This was the last of 12 health-insurance adjustments that pushed down core CPI and core services CPI; it will swing the other way next month.

By Wolf Richter for WOLF STREET.

The Consumer Price Index (CPI) jumped by 0.40% in September from August, despite the still ongoing ridiculous monthly adjustments to the health insurance CPI that caused it to collapse by 37.3% year-over-year. Today’s CPI release is the last month with that adjustment; with the October CPI, to be released next month, the health insurance CPI will flip, adding further upward momentum to the CPI readings, instead of pushing them down.

The health insurance adjustment has caused CPI, core CPI, and core services CPI to be understated to an increasingly significant extent since October 2022, when the monthly health insurance adjustment started, one of the biggest data distortions resulting from the data chaos of the pandemic (more in a moment).

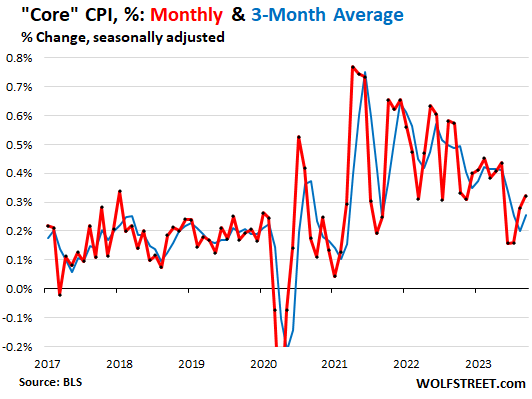

Core CPI, month-to-month accelerated to 0.32% in September from August even though it was held down by the collapse of the health insurance CPI:

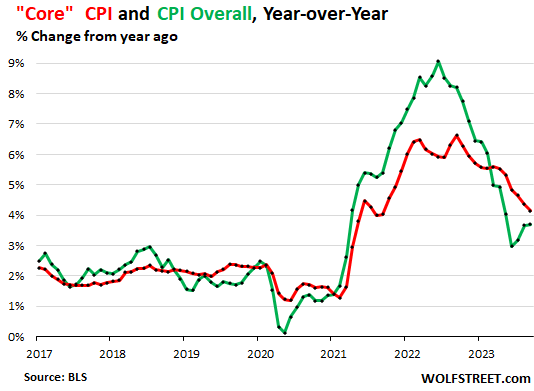

The year-over-year CPI accelerated to 3.70%, the third year-over-year acceleration in a row, after it had accelerated to 3.67% in August, and to 3.18% in July, from 2.97% in June, according to the Bureau of Labor Statistics today (green in the chart below).

The year-over-year “Core” CPI, which is designed to track underlying inflation by excluding the volatile food and energy products, rose by 4.1% year-over-year in September, seriously dragged down by the 37% year-over-year plunge in the health insurance CPI due to the odious adjustments that finally ended with September.

Fuel prices are rising.

After a steep hard plunge in energy prices in the second half last year, the process reversed this year, and in September overall energy prices rose 1.5% from August, and nearly wiped out the year-over-year plunge that had persisted since late last year.

On a month-to-month basis, gasoline prices have been surging all year – they jumped 2.1% in September from August and turned positive year-over-year (+3.0%). Gasoline accounts for about half of the total energy CPI.

Fuel prices – gasoline, diesel, jet fuel – also make their way into consumer products that are shipped by delivery van, truck, rail, or air as are nearly all consumer products. Jet fuel also makes its way into services via air fares. These products and services are included in core CPI, which is how core CPI reacts indirectly to rising energy costs.

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | 1.5% | -0.5% |

| Gasoline | 2.1% | 3.0% |

| Utility natural gas to home | -1.9% | -19.9% |

| Electricity service | 1.3% | 2.6% |

| Heating oil, propane, kerosene, firewood | 4.8% | -5.6% |

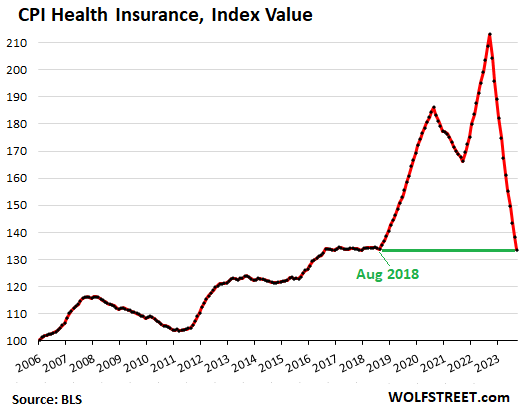

The 37% collapse of the health insurance CPI.

September (this CPI release!) was the last month of the monthly push-down adjustments to the health insurance CPI, which started with the October CPI last year. For the October CPI, to be released in November, the adjustment will swing (I discussed the gory details here).

The adjustment pushed down the health insurance CPI every month on a month-to-month basis by 3.4%-4.3%, which has now caused the year-to-year health insurance CPI to collapse by 37.3%, despite widespread and big price increases of health insurance.

A 4% month-to-month plunge, as opposed to a 1% month-to-month rise, as would be the case, represents a month-to-month swing of 5 percentage points!

The 37.3% year-over-year collapse, instead of something like a 12% increase, as would be the case, represents a swing of nearly 50 percentage points!

The more we narrow down the CPI metrics – overall CPI to core CPI to services CPI to core services CPI – the worse this adjustment distorts the narrowed-down figures.

The health insurance CPI as a price index itself (not percent change) in September collapsed to the price level of August 2018, despite big health insurance increases since then. This adjustment has understated “core CPI” and even more so “core services CPI.” Mind-bendingly nuts:

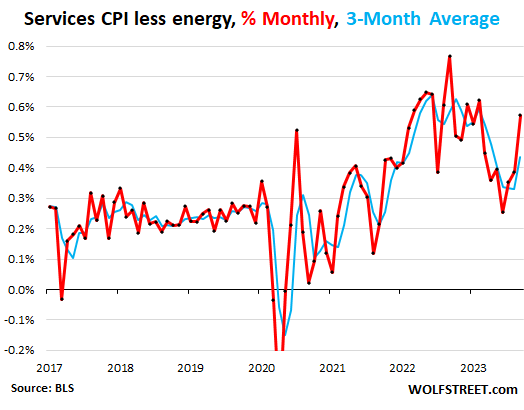

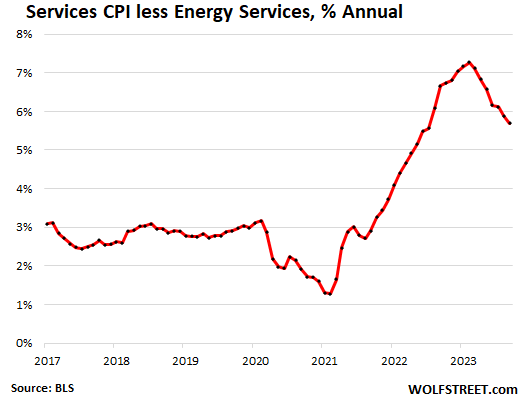

Core Services CPI spiked month-to-month, despite collapse of health insurance CPI.

The index for core services (without energy services) accelerated to 0.57% in September from August, the biggest increase since February, and the third month in a row of acceleration, despite the odious adjustment to the CPI for health insurance that weighs so heavily in this index.

Year-over-year, the core services CPI rose by a still red-hot 5.7%, despite the 37.3% collapse of the health insurance CPI within it, and also due to the base effect related to the surge of the index a year ago:

Services CPI by category.

The table shows how hot many price increases in services are. The table is sorted by weight of each service category in the overall CPI. The CPI for medical services is the third largest item, with a weight of 6.3% in overall CPI, and over 10% in the services CPI, and it has been repressed by the collapse of the health insurance CPI within it, and turned negative year-over-year (-2.6%):

| Major Services without Energy | Weight in CPI | MoM | YoY |

| Services without Energy | 61.3% | 0.6% | 5.7% |

| Owner’s equivalent of rent | 25.6% | 0.6% | 7.1% |

| Rent of primary residence | 7.6% | 0.5% | 7.4% |

| Medical care services & insurance | 6.3% | 0.3% | -2.6% |

| Education and communication services | 4.8% | 0.1% | 2.5% |

| Food services (food away from home) | 4.8% | 0.4% | 6.0% |

| Recreation services, admission, movies, concerts, sports events | 2.2% | 0.3% | 0.2% |

| Motor vehicle insurance | 2.7% | 1.3% | 18.9% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.5% | 0.6% | 6.8% |

| Motor vehicle maintenance & repair | 1.0% | 0.2% | 10.2% |

| Hotels, motels, etc. | 1.1% | 4.2% | 8.0% |

| Water, sewer, trash collection services | 1.1% | 0.2% | 5.2% |

| Video and audio services, cable | 1.0% | 0.2% | 6.3% |

| Airline fares | 0.5% | 0.3% | -13.4% |

| Pet services, including veterinary | 0.6% | 0.0% | 7.0% |

| Tenants’ & Household insurance | 0.4% | 0.9% | 2.8% |

| Car and truck rental | 0.1% | 0.0% | -8.6% |

| Postage & delivery services | 0.1% | 0.5% | 4.6% |

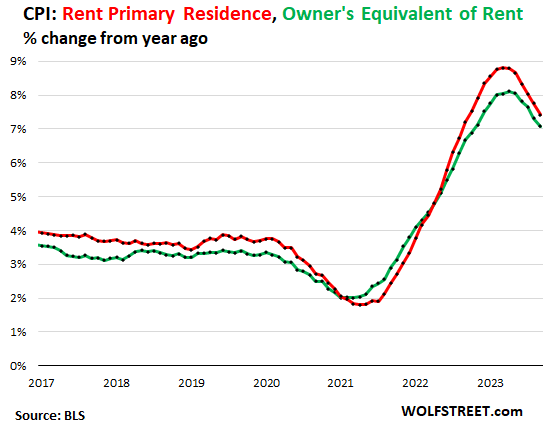

The two CPIs for housing as a service (“shelter”).

“Rent of primary residence” accelerated to +0.49% for September (6.0% annualized), matching May, and both were the highest since June. There has been no slowdown at all since June, which disappoints a lot of folks, including Powell, who’d said for well over a year that rents were lagging, and that we’d soon see this slowdown back to normal levels any moment now.

What did happen was a slowdown from the 8% year-over-year range to the 6% range, and it has gotten stuck at the 6% range over the past five months.

Year-over-year, the CPI for rent increased by 7.4% (red in the chart below).

The survey follows the same large group of rental houses and apartments over time and tracks what tenants, who come and go, are actually paying in these units.

Owners’ equivalent of rent accelerated sharply to 0.56% in September from for August (6.9% annual rate), the biggest increase since February, and there has been no improvement since February.

Year-over-year, the OER index increased by 7.1% (green). This is based on what a large group of homeowners estimates their home would rent for:

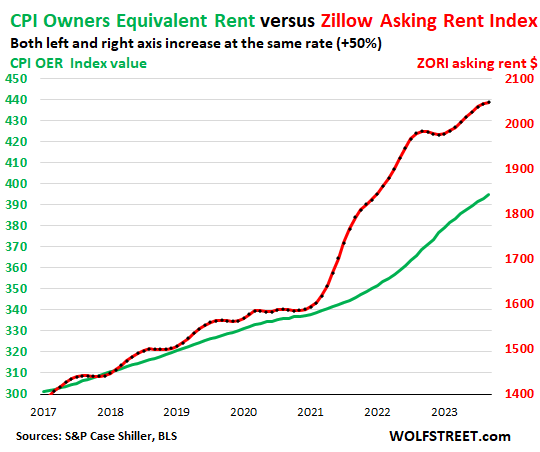

“Asking rents…” The Zillow Observed Rent Index (ZORI) and other private-sector rent indices track “asking rents,” which are advertised rents of vacant units on the market. Because rentals don’t turn over that much, the ZORI’s spike in 2021 through mid-2022 never fully made it into the CPI indices, as not many people actually ended up paying those spiking asking rents.

In late 2022, asking rents in dollar-terms began to dip, but then began to rise again this year, and started hitting new records in dollar-terms.

Asking rents are very seasonal, though actual rents don’t show much seasonality. This time of the year is normally the slowest time for asking rents. In a number of Septembers before the pandemic, the ZORI showed actual declines from the prior month. This September, the ZORI rose 0.2%.

The chart shows the OER (green, left scale) as index values, not percent change; and the ZORI (red, right scale). The left and right axes are set so that they increase each by 50%, with the ZORI up by 47.7% since the beginning of 2017 and the OER up by 31.2%:

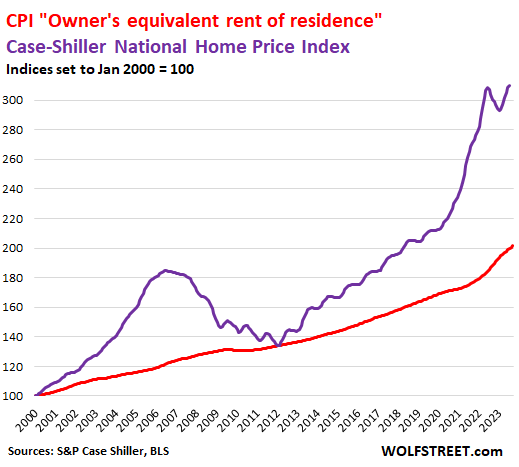

Rent inflation vs. home-price inflation: The red line represents the OER. The purple line represents the Case-Shiller Home Price Index. The CS index lags about three months. Both lines are index values set to 100 for January 2000:

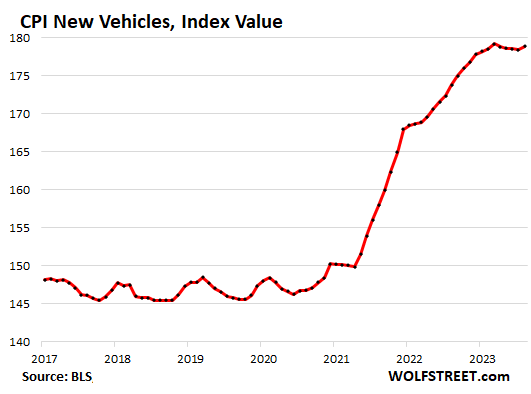

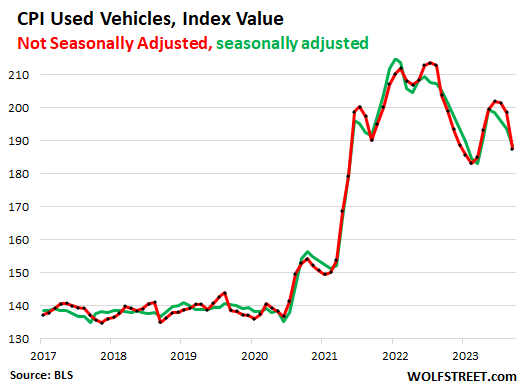

Durable goods prices drift lower from nosebleed levels.

The CPI for durable goods, after blowing to astronomical zone, has been meandering lower:

| Durable goods by category | MoM | YoY |

| Durable goods overall | -0.4% | -2.2% |

| New vehicles | 0.3% | 2.5% |

| Used vehicles | -2.5% | -8.0% |

| Information technology (computers, smartphones, etc.) | 0.3% | -7.9% |

| Sporting goods (bicycles, equipment, etc.) | 0.0% | -0.1% |

| Household furnishings (furniture, appliances, floor coverings, tools) | -0.3% | 0.9% |

New vehicles CPI rose for the second month in a row in September from August (+0.4%), and the index value set a new all-time high and was up 2.2% year-over-year.

For many years before the pandemic, the new vehicle CPI was essentially flat with some ups and downs, despite large increases of actual vehicle prices. This is the effect of “hedonic quality adjustments” to the CPIs for new and used vehicles and also other products (here’s my chart and detailed explanation of hedonic quality adjustments).

Used vehicle CPI has gyrated all over the place after the historic spike in used vehicle prices that started in 2020 and peaked at the end of 2021. The used vehicle CPI fell by 2.5% seasonally adjusted in September from August, and by 8.0% year-over-year. From the peak, it has now fallen by 12%, but it’s still up by 35% from September 2019.

Note the effects of the hedonic quality adjustments in keeping prices level in the years before the pandemic even as actual used vehicle prices rose:

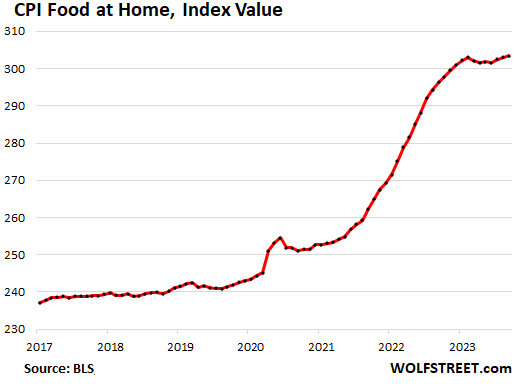

Food at home: price increases calmed down, prices remain very high.

Price increases of food bought at grocery stores and markets have calmed down but prices remain astronomically high, following the 24% spike during the pandemic.

The CPI for “food at home” rose by 0.1% month-to-month, and by 2.4% year-over-year, the least in over two years.

| Food at home by category | MoM | YoY |

| Overall Food at home | 0.1% | 2.4% |

| Cereals and cereal products | 0.2% | 3.6% |

| Beef and veal | 0.6% | 7.0% |

| Pork | 1.6% | -1.7% |

| Poultry | 0.4% | -0.4% |

| Fish and seafood | -1.2% | -1.5% |

| Eggs | 0.9% | -14.5% |

| Dairy and related products | 0.1% | -0.2% |

| Fresh fruits | -0.1% | 0.1% |

| Fresh vegetables | -0.4% | -1.2% |

| Juices and nonalcoholic drinks | -0.4% | 4.4% |

| Coffee | 0.7% | 1.6% |

| Fats and oils | -0.5% | 2.7% |

| Baby food & formula | 2.3% | 9.2% |

| Alcoholic beverages at home | 0.8% | 2.9% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just got notice yesterday that my wife’s health insurance premium is going up from $1,318.69/month to 1,603.52/month, a 21.6% increase. She has a premium plan, but still…

Your premium is more then my entire budget for a month………..

Wolf chart clearly shows that your premium today should be same as Aug 2018 as per BLS BS. So you must be lying!

Primary objective of Fed QE and slow QT is to manipulate all indicators that tell you how badly you were screwed!

And it looks like the BLS realized their mistake so are going to change their methodology so that CPI doesn’t go up next month. See Wolf’s posts below. Sick to death of our corrupt government and its manipulation. They were just fine with that methodology as long as it was lowering CPI.

Good lord. It’s modelling, not corruption!

Models are simplified approximations of a real system used for experimentation and planning. When things happen that violate the assumptions of that model, you need to change it (or create a new one).

That’s just how science (including economics) works.

Brian:

I don’t agree with you. They should have known it was wrong the entire year and did nothing about it. How convenient they are correcting it now. Good Lord, wake up!

They’re correcting it at the end of the 12-month cycle of the model. Correcting a model at the end of the cycle is classic timing.

They should have never used this model in the first place. But correcting the model adds new problems to the equation, and correcting it in mid-course adds even more problems. This is now a huge mess that cannot be fixed very easily.

I’m okay with correcting it now as long as they retroactively adjust all of the previous numbers to let everyone know what they really were.

Agreed. My BCBS premium went up 10.9% for 2024. BCBS is a NATIONAL “Health” Insurance corporation. Their premium increase is at the LOW END of most national “Health” (lol!) Insurance corporation premium increases. ANY “official” claim that DOWNWARD “Health” Insurance cost adjustments “took place” is a BOLD FACED LIE! Enjoy you HELLTH Insurance courtesy of the BLS BS.

This comment I just read basically sums up the situation:

[b]Ben Hunt @EpsilonTheory[/b]

Yes, if it weren’t for our consumption of food, housing and energy we would be experiencing ‘manageable’ inflation.

And the WH is mystified that Americans are dissatisfied with the economy and think inflation is a problem.

Krugmanize those numbers and declare Victory!

Welllllll…you all know the ole saw:

How is a drunk leaning against a lamppost like a statistician?

The lamppost is used for support rather than illumination.

Welcome to America.

ConspiracyTheory’Murica

Take your ssri pills people

Latest Marc Maron standup “Hey the Uniforms are in!”

Lol

Yeah, welcome to the show!

Seems if we all don’t have several people and institutions that are “stupider than us” to blame for the most deserving problems (again, our superior minds must also know what these problems are and in some order of importance) then we might as well watch WWE and reality shows and sitcoms, go to church, and await the rapture…..or whatever deity you follow has promised you, according to those who have been or are in contact with it.

Me? I hate not knowing enough to be able to play this popular game. (I know the get all the money one can game, most everyone agrees with the basic “get” money and stuff goal) Playing blame is difficult because since this society is either too complex or too sick (or both) for me to really hold forth, I have to mostly just mutter and watch. Fortunately the English language is flexible enough to write or speak and communicate nothing or surprise and confusion….my normal condition…..I think.

See? All insults and corrective thinking.

At least PLEASE let us know who the moron here is…..thanks.

Should say YOUR chosen one. I’ll accept that adjective full time, no problem.

Even when Wolf presents a good picture (make that best available to him) of a part of the puzzle, I’m usually baffled as to how it fits in with the rest, but after a while one gets intuitive feelings, Kida like learning chemistry. Kept learning seemingly unrelate bits and pieces for years, and ones intuition starts growing what I call shortcuts.

Have a theory of how that works in just the 6 or so layers of the cerebral cortex (grey and white matter, but many other players in there, glial cells, etc) but am way off topic….and too much coffee.

I’ve got a feeling the hard times are right

around the corner. People are beginning

to notice their lower standard of living.

lol people have been noticing for 20 years but the older generations who already owned houses and were benefiting from QE inflating their preexisting portfolios just ignored it and yelled at the kids they gave participation trophies too for somehow being responsible for the trophies existing in the first place.

Itll all trickle down though any minute

I’ve never seen such a whiny, spoiled generation as yours. Quit reading propaganda on Business Insider and read what life was like in the 1970s into the early 1980s. But you’d rather blame someone else for your own failures.

I second Fedup’s opinion.

Numbers tell a different story Fedup

58y.o. here. I have lived in my home for almost 30 years. I have been voting 3rd party for decades now. I sacrificed personal comforts and wants to ensure my daughters (31y.o. and 35y.o.) had a chance to survive in this cruel world.

Herpderp, your personal bias might be clouding your judgement.

Yeah, the 70s and early 80s were rough. But since then, it’s been smooth sailing for those lucky enough to be in the workforce after that.

I remember a very nasty double recession in the early eighties. Long lines for pitiful jobs, 15% mortgages, double digit inflation. It was all such a cakewalk. You lucky younger generations aren’t permitted a recession that would liquidate all the misallocations.

I always find generational bickering to be pretty silly. I’d say boomers, millenials (my gen), and gen z all have our faults and strengths. I think I actually tend to like gen-Xers the best… They sort of just quietly move along under the radar.

Though I think boomers really need to pay attention to 2 things before whining about millenials: First, y’all invented American youth entitlement and generational narcissism as the first true “me” generation. Second, y’all raised us this way, so maybe take a good look in the mirror before you gripe about your own kids.

You sound angry, like a loser. Maybe you should have gotten more trophies when you were a child.

60s and 70s were absolutely the best times of my life!! Young, super athletic…sex drugs R&R, etc….then I got laid off and the 80s double dip recession kept me hanging on by fingernails for 5 years till I was hired by the P/O. Vets points and a couple other lucky breaks got me in.

So then, this rich relative (had/have several) and aware of my struggles, said, “That will do for now”, and I thought “You are FN nuts, lady! I’m never leaving this place till my clock punching life is OVER”…..and I did. Then I moved off grid FT on what in 1990 was bare land and worked harder than I ever did in my life…Hd gotten used to living in dumps, and stayed in them and worked every weekend and vacation, and saved $$$, but it was all MY call, every morning, shivering or not, unless I had rain problems, ditching, road washouts, leaks, storage, oaks or limbs falling, etc,etc. Still didn’t “feel” like clock punch work.

Everyones life is different, but we are all people…..all people………….ALL people.

You are right.

The following is more truth based than snarky:

The Government will provide Seniors with a pup tent and a collapsible aluminum cooking kit, with Far Eastern recipes for dog, cat and rat.

I just just read this. I completely agree with it, along with at least 90% of the public:

Ben Hunt @EpsilonTheory

Yes, if it weren’t for our consumption of food, housing and energy we would be experiencing ‘manageable’ inflation.

And the WH is mystified that Americans are dissatisfied with the economy and think inflation is a problem.

Already did that, AG, mid 40’s and no meat, just PB out of jar with finger in back of ’72 Volvo wagon, with cement, cinder blocks, lumber, or other bldn’g mat’l as bedmates.

What do you or this “Ben” live in?

And don’t you have a piece of rope if it gets too bad?

“Creeping austerity” is what I call it.

But then we are the world’s super pigs and have been since 1776.

It’s just that some pigs are WAAAAAY fatter than the rest, and “can’t” (debatable) live any other way.

Glad I bumped along the bottom and pissed most of my youth away having fun (as some would say…but I don’t think so), so I’m a great downsizer. Yeah, I deserve what I got, and am STILL damned lucky at that!

According to Paul Krugman, the war on inflation is over and we won!

Just exclude food, energy, shelter, used cars, etc.

Hope Paul gets a second Nobel. Or third!

I was more hoping he gets a tumor.

“I was more hoping he gets a tumor.”

“Only the good die young.”

~Billy Joel

In that case Paul better hope Nobel Prizes aren’t included in CPI.

I saw that. The man should be driven off the stage for such a titanic insult to intelligence, but – whatever. Just throw it on the pile of stupid Hot Takes from talking heads.

Must be more fun commenting on article when everyone hates same guy, yes?

Good thing people don’t need food, energy, shelter, and transportation. As W said, mission accomplished

My high deductible plan premiums for 2024 will go up 18%. That’s in addition to the 6% higher deductible and max out of pocket.

I have a Plan F with MOO. They raised it over 10% (don’t remember the actual number as I shredded the notice). I called my broker and had her search for a better deal since I can pass the “health screening” questionnaire. I could have saved more money with other companies, but I just reapplied to MOO for the same Plan F – just a different insured pool. Premium is much lower (in the neighborhood of 30% lower). Might be worth a call.

Will this be for starting on the month of January 2024?

“Will this be for starting on the month of January 2024?”

Yes, for Blue Shield of CA.

Did you know that the average American mortgage is just over $2,000 for a 30 year loan.

Mind boggling how that is.

And people who bought with the 2.75-3% rates got to pocket an extra $1,000 a month over someone who either a. Did not refinance or b. Did not buy with a low low mortgage rate.

I just envision these people with a whee barrel full of cash, heading to Costco once a month. Haha

Those who did not buy when interest rates were low had 15 years to make that decision. And they had plenty of notice that rates were going to rise also.

I have as much sympathy for those crying about that now as they showed me when my first mortgage was at 13.4% and I could only get that by paying 20% down.

Which is none.

If you’re not making enough money to live the life you want that’s entirely on you.

Yeah and for people who were only 10-20 years old during that 15 years, well that just sucks for them, huh?

There are plenty of young people in their 20s who did not have 15 years decision to buy or re-finance when rates were sub 3%…

Cantillon effect worked in your favour?

I got mine, so fvck the next generation

That’s more then over spent on healthcare my entire life.

F this countries healthcare system

Sickcare system. They make more money that way

You should try a health share program. I switched over to one five years ago. Very happy with it. My monthly bill is $175 and the wife selected the more expensive one and pays $275 per month.

Have you filed a claim?

Are you really going to pay that? I would just drop it and self insure. In two years you will have 40K in the bank for emergencies. If something really bad happens you can always fly first class to Asia, South America or Europe.

We spent many years without any health insurance without any problem. We were the poorest when we had great health insurance we couldn’t afford to use, because we couldn’t afford the $1500 deductible.

Or you can buy the cheapest plan and save the rest.

Self insuring is not smart.

At most with insurance you owe the premiums and deductible. Say for instance $15,000 in premiums + $8,000 in deductible (max pay outs 8k).

With your 40k, you fall into the “uninsured” category and you pay 3x the rates an insured person pays. And sometimes you get worse medical care or are looked down on. I mean you shouldn’t be, but it happens a lot in our healthcare system.

Health Insurance is expensive, but it’s a hedge against much larger bills, like hundreds of thousands versus tens of thousands in premiums.

I pay cash for the very occasional health care services I use and get large discounts compared to what it would have cost for similar services on a claim. True I don’t pay claim costs immediately but will over time, at the rates described above.

I do carry disaster insurance tho with a high deductible to avoid bankruptcy if the odds go against me.

DISagree sufferer:::

Done with any insurance NOT mandated by Insurance Industry controlled GUVMINT long time ago, including especially ”health.”

DO your own health maintenance by staying as far from ”doctors” and ”lawyers” as possible while doing your best to eat healthy, exercise EVERY DAY, etc., etc.

So far as the information is available, and to be clear such information is usually available in the so called alternative news, especially these days, MUCH earlier than it is in what is called MSM…

Keep in mind always that the MSM is owned and operated to convince the sheeples.

Suffer,

Your max payout is more than 23K which is crazy. Don’t forget they rarely pay 100% over the deductible. You can pay for the cheapest plan you can find if you just want to get charged the “insured” rates. This would give you some protection and should be a huge savings. Otherwise, you are just blowing money because you can.

Wrong. I have insurance and the dentist is paid $275 for a regular cleaning. My GF pays $85 cash with no insurance

If you needed health care, you could fly to the UK or other socialized medicine country and walk into an ER (A&E). After being admitted and expensive surgery and/or procedures. you just take a taxi to the airport and leave. Thousands do this every year. Unethical? Who cares?

You may be in for a nasty surprise if you expect that to happen these days in the UK. Unless you are actually dying there and then your chances of expensive treatment in A and E are zero as a non national and there is a 7.5 million waiting list for elective care.

And they have tightened up massively on overseas visitors and will expect payment there and then.

“Unethical? Who cares?”

Literally or figuratively:

“Why hast thou said, “I have sinned so much,

And God in His mercy has not punished my sins”?

How many times do I smite thee, and thou knowest not!

Thou art bound in my chains from head to foot.

On thy heart is rust on rust collected

So that thou art blind to divine mysteries.

When a man is stubborn and follows evil practices,

He casts dust in the eyes of his discernment.

Old shame for sin and calling on God quit him;

Dust five layers deep settles on his mirror,

Rust spots begin to gnaw his iron,

The colour of his jewel grows less and less.

— Jalal-uddin Rumi via Aldous Huxley, The Perennial Philosophy, 1945

“Unethical? Who cares?”

Consider the intrinsic up front costs and blossoming payments.

Hey White Bob,

Dental insurance is different.

Dental insurance is like:

I pay you $500 in premiums a year.

Then you get $500 back at best during the year for seeing your dentist. Perhaps a $1000 if you need a crown. But they begrudge more than $500 usually.

Health insurance is all pre agreed contract rates. Saves the insured from having our financial azzes handed to us.

Good year and no problems you pay 10k in premiums. You save 2k in contracted doc bill rates and prescription drugs.

Bad year, you pay 10k in premiums. You get in a bad car wreck, have trauma. You need the uninsured equivalent of 300k to get thru surgeries, hospital stay, specialists, rehab. But hey contract rates knock it down to 20-30k. You just owe that plus your deductible of say $5k. You’re out max 45k, but you do not owe 300k! And you would, and they’d own your soul.

An added plus is that you get better care. Docs hate working for free.

OMG. Never do that in the US if you own anything. Each bill will be about double everyone else (no insurance discount) and they WILL go after your assets including your wages, until you file for bankrupcy. Not a smart choice.

Agree 100%

The US healthcare system is broken.

Some years ago, I spent three weeks in a German hospital for a septic infection. Two surgeries and three weeks later the infection was gone and I was billed just over $5,000 all-in. The surgeon checked on me daily. I learned that prices are capped, and the services for uninsured foreigners are capped at exactly what the German public health insurance pays.

Something similar happened to a friend who was on a trip to Italy – her son with juvenile diabetes – a week in the hospital with round-the-clock care – the staff was very apologetic when they presented her with a bill for less then $2,000.

A few years after that, I underwent an outpatient cardiac ablation in the US and was presented with a 6-figure hospital bill. Adding insult to injury, the procedure was unsuccessful. The insurance company paid their “negotiated rate” of around $30k.

Will that work when you have a heart attack?

Asking for a friend.

I just spoke to a guy yesterday about “long term care/life insurance”. I asked for a ball park quote for somebody my age (60). He said $250 – $400 per month. However, this is the 1st conversation I’ve had with somebody about life insurance so I have no way of knowing how much inflation has affected it. But, I’m sure it is a lot.

just trying to imagine how bad the CPI will get when the prop from the health insurance adjustment is removed. Ugly and getting uglier in a hurry

my experience is the opposite, I’m paying basically nothing thanks to ACA after killing fixed costs, starting with housing

In my case, getting rid of rent/mortgage actually ended up freeing me from US healthcare costs. Pretty neat as I absolutely love deflation

Whats the weight of the medical insurance in CPI? And if it had increased by say 20% instead of falling 36%, what would have been the overall impact on the Core CPI YoY? Thanks

1. What matters to the Fed is core CPI. So health insurance weighs more heavily in core CPI.

2. It’s cumulative, 12 months in a row, relentlessly. And so the distortion grows every month, reaching the peak today.

3. What matters even more for the direction of inflation is core services CPI; core services CPI is about 61% of total CPI. Health insurance CPI weighs about 1% in core services CPI.

4. As I said, if the 37.3% plunge had been are a more realistic 12% increase, it’s a swing of nearly 50%!

5. That would add about 0.5 percentage points (50 basis points) to yoy core services CPI, which would move it from +5.7% to +6.2%.

Mr Richter, thank you for your analysis and summary of the government data base.

I think the government has another one to 3 columns of relevant data that goes 1, 2 and 3 years beyond YoY. Those numbers when excluded make the inflation look more under control than it is, which allows for political back slapping approval, when there is no success … as evidenced by how people feel. More specifically a year over year of +3% is not feeling like 3% if the previous 2 years were 6% and 5% … or more. People spend dollars not percentage points . No wonder they are not feeling the relief that their government espouses. And as you wisely point out, it’s about to get tougher yet.

I used the actual indices and can calculate any percentage time range I want, from two years ago, from five years ago, from 2018 (see my discussion of the health insurance index), or from the beginning of pandemic (see my discussion of food). In addition, I’m showing you the actual indices, not percent changes, for various categories (Food, cars, etc.). So look at those.

But to discuss something common, you have to use common terms, such as YoY or MoM or 3mma of MoM (blue line). The purpose here is not to shock, but to present data in a way that it makes sense and fits within the common framework.

So…..is higher and longer not working yet due to lag effect? Or Pow Pow has kind of failed and needs to go even higher than high now faster to tame this inflation wild bronco?

Pow Pow has failed. The CME FFR report still shows an 88%+ chance of a stay on 11/1 which is utterly crazy.

I get the Sept pass, but it’s obvious that Pow Pow & his “heads stuck in the sand” FMOC are unwilling to push further, at least in a timely manner.

It’s almost as if they’re hoping & praying the UAW strike will singlehandedly push the economy into a real soft landing with “maybe” 4.5% unemployment.

Rent inflation is up due to the NEW “residents” we have in the US since Jan ’21, and everything else is up mainly due to the fact that Uncle Sam will run a $2T deficit this year, and then next, etc.

hmm…so much for Pow Pow’s wish to create a legacy of being remembered as a better version of Volcker 2.0 without committing the same mistake to allow for inflation to re-ignite, especially since he has the hindsight of history to learn from…

Then again, can’t expect too much from someone that is pretty much a meme for such classic hit as “Inflation is transitory” to “Not thinking about thinking of raising rates” to biggest QE ever in history in the shortest amount of time and juice up housing market so much that it might be forever broken… So many classic hits to choose from…

“juice up housing market so much that it might be forever broken… ”

Ouch. That one rips into my gut. I’m still hoping for some kind of meaningful correction back to normalcy, though hard right now to see how.

Zest, housing will never correct. A minority of metros will have small adjustments but still have average prices orders of magnitude higher than the average income. Cost of housing will never be cheaper than it is now. Unless a nuclear war wipes millions of people off the face of the earth, its only going to get much, much worse. This is it. This is the bottom. Enjoy the minor seasonal dip till feb.

US homes for sale, 2008: Roughly 4 million.

US homes for sale, 2023: Roughly 1 million.

Sure, maybe some compression for a shorter sales cycle, but lack of inventory is real. With the great Recession and housing collapse of 2008 the whole housing construction industry was shaken. Specialized workers and builders left that industry and haven’t come back. Supply is still lagging 15 years later. New housing starts was at 2.2 Million in Jan 2006, and dropped to 478,000 by Apr 2009. It’s improved since, up to 1.2 Million in August 2023. But that’s barely half of what it was in 2006.

You want to guess how much the US Population has grown since 2006? 39 million!

Add to that the fact that existing homeowners sitting on 3% mortgages are going to be hesitant to sell and have to buy a home with a 7% mortgage.

Inventory is going to remain very tight. And population will grow.

Supply and demand. Home prices are going to continue to go up, up, up.

Total nonsense. You housing bulls act like people can just pay whatever the seller wants. That’s completely stupid.

Funny how people keep pretending homebuilders don’t exist and the banks don’t have lending standards like DTI

The deficits are now $2.5T to $3T, the next few years, absent a recession, which would make them even greater.

Powell is now on course. Almost all demand drafts clear through demand deposits. M2 is mud pie. DDs are showing no growth, but the transactions’ velocity of funds has risen.

“Housing’s share of the economy remained at 15.8% at the end of the second quarter of 2023.”

Link: “HOUSING IS THE BUSINESS CYCLE” Edward E. Leamer

Good summary TS: Thanks.

The rates are not the problem. Congress’ deficit spending and the Fed’s grotesque balance sheet are the problem.

Agreed! The NAR wrote Powell a letter recently imploring him to stop raising rates. Housing just can’t handle higher mortgage rates. ROTFLMAO, so let’s add to your astute short list of issue a grotesquely overpriced housing market that JPowell is doing everything he can to ensure doesn’t actually move towards real price drops all over the US, instead of the 10-20 market CS Index that everyone yacks about. Housing, new & existing, is 30% overvalued.

Like an economist said today on CNBC. We don’t get anywhere near 2% core PCE inflation without a recession. It’s just NOT going to happen.

And honestly, I’m not sure a 6% FFR would cause a recession with all the Fed & local (property tax) spending that’s going on nowadays. It’s been 7 months since the run on SVB created some necessary OMG panic. And still nothing else as really broken. AS of yet, I don’t see a line of CRE lining up for foreclosure do to higher borrowing costs. Everyone keeps saying it’s coming.

Well, what the heck does the Fed do if they take a pass on 11/1 and then all of those CRE failures don’t materialize by the Dec FMOC meeting?

He simply should not have taken his foot off the gas so soon. It’s just comical how oblivious it is that the Fed doesn’t want housing to reall rollover and get pushed down across the board nationally across all types of homes.

In fact, the loses need to be bad enough that it stymies invertors from jumping back in long enough for Congress to put some controls around investor-owned properties. Either put some limits on it or seriously get rid of some of the tax breaks or both!

Exactly. People still have faith in the Fed to keep their assets high. Until that dissipates, we’ll never get inflation under control.

Nobody believes the Fed won’t cave if there are any real problems.

To the extent that Powell “took his foot off the brakes”, I believe it is due to the fact that the October-December period is when many retailers make most of their annual sales and earnings.

All the while the so-called tightening has happened, the earnings of the country’s largest corporations have moved to a new record high, so because of Powell’s belief that the Fed shouldn’t tighten too much because of Christmas retail shopping, I believe we are likely to have even higher inflation readings in the next six months or so.

Powell knows that the Fed absolutely has to slow down the economy (thus also slowing down corporate earnings and the stock market). Oh, and then there’s Wolf’s health insurance index issue, and the election coming up soon. I think the Fed is caught between a rock and the hard place…

CRE doesn’t go to foreclosure if the owner doesn’t want it. It’s non- recourse and simply given back to the lender. This site has had all kinds of examples of this. Recently it mentioned an outfit called Ashford that just handed back nineteen properties of lodging including two Courtyards. That was a bit unusual because the main tide has been office towers preceded by malls with Simon Group having handed back eight of them. Last month two SF towers were mentioned on this site when they sold for far less than the original loan.

CRE is a disaster getting worse every month.

On the plus side, a big recession would be like a sudden flash of sanitizing light: all of the many, many, many overleveraged companies, banks, etc., run by people like SBF all too frequently, would suddenly get exposed when their companies could not meet their current expenses and actually, secretly went bust long ago. LOL

They don’t need to raise the FFR. Simply start selling assets and long yields will go up

The longer the Fed waits to continue raising rates the more likely it is that we see unemployment eventually reach 1982 levels. Just heard about someone who paid 1500 to have their cats teeth cleaned. Its like we’re living in a cartoon world now. Five or six percent is literally a gift to the [usual suspects]

Pow Pow and his Team of hundreds of PhD’s are stuck in voodoo economics called “Keynesianism” which has no connection to the real world but gets you a safe, high-paying job if you repeat its mantras “Deficits don’t Matter”, “recessions are caused by too little demand (so the gubment has to “stimulate” the economy) and “inflation is caused by too much demand (so the Fed has to kill the economy to bring it down)”. None of this is true and no Data supports it, but it’s your entry ticket to the Club.

“Mind-bendingly nuts” is absolutely the right way to describe that graph of healthcare CPI as an index. Nobody has seen their healthcare costs return to 2017/2018 levels, nobody. And even more mind-bending is the graph showing the index value to be only 30% higher today than in 2006! For the government to report that healthcare is only 30% more expensive than nearly 2 decades ago is not only nuts, it’s nothing short of criminal. This is blatant misreporting that zero Americans would believe. There are 3 kinds of lies… Lies, damn lies, and statistics (revisions & adjustments).

Oh no! You mean, the government which has caused this inflation, is not truthful in its reporting of the data? /s

Where are you getting the seasonally adjusted amounts carried out to 2 decimal places. The BLS news release shows levels with 1982-1984 being 100 and the all items current number of 307.789. I could divide the current month by the prior month level to go out 2 decimal places but these are unadjusted amounts.

I wish they would carry out seasonally adjusted monthly changes using 2 decimal places.

Downloaded indexes from the BLS via its “BLS Data Finder.” The percentages are calculations from the indexes, seasonally adjusted (for MOM) and not seasonally adjusted (for YOY).

Is there any more “opportunities” for the CPI wizards to use the “monthly push-down adjustment” trick on another category, now that healthcare trickery has run it’s course?

SPR drained and Healthcare trickery drained…should be an interesting 2024 as a lot of the “TOOLS” have been used, which will make those who used said “TOOLS” into actual “tools to reality” soon enough…

They still have the tool of adjusting the target inflation rate to let’s say 4%. Probably working on why 4% is “more suitable” story.

I’m guessing changing the target to say 3.25% from 2.0% would not be feasible until a global recession brings us first to 2% range (say 2.8%). Else the Fed loses credibility, in an inflation game that has has a human emotional factor that plays a very large role.

Waiting or the “Rent control” cries from Congress. That sure has worked great in the past (sarcasm)…

Like many things in life, you can legislate it to be illegal until it goes underground and pops out at the most inopportune time, in a manner that is exponentially more difficult to control.

War on drugs, war on “inflation, war on “fill in the blank”…might as well call it “War on human nature”, so good luck with that…HA

You mean Venezuela and Cuba aren’t success stories?

They’re not going to do that, and the reason is quite simple. With an annual deficit approaching $2 trillion, they have to sell a lot of debt. If they don’t stick to their 2% story, the markets are going to demand more interest on those long bonds. Also, look at all these countries that bought our debt – if we say so long 2% target, we’re basically saying to these countries “You’ve been had”.

Now, they have been had, but I don’t think they want to come out and say it.

Those are good points. They do need new suckers to be settled with debt. Perhaps that’s why they do not teach math anymore.

They just lost 20% to inflation since 2020, without major objection from markets. You think a change from 2% to 3% is going to worry them?

Bobber – its whether or not the /official/ target is raised.

Clearly bond yields have not (yet) blown out with current inflation, but if the Fed publicly acknowledges inflation can’t/won’t go back to 2%, well that’s a different story.

Thanks for the two decimal places. When the media says 0.3%, all I know is that it is somewhere between 0.25% and 0.34% because of rounding. Core CPI, month-to-month is 0.32%, as you say, which is the most important figure to me. That translates into 3.91% annualized, far above the Fed’s 2% target. Of course this assumes every month for 12 months is 0.32%. But I have learned, if you have to predict, and you have no other variables in your model, the best predictor of the future is the most recent data point. Higher, longer.

From what I’ve seen locally, a lot of the buying pressure for single-family homes is from investors, big and small, snatching up properties to take advantage of rapidly increasing rents.

I don’t see home prices in the average price range coming down until rents start declining. And I don’t see rents declining until young low-wage workers get squeezed enough to move back in with mom and dad. Jobs data doesn’t make it look like that is happening anytime soon.

As a matter of fact, investors have cut back purchases more than owner/users. So no, it’s not investors buying up all the properties. Returns no longer work for investors, given the 8-9% interest rates for investment properties, higher taxes and much higher insurance rates.

Not to mention that they’re reaching their limits on ability to increase rents. House PRICES are set by the availability of credit/money. House RENTS are set by average incomes.

The two are not necessarily correlated. There’s still plenty of money out there, but it’s not evenly distributed, so the idea that they can raise rents every year by 10% is just a fantasy.

“they’re reaching their limits on ability to increase rents”

I disagree – the limit to how high rent can go up is much higher.

Everyone says tenants can just move out, forgetting how expensive and time-consuming moving itself is.

Rents are also much to low vis-a-vis home prices. Why would anyone landlord for less than 5% return when they can simply park their cash in a MMF?

too* low

MM, first, not everyone has unlimited income. Second, that rents are too low vis-a-vis home prices is an argument for the idea that home prices should come down, not that rents should go up.

In Canada they just put more renters into one house or one apartment as rents skyrocket. This keep rents rising.

No but they have to live somewhere. And,if they have to choose between giving up takeout every week or the roof over their heads, I’m sure they’ll choose to give up the former.

Or just get a roommate. I’ve never not had one while renting (and usually had 3-4 roommates). I could never afford to rent anywhere in my city (Boston) without roommates splitting the cost.

For small investors yes, but the big boys are generally “cash buyers”, so rates don’t matter to them, they’re allocating their own capital.

Not true at all. The big boys might pay with cash as seen by the seller, but they have large credit facilities that are usually not fixed rate. So their cost of capital is not 0.

Rob B.,

1. The Big Boys are not using their own cash. They’re borrowing at the institutional level by issuing bonds, rent-backed structured securities, etc.

2. They’re not buying either, they have pulled back massively, they’re waiting. What they ARE doing is buying from each other — entire portfolios of thousands of homes are getting shuffled around between big companies at who knows what fire-sale prices.

Big boys either borrow or have investors who demand 8% or more return

CCCB: I agree that investors aren’t as eager to buy single family homes, at least that’s my observation in the Minneapolis metro area. Maybe I’m biased, but the labor pool to support cheap repairs and maintenance just isn’t there. As a remodeler, I charge retail prices and refuse to do shoddy landlord specials. I’m fortunate to be able to turn down undesirable work, but those are the cards the market gave me.

In KC, several people advertise that they will buy any house, in any condition, any time.

Lowball prices

Where’s that cartoon of Jerome pulling out his hair.

He must feel like a marked man. His masters are screaming lower…LOWER, yet inexorable inflation, even measured with the gamed numbers, rises.

Not unlike a balloon filled with the hot gasses expelled from the various orifices of politicians.

Go for it Jerry!!!!

That cartoon always makes me lol.

Yellen should get a framed and signed copy, place it on his desk. Haha

Love that picture too, for a while I was using it as forum avatar…sadly about 90% of the people don’t even know who the clown is…

The picture is copyrighted. Please don’t used it. Thanks.

Hi Wolf – can you give us a feel for what Core CPI would have been if health insurance CPI adjustment had not been -37% but for instance 0 so that we can understand what the forward effect might be?

I just walked through this thinking here in another reply a minute ago. I have a better feel for core services CPI, where health insurance weighs about 1%. The yoy core services CPI might be 6.2% instead of 5.7%, if health insurance CPI would have been a more appropriate +12% than -37% (a swing of 50 percentage points).

I’ve literally been waiting all year for this. Everyone hoping for a Santa rally into EOY might end up with coal for Christmas. Time for bears to wake up early out of hibernation.

Friday 13th is as good day as any to get the ball rolling on the market crash.

10 year bonds getting ready to bump up on 5% and then move up to 6%.

They say at some point in time every ponzi ends. I’d say Bitcoin has much much better fundamentals than Wall Street past, present and future. All we know is someday the bankers will pull the rug out from under everyone and the stock market will implode.

Is there a reason Core CPI lags behind CPI?

It makes these news releases more muted when core looks more positive than overall CPI.

When the core starts going up in the charts isn’t it months later? And the fed can just talk about current issues.

Just wondering

“Is there a reason Core CPI lags behind CPI?”

Assuming this is correct (I’m not saying it is or it isn’t), Wolf answered here (copy/pasted from the article above):

“Fuel prices – gasoline, diesel, jet fuel – also make their way into consumer products that are shipped by delivery van, truck, rail, or air as are nearly all consumer products. Jet fuel also makes its way into services via air fares. These products and services are included in core CPI, which is how core CPI reacts indirectly to rising energy costs.”

Personally, I apply the same logic to the producer price index — using that to anticipate inflationary trends in the next 2-3 months. Which sounds like it should work! On a macro level, at least…

The core and headline inflation seem to meet around 4%. If there is no recession (and it doesn’t appear to be for the foreseeable future), I think they will stay there for years. I don’t know how much these statistics reflect the reality. Even considering that it actually reflects the reality (which I don’t believe), when combined with the inflation of 2021, 2022, it makes a massive total more than 20%.

Wolf, you were totally right. Something has broken long time ago: price stability. And FED is responsible for it 100% by reckless money printing. They could have ended the inflationary cycle in March 2023. But instead, they printed another $400B and invented the BTFP backdoor, which gives the creditors complacency and constantly fuels the inflation.

At this point, I strongly believe that no further rate hikes will bring the inflation under 2%. It doesn’t matter even if they raise the rates to 7%. My observation is that consumers and investors became insensitive to rates. The remaining asset prices (stocks, crypto, RE) are diverged from the bonds. The only thing that can shake the markets and the consumers is a speeding up of QT. The only way to speed up is to shut down BTFP and sell the mortgage BS immediately.

Agree. In my opinion, it wasn’t the $400 billion “printed” per se that was the problem, as most of that has been taken back out of the economy. It was more the message. The message being that, while the Fed will tolerate a slow down in the economy if it happens in an extremely orderly fashion, it won’t tolerate any real pain.

That makes the risk-taking and other acts by the banks and other “investors” resume, as the “Fed put” is back.

People have asked why the stock market and housing market have been so resilient. Well, this is why. And it’s also the job market, as employers are less likely to hire if there’s real uncertainty. If Congress and the Fed sends the message that there is no real uncertainty, it’s back to business as usual.

Einhal, I agree 200% with you. It was not actually the amount ($400B) printed. It was absolutely the message: “Dear government and markets. Be absolutely assured that my finger is on the money printer button. Whenever there is the slightest risk of recession, I will print like a drunken sailor. I will not let any stupidly managed financial institution that takes excessive risk to fail. Here is your BFTP. You can lend and invest, disregarding the risk.” The govt, corporations, consumers, investors and buyers got the message. Now, all of them are like spending, hiring, investing and buying without worrying about risk at all. Because they got the message that the FED has their back, whatever stupidity they do. This caused a massive loosening of credits, inflating the prices of assets, commodities and services. Housing market is nuts. Most don’t care about the rates any more. The inflation is now entrenched THANKS TO THE FED. They could have stopped it by just doing nothing in the March 2023, but they knowingly didn’t. That was one of the many many monetary mistakes they did. And they lost their credibility for most spenders.

7% has been in my mind as well. At 7% borrowing costs for many small and medium business become too high for investing capital. We would see a huge slowdown in business spending, a contributor to GDP. Also hiring freezes and layoffs. I think at 7% the whole floor starts to get gummed up and the dancers become a lot less free to move around. But, we probably don’t get to 7% this cycle the way this Fed has been communicating.

What caused the first over-adjustment to Health Insurance CPI in 2018? It seems like we’ve spent the last 5 years making wild counter-adjustments. In 12 months from now, the Health Insurance Index value will be about 12.68% higher than it was in the fall of 2018, which would annualize Health Insurance Index increases at about 2% per year over that 6-year span.

Wondering the same thing. Data looks suspect from that point on, untethered by reality.

And I also think the Fed is pausing here because they don’t want to raise while there is so much debt being issued. Be good to know if there is an historical pattern that confirms this theory.

I for one am tired of my salary getting battered like a rented mule.

Does a slow fed toying with the economy help the rich more? Or is inflation eating them alive as well?

Let’s Jack these rates to 15 and be done with these rising prices.

You should be retired ,like getting kicked in the nuts =painful

Jacking interest rates up would just bankrupt the U.S. Government.

At this point the only thing that will bring inflation down is a hard crash landing of the economy. These interest rate increases are too little and too late and are not working. Without fiscal policy to eliminate 2 trillion deficits as far the eye can see, interest rate increases by the Fed will never work, and are actually causing worse inflation as all these financing costs are curtailing the supply of goods and services, and are being passed on to the consumer. Judy Sheldon, stated this obvious fact on the financial news station the other day. John Williams says the inflation rate is more like 7.2% right now not the 4.0% being reported by the government. I agree. All the items I purchase every month, which are necessities are up double digits, which is worse than even the 7.2%.

Some say Volcker’s 16% Fed Funds Rate in 1981 worked, but it took a while. However, Powell is no Volcker.

He would love to gaslight you to think he is second coming of Volcker..

Perhaps so if Volcker is missing a spine..

I really don’t want to see that kind of nasty double-dip recession again. That stuff is horrible for young people graduating into this kind of mess. I went through it, and I don’t wish that on anyone. If that can be avoided by moving more slowly, it would be a good thing.

Nobody who has goofed around with this stuff for a while has ever said the markets were fair. Life is full of big IFs and big BUTTs (especially in the US), and I would be okay if slow is the way to go. But as you, Wolf, say in your current headline “Acceleration of Inflation Continues”. Do you think Fed policy is working, even though they have raised rates at the fastest pace in history? Realize they are coming off a prolonged period of the lowest interest rates in history.

Certainly overall and core inflation are way down from their peaks. But are they accelerating again as your headline says? Has inflation become entrenched? Is a soft landing just another Wall Street dream? I say yes to all three. We shall see.

JFK once said “life is not always fair”.

“That stuff is horrible for young people.”

And 12x median income housing isn’t? This snail’s pace inflation fight is bullsh!t. Sell some f***in’ MBS, Powell, you asshole.

Lmao! Depth Charge.. freaking hilarious!

Volcker stopped inflation by imposing reserve requirements against NOW accounts in April 1981.

True, too little.

Just look at those home prices in the nose bleed seats. Insane!

Well said. I agree that inflation is at least 7.2%.

Any claim by the BLS that that “Health” Insurance premiums “went down” ANY time in the las DECADE, never mind “last year”, is a masterpiece of Orwellian mindfork.

Just adjust your income to match the adjustments to CPI and you’ll be fine

Howdy Folks. Ah, Houston, we have a problem. No, worries, all planned this way from the beginning. Pretty sure Reagan did the same thing. Boogie down folks, disco fever is back.

A mind-bendingly excellent report. Thanks Wolf.

Tying your reporting on wacky healthcare cost adjustment process to your last article on 2024 Social Security COLA…

…Is CPI-W effected by the healthcare adjustment, and were the 2023 SS big increase and the much smaller increase announced for 2024 impacted by the healthcare adjustment?

What a confused cauldron of simmering fish!

Thanks

“Acceleration of Inflation Continues, Core Services Inflation Spikes despite the Massive Health-Insurance Adjustment ”

A very benign title for a serious problem. No predictions on Fed policy? Or do you think it is impossible for the Fed to hike to 7 or 8%?

Inflation like this is a long-term problem. This won’t go away in a year of two. The Fed may well be at 8% two years from now, or might still be at 5.5%, with core CPI at 4% to 6%. It would be just a guess to predict inflation this far out, nothing more, but you can predict that it won’t just go away.

Howdy Mr Lone Wolf. If you consider the amount of govern ment spending , the FED rate could be double digits?

You know for a fact they’ll be at 5.5% while talkin’ about seeing some green shoots of disinflation just around the corner.

So disinflation huh?

Does someone bring that money by on a certain day?

I’ll pencil it into my scheduler.

Agree it does not feel like 4% but this might be because we are reacting the total price change over the last 4 years or so.

Some people compute “inflation” by dividing our fiscal deficit (2T) by our GDP (27T). This would yield about 7.4%. Not sure that is a good metric though. In the absence of printing, the dollars to buy the treasuries funding the deficit would have to come from existing/previously printed money.

This is further proof that Powell doesn’t know what he’s doing.

Howdy Lucca He raised rates during the Trump Presidency but caved.

Wolf, thanks for the real data, I was waiting to read your analysis concerning the recent CPI report. MSM said it was the same as August, as somebody else pointed out, they decided to leave off a decimal in that comparison. Bunch of Jokesters

I did note this: “Owners’ equivalent of rent accelerated sharply to 0.56% in September from ___ for August (6.9% annual rate)…”

I believe you wanted another number to reference in the blank for August.

Thanks for the solid data, As always.

On its face the CPI calculation is a joke. “Recreation” and “Food away from home” have nearly the additive percentage weight equivalent of “Owner equivalent rent” housing costs.

????

OER = 25.6%

Recreation services = 3.1%

Food away from home = 4.8%

Did you see the decimals in the wrong place?

We are shopping our health insurance again.

Self employed, both of us are healthy, early 60’s.

Currently at 1350/month + 7.5k deductibles. Scheduled to go to 1550/month.

I haven’t seen my increases yet. But in NC there was a press release that the Affordable Care Act policies would be going down 4%.

So anyway I’m factoring in a 5% increase because I’m self pay. Cuz my work’s insurance is bottom of the barrel. The executives raided the benefits packages a few years ago to justify their salary increases.

“These underlings do not need good insurance! My wife needs a shoe room!” – Executive

I was very happy when I hit 65 and could get on Medicare. Health insurance is brutal, especially 60-64. Made me want a single payer national health care system. Get rid of the insurance companies completely. Those b tards actually control the pricing and procedures of the entire medical system, probably more than you could ever know. Your life is in their hands.

So you suddenly wanted single payer care when it benefited you.

How selfless and altruistic of you.

I want single payer because the massive unemployment from the former insurance industry would trigger a Fed pivot. /s

Thanks, but it is more like enlightened self-interest. Some grow, some learn, some adapt, some eventually recognize the evil of commercial health insurers and their peddlers.

So 12 months from now are we going to be talking about the big negative health insurance adjustment again, pushing CPI down?

These radical swings… hard to drive straight and true when you’re speeding and oversteering down the road.

The fed has to see this and adjust using some sort of moving average to smooth things out in their decision making? Just the markets that react to every jerk in the other direction?

The Fed prefers PCE which doesn’t include the health ins adjustment

VT,

The BLS announced that they will tweak the system of calculating the health insurance CPI. It’s still on the same basis of “retained earnings,” but the effects will be spread differently, so that it doesn’t do this kind of crazy thing. So we’ll see.

The thing is now that the health insurance index has been lowered to 2018 levels, and I have no idea how that will distort the index going forward, when you look at it on a long-term chart. This is one of the biggest data messes I have ever seen. It worked relatively fine for years until it suddenly blew up during the pandemic.

Re; all comments about health care. It is well documented fact, including a Harvard study, that costs for every procedure and drug are the highest in the world in the US. It is kind of mind boggling that until a year or so ago, insulin in the US cost 1000 percent of the price in Canada. They can’t claim the costs of research for that drug.

Agreed. I think it’s sometimes referred to as being a captive audience. Love it or leave it, as they say. How many Americans actually want pick up and permanent leave the US? Close to zero.

It’s so easy to google this stuff. Between 1999 and 2018, the number of Americans living abroad doubled from 4.1 million to over 9 million. The numbers have probably continued increasing since then. Very few people are content in the US but most of them lack the initiative or knowledge to leave. Mexico City is currently experiencing a boom in the number of Americans moving there.

I am referring to americans who voluntarily and permanently give up their citenship due to inflation, the topic of this discussion.

You are referring to xpats who play the geographic arbitrage game and head home as soon as things aren’t working out. We agree.

It’s economic rents, full stop.

Wolf

Can you please comment on who is bearing, or will bear, the costs of the massive decreases in long term bond prices and on what the consequences of these are likely to be?

Thanks

I predict long term 30yr treasuries will decline to .25 to .30 on a dollar before this carnage is over. Many long term corporate investors will fare worse as credit issue surface.

Thanks sc. What about more banks? Hedge funds?

More banks, hedge funds, insurance companies, and pension funds will be hurt badly. Mark to market makes them take unrealized losses.

Non fed repo would show you the real market interest rate. Probably closer to credit card rates.

Bruce A Forbes-

If the 30 year Treasuries drop as SC plausibly predicts above, the long list of losers will include:

~ Short-term corporate borrowers with maturing debt that needs to be rolled over. (Expect many bankruptcies.)

~ 401k investors who bought into the 60:40 rule of diversification and selected the bond fund with the best backward looking bond fund from their company’s investment menu. (If the stock market meaningfully corrects too, the old line about “my 401k just became a 201k” will make its decennial return.)

https://wolfstreet.com/2023/10/07/my-take-on-what-qt-has-done-to-stocks-bonds-commercial-real-estate-lots-of-bloodletting-what-it-will-do-going-forward/

Thanks, andy!

Flower at costco went from 5.99 to 12.99. CPI lies.

The 100lb bag?

How many muffins are you making? ;)

I regularly buy 6-packs of a super-good craft-brew IPA at Trader Joe’s for $6.99, lowest price in at least five years for this kind of beer. Ales Necas lies.

I read that craft beer sales have dropped, but I see what you did there (cherry picking data).

I defeated cherry-picked BS with cherry-picked BS. There is always some goofball that thinks that inflation in the US is 25% because the price of his shoelaces went up 25% or whatever. That kind of stuff is patently idiotic, and I shoot it down in kind.

Big Beer sales (in volume) have been dropping for many years. Craft brews exploded on the scene and ate Big Beer’s lunch. Overall beer sales in the US have been dropping for years. I used to report on it a decade ago. Most Americans don’t like the taste of real beer. So Big Beer came along with lite beers that taste like slightly flavored sparkling water, hoping to get people interested in beer, but still, beer sales went down.

Americans drink more and more mine, and hard liquor too, I believe.

Not sure if craft beer sales went down, or if Big-Beer-owned craft beer sales went down. Big Beer has bought out many craft brewers, and then ruined their beers. Big Beer is the kiss of death for their acquisition targets.

There’s also lots of competition from other 5% beverages. Spiked seltzer, tea, soda pop… they’ll put 5% alcohol in anything these days.

I like Dos XX Amber and Newcastle

haven’t had Newcastle in a while though.

It’s hard to get thru a case. With dos xx at least I making Mexican a few nights a week and it meshes.

Prices for a 12 pack are a much better price per bottle. When on sale

I don’t drink anymore (or any less) but when I did I drank the best brew in America – that’s right, San Francisco’s own ANCHOR STEAM beer.

And now they’re going to close shop – a true tragedy.

That was a lousy beer. But taste cannot be argued with. If you liked it, great. Anchor didn’t have even a decent IPA. They were owned by Big Beer (Sapporo), and they got even worse because of it. Not sorry they’re gone. All Big-Beer-owned craft brewers should die.

What do you mean by big? I love Voodoo Ranger, as an example.

Einhal,

It is possible that Kirin has not yet screwed up Voodoo Ranger. Keep your fingers crossed.

Heineken screwed up one of my favorites, Lagunitas IPA, and I stopped drinking it. The Indian conglomerate that owned Mendocino Brewing Co – one of the earliest craft brewers with some great beers – killed the entire brewer. There are many others. So keep your fingers crossed. It’s a sad day when the corporate cost cutters move in to degrade your favorite brew.

Don’t tell me you don’t like Sapporo…my God, it’s like angels waltzing on your tastebuds

Alcohol at home +2.9%? Now that crosses every line.

Back in 2018 I could stay three nights and ski two days with a family of four for only $800, all in. The same exact package is now about $2000. Ski prices and related lodging has gone through the roof, largely due to industry consolidation and rocketing RE prices.

Skiing is a rich person’s sport. Always has been.

In 2011 I took a road trip to ski in the Rocky Mountains, and stayed with old college buddies who had moved out of Minnesota. I bought a pair of used Rosignol skis and poles for $250. H/H ski jacket and snow pants for $350. One of my friends was an experienced skier and taught me how to ski in a few days, after I got acclimated to the altitude. He also showed me how to find cheap lift tickets. Lift tickets at Steamboat were $50/day. Aspen was $45. Vail was $70 (also the most not-worth-it). Alta was $60. A not-worth-mentioning place in Coeur d’alene was $45, and I finished my trip in Big Sky, Montana, at $50/day. Big Sky was also the best skiing I’d ever experienced, with the summit at close to 12000ft. The sky was so blue it had hints of black, like I could almost see the stars in broad daylight. But not quite. I enjoyed almost a half hour of non-stop skiing through powder each run. Including the cost of fuel, food, and couch surfing, a 2 week trip cost me about $800. I did it in a Chrysler Sebring with winter tires. I don’t know how rich you’re supposed to be to ski, but poor and middle class folks should try it.

Nowadays it’s different than 1972 when you owned a wood paneled cheese wagon.

NYT did a few stories on how ridiculous it is now. So many people the mountains are literally overrun.

I feel like it’s a social status “we belong” thing now. Back in the 70’s-90’s looked like a fun care free lifestyle. Kinda like golf country clubs, but nowadays those are all screwed up as well.

Oh well

I did this in 2011. And my cheesewagon was an ’06 Sebring with leather seats and a badass Alpine navigation system with Bose speakers. I bought it at a salvage auction and found a mechanic to fix it up. I was in my twenties, and the point I was trying to make is you can find ways to enjoy your life if you don’t follow the herd.

Sorry the Rockies are played out and every hill is overpriced. You can be a forward thinker and try to enjoy something that isn’t so bought up. Get ahead of the game. Go take some risks. Otherwise you’ll be 90 with a cat, wondering why you don’t have a house in Vail.

I’m not rich, so I had to stop skiing due to crazy lift prices

Volcker part Deux.

If you’re young and don’t know, you’re gonna LOVE it.

Ala Jerome?

Never,never,never,never, ad infinitum.

I wonder how much the states and the Federal government is impacted by increase in healthcare costs. A significant number of Americans are on Medicaid, Medicare or CHIP. Many are getting rolled off post COVID but CA had 40% of the population on Medi-Cal alone.

Will be interesting to see if we actually get a decent bump in core inflation due to the health adjustment going the other way.

Also looking to see how far it does go the other way since this last year has seemed drastic.

Conspiracist can wonder…

The BLS announced that they will tweak the system of calculating the health insurance CPI. It’s still on the same basis of “retained earnings,” but the effects will be spread differently, so that it doesn’t do this kind of crazy thing. I think they’re trying to avoid that it will whip back the other way. I do agree that they have to change how this is done. It’s just inexcusably bad. So we’ll see.

The thing is now that the health insurance index has been lowered to 2018 levels, and I have no idea how that will distort the index going forward, when you look at it on a long-term chart.

This is one of the biggest data messes I have ever seen. It worked relatively fine for years until it suddenly and totally blew up during the pandemic.

5 years ago a 1 ton diesel work truck in the bottom trim could be had for under $40k. I just saw one with an msrp of $75,000. Sum beach. Factor in insurance, $6.50 diesel, maintenance, etc. and the math is real crooked. Real fuzzy.

The Fed should NOT have the power to expand the money supply to the degree they do now.

Whom do we call?

Ghostbusters?

Macron, cuz he’d bring crunchy French cookies!

Notice…

all the “flawed” inputs are reading lower than reality.

OER and health insurance, etc….

Who compiles this survey or OER? Lots of “wiggle room”.

Can’t wait for the next CPI without the healthcare adjustment. Wall Street’s heads will explode. Will be most enjoyable to watch.

Most importantly, it should mean higher for longer. An early Christmas present.

Just saw Wolf’s post on the BLS possibly trying to avoid it swinging back the other way. Crap. They had the benefit of it lowering CPI, so they need to continue when it isn’t in their favor. This is BS.

I’m so damn sick of the manipulation.

What are your thoughts on the theory that the Fed doesn’t want to slow inflation that much because devaluation of the currency is needed to address the National debt?

It makes sense to me, but how to verify this motive?

The “slow” fed actions could point to this or to cautious approach to avoid severe recession.

Thoughtful opinions encouraged

I’m absolutely convinced that’s what’s happening. Let inflation run out of control for years, all while pretending you care about it, prevents yields from blowing out while still devaluing the debt by 40-50%

I have heard this argument about inflating away the debt, but I’m really questioning it.

Inflation forces higher interest rates and the government must refinance at higher rates. This drives up the interest payments on the debt, which leads to a larger deficit and runs the debt even higher.

How is this a formula for eliminating the debt?

I guess the idea is that inflation will lead to higher tax revenues and the increase in tax revenues will be greater than the extra interest payments? But if the Fed is forced to raise rates to fight inflation and cause a recession, that will lead to job losses and less tax revenues in my estimation.

Not sure i believe that inflating away the debt actually works in the real world.

No, it doesn’t work in the real world, because the government spends more than you’re ever inflating away.

The logic though is keep inflation high, but make people think you’re trying to address it, so long term yields stay low. This way, inflation eats away the debt while not correspondingly increasing interest payments.

I’m not saying it works, but that’s the theory.

QT increases the real rate of interest. QE decreases the real rate of interest. Negative real rates of interest were because of QE, the artificial suppression of interest rates.

Higher nominal rates of interest are not restrictive when there is an increase in the transactions’ velocity of funds.

If the Fed didn’t want to bring inflation down, they wouldn’t have jacked up interest rates from 0.25% to 5.5% in a little over a year. This was a huge move, a proportionately much bigger move than going from 10% to 15%. In addition, they’re doing record QT, already unloaded $1 trillion in a little over a year. People who say that the Fed is not serious about inflation are goofballs.

I think there’s a difference between being serious about inflation at all costs and being serious about inflation as long as you can reduce it and slow the economy is a very neat, orderly manner with no real pain to anyone, corporate or individual.

Many people, myself think they are serious in the latter respect. But we’re not convinced they’re serious in that they would allow any real recession.

“People who say that the Fed is not serious about inflation are goofballs.”

The Fed IS serious but their policies do not seem to be working. I wish they would. We just went out the other day to do some appraisals in DC and I don’t see any letup in the price of homes and condos even with these high interest rates. Everyone and everywhere you go you hear the same people belly aching about inflation. The Fed can’t do its’ job because the Congress and Executive branch of our government are spending like drunken sailors, to the tune of 2 Trillion+ as far the eye can see. Until this spending is curtailed interest rates nd inflation will keep going up no matter what the Fed does.

I think it may be a mistake to blame the Fed one way or the other, because the Fed in fact does not really know what to do. Powell is clearly flying by the seat of his pants. He has said as much many times in his press conferences. He says they wait for “data” (much of questionable validity I might add) to see if their policies are working and if they have to do “more” or “less”. He is often “surprised”, for example the continuing strong labor market. Such action and comments do not inspire confidence. Attempts at centrally planned economies have been disasters historically, the Soviet Union being the best example.