SVB is massively involved in all segments of the startup scene that is now facing a mass extinction event.

By Wolf Richter for WOLF STREET.

SVB Financial, which owns Silicon Valley Bank, the 16th largest bank in the US with $210 billion in assets, came out with some fascinating announcements late yesterday and early today about shoring up its balance sheet and liquidity.

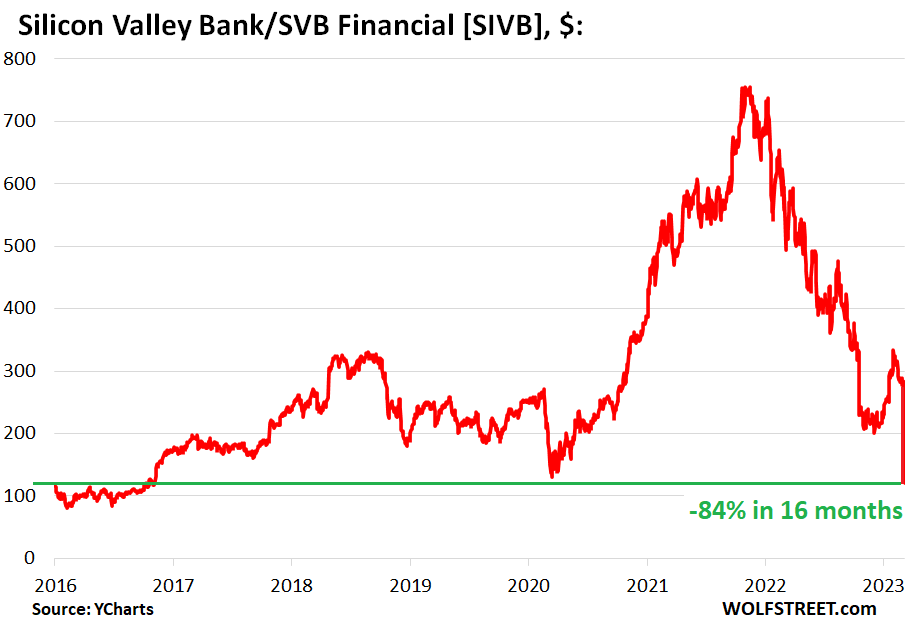

After having already plunged 65% in a series of breath-taking dives, and dead-cat bounces from their startup-and-crypto consensual-hallucination peak in November 2021, shares of SVB Financial [SIVB] kathoomphed so far today another 55%, to around $119 at the moment, the lowest since 2016, and are now down 84% from the November 2021 high, thereby getting inducted into my pantheon of Imploded Stocks. [Update: SIVB closed at $106, -60%; now trading at $85 afterhours, -69% in total for the day; updated chart in the comments. This is just stunning].

The 84% plunge from the high already exceeds SVB’s Dotcom Bust plunge of 77% from September 2000 through October 2002 (my discussion in July of this SVB phenomenon) The Dotcom Bust was a horrible creature for Silicon Valley, and SVB Financial is another indication that this current bust – we still have to come up with an appropriate name – promises to outdo the Dotcom Bust.

Silicon Valley Bank is heavily involved with all aspects of the startup scene. And the startup scene – across all sectors, from biotech to crypto, and across all stages, from early-stage outfits to companies that already went public – is getting the rug pulled out from under it by the collapse of consensual hallucination.

It had to happen some day anyway. It always does sooner or later. But now the end of easy money, after years of central-bank money printing and interest rate repression, is getting blamed, including by SVB Financial.

Get more equity capital.

SVB said in a series of filings with the SEC late yesterday and today that it would raise $2.25 billion in equity capital in a three-pronged approach that is heavily dilutive for existing stockholders:

- A public stock offering of $1.25 billion of common shares;

- A private sale of $500 million of “depositary shares” to General Atlantic, a growth equity firm, which happens to be a “longstanding client of SVB”;

- And the sale of $500 million of mandatory convertible preferred shares.

Get lots of liquidity.

SVB said that it was “repositioning” its balance sheet by having sold all of its $21 billion in available-for-sale securities, and that it booked a staggering loss of $1.8 billion on those sales in Q1 – so Q1 earnings are going to be a massive loss.

It said that it would place the proceeds in short-term securities and on deposit at the Fed to earn the higher short-term rates and improve its liquidity.

In addition, “to further strengthen balance sheet liquidity,” it said it would double its “term borrowings from $15 billion to $30 billion and hedge these borrowings to mitigate higher funding costs in the future.”

Preparing for the mass extinction event among startups.

“We are taking these actions because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients as they invest in their businesses,” SVB said in one of the filings with the SEC today.

“We expect these actions to better support earnings in a higher-for-longer rate environment, providing the flexibility to support our business, including funding loans, while delivering improved returns for shareholders,” it said.

So this is in preparation for what it sees will come its way in the startup scene after the free-money era ended.

When consensual hallucination collapsed, the IPO and SPAC bubbles collapsed and closed the exit doors for VC investors, so they stopped funding many of these companies. And suddenly, these companies have to survive with what they’ve got, but they’re burning cash like there’s no tomorrow, and they cannot cut costs fast enough, and they cannot get new funding – neither the still private companies from private investors, nor the already publicly traded companies via stock offerings.

“Mass extinction event” is now the term used by the VC community to describe what will happen to the vast majority of startups when they run out of money.

Many of these startups and their founders are clients of SVB across its divisions:

- Silicon Valley Bank: deposit outflow as startups burn cash until it’s gone and they shut down. And some loans may go bad.

- SVB Securities, the investment banking division.

- SVB Capital, the venture capital division.

- SVB Private, the private banking and wealth management division to cater to the (erstwhile?) multi-millionaire or billionaire founders.

All of them have fallen off Cloud 9 in a spectacular manner. And SVB is doing what it can to remain relevant.

Moody’s downgraded SVB Financial and Silicon Valley Bank by one notch, from A-3 to Baa1. Moody’s report said that this “reflects the deterioration in the bank’s funding, liquidity and profitability, which prompted SVB to announce actions to restructure its balance sheet.”

Moody’s also downgraded the rating outlook from “stable” to “negative,” meaning another downgrade might be next, “reflecting the uncertain macroenvironment and specifically, the potential negative implications for SVB if the declining venture capital investment activity and high cash burn does not subside.”

OK, folks, we need to find an evocative name for this bust, a name that will make it into the annals of history, as did “Dotcom Bust.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

SVB is now a dead duck…oh well!

It’s FDIC FRYDAY once again, as fond memories of 2009 return!!!

Who to blame for the failure to require banks to engage in realistic mark to market of their assets daily? SEC and FDIC in 2009, it seems. Now we get the threat of an even larger “mass extinction event.”

The Free Candy Sugar Crash

In startups I have seen personally that got infusions of cash from finance backers, initially there were a LOT of parties with exotic food and booze, new cars and houses and furniture, bursts of newspaper articles touting how wonderful they were, then employees laid off, then I quit watching.

Great/spectacular work as always Wolf – thank you! :)

The name for this bust is obvious to me, and I’m very surprised nobody else has already suggested it (that I can see?)…

Perhaps you can take a lot of the credit for the name (?)…

A little bit irreverent – but perhaps that is appropriate: WTF Bust

LOL.

“Moody’s downgraded SVB Financial and Silicon Valley Bank by one notch.”

—————————————–

too little, too late

says something about Moody’s

Yes funny, isn’t it. Still investment-grade too, on the day of collapse, LOL.

But this went very fast.

It didn’t quite go to heck in a straight line, but it was pretty close there at the end…

The Scumbag FED Bust

That is the cause

not to worry, the bust will be blamed it on covid

Aaaand SVB is gone. FDIC seized it this morning.

Death Valley Bust or

Death Valley Disintermediation.

Silicon Implode

Silicon Faceplant

Honestly, this doesn’t worry me at all for the economy at large.

BEFORE COVID, available jobs had climbed to ridiculous heights. This (IMO), is about demographics. The ratio of new workers to retiring workers has been moving toward 1:1 for long, long time. But, 2010 is actually when we would’ve seen the impact of the Great Boomer Migration (out of the workforce) — except all that data was hidden under the Housing Bust Rubble.

So, we maintained the illusion of a decent new:leaving ratio for another decade, because it took so long to rehire the millions who get canned in 2009.

Go look at the monthly NFP numbers from 2019 to get a feel for what’s coming. The COVID recovery phase is all but over – (and we lost 2 full years of legal immigrant workers in there, too).

Nobody has a model for a recession where there are 2 jobs for everyone looking. Heck, we don’t have any models for that in a good economy, because it never happened, (far as we know).

Yeah, the tech sector will take a hit. But, it’s not like the need for tech will vanish. This is trimming at the margins of a much, much larger workforce. And, (so far), the big name layoffs haven’t touched the U3, because nobody has an easier job finding work in the modern age than college educated tech workers. (And remote work means moving is no longer mandatory). How many Silicon Valley workers will be working in Durham without having to move?

The fact Openings was 10 million BEFORE COVID tells me the Openings numbers are not a post-COVID spasm (like some of the other stuff). My view — until Openings drops to about 7 million, recession is nearly impossible, (as is getting inflation down to 2%). I think it may drop to 4% before it stalls, but we are not heading for the 70s again, nor the 2000s. It’s a whole new ballgame, and NOBODY knows the rules …. yet.

The aftermath will be the true Great Reset: gold-backed money, small, responsive government, death of Empire, etc.

Was SVB’s business model unique? Are there other banks as massively exposed to the private equity space as SVB?

I thought that post GFC regulations shored up bank balance sheets and prevented this kind of thing?

SVB had about half of all startups in the US. The other half was spread over all the other banks.