First Republic, is this you?

By Wolf Richter for WOLF STREET.

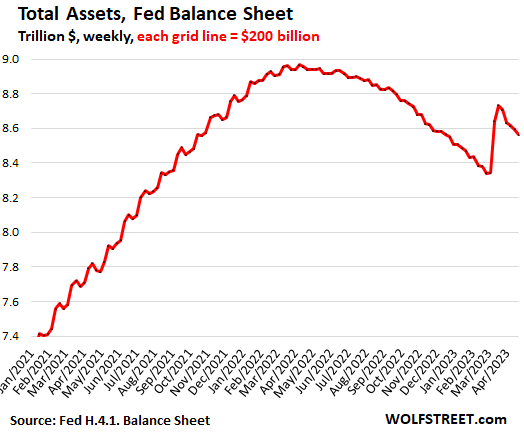

The Federal Reserve’s balance sheet, released today, dropped another $30 billion for the week, to $8.56 trillion, bringing the plunge in the five weeks since peak bank bailout to $171 billion, as quantitative tightening (QT) continued at the normal pace and liquidity support shifts and unwinds, though First Republic seems to be sucking hard on the Fed’s teat.

The new principle of separating QT from bank liquidity support was laid out by Powell during the last post-meeting press conference, where the Fed can let QT run on track in the background, while briefly stepping in as lender of last resort to a bank. Looking at it with a magnifying glass to see the details of the banking crisis:

QT continued:

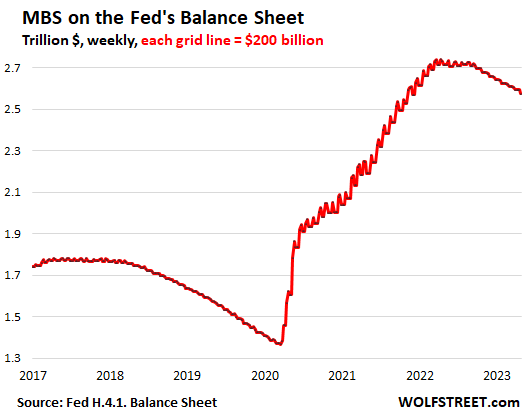

MBS -$17 billion for the week, -$164 billion from peak, to $2.58 trillion. The Fed only holds government-backed “Agency MBS” where the taxpayer carries the credit risk, not the Fed.

Mortgage-backed securities roll off the balance sheet primarily through the pass-through principal payments that holders receive when mortgages are paid off, such as when mortgaged homes are sold or mortgages are refinanced, and when regular mortgage payments are made.

The roll-off has been below the cap of $35 billion per month because home sales have plunged and refis have collapsed, and therefor fewer mortgages are getting paid off.

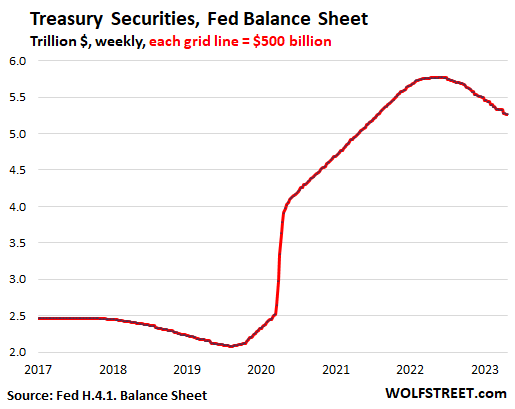

Treasury notes and bonds “roll off” the balance sheet when they mature and the Fed gets paid face value for them. Maturity dates fall either on the middle of the month or at the end of the month. Today’s balance sheet was in between. Next week, over $40 billion in Treasuries will roll off the balance sheet.

Liquidity support.

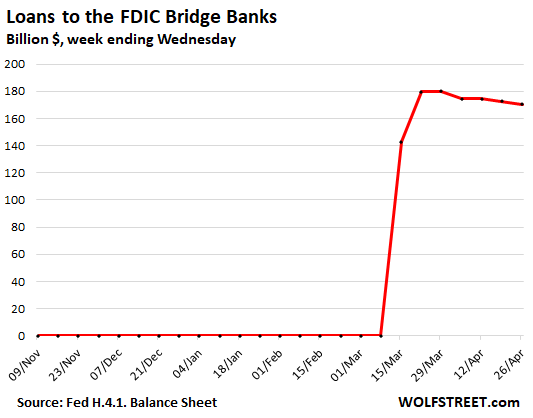

Loans to FDIC bridge banks: -$2 billion in the week, to $170 billion. The FDIC bridge banks have been and still are the largest of the bank liquidity support programs. They took over the collapsed Silicon Valley Bank and Signature Bank. The FDIC has made deals to sell a large part of the assets and transfer the deposits to other banks. It’s now auctioning off in bits and pieces the MBS and Treasury securities that the bridge banks still hold. When these deals close, the funds will go back to the Fed. When everything is said and done, this balance goes to zero:

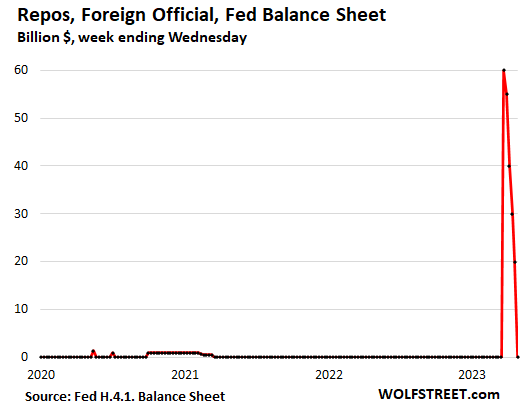

Repos with “foreign official” counterparties: -$20 billion in the week, to $0. They’re now paid off. This was likely the program that the Swiss National Bank used to provide dollar-liquidity support for the take-under of Credit Suisse by UBS. The Fed has for years offered these repos to foreign central banks so that they can access short-term dollar liquidity against collateral of eligible US securities that they’re holding.

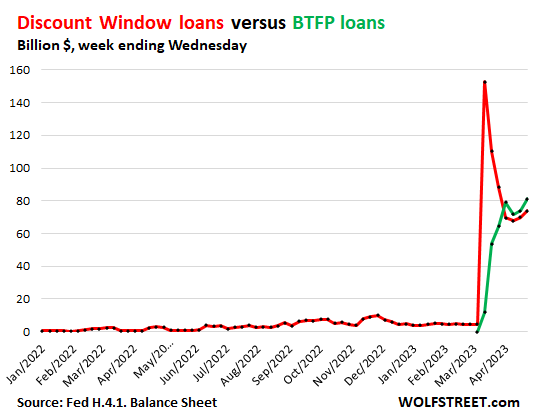

The Discount Window (“Primary Credit”): +$4 billion for the week, to $74 billion, less than half of its bank-bailout peak of $153 billion. The Fed charges banks 5.0%. Banks also have to post collateral, valued at “fair market value.” These are punitive terms for banks who can normally borrow from depositors for a lot less without having to post collateral. It’s only when banks need liquidity badly during a run on the deposits, but cannot sell their assets quickly enough without losing a ton of money, that they will avail themselves of the Fed as lender of last resort.

Bank Term Funding Program (BTFP): +$7 billion to $81 billion. Under this new program, rolled out on March 13, banks can borrow for up to one year, at a fixed rate, pegged to the one-year overnight index swap rate plus 10 basis points. Banks have to post collateral, but valued “at par.” For banks, the terms of BTFP are still punitive, though less punitive than the Discount Window.

Renewed turmoil is bogging down First Republic – First Republic Discloses it’s a Zombie – and it said that it was heavily relying on the Fed’s liquidity programs to cover the massive flight of uninsured deposits. First Republic is a substantial part of what we’re looking at here at the Discount Window and at the BTFP.

This chart shows both, the loans at the Discount Window (red) and the loans at the BTFP (green):

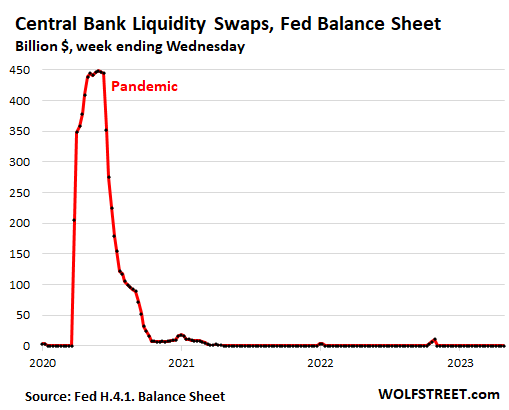

Central Bank Liquidity Swaps: No activity.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf: You want me to be elated that FED balance sheet went down by $175B but chastised me for saying the vertical move by $500 B is indeed QE (if something walks like a wolf and sounds like a wolf, it is indeed a wolf). :)

#1 the vertical move was $391 billion NOT $500 billion.

#2. The $391 billion wasn’t QE, it was liquidity support.

#3. But if you call that $391 billion QE, YOU HAVE TO NOW CALL THE $171 BILLION QT.

#4. QT = Treasury and MBS roll-off not the whole $171 billion

#5. The unwind of the liquidity support is NOT QT, just like the spike was NOT QE.

I’m getting tired of fighting the ZH BS here over and over again. What goes on at ZH stays at ZH.

The “Not QE” went from $390 Billion to ~$305 Billion.

Wolf, if banks posted collateral, shouldn’t they count as Fed liability canceling out Fed asset jump? Or were these collaterals questionable and so were accounted at much lower value?

When you get a mortgage on your house, the house is the collateral. But it doesn’t cancel out the mortgage for the bank. The bank doesn’t even consider the collateral (the house) on its books until the sad day when the bank owns the collateral. Same at the Fed. Same with any secured loan.

Wolf is correct.

QE is outright purchases of bonds. Credit facilities are not outright purchases.

This is not QE, which is why the Fed’s balance sheet is shrinking.

It is the curse of the web. People read a headline and think they know something.

The cash from liquidity support isn’t circulating in the economy; it’s sitting at First Republic et al. This would be obvious to anyone who looked at FRB’s balance sheet from earlier this week.

If anything, that liquidity support is removing money from circulation as FRB is paying something like $100m per week to the Fed in interest on their $100B loan.

Is FRB or some other entity getting IOR (interest on reserves) from the Fed on the money FRB borrowed? If so, the interest received by a bank or MM on the increased reserves should approximately cancel out the interest paid by FRB to the Fed.

When first republic defaults on the fed loan than that becomes qe

When the Fed makes loans and other accommodations to distressed financial institutions it is performing its core function as lender of last resort under the FRA and is countering the threat of deflation and financial panic due to bank failures. Three cheers for the Fed. When it engages in QE it creates new money to buy Treasuries and MBS in the secondary market, thus artificially increasing the price of the targeted debt instruments and other financial assets and to a degree unsterilizing prior money creation. The financial system is the beneficiary of QE and the general price level is affected only to a small degree as demonstrated by the GFC and years following. No cheers for the Fed. When the Fed and Treasury act hand in glove to create new money by the trillions and carelessly drop it into the real economy via transfer payments without much regard to need (e.g., the Covid response; PPP being the worst offense) their action is inherently inflationary and counter to the Fed’s mandate. Boos to the Fed. The total size of the Fed’s balance sheet isn’t the primary consideration; how the new money that was created is deployed and with what level of due care and necessity under the FRA are what matter. Reducing the size of the Fed’s balance sheet will reduce the price of the assets being sold or rolled off; after 15 years of near ZIRP we have trillions of dollars worth of debt instruments world-wide that are already impaired by the rapid rise in rates. QT will inevitably be very slow.

The main point is that this QT argument is just an experiment, just the way QE was an experiment and no-one really knows, where or how this is going to end.

The system has become really fragile and I’m really not sure that Powell & Co. is able to comprehend, weather this is really a solution for all the problems that have accomulated in the past 10 years of QE.

According to Kondratieff there’s a crisis nearly every 7 years and a major one every 20 years, and the pace of the QT is too little and too slow to clean up the balance sheet of the FED (or to get it to the level it should be). So I’m of the opinion that QE will soon become “a tool” for system stabilisation, which will be used sooner than later.

There needs to be a severe downturn in order to clean the system and the FED is not willing to do that. It is not in the political interest of anyone in the US to have a prolonged QT …

It’s like what Aristoteles said: “If you know what is Good, it’s not enough. You have to DO good.” Between knowing and doing … well, that’s the main problem, isn’t is?

People who get to the top of these orgs have spent their entire lives doing the expeditious thing instead of the right thing.

The institutions have zero credibility.

Last call at The West bar, last call please.

It’ll end around March 2024 when the Fed cuts the Fed funds rate.

The quote “a rose by any other name” seems appropriate for the discussion.

I see all your very valid arguments Wolf but the balance sheet is moar now than March.

Thats alot of roses IMO.

Team QT here. Frustrated that these credit facilities are blank checks to undo all of the rolloff and possibly more.

AV8R,

Look, you need to think about what happens with the money the Fed lent out. Simplistic approaches are a lot of fun and make great clickbait headlines that are BS.

For example, the Fed lent $170 billion to the FDIC to cover the deposit outflow of the bridge banks. That money is not going anywhere. It just sits there (in the bridge banks’ reserves accounts at the Fed). NO ONE BOUGHT ANY SECURITIES with the $170 billion. That money was created and is on ice. The FDIC has made a deal to transfer the deposits to other banks (deposits are liabilities). And it’s selling the assets of those banks. When these deals are done and closed, and the bridge banks resolved, that $170 billion will go from the bridge banks reserve accounts at the Fed to pay off the $170 billion loan from the Fed, and vanish. There has been zero QE activity associated with this $170 billion as NO ONE BOUGHT ANY SECURITIES with it.

I find the argument that “no one bought anything with the money” as missing the point.

What happens if the assets that are being sold by the FDIC crash in value before the sales are completed, so that the FDIC cannot recover the $170 B? Would you still say that “no one bought anything with the $170B”?

The money certainly affects the entire system.. even if no transactions are conducted with it. It changes the numbers out there, and influences the behavior of investors across the board. In fact, that’s sort of the point! But you cannot conclude that it only prevents bank runs and has no other effect on investors and prices.

Anup Rao

“… assets that are being sold by the FDIC crash in value before the sales are completed, so that the FDIC cannot recover the $170 B?”

This is pure imaginary fabrication. It’s not how the FDIC is set up. The FDIC covers its losses from the FDIC fund. It estimated that its losses on selling the assets of those banks combined will be $22.5 billion, and it will fund these losses from its deposit insurance fund and then recuperate those losses by charging a special assessment to other banks. I have explained this a gazillion times.

The $170 billion has zero to do with those losses and asset prices and assets. It’s just temporary liquidity to be able to cover the deposit outflow and keep the bridge banks liquid in the wind-down period.

whats ZH?

The online publication Zero Hedge.

The MBS chart (2nd chart) shows why the house prices went up so much. F-ing FED

Wolf ,

Wall Street has become a casino nothing makes sense.

Am I not right in this observation?

I thank you for your reply in advance

1. Yes. Long ago.

2. Trying to resolve that issue here, trying to make sense of things…

3. Yes

4. You’re welcome

I know the recent review of the Fed intervention in this crisis revealed failures to properly respond to early warnings at SVB, but is anyone going to attempt to assess whether the bailout of depositors was really necessary to avoid systemic risk?

So what if 20 midsized banks fold? What is the seriously bad part of the fallout for citizens of the US on the whole? Isn’t living with this inflation worse for the average American than rich people taking a haircut on high risk deposits?

How does this natural result of tightening undermine the entire US banking system?

It’s Socialism for the 1% and screw-ism for the 99%.

Wait, so you work at Kroger Corp?

Cuz that’s their biz model 100%!

Squeeze upper middle class with “fancy groceries”. Customers feel upper class and spend upper class. Then Kroger closes the “poor” stores. And charges more at the “fancy” stores.

I saw a lady wearing designer everything the other day. Standing 10th in line to be checked out by a human (at the only open full serv). While self checkout had 10 open spots. Think she cares what she pays for groceries? Prob not.

So the rich woman 10th in line is somehow worth calling out but the 9 in front of her also not using self-checkout are… what, exactly?

in terms of not using the self-checkout…

Also depends on state liquor laws, I guess. We here in CA can buy booze at the grocery store but must provide an ID at the cashier. So our Safeway here has a large selection of local craft brews, plus Big Beer stuff, plus a big section full of wines, including fairly high-dollar wines, plus a whole section of Scotches, Bourbons, etc.

When I have some beer in the cart, I cannot go through self-checkout. As soon as I try to scan the beer, the machine beeps and tells me to go find the self-checkout supervisor, who then tells me to go pack all my shit back into the cart and to get in the back of the line at a human cashier so they can check my ID, yeah, I know, but speaking from experience.

A lot of us – designer clothes or not – do the same thing, get in the checkout line with a human cashier.

After you hear “unexpected item in bagging area” for the 25th time, self-checkout is not worth the hassle, even if the line is shorter.

This is not a class warfare phenomenon. I’d wager that woman cares as much about the price of her groceries as the rest of us do.

Wolf,

You can Totally self checkout beer and wine here in NC. All day long. They literally look “to see if you look 30ish”. I watched a guy be trained and this was their nudge nudge “hint”.

Liquor is still tightly controlled because the district managers over the stores have salaries from 500k to a Million I think. It blows the mind. Very 50-60’s scrutiny feeling comes thru in the Liquor stores. Meanwhile in Arkansas I think you can do drive thru fruity sodas with lots of shots! Drive Thru!

Glad california is still sensible. Love that state when I visit.

sufferinsucatash,

Funny (tragic?) thing is that no one has checked my ID at the cashier for at least two decades, LOL

It’s just how the system is set up.

@sufferinsucatash

Why is it Kroger’s responsibility to open or keep a store open anywhere? They open where they feel they can make a profit and close where they cannot.

Should I start complaining about not having a Gucci or a Dollar General in my neighborhood?

Btw, using a human checkout lane provides employment security to the checkout clerks. You should try that more often.

I try not to use slef checkout if possible.

I hate taking jobs away from these low wage earners

Ianal, but seems that the liability of incorrectly scanning or completely skipping an item when using self checkout is transferred from the cashier to customer. Retailers have gone after customers who missed items. Not sure how widespread the practice is, but I would rather not risk it unless I only have a couple items in hand.

Fun fact: With some retailers, the shape of the self checkout area tells you what kind of neighborhood you’re in.

A straight through design with wide entrance/exit means low loss, honest customers.

A carousel or N shape with one entrance, turns, one exit, means high loss, dishonest customers.

I would imagine that if so many midsize banks were allowed to fold, there would be a rush to move money from the remaining small and midsize banks to the largest “too big to fail” banks. This would increase consolidation and likely harm the average American. Especially given that small banks provide significant funding to small businesses.

The solution is for the big banks to buy a significant amount of stocks in the smaller banks. Then nobody goes broke ever.

Tom Jones

Buy the stocks in the smaller banks. On what basis? Is there a rational business reason or just to save the small banking system?

Why NOT Fed buy them under SPV fund created in the name of ‘financial stability’?

The whole banking system is out of synchrony in our financial system, thanks to Fed’s policies since ’09. WE need a great RESET but they won’t let it happen.

They had to Bailout the Depositors to prevent further bank runs and assure us that the fractional reserve Fiat currency system is Sound. Yellen was really driving that point in March, the banking system ‘remains sound’…

The USD is backed by the full FAITH and credit of the US. If the sheeple lose Faith it’s Game Over… When the FED stopped holding rates Artificially Low it made US Treasuries with a maturity beyond 2022 worth LESS than what (All) banks had initially paid for them, since a newer higher yielding bond is more attractive. If banks can hold them to maturity, no big deal. If banks have to sell them prior to maturity to cover outflows of deposits, they incur a loss. Arguably, you could create a bank run on even the BIG banks if you had enough Depositors demand their money. The FED need to contain the Contagion to avoid systemic risk.

I wish we could trade our Fiat currency for a Mercedes-Benz currency…

ktini – mebbe Ferrari/Maserati currency (FIAT owns them, oh, yeah (cough) and Chrysler, too…).

may we all find a better day.

Spoiler: If you say “sheeple” you’re probably on too many conspiracy theory websites.

Ironically, people who believe this stuff are being tricked by morons. Half the YouTubers that spout this crap look like they work at DMV and got a C- in high school Econ.

No, Hydra isn’t trying to take over the world Batman. Chill out.

As for the bank run… Boomers in their 60s won’t even switch banks when they’re earning .09%. Americans are too lazy for a bank run. My Mom is 67 and Wells Fargo has been screwing her over for years. She refuses to switch.

Struck a nerve there with the term “sheeple” huh? I thought it was cute word play since this is WOLF street.

You certainly have a lot of constructive and positive things to say. Thank you for your valuable contribution. LOL

If People lose Faith in a currency backed solely by FAITH, it does tend to End the Currency… Hence ‘Game Over’. Now, that’s not to say that it won’t be replaced by something else. Potentially something worse…

If a Bank Run is impossible due to laziness in your humble opinion, why do YOU think the FED stepped in and bailed out all Depositors??

Ironically, I too have a Boomer parent with an account at WFC. I have also tried to get them to move their money for a few years now. Surprisingly at the end of March even Wells Fargo has started offering “competitive” rates to their customers whom qualify for a personal banker. Almost as though they are Actually Trying to retain deposits…

AJ

‘fractional reserve Fiat currency system is Sound’

?

There has never been ‘fractional’ reserve but ZERO reserve, since March of 2020.

Mr. Powell supported the losing of bank regulations in 2018 and designating SVB as a regional bank and NOT a systemically important. The CEO of SVB was sitting at the San Fransisco Fed!

With this kind of regulation where ‘foxes in charge of hen houses’ expect more small & regional bank failures. First Republic stock has lost 97% of it’s value as of now. FDIC take over is just a matter of time.

Can the economy take QT? Or will it cause more earthquakes? Hmmmm

Minor earthquakes, no biggie. Inflation causes the big earthquakes.

Looking at the first chart in this article, I got an impression that Federal Reserve’s balance sheet went from $9T to $8.6T over the course of a year. This $0.4T reduction amounts to roughly 5% of the current size of balance sheet. Looks kind of underwhelming, especially in light of how aggressive they were in driving balance sheet up. Hopefully they will speed it up later this year…

“Underwhelming”??? How about “Normal”?

You can buy a car in an hour… getting rid of it takes longer.

You can meet someone, fall in love, and get married in a week (I have seen it happen)… getting out of a marriage takes… LONGER.

The Fed ran up the assets (and liabilities) on its Balance Sheet as a response to two different crisis situations (QE) over the course of fifteen years… the unwinding of that Balance Sheet (QT) will take more time than the spikes did simply in order to prevent a future crisis. Maybe they will speed it up )like they did last time) and maybe they won’t… but the Fed deserves praise for trying to avoid being the CAUSE of the next financial crisis.

That’s a fun week tho!

Some of us work all year for that week! Lol

LOL… they were an odd couple actually. But it seemed to work for them.

Unfortunately, the FEDS are reducing liquidity slower than the Government is adding liquidity via more debt.

Sort of feels like a wash.

The Government debt is supposed to be 9 trillion higher by 2030 (Which means it will actually be probably 12 trillion) . Even if they FED can reduce the remaining 8.5 trillion in 7 years, it is a wash.

Fed spending is inflationary but so is Government Debt.

I don’t disagree. But the Fed can only control what the Fed can control. Reining in a spendthrift Congress is really not what it is there for. Frankly a LARGE part of what went wrong for the past 15 years was the Fed trying to counteract the elected teenager-wannabees running the government.

They should never have bought MBS.

Ever.

We are dealing with lunatics.

“They should never have bought MBS”

and why are they in the long end at all? The heralded “dual mandate” deals with immediate issues…prices and employment?

Prior to 2009, they were not. And for good reason. For when they are caught with a giant ($5 Trillion) long paper portfolio and then must raise rates, they put themselves in a delicate position.

I guess this is how Nobel Prizes are awarded (Bernanke)…..solve an issue temporarily and create a bigger issue down the road.

Ignoring the liquidity support, it still looks like the Fed is doing one helluva slow walk. Very quick to prop the market up at warp 9, but they only pull the rug out at warp 1.

They are indeed moving very slow.

Fed response has been asymmetric as long as I can remember. When it wants to ease, it can make a decision in a matter of days or weeks. Tightening takes months or years.

Exhibit A: March 2020.

Exhibit B: 2021-2023.

Stuff is already blowing up. How fast do you want the Fed to blow up stuff? That’s what you need to ask yourself.

Much, MUCH faster. This is the most pathetic inflation fight in history.

Volcker, who was a hawk, initiated a recession in 1980. He was also the pivotal voice in Nixon’s abandoning of the gold standard.

After Volcker LOWERED RATES due to the 1980 recession, inflation reared up again, even higher. Volcker then dramatically increased rates causing the much deeper recession in ’81-82. Volcker backed down, briefly. Inflation had been a problem for 20 years, and it was much worse than what we’re dealing with now.

Exactly right. I WANT them to detonate the economy. That is the only way this insane spending will stop. There needs to be blood in the streets and FEAR among the citizens. That’s the only way this will end.

Is there a legitimate worry that some of the stuff that gets blown up can’t be reassembled when it needs to be later on, in the same way an egg can’t be uncooked?

Why are they allowed to go and inflate everything beyond belief but they can’t bring it back down to earth?

Crash the system and let me get a house for an affordable price

Sounds reasonable: crash the system so you can buy a house.

Troy,

1. Why don’t you just rent the same house for a lot less than the mortgage payment? Lots of people do this arbitrage. Let the landlord take the loss. The house is the same.

2. “Crash the system and let me get a house for an affordable price.” Well, that might work except if they “crash the system,” you won’t be able to buy anything because you won’t have a job, and you might not even have bank accounts and credit cards anymore, and anything you squirreled away in stocks and bonds and cryptos is gone. Careful what you wish for.

Faster. Until the markets get it. Unemployment is too low and corporate America is still spending wildly. I don’t want 10 years of inflation because the Fed can’t bring itself to hurt asset holders.

The MMT crowd thought you could create money infinitely without consequences. Why can’t we test the theory now about removing money from the economy just as quickly? We should get to see the results of that test at least once.

Maybe if quick QT means instability and quick QE means out of control inflation that Fed will end both of these programs for good.

Employment is not too high. The problem is too many abled body men in the prime working age sitting around and doing nothing. I was in a somewhat sketchy neighborhood in the heart of Washington DC yesterday, I( saw at least 25 men on one corner alone standing or sitting and doing nothing but loitering in the middle of the working day.

Why are men doing nothing?

Because when rents are too high many economic endeavors become unprofitable.

Solution?

Tank asset prices.

Read “Progress and Poverty”, second best selling book at the end of the 19th century behind something called “The Bible”.

SC:

Be dealer buds taking a break, eh?

Please folks on here, do NOT be confused by the HUGE and growing delta between those ”working for da man” and those working the street…

From what I hear, it’s much more profitable per hour to work the streets these days,,, even as the lowest of the low level dealer, not to mention the various and sundry and now extensive ”mid and high level dealers.”

IMHO, sooner or later WE the PEEDONs absolutely MUST insist that ALL drugs now considered to be illegal, etc., MUST BE LEGAL…

Surely WE can be sure that most of the profits of the current ”illegal” drug trade are going straight to the folks ”ENABLING” that trade, including especially ”politicians” at all levels, etc., etc.

LE folks are clearly VERY divided on this subject, with some definitely part of the problem, and some others clearly too honest and ethical and sufficiently well paid not to participate.

With all due respect, what is actually blowing up? Employment is still high. Inflation is still high. Housing prices are still in an enormous bubble. Stonks are teetering only maybe 15% below all time highs. Crypto has skyrocketed in the past few months.

I’m not seeing “blowing up.” I’m seeing, at most, a slightly more controlled environment than early 2022.

Today at the grocery store.

(I’m always at a grocery store haha!)

I saw some managers chewing out a guy for not stocking shelves fast enough. The guy was vigorously defending himself. They closed the conversation by saying “He is a lot faster than you!”.

So management is using a mythical stock speed some employee the aggrieved employee doesn’t know to Establish grounds to manipulated his job.

This is the abuse I see everywhere. No one respects employees anymore and just want to cut cut cut jobs. Yeah sure the reports look good on paper. But workers are being abused out there.

It’s corporate abuse of employees and it trickles down from the top.

In 1991 I bought Bank of New England stock because eight insiders bought. It went to zero. You have to pay for your education in the stock market (Jesse Livermore/Edwin Lefevre). It was the last bank stock I ever owned since they are really just legalized Ponzi schemes. However, this piece of history is well worth knowing concerning the failure of Bank of New England:

“My Treasury colleagues and I joined representatives of the [FDIC] and the Federal Reserve Board in a conference room on a Sunday morning. We came to understand that either the FDIC would protect all of the bank’s depositors, without regard to deposit insurance limits, or there would likely be a run on all the money center banks the next morning – the first such run since 1933. We chose the first option, without dissent.”

— Now-Federal Reserve Chair Jerome Powell, speaking about the Bank of New England failure in a 2013 speech about “too big to fail” banks

History repeats itself with Silicon Valley Bank. Whatever the next financial disaster the majority of investors believe the Fed will step in, and they might. But all the Fed really wants is an orderly decline in the stock market (good luck) since asset values are causing persistent inflation. History repeatedly shows huge fast rallies in bear markets. When you own a stock long you can only lose what you paid for it, but when you own it short you can lose orders of magnitude more.

There is a saying in technical analysis that ‘there are no triple tops’ (see QQQ) so maybe there will be a giant blistering rally with the Nasdaq 100 going to who knows 14,000? 15,000? That is why I am 60% SQQQ and SPXU and 40% cash. Probably not, but I am ready.

Microsoft at 11 times sales is closer to a market top than a market bottom.

Yeah who woulda thought a bank, where all the money is, could go under.

It defies logic

Perhaps the Reddit forum Wall Street Bets can keep one open indefinitely. Haha. Those guys over there are completely insane

“How fast do you want the Fed to blow up stuff? ”

I know what you are saying (and the longer ZIRP was allowed to continue, the more interlinked/correlated all “assets” became) *but* the Fed played a central role in creating the US’ ZIRP crackhouse economy – the destruction of the crackhouses is not only necessary…it is inevitable.

The argument is that “slow walking” the detox process avoids/limits cascading panic (that would cause *uneccessary* destruction…in contrast to the inevitable destruction of assets that cannot survive without phonied-up ZIRP).

Would that 1% of that concern/worry been displayed by DC decision makers over the 20 years of saver expropriating ZIRP.

12 months into QT….

Did anyone imagine the balance sheet would be circa 8.5?

As the Fed attempts to reduce the balance sheet and cure one problem, other problems pop up in the banking system requiring liquidity measures.

Seems like for every action, there is an equal and opposite ‘reaction’.

Oh what tangled webs they weave…

When you have a multi-year crack orgy, a hangover is pretty predictable.

This isn’t a case of “poor DC” being blindsided/backed into a tragic corner…it is the inevitable consequence of 50+ years of absolute crap decisions and ignoring the (apparent) 49% of the population screaming warnings…for the sake of an utterly insular political class (which includes those “businesses” that exist only because of political patronage).

This is why I come here over and over: “I’m getting tired of fighting the ZH BS here over and over again. What goes on at ZH stays at ZH.”

ZH turned into a disinfo clickbait mill. But what really soured me on them was the ethics, or lack thereof. After a decade of whining about QE, they instantly started on the pivotmania BS once Powell started tightening. You can’t do something like that without shattering your credibility into 1000000 pieces. Oh and they were wrong about it too. Both deceitful and incompetent is a bad mix.

What is ZH????

The online publication Zero Hedge.

…just gotta love the arrival of a possible inflection point when folks are asking ‘what’s ZH’ on Wolf Street!

(I trust our esteemed host is sporting a bit of a grin…).

may we all find a better day.

The MBS chart is interesting. If you extrapolate MBS movement, the Fed won’t have MBS back to pre-pandemic levels until around 2035.

The pace of MBS decline is WAY TOO SLOW. It will be distorting housing markets for decades. This is NOT part of the Fed’s mandate by any stretch of the imagination.

Housing is the biggest asset in the economy, in dire need of stability, yet the Fed is flooring the gas peddle like Thelma & Louise.

Please sell the MBS for sanity’s sake.

100% agreed. They really are dragging this out. I’m sure they have their reasons, but drawing this down does seem painfully slow.

Djreef,

Stuff is already blowing up. How fast do you want the Fed to blow up stuff? That’s what you need to ask yourself.

Bobber et al:

You’re wrong about 2035. You need to understand how MBS work.

1. If the Fed ever cuts interest rates, the roll-off of MBS will become a HUGE torrent because there will be a tsunami of refis, which means mortgage payoffs, and the principal is passed through to MBS holders. And those MBS will vanish off the balance sheet.

Back during the pandemic when interest rates dropped, and refis exploded, the roll-offs were in excess of $100 billion a month. And the Fed had to buy a HUGE amount in MBS to replace them, and buy a huge amount on top of it to add to its balance sheet.

2. this torrent of refis and therefore mortgage payoffs cause the pool of mortgages backing the MBS to shrink to such a point that it’s not worth maintaining the MBS, and the issuer (such as Fannie Mae) will call the MBS, meaning pay holders for it and withdraw it, and repackage the remaining mortgages into new MBS.

3. The average 30-year fixed rate mortgage gets paid off in about 8 years.

4. Calling MBS happens even if there isn’t a torrent of refis, it will happen just a little more slowly. MBS are called within a number of years – sooner during a refi boom, and later when there are fewer refis.

So don’t worry, those MBS will come off quickly if mortgage rates drop, and more slowly if they don’t but they will all be completely gone by 2035.

If I were to guess, just extrapolating how quickly things went south after 4.5% interest rates, then I’d wager that MBS never fully rolls off the feds balance sheet

They’re done nothing but go up since 2012.

The next hiccup, whether it happens 2-5 years from now, fed will just start buying MBs all over again

Troy,

The prior QT ended in the summer of 2019. But MBS continued to run off until the March 2020 pandemic emergency. The Fed let them run off and replaced them with Treasury securities after QT had ended. They will do that again. After QT ends, MBS will continue to run off, and will be replaced by Treasuries. The Fed doesn’t like MBS on its balance sheet for lots of reasons, including that they’re messy to administer and are very unpredictable because of the pass-through principal payments.

Yes exactly. The real Fed put is on housing.

They had no mandate to buy MBS.

They’re ruining our entire society.

The Fed are the problem.

You’re right. I guess it’s wishful thinking that they might get back down to 2% more quickly.

Wolf,

What’s your take on inflation though?

P&G and Coke have been raising prices like crazy (double digits). McDonalds CEO mentioned broad-based inflation and grain prices feeding into the proteins.

We also have sticky service inflation.

Unemployment is still crazy low and consumer spending is high.

People aren’t getting the message!

50 bps vs. 25 bps probably won’t blow anything up, but it may drive home that the FED is serious.

Stock Market, Bond Market, Housing and Crypto are all still inflated.

Stocks are historically expensive.

Junk bonds have a low risk premia.

Housing crazy unaffordable.

Crypto… shouldn’t exist (as a risk asset)

J. Pow says he doesn’t care, but what about the “Wealth Effect” where people spend more? They feel rich and spend more, causing inflation.

*Feels* to me like the FED’s “soft landing” is a glacial move. A mild recession is not the end of the world.

Honestly, I’m of the belief that a mild recession can be good (clear out the garbage, teach people to save money, etc.)

The Fed, Govt, and consumers are all share responsibility for the housing inflation fiasco, by differing degrees of course. Yet we all have a role in this “Housing is an Asset” chaos mentality, which has created social, demographic, environmental, etc issues that could take decades to unwind and resolve.

Companies sell what consumers want, and being a consumption driven species, we can’t seem to stop wanting for more. Even the states get involved wanting more, by require mega sized homes be built in order get into the best school districts. Short term Win-Win with higher property taxes and more state level “GDP” to service these mega homes. Long term, not sustainable…

Per NAHB, the Average (mean) square footage for new single-family homes increased to 2,561 in 2022.

Prior decades:

1920: 1,048 square feet

1930: 1,129

1940: 1,177

1950: 983

1960: 1,289

1970: 1,500

1980: 1,740

1990: 2,080

2000: 2,266

2010: 2,392

It’s way too slow. We need Paul Volcker 2.0 on steroids.

Volcker’s Fed Funds rate was 21% in 1981 Prime rate was 22.5% approx.

Ah….. history

I agree. My guess is that the fed knows that the housing market is giant bubble, and they are way too scared to really deal with it.

No.

If the Fed sells a bunch of MBS into the market, the price of those MBS will fall (even more than they have already fallen). That will imperil the balance sheets of banks that are holding those MBS.

SVB died from this exact problem, without the Fed selling any MBS.

I thought the problem you are describing involved CMBS as opposed to RMBS, but I’m no expert on this.

That’s not to say that selling RMBS wouldn’t cause their price to drop. It would, from what I understand, just as you’ve described. But I thought that the SVB failure was affected more by CMBS. In any event, I think that many people would like to see RMBS selling by the fed because it would elevate rates and speed up the housing correction. As you have indicated, it would also depress existing RMBS prices, and that could cause stress for RMBS holders.

“The roll-off has been below the cap of $35 billion per month because home sales have plunged and refis have collapsed, and therefor fewer mortgages are getting paid off.”

When sales/refinance increase, so will the rolloff, all things being equal.

Mortgage rates more than doubled, with prices stagnating/decreasing, but selling mbs and raising mortgage rates further is stability? Lol what?

Price aren’t decreasing relative to 2019 levels. Prices are up 100% in many locations. Prices must come down a long way to achieve a sustainable market that can stand on its own without constant Fed intervention.

The baseline is 2019 or 2000, not the recent price peak. The artificial stimulus has been in place for decades, destroying price discovery in the housing market.

Bobber,

Couldn’t agree more and the fed needs to be less responsive to default issues, ie liquidity provision, if it wants disinfection it must not fight price discovery nor the exo3cted and desireous affects of interest rate hikes,

“Please sell the MBS for sanity’s sake.”

Dare they actually take a loss? Ney

hey floating one:

sooner AND later ALL of WE the PEEDONs mUsT come to realize the FRB is NOT working for US, and never has done

FRB works FOR their owners, as do most folks.

FRB owners are BANKS far damn shore…

Let’s at least try to get that very very important delta between what they say and what they do very very clear on Wolf’s Wonder.

I still don’t understand why the Fed didn’t sell off MBS’s before they started raising rates. They could have unloaded most of their MBS’s at a profit before they threw the buyers under the bus by raising rates.

Sellling the MBS’s first would have also put a damper on the housing bubble since selling the MBS’s would have raised mortgage rates.

MBS’s seem to specifically target mortgages so specifically selling MBS’s to target the housing bubble would have been more surgical.

Am I just being a armchair quarterback? Was there a reason for the order of what the Fed did?

There is so much complexity and interactions in the Federal Reserve’s operations that it is amazing that an independent US Government Inspector General office is not a part of Federal Reserve operations.

I keep hearing folks talk about how insuring all deposits without limit would create moral hazard and that big depositors are supposed to be aware of the risk they’re taking when the have deposits over the FDIC limit.

That sounds reasonable on the surface, but how is a prudent depositor supposed to evaluate specific banks?

I tried looking up some stats for FRC on the FDIC site and the data there is from last quarter; so totally out of date and was quite limited. I wanted to find the percentage and total on uninsured deposits as well as some idea of what their assets look like, but FDIC had nothing like this (at least that I could find).

The day SVC started failing, Moody’s still had them rated highly and of course, SVC passed the FED’s stress test and presumably was in reasonable compliance with FED regulations. I have read that regulators were concerned about the level of uninsured deposits and their asset mix, but apparently not concerned enough to force SVB to make significant changes.

So how is a relatively unsophisticated SMB with say a $1-5M operating account supposed to vet individual bank risk, especially when things can change dramatically overnight (especially when the likes of Moody’s didn’t see this coming)? Quarterly reporting just isn’t enough, especially for SMB accountants.

It seems like something close to a real-time reporting system with way more detail and perhaps health scores is required if the FDIC expects under insured depositors to be able to actually vet banks and since bad things can happen fast, there should probably be some kind of service that can alert depositors when a bank’s health changes significantly so depositors can quickly transfer their money elsewhere. Some kind of stop-loss service that could do that automatically might also make sense.

The problem though is that real-time info like this could encourage bank runs: exactly what the FED and FDIC want to avoid. That’s why they don’t publicize for years when after bank has to use the Discount Window, which is exactly the sort of information under insured depositors need in real time.

So, I believe it’s only fair for FDIC to cover all deposits without limit. There’s really no way for regular people or SMBs to proactively evaluate bank risk until after it’s probably too late.

Now share and bond holders are a different story. They presumably know that they’re taking a significant risk and are presumably better suited to evaluate risks.

I’ve also seen people talk that banks take excessive risk if they are not disciplined by under insured depositors. That seems ridiculous when there’s so little information available to assess risk. Share and bond holders are in a much better position to do that, and isn’t that what the regulators are for anyway?

“I wanted to find the percentage and total on uninsured deposits “: Visual Capitalist has a graphic at one glance. I saw it and was shocked. Citi especially seemed to me (as historically) a tower of moral hazard. But all the big banks are somewhere around 50% uninsured.

Next question: where would a run, run to? Just bigger banks. This could scramble a lot of regional banking/finances. IN an age of instant digital runs, it could put sudden loads on regulators they are not staffed to handle, IMO. So, anything like a medium-to-worst-case panic concerns me.

Yellen’s decision to insure all deposits of recent failures sets a precedent that suggests that “non coverage” of any deposits going forward would meet with legal objection by the uncovered …..and likely lead to all deposits being insured.

That’s a $17 Trillion decision by Yellen.

What Yellen did …. seemingly unilaterally and with questionable authority….is HUGE, and dangerous.

Uninsured deposits is a form of market discipline.

Yes yet another case of illegal overreach and massive incompetence from the Fed/Treasury. Huge decision taken seemingly reactively and without a mandate that yet again sees these incompetent bureaucras, plugging holes to hide the implosion of the huge bubble blown on their watch.

There is a service (brokered deposits) for businesses to spread their deposits across many banks for a fee. the depositors are creating this risk to save a few nickels, and exposing us all to it. “Blame the government for everything in lurid terms of contempt” is my last resort when considering such things. There is a problem, there is a risk here, and energy is best put toward figuring out actual solutions,, or considering who should bear it and how. Hasty blaming is the easiest low-calculation thing to do: call someone stupid or crooked. Any illiterate can do that (and does as a first resort).

Yellen did this to protect friends and family members aka donors of democrat party.

We all should know for whom the FED works for and it’s not the common people.

FED likes to hide behind the mandate of price stability and employment rate to not show their true motives.

If you have enough money to be concerned about losing your deposits, you have enough to do due diligence.

Scenario 1) you have <$250k: no deposit concerns.

Scenario 2) you have $250k to $3mil: put your money in 5 different banks (minimal risk all will fail, and even if one fails you still get most money back) or use treasury direct.

Scenario 3) you have more than $3mil cash: pay someone to do the research. Hedge.

My point is that middle net worth individuals may have to do a little more work to protect their deposits, but they can. High net worth individuals need to do the research that holds bad banks accountable or accept the risk of not doing the research.

Government must decide whether banks should be self-monitored or be monitored via increased regulation. We cannot have a situation where long-term risky loans are funded by demand deposits. That is inherently stable and leads to taxpayer losses.

In my view, the best solution is a requirement for banks to match the duration of deposits with the duration of loans. If banks can’t attract long-term deposits, banks shouldn’t be issuing long-term loans. In reality, they will be able to attract long-term deposit money if the price is right and they set loan rates above that.

The historical bank practice of duration conversion artificially suppresses long-term interest rates at taxpayer expense and promotes excessive debt buildup.

“We cannot have a situation where long-term risky loans are funded by demand deposits.”

Haha. That is the basic definition of our banking system. And of finance itaelf: match savers with those who use the savings in (risky) long-term enterprises and projects. That is finance capitalism. We MUST have that situation, but mitigate its risks. This is through good underwriting, insurance, etc.

The level of unrealistic “idealism” around here astounds me. Everybody who doesn’t get it perfectly right is a crook and a fool, and we should never lose? In what universe? Not this one.

An unrealistic idealist thinks the status quo can continue. Major changes are necessary the next few years to prevent financial system collapse.

Tax increases

Spending cuts

Banking reform

Debt write-downs

Read it and weep.

Also, please explain why banking must involve duration conversion, if you can.

The reason “depositors” don’t care about the LOANS they make to their bank is because they have been told they will be paid back “in full” no matter how badly the bank is managed.

That’s insane.

People should be provided with the choice to make loans to banks or actual deposits which cannot be lent out. If they choose to make a loan where the bank can use it to fund their loans, it should not be guaranteed by the taxpayer.

Banking system moral hazard has been possible for 90 years due to systemic confidence. Problem is over time, the unsound banking system the US actually has is only one of many “fault lines” in the financial system.

Every time I read about how it’s a non-problem (including on this site), it’s always based upon the implicit assumption that the entire financial system can’t fail with it.

What recently happened in the UK with pension funds is only one example of how a run on the entire financial system can start. The BOE was able to keep the system from crashing due to remaining market confidence.

One day, that will be missing and it’s “game over”. There are no “wizards” behind the curtain any more than there is in “Oz”.

I learn a lot from wolf street and the comments after.. Thank you!!

“Learn something new every day at Wolf Street.”

+++

EXACTLY why I send $$$ to Wolf every year!

And not many others of any ”ilk.”

Why the heck did the Fed buy MBS in 2021 when it was obvious to everyone that the housing market was overheating like Chernobyl. I’ve never read an explanation for that. It seems inexcusable. At the current pace of roll-offs, it may take 5+ years just to undo that 1 year of recklessness.

You have answered your own question. It was a colossal policy error–either the worst or the second worst policy error ever committed by a central bank–and one for which absolutely no excuse.

There’s no plausible lie that could explain it, and the truth is the sort of thing that can’t be admitted publicly (at least not contemporaneously; people tend to confess these things after they have excited public life).

Er, “for which there is no excuse.”

They bought MBS for the same reason they always prop up housing: because housing inflation doesn’t fully show up on inflation statistics.

This then means they can do more stimulus without people saying they should stop.

They’ve done this over and over since 1997. Over and over every single commentary states “inflation is 2%” when housing is up far ahead of wages.

Every single financial journalist writing these stories owns at least one house.

I think your probably spot on. The FED knew QE would cause housing prices to go up. They knew QE would benefit the top 1%.

They did this at the expense of dropping unemployment.

It is better to have people employed and complaining about inflation then having them unemployed with nothing to do but to go marching in the streets and rioting about not having a job.

Plus they have a solution to high housing to make sure people have shelters. They get the Government to offer low income housing subsidies or build low income housing.

3 things governments want to do to keep stability. They need to to make sure people have jobs (or unemployment money), shelter (or subsidies for low income shelter), and food (or food stamps).

That will keep people complacent. They do not want to tip the apple cart and lose any of those benefits.

I think the consensus is, the Fed was wrong-footed in 2021. It openly under-estimated expected inflation (as “transitory”).

That doesn’t mean it is always wrong, or a conspiracy. I appreciate Wolf’s calm and open disassembly of the parts, because a conspiracy theory is always far simpler to concoct and post, and is more sensational, attracting clicks (hello ZH). The Fed’s approach (now, not in ’19, not in ’21) appears pretty sound, to me, for now. It is edging up to breaking things, and pulling back carefully when it does. I wouldn’t want it to have things slip too badly out of control, and I doubt anyone here would (despite the posturing).

WRONG on 2 counts plp:

1. ”or a conspiracy” FRB is CERTAINLY ”a conspiracy” ,,, far damn shore. certainly ”A” conspiracy of and including ALL the ”banksters”… and certainly YOU know that.

2. I would absolutely want to see the ”GRANDEST CRASH” of all time, and in this case sooner rather than later…

This due to being one of those now considered elderly who have saved and so forth for the last several DECADES to be sure my beloved spouse will be OK. TOTALLY with DC on this,,, and I suspect ALL the old folks with good spouses almost certain to outlive them will agree…

”STABILITY” for me means my spouse will be able to live at least as well as my grandmother did, by herself, with her annuities and SS.

US old and elderly guys are likely to become much more angry with ALL the politician puppets IF we cannot make sure our beloved(s) will not be safe.

Vintage, I certainly respect your motives there.

Mistakes should be corrected as soon as possible, otherwise the mistakes become embedded, create reliance, and lead to other problems. A correction should be proportional to the underlying mistake in terms of speed and magnitude.

>>Why the heck did the Fed buy MBS in 2021 when it was obvious to everyone that the housing market was overheating like Chernobyl.

The possible answers in my mind, and all three may be true:

1. Fed is depraved and will do anything to enrich the rich and devalue the labor of the poor.

2. Fed thought the rest of the world would still accept USD printing and sell us goods at lower real prices, and that the “wealth-effect” from house price inflation would maintain the consumption economy during pandemic.

3. Because of perceived (not real) mortgage guarantees by US gov, Fed wanted to suppress mortgage rates, because a weakness in MBS valuations could be construed as a weakness of USG bonds. Said in another way, Fed wanted to limit the rate spread between USG and MBS.

Of course, number2 is no longer feasible. De-dollarization ov global trade (no more reserve currncy) and inflation means MBS no longer realisticall can be supported, and Fed has to concentrate on supporting USG bonds.

I meant to say number3 is no longer feasible. Fell free to correct comment and delete this meta-comment. Can we get an edit button please :). I know it is a spam danger but …

NAR – not to worry, having to return to clear up our faux pas is a better indicator that we’re probably human…

may we all find a better day.

How is the yield curve so messed up with the Fed shedding treasuries?

What we need is a normal POSITIVE yield curve.

Long maturities with the risk and uncertainty deserve higher rates, IMO.

Inverted yield curve is a signal that Wall St is front-running.

Existing long bonds are bid up (means: interest rate bid down) because Wall St is thinking it can buy long bonds and profit on them when Fed lowers interest rates again. Also known as front-running the anticipated Fed response.

BUT: the Fed is limited by two very inconvenient realities: De-dollarization (weakening reserve currency privilege) and inflation. There is no choice except keeping interest rates up.

Wolf

Today I red this

On Wednesday, House Republicans passed legislation that would tie last year’s increase in the debt limit to measures to reduce the deficit by nearly $4.8 trillion.

They argue that this should prompt Democrats to negotiate the terms of raising the nation’s borrowing limit.

The main components include:

Raising the debt limit by $1.5 trillion

Cut and limit discretionary spending

IRS Cancellation of Irrelevant Tax Enforcement Funds

COVID-19 relief

Revision of infrastructure and energy permitting laws

House Democrats voted against the proposed bill and called on Congress to raise the debt limit unconditionally. They highlighted the significant impact of the proposed spending cuts on various government programs.

The Senate is expected not to take up the bill; however, he will face increasing pressure to discuss or implement another proposal.

President Biden has warned he will veto the Republican bill and remains steadfast in his demand for an unconditional increase in the debt limit.

My question is, do you think this law will pass or will the debt ceiling be unlimited again?

I don’t think anyone knows the answer to your question. From the unwillingness of both sides to compromise, it looks like the debt ceiling crisis will be a major market mover. The strong estimated tax payments around April 18 raised the Treasury General Account balance to over $300 Billion exceeding $200 Billion estimates. Per Goldman Sachs this probably means the deadline for hiking the debt limit moves to late July. Stay tuned.

I think the stock market is shrugging off the debt ceiling issue. I suspect “the market thinks” the main thing that will happen is an interval of more posturing, followed by the usual hike. There is a limited window of dipped short-term treasury interest rates, is the reflection in the markets now. Congress will not seriously risk a sustained sovereign default. The GOP donors won’t sit around and lose trillions behind that. The adults in the room will school the noisemakers.

RickV

Debt ceiling has been raised more than 60 times by the Congress after the kabuki circus show!

Last year Sen Rand Paul introduced a bill to hold the budget at 2018 level. It got defeated soundly in the Senate (67 vs 30(?) This included 17 so called conservative GOP members.

Without deficit spending, the lawmakers will be out if their ‘lucrative’ careers/jobs!

“law will pass or will the debt ceiling be unlimited again?”

Which option is worse for the masses? That scenario will play out.

Why do they even have a debt ceiling when it is never enforced. They always expand it. They should have the debt ceiling automatically adjust to the CPI data.

Several of these graphs are weird. A monetary gimmick exists in theory for a long time and then gets used exactly once.

Reminds me of joke histograms like “Frequency of occurrence of March 2023.”

Love the graphs that show immediate context.

The magnitude and duration of Powell’s monetary policy blunder ensures that problems will metastasize.

Powell’s problem is that he thinks banks are intermediaries. Sure, banks need a positive balance of payments, but runs are what discounting is supposed to solve. And like Volcker, it shouldn’t be done as in Bagehot’s dictum.

You know current situation is only temporary. US can’t finance its debt at 5%. Long end of the market knows it.

What we are witnessing is a gradual silent government takeover of the financial system. When unsustainable behaviors exist for too long, the reckoning is too great to accept. The only palatable way out is complete government control over markets. Unfortunately, government can’t competently manage it, so the result will be complete chaos.

Look at Continental Illinois bank bailout: “Paul A. Volcker, announced that Continental Illinois would have unlimited access to low-interest loans”.

And unlike SVC, etc., bailouts Volcker didn’t expand overall FED credit in spite of the 6b dollar infusion. Using the net free (or net borrowed) reserve position of the member banks as a day-to-day guide in executing open market policy, the FED offset CI’s borrowings.

The rescue operation of the Continental Illinois’ dimension was limited and of short duration.

I think the slow roll is as perfect as we can expect. The weak are getting exposed, but with little collateral damage.

I don’t think we will have anything like the 70’s inflation despite the horrid money printing. What percent of the workforce were in union jobs with COLA built into their wage contract in 1978 vs. 2023? It was a self-reinforcing cycle.

I agree that the slow roll is the way out of the Fed’s Balance Sheet situation. It worked well for a while in 2017-2019.

But in an economy that is going well, you don’t need union contracts to keep inflation rolling… my employer just gave my division a 15% wage increase as a replacement to this year’s COLA… they are already having trouble hiring new employees and don’t need the existing ones giving notice.

On the NPR’s website is a page titled

“Fifty Years Of Shrinking Union Membership In One Map”.

It covers 1964 – 2014, state by state.

Just got my yearly union financial statement,seems to be losing principle at 3-4% a year . Should hire a qualified financial planner .

I overall dont agree with the notion that the pace of Fed QT is really that aggressive. They ran up that balance sheet so fast and the downside move is much slower. But the Fed is actually withdrawing QE much faster than the ECB or the BOJ, which are so far behind the curve. IMarkets are global and money is fungible, so the large balances of debt owned by the ECB and BOJ (which owns equity too)impacts our markets also.

Ask yourself just one question. If the global central bankers were to announce that they intended to sell off the balance sheets to zero, irrespective of the economy, how would market prices change? Would the PE ratio of the stock markets remain unchanged? The one thing holding up the PE ratio of all global markets is central banking activity.

Late 2023 and 2024 are shaping up to be very transformative years. Will we see a return to honest fundamental economics, or continue the charade of MMT theories?

They can keep the illusion alive for several more years by targeting 4-6% inflation, understating the subjective elements of inflation metrics, and communicating a 2% inflation goal. They might get away with this under the guise of “being careful”.

I agree with you.

They have kept this charade going on for few decades or so.

Only thing happening is: dollar is losing value gradually.

In the last 3 decades or so, dollar lost almost 75% plus or more.

DM: Silicon Valley Bank failed due to ‘textbook case of mismanagement’ along with weak regulations and lax supervision, the Federa; Reserve says in scathing report – as it blames social media for driving bank run within HOURS

The report on Friday, authored by Fed staff and Michael Barr, the Fed’s vice chair for supervision, takes a critical look at what the Fed missed as Silicon Valley Bank ballooned in size in recent years.

Could be First Republic. Some analysts say today is the day FDIC steps in. Of course analysts will say anything, but FRC is at $3.50, down 48% for the day, and it is Friday. I still wonder what happens to that $30 billion the TBTF banks deposited in First Republic if it goes belly up. I am sure that $30 billion is not insured, except for $250,000 per bank.

On a perhaps not unrelated event, Treasury released its new fixed rate today on I-bonds, in advance of May 1 which is the usual date of such releases. The new fixed rate is .9%, relatively high, with a new composite rate of 4.3%. It is still well below 3, 4, and 6 month Treasury yields.

“JPMorgan, PNC Bidding for First Republic as Part of FDIC Takeover.

Seizure and sale of the distressed lender could come as soon as this weekend.” – Wall Street Journal 11:03 pm ET.

The details will be interesting.

There was 1/2 Billions $ worth of FRC stocks traded this last Friday.

Really weird that many people ignored the reality staring them in the face. The $5 stock will become 10cents over the weekend. Why do people take that risk? Just nut.

Terrific, much-needed distillation of recent financial whizbangs.

The rate of decrease is about $1Trillion/yr. We want to see at least below $6T, so we are looking at another 2.5 year of QT. We might have some up and down and that will drag this out another 1 year, like the banking snafu. Next 3-5 years, the market will be in turmoil. It had been on a tear since January since everyone is expecting the FED to pivot. But with QT and credit tightening at banks, we will see if all this bull talks are but craps.