New Highs in Miami, Los Angeles, San Diego, Boston, Chicago…

By Wolf Richter for WOLF STREET.

The S&P CoreLogic Case-Shiller Home Price Index, released today and dubbed “March,” is a three-month moving average of home prices whose sales were entered into public records in January, February, and March. So that’s the time-frame we’re looking at here. It reflects Rate-Cut Mania that commenced in November and peaked February 13, when the first of three nasty CPI reports in a row interfered.

During that time, the average 30-year fixed mortgage rate dropped from 7.8% at the end of October to about 6.6% in mid-February. Mortgage rates have since then zigzagged higher, with the daily measure of Mortgage New Daily pegging the average 30-year fixed rate mortgage today at 7.28%.

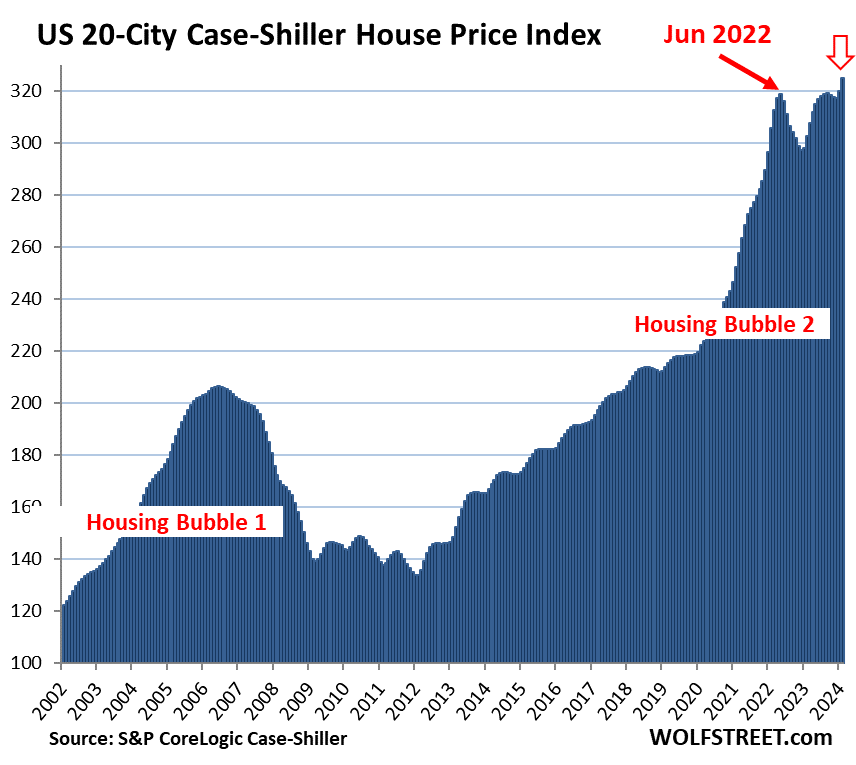

The 20-City Case-Shiller Home Price Index jumped by 1.6% in “March” (moving average of January, February, and March), from the prior month:

- Month-to-month, prices rose in all 20 metros covered by the index.

- Year-over-year, the 20-City Index was up 7.4%.

- Compared to the previous all-time high of June 2022, the index was up 2.0%.

Prices were below their 2022 highs in 8 of the 20 metros in the Case-Shiller index (month of peak):

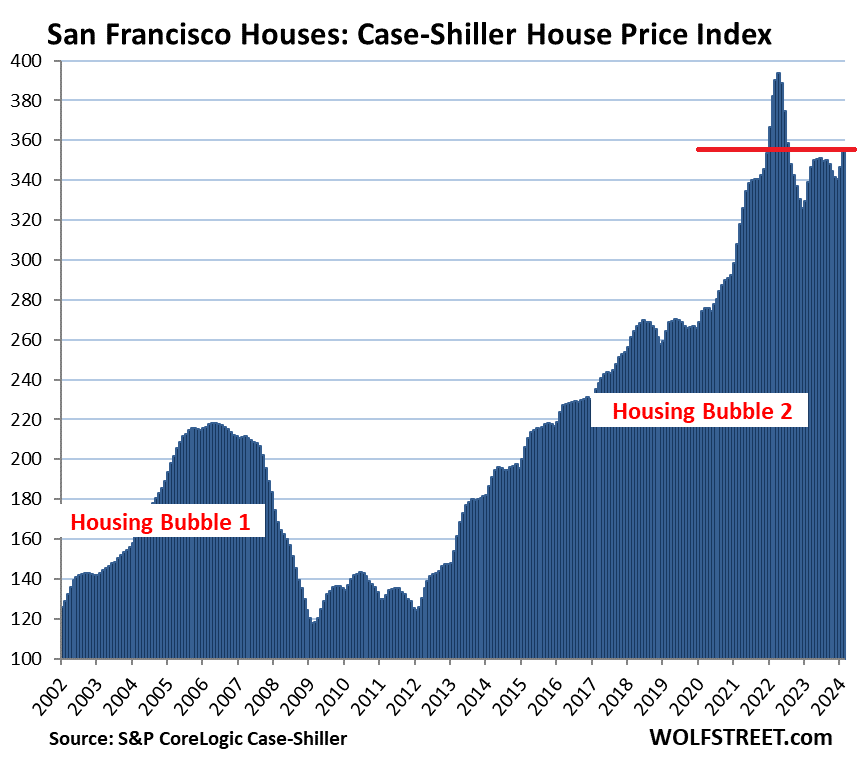

- San Francisco Bay Area: -9.7% (May 2022)

- Seattle: -8.2% (May 2022)

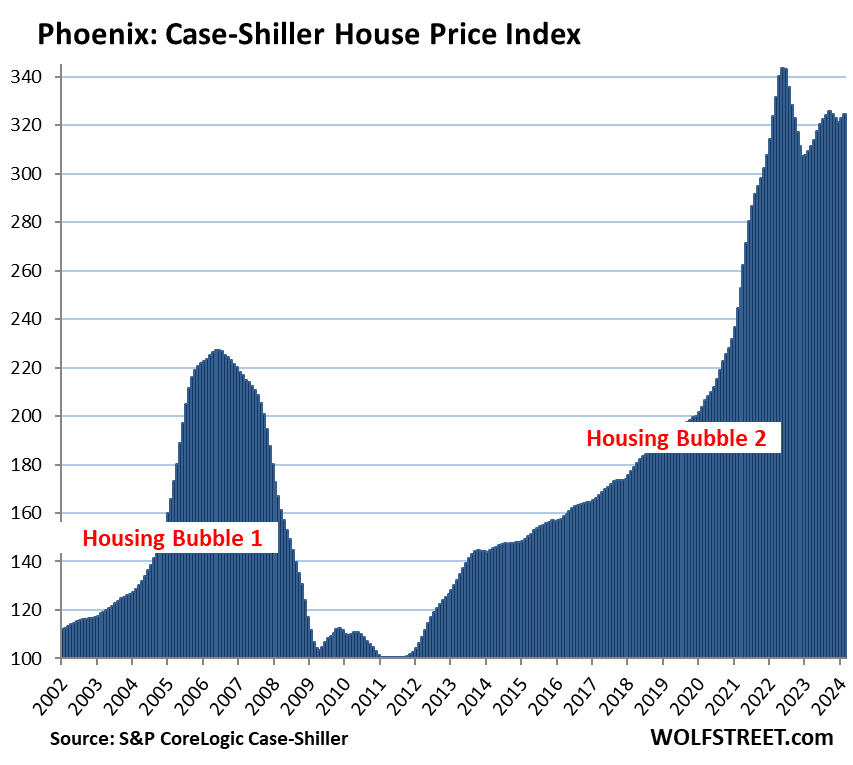

- Phoenix: -5.5% (June 2022)

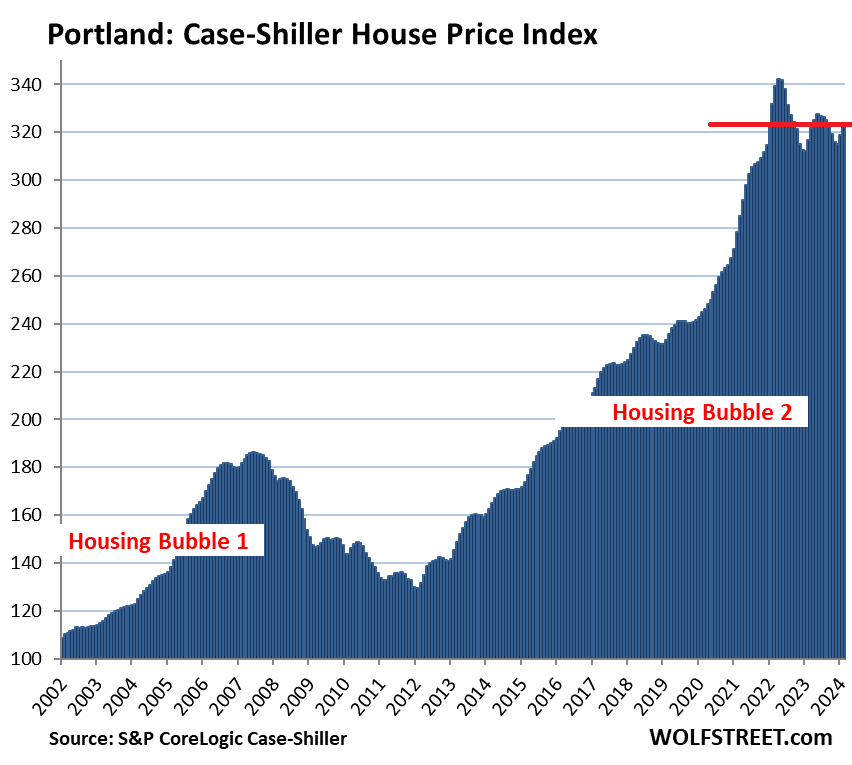

- Portland: -5.4% (May 2022)

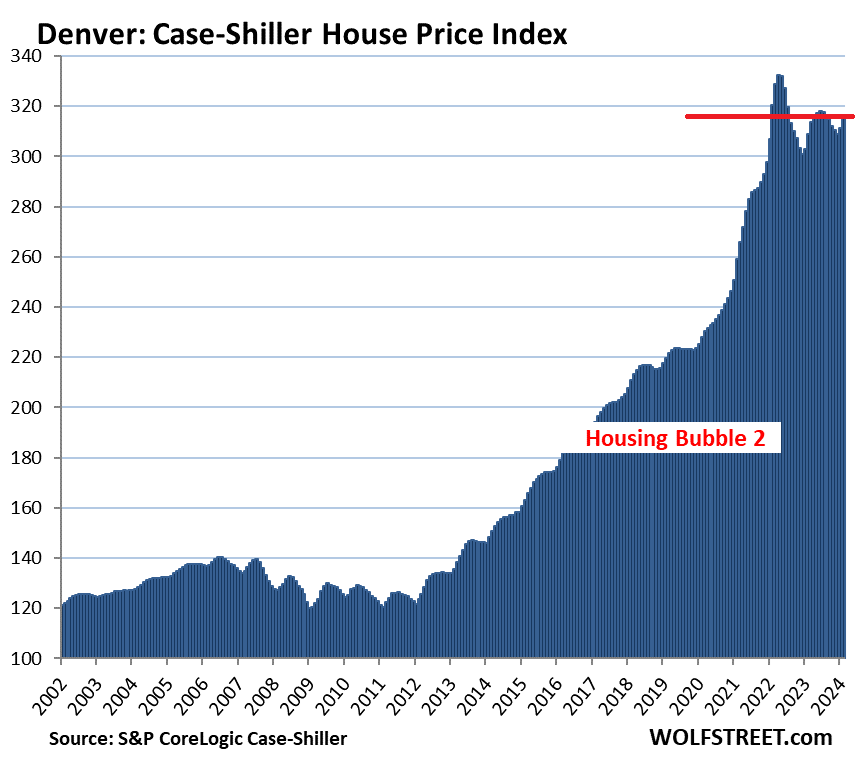

- Denver: -5.0% (May 2022)

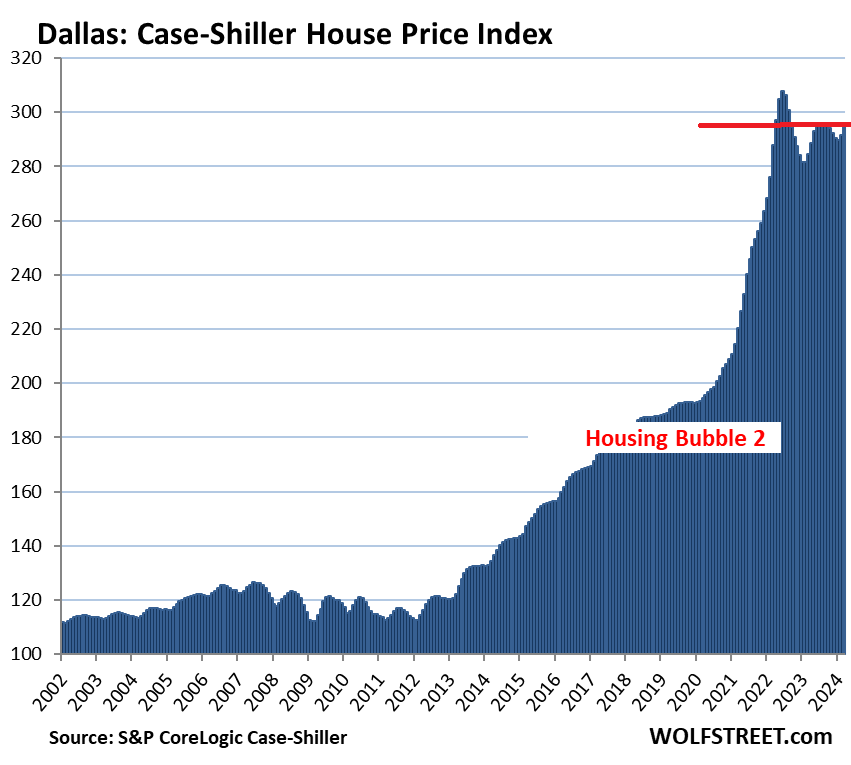

- Dallas: -4.2% (June 2022)

- Las Vegas: -3.6% (July 2022)

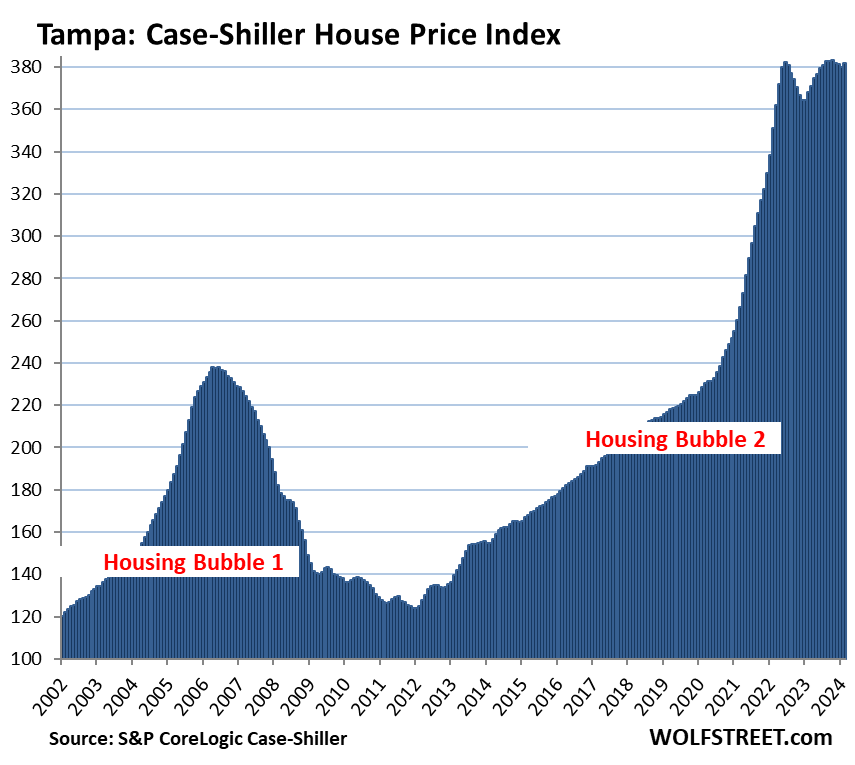

- Tampa: -0.14% (July 2022)

The most splendid housing bubbles by metro.

San Francisco Bay Area single family houses: the San Francisco metro in the Case-Shiller Index covers a five-county portion of the nine-county Bay Area (San Francisco, San Mateo, Contra Costa, Alameda, and Marin).

- Month to month: +2.6%

- Year over year: +4.9%.

- From the peak in May 2022: -9.7%.

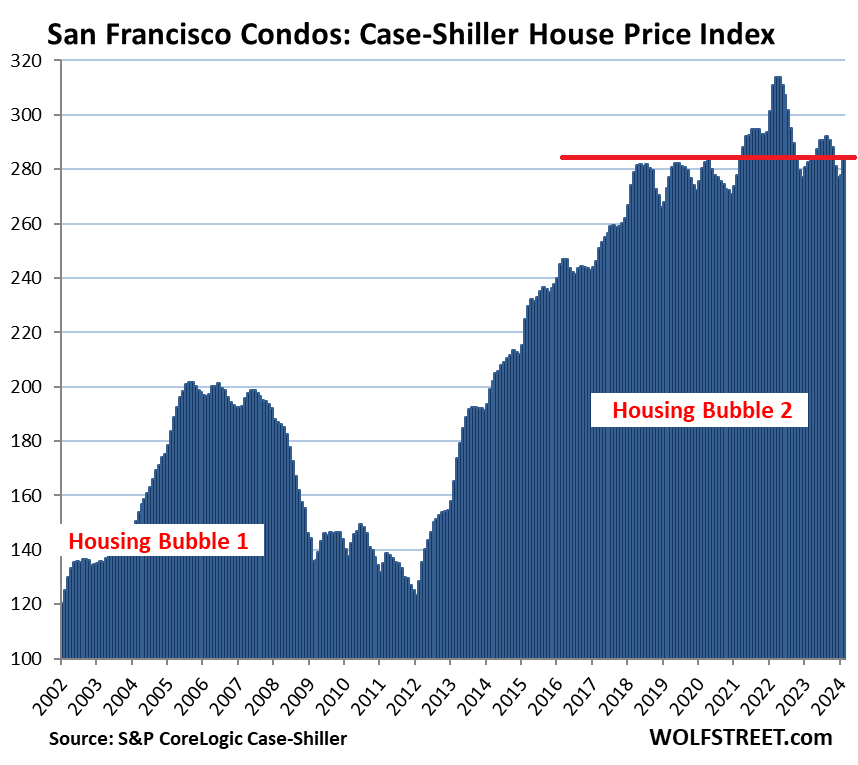

San Francisco Bay Area condos: Condos are a big part of the market in the Bay Area, particularly in San Francisco itself.

- Month to month: +2.2%.

- Year over year: +0.5%.

- From the peak in May 2022: -9.6%.

- Back to April 2018.

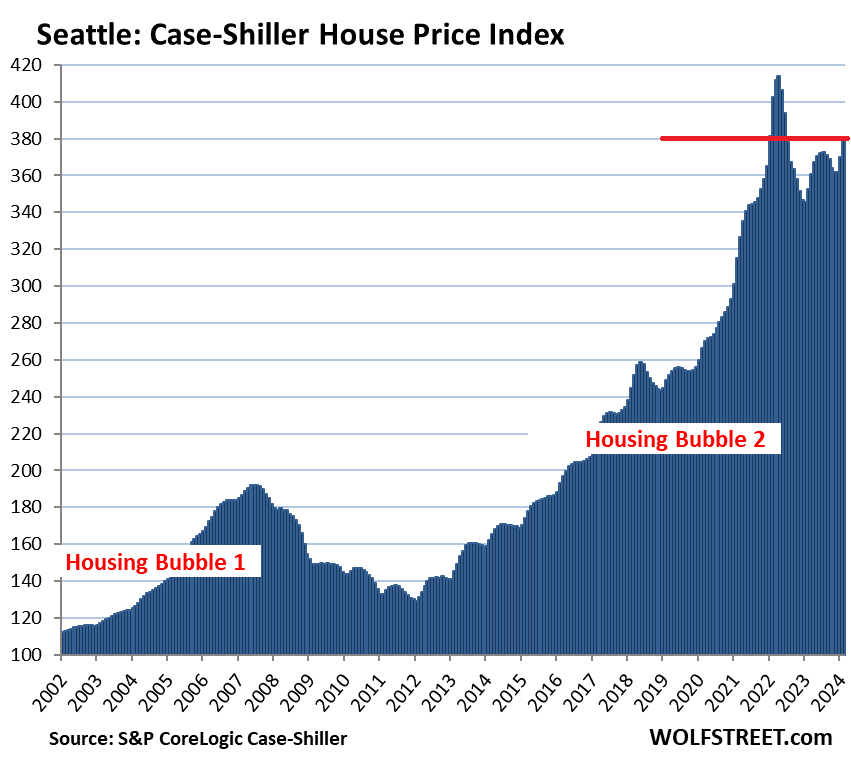

Seattle metro:

- Month to month: +2.7%.

- Year over year: +7.8%.

- From the peak in May 2022: -8.2%.

Phoenix metro:

- Month to month: +0.5%.

- Year over year: +4.9%.

- From the peak in June 2022: -5.5%.

Portland metro:

- Month to month: +1.5%.

- Year over year: +2.2%.

- From the peak in May 2022: -5.4%.

Denver metro:

- Month to month: +1.3%.

- Year over year: +2.1%.

- From the peak in May 2022: -5.0%.

Dallas metro:

- Month to month: +1.2%.

- Year over year: +3.6%.

- From the peak in June 2022: -4.2%.

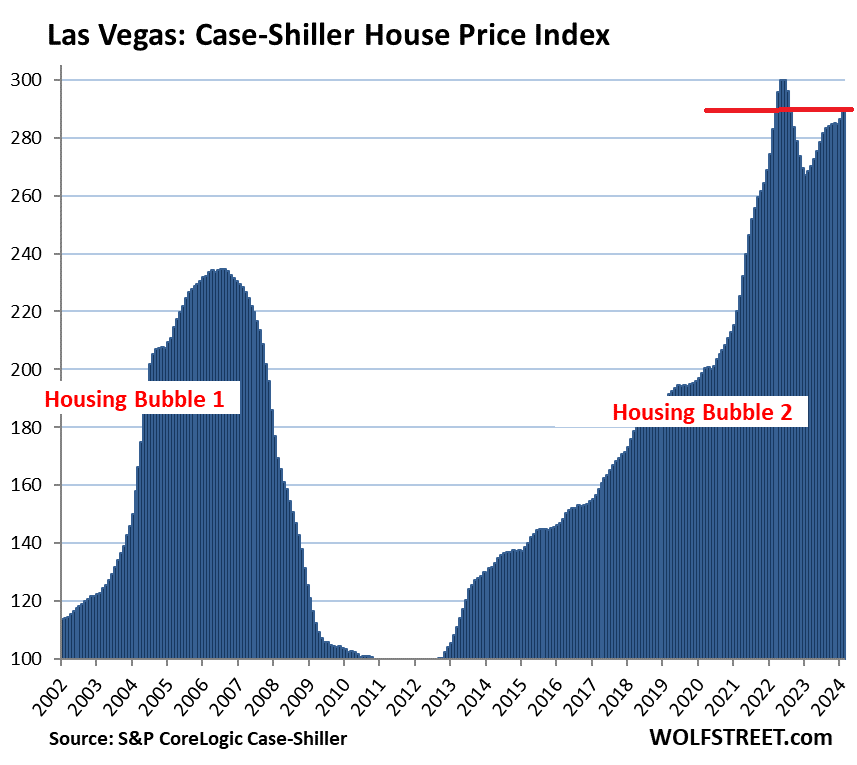

Las Vegas metro:

- Month to month: +0.9%.

- Year over year: +7.7%.

- From the peak in July 2022: -3.6%.

Tampa metro:

- Month to month: +0.5%.

- Year over year: +3.8%.

- From high in November 2023: -0.14%.

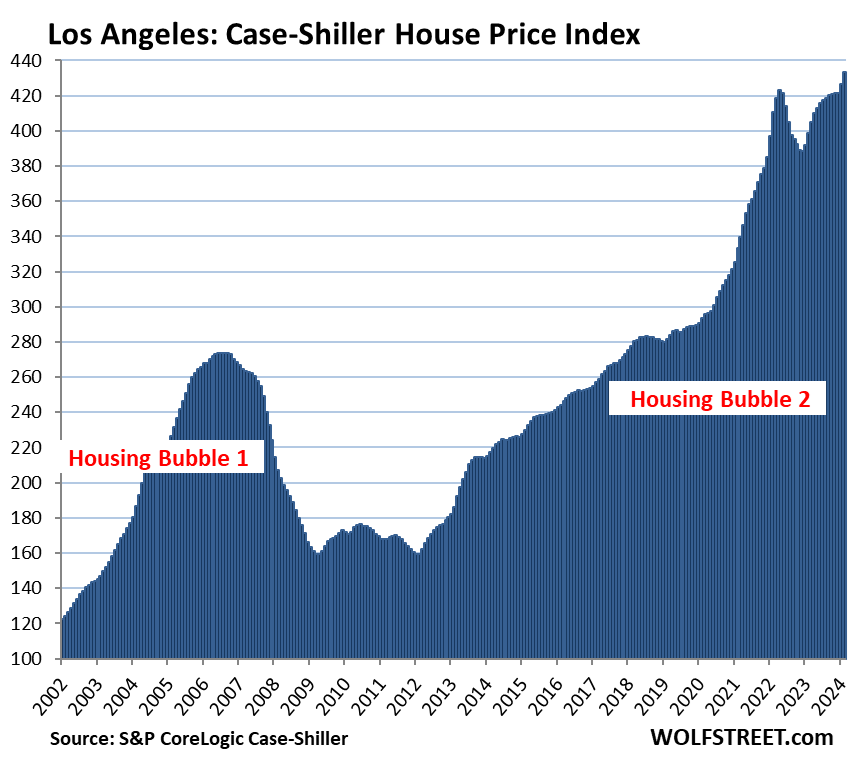

Los Angeles metro

- Month to month: +1.7%.

- Year over year: +8.8%.

- New high, 2.5% above the prior high in May 2022.

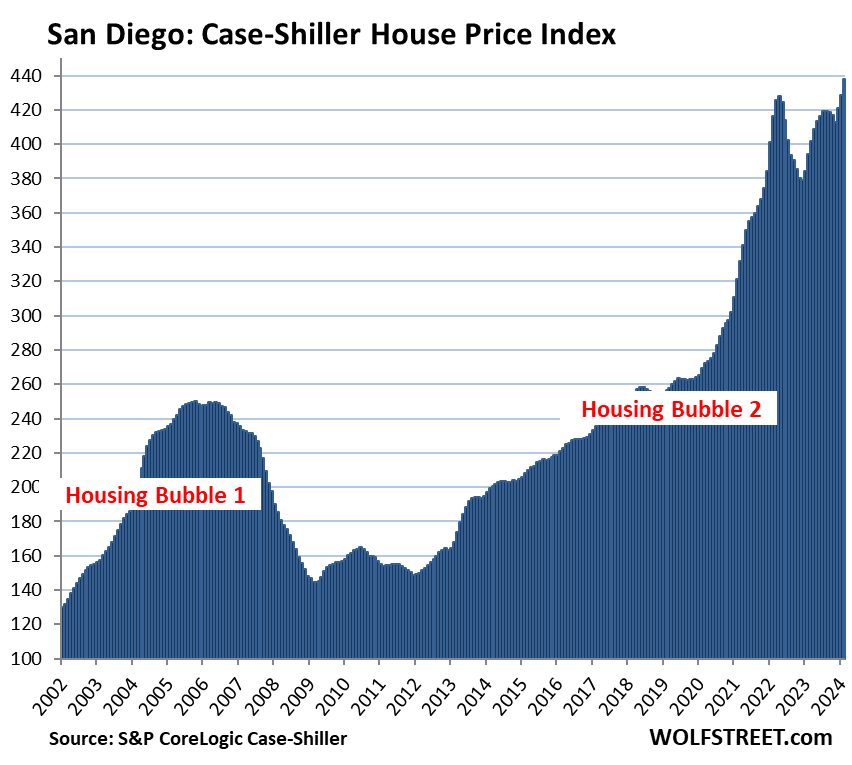

San Diego metro:

- Month to month: +2.2%.

- Year over year: +11.1%.

- New high, 2.4% above the prior high in May 2022.

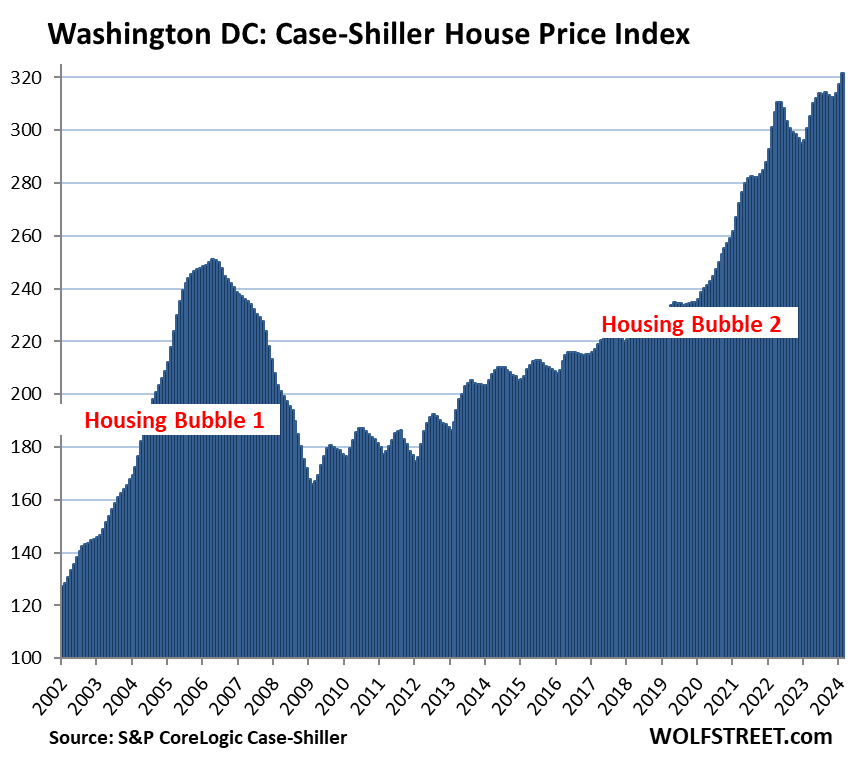

Washington D.C. metro:

- Month to month: +1.2%.

- Year over year: +7.0%.

- New high.

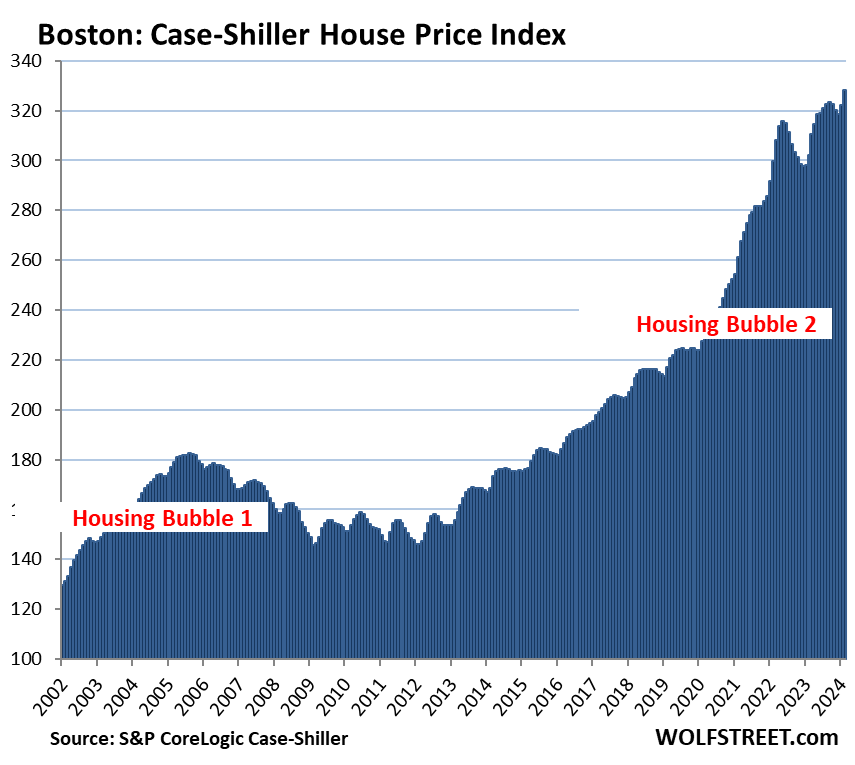

Boston metro:

- Month to month: +1.9%.

- Year over year: +8.7%.

- New high., +3.9% from June 2022.

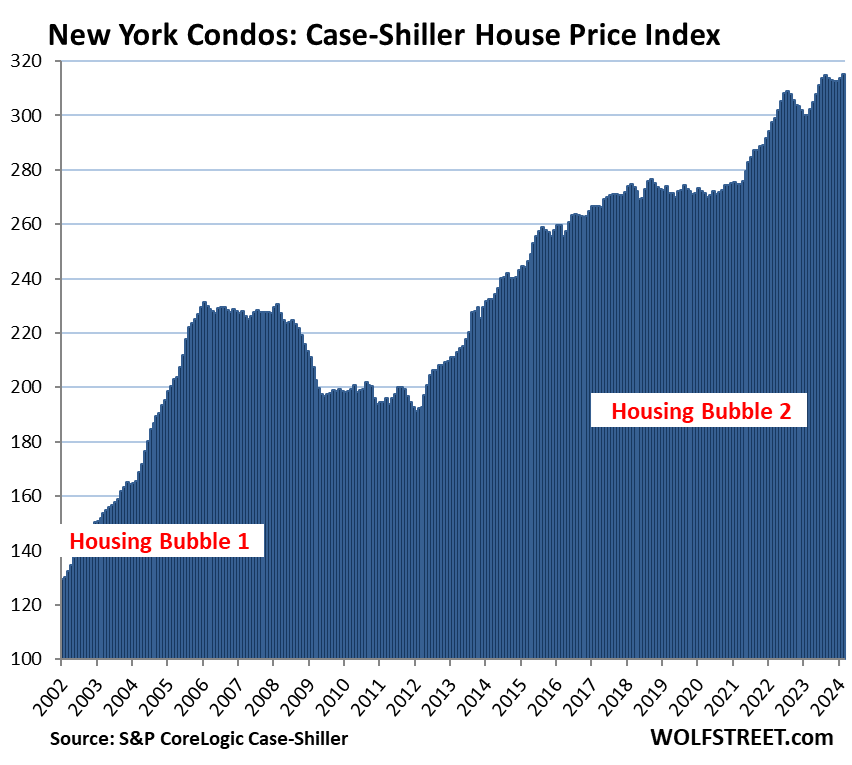

New York metro:

- Month to month: 1.5%.

- Year over year: +9.2%.

- Set new high.

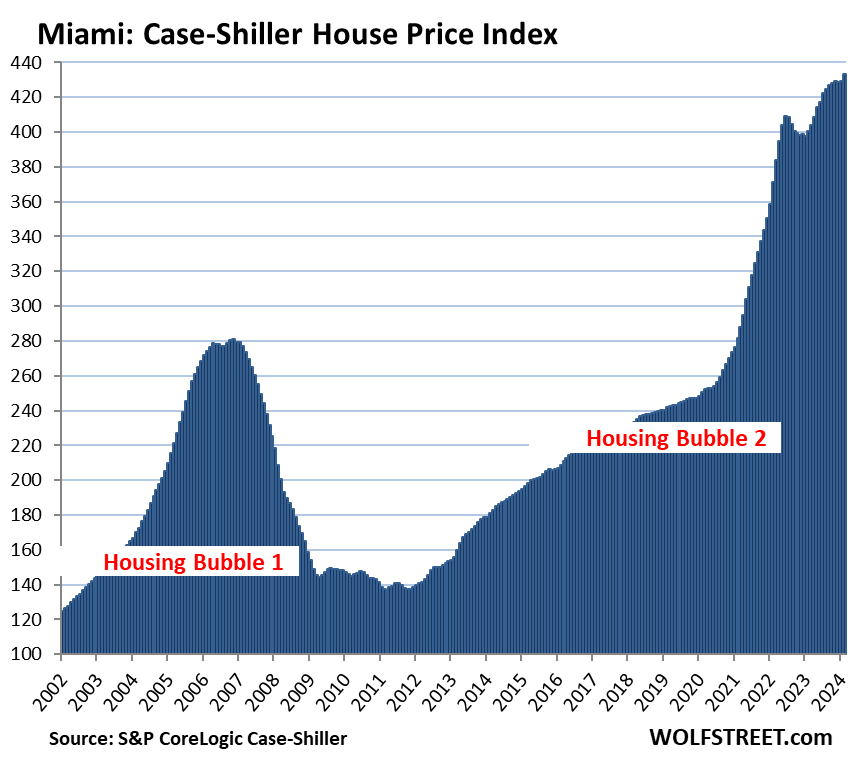

Miami metro:

- Month to month: +1.0%.

- Year over year: +8.2%.

- New high.

To qualify for the Most Splendid Housing Bubbles, the metro must have experienced home-price inflation since 2000 of about 200% or more at the peak. The indices were set at 100 for the year 2000. Today’s index value for San Diego of 438 is up 338% since 2000, making San Diego the most splendid housing bubble on this list, a hair ahead of Miami and Los Angeles.

Home-Price Inflation. By measuring how many dollars it takes to buy the same house over time via the “sales pairs” method, the Case-Shiller index is a measure of home-price inflation. San Diego had 338% home price inflation since 2000. Over the same period, the Consumer Price Index, which tracks prices of goods and services that consumers “consume,” rose 86%.

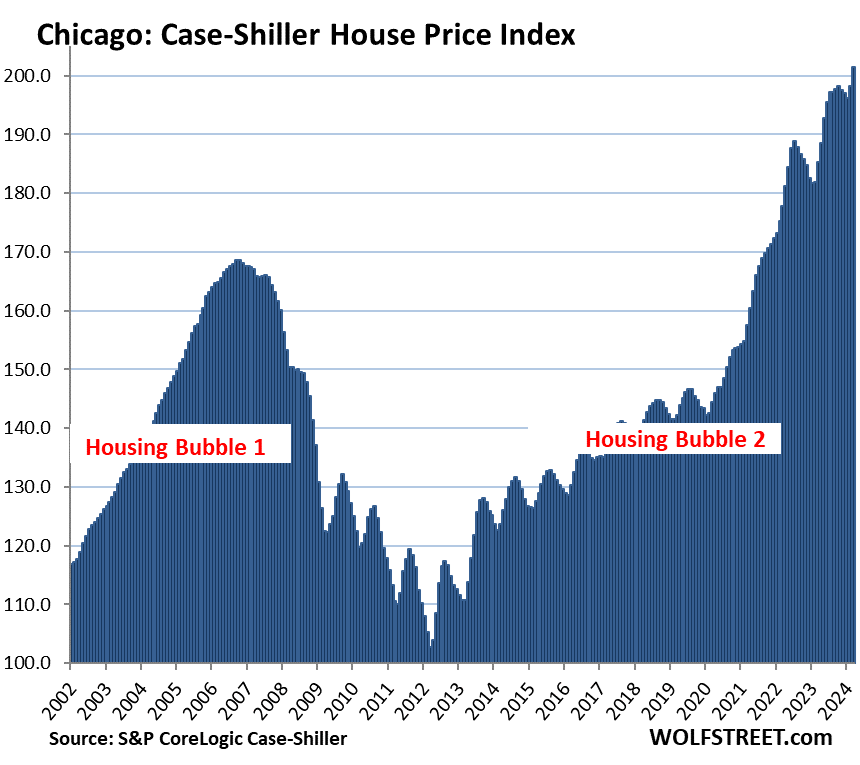

The remaining 6 of the 20 metros in the Case-Shiller index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) had a lot less home-price inflation since 2000, despite the price spikes in recent years.

Chicago, with an index value of 201 is up by 101% from the year 2000, and therefore far from qualifying for this illustrious list of the Most Splendid Housing Bubbles. But the price spike in recent years was quite something, so here it is anyway:

- Month to month: +1.7%

- Year over year: +8.9%.

- New high.

Methodology. The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses were sold previously. The price changes are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors (37-page methodology, including the counties that are included in each metro).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Even more splendid than before.

I would say the bear went over the mountain, but the way these peaks keep rising I fear the bear is doomed to failure as are those waiting for an affordable home.

Wolf I was wondering, with the adjustments made last week by the census bureau, lopping off 25% on the new single family houses, does that effect today’s numbers in any way?

Your #2. What the Census Bureau revised last week was the median price of NEW Houses that builders sell. The Case-Shiller data here has nothing to do with that. Case-Shiller data here is based on the sales-pairs method, comparing the prior sale to the current sale. So a house must have been sold at least twice before it enters into the data. Therefore, by definition, new houses that builders sell are never part of the Case-Shiller data here.

Ain’t no housing bubble. The “experts” have been calling for a crash since 2021. There is a massive deficit of supply coupled with the people who locked in at 3% being effectively removed from the market.

If you didn’t grab a house while intrest rates were low you have been priced out of the market for the foreseeable future. Interest rates will not see sub 5% for many many years if ever.

This is the new normal while home prices may come down a couple of % those waiting out for a crash will be disappointed.

Wrong. There not only is a housing bubble, but as people max out their debt and credit along with the higher interest of 2nd mortgages, with inflation and other rising costs, repossessions will increase and then you will see the bubble burst, just like in 2008.

There aren’t a lot of transactions like you saw leading up to the 2008 crash. Homeowners have been mostly locked in. Those buying recently have significant buying power from this very long bull run, but this is a small percentage of current homeowners. Other people continue to rent. Those locked in have significant equity to go with their low rates.

Not even remotely close to 2008. Also a recession rarely ever means “housing crash”. The housing crash in 2008 CAUSED the recession, not the other way around.

You clearly have not been reading the articles. While credit card debt is an at all time high debt to income is at historic lows. Consumers are in great shape. These are NOT the same homeowners as 2008.

Foreclosures are at historic lows again. Look up the data.

The only leg you have to stand on is the people who bought homes at record prices with 8% intrest rates. Those buyers will be in trouble but that will take many years to come to fruition.

The 2008 crash will not happen. Keep dreaming.

Peter Shit has been draining my time since covid with the recession talk. 4 years of my life gone listening to this dude

Have you really listened?

For four years his advice has been to buy precious metals, commodities, and low p/e foreign companies. If you did that, you’ve done well. If you’ve done something different that hasn’t worked, take responsibility for it.

So interest rates are going to stay high and housing prices are going to stay high.

Oh.

It might be possible that those who who believe a housing crash will never happen will be disappointed.

So true. We live in Savannah, Georgia. Prices are skyrocketing here. They slowed down a little bit, but still constantly going up. We’re so glad we bought our house 5 years ago. We could never afford this house today

It’s a good thing all those “locked in” owners never being able to buy another house won’t affect demand at all.

Whenever a price bubble appears in a metro area it is quite likely because there is an excess of built out/purchased rentals acquired by the big boys.

When prices are down, they buy in a metro area, then drive the price up to unaffordable levels to fill their rentals (apartments and homes).

The interesting statistic is how many of these sales are cash sales, which indicates either foreign or investment companies whose cost of money is near zero.

No matter what, if any economic factors are still in play, if the price of a house exceeds 3x the household income for that area, somebody is getting screwed.

My research shows that the law of supply and demand is no longer in effect in the USA, and has been gone for years. Prices are now determined by the MBP principle, management by perception, and just some good old (fraudulent) manipulation.

Remember the guy who shorted Apple stock and then strategically placed a negative rumor? They caught him, but they don’t catch the big boys for some reason or another. Or if they do, the fine is so minuscule it’s just a profitable cost of business. His actions were just proof of concept. It works.

And why do folks keep buying this overpriced stuff? “Nobody ever went broke underestimating the intelligence of the American public.” It’s not the families of the one in seven children living in poverty! And it’s not the half of the households who cannot handle an unexpected $300 expense without going to the credit cards.

“…by the big boys”

The big boys stopped buying houses two years ago because they cannot make enough in rents to make those high prices work. What they and homebuilders are doing now is building their own build-for-rent developments, entire new neighborhoods of for-rent single-family houses that rent at premium rents to renters of choice with above median incomes. That’s a hot thing in homebuilding right now. These developments are more cost-efficient to manage and lease than individual rentals scattered all over the place. And many of the big boys are selling some of their scattered houses they bought years ago to lock in the high prices and cut their operating costs.

So the big boys are actually adding supply to the rental market by building their own rental houses, and they’re adding supply to the for-sale market by selling some of the houses they bought years ago. We’re no longer in 2012.

https://wolfstreet.com/2024/04/24/biggest-landlords-pile-into-build-to-rent-single-family-houses-but-are-selling-older-houses-into-this-overpriced-market/

When I lived in Doha there were thousands of wonderful communities and master planned developments that were 3000 to 5000 sq ft homes for rent built for just that purpose. Wonderful way to live !! 7 star living ! Jobs population growth and higher energy costs and land values will continue to drive these types of communities . I love seeing these changes with wonderful new options for safe clean and well managed homes and condo communities .

The Census Bureau revised away that 2022 peak. It was a statistical anomaly that never happened.

What the Census Bureau revised last week was the median price of NEW Houses that builders sell. The Case-Shiller data here has nothing to do with that. Case-Shiller data here is based on the sales-pairs method, comparing the prior sale to the current sale. So a house must have been sold at least twice before it enters into the data. Therefore, by definition, new houses that builders sell are never part of the Case-Shiller data here.

Joking.

Los Angeles made a new high. Shocker. Some of us in the area were trying to warn about this rebirth of the bubble a year ago, and were dismissed as RE shills when we described the crowded open houses and general house-horniness on open display in our area.

As long as monetary policy is reckless on the way up and eggshell-cautious on the way down, these serial bubbles will continue to occur.

of course it did. people know that central bankers worldwide have no real intention to defend fiat currencies, and that it’s all a dog and pony show.

therefore, exchanging currency for hard assets is going to continue uncontained.

I whole heartedly agree with this sentiment. At the moment when I attend open houses or look at rentals it all feels like foreign ownership or PE on many levels. One property management company did their scheduling from Philippines. The agent also no showed. Just scheduling to see this stuff is buried under layers and layers of management offices that could care less.

Pea Sea,

If you promote RE here, you are a promoter. You need to pay for ads if you want to promote something on this site. I’m so tired of these promoters wanting to abuse this site to spread their promos for free. Cheapskates!!!

Same thing with QE mongers, QT deniers, or rate-cut hustlers, if they want to promote their stuff, they need to pay for an ad here. I stopped the crypto promoters years ago. I stopped the MMT promoters about a decade ago. I had these people all over the place here. I have been way too lenient with RE promoters, but it’s over.

Howdy Lone Wolf. Scared me as I read your post. I thought maybe Squirrel Promoters were gonna be added. HEE HEE

Crypto will be worthless when the grid goes down.

Stan Sexton,

So will be just about anything else. This modern economy cannot function without electricity, like your body cannot function without blood.

I wasn’t and am not promoting anything, as you well know. I detest this bubble to the point of bitterness, because it affects me personally. I’m priced out.

But I wasn’t and am not delusional, and when I saw signs that the brief correction of 2022 was reversing, I reported them. Pretending something isn’t happening doesn’t make it go away.

And now the numbers have borne those observations out. I was sadly right, and those who thought the correction would continue were gleefully wrong.

When I start to see empty open houses and desperate sellers again, I’ll report that too. And I’ll be less pissy about it, lol, because things economically will be going my way for a change.

Like Pea Sea I’m not a “promoter” just another guy who can’t believe the bubble has not popped even more, especially the prices for high end stuff in the Bay Area and Tahoe. We all know interest rates have gone up but many may not be aware how much fire insurance has gone up in parts of CA. A decade ago we were paying just over $1K a year for insurance at the cabin, today we are pushing $10K a year. I just saw that a (bigger, nicer and newer) cabin near me that sold in 2022 for $3.5mm is back on the market for $4.2mm. The Redfin site estimates the MONTHLY cost will be over $23K for P&I, over $4K for Property Tax and “over” $1K (more than $12K a year) for insurance. The people buying stuff like this are probably richer than me and have plenty of money to rent a place unless they think values are going up and I can’t understand why anyone is buying today.

Yea, we are not promoters, we just wanted to buy a house for our family and listened to Wolf’s nice stories, and now we are even in a more bad situation than before. Not sure when this bubble ( balloon 🎈) will pup.

I only follow the Chinese money which is heavy in Washington because of the low tax rate.

I prefer to hear info/opinions from all sides. Otherwise we just end up in an echo chamber. Personally I don’t see the comment as some type of promotion. I think a lot of people here just want to see an end to these endless bubbles and are getting frustrated, myself included.

Yes, there was a lot of negative sentiment toward people describing this phenomenon in SoCal, and I think with the benefit of the last year, the data are showing that this is a real thing.

These are stories from SoCal: Our family member is going through a divorce. Their house just sold significantly over asking. My old boss is retiring and moving to Phoenix. He sold his house in North County over asking. I would describe the market as insane: normal people (not high earning couples) can’t afford anything with prices sky high and rates sky high. (I know rates aren’t sky high historically speaking but if 1M is your price, 7% is sky high compared to 3% just a few years ago). Those that sell are in the driver seat but unless they move to a lower cost state they are screwed as well. Nobody sells and buys in the same area just to replace their low rate with a 7% rate. No idea how first time buyers are supposed to buy without significant help / inheritance.

The question is who is buying and pricing out the masses?

I think you have your answer – they are buying with inheritances. My family is in a position to help us into a property we could never otherwise afford, and we can still barely afford anything where I am (UK). Here it’s something like half of all first time purchases are done with family assistance.

I figure this trend will accelerate as peak boomer retirement moves towards peak boomers passing away. Essentially we are now at the start of a massive intergenerational wealth transfer. Even people with rich parents will get priced out by those with even richer ones. The insanity continues.

Jon W, not sure what the UK retirement situation is, but in the US, what’s left of the middle class is utterly screwed come retirement time unless they get their finances strategically sorted before their health deteriorates.

Boomers are just discovering how insanely costly medical care is, particularly when a spouse needs specialized care. Unfortunately I see this every day: one spouse entering a nursing home can potentially make the other homeless, home care isn’t free unless you’re below the poverty level, and its not affordable unless you’re quite wealthy. Lots of dementia and strokes ruining whole retirements for both spouses and their working children who are pressed to assume their care.

Millennials who weren’t born well heeled are not necessarily going to be on the receiving end of the wealth transfer. The top brass of medical industry and the folks who hired Magnum PI to huck reverse mortgages will be raking it in.

Why would anyone pull back spending?

The federal government is spending massive amounts of money to keep the economy afloat and the federal reserve has shown they have no real intention of solving inflation. It’s been over two years since they started raising rates and they’ve solved nothing.

It’s not a bubble at this point. It’s the devaluing of the currency and robbing from the next generation to prop up asset holders.

Bingo. It takes more of a devalued currency to buy the same house. Is that a bubble? I am not sure.

During the HB1, we really did not have rising construction cost or labor cost thus prices could drop. The builders and developer and flippers were making crazy profits.

This time we have had a lot of inflation but I don’t think the builders are seeing the same profit margins. Sure house price can drop if construction material and labor wages drop. But will they?

That being said, there are some regions that house prices do not make sense. I live in flyover land and existing house prices are still only selling at $100 to $150 sq ft. I think that is probably 50% to 70% less than coastal and mountain regions.

Federal government spending is not keeping the economy afloat. To believe thus you have to ignore all of the private spending the continues unabashed.

As for your FED comments, you are just ignoring what they have accomplished. Inflation was nearing double digits when they started. We are no where near that all anymore while some of the rest of the world has flirted with recession and the U.S. has not.

Amen. When buyers’ “strike” though, real FMVs already decreased: you cannot force them to pay more. LA, higher end, residential RE is way too high. When other bubbles get holed, that RE will plunge in value due to fear, probably way too much.

For a laugh, read a certain media company’s attempts to hold back the sellers alone by claiming a certain country is flush with capital and doing well –as that country’s FDI and RE markets imploded. Brave petite billionaire!

Forgot to add what he would have claimed: “No, the Titanic did not sink; we converted it into a luxury, submarine resort!”

Does CS report the number of transactions for each city? Seems to me some of the stats could be of little value because of the small number of transactions.

No surprise the peaks for some of the cities given this data is lagging are just a few months after the first rate hike, just like the last bubble.

Yes, it reports the number of transactions.

These are HUGE metros, not “cities.” For example, the index for San Francisco is for the five counties that form a big part of the Bay Area (I listed them in the article).

For example, the index for San Francisco included 2,191 sales pairs for March (three month average of Jan, Feb, and March). But that’s still down a lot from the prepandemic years as sales volume has plunged.

Does anybody do a “Money Flow” Case Shiller with prices x number of house sales? Could be informative, or at least interesting.

Case-Shiller doesn’t give “prices.” It’s all converted to an index.

45 minute commute edge of the Bay Area city here to SF. Cookie cutter houses slapped together with frosting are selling for almost 1 million here. Realty sites not posting previous sales data so the potential buyer sees they are about to get ripped off. Up 400k in 4 years? Insanity ensues in this manipulated market.

Must be beautiful Daly City………How anyone could pay 1.5 million for one of those is beyond me but the power of inflation is remarkable.

NYGuy,

Excellent point about transaction volume being an important factor to take into consideration when reflecting upon price trends. A few loons at the margin are able to distort impressions if price is the only thing anybody looks at.

That said, *national* transaction volume is significantly down from the reign of ZIRP – at the 2021-2022 peak of paint huffing, national annual sales were in the 5.5 million to 6 million range (out of about 85 million existing SFH, I think…pointing out the thinnish liquidity of the SFH mkt…).

Post unZIRP, transaction volumes are down to about 4 – 4.5 million per year.

So, semi-normalized interest rates led to a 25-30% decline in SFH sales volumes.

My guess is that this number could fall quite a bit more, unless sellers-on-the-sidelines start to panic and finally increase for-sale inventories to something above the approx 60% of normal levels we’ve seen for 3 years.

What I take from this is that asset prices really aren’t going to come down much in most areas and that when rate cuts come, which they will, it will initially have little influence, but once they add up then assets could increase again. Not a great affordability picture for those without serious incomes or inheritances. If a fall does come then the cash buyers run in like the great recession and buy up homes as investment properties. Admittedly there are other possible outcomes but they seem unlikely.

Buying dips works until it doesn’t.

FOMO to FOGS can happen quickly

Life in the Fast Lane turns into Life In The Guard Rails. Happened to me in the late Eighties. House prices dropped 50% in the Farmington Valley area of CT (Avon, Farmington, Simsbury, Canton), some of the best RE in New England. All the people who went through that are retired or dead now. I’m 76. People think it can’t happen. It did, and it will.

Fear Of Getting Screwed?

👍

Don’t count on inheritances before your midlife crisis arrives. US life expectancy is 79.9 in 2024 according to the CBO, and average age at first birth is 27.3. That means you will likely be at least 52.6 years old when you get an inheritance as an only child, aka almost retired. 52.6 is an “optimistic” inheritance age, because single life mortality is lower than joint life (married) mortality, hence the difference in annuity payouts.

I consider myself “retired” long before age 52, but I fully recognize that I am the outlier and not the norm.

Most people don’t consider themselves anywhere near retirement at age 52. If you consider 52 to be “near retirement”, I am guessing you are very young.

I would say some folks with cash will run in just to buy a home at a more reasonable price,just a investment in their life/place to hang your hat ect.,not all who rush in on a market fall out to buy multiple properties though sure that would happen with lower pricing,me,just want the home for me self,that’s all.

I fear that when the 10y treasury yields drop at some point and mortgage rates continue their dance (drop along the 10y) it will just result in what we have seen for the past decades…..lower rates act as a tailwind for RE prices :( what are potential buyers gna do who are already priced out? How is this nightmare gna end? People say, just wait for a recession. As if we are not going to print our way out.

the other outcome is a renters collapse/exodus from layoffs which will pop the bubble.

I suspect watching this whole thing unwind is going to be a truly spectacular experience. While shortages are likely to continue for quite some time in areas already built out with single family homes, prices are likely to continue to soften as the economy weakens.

But looking forward 10 to 20 years, there is likely to be quite a glut of very large properties selling for a fraction of their original costs as the baby boomers begin to downsize, move into assisted living, etc.

Lord willing, I will be retired by then myself. But the glut in larger properties should hopefully soften pricing and rents across the board. On the flip side, we might continue to see nominal pricing remain stronger than expected due to continued monetary debasement.

We’re at least 5 years into the “Baby Boomers selling assets theory” not coming to fruition as predicted. It may still: McMansions, equities, etc. But as sounds as the theory may sound, the population of the US is still growing, household wealth still increasing, and all that money keeps the economy cranking. Do what’s right for yourself financially without going all in on any “this time it’s different” hypothesis.

And for those worried about inflation, TIPS are still yielding a real return between 2.1% & 2.4% depending on how far out in the yield curve you go. You’re not going to get rich on that, but you won’t be eating cat food in your golden years either.

I have an 82 year old neighbour….who lives in a big house with his wife. She is slowly declining with untreatable cancer. He has a very dodgy heart and type 2 diabetes. They are not well. Their kids were after them to move many many years ago, but they refused to move back to the city. Now, the home care nurse suggests they move to a nearby smaller city to be closer to the hospital and services. They refuse. Solution? Most of the house is closed off and they now have a younger neighbour come in to help with cleaning. They just bought a new Nissan for a safer drive to appointments, and just because.

In short, they are happy where they are, moving is a nightmare at the best of times, and they aren’t going anywhere they say over and over. Their house is two stories with many bedrooms, three bathrooms, etc etc.

I have many many examples like this, but the point is that if people are waiting for a big shift based on their expectations of what older people should and will do, don’t hold your breath. And with the adds for reverse mortgages, options to defer property taxes, etc the situation is even more sticky.

I was *that* couple, a year and a half ago, except I am very healthy and my wife was really sick. She passed away and I didn’t want to stay in the BIG house for many reasons, so I sold it (over asking) and moved into a new 1,459 square foot Builder Grade single level house (El Cheapo home, but sufficient). So I didn’t add to the statistics (essentially a house trade) and I paid cash.

The moving part was a HUGE PIA as I had tons of “stuff” to get rid off, and the new house was not completely done so I had to move in with my daughter for a couple of months.

Well, at least I learned that when I get real old (I’m 80 now) I won’t want to live with my daughter! (LOL)

BTW, I like this cheap little house!

about household wealth still increasing, this is kind of circular, as much of the wealth is based on the asset bubble. actual productivity increases, which is the building block for growth, has stalled throughout the developed economies. that means wealth isn’t really increasing, just the illusion of it.

To CH

WTF R U talking about? Population of US is growing? With whom? Illegal immigrants? Housing since .com bust EVERYBODY tought is the next get quick rich. Some did but majority are fucked.

Howdy makruger. YEP, this should be something. I thought the 70s 80s were crazy. Then came the first housing bubble. Then ZIRPing in the USA and lets shut down the worlds economies too and see what happens.

Get lots of your favorite snacks and drinks, this will not end for years…..

I startin to think the Lone Wolf charts are plateaus that will never POP.

So how does this end?

Rate cut mania caused the housing market in SOCAL to start back up with the craziness.

Right now, the middle class dream is dead. An entire generation locked out of housing and a middle class life due to irresponsible monetary policy.

Maybe the middle class millennials are making more money and paying up for housing.

I was just talking to another RE Investor and he said he is renting a home in Redwood City to four “kids” (under 22 that never went to college) their total income was almost $200K. CA is already at a $20/hr (~$40K/yr) for fast food workers and will soon have a minimum wage of $25/hr (~$50K a year for anyone that works in health care). I just found out about the new CA “healthcare” minimum wage from a guy buying up homes and apartments around (rough area that he hopes will gentrify) the UC Davis Medical Center in Sacramento.

After those “kids” move out, I’d imagine there will be $50k worth of damage to repair.

“After those “kids” move out, I’d imagine there will be $50k worth of damage to repair.”

Maybe that much per kid….it is California, you know!

Pennys from Heaven? We’ve gone from the days of borrowing daddy’s gas card to six figure graduation gifts.

I live in San Diego.

Both my neighbors are public servants in their 40s. They own houses that doubled in value since 2020.

A family just starting out would need a HHI of $400K to even qualify to buy a house in one of these neighborhoods. Hardly any millennials make that sort of money.

Where I am in half moon bay just about everything decent is going for more than 2 million. That is like a monthly payment of 15000 or 200000 per year rounded up for maintenance. So one should be making at least 600000 per year to afford to buy here. And houses sell here fast. One up the street for 3 million sold in a couple of weeks. I think the solution is for people to double up like they did in the past. That seems to be why the government passed this ADU law.

I think there a lot of people here who need to figure out what anchoring means.

There are plenty of Millennials buying houses. Some might be struggling to afford it, but that is no different than their parents.

It will end when YOU, ME AND THE REST OF THE PLEBE start boycotting greedy companies CEO’s and their masters. Stop complaining and start acting.

What a freaking cruel joke….guess this time is different after all. At this point, I have more faith in an asteroid hitting us and giving us a dinosaur reset that to see these markets correct to any meaningful level…

Los Angeles metro

Month to month: +1.7%.

Year over year: +8.8%.

New high, 2.5% above the prior high in May 2022.

San Diego metro:

Month to month: +2.2%.

Year over year: +11.1%.

New high, 2.4% above the prior high in May 2022.

All it takes is an uptick in unemployment and a drop in the stock market, i.e. a recession.

But no, you’re not going to get a correction with the stock market at all time highs and so much FOMO – gotta buy before the fed cuts rates and prices jump another 40% mindset in the general population.

LA and San Diego aren’t the only places with houses for sale.

Boston, you’re killing me. I really don’t understand where these buyers are coming from, unless it’s all foreign money. Wages haven’t gone up enough.

My SIL had a home just down the street sell for 1.7 in Tustin in Orange County. Cash. Chinese buyer. These were $600 range in 2019. Where I live I’m seeing a whole ton of mainland Chinese everywhere now. Not happy but it’s reality.

@Tom.

When the world is on fire, folks run into the US for safety. These folks are the wealthy and educated Chinese, not the mad dash across the border types. Think of it this way, these folks (the educated and the dregs) know the border is closing when Trump wins this fall.

If I had to choose, I rather have educated and moneyed folks in our country, rather than these dregs fleeing from their mess into our mess. Good luck.

The Chinese love Irvine.

As we said, this data here is months behind. Volume is way down, and supply is way up, active listings have been surging to a four-year high on slow sales and rise in new listings, and price reductions as percent of active listings were at the highest for any April in the data by realtor.com going back to 2017:

https://wolfstreet.com/2024/05/22/home-sales-whacked-by-mortgage-rates-active-listings-price-reductions-jump-to-highest-in-years-but-sales-of-high-end-homes-surge/

The data is behind but not that behind. It reports moving averages of transactions in the past 3 months. Interest rates have now risen significantly for 2 years. If multiple large metro regions are hitting new all time highs despite interest rates being double what they were (even during rate cut mania) then I don’t think we can just blame it on lagging data.

This is where you and I disagree on whether the Fed is being aggressive enough with QT. The Fed is obsessed with the downsides of moving too fast such as the repo market blowing up or the economy being pushed into a recession. But they don’t seem to care about the risks of moving too slow. Keeping the housing market too high for say 5 years because Powell wants to be “gentle” with QT means lots of people delay significant life choices for those 5 years which can have big effects. How many children will not be born in those 5 years because would-be parents decided they can’t afford it? How many people decline moving for a job due to housing costs, thereby decreasing overall productivity growth?

If the repo market tightens some poor REIT blows up? Boohoo. They’re paid to take those risks and should be able to handle the fallout and recover. But someone who decides not to have children is a decision that has ramifications for decades.

The Fed seems to understand acting too slowly when it’s Wall St profits on the line. God forbid they have a bad quarter. But it seems to think that everyone else has the ability to spend years in an irrational market without permanent damage to their lives.

And now that they’ve announced they’re slowing QT despite no evidence that the financial markets are hurting whatsoever, they’re basically condemning young people to delay their asset building, family building, and career building for another few years so that those poor poor hedge funders don’t have to suffer a theoretical setback to their health.

This has literally happened to us. We’ve delayed having a second kid because we wanted to provide housing stability by buying first – which didn’t work out – and now rents have gone up so much we can’t really afford a larger family even if we give up on buying. At our age, that probably means only one kid.

The strain this has put on the family is in serious danger of breaking it up completely.

Your comment is one of the best I have seen. Renting is a good option at this point. People were I am in Ca are happy to get 5000 to 6000 per month for a 3 BR property that would sell for 1.8 million. The next door neighbors here, for example, who have one child. There are a lot of empty houses in California. You are either going to rent the house or rent the money and if you pay the rent it is pretty hard to throw you out in Ca.

All true but also if the fed implodes the economy. Then you have the same problems in a different way. Not arguing either way i will leave that to smarter people then me……

According to my pet theory that nobody else on these comments seems to want to speculate on, some houses are being wash traded just to increase the comps for “real” sales or HELOCs. Since the Case-Shiller only measures houses that have been sold multiple times, those wash trade houses are overrepresented in the data.

Is there any evidence of this at all?

Buying and selling a house involves lots of frictional costs, even among people trying to do it cheaply. Doing wash sales would be really expensive and I would think there is better use of capital.

Boston has almost zero competition from new builds, hence existing home prices are more stubborn vs other areas.

Also: the CS ‘Boston Metro’ includes a bunch of wealthy areas of NH, including the Seacost and towns near Lake Winnipesaukee.

There’s more to New England than Boston and the Hamptons.

I’m wondering what the Chicago metro area encompasses. The whole area is experiencing decline as property taxes are ever increasing. People move out, property values decline, and they raise taxes perpetuating the cycle. I can think of 2 things affecting it. Affluent areas of the North shore, Schaumburg and Naperville, and if they include Northwest Indiana in the Chicago Metro area, which has seen large gains.

It’s the Chicago-Naperville-Joliet metro. It includes the counties of Cook, DeKalb, Du Page, Grundy, Kane, Kendal, McHenry, and Will.

“The whole area is experiencing decline due to high taxes”

Maybe you’re just not paying attention to the data because not only has the metro area grown since the last census but home values are hitting new highs.

Guys I’m dying here, I don’t know what to do! Just moved to D.C and have been looking at houses to move in! Hopefully expand this 2 person family. But cannot find affordable homes to buy and on top of terrible rates, was thinking of maybe putting off for a while and take a look around October where there aren’t many buyers. I feel stuck as this is a difficult decision. Should I or shouldn’t? I’ve been outbid at every offer I’ve put down. For houses that shouldn’t be worth nothing, poorly constructed, terrible conditions

“on top of terrible rates…”

Mortgage rates are not terrible, they’re now historically normal to low-ish. They’re just not ridiculous rock-bottom anymore.

You might be right, I am just not familiar with the US market. I am more familiar with the markets of some countries in Europe, so it is hard for me to comprehend the way things are perceived here. Even then, the rate do look bad to me

Thanks for your information and hopefully the Fed and QE for almost 2 decades will be off the table for decades to come .

1. Don’t buy what you can’t afford.

2. Be honest with yourself about what you can’t afford.

3. My opinion- lack of money is a good reason to delay having children, not being a homeowner isn’t.

Since not being American the mindset when it comes to spending is very different. Debt isn’t a common thing where I come from(France) be it student loans, credit cards, etc. the only real debt you ever get into is for a real estate. Hence the prospect of debt is quite daunting, even when we have constricted our budget well below our capacity. On top of that having to work with lenders feels like being preyed upon by predators constantly manipulating us to push our budget since ‘we can afford it’. All in all it hasn’t been a good experience.

Well, in the U.S. for whatever reason, real estate is about the only investment where people act like there’s no possible downside. There’s a lot of scammers in the industry too, I have no idea why. Good luck!

Wise words. We decided to have kids and rent in early 2021 when we thought housing prices were too high, and that they had to come down (they would continue to go up another 30%+ here in San Diego County). I was upset for a while, especially when my landlord kicked my family out because his own daughter couldn’t afford a home and needed to move in. Fast forward two years later and here I am with a bigger family, still renting, with a landlord that really appreciates us and hasn’t raised the rent once. I feel a lot better now not worrying about affording a house so I can use that money for vacations and visiting our families, basically giving our kids more experiences instead of being seriously house poor. I can easily move for a better school system if needed or move to be 30min closer to a job without a huge increase in overhead.

You forgot, “Live in a tent”.

The California Association of Realtors just published the income needed just to qualify for a loan, assuming a 20% down payment. That qualifying household income is $349,200/yr in Orange County to buy a median priced home.

Why are you in DC? Ahhhh another lobbyist. We have enough, 4 or 5 lobbyist for every congressman. You contributed or will contribute to more of the USA demise. Every empire falls, and very bad.

I’m so confused what would be the right time to buy in DC because it seems like the prices never fall

So true, as long as the US Gov spends money like no tomorrow, home price in DC won’t go down.

We’d seen the word bubble here for a while now. If you read too much econ news, your mind got stuck and wasn’t able to pull the trigger to buy a home last year. Now, you’re looking at another 5% increase in home price and the interest rate is not budging.

And every time someone so much as whispers rate cuts it catapults the prices back up and then the rates don’t back down.

DC had less of a spectacular rise in bubble number 1, and less of a burst as well.

Still expensive, but for QoLife, check out Frederick.

The north is completely priced out, so is Arlington, Alexandria. Literal boxes of homes that have terrible conditions like mold, fire damage are priced around 400,000. And the SE, so close by to downtown DC but a terrible neighborhood. Next best option I suspect is national harbor and Fort Washington. Especially national harbor. The only place that is still rationally priced and at the moment of what I have seen so far it’s a 50/50 sale of houses over and under asking price.

Just look at history, there was a bubble and bust less than 20 years ago. We have another bubble now that can and probably will bust again. To me, waiting gives the chance of a better deal and a way to oppose the senseless, damaging QE that was carried out by the govt and the careless risk on behavior of buyers.

Go back home

Wild ride. It really does feel so unknown and out of sorts like a puzzle with a bunch of pieces that just don’t seem to fit as expected. Apparently I am no puzzle master or prophet. Always looking forward to the next article! Thanks wolf.

I’d like to take a moment to appreciate wolf’s wisdom when all this started:

“Inflationary mindsets are hard to break once they become imbedded in the population.’

I’m thinking that is likely what is going on here. I’ve been a lower wage worker for the past decade. Granted I moved from a depressed rural southern area to a MCOL area but my wages went from 10 dollars an hour truck driving as late as 2019 to 34/hr. Some of that is due to experience and relocating but that is absolutely phenomenal wage growth. When us bottom feeders are making that much more money everything is going to become vastly more expensive.

My group of wage earners aren’t buying houses unless they’re married or have significant help from family but they are renting and getting raked over the coals there and also blowing money on toys.

I’ve said it before and this data is only further causing me to about-face. I don’t see the housing market breaking anytime soon. And if it does, it will be too little to make a difference. I think prices have risen so much and so many people have leveraged so much of their financial situation on this real estate bubble that the govt is in no position to allow it to pop. Another case of too big to fail; aka bailouts.

I think the US has come full stop into the Western world when it comes to housing. Western Europe, Canada, and Australia are all murderous housing markets to navigate as a working stiff. Seems the US is finally catching up.

Don’t think that there are no declines in Europe and that the market is in flourishing health.

Complete, total collapse and absolute economic, social and banking disaster in Sweden. Dozens of builders have already gone bankrupt there. In Stockholm, house prices fell by 22% in 12 months. The situation in Frankfurt is also tragic – 16% total collapse. Amsterdam 14%, London 14%, Munich 14%, Sydney 11%, Warsaw 9% . Stable destinations such as Hong Kong also saw a 7% decline”

Maybe but if you make 1 dollar a day and a loaf of bread drops from 5 dollars to 3 dollars, it’s still unaffordable and obscenely overpriced.

I don’t pay very close attention to the European market due to how different it is but I know Australia and Canada are very bad off right now. I’ve talked to a few Canadian truckers, (the rare times they speak English) and the pay is brutally low while housing is more costly than the US on average.

These little minor dips in prices here and there are little more than noise unless it turns into year after year steady declines.

Wolf’s data is showing year over year increases consistently and only a sub-10% decrease since the 2022 peaks. And only in the handful of markets that haven’t hit all time highs recently. I know in my area, housing has went on a tear again, we had some softening during the winter only for it to come roaring back. I don’t see the 2022 bidding wars to the same extent nor the “everyone became a realtor” but the prices speak for themselves.

We shall see in due time. Housing is a slow moving thing. But I maintain my previous point, I don’t think the g-men will let the housing market turn into the bloodbath it needs to be. Far too many people have built their lives around it. I’m beginning to think the US housing market is going to follow the Canadian example.

@Trucker Guy: The g-men may not have much of a choice this time around. Previously, they were able to have a free hand with China and the rest of the world buying US Treasuries for their foreign reserves. China is dumping a lot of them now and the rest of the world is itching to move away from USD.

Further, just within the last couple of weeks, I recall that a Fed governor saying (and I am paraphrasing here) that most of the inflation is tied to housing costs and he doesn’t see any way inflation comes down without housing costs coming down. I recall one of the posters here saying that the Fed finally seems to get it.

So I don’t think that the Fed is going to bail out all the markets -CRE and consequently some banking, and housing. This time will be different – and yet not so different from previous crashes.

30 Year Fixed Rate Mortgages are trademarked in the US ONLY.

Therefore, there is no major collapse in prices for you.

It might not.

So there could soon be a bloodbath in Canada and Europe and a little in the US

As you said and I agree with you “Housing is a slow moving thing.”

So we’ll see..

Trucker,

I just read an article on affordable RE in Canada…before I read Wolf’s latest (excellent as always). One quote stood out in the CBC article, and I guess it is an agent quip. “Drive until you qualify”. That is what growth trends indicate what is happening here, people are ditching Toronto and Vancouver for Edmonton for God’s sake. Now Edmonton is nice is along the river in the old town, but the rest?

Another thing I see is younger people looking for careers in portable areas, as opposed to being forced to live in a high priced city. Throw in the threat of AI doing all the coding and mid level management drudgery in the near future, maybe even some truck driving but it sure won’t be logging trucks :-), younger folks are looking at durable options. We’ll always need medical based skills, builders, plumbers, mechanics, stuff like that. Big surge into nursing and the trades.

Great observations/comment. And it’s true what you say: there are a number of people I know who ten years ago were hand-to-mouth who’ve since retooled the shop and boosted their salaries accordingly. But in some cases, instead of it advancing them, it seems like it’s just kept them from totally drowning.

which is why people are so sour on the economy. yeah everyone has a job if they want one, but that job that they have for many middle class and working class people doesn’t make ends meet.

Exciting times for these vibrant cities hitting new highs! The growth in Miami, LA, San Diego, Boston, and Chicago is truly remarkable.

This sky high housing market is why I think so many 25-30 year-olds are frustrated with the economy. Many (but not all) see the American dream of home ownership moving farther and farther away. Anecdotal here but I have two friends with good jobs in their mid-20s who keep getting overbid by $10k plus or losing out to all cash offers in areas an hour away from Boston in what used to be starter home areas. I’m also seeing 2-family homes in Manchester/Nashua NH selling for close to $600k when the same homes were $240k in 2018/2019. To me the math still doesn’t add up here but nothing seems to give.

I’ve pretty much given up on it myself. I’m 30 and making around 90k a year. Within the next 6-8 months I’ll be moved to a different sector of the company and will pull in 110-130k/yr depending on the bid I get.

I’ve saved plenty of money in the past year or two and have no debt but when I started to look into housing the banks basically laughed me out the door. My bank won’t finance mobile homes and anything with a foundation that doesn’t have a massive HOA fee or lot fee are 400k and up. With the massive rate jumps to boot. Got a better job to make more money to qualify for more but I’ve another year to really be pulling in an appreciable difference. By then the market might be at 500k and 10% interest rates.

Everytime I get a little more ahead and make smarter decisions, the more outside factors screw me over. It’s very very easy to get bitter. I’ve stopped caring. I’m just letting all my money get dumped into the casino…. I mean stock market. At least the idiotic bubble there is paying me back some. For now. In the meantime most of my real estate learnin’ comes from the depressing stats posted here on — WolfStreet.com, where we learn the stories behind Business, Finance, and Money!

Suggestion: Go bank shopping or look at credit unions.

Also, newer mobiles are now called modulars and are every bit as good as new construction single family. They also qualify for the same mortgages. I have built many many structures from single family to apartments/condos. Modulars follow our building code and have new home warranty protection. The older concept of flimsy crap shack trailer homes might exist in the boonies or the warmer south, but it is really a bygone era and just waiting to all fall down or blow away.

Now off to work. Cheers.

No they are not the same. A mobile home can still be moved and taken elsewhere and is not built to local codes. A modular is built to local codes and is put on a permanent foundation. The ins is and mortgage rates are different as well. There are still many mobile home manufacturers throughout the country, including the northern states. Drives me nuts to hear people denigrating a certain area of the country out of their own ignorance.

The only thing you said that actually is sensible is for him to find a credit union.

John,

I didn’t mean they were the same, but it did come out that way. Apologies. My point is that once straight mobile home manufacturers now offer mainly modulars and sell very few ‘trailers’. As for trailer parks, they are on life support when property values increase with tenants getting eviction notices. Many parks do not accept older trailers. They have to be newer ones.

Two people on my street have mobiles. They cannot even get insurance on them. One has been upgraded with 200 amp service, a heat pump, etc etc. just two years ago. I built them a new kitchen as well. They cannot get replacement or fire insurance on the place. A local park was just sold and a 4plex is being built in its place.

With our colder weather in Canada and high heating costs, gone are the days of 2X3 stud walls with a wee bit of spray in foam insulation being okay. And yes, I have worked on tons of trailers of the old variety. They are crap. I know what I am talking about as a carpenter. Plus, there is a lot of rot on the corners as the moulding leaks pretty much always. And the roof corners. The windows.

Trucker – There is another option of On-Frame Modulars which are still set up with the metal chassis under it but the superstructure is built to the Modular code, with 2×6 walls and a roof that has the appropriate pitch and overhang. Look for the certification sticker that says it’s built to modular standards. Put one of those on a concrete skirt foundation and they (around here) will loan and insure it. I am not sure how many manufacturers are building these still but ask about the option anyway.

When I say concrete skirt I mean block wall skirt btw…

Search for a mortgage broker who can shop multiple mortgage and loan options

I would suggest changing your perception that the markets are a casino. The markets are often the average person’s only shot at truly getting ahead. If you invest in low cost total market funds and hold forever, you will do quite well over a long timeframe.

yes, as an outsider, i’ve noticed a parallel between trump’s handling of covid and biden’s handling of the economy.

in both cases, it’s not what they did or didn’t do. it’s that they appear to have no empathy for what’s happening. people don’t expect you to have no problems, but they don’t want to be lied to and told there is no problem.

trump going on about how covid was under control turned off people, just like biden telling people how great the economy is turning off people.

Have they looked in Fitchburg or Worcester lately?

Too far from work for both of them. Having said that, Worcester is pretty expensive now. I remember 3-families selling for $165k 10-12 years ago now going for $600k +

It would be great to see sales volume (and maybe also “for sale” volume) charts included with the price level charts. In my area, it seems the prices are going ever higher and the homes for sale volume is too, but the number of homes that actually sell seems to be pretty low. This reminds me of major tops in the stock market, but hard to tell without seeing the charts.

Sales volumes are way down.

https://wolfstreet.com/2024/05/22/home-sales-whacked-by-mortgage-rates-active-listings-price-reductions-jump-to-highest-in-years-but-sales-of-high-end-homes-surge/

I think we are in the beginnings of a 30 year Japanese style real estate deflation period. We are at the same point as Wiley Coyote when he ends up over the canyon and he keeps spinning his legs and for a bit he hangs in thin air but sooner or later reality catches up with him and down he goes.

The Fed, The RE Investors, The Flippers, The Landlords and Realtors@ are frantically spinning their legs and yelling out ,” everything is fine, we are hitting new highs” while interest rates creep higher, the federal deficit grows like a thistle in a horse pasture and the US’s geopolitical position in the world shrinks like an ice cream cake at an office party. Hang on!

It would be interesting to get opinions as to why Chicago in particular has been much slower to soar to absurd price heights since 2000.

(Doubling in price vs. tripling or quadrupling…)

Illinois has bad demographics (shrinking) but that is really only a marked trend in last 5 or so years whereas Chicago has been a (smart) price laggard for pretty much the past 23 years.

Does Chicago (and metro environs) allow much greater build density?

(Still hemmed in by water on one side like a lot of mega-price metros, though)

Are those in the Chicago area willing to live much further away than those in other metros?

I tend to think there must be organic causes for why Chicago has resisted a fair amount of the post 2000 price insanity.

Nobody wants to live there.

Sure…but NYC, DC, and Boston aint picnics either…for the middle mass of people who have to buy in, in order for macro needle to move.

There is the magnet of high-pay jobs to offset the cold, grimy, low quality of life…but Chicago has high paying jobs too.

I suspect it has something to do with freer SFH supply conditions in the Chicago area…but I’ve never seen an article highlighting it.

I can’t speak for the other two, but Boston is highly gentrified now with very high-earning people with good Jobs. Even some of the former rough neighborhoods are very expensive and full of mostly high-earners in their 20s-40s

They’re much less restrictive about building density. The Chicago downtown area at one point was the fastest growing residential region in the country, because the city is generally tolerant of high density housing in the city core.

SF would have a freakout if someone built an ADU over their garage. Meanwhile Chicago was approving multiple 60 story buildings every year (not all of them get built if eg funding falls through).

“SF would have a freakout if someone built an ADU over their garage.”

Once upon a time, yes. Now ADU approvals have been streamlined and they’re happening all over the place.

“Meanwhile Chicago was approving multiple 60 story buildings every year”

SF has about 70,000 housing units in the pipeline, nearly all of it multistory to high-rise. There are huge areas that are being redeveloped, such as Treasury Island (once a Navy property); Hunters Point/Naval Shipyards (an old industrial and military zone with nuclear contamination whose cleanup turned out to be more complex and scandal-infused than expected); the old Potrero Power Station; the Stonestown shopping center (3,500 housing units), etc., etc. There are a bunch of them. All these are mega-projects that take years to pull off. Plus there are lots of smaller projects. SF (7 square miles, 820,000 pop) is just a fraction of the size of Chicago, but is has a lot of old industrial and former Navy land that is being redeveloped.

As with developers everywhere, funding issues have cropped up due to the higher interest rates, and tightening of CRE lending by banks, and many early-stage projects have stalled because developers cannot get funding — at least not at rates that they figured into their models.

Property taxes are very high. If people are buying a monthly payment, they have to consider setting aside a grand a month for property taxes. This level of property taxes is very common in Lake, McHenry and Dupage Counties. This keeps prices down.

I feel like this data may not indicate a whole lot at the moment given the current freeze-up in the housing market that Wolf has pointed out previously with the total transaction volume plummeting since the rate increases.

What would really be useful would be an apples-to-apples price comparison based on selling price vs. house square footage, but I’m not sure if any such index exists.

These indexes are apples to apples. They’re based on the sales-pairs method. So when a house sells this month, the price is compared to when the same house sold last, maybe two years ago or maybe 20 years ago. The price difference is weighted by the magnitude of the time between the sales. And other adjustments are made. I linked the methodology towards the bottom. You can read all about it. Sales volume should not have any direct impact on the sales-pairs prices. But the index is about 3-4 months behind, and that’s a big problem.

Ben,

Square foot price alone cannot give you any indication. Monthly payment is a better guide. I sold my house in NY, moved to TX and bought another home. In order to understand if I was getting a better deal and to see if the home I was buyign was cheap/expensive, I broke it down to $/SF/Month. Example: $3,000 monthly mortgage on a 3,000 SF home = $1 per SF/MO. Folks in the commercial real estate world work on these terms day in and day out (mostly $/SF/YR). Investors who rent out homes/apartments/etc typically use the $/SF/MO metric.

In the end, cash flow is king so even if you’re getting a great deal in terms of $/SF/MO, you could be spending too much because the house is too large (considering other factors family equal). What matters to most people is how much money you end up with in your bank account at the end of the month for discretionary spending.

Most people I know do not break it down into these terms, they look at monthly payment. I sold my house in NY for $300 per SF, bought a house in TX for $160 per SF. The house in TX is 50% bigger than the house in NY. Details matter.

No matter what the data tell us, bears will keep bearing and bulls will keep bulling.

The bears see this data and say “prices going up?! Well that is even more evidence of the crash we’ve been predicting for the past 5 years!”

And when prices drop, bulls say there’s more scarcity than we realize, open houses are packed and surely a new peak is coming.

From where I’m sitting, the bulls continue to be right, while the bears watch their prophesy of a $150k house slip away indefinitely.

I bought a small 2 bedroom 1 bathroom house that I could afford last year, when commenters here were blue in the face screaming about the crash around the corner. Glad I didn’t listen.

Oh, I more suspect anyone with basic numeracy skills just wants to see things suddenly start making sense, and then they get impatient & wax pessimistic every time an index zags up on its inexorable, painfully slow slalom back down to the mean. It’s interesting to behold…it’s like a game of he loves me/he loves me not, where every petal plucked results in either gonzo euphoria or a massive coronary.

Incidentally, I’d wager that a lot of these sales in areas where local would-be first-time buyers are scratching their heads, wondering how these clueless jockeys are managing to overpay by shocking amounts over-asking are often just instances of lucky pandemic sellers capitulating and jumping back into the market after being on the sidelines for a few years with their winnings. I’ve seen it right here in the comments — do you really think some gimper talking about having $500K sitting around in cash to put down on a house is someone who saved that money by way of their labor & deferred gratification?

Probably not?

You will find out when it does crash. And it will happen.

People in this blog are waiting for this crash since 2016 or so..

Now, you decide, was that wait worth it ? and compare the homes prices from 2016 to Now.

“No matter what the data tell us, bears will keep bearing and bulls will keep bulling.”

A comment like this deserves more love.

Unfortunately there are lots of people who approach stuff like this with preconceived views and then simply cherry pick the information that reinforces that preconceived view and focus on that rather than using the data to truly try to understand what is happening.

@Pants Explosion I agree with you that most (over half of the population) is locked into a “permabull” or “permabear” worldview (in a weird way like so many are locked into political views that are 100% RNC or 100% DNC “talking points”). Congratulations on buying your house. This site seems to have more “out of the box” thinkers than others (who will understand that just because homes are going up near Nvidia HQ does not mean we are entering another bull market and because prices are dropping fast near a closed auto plant does not mean we are in a global bear market)…

Howdy Youngins. Bubba is pretty sure more lenders are offering

” NO money down mortgages “. Just sign your name for the American Dream…… UWM.

Message brought to you by the ANTI Silly Squirrel Association. ASSA

I’ve started seeing adverts from lenders for loans with rates of 6.5…must be with some serious point buydowns.

Howdy bulfinch We all need to pay attention to the Lone Wolf Charts.

Will the ones above ever show a downward trend???? We shall see.

Just have to live long enough I guess.

I think that much is a forgone conclusion. How long it takes for the fat lady to hit that note is something nobody knows.

Mortgage rates are going much higher than 8%.

Why do you feel so certain of that?

Because higher for longer.

Your “Howdy Youngins” is annoying as hell.

Howdy codedude. Thanks. Its meant to be.

Finally !

DFB admits his posts are largely passive aggressive !

I still think DFB is a Bot.

You’ll learn to just scroll past his hokey drivel soon enough.

Scary data out here.

Perfect storm of 4 factors.

Mass commoditization of the housing market. (YieldStar, AirDNA, hyper low fed rates etc)

Millennials (myself) moving to home buying age.

Excessive and hyper restrictive zoning.

Egregious soft costs demanded from cities (sewer, water, permit fees adding $50k to small 900 sqft projects).

The way out?

#1. Liberalize zoning. Abolish minimum lot sizes, allow small builds of 500-900 sqft homes on sub divided lots ~1500 sqft instead of 5000sqft. Reduction of land costs is very important, way more important to a projects cost than then often talked about labor cost.

#2 Legalize backyard cottage homes and allow duplex, triplex zoning by right.

#3 Legalize light tough businesses in residential areas to drive down commercial rent induced inflation.

#4 Speed up permitting need 60 day shot clocks instead of 6 months. Time is money.

#5 Scrub out all regressive soft cost. Costs should be made whole with property tax not impact fees.

#6 Remove quacky pseudo science parking minimums which destroy so many projects.

#6 Implement and wait.

If the above workout, our housing system will have a chance to actually be anchored to something instead of being yo-yoed by the fed.

Homeowners will be able to tap into their equity by adding units or subdiving and selling of parents of their land, instead of just hitching themselves to the ‘infinite’ growth mindset of fed rates.

My 2c.

@Deep Dive: You are assuming that the powers-that-be want to do something to bring home prices down. Methinks it is a completely wrong assumption – in fact, I think it is exactly the opposite.

We’re talking about a very organized consortium of industries (banks, mortgage lenders, developers/builders, realtors and appraisers) which have every piece of data needed to keep the supply of housing at a level where they can make the maximum amount of revenues and profits. Yes, there are smaller builders but they follow the market. The big guys set the market and everyone else including the Federal, State, and local governments just play along.

@Deep Dive a typical single tennis court is about 5,000sf inside the fenced area (the doubles playing court is just over 2,800sf). Do you really want to live in a 900sf home surrounded by three other 900sf homes on four “lots” a little bigger than a typical fenced area with a single tennis court at a park (why not just buy a condo)? P.S. Cities are never going to give up all the “fees” they charge since they like the money more than they like making it easier to build.

I see people that paid a half million for a tiny house (meaning young people that have some means) that have 25 sq. ft. of front yard that is all weeds and blankets hanging in the window where blinds would normally be (meaning they give the appearance of being classless trash).

There is a reason for NIMBYism. And even if you don’t like rich people, at least they usually take care of their property.

Fees are what they are. When has any entity not screwed you on any fee when they could?

I don’t mind rich people — I just tend to find the reasonably solvent much more takeable.

And I’ll take blankets in the windows & weeds all over versus the increasingly homogenous blah-fest of covetous frothing Joneses laboring to help keep aloft the lead balloon of the US economy any day. The bland leading the blind. What a lost bunch.

“Liberalize zoning. Abolish minimum lot sizes, allow small builds of 500-900 sqft homes on sub divided lots ~1500 sqft instead of 5000sqft.”

Two comments:

1. My house is 960 sqft and my lot size is ~8700 sqft. There’s no way in hell you could fit three more of my house on my lot. Remember, the actual footprint of the house itself is much larger than the *interior* square footage listed in the county records. And a driveway also uses a lot of the space.

2. You should take your argument a step further and suggest abolishing protected conservation land such as forests and wetlands.

The funny thing is all the replies to my comment prove my point.

A lot of interia against lowering prices, being said by people likely with high home prices.

But regardless land use is mandated at the local level, most of these are local fixable issues with a little bit of local advocacy.

Which I’ve partially completed these in my city.

We shouldn’t be preaching what others should live in that’s the definition of soviet top down planning that got us into this mess.

If you want space buy it I’m not denying it and neither are these changes.

We just need to get over telling people what they can and can’t do with their land.

Currently our housing comes in Kirkland sized portions all I’m saying is allow people to buy and chew less.

A good example is to research cottage courts housing, that would give the other replier a chance to see how cute 4 small homes on a tennis court sized lot actually is.

Also I hope I’m mistaken, but if you’re implying your grass around your house is equal to a conservation easement in importance that’s comical.

I live in Florida where wetlands are being destroyed at a rapid fire rate to make way for Lennars latest lame product.

Gentle density is the key to solving this.

Lennar builds what people want to buy. If people wanted cottage court homes, they’d build them. That’s the business they’re in. It’s cheaper for them, but that always doesn’t equate to affordability of the final product.

Look at “Pillars” in Fountain Hills, AZ. Similar concept to your cottage court. Last I heard, it was fully leased out. But you honestly couldn’t pay me to live there. It’s claustrophobic.

IMHO, and based on developments I’ve seen where the zoning allowed increased density, all it results in is the person that owns the property with sufficient space to subdivide gets to keep his current home and turn the rest of the property into instant cash. Prices don’t necessarily drop to what one would consider affordable… and even a small place (a friend of my daughter lives in 400 square feet) isn’t cheap to rent and, based on what that property is now worth (since it has 3 dwellings rather than one on the same lot) the only economic benefit was derived by the previous owner.

I think you are ignoring the fact that land use affects more than just your land.

The way your land is used also affects the neighborhood in many ways. You may refuse to see this, but it doesn’t make it any less true.

“A lot of interia against lowering prices, being said by people likely with high home prices.”

Yes, greedy municipal gov’ts love higher home prices because they get to raise assessents and bring in more $$$. My city just assessed my house at $15k higher than last year even though its exactly the same house – no improvements. I think this is BS.

“A good example is to research cottage courts housing, that would give the other replier a chance to see how cute 4 small homes on a tennis court sized lot actually is.”

But we already have plenty of condos which satisfy that need. That’s the point I was trying to make. If you’re trying to squeeze a bunch of units into a small plot, it makes a lot more sense to have shared walls.

“I live in Florida where wetlands are being destroyed at a rapid fire rate to make way for Lennars latest lame product.”

…so you don’t want more homes to be built and add supply to the market? I’m confused now. This sounds like a good thing if you want lower home prices.

Where to start… “eliminate egregious soft costs”? How so? There is a hard cost associated with effluent disposal and water supply. Some city sewage systems can’t handle the volume they already have. You do realize there’s pipes in the streets, don’t you? You do realize that there’s science associated with how all that works…. and overtaxing such systems can cause backups into homes. Whoops.

Make zoning looser? Sure! Why not? Imagine that I live next door to you and decide to park a bunch of trailers in my yard and rent them to improve access to “housing”. Would you have a problem with that? The “loose zoning” thing has been tried before. That’s how you get shanty towns and slums. That’s why some people seek refuge in HOA controlled communities.

Small industry/business in residential? I guess you never had a body man do “siders” in his garage next to your kid’s bedroom window. Of course, people always do the right thing… Yes, they do.

Parking…. ummm…. not everyone is going to bicycle around town. Would be hard in Boston or Chicago in January.

“Pseudo science parking requirements”: Explain that to someone who is physically disabled or has three kids to wrangle. Cars do make nice lawn art, but you need a yard to park them on… you just built your lot out.

Power distribution. Brown outs anyone? Nothing wrong with the power grid, is there?

Urban flooding (increased density / hard surfaces / roof runoff create more water volume. Where will that go?).

Other infrastructure like “food deserts”. Inadequate surface streets. Recreation areas/parks for kids. Schools. Fire. Police.

The housing you describe is already being / has been built. For example – In Redondo Beach, CA (for example) there are “three on a lots”. On street parking. Postage stamp patio. Gangways to access your house. The infrastructure i.e., exterior lighting for gangways, the walks, landscaping, irrigation, common property liability insurance – (common property would be things like easements to get to the units in back). Then there’s fire codes. When you build higher density, fire codes would likely require that you have sprinkler systems in each dwelling (even out here in the middle of nowhere they’re now required by code). Price one of those lately? (IIRC, the water line from the city source has to be larger than a current residential meter – which would require digging up the street to replace). Firewalls when buildings are close together… fewer windows for privacy.

There’s so much wrong with your “solution” it’s mind boggling.

DD is arguing for ways to increase density in urban/suburban areas directly outside city cores. But these areas are not setup to handle the density for all the reasons you point out.

Building farther outside the city makes more sense. The builds can still be small and affordable.

I wouldn’t recommend building outside the city.

We need to add density inside the limits of our current built infrastructure to help absorb the costs our municipalities currently carry.

Right now we have massively overbuilt our infrastructure hence why we ‘needed’ a federal infrastructure bailout via the infrastructure act for all our failing bridges and roads.

It’s time we thicken up our cities and suburbs and start having municipalities straighten their finances out and cut some of this gov debt out they are liable for.

Look up the Strong Towns movement to understand the finances or GIS data from Urban3 to understand what I’m talking about.

(I’ll stop here Wolf to not hijack the post)

But lots of people don’t want to live in that kind of population density. Many cities are already overcrowded and have infrastructure that can’t handle more density.

How do you address that?

#7: Remove all women from the workforce. This has driven real estate prices (much) higher over the past say 7 decades. From say 1950 up to now onwards the % of women in the workforce has gradually gone higher and higher.