of the world population that doesn’t live in the US… Been there and seen it – not pretty. Let them eat cake or what? Sheesh.

…supply and demand. Like it or don’t, our spacecraft’s stores are subject to the relentless, and ongoing, appetites of we, it’s technologically-burgeoned crew-more and more often reflected in our scorekeeping (see Darrin’s first paragraph, and consider friend NBay’s commitment to the job of downsizing, YOLO’ers, of course, will disregard)…

may we all find a better day.

A good way to go broke is to try and time the market.

With that said, the current “wealthy” geezers will eventually die. If they have heirs, that younger generation will benefit from any wealth transfer. That is if the geezers don’t get sick or pay someone to manage their money (which they somehow manage to transfer into their own pocket).

There’s always been a wealth disparity throughout the history of man. It’s just that people are more aware of it….. they think reality TV / TikTok is reality.

Median prices are up only because the rich people are the one’s buying

If you require a mortgage, you can’t afford to buy.

Happy hour at the bar

Put that on my tab Jenkins, I’m a little tight this week.

Now with everyone on the “pay you later” plan, the bar is close to closing down because of lack of funds in its tills. But in the back room, lefty prints up a quick 10 grand and heads to the liquor store to stock up. The drunk sailors will be arriving soon.

The point I’m making is that 34 trillion in debt, printing money and the end of the line for this poorly run casino makes one thirsty.

Home prices are at bargain basement levels and sooner or later the buyers will figure it out. Prices should double in 3 years or less when the buyers figure it out.

🤣

Since you’re self-professed in the Toronto area:

Would it be possible to get a graphical breakdown of supply by the price ranges you have in the sales section plotted over the last few years? This is probably a big ask, just curious what kind of wizardry can be done with the data you have. Thanks for this update and for reminding readers of the shortcomings of the median prices.

House prices are up 150% in 10 years. Stock markets are up 100-150% in the last 5 years. US national debt is up more than 100% in 10 years. Impressive. Keep printing money to pump up the stocks and asset prices. How long they will be able to do it? Hopefully sanity will prevail at some point.

What’s really impressive, in a dark way, is how they printed so much money that the bubbles persist years after they stopped printing.

Of course it doesn’t help that, in terms of aggressivesness during tightening vs. easing, they did the equivalent of running a Lamborghini up to top speed and then trying to stop it with their feet like Fred Flintstone.

More like rocket fuel and one of those funny car parachutes they put behind them. Lambo isn’t going to the moon

That’s because 10% of the country is now, “nosebleed rich”, meaning their wealth is so far above the general population that they literally don’t care how much they pay for *anything*. The pandemic “error” of dumping $10 Trillion into the money supply over a two year period, just to end up in the hands of this already wealthy 10%, allows these people to make “pay whatever”, even for purchases as large as homes. An extra $100K or $200K over asking for a house they want? Who cares! They have an extra $1.5 million of equity in their asset holdings. These people have no clue (or care) what their spending patterns are doing to the lowest 50% of earners.

Moreover, it’ll take a generation or more of this money-is-no-object cavalier spending to finally burn through most of that froth and reset things — and that’s assuming another gravy train doesn’t come blasting down the rails without any brakes before then.

That’s why, at this point, I’m in favor of seizing the assets of all billionaires. “Sorry, you cheated. Buh-bye.” It’s time. What they did is filthy beyond words.

i agree that’s what’s happening. it’s also why even prices of pizzas have gone from $16 to $24. there are enough people who are just willing to pay whatever. but you don’t need to confiscate billionaire’s assets. all you need to do is pop the world wide asset buy everything bubble and the wealth effect spending jeffd describes goes away.

I just saw my first Cybertruck in the wild, at a campground. They probably weren’t concerned that camp fees have increased from $10 to $30 in the last decade. Ditto all the people with the latest $100k super ultra heavy duty tanks towing a mobile home, the trucks parked sideways to fit in the driveway. The mobile home had 4 side extenders and more sqf than a condo. It somehow also pooped out a two person motorcycle. The unlocked titanium ebikes on the lawn complete the look. They never came outside because it was 80 degrees and 40% humidity, so you know, must have AC set to 62 to keep the fat from melting.

Ok, I’m done. Glad I brought edibles.

If I recall, “Let Them Eat Cake”, comes to mind.

Adam, the printing has stopped some. Wolfman has been reporting about the reduction in the Federal Reserve balance sheet. And the Fed Funds rate is around a 22 year high.

Granted, the Federal Government is projected at having a $1.9 trillion deficit this year which includes about $150 billion for student loan forgiveness.

Right now the debt to GDP ratio is around 122%, compared to 100% to 105% from 2013 to 2019.

I hope interest rates go down so federal debt service is no longer greater than the Pentagon budget.

I hope both political parties can come to a consensus on spending and taxes to at least reduce the deficit to more sustainable levels.

“If something cannot go on forever, it will stop.”

― Herbert Stein

They will keep doing it as long as they can. The only sanity to prevail will be Mother Nature nipping this all in the bud.

Here is what I am seeing from boots on the ground and then my amateur analysis.

I am getting more calls, text, postcards, and fake written check offers for my rental properties now than ever before. Even during the 2021 year.

But I do seen inventory creeping up and people talking about how the FED is going to cut rates and mortgages will be cheaper later this year.

My take: Home buyers are holding out for promised lower rates to buy but investors with cash are trying to front run the rate cut. Mortgage rates do not matter to them if they are paying cash. I am guessing they think if rates drop, there will be a rush to buy houses, inventory drops, and price go up.

I may be totally off base but that is what it feels like in my neck of the woods. Mortgage rate cuts was all my sheet rock contractor could talk about is the upcoming mortgage rate drop.

Most of these callers I think are lead finders for investment companies. Everyone says if I am interested in selling, they will have someone call me back and they will make a cash offer within 48 hours. So, the person who called and I am talking to has no authority. Lots of calls sound like call centers and young people.

I’m not so sure the investors have the purchase prices in cash.

If they “know” that rates will drop, then they may well be planning to refinance/sell after rates drop and prices soar. As long as they can deal with the cash burn between now and then, it’s all good.

If rates don’t drop, and prices don’t soar, they may be on the hook, but such is life.

I’m just not sure a 5.5% mortgage is going to create a rush of new housing demand at these prices.

I’m thinking the ten year falls 75 to 100 bips Max over the next year so 5.5 would still be the lower end of rates based on that estimate.

Plus I’m thinking the market will lower rates more then the Fed will so it’ll be uneven and with lots of push back on lower rates from the Fed.

Good point, and I think if sellers (including home builders) are motivated to sell then they can offer to buy 4 discounts points to lower the buyers mortgage from 5.5% to 4.5%.

Let alone they can let the buyer assume their VA or FHA mortgage as well if it is worthwhile (i.e., the 30 year rate is less than 4.5%).

From what I’ve seen of various data, seems like the locked-in 30 year mortgage rate was around 3% when prices peaked back in early 2022.

There definitely was a mad rush or mania to buy from late 2020 to early 2022.

the 10 year and the mortgage rates have already dropped based on rate cut projections. i think the rate cuts will cause a drop in short term rates, but leave the 10 year largely intact. i don’t see the 10 year dropping back to 3% anytime soon.

Too many people still betting on rate cuts. If they cut rates the attendant inflation will make the assets worthless all the same. Just not in nominal terms. You just won’t be able to convince someone to trade their time and energy for what you have anymore.

Everyone is hoping for a rate cuts because fed has conditioned them.

Fed is itching to cut rates and is trigger happy at tgr moment for rate cuts.

Fed declared victory over infllast Dec.

Only if Fed has been firmer about inflation not dying down and be very clear and hawkish .

“inflation will make the assets worthless” .. that is literally the opposite of inflation though: assets are worth more.

Not sure what the time & energy part is? If you have a nice home for rent or sale, and someone wants to live there, then of course they put time & energy into obtaining it.

his point i think is that if you continue debasing the value of labor, people won’t be willing to trade it for cash. that’s what causes a crack up boom.

Have you ever tried to price a service where no one can afford to live? How things turn to dust from deferred maintenance? How hard would it be to commit to a year long project when your input costs may double tomorrow? Would anyone lend you money if they might get less back in real terms? Can anyone really upkeep or effectively utilize any asset with high inflation?

You may love the nominal asset price but when your insurance rates, property taxes and maintenance costs effectively double are you still happy? Will you still be able to afford to live there?

Any investor worth his salt would buy bonds, not houses, if he thought rates would decrease.

No logical investor is going to disregard opportunity costs.

Buying houses vs. bonds you bank on accelerating currency debasement.

The trick is to ignore quality deterioration for CPI calculation. Look at furniture, clothes, cars, flight services, food or homes. What used to be an average 50 years ago now commands a 50-200% premium.

Pocket listings are the new “thing” in real estate. Most of the real estate investors I follow also have a brokers license.

Pocket listings have been around since Moby Dick was a minnow.

Prudent buyers always pay cash that way you never have to take out house insurance because of a mortgage.

Prudent buyers don’t purchase insurance?

Your definition of “prudent” and mine are diametrically opposed.

“But I do seen inventory creeping up and people talking about how the FED is going to cut rates and mortgages will be cheaper later this year.”

They have been hoping for a couple of years now. I don’t think lower rates alone will cause a frenzy again in real estate. I believe price matters to many.

Good to see for sure, although in looking at selected market in SoCal like Ladera Ranch or south OC, it definitely doesn’t feel like there’s any slow down and people still tripping over themselves buy overpriced tiny houses..

Guess for SoCal, will just have to see how this Mexican standoff will unfold, who’s going to blink first. Majority of folks out here still think rate cuts is right around the corner, inventory will be low forever and the next boom by year end..I personally just can’t make any sense of jt…

Not all of Southern California. Here’s L.A. County, por ejemplo, roughly back where it had been in May/June 2021:

The situation in neighboring Orange County is insane,

Howdy Folks. Most other headlines just quote ” Home values rise again”, NO mention as to why. Truth, by the Lone Wolf, again today……

Plenty of us know why. Only fools get their financial news from corporate media

Why have people been so conditioned to interest rates when it’s price that’s the real culprit. Do the math.

Howdy David. Most people in our country were ZIRPed to stupidity.

OR, most people were NARed to stupidity. Houses are the best investment/prices never go down/now is the best time to buy, that sort of thing.

Howdy Louie YEP agreed. Those same silly folks don t even know they were made prisoners of their own home…. HEE HEE

Turns out all the stupid people that have been NARed have done quite well, while the smart folks have missed the bus. It’s actually even worse than that. Some smart folks could possibly be screwed for life because they refused to be NARed in 2019.

A two year old can figure out that homes go down in value. All one needs to do is review a Redfin listing and look at prior sales data on older/existing homes. What is potentially masked in that data are improvements to the property…. and those need to also be considered in the “prices never go down” equation.

Anyone who relies on a single source of information to make a major financial decision pretty much deserves what they get.

I’d be a big buyer in Fort Wayne and Indianapolis, Indiana. The return should be better than the T-bill rate.

It’s truly astonishing, and it’s not just the average idiot on the street. People who make their living writing or speaking about finance and the economy can go on and on about mortgage rates but never so much as mention the bright orange rampaging elephant in the room.

This has been a phenomena forever. At least in the U.S., people are payment buyers. Rarely do they ever calculate the total cost of the purchase (principal and interest) nor do they really consider the purchase price…. just if they can make the monthlies.

I was going to answer this but it dawned on me that your question surely must be rhetorical. I mean we all know people for whom numbers might as well be letters from a long forgotten language

All I see is higher supply, lower demand, and the prices are still going higher. That’s not the economics I learned in university and will lead to collapse.

New home prices are lower than pre-owned

The only thing sustaining the higher pre-owned prices is the lack of inventory. Once inventory goes higher, prices of pre-owned homes will have to come down.

Inventory would only go higher with recession leading to unemployment

Probably not on a per-square-foot basis. A generic number for “price” is often misleading, as this article shows.

1. “Probably not on a per-square-foot basis.”

Not on ANY basis. What Bob said was not correct, and you should have called him out on it. He may have mixed up something here. New houses are more expensive than resale in the same market, but with mortgage-rate buydowns from the builders’ mortgage companies, the payment can be lower. HUGE difference. We’ve discussed this a lot here.

2. A generic number for “price” is often misleading, as this article shows.

A national per-sf price is a BS number because there are homes in San Francisco that are a fraction of the size of a McMansion in Tulsa, and cost 10x as much. Same in San Diego and Oklahoma City, or Orange County and Omaha, or New York City and Detroit, etc. Per SF is only NOT misleading when it compares sales in the same neighborhood.

“Prices” are always subject to the vagaries of the sales mix. Median and average will rise if the sales volume mix favors the higher end properties. This confuses the math challenged as they think the price of their home increased as well, not considering the fact that properties in their price range are frozen and the higher end properties, where the cash buyers flock, that are in good condition, location, etc., are the bulk of sales in their zip code. None of this is rocket surgery.

On the charts that have monthly data points, but a yearly legend due to size, can the current month “dot” be modified to a different shape/color along with the same “dot” markers for previous year? That way it’s easy to determine which point in previous years is associated with the current month. I love your data, but this is one thing I’ve always wished for.

Great article, as always! The active listings number starting to trend upwards is good news for those hoping for future price discovery. It just may be a while until people who might own a home but not be enamored with it to make a move if they have a low interest rate, but data supporting the “top” being in will help with that motivation. Time will tell!

We’re getting closer to the “sell now of be trapped forever” phase of the “buy now or be priced out forever” boom/bust cycle.

It will be long, slow, brutal, and heart-wrenching to watch even though people are bringing it on themselves…

Nothing changed from the last time.

You could watch the irrational exuberance all the way to the top when people were paying double what a home went for two years prior.

Then you started to hear the same dumb talking points from the crowd who thought they were smarter than everyone else.

“It’s different this time”

“Buy now or be priced out forever”

“There’s a shortage, homes can never go down”

It’s like Americans learned nothing from 2008

”It’s like Americans learned nothing from 2008”

No, people over the world learned nothing from 2008

Anyone who bought at the peak prices in 2008 has seen their property value rise drastically.

So clearly the lesson to learn is “even if your timing is wrong, holding for the long term will fix that mistake”

over 15 years, sure.

After 15 years of ZIRP, QE, and endless money printing…

Not everyone got their equity back. I know someone in Brookfield, IL who bought in 08’ and to this day has not broken even on his purchase. Same for my aunt who bought in 2002 near Orland Park, IL and sole in 2022. Didn’t come out with a lot of equity

Being trapped and priced out could the next shoe to drop…weird casino where you go shoeless.

No one is wearing shoes, this place has stickers.

I think Next is right. Jingle mail coming soon….or will it take 25- 30 years of normal rates for the 30 year fixed low rate terms to work their way through the market? And an above comment stated RE increased 150% last 10 years. The local guys in my neighbourhood trying (and failing) to sell are holding out for their 400% for the last 5.

Wolf used the term aspirational price setting. I had never heard that before and it is bang on. Delusional works, too.

Let’s just drop rates and rehash this bs about low inventory once more. We just eclipsed 2020 numbers and even those were about 400k-600k units off of norm.

Gfc, people lived a champagne life on a beer budget. Today investors control housing at higher rates than ever before.

Maybe if folks reviewed local rents, they could rationalize a floor price. Also, buying new can be advantageous if you live in a state where home building occurs. Finally, your dollar is 25% less valuable than it was 5 years ago…

“Today investors control housing”

They don’t control anything about it. Sheesh.

In my mind, this is about a buyer and sellers strike.

The mortgage rate isn’t that big of deal, with home prices at the current level, obviously, because most average people don’t have the income to play this game; the decline of rates by a few basis points is meaningless for someone that can’t afford a $400k starter home.

On the other side of coin, sellers within the last 5 years, have bought expensive homes, then poured money into beautiful upgrades, pushing overvalued homes into money pits that nobody can afford.

As inventory grows, sellers are trapped in money pits that are disconnected from buyer reality. It’ll take years to find a true balance

One problem might be that you and by chance the general buying public now perceive that $400K is a “starter home.” The fear is that this shift/distortion in the perception of the value of things — especially when taken against the sheer amount of (ultimately finite) time and energy one must invest in order to generate the necessary capital — seems permanent.

Precisely. As American capitalism continues its cannibalistic trajectory, the pool of people who can afford anything at all continues to diminish. The rich commenters here will disagree, for their wealth blinds them.

I was reflecting on a time when I was offered a “promotion” to move from the Northeast U.S. to our California corporate office. I went there a day early and looked at the real estate situation – and this was back in circa 1990.

I would be trading a 3,200 square foot home on a half acre lot with great schools and reasonable property taxes (sold it not long after for $240K – 3.5x’s annual income at the time) in Bucks County for a 1,000 square foot termite bitten, three closet sized bedrooms, one bath and a one car garage – which is where the laundry was located – home on a crawl space, situated on a luxurious postage stamp lot with mediocre schools with a price tag of 2.5 x’s our existing home (10x’s annual income). Taxes were also more than double. This was not some fancy beach town nor OC paradise…. it was in the citified portion of Torrance. Long Beach wasn’t much better – just a longer commute. Orange County? Fuggedaboudit.

These price disparities have existed for decades and decades. Some think it’s a recent phenomena, but it’s not. I passed on the “promotion” as there was no way in heck that it penciled with a stay at home wife and two young kids, despite owning the PA house outright – which would have given us a substantial down payment. That financial insult plus the deterioration of lifestyle wasn’t appealing at all.

Wolf,

Do you have any of these charts that are inflation adjusted?

That would be very interesting.

Adjusted for what kind of inflation? Wage inflation? Asset price inflation, such as stocks (use the S&P 500 index as deflator)? Food CPI? Motor vehicle CPI? Wholesale inflation? This site is full of inflation measures. You can pick and choose.

Home price inflation is one form of inflation. So now you adjust one form of inflation (home price inflation) by another form of inflation (consumer price inflation), and the result is what? All it does it shows which form of inflation was bigger.

If you want to measure “affordability,” you can adjust home price inflation to wage inflation, which makes some sense.

But adjusting home price inflation to consumer price inflation makes no more sense than adjusting the S&P500 to consumer price inflation — though obviously you can do anything with a spreadsheet, and people do it, I guess to find out which inflation was worse?

Absolutely top notch answer, Wolf.

Everyone should hammer this comment into their psyche as they go about their day.

This train is so far off the rails that its a multiverse of relativity that is custom to each individual.

Most of all of us are not worth tens of millions of dollars and therefore you ought to be hunkering down in every way you can.

Drive your car slow and gently, God forbid you need to buy a new one or repair it.

Keep your health in tip top shape, God forbid you need medical care & have to further interact with insurance and the games they play.

Keep on top of the condition of your home, God forbid you need to do major repairs, have you seen what it costs to redo your roof ?!

Lots of good people who don’t deserve it are going to get hurt in the coming years.

DONT LET IT BE YOU AND YOUR FAMILY.

Jim Grant (of Grant’s Interest Rate Observer) was talking about this.

He basically described how 2% inflation targeting is 2% annual currency value destruction.

He also talked about how in the 18th and 19th centuries inflation was followed by deflation, and currency values didn’t change on a long term basis.

Now inflation just goes one way because government policy is to slowly destroy the currency (and hurt the holders).

The discussion was interesting because targeted inflation helps to herd investors into assets, which obviously benefits certain parts of society.

As he explained it, everything is a game of getting into assets which are inflating faster than CPI is inflating.

That is why these inflation adjusted charts are interesting.

What do you think?

Deflation is worse than inflation because it is much harder to leverage assets to grow the economy. This inevitably leads to instability and bankruptcy. The late 19th century was one depression after another. It was so bad that at one point the government of St Louis was overrun and a socialist republic declared. Deflation in theory is much, much better than deflation in practice.

Credit default is always deflationary and absolutely necessary to clear the excesses, speculative manias, and capital misallocation from the market. Incompetently run systems must lose or the distortions will start killing people as certainly as credit collapse. The pain of periodic credit default is much less than the alternatives. Deflation caused by increased productivity is an absolute win and never bad.

The term “inflation” is being conflated with another: escalation.

Inflation: an economy-wide increase in the average price level. Escalation: reflects changes in the prices of specific goods and services.

Transactions are down. In the flyover areas prices are rising faster, starting from a low base in 2011/12. Renters turnover is rising. In safer areas, where vacancies are rare, the waiting list is long. Good prospects are bidding 10%/20% higher. The owners are able to cover their monthly expenses. Those houses, especially small ones, are snapped within days. New immigrants with no history or credential are packed like sardines.

I’m sorry, I can’t understand your posts unless they are numbered bullet points!

Oh dear, these poor rate cut fantasies are about to get dashed…

The big reason for rate cuts, is a recession or the fear of a recession. As you know, from 2008 if one kicks in, as Wolf showed, prices can fall for five years. Central banks don’t tend to cut rates into a boom, unless they go into blind panic mode as from 2018 to 2021……

IMO, price per square foot is a better metric than total price when looking at house prices.

Could it be that sales of homes priced below $250K are down because prices have risen so much that in many areas there is no such thing as a $250K house? Ditto for $250-$500K in places like San Jose or Boston.

Very possible. Seems at least in the markets I watch (Central FL primarily), anything <250K is either an old mobile/manufactured home, or a bulldoze-worthy site-built home that's had hoarders or rodents (or both) as its occupants.

I will say that I've seen a small up-tick in auction listings and foreclosure listings in the above price range, recently.

dtj,

“…homes priced below $250K are down because…”

1. Lots of homes for sale at $250K, nice homes too, in places like Tulsa (50% of the homes that sold had prices BELOW $206,000) and Oklahoma City (50% of the homes sold had prices BELOW $206,000). Those are fairly big metros — metro of OKC is over 1.4 million pop, Tulsa metro is over 1 million pop. Nice city too, highly recommended, used to live there, basically grew up there.

2. I didn’t specifically mention homes below $250k. The lowest range I mentioned specifically was $250-500K.

3. Look at the yoy % increase in sales of the high-end homes — even as overall sales have fallen: over $1,000,000: +22.6% YoY, $750,000 to $1,000,000 +12.9% YoY. These are massive sales increases in an overall declining market. So a little bit of the increase may be price drift, if there even was any, and the rest is the shift in mix.

That is interesting. So do you think that it will be LUXURY home sales that ultimately decline and cause the entire bubble to burst because right now the high-end homes are keeping the numbers seemingly afloat?

Do you have a chart of home price values changing in the categories you mention, 250-500, 500-750, 750-1,000, and 1,000+? That would likely show maybe 4 different bubbles bursting at different rates.

“Do you have a chart of home price values changing in the categories you mention, 250-500, 500-750, 750-1,000, and 1,000”

So what I’m trying to explain is this principle of how shifts in the mix change the median price even if actual prices don’t change.

I explained this in detail here:

https://wolfstreet.com/how-median-home-prices-are-skewed-by-changes-in-the-mix/

Quoted from the piece:

To illustrate the principle of how a change in the mix skews the median price, we look at our illustration market where 11 homes were in inventory at the beginning of the month, and 9 of those homes then sold.

The median price is the price in the middle of those 9 homes that sold. To get the median price, we make a list of the 9 homes that sold in order of price: The price of the fifth home from the top (or fifth home from the bottom) is the price in the middle = median price.

In the left column, the bottom nine homes sold (blue), and the top two (black) didn’t sell. The median price is the price in the middle of the 9 homes that sold: $400,000.

In the right column, we see the same homes, same prices, but the top two higher-end homes sold, while the bottom two didn’t sell. So this shift in mix shifted the price in the middle (median price) up to $500,000.

In other words, the median price jumped by 100,000 though the actual home prices did NOT change. This is one of the infamous shortcomings of median prices — that they’re skewed by changes in the mix.

I see the same here. You cannot buy a 250K home. They do not exist so sales are by default down. You can buy a 250K lot and build a 500K home on the lot.

It is my limited view while living in an overpriced market.

Today I read a listing for 400K, which the agent described as “affordable.” 😂

Maybe “practically free” would have been a better adjective? Because that’s what $400k is in a whole lot of the country.

So many people lack perspective, and think what’s affordable or unaffordable to them is the case for all.

That 400 thousand people pay for the house, that much money with interest included gets you a place in the zoo by the giraffe and the koala bear.

I can only afford to live next to the muskrat and the weasel.

Many houses are priced correctly, with the higher prices of construction, land….everything.

Prices could be most comfortable where they are.

Those $250k lots will be $25k when all is said and done. You can’t even give some land away after a bust. It’s purely a money-suck through taxation.

My boss who is french bought an apartment in Chicago for 85k, 90 m2., at the coast of the lake.

By the way in Chicago there are plenty of properties under $200k. In some of them you can move in and live, in others a light refreshment is needed.

And an armored personnel carrier.

I am guessing that El Katz has never been to Chicago and gets his need from sources that take advantage of his ignorance.

El Katz is correct. I live here. Only bad neighborhoods have the deals, and it’s not even a deal when you can’t even relax by your own window inside your house or sit on your stoop. The cost of living in Chgo is HIGH,

Unless you choose to live in a war zone

In my little slice of flyover, I have no issues finding a house for 250K.

Who is buying @ 250K?

Sure wages have increased. Not in the same league as groceries, day care,

property taxes & insurance.

And that brings to mind another variable, property taxes, as Chicago/Illinois has high property taxes (as do New Jersey and other areas). If taxes are high, that can put downward pressure on prices relative to neighboring areas with lower taxes.

Chicago and NJ with high property taxes?

Just for fun I picked a random house for sale in Highland Park at 102 S Central Ave, Highwood, IL 60040 for sale at $450k. The annual taxes are $9384 and insurance is $1236 for a total of $10,620.

I picked a random house in San Antonio, Texas at 311 E Ashby Pl, San Antonio, TX 78212 for sale at $449k. The annual taxes are $9972 and insurance is $4212 for a total of $14,184.

Low tax Texas? NO. Skyrocketing taxes and property insurance together with poor infrastructure and a low quality of life.

Unless you don’t have an income, that’s not a comparison. Don’t forget TX doesn’t have a state income tax either. Also insurance is fairly location dependent, even within TX.

Like a sour note on a piano where could have been a virtuoso.

Why do people flee Chicago, 3rd worst in nation?

Texas the 3rd fastest growing state in the US.

Must be that low quality of life that’s in demand, and no income tax …Texas.

Oh, the poor infrastructure could be the draw?

But wherever you go bring flowers and chocolates and your ace in the hole.

I would guess, as USA property taxes are percentage based, that property taxes are high everywhere that property has boomed.

My son lives in Austin, TX. He lives in unincorporated Travis county with an Austin mailing address. The same house a few blocks away has much higher property taxes than he does. His decision to purchase at that location was driven, in part, by the tax load variation – which is significant.

Few things are lineal…. a little study has to go into property searches beyond granite waterfall countertops.

Not sure where people get the idea that Texas has poor infrastructure. Roads are well-maintained and constantly being upgraded and expanded.

Price per square foot is only relevant in very few instances, if at all.

A home on a lake is worth more than one backing to the loading dock of a supermarket – same house, same builder, same condition. That’s why there’s a thing builder’s use called “lot premium” – which will add to the purchase price, but not to the cost of the structure. The price per square foot does not reflect only the structure, but the land value. That’s how you get an 800 square foot ramshackle shack selling in the millions and a 10,000 square foot custom home languishing at a price half that.

The people who made the most leveraged choice on how much to spend on their house several years ago before the bubble are precisely the ones who have more house equity relative to income right now.

Not surprising to see them repackage their equity and make a leveraged bet on house prices again after their success.

(And skew the mix in the process)

And that’s how you end up losing everything. Markets are non-stationary, and strategies that worked in the past are likely to revert to the mean.

All markets are local- Manchester NH Zillow Price Index up 10.4% YOY. Seeing 2-family multis selling for close to $600k with gross rents of $3400/month. At some point math has to start making sense again!

Have you seen all the luxury apt complexes that have been / are being built in Merrimack along rte 3? I’ve always thought it was an odd location for that type of housing, but hopefully they will help alleviate price pressures in the area.

Just a disgusting, grotesquely overinflated bubble created by the FED. The FED should be done away with. They are a cancer upon society.

The Fed was created to help regulate. Unfortunately, they don’t know what they’re doing.

That depends on what the goal of said regulation is. If the regulations were intended to protect John Q. Public, then yes. It appears that they don’t know what they’re doing. However, if the regulations are to protect the blob, then they’re likely spot on.

The Federal Reserve has nothing whatsoever to do with either the real estate or stock market bubbles, the real estate bubble is already crashing big time in Commercial Real Estate (CRE).

I see you picked the wrong day to stop sniffing bath salts.

yes and no. the fed balance sheet is back to where it was at the end of 2020 but stock prices are like 70% higher and housing prices 20-80% higher depending on market. the current bubble is not based on printing or rates, but about psychology of the fed put. the fed has not done a good enough job convincing people it’s serious this time and won’t be back with the money bazooka.

that’s why investors are willing to pay stupid prices for nvidia shares. they figure even if rate cuts are slower, they’ll be there eventually, and probably back to zero.

not saying it’s true, but that’s what the thought is.

Hmmm…… Literally every first world country has a central bank. Wonder why that is?

When will people realize that the next generation will be in the poor house? Housing price will not come down for the simple reason that dollar has deprecated by a lot and housing price just reflects that reality.

This is the same reason that “Since 1975, it has taken an average of 218 ounces of gold to purchase an average single family home”.

“This is the same reason that “Since 1975, it has taken an average of 218 ounces of gold to purchase an average single family home”.”

This statement is completely meaningless because an average since a specific date (1975) is always going to be some specific number when compared to the average value of another asset (in this case 218 ounces of gold). This statement would be meaningful if in every year since 1975 the average price of a single family home, priced in some specific amount of gold, was say 200 to 240 ounces. That would establish a connection between gold and single family homes. As stated, you’re simply taking the average house price each year, the average gold price each year, and concluding it equals 218 ounces over a 50 year period. So what? That says nothing about the value of gold relative to housing in each of those 50 years.

For example, gold averaged 280/ounce in 2000. That translates to a house price of $61,040 for 218 ounces. Was housing that inexpensive in 2000, or was gold at a low point? The point is that house and gold prices fluctuate significantly and stating the average connection over a half century doesn’t provide any useful data about there being a direct connection, each year, between gold and home prices.

MSN; Will Debt Sink the American Empire?

America is cruising into an uncharted sea of federal debt, with a public seemingly untroubled by the stark numbers and a government seemingly incapable of turning them around.In the presidential race, there’s not much partisan difference or advantage on this subject. Donald Trump and President Biden have overseen similar additions to the nation’s accumulated debt—in the range of $7 trillion in each case—during their terms. The national response to both has been, by and large, to look the other way.History, however, offers some cautionary notes about the consequences of swimming in debt.

Over the centuries and across the globe, nations and empires that blithely piled up debt have, sooner or later, met unhappy ends.Historian Niall Ferguson recently invoked what he calls his own personal law of history: “Any great power that spends more on debt service (interest payments on the national debt) than on defense will not stay great for very long. True of Habsburg Spain, true of ancien régime France, true of the Ottoman Empire, true of the British Empire, this law is about to be put to the test by the U.S. beginning this very year.” Indeed, the Congressional Budget Office projects that, in part because of rising interest rates, the federal government will spend $892 billion during the current fiscal year for interest payments on the accumulated national debt of $28 trillion—meaning that interest payments now surpass the amount spent on defense and nearly match spending on Medicare.

I have written this before. I believe that the “homeowners” that have 3% mortgages will feel the heat when their home comes down to fair value. 30% haircut?

So they take a 30% haircut? It’s only realized if they sell. Traditionally, markets move somewhat in concert so any replacement will be similarly situated.

It will still come down to: Can I replace/improve my situation for a comparable monthly payment? No? Then I keep going in situ. If I can? Then it’s a value proposition as to whether the juice is worth the squeeze.

No decision is lineal.

As a “homeowner” I avoid that problem by not selling.

What I believe just for fun…….I’am reading all these….wait and buy low comments……for your consideration……here we go!

Home prices have permanently been priced higher and reflect a reduction in standard of living in the US. The boys are salivating over international demand when/if the dollar drops and don’t really need a fat middle class in the US to buy all their stuff. They are doing things internationally deliberately to encourage dollar weakness. Henry Ford is dead.

The dollar drop will goose employment in the US so expecting a hard landing that lasts more than a short period…..nope.

The dollar will come under pressure if rates drop driving inflation upward.

The fed has become so highly political I suspect at the first sign of unemployment……lets cut.

This is in addition to the already wage embedded mess the fomc has created. The housing construction industry is already showing slowing so I suspect the fomc will curtail its QT soon.

The millennials want more housing so any reduction in rates will drive demand upward.

Lots of markets, particularly in areas most think are unattractive will remain tight.

Having stated all this there are some markets where opportunities for lower prices exist…..such as Florida, Texas and Arizona. The boomers that moved to these markets and goosed demand after retirement have largely retired……the leading edge of boomers are now approaching the age when death occurs. Lots of construction to fill demand that is fading will be in trouble.

So not only will prices stop increasing, they will adjust downward……somewhat.

Those expecting a 2008 price reduction in housing…..nope…..bankers always fight the last war…..so…….credit quality is far better than 2008. Most people have quite a lot of equity in their homes and most importantly home construction never really got to the level where tons of excess homes were being constructed over family formation.

Bottom line……those in some markets will see a minor opportunity…..others will just wait for no reason.

The Florida condo market is an exception for other reasons and may get a good wack.

Happy to hear others tear this to pieces. Have fun!

i think you’re largely right that they want to damage the currency to fluff spending today. i think the part you’re missing is the civil unrest that will eventually come with the wealth disparity and housing costs where they are.

I want to play a game for bragging rights. Here is a house in a bad school district but you do get 9 acres in the country and this in Wisconsin.

04/29/2024 Sold $375,000

What is the listed price now, 2 months later?

Wolf feel free to take down if you find this annoying or it eats up the thread

Howdy Some Midwest Guy. Depends on too many other factors. Any rehab done or just a quick flip? Newcomers to the Midwest love the lower prices, but the climate is the killer. A/C and Furnace better be in tip top shape…… Misery ( MO ) is the worst……One or the other will be running constantly in Misery…….

Nothing, no rehab, no updates, same cruddy 1980s cabinets and vinyl floor, nothing

Howdy Midwest. OK got it. In the olden days, speculators would purchase Foreclosures, add 10 to 20 percent and flip. Some would caulk and paint and kinda update and flip. Some would go all out and with total updates to the max and then flip. So, during these times????? Just a simple purchase and flip??? 10 to 30 percent more. Will it sell????? If not, speculators would then rent or repair and then flip. If someone pays too much???? Not the speculators fault…….

Howdy Folks would like to mention here about how important information is when purchasing a home. No app will save you. Property History information, mortgage amounts, who , when , where and why…….. Don t worry, the seller will disclose properly….. HEE HEE

Alright no one seems to care, so they relisted 2 months later for 475,000!!!! I’m blown away!!!! I also am ticked because I thought prices in this area when I moved back were outrageous (2019). Now my wife and I probably won’t own a home even though we are debt free and have a significant down payment because the cost to rent is way cheaper problem is dealing with a landlord. Anyway, that’s my rant.

Howdy Midwest. Looks like my 10 to 30 % increase is right on the money. Lots of details were left out. So very important to know everything about a home for purchase. The inspection period of a used home is where $$$$ is lost or gained. A Sale price of a home could have so many numbers baked into it. Seller can pay buyers costs that are hidden in the sales price. Good Luck Youngins, that awful NAR is getting ready to line up for sellers…… Better download a FSBO app ASAP.

“dealing with a landlord”

…a landlord who would have mowed those 9 acres for you instead of you needing to do it yourself. Gotta take the bad with the good.

I only have a quarter acre to mow, but sometimes it makes me miss renting.

Re: “ In the latest week, mortgage rates averaged 6.87%@

The CME fedwatch casino wheel implies rate cuts coming in September, with 60% probability.

That connects with the concept that a recession is unfolding faster, because of various revised data that will arrive around that the September fed meeting.

Although Powell, et al, jawbone no cuts until possibly December, revised lagging data will be newsworthy enough, to shine a light on reality.

Ipso facto, that puts Schrödinger’s Cat in the crosshairs before the election — and probably goosing yields lower, including mortgage rates.

However, the reality of this possibility, more than likely isn’t going to be stimulative in terms of getting buyers excited about taking mortgages out on super over priced homes that are unaffordable.

A series of extremely anticipated rate cuts will essentially reduce interest income that a lot of people have been enjoying and most likely do nothing for housing volume.

The buyer and seller strike will linger with extreme malaise, as buyers remain hesitant and sellers remain entrenched in their money pit moats ( holding out for top of bubble values, amplified by remodeling upgrades that have made overvalued homes into highly inaccessible assets that nobody will want).

Will mortgage rates go down? Yes, but everything about the Everything Bubble will be pulled down alongside — but, the wild card of federal spending most likely will feed inflation and make all forms of investing very precarious.

“The CME fedwatch casino wheel implies rate cuts coming in September, with 60% probability.”

These are the same morons that at one point bet on seven rate cuts in 2024, starting with a cut in January. Why is anyone still paying attention to them?

They keep putting free drinks in front of me and plates of snacks — which makes the casino entertaining — even if the game is rigged. It’s hard to ignore their siren song which compels everyone to dance, while the music is still playing.

Btw, the downward BLS revisions in September seem like they may coincide with CME being more right — this time is different?

CME futures for the federal funds rate were practically NEVER right. They are betting instruments. It’s not about being “right.”

…and here I was trying to figure out what Coronal Mass Ejections has to do with it when everyone knows it’s sunspots…

may we all find a better day.

So renters are waiting for rates to drop back to 3% so that they can buy the $500k house that will definitely not change in price as rates drop, and in the meantime they are spending $2-3k a month in rent as they wait?

What if mortgage rates drop to 5% but prices increase by another 20% and the monthly payment is just the same?

This is so ugly. Basically everyone who didn’t own something before 2019 is hosed. People that bought at top dollar in 2021, people trapped in 3% mortgages, renters. It’s going to take a long time to clear this out.

“in the meantime they are spending $2-3k a month in rent”

“if mortgage rates drop to 5% but prices increase by another 20%”

Take your 500K house – even when mortgaging only 400K at 5%, that’s still >2K/mo in P+I, and that doesn’t factor in other expenses.

And with current rates, that monthly payment is even higher. In that context, how are they worse off paying 2-3k in rent?

Real Estate = Location, Location, Location.

There seems to be a slow change in preferred location. Some of the old popular locations are being left and people are moving to new locations that dont have the infrastructure in place to quickly build more housing and so prices are bid up.

Interest rates of 6% or 7% are not impossible. Yes, certainly, higher rates should translate into lower prices. But if 100 people move into an area that can only produce 50 houses per year, prices will be sticky.

A political change in locations that are currently less popular, back to policies that promote social order, protect property and suppresses disorder will slow the flight and the flight is only on the margins anyway. How likely is that to happen ? Slim or none in my opinion, but I’m willing to be proven wrong.

Mortgage interest rates of 10% and higher are not only not impossible, but are quite probable in the US in the years ahead.

I rewatched the movie “The Big Short” last night. See https://en.wikipedia.org/wiki/The_Big_Short_(film)

The parallels between that movie and today’s housing market is uncanny, particularly the scene where the character Mark Baum and his investment team fly to Miami to get a first hand look at the housing market. The scene where they are driving around with the lady real estate agent made me think “this shit is happening all over again”.

I think we are going to have a repeat of the 2008 crisis, but this time it will be caused by bond traders refusing to buy long term govt bonds at low rates, and the curve inverting back to normal, with much much higher long term rates. I was an active participant in the peak of that mortgage interest rate graph around 1982 (bought a townhouse at 14%). If interest rates peak again, we will have a recession, and the Fed won’t be able to stop it.

Howdy Bruce Foreclosures could be on the rise??? Maybe, they would not allow property owners to even kick out dead beat tenants. So, is there a flood coming????? Will be fun to watch…….

I wanted to share some interesting observations about the housing market in my neighborhood. The house next door is currently for sale for $969,000, and it has four bedrooms and two bathrooms. Surprisingly, a smaller house next to it, which was previously owned by drug dealers, was sold for $370,000 about ten years ago. The current estimated price for that house is $944,000, according to Zillow.

I find it quite perplexing that these houses are being sold for such high prices, considering their average condition and less-than-ideal location. There have been several houses for sale on my block, and all have been selling quickly. I’m curious to see who the new neighbors will be – whether they’ll be investors or single-family homeowners. The demographic of the people moving here has been single and older. Lots of these houses are tiny and overpriced.

Whats Up Doc besides housing???? They created one heck of a bubble that may never pop. Not in my lifetime maybe……

Zillow “Zestimates” are algorithm driven and have little to do with actual value. The houses that are in better condition, and have recently sold, feed the algo.

It also depends on where the people are coming from. If they’re fleeing high cost of living areas, the $900K price tag might look like a bargain to them.

Older? Older people are more likely to have assets. If they’re at all like us, we stopped buying rooms full of *stuff* years ago. We bought quality things that have lasted for decades… no need to replace solid wood furniture to chase the latest HGTV particle board trends. We bought “shaker” before “shaker” was cool. Simplicity is always a lasting design. I even have the first “home improvement” tool I bought (circa 1975 basin wrench that still has it’s price tag on it despite being used for decades – quality tool and an equally quality price sticker).

The wise spend their money once on things that withstand the test of time. I’d rather have one high quality comfortable chair than a room full of Ikea.

Apologies if I didn’t RTGDA closely enough and missed this, but could it not be that the more expensive markets are behaving differently, as opposed to the different quality homes? I don’t think many people would describe as “high end” what 1M gets you in any of our nearby towns.

These are national median prices. Not local prices.

The California median price chart of single family looks similar to the national median price chart of single family. It’s not behaving differently.

Real estate and rentals are a hard-knock business. The main difference between the 2008 & 2024 prices: in 2024 buyers are more qualified than then in 2008. The housing market is short 4 to 5 million homes (and is this number growing). Supply and demand typically dictate price changes. Inflation has been running since 2010 and running hot since 2019 it all adds up. Every time we turn around our leadership has spent more billions on the US taxpayer’s behalf, often on questionable or low priority causes, and thus superfluous money enters the system. As fiat money becomes worth less and less, home values rise more and more.

“The housing market is short 4 to 5 million homes (and is this number growing).”

That’s a real-estate industry promo myth, put out there to pump up prices. What there is, is a shortage of homes people can afford because prices have spiked out of people’s reach. So now you’re seeing the inventory (that doesn’t exist?) coming out of the woodwork?

Here is housing starts (multifamily = apartments and condos):

Wolf, thanks for another useful post, but for the graphs above, I would divide the construction starts by US population to get a better picture; a population of 189,700,000 in 1965 verses 336,600,000 in 2023, up 77.5%. Changes the graph somewhat. For example, 1,000,000 single family construction starts in 1965 is equivalent to 563,500 starts in 2023, and the 500,000 multifamily residential starts in 1965 is equivalent to 281,800 multifamily starts in 2023. It looks like there is a shortage of new home construction to me. Maybe the builders are too greedy and are over pricing their product?

Wolf, I’m trying to wrap my head around your response comment above.

Fields of Green states there is a shortage of supply, causing the high prices.

Your response is that there is a shortage of homes people can afford.

I don’t think these two statements are mutually exclusive. If there was a tremendous, ample supply of inventory, wouldn’t prices necessarily come down to affordable ranges?

yes, we’ll see that through a mix of price declines and inflation (wage inflation). This is already well underway in many markets.

“I don’t think these two statements are mutually exclusive. If there was a tremendous, ample supply of inventory, wouldn’t prices necessarily come down to affordable ranges?”

Not necessarily. Homes in the desirable areas (think Hinsdale, IL – rail commute to The Loop) will be purchased and scraped, rebuilt with a McMansion on the dirt (leave a chimney or all up so it’s considered a “remodel”, not a new build). Ditto places like Rossmoor, CA (actually Los Alamitos). Why? Because of proximity to roads and transportation.. access to employment…. and those high values equate to better quality schools due to parental involvement and stronger tax bases. Amenities follow the money and those who can afford to, gravitate to those areas.

Building more “field of dreams” homes might be more affordable (no amenities) as far as purchase price, but the added commuting time and cost (time spent in a car is a hidden cost), and time spent wandering the globe to get to a food store or home center (and, no, not all areas have food delivery), can offset some of the variance in monthly expense. If you want to spend 10 days on a camel to get home, have at it. Few people want a “tiny home”…. and overcrowding by building two on a lot, without adding the infrastructure (electric capacity, water mains, sewer, storm water management), isn’t a solution.

Lowering the standard of living for people so others can benefit hasn’t worked in forever. Those that can, leave. What you end up with is Detroit.

Wolf, I consider you a valuable resource for our on-line community, and don’t want to get into what an old Deloitte Touch auditor of mine (with a PhD) called a pissing contest, but you have moved the goal posts to 2000 – 2023 from 1965 – 2023. Yes, during this period population went up 19.6% from 281,400,000 to 336,600,000 while housing starts combined were unchanged at approximately 1,500,000, and that combined with the decrease in family size has left US housing Units per capita aproximately constant. but you’re cherry picking the numbers. Its fine with me if you don’t post this comment. its Just for the record.

What many are missing is what the idea home will be.

Dose the next generation what big shacks and huge yards?

As many areas become less desirable and social pressure (global warming, etc.).

Just visited family in an upscale Dallas area. Even on the weekend, few were outside except yard crews.

I would expect much more regulation as immagration and homelessness increases.

And there is always the arch villain GLOBAL WARMING!

I would vote for higher property taxes and energy costs for all the evil doers in McMansion Hell.

In Texas, higher energy costs are a feature, not a bug, due to the way that customers purchase electricity (it’s not a single monopoly company, but sold through a variety of companies for “consumer choice”, but in reality, simply a way to gouge). The grid in TX is unstable because of the increase in solar and sWINDle production that is not cost effective. Nor stable. Nor environmentally friendly. Not always windy and not always sunny.

If you look at the building trade magazines and consumer surveys, the expectations of the next generation of home buyers is not a shipping container. They have much higher aspirations than that. Lower the price of the McMansion in Dallas and watch them flock.

I talk to these sellers every day, and they still have zero fear!

As Wolf points out, they’ve already spent the $1 million in their head.

I had one seller say “I’d rather die than sell my house for $400,000”, and that is exactly what happened. He held out for an exuberant price until he died.

Not directly related, but have there been any successful laws/taxes in other countries or eras that have discouraged people from owning more than 1 home? For the purpose of having a higher % of the population own homes instead of renting. Like maybe the first home is tax advantageous, 2nd home is more taxed, 3rd taxed even more…

Hello. I have a hunch what you might say, but what is your definition of “success” from a policy that discourages all citizens from owning more than one home?

Home sales may be sagging nationwide, but we’re busy as hell here in the Swamp. All RE is local. There is a massive shortage of housing here. Even refi’s have picked up. A lot of this housing activity is investor driven. These are mom & pop operations. They are trying to make a quick buck emulating the big time investors. The Fed needs get off their sorry asses and bring this to an end by raising interest rates substantially. I’m talking 10% mortgage rates will be the only thing that brings an end to this insanity.

Your assumption is based on people selling. Interest rates could be 100%. Some don’t care. They have access to other capital markets and don’t need no stinkin’ mortgage. The proles, however, would be doomed.

Keep in mind that, if interest rates were 10%, people who have loose cash now have a higher return on that invested money. This adds to their ability to pay “whatever” for anything they choose to buy. It changes nothing.

Nothing happens in a vacuum. That’s the problem with *easy* solutions. No one thinks them through.

People will sell if there’s a recession. Travel will die down and airbnb’s won’t be profitable. Already happening here in the mountain/vacation towns in CO just as travel normalizes. Also if there’s a recession people start getting roommates again or getting rid of their second homes – we will start to see a normalization back to pre-covid housing trends. As people get called back to the office, a lot of those CA people moving to low cost areas and biding up prices will sell as they have to move back or they will have to find a local job with a more local salary. Once prices start to drop people will try get as much for their houses as they can while they still can and there will be a race to the door. People are only holding on now because the media has pushed the idea of lower interest rates soon making them think they can get another 10-20% out of their properties soon. It’s hard to time the market, but assuming the fed doesn’t cut rates prematurely due to political pressure there should be something of a correction.