All major categories of spending and investment pulled in the same direction.

By Wolf Richter for WOLF STREET.

The year 2023 was supposed to be the year of the recession. It was the most anticipated recession ever, the most hoped-for recession. Starting in 2022 with the initial rate hikes, the “Leading Economic Index” predicted a recession for late 2022; and when that didn’t come, for early 2023; and when that didn’t come, for mid-2023, and then late 2023, and then early 2024… (we’ve shredded the LEI’s predictions here). A year ago, even the Fed staff predicted a recession for late 2023. You get the drift: the Recession that Didn’t Come.

It didn’t come because our Drunken Sailors got together and partied – consumers, governments, and even businesses. They didn’t want to have any part of this recession.

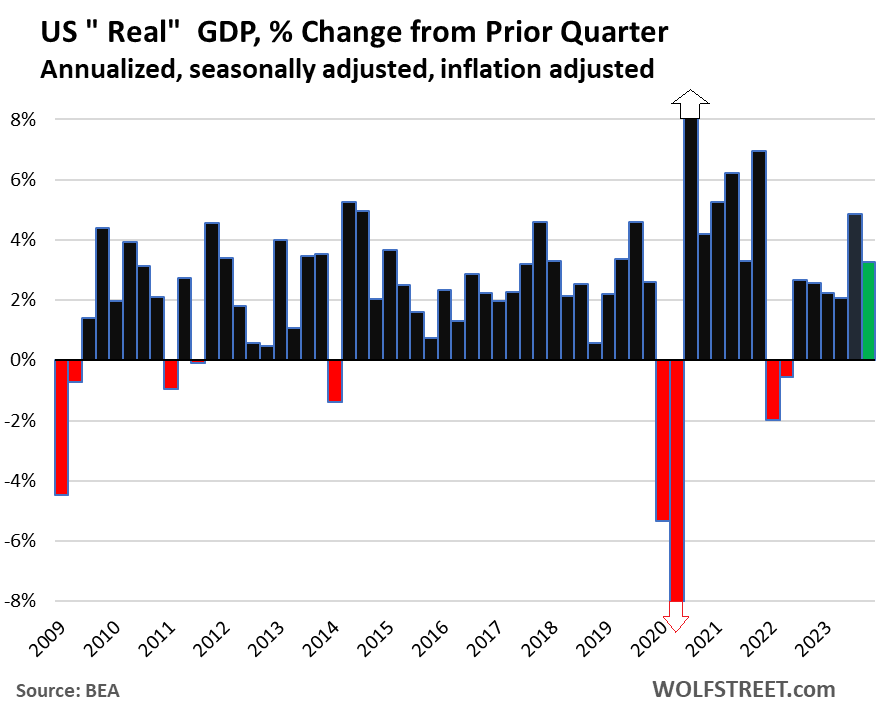

“Real GDP” in Q4 (adjusted for inflation via 2017 dollars) jumped by an annualized rate of 3.3% from Q3, after the 4.9% jump in Q3, according to the Bureau of Economic Analysis today.

All major categories pulled in the right direction (adjusted for inflation):

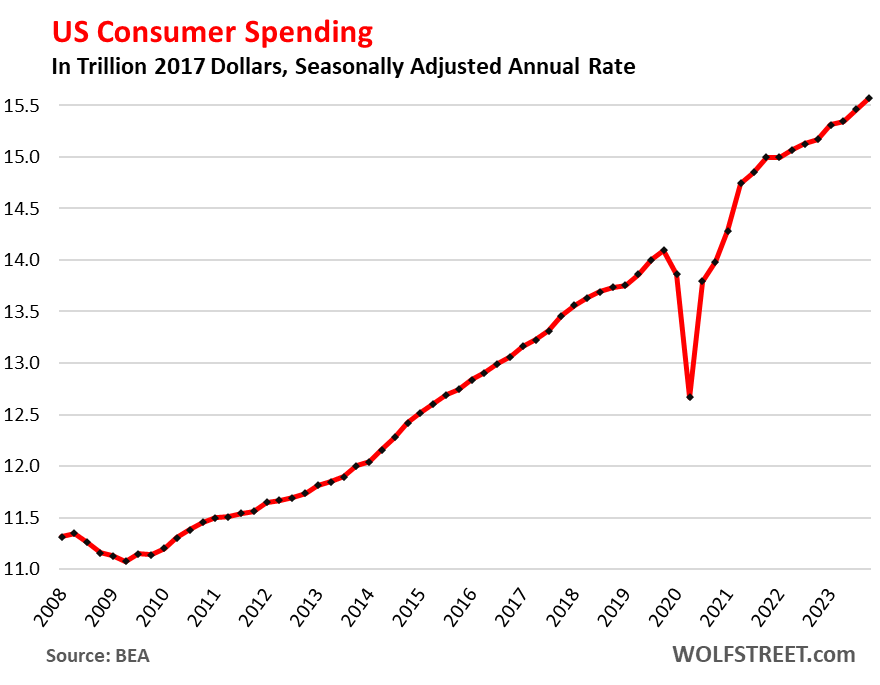

- Consumer spending (69% of GDP): +2.8%.

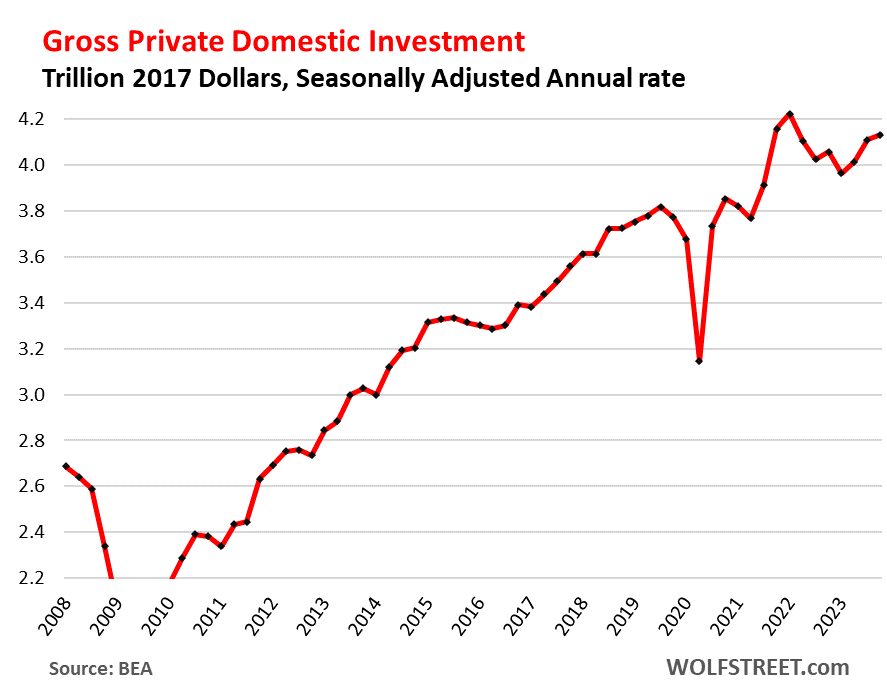

- Gross private investment (18% of GDP): +2.1%.

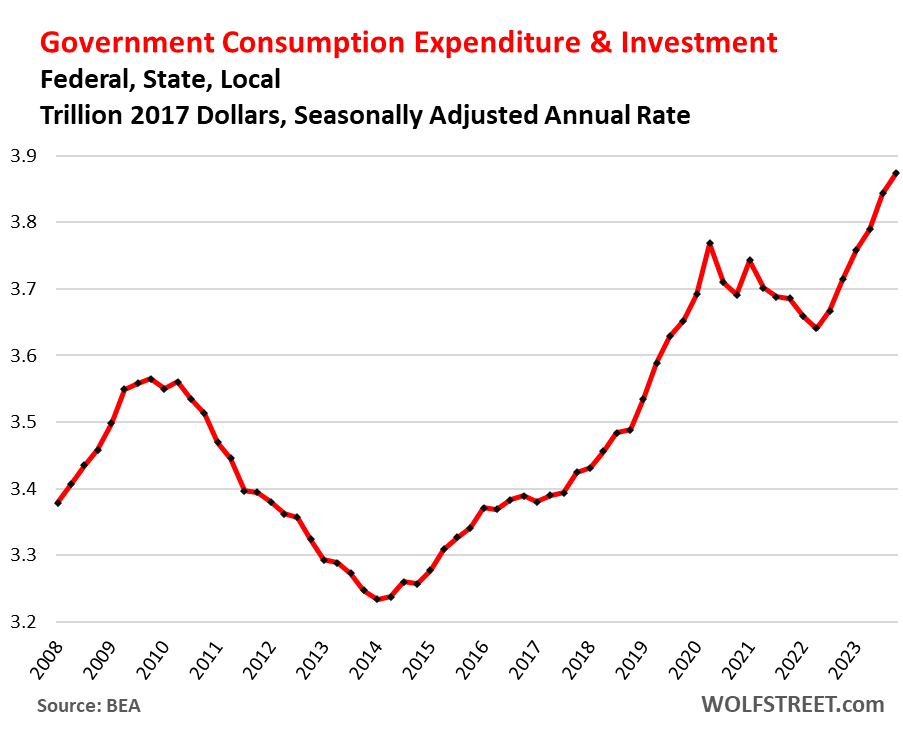

- Government consumption and investment (17% of GDP): +3.3%.

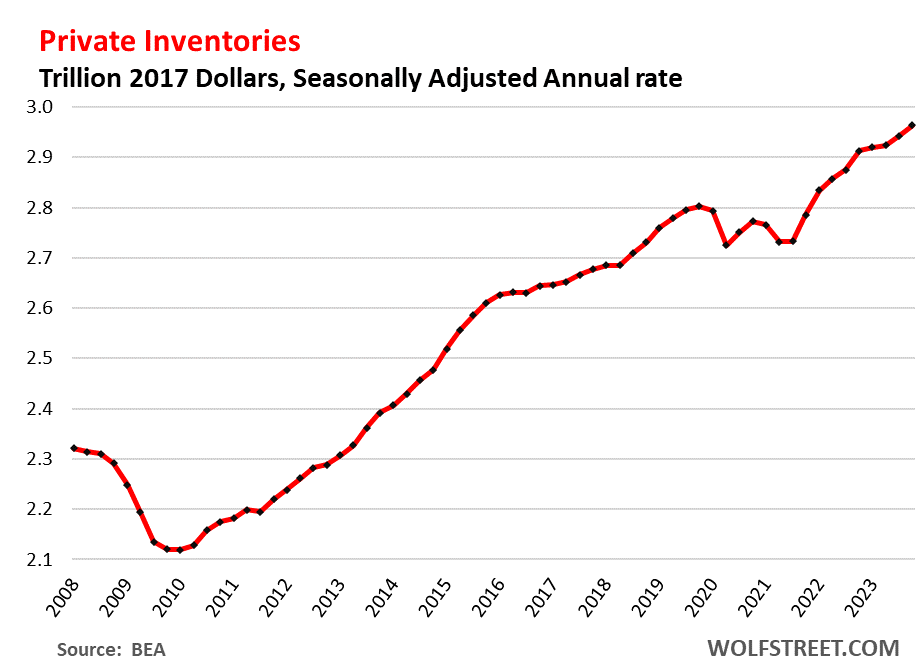

- Private inventory investment increased faster and added to GDP.

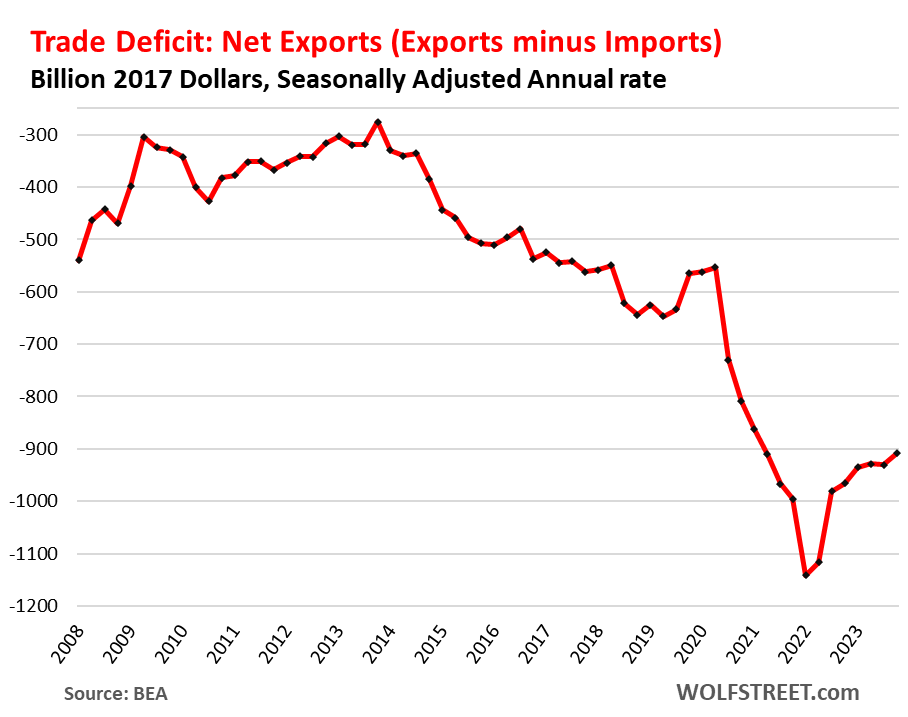

- The trade deficit (“net exports”) got less horrible and was a smaller drag on GDP.

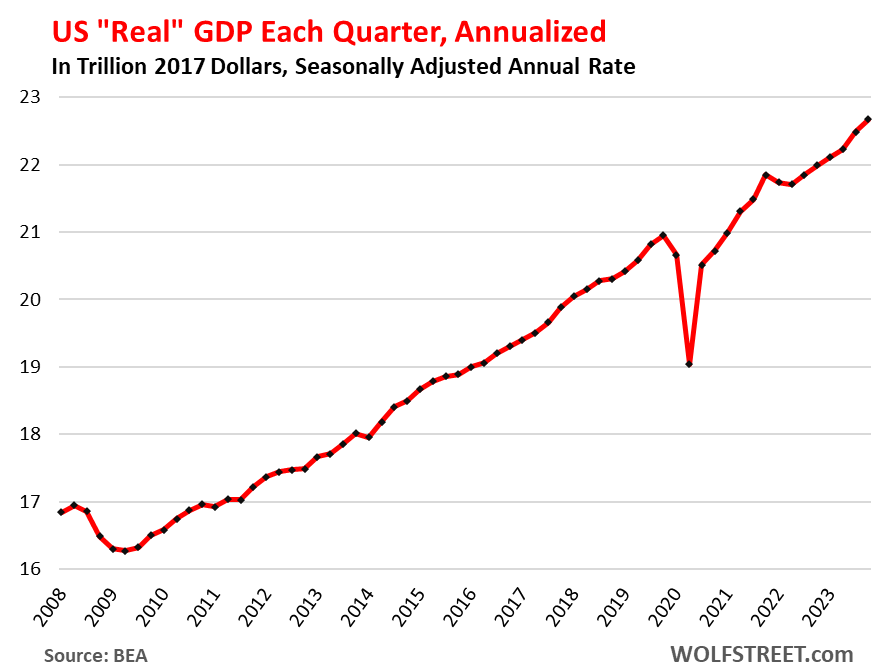

“Real” GDP in dollar terms, adjusted for inflation and expressed in 2017 dollars, was $22.7 trillion annualized.

“Current-dollar” GDP (“nominal” GDP, not adjusted for inflation and expressed in current dollars) jumped by 4.8%, to $27.9 trillion annualized. This $27.9 trillion represents the actual size of the US economy, measured in today’s dollars.

Annual “real” GDP (adjusted for inflation) grew by 2.5% in 2023, right in the range before the pandemic and a tad above the 10-year average before the pandemic (2.3%):

Consumer spending on goods and services rose by 2.8% in Q4 from Q3, annualized and adjusted for inflation.

- Spending on goods rose by 3.8%, including 4.6% for durable goods, which we’ve seen in the surge in motor vehicle sales).

- Spending on services rose by 2.4%.

Gross private domestic investment rose by 2.1%, after the 10% spike in Q3. Of which:

Fixed investment (part of gross private domestic investment): +1.7%, of which:

- Residential fixed investment: +1.1%.

- Nonresidential fixed investments: +1.9%:

- Structures: +3.2%.

- Equipment: -+1.0%%.

- Intellectual property products (software, movies, etc.): +2.1%.

Government consumption and investment rose by 3.3%, the sixth quarter in a row of steep increases. This does not include transfer payments and other direct payments to consumers (stimulus payments, unemployment payments, Social Security payments, etc.), which are counted in GDP when consumers and businesses spend or invest these funds.

The most reckless drunken sailor, the federal government, is blowing vast sums in every direction, relentlessly running up gigantic deficits and piling them on its $34 trillion mountain of debt.

- Federal government: +2.5% (national defense +0.9%, nondefense +4.6%), on top of the 7.1% spike in Q3

- State and local governments: +3.7%.

The Trade Deficit (“net exports”) in goods & services got a little less horrible:

- Exports: +6.3%.

- Imports: +1.9%.

Exports add to GDP. Imports subtract from GDP. Exports are much smaller in dollars than imports (hence the trade deficit, or negative “net exports”).

The stimulus-driven buying binge of goods in the US during the pandemic and the lack of foreign tourism during the travel bans (considered “exports” as money from foreign sources is paid to US businesses) caused the trade deficit to totally blow out. It has since recovered some, but remains far worse than in 2019:

Change in private inventories added 0.07 percentage points to GDP growth. Increases in inventories count as a business investment. Inventories rose by 2.8% annualized in Q4 from Q3. This growth rate was a hair faster than the growth rate in Q3 from Q2 (+2.7%), hence a small contribution to GDP growth. Note the period of inventory shortages during the pandemic.

So in 2023, all our drunken sailors – especially consumers and governments – did their part to keep the spending party going. The recession watch for 2023 is over. The recession didn’t come. Now the recession watch is on for 2024, and recessions are already being predicted to start ASAP.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The most reckless drunken sailor, the federal government, is blowing vast sums in every direction, relentlessly running up gigantic deficits and piling them on its $34 trillion mountain of debt.

As long as the treasury market keeps assimilating the surging supply of new debt, this drunken sailor can continue his drinking spree singing his favorite tune of -deficits don’t matter- and scoffing at any mention of bond vigilantes.

Meanwhile, the Chinese, German, and Russian economies collapse within my lifetime. We Americans are in a fairly good position comparatively, I’d say…

Don’t count on it!

This monetization scheme for debt can only be played for so long.

The rest of the world is waking up to the fact that they have been the patsies. It’s a long-term game but one can see the pieces being moved on the board.

The American Tax payor is the patsies.

Wait until the dollar becomes one of the dirtiest shirts in the hamper rather than the the cleanest shirt in the hamper right now.

Recessions are much less likely since Bernanke’s QE and QT.

With that, the tech bloom, and the tax structure I don’t see any alternative to being a ‘buy and hold long’.

Ohhh, the shame of it all! 😭.

Buy and Hold would works good until it does not work.

But I agree, Fiscal Deficit and QE in general have changed/delayed biz cycles.

As long as people have faith in usd, FED can print till ad infinitum.

Absolutely!

The dollar is like any other commodity…it responds to the dynamics of supply and demand.

And worldwide, nobody can get enough of them. LMAO

MOFO, that’s only because they are confident that the 2020 printing binge was a one time thing because of COVID. If they do it every 3-4 years, I don’t think foreigners will be as eager to hold dollars at 2-4% yields.

Thomas…

Yes….everything changed in 2009..

The “new” Fed will not allow normal cycles to occur. They seem to want all charts to move up to the upper right hand corner.

This prevents the necessary and functional periodic flushing of excesses, thus allowing excesses to build. The eventual “flush” then becomes systemic threatening. Enter the central banker to save, and in so doing, accrue more powers.

Agreed. I think we are 2 years, max, away from the next round of QE, and it will make the covid QE look like pocket change. We could be looking at 100 trillion dollars printed by the fed in a single year.

But hey it would be even more fun! Imagine all the job creation that could be performed by the Graceful Saviours.

Hope it collapses. Disgusting!

Wolf, thoughts on a “rolling recession”? Right now life sciences (biotech/pharma) are in a recession I believe.

In the past people cut back spending, paid off debt, and increased savings when the buzz of recession was in the wind. Could personal spending be so intrenched this time to the point of addiction and they won’t stop until they are just unable to spend right to the bitter end. They may think this time the government will somehow step in and bail them out like they did in the pandemic? Did the pandemic create moral hazard?

I don’t think that’s it, actually. Sure, the pandemic did create some moral hazard, but the real reason people haven’t cut back on spending is simple. People stop spending when they lose their jobs (obviously) and when they see OTHER people losing their jobs, and are fearful that they might be next.

Outside of some media doom porn about layoffs, there really haven’t been any outside of the bubblicious tech sector.

People have no issue finding jobs, but many are not making ends meet or being able to afford housing, which is why the public opinion of the economy is so sour.

Great point. I guess I am just the minority.

Correct Einhal. One of the most glaring non-events of 2023 was the lack of large-scale layoffs. Layoffs were a widely anticipated interest-rate hike consequence that did not happen.

Hard to fault the people who predicted it, however. Interest rate increases USUALLY result in layoffs which then impact other economic activity. Not in 2023, however.

Which supports William Sherdan’s observation: “consumers do not behave according to rational equations built on the assumption that money is the only driver of human behavior.”

Many other motives are in play. This site has discussed some such motives including FOMO and YOLO. Of course, there are many more including envy, greed, power, revenge, jealousy and conformity just to name a few.

The year 2023 also supports Michael Evans prescient contention that “the problem with macro economic forecasting is that no one can do it.” However, the big business of making and selling economic predictions will continue. That is one economic activity upon which you can count.

Consumers will consume…until they can’t.

What makes you think the US government won’t send out checks in the next recession? They’re politically popular, and people have now come to expect them. Recent polls from 2023 suggest two-thirds of Americans support the idea of stimulus checks to help with rising inflation, even with the risk of worsening the underlying problem.

I find this to be one of the funniest and ironic things of all time. But, basic economics are complicated to most.

“What makes you think the US government won’t send out checks in the next recession?”

Inflation.

MJ,

Not sure about this comment so all are welcome to chew it up.

Most of this is from memory though I did research the dates for the IRAs. An a phone calculated the 41.

In 1975 IRA’s for small business were begun. But only for people without a company retirement plan.

In 1981 access was given to all employees, even those with a company pension. The contribution amount was also increased to 2K as both my wife and I began building savings. She is at the beginning of the Boomer class, I’m a little ahead as in Silent Generation.

2022 was 41 years after all the IRA contributions began. It was probably the beginning of the Boomer retirements.

When many people gain access to their life savings they begin to spend. I know from experience we spent a lot after retiring. In our case we slowed in 2019 as age began to creep in and it became less fun to roam. It also meant saving about 1K a month.

Just throwing out some thoughts.

“Could personal spending be so intrenched this time to the point of addiction”

You’ve heard of the Fed put? This is the Biden put. Three years of pavlovian training at every turn that the government will subsidize or bail you out whenever you “feel bad” about your financial obligations. The mindset is now entrenched. Uncle Sugar is there for you.

Let me take issue with the numbers. The following is very misleading:

“Consumer spending (69% of GDP): +2.8%.

Gross private investment (18% of GDP): +2.1%.

Government consumption and investment (17% of GDP): +3.3%.”

Welfare spending financed by deficits is a pretty new thing. Deficits historically financed planes and bridges and bombs and such. A large portion of the alleged “consumer GDP” is, today, is simply deficit financed welfare. Classifying deficit-financed transfer payments and subsidies as “Government Consumption and Investment” puts that category at over 40% of GDP. Also, GDP is nonergodic, but that’s a different problem.

RTGDFA.

YOU are misleading.

Transfer payments (such as welfare) from the government are NOT included in GDP. In addition, welfare payments are small. The biggest portion of transfer payments are Social Security payments to the retirees who paid into the Trust Fund during their working years — that’s not welfare, that’s a pension.

Corporate welfare is an issue, and when government subsidies to companies are spent or invested (to build factories, weapons, etc.) they do go into GDP.

In addition, consumers make most of their money from sources other than the government — from wages and salaries, interest, dividends, rental income, etc.

Here is consumer income, adjusted for inflation, WITHOUT transfer payments:

Wolf:

I wonder if your statement is

“The biggest portion of transfer payments are Social Security payments to the retirees who paid into the Trust Fund during their working years — that’s not welfare, that’s a pension.”

is really correct under what is happening now.

1. The government went for a tiered pricing for the Medicare par B and D. I put in the same money as others (in fact more as my income was on the higher end) but now I am being asked to pay more so that they can keep paying those with less income. That is welfare.

2. I did not get money from my wife’s contributions when I retired before her like others do because I also happen to have other pension. When they took money from my wife, they did not take less in contributions knowing this possibility. That is again a welfare.

Most folks when they hear or say the word, Welfare, they assume the regular stereo type but we have many other forms of welfare.

I was replying to Ken’s line:

“Welfare spending financed by deficits is a pretty new thing.”

So it’s about “welfare spending.”

All numbers SAAR, inflation adjusted 2017 dollars:

Social security is not welfare, it’s a pension, that people paid into: $1.37 trillion. Over the past 20 years, it accumulated a surplus of $2.7 trillion (people paid into it more than they received).

Medicare is not welfare, it’s a health insurance plan people paid into it while working, and still pay into while receiving it: $951 billion

VA benefits are not “welfare”: $173 billion.

Medicaid is a health insurance plan for the needy. So it might fall into the category of “welfare”: $863 billion

Unemployment insurance … companies pay for this as part of their payroll taxes via the government, so it’s not welfare: $22 billion

“Other”… this is all kinds of stuff and includes “welfare”: $582 billion

yes, I don’t pay more for a loaf of bread or for auto insurance based on my income, but medicare premiums go up drastically for higher incomes. That pushes it into the welfare category.

Deficit spending for wars is certainly more beneficial for some than welfare related deficit spending. Long term deficit spending is surely problematic but where it occurs is very subjective. Pretty sure the 8 trillion spent on conflicts mostly in the Middle East was solid for the defense industries, perhaps defense industry welfare is a valid term?

Deficit spending for wars is a transfer program that moves money into the pockets of a few from the pockets of taxpayers of the present and future.

…Eisenhower’s farewell speech comments that coined the term ‘Military-Indusrial Complex’ are evergreen…

may we all find a better day.

Ken

69% + 18% + 17% = 104%

but we live in the 2 + 2 = 5 (for large values of 2) world

BS. Negative net exports are a minus in GDP and deduct from GDP.

We live in a world where people can’t read the rest of it?

Yes, the gentlemen forgot about net exports. Since I can’t reply yet to my own comment above, I will note here a typo: “That the economy has been roughly “70%” of GDP since we were both in diapers, does, I believe, produce a distorted view.”

Please replace “economy” with Consumer Spending. You probably thought that. Sorry for that error.

Wolf, I see that Gross Domestic Income actually fell in 2023 (Q4 est) and that there has never been a gap this big between GDP and GDI.

Do you care to comment on that?

Thanks

Did God tell you that GDI fell in Q4? The BEA surely didn’t tell you because it hasn’t released the figure yet.

The BEA told us so far only that GDI rose in Q1, Q2, and Q3.

All adjusted for inflation.

Ok, Ok, no, God didn’t tell me anything. Yet …….

What I heard from a couple of respected commentators was that there has never been as large a gap between GDP & GDI in 2023.

So when the Gov’t is running obscene amounts of Deficits boosting spending

And GDP is running far ahead of GDI

It seems a fair question to ask

it seems fair to ask about the durability

of this recovery

(sorry about the clunkiness of my reply)

Looks like real GDI growth flat lined since Q4 2022 and even a little negative Q3 2023.

https://fred.stlouisfed.org/series/A261RX1Q020SBEA#0

From the past recessions, it appears that US is either entering a recession or is in one already. However, QE/QT and ample reserve are new things that Fed invented since 2009. It is hard to say what this data all means.

One thing is for sure. Fiscal spending created a lot of the GDP. All my economics courses from decades ago told me that fiscal spending can only have short term effect to the economy and the net result after a year or two is crowding out of the private investment via either taxation, higher interest rate, or inflation.

“even a little negative Q3 2023.”

No. It grew by 1.5% annualized in Q3.

Here’s a “free” lesson in how to use the St. Louis Fed’s FRED system:

1. go to the chart

2. click on “Edit Graph”

3. In the first box where is says “billions of chained 2017 dollars,” click on the down-arrow, which opens the menu

4. choose: “compound annual rate of change”

Now it shows the quarter-to-quarter percent change, annualized … this is how we look at GDP also.

5. Move the left slider button to the right for a close-up of the past few years. You’ll see that all three quarters so far in 2023 were positive.

6. Hover over the line, and you see the bubbles pop up with the figures

The percentage change from a year ago is -0.15%.

If you look at the absolute number, Q3 2023 is a little lower than Q3 2022.

These figures don’t seem to mean much in the current settings. In the past, it indicates recession already.

That has zero to do with 2023. This is due to the base effect from what went on in 2022. In Q3 2022, GNI jumped, so that high level is the base for the Q3 yoy comparison. But in Q4 2022, it fell sharply from Q3 2022. So Q3 2023 YOY uses Q3 2022 as the base (high), and then there is this big drop in Q4 2022 that GNI in 2023 is digging out of.

It doesn’t indicate anything. It has been the same BS for 18 months: we’re in a recession already because of yada-yada-yada. That’s just wishful and dumb BS-ing.

I am moving more towards a psychological view of recessions rather than a purely economic one.

Anyway another round of pundits and commentators that are going to try to spin tried as secretly bad as they have been doing for years now.

Rate cut probabilities just went up in federal funds futures:

March: 40% yesterday to 52% today

December: 5.9 cuts to 6.2 cuts today (assuming 0.25% decrements)

Treasury yields also went down.

Markets focused on the 2.0% PCE deflators in 23Q3 & 23Q4 as a sign the Federal Reserve could soon declare Mission Accomplished.

But again, the quesiton is, WHY cut if the economy is still growing. You need a reason to cut. Not a reason to not cut.

Markets are delusional if they think there will be a rate cut in March. But all you’re looking at is gambling. People or algos are making short-term bets in that market. That’s all you’re looking at.

That market is nearly always wrong in its rate predictions. There are funny charts out there to show how wrong they are. I posted one of them here in 2019 (from Deutsche Bank Research):

Jeff Gundlach is always pointing out how the 2 year Treasury is a great predictor of the Fed Funds rate.

Isn’t the 2 year a function of market “gambling” on the outlook for the Fed Funds rate?

The two-year completely underestimated the rate hikes. In the past, it ALWAYS ran ahead of the rate hikes and eventually overshot. This time around it ran way behind the rate hikes and didn’t even get close to 5.5% much less overshoot.

Even in 2018, it overshot (3.0%), when the Fed’s top policy rate maxed out at 2.5%. It was always leading and overshooting rate hikes, except this time. This time it was lagging by a lot, and never even reached the top. I don’t think this has ever happened before. So it failed in its traditional role of predicting policy.

Part of this makes me think that inflation and the rate hikes aren’t over until the two-year overshoots.

@Wolf,

Good insight and something to keep an eye on.

I sincerely hope you’re right Wolf and that we don’t get a rate cut in March. I was hoping for a hike later last year, but can’t even remember last time it was raised (July?). Way too much liquidity out there still imo.

Z33,

Oil began to rise today and I think it will raise inflation. At least my investments are set along this line.

Inflation came down much too fast. Like yu I would like to see an increase in the Fed rate.

“Markets are delusional ”

Exactly

Selling treasuries futures on the news and then closing out the position quickly?

I’m beginning to wonder if this time is different. Perhaps we will never have a recession again. If QT is only being done to make room for QE when the economy slows, we can theoretically do this forever if deficit spending is slowed and the ratio of debt payments to GDP remains reasonable.

IF in fact QE resumes, then yes, we’ll never have another recession. That’s really the question.

Maybe someone has decided a period of higher inflation is better than a period of higher unemployment associated with a recession. IF inflation can be dialed back by interest rates in the 5’s, which historically is actually normal, then why not?

Like wolf commented, watch the 2 year.

Not even a question. As far as Fed officials are concerned, Bernanke saved the world with QE, and JPow saved the world again with even bigger and bolder QE. As far as those scumbags are concerned, maybe transitory inflation ran a little hot after years of not enough inflation, but QE worked. QE’s record is now 2-0 in their book.

The next time they even suspect a recession is starting, they will use QE, BTFP, RRP, and every other acronym available plus whatever new acronyms they invent custom-suited to the next disaster. We are likely a late stage empire now, and this is usually how it works out. We will print our way out of every recession until the dollar has no more life in it and somebody else dethrones us.

The good news is that this could still go on for a very very long time. China’s economy is showing more cracks ever day and they’re facing a demographic crisis that is unprecedented in human history, so they may not be able to dethrone us. The EU, Russia, or Japan aren’t going to do it. So USD dominance could still hang on for decades or longer. It will continue to lose value as we print more of it, but it could hang in there simply for the lack of a better competitor.

The current generation of policymakers seem forever scarred by 2008. They seem to think that recessions are so intolerably bad for society that it’s worth preventing them at any financial & monetary cost.

In reality, the vast majority of recessions were garden-variety ones that historically occurred every 3-5 years. They resolved themselves within months, didn’t require trillions in government stimulus or QE, and they were part of a healthy economy that prevented bubbles & speculative mania from getting out of control. Frauds like Enron, Madoff, etc. would never have been uncovered in a forever-expanding economy.

I think rising interest rates had SOME of those corrective effects. I cite as evidence, the latest Crypto winter, and lots of Wolf’s imploded stocks.

“Government consumption and investment rose by 3.3%, ”

pretty close to the inflation rates of late…real close

2 trillion a year pumped into a ,phony economy of course we’re partying,free monopoly moneteverywhere

How is it a phony economy?

In the last week I have bought a house, bought a used car, bought groceries, bought dinner out multiple times, and tomorrow I am getting on an airplane and flying across the country.

I pretty sure all of that was real economic activity despite your best efforts to handwave it away with your silly “phony” comment.

Also, money is not free. Currently it costs more than 5% interest to get it for less than a year.

Because it was borrowed from the future. It was money created, but at a cost. Is maybe what they meant.

This is the opposite of almost all informed predictions. Goes to show that predictions over a 12-24 month timeframe are close to useless. Hence the stupid “dot plot” is so worthless.

Yogi Berra – “It’s tough to make predictions, especially about the future.”

The yield curve is still inverted.

Ever since non-recessionary rate cuts became a thing, the yield curve has ceased to have predictive value.

The lower long term rates are in anticipation of rate cuts for so-called policy normalization due to disinflation, not a recession.

The yield curve similarly inverted in 2019 before the Federal Reserve cut rates amid a booming economy.

That’s a great point

Thanks wolf

Didn’t know about the two year overshooting.

I wouldn’t say the yield curve inverted “similarly” in 2019.

On my charts it has never been so inverted? 10y-2y or 10y-3M.

Yes, distortions everywhere. The journey into the desert analogy seems most fitting:

We know we don’t have enough water to turn around so we must keep moving forward.

Unless ‘this time is different’ than all previous world economic conditions: this does not end well.

I agree that this can go on much longer than most people believe (maybe already has?).

“When all else fails, take them to war” comes to mind. Seeing that housing affordability has “priced out 50% of renters” makes me think of civil unrest.

Granted it’s a CNBC clickbait (that I didn’t read) and I live in an unaffordable place with ample vacant square footage: something will give eventually (somewhere), and probably in a big way?

Yield curve has no more significance in this era of FED’s intervention.

Yield curve would matter in relatively free economy.

The central banks have a policy called “yield curve control”. As long as central banks and not free markets control interest rates, the yield curve is less useful as a predictor.

Lately, the treasury printed a schedule of what bonds would be sold, and it was opined that the issues were tilted to short term issue and not long term issue. It could easily be the other way around. Also, the QT is set to let bonds expire, and short term expires faster. I’m not seeing an effort by the Fed to keep the proportion of short, medium and long term debt constant.

TL:DR – governmental intervention interfering with the price discovery in debt markets reduces the reliability of the yield curve predicting future economic outcomes.

The change in the composition of the money supply, more transaction accounts than gated deposits, fueled the momentum in N-gDp, in AD.

The 24 mo rate-of-change in money flows, proxy for inflation, has reversed to the upside in December.

The 10 mo rate-of-change in money flows, proxy for the real output of goods and services, rebounds in the first half of 2024.

Wolf, when we compare with China why do world bank or IMF use the $27 trillion GDP rather than the $23 trillion real GDP? Any idea?

Yes. If you compare the GDP to anything else, you use “current dollars” because those are the actual dollars. So the US has a “$27-trillion economy.” Debt-to-GDP ratios are calculated with current-dollar GDP and current-dollar debt (apples to apples). I will post an article shortly with debt-to-GDP calculations based on current dollar debt ($34 trillion) and current-dollar GDP ($27 trillion).

And when you compare the GDP of one country to another, you use current-dollar GDP for both (you convert the current-local-currency GDP into a current-dollar GDP for that country), and then you compare both current-dollar GDPs.

The “real” GDP uses 2017 dollars for an inflation adjustment. Those are not current dollars, those are 2017 dollars — so the amounts are a lot lower. This is used to calculate inflation-adjusted growth rates. It really doesn’t have any other purpose, other than getting inflation adjusted growth rates.

If Janet and co don’t run the economy flat out then how do they hope to inflate away the debt ? Therefore they have to.

Personally I thought the dollar may have started to decline a bit by now but so far no dice on that.

I think we (drunken sailors) are running the economy, not not the Treasury.

Sail on, sailors! I’m feeling some of that wind in my sails.

GDP went from $16T in 2009 to $23T in 2023. That’s almost a 50% increase. How many people have seen their income go up by 50% since 2009?

Not many, I’m thinking. Wages certainly haven’t increased that much.

GDP includes the whole economy, not just consumers, and it includes investments, not just consumption. It includes everything that businesses and governments consume and invest.

Real GDP 2017 dollars:

2009: $15.50 trillion

2023: $22.67 trillion

growth: 46%

Personal income without transfer payments:

2009: 11.3 trillion

2023: 15.9 trillion

Growth: 41%

I’ve never met a sailor as drunk as a typical Cubs fan in the bleachers.

Annecdote: Working in construction, procurement, so we are always looking ahead 3-5 years to account for changing costs such as labor, materials, fuel, etc. Back in 2022, upper execs said “This inflation is slowing, there’s going to be a recession in 2023, so we shouldn’t get too carried away with escalation/inflation/shortages adjustment.” Fast forward, no recession.

Our subs are still jacking up prices, ignoring their signed contracts and telling us “I’m not honoring that price, this is my new price. You don’t like it? Sue me!” Crazy stuff. Where is this recession? Back in 2008-2010, construction costs went through a huge deflationary period. Two polar opposite worlds.

A few years ago I did some consulting for a bunch of small businesses. I still keep in touch with many of the owners. About a month ago I dinner with a guy whose business worked in a construction adjacent area.

He was always a very conservative person. He was always hedging his risks wherever he could. He always tried to have as many suppliers as possible. He would sign supply contracts with 3 suppliers at different prices just to make sure he had other options if something went wrong. Obviously of the 3 the better suppliers always got most of his business, but he always gave the other two enough business to keep them interested.

So about 8 months ago he put in a monthly order with one of the suppliers he had a contract with and the supplier basically did what you said. The supplier told him “Sorry. This is the new price. Sue us if you want.” So he paid the new price, but immediately called the other two suppliers and asked them if he could increase his orders with them at the same prices he was getting (higher than the initial price he was getting from the first supplier, but lower than their price increase). They told him it would take about a month to ramp production. They signed an amended contract.

After a month he stopped ordering from the first supplier. After some time when he hadn’t ordered anything from them, they called him and asked what was up. He said he was having some issues, but everything would be cleared up by the next month. So he ghosts them again. After a while the supplier keeps trying to contact him the supplier tells him that he has a huge inventory of supply that has built up, he blows them off. Ghosts them some more.

Finally the supplier has a lawyer send him a certified letter threatening him with a lawsuit if he doesn’t place his contractually obligated orders soon.

My friend responds to the lawyers letter by telling him that they do not have a contract. He says that the supplier broke the contract when he raised prices. He then sends along a copy of the email where the supplier basically tells him to sue him over the price increase.

He didn’t hear anything back for a couple months. Then one day he receives a message from the lawyer asking him if he wanted to buy out the suppliers inventory of product. He responds and asks at what price. The lawyer gives him a fairly very low price. So low that my friend suspects something is going on.

He does some research and finds that the supplier is declaring bankruptcy and going out of business. This supplier had done the same thing with multiple companies. Basically raised prices and told them to sue him if they didn’t like it. A couple did sue him and most just went elsewhere knowing the contract was now invalid.

My friend, put in a real low ball bid for the product, so low that he almost lost it to one of those disposal companies that bid on bankruptcy assets (everything from product to office furniture). He raised his bid enough to win, but still got a phenomenal price on about 3 months worth of product.

The story made me think there might be some karma in the world after all.

Kinda nuts how soft landing things have felt on one side of the sentiment… Inflation coming down, rates normalizing, stocks at ATH, no housing crash, no recession.

On the other side of sentiment… Can’t afford food, rent, childcare, car loans not to mention lame duck election and ballooning government debt

Calm before the storm or did the hurricane run outta warm water?

I imagine we’ll see a ton of patting ones self on the back next week from Powell

The GDP and spending seem to have stabilized at the same rate (linear from 2009-2023. The ZIRP mania) but at big cost (debt ballooned). We might need few more years to see if even that would be sustained if there is no more ZIRP (folks seem to forget that if the inflation drops to 2%, FED rate has to be around 3 plus) and QT continues. Already private investment seems to be stagnating or declining and P inventory bulging.

The government part seemed to have exploded (in a relative sense) from 2014 – I guess all the housing and stock appreciation.

Trade deficit: Is it MAGA or MNIA (made not in America) winning?

I don’t think you understand who has brought more manufacturing jobs back into America. It wasn’t MAGA.

Who would have thought it? I am happy to see net exports rise. Let’s get some manufacturing from China.

2023 is a good example of “markets can stay irrational for longer than you can stay solvent.” No nation can print trillions of dollars of money without severe economic backlash. However, they can kick the can down the road for a long time. If you want to gamble, go to a casino. They have a better buffet than Wall Street.

When a nation recklessly prints money it shows up in yield. Oddly enough that isn’t really happening yet to the U.S.

There’s a step in between: inflation. If there is no inflation, yields stay low. If inflation rises, eventually yields catch up. If then a central bank tries to push yields back down by asset purchases (money printing) despite inflation, you get financial repression, which leads to even greater inflation. It’s ultimately all about inflation. As long as there is little inflation, central banks get away with nearly anything.

This is a mystery to me. There is a talk of a stopping QT and keep fed balance at a level not much lower than the current level. Isn’t that permanently creating money? How is that not inflationary? Fed finances US government debt by holding on to the long bonds. If any other countries do this, their currency would devalue rapidly to reflect this. Is US able to export inflation to other countries?

“This is a mystery to me. There is a talk of a stopping QT and keep fed balance at a level not much lower than the current level.”

That talk may be on Zero Hedge et al, but it’s wishful BS-ing, it’s not coming from the Fed.

I cannot respond to a question framed in a BS premise. I can only shoot down the BS premise.

Is this just the inflationary mindset in action; i.e. “Spend money today because tomorrow it will buy you less”

You must have missed Wolf’s last article on this. They aren’t just spending. They are saving at reasonable rates as well.

People are spending because wages have risen much faster than goods inflation.

People feel rich because their paychecks are increasing.

Not to draw comparisons between this cycle and prior ones, but for those that remember the GDP grew in Q1 Q2 and Q3 of 2008. It also grew in Q3 of 2009. Similarly the GDP remained flat or grew slightly in 2000-2001 dot com crash.

So recessions don’t mean the end of the world, They are minor fluctuations in aggregate output but those minor fluctuations are enough to wipe out almost 50-60% of corporate profits. And when you start with high valuations as they are today, the damage to paper wealth can be quite serious.

If I were to guess, I think the asset deflation will eventually cause the recession rather than recession causing asset deflation.

But then who knows the future :)

GDP +2,5% for the year

Gov spending is 17% of it, approximately +0,48% to GDP

0,48% out of 28 trillion equals around 140 billions

Debt growth was above 2 trillion

2 trillion spent to add 140 billion to GDP

Looks like not very efficient way to deploy capital, especially considering that at 5% rate yearly cost of this capital is 100 billion

“The most reckless drunken sailor, the federal government, is blowing vast sums in every direction, relentlessly running up gigantic deficits and piling them on its $34 trillion mountain of debt.”

It’s disgusting, and the idiots in Congress won’t stop. And, of course, greed street loves its uncle sugar spending, can’t make it without it.

I’m sure that healthcare has the PCE up there.