The startup and VC bubble is tied to a booming stock market, but stocks are unraveling, and that strangles the money flow.

By Wolf Richter for WOLF STREET.

Silicon Valley Bank, under the holding company name of SVB Financial Group, is the 13th largest bank in the US, with $214 billion in assets. It is heavily involved in the ecosystem of startups, venture capital firms, and private equity firms in Silicon Valley and other cities in the US, and globally.

It reported earnings Thursday evening, which included a lament about the downturn in the venture capital and startup ecosystem and the “volatility” in the stock market – “volatility” meaning that the Nasdaq Composite is down 27% so far, which is strangling the money-flow into the startup ecosystem.

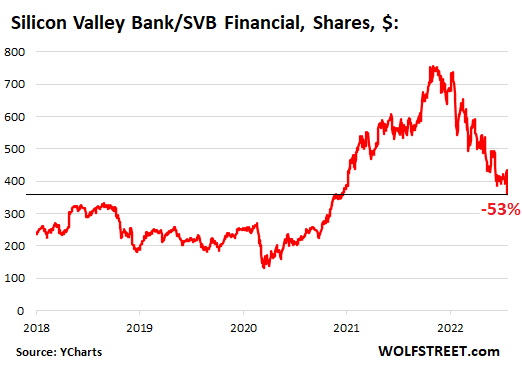

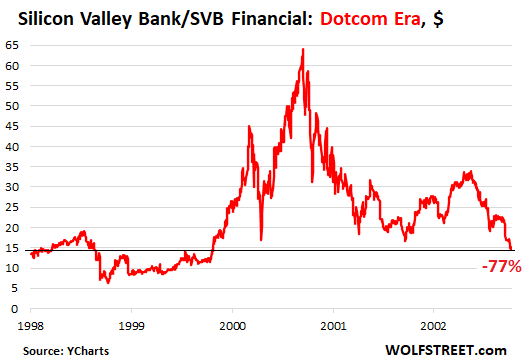

On Friday, its shares [SIVB] plunged 17.1%, and are now down by 53% from the peak in early November, 2021, which was about when the Nasdaq peaked. Silicon Valley Bank also went through the Dotcom Bust: After a huge run-up, its shares collapsed by 77%, about the same as the Nasdaq. So here we are today, with its shares, after a huge run-up, down 53% so far (data via YCharts).

“The IPO window remained closed.”

In the CEO Letter to shareholders, the bank lamented that the “IPO window remained closed,” and that “companies across all investment stages experienced challenges to accessing liquidity, with total VC investment declining 24 percent quarter-over-quarter.”

It said that the reduction in fundraising by its startup clients, “coupled with increased burn rates – as companies with already accelerated burn rates took proactive actions to reduce future spending – pressured Q2 balance sheet growth.”

It warned that “the increase in unreserved charge-offs and new NPLs [non-performing loans] may indicate potential emerging pressure from market volatility.”

This “market volatility” means the decline in the stock market because in this ecosystem everything hinges on a booming stock market that gives early investors, such as VC and PE firms, a chance to get out and sell their shares to the public at huge prices, and it gives startups a chance to raise lots of money, and pay off all obligations. But now that IPO window has closed.

And the letter said, “We have adjusted our full-year 2022 outlook to reflect our expectations that challenged public equity markets and declines in venture deployment will continue for the remainder of 2022, which will pressure our balance sheet growth.”

During the earnings call, CFO Dan Beck said that the expects another 20% sequential decline in Q3 and Q4 in private venture investing.

The letter also noted that venture capital and private equity firm are sitting on “record levels of dry powder (8 times higher than 2000 levels) to put to work, and we believe they will do so as valuations stabilize.”

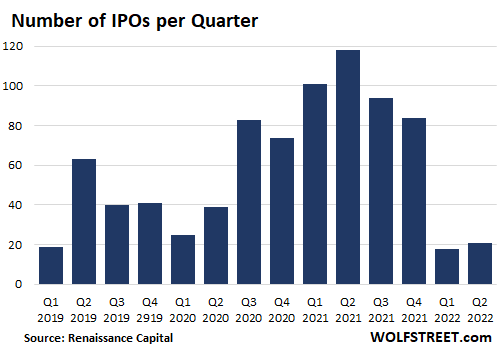

In Q2, there were only 21 IPOs, and most of them were minuscule, according to Renaissance Capital, compared to Q2 last year, when there were 118 IPOs:

Then there’s the suddenly plunging income.

Net income in Q2 dropped by 34% year-over-year to $333 million, the bank reported. Net income per share dropped by 38% year-over-year to $5.60 per share. This was way below analysts’ expectations, as polled by FactSet, of $7.82 per share.

The Parallels to the Dotcom Bust.

Silicon Valley Bank survived the dotcom bust that ravaged the Nasdaq, Silicon Valley, San Francisco, and investors all around. The Nasdaq plunged 78% from the peak of 5,046 in March 2000 to the trough of 1,114 in October 2002. And with lots of help from the Fed’s money-printing and interest-rate repression that inflated all asset prices, the Nasdaq finally reclaimed 5,000 in 2015. It took 15 years.

During the Dotcom Bubble, shares of Silicon Valley Bank skyrocketed, multiplying by four, from early 1999 to September 2000, but then shares plunged by 77%, giving up nearly all the gains, and taking it back to 1998 levels.

Not shown on this chart, but I’ll mention it for your amusement: It took SIVB until 2013 and lots of money-printing and interest-rate repression by the Fed to reclaim its 2000 high for more than just a brief moment:

In this crazy era, SIVB multiplied by nearly four, from $190 to $750, between late 2019 and the peak in November 2021. And so far, shares have given up about two-thirds of that gain.

SIVB is a barometer of what is happening in the startup ecosystem: The funds from the stock market have nearly stopped flowing into the ecosystem, and early investors are having trouble unloading their shares at sky-high prices, which changes everything.

There is now a new prudence among these investors. Valuations are getting slashed. Suddenly startups are exhorted to cut their cash burn-rates because they won’t be able to raise new money to burn if the prospects of positive cash-flow are in eternity somewhere.

There is now talk among startup CEOs about the length of their “runway,” meaning how much time they have left before they run out of money.

Startups of all kinds, from crypto to biotech, are laying off people left and right in order to cut their expenses and lengthen their runway. And they’re cutting advertising expenses, because that’s the easiest to cut.

And the whole thing goes into low gear, and when these companies run out of money, they vanish, and their employees go somewhere else to find a job. At this point, there is still huge demand for tech workers, and it seems they’re getting picked up pretty quickly for now. But this is just the beginning – the first two quarters of deflating the biggest startup bubble and stock-market bubble ever.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

First!

Lol

…and you squandered it.

Bought March Tesla otm puts today. It is going to $100. Then $50.

Fool. Tesla shorts lost $1B in one day this week. Fools never learn.

Never bet against Elon Musk. Everyone who did went bankrupt.

Kunal,

Hold your enthusiasm. Tesla shorts made lots of money since November. As of the close today, TSLA is down 34% since November 4. They can “short and hold.”

Folks, short ARKK. Not because I like to, but because you get TSLA and then all the other junk that’s headed to $0 as a bonus!

Kunal has really drunk the kool Ad.

He can’t see the forest for trees.

Yes, we know real estate can never lose a lot of value or crash again either, especially in SF.

Kunal,

I will cover my short as soon as Enron Musk scrapes enough cash to buy Twitter. But, chances are I will cover it 3/4 $Trillion down from here.

No need to short arkk.

Just be long Sark.

I swing trade between ARKK vs SARK b/c of whiplash from HOPIUM dip buyers, front running on the hope that Fed will pivot back before the year!?

I bought long call on ARKK with short and intermediate puts.

Not that hard to google really, I guess $7B and bankrupt is all the same. Also, pretty sure that Spiegel and Burry are all bankrupted as well and living under a bridge.

“Tesla short sellers have made nearly $7 billion so far this year” – Marketwatch published in May 2022

They only lose if they cover, Dumbo! Till then they are sitting on cash from borrowed shares, and elon will have hard time to pay interest to maintain that corner, as interest rates goes up. Seller has sold, its the buyer who pays the interest right?

Not quite works this way. In any case, it is best not to sell borrowed shares, if you want to sleep at night. You can lose more than you know. Better use short ETF or put contracts if you must.

> Never bet against Elon Musk.

That tone of fanboy enthusiasm says it all. NOBODY, EVER, gets that from me. The only being in this uncertain universe that gets it is a theoretical being, not a human.

I love somebody spouting such a “never” with “advice.” that’s where I make all my money.

But should we still…

Not fight the Fed?

When you short, you have given up your destiny to things out of your control. If you buy a few high quality dividend payers at the right price, then price action in the market doesn’t matter as you get paid whether stock price is in bull or bear market.

You still have to know what you are buying, and probably need to buy at least 10 in case one or two go south. But the bottom line is you get paid to hold a position no matter what the Fed, Putin or other market players do.

I bought some TSLA calendar puts today as well. It was outperforming both SPY and QQQ by such a margin that it looked unsustainable on a very short term.

Only did 8/19 on the long side. That should be long enough for the fed to work their magic.

When Tesla crashes QQQ is going to look like a flat line.

Case in point biggest Canadian stock Shopify (SHOP).

Appropos of everything wrong with Underpants Gnome VC, I always wondered what exactly SVB’s business model was – how exactly was it supposed to make money from zero revenue/mighty negative income startups?

The very few which made it to IPO (or a lot less profitable acquisition) could deal with any bank for any bank things.

What was SVB’s unique selling proposition supposed to be and was it one that wouldn’t repeatedly bite them in the ass (ie, traditional loans to startups losing tens of millions…)

These startups have lots of cash, which they raised from VCs and other investors. It’s their bank, it lends them money, takes their deposits, charges them fees, lends their executives lots of money with the shares of their company as collateral… It does business with the VC firms and PE firms that fund these companies, and those are big deals, and it’s involved in every aspect of this huge industry, and in the transactions, and it’s taking fees and charging interest. It has about $70 billion in loans outstanding, among other things.

I worked for a PE backed startup in 2014-2015. We had our debt serviced by SVB. We weren’t running a profit and our PE goal was to grow Rev 3x and then flip to another bigger PE firm. Little concern to actual profitability, mainly growth through M&A. Problem is we kept funding our acquisitions with cash and then couldn’t afford operations due to revenue cannabilization from poor M&A targets. It was just a huge mess. I worked for the CFO and was responsible for FP&A. We were having cash flow issues and missing bank covenants. CFO asked our controller to do some shady JE/accounting to avoid us missing bank covenants to buy us time for another round of VC capital raise. I quickly left after this bc of moral and ethical concerns. Was a big wake up for me. And I doubt they were the only company out there playing with the numbers…with debt from SVB.

Good for you for having a moral compass. I am sure you have some amazing stories and salivating stories around the trusted friends. Thanks for sharing some of the details behind the scenes.

Cooking the books almost Enron-style probably represents at least 25% of the venture capital world.

How has your former PE firm fared since you left ? Are they still in business ?

Thank you for sharing your experiences.

It might be a silly question but I’m from outside the States. Weren’t your management afraid of this shady shit getting exposed via regular audits of some kind of federal agency or something?

Interesting times. I’m the medical field here. I know of numerous doctors who’ve sold their practices to P.E. over the last few years. These P.E. companies want to extract every dollar and then re-sell them later.

But will the P.E. model survive? After all, it’s all dependent on access to cheap capital. And capital is no longer cheap.

From what I know, 30 years ago, PE firms typically would look to buy a struggling company that could be righted with some good management skills. Turn the company around and then do an IPO in 5 to 7 years and get their big payout.

Now from my understanding, they look for healthy companies with cash, low debt, good assets. It may be a public company they take private. It is easy to go to bank or investors to get a big buyout loan. Now the payout is immediate with the big consulting fees for the buyout. The CEO typically gets a big buyout too. The buyout loan they took out is now the responsibility of the company to pay back.

Now the once healthy company has lots of debt and big debt servicing payments. They have to sell assets or lay people off.

I wonder if there is anyone who keeps a track record of how man PE buyouts go into bankruptcy within 5 years.

Thanks for the insidery info. SVB may have $70 billion in outstanding loans…but what *really* matters is who the loans are *to*.

As a class, startups that are hugely cash flow negative, with pretty damn vaporous business models on the unit economics, seem like really bad credit risks.

Traditional lenders would not even consider debtors like these.

Sure, SVB may have a “niche” but not every transient niche is sustainable.

I like the idea of SVB as a concept (startups need all the help they can get and many players are too hidebound to even consider helping) but…some risks seem fundamentally bad unless transformed in some clever way.

I just never grasped the supposed SVB “magic” that allowed them to lend profitably to startups that horrified traditional lenders.

They all but created ARR lending – lending to VC and early stage PE backed companies based only on annual recurring revenues, not actual cash flow. Companies burning cash, but the only covenants are based on recurring revenues (SaaS models). Usually three year loans, backing lots of VC equity below you.

Your way out of the loan as a lender is not through cash flows paying down debt, but the next series raise or sale to a PE/strategic buyer, thinking they will pay for the revenue base and fold it into their cost structure and make it profitable.

If no next series raise or IPO, the lender takes it on the chin because there really isn’t anything to recover.

Lots of banks and nonbanks piling into that asset class playing follow the leader the last few years. Could get dicey if valuations keep puking.

So is Softbank the Pac man that gobbles up all of this garbage?

Thanks for the pro level info.

But still seems pretty damn risky for an FDIC commercial bank and not *that* far removed from lending to MLM players (ie things go to hell fast if the next round of hopium addicts don’t take the current round out).

A lot of banks stick around for decades because 1) they avoid riskier deals like the plague and 2) in the deals they *do*, they structure their loans so that everybody else tends to get wiped out before the banks get a scratch if valuations are off.

In VC, the valuations seem to become so crack addled, that *everybody* ends up being taken out and shot.

They invented the concept but they aren’t doing the riskier stuff.

These days, banks will maybe lend the revolver and 1.0- 1.5x ARR to a company, but the nonbanks take the deeper risk, up to 3.0 and even 4.0x ARR (prior to this pullback).

I think banks loan books and balance sheets are comparatively much healthier than 2009 and even 2001; the direct lenders are probably sitting on the most risk in these tech deals. They’ve become so large it’s amazing they get by without any regulation.

Thanks for the addtl info, and I get that there are players further down the debt stack who get hurt first/wiped out before groups like SVB might lose a penny…but…lending against ARR is still lending against *revenue*…which isn’t income.

And if a startup’s unit economics are sufficiently screwed up (many/most are) then the cost of obtaining $1 of revenue might exceed $1 (forget about covering overhead).

Basically such startups are *paying* for “revenue” growth and there is nothing left to cover for all other costs (admin, loan repmt, etc).

In these cases, once the successive lending suckers back away, the startup turns into a pure loan incineration machine and even bank intervention due to covenant violations can’t stop it…because the unit economics have never made sense (it takes more than $1 to acquire/retain $1 in revenue).

I get there are degrees of unprofitability and shades of gray but the latest batches of idiot startups seem particularly bad on the unit economics (and are operating/learning/screwing up on a massive scale, very quickly)

I gotta learn me some of this new-fangled accounting stuff. Wow!

“$7 REIT with 16.5% Dividend”

I saw this text with the picture of a happy couple at the top of the comments section. Should we invest? :-)

Were they “dancing through the tulips”?

I saw the same ad just now. Crypto REIT? 🤣

Sounds like a great example of Zeno’s paradox. You can get 16.5% for forever and still never break even.

“SIVB is a barometer of what is happening in the startup ecosystem”

The former vice president of Silicon Valley Bank has agreed to plead guilty to two counts of securities fraud, according to the U.S. Attorney’s Office. Nathan Guido, 38, of San Jose was also charged with two counts of securities fraud. Gad and Guido face up to 20 years in prison and a $5 million fine for each count.

Mercury News, July 1, 2021

Other counts include document tampering, fraudulent loans, identity theft, criminal contempt, and so forth. Gad could face up to 25 years in prison and $1,000,000 in fines for document tampering and identity theft. There is no maximum penalty for criminal contempt.

CBS News, November 23, 2021

Business as usual. Happens all the time. It’s rare to get caught.

Don’t think of it as ‘finance’. Think of it as a full-employment program for grifters.

Not a violent crime, otherwise out on parole.

If he worked on Wall Street nothing probably would happen. Is California tougher on these crimes or will he eventually plea deal for 1 year probation. LOL

Interesting the co-founders from Three Arrow Capital are now in Dubai. Singapore is probably more strict on fraud.

Also, I guess a worker at coinbase was doing some insider trading. But Coinbase has said crytpo’s are not securities so insider trading should be okay. LOL There are just very few rules in cryptos and ripe for scamming and bending moral rules.

Guido the Banker.

Sounds promising.

And I’m Italian American.

And speaking of “Risky Business”…

Cas127 – I thought Guido was “the killer pimp.”

Too late to the game now but wish I can fancy package my idea of selling fart in a jar. I think certain social influencer had some success on doing that. If there’s a way to market that to VC when the liquidity market was still free flowing…

Phoenix_Ikki – That’s methane capture! You would be in good with the ESG investors also.

WOLF

Your closing comment

“…But this is just the beginning – the first two quarters of deflating the biggest startup bubble and stock-market bubble ever…”

is both scary and fascinating. I spoke with my investment Mentor today and he believes we are looking at 6 to 7 years of limited / no growth.

Holy Toledo. I’m pretty bearish, but I wouldn’t have guessed 6 to 7 years.

Usually stock marker runs in 14-17 year cycle,but it’s been manipulated for last 40 years.

Society just isn’t prepared for a really long stock draw down. If I am not mistaken there has been one period in 20th century that holding t-bills would have outperformed stocks for 19 years as the stock market burst and took a long time to recover.

Who knows, we could be on the verge of that again as Fed blew the biggest asset bubble and then is trying to prick it before inflation eats us all.

But we had it so good for so long!!

It was nowhere near “so good” for the vast majority.

Just barely shy of “torches and pitchforks”.

And DC has known it.

My Mentor was in markets since 2012. Totally on the same page.

Is that a typo? If your mentor has only been in the markets since 2012, ask if his dad is available. Grandpa would be ideal.

All would depend on whether the Fed caves in or not. It is unbelievable that America calls itself a capitalist country when everything depends on what the money printer does. Cutting the Fed to size is what we need if we want a true capitalistic society.

Who knows when the Fed will cave?

If FED caves in before bringing the inflation down then the bond market may lose the trust on FED.

It means yield have to go quite a lot higher to sell bonds.

It is the ultimate capitalist country for those that have access to digitized capital. That would be the FED, bankers, wall street and favored customers.

Goldman, Buffet, Romney ………………… Jim Cramer ……..

Greenspan, Powell

all the stock market cheerleaders

crypto kings

they think themselves rugged capitalists

and so do their sycophants

(what have any of them created?)

There is an incredibly elaborate shell game, a perpetual motion machine as long as one can con enough actually productive people to buy into it.

We know exactly when the Fed will cave. Look at the FEDFUNDS series on the St. Louis Fed’s FRED tool. It shows the federal funds rate since 1954 and highlights all recessions in grey. The Fed has dropped the fed funds rate significantly in every recession on that record (even both Volcker recessions). In wartime, peacetime, during high or low inflation, and regardless of the severity, they dropped the rate every time recession hit.

So the Fed will ease up on interest once we’re in a recession. It might take more than just entering a technical recession… The fed might wait until they see some actual job destruction, but they’ll chicken out in the next recession. This time won’t be different.

“Things that never happened before, happen all the time”.

In the 1970s they only lowered rates when inflation came down.

It’s possible to have a recession without inflation dropping, and then your thesis may break down. Arguably this has already been going on for 6 months, based on the GDP estimates. It also happened in 1973, when rates went up first half of the recession – and didn’t come down much either.

It will be very interesting to see what sort of forward guidance the Fed provides this week.

P.S. When the Fed’s lowering rates, the stock market is often tanking (see 2000-2002, 2007-2009). I’m not sure how so many people fell for the idea that falling interest rates are good for the stock market, because the empirical evidence is the opposite. A lot of people are going to be very surprised over the next couple of years.

WS,

I imagine that IF the Fed’s actions have indeed softened demand sufficiently to plunge us into a real recession, especially as unemployment grows, then inflation will drop off quite a bit. That would pave the way for Fed to change direction on the federal funds rate. The 1973-74 recession began with the FFR at ~10% and the recession ended with the FFR ~5%. It peaked near 13% in ’74. But about half-way through that recession, the Fed started dropping their rate aggressively. The FFR was cut in half from the recession’s beginning to its end… Still a pretty big drop.

Sure, there’s always a possibility that the Fed will behave differently than they have consistently behaved since the post-WWII period began, but what’s the probability of that? Pretty low. 100% of recessions in the last 7 decades shown in the FRED tool have ended with the FFR lower than when the recession began, so my answer is reasonable. The FFR is very likely to be lower at the end of the next recession than it will be when the next recession begins (or is beginning).

Excellent point – it isn’t *that* much of a stretch to call the US a centrally managed economy given the mega levels of jiggery pokery the Fed engages in to manipulate money supply/interest rates.

Sure, the Fed ain’t setting production quotas for potato vodka in Boise, but their brand of centrally managed totalitarian monetary “control” seems to have operated as poorly in practice – 20 yrs of fevered ZIRP have led to idiot boom after idiot boom and certain bust after certain bust.

That’s some Soviet levels of success, DC.

Despite all the financial gimmickry, new economics, ‘it’s different this time’, and the usual mischief and avoidance of reality by authorities, the ‘biblical’ 7-year natural cycle seems to still exist.

Paraphrasing Francis Bacon: ‘Suppressing nature makes it more forceful in the return’.

We are already deep in negative real growth. ~10% CPI inflation!

Dum, da dum dum!

So if you bought there shares at the peek of the dotcom madness they were $65 a share, you could have sold them last year for almost $750 a share? Or today for $361. Not too bad

They’re not done yet.

There is no way of knowing if they would have been in business today. They could’ve gone to zero. Any company could go to zero.

What you said proves that for LONG TERM investors, entry point doesn’t matter too much. What matters the most is when do you SELL. Not many people buy a stock and say “I will sell when I reach XX percent. ” They say stuff like “I’m holding forever” or “This stock should double in 5 years. ”

Most people then sell it because it never met their expectations. Their expectations were probably wrong to begin with. Or they sell when it drops 20% and say “so glad I got out.” But like Buffet says “If you liked it at $10, you should love it at $5.”

Good last sentence N: Exactly what my SM ( stock market(s)) mentor said waaaayyy before WB who is also an absolute ”mensch.” or at least how I understand that word.

Listen and LEARN, here on Wolf’s Wonder and perhaps many other places on web and in library(s)…

BEFORE you invest and you are likely to save a TON…

BTC…LOVE LOVE LOVED it at $65K.

Should I double down with the rest of my nest egg at $22K?

/snark

Low income people keep chasing cryptos as a way to become rich doing nothing. The scams just keep popping up all the time.

——————————————————–

But to this community of family, friends and fellow church members, Alexandre was like a shepherd leading a flock to what they hoped would be life-changing fortunes.

The weekly returns were so big and consistent, a minimum of 5 percent and sometimes almost 10 percent, that Victorin projected he would become a millionaire after a little less than a year of investing with EminiFX.

“I took out at least four loans from different banks to make sure the dream he was talking about, as a family, we were ready,” Victorin said. He still has faith in Alexandre.

“We believe in this guy,” Victorin said. “We believe in our CEO. He is a good guy, a great guy. And we never met somebody like that, very down-to-earth, very respectful, transparent with a lot of charisma.”

Like so many other investors, Victorin, who lives in Massachusetts, attended Thursday night Zoom meetings, where he said Alexandre talked about being a part of a system where people could make their money work for them instead of them working for money.

“EminiFX is your sure path to financial freedom,” the company website promised. It was an appealing pitch that brought in millions of dollars from thousands of investors in the United States and abroad.

Eddy Alexandre has been charged with commodities fraud and wire fraud offenses. (Department of Justice)

The FBI says the purported proprietary trading platform used by EminiFX was a fraud and that Alexandre was operating a cryptocurrency and foreign exchange Ponzi-like scheme that collected more than $59 million starting in September 2021 until he was taken into custody by the FBI in May.

More TV material for American Greed! Seems like there is a bottomless pit of this kind of stuff.

The most reckless fed ever starting in 2009 with suppressed interest rates all the way to zero and QE infinity when the markets blinked. I have no idea what the future looks like with tightening and a liquidity work through. Forget the stock markets that’s a game looking for someone to sell higher to since the only returns one gets is stock buybacks and maybe 2 percent dividend or less for most. I’m taking real economy with jobs manufacturing sales services housing infrastructure food production energy transportation (autos) and leisure.

Lots of real jobs happening everyday that are productive and value creation.

However the most reckless federal government ever has spent trillions recently on capital destruction projects like PPL and direct payments to folks with a social security number. That comes with a cost and the low interest rates and free money brought forward a large 5 trillion spend that was not earned and those goods and services will not be needed for the 7 years hence the slowdown

Well, at least they built the highways across the continent. That’s good for something.

”Eisenhower Multi Lane Interstate Highway System” was built with the clear intention of being able to move masses of troops as fast as possible in the event the trains/planes were disabled.

Hence the ”drive around” on almost all overpasses in the event the overpasses are collapsed and block the main lanes.

Keep ALL your powder dry folks, it may actually be needed sooner than had been anticipated, even more recently than, when Interstates were designed.

And remember to work with ALL the neighbors who are willing,,, gonna be the #1 best survival effort everywhere.

VVNV-your last sentence both the best, but in contemporary ‘Murica hardest to process, advice that can be given. (Great civilizations arise from general cooperation rather than ‘rugged individualists’…).

may we all find good neighbors and a better day.

Ban said: ” I’m taking real economy with jobs manufacturing sales services housing infrastructure food production energy transportation (autos) and leisure.”

———————————————

Why do real work if you can be the ultimate capitalist ,,,,,,,,,,,, a financial engineer with access to cheap capital. Isn’t that want all the well born aspire to?

Get close to the money created within the FED/banking/wall street system and financially engineer your wealth. Even the marginally trained ones mitigate their risk with Limited Liability companies so they keep their winnings as they plunder.

Isn’t this taught in the right prep schools?

And all the examples ………….. Goldman, Buffet, Romney, Powell, etc.

(These guys really believe they produced something; that’s what happens when you are brought up on Daddy’s knee, Mommy tells you that you are wonderful, and you believe your own propaganda)

I still think the Greenspan fed of the ’00s was worse. Good lord the aughts sucked.

The world hit quite a brick wall there. But it wasn’t enough, to prevent Powell from trying his best to emulate it. I presume we will keep it up until we hit a truly sufficient barrier.

Exactly right Wolf, it reminds me too of the 2000 dot com crash.

They were doing the same with “shell companies” that were being touted as the next Microsoft galore, and would do reverse splits to get on the Amex.

Even mutual funds were touted, and the infamous Janus 20 was very similar to Cathie Wood’s ARKK fund today, touting they were buying the future leading companies, and their stocks weren’t generating income at all.

All fell like a deck of cards to the ground.

I read recently that fund managers, and institutions have sold stocks and have moved their proceeds into bonds, making them the largest allocation ever! – This was a report from BOA.

So that means there are more sellers, and less buyers, and when liquidity in stocks gets low, – look out below, because this market will drop like a elevator.

Argh, Janus 20. Just got a twitch in my neck. I fell for that one too.

I had to turn off the ad blocker to see the ads people are talking about. Ads for VC services and ARKK ETF on the site that explains why you shouldn’t patronize such things. I guess they figure people who are INTERESTED in the subject, whether positive or negative, are more likely to fall for their pitch than people who don’t know anythng about the subject.

It seems the AI bots have a file on me entitled “Bigger Fool.”

Honestly this was the scariest quote of the article for me:

“The letter also noted that venture capital and private equity firm are sitting on “record levels of dry powder (8 times higher than 2000 levels) to put to work, and we believe they will do so as valuations stabilize.””

What the heck are these VCs going to do with all that money? Wolf often mentions that there isn’t really “money sitting on the sidelines” but this seems to contradict that. On the other hand William Ackman just announced that he would return $4B he had raised for a SPAC since he couldn’t find anything to invest it in so maybe the VCs will also start returning the money they raised. Ha!

There’s over $2.2 trillion being absorbed by the Fed’s RRPs, so there’s a lot of “dry powder” out there.

As the Fed reduces its balance sheet, that dry powder will be slowly absorbed into longer term treasury securities.

Very slowly, and in the meantime the speculative frenzy will continue because people absolutely hate being stuck with cash paying below inflation.

“Dry powder” — good phrase — isn’t that stuff that easily blows up?

I’m re-reading “The Big Short” (what a great book it is!). It’s scary how much that madness reminds me of the present. I can almost hear Steve Eisman screaming obscenities.

this is nothing compared to 1200 banks going down and essentially rescuing the world from Hades…

After this week, 1/4 will be it for the year, Inflation is backing down fast,

rates are backing down, Natural gas will be high for years, if your not investing in MLP or royalty type streams your missing out for years..

I love my 11% yield, I just keep adding

App crap snap.

Anecdotally – I’m seeing lots of VC funded mid-level startups cut their budgets.

Nothing to do with performance, all about investors getting spooked and tightening the strings.

ahhhh memories ! made a lot of money with firsthand technology funds – think a 2008 version of ms wood’s – magical thinking investment funds – lost most of it in biotech

Both of them are like shooting craps. Only all-in high rollers would understand. I do understand, and it keeps me out of the casinos.

Alternatively, the world of Buffet is long term boring. It does have its ups and downs but doesn’t go to zero. Unfortunately, he loves collecting dividends but hates to pay them, but you could sell a share occasionally for walking around money or a down payment on a house, and show up at the annual meeting for a free ice cream.

The Big Short, Margin Call, etc are all worthy of review again. Nothing new with SVB at all. First hand experience decades ago. Now just reconfirming what lots of people knew then. 😬💸💰🤪

I was working for various dotcoms (now all out of business) during the ’97-01 craziness. Every week I’d see something that said it was unsustainable: perhaps a CEO who couldn’t explain what a database was, or a first class ticket to Manhattan and a $1,000 hotel room to have a two hour meeting about a project that everyone knew was going to be scrapped. And no one seemed to care about the waste or incompetence.

Part of this tragic system was enabled by slight-of-hand language tricks… Such as subtle changes to valuation models using “anticipated” revenues – not “forecasted.” My favorite was hearing about the “static” in reported numbers. Yup, that static was that they were awful.

Anyway, yes, the word “volatility” is now getting misused to… wonder how many people are catching on?

[My favorite was hearing about the “static” in reported numbers. Yup, that static was that they were awful.]

That kind of wording reminds me of the town hall meetings that the CEO of the company that I work for gives. I don’t attend anymore. Now I just ask my friend if anything important was mentioned in the meeting. Usually the answer is no.

but for every bad story, there are the good ones, I put the first ASP fixed ops product into dealership websites and had 3000 dealer customers at one point, UPS, American Golf for every course. Would be at Toyota, Honda and Nissan same day for meetings. In fact, our little product was so far ahead of marketing departments they had to grasp it for a bit.

All from a garage….or in Cabo surfing…..dot bombs were a plenty but that is why simple and sound works….

Depends upon “what your definition of is, is”.

Yesterday startup.

Next week the AAPL and MSFT might send the markets up. On Aug 5 BRK.B might need a jump start, but BRK/B battery is 100Y old.

Mohamed El-Erian: Signs the global economy is slowing rapidly …

Before you know it Sand Hill Road will be nothing but check cashing shops and second hand stores where the VC’s used to be.

And cougar night at the Rosewood. Can’t forget that.

Again, Wolf Richter does all the heavy lifting. His work and stewardship of the comments gives me the confidence that, no matter how sharp or high the markets bounce in the short term, they will be returning to at least their lows and below.

Ukrainians live like partisans. Germany conserve less natgas.

We might indulge less. AMZN gap lower between Apr28/29 on negative surprise.

If we are in a real recession, not a technical one, AMZN shouldn’t be able to filled the gap.

1) SVB Financial Group (SIVB) backbone #1 : Nov 9/12 2020, 346.80/324.56.

BB #2 : Jan 22/29 2021, 497.85/435.77.

2) SIVB was breaking apart on BB #2.

3) July 21 negative surprise on earnings and volume sent it down to the congestion area above BB #1.

4) If we are in a real recession SIVB should be able to fill July 21/22 and

June 9/10 gaps.

5) SIVB downtrend channel : Feb 16 to Mar 29 to May 4 highs. // Parallel

from Mar 7 low.

6) SIVB might breach above this channel, before plunging below later on. After Oct lows a mighty bear market rally….

7) For silicon valley entertainment only.

Tsunami can flood Archengel in the White sea near the Barents sea.

Mr. Richter, what to you get, 10 cents for clicking on one of your advertisement’s? How many would it take to pay for a mug?

Thanks

Please do NOT click on the ads to do me a favor. Google penalizes me for that. Their algos can figure this out in no time. It ends up costing me a lot of money.

I’m not sure what my take-away from your comparison with the dot com bubble bursting, which, by the way, I suggest was the beginning of the make the people pay to bail out the speculators philosophy. After so many feigns by the central bank that ultimately transferred income and savings to their clients, the oligopoly banking structure, I have my hand on my wallet as the Federal Reserve makes its next move.

As Grantham has pointed out, the dot com bubble was a singular bubble. This is a multiple bubble phenomenon in which three bubbles have been inflated, simultaneously, and are now deflating at a coordinated rate.

At the same time, the ocean of cash ( provided by the inflator) available for speculation is scheduled to be reduced. The thing about deflating bubbles is that the economic effect is painful and deflationary.

Invest short term, the long term is a big question mark. Sometimes, I think because the prospects seem bleak. People avoid bleak prospects and the euphoria gives way to the drab reality.

In my view this afternoon, I assert that America cannot continue to be the consumers paradise with a chronic trade deficit of 6 – 9 pct while the consumers are broke.

A big portion of deflation seems appropriate at this moment in American life. Let the prices fall to meet the increases in wages Americans have enjoyed these past 40 sum years.

Hopefully, the Fed has by now realized that the interest rate is a result of the free market transactions, the independent variable, determined by the interactions between the dependent variables of transactions.

Which brings me to my primary point which was to relate an uplifting experience I had yesterday. Walking through Costco, a red neck looking dude was wearing a tee shirt with a printed paragraph that for at least a moment clarified my confusion. The tee shirt hand bill read:

“We” have the government our founders warned us about.

So, as I turn control of the world over to the next generation, which changes every year, good luck.

Don’t forget the old people. You know, Grandma and Grandpa, remember them. They weren’t so bad, were they.

Grandpa and Grandma weren’t bad…but their kids absolutely sucked.

Signed,

The Grandkids

On Wednesday, the Fed is scheduled to increase the fed funds rate by 75 basis points raising the target rate too, I think, a puny 2.25 and 2.5 pct, while inflation rages at 10 pct.

Has the Fed brought a pea shooter to a paint ball contest.

On the one hand , yes. They are monetizing the Wall Street losses by allowing inflation to inflate the general price level and cushion the asset price inflation.

On the other hand, no. They are moving slowly to minimize the financial shock that a more aggressive approach would likely cause. Like massive bankruptcies, massive job loss, and greater losses to the long suffering savers who have clung to zirp treasuries.

Right now, I choose the other hand.

“It warned that “the increase in unreserved charge-offs and new NPLs [non-performing loans] may indicate potential emerging pressure from market volatility.”

There is only one source of recovering cash from a non reserved charge offs. That is from net profits. Hope they are very fat net profits to cover the non reserved charge offs that are in their pipelines. This is why reserves for charge offs impact net profits, they are a portion of them that are reasonably not expected to arrive at the bottom line.

The lights are all on, but nobody at home.

I remember talking to somebody from Silly Valley Bank back in 2002. This was just after Tech Bubble I, and they were putting a lot of money into farm land. In Sonoma County. With grapes growing on it.

It was a little confusing to me, but they said that there was nothing in Santa Clara County worth investing in. Apparently, the soil there gives the wine a funny taste.

. . .and the startups didn’t taste so good, either.