Income from all sources minus government transfer payments outruns inflation again.

By Wolf Richter for WOLF STREET.

So here we go again. Every five years, the Bureau of Economic Analysis adjusts its Personal Consumption Expenditure data going back years as part of its “comprehensive update of the National Economic Accounts.” We’ve already seen the effects of these adjustments on the PCE inflation indexes, which were revised substantially higher for the past two years (I show the old data in green, overlaid with the new data in red here).

In terms of the inflation adjustment of consumer income and spending, the BEA, when it released the August figures today, also shifted the inflation adjustment from “2012 dollars” to “2017 dollars,” which obviously changed all the dollar figures for “real” income and “real” spending in a massive way.

The income from all sources but without transfer payments from the government (so minus Social Security benefits, unemployment insurance, VA benefits, etc.) has been outrunning inflation for months, after a steep setback last year. So this is income from wages and salaries, interest, dividends, rental property, and personal business, but without transfer payments.

Adjusted for inflation, so “real” income rose by 0.1% in July from June. The three-month moving average, which irons out the monthly ups and downs, also rose by 0.1%, and was up 2.1% year-over-year: Consumers again out-earned inflation.

But in the first half of 2022, consumers’ real income dropped sharply for six months on the surge of inflation, and when real income began to rise, it took another six months to get back where they’d been at the beginning of 2022, and then languished there for months. In April 2023, real income finally started setting records again and has continued to do so every month since then.

This income growth is a function of rising employment, rising wages and salaries, rising interest incomes, rising rental incomes, etc.

![]()

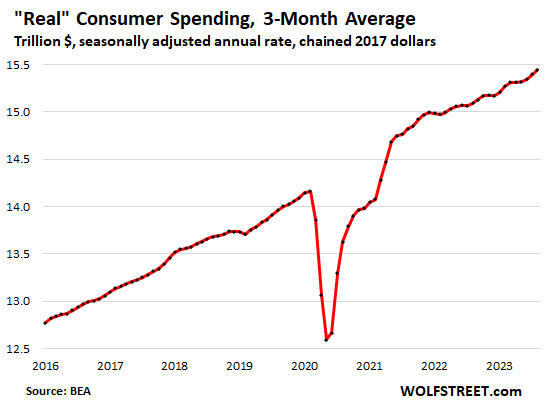

“Real” consumer spending (adjusted for inflation and for seasonal factors) rose 0.1% in August after the 0.6% spike in July.

The three-month moving average, which irons out the drama of those monthly ups and downs, rose 0.3% for the month and 2.3% year-over-year. This roughly matches the average growth of the Good Times before the pandemic.

You can see the acceleration of growth over the past few months:

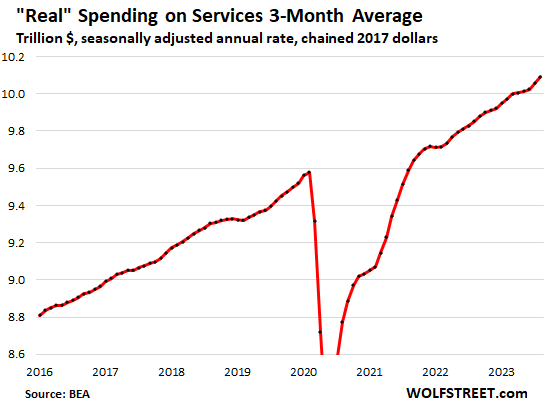

“Real” spending on services (adjusted for inflation) rose by 0.2% in August from July. The three-month moving average rose by 0.3%. Year-over-year, real spending on services rose by 2.4%.

This inflation-adjusted growth of spending on services is astonishing because it’s in services where inflation is still red hot: Core services inflation rose by 5.1% in August, according to the PCE price index.

Not adjusted for inflation, spending on services spiked by 7.4% year-over-year!

Services, which accounted for 65% of total consumer spending in July, include housing, insurance, healthcare, travel bookings, concert tickets, streaming, subscriptions, repairs, cleaning services, haircuts, etc.

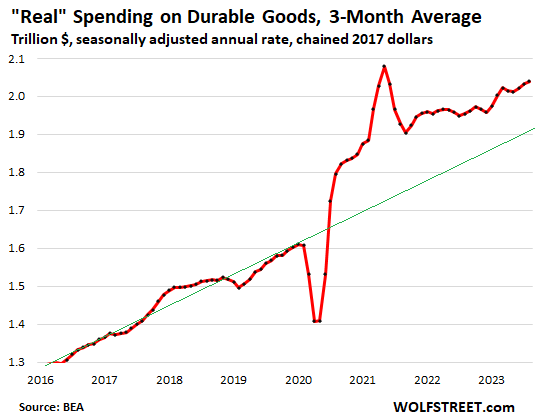

“Real” spending on durable goods (adjusted for inflation) fell by 0.3% in August from July. The three-month moving average rose by 0.3%, after the jump in the prior month. Year-over-year, the three-month average jumped by 4.3%. The PCE price index for durable goods has been dipping on a month-to-month basis and year-over-year, from the huge spike in 2022. So adjusted for inflation, falling prices boost “real” spending.

The pandemic spike of spending on durable goods, adjusted for inflation, still hasn’t returned to trend, and in fact seems to run permanently higher compared to pre-pandemic trend, which is another indication that our Drunken Sailors like their stuff and don’t just quit buying it because economists said they would.

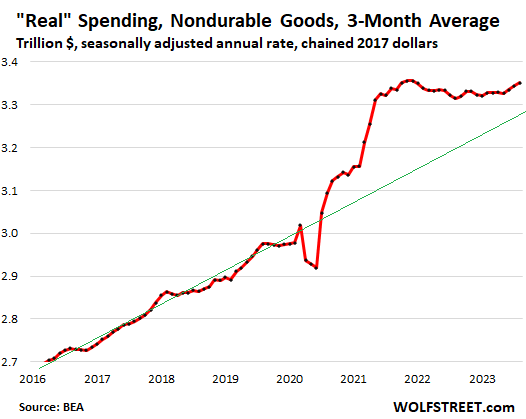

“Real” spending on nondurable goods (adjusted for inflation) dipped by 0.1% for the month. The three-month average rose by 0.2%. Year-over-year, it rose by 1.1%. Nondurable goods include food, fuel, clothes, shoes, and supplies.

And it’s in gasoline where inflation is now raging. Not adjusted for inflation, spending on nondurable goods spiked by 1.3% in August from July!

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In chart #1 Real income seem to run below the trend( you didn’t add a green line to show that) but in charts 2 to 4 real spending seems to be higher than the trend in case of goods and almost on trend for services.

So where the extra money comes from if ppl make less money than the long term trend but spend more than the long term trend? I’m assuming from pandemic savings? For how long that can continue?

Inflation is a bitch. The huge bout of inflation in 2021 and 2022 was a massive setback for lots of people.

But people are still earning more than they’re spending. Personal saving was $794 billion SAAR in August; the personal saving rate was 3.9%. So the money for all this spending comes from all this income. And the savings keep growing.

The savings rate is abysmal though – trending to all time lows of the mid-aughts per the Feds charts, showing that people are throwing all of their gains right back into the consumer economy. Gonna be really hard to break the ingrained “I’m a consumer first” mentality. My fear is that eventually it will break, and consumers will be so ill prepared to deal with the consequences of a recession that Congress and the Feds will once again throw gobs of money into the population and supercharge inflation. Rinse, repeat.

As Wolf said: “which is another indication that our Drunken Sailors like their stuff and don’t just quit buying it because economists said they would.”

Exactly. Consume first, save second. Those two should be in reverse order but a large percentage of US consumers do not see it that way.

Which reminds me of an observation from William Sherden: “Consumers do not behave according to rational equations built on the assumption that money is the only driver of human behavior.” Or, as a sales trainer once told me, “People make purchasing decisions emotionally and justify them logically.” Rationality goes out the window when emotions come into play.

Many emotional economic decisions are being made these days – that is part of what keeps the drunken sailors partying and why most economic models and forecasts are wrong. And always will be. Human behavior is simply too difficult to predict.

Another observation: despite the correct concern of the lopsided wealth concentration in the US, some of that has nothing to do with Fed policy. Policy has certainly exacerbated that issue, but another part of it is the foolish manner in which many people handle their money. They blow it on toys rather than saving it. A higher savings rate would be a major step toward more equitable wealth distribution.

Artifically-low interest rates have discouraged saving for years. Now inflation is doing the same.

This is why interest rates need to be much higher.

“Artificially low interest rates have discouraged savings for years….” only to those who are myopic.

Those who continued to save, despite the low interest rates (and, yes, I too got the calls from my broker(s) that I was losing ground to inflation) are the ones who are now reaping the benefits of their decision to save vs those who blew it on $100K pickups and now have a truck worth far less than they paid and a gigantic payment/debt to go with it. Many are trapped with no way out. Can’t even sell / trade it because they have negative equity, and if they have it “stolen” they’re still screwed unless they have gap insurance.

You want to improve your position on “wealth imbalance” game? Stop playing the short game.

El Katz, to a point, yes, but at least half of the “gains” from 2009 to the present are undeserved, and are not based on thrift or foresight, but based on poor government policy.

That means that the person who has saved and invested a lot and has $20 million in net worth really only should have $10 million of it, if we truly had a free market.

“…one man’s ceiling is another man’s floor…”

-p. simon

may we all find a better day.

*some people. Correct me if I’m wrong, but isn’t this just total earnings across the population? Dividends, interest, rental income, etc, these things aren’t a factor for more than half the population. Isn’t this just the top 10% or maybe 20% of people seeing massive income rises?

The real figure we need is what % of people are seeing real income increase?

Always the same “Most Americans are poor and live paycheck to paycheck,” and then people are surprised that consumer spending keeps growing and come up with crazy theories to explain it.

The income increases since 2020 were most pronounced at the lower levels of the income scale — this has been well-documented — in part because people refused to go back to work when the pay was bad and working conditions and shifts were awful, leading to a massive labor shortage across those jobs. We’ve reported on this many times here. Did you miss all that?

And here is the wealth of Americans by Wealth Category:

https://wolfstreet.com/2023/09/24/my-wealth-disparity-monitor-of-the-feds-money-printer-era-september-2023-now-theres-inflation-qt-and-rate-hikes/

I think when spending goes up across the board we can throw out the idea that only a small percentage of the pop (Top X%) are the ones doing it.

After 2008 a lot of money got injected into many economies across the globe to “save them’, most common inflation measures were pretty reasonable through a lot of it, but asset prices started to explode. That would suggest to me a “Top X%” of the population was getting to that money, which makes sense because if you’re worth millions you won’t all of a sudden buy 100x the eggs you’d normally buy or 20 Toyota Camrys just cause. It doesn’t look like that to me now, and with higher prices expenditures are up.

That’s the way I’m reading this anyway. Ofcourse in my close circle of blue collar friends/family I know limited numbers of people making more money to keep spending normally but some are and do, I’ve definately cut back.

Wolf,

Thanks for the snarky reply that didn’t answer my question. The question I asked very simply was, what % of individuals have seen an increase in their real income?

Not households, not wealth, not what arbitrary segmentation.

Individuals. Percentage of the total.

LOL, I didn’t give you a percentage figure (such as 86.98%), but I told you that the biggest percentage gains were at the lower end of the pay scales, far outpacing inflation, and I explained why. You need to wrap you brains around that.

Just got a quote Wednesday for $5100 for home insurance that cost us $2400 last year. I almost crapped myself.

Looks like we’re gonna have to do some shopping.

Where?

Yep, I know someone who has a similar scenario in Colorado.

Investors are prone to behave rashly when interest rates fall below a certain level. A desire to maintain the income of their investments induces them to speculate. When government bond yields fall below average investors take on more risk. They won’t accept a loss of income. Their propensity to assume risk moves inversely with the interest rate. Risk-taking becomes extreme when bond yields fall below 3 percent–not the 2 percent level. My take away is that inflation should be stabilizing–at least in relationship to interest rate income. Monopoly pricing and private market failures can give inflation a boost. Strong regulation can mitigate that problem. But we no longer regulate.

Your long lost cousin (Rachel Wolfe) at WSJ agrees =)….:

Americans Are Still Spending Like There’s No Tomorrow

Concerts, trips and designer handbags are taking priority over saving for a home or rainy day

Consumers should be spending less by now.

Interest rates are up. Inflation remains high. Pandemic savings have shrunk. And the labor market is cooling.

Yet household spending, the primary driver of the nation’s economic growth, remains robust. Americans spent 5.8% more in August than a year earlier, well outstripping less than 4% inflation.

These figures shows that the Sailors keep adjusting themselves to the rolling waves of the sea of inflation.

A great learning academy Wolf.

This is one of the most consistent learning site with a dedicated moderator and followers.Thank you all

Looks like we gotta have unemployment to stop the borrachos spending

government spending, I think, is up to about 25% of GDP, US has a budget deficit of $2 Trillion and now rapidly rising bond yields leading to rapidly rising interest costs to future deficits.

My doubt is the sustainability of this aggregate spending.

My presumption is that underlying this surprisingly strong spending is an underlying weak artifice of unsustainable government spending.

And thus can’t go on, therefore US growth is unsustainable.

What is your take on that Wolf?

Or are you thinking you’ll cross that bridge in your analysis if and when the government gravy train is actually impeded?

Government gravy train impeded? What?

Breaking news from Babylon Bee:

Congress Passes Trillion Dollar Stopgap Bill That Will Fund Government Until About 2 PM Tomorrow

How much of this spending spree can be explained by the fact that the primary beneficiaries of QE have not yet experienced the pain of QT?

I was also wondering how all this spending is related to the [3 trillion?] deficit spending sloshing around?

Country Clubs FULL…..with waiting lists

UAW and others striking…

nuff said.

Catillion was correct

That was caused by the last of the stimmy money. It is now gone.

Note the first chart — that’s income “without transfer payments.” Stimmies were transfer payments, so they’re excluded from this chart. That’s why I post this chart, and not the overall income figures because, in 2020 and 2021, they were massively distorted by transfer payments, including stimmies and forgivable and forgiven PPP loans.

As much fun as it is to say the word “stimmy” I hope to never see one again…

I understand “income” is excluding transfer payments (transfer payments are not included in income). However, it can’t exclude savings that is a result of transfer payments. Meaning, people spent their savings, from transfer payments, into the economy. Right?

Age will take care of the drunken sailor syndrome, not to worry!

When young, I was the biggest fool on the planet with money.

Now old with no one left to spend it on, my savings instruments

have become my children, my dividends and interest their off-spring

which I tend lovingly with MORE savings instruments. My great-niece, who was a recipient of my largess for her college graduation, never even bothered to acknowledge it, let alone thank me. What can I conclude other than she is so well-fixed by her parents that she doesn’t need or appreciate it and I won’t do it again. My monthly income only increases every month. It’s a new world indeed. My world is still the post-Depression world of the 1930s, and wars which left ugly scars

Dude, that is so freakin’ depressing, it’s unbelievable. I always wonder about leaving for my nieces should I not have children. But as much as I love them, they never say thank you when I give them presents.

Not sure I get the nuances of everything you’re saying, but that one sure hits home.

Adopt an adult or elderly pet. It will show love and gratitude and you seem to be able to handle the inevitable vet bills better than most people.

The drunkest sailors are the elected folks in Washington, D.C., are they not? The Debt Clock ⏰ shows $1.922 trillion so far this year. The government’s deficit is our surplus, am l not right?

If the US government continues to behave like the government in Weimar Germany in the early 1920’s, should the results be any different?

Both parties went all in on free money for everyone. It’s going to be hard to break that habit, despite what they say now. Will the Fed buckle under political pressure once again as well? I want to believe no, but we know how fickle and entrenched in the system the are – when their wealthy friends and their gilded lifestyle, and the revolving door between the two groups is threatened, will they still have the same resolve?

Other commentators have opined elsewhere that the rise in interest rates benefits the rich at the expense of workers…

Most rich people are just better with money, or at least have the self control to not spend it all and also get financial advisers to help out, if needed. You play the game based on the cards you’re dealt (stocks or bonds or cash, etc. )

“Other commentators have opined elsewhere that the rise in interest rates benefits the rich at the expense of workers…”

Those “opiners” should spend as much time analyzing how many of those folks got *rich* to begin with – and then try to emulate that behavior – as they do demonizing people more prudent than they. They might just learn something.

That’s one of the problems for people who choose to frequent “echo chambers” where they hear their same thoughts consistently repeated. They’re comfortable in that environment, but they also learn nothing in the process. You can toss out all the “yeah, buts” you want, but every generation has been served their own crap sandwiches…. Some prospered and others did not. There’s been stories of the “millionaire next door” for as far back as I can remember. It’s not a new phenomena.

Digger Dave-

You said: “Will the Fed buckle under political pressure once again as well?“

I agree with your skepticism about the Fed’s resolve in tackling the inflation problem. But I’m not sure I would characterize their attempts to control the economy as buckling to “political pressure.”

From the Fed: “The Federal Reserve Act mandates that the Federal Reserve conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.””

Summary:

1. Max employment

2. Stable prices

3. Moderate long-term rates

Powell and the Fed are responding to a lawful, but terribly misguided triple mandate from our lawmakers. It is the LAW that is bad, and to which they respond when they take actions Fulfilling all three mandates on an ongoing basis is impossible, and attempting to do so got us painted into the current corner we’re in, as well as similar problems in past decades.

Under current law we ask the impossible of the Fed. The law and the Fed triple mandate need to be reviewed and reformed.

The only issue is that QE was pulled out of their @sses during the GFC, which was a wholly political step – buckling to the pressure from politicians and the extremely wealthy in a way that was not previously viewed to be within their responsibilities. And then again counterproductively lowering rates due to the heckling of the President. And finally, because no one seriously questioned their newfound QE and ZIRP orthodoxy, going all-in on steroids due to COVID. A responsible Fed would have stayed out of all three messes using traditional tools and left the pathetic free money approach to Congress.

So no, I have little faith that the next crisis will not give them an excuse to go back to their newfound ways.

Borrowed money is NEVER ‘free money’ and always has to b e repaid with interest.

Tell that to the people who got PPP “loans.”

Loans to students and 3rd world governments would appear to be the exception.

On occasions I have loaned money expected to be repaid with out interest. So far it always was repaid.

I think about an old gentleman who carried a bible on his car’s dash. The bible had an untold amount of money in between the leaves. When a person needing money asked he would open it and select an amount to be given. I never heard of any who did not return the favor.

This was many years past when one’s car was never locked.

Borrowed money is free money if the real interest rate is negative. (Interest rate – inflation rate).

The manipulation of price discovery in debt markets via quantitative easing (QE) in order to cause negative interest rates is the point of QE. That was what the Fed was up to.

Well, if you die with a huge debt, no one will go after you to collect the money.

The Fed will always buckle under enough pressure….

Spending habits remain ingrained for quite some time before people finally realize they have to pull-back. Credit is the main factor that facilitates this reality.

If as is concluded above, income has grown faster than inflation, I would temper that with the reality of the huge level of economic disparity we have in the US. All have-to-have services have jacked up compensation big time, but nice-to-have, struggling I believe. And of course, those on the higher end with financial assets have been able to earn quite a bit more via higher interest.

Without government deficits and support for the low earners in our society, all hell will break loose. It already is manifesting in major cities if anyone hasn’t noticed. So the big deficits are key to keeping a lid on this boiling pot we call our economy.

If the upcoming government shutdown succeeds in slashing budgets, we are in for a rude awakening.

Hooch from Federal Reserve distilleries has no hangover possibilities, На здоро́вье!

I was asked the other day when I thought something was going to “break” in this economy. I of course didn’t have an answer, and now this article makes it clear that economists and The Fed have no idea either. Wow! Drunken Sailors keep saying “Pour me another, Cheers!”.

The economy will break when the Dollar loses it’s reserve status.

And when that happens, all bets are off, and the ugly will be Yyuuugggeee!!!

There are lots of reserve currencies. The dollar is the biggest by share of total reserve currencies, the euro the second biggest, the yen the third biggest. Read all about it here:

https://wolfstreet.com/2023/07/15/us-dollars-status-as-global-reserve-currency-on-slow-long-term-decline-but-not-going-down-in-a-straight-line/

Here is the share of the top reserve currencies — you people have zero patience. The dollar’s share is declining at snail’s pace. You need to look at it in terms of years and decades, not next month or next year. And what currency is going to replace it 🤣?

Chinese fortune cookies🤣

$20 per hour minimum wage coming to California and workers will still only be able to live at home with the parents. The Fed will have to work harder to break inflation by creating a recession that puts $50 per hour workers out of a job. Then they can get $20 per hour jobs. Is that the recession safety net?

In Manhattan the middle class threshold is factually (maybe not academically) 300k/year. And most of those earners have nothing to show for it at the end of the year.

I picture rats on a treadmill wearing business attire…

kra – …’faster rats’ replaced with treadmill racing? (…the Peloton or similar thing is starting to make more sense to me, now…).

may we all find a better day.

No surprised at all. Everything is going well. We are in an economy where money is depreciating its value every individual day. Nobody wants to hold money. Everyone wants to hold assets, goods and debt instead. As real value of the debt goes down every time fed prints money whereas the real value of everything else goes up.

*Nobody wants to hold money. Everyone wants to hold assets, goods and debt instead.*

*But people are still earning more than they’re spending. Personal saving was $794 billion SAAR in August; the personal saving rate was 3.9%. So the money for all this spending comes from all this income. And the savings keep growing.*

Are government savings growing?

The title of the article is

*Our Drunken Sailors*

and for their savings.

NOT for the government savings.

Laughably false. The US Dollar is soaring upwards and the prices of most of the world’s 28 commodities are falling substantially.

No, bitcoin is 5 times higher when compared to 5 years ago. RE is doubled in 5 years. Stocks are similar. All asset prices are went up like crazy in 5 years, which means the real value of the dollar has reduced dramatically. Some other currencies lost even more.

BitCON has no value and is nothing but a speculative fraud and complete and total Ponzi scheme. Most stocks are down very significantly over the past 5 years, and in case you haven’t heard, most of the ‘value’ (price appreciation) in the markets comes down to only about 8 stocks, and most commodities have been plunging in price over the same past 5 years during which the value of the US dollar has been very stable and constant – which, of course, is the goal and purpose of a currency.

Bitcoin plunged 60% from Nov 2021. Neither stocks nor residential RE plunged that much. Some parts of CRE maybe

Who is this “nobody” that doesn’t want to hold money? I think Wolf has more than adequately described the cash reserves of the American population and pooh-poohed the notion of “most Americans can’t pay for a $400 emergency”.

The nobodies that make up your “nobody” list are nobodies because they don’t understand the basics of running their life as a business. The ones bemoaning that “it’s only going to get more expensive” are the ones who are creating the environment where everything DOES get more expensive due to their excess spending on stupid things they don’t need and have a value of bupkus when things turn (and they do). Key “$100K pickup truck” violin and the 3 year old used car they bought for more than the sticker price of when it was new.

The economy is doing well but it’s dependent on a rising debt/GDP ratio, $2.5T deficits, and stock/RE markets that stay extremely overvalued.

All that is meant as to the word ‘economy’ is GDP which does not take into account the principles of assets and liabilities and therefore is a totally irrelevant and meaningless construct.

GDP is a measure of FLOW (spending and investment, money changing hands).

Assets and liabilities are a measure of STOCK (like inventory).

On financial statements, there is a statement of flow (income statement) and a statement of stock (balance sheet).

GDP does not measure value as it purports to but rather merely measures spending…

Wolf, with income level rising, do you think inflation will start going up? Friday’s PCE report seems to indicate that inflation is going down.

Let’s hope the public housing authorities’ budget doesn’t get cut.

“The 2024 President’s Budget requests $73.3 billion for the Department of Housing and Urban Development (HUD), approximately $1.1 billion more than the 2023 enacted funding level. “

The FED never took the punchbowl away.

1) The sticky inflation started to deflate. The unions herd together,

imitating each other, flexing their muscles for the first time in fifty years.

2) They built a bubble, a strike bubble. They extrapolate previous inflation to the future.

3) The biggest strike will start today after midnight. Millions of US gov employees will get an IOU or be out of work.

3) Shame on those who misbehave and refuse to lift the debt ceiling.

4) The buck stops at the Biden’s desk. Eventually he will have to settle with the other side. It will be brutal. Unfunded entitlement promises will deflate.

1) The Real Personal Income excluding transfer money is rising in a

turtle speed. It’s up from 15.56T in Oct 2021 to 15.7T in Aug 2023, up

135B, or 0.85% in two years.

2) But the Real Disposable Income is 16.76T. Down 3.66T since Mar 2021.

3) Consumers lost 3.66T / 20.42T = (-)18% of their Disposable Income

in two years. They are worried and angry about it .

“Real Disposable Income is 16.76T. Down 3.66T since Mar 2021.”

1. The dollars you cite are not actual amounts per month, but “annual rates” for each month. So divide them by 12 to get a feel for actual amounts.

2. In 2021, it included the stimmies, PPP loans (forgiven), and the all the other transfer payments that consumers got.

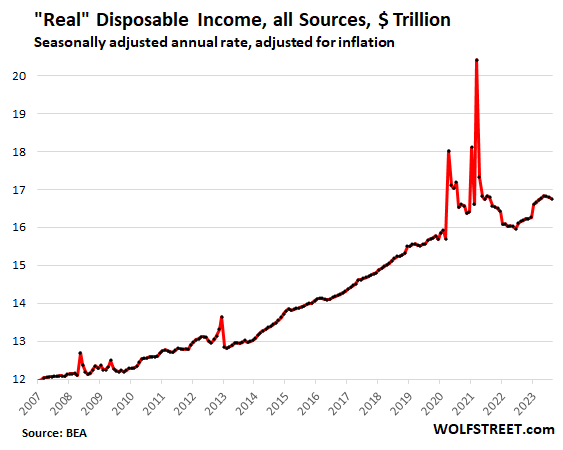

The charts that include those transfer payments (total income and disposable income) are totally nuts, made nuttier because the data is in “annual rates,” which multiply one-month events, such as stimmies, roughly by 12 to show what it would be if consumers got those stimmies at those amounts EVERY month for an ENTIRE YEAR. These are the most useless stupid charts, which is why I no longer use them, and instead I use the data without transfer payments.

So here it is, “real disposable income” expressed in “annual rates” (LOL) including transfer payments, such as stimmies. Just nuts and stupid and useless:

Color me skeptical, but I don’t have a lot of faith in “government numbers”.

Have they lied before?

Is it in their interest to lie?

“Faith” is something you deal with in church. This is data, not God. You want 100% certainty, go to church.

Consumer price index numbers are real and not manipulated. On the other hand the way the CPI is assembled may have some shortcommings. One pointed out by Mr. Wolfe with his Toyota Camry and Ford Picup truck price index.

Another thing to be aware of about the CPI numbers, they are a snapshot. The CPI is one possible snapshot, change something in the methodology and there is a different snapshot. I wouls say probably equally correct.

Then, due to the methodology the point of view changes over time. An example, today mobile phones is part of the CPI, fifty years ago they where not. Changing consumer behaviour will over time change the CPI as much as changes in prices. After all the CPI put weights on each item depending on how much consumers spend on that type of items.

Last, CPI number can not be used for “what if” calculations as a change the price of one item changes the CPI itself.

The house just caved…..again…… and passed a 45 day extension……but of course included is an additional 16 billion for disaster relief…….I suspect the senate….after much posturing will go along.

Yep……we stand at the door to higher rates and inflation…..so let us help you by goosing another 16 billion.

It’s like the the horses on the stagecoach are being whipped while the dude in the coach with the babe sitting next to him (Powell) is holding his hat out the window to slow things down.

Powell just paused rate hikes. He isn’t holding his hat out the window, he’s whipping the horses himself.

Senate just passed it. Ukraine funding was stripped out of it, but word is Mccarthy is expected to advance a separate Ukraine aid bill in exchange for getting the votes to get it through Congress today. This country is a dumpster fire. I don’t think we will get away with the out of control spending much longer. We are used to getting our way, so we expect it to continue, but I think those days are numbered.

Weren’t they saying the extension won’t even cover 45 days though? That was the first claim when they started discussing the amount a week ago but US deficits are exploding so fast now, yields are rising it’s looking like it won’t cover more than around 35 days or even less than that. It’s why the extension bill was stripped so bare and doesn’t actually cover much of anything that was being debated. So Congress is fast under pressure to figure out the budget and the knives are already coming out again. And McCarthy is probably toast as speaker, he’s pulled off something unique, made himself hated by all sides.

1) The Fed wants your money. They get u in the roach motel by hiking to 5.5%. There is no more stimmie money, after the raids.

2) No PPP loans, no shingle mums, rent, student loans…

Consumers got their money in several pulses when US econ was comatose. The System Control with the positive feedback loop stopped working after 2020/2021 for two years :

Student loans have to be paid. Rent popped up. C/C to 30%. Mortgage rates at 7%. Car price. RE prices… gov debt at 34T up from 10T in Q2 2008.

3) The upper middle class and the rich funfunfun, but the rest are struggling, because their Real Disposable Income, – monthly adjusted annual rate, – is down.

4) Congress kicked the can down for another 45 days, but they can’t stop the strikes bubble.

I am having trouble reconciling the notion that credit card debt is also soaring to record highs, surpassing $1 trillion.

Income is increasing and so are credit card balances (ave rate 20.53%).

Inflation.

This is much cited ignorant BS. Credit cards are the dominant consumer payments method in the US. $5.76 trillion in payments were made in 2022 with credit cards. Each of the other payment methods (debit cards, ACH, checks, cash, etc.) lagged far behind credit cards.

That $1 trillion in credit card balances = the statement balances. But most of the credit card balances are paid off the next month and never accrue interest.

Growing credit card balances show increased SPENDING (in part due to higher prices), not increased interest-bearing debt.

Most consumers with credit cards collect their 1% or 2% cash-back, or their double-miles, or loyalty points, or whatever, feel good about the kickback, and pay off their cards by due date. And there is no interest to be paid.

Credit cards are not primarily used as a borrowing method, but as a payments method.

Only about 28% of adult consumers (18 years old and over) have one or more cards with interest-accruing balances.

Read this before you abuse my site to spread ignorant BS:

https://wolfstreet.com/2023/08/19/how-many-americans-have-interest-bearing-credit-card-debt/

https://wolfstreet.com/2023/08/08/our-drunken-sailors-still-not-getting-in-trouble-with-their-credit-cards/

I am trying to understand how all of the numbers work together and not trying to spread any information. It was more of a question than a statement. Sorry if it came out that way.

Brian,

No problem. I’m just really sick of this “consumers sinking deeper into debt” stuff on CNBC, Bloomberg, et al.

I have written about this once a quarter for while, when I cover credit cards.

That 28% is an interesting number.

Adding in the unsecured loans based on the same TransUnion report, I’m calculating around 36% of adults paying monthly interest.

260 — million adults in US

518.4 — credit cards

166 — people with a credit card

3.12 — ave number of cards per person 518.4/166

43% — cards pay interest

222.91 — million cards pay interest 43% of 518

71.38 — million people with card balance 222.91/3.12

27.45% – adults carrying a balance (close to 28% cited by Wolf)

22.5 — million adults with unsecured loans (from TransUnion)

93.88 – million paying credit card interest and loans 71.38+22.5

36.1% of adults paying CC or loan interest 93.88 93.88/260*100

(This is back-of-napkin math and may be inaccurate.)

I’m seeing recently ACH payments getting 2-3% discounts off payments by credit card. My medical policy, a mailing service I use as 2 examples.

I’d rather do that especially on recurring payments than get some cash back type deal on a credit card.

Yes, got a $25 a month Comcast special for broadband. Only way they do the special is with ACH. Beats cash-back by a factor of 10 or so, LOL

My PG& bill is also ACH.

Glad companies are getting smarter about credit card fees.

There’s a little extra risk attached to automatic ACH payments since that’s direct access to your bank account, but not nearly as risky as checks, I hear (I’ve never had a problem with any of them).

It’s really simple: as long as the government is running gargantuan deficits and the banks – “helped” by the central bank – or the rest of the world Finance them, that debt/money has to end up in the private sector. It’s simple balance sheet arithmetic. Then it’s up to the private sector to either save/invest or spend. In the US, it’s “spend” and “speculate”.

It’s a hand-to-mouth economy with the hand being government deficits and the mouth being the casino.