Massively inflated during the pandemic, corporate profits are still not normalizing, and bode well for future investments and economic growth.

By Wolf Richter for WOLF STREET.

So I’ll just start with this, and then I’ll follow with the essential nitty-gritty:

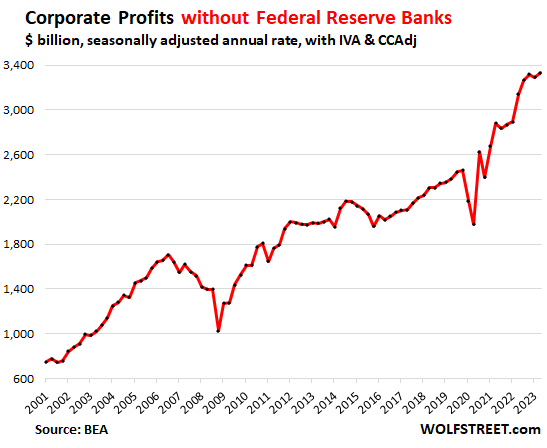

“Corporate profits” (all businesses that file corporate tax returns, including LLCs and S corporations, see nitty-gritty #2 below) before taxes (nitty-gritty #3) and excluding the Federal Reserve (nitty-gritty #1) but with “CCAdj” (nitty-gritty #6) and with “IVA” (nitty-gritty #7)…

…rose 1.3% from the prior quarter and 6.2% year-over-year, to a seasonally adjusted annual rate of $3.33 trillion in Q2, the highest ever, driven by record profits in nonfinancial industries. according to the Bureau of Economic Analysis today.

Corporate profits: no recession on the horizon.

“Profitability provides a summary measure of corporate financial health and thus serves as an essential indicator of economic performance. Profits are a source of retained earnings, providing much of the funding for capital investments that raise productive capacity,” the BEA explains in its methodology.

You can see in the chart above how the Great Recession was preceded for a whole year by a decline in corporate profits that started in Q4 2006. The Great Recession began in December 2007.

The nitty-gritty about “corporate profits.”

1. What the heck is the Fed doing in here? Well… The 12 regional Federal Reserve Banks, on whose financial statements the Fed’s profits are accounted for, are private corporations and are therefore included in the headline figures for corporate profits by the Bureau of Economic Analysis. The Fed has been losing large amounts of money by paying out more in interest to banks and money market funds than it earns in interest on its still vast but shrinking portfolio of securities. But in terms of profits from current production by US businesses, the Fed’s profits or losses are irrelevant. So I exclude them here (and I rail about them there).

2. A broad measure of business profits. “Corporations” is the term used by the BEA for all entities that are required to file federal corporate tax returns, including private corporations, LLCs, and S corporations, plus by some organizations that do not file corporate tax returns. So this is a very broad measure of business profits from current production.

3. Before income taxes: by measuring profits before income taxes, it eliminates the effects of changes in tax policies.

4. Before capital gains received & dividends received. By eliminating capital gains and dividends received, the measure shows profits from current production, rather than financial gains.

5. Based on corporate tax return data and financial accounting data. The BEA obtains this data from the IRS and from financial accounting data of public companies, and it combines and adjusts the data.

6. With capital consumption adjustment (CCAdj). Tax-return measures of depreciation (based on historical-cost accounting) are converted to measures of consumption of fixed capital, based on current cost with consistent service lives and with empirically based depreciation schedules.

7. With inventory valuation adjustments (IVA). An adjustment to corporate profits and to proprietors’ income in order to remove inventory “profits” (company buys a widget for $1, and after having it in inventory for a month, the supplier raises prices by 20%, and now the value of the inventory jumps to $1.20, creating $0.20 in profits from inventory, with a related increase in sales price), which are more like a capital-gain than profits from current production.

So, OK, now….

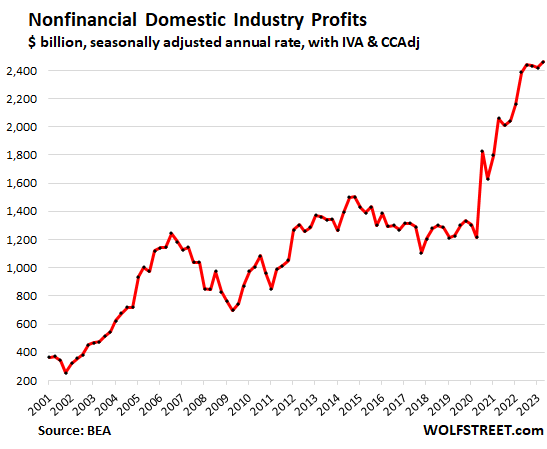

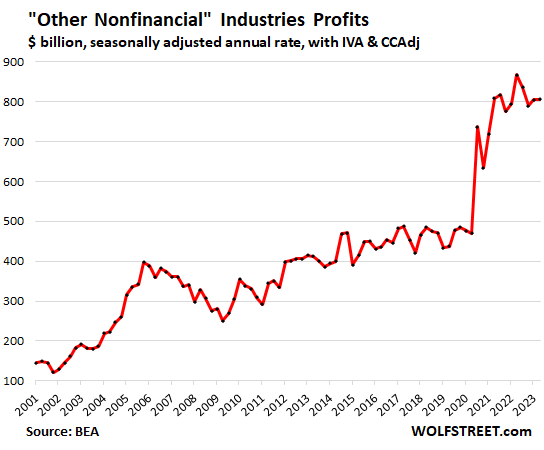

Profits by nonfinancial domestic Industries.

Nonfinancial industries include Utilities, Manufacturing, Wholesale trade, Retail trade, Transportation and warehousing, Information, and Other nonfinancial (a huge category we’ll look at in a moment).

Total profits in nonfinancial domestic industries rose by 1.8% for the quarter, and by 3.2% year-over-year, to a record seasonally adjusted annual rate of $2.46 trillion. This does not include foreign profits by US companies.

Profits have doubled from 2019! This stuff is just astounding when you look at it:

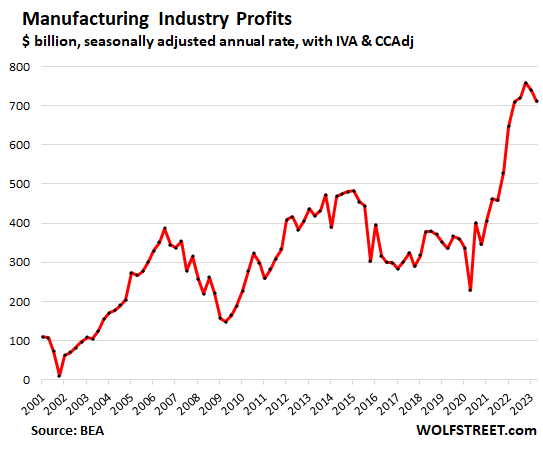

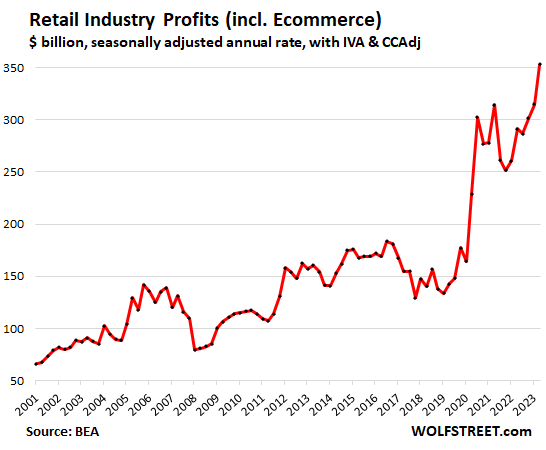

The three largest nonfinancial categories by profit:

Profits in the manufacturing industries fell 3.7% for the quarter, but still rose a hair year-over-year to $711 billion seasonally adjusted annual rate, the second quarter-to-quarter decline in a row, after the gigantic spike during the pandemic. Profits remain extremely high.

Profits in the retail trade, incl. Ecommerce, spiked by 12.1% for the quarter and by 21% year-over-year to a record $353 billion seasonally adjusted annual rate. Just astounding, in part because retailers’ costs have gone up more slowly (or actually fell) than they’d jacked up their prices:

Profits in “Other nonfinancial” industries was roughly flat for the quarter and fell 7.1% year-over-year, after the gigantic spike during the pandemic.

This is a huge category that includes mining; construction; real estate and rental and leasing; professional, scientific, and technical services; administrative and waste management services; educational services; health care and social assistance; arts, entertainment, and recreation; accommodation and food services; agriculture, forestry, fishing, and hunting; and other services, except government.

These kinds of charts show just how distorted pricing and sales were during the pandemic.

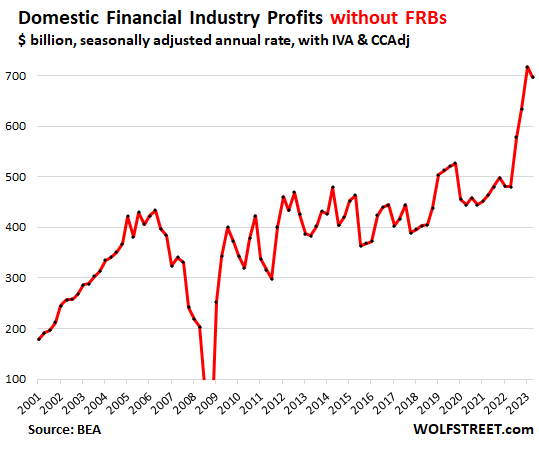

Profits by financial domestic Industries.

This includes all financial companies except the Federal Reserve Banks, so domestic profits from banks and bank holding companies, other credit intermediation and related activities; securities, commodity contracts, and other financial investments and related activities; insurance carriers and related activities; and funds, trusts, and other financial vehicles.

Profits dipped by 2.8% for the quarter, but were still up by 45% (not a typo) year-over-year after the huge spike in profits in 2022 and Q1 2023. Remember, this is profits without dividends and without capital gains and losses (nitty-gritty #4), but profits from current production.

Another nutty pandemic-era financial-distortion chart:

So what we can see here is that corporate profits were massively distorted during and after the pandemic, with price increases far outstripping cost increases, and that they should be normalizing — meaning, dropping back to trend — but in Q2 were still not normalizing, far from it. And these profits bode well for future corporate investment and expansion projects – fueling more economic growth from the business-end of the economy.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I am in manufacturing and I approve this message.

Great article. Thanks much. Lately your content is the only stuff I’ll read. Market Watch etc. is plain crap. I don’t think the younger anylysts etc. get the bigger picture. They are bogged down with a lot of “I don’t even know what to call it”. I have also noticed that financial planners are starting to behave like Traders, at least with the speak I hear out there

This has been an interesting time for me personally. I’ve been a professional Trader since 1996. Thousands of trades; even the times when you called in every order and had a satellite dish that when the snow came you had to go brush it off. Thanks again for your bright insightfulness.

“Market Watch etc. is plain crap.”

SoCalBeachDude – please take notice and stop copy-pasting MW headlines here!

🤣

I’d rather he stick “MW” headlines here than “DM” headlines. Lesser evil?

MarketWatch (MW) is owned by DOW JONES just like The Wall Street Journal and has many EXCELLENT AND TIMELY articles on an array of financial topics every day, just as does Daily Mail (DM) which is the largest news publication in the world and has superb in depth coverage on many financial and other topics.

there is no point of copying just the headline – from any source.

We come here for insight/ideas.

And please no excerpts from EWI :)

More ammunition for unions and workers to win big raises, which is inflationary.

The price gouging by corporations is inflationary. Workers are merely trying to maintain their lifestyle.

“Workers are merely trying to maintain their lifestyle.”

Perhaps some of them, but I’m not sure a 46% raise and 32 hour work week qualifies.

46% would qualify just fine. I’m on the market for another jet sky. Planning for two-month paid vacay. Like in France.

The 46% raise is likely from levels set years ago, before the 20% inflationary spike of 2020 to 2023. So, it’s a reasonable ask for a contract covering several future years.

Why in hell not? How does one single individual qualify for a 29 million dollar annual compensation package?

It’s all unhinged — so why not.

Don’t forget $1 Trillion on credit cards, $1 Trillion in car loans, and a $Trillion or two in student debt. Gotta maintain the lifestyle.

High interest rates have not slowed down discretionary spending.

Carnival Cruise lines recently reported Record sales

Total bookings hit a 2023, Q3 record of $6.3 billion, surpassing the previous record of $4.9 billion from 2019 by 28%.

Wow. 28% Better yet. 2024 looks to be even better. They must be putting people on cots as occupancy rate is 107%.

—————————–

Carnival’s occupancy rate returned to “historical levels” and improved to 109% from 84.2% last year. Analysts expected an occupancy rate of 107.4% for the quarter.

“The outperformance was driven by strength in demand, with both our North America and Australia segment and Europe segment equally outperforming across expectations,” CEO Josh Weinstein said in the release. Weinstein noted North American bookings are exceeding historical highs and European brands achieved its pre-pandemic levels.

“Our booked position for 2024 is further out than we have ever seen and at strong prices,” Weinstein said.

—————————————

Its a self-fulfilling prophecy: workers get a big raise and spend more, which puts upward pressure on prices, causing them to rise etc.

Not making a moral judgement, just thinking about the mechanics. Obviously we’d all like more money.

Yes, I don’t see any recession on the horizon either. Recession is not a good thing as it increases unemployment. But as long as they are mild, they eliminate unproductive and reckless business and improve the productivity in the long term. I see some mild recessions as minor fires that serve the well being of the forest.

We should accept that the FED eliminated any risk of potential recession on March ’23, by raining money from the sky (again), at the expense of persistently high asset prices and stubborn inflation. Thanks to this decision, instead of a recession, we are in an obese economy now: High consumption, high wealth disparity, high asset prices, low productivity, low equality.

China should be criticized in many aspects (especially human rights), but for the economic policies, at least we need to give them that they act more wisely by allowing reckless and unproductive companies to fail, instead of inflating their assets by printing large sums of money. They don’t have the problem of inflation, but they are refusing to print like crazy.

I don’t think you ever visited China. Go visit Xinjiang.

These are nominal numbers . Inflation adjusted profits are down and margins on revenues are down. Also it is too selective to include higher net income from banks without recognizing losses on their asset/liability mis-match. Bank shareholders have less real equity now than they did a year ago.

1. “Inflation adjusted profits are down and margins on revenues are down.”

Being silly? Corporate profits +6.2% yoy in Q2. DOUBLE yoy CPI at the end of Q2 (+3.1%).

2. “Also it is too selective to include higher net income from banks without recognizing losses on their asset/liability mis-match.”

Nonsense, part 1. Look at “nonfinancial profits” — second chart from top. It doesn’t include banks at all. And they hit a record. Financial profits (last chart) actually dipped a little.

Nonsense, part 2: That may factor into a decision whether or not to buy bank stocks, but not everything is about stocks, and this here has zero to do with stocks, though your text tells me that’s all you’re thinking about. Stocks can go to hell, and they ARE going to hell, while the economy can still do just fine.

This is profits from “current production” — that’s the recession indicator, not a stock market buy-sell signal, and it doesn’t make one iota of difference if bank stockholders lost their shirts.

You need to look away from stocks for a few minutes every now and then. It’s good for your health 😎

Amen brother Wolf !

Higher for longer is the Fed story at the moment the 10 year hit 4.69 during intraday trading! Probably a 15 year high ! Stock prices and profits can be decoupled for decades

Reminds me of the famous imploding stock prices from unprofitable companies maybe Mr Issac can explain those charts .

“You need to look away from stocks for a few minutes every now and then. It’s good for your health 😎”

Amen!

“…but the casino has ALWAYS had an open bar! (…hasn’t it???)”.

may we all find a better day.

“Corporate profits +6.2% yoy in Q2. DOUBLE yoy CPI at the end of Q2 (+3.1%).”

But are official inflation numbers representative of real inflation?

There is no “real inflation.” Everyone has their own inflation rate, depending on where they live, and on their life style (what kind of goods and services they spend much of their money on). So what we’re looking at here are summary figures that show overall trends.

But there are newsletter-mongers and others out there that try to scare those who cannot do even basic compounding math with stupid inflation rates year after year. If you know how to do basic compounding math, you can destroy this BS in a NY minute, and I have done it here publicly a few times — which turns out to be a waste of time because people who cannot do compounding math and believe in BS don’t want to see their beliefs destroyed, and refuse to see it. So fine with me.

Rear view mirror. What will Q3 Q4 be with higher energy prices and a pullback in spending?

Q3: we already have a feel for spending growth from the data so far: pretty good.

Q4: we’ll start finding out over the next few months.

Higher energy prices mostly don’t cause a “pullback” in overall spending, they shift spending. Prices always do that; lower or higher prices shift spending.

Profits will continue to increase for a while until cash runs short since, even if inflation goes to zero, prices (and profits) for virtually all goods and services are substantially higher than pre pandemic and not headed down until after we DO have a recession, whenever that may be… post election?

1. October shutdown + November Pivot = Another bull run

2. People in my swamp area are already booking vacations on anticipation of a shutdown.

3. Now feds are raising rates. At some point they must pivot and reduce rates. Why sell or cause recession artificially.

4. My bank (a big one) still refuses to increase rates for savings account. I buy T-bills anyway.

5. Before I was born, fed rates were very high > 10%, still corporate were able to make profit. USA was manufacturing back then.

6. This growth may not stop or we can redefine it.

Pivot. Lol.

Funny how they claim the economy is booming, so the Fed will pivot this year. There’s some sort of disconnect

The Fed is not going to pivot. ZIRP is done, get over it & get on with your life.

CSH-

You imply that ZIRP is done “forever” then?

I’ll take that bet if you’re offering.

I bet a pal back in mid 1990’s that we’d see 10 year treasury at 4% some day. Enjoyed a wonderful porterhouse steak at his expense not too many years later. He foolishly neglected to put a time limit on it!

Forever is a long time.

John – I’ll take the that bet if *you’re* offering. I’m 33 and don’t believe I’ll see zirp again in my lifetime. The 40 year bond bull market ended in 2021.

MM, I think youre wrong. ZIRP is a terrible policy, but the rich made trillions off it for 14 years. They are going to pressure and work to get fed chairs who support ZIRP back in office likely for the rest of forever. The cost of ZIRP is not paid by them, so they dont care. If every decade and a half someone needs to raise rates slightly to pretend to fight inflation after they quadruple their wealth, so be it. I think we are going to see cycles of ZIRP multiple times. And every time they will say “look how the markets and housing exploded! Things are better than ever!” and every time the homeless population will grow.

I should add I would absolutely LOVE to be wrong about this. But Im not going to pretend these people work for us.

That’s an odd bet. The 10 year treasury was above 4% every day throughout the 1990s.

I think I got the direction of the interest rate backwards. The trend was certainly in your favor in terms of rates going down.

@Herpderp

What are your thoughts on NIRP. Negative interest is even crazier than ZIRP. Europe had over 8 Trillion bonds at Negative interest rates a few years ago. Get paid to borrow money. LOL

That in theory should boost spending?

MM

Let’s get the bet specifics down:

1. Statistic = FFR

2. Payoff trigger = 0 – 0.25% or less

3. Effective Deadline = the first date of death between the two of us. If the rate has not declined to the trigger before then, then the bet is canceled (unless you can think of some way for us to settle collect settlement from the others estate).

I propose we bet a 1/10th oz. American Eagle, worth approx. $200 in 2023, as representing a dinner for 2 at a premium steak house in today’s dollars.

ZIRP is bad for the dollar and the country. It always has been. But if we get another selfish idiot in the white house to press the Fed to do his bidding (which is unethical), we’ll have it again. You’d be wise to try to hedge your bets. No one knows what is coming.

We had ZIRP for 14 years and you blame one guy? LOL

So companies can easily afford and need to pass on a significant share of the gains to workers hammered by inflation. Wages need to go up for people just to get even.

“So companies can easily afford and need to pass on a significant share of the gains to workers”

Depends on the company. Whether they should or not is a different matter.

So message is: Buy equity.

That’s not the message at all. Equity is incredibly overvalued, which is why stocks have dropped since their peak in late 2021. They dropped not because the economy is bad but because they had been driven to ridiculous highs by 14 years of QE and interest rate repression, and now we have the opposite, QT and much higher rates, and that’s what caused stocks to drop, not the economy, which is doing fine.

The only reason ‘the economy’ APPEARS to be ‘doing fine’ is due to the vast government overspending of more than $2 trillion a year just on the federal level which is now hitting a brick wall and impeding federal government shut down and federal spending is now about 44% of US GDP is which an outrageous record high.

Yes, government deficits are a huge problem for current inflation and future government finances, but they do stimulate economic growth, and economic growth is what we’re talking about here.

BTW, no one knows how to turn off that spigot. A government shutdown just puts a bucket under the spigot, and when the shutdown is over, the bucket, which by then is full, gets poured out into the economy, and the spigot keeps running. That’s how it always happened.

They will break through the brick wall after a little bit of a scare. They will make superman look like a weakling. We will see $50 trillion of debt by 2033. Congress has spending superpowers. :)

What ever you want to call it that being played out be it inflation or depreciating currency. Prices will continue to go up because of government debt. What will be very interesting in a couple of years when the FED will have to buy the excess Government debt because they will be issuing so much it will be more than the public can absorb. Just look at Japan as a playbook.

In theory, the longer the economy holds up, the longer the Fed can continue with higher interest rates and QT, so the more asset prices can be suppressed before the Fed pivots to lower rates.

So actually, this strong economy might kill the stock market before the economy softens.

But looking forward, we DO have student loan repayments starting (or is did that get put off again) so forward-looking there is a reason to be cautious on revenues and profits. I keep hearing companies announcing softness in their unit sales.

Pure wisdom served up fresh daily.

If the economy needs $2 trillion of deficit spending to eek out real GDP growth of 2%, then we’re in trouble

God, get over it. This is one of many things wrong with this country, the obsession with the casino.

We could have nuclear warheads headed our way, and the first thing many will worry about is what nuclear fallout will do to the casino. I can see it now, Nick the Pig will tweet ” good news, the Fed will have to pivot now.”

I’m so sick of Wall Street.

Be selective on equity. As Wolf warns, U.S. markets are overvalued. I like overseas equity. It is not near as inflated as U.S. equity. It also will benefit when the dollar eventually falls. Finally, China is making progress and Xi is talking about pumping the economy and growth. That and the U.S. will add to growth everywhere.

Some observations and comments on this information:

– The BEA must be relying on other data sources than just the IRS for 2023 as most companies have not reported any business activity to the IRS yet for 2023 (given that most companies utilize a traditional calendar year end for tax reporting). Are they also pulling information from public 10-Q filings for Q1 and Q2 2023 for their assessment? If so, this may skew the results somewhat as it captures information from public companies only (for 2023).

– Remember that while the income statement or P&L represents the source of this information, two other financial statements are equally important to understand – the balance sheet and cash flow statement. As for the balance sheet, remember this is where cash goes to die, losses go to hide, and the BS goes to lie. I’m not saying that companies are intentionally inflating earnings but in my experience, losses tend to “catch-up” (and are finally reported in the income statement) when financial stress levels begin to elevate which we are just beginning to see as a result of increasing interest rates, QT, and other factors. Trust me when I say, its amazing how fast inventory loses value, receivables become uncollectible, hard/soft capital assets are abandoned, and previously unforeseen liabilities begin to amass, all triggering losses.

– As for the recent record profits, actually, this is not a surprise given the massive combination of monetary (think QE/Fed balance sheet expansion and zero interest rates through 2022) and fiscal stimulants (think PPP, ERTC, loan deferrals, record current deficits, etc.) provided to the economy over the past 3+ years. As a reference point, per FRED, the measure of M1 amounted to $4 trillion as of 1/20. This ballooned to $20.6 trillion as of 2/22 and has only begun to recede to $18.3 trillion as of 8/23. Too be quite honest, it would be almost impossible to have not increased profits over the past three years given the levels of monetary and fiscal stimulus injected into the economy. If the Fed and federal government are going to really tackle inflation (which I don’t believe they want to do as it is easier to inflate away old debts), a coordinated effort will be needed to decreases federal spending, accelerates QT, contracts the money supply, and yes, forces a nasty recession on the economy.

– On the inflation front, anyone who thinks that the FED can “tame” inflation over a relatively short period (i.e., 12 to 24 months) without the benefit of a deep recession occurring is delusional. Looking back at the fact pattern starting with the end of the Great Recession, it took over a dozen years of massive increases in federal deficits/debt levels, damn near close to 0% short-term interest rates, a FED balance sheet that ballooned from $2 trillion in early 2010 to a peak of $9 trillion in 2022, and in the end, having to resort to “helicopter money hand outs to the masses” via all kinds of federal programs to finally ignite inflation and let the beast out of the cave. Thinking that inflation is going to be tackled over a one to two year period after the run-up and “juice” provided since 2010 is a fools’ errand. Its going to take years if not a decade to normalize the Feds balances sheet, money supply, and federal spending.

– One final comment/question – Wolf, can this information be translated into real/constant dollars and earnings? It would be interesting to evaluate these trends without the impact of inflation.

Just my two cents but from my perspective, the earnings information presented is a trailing indicator (in the current environment) as the overall economy has not yet normalized to a real/true economy, one that is not addicted to monetary and fiscal stimulus (which has clearly been the case over the past 3 years).

“– One final comment/question”

Stock prices are not adjusted for inflation, nor are stock indices, nor are cooperate revenues. So why should corporate profits suddenly be adjusted for inflation?

FYI: corporate profits +6.2% yoy in Q2, CPI yoy +3.1% at the end of Q2.

Rates were under 4% and oil under $65 for Q2.

“two other financial statements are equally important to understand – the balance sheet and cash flow statement. As for the balance sheet, remember this is where cash goes to die, losses go to hide, and the BS goes to lie.”

Exactly. Any accountant worth his weight understands this. I would go even further and state that the balance sheet is a far more incisive view of the financial health of a company.

The balance sheet is a statement of condition on that one day at the close of business (for example 6 pm on Dec 31). The income statement is a statement of flows over the entire time periods, such as Oct 1 through Dec 31. So don’t get too hung up in nonsense.

Wolf. I’m going to call you out on this as remember, of the three financial statements, the income statement is the easiest to manipulate. The advice I always give to people is to understand the income statement, trust your balance sheet, and most importantly, rely on the cash flow statement (as this really helps readers understand how cash is generated and consumed in a business). Yes, the income statement is a measurement of profit and loss over a period of time but if the balance sheet is misstated, so is the income statement.

If you would like to challenge me on my expertise with financial statements, please feel free but I would recommend you research my credentials first as trust me in my 40+ year career, I’ve more seen more BS in financial statements than 1,000 people in their lifetimes.

You can manipulate the balance sheet just as much as the income statement. A company blows up, and while sorting through the debris, they find that the balance sheet assets were full of hot air, that loans were still carried at full value years after the borrower had defaulted a long time ago, and that trade accounts payable were actually financial debt (undisclosed reverse factoring), etc. This happens all the time. And we have covered some of those balance sheet implosions here. Then look at the Fed’s operating losses, over $100 billion of them: they’re parked as a negative liability on the balance sheet. Goodwill is an asset that includes losses that have already been incurred but not yet recognized on the income statement. Etc. Balance sheet and income statement go hand in hand, and you can do anything you want to with them. That’s why there are auditors who are supposed to see to it that the manipulations stay within the FASB standards.

Very well explained. Nothing organic going on. Just massive wealth transfer from a virtual banana republic. End stage. Q4 23 results start to show reality. World of swimmers swimming naked. Imho whoever is lending on RE now will be bankrupt

whether investors, wall st, banks or Washington. Country riding only now on one last thing: its established good faith which is gone imho. Last stage is chaos and anarchy. Target closing stores due to theft? Already started. Massive homeless and massive immigrants overloading cities? Im expecting Government shutdowns and sovereign defaults. Anyone can make a ledger or a chart to fit their narrative. China is a master. But you can turn a blind eye to reality only until you can’t. So says the unadulterated math(truth).

Management Bonuses are tied to reported profits.

I think that is enough of an explanation.

Unless something blows up, it looks like rates are staying “high”. Are 8% mortgages coming soon? That would mean the 30 year bonds would pay at least 5.5%; no?

Yes.

imagine the SHORT opportunity on the 10yr german bund….2.92% currently! LOL.

I’m predicting 8% 30yr morts by the end of this year.

Mortgage rates are based on the 10yr. Roughly 80% of mortgages refi or sell before 10 years.

This basically means much higher for longer.

A lot of people thought that this much high rates would break something badly. But here we are, nothing is broken, except inflation which hits the poor the most.

Also, mortgage rates need to go much higher.

I think taxing back the printed money where it lands would achieve the goal quicker than higher rates.

FED doesn’t have the right tool to fix the problems they caused!

Costco is destroying your printed money and exchanging it for ounces of gold.

Haha what a world were living in.

“I think taxing back the printed money where it lands would achieve the goal quicker than higher rates.”

Been loving this concept for awhile. Especially all (ALL) PPP money.

Gattopardo

You point to something I worry about. Real estate taxes.

If the UAW receives their request we can expect every union to follow suite. This increase in wages will have an enormous increase for government public union employees pay. In other words all real estate taxes will increase hugely. Only way to pay the increase.

How will this be handled by the poor, much less the middle class in the mansions they own.

Down below Wolf wonders how we turn off the spigot?

Well if memory serves me correctly thee House controls the purse strings. Exactly what a group is attempting now. If a shutdown occurs we must not pay any worker that is nonessential! This would be very painful, no doubt, but how else can spending be reduced?

After this point many other projects will need to be reduced spreading the pain.

Yeah. too late as most of the PPP windfall money has been spent/invested. But we are still juicing the economy with IRA money, while trying to cool the economy with higher interest rates?

In the kindest way possible in response to Softtail Rider you’re delusional. The rich spent the past 3 years robbing the rest of us blind under the guise of “inflation” (yes, some costs did increase, but not in proportion with prices – if they did would we have seen record breaking profits over and over?) and now normal people want a piece of the pie and *thats* a problem?

No. Normal people want their fair share. That means a 40% wage increase to counteract a 20% increase in prices that’s already happened + continuing inflation that’ll take time to abate. The Obama admin recovery was so anemic and ineffectual because they threw lots of supply side stimulus at greedy companies that pocketed it and didn’t do anything. Remember telecoms getting billions for network improvements that they didn’t do?

No, the cause of the inflation problem is squarely at the feet of the greedy people running these companies. The solution is not to destroy millions of lives through a second great depression, it’s to support unions as they fight for a more equitable allocation of resources and pay. You can’t solve a supply problem with decreased demand, and you can’t solve a greed problem by enabling more greed.

@Naren,

“The rich spent the past 3 years robbing the rest of us blind”

Where do people get this crap??? Or maybe all my rich, philanthropic friends missed the “Greedy Screw the Normal Guy” meeting? Give this class warfare garbage a break.

“Normal people want their fair share”

There is no such thing as “fair” share. No one is owed anything. Supply and demand for labor. Simple as that. Just because cost of living goes up doesn’t mean anyone’s (and I mean ANYone’s) compensation should go up. Those are two separate things.

You’ve got to be kidding me. This is the problem with short memories. We’ve had a banking crisis just recently where the fed had to step in and essentially guarantee all deposits and backstop banks that were carrying devalued paper.

It would have been catastrophic if they didn’t but once again new precedence is set without second thought.

It is broken now. Credit markets are starting to freeze. look for a deep dive in Q4 23 results if you can find any unadulterated results that take debts into account accurately. Just one news event now, any certain one, could start a full blown panic now.

Howdy Folks and Lone Wolf. More proof higher for longer is Higher for forever? THANKS

My personal take on what might be adding to corporate profitability.

1. Our benefits have been reduced substantially, including healthcare. Premiums have gone up a lot and some 401k contributions from the companies have been reduced. Recently, in my own company (and several others I work closely with) the companies do not pay for unused vacation (except for CA and a couple of others where it is mandatory). If you are fired or quit, good luck getting paid for unused vacation.

2. Monopoly could possibly be driving some of the profits as some smaller players were wiped out. We see this with banks.

3. There is still a lot of Covid money out there, and students were splurging like crazy during the moratorium.

4. I work with people who have not gotten a raise in years. Some younger folks who were hired during the pandemic make as much or more than those with several years more experience.

Retailers are still pouring it on to the point some items are ridiculously high cost. Beef keeps inching up. Couch food snacks and drinks of course keep going up because of their popularity and American tradition. Freetos are darn well worth $7 a bag, corn shortage or not. 60% paid for by food stamps.

Brant – remember that retailers must buy every item on their shelves from a wholesaler, with the same issues as the ultimate consumer (Henry Ford at one point sought to ameliorate this by owning his supply chain). Wholesale costs are always a pressure point. Without a buyers’ strike from consumers, retailers will always charge ‘what the traffic will bear’, especially if not offset to some relative price stability by broad-based competition (always good to review the history of anti-trust emerging from the Gilded Age, here, which spawned not only the anti-trust movement, but the labor union, socialist, and communist movements (again, Tuchman’s ‘The Proud Tower’ remains an accessible read).

may we all find a better day.

Wolf :

Please do add a plot of corporate tax revenjue from 2001 to present.

Then look at the ratio of that tax to profit.

Here is just 2 points

2006 Q3 : 380B/1750B (tax/profit)

2023 Q2 : 403B/3375B

They are making out like bandits and not paying back to tax. No wonder the budget deficit is going to sheesh.

Yes, that’s an ancient problem. Corporate welfare state. The bigger the corporation, the bigger the welfare queen.

“They are making out like bandits”

Many would argue it doesn’t matter. Eventually those earnings get taxed either at source or as dividends to shareholders.

My instinct is that your numbers are skewed because you are using a numerator based on the tax definition of profit and a denominator based on the GAAP definition of profit. Mixing apples and oranges.

Take $2T of government debt out of this economy and see what corporate profits will do.

Yes. But no one knows how to turn off the spigot. So it’s not going to happen. We might dream about it, but it’s not going to happen.

“Massively inflated during the pandemic, corporate profits are still not normalizing, and bode well for future investments and economic growth.”

Such a statement on the surface looks depressing and will contribute to an overheated economy; therefore, inflation. However, there is hope that all that money will go into stock buybacks pumping up the elite, and the companies will still be saddled with enough debt to keep their “zombie” title. Also there doesn’t seem to be anywhere near the corporate basic science research of old, so these companies should slow into a “buggywhip” obsolete fate again helping reduce inflation.

Its called a sovereign default. I expect it at some point as the last only option. Trump even alluded to it.

“Sovereign default” CANNOT happen with a country that controls its own currency and that borrows in its own currency, such as the US, Japan, China, etc. It can only happen to countries that borrow in foreign currency (Argentina borrowing in USD) or that don’t control the currency they borrow in (Greece borrowing in euros).

What CAN happen to countries that borrow in their own currency is INFLATION (some call it a soft default).

Hopefully a catalyst forces us to take it out. I think it could happen and pray for it.

If everything’s so awesome, let’s see more rate hikes and a lot more QT.

Enough of this pause and pivot baloney.

Your data support my notion that banks make a lot of money off of stupid customers. These are the ones who stick with .01% APY on savings, who pay overdraft fees, who do not pay off their credit cards on time, who withdraw from bank money market accounts more than six times a month, who pay big early withdrawal penalties on CDs, who buy bank CD’s at 4.5% or less, who have to pay for a new book of checks, who pay a fee for a bank “financial advisor”, and on and on with seemingly never-ending fees. The spread (difference in the borrowing and lending interest rates) must be enormous now. Now they just need to find enough suckers to take out loans.

And yet all the commercials say “let us handle your money, you live your life!”

And some orange bunny hops out. Like WTH? Is OSU celebrating Easter here?

Went to my credit union yesterday, and the only product they offer yielding >5% is a 13-month CD @ 5.25 apy. Disappointing.

When I mentioned to the teller that I was considering moving money out and putting it in a MMF, she got rather defensive, trying to convince me that a couple % higher apy wouldn’t make me *that* much more in interest.

The early withdrawal penalties on CDs are sometimes draconian. Why lock your money up in a bank when you can get 5.40% at SWVXX or VMFXX which you can get anytime you want for no penalty? I suggest everybody to get a brokerage account. You can buy T-bills and CDs (which have no early withdrawal penalties), meaning you can sell them when you want, although maybe at a loss or at a gain. I use Schwab. Vanguard’s web site is too flaky for me. I imagine Fidelity is adequate. I don’t know about the rest.

I concur. Schwab scalps a decent little bit off t-bills but it’s nothing to get bothered about. And you can buy at auction scalp-free. No reason to buy CDs as t-bills yield the same +/- and are state tax-exempt, and zero credit risk.

This must be the Greed Indicator. I cannot wait to see this next year.

We’ll all be talking about being in the R… oh don’t say it! And these (bad) numbers will have CEOs apologizing and blaming the “perfect storm no one saw coming!”

My fingers are crossed.

$7,000,000,000,000 Cantillon Effect.

Woocoodanode?

CONgress.

It would be useful to see graphs of profits as a percentage of revenue. Although profits have doubled in some cases, revenues have increased by 30% or more. Likely much more than 30% for e-commerce.

This is irrelevant here. If you want to look at corporate performance, look at SEC filings. This is an indicator of the economy: future business investments funded by retained earnings from current operations. That’s why this data series exists.

Corp profit stalled @$3.4T. SPX quarterly 3M is a trigger.

Recession risk is high !

RTGDFA. Corporate profit rose to a new high. See first chart!!!

Hi Wolf.

While these corporate profits figures are rising, bankruptcy filings are also rising to record levels. My inference would be the data is skewed by the large companies siting on big pile of reserves (just like the savings data of citizens).

Just based on chart observation the profits reversion to the mean and bottoming in 2007 probably took around 3 years. This might take even longer this time may be half a decade or more. Probably a longer business cycle and recession much farther away?

Would be great to know your thoughts on this?

Thanks.

Sandy,

Nah. The companies that file for bankruptcy now are zombies — deep-junk rated companies — that have not made a profit in years, and many have never made a profit, and they haven’t made enough cash flow to pay even their interest, and they have to borrow money to pay interest, which is why they’re deep-junk-rated, and they have a huge pile of debt, which is also why they’re deep-junk-rated. And now credit costs are rising, and the zombies are taken out the back and shot. That should have happened years ago, and just free money kept them alive. That’s a good thing. The fact that they haven’t made a profit in years kept them out of this profit data for all these years. They don’t play a role in it.

Enriching corporations at the expense of future generations. As long as the government runs such huge deficits they have to show up as private sector surplus.

The bond market is sleeping. I wonder why long yields aren’t up that much? Maybe there is just too much liquidity still out there to support asset prices.

Somethings eventually got to give. Some area of the market is going to end up with huge losses. Likely bond holders as they have been through centuries. But likely this time they will be responsible for it…..for buying long bonds :)

Agree with Wolf here that the likely outcome of such fiscal spending is that the economy does just fine but asset prices fall, bond losses become huge and future bond holders insist on higher yields putting a stop to fiscal spending…..and boom we then finally have a recession.

” As long as the government runs such huge deficits they have to show up as private sector surplus.”

Exactly. There’s no miracle here, just simple balance sheet arithmetic. Add infinite tax loopholes and financialization and you get a low productivity, sticky inflation, inflated asset price economy that -in the case of the US – only still “works” because of the reserve status of the dollar and the US dominance in financial markets. Nothing to cheer here. That US debt is still rated AAA is laughable. But the Bond market is waking up, see the last two weeks. You ain’t seen nothing yet. At 5% for the ten year this market will break.

US debt is rated AAA because, by definition, the US cannot be forced to default on debts denominated in $USD.

Just want to commend Wolf for his work. It is unique and practical.

Wolf separates news from noise which is valuable to everyone.

I’ve been involved in the markets in a professional capacity since the late 1970s, retired for awhile now but still following the market closely.

This is useful to me.

Thanks Wolf

Point taken.

But was any of this data adjusted for inflation?

I now see you addressed this .

longstreet,

Are corporate revenues adjusted for inflation? Are earnings adjusted to inflation? Are stock prices adjusted for inflation? Are stock indices adjusted for inflation?

What is this BS suddenly about adjusting corporate profits to inflation? This has been brought up a billion times here. Suddenly everyone wants to adjust profits to inflation because they cannot handle that profits are still rising – it somehow goes against your narrative?

BTW: Corporate profits +6.2% yoy; CPI at the same time +3.1%. So there.

Wolf: It appears price gouging (using inflation as an excuse) is Just one reason. Many corporations got rock bottom loans during pandemic because of ZIRP, bought back stocks to juice up the income and the peasants went and spent because their stonks went up. Known as positive feedback in engineering controls area, that is unhealthy (can explode). Similar to homeowners sitting on 3% home mortgage. All financil engineering (a young guy who became a billionaire using FE while promising drugs for diseases wants to be our leader and teach everyone how to become a billionaire). So recession has taken time to arrive and would have the same explosive positive feedback effect when it arrives — unless of course, FED doesn’t come up another $500B or more to prop up the

“Many corporations got rock bottom loans during pandemic because of ZIRP”

Not only that – but they’re now earning a much higher interest rate on their cash. I recently read an article explaining that corporate interest income is at record highs because of this.

But I doubt that shows up here: nity grity #4 says these figures are before cap gains and dividends, which I assume includes interest income.

Zoom has almost 5 billion dollars in cash. Interest on that income alone is enough to pay their workforce.

It sounds like corporations are being smart and engaging in “in substance defeasance” where they buy high interest treasuries to pay off their lower interest corporate debt. Both the debt and treasuries are kept on the balance sheet until the debt would need to be refinanced and then the principal from the treasuries is used to pay off the principal.

…pay off the principal on the debt.

Certainly the extra cash being pocketed by corporations gives them the ammunition to increase investment. But higher interest rates reduce their incentive to do so. The smart corporate response to the temporary excess liquidity in the economy is to raise prices and then use the proceeds to pay down debt to avoid having to refinance at higher rates.

I think this is a reflection of the US business model compared to the rest of the world. Compared to heavily regulated and centrally planned economies, the independence of US companies speeds up reactions to macroeconomic changes.

Thank you Wolf for cutting through the Noise with your hard data approach. We all appreciate it.

I’ve been an avid reader for a few years now, but cannot recall seeing this metric here before. I would love to see this analysis added into the normal rotation with the QT/fed balance sheet, Fed policy updates, “splendid” housing bubbles, wealth disparity updates etc.

Seems like a great indicator of where the overall economy is headed.

Thanks again!

It’s new. And it will show up again, don’t worry.

Fantastic! Thank you

Great information that, I suspect, The Fed is also looking at. Why? Simply because the pandemic gave cover for the first real experiment in issuing a tremendous amount of currency and handing it out to the population.

The pandemic gave cover for this, as well as new data on how much the average American is willing to subject themselves to government decrees (i.e. control).

The smart money profited from the rush to online retailers, but interesting times non the less. Very interested in seeing where the American housing market goes now with all these “refugees” flooding across our southern border.

Interesting times.

1) Corp profit has been rising in three waves since 2001. The last wave is

vertical.

2) Corp profit suddenly collapsed, without warnings, in 2006 and in 2019.

3) They might be decimated by gov shut down, strikes, higher wages,

higher interest rates, higher energy, higher RE, struggling consumers..

4) CA 20/hr junk food workers wages might finally eliminate the standard American diet.

“2) Corp profit suddenly collapsed, without warnings, in 2006…”

That WAS the warning. A little over a year later, the Great Recession began.

Williams just stated that interest rates are at a peak…….I guess he just can’t stand the pain of only 5 job offers instead of 9.

Is this the pivot……

or another crooked bubble head just blathering away for a couple grand of spending money on a Friday in order to get his options in the money before the end of the day.

I vote for number 2.

If unemployment claims drop any further my dead mother is going to have to get a job. I guess the PCE of 3.5% was the target all along. Sarcasm.

These guys are a bad joke…….I just wished their trades were really banned. Which son or daughter put thru the buy this time.

I guess these profit charts explain the crazy small gap between investment grade bonds and junk.

Interesting. Thank you. Your data shows Corporate profits increased by a 7.3% cagr the last 23 years. That roughly matches the s&p return. Sure we have selected Bubbles but it looks like over the long term profits are matching the market growth.

How much has debt gone up the past 23 years?

Atlanta GDPNow’s Latest estimate: 4.9 percent — September 29, 2023

The economy is accelerating.

GDP is consumption. Specifically government spending, consumer spending, private investment, and net exports. We are having massive government spending in 2023 and since 2020. That’s why GDP is up. It will keep going up a lot as the government keeps spending a lot. This isn’t news.

I bet that extra two trillion they’ve been spending per year since 2020 has nothing to do with these stubborn indicators…………..

Wolf is starting to sound a little like Jim Cramer of CNBC’s “Mad Money”.

Everything is rosy, profits are up, the economy is booming,

It’s time to

Buy, Buy, Buy!

No, but higher for longer plus QT.

You don’t get it apparently though I have said it a million times: QT and higher interest rates are the forces that push down asset prices, not a lousy economy. So we have a decent economy and falling asset prices because of QT and higher rates.

Wall Street wants a recession more than anything, and the recession-mongers are everywhere, in the hope that the Fed drops the rates back to 0% and restarts QE, and you’re falling for this BS.

Looks like Isabella Weber’s “price setter’s inflation” to me.