It’s just not encouraging at all. Inflation is just shifting around, dropping in some product categories, rising in others.

By Wolf Richter for WOLF STREET.

Prices of energy goods and services that consumers buy plunged in March from February, and have been dropping for months, according to the PCE price index data from the Bureau of Economic Analysis today. Food prices dipped in March from February for the first time, after months of slowing price increases following the huge price spike through mid-2022. Durable goods prices dipped but barely, and at the lowest rate in months; they appear to be bottoming out. And prices of services rose. And much of the month-ago released PCE price index data for February was revised higher today.

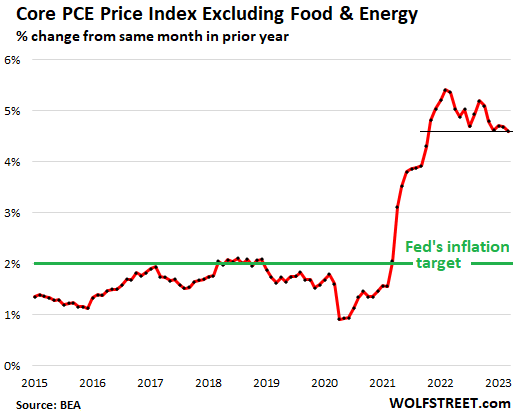

It boils down to this: Core PCE price index is stuck and stubbornly high, as inflation churns from one product category to another.

The “core” PCE price index is the yardstick for the Fed’s inflation target. Its the PCE price index without food and energy products. On a year-over-year basis, it jumped by 4.6%, same as in December and July 2022, nine months ago! The Fed’s inflation target is 2%, and it uses this core PCE index as yardstick. But core PCE has been going sideways at just under 5% for months.

A month ago, the BEA reported the February core PCE increase as having risen by 4.6%. Today this was revised up to a 4.7% increase.

How the core PCE price index has remained in the same high range can be seen in the month-to-month movements, which have been jumping up and down in the same range since 2021, where a couple of drops were followed by another jump or two.

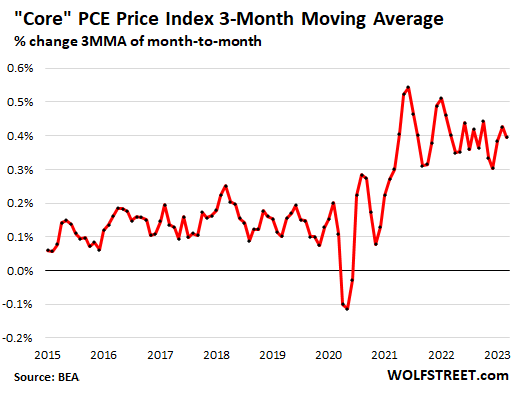

The three-month moving average smoothens out the month-to-month ups and downs of the core PCE and shows the trends more clearly. It’s just not encouraging at all. It shows that underlying inflation is stubbornly entrenched, shifting around, dropping in some product categories while rising in others.

This is just not encouraging at all:

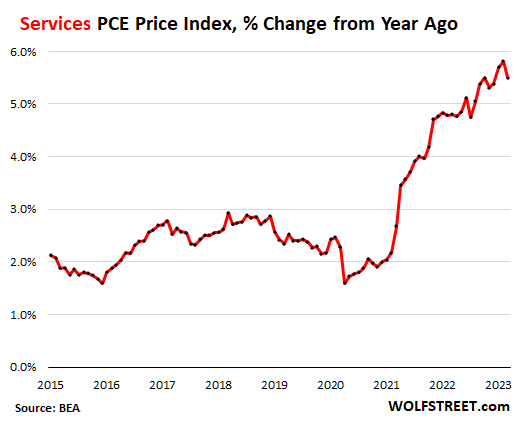

Inflation in services.

Services is where the majority of consumer spending ends up. Services matter. They include healthcare, housing, utilities, education, travel, entertainment, restaurant meals, streaming, subscriptions, broadband, cellphone services, etc. Inflation is particularly difficult to wring out of services.

The PCE price index for services jumped by 5.5% year-over-year in March, compared to the upwardly revised 5.8% in February, which had been the worst since 1984:

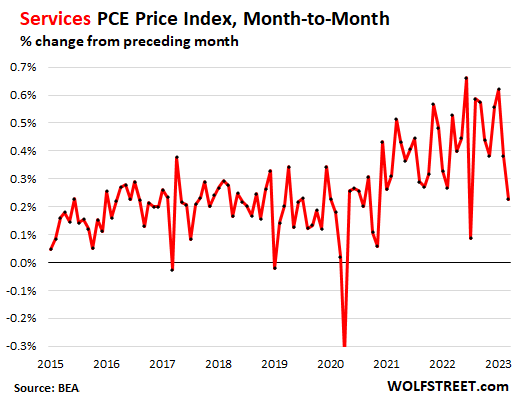

On a month-to-month basis, the PCE price index for services rose by 0.2% in March from February. Services here includes household energy services, such as gas and electricity, which plunged (especially natural gas) from February.

There had been a similar only bigger outlier in July 2022 that then promptly reversed the following month:

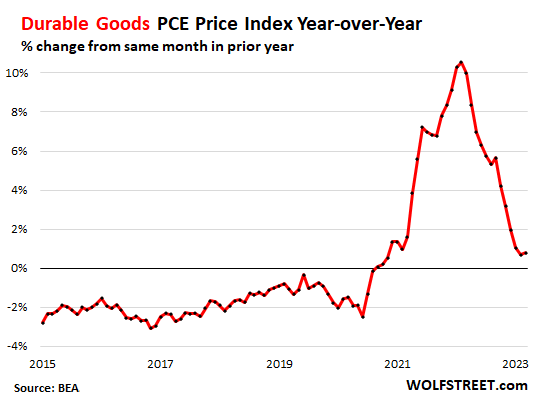

Durable goods prices.

The PCE price index for durable goods – new and used vehicles, appliances, furniture, etc. – dipped by 0.1% in March from February, the smallest decline in months, as price declines are fading. Year-over-year, durable goods inflation was 0.8%:

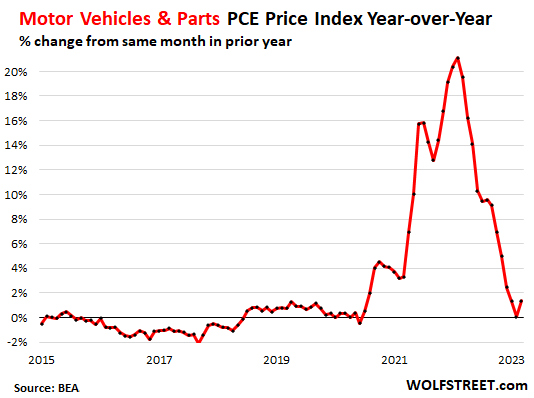

Motor vehicles and parts were flat month to month for the first time after five months of drops. This caused the price index, on a year-over-year basis to bounce off the 0%-line.

The price drops in used vehicles have been a big factor in pushing down durable goods prices and the core PCE priced index. But it looks like that factor is somewhat fading – another sign of how inflation is shifting from one product category to another:

The PCE price index for gasoline and other energy goods plunged by 4.6% in March from February and by 20% year-over-year.

The PCE price index for food fell by 0.2% in March from February, which pushed down the year-over-year increase further, to 8.0%, the least terrible year-over-year increase since February 2022.

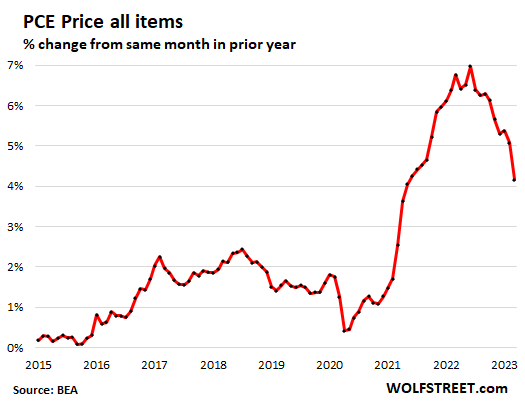

The overall PCE price index rose by 4.2% year-over-year, the slowest rate since May 2021, pushed down by plunging energy prices and by some durable goods prices, but pushed up by services prices:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Inflation also comes in waves if historical episodes are studied.

“as inflation churns from one product category to another…”

I can tell you that I’ve seen ‘categories’ go from 20% prices increases to many times these

why? because they can and about time from holding back

Services are out of control

2 weeks ago my son needed new AC

he bid it out before I gave him my AC guy

1st bid on 5 ton AC – $14,000

2nd bid – $22,000

my guy who doesn’t mark up and charges $1,500 per install

$5600

guess who got job and prompt PAYMENT

in 2022 – he made simple $300k

“as inflation churns from one product category to another…”

and there is good reason and wisdom why the Federal Reserve Act instructed/mandated the Fed to “stable prices”. For once inflation, and the perception and psychology of it permeates an economy, it is difficult to extinguish. Producers know they can raise prices, and they do. As does the service industry. And unions go on strike. And it aint over yet.

spoke with my brother yesterday

he was ecstatic about PCE

was buying I-bonds and gloated about yield

I did inform him

that ‘inflation’ is really DEVALUATION of fiat $dollar

he quipped about buying more gold/silver

Yup. Too much stimulus. Demand outstripping supply.

As our company’s pricing guy, it is hard to justify price reductions right now. I have dropped prices strategically in the past in the name of capturing market share. I will wheel and deal to get an order when the situation calls for it. It is a different market right now.

Our production capacity is 100% booked. Same for our competitors. Normally we would tolerate business with 5-15% gross margins to help cover overhead and keep utilization high, where target is 25-30%. Keeping that low-margin garbage work out of the backlog is my primary concern right now. If I’m going to sell any remaining finite shop capacity to anyone, it’s going to yield 10% net, not 1%. Our employees have mouths to feed too.

As long as demand outstrips supply, inflation will run hot. There is just no real incentive to reduce prices right now. I will be the first to do so when price pressure shows up again.

Perfect example why PPP was a bad idea. All it did was create monsters as that one…

There is also an incentive to slip in a price increase while the increasing is good. Same as 2008-9-10. Long ago pricing was costs+margin. Now pricing is what the market will bear and much less to do with costs.

This is why defeating inflation, once it has reached this high, has always required the FFR to be significantly in excess of CPI YoY.

I think we’re looking at an FFR of 8% or above, assuming the Fed is serious.

Their “inflation fight” is actually an operation to try to entrench asset pries at a higher level while pretending to be serious about their stable price mandate. It’s a massive fraud scheme.

This is very close to one of my theories. US corporate profits have increased 60% since pre-pandemic. I think they want to hold on to those profits. The RE and tech ponzies are part of that, but at least the RE ponzi has to be broken or there will be tremendous pressure for more fiscal stimulus.

Powell screwed up and created this beast with his $15T M1 money print in April 2020. Why is this arrogant fox STILL in charge of this ravaged henhouse?

The legal definition of “transitory” is (essentially): moving from place to place. When JPow said inflationary is transitory, he was using the legal definition, not the plain english definition. They always stick with legal definitions if at all possible. So, in that context he and Yellen were actually telling the truth back then. Inflation was and is “transitory”, as in moving from place to place.

The big tech posted quaterly results with negligible revenue growth, when corrected for inflation (-2% to +2%). The year on year EPS actually decreased, even without inflation correction.

These are pathetic results for growth companies with P/E above 25 and even announced stock buybacks won’t make up for future declines.

The mainstream media only covered analyst expectations beat and markets jumped. With this circus, wallstreet once again proved that it believes that it’s investors are morons and they can easily be manipulated and screwed.

I hope these investors remembered how to invest on fundamentals and not on meme.

It was funny how they said Microsoft was saved by their cloud unit. Yet, Amazons AWS tanked, due to customer company budget cuts.

Who to believe?

Microsoft one of the most expensive tech companies 😑

True Leo, check out this Thursday’s after hours trading for Amazon. Some fools bought it at $122 and then it crashed an hour later to $107.

Amazon’s earnings call was a major emotional roller coaster ride for those after hours speculators.

I think the April CPI to be released in May will be a shocker as it would change direction to increasing like it did in UK.

I guess Fed’s 0.25% hikes is inflationary policy as wallstreet is able to sell their pending Pivot story.

UK treasuries are already yielding more than US, and still no control of inflation.

Oil and gas are moving up again. The saudis have restated their intent to lower supply to keep prices where they like it.

The US is getting no help from oil producers to punish russia with low prices. They are on their own with releases from the strategic reserve.

Restarting our domestic oil production would go a long way in breaking the inflation psychology. One wonders why this is not done.

I don’t wonder about it at all. You would have had to be on a mountain in the Rockies to have missed the reason…

Where did you get the malformed idea that domestic oil production had stopped?

And casino is certain pivot any moment. Think this time is different though….we have landed in a parallel universe where make belief is the norm.

So bad news for consumers is good news for Wall Street. Layoffs : bad for consumers, celebrated by Wallstreet. High gas prices : Bad news for consumers, good news for Chevron translating to good news for Wallstreet. 0% interest rates: Wallstreet gets free money to gamble without any consequences, consumers are told its good for them, but really they get shafted 3 different ways without even realizing it. So I guess it is in Wallstreets interest to keep the misery going.

Don’t think we can expect more from the degenerate gambles in the Wall Street. What amazes me how your own government and policy makers chosen to supposedly help the Main Street are hell bent on making their life difficult. That’s the question imo

And JP Morgan predicting $380 a barrel oil ,game over

Seems like consumers are doing well, no? Buying stuff despite higher financing costs. Few worries about their jobs or banking cash for a rainy day. Buying upmarket cars rather than $20k entry level Nissans and Kias. Lots of luxury goods spending.

It actually is a pretty rosy picture. Now, what is reassuring to “Wall Street” is inflation never did spiral higher despite demand not cratering. No stagflation when the drivers of inflation today are more discretionary than forced / fixed. Of course, to the impatient the sideways trend as demand adjusts is somehow perpetual – when in fact the turning point from all leading indicators is right around the corner.

We will see employment slacken, demand will drop as cash is depleted at the same time as rates remain high, and inflation will fall back to normal (2%-ish) levels. Of course there will be overcorrection too – demand dropping a bit more and inflation possibly cutting across the 1% mark and dangerously close to deflation.

For those cheering the thought of lower price levels (rather than lower rate of increase) it is akin to reminiscing about the middle ages when life was quaint. Makes for nice picture books for middle schoolers.

“For those cheering the thought of lower price levels (rather than lower rate of increase) it is akin to reminiscing about the middle ages when life was quaint. ”

How is that? Is reminiscing about life in the Middle Ages common?

Yes. It is both common and reflects ignorance of conditions and consequence.

Life was “simpler” but also nasty, brutish and short.

Maybe “simpler” applies to some idealized view of 1950s America, but I’ve never heard that view applied to the Middle Ages. When I think of the Middle Ages, I generally think of mass death from the plague, religious war in the form of Crusades, and Vikings pillaging Europe. When it comes to the condition of life in the Middle Ages, I’m guessing people are less ignorant than you think.

Nothing much has changed since Hobbes’ day in that regard — still nasty, still brutish, and getting shorter every season.

We live to serve the job creators. Stop noticing things and get back to work, wagie. The stock market is up, things are good. Think of all the jobs you create with that 30% rent increase.

“We’ll make them so poor they can’t afford not to work”

It’s a simple game inflate homes,stocks,precious metals. Crash asset prices buy everted for 30- 40 cents on the dollar . Rinse repeat .It’s such a mess even the Pros can’t figure it out ,unless your in the billionaire CLUB

For the last time, precious metals are NOT inflating! Gold and silver are both circling the toilet! Do you see gold at $2000? Or silver at $25? Both prices they attained decades ago! So, no, they are not inflating! They are never going to inflate! Enough already!

PMs will inflate when the dollar starts to wobble as the premier reserve currency. The physical PM market is so small that derivatives can easily blow it around to the downside, where Western CBs like it. However, CBs seem to be net buyers of gold these days, and its utility as a reserve asset is once again recognized. No modern nation will ever adopt a gold standard for domestic purposes because pure fiat is too useful to central governments, but gold CB reserves as insurance against hostile sanctions and geopolitical upsets, and as support for international trade, have good logic behind them. Gold was $20/oz in 1933 and it’s $2000/oz ninety years later, and so it’s a decent long term inflation hedge, but it’s not tradeable for most investors. It’s insurance.

Occam, I think your explanation is about as good of one I’ve ever read. That is… I agree with you.

Escierto ‐ think of gold/silver as a CDS against the USD.

Its insurance that costs money as long as it doesn’t pay out. But if the goldbugs are right I wouldn’t want to be on the other side of that trade.

From goldprice dot org website, price of gold in USD:

1 year. +5%

5 years. +50%

25 years. +499%

Silver shows similar change in price.

What’s good for General Bullmoose is good for the USA.

We are back to the 70s with on and off inflation, with a big difference this time, there is no Volcker around. Bond holders will be taken to the cleaners while waiting for deflation that will never come.

If there is a small crisis or inflation comes down to 4%, Fed will overreact as usual on easing side and inflation will shoot up again. It’s unwise to keep your savings in the currency of a debtor nation.

All assets are being devalued equally by the loss of purchasing power of the dollar (inflation).

But asset prices have also tanked or have started to tank: stocks, cryptos, bonds, RE, CRE, etc., and these losses are on top of the loss due to inflation. Gold has been spared the selloff, but it’s not paying 5% interest either, so you have to take that into consideration.

Hey now, no talking about RE drop and adding inflation drop. :)

Wolf,

So one has to assume 25 basis is a lock w a chance for 50 maybe.

I would put the odds on a 50 bps increase in the FFR as less than five percent. That being said, I think the meeting of the Federal Open Market Committee (FOMC) of the Federal Reserve Bank of the United States next week should be contentious.

On the one hand we have the doves while on the other hand are the hawks. The doves seem too feel that loose monetary policy is preferable to restrictions on the creation of fiat.

The hawks are like the doves of a by-gone era. Afraid of the consequences that could happen if Jay “Volcker” Powell emerged from the shadows in frustration that his loss in his fight against inflation, like Volker.

I’m not counting on 50. I think that’s a real stretch.

IMO we will get the word “pause” in the next hike announcement.

The language will be cautionary but perceived bullish. Just a guess.

Wolf, DJIA just went positive on a year basis :P

DJIA 34,098.16 it’s up 796.23 which is 2.39%

They’re all up huge in the last 5 months or so though.

Nothing says looming recession like a rallying market haha. Valuations still suck too.

Bond yields don’t look great and Junk Bonds are in a bubble (low risk premium).

Sheller CAPE 10 still elevated. Housing unaffordable. BTC is still at like $29k.

Unemployment still low, spending still strong.

Powell wants to be famous for his soft landing.

As long as bad news (recession or uncontrolled inflation) is met by markets going up the system is broken. We are on the wrong side of the feedback curve. If the system is working correctly, Fed loosening is a bad sign and should correlate with market declines.

My opinion is that until good news correlates with market increases and vice versa, the tightening must continue. Until the market is looking for future real growth rather than future opportunities for rent seeking money transfers, the Fed is not doing its job of making the money supply stable.

As a mechanical example, in a car with a slipping clutch higher RPM often correlates with lower speed. The answer is not to give more gas but to fix the clutch so that the power source can transmit its power to desired motion. The Fed lowering rates is pressing on the gas. The market celebrates the increase in RPM but the car isn’t going faster. Fix the clutch by removing rentier liquidity and then we we can celebrate the increase in RPM because the car will be going faster.

WaterDog

1. The DJIA is not a stock market index, it’s an “average” of the price of 30 stocks, dominated by United Health, which weighs nearly 10%, and Goldman Sachs, which weighs about 7%. It never went down a whole lot to begin with.

2. A year ago was during the big sell-off, and stocks were down a lot, so compared to that sell-off, yes, it’s up.

3. The DJIA is down 7.7% from it’s high on Jan 5, 2022

4. The DJIA is back where it had first been two years ago, on Apr 16, 2021

Also:

5. the Nasdaq is down 24.6% from its high in Nov 2021 and is back where it had first been in Nov 2020.

6. the S&P 500 is down 13.5% from its high in Jan 2022 and is back where it had first been in April 2021, two years ago exactly.

“Nothing says looming recession like a rallying market haha. ”

Prior to the GFC the S&P 500 topped in October 2007. The subsequent recession was dated from December 2007. The big stock market declines didn’t really start until early fall 2008. I don’t know how close a recession is, but I know markets can rally heading into one.

Wolf,

My point though is that assets are re-flating. They should be de-flating for an orderly soft landing.

Yes, it initially dropped on inflation. But now, with all the rate increases the market re-flates???

Yes, the bubble is smaller than the peak. I agree.

Warren Buffett has famously said that rates are gravity to stocks.

Gravity isn’t working, because the market doesn’t believe the FED.

The talk of pivot simply proves it. The FED has clearly said over and over it’s not in the baseline scenario.

FED has no cred.

You can thank me for the runup in gold. I sold my gold near the end of December last year and two days later it ran about 200 dollars higher. Technically gold should have had a big rally at the end of 2022 and it didn’t so I sold my gold.

Wolf I used to see gold and silver only for the purpose of insurance against the worst case scenario of fiat collapse or devaluation, it has served well for Venezuelan’s among others in devaluation and Zimbabwean’s again among others in total fiat collapse. As a former coin dealer, I always recommended a mere 2%-10% position for this purpose.

With the threat of CBDC’s and bail-ins, first tested in Cyprus over10 years ago I lean towards the higher percentage today for others.

Disclaimer: I’ve had more percentage for the last 30-40 years and have slept well watching both metals gaining 5X-7X during that duration due to inflation failed FED policies.

Hi Wolf,

You stated below:

“the S&P 500 is down 13.5% from its high in Jan 2022 and is back where it had first been in April 2021, two years ago exactly.”

True for the index price. However funds that track the index such as FXAIX (Fidelity 500 index) pay dividends quarterly.

They typically pay capital gains in December but the Fidelity website indicated no capitalbgain payouts the last 2 Decembers.

Over the course of 2 years, FXAIX had 8 payouts worth

$4.37 at roughly average price of 150, so about 2.9% return worth.

So yes looking at FXAIX chart it ranged 140-145 two years ago April 2021.

Recently 143-144.72 so basically flat price.

But total return would be about 2.9% higher.

Its difficult to find a 2 year return for a fund online, typically 1,3,5, 10 year returns are all that are quoted.

The S&P 500 (FXAIX anyhow) appears to have peaked 12/29/21 at 166.23.

Indeed on 4/27/23 @ 143.58 the price is off about 13.6%. FXAIX paid 5 dividends worth $2.33 over that timeframe, at approximate average price 133, adds 1.75% to total return (for that timeframe December 21 to 5/1/23).

Fidelity quotes FXAIX returns as follows (as of 5/1/23):

1 year: 2.65%

3 year: 14.51%

5 year: 11.43%

All reflect dividend payouts.

When one speaks of the S&P 500 (the index, independent of any fund) 3 year return, for example, I’m pretty sure it also takes dividend and capital gains payouts into account. Fidelity, Vanguard ,etc index funds that track the S&P 500 will have fairly minor

differences in their performances. That is for another time perhaps.

This is helpful from Investopedia, distinguishing between the plain index and the total return index (SPTR).

“However, the value of the S&P 500 index is not a total return index, meaning it doesn’t include the gains earned from cash dividends paid by companies to their shareholders. Since many companies in the S&P pay dividends, investors should factor those cash payments into their overall investment return. There are total return indexes that track capital gains (stock price increases) as well as dividends. The S&P 500 Total Return Index (SPTR) is one such index.”

When a fund pays a dividend or cap gain (reflecting payouts by its holdings) its share price is reduced accordingly (e.g., it pays a cap gain of

1.45/share then the share price is reduced 1.45/share) on the

ex dividend (a.k.a. reinvestment) date.

I presume the SPTR behaves similarly but am not 100% sure.

Bottom line: the index price changes will typically understate the overall performance of an index’s total return since it does not account for the dividend and cap gain payouts that occur by companies making up the index.

Also I found the Seeking Alpha website provides dividend payouts going back many years (Fidelity only had one year’s worth).

One last comment on index returns…

cftech has a detailed writeup on how index values are calculated and how their associated total returns are calculated.

[I dont know who cftech is… they just came up with a Google search].

It turns out to be rather involved.

It says the following :

“The total return for the S&P 500 Index is calculated similarly; an indexed dividend return is added to the Index price change for a given time period.”

It goes on to describe how the S&P 500 Index [in particular] is maintained.

In its discussion it says:

“Maintenance of the Standard & Poor’s 500 Index is detail oriented and time consuming. Index maintenance includes monitoring and completing the adjustments for company additions and deletions, share changes, stock splits, stock dividends, and stock price adjustments due to company restructurings or spinoffs. ”

I understand why non index funds have capital gains. Index funds are a little less clear… perhaps they typically have capital gains (only ?) when the index itself removes (essentially selling ?) a company from the index replacing it with another company.

Here’s the link to the cftech article, hope you are ok with its inclusion here. A bit nerdy but pretty good.

https://www.cftech.com/en/the-brainbank-archive/finance/138-standard-poor-s-500-index-calculation

And one LAST comment:

Big Charts has very good charts (many time frame options) and price lookup capability.

I previously mentioned that FXAIX (Fidelity 500 index fund) price maxed out 12/29/21. Wolf had mentioned S&P 500 peaked in Jan. 2022.

Using Big charts I obtained the following results for the

S&P 500 index:

12/29/21: 4793

12/31/21: 4766

1/3/22: 4796

1/4/22: 4793

1/5/22: 4700

Didn’t continue… charts show the index declining thereafter i believe.

So it looks like SPX peaked on 1/3/22.

Eolf was right, January 2022.

Looks like I misread the FXAIX chart a bit. Not that it detracts from my other discussions but FXAIX actually peaked 1/3/22 just like SPX (good, I was concerned why wouldn’t they peak the same day ?!) and not

on 12/29/21 as I had previously stated.

FXAIX 12/29/21: 166.23

FXAIX 1/3/22: 166.37

The chart I looked at was quite small and so I’ll have to forgive myself for mistaking the peak a couple business days earlier than when it truly peaked.

Which country in world isn’t a debtor nation ,as they sat were they cleanest shirt in laundry, scary

So will there be more rate hikes after the May rate hike?

Also shouldn’t this be another clue to do faster QT (including MBS selloff)?

They wanted inflation which they got. I think the raising is just so he can lower when shtf. They never wanted to fight inflation, it’s just a pr.

Two months ago, I would have disagreed with you, but now I agree. I do think they want to get CPI inflation down, but they would love for assets to stay at their current levels or go up. In other words, they would be happier than a pig in poop for the average house to cost $2 million, even if the average income is $40k, as long as eggs and gasoline aren’t going up by more than 2% per year.

Yes and like you have said before and I also believe the same, the stonks, housing crypto and other assets will have to drop at least 30% to have any impact on inflation. Don’t think they will allow that to happen.

Like dc says soft landing is for them to keep their high asset prices and Main Street to sell kidneys just to survive.

Noone ever really asks the Fed about the size of the balance sheet, only the interest rates. That is really what is propping up asset prices are the massive balances at the Fed, ECB and BOJ and others

Raleigh real estate Report!

50k over asking for a 600k+ house is back!

somewhere a house flipper got their wings.

The Blinders are back on boys. Close those ears and act like it’s free money. I guess?

Scuse me while I put on the Stones with “I can’t get no Satisfaction!”

Seems appropriate

Realtor alert!

Crypto by most measures (broadly) has dropped 50-90%. Stonks too.

Those speculative slices got knocked backwards early in anticipation. It sometimes seems like few people are familiar with actual data – readily at hand. Might be for the best since fewer still know how to interpret it…

sufferinsucatash,

Try DEVO’s cover version instead. “The vocals don’t give you any warm and fuzzies as they are flat. They get in and get out delivering their message in a more efficient manner. The sterileness is actually what is so magical about this version.”

Q: Are We Not Men? A: We Are Devo!

side 1, track 2

Our national debt, plus our corporate debt, plus total individual debt is just too high. GDP in the USA is slowing down. Inflation, while a vile disease that reduces the quality of life for the masses, is needed. Needed in order to grow the economy alongside the debt, if not fast enough to outpace the debt.

Those opinions were put forward quite persuasively in mid-October 2022 by Russell Napier. He thinks that this “PCE price index moves sideways stubbornly high @ 5%” is in the cards for the next 15 years.

I hope he is wrong, but the cost to service Uncle Sam’s monkey on the back just keeps growing as debt climbs and interest rates rise. Wolf has accurately said that inflation this does increase Treasury revenue through taxes as a result of wage growth. But to me, it is a losing fight to try and deal with the $31.5 T (and counting) this way. Napier reckons we need 6 to 8% nominal GDP growth to handle where we are now.

I’d like to turn down the faucets of dollars flowing out of D.C. as the way to handle this mess we’re in.

DEVO’s album kicks off with ‘Uncontrollable Urge’ before ‘Satisfaction.’

P.S. To John below,

Kudos to you. My bike @ University was a ’78 Kawi KZ 550 modified as a café racer. Classic and perfect!

Prairie:

“I’d like to turn down the faucets of dollars flowing out of D.C. as the way to handle this mess we’re in.”

Understatement. I wish. Will never happen for the next two years, unfortunately.

Butters, I believe you. I also never believed Powell when he said the housing sector needed a reset and housing needed to get back to being affordable again. Powell has never cared about the housing market and I wish he’d stop pretending he does.

He would be fired so quickly.

You are 100% wrong

Hypothetically, negative interest rates are likely to be inflationary, per se. Therefore, the current rate is stimulative as one would expect during the approach to a presidential election.

An insufferable, orchistrated drama.

Why would they want to sell off any MBS instruments? What purpose would such a stupid move serve?

Getting the housing market down to the level where the fiscally responsible common people can afford to buy a home (to live in).

Yes for the people who wish to keep housing prices very very inflated (or who already own their home and have an attitude of ‘I got mine, f u’), only they would think it is stupid move.

I agree with your sentiment about a better world, brings back the music from the useful idiots of the 60’s and 70’s. Unfortunately, the real world is much more cutthroat. There no longer is a price set by the sentiment of a previous generation. The price is being determined by the sentiments of the current generation.

@dang

Whatever is the generation, you don’t want the reality hidden.

Fed owns 20% of all the US residential mortgage. That’s created a massive skew in pricing and demand. No generation wants that.

Now Fed can’t even sell those MBS without taking a huge loss because of current interest rates. Rolloff rate is too slow.

MBS price discovery would be an indirect way to increase capital buffers in mid size banks. It would demonstrate the folly of.pension funds on blindly following Wallstreet investment recommendations.

It would encourage more integrity in regulating the finance industry and debunk the horse stuff notion that aggregating risk in one asset class provides stability through numbers. Top of head

It’s interesting to look at history of Fed fund rates. Powell indicates he is going to raise rates and then keep them there for a while. That is not the way it usually works and the bond market knows it.

Fed normally raises til something big breaks and immediately cuts. There are hardly any plateaus with the funds rate except at zero. The majority of the time its either getting raised or getting cut.

old school,

Take a good look at history (chart below). For most of the time since the 1950s, the Effective Federal Funds RATE (EFFR), the purple line, was ABOVE core PCE (red). The big exception was the era of QE starting in 2008. But QE is over. Now is QT.

The EFFR has just risen enough to touch core PCE. If the EFFR rises ABOVE core PCE and stays above it for years, that would the old normal.

Don’t think that QE was normal. It was the exception, and it led to the worst inflation in 40 years. And everyone knows that, even the Fed.

Amen.

The powers have “gaslighted” everyone into thinking FF belong under inflation. Would love to hear some good Congressional questioning in one of these hearings.

All I am saying is the history of max fed rate is a mountain top not a plateau. It could be different this time, but I don’t think so.

How come they don’t admit they were wrong Wolf???

Powell touted how great the FED was during the last press conference…

“CHAIR POWELL. Well, it depends on whether you—so recessions tend to be nonlinear,

and so they’re very hard to model. You know, the models all work in a kind of linear way—if you have more of this, you get more of that. But when a recession happens, the reactions tend to be nonlinear and that’s what—so we don’t know whether that’ll happen this time. We don’t

know—if so, we don’t know how significant it will be, and so, you know, we’re very focused on getting inflation down because we know in the longer run that that is the thing that will most

benefit the people we serve. That’s how we can have a long—you know, we’ve had very strong labor markets through these long expansions that we’ve had. Four of the five longest, or three of

the four longest expansions in U.S. history have been really since the high-inflation period. And the reason was inflation wasn’t forcing the central bank to come in and stop an incipient or, or,

you know, an expansion. You can have very, very long expansions without high inflation, and we had several of those, and they’re very good for people. You see late in an expansion—you

see low unemployment, you see the benefits of wages going to people at the lower end of the wage spectrum. It’s just a place that we should try to get back to”

I see no admissions of guilt in this statement. The Great Recession screwed people pretty hard, which Greenspan and co. arguably bear some blame for. Some people also claim they have a role Dot Com Bubble, but I don’t know.

It’s conventional wisdom that “QE caused the worst inflation in 40 years”.

I think, on the other hand, that this oversimplifies the situation, in 2 ways:

1) It’s not QE per se that “caused inflation”; it’s QE carried out beyond the point where other factors could be expected to counterbalance its effect on the pricing of goods and services. Some – even a substantial amount of – QE didn’t seem to lead to inflation for a surprisingly extended period of time. Until it did, when it was overdone given the circumstances, and an inflection point was reached.

2) Even that “overdone” QE might have caused far less inflation, had it not been coincident with the most severe supply chain shock in living memory.

The Fed (and Biden, with his final shovelfuls of likely unnecessary stimulus money) might have done better to curtail their efforts – but perhaps not as drastically as I think your comment implies, Wolf.

But it’s a matter of degree, not directionality; I think their efforts (QE & stimulus) would have had far less negative effects, had they been based on a more sober assessment of the accelerating (compounding) effect on prices that supply chain constraints were bound to have. These compounding effects – and this is my point – were an integral part of the story; QE and stimulus did not, by themselves, “cause the worst inflation in 40 years”.

Looking back, I’m left with the intuition that the QE and stimulus decisions were taken with insufficient (or perhaps little to no) attention to the escalatory pricing effects that well-publicized supply chain disruptions were, predictably, going to exert. That’s a mistake we can hope is not made again in the future. But it’s also desirable that future QE/stimulus decisions not be constrained by oversimplified interpretations of the events of the past 3 years.

But heck, who knows; I could be wrong.

Adam Smith,

I’m not disagreeing. But you left a hugely important element.

The instant reaction that QE caused starting in 2008 was horrendous “asset price inflation,” including “home price inflation,” but it did NOT cause “wage inflation,” and initially it didn’t cause “consumer price inflation” because the beneficiaries were primarily the top 10% that hold most of the assets, and those assets were being inflated, but that top 10% didn’t increase their spending because of it, they just got richer. This produced the biggest wealth disparity ever. See chart below.

But the super-mega QE starting in March 2020, in addition to triggering hair-raising asset price inflation and home price inflation, also seeped into spending and in conjunction with the stimulus spending, unleashed consumer price inflation. Now all this extra money that had been created since 2008 is out there, and has been unleashed, and it keeps fueling consumer price inflation.

The FRB has become a government agency. It has 3 priorities: stability of the banking system, funding the Treasury, and keeping the dollar afloat- in that order. To that extent, the FRB and Congress can and will do whatever it takes to salvage this failed morally bankrupt system. Including QE, inflation, market crashes or bubbles. Nothing is off limits, it would be disingenuous to claim otherwise.

From Wall Street’s perspective, borrowing money from the Federal Reserve at 4.75-5% while inflation is running at 4.6% isn’t a bad deal. Money is still effectively free. No wonder the stock market is exuberant & speculation is running rampant.

I reviewed a REIT that reported this week. I have owned a few times. Their cost of funds is lagged by about five years. Currently their average loan rate is 3.5% up from 3.1%.

If those who created the money are unwilling to destroy it, there’s nowhere for the printed money to go but to inflate everyday expenses or to be dumped down the black hole of financialized assets

A) Create Wall St profits by reducing the cost of labor. B) To achieve A, offshore jobs, and provide govt assistance to offset less than living wage. C) To achieve B Govt pays for assistance with deficit spending (subsidizing corporations further with tax breaks). D) It all works as long as everyone remembers their place.

Oh, we have other wars, all the time. Please check the budget of the USofA.

Your observation is eerily logical. ” who created the money are unwilling to destroy it” is sentence filled with meaning. Nice mix of the words, but a bit of the hair on fire interpretation for me.

They get it back in higher taxes,so easy to figure out

Inflation on individual items vary greatly! This is of course anecdotal evidence but I restore classic Japanize motorcycles. When ordering parts and shop supplies some prices just stay the way they are for quite a while and then bang shoot up by 30-50%, way more than the 5-6% advertised inflation rate. ” things don’t go to heck in a strait line”. The things I order are not everyday items and probably have very low demand. Those items are probably manufactured every one or two years so they sell all the existing inventory and when they re-tool for a new run and have a huge price increase!

Most automotive (includes cycles) parts houses and dealerships operate on a LIFO accounting model for tax reasons. Not unusual for parts to climb in retail price, regardless of when they were produced. Manufacturer publishes new price? Bang! Up she goes!

A spoke set for a 1977 Yamaha YZ125 may not fall into that LIFO category? LOL

John – do a little moto-resto/renovating

myself, and concur…best.

may we all find a better day.

The time I spend in the shop Zink plating old spokes or bead blasting an old hub is the only time I can completely detach from the constant barrage of crazy news and world affairs. You must know what I’m talking about, right? You and I have therapy. I wonder what others do?

Well firstly the revelation that “I restore classic Japanize motorcycles.” immediately set off my BS alarm as too the veracity of your anecdotal observation.

dang – trying to parse if you’re doubting the ‘classic’ term for Japanese machinery in general (‘vintage’, ‘veteran’, ‘classic’, ‘twinshock’, etc., are long-running terms of discussion in concours and historic racing moto circles re: age, but not country of origin), or John’s ‘Japanese’ spell-check misfire…

The parts and their pricing for ‘classics’ are where you find them…regards.

may we all find a better day.

Fed wants conclusive evidence before slowing the hikes . QT will continue longer. Hard to predict what conclusive means in my opinion wish they would spell out that definition. I want higher rates for longer.

The FED already slowed the hikes.

No central bank can raise interest rates indefinitely. She has to stop sometime. It is important that it stays there as long as it is needed

Well now is not the time to let up. I’m sick of it, what they have done to us, the Fed from Greenspan on, the never ending spending out of DC. This can’t be the new normal.

“No central bank can raise interest rates indefinitely.”

True enough. And what of inflation indefinitely? How does that end?

Rates are still historically low to inflation….especially the long end which never exceeded the inflation rate during this hiking cycle.

Further rate hikes are needed, and further rate hikes will drive vulnerable banks to the larger ones with Federal assistance. This is a boondoggle for the larger banks. The deals will have backstops and “locks” in which the acquiring bank “can’t lose.”

Fed up

We are all fed up. Do you think I enjoy watching my money in the bank melt or that I don’t get mad watching the property I sold in 2013 now cost double.

I am disgusted by both the ECB and the Fed. But what if their interest rates skyrocket and crash the economy and the job market? Do you think the Fed and the ECB won’t be content to drop interest rates back to 0 and keep printing notes? I want this nightmare to never happen again. And that’s why I think it’s better to proceed carefully

JuliaB: I don’t want it to happen ever again either. Do you think I want that? But I don’t think pausing now is a good idea. The economy could crash with skyrocketing inflation as well. The Fed could resort to QE and low interest rates without the economy crashing as we have seen. We don’t know what they will do. I just know this can’t be the new normal.

It’s time for the market to accept “higher for longer”. That’s the big picture. I predict a near-term bloodbath.

And the sideshows are fun to watch as well. Look at all the speculators getting burned on FRC this week. It’s dropping 20-50% daily. Talk about a falling knife. I shiver to think about the many young folks who might be doubling down on that garbage.

Wonder if it will become a MEME stock?

We’re a meme country at this point. Everything is openly mocked because its all so corrupt and absurd.

…is ‘me, me, me!’ considered a ‘meme’?

may we all find a better day

Yes and no. I feel that the seed corn growing up in this great country are not a meme. We may have been but I don’t think they are.

They are not as backward as they appear.

Another 30$ billion down the toilet ,on taxpayers dime .so tired of this shit pubertal rica looking good .30$ billion to the rich as merry go round keeps spinning .Citizens unite force change

“Citizens unite force change”

That’s what it’s going to take. Good luck getting the average apathetic American off their butts. I’m on board, btw.

While you can count me as an ally of the idea that the butts are reticent to vote against their comfort zone, however, there is a counterfactual argument that draws a completely different conclusion.

That the American workforce is ready to negotiate an equitable workplace with management. One can think of this in one of two way: a threat on the absolute rule of the owner or a share of the profitability with those who made it possible.

@Dang:

I have found this idea appealing in the past as well: create more structural opportunities or requirements for workers to acquire ownership stakes in the company. But there are several key issues that prevent this from achieving what we’d imagine.

First is that many businesses are privately owned. Forcing such businesses to give up ownership rights (even if piecemeal) is a terrible precedent. We definitely don’t want the government in the business of telling people what they can and can’t own, and using their power to take it.

Second, having an ownership stake in a company is only meaningful if you intend to keep it. But far too many workers won’t keep it. They’ll sell it as soon as they acquire it. Either because they actually need the cash, or because they have no interest in holding a risky asset. After the fall of the Soviet union, they divided up the country’s business and industrial assets by giving stock coupons to all citizens. It didn’t take long for all average people to sell their shares to oligarchs in exchange for money to pay rent and buy food.

You might suggest, “Well, then they shouldn’t be allowed to sell! They should be forced to hold the asset.” This idea has its own downsides. If they can’t sell, they can never realize profit or extract value. It essentially becomes meaningless to the worker because they can never sell. Why should they care about company performance?

Third, at any publicly traded company, employees can go buy stocks right now if they want. But few will without some ESPP program. And it’s not really advisable that they do. It’s too much concentration of risk in one company. If it goes south, they could lose their job and a big portion of their investments on the same day.

The system we have right now (while not perfect) does some things really well. Protects property rights, gives liquidity to assets (enables buying and selling pretty easily), and gives people freedom to spend their money how they wish. If they want to buy stocks, they are welcome to do it. If they want to live for now, they can choose that path and reap the consequences. In the meantime, almost everyone has decent housing, good longevity, and plenty of food and entertainment. All things considered, not a bad life.

the rich move their money/inflation around prolonging the inevitable declines. After a few months of slight declines in used trucks, the auction yesterday I witnessed a huge spike unimaginable in everything. It was like panic buying like with laundered money looking for assets. Im totally shocked and cant get it There are little to no sales. Something weird must be going on.

Wrong. There cannot be any change. There are only about 30 to 40 competitive house districts and they are getting fewer and fewer. North Carolina has now allowed extreme gerrymandering. New York and California will follow once the Supremes give the green light. The representatives chose their voters not the other way around.

Yep the neofascists are moving into their endgame. :(

You left out Illinois, an extreme left gerrymander that doesn’t get press coverage like the gerrymanders on the right. The press largely doesn’t care about gerrymanders by the left, hence this issue generally was ignored until the last 20 years, as most gerrymanders before that were in left leaning states. CA redistricting is done by a commission, so there won’t be large changes there, unless the US supreme court invalidates commission based redistricting, which could happen, but I’d far from a certain thing, and would affect some states of both left and right leaning varieties.

Bobber,

I bonds .9% fixed rate.

Inflation higher for longer? No worries :P

I’m encouraged by the prospect of interest rates being higher for longer. Sticky inflation may also serve as a lesson against the more extreme aspects of monetary policy the Fed previously engaged in.

They wanted the inflation. It was intentional. They are trying to park asset prices at a new, higher level. The working class and the poor are being milked to death by the wealthy who will own almost everything when all is said and done. There is never a “mistake” by the FED. Ever.

You say that like it’s a bad thing? The wealthy oligarchs have always controlled the country. Now they are just going to tighten the screws on the sheeple.

Escierto,

You’re on to us!!! Oh no!

I hope you don’t know that we’re secretly robot vampire aliens!!!!

I better call the Bilderberg group and the Knights Templar to let them know that we’re found out!

We must enslave the earth sheeple!

I for one welcome our vampire overlords, and like to remind them that as a trusted and verified PTA member, I can be helpful in rounding up other sheeple to work in there underground lair caves.

I think that is closer to the truth than most of us are willing to admit.

I keep looking for the legendary moral justice that American naivete claims as the corner stone.

Tentatively, I tend to agree that the mistakes are not the result of the Fed Chairman or the FOMC. Which automatically questions the Fed’s independence. Were the mistakes as a result of miscalculation by the board’s of directors from the organized banks that actually own the FRB, the political maw constantly demanding to be fed, the Constitution and Declaration wagging a finger at the poor, poor Fed. Like Atlas, the weight of the world, resting on the thin shoulders of J Powell and the FOMC come Wednesday, this week.

First-time comment here…likely a rare thing…please be kind. My comment is about the real-world affect of inflation and the labor market on our employees. In my business of wholesale and manufacturing, we continue to struggle to hire good, reliable people. And that’s in multiple states. In the past few years, we’ve raised wages multiple times overall, and also with specific people to get them to stay. Our employees are making a LOT more (like 40-50% or more) than just a few years ago, but it’s still tempting to job-hop. I get that, and some of them hopped TO us. Regardless of wage increases, they still struggle to buy gas and groceries, not to mention children and doctor bills. In my humble opinion, wages continue to rise, but it’s still not keeping pace with the cumulative “overall” affect of inflation on our good, hard working Americans. We do everything we can to help them and still make a profit, but it’s not enough. I support the Fed’s efforts, but I wish they had come much sooner. And as a business owner, we’ll figure out what to do.

Wolf, thank you for your dedicated, detailed and helpful information. For me, it cuts through the crap and gives me something believable. May you enjoy the benefits of your efforts.

The Fed’s monetary policy has inflated the two largest purchases of working people – homes and autos – for decades without any real increase in wages.

Younger generations are paying the price for this generational theft and gross mismanagement.

Greedy corporations that insist on paying less than a living wage are to blame.

Corps are not greedy the people on the board are greedy. In the 70’s average CEO pay was about 70 times rank and file workers. I believe it is now about 400 times! BTW ammo is getting cheaper.

Greedy corporations did not print trillions of dollars or keep interest rates near zero for over a decade.

Don’t hate the player, hate the game,

Cheap labor flooding into the country has its impact. That is not a political comment but a fact of supply and demand.

MM comment below is correct, it is the Fed that is eroding the value of the wages of working people and retirees.

So are older generations. I’m seeing people in their 90s being kicked out of senior apartments because their COLAs don’t keep up with the outrageous rent increases.

Autos are significantly less expensive today than decades ago. You can go out and buy a car that outperforms in every measurable way (performance, safety, amenities) for a far lower share if median income. They are the worst representation of the harms of inflation because they are quite frankly dirt cheap.

Just because people feel entitled to more, it doesn’t change the above facts. What this does mean is that affordability is far better today than decades ago, even after the recent run-up in prices.

Housing is more complicated but reflects a similar story. At least in the US. The median price for a home per square foot has roughly doubled in the last 20 years. So has median income (slightly lagging after the big housing run-up of 2020-2022 but now catching up rapidly after the latest housing price declines).

This is not at all similar to global ratios where in Europe, Asia, Canada, Australia the rate of increase of housing is closer to double the increase of wages. Of course populations are increasing (a supply and demand impact for most goods production but more of a demand-only impact on housing).

Relatively speaking, US housing costs overall are very affordable. Combined with no systemic risk (mortgage fraud) there is no pending national crisis, just regional corrections.

I don’t think you are serious. You can’t possibly believe what you just wrote. “Relatively speaking, US housing costs overall are very affordable. ” I really think you are trolling. I think I’ve seen your posts on other sites under different names. Waverider comes to mind on another site.

Here’s another doozy: “Just because people feel entitled to more, it doesn’t change the above facts.” Lol. And another one, “Autos are significantly less expensive today than decades ago.” “…….they are quite frankly dirt cheap.”

Doesn’t sound like you live in the US, so maybe you shouldn’t be commenting on what is acceptable or not in this country. And trolling is not cool.

Truth,

Your first two paragraphs totally (and willfully?) ignore the BIG issue of going upscale by ALL automakers together in their oligopolistic manner because that’s where the big revenues and fat profit margins are (a price of $30,000 on a vehicle v. $15,000 = double the revenues and in dollar terms at least double the profit margins). Yes, the $30k vehicle is a lot better than the $15k vehicle. But people cannot afford it, and the $15k vehicle has disappeared. And now the sub-$25k vehicles are starting to disappear, and people can no longer afford to buy a new vehicle.

This is called an “affordability crisis.” It has nothing to do with inflation but with going upscale across the auto industry because it boosts revenues and profit margins.

It boggles my mind that you cannot see that. And your comment about housing affordability is just silly.

BS.

Median household income in 1990 35K, average new car 15K

Median household income in 2021 89K, average new car 42K.

And that’s before inflation really started ripping.

These are per Statista. So a car in 1990 cost 42% of median household income, and 47% now. This is before most of the massive inflation of the last 2 years, it is probably far worse now.

I’m sure you will try to argue about the vast improvements in technology and quality since 1990. Yeah cars are a little better. But the bottom line is they get you from point A to point B. Maybe they need to be repaired a little less frequently? That’s about the only benefit. Maybe ABS has made them a little bit safer .

Compare that to the changes in the value of the telephone. In 1990 the telephone was a thing with a rotary dial attached by a cord to the wall. Now it’s a device that contains all the accumulated knowledge and connection of the human race in the palm of my hand. The phone is worth about 1 million times more than in 1990. Maybe a car is worth 10% more?

This is a very useful report since it describes a real situation at an actual company. Thank you.

Agreed.

Pardon me if I step wrong, but your complaint seems hollow. Are you wining that there are not enough qualified candidates too fill your job or is it that after incremental increases in your pay scale you are only able to attract the most desperate people, or perhaps, your reputation as a an honest employer is so tarnished that no one would work for you unless under duress. Which I think your fishing for, absolution for your employment practices that make people decide not to go to work for you.

Good alternatives, according to my taste:

Are you beering that there are not enough qualified candidates?

Are you scotching that there are not enough qualified candidates

Are you bourboning that there are not enough qualified candidates

See? That’s in return for making making fun of someone here who’d said, “I restore classic Japanize motorcycles,” a phrase, that you said “immediately set off my BS alarm as too the veracity of your anecdotal observation.”

Autocorrect humor will get you every time.

You’re doing more good than most people, finding ways to produce and profit here in the States. Thanks for that. It can be done on a smaller level than huge corporations on the dam stock market.

If you paid a living wage to the Good Hard Working Americans and the work is tolerable I doubt you’d struggle to hire Good Reliable People. I get it…I’ve run a business before and it’s tough. Sometimes you have to pony up the cash to pay the people who are producing most of your profits.

They printed too much and don’t want to do what is necessary. They should have NEVER scaled back the hikes from 75 basis points. It was yet another give to wealthy speculators. This is the end result.

Consider the insidious narrative that a “pause” will soon be necessary as levels continue to creep higher. Once parked and with the lot full, higher for longer is just something those who didnt get a spot have to deal with.

I agree with you, DC. However, Wolf once said that the Fed can’t raise too aggressively or too fast, or it will break things (markets/global economies) … ok, I’m paraphrasing, but you get the drift.

If it’s any consolation, the rates will stay “higher” for longer … well, I am hoping J-Pow will come to his senses, and do what’s needed, what’s right, what is necessary.

Rate hikes aren’t the issue. The issue is the $8.5 trillion balance sheet, that is about $6.5 trillion too large.

exactly. The 8.5 trillion balance sheet is the reason why the speculation in the stock market is still rampant. Meme stocks popping left and right every day. Big tech stocks going up without restraint. It is crazy and wrong.

Agreed.

There is still TOO MUCH MONEY sloshing around in the economy.

IF one buys into the trend of money growth from pre COVID, we are still about $4 Trillion above and off that trend line.

QT is the key…..and woefully slow IMO.

Wolf ran an article about how the balance sheet realistically cant get below 5.5 Trillion.

Looks like 8 is a tough number.

+1000. Set the QT runoff on unstoppable autopilot and outlaw any Fed purchase of any financial instrument ever again.

Plus 1,000 % to this. Googled Volcker for this :

What was the highest fed funds rate under Volcker?

The Federal Reserve board led by Volcker raised the federal funds rate, which had averaged 11.2% in 1979, to a peak of 20% in June 1981. The prime rate rose to 21.5% in 1981 as well, which helped lead to the 1980–1982 recession, in which the national unemployment rate rose to over 10%.

I made a fortune thanks to Paul Volcker while most lost a lot of money.

Great charts but what would be interesting to see are charts that are integrals of these percent change charts. For instance the autos chart is deceptively optimistic at first glance. What is not clear is you have 30 periods of compounded inflation, so even if the inflation measure goes to 0, the result is a stable yet massively higher price. Would be valuable to see how much deflation you would need to have to get back to say 2018 prices.

I’ve posted plenty of those types charts when they were appropriate for the topic. But you don’t get all possible charts in every article. I pick and choose for very good reasons — today to deal with inflation in percentages because that’s what the Fed does, and this is the Fed’s preferred index, period.

And this being Wolf’s kitchen, you eat what you’re served or you don’t eat, LOL

If there is a different topic concerning price increases, I might use a different chart, for example below — for today’s topic in terms of the Fed’s favorite inflation index, this type of chart is irrelevant.

https://wolfstreet.com/2023/04/13/turning-point-cpi-used-vehicles-not-seasonally-adjusted-jumped-for-first-time-since-july-tracked-wholesale-price-surge-with-two-month-lag/

It would be great if our gas prices would go down in AZ. We are higher than LA, according to ABC15. AZ used to be inexpensive. Not anymore. Meanwhile, rents are going up, up, up with more BS fees being tacked on to the base rent.

Move

Looking into it. Just don’t know where.

There are many suitable safe Latin American countries where you can live like a king. Heck, you can even try the Philippines or Thailand if you are adventurous. Try it. You’ll like it.

Escierto,do you convert your Us currency to country ,I would go to

Home prices in the Hamptons still soaring in the first quarter. Guess that options out.

Yeah, I noticed that the price of gasoline in AZ skyrocketed from 3.59 to 4.79 in two weeks. There must be a free market explanation other than the likely explanation that business has too little competition in a fundamentally important consumer market like gasoline. While XON reports record profits.

Some blathering about being at the “end of the pipeline”, switching to summer blends, refinery maintenance…… blah blah blah.

Down to a half tank every two weeks. Eff ’em.

In my parents days, I remember people walking to work . Riding bicycles so there are alternatives,we’re just LAZY

Still don’t understand why the yield curve is so badly inverted. Stock response is because the Fed loaded up the short end. If Fed would drop interest rates, YC would steepen, and the banks would be fine. That would move inflation out to longer maturities, make bonds a better investment relative to stocks. They also have to admit that inflation is sticky. They’re not going to do that. Soon anyway you should be able to take out a second mortgage and put the funds in overnight MM and generate a positive return.

I’m also perplexed by the yield curve. Maybe it will change when the debt ceiling is raised, but it seems like something else is affecting it. The bond market seems like it’s been broken ever since Bernanke decided to strangle it.

Ambrose.

“Still don’t understand why the yield curve is so badly inverted.”

Pre 2009 the Fed stayed out of the long end.

Since then they have acquired around $2.6 Trillion in MBSs and have a couple of Trillion more in Treasury paper with maturities of greater than 10 yrs.

IMAGINE……that $5 Trillion out in the real market looking for a bid. It has been absorbed, sopped up, disappeared from the market to the balance sheet. Never has the Fed delved into such yield curve control. And, it has been admitted the purpose was to force investors to take more risk. And look who invested in those long maturities…..they are in the banking news each day.

“This inflation is stuck”: I don’t think that Treasury and Fed think the same.

If Fed really believe that inflation is stuck then they would raise by at least 50bps next week.

Quite the opposite, heard Powell saying that deflation is happening.

jon,

I said that in Wolf’s last article.

Do 50 bps.

Stock market, bond market, crypto, housing… Nobody believes J. Pow.

The reporters kept asking him about a FED pivot during the last presser. Over and over.

He scared to spook markets, but inflation is entrenched. Mohammad El Erian kept talking about J. Pow’s credibility problem awhile back.

Do 1.0 in May.

He should raise two and say that FED might consider slight pivot next time around, contingent on how things react to this one. Drop .25% next time, then keep going from there accordingly. Reporters and wall street will get their wish and then they’ll stop asking for pivot going forward.

There must be a distinguishing between “deflation” and “disinflation”.

IMO, “disinflation” would be a retracement of inflation “spikes”. (likely what we might see)

“Deflation” seems more of starting at some normal level and going backwards in price in some UNWANTED fashion.

The later, hardly the case. Backwards now would be very welcome to most.

Only place I see it is eggs, The real goal is wage deflation

The Fed needs us to believe that they believe inflation will come down, even if they don’t believe it themselves.

Its all about inflation expectations / the iflationary mindset, i.e. the “why bother saving just spend it now” crowd.

Nonsense. It takes a long while from the passage of an act to actually getting the money flowing. A lot of it were tax credits, and you have to wait a year before you get the tax savings.

Higher for longer, ’cause inflation is stronger, too bad pivot monger, you couldn’t be wronger.

Here’s my little anecdote from the world of IT: big G is raising its Google Workspace prices across the board by 20% this month, and they are already talking about another 20% raise this time next year.

13 months and counting since the first hike. Good thing the first interest rate hike last March was 25bps.

/s

Something needs to break. Raise rates

Higher and faster. Otherwise in a year,

There will be no working class or middle class whatsoever.

Where will they go? You act like they will disappear! In spite of the weeping and wailing, millions of people in this country are making more money than they ever imagined. One of my sons makes over $400K a year working three jobs remotely.

Statistical outliers mean nothing. A family member of yours that is a 1%er doesn’t mean jack sh!t when you look at median incomes.

Another daughter who is a travel nurse doesn’t take any gigs that pay less than $5000 a week. Another son had to move because his wife got a job in another city. He gave in his notice but his employer told him he could work remotely and gave him a $25k raise. Another son who is remodeling his house said it was going to cost nearly a million dollars. I could go on and on – the younger generations are swimming in money!

Escierto: Traveling nurses I believe. They make good money now, although there was a time not so long ago nurses didn’t make diddly. I don’t believe most make 400k on the internet, and I don’t believe the average young person is swimming in money. I know too many who aren’t. I also know some who are making ends meet, but they aren’t necessarily swimming in money. I think most people are up to their eyeballs in debt and give the appearance of doing well. I know I’m right about that as I was in 2008 when it appeared everyone had money then. I don’t care about the credit card figures they release, don’t trust a thing Wallstreet says or the government. It will all come out when it finally hits the fan. I also don’t believe most employers are giving 25k raises to keep employees either. May have been a few cases during the height of the plandemic but definitely not the norm and doubtful it’s happening too much now.

I agree with you

People live in their own bubble.

So, the traveling nurse daughter that you’re so proud of is contributing to the medical services inflation that everyone is experiencing and Medicare is likely paying a portion of those fees, further taxing the system.

OK. Got it.

Escierto & Depth Charge,

“One of my sons makes over $400K a year working three jobs remotely.”

This is Exhibit A why Musk got away with firing 80% of the workforce at Twitter, and not much happened.

When people get paid and don’t work, or only work a few hours a week on each job, and you lay them off, no one at the company except the payroll department can even tell the difference.

That’s why there are so many tech and social media layoffs. People working from home and getting paid for two or three jobs are losing one or two of those jobs, or maybe all of them, and eventually they may have to actually work full-time again to get paid, and that’s a good thing.

Escierto,

“One of my sons makes over $400K a year working three jobs remotely.”

Lol he’s not “working” than.

The word you’re searching for is “grifting” maybe. How about “defrauding?”

I mean, I’m all about sticking it to the man… but he’s gotta be a big liar or a booty kisser.

Those guys at work who are “sooo busy” and push work off on colleagues. He’s also screwing legit work from home people over. Return to Office anyone?

I wouldn’t be proud of your son. Maybe talk to him about honesty?

Is his hero Elizabeth Holmes or does he swing more towards Enron?

He may be “working” but he’s not able to focus his full attention to all three employers and, thereby, cheating them out of value for the wages he’s taking.

Announced today, 1st Republic placed in receivership by the FDIC. Goodby!

I thought they might last another week, but this isn’t surprising. Another one bites the dust.

The cause was money printing. A lot of it. Money printing above actual growth is always, ultimately, the cause of inflation. Interest rate hikes just don’t bite that hard when there’s so much cash out there. The fed created too much money too quickly, period. We will have high inflation until all of those trillions are digested by the economy and prices have found their equilibrium with the now-much-larger money supply. Toothless .25%-.50% rate hikes won’t stop inflation. Removing money from the system at a sufficient rate is the only cure for inflation. But that would hurt Powell’s puppet masters, so don’t bet on it. There will be stubbornly hot whack-a-mole inflation ahead for at least the remainder of the 2020s, and that’s the best-case scenario.

The cause was poor Republic’s management.

I imagine they paid out large bonuses when the end became inevitable like SVB did.

Swamp Creature,

Patience, dude!

FDIC “to place” and “may place” and “prepares to place” and “prepares to take over” and “is set to take over”….

The headlines have been going on all day, after a story by Reuters, based on sources.

It isn’t over until the fat lady sings, and the fat lady is still at the bar finishing up her Bloody Mary.

Maybe on Sunday, the fat lady will emerge from the bar and sing.

I didn’t know Granny Yellen liked vodka. She looks more like the rubbing alcohol type.

Captain Kangaroo.

NOT YET. Probably by late Sunday afternoon!

First Republic had a pretty nice branch system, nearly all branches are located in well-to-do or wealthy areas. I can see who their clientele is. No surprise they pulled their money out at the first sign of distress. No more free lattes.

Inflation still high, huh? That didn’t stop the feds from lowering the hammer on my ibonds, which are supposedly indexed to inflation. Instead of 6.9 it was paying since last year, it will be going to 4.3, which I can get easy on a sub 2 year brokered treasury.

So someone in the government didn’t get the memo. Or maybe they did?

If you buy ibonds, you should know how the interest is calculated. So here we go:

The interest rate is indexed to overall CPI-U, month-to-month rate, not seasonally adjusted, last six months. This headline CPI was much lower in recent month due to the collapse in energy prices.

If you buy NEW ibonds after May 1:

Oct/2022; 0.406

Nov/2022: -0.101

Dec/2022: -0.307

Jan/2023: 0.800

Feb/2023: 0.558

Mar/2023: 0.331

Total change: 1.69

to get APR (2x) = 3.37%

Plus base rate of: 0.9%

= total APR: 4.27% or rounded up 4.3%

The six-month rate will be half of that: 2.14%, which you will get over the next six month. Then there will be a new rate.

But the ibonds that you already bought will have the base rate in effect at the time you bought them, plus 1.7% (3.4% APR) for the six month period.

Your numbers are off slightly. The round up is from 0.0429521 or 4.29521 percent. Treasury would not round up 4.27% to 4.30%. Why would they.

https://www.treasurydirect.gov/savings-bonds/i-bonds/i-bonds-interest-rates/

At least you can defer paying income taxes on the I bond interest, unlike a regular treasury bill. I bonds allow for compounded tax deferred growth.

Yes, Ibonds are a place to put money every year and leave it. Put on automatic, if possible. Leave it for a long time, if possible. It is not a short term place for money. But it is a great place to grow a bit of money tax free over a long period. Get started early.

Though rates of change charts can be telling, it is the accumulation, the stacking and compounding of the repeated increases that are damaging.

5% on top of 5% on top of 5%……inflation rate is steady, rate of change dropping. But the damage……we are still beating our head against the wall, just not faster anymore….still hurts.

I bond rates show inflation has been cut in half. HEE HEE

Collapse in energy prices did that to headline CPI

I sure hope that oil doesn’t fall to negative $30 per barrel like it did a few years ago as that will really mess up the headline CPI!

LOL. That -$30 price was for WTI futures, for brief moments, and it never translated into the price of physical oil. And so it never translated into gasoline prices. Annual CPI even during the middle of the lockdowns, with something like 25 million people out of a job amid huge economic uncertainty, remained positive. Now the economy is growing, the labor market is tight, prices of services and some goods are surging, and we may not be lucky enough to even see $50 WTI again (though it would be nice).

Core CPI average 1971 to 2022 was 3.9%. Current core CPI, about 5.6%, is certainly above average, but not insanely higher. Future Fed fund rates: higher, longer.

Kind of moves around like the walnut shells in the infamous “shell game”.

I recall many meetings where we debated whether our customer base would accept a small price increase. With profit the goal, it’s either charge more or pay less. Today, all of us are grumbling but still resigned to prices rising. Until that changes, prices will sneak higher wherever there is an opportunity. People are still spending so inflation will continue. What does Vail Ski Resort call it? Dynamic pricing I think. We need to see sales falling to know inflation is going down.

The economy is still hot and I think there is some gouging going on in services because they can.

Quotes on a new roof on my small house were between 7 and 10k. The 10 was gouging. The 7 was about the same price I was quoted 5 yrs ago.

There were 10 houses for sale at the beginning of the year in my town and today there is 1. I expect that to sell fast.

You must live in a cheap market. I paid a roofer almost $10k for a new roof and decking 18 years ago. I got 3 bids and they were all right in that vicinity.

I know somebody who just paid close to $75k for a new roof and decking, which included removal/reinstall of solar panels.

It has a lot to do with the complexity of the roof, the number of squares of material, what underlayment is spec’d, if the sheathing is OSB, plywood, or product such as Zip Systems, if ice dams are a problem, venting, fascia condition, if the gutters need to be removed and replaced (if any), the number of vent jacks, quality of roofing (architectural or three tab)… so just tossing out comments such as he’s “in a cheap market” is meaningless.

I’ve been building things for 35 years. A $10k roof is dirt cheap these days.

How’s that announced OPEC+ production cut going? Is today’s CPI just us out on the exposed beach ogling the pretty sea shells as the tsunami gains it’s momenentum off shore?

Of course it is stuck- short term interest rates have been held below actual inflation for almost 15 years now- even with Powell raising rates for the last 15 months, that still hasn’t changed. The funds rate needs to be above the inflation rate- I have written that over a year now- Powell is acting far too slowly.

“held below actual inflation for almost 15 years now”

Gaslighting….all the talking heads on cable would scoff at FF above inflation…..though thats how it was for most of the 20th Century.

I will suggest this…..

…….for the Congress who pass large spending bills and the Fed who QEs …..Fed Funds must equal a 3 month moving average of YOY inflation as measured by a legitimate inflation metric.

Maybe then spending and printing might meet its just due.

The Fed has to know that April headline CPI (published in May) is not going to look good. The rolloff number for March was 1.2% so 6.0 – 1.2 + 0.2 -> 5.0%. Energy was the major factor pushing the new delta down to 0.2. It has turned around. The April rolloff number is only 0.3%. I could see headline YoY CPI going up to 5.3-5.5%. I expect the statements by the Fed to include the idea that we may not continue to see declines and they may have to act more.

So … we were told the covering by the FDIC all SVB deposits was a special situation…

and now…..First Republic…….one more special situation.

The FDIC has no intention or interest in ‘covering’ any uninsured deposits at First Republic.