Condos in Toronto hit 28-month low. But Vancouver house prices only -3.9% from peak in 2022. Calgary house prices jump to new high; oil boom helps.

By Wolf Richter for WOLF STREET.

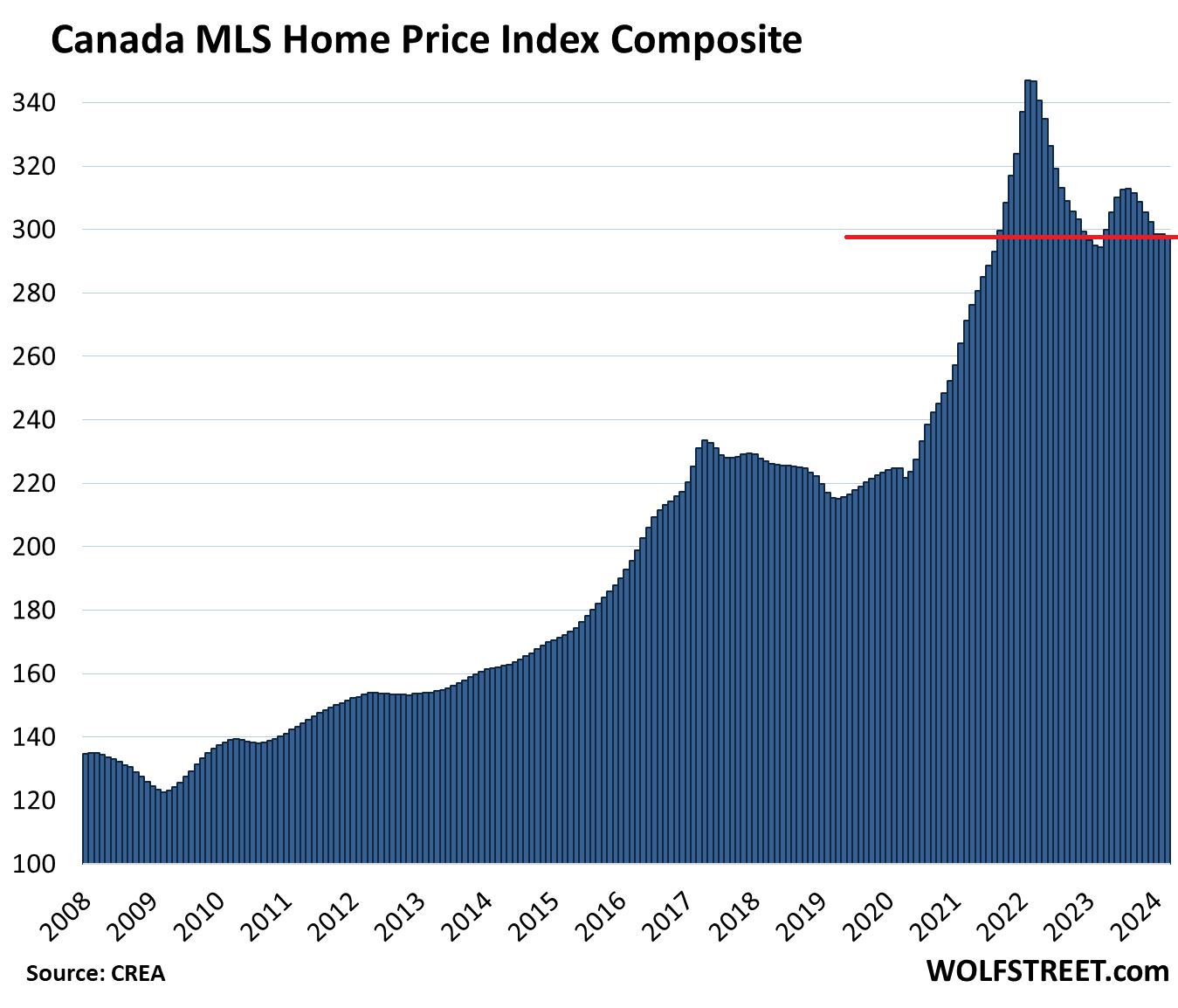

Condo prices in Canada fell 0.7% in March from February, seasonally adjusted, while house prices edged up 0.3%, and so the Composite MLS Home Price Index edged down 0.1%, according to data from the Canadian Real Estate Association (CREA) today.

The index has now fallen 14.1% from two years ago, from the peak in March 2022, and is back where it had first been in September 2021.

Year-over-year, the index was up 1.2%, same as in February. But there was a wide divergence between the major markets, and between houses and condos in some markets. And we’ll get to them.

Home sales inched up 0.5% in March from February but remain about 10% below the 10-year average. From the beaten-down levels in March last year, sales rose 1.7%.

In terms of supply coming on the market for the spring, it appears to be happening: “Weekly tracking showed a bounce in new supply around the second week of March, which led to a burst of sales in the last week of the month, and a jump in listings in the first week of April,” CREA said.

“Will the story be high interest rates keeping a lot of people on the sidelines this year, or the much expected and anticipated first rate cuts enticing a lot of people back into the market? Probably a bit of both,” CREA said.

The Bank of Canada has tightened policy to deal with inflation, hiking its overnight rate to 5.0% in July and keeping it there. Under its QT program, the BOC has also shed 64% of its pandemic QE assets. Canada’s economy is slowing, home prices have fallen off their peak in 2022, inflation has cooled, except for rents, where inflation rages with historic fervor, with rents spiking 10% fueled by a 3.2% surge in the population due to an explosion of immigration. It’s the rental market that feels the onslaught of immigration, not the purchase market.

Home Prices by major Housing-Bubble Market.

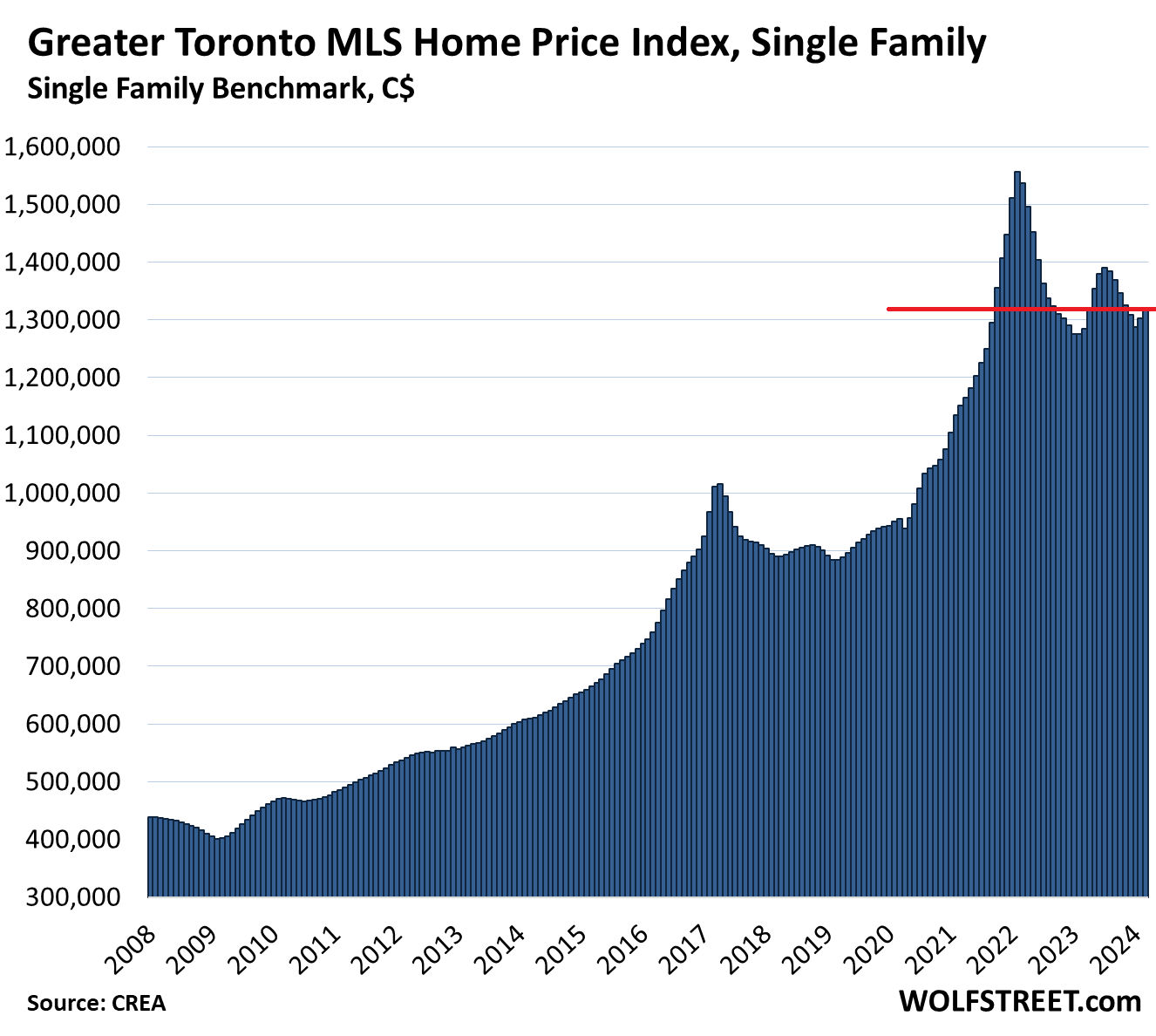

Greater Toronto Area, single-family houses: The MLS Home Price Benchmark Index for single-family houses (all prices in Canadian dollars):

- Month-to-month: +1.3% to $1,319,000; below October 2021

- From peak in February 2022: -15.3%, or -$237,800

- Year-over-year: +2.7%.

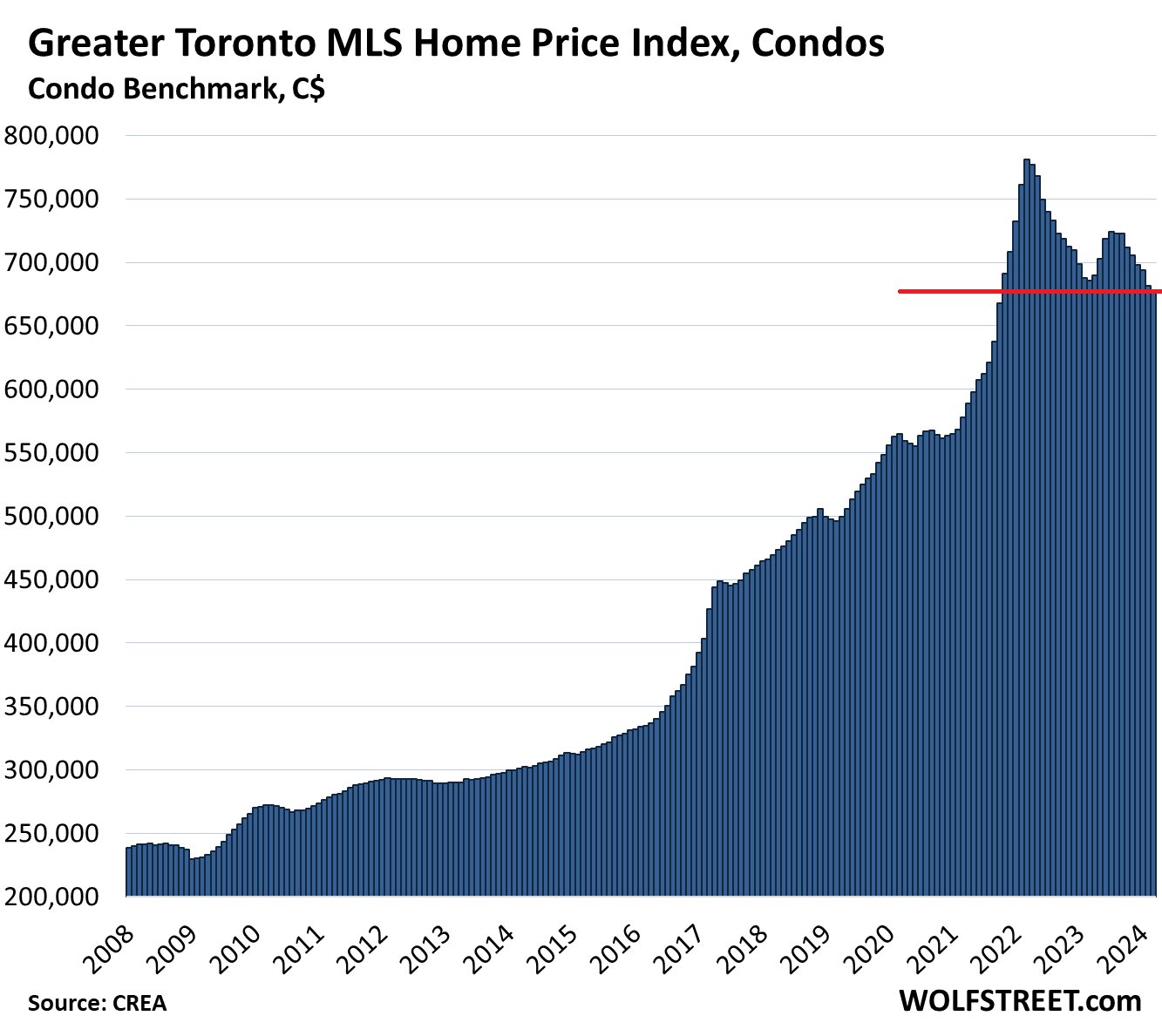

Greater Toronto Area, Condos:

- Month-to-month: -0.5% to $678,400, back to October 2021

- From peak in February 2022: -13.2%

- Year-over-year: -1.1%

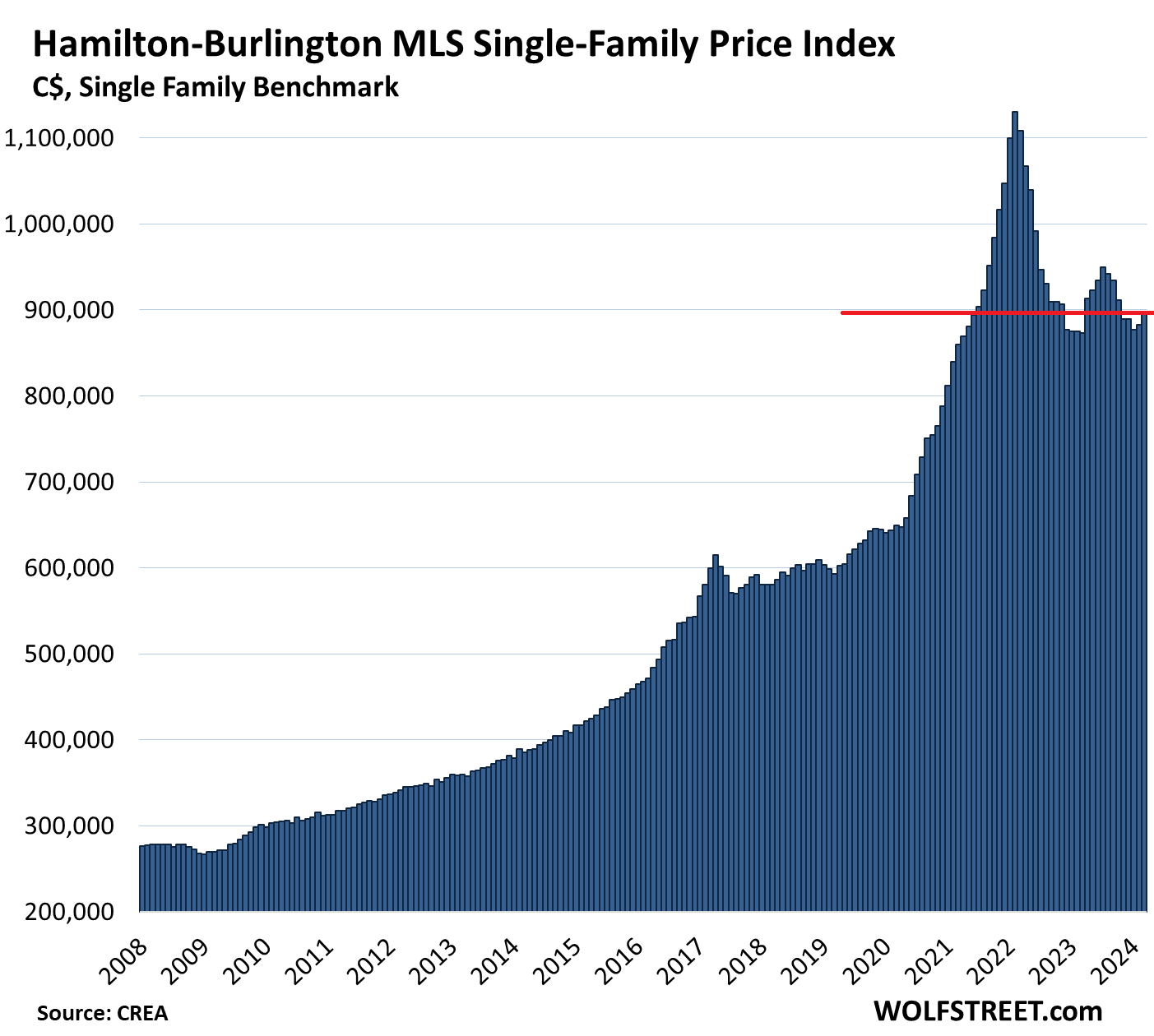

Hamilton-Burlington metro single family houses (in the “Greater Toronto and Hamilton Area”): Single-family benchmark price:

- Month-to-month: +1.7% to $897,600, back to June 2021

- From peak in February 2022: -20.6% or -$232,700

- Year-over-year: +2.8%

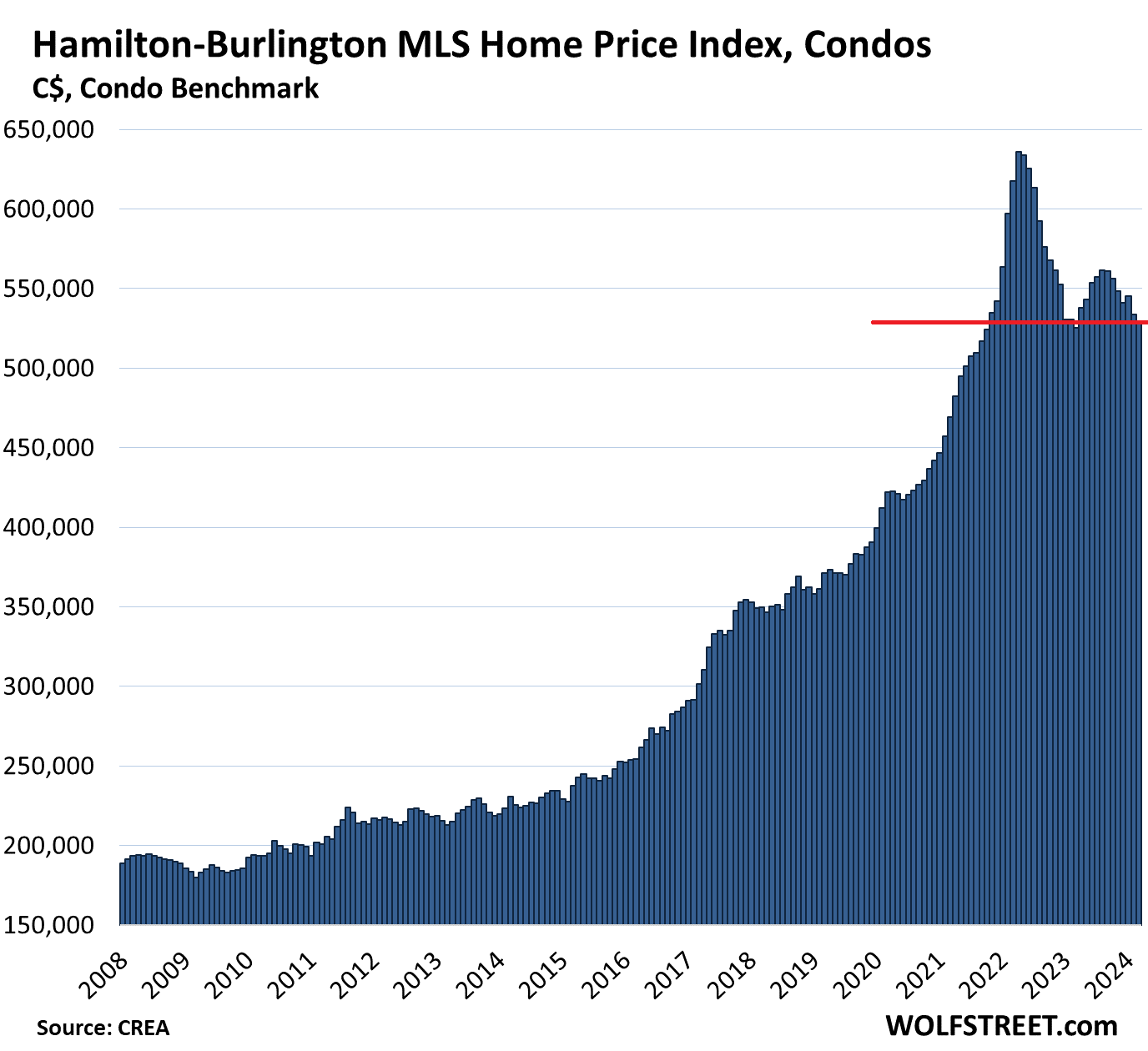

Hamilton-Burlington metro condos:

- Month-to-month: -0.8%, to $529,700, back to October 2021

- From peak in April 2022: -16.5%

- Year-over-year: -0.8%

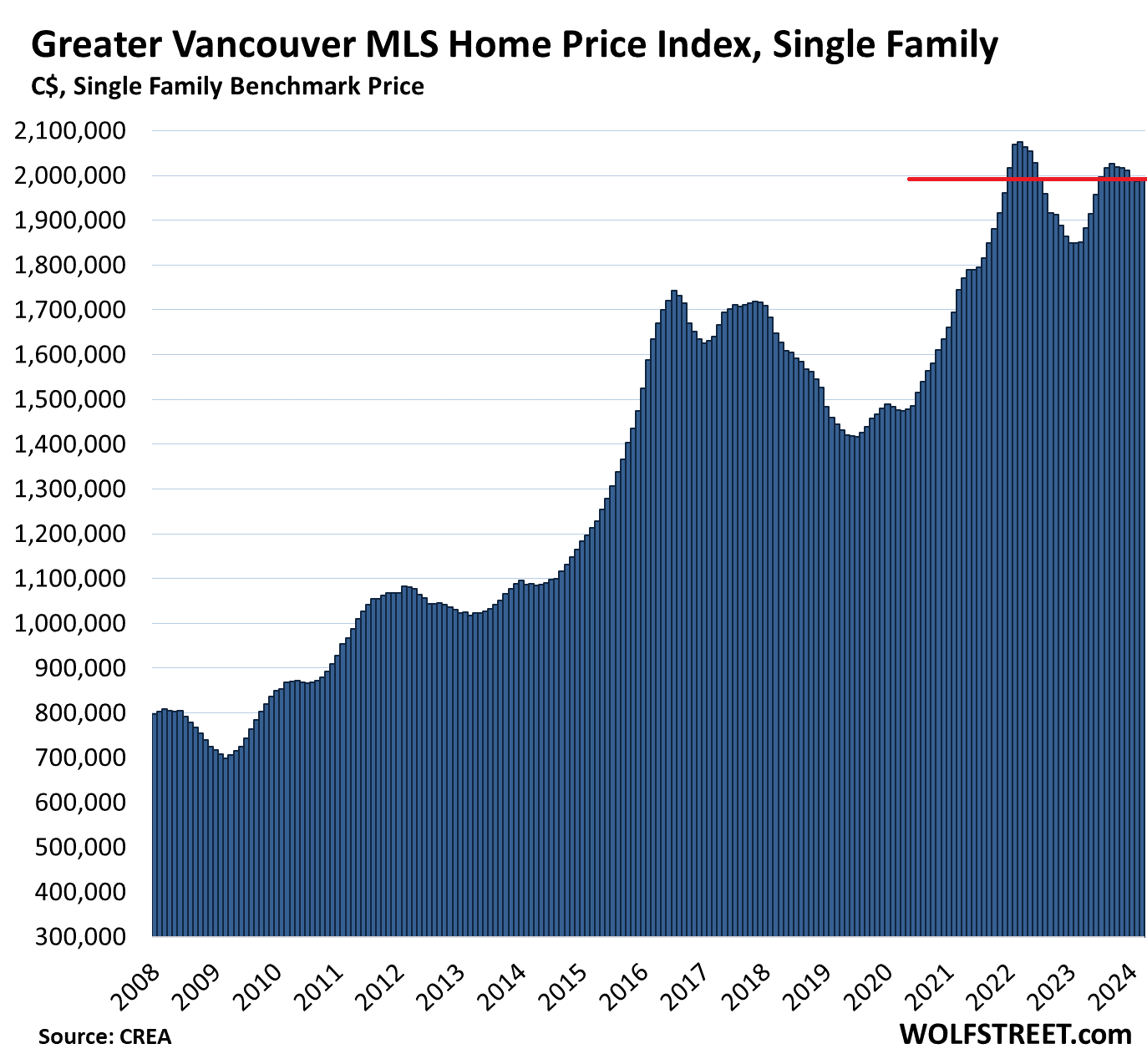

Greater Vancouver single-family houses:

- Month-to-month: +0.3% to $1,986,700 (essentially flat for three months)

- From peak in April 2022: -3.9% or -$70,700

- Year-over-year: +7.7%

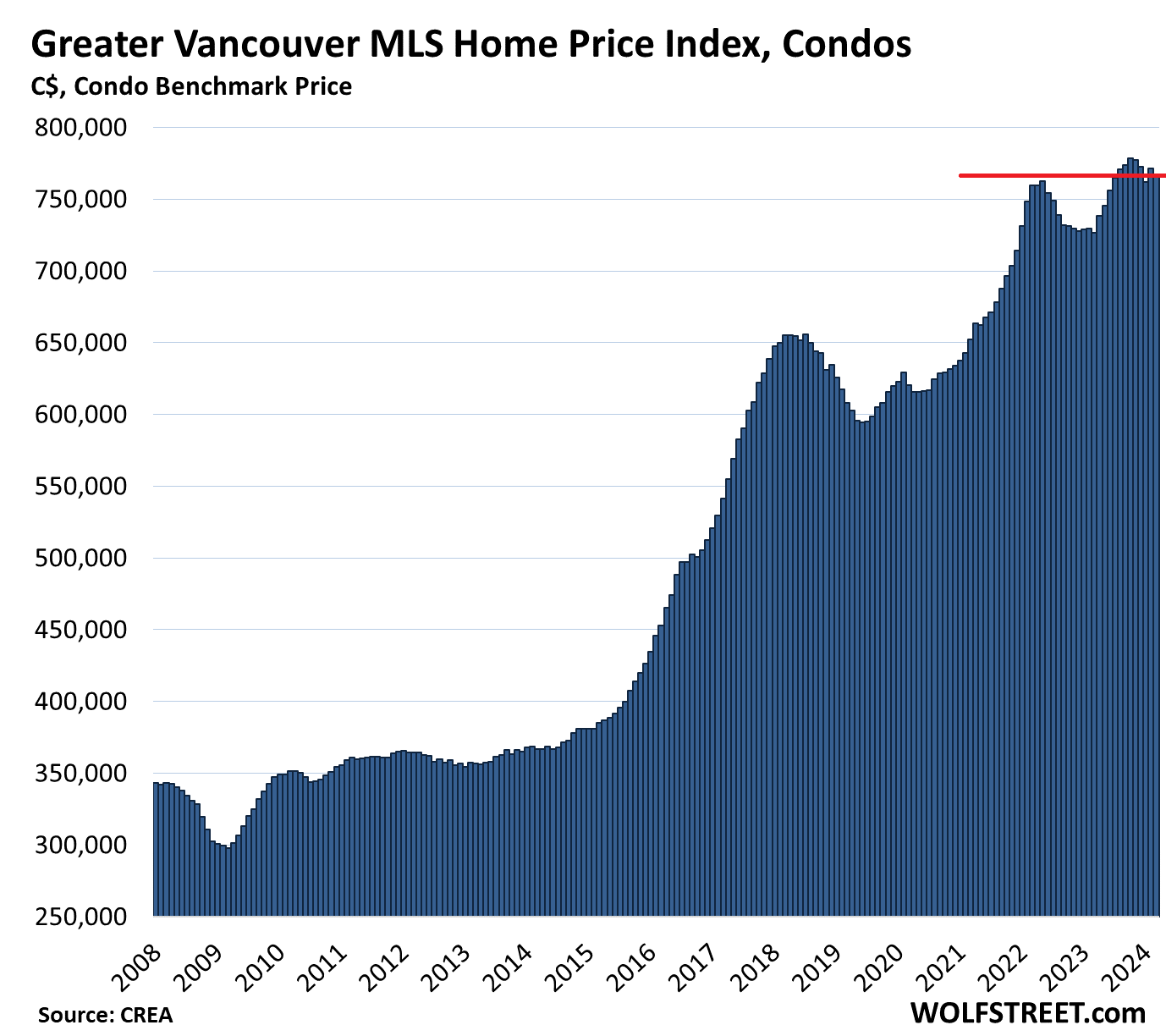

Greater Vancouver condos:

- Month-to-month: -0.6%% to $767,100

- Year-over-year: +5.6%

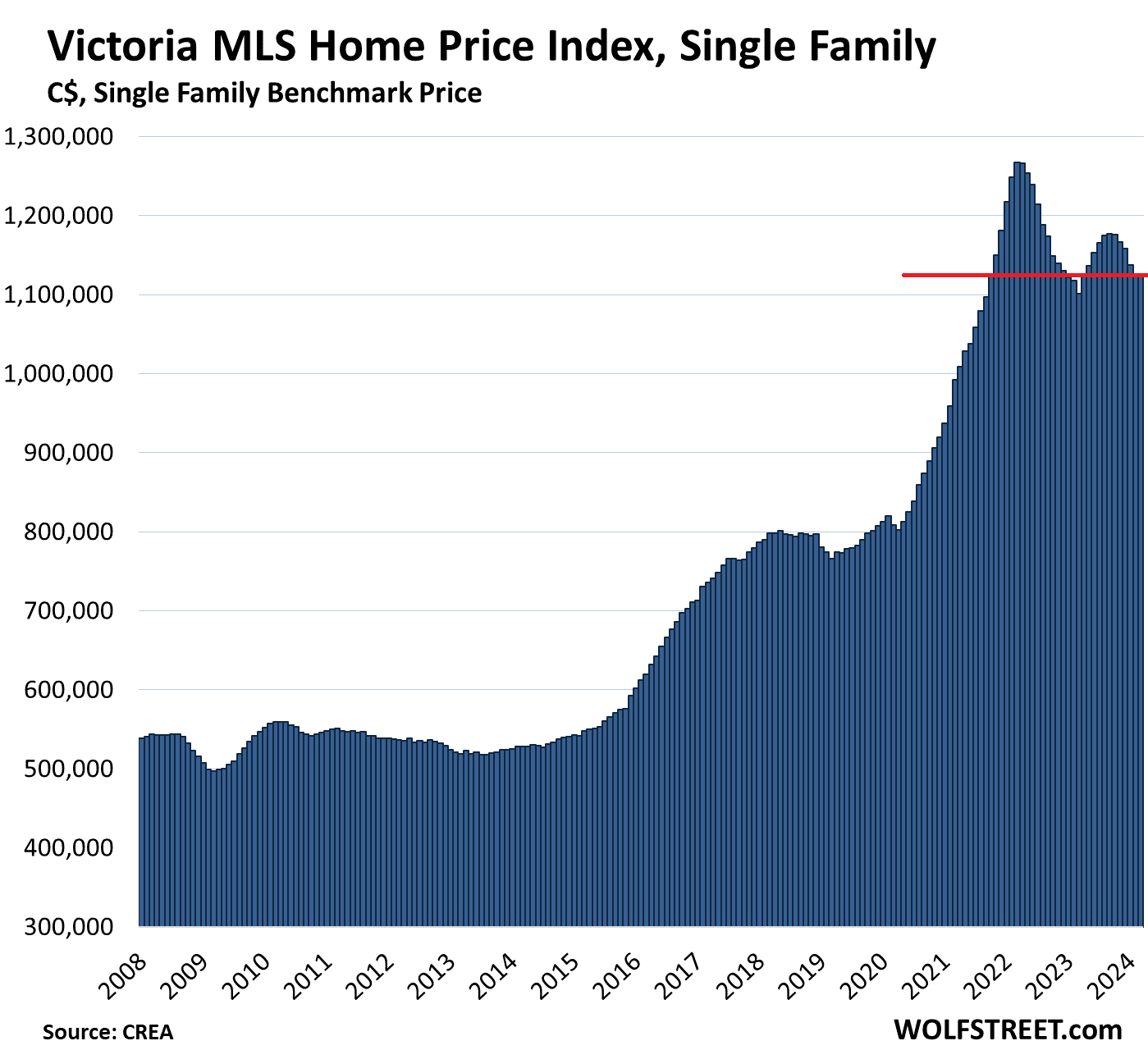

Victoria, single-family houses:

- Month-to-month: unchanged, at $1,125,300, back to October 2021

- From peak in April 2022: -11.2% or -$142,000

- Year-over-year: +2.2%

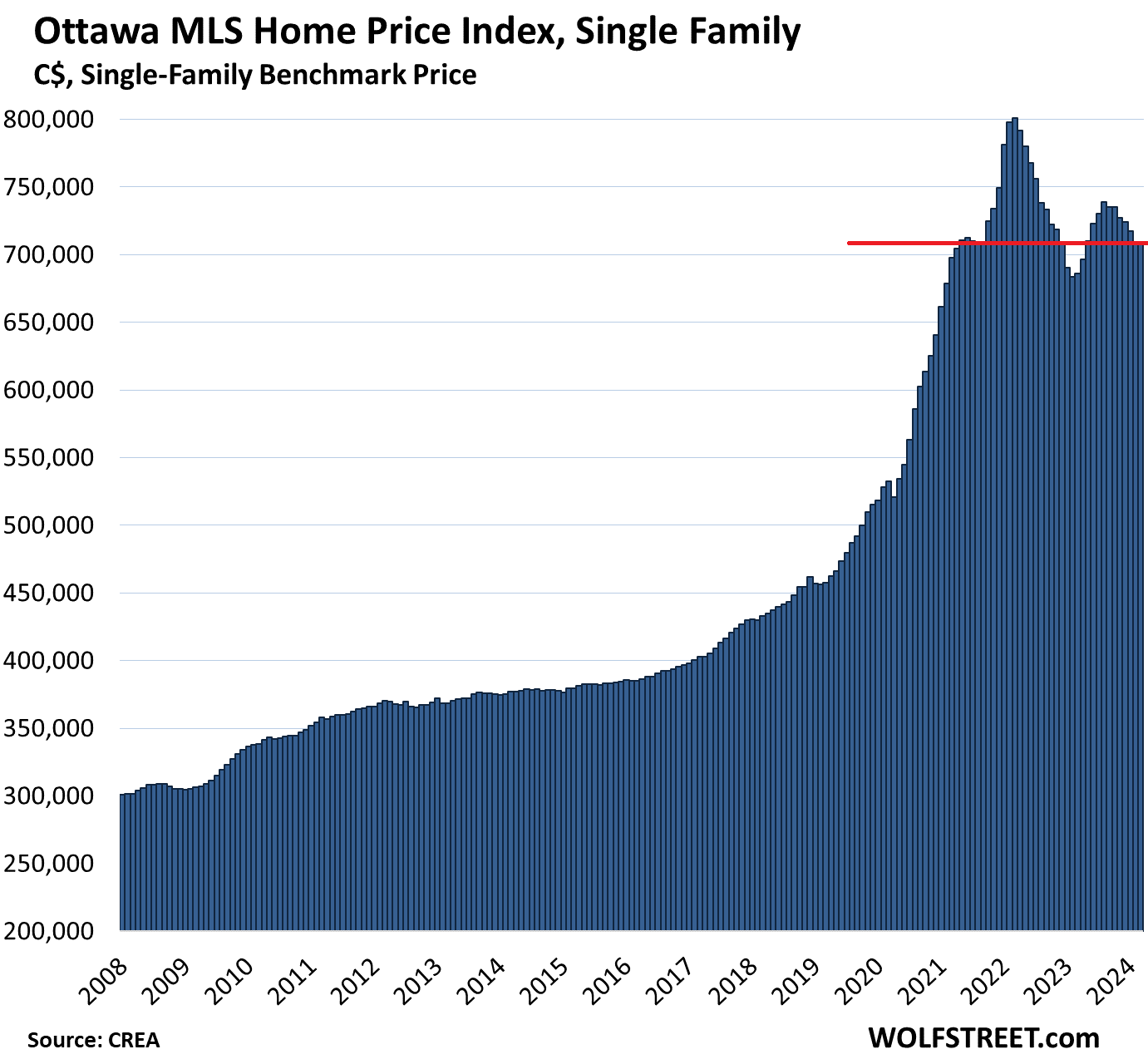

Ottawa, single family houses:

- Month-to-month: essentially unchanged at $709,200, back to May 2021

- From peak in March 2022: -11.4% or -$91,500

- Year-over-year: +3.3%.

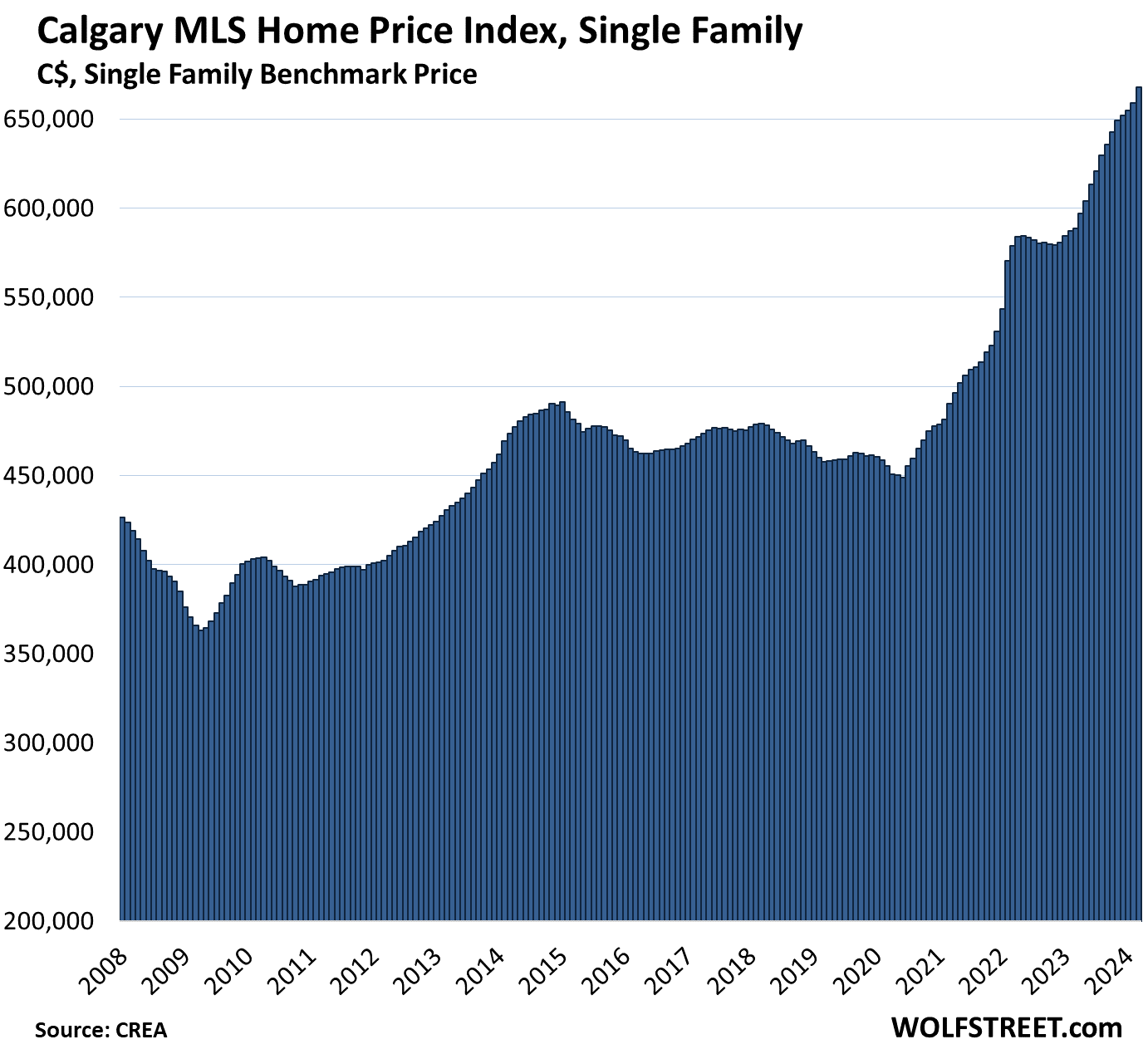

Calgary, single family houses, oil boom helps:

- Month-to-month: +1.3% to new high of $667,700

- Year-over-year: +13.4%.

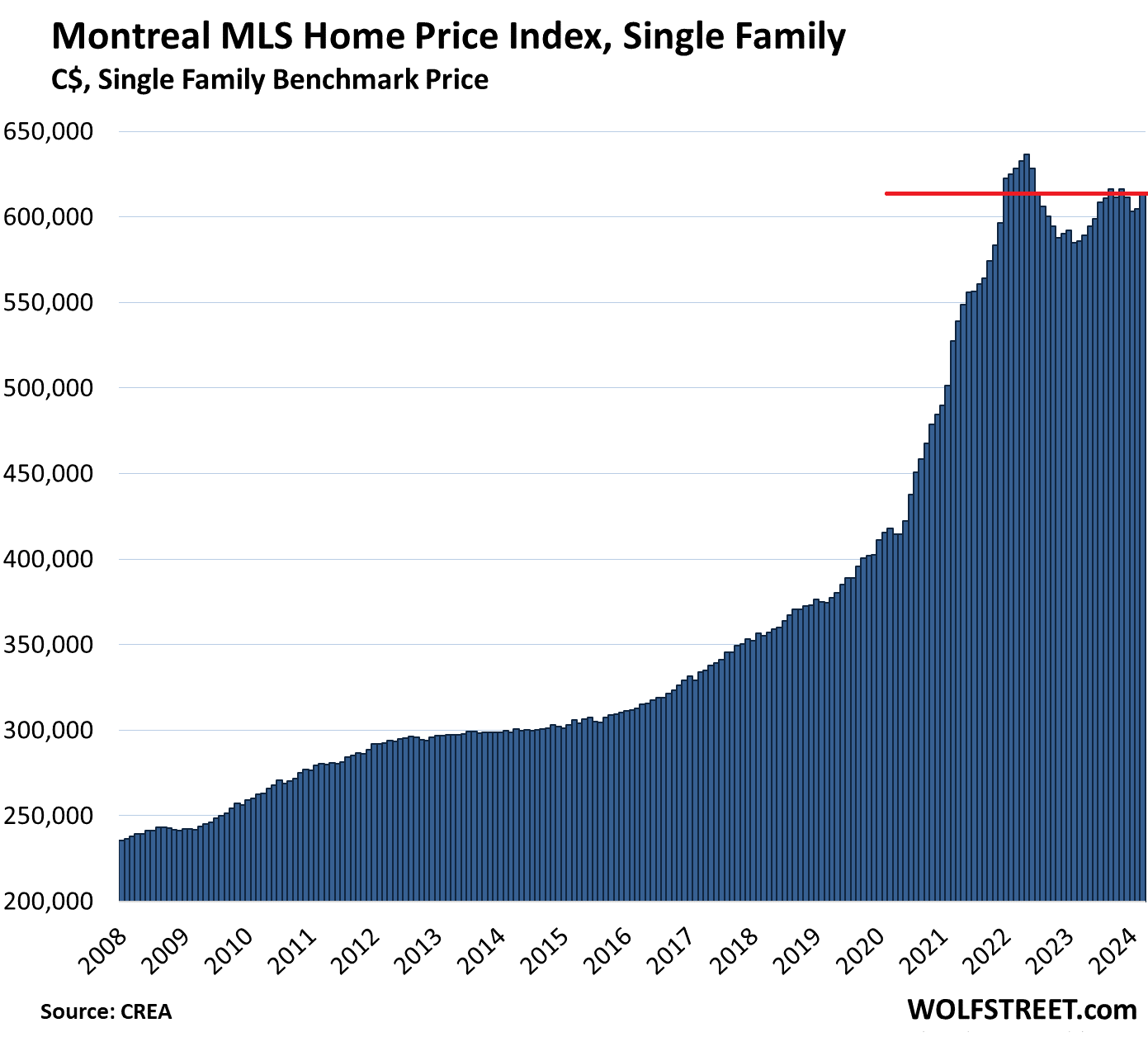

Montreal, single family houses:

- Month-to-month: +1.4%, to $613,400, below January 2022

- From peak in May 2022: -3.6%

- Year-over-year: +4.7%.

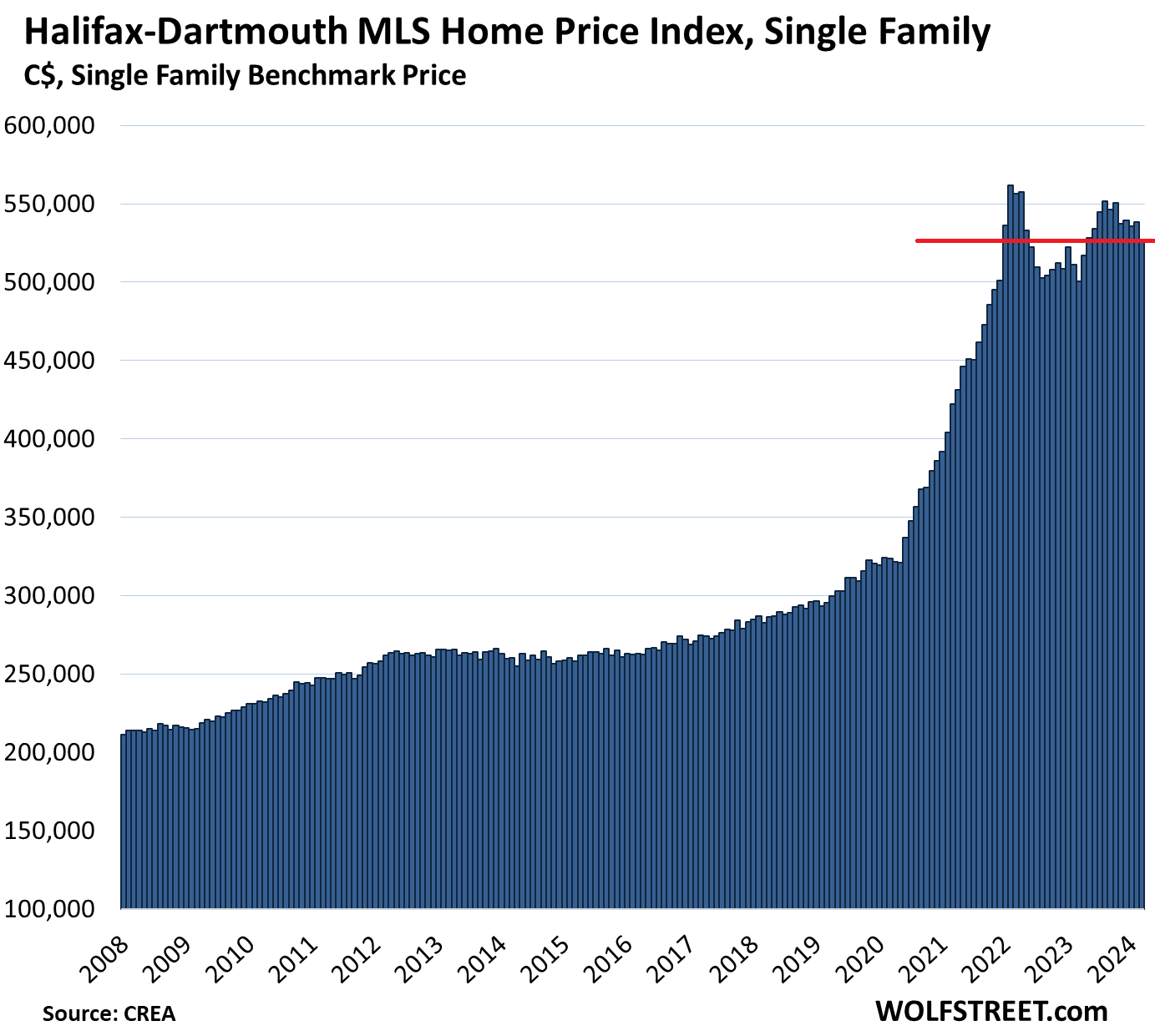

Halifax-Dartmouth, single family houses:

- Month-to-month: -2.1% to $526,700

- From peak in April 2022: -6.2%

- Year-over-year: +5.3%.

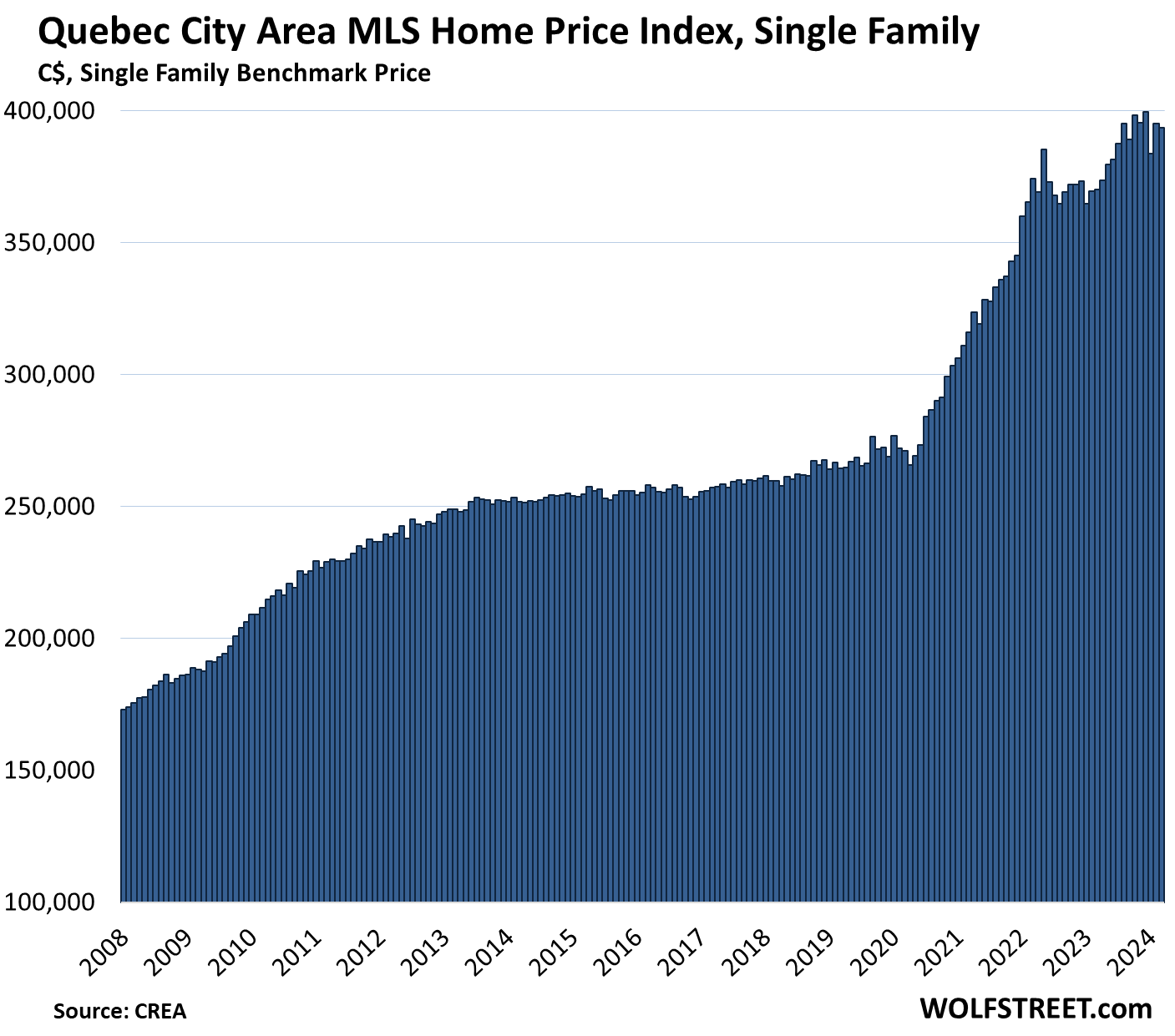

Quebec City Area, single-family houses:

- Month-to-month: -0.4% to $393,600

- Year-over-year: +6.9%

- High was in December 2023.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I live in Vancouver, on the West Coast of Canada by the Pacific, and the tight housing market has become a political issue.

Politicians keep saying they’ll “fix the problem” but this is a macroeconomic issue that’s far bigger than them. The biggest problem is the number of immigrants and international students let into the country — the students alone are a staggering drain on the housing stock. Businesses love them because they can hire int’l university students with brains to work their slots at low, low wages …

And who let the 2m newcomers to Canada last year? Politicians.

Canada’s population jumped by 1.27 million people in 2023, to 40.77 million, an increase of 3.2% from a year ago, the highest year-over-year growth rate since 1957 (3.3%): Statistics Canada.

Immigration hasn’t hit home prices – across Canada, home prices are down 14% from two years ago, see first chart.

Immigration hit RENTS. The CPI for rent in February spiked by 10% annualized from January. The six-month annualized rent CPI, which irons out the large month-to-month variability, spiked by 10.3%, the worst since 1983.

The rent CPI is a measure of what tenants actually pay in rents, not a measure of asking rents, and includes rents paid by tenants in rent-controlled markets.

https://wolfstreet.com/2024/03/27/amid-canadas-huge-immigration-surge-population-growth-hits-3-2-triggers-10-rent-inflation-even-as-home-prices-drop/

+ temporary workers, students, etc. Tons.

Biker

” + temporary workers, students, etc. Tons.”

They’re included in the numbers here. Temporary and permanent visa holders, plus asylum seekers are all included in the numbers here.

Rents prop up home prices.

By deliberately importing an absurd number of people the govt has set a new floor on rents, which puts a higher floor on prices.

Rents absolutely impact house prices.

You might not see it in the chart due to lags, but it absolutely does.

The government knew they couldn’t do a 2008 style bailout when the USA is strong, so instead they printed people.

The huge immigration was a banking bailout.

This rental Ponzi scheme in Canada is terrible. Slumlords are demanding vegetarian girls as tenants and asking for stuff that would be considered coercive in criminal and family law.

Gen Z…waaa? Try making sense, it will only lead to good things.

@Adrian I’m not going to post exactly what those “Brampton landlords” want from mainly young vegetarian women who pay rent to share beds with male strangers. It’s sickening how the rental crisis gives more power to the sickos.

As a Canadian I agree that high immigration has mostly resulted in high rents. But I would also argue that it has prevented house prices from declining further. Rents and home prices are at least somewhat correlated.

I agree with those saying immigration helps support home prices, they’re declining but I think they’d decline further and faster if rents weren’t skyrocketing. Maybe it’s just psychology but talk to any property investor in TO or Van and they will all cite pop growth from immigration as their reason for longer term optimism. So I think demand would be lower without this immigration dynamic and by extension prices would fall faster, we’d probably go into recession faster too because of our overall heavy reliance on RE and construction for growth.

The price of housing hasn’t dropped significantly while the cost of housing has at least doubled. Beneath the surface lurks a reconciliation to this paradox.

I doubt newcomers come to Canada for the weather, pull up the seven day forecast for Toronto.

I doubt newcomers come to Canada for the housing prices, read this article.

I’m guessing newcomers come because wherever they come from, it must be much more difficult to survive.

Thus if politicians focused on helping countries that had high exodus rates, perhaps the immigration concerns would be less of and issue?

I bet that most people would rather stay in their country of origin if it was safer and they could more easily survive and thrive.

They’re wanting the immigrants to come, why would they want to help them not to come?

The strong and young make this trip up north, leaving behind mucho.

@Home Toad: Exactly. Businesses and “their toady” (excuse the bad pun) politicians want immigrants to keep wages low, build a bigger population (according to economists, it is a strength), and have younger people pay the social security costs of older domestic populations.

Each country is looking out for itself in a short-sighted way – there is no global perspective. If there was a global perspective, what Name* suggests would be a better way as it will reduce huge stresses in migration.

Some rain and 48 to 54 above. we had maybe 3 or 4 days of snow this winter. Toronto is quite temperate.

Up North, not so much.

Straight out of the summer of love that turned into what we have now. Reasonable approach for a well fed, educated professional with the luxury to suggest that man, meaning everyone else, needs to conform.

A number of years ago, I went to a meeting with Vicente Fox, who was president of Mexico from 2000-2006. He said exactly what you are saying – that most of the immigrants would prefer to stay home if they had reasonable opportunity there.

In the Greater Toronto Area, 2021 was the year of the international student.

Why?

Whenever there’s an intersection near an industrial area after the 3pm and midnight shifts, people have to drive very carefully, because they just run across the road just like that.

Hudson Bay and Walmart fulfillment centres would only hire international students during that time. Amazon did at first, but many of the international students just weren’t fit for such intensive jobs at $20/hr. Middle-aged newcomers were better suited for the job than these so-called “Stanford College” and “Oxford College University-Harvard campus” ‘students’.

Many Canadian parents were even warned that their child will not get hired in their field if they study at public colleges like Seneca, Conestoga, and Humber.

It doesn’t sound like a political issue – the people keep voting for the same politicians and policies, so one can only assume they love what they’re getting.

That’s inaccurate.

We cannot vote for the prime minister and most policies originate with him. Nobody loves what they’re getting unless they’re deranged.

No governing party wants to be stuck holding the bag on any sizeable housing correction. Seems that many voters are either gullible or naive (or their individual preference for the current liberal party over others). Now Canada is shoveling billions into the housing market and promising the fairy tale of over supplying the market to such an extent that we achieve affordability.

Unlike in America new home prices are about 50 percent more than a resale house so building more will skew prices much higher instead of lower. Canada is much different than America.

Not exactly Depth Charge, there was what some might consider “aggressive” immigration policy in Canada for many years and that’s something voters seemingly had no issue with. The recent massive spike, and it is quite large, came after last elections, but prior to next. So if you want to judge the political mood you have to wait until next elections to figure what majority of Canadians think.

There is a very big difference between high levels (relative to other nations or people’s feelings on what appropriate levels are) of STEADY immigration and a sudden, rapid, massive spike. One can be planned for, and the other creates chaos. If you know x amount of new people will arrive next year and the following year, and the year after that, and y amount of people roughly will be born as well, then you can manage the expansion of infrastructure and social services etc. a little easier than if you’ve built up capacity for those amounts (or tried to) but instead you get 3x or 4x or whatever, I mean it takes almost 10yrs to build a new hospital for instance, housing is quicker but you can’t ramp that up as quickly as all the new people are coming either. That’s what we have now.

So, let’s see what happens after next elections. If there’s a change we’ll also see how much of the other parties talk is empty, in which case it would mean “the people” don’t “love what they’re getting”, they just have no say in what they’re getting. This BTW was the case when Conservatives gained power last time with Harper, lots of verbal placating to people who didn’t support immigration policy of that era, but no actual change in the quota lol, 200k year in year out at the time.. they just didn’t increase that number and tried to make it so you couldn’t have a passport pic with a burka on 😂🤣.

“…the people don’t love what they’re getting, they just have no say in what they’re getting.”

Exactly, the people have no say. The Liberals and Conservatives are basically a uniparty, and the Democrats and Republicans are too. There’s very little variation between them, especially on immigration.

Big multinational corporations control the politicians, not the people. Whatever they tell the politicians to do, they do it.

Immigration at this level was never an issue in the last federal election, the current govt kept this policy in the dark, and the housing affordability crisis they caused has pretty much killed any chance of re-election next year.

Canada accepted approx. 350000 immigrants in the years prior to the last election. All three major political parties were loudly pro immigration.

No one had a chance to vote for or against this.

I totally agree with you

Have you seen the new amortization rules and the mortgage relief blurb ?

Google “Solving the Housing Crisis: Canada’s Housing Plan”.

The government are getting super desperate up here.

Not long now!

Yes they are desperate georgist. The extended amortization could’ve been worse, still adding 5 years to try and slightly reduce monthly payments (increase interest and overall cost) seems like it will have minimal effectiveness…. because…. it only applies to new builds. If trying to achieve “affordability” is really one of the main goals – why not give potential first time buyers the most options? If Wolf and his reporting of the German real estate market has shown anything, it’s that existing housing can and does depreciate more in price more than new builds. As for increasing the RRSP withdrawal level: I have my doubts to how many possess near this level of savings and those who do, well it’s their money and choice – however, at a time when retirement savings and corporate pensions are reduced, there’s definitely a part of me that finds it morally wrong to purposely tempt young ones to compromise their retirement savings. Let’s face it, unless the government pushes for multi generational amortizations, the gains in real estate experienced in the last 20 years won’t increase at the same rate in the next (hopefully) 30 years, nor should they. But, when trailing in the polls and desperate to hang on to power – why worry about the future.

From Econ 101: the only way a country can grow its GDP is either through increased productivity (which is stalled), or increased immigration. Just sayin’

Actually I think it’s increased productivity and/or increased population, which recently requires immigration because young women would rather pursue a career after getting educated, instead of staying home with the kid(s). I can’t really blame them.

The drop in birth rate in developed nations is an impending enormous challenge in the coming decades and which doesn’t seem to be attracting the attention required to respond to it. I suppose AI might provide a solution, if anyone can ever actually define what that is.

Failing that, the only other solution seems immigration, which so many folks are opposed to regardless of which shrinking-population county you are talking about. Can you see China turning to immigration to deal with it’s population problems?

Is quicker QT than in the US having a quicker impact on housing prices?

I guess, Canadians don’t have the luxury of 30 year fixed mortgage and thus things are unraveling there faster than USA.

I don’t see Canadian home prices going up again in the future unless immigration increases big time.

I hope USA sees similar price drop, good for the society.

As I remember it, the 30-year fixed mortgage is what broke the S&Ls in the early ’80s. The government ‘deregulated’ the industry. The only problem was they deregulated the interest S&Ls had to pay for money/deposits but still had to lend at fixed rates.

Kind of like California deregulating the input cost of electricity, but fixing the price they could charge customers. Once again, as I remember it; it was many moons ago.

Yes, the mortgage short locks and the falling productivity for decades. And the flood of newcomers that cannot easily integrate because of the red tape.

Actually, the flood of newcomers is a significant reason for lowering the productivity. Most of them end up in lower end jobs, manual labor, even these with a good education and some experience abroad (not recognized in Canada).

All this makes less reasons for businesses to invest, automate. Why bother when they have tons of minimum wage takers doing the work the old school way.

Long ago a newcomer would be more than happy to work general labour, because they were through the company and at least you saved some money to retire in the homeland.

But today, ppfftt! Temp agencies expecting indentured labourers while greedy slumlords demand rent like feudal lords. Many young men have deleted themselves in Canada at a higher rate than before. They were caught in a trap they can never escape in this realm.

Does Canada have a red province/blue province dynamic as in the US (red state/blue state)? If so, maybe Calgary is growing in part because it is, I presume, a “red” province.

Just curious.

Oil. Calgary is the oil capital of Canada.

Alberta was the place to be in the early 2000s: The oil companies would pay $30/hr that time just to use a shovel.

Today many have closed shop, and Exxon went to South America after discovering at least 15 billion barrels of new oil reserves.

It’s not really a red/blue thing unless Saskatchewan has a similar chart. It’s just that AB is the only province that is PST/state tax free.

The whole of Canada is a weird pinkish color.

What is in Vancouver that would make the house worth 2 million dollars… Nothing at all, but that’s what they are.

They probably feel special, everybody being a millionaire.

Isn’t it cold up there,maybe the houses are special too.

There is no winter in Vancouver unlike the rest of Canada. This is one of the reasons why everyone wants to live there

I read some time ago that real estate in Vancouver was inordinately effected by buyers from China trying to stash some wealth out of reach of CCP? (Maybe same in west-coast US communities?)

Is past capital flight from China a myth, and if not, does it continue?

Several factors drive Asians to the West Coast, including Vancouver. High paid tech jobs, increasing home prices and investment opportunity, better education, growing Asian cultural communities, climate, natural beauty, supportive immigration policies, and not least – escape from extreme Asian crowding.

In the past it was a no brainer. With prices now astronomical and tech looking bubbly, some of it should be abating.

Vancouver and Toronto are over priced markets because of foreign buyers. All the new rules for foreign buyers will only effect future buyers, the bottom of the dip will be based on how many of the Vancouver homes are paid off and how many will be up for a mortgage renewal. Only a couple more years of this interest rate level and the last of the low interest 5 year terms will be cleared out.

Because what kinda idiot would want to live in a n

Blue state lol.. like it matters lol

@MiTurn: The main reason “red” states grow is the spillover effect from “blue” states. Look at the stats, they are very clear on which states are highly innovative and productive.

SS

The Canadian goose during migration

does favor blue states, California, Vermont.

So, you’ve got the foul thing. Stats for birds.

Complete biased BS. You are measuring “productivity” the way the government does, so billions in “economic activity” from Wall Street counts as way more than the equivalent amount of farming.

Alberta and Saskatchewan are purple provinces. There are no blue provinces here. Oil revenue in Alberta is being used to transform this province into a pink-red province. Alberta is the oil capital of Canada and also the immigration and price-inflation capital.

We do to some extent and some people here foolishly try to paint every issue with a tribalistic political brush as well. The reason is that Alberta has oil and after the oil crash of 08 neither Calgary nor Edmonton saw the growth in RE prices that Toronto and Vancouver saw which was fueled by cheap money. Now the dynamic is different because the gap in affordability between Midwest and coasts is huge. On top of it, population growth in Calgary as a percentage is actually larger than TO and Van, partly because it’s a smaller city to begin with and partly because of the affordability issue, Calgary is growing through large amounts of immigration.. So I think that would not be a very “red” thing would it?

I worked in Alberta for 1 year and it was enough. Anti union, and thinks it’s Texas. I remember my first foreman telling me not to ask what the other guys were making. I couldn’t figure out the work schedule so I finally asked. “Well” he said, “8.5 hours per day on the tools, we like 9 hours, 10 hours is fine, or you can work all the hours you want”. For straight time, of course. I ended up as the concrete foreman on a big job in Lethbridge simply to get the hell out of Calgary. Watched the company go broke. Worst construction I have ever seen. Never again, never again. I think the ‘in house’ engineer was paid off and the super showed up drunk every morning.

The only province in Canada that could be considered ‘red state’ is Alberta, except for a stint with the NDP (left) party possibly due to the migration from East (Atlantic) provinces and Ontario, voters who tend to not be conservative voters. The Conservative Party and its variants had held power continuously for 44 years until 2015 , and are back in office since 2019.

In the Alberta population there historically has been generally anti-East in sentiment and frustration due to the history of tapping Alberta for royalties and taxes and sending the revenue East – the Federal ‘equalization’ formula. The Liberal Feds have been hostile to Alberta since the elder Trudeau’s regime beginning in the ’60s.

In that era, the Feds also created the state owned Petro Canada (‘Its Ours’), a nationalist money sinkhole created by the federal Liberal-NDP coalition (a frequent occurrence when the Liberals don’t get a majority in an election – including the last one).

More recently, the TransMountain pipeline expansion by US developers finally gave up in frustration and left Canada after their years of permit approvals and native negotiations were arbitrarily cancelled by the Feds.

The project would have been finished in about a year or so at no cost to taxpayers, by twinning with an existing pipeline on a cleared route. They sold their investment to the Feds for about $4.6B, the Feds took over the project and the cost has since increased to $34B after several years.

There was also to be an augmented pipeline to the States, but that was cancelled by the US government due to environmental activism. The Alberta NDP government at the time then bought railcars to ship by rail, hardly an environmentally sensitive solution.

I visited Alberta many times in the past – there used to be a sort of Wild West attitude in past years, and I suppose relative to the rest of Canada there still is, but somewhat tempered by newcomers from the East over the years.

What is the difference between Petro Canada and PetroChina Canada? Are these pipelines- terminals companies?

“In the Alberta population there historically has been generally anti-East in sentiment and frustration due to the history of tapping Alberta for royalties and taxes and sending the revenue East – the Federal ‘equalization’ formula.”

Albertans have short memories on this file. The “Equalization” program in Canada was implemented to supplement tax receipts in the poorer provinces in 1957 in response to one province in particular which was a serial defaulter on its provincially issued bonds — that province was Alberta. It wasn’t until the 1970s that Alberta became one of the rich provinces.

Albertans also reliably don’t know how the Equalization program works.

Yep, now you see why the trucker convoy was started and why Alberta’s premier Danielle Smith is trying to separate Alberta from the country. Oil is all they have, if it goes away Alberta becomes “have not’s” once again and the Christo-fascist reform party who has taken over the provincial and federal conservatives wont stand for it.

Crap from search machine:

“Uncle Sam’s inflation flare-up and a dud of a bond auction jacked five-year Treasury yields up a staggering 23 bps. Given the cozy link between our countries’ bond markets, soaring U.S. yields dragged Canadian five-year yields 14 basis points higher. It was the biggest spike since October and a reminder that Canada does not control its destiny on mortgage rates”

Seems like rates don’t matter to anybody these days and probably the exchange rate is also pointless, as well as incomes and future value, etc.

Can’t help but ponder the aspect of the federal liberals releasing the “Canadian mortgage charter” to lenders last year and then more recently announcing a plan to buy up to $30 billion worth of canadian mortgage bonds annually from lenders.

The mortgage charter hasn’t been passed into law (yet?). Meaning at this point in time it’s really only recommendations and wants on behalf of the government. Lenders are not legally obligated to follow the charter’s requests.

The new Canadian mortgage bond buying program frees up liquidity for banks. Banks don’t insure loans (no risk to banks) that are under $1 million with less than a 20% down payment (most first time buyers). Sweet deal for the banks, I’m sure we all agree. Hey banks don’t make the rules (OSFI does).

Some of that CMB buying program seems like a bought and paid for compliance when they can turn around and offload part of their mortgage portfolios to the government.

CMBs are traded in the market, and there is decent liquidity. So the banks that need to shed some CMBs could just sell them to the market. Also my understanding is that the government is buying the CMBs in the market, and so any CMB-holder can sell to the government.

It is my understanding Wolf that CMBs are packaged insured mortgages. What has become the elephant in the room is the CMHC on its ever increasing volume of insured loans – even surpassing it’s 2 competitors as being the largest provider of mortgage insurance. Currently Canada’s big banks hold around 85% of current mortgage loans. With the CMB program currently buying up to 75% of the old limit ($40 billion) and up to 50% of the new limit ($60 billion) coupled with the big banks market share of loans – I find it challenging not interpreting this as the government freeing up financial room for the banks.

Let’s make sure we’re all on the same page. CMBs (Canada Mortgage Bonds) are bonds that are backed by pools of mortgages. It’s a way to “securitize” residential mortgages, like MBS in the US. CMBs are guaranteed by the government and are issued by a federal Crown Corporation, the CMHC. So these bonds are a government-issued and government-guaranteed financial instrument.

Under the purchase program, the government raises $30 billion by issuing Government of Canada Bonds and uses the proceeds to buy $30 billion of Canada Mortgage Bonds. So the government is swapping its own bonds.

It doesn’t matter who holds CMBs, they’re a marketable security, and actively traded in the market, banks and other institutional investors, including foreign institutions, hold large amounts of them. Anyone can buy and sell. And the Bank of Canada bought some too back in 2020/21.

Mortgages that banks hold have not been securitized and have nothing to do with the CMBs. By buying the CMBs, the government is NOT taking mortgages off the banks’ books.

There is zero credit risk to the holders of CMBs – including the banks – because the government guarantees the bonds.

I don’t think this purchase has anything to do with the banks. It’s more of an effort to create more demand for the bonds so that their yields dip a little so that maybe mortgage rates come down a little. But so far, the two purchases in Feb and Mar haven’t had much impact on mortgage rates.

The government is also creating more SUPPLY of government bonds because it has to issue GoC bonds to get the funds to buy the CMBs. So it’s essentially replacing government CMB bonds with regular government bonds. It’s creating supply of GoC bonds and demand for CMBs bonds in the same amount. And both are government-type bonds.

How many rabbits are left in the magic trick hat? Not many, the Libs are just buying time till election where they’ll default lose to the PCs and then the bubble will blow.

Meanwhile, I’m sure the PCs will reintroduce 40 year Mortgages like Harper tried back in the 2000s.

Canada is FKed. Period.

In a race to the bottom the UK is well ahead. The worst housing stock in Europe and yet it feels like 2021 all over again with people desperate to buy because next month is the rate cut. Prices in my area ( north Yorkshire) for the decent homes are up 20% from 2023 whilst the shitholes just stay unsold year after year with no pressure for the majority to lower the price.

Then on top of the housing shitshow we have holiday hotels being taken over by big contractors to house the flood of migrants ( all young males) . It is now virtually impossible to see a Dr or dentist on the NHS and the entire infrastructure looks like it has undergone carpet bombing.

I only need to read UK news and financials to see the path that Canada is on.

Then you don’t know much about UK. The single biggest card missing in UK hand is energy. Did u know there is an undersea nat gas pipeline from Norway to UK? U can’t drill in Alberta without hittinq nat gas.

Next: the insane Brexit. Canada is in trade agreement with US and Mex. Whos is UK with?

Good write up in New Yorker re Brexit. It was replaced with …nothing. In a very polite way Japan tried to warn: We can’t build new plant or guarantee existing without duty free access to EU.

The slogan goes: there isn’t a Brit car industry but there is a car industry in Britain. Eg: Germany saved Mini.

Main lesson re: Brexit; Don’t ask lads at pub about trade policy.

There is no mechanism to expel member from EU. Hungary gets away with murder. The UK could have tightened immigration etc. and got flack frpm EU…so?

I am dual Can/ UK citizen and think it’s tragic UK clung to the past/

It’s virtually common ground in UK that Brexit wouldn’t fly today.

Speaking of the past: next shoe to drop may be approach to IMF.

In 74 the task of lead IMF, the US was to convince Brits ‘they had run out of string.’

Thanks for the response Wolf – and yes we’re on the same page.

Again Wolf, thanks for the clarity. I actually find it a bit disturbing and concerning that the government would potentially take on that much new debt with the intent of trying to manipulate rates lower (plus more favorable rate on GOC bonds compared to CMBs) and try to induce more private CMB purchases. Seems like it potentially runs a greater risk of scaring away investors never mind the new additional debt.

Yes, agreed.

The whole thing seems kind of silly. The government is already on the hook for the CMBs through its guarantees, so it’s effectively not changing its risk profile. But in terms of how investors look at the government’s debt-to-GDP ratio, it’s based on GoC bonds and doesn’t include guaranteed bonds, such as CMBs. So by swapping CMBs for GoC bonds, the debt-to-GDP ratio will get worse with this deal.

To be honest, I really don’t understand why the government is doing this. It seems silly. But then a lot of stuff that governments do seem silly to me.

DM: The US cities where home prices have DOUBLED the fastest – with one city seeing values rise twofold in less than 5 years

REVEALED: The US cities where home prices have DOUBLED the fastest – with one city seeing

Home prices have doubled in less than ten years in 68 of the 100 largest cities in the US, a sobering new study shows. And in some major American cities, the cost of the average property has doubled in as little as five years. In Detroit, home prices were half of what they are now as recently as 2019, data from real estate marketplace Point2 reveals. Home prices in Miami and Tampa, Florida, have doubled since 2018, as they have in Baltimore, Maryland, and Spokane, Washington.

“In Detroit, home prices were half of what they are now as recently as 2019,”

1. So that means home price in Detroit would have doubled since 2019. Alas, the Case-Shiller index says home prices in Detroit increased by 45% from the January 2019 reading to the January 2024 reading (most current).

2. Did you look at home prices in Detroit in 2019? They may be up 45%, but from very low levels, and they’re STILL VERY LOW.

It’s really not good for your brain to read a tabloid such as DM. I think extended exposure to DM causes Alzheimer’s

DM is one of the very best sources of new in the world, and what they stated in that article is 100% accurate.

🤣❤️👍

So that everyone knows, DM = Daily Mail, the UK tabloid.

The print version recently ran a 2-page article on How To Prepare For A Nuclear War…

Clarity?

So who pays out the gocs? Taxpayers?

So much financial complexity…no wonder shit heels like junk bond ex con Milken is worth six billion today.

It’s a wonderful life….

Bit in Globe a few days ago: the folks who are really in trouble put big deposits on pre-builds or buying ‘off plan’ 3 to 4 years ago. This worked great for years. ‘Lock in’ price and enjoy appreciation. Now ‘locked in’ has different context.

One guy put 150K down on a a 550K condo in TO. For 375 square feet!

Now it’s time to close but at new rates he doesn’t qualify with bank, so off to alternate lender. Alt appraises unit at 450K or 100 k less than he paid. Of course developer wants 550 as per contract, but worse about 50K of extra costs which contract allowed in this pre- build. Also, alt lender is not going to advance 450K. I don’t have paper at hand but he has to come up with at least another 100K to close.

I feel a bit for this guy cuz it sounds like he just wanted to live there, not a flipper.

There are thousands of these situations. Many buyers are walking away. One guy walked on a million dollar deposit on a nine million dollar Van condo. Much legal work looms in the prebuild ecosystem.

Hey Nick,

There was recently a similar incident that made the news in Carleton Place, Ontario. A couple putting a down payment on a townhouse and buying for $900,000. Well, same thing as you stated, higher interest rates then when they signed the agreement and now they no longer qualified. Except they either couldn’t get or didn’t pursue alternate funding. Their down payment eaten up with nothing to show for it and the developer turned and sold for I think $500,000 with the legal option to take the original couple to court and could’ve easily gotten the difference between the original agreed upon price and the end sale price (minus down payment). I don’t know if the developer took them to court or not. What a painful lesson.

What is the exposure of the big Canadian banks?

Wolf-

1. In thinking about the central banks’ efforts to reduce inflation, is BOC in a materially different struggle than the Fed?

In particular, I’m wondering about timing, broadness of US economy v. narrowness of Canadian economy, available tools, the fact that US$ is a major reserve currency (at least for the time being), and global impact realities.

2. As a follow-on, I’m wondering if Canadian residential real estate is in any way a dress rehearsal for residential RE in US, or under what circumstances they might diverge?

Thanks for any insights you care to offer.

The strength of the US economy despite the 5.5% policy rates has surprised a lot of people. There are a variety of reasons for that, including that 5.5% rates turn out to be not restrictive in the US, which is a surprise. In Canada, where the economy is so concentrated on housing, that’s not the case. The economy slowed down.

That said, what I’m kind of expecting is that the economic growth will start picking up again in Canada and in Europe, we’re already seeing a little of that, and underlying inflation measures in Europe are picking up again, and rents remain super-hot in Canada. So I think all these central banks are watching the US to see if that re-acceleration of inflation will also happen in their bailiwick. And there’s a good chance of that.

Canadian and US real estate have behaved different. Back in 2006-2012, the US had the huge mortgage crisis and housing bust. And Canada had just a little blip. So I don’t think one is a dress rehearsal for the other.

The GFC + Japan 1990s is the dress rehearsal for what’s coming to Canada and beyond (AUS, NZ, DE). Roaring 2020’s is an app name for this huge global debt/everything bubble.

I hope I am wrong, but there are forces at work here that are in the shadows.

The headline of the February update says: Canada: National House Prices Flat in Feb., -16% from Peak.

So is this actually and increase?

No. You gotta read both articles, not just the headlines. Let’s see if you can figure it out. The first few paragraphs should actually be enough. Actually, the first paragraph should be enough, LOL. Go try to read something, doesn’t bite.

Actually, if you read the titles carefully, you will get the message. And then get that message confirmed in the first paragraph.

WOLF, WHAT YOU SAID ABOUT PRINTING PEOPLE INSTEAD OF MONEY IS QUITE DEDUCTIVE. THERE IS NO WAY OF TAKING THAT OUT OF ANY CALCULATION, YET IT’S NOT DISCUSSED MUCH. EVERY TIME A CHILD IS BORN HE NEEDS A PLACE TO LIVE AND I OWN EVERY LIVING SPACE. SO POPULATION COLLAPSE MAKES MY RENTALS WORTHLESS . MORE PEOPLE PLEASE. IT ACTUALLY IS A MATTER OF DEMOGRAPHICS, NOT MMT.

Please figure out how to type in lower-case on your device. Thanks. Future all-cap comments will be deleted.

Usa has historically most homes per capita.

There isno dearth of homes.

What is lacking is .. inventory.

People are holding homes in hope of rare cuts and thinking hone prices won’t go down.

Once they realize no rate cuts and hone prices are way out of reality i am sure a lot of inventory would cone online

It may take a recession for this to happen…

Canada has the least concentration of humans per square meter or whatever, while at the same time embraced an economic doctrine that enforced one particular point of view that the equilibrium market structure should be determined by the monetary policy. With no regard for the impact on the majority of the population that won the peace.

As a first step don’t re-elect your representative to the legislative branch who, while being paid by the taxpayer, makes more money lobbying for special interests.

I know nothing about your circumstance and have no advice to give.

15% down market on 20% down payment= wiped out equity.

Painful. Very painful.

Question for Wolf and the commentators here. A mortgage at a fixed rate of 3% is worth way less than the face value of the debt. However, for the consumer it still in many cases is valued at the nominal level (even if the consumer had the cash to pay off some or all of the mortgage debt and invests it in t-bills paying 5%+ after tax it still might not be enough to cover the 3% mortgage interest. Why doesn’t whoever holds that mortgage (such as a bank) sell it to the homeowner for less than the nominal value of the debt but more than its market value? Seems like a win win.

There are lots of reasons for a bank not to do this. Here are three of them.

1. Bank earn interest income on the mortgage. They don’t really care about the market value of the mortgage. It’s just normal banking business.

2. If the bank sells the mortgage at a discounted value, they would have to book an actual loss on the mortgage, in addition to losing the interest income going forward. That’s like a double-no-no.

3. In the past, the average 30-year mortgage was paid off in about 7 years – people die, get divorced, re-marry, downsize, upsize, move for a new job, etc. plus refis. Now refis aren’t happening, but people still do the other things. So maybe now the average 30-year fixed will pay off in 10 years. But if a bank has had the 3% mortgage on the books for 5 years, on average there may only be 5 more years to go before the borrower pays it off, at which point the bank gets the REMAINING PRINCIPAL VALUE, and there is zero loss for the bank.

Thanks Wolf, that’s helpful, though with respect to #1 if they sold the mortgage back to the homeowner at a discount to nominal but premium to market value they could buy a security that paid more total interest. #2 is interesting since it suggests a reluctance to realize a paper loss even though based on market value the loss has already occurred. Thanks again for the insight.

It just doesn’t work that way. It’s just dreaming. Banks know how to make a profit, and buying back mortgages at a loss isn’t part of it. Wells Fargo made $4.6 billion in the last quarter and $15 billion over the past four quarters, despite some credit losses. If you think you know better how to run a bank, and you’re going to make money buying back mortgages at a loss, start your own bank.

But Fannie Mae, Freddie Mac, et al. can force banks to buy back mortgages that the banks had sold them for securitization. This can happen if the bank didn’t do its due diligence, and there was some misrepresentation in the mortgage app. Banks try hard to avoid that fate.

I appreciate the points, I definitely won’t be running a bank, it’s just something that aroused my curiosity as a homeowner with a mortgage around 3% that’s basically breaking even by holding t-bills after taxes not to mention the administrative overhead of buying new bills each time the old ones expire, tax accounting, etc.

As you mentioned a lot of mortgages are sold and securitized, and when sold those mortgages with a 3% rate presumably are sold at less than the nominal value of the debt, no?

A BANK IS NOT GOING TO LOSE MONEY ON A MORTGAGE BY BUYING IT BACK AT A LOSS. That’s just stupid. You’re dreaming. Give it up.

The GSEs bought 95% to 98% of all Mortgages from 2010 until 2021. There were no banks who wanted to only make 3% on a 30 year loan. To much risk for return. They just did the origination and act as the loan servicer.

The best way for a homeowner to lock in the 3% financing gain to eternity is to sell the house at today’s elevated prices. Anything else risks losing the gain.

immigration is HIGHLY HIGHLY inflationary with today’s socialist governments.

It baffles my mind that Canadian houses cost this much. Why even move to Canada? There are plenty of places where housing is cheaper.

Mexico comes to mind and Central America? How about Vietnam if someone is from China?

All kidding aside. It certainly does not cost that much to build a new house in Canada or am I missing something?

The rich Chinese moved to Canada in 2015 and 2016. That was all she wrote. The news media will never tell you that.

The issue here is the politicians are reluctant to introduce higher property taxes. Vancouver has one of the lowest carrying costs in property taxes, so the rich pile in to buy appreciating assets that cost less than the appreciation.

Then they (investors, flippers, mom&pops) approach the banks to HELOC this “free equity” and bid up more housing.

It’s a giant house of cards as long as value is ever-increasing. However, in the downturn AKA Recession, it all comes crashing down.

Throw in some money laundering and we are here today. On top of that, epic housing shortages because government stopped building social/low-cost rental housing for people making minimum wages.

That’s Canada RRE in a nutshell.

I won’t be posting as much for at least the next month I broke my left arm right below the shoulder. In a freak accident it actually happened trying to kill a spider. My fire alarm the breaker to it was off and I ran into the bathroom to get toilet paper to squash him with and I was in a hurry as he was moving and I slipped on a tray of grease and the bottom of my shoulder hit full force on the edge of a George Forman grill. The breaker kills the power to the light switch. A lesser man might have died. The muscle fibers in my shoulder saved the bone from getting destroyed as I still have a body builder type body. My hand came down first but nothing was there. I was in the dark. It happened Friday night.

Sorry to hear. I wish you a speedy recovery.

I live in Vancouver. Housing prices are still three to four times what the average worker can afford. Eventually, this will lead to an exodus of workers from Vancouver, causing a cascade of business failures. Politicians have absolutely screwed the economy. Real Estate is a casino. The capitalists own everything and want us all as renting debt slaves who own nothing.