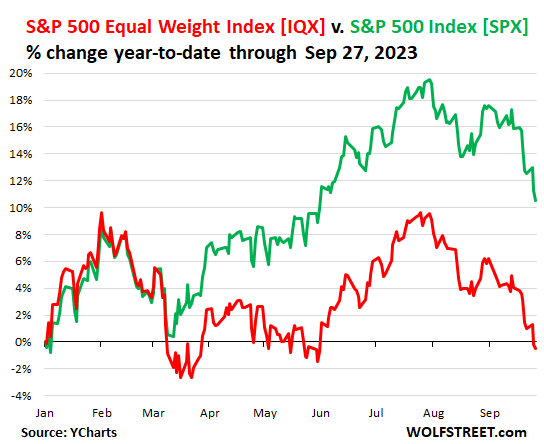

QE giveth, QT taketh away. The two sucker rallies this year of the S&P 500 Equal Weight Index got wiped out.

By Wolf Richter for WOLF STREET.

Stocks in the S&P 500 Equal Weight index [IQX] are not weighted by market capitalization. It contains the same stocks as the S&P 500 index, but each stock weighs the same within the index. The purpose is to see if the performance of a small number of stocks with huge market capitalizations is driving the overall index and is in effect hiding what is happening to the rest of the market.

The S&P 500 Equal Weight index today fell into the negative year-to-date (-0.6% YTD at the moment), after having dropped over 9% since July 31. It thereby has totally wiped out the two big sucker rallies this year (red line in the chart below).

- sucker rally in January through February 2 was wiped out by mid-March

- sucker rally from mid-March through July 31 now also wiped out.

But the market-capitalization-weighted S&P 500 index [SPX] is dominated by 8 companies with huge market capitalizations that account for 29% of the index. Those eight stocks have experienced a massive run-up this year through July 31 amid the tech and AI hype-and-hoopla show. That rally has only been partially wiped out. And those companies carry the S&P 500. Since July 31, the S&P 500 index has dropped 7% but is still up 10.5% year-to-date (green line):

The sucker rally starting in mid-March was fueled by the $400 billion in insta-liquidity that the Fed threw at the banking sector over a matter of weeks. The Fed has now drained that $400 billion, plus it has drained another $318 billion with its record QT. Since peak-balance-sheet in April 2022, its assets have dropped by nearly $1 trillion.

The top 8 companies by market capitalization in the S&P 500 index that account for 29% of the index include these standouts:

Nvidia [NVDA] spiked by 244% in seven months from January through July, amid the glorious AI hype-and-hoopla show. Since July 31, Nvidia has dropped 15%. But it’s still up 193% year-to-date. It weighs 2.9% of the S&P 500 index.

Tesla [TSLA] exploded by 171% from January through July 18 and has since then dropped 18% but is still up 119% year-to-date. And it’s still down 43% from its all-time high in November 2021. Tesla weighs 1.9% in the S&P 500 index.

Meta [META] spiked by 162% from January through July 28, and has since then dropped about 10%. It’s still down 24% from its all-time higher in September 2021. Meta weighs 1.9% in the S&P 500.

Apple [AAPL] surged 57% from January through July 31 to a new all-time high of $198.23, and has since then dropped 13%. But it’s still up 36% year-to-date. Apple weighs 7.1% in the S&P 500 index.

Alphabet’s two classes of shares, [GOOGL] and [GOOG], have a weight of 2.13% and 1.82% respectively in the S&P 500 index, giving the company a combined weight of 3.95%. It surged by 55% through September 19, but didn’t get back to its all-time high, and has since then dropped by 6%. Year-to-date, the stock is still up 45%. From its all-time high in November 2021, the stock is down about 13%.

Because Alphabet is listed as two stocks, the 8 companies consist of 9 stocks that make up 29% of the S&P 500 index. The right column shows the year-to-date gain at the moment:

| Top 8 Companies by market cap in the S&P 500 Index | Weight | Gain YTD | ||

| 1 | Apple | AAPL | 7.1% | 36% |

| 2 | Microsoft | MSFT | 6.5% | 30% |

| 3 | Amazon | AMZN | 3.2% | 45% |

| 4 | Nvidia | NVDA | 2.9% | 192% |

| 5 | Alphabet Cl A | GOOGL | 2.1% | 45% |

| 6 | Tesla | TSLA | 1.9% | 119% |

| 7 | Meta Platforms | META | 1.9% | 134% |

| 8 | Berkshire Hathaway Cl B | BRK.B | 1.8% | 15% |

| 9 | Alphabet Cl C | GOOG | 1.8% | 45% |

| Total | 29.1% | |||

The top-heaviness of the S&P 500 makes the overall stock market indices and funds that track them immensely vulnerable to a deflation in just a handful of the tech-bubble stocks.

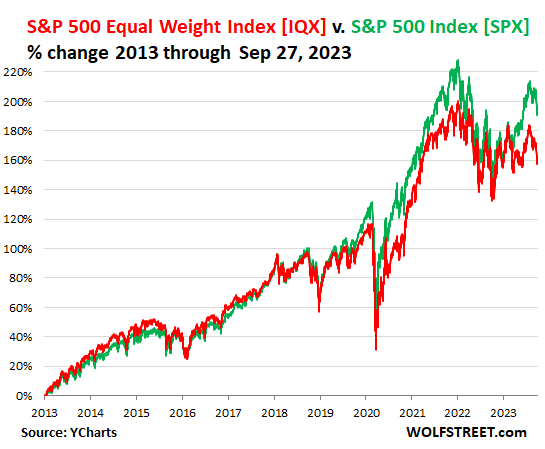

The peeling-away of the S&P 500 index from the S&P 500 Equal Weight index took form in 2018 as the entire world focused their investments on just a handful of US stocks and drove their prices and market caps – and therefore their weight in the index – into the wild blue yonder.

The peak of the indices on January 3, 2022 occurred just after the Fed began tapering QE and after it put the first-rate hike in this cycle on the table for March 2022. QE and interest rate repression fueled this market, and now the record QT approaching $1 trillion and much higher rates for much longer are sapping the markets. QE giveth, QT taketh away.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

All that currency and stimulus has to go somewhere Wolf!

But I digress, if you are not a professional trader, or in the banking/finance/government club with access to inside information, then keep your “investing” simple; buy stock in companies that deliver services and items you use every day. Make sure they pay a decent dividend, have reasonable P/E ratios, and are well managed. If you are fortunate to “hit” some of those big gains, book some profits. Buy short term T-bills while you look for other entry points, and opportunities.

I have nothing but disgust for those who gamble/speculate and have turned the “market” into this lawless casino. That is NOT the role of an efficient market. No surprise the USA is no longer leading innovation globally. Gambling and financial “products” do nothing to advance our economy. More like eating your seed corn.

It’s the trading of the AI, by the AI, for the AI.

Imagine how dumb the average person is, and realize all of AI is dumber than that.

Who checks the work? Seems like infinite regress. And when it fails who’s to blame? It’s a great opportunity for c suite bozos to muck things up after promising magic. Update the resume, buy some Botox and move on down the line. Every day we thank these types for their superb efforts with phone answering robots.

program trading has been around for decades.

What is the difference between program trading and AI?

…another way to make a tool more important than the mission?

may we all find a better day.

“But I digress, if you are not a professional trader, or in the banking/finance/government club with access to inside information, then keep your “investing” simple; buy stock in companies that deliver services and items you use every day.”

How is that working for Intel and Cisco?

I don’t do big box stores, sorry. My servers also run on AMD chipsets…

Also Apple already said they will end intel support and all their computer will be using their “M” chips. Pay attention!!!

Also as I clearly state, there is a bit of timing as well. When you get a good run, sell, some and BOOK PROFITS!

LOL!

90% of stocks are owned by the top 10%. 99% of BTC is owned by the top 1% of BTC addresses. When the market is that cornered and you’re not in the club, you won’t do so hot and probably better off investing elsewhere.

Jesse Livermore “gambled” in the stock market and made really decent returns, in 1929.

Gambling has always been with us. The markets were never turned, the world was and continues to be a casino from the day the crust solidified…

Ha he did, and how did his story end?

+1

Livermore have not (mostly) gambled, but speculated. And there is nothing wrong with speculating. In fact, speculation is a necessity. And those who can’t tell a difference need to read a book or something.

And if you must short something, let’s not overlook Eli Lilly.

Speculation is indeed a necessity.

Speculators buy from those who wish to sell, and sell to those who wish to buy. Liquidity.

Only when they get “too big” ( a subjective measure for sure) can they distort. But they must always sell what they bought and buy what they sold (short).

Speculators attempt to predict tomorrow’s prices….and the ones who are adept survive and proseper.

Speculation is fine, so long as you don’t ask the taxpayer to BAIL YOU OUT when your “speculation” FAILS!!!

Are you really going to argue that free money hasn’t facilitated massive capital MIS-ALLOCATION?!? LMFAO!!!

Are you really going to argue we haven’t been socializing losses?!?! Again, LMFAO!!!!

WB – this.

may we all find a better day.

If US is not leading innovation, then who is? I can’t even fathom who you think is the global leader in tech and innovation.

The US may suck, it is sucks less than everyone else (just look at the USD). It is pretty easy to compete against socialism.

I’m no expert in the field of innovation.

That said, while patents surely dont tell the whole story regarding innovation they are relevant.

I read that the US granted about 320k patents in 2022. East Asian technology companies largely made up the top 10.

China granted about twice as many patents as the US in 2021 and 2022. FWIW.

…just because a nation has long led the way is no guaranty it always will. Laurel-resting, rather than steady, and critical, self-reflection leads to self-deception (in the words of R.A. Heinlein: ‘…the root of all evil…’).

may we all find a better day.

I remember what an eye-opener it was, years ago, when I learned how many more funds there were than stocks to invest in. All that unnecessary churn and trillions in commissions. Don’t forget, this is all included in GDP, just like a company that makes jet engines or trators.

You are making the fatally flawed assumption that the prices of any stocks — not just AAPL & co — currently bear any relationship to any value that might be present.

The entire stock “market” — analogously to craptocurrencies — has degenerated into a “greater fool” playground where stocks are bought in the hope that someone will buy them off you at later a higher price.

Plus a big component of machines selling to machines. What was the estimate of the proportion of pure computer-generated trading –75% if I remember?

I’m not sure that most people realize what Wolf tells us. They buy the Index thinking it is a stock market Index. They are fooled by a lack of information.

When did we get forced into 401K-land, anyway? When I was a kid “stocks” were seldom mentioned, and then it was “something rich people did”. We all had 2-3bed/one bath homes, 1000-1300 sq ft, 1 car, almost no wives worked (good union jobs for the old man) and we had the tax rates and gov’t business regulations the Roosevelts, Truman, and Ike left us, to insure we wouldn’t be forced into a Gilded Age and a depression again. And us hippies later decided even that was an planetary unsustainable level and we should ALL have a lot of fat trimmed off our lifestyles. Unfortunately we weren’t political, but greedy rich people WERE, and really got busy pushing all sorts of needless consumption/laws so they could all make EXCESSIVE AMOUNTS OF MONEY! Very sick….the American Dream is an admired psychosis.

Few understand how an index or a fund works, but are now forced into them, and FWIW;

Yahoo Finance just pointed out EXACTLY what this WS article does in an article TODAY.

His Rockefeller friend once told Bucky Fuller, “Why make business simple when you can make it complicated?” Modern Corporate Law now fits that wish….this article being an example.

Fuller also said, “All the real talent goes into the Arts and Sciences, and that leaves the DREGS to put it all together.”

Guess they went after education as part of their program….needed more dregs to change things back to the Gilded Age……which is the REAL MAGA program, and BSing the people was part of the program to get there.

When I was living on Haight St with the other hippies, a standard lament was that if things didn’t change, “ITT would some day have it’s own army.”

Like I said, we thought it was self evident we were right, and didn’t get political…..but the dregs did.

“the USA is no longer leading innovation globally” You must be joking or plain ignorant.

Just a reminder the average (however defined) can be either the most useful or most misleading statistic.

Sooo negative. Hey Bed and Bath is up 5 cents or 13% !

I feel a short squeeze coming. Might make a move.

Re: their symbol: BBBYQ, does the Q mean anything?

The correct term is BBBYQ+

ROTFL

Or it could be BBB’s new streaming service?

Seriously though, Q means the company is in bankruptcy.

Or it’s cooked….. (BBBYQ reads like BBQ)

Thank you, squeeze and what’s Q mean omfg lmfao

I thought it starts with 2S, as in two-spirit person. Could be totally wrong., sorry. Heard it in Canadian news.

Q means “in bankruptcy”.

That thing is a trap!

You’ll be able to buy it, and then one day your app tells you it’s frozen, and you can’t sell it until it goes for pennies on the dollar.

Thanks to all about ‘Q’ didn’t know that. Does Q+ mean extra BK?

I’m not sure that one reply grasped that my ‘enthusiasm’ for BB is of course sarc.

This market is just stupid and feels like ponzi scheme for the rich, sucker rally little peeps into hype big cap, pump and dump, rinse and repeat…

Another sign of stupidity and insanity, look at the many SPACS stock or the likes of Vinfast, WeWork..etc as Wolf pointed out many times here. Can’t help to roll my eyes hard enough everytime I hear MSM financial pundit talking about the market like it’s some wise sage with infinite wisdom..

…the heart and soul of every confidence man…

may we all find a better day.

Wolf,

Good, useful stuff.

I don’t think I saw the respective PE ratios listed…but they are a useful measure of “air” in a valuation.

Apple/MS/Google have (massive) real earnings…some others less so…

On the other hand, some measure of Apple/MS/Google mkt penetration (revenue to ? Ratio…) would be helpful too. 30-35 PE ratios don’t look horrific until you realize that A/M/G already thoroughly dominate their sectors…the 2x-3x normal growth implied by a 35 PE makes A/M/G look a lot more vulnerable (Is Google going to start building $50k homes? Is Apple going to build $1000 cars? Is MS going to patent a cancer cure?)

Giants can’t grow to the moon…if anything they stagnate and topple.

The concern with the big companies like Apple, Microsoft, Google, etc, is they become (if not already) monopolistic. As far as growth, it would be cantillon effect related. So moving away from business to consumers, to focus on B2B, and then more on govt contracts to get as close to the money printer. Consumers will start to matter less and less as they can just get massive govt contracts and with other businesses as needed.

P/E: Forward or trailing earnings? The former is a fantasy and the latter assumes no accounting shenanigans.

Trailing.

You are right about accounting scams but if the Endangered 8 are already doubly overvalued at an admitted 35 PE, overvaluation can only be worse at an honest PE (which would be higher).

The point is the general scale of the ZIRP’ed overvaluation (be it 100%, 150%, 200%, etc) – the exact amount matters less.

Decades of Fed/Wall Street stupidity (and half-educated 401k auto-destructs) have the equity mkts tap dancing in a mine-field…that is what matters.

Very interesting point. I didn’t know the details of the S&P index before. it would be very interesting to see the same thing for the NASDAQ, as most startups lost more than 80% value in last two years. I see no story pushing up asset prices other than the another round of money printing expectations from the FED.

On a broad perspective, unless the FED manipulates the asset prices by printing money and raining it from the sky whenever there is a minor liquidity stress, and lets the balance sheet roll down naturally instead, the asset prices (stocks, RE, crypto) should eventually go down. Even if the FED cuts rates in November (which nobody thinks they will do, including me) the assets will go down to healthy reasonable levels with a stable, determined QT. The only unpredictable variable is the FED’s money printing addiction here. Will they allow the reckless spenders and lenders fail and let a productive economy to take on or lead to obese economy with bubbles and hypes with no real productivity? Will see the answer in next 12 months.

I held all cash, no stocks. Would like to say no FOMO here, but I took a calculated risk and got out ahead. I am waiting for bargains in RE. Considered joining in with a friend’s group for hard money lending, but I am going to sit very still and watch carefully. Higher and longer message is starting to really sink in.

You can start seeing the cracks in RE industry in my big tech city. Nobody wants to show what the new comps are going to be. Lots of “Call the broker for prices” or “Negotiable” on the listings. Don’t want to jinx their listing. Certain asset types being carefully monitored as signals for comps with the new reality. Office and retail I feel really bad. Industrial mix bag and MF ok for now.

Raw land without entitlements, no dice. Refi in the next couple years will be bad. Have to wait to get a more clearer picture, but my CRE amigos are grim. Architects are nervous, watch their billable hours stats when the projects dry up. City is grim with their REET budget forecasts. But otherwise, lots of drunk sailors in my high tech neighborhood.

Houses in my neighborhood are still selling at list or above. Means nothing to me because I own my home and I am going to sit very still and watch. Or go to somewhere warm and chill for a few months and forget my troubles.

Stay safe.

So, I’m shorting s&p, the pe multiples of companies discussed are bananas, further as likely are the remaining companies in the s&p.

All these firms have been on a borrowing binge, with higher for longer and increasing interest expense, dropping margins I see all these guys PE multiples contracting from avg 23.4, if to median of 15, I’m hoping I see a 50% in value of my short etf.

I think 2023 so far has just been a massive bear market rally(from AI mostly) that has ended. The first big drop always gets that big bounce before the long downside of the mountain.

Where is Michael Engels with his Elliott wave number speak when you need him?

Patience. Oil prices and interest rates will eventually work their way into stock prices, real estate prices, etc. It’s just going to take a while – or a catalyst.

Govt shutdown? Some news event will do it but which one?

Wolf…… if you have a 7 year time horizon, would you dollar cost average into DIA or SPY or both ?

With a seven year time horizon probably better off dollar averaging into silver gold or Bitcoin…I don’t know if you read the article but it’s about inflated stock prices so the idea that over time they will continue to go up is the exact opposite take away of what you should be thinking from this article🤷🤦

Not again. What are these rocks you speak of? Gold and silver? Relics of a bygone age.

Nothing wrong with gold and silver, as long as you heed the old refugee’s rule: carry no more silver than you can run away with, and no more gold than you can swim away with.

Gold and silver are holy relics for some, and life’s too short to argue with true believers. Buy a little, put it away, and keep quiet about it. At present it’s not much good for anything except storing value over longer time intervals without significant counterparty risks.

Right from the article:

“The top-heaviness of the S&P 500 makes the overall stock market indices and funds that track them immensely vulnerable to a deflation in just a handful of the tech-bubble stocks.”

In my mind, laddering T-bills to chase rates higher is the better trade for a 7-year horizon.

Joe

Dca into stocks ready to decline is just a bad strategy, see how far they fall on fundamentals and shocks to come, then dca in then. Meantime short these stocks through etfs and them Park in short term treasuries.

I disagree w trope that u cannot market time, its a false premise. One can generally tell w rudimentary analysis that prospects for secular stocks are downside, wait for the drop then enter.

If you must dollar-cost-average into stocks, please pick smaller ones that aren’t abusing us all with their monopoly powers.

Also, when the rally finally resumes, the small-cap and mid-cap indexes will often outperform the behemoths.

Wolf,

How much of these gains for the big 8 have depended on stock buybacks? For example, FB announced 45 billion after the stock hit $90 (and then it went up to $300), Apple 90 billion in buybacks for this year.

How long do you estimate this can continue before higher interest rates and tax on buybacks put a stop to this charade?

I did some digging and I hope these numbers are accurate to illustrate the point.

– Apple long term debt for the quarter ending June 30, 2023 was $98.071B, a 3.56% increase year-over-year

-Microsoft long term debt for the quarter ending June 30, 2023 was $41.990B, a 10.72% decline year-over-year.

– Amazon long term debt for the quarter ending June 30, 2023 was $63.092B, a 8.68% increase year-over-year.

Stock buybacks are a huge driver in pushing up the stock price.

Go look at Dillards

Dillards stock in 2019 was 60. Now it is 334. It is up 350%. Guess what. They have not grown sales at all. Sales has not dropped but remained flat at 7 Billion the past 6 or 7 years. Income has not increased. But they take their profit and buy the stock back. Thus a constant income while the common share decrease means you have EPS growth YOY. Dillards Market cap is 5 billion on 7 billion in sales. The market does not go up….just the price of the shares. Actually Dillards Market cap was about 6.5 billion when the stock was at 60. The value of the company has shrunk while the stock has gone up over 300%.

If Macys would take their 800 million in profit and buy back stock they could buy back almost 25% of the company. This would cause the stock to jump at least 25% as long as sales and income stay flat.

“The value of the company has shrunk while the stock has gone up over 300%.”

Nothing necessarily wrong with that. With fewer shares remaining, each share represents a bigger piece of the company. The question is whether the buybacks were in the interests of shareholders. That depends on the circumstances.

How is a five-bagger NOT in the interests of shareholders? Especially in an obviously stagnant-to-declining industry and in comparison to the competition (Macy’s, Kohl’s).

Returning cash to shareholders is precisely what DDS should do.

Dillards had massive earnings growth, on a nominal and per share basis, so yes their stock would go up.

Sometimes offering shares to the public is good for business when it needs equity capital. Sometimes reversing that through buybacks is a good idea when there excess cash. It is highly unlikely that any business will generate the exact amount of cash it needs to reinvest in operations. And leaving excess cash in the business to allow management to engage in empire building rarely ends well.

Stock buyback use to be illegal, and for good reason. They were a large part of the stock market run-up in the 30’s. Here we are again…

Nothing wrong. I was just pointing out how stock buybacks and lift the stock price.

Some people think that a company is growing if the stock goes up. Not the case.

I read that 20% of the rise of the S&P 500 over the past several years can be contributed to stock buybacks.

Companies have a choice of taking the profits

1)buying back stock,

2) Pay dividends

3) M&A

4) expansion

Buying back stocks is the most beneficial return for executives who typically have stock lots of stock options or RSUs. Stock options and RSUs do not pay dividends.

Personally, I am not the fan of shares buyback. On most instances, corporate America uses debt to buyback own shares in order to artificially propping up share price. Corporate executives enjoy the windfall while the company suffers eventually. How many cooperation are using their own profit to buyback share?

When the sales stagnant, rate environment getting tighter like now, the refinancing of bond surely getting hit. But these executives already pocket what they looted earlier and company share crash. They are not responsible for any of these consequences of their making. This is the game average Joes are playing now with the Casino stock market.

Good catch on the FB buyback…they got nailed early circa Nov 21 and it is hard to see their actual market (advertising) going gangbusters anytime soon.

And they have to battle Google for ad spend (which is finite).

In retrospect, the whole meta-world con becomes clear.

Knowing they inevitably had to battle Google for ad dollars, they tried to pivot to a pseudo real estate play (VR meta-land) where they owned *all* the walled-garden make-believe real estate.

Their own monopolist, test tube intranet they tried to hype the world into believing.

(AI, cough, AI…)

MW: US Treasury yields move toward or above 5%, raising risk ‘something may break’…

These “until something breaks” headlines are for 🤣 because the biggest thing that the Fed is in charge of already broke: price stability. Now the Fed is trying to glue it back together with higher rates.

Inflation has upended everything and thrown all assumptions out the window. Price stability is a huge thing, and it broke into a million little pieces.

Well…if you French kiss a pit bull for 50 years, you can’t be surprised if your face eventually gets ripped off.

“These “until something breaks” headlines are for…”

But when something broke in Mar then the Fed did come riding in “with $400 billion in insta-liquidity to the banking sector over a matter of weeks”

It just shows the Fed does ride in when “something breaks”. Okay they have withdrawn the liquidity since. That is because they were able to contain the fire. What if next time they can contain it only with $1 Trillion or printing to heaven?

When something breaks (other than the broken Price Stability) it becomes a question of putting out the fire else the system may well be engulfed.

The Fed removed this short-term liquidity within 2 months. Whoosh gone. QT now faster than ever. Nearly $1 trillion.

Those 8 companies are about the only ones growing sales. People are chasing growth. A big cap mutual fund in my 401k is up 32% YTD. Crazy.

The market still hasn’t reached capitulation stage. The big five are still holding up and trashcoin is still above 26000. Investors are still complacent. It will get to them eventually.

PIVOT stories for November circulating.

FED pausing interest hikes or even cutting rates won’t lift the market up. But if they start money printing binge (again) that will change the equation.

Exactly. Retail investors have not sold stocks at all even during the bear market in 2022. Fidelity said over 90% did not change any fund elections and actually increased the percent of their paycheck % that goes into the stock market. Buy the dip.

I talk to some of my friends. They just say let it ride. When they talk to their financial advisors the advisor tells them yes, you are down a little from 2022 but you are now positioned for the next wave of growth.

Everyone is taught to not sell and stay invested and average down. It has worked for 40 years. Buy the HB1 crash. Buy the COVID crash. Buy the QE crash of 2023.

Of course there FA says ride it out… Either that or lose trails. Disgusting world we live in

Yes BUT since the death of defined benefits pensions aren’t all us working stiffs stuck with saving/investing/speculating our 401k money in the stock market in the HOPE of retiring someday? Because that’s the only hope we have of getting our savings to grow faster than inflation shrinks it?

Yeah yeah, 60/40 buy and hold and rebalance and all that, 10+ year time horizon etc.

Let’s assume I don’t want to milk cows or hoe weeds in the vegetable patch or play slum lord with rental properties. WHAT ELSE are we supposed to do? What other accessible option is there? T-bills and hustling in the gig economy? Swing for the fences as an entrepreneur and hope for the best?

Minor wording correction, below comment:

Presumably non fund inflows (i.e. direct stock purchases) and stock buybacks were responsible for driving the market higher in spite of fund net outflows (my comment).

Save, USD is a store of value ;-)

Inflation screws over defined benefit plans too.

I-bonds, and saving as much of your money as you can.

I’ve been eating canned soup for lunch all week, while some of my co-workers at the office spend $15-$20 on takeout every day.

You’ll never build wealth if you’re not comfortable living poor.

I couldn’t get numbers for the stock market as a whole using google. Grrrr.

Per Morningstar article, 1/15/2020.

Net investment into equity (mutual) funds for 2015 thru 2019 per Morningstar article (chart) shows outflows for 2015, 2016, 2019. Inflows 2017, 2018.

This is for the Morningstar’s equity category.

This is somewhat interesting…

Additionally in 2019 US equity, sector equity, allocation and alternative equity (Morningstar) categories all showed negative outflows even though s&p 500 was up about 29% that year, Russell 2000 about 25%.

Funds had outflows for equity category in 2015, 2016 yet s&p 500, R2000 both up in 2016 and in 2015 s&p 500 essentially flat, R2000 up.

Presumably (non fund, i.e. direct stock purchases) inflows and stock buybacks were responsible for driving the market higher in spite of fund net outflows (my comment).

Bond funds (2019) had huge inflows. Passive equity fund inflows quite positive but outflow of active managed equity funds exceeded those inflows.

Article authors Katherine Lynch, Tom Lauricella.

There cannot be any “outflow” out of the stock market except through share buybacks.

IPOs and direct listings represent inflows into the stock market (new money coming in to buy newly issued shares or to buy shares previously not available in the public stock market).

Follow-on offerings (a publicly traded company raises cash by issuing and selling more shares) also represent inflows of new money into the stock market to buy those new shares.

What you point at are flows out of stock mutual funds or exchange-traded funds (ETFs), that investors get out of. But the money never leaves the stock market. If people, in trying to get out of their stock mutual fund, sell their mutual fund units back to the fund provider, the fund provider has to sell the underlying stocks to some other investors, either other mutual funds, or investors buying stocks directly (new money coming in to replace old money leaving), and on net, no money leaves the market. But prices can go down if there is more selling pressure than buying pressure.

Wolf,

If you already know this, fine.

Per Fidelity trader:

I sell shares in a fund. Someone may not be buying the fund at this time, so a market maker buys shares using his inventory. This allows my sell to occur immediately, i.e., i don’t have to wait for an investor to place a buy order.

(Same story for share redemptions, market maker accesses his inventory).

So yes for every buy there is a sell (apparently) and vice versa taking into account market maker’s activity.

From the fund share perspective though, I sold shares, net outflow.

It would be a very odd day or year if the number of investor purchases and redemptions in a particular fund

were equal ! The market makers create the equilibrium.

I asked the Fidelity trader if the process of maintaining inventory (that market makers make use of) is complicated. He said its quite complicated. I take his word for it.

I asked about certificate of deposits… how does it work for the secondary market. He said there are not market makers for CDs and so yes there does need to be a buyer (investor) willing to purchase your CD in order for the transaction to take place. So CDs are less liquid than stocks in that regard.

Back to Morningstar. They stated there were net outflows from their equity category. This simply means at the investor level, market makers ignored, the redemptions for the year exceeded the purchases in dollar amounts.

Of course, as I mentioned, there can be direct purchase and redemption of stocks that do not have bearing on the numbers Morningstar was reporting (solely mutual fund transactions).

Finally, if I exchange shares to a money market and then sell the money market shares… money has left the stock market.

That’s what I was told.

My response below or above was somewhat misleading.

Which is odd as I have sold fund shares many times.

What I have described… as probably 90% or more of the readers here understand ….pertains to stock trading. Yes when one sells fund shares some portion of the underlying stocks get sold… so my response is relevant but only as regards that aspect of the fund redemption.

When one sells fund shares the closing prices for the (underlying) stocks sold are multipled by number of shares sold thereby in sum providing the amount the fund redeems to the seller.

The intricacies of the stock selling, again, was what my previous post describes. I dont believe there are typically market makers for mutual funds.

Morningstar does seem reasonable to discuss net inflows or outflows of funds over a period of time.

I briefly looked at the Statements of Assets and Liabilities from 2 fund semi annual reports. These are both stock funds, their stated objectives are to make money being entirely invested in the markets 100% of the time. (An

allocation fund such as PRWCX, VWELX, FPACX, LCORX might have 25% to 60% of their fund in cash equivalents at some point in time). My memory suggested these funds would have 5% or so in cash. I dont see it though. There is a rather trivial amount, 0.1% of Total Assets, in Prepaid expenses and other assets in the one fund. Its even less than that in the other fund. The one has Foreign cash at 0.03% of Total assets (its an international fund). The other fund does not list cash as an asset.

What they do have as Assets:

1. Primarily: Investments, at value (vs. at cost)

2. Much smaller amounts of Receivables (various categories)

3. Repurchase agreements (just the one fund)

One fund has about 4% tied up in items 2, 3.

In both cases their Total Liabilities were about 0.8% of Total Assets.

Aside: I talked to another Fidelity trader. He said that when stocks are sold/bought they often (sometimes?) find a corresponding buyer/seller and match them up as best as possible. Only if (?) no buyers or sellers exist do they use their inventory to satisfy the transaction request.

There are typically 5 statements available to view in a fund’s semi annual or annual report:

1. Portfolio (Schedule) of Investments

2. Statement of Assets and Liabilities

3. Statement of Operations

4. Statements of Changes in Net Assets

5. Financial Highlights

Does the real estate industry have this degree of disclosure ?

I totally agree that market players are in the complacency stage.

Nvidia at 2.9% weight and a return of 192% (2.9 X 1.92) is responsible for 5.5% of the SP gain. Surreal.

When I noticed the Dow’s YTD was nearly zero, I wondered what impact the top SP top market caps were having….and now that I know…..I am going to calculate the weighted average forward PE and these top stocks.

for another shock.

Wolf…hope this isn’t verboten….but here’s an observation from boots son the ground. Your wisdom would be much valued here.

We keep hearing that Treasuries, primarily longer term are getting whacked with higher rates which is affecting the stock market. I do understand that higher rates = lower prices (if not held to term) but

this happened to me just 2 days ago.

I went to my brokerage co. and bought a 3 month T-Bill. There were about 10 choices with slightly different yields…about 5.45%.

Today I logged in again just to check what might be available & at what yields & prices…..NOTHING available. All sold out! I was quite surprised.

What do you think about this versus the MSM the last few days and the

“suckler rally” in the S&P?

Wait a minute. Confusion is breaking out?

When you go to a broker to buy a 3-month Treasury security in the secondary market (under the tab “3 Mo” or similar), you might be offered a 3-month T-bill that was issued a few weeks ago, with less than 3 months to run, or 1-year T-bill with 3 months left to run before maturity, or a 2-year note with 3 months left to run before maturity, or whatever.

I just looked at my broker, and it offers all kinds of Treasuries that mature in roughly three months, from 3-month T-bills issued earlier in September that mature in December, to others that mature in January. No shortage there. The yield to maturity (YTM) depends on the price you’re able to buy them at.

The entire range of maturities was plentifully available under the tabs: 3 Mo, 6 Mo, 9 Mo, 1 Yr, etc.

If you were looking for “STRIPS” (zero-coupon bonds), there might be none available below 1-yr.

If you buy a 3-month T-bill through your broker in the secondary market (meaning someone bought it at auction and is now trying to sell it), it will likely mature in less than three months. If it was issued one month ago, it will mature in two months, and you’re buying a 2-month yield.

If you buy a 3-month T-bill at auction from the government, you have to give your broker the order to buy them at the next auction date or you can order them directly at TreasuryDirect. There’s nothing to negotiate, and you get what the auction determines you get.

The government sold $71 billion in 3-month T-bills at the auction two days ago. There is another 3-month auction next week. These are now HUGE auctions because so much in T-bills needs to be rolled over plus the new issuance. So there are plenty of them to go around.

Howdy Folks and Lone Wolf. Feel like educating me? I understand if a tbill is purchased at treasury direct, it can only be sold before maturity after the transfer to a Brokerage. Besides that, what are some other advantages to purchasing t bills in the secondary market instead of Treasury Direct? Any additional interest to be earned? Is there a bid sell thingy? Thanks

Bonds are not regulated by the SEC like stocks. I used to trade Bonds and the spread of different brokerages vary substantially. It can be difficult to find a good price. I don’t trade them anymore. Perhaps if had several million it would be OK.

There is a lot of educational material at Treasury Direct. There is also auction history, etc. You don’t need to sign up to read their educational stuff. Not the flasiest website, but follow the directions and it works well.

Good luck from another debt free human…

Biggest reason I buy bonds thru my broker, is that their website is much better than treasurydirect.gov LOL

Wolf, you’ve said this before, but given some of the other comments, it may be time for another Public Service Announcement.

Retail investors will incur ZERO fees and commissions if they buy new issue Treasuries at the auction, and then let them mature. Given the wide variety of durations available, there’s no reason not to do this.

On the other hand, retail investors will be charged a shocking array of fees and commissions when buying or selling Treasuries on the secondary market. As a percentage of the interest earned, these charges are Trumpian HUUUUUGE.

Actually 3 month AND 6 month T-Bills were NOT available…only one year+

Who is your broker?

Here are T-Bill from the Fidelity website

3mo 6mo 9mo 1yr

U.S. Treasury 5.50% 5.53% 5.49% 5.51%

You can purchase “New Issues” US Treasury Bills through Schwab.com. I maintain my fixed income ladder there. Every month or so I have T-Bills maturing then I pick up more. No broker fees on “New Issues”. Create a Schwab account, go to Trade –> Bonds –> Treasury Auctions –> and then you will see the upcoming auction dates. Right now they are showing 1 month, 2 months, 3 months, and 7 years available. The duration changes weekly.

There are no T-bills beyond 1 year issued. Beyond that are Notes, TIPS, and Bonds. You can buy any of those that will mature in 3 months on the secondary market. Plenty available right now on at least two online platforms I use.

A Fidelity rep told me a week or so ago their treasury bills, notes get replenished every Thursday. This is not the secondary market I am describing.

Thats what I was told (I looked on a Tuesday and there were only 2 very short maturity bills I could buy, 1 and 2 month I believe….hence my question for him). On Thursday they had longer length notes available (e.g., 5 year). I ended up buying a CD instead (very large institution) as it had a slightly higher yield and its in a Roth account, no tax issues.

The auctions for the 1 to 3 month T-bills are on Thursday morning. They mature on Tuesday. You can order them (for the auction) starting around noon Tuesday (Central) and all day Wednesday.

Some brokers list them all, but have a clickable dot only when they are taking orders. Others may only list the currently open auctions.

If you’re looking for 1 to 3 month T-bills, check your broker’s site each Wednesday.

Here is Treasury’s Tentative Auction Calendar. It is all you need to know about availability and timing of all Treasuries.

https://home.treasury.gov/system/files/221/Tentative-Auction-Schedule.pdf

Mike Wilson pointed to the fact that the earnings recovery of half of these big 8 over the last year was fueled by cost reduction and not through top-line growth. High PEs cannot be sustained for those companies

True but they each have a big moat around them and have monopolies in their specific spaces. I am not sure how anyone can unseat them? Are their PE ratios high? Yes. But stock buybacks on even flat income will boost EPS growth.

These 4 are global monopolistic companies:

Google has very little search competition.

Microsoft has very little Software competition

Facebook has very little social media competition.

Amazon has crush retail.

Microsoft, Google, and Amazon pretty much own the cloud.

These 4 almost get all ad revenue from the whole world except for the counties that ban them. (China). All that add money leaving Europe, Asia, Africa heads to these 3 or 4 companies.

They are pretty insulated for now. I am amazed other countries do not try to put tariffs on ad revenue. Crazy how much of the advertising profits flows out of their countries into the US.

Big tech companies have more power than governments. They were allowed to become so large, they can claim to be the sole source of jobs and development. They have the support of most legislatures, so governments cannot seriously enforce antitrust, taxation, or other types of regulation against them. They drive the government agenda. And now AI will give them even more power.

Facebook’s the most vulnerable of the bunch. Fewer barriers to entry than the others, has happened with similar companies (Myspace), and the metaverse is dead.

Tariffs can trigger reciprocating tariffs, or at least threats of such. Easier to impose massive fines (with minimal or no pretext) and pocket those.

Assume that each control 95% of their markets. Does their current PE’s justify the organic growth of their respective markets? To justify, they need to break into new markets.

Mostly by buying companies in other markets.

@NR – The high PEs do not justify the growth projections but they do justify future stock buybacks which will lower the PE ratio as the EPS will rise as profit is divided by less common stock.

EPS = Earnings / common stock (EPS goes up with stock buybacks)

PE = Price / EPS (Thus EPS goes up then the PE ratio goes down)

Go look at my previous post on Dillards. No sales or income growth but stock appreciation via stock buybacks. Either the stock price stays the same and PE ratio goes down or the PE ratio stays the same and stock goes up. As long as income stays flat.

VTV, the Vanguard ETF, is also down on the year.

This is the problem with indexing. The more people who index, the more money that proportionately flows into the biggest names in the index. Has to be that way, basic math. Apple gets seven cents of every dollar thrown into the S&P, Microsoft gets 6½¢ and so on. Never mind the separate effect of people chasing performance and creating bubbles.

Most dividend stocks are going nowhere or getting killed, with the exception of oil. Look up phone companies, pharma or even consumer staples.

I don’t when this ends or what happens when it does, but at some point valuation wins. It ALWAYS does.

1) The Dow 1D : a buying tail. Aug 1 high minus Aug 25 low = 1650.

Sept 14 high minus today low = 1,692. The correction might be over.

2) The Dow isn’t H&S. The neckline is tilting too much. The Dow w/ a

cloud : equilibrium is too high above. It’s paper thin. It flipped on

Sept 18. Tomorrow DM #9.

3) SPX 1D : it flipped on Sept 15. Today DM #9. The rest : same bs.

4) SPX 1M : only 2TD left in Sept. Sept bar is larger than Aug and July,

on a lower vol. Something is wrong.

5) SPX 3M, quarterly : The lowest red Vol since 2009.

6)

Generally P/E ratios reduce as interest rates rise. I think the stock market has been buoyed by all of this talk about inflation receding.

But now, we’re hearing about “higher for longer”, referring to interest rates. My takeaway is, if interest rates need to be higher for longer, then the reason, inflation, is being seen as higher for longer.

So, I can see a P/E multiple reduction.

I saw another reduction today, at the Strategic Petroleum Reserves. While one week is not much of a trend, me thinks that the government might be thinking that this inflation isn’t wrapped up like they’ve been saying it is. And, if it isn’t wrapped up, there is going to be pressure on P/E multiples.

Many international equity funds sport P/Es much lower than the domestic funds. Typically 10 to 12. DODFX, ARTKX, TBGVX (Its global, not strictly international). The Ukraine war and China tensions might factor into the lower P/Es a bit.

Might get interesting if and when they start to refill the SPR. ‘strategic’ had a different meaning when it was established.

When an index replaces a floundering company with a more successful one, my funds in the former are automatically moved to the latter, right?

Publius,

Actually, a post about the specific selection mechanics of index deletions/additions would be most useful.

The Big 8 aren’t going anywhere, and the SP 500 has a large number of stocks…but addition/deletion mechanics for smaller indexes might really matter.

And, I’ll be honest…even for the 500, the “rules” seem a little hazy.

The point of Wolf’s post makes the issue a bit moot, but like I said, indices tend to do a fairly poor job of publicizing their addition/deletion rules.

I can remember looking to diversify, so I looked at several ETFs, ostensibly each with a different emphasis and perspective.

Lo and behold, their top holdings were all the same few tech darlings.

A couple years ago I looked into doing the same thing. You basically have to get into very specific sector funds and even then there’s a high degree of overlap.

I “liked” VTV , XLI , XLU, etc. I wanted to buy into SPY, like buffet advises, but the weighting of SPY really bothers me. For the reasons demonstrated in this article.

There’s no breadth to this market, and hasn’t been for several years, yet somehow it keeps defying gravity.

I’m starting to second guess being on the sidelines, although the money market and short term CDs are starting to actually pay something, but nothing close to what I could have made in Amazon or Msft this year(which I had considered). Outside of a few nice weeks with SQQ I’ve mostly stayed out. No time to follow the Inverses now, new job keeps me busy.

I’m still waiting, been waiting this long would seem foolish to rush into this market now.

As always, thanks to Wolf for the great data and analysis.

Cmon baby, drop to the 60-80% mark on the wolf charts!

I’ve been waiting for these drops since 2020. They just kept being deferred to later.

This would barely get us back to where everything was pre-covid.

I’m beginning to think that there’s just far too much money sloshing around out there for this large of a drop to actually happen.

Even with almost 1 trillion in QT, there’s still a massive amount of liquidity that was added in just the last few years.

Also, with interest rates actually paying people for money market or treasuries, isn’t there the potential for some of that cash flow to end up in the equities market?

What’s the break even point where treasuries are so rewarding that people allocate everything into treasuries versus putting some of that interest payment into SP500 for “diversification”? At least that’s what I’ve been contemplating lately.

Interest paid by government on treasuries will be plowed back into new treasuries issued to pay the interest.

“What’s the break even point where treasuries are so rewarding…”

I would argue we’re almost there. I have 75% of my portfolio in Bills right now.

Yeah, too much money. And the latest GDP figures point to deceleration. DXY is down sharply today.

That’s how classic ponzi’s playout.

The looming shutdown and impeachment will send the S&P soaring to the moon. The Dow? Dow 100K at least.

The old fraud ponzi or ponzi fraud. Fraud Street all based on the four stages of burnout (disillusionment) as enthusiasm, stagnation, frustration, and apathy.

APPL is in the midst of a huge technical breakdown.

Take a look at the chart.

Not to mention it seems they have hit the wall as far as innovations to an Iphone…..

An expected $1.00 earned (forward PE) in the top 8 creates market value of $32.93

For the rest of the SP500, the $1.00 creates market value of $20.97

Average Forward PE on top 8….32.93, for all of SP 500…… 24.46

Forward PE on #10 to #500 Companies is …….20.97

Forward PE SP 500 op 8 Companies by market cap in the S&P 500 Index SP 500 Weight Weight in top 9 Forward PE Weighted PE

1 Apple AAPL 7.10% 24.4% 27.07 6.60

2 Microsoft MSFT 6.50% 22.3% 29.42 6.57

3 Amazon AMZN 3.20% 11.0% 58.29 6.41

4 Nvidia NVDA 2.90% 10.0% 33.11 3.30

5 Alphabet Cl A GOOGL 2.10% 7.2% 23.13 1.67

6 Tesla TSLA 1.90% 6.5% 65.94 4.31

7 Meta Platforms META 1.90% 6.5% 22.76 1.49

8 Berkshire Hathaway Cl B BRK.B 1.80% 6.2% 20.43 1.26

9 Alphabet Cl C GOOG 1.80% 6.2% 21.37 1.32

Average Forward PE 29.10% 32.93

Should the big guys tumble, eventually, do the little guys follow? (Notwithstanding the fact that they’re already in lower territory.)

U.S. equity markets are heavily focused on growth stocks that don’t pay dividends. Retail investors don’t have enough information to compete evenly in growth.

Overseas markets generally pay higher dividends. They are cheaper relative to the currently higher dollar. Some such as London and Brazil do not tax dividends paid to U.S. share owners. You can also find shares who’s dividends are treated as QUALIFIED by the IRS so they are taxed at Long Term Capital Gain rates. For a married couple who’s income is less than $82k there is no tax on Qualified dividends. There are many old companies overseas that pay large dependable dividends because they have ‘moats’ about their business. Big miners are my favorite.

My overseas dividend payers have not participated in the S&P-non-eight sell off. BHP Billiton has had an average yearly return (dividends and price appreciation) of 15% for the last 5 years and mining in general looks good going forward.

You can’t build or do much without metals and minerals.

I am buying aggressively at Dow 3,000.

MW: Brutal U.S. bond-market selloff puts popular ETF on cusp of lowest close since 2008

Never buy bond mutual funds or etfs. Okay to buy the bond money market funds. Also do not buy long term bonds. Stick with T-bills, buy them at a broker or TD.

I have never sold an equity or equity ETF. I only buy with money I don’t think I’ll need for anything else. Whoever gets my estate will be responsible for timing the sale — so that’s one less market timing error I get to make …