Consumers still on a buying binge at retailers, fired up by big income increases that this year outran goods-inflation by a wide margin.

By Wolf Richter for WOLF STREET.

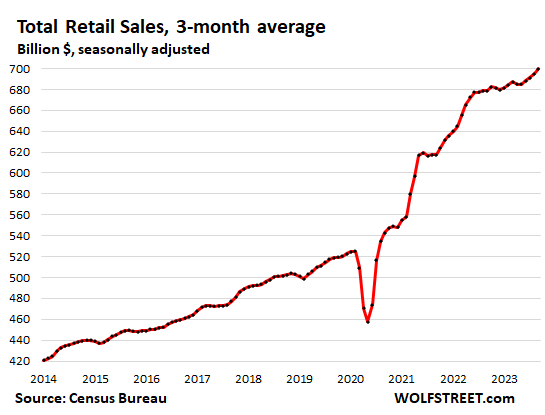

Total retail sales, including at bars and restaurants, jumped 0.7% in September, after the upwardly revised 0.8% jump in August, and the 0.6% jump in July. Over the past three months annualized, retail sales jumped by 8.7%, a sharp acceleration from late last year and earlier this year.

Compared to a year ago, retail sales rose 3.8%, seasonally adjusted. Our beloved drunken sailors, as we’ve come to call them because they just refuse to slow down, went on another buying binge at retailers, fired up by the biggest income increases in decades.

The chart above shows the three-month moving average to tamp down on the monthly squiggles that can obscure the trends.

Retail sales outran inflation in goods by a wide margin. Retailers sell goods, and inflation has shifted from goods (from retailers) to services that retailers don’t sell, and the prices of many goods that retailers sell have dropped. The CPI for durable goods has dropped 2.2% year-over-year. The CPI for nondurable goods rose 3.2% year-over-year. Combined, total goods inflation rose by 1.5% year-over-year, less than half the year-over-year increase of retail sales of 3.8% (my discussion of CPI inflation, including lots of charts, is here).

Disposable income outran inflation in goods by a wide margin. That’s where the money for the additional spending came from. Disposable income jumped by 7.3% year-over-year, outrunning goods-inflation of 1.5% by a wide margin.

Retail sales are not a measure of “consumer spending.” Consumer spending is far broader than retail sales. Consumer spending includes spending on goods at retailers but is dominated by spending on services that retailers don’t sell, and we track this overall spending by our drunken sailors separately and adjusted for inflation.

Retail sales by major segment of retailers.

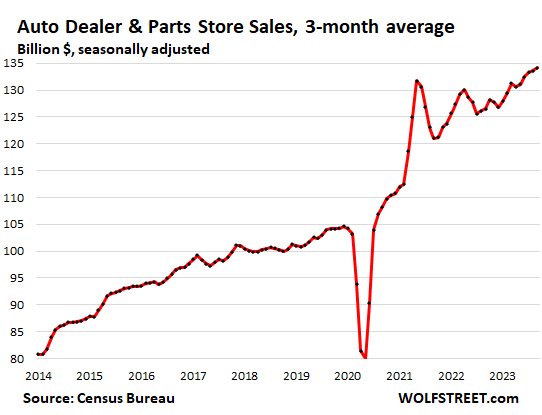

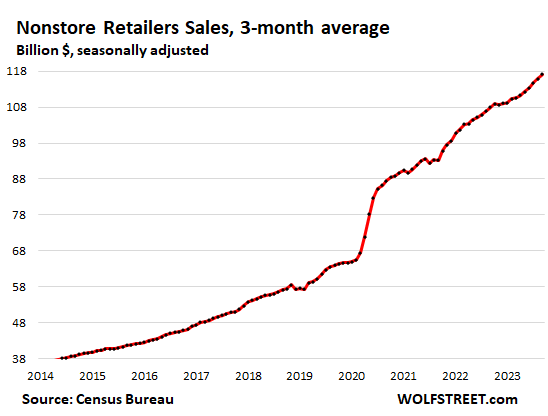

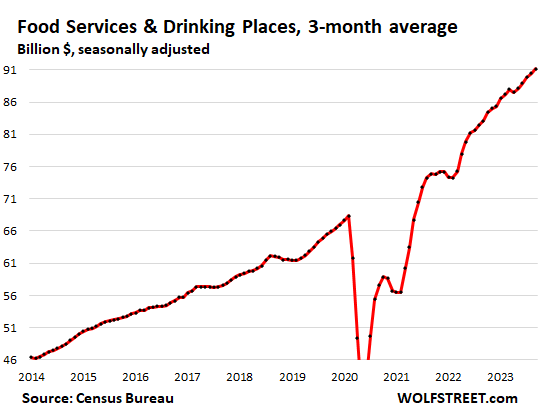

Among the big retailer segments, the standouts were ecommerce retailers (which include the ecommerce sales of brick-and-mortar retailers, such as Walmart’s ecommerce sales), auto dealers, and bars & restaurants. Clearly, consumers are operating on the time-honored principle of YOLO.

All dollar amounts are seasonally adjusted. All charts show the three-month moving average to reduce the monthly squiggles that can obscure the trends. The charts are in order of magnitude of the segment, from biggest to smallest:

New and Used Vehicle and Parts Dealers (22% of total retail sales):

- Sales: $135 billion

- From prior month: +1.0%

- From prior month, 3mma: +0.4%

- Year-over-year, 3mma: +6.0%

Ecommerce and other “nonstore retailers” (16% of total retail sales), ecommerce retailers, ecommerce operations of brick-and-mortar retailers, and stalls and markets:

- Sales: $118 billion

- From prior month: +1.1%

- From prior month, 3mma: +1.0%

- Year-over-year, 3mma: +8.4%

Bars & restaurants (officially, “Food services and drinking places,” 13% of total retail), Our drunken sailors are spending a lot more eating and drinking out than at food & beverage stores:

- Sales: $92 billion

- From prior month: +0.9%

- From prior month, 3mma: +0.8%

- Year-over-year: +9.7%

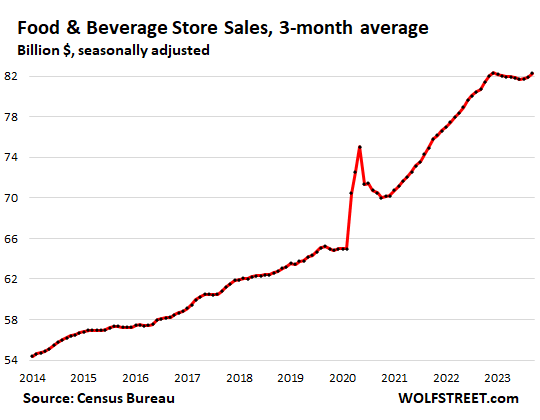

Food and Beverage Stores (12% of total retail). Sales were roughly flat earlier this year as food prices, after spiking, flattened. Recently, food prices have been ticking up again:

- Sales: $83 billion

- From prior month: +0.4%

- From prior month, 3mma: +0.4%

- Year-over-year, 3mma: +1.9%

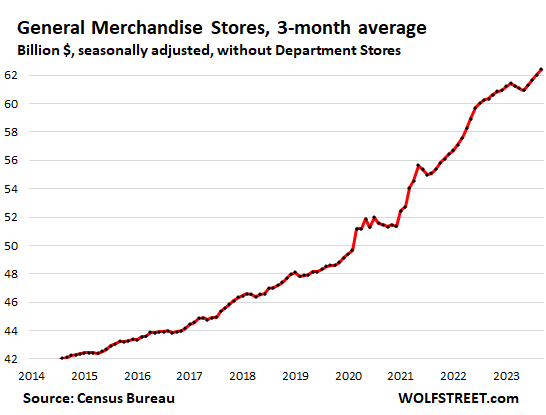

General merchandise stores, without department stores (9% of total retail):

- Sales: $63 billion

- From prior month: +0.5%

- From prior month, 3mma: +0.6%

- Year-over-year, 3mma: +3.5%

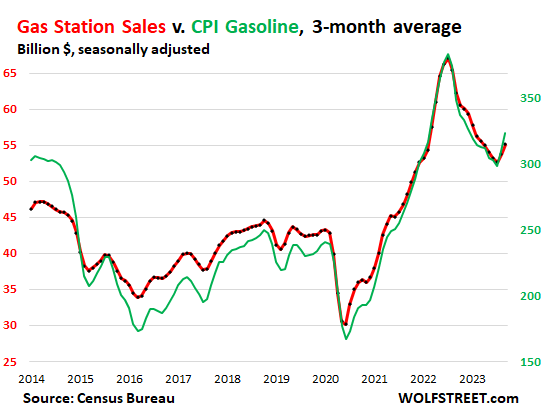

Gas stations got a boost from price increases (8% of total retail sales). Sales at gas stations move in near-lockstep with the price of gasoline. But gasoline prices, despite the recent price increases, are still a lot lower than they’d been in the first half last year:

- Sales: $57 billion

- From prior month: +0.9%

- From prior month, 3mma: +2.6%

- Year-over-year, 3mma: -11.3%

This chart shows the CPI for gasoline (green, right axis) and sales in billions of dollars at gas stations, including other merchandise that gas stations sell (red, left axis):

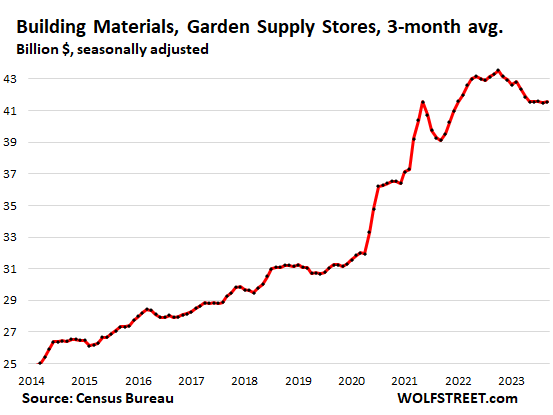

Building materials, garden supply and equipment stores (6% of total retail). Pandemic bubble bye-bye:

- Sales: $42 billion

- From prior month: -0.2%

- From prior month, 3mma: +0.2%

- Year-over-year, 3mma: -4.0%

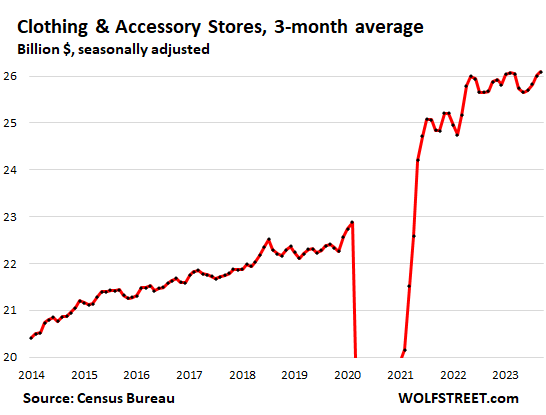

Clothing and accessory stores (3.7% of retail):

- Sales: $26 billion

- From prior month: -0.8%

- From prior month, 3mma: +0.4%

- Year-over-year, 3mma: +1.6%

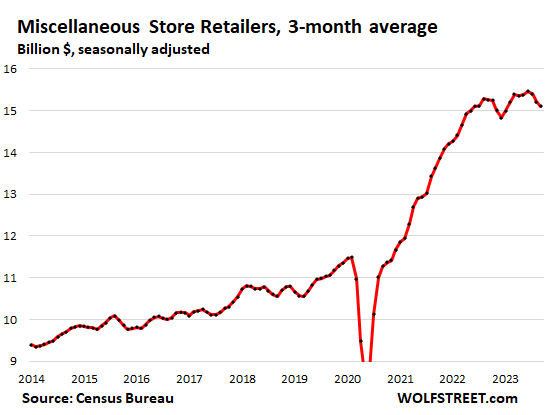

Miscellaneous store retailers (2.2% of total retail): Specialty stores, from art-supply stores to cannabis stores.

- Sales: $15.2 billion

- Month over month: +3.0%

- Month over month 3mma: -0.7%

- Year-over-year, 3mma: -1.0%

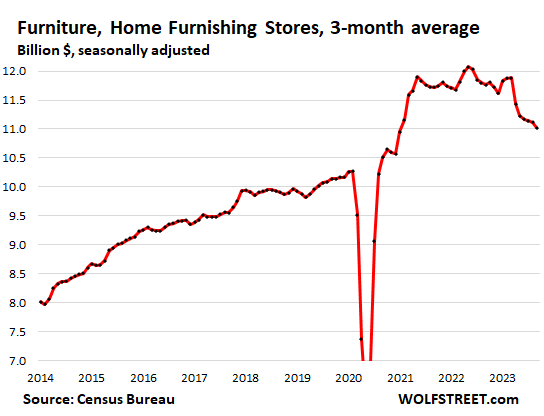

Furniture and home furnishing stores (1.6% of total retail). A big portion of furniture and furnishing sales have wandered off to the internet, with huge online retailers, such as Wayfair, dominating the scene. This is what’s left over at brick-and-mortar retailers that specialize in furniture and furnishings:

- Sales: $11.0 billion

- From prior month: 0%

- From prior month, 3mma: -0.8%

- Year-over-year, 3mma: -6.3%

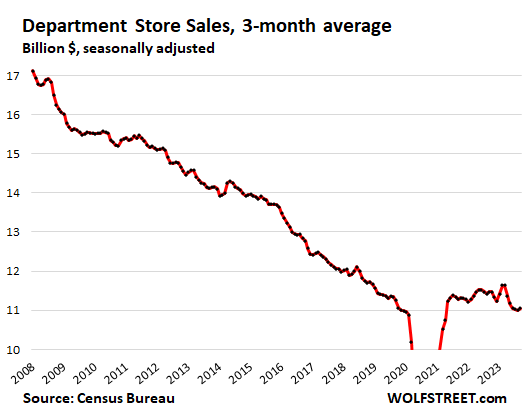

Department stores (1.6% of total retail sales, down from around 10% in the 1990s). Ecommerce sales by department store chains are not included here, but are included in ecommerce retail sales above.

- Sales: $11.1 billion

- From prior month: 0%

- From prior month, 3mma: +0.5%

- Year-over-year, 3mma: -3.6%

- From peak in 2001: -40% despite 22 years of inflation.

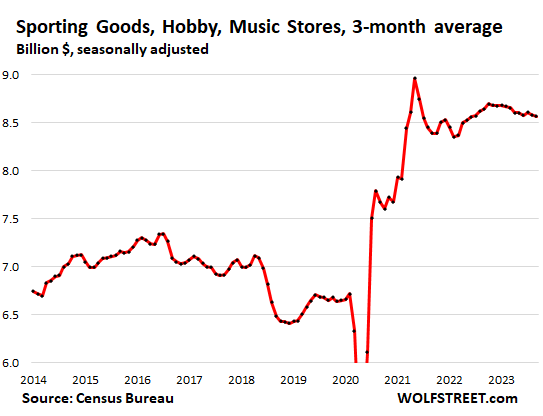

Sporting goods, hobby, book and music stores (1.2% of total retail):

- Sales: $8.5 billion

- Month over month: 0%

- Month over month, 3mma: -0.1%

- Year-over-year, 3mma: -0.9%.

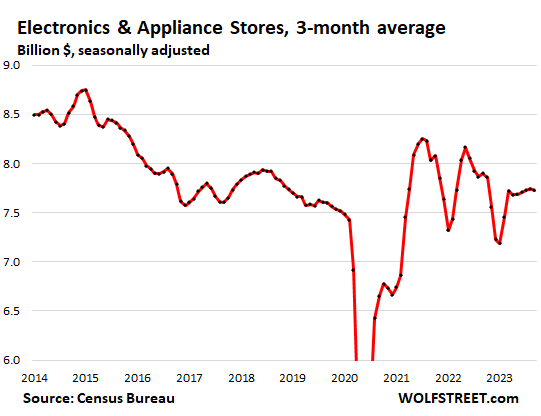

Electronics & appliance stores (1.1% of total retail):

- Sales: $7.7 billion

- Month over month: -0.8%

- Month over month, 3mma: -0.2%

- Year-over-year, 3mma: -2.2%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

GDP Now popped up to 5.4% today.

30YFRM jumped to 7.92%.

CME still shows an 88% chance of an 11/1 stay put.

Unbelievable! Somebody is lying.

This is getting ridiculous! (Rushes out to buy tulips).

The purpose of QE, deficit spending and low interest is to suppress all the standard economic indicators.

Now the Fed is flying blind, so is the government, the markets, the businesses, the consumers and even the media.

The American dream keeps getting more and more distant from reality.

The decision to explode the money supply in 2020 was the most ill advised and truly unauthorized move in our nation’s financial history.

How is it that the “lender of last resort” (The Fed) accrued such powers as to central plan and intentionally distort the value of our currency?

The Constitution is clear that the amount of money in the system is a Congressional power (the power to mint), and at least Congress answers to voters. Physical minting and digital minting are akin.

Markets believe that as long as inflation continues its slow downward trend (especially in the 1-year annualized rates), peak interest rates don’t need to be much higher to snuff out inflation.

But they are coming around to “higher for longer.” Federal funds futures for December 2024 have priced in a bell curve centered around 4.75-5.00%, with a range of 4.00-4.25% to 5.50-5.75%. This is reasonable given the range of possible outcomes includes everything from a moderate recession to a perfect soft landing. Markets are now pricing in a small but non-zero chance of no rate cuts next year, which had previously never been the case.

Here’s the problem with that pivot monger “market” thinking. As long as government refuses to compromise, refuses to raise taxes or decrease spending, engages in foreign wars, and runs $2-$3 deficits, there will be no landing whatsoever. The economy will be completely dependent on continued fiscal stimulus and we will stay in the inflationary jet stream.

Let’s say the market is right in the short-term and the government can pump $2-$3T of artificial stimulus into the economy while keeping inflation at 2%. What does that say about the strength of the real economy? It’s not a good thing. It means the real economy has lost massive amounts of growth potential and efficiency. It means there’s a deflationary bust waiting to pounce as soon as the excessive fiscal stimulus ends.

Looking at Fed St Louis, credit card defaults and consumer loan defaults are on the rise. Still overall low percentages but rising. CC defaults are now highest they’ve been since 2011. This info is a bit late, only showing Q2. But there are other articles showing even higher more recent percentages. Auto loan defaults are also highest since 2011. So a lot of spending there might be, but there is an underbelly to this. A growing portion of people getting into trouble.

Until the very very recently, government outlays have not grown as fast as overall GDP.

That doesn’t mean their is no importance to the debt fueled portion of the growing government outlays, but it does seem to indicate that if their is a debt driven spending problem, it is more likely in the private sector.

Perhaps, or, markets are still under the control of the abundance of Federal Reserve er, reserves.

The Fed is walking a plank about how to withdraw the excess script without causing the everyday economy to freeze.

Sometimes, one has to allow the fool to make it right.

At the current reverse repo burn rate to prop up the wall of new Treasury issuance, the Fed has about two months before the flying buttresses collapse:

https://fred.stlouisfed.org/series/RRPONTSYD

RRPs were at $0 before April 2021, and they’ll revert to $0 just fine. They represent one aspect of excess liquidity in the system, as a result of QE. And QT is wringing out that excess liquidity.

I told you in September 2022 that they could go back to $0 where they’d been. This is what I said:

“In theory, they can drop to near-zero as liquidity is wrung from the system via QT. There is no reason for the Fed to maintain a minimum balance of RRPs. This is demand based, and as other interest rates rise and liquidity vanishes, RRPs could drop to very low levels four years from now. So for our theoretical minimum, let’s say this is near $0.”

So we’re 13 months into this prediction, and there’s still $1.1 trillion left to be wrung out of RRPs.

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

You need to keep your eyes on reserves. They cannot go to $0 and they were never at $0. When they drop too low, there will be problems in the banking system.

Price of gas dropping

as the Mideast goes nuts…

put that in an algo

Eat, drink, and be merry.

You know the rest.

will do, wife’s b-day today

going to new place(nothing under $30)

even get to play corn hole at place

should be $300 today – hope they take CASH

Can’t help but feel there’s a gigantic black swan floating out there disguised as a party boat.

Isn’t this what we would expect to see? Very high cost items (cars) are selling out of fear that their prices will go up even further. Very low cost restaurant spending is continuing to go up because it is a “treat” one can give oneself… plus so much of modern socializing happens in bars and restaurants.

So if it costs more than $15,000 (cars) then consumers are spending… and if it costs less than $150 (F&B) then consumers are spending. But almost every category where items cost a few hundred to a few thousand the spending has flatlined or declined.

Ecommerce sales exploded, and ecommerce goes across the spectrum, from low-cost doodads to $50,000 used pickups. So your theory is very hard to prove unless you can dig up data on ecommerce sales.

Good point.

Hey Wolf, do you have any data on credit card debt or consumer savings to accompany this data? It would be useful to know if this spending is funded by debt, dipping into savings, or if everyone got big pay raises and is just living their best lives and spending responsibility.

Monica Boomgaarden,

Yes, lots of data, and I gave you some in the article.

It’s not funded by debt. I gave you the income figures in the article. Disposable income jumped 7.2% yoy! That’s where this money is coming from. From INCOME!

Over $5 trillion a year gets paid for by credit cards as a payment device, and nearly all of it gets paid off before due date. And only a small portion, if any, gets added to the interest-bearing balances.

Reported credit card balances — that $1 trillion you hear about — are statement balances, most of which will be paid off in full before due date and never incur interest. People just collect their 25 cash-back or their frequent flier miles at the merchants’ expense, and then pay off their statement balances.

Here is something to chew on:

https://wolfstreet.com/2023/08/19/how-many-americans-have-interest-bearing-credit-card-debt/

Wolf,

Regarding disposable income, a graph of “Real Disposable Personal Income” at the stlouisfed website shows a significant jump in December 2022. Any idea what caused that?

Overall, disposable income seems to hover well above pre-pandemic levels. Perhaps paradoxically, saving rate is about 50% lower than pre-pandemic average.

Hi Wolf, what a wretched business model for the likes of Capital One, etc.

Credit card company borrows at 6%+, lends to us at 0%. We pay in full on the due date. No interest, no fees, they pay us cash rewards and we even collect interest on the float.

How long until one of these companies goes tits up?

Big Bongo,

Great business model. For every $100 you pay for with your card, the bank collects about $3 (sometimes more, sometimes less) in fees from the merchant, even if you pay off the full amount by due date. The more you spend, the more the bank makes in fees, even if you pay off everything by due date and never pay interest.

Credit Cards were used to pay for over $5 trillion in merchandise in 2022. These 3% fees add up quickly!

BigBongo nobody is going TU. You are forgetting swipe fees. That’s where the money is.

Big bongo…those rewards are paid by the merchants fees where you used your card! Nothing is free, and trust me, Cap. One is not losing money.

“Great business model. For every $100 you pay for with your card, the bank collects about $3 (sometimes more, sometimes less) in fees from the merchant, even if you pay off the full amount by due date.”

This is the main reason why banks want to get rid of cash – to get a cut of EVERY single transaction.

The top 40% are the ones who are mostly spending all the money. The bottom 60% are either treading water or getting hammered.

“Yo Ho”!! – Captain Jack Sparrow

These numbers are eye-popping.

Isn’t there an argument to be made that people aren’t actually spending like drunken sailors (IE irresponsibly and without concern for future solvency), but are actually spending like sober accountants?

Their income is increasing, savings rates are staying relatively stable, and inflation’s constant grind makes it more responsible to buy now than in a year when you may lose 3 to 9 percent of your buying power. It seems like a logical choice, despite the wild increases in spending over the last few years.

Yes. Drunken Sailors is tongue in cheek.

I suggest that perhaps the old butts are starting too spend, after spending 15 years or so in the desert of ZIRP, QE.

The whip on the back of the savers for the benefit of the speculators.

“makes it more responsible to buy now than in a year when you may lose 3 to 9 percent of your buying power.”

Hello, Fed? Are you listening? Or are you just timidly sitting on your hands?

The top 40% are the ones who are mostly spending all the money. The bottom 60% are either treading water or getting hammered. Wolf covered the income intervals a couple of weeks ago. Very eye opening stuff.

Well, I’m not spending even though I have a huge jump in income. I prefer to watch my balances grow than to spend on stupidity like many do. I highly doubt the average American thinks that far ahead to say they better buy now before inflation gets worse. I also think some of us super saver types skew the savings rates, but I don’t believe many are both saving and spending more at the same time. Knowing the mentality of the average American (spend now and not worry about tomorrow), I find it hard to believe.

What would it take for this party to come to a very quick end? Obviously whatever that is, the drunken spree is not going to stop until that happens.

Powell decides to knock down all the bulls(hit), or not. Fed loves to play cat & mouse with the stock market. Flush it and the inflation scare is kaput. Instead there is just more teasing. So now it’s Santa takes us to 4800, and for what? Tu run the play again in 2024?

My guess is the Fed stays pat on Fed Funds…

but lets the reality of more debt supply and QT take care of the yield curve

Yes, perhaps, the safety of consensus while destruction reigns.

The yield curve is currently a fictitious machination about what a free market might look like if it was actually a free market.

But, of course, it is the antithesis of a free market. One controlled by the Federal Reserve,

pretending that their decisions are always what is the best thing for everyone, all the while working for the super rich.

dang

I agree. This nonsense of suggesting the yield curve is predicting something (recession due to inversion) is nonsense.

The Fed makes the curve look just the way they want it too look…..due to the fact that they have, in the past 14 years, become VERY involved in the long end. (MBSs)

The cable show talking heads refuse to acknowledge this.

What would it take for this party to come to a very quick end?

The escalation of geopolitical conflict would do it. At some point based upon the headlines I read, fear may overwhelm the average american to the extent that they cut back on spending and focus more on saving/preparing for an unknown future.

I’m well beyond that point.

The question too ask is are the 75 pct of people that work for a living getting more of the pie. The spending measurements are indicating that finally, people have a couple of bucks for the family, that they are going too spend. The secret of the American economy.

Management has stolen the productivity gains from labor for the past 60 or 70 years.

How much of the productivity gains are from the laborer and how much from the improvement in tools used by the laborer? Agriculture used to employ a majority of the workforce, and now it’s far more productive using a small percentage of the workforce. Are farm laborers as fast as the Flash? Or is it technology?

Maybe not as spending in wars and geopolitical crises can add new bills to spend more on domestically like the chips bill and other subsidies.

Maybe SPR refill more spending ?

Look, people are working hard, they’re working long hours, they’re putting up with a load of BS at work, in order to earn some money, and so what are they going to do with this money? They save some, and they spend the rest because life needs to be enjoyable too. You live only once (YOLO) has a lot of wisdom to it. Drudgery and misery need to be counterbalanced. People are doing that. It makes perfect sense.

Amen! Now I don’t feel so bad contributing to the drunken sailor party by going out to eat with my family two nights in the last week. We paid cash, from our drunken sailor fund :)

“Look, people are working hard, they’re working long hours”

I don’t believe the vast majority of Americans work as hard as they advertise. I could throw out all kinds of anecdotes. Instead, I’ll just point out traffic peaks. The worst jams in San Diego seem to be around 8:30am and 4:30pm. If people really working long hours, peaks would be at 7am and 7pm. Nah!

I work 60+ hours a week doing food service trucking, aka hand unloading a full tractor trailer every night working 12-14 hours a day.

It’s incredibly hard to live such a work centric life and not waste money on dumb stuff. I’ll slip up here and there for sure. Not as bad as most people. Most guys at my job drive nice new insanely costly vehicles and burn a lot of money on toy payments.

Not even being all, “Keeping up with the Jones’s” just the misery of working so many hours sucks the life out of you. It’s kind of nice to waste 200 dollars on some Amazon crap to open up when you get home or drive 30 minutes to town to buy “cheap” fast food just to get out of the house for a reason other than work.

Gattopardo,

The people that get to work at 6:30 am to beat rush hour leave work at 4:30 pm, and the and the people that get to work at 9 am leave work at 7 pm? Rush hour is a multi-hour process. You need to look past the peak.

And you totally ignore the people that work from home. I’m still working, and it’s 10:30 pm here.

It has always been like that. That is when school in and school out, and non-worker (retirees, stay at home parents, etc.) traffic intersects with normal business traffic.

On top of volume, because they are typically shorter than trips than commutes, people aren’t driving like lockstep speed demons. It all adds up to very tedious travel if you are trying to go any great distance.

Or you could move to Atlanta where it is rush hour from 4am to 10pm. Unless it’s a weekday. Then it’s always rush hour except for the blissful lull between 2:30am and 3am…. Monday morning.

I was in Costco yesterday and it was full!

I spent $40.

Most were spending $300-$500 id guess.

Oh and I guess I was wrong about things coming down.

I didn’t know that you can only spend $40 at COSTCO. I’m surprised they let you leave.

HowNow

Funny you should say that. I went in for one small (in price) item not too long ago, and one of the checkers was teasing me that you can’t just buy one item in Costco.

Sufferin’ bought a pizza.

“…Look, people are working hard, they’re working long hours, they’re putting up with a load of BS at work…”

Nah, they’re faking it with 2 full time WFH jobs, ripping off employers, while they’re out mountain biking, etc. instead of “pretending to work.” Too much liquidity in the system from grotesque money-printing led to companies playing fast and loose with salaries and positions, with zero oversight. It’s the biggest economic bubble in history, and Powell refuses to stop it.

I thought YOU were working hard. I’m working hard too. So that makes two already, and there are others.

I disagree. About half my team works from home. It is easy to measure their productivity, and if they get their projects done on time, I couldn’t care less that they walk the dog at 2 PM or go for a motorcycle ride on one of the last warm fall days. They appreciate the flexibility, which keeps them productive. Not everyone acts like a child when given the flexibility to do so. I fear the opposite, that work/life balance is thrown out of whack and they get burned out from it.

I concur. I work for an MLB team and can see the parking lot from my office. it’s amazing how many cars with local license plates fill up that parking lot in the middle of the week, at the middle of the day. There is no rush hour anymore as the freeways are always packed unless very early in the morning or late at night. I know of 5 people I worked with personally who refused to do their jobs because they knew the company wouldn’t fire them. So that department had to contract out freelancers to do their jobs for them. I guess the company wasn’t going to risk letting go of that PPP “loan” no mater what. I also heard around the office that these guys were ‘working’ other jobs from home in the same field. Not all of us were so lucky. Some of us were needed to show up to the office everyday, including during portions of the lockdown period. Sad.

My comment above was to Depth Charge. Still getting used to the site’s layout.

I did the whole work at home thing.

In my particular case it was less productive. A lot less productive.

I make the company 3 times as much money being in the office.

So that’s one example.

Alot of people that push the narrative of WFH is a scam are also the same people who are in CRE, are losing their shirt because of WFH, or who have a bunch of money tied up in REITs.

I know people that love working in an office and love WFH. There’s no reason to bash one or the other at this point. Plenty of jobs for both crowds.

I AM working hard, Wolf, but I’m not participating in this gluttonous spending nor was I a recipient of any of the largesse. I just got stuck with the higher prices on life’s necessities. The whole situation blows.

It is my belief that most of the spending that is driving the inflation is from the asset holders and fake WFHers (the latter who are a byproduct of corporations sitting on too much cheap money with nowhere to throw it).

Even despite this, I have a feeling come Nov 2nd FOMC, we will get to hear the rate will stay the same and we are data-dependent speech all over again from Pow Pow…while that 2% target becomes more and more elusive…

Great job Pow Pow :)

There is no doubt that rate hike won’t happen.

Would not be surprised if you’re correct (while quietly hoping you’re not).

FOMC guys are smart, probably smart enough to know what happens when the 10 year gets to 5%. That giant sucking sound? That’s not just money moving from assets to treasuries, nothing to see here

edit – “not just my money moving…”

Data dependent is a phrase created for obvuscation.

The only data these assholes seem to be focused on, is maintaining the asset valuations the American aristocracy have the Fed provided liquidity sufficient too suspend the decline in price, from happening.

Yes, I’ll watch as they proclaim that inflation has been tamed, while the data indicate something completely different.

They should raise the FFR by 0.25 pct at the November gathering of the FOMC.

“Eat, drink and be merry, for tomorrow we may die.” I wonder if it has come to that for a lot of people. As for short term interest rates, higher for longer.

I am sensing this attitude among my peers.

It has come to that with the baby boomers. The birth rate peaked in 1955. Those boomers had their 50th high school class reunions this year. Those with money are spending it like sailors drinking in any port they can find. In 10 more years nearly half will be dead or too ill to do much travel or anything else. Spend it if you have it. YOLO and time is running out to enjoy it.

The Me generation spending on themselves until the bitter end.

Moron who said that. Retail sales are HUGELY seasonal. So:

1. The average drop over the past 11 years was 5.9%! This year, it was only 5.4%! Did that moron you cite forget to point that out?

2. The 2022 drop (-5.4%) = 2023 drop (-5.4%). Did that moron you cite forget to point that out? Or did they have to go to the third decimal to come up with a rounding error?

3. 2020 was special because of stimulus checks and coming-out of lockdown. 2021 was special because of stimulus checks. LOOK AT THE CHARTS — how distorted they were during those years. Only a moron doesn’t know this.

4. Aug-to-Sep drops:

2013: -8.9%

2014: -6.6%

2015: -5.5%

2016: -4.9%

2017: -4.2%

2018: -8.4% second to last normal year

2019: -9.0% last normal year

2020: -2.7% coming out of lockdown with stimulus checks

2021: -3.9% Stimulus check boom-spike year

2022: -5.4%

2023: -5.4%

The internet is full of bullshit. Don’t spread it here. If you cite a moron’s BS, you become the moron.

At least with WFH I won’t be dying at my desk in a cubical in an office building.

Just a note on RTW….check out State Street Bank New office building in Boston. OMG….amazing, beautiful, many amenities, NO CUBICLES, well planned work space. This is how it should be working in an office!!!! More like Club Med!. It would certainly make it pleasurable coming to the office.

10’s of thousands living in tents proclaiming this.

NYT has a story about a few people living in their cars. And apparently there is a waiting list for the Safe designated parking lots for them to sleep in.

Oh and the lady makes 75k a year. Great job america!

First heard of “safe parking lots” for women in Seattle back in 2015 or so. I’d like to see the FED board face capital punishment for what they have done. QE is a crime against humanity. Love to see Greenspan, Powell, Bernanke and Yellen “ride the lightning.”

That’s always been the American mentality. That’s why people were crushed in the 2008 recession. They didn’t adequately prepare. They spent beyond their means and didn’t save. I was fine that time because I had a huge cushion because I’m a saver. That’s why I have a very hard time believing the numbers above, that people are both saving and spending at the same time. That’s not the norm in the US.

And I hear you can afford two wars!

Least dirty shirt, and may it always be! Crank up the printers.

Prob can’t afford not to fight those wars actually.

You’re not fighting them, you’re just paying for them.

Unadjusted yoy looks materially different..

Moron blogger who said that. Retail sales are HUGELY seasonal. So:

1. The average drop over the past 11 years was 5.9%! This year, it was only 5.4%! Did that moron you cite forget to point that out?

2. The 2022 drop (-5.4%) = 2023 drop (-5.4%). Did that moron you cite forget to point that out? Or did they have to go to the third decimal to come up with a rounding error?

3. 2020 was special because of stimulus checks and coming-out of lockdown. 2021 was special because of stimulus checks. LOOK AT THE CHARTS — how distorted they were during those years. Only a moron doesn’t know this.

4. Aug-to-Sep drops:

2013: -8.9%

2014: -6.6%

2015: -5.5%

2016: -4.9%

2017: -4.2%

2018: -8.4% second to last normal year

2019: -9.0% last normal year

2020: -2.7% coming out of lockdown with stimulus checks

2021: -3.9% Stimulus check boom-spike year

2022: -5.4%

2023: -5.4%

The internet is full of bullshit. Don’t spread it here. If you cite a moron’s BS, you become the moron.

Fed is as clueless as when they were buying MBS in the billions last March with house prices recording 20% increases.

If they arent clueless, then they are downright criminal.

Interest rates should be 7% right now as inflation is destroying the working people and is re-accelerating.

Our restaurant menu increased all prices by 30% this year (this on top of another 30% increase last year) and its still booked in full, cant find people to work, quality of service worse than before yet people are paying top dollar plus included 25% tip no matter what , absolutely insane the amount of money in out there.

FED has never been clueless. They did what they did had good reasons.

Don’t go by the explicit mandate of FED.

“They did what they had to”.

For whom? The top 10% of asset holders? They certainly didn’t do the bottom 70% any favors.

They’re not clueless. They are the other thing you mentioned. They are also above the law, including the law of economics.

“on a non-seasonally-adjusted basis, retail sales actually crashed 5.4% MoM in September – that is the biggest drop for September since 2019…”

Something is funny about the monkey.

Moron blogger who said that. Retail sales are HUGELY seasonal. So:

1. The average drop over the past 11 years was 5.9%! This year, it was only 5.4%! Did that moron you cite forget to point that out?

2. The 2022 drop (-5.4%) = 2023 drop (-5.4%). Did that moron you cite forget to point that out? Or did they have to go to the third decimal to come up with a rounding error?

3. 2020 was special because of stimulus checks and coming-out of lockdown. 2021 was special because of stimulus checks. LOOK AT THE CHARTS — how distorted they were during those years. Only a moron doesn’t know this.

4. Aug-to-Sep drops:

2013: -8.9%

2014: -6.6%

2015: -5.5%

2016: -4.9%

2017: -4.2%

2018: -8.4% second to last normal year

2019: -9.0% last normal year

2020: -2.7% coming out of lockdown with stimulus checks

2021: -3.9% Stimulus check boom-spike year

2022: -5.4%

2023: -5.4%

The internet is full of BS. Don’t spread it here.

This is getting more ridiculous day by day. 10 year yield is pushing 5, has been for a while now. Full 155 bps more since lowest point of the year in April. But Stocks down single digit from ATH. Junk bond spreads, corporate credit spreads still very tight. I mean cmon. Break something already and give me some closure. I simply cannot abandon all rational thinking and economic theories and jump in here. And I am tired of staying out.

I mean.. Money MKT is above 5%. What’s the downside of staying out?

And btw, there’s plenty of firepower in the backend. You are not the only one “staying out”.

A lot of people don’t realize how much wealth is sitting on the sidelines.

I’d love to see if there’s a way to put data around it. Understand how much hard cash is sitting un-invested, only then there could be a real understanding of the problem.

The biggest inflation happened in the amount of cash that people don’t even need to invest and everyday the interest it earns goes up. What folly! :)

It doesn’t boggle me that housing supply is constrained – what boggles me is that there are people getting into 7 – 10K$ / mo mortgage payments. Even with the supply constraints, prices should have come down a bit. But no, too much firepower with plenty of people from years of asset inflation that never shows up in any of the Govt Inflation trackers.

“A lot of people don’t realize how much wealth is sitting on the sidelines.

I’d love to see if there’s a way to put data around it. Understand how much hard cash is sitting un-invested, only then there could be a real understanding of the problem.”

Cash on the sidelines is a fundamental misconception that I believe Wolf has addressed. Cash sitting uninvested will always be cash sitting uninvested. Cash can’t change form, it can only change hands. Therefore, when someone takes their uninvested cash to buy stock, someone else takes the cash in exchange for their shares. Any cash entering the market immediately leaves the market, except in the limited cases of an IPO or secondary share issuance where the cash goes to the company for business purposes.

I’m guessing Wall St. came up with the “cash on the sidelines” phrase to take advantage of retail investors.

Here’s what Wolf had to say in 2018:

https://wolfstreet.com/2018/02/05/so-what-do-i-think-about-the-crash-in-stocks/#comment-122824

It differs from my conception in that Wolf says their are investors with cash waiting to deploy it, which can provide market liquidity in the event of a sell-off. I just wasn’t sure if my memory was correct, and it wasn’t.

Wolf’s comment makes sense to me. However, that source of liquidity could dry up in a prolonged sell-off as those investors deploy their cash, even as the total amount of cash held in aggregate remains the same.

I think we are talking about different things. you are referring to money supply / quantity.

I’m talking about “value”: money moving through the system and as it does it ascribes value to whats bought. My intuition is: there’s plenty of money that can be put in circulation. Hence, plenty of bandwidth to keep “values” elevated.

How is bond issuance different from IPO? It’s giving money to a company/govt which it will use to pay forward others. I don’t understand how even in the case of IPO money changed forms.

I believe we are in a positive feedback loop. The money is circulating without much constraint. And if demand does slow, there are others willing to pick-up slack.

Inflation can slow either due to rise in unemployment – demand craters. Or supply overcomes demand.

I have a further comment awaiting moderation which may provide some clarification. If I understand you correctly here, what you’re saying seems to align with what Wolf discusses in the link in that comment.

I’ll add that cash never changes form. However, when stock is traded in the secondary market cash merely goes from one investor to another. In the case of an IPO or bond issuance, cash goes to the business or borrower presumably to be used in the economy in some form. In one case the cash is still on the “sidelines,” in the other case the cash can be used for business of governmental purposes.

““A lot of people don’t realize how much wealth is sitting on the sidelines.”

That money has been borrowed by the Federal Govt. (Treasury sales)

The leviathan is pulling money from the private sector to the use of the government.

What’s not to like, from a savers POV. Now the next generation have been bludgeoned by the last generations tactics.

Since I’m about to die, I don’t really care about the future of the World.

Unfortunately, it has come to this. The “F you, I got mine” attitude among the older asset holders has destroyed the future for the vast majority of people under 30yo who just want a decent, not even great, place to live comfortably. The problem is that there are too many people who own five+ houses, and not enough people who own one, all due to horribly conceived investor tax breaks and regulations surrounding housing.

I don’t think the fundamental issue around housing is more than 1 house. That accounts for about 5% of housing stock. Obviously now the issue is finding a house and being able to afford the mortgage. Admittedly I do agree much of the culture is absorbed in the me and mine versus health of society but that is hardly new

Hmm.. there are 144 million homes (housing units to be more precise) in the United States, and 42 million of those are rental homes. Sounds like more than 5%.

No one in previous generations said that. Quit reading propaganda. None of us wanted this. I myself hate QE and ZIRP and the federal reserve, never wanted it and loathe it. We couldn’t do anything more about it than your generation is doing anything about it. Not us commoners anyhow didn’t think that. Maybe the 1%ers did, but that is not reflective of an entire generation so quit with that crap.

FOMO the sh!t out of it. Go all in. Once you’re back here broke and crying – assuming you’d even show your face – we’ll know we’re finally getting somewhere. There’s too much money out there sloshing around, including yours. We need you broke as a joke to finally get back to sanity.

“FOMO the sh!t out of it.”

All those folks who rushed to FL now getting whacked by outrageous home insurance. Many are forgoing that insurance.

Now imagine being in a community that is hit by a storm. You’re covered but half your neighbors are not. They toss the keys in the mailbox and walk. What then of your real estate values?

If they own the property outright, the city/county won’t let them “toss the keys in the mailbox and walk”. They, as owners, will likely have to pay to have the house razed, the pool pulled out, and the land flattened. If someone gets injured on an abandoned property, they will likely sue you back to your diapers.

You’re delusional.

If it’s a purchase mortgage, they might be able to send jingle mail. If they refied or took a HELOC, no such luck. The bank has recourse, can sue, and attach anything you think you own. If they have a mortgage, and have no insurance, they’re in violation of the mortgage agreement and have zero protection.

This. I have to wonder how much cash is sitting on the sidelines with this sentiment. Apparently not enough, as equities suggest. What would happen if the bears capitulate at this point? Is that even possible? Investors know that the Fed will save them, no matter what. There is no perceived risk in the market.

I don’t want things to “break” financially and as Wolf says things have broken with raging inflation don’t forget that glaring fact which will drive your behaviors . We need a consumer strike and we don’t have one . That’s what I see no strike by consumer .

“Our Drunken Sailors Now Guzzling Directly from Punch Bowl”

If you think they are on binge now, wait till the christmas shoping starts!!!

You may have to come up with a new term, as Todays drunken sailers, compared to those later this year, may look like sober sailers!!!

I think many people genuinely don’t realise how much more they’re spending. Autopay, contactless, Venmo etc…it’s all become very disconnected and abstract.

The savings rate would give a good contrast on this.

I think people know, not in the way an accountant knows but intuitively they realize they’re paying more for things than before, I mean everyone has recurring payments of some sort and we all notice paying more. If people are getting those raises though they just adjust and keep moving forward. In the end we’re all aware if our savings/debts change dramatically.

It’s an election year coming up. Congress

will keep spending and the Fed will stay

put. The top 50% will keep partying but the bottom 50% will get the bill.

The bottom 50% pay nothing in taxes.

More like the top 5% will keep partying (most of their taxes are 15% capital gains taxes), the bottom 50% will keep partying, and the middle 45% will get WRECKED.

“the middle 45% will get WRECKED”

How so? They going to magically pay more tax or something? Let me guess, you are in the middle…everyone always thinks their bracket gets screwed.

Yeah I get it. 5 percent is fine but I personally prefer more active management and better returns.

For money sitting on sidelines I would look at Fred money market funds charts. Those do indicate trillions of dollars sitting out however not everything there is sideline cash. I would take the difference between today and pre pandemic.

Checkable deposits:

https://fred.stlouisfed.org/graph/?id=BOGZ1FL193020005Q,

Money is never siting on sidelines . When a stock trades there is a buyer and a seller cash in cash out . QE money creation that’s what drives some of increases. The other is stock buybacks as that equity is removed from the system as well . Similar to QT but has opposite effect .

I’m one of those “drunkin’ sailors”, me and another several million recently-retired boomers squandering our savings on vacations and stuff. Let’s give credit where credit is due!

By all accounts, consumers have lots of cash burning a hole in their collective pockets.

Its almost as if they have enough to afford rent increases without suddenly finding themselves in abject poverty.

They’ll be fine, as long as they don’t FOMO out and decide to buy a home that appreciated 200-300% the past decade. In that case, they’ll be personally picking up the tab for somebody else’s retirement.

Moron who said that. Retail sales are HUGELY seasonal. So:

1. The average drop over those 11 years was 5.9%! This year, it was only 5.4%! Did that moron you cite forget to point that out?

2. The 2022 drop (-5.4%) = 2023 drop (-5.4%). Did that moron you cite forget to point that out? Or did they have to go to the third decimal to come up with a rounding error?

3. 2020 was special because of stimulus checks and coming-out of lockdown. 2021 was special because of stimulus checks. LOOK AT THE CHARTS — how distorted they were during those years. Only a moron doesn’t know this.

4. Aug-to-Sep drops:

2013: -8.9%

2014: -6.6%

2015: -5.5%

2016: -4.9%

2017: -4.2%

2018: -8.4% second to last normal year

2019: -9.0% last normal year

2020: -2.7% coming out of lockdown spending with stimulus checks

2021: -3.9% Stimulus boom-spike year

2022: -5.4%

2023: -5.4%

The internet is full of bullshit. Don’t spread it here.

Seriously, you Doom Scrollers really need to go out and have a beer or two. Buy the happy hour specials. Have some laughs. Then, you can go back with your bugout bag waiting for the end of times. I know, you all are waiting for the “I TOLD you so!” moment. Egg on my face, got it.

Where did you get the facts and numbers for your post?

🤣❤

Inflation won’t stop until people stop spending so no where close to done with. Simple as that

Wolf, thanks for the updates and your analysis. You mention “Disposable income jumped by 7.3% year-over-year”. Was this number from the retail sales data just released? The BEA data show disposable personal income rising 3.7% in Aug. Thanks ..

All data here is in current dollars, so compare current-dollar disposable income (+7.3%) to current-dollar retail sales (+3.8%). You’re citing inflation-adjusted (“real”) disposable income in 2017 dollars, which is not comparable to current-dollar retail spending.

Wolf,

Do you think there is any way to get to 2% inflation without a recession?

I’ve a similar question: it’s been suggested here that inflation will come under control through the rise in unemployment that the rising interest rates finally create. That, that will be the first real sign of recession.

Can inflation be tamed through supply side glut? Can we overproduce our way to 2%? When I look at Tesla / EV sales, I feel like that exactly what happened.

“Do you think there is any way to get to 2% inflation without a recession?”

The answer is NO

2% inflation is NOT a victory.

We have had 2.5 years of inflation. IF the goal is 2%, then prices 5% higher than 2.5 years ago would be the norm.

But they are 17% (or more higher) than when this inflation started.

So there is an excess of AT LEAST 12% of “unwanted” inflation baked in even if the rate returns to 2%.

YOY comparisons are designed to hide that fact. Let’s measure from when this debacle began…2021

If there’s one thing I’ve learned from this site it’s never to underestimate the American consumer. Flush with cash and ready to spend, no recession in sight.

Contrary to that point though is many commodity prices (food/metals) have softened substantially from the recent all time highs, which does make me wonder if there could be a slowdown closer around the corner than people think.

The data drop today had me playing around on the census.gov site, looking at poverty statistics for major cities. It’s worse out there for more families than meets the eye, 16-18% of households in New York, Chicago, LA, are below the poverty threshold (at least, by 2021 definition). I think that’s the rub here, there’s no small percentage of people drifting along that $30k household income line that are one job loss away from real catastrophe and extreme poverty. And those minimum wage type jobs sadly are the first who will be canned if Powell gets the labor market softening he openly pines for. So I think these numbers show that plane is still humming along for now (i mean, people do need their “stuff”), but I also suspect there is turbulence buildimg beneath the wings. The bottom falling out is more than enough to send GDP figures into a technical recession, and the costs to bring the bottom 20% back from that type of situation would be immense. There is a lot of fear at the fed for both overshooting and undershooting that 2% target. So much of their rhetoric seems to wish the 2% into existence. Positive spending numbers like this might feel better than the alternative, but the spector of inflation and all of the agnst and pain it causes is the giant elephant that just won’t leave the federal reserve building. And the current plan Powell is proposing is to make the poor and middle class lose their jobs. The plane is lost somewhere in the Bermuda triangle.

There are no tools anymore that the Federal Reserve has to cool off an overheated economy. Tools: First the Federal Reserve has Quantitative Easing (QE) stimulus. Second the Federal Reserve can raise interest rates, but with a large unrealized underwater balance sheet it is like putting a foot simultaneously on the brake and gas. Since the interest the Federal Reserve receives on its balance sheet is less than it pays out in interest, it has to print the difference with the effect of a stealth stimulus. We can only pray that the German economy engine of Europe goes stone cold and drops demand for our exports to the European Union. The Smoot – Hawley tariff act of the 1930s cooled of our overheated economy, maybe similar Geopolitical effects, although a different cause, can do the same.

Bond yields are set by the market and higher bond yield basically implies higher inflation in the long run. I bet bond yields will keep rising because Fed’s true goal is to create more inflation so debt can be watered down, and the world is waking up to this reality . Asset holders will prosper as always and holders of USD bonds and USD debt will be screwed as always. I just feel bad for the savers in the US and around the world. Yields on paper will never keep up with inflation, when printing press is running at full speed. So all holders of USD paper are being screwed, willingly, which is ironic.

Their true intent is always to look out for an excuse to create more inflation under the guise of maintaining price stability to fool the sheeps. Pandemic gave them a perfect one and now wars will be another grand opportunity. Its coming. It’s all planned.

These two statements of yours are mutually exclusive — seems you don’t understand the concept of “yield”:

1. “I bet bond yields will keep rising because …”

2. “Asset holders will prosper as always….”

Higher yields mean lower asset prices by definition, such as dividend stocks, CRE including rentals, housing in general, anything operating on leverage (including stocks, housing, etc.), bonds that were bought at the low yields before rates rose, etc.

So this phase needs to be corrected: “holders of USD bonds and USD debt will be screwed as always” to “holders of USD bonds who’d bought before rates went up will be screwed…” Timing is everything. Buy at the wrong time, you lose. Buy at the right time, you win.

The Fed is losing credibility. Inflation is now not only entrenched, but rising. The Fed timidly sits on its hands while long bond yields rise. The entrenched core CPI will pull overall CPI higher going forward. Wages will be pressured even higher, as rents are due for another leg up after this data release emboldens landlords.

You got your FED pauses, Wolf, are you enjoying them?

Yes, I sort of am. This is kind of a normal economy, 5.5% short-term rates, 8% mortgage rates, decent demand by consumers, dropping asset prices without chaos… I like for things to not blow up only to then trigger more Fed QE and 0%. I hate QE and 0%. I’m fine with this.

Is this just the (post-pandemic) Roaring Twenties redux?

I agree with your conclusions Wolf. I am a curb shopper, trash picker, call me what you want, I run a small route twice a week and can quite accurately predict retail sales based on boxes on the curb. It’s true that “retail” is down based on the dearth of empty boxes over the last 6-8 weeks or so but according to you the real retail numbers are hidden in services. I can also get a feel for evictions and “midnight moves” where properties are just abandoned and cleared out. I also get insights about re-modeling, furniture and appliance sales, etc.

This week I’m particularly interested in how Amazon’s “Prime Big Deal Days” went. I’ll know more tomorrow and may report back, so far I’m not seeing any indications that they blew the doors off but it takes a week or two to get a good read on that as old stuff hits the curb along with new boxes. I did see a big uptick in TVs recently but that is typical of the football season starting.

Interesting. I hope you do report back.

It’s still crazy to think that 3/4 of the country can’t afford a new car or a home due to inflation and interest rates.

People are spending money here in rural Red America. Locally, owner-financed custom home construction permits are only 10% off the 2022 peak, which puts the local building industry in a more manageable position. Framing for my home starts next week, and I was pleasantly surprised with the price of the lumber package.

As a small debt-free chemical manufacturer, the first half of this year was good without any complaints. The second half of this year took off like a rocket, and I can’t put my finger on it. We barely advertise and don’t have outside salespeople, so that isn’t it.

I don’t foresee a price increase in 2024. Our last price increase was Sept 2022.

“rural Red America”

I would suggest it is they who tend to save and may be spending some of the “fair return” on their savings.

People getting a fair return on their dollar holdings IS INDEED an economic engine.

Its not that crazy that 3/4ths can’t afford a new car. Buying vehicles new is a luxury for the rich.

I’ve bought all my cars used because I don’t consider myself wealthy enough to buy new. I’m fine with this. Currently driving a 2011 with 160k+ miles and no plans to replace it.

Be interested in how all of this impacts state and local governments who don’t get to deficit spend. I know in my state, CA, they are working on getting a balanced budget, this combined with underfunded pension funds with huge parts of the state work force retiring. They arent issuing bonds yet to service debt, versus infrastructure for example, but they aren’t far away either. Happy to be getting into more treasuries as they can’t get that piece of pie unless you do bond funds where they have special laws for that.

These are NOMINAL sales gains, not INFLATION adjusted. WTFU.

RTGDFA.

If you let in millions of illegals, don’t be shocked when they buy food, necessities, and cars.