SVB is massively involved in all segments of the startup scene that is now facing a mass extinction event.

By Wolf Richter for WOLF STREET.

SVB Financial, which owns Silicon Valley Bank, the 16th largest bank in the US with $210 billion in assets, came out with some fascinating announcements late yesterday and early today about shoring up its balance sheet and liquidity.

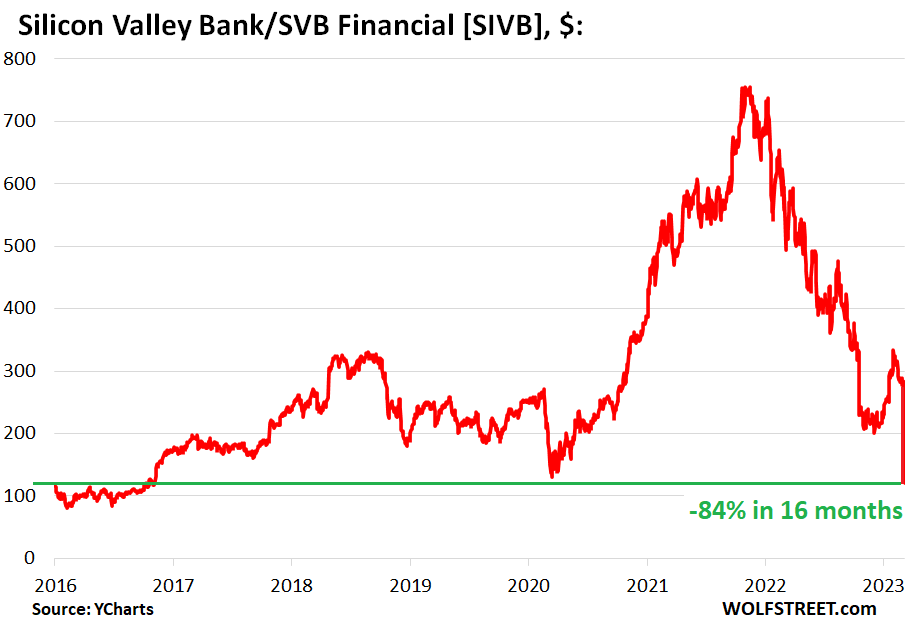

After having already plunged 65% in a series of breath-taking dives, and dead-cat bounces from their startup-and-crypto consensual-hallucination peak in November 2021, shares of SVB Financial [SIVB] kathoomphed so far today another 55%, to around $119 at the moment, the lowest since 2016, and are now down 84% from the November 2021 high, thereby getting inducted into my pantheon of Imploded Stocks. [Update: SIVB closed at $106, -60%; now trading at $85 afterhours, -69% in total for the day; updated chart in the comments. This is just stunning].

The 84% plunge from the high already exceeds SVB’s Dotcom Bust plunge of 77% from September 2000 through October 2002 (my discussion in July of this SVB phenomenon) The Dotcom Bust was a horrible creature for Silicon Valley, and SVB Financial is another indication that this current bust – we still have to come up with an appropriate name – promises to outdo the Dotcom Bust.

Silicon Valley Bank is heavily involved with all aspects of the startup scene. And the startup scene – across all sectors, from biotech to crypto, and across all stages, from early-stage outfits to companies that already went public – is getting the rug pulled out from under it by the collapse of consensual hallucination.

It had to happen some day anyway. It always does sooner or later. But now the end of easy money, after years of central-bank money printing and interest rate repression, is getting blamed, including by SVB Financial.

Get more equity capital.

SVB said in a series of filings with the SEC late yesterday and today that it would raise $2.25 billion in equity capital in a three-pronged approach that is heavily dilutive for existing stockholders:

- A public stock offering of $1.25 billion of common shares;

- A private sale of $500 million of “depositary shares” to General Atlantic, a growth equity firm, which happens to be a “longstanding client of SVB”;

- And the sale of $500 million of mandatory convertible preferred shares.

Get lots of liquidity.

SVB said that it was “repositioning” its balance sheet by having sold all of its $21 billion in available-for-sale securities, and that it booked a staggering loss of $1.8 billion on those sales in Q1 – so Q1 earnings are going to be a massive loss.

It said that it would place the proceeds in short-term securities and on deposit at the Fed to earn the higher short-term rates and improve its liquidity.

In addition, “to further strengthen balance sheet liquidity,” it said it would double its “term borrowings from $15 billion to $30 billion and hedge these borrowings to mitigate higher funding costs in the future.”

Preparing for the mass extinction event among startups.

“We are taking these actions because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients as they invest in their businesses,” SVB said in one of the filings with the SEC today.

“We expect these actions to better support earnings in a higher-for-longer rate environment, providing the flexibility to support our business, including funding loans, while delivering improved returns for shareholders,” it said.

So this is in preparation for what it sees will come its way in the startup scene after the free-money era ended.

When consensual hallucination collapsed, the IPO and SPAC bubbles collapsed and closed the exit doors for VC investors, so they stopped funding many of these companies. And suddenly, these companies have to survive with what they’ve got, but they’re burning cash like there’s no tomorrow, and they cannot cut costs fast enough, and they cannot get new funding – neither the still private companies from private investors, nor the already publicly traded companies via stock offerings.

“Mass extinction event” is now the term used by the VC community to describe what will happen to the vast majority of startups when they run out of money.

Many of these startups and their founders are clients of SVB across its divisions:

- Silicon Valley Bank: deposit outflow as startups burn cash until it’s gone and they shut down. And some loans may go bad.

- SVB Securities, the investment banking division.

- SVB Capital, the venture capital division.

- SVB Private, the private banking and wealth management division to cater to the (erstwhile?) multi-millionaire or billionaire founders.

All of them have fallen off Cloud 9 in a spectacular manner. And SVB is doing what it can to remain relevant.

Moody’s downgraded SVB Financial and Silicon Valley Bank by one notch, from A-3 to Baa1. Moody’s report said that this “reflects the deterioration in the bank’s funding, liquidity and profitability, which prompted SVB to announce actions to restructure its balance sheet.”

Moody’s also downgraded the rating outlook from “stable” to “negative,” meaning another downgrade might be next, “reflecting the uncertain macroenvironment and specifically, the potential negative implications for SVB if the declining venture capital investment activity and high cash burn does not subside.”

OK, folks, we need to find an evocative name for this bust, a name that will make it into the annals of history, as did “Dotcom Bust.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

VC Firepit? When I look at all those hundreds of billions I wonder where they come from. Granny’s savings, borrowed from somewhere, rolls of Benjamins from Vegas?

dotgone

Silly-Con Bust

fold@Si

(fold dat Silly-Con)

Siv@fold

(Silicon Valley suicide)

SiO2much

Vinegar stroke…aussie slang

Just give it another year or so (for real estate to catch up) and we can call it the Everything Bust.

Fitting ending for the Everything Bubble but “Everything Bust” is a little tiring

How about the wet-dream draught?

“Where did the dumb, doomed VC money come from”

CALPERS, CALSTERS, and really you, dear taxpayer-guarantor of grossly inflated public employee pension funds.

Hi Wolf,

How about “FreeMoney.gone”?

Love your articles!

I am not smart enough to buy stock in a bank. Seems like they can surprise you with bad loans at any time, especially when the expansion cycle ends.

You really, really don’t ever want to wake up to something like this in your portfolio.

I would never be able to sleep again with something like this in my portfolio.

I learned to sleep again after the Dotcom bust 😎

MetaBust

I like MetaBust, catchy & befitting.

The Everything Bust

The Artificial Investment (AI).

Flat tire era??

How about “End of an Error”or Disruptor Combustor.

Startup Bust

(longer version: Startup shutdown bust)

DumbCom Bust

(Those who refuse to learn from history are doomed to repeat it.)

For Chrissakes…*South Park’s* “Underpants Gnomes” episode (on the insanity of having a business plan with no real/realistic revenue model) came out over 20 years ago.

A friggin cartoon had these worthies figured out over a decade before DoomBoom 2.0.

So, circa 2014-2015 a bunch of self-proclaimed SV geniuses (riding ZIRP like a…merry-go-round, ahem) say, “Screw it!! Lets do it again!!”

Gotta like “Artificial Investment”…extra points for skewering *newest* revenue mystery machine that’s gonna save us all!!

I know a lot of people complain about the big banks, but they are good investments: they pay dividends, and if they die, then you are probably next.

Although most people are probably better off in banking ETFs.

Silicon Valley Bank and Silvergate are tied to a particular industry and/or region, so that is a red flag. Being tied to a questionable industry is a bigger red flag.

We might as well call this Dotcom Bust II. Once again, Silicon Valley propped up companies that were not making any profit, they told the rest of us that we just didn’t understand how the world works, and it turns out they were wrong. Again.

“big banks…are good investments: they pay dividends, and if they die, then you are probably next.”

I’m putting this quote at the top of my investing spreadsheet – and maybe on a shirt!

“if they die…”

So, by all means, because thinking hard is…hard, let’s lay back, spread ’em, and think of the fate of the Pound Sterling (invulnerable guarantor of the Empire That Could Never Die…).

More briefly, “The US economy is hopeless sh*t, so embrace the sh*t”

Golly, I wonder what kinda thinking led us *here*…

I’d like to see what’s really on their balance sheets, outside of what everyone presumably already knows.

Their health is still ultimately tied to the asset mania which is going to implode. It just hasn’t happened, yet. Recently, I read that BAC has something like $100B in unrealized losses on their MBS portfolio. It’s not enough alone to sink the bank but there is a lot more where that came from in the future.

Just wait until the garbage on all these bank balance sheets (supposedly sound loans) shows its real credit quality and interest rates “blow out” later.

real estate values have not plunged quickly and there is plenty of denial in that area. there will be much bigger losses in many of these areas.

Is this CMBS (Commercial) or MBS (Residential). I thought almost all residentials are guaranteed by the GSEs.

If a residential unit is bought as an investment then it is a commercial loan.

I am not a sophisticated investor and I don’t doubt your reasoning.

My interpretation of EF’s post is that BOA, Citi, and especially JPM are the backbone of the USA’s economy – and the source of it’s power. It would not surprise me at if their large vaults contain vacuum. : ) As long at the vault doors are closed the finanicalization game continues and the world turns.

It’s not the type of securities they have on the balance sheet that’s the problem (they’re mostly government guaranteed), but that they bought them at much lower yields some time ago, and now yields have jumped and prices of those securities have fallen, and if they have to sell them now, rather than holding them to maturity, they’ll have a big loss on them.

If they hold them to maturity, there won’t be a loss. But they are now FORCED to sell them for liquidity. And that’s a problem.

Usual wisdom from AF.

A decent reporter (any left at MSM lapdogs?) would ask about close details of this year’s bank stress tests/living wills.

“I know a lot of people complain about the big banks, but they are good investments: they pay dividends, and if they die, then you are probably next.”

Wow – do you actually believe that?

What are your thoughts on the big EU banks at the moment – such as DB or CS, for example? Do these strike you as “good investments”? In fact, why do you suppose that all of the EU majors have stock prices so low that it’s impossible to write puts on them that make any sense?

How did those dividends work out for Lehman or Bear shareholders 15 years ago? Did dividends make up for Citi’s share price collapse or would capital have been better deployed elsewhere? Those are just the hugest & bigliest banks: Wachovia? WaMu? Northen Rock? or any of the huge-but-now-gone banks that dissappeared in 2009… My favorite “good investment” of all time might possibly be Barings Bank which made it to 230 years old before it wiped out everyone that had touched it…

If you really want dividends why not invest in a company that pays them that’s actually understandable – such as a utility or a food company? Huge banks are completely opaque with deeply nebulous risk management and tend to be run and manned by the most unscrupulous idiots in the universe. The fact that they have to be levered 30x just to make their earnings seem vaguely reasonable should be enough for anyone with any common sense to simply walk the other direction.

I don’t comment on WS much, but this statement is one that I’m surprised no one else had a visceral opinion on..

Oh, and as for naming the new dotcom bust (I always personally liked “dot.crash” better)…

“The Great Recession” wasn’t a very original name, and wasn’t very descriptive, I think most people remember it moreso as the Housing Crash/Bust.

I predict that the next go-around will be similarly uninspiring*: “Great Depression 2 (or 2.0),” History may name it something else with the full benefit of hindsight, especially if no one alive today lives to see the end of it. After all, if living standards fall for the rest of everyones’ lives, when does the downturn actually end?

Perhaps “the Final Unwind” or some such will be an appropriate name, if that’s the case.

Call me a pessimist, but there’s a non-zero probability of the above. I wouldn’t even put it in “fat tail” category, but we’ll see. I also do not think that this outcome is investable really, although mitigating harm is a worthwhile endeavor.

*note: society cannot even innovate the names of generations which went from “Great,” “Silent,” “Boomers” etc, to utterly undescriptive names like X, Y, Z – although it occurred to someone that the passing of the millenium was special so “Y” turned into “Millenials” so at least we’re 1 for 3. We’re on about our 600th Superhero/Batman/Xman/SuperDuperMan whatever movie at this point. It might seem trite to complain about this, but the fact that our culture is so sclerosed and has narrowed so significantly does not give me great hope for the future (or managing to adequately address the challenges at hand).

“Wow – do you actually believe that?”

I do – because, per my post above, these banks are necessary.

No Bad Cake,

Being necessary and being a good investment are very different things. Big banks have managed to blow themselves up at an alarming rate. Will the government always bail them out? Citigroup is still down over 90% from its 2006 highs. So is the 4.2% dividend it currently pays a high return or picking up nickels in front of a steam roller? We’ll eventually find out…

rojogrande,

“Big banks have managed to blow themselves up at an alarming rate.”

I hear ya and don’t disagree but what has been left standing after the 2008 debacle I believe to be “necessary” and therefore a relatively safe investment. To further my metaphor, the world’s largest army stands in front of those closed vault doors. Granted, the Spanish Armada was impressive as well. : ) Lastly, until we are reduced to bartering farm animals and the like these remaining big banks will be standing. They are the gambling houses, imo, that always w..

You tell ’em, Will.

The “if banks die” comment is little more than lazy investment nihilism…exactly the kind of thinking that *creates* Disaster 1.0, Disaster 2.0, Disaster 3.0…

Nothing is necessary or too big to fail! We didn’t learn that lesson the last time through!

I only invest in companies that have been increasing their dividends for 25 years. Granted, it’s not a guarantee, but there are no guarantees in investing.

WRT Bear Stearns or Lehman Brothers: I do not think either of them met the threshold of increasing dividends for 25 years when they went under.

The problem with giving specific counter-examples is you are assuming I gave you all my criteria.

Seriously, if I had a dollar every time someone though Bear or Lehman was a counter-example to anything I say, I could retire.

cas127: ‘“if banks die” comment is little more than lazy investment nihilism’

Everyday Freethought: “you are assuming I gave you all my criteria”

—–

Big banks is ONE stable component for diversification for the reasons given (and not given). To say it was “lazy” or “nihili[stic]” is a misrepresentation. cas127, Shame! : )

WiM – recall the period of ’07-9 usually being referred to in the comments as ‘the GFC’ (Great Financial Crisis). Would suggest bringing it to present day, changing the first letter to ,’O’ (as in ‘ongoing’).

may we all find a better day.

It’s safe enough with proper timing, just need to do some research.

Find what they call “systemically important” banks, then make up a small portfolio of them, and begin tracking the news and the stock prices of it.

At some point, inevitably, a fresh tranche of bad lending, or even better, money laundering will be revealed on someone and their stock tanks.

Wait a while, maybe for the legal proceedings to draw nearer to a summary conclusion, scary numbers will be thrown about as part of the negotiation of a settlement, and the stock price will settle, about at a PE below 5.

Then start buying stock with confidence, because the scandal will be soon be forgotten once the settlement amount is finalised. Then the stock will go up, easily yielding 100% or More.

Sell when it flattens out – usually around PE 10-15 (banks are boring).

It’s a slow strategy , but, it works. I like Danske Bank and Swedbank very much, they paid for many vacations. My tax kroner at work, as they say.

The Great Elation Deflation

The Grand Con

CrEptomanical headbangers ball hangover or maybe just CreptoBang!

Left an “a” out…CrEptomaniaCal (emphasize that Cal).

Final Fed fecal dump

Fed-pocalypse.

ZIRP-CON B.

Great (Bubble) Bust

The Bust for Dummies

Fiat Bust

Cheap Money Bust

QE Bust

All Bubbles Bust

I vote for the QE Bust!

Or maybe the Bernake Bust!

Zimbabwe Ben Bernanke’s Big Blow Off Top.

The Great Money Printing Bust

Cypto is in the Cypt

The great Unicorn extinction event.

The meteors name was Putin ;)

Cristy, I think those four get to the crux of the matter, especially the last one.

I see this as becoming:

All bubble bust

Fiat bust

Central bank bust

Brainwashing bust

All powerful government bust

Military hegemony bust

And, most importantly:

Cabal bust

Imagine having all of your money in SPACS, NFTs and crypto. Bahahahahaha!!! Suckers.

Not exactly ……

Growth looking muted at best for business in just about every sector. Real GDP could struggle the next few years. I’m afraid with elevated inflation we are simply out of monetary options and must innovate and produce our way out of this.

Not going to happen

There is no “deus ex machina” to get the country or world economy out of this mess. The end of the road will be evident when changing psychology turns credit conditions noticeably tighter, probably with future higher interest rates but even without it.

The majority of Americans are destined to become poorer or a lot poorer over the indefinite future.

I agree with your comment, so long as stocks, RE, and other assets are overvalued.

On the other hand, if all asset values dropped by 70%, think how productive the world would be. Rent seekers would have to pursue active occupations to make money. People who “retired” would be back in the work force quickly. The workforce would enlarge. People could invest in assets with a reasonable expectation of profit. There would be a more level playing field and greater opportunities for all.

We need that reset.

People won’t work hard and be productive if the Fed allows them to make quick money via speculation, scams, government largesse, and rent-seeking.

I say we just call it what it is. The Fed Bust.

Fedbust it is.

SvB isn’t/wasn’t even a crypto player, financier, nor supporter.

What they are/were, is an organization quite tightly coupled with the businesses that stupid speculation gravitate toward.

Fed busted bust busted, even.

The Cryptocalypse.

+1

The bank indicated they had minimal exposure to crypto

Need a broader name for this burst

And yet we will be told by the crypto bros that bitcoin fixes all this. LMAO!

Cryptosis was my thought, but I like Stegelberg’s suggestion, perhaps adding a “the” to make it an official moniker; “The Great Depression”, “The DotCom Bust”, and now “The Cryptocalypse”.

@Stegelberg

“Cryptocalypse Now”

:-)

Easy-money Bust, or maybe Psychedelic Bust?

The Cash Burn Crash. Because all most of them have ever done is burn cash.

What we are seeing is, “Franken-Bankin’ Tankin’.”

The International ZIRP Bust

Zirqphi

Looking at my Fidelity screener and looks like in just one day the banking sector has lost $275B in market value since the Silicon Valley Bank announcement. This is $95B more than the entire value of Ethereum (which folks on this board consider risky, LOL)!

You are bad at numbers

There are more dollars in the non-crypto side than crypto.

Larry McDonald, the author of the book “A Colossal failure of common sense” which I read, about the meltdown in Lehman Brothers in 2008, just predicted a 20% to 30% crash in the stock market in the next 60 days. He has a pretty good track record.

Defintely something a brewin, It could finally start getting interesting. Those black swans disguise themselves well as angels when the money’s loose.

Just another billionaire buying opportunity.

Capitalism continues to consolidate.

But, but … one of IBD’s darlings now turned to trash?

Good job Wolf. I think you called out SVB in some form or manner in the past.

Yes, thanks for remembering the good old days:

July 2022:

https://wolfstreet.com/2022/07/22/the-silicon-valley-startup-and-venture-capital-barometer-plunges-silicon-valley-bank-svb-financial-today-v-dotcom-bust/

November 2022:

https://wolfstreet.com/2022/11/16/wheres-the-contagion-from-the-crypto-implosion/

Your intellect is astonishing Wolf, Not sure where you get your energy and time to assemble these nuggets of wisdom but I and am sure many others really appreciate. Maybe someday you will share where you got somewhat of a start from? What and who influenced you is what I am saying. Anyway, thanks I really enjoy everything you put out.

I would guess it is just from a lifetime of hard work studying economics and finance, and also learning from history, and from his own mistakes or those of others.

Wolf,

Thank you for all your hard work and insight

Kudos, anyone who listened and acted accordingly was ready for this

Definitely worth a victory lap, that is for sure. I think if all readers shared 10% of the money they saved/made by reading this site with you, you’d be a rich(er) man…

“The Dotcom Bust was a horrible creature for Silicon Valley”

Sillicon Valley seems to be a sort of creature itself, some would call it horrible too

I don’t think it’s Silicon Valley itself, per se, it’s that investors seem to be incapable of properly valuating technology.

Prepare for the AI bubble that’s already inflating and we haven’t even named the current bubble.

As a famous playwright once said: all that glitters is no gold.

There’s some cryptohead named Jeffrey Berns who has been buying up banks and Lake Tahoe properties and all sorts of stuff. I keep expecting to hear something similar about that guy.

You might be on to something here. Reaching dizzying altitudes higher than the Cartwright Ranch. Holding more empty air space than Hoss’ ten gallon hat. Deeper sh*t than the snows around Donner Pass. Now going colder than the waters around a sunken steamer at the bottom of the lake. It’s the Ponderosa Plunge. Of course, there could always be a Rocky Mountain Rally or two before the real Ponderosa Plummet sets in.

> A private sale of $500 million of “depositary shares” to … a growth equity firm, which happens to be a “longstanding client of SVB” …

Spooky, maybe? I don;’t know details, but might this be vaguely like some of the daisy chains of financially-linked firms that went down in concert in the Crypto Crash? Like, maybe these firms mutually need each other to stay afloat? And if the market value of some of their magic beans goes down, the whole deal is suddenly wobbly? I’m sure there are some chains of dominos out there, if not here.

Yes. As in if you don’t buy my equity I am taking you down with me.

Crypto-centric journalism is still operating, and industry lobbyists are still chatting up members of Congress. To listen to some of these folks, it is as if the Crypto winter never happened. Talk about plastering a smily face sticker on a disaster.

The ” App Crash “

Definitely the App Bubble. All these companies HAD to have an app and any moron who could throw one together got a few billion dollars and it turns out bad ideas aren’t worth billions.

Like when Woolworths became Woolworths.Com and shares rocketed.

Or The ” App For That Crash “

The CrApp Dash.

Instacrash lol

Nice!!!

I sure hope this isn’t another “Lehman Brothers Moment” where one failure spreads to the entire financial system.

Looks like about 91 billion in MBS.

There are presently millions of failures sloshing around the global financial systems which are in worse shape than they’ve ever been. Just let them go bad and fail and then move on.

“OK, folks, we need to find an evocative name for this bust, a name that will make it into the annals of history, as did “Dotcom Bust.””

“The Great FED Fuc*up”

“Powell’s Pilfering”

“Jerome’s Jetfuel Inferno”

“The BrrrrrBOOM”

“QEInsanity”

“QEMisery”

“Jerry’s Dysentery”

Or, simply, “Quantitative Seizing.”

I like this one, it has a nice sound to it.

“The Show-off Blow-off”

“The ZIRP Burp”

“The Sheep Reap”

“The Rate Yikes”

Benanke and Yellen had a big hand in this too.

Silly Valley RE is going to end up a smoking crater

Covid Bust

Post Pandemic Bust

The empty trough

Investor’s loop collapse

Credit Suisse isn’t the only Primary Dealer with liquidity problems and when push comes to shove solvency problem. Treasury pumping out trillions in underwater debt, that they couldn’t offload to some sucker pension fund, that sit on primary dealers balance sheets. Falling domino time coming soon to a bank near you.

There has been lots of leverage and reckless lending in the last two years, especially to unicorns and startups. No risk was seen as long as stocks would go up and everyone was convinced interest rates would never rise.

There are three possibilities now facing the Republic:

1. The Fed stays the course and crash the asset and housing markets, but will save the economy in the long run by removing the financial excess and speculation.

2. The Fed reverses and starts QE and ZIRP, and it will destroy the currency and eventually crash the economy even after juicing the markets a little.

3. Tax payers will be once again asked to bail out the failed institutions, but then many tax payers will see no incentive to work or will not have any money left over, and the economy will crash as a result.

I vote they pick number3 ,it’s all the Roth Childs want

It’s always the taxpayers, always.

Think 1 or 3 are most likely, but in any case it will likely open the door to someone in power (or someone coming into power) who will politically weaponize the situation to our further detriment. When things are bad, people want someone to blame, and with the state of the US right now… I just fear much worse things could be waiting around the corner.

Fools Bust

Steven, this might stick as I was also about to post this, (so there must be others). Wolf?

I think some day I’m going to post all of them. They’re funny. One of them might stick.

But Dotcom Bust is hard to beat. It followed the beloved Dotcom Bubble. That was great one too. But there is still no agreement on how to spell them.

I vote for Silicon slide

The Appocalypse

Okay:

Stimmiegate

Spac Out from

Definition of ‘spark out’

1. to render unconscious. adjective, adverb. 2. completely unconscious.

The Crypto Crapout

Ping-Pong, it’s a Crypto Bomb?

So much, so fast

Whizzing numbers like digital craps

Back and forth ’till the whole thing snaps

‐Cash‐

Tech on blast

delusions en masse

Assets in the gutter ’cause they paid with trash

(PS-I’m a snake…ya know I can’t rap)

I’ll nominate:

Stimmie Slump

ZIRP Failure

Covid Cash Hangover

ZIRP Finale

Stimmie Slam

Zirp-Spac Era

Alright, I got to join in, how about:

MMT sucker punch

SPAC busted

SPAC KO

Crypto clobbering

IPO thwack

QE thrashing

MMT bust.

Could stand for Modern Monetary Theory bust or Monopoly Money Trust bust. I prefer the former to finally put that bufoonery in the ground and shame any economist in perpetuity that invokes or even alludes to it as being viable.

Think of the absurdity of MMT, and the end game.

First to the absurdity…..spend and borrow, but when inflation hits, TAXATION (the MMT answer) is the remedy to tamper down that inflation. So, people and businesses, strapped and punished by inflation would then be FURTHER PUNISHED by higher taxes.

The end game…..the inevitable inflation from the “borrowing and spending” and the then TAXATION “remedy” to tamp down that inflation would draw money and capital from the private sector and deposit it with the Government that is spending recklessly. Government bigger, private sector smaller. Round and round we go….for a while.

Yes. We’ve forgotten that MMT was the theory behind most of this crap. MMT economists like Bill Black and Stephanie Kelton moved into government and “justified” the free counterfeit.

had a little pstd memory – had a large position in a biotech – dendreon-had a massive profit in it and eventually had a large loss – learned an expensive lesson

Can Wolf enlighten us on why there was no dip-buying today in the stock market? They have been extremely resilient for the past year. Every dip, even the intraday ones, was bought, which caused a collapse in Vix. I guess they have run out of money?

I’ve posted on another thread, In the preceding, few days was a 4-sigma pump on social media. Do the big boys rush for the exit?

There was a lot. In fact, every singly buyer and all buyers were dip buyers.

Every single share that was sold today was bought by someone who thought that the price was a good deal and that it would bounce off. That’s what makes a market.

There just weren’t enough of them to outbid each other and step all over each other and overpower each other with higher prices. That’s the thing that didn’t happen.

There was a bit of a bounce (really a stop to the bleeding) around 3-4pm today. Likely a bit of dip buying, we’ll see how badly they get shredded tomorrow.

“why there was no dip-buying today”

technical breakdown of the markets.

Someone superglued Cathie Wood’s hands to her desk so she couldnt buy any.

Banks massacre day. SPX to form a RS of a H&S, or to reach/breach Aug high.

The Ellie Bust.

(That’s actually E.L.E. or Extinction Level Event.)

Check the excellent disaster movie “Deep Impact” for what it involves.

“Digital Depression” or “The Big Pop”

Wasn’t that last one the name of a 1970’s Pussycat Theaters feature flick about a guy named Dirk Vader who fathers a slew of pizza delivery boys on a desert plant long, long ago in the back seat of a Galaxie 500 far, far away?

Hey….I saw that movie. It was a great flick….

Digital depression could be what follows, right? I like that one. Although I also think it’s an apt term for many of our states of mind after accidentally spending endless hours online.

“It said that it would place the proceeds in short-term securities and on deposit at the Fed to earn the higher short-term rates and improve its liquidity.”

Uhh, customers should do the same. It is simple enough. Why bother dealing with a bank teetering on the brink of default.

How many of the “tech savvy”, generation ___(what letter are we on now?) have a great deal of their wealth in cryptos?

Bitcoin down nearly 10% today.

Now, add in any real estate ownership…..

An entire generation only saw UP in assets, crypto, etc. for years, thanks to Fed manipulated reality.

No savings, and plowed into ephemeral “asset” classes.

Lots of good comments about what to call this financial mess, and I have seen this movie before in 2000 and 2008, and wonder what the ripple effect will be, — obviously there will be more fallouts, and from all that I read which is tons of financial articles, a 20-30% drop will happen in 2023, — maybe more.

I like what one poster called it “DotCom Crash II” or maybe call it

“DotCom Crash Part2”

My idea for it to be called:

“The Bubble of Everything Crash” – I believe Wolf had this as a topic.

Wolf you should be very proud of calling out all these BS bubbles of CryptoTrash, Housing Prices, Autos, NFT, Meme Stocks, WallStreetMoronBets group on Reddit, etc, and especially the stupidity and antics, and dereliction of duty by the Fed falling asleep at the wheel for so many years.

This will all end very badly, and just yesterday Blackrock said Treasuries and gold are good ideas to be invested in, and I agree.

SVB Financial is at $85 after hours. That makes for a 69% cliff-dive in one day, and -89% since the November 2021 high.

Here is the updated chart as of afterhours trading. This is just stunning:

Thanks for tuning in to the Broku Channel. You’re enjoying Pelvis Wresley leading the daily diving competition in Fun In Spacapulco.

@BuySome – please explain Broku Channel

It’s like Roku, only you get to choose from shows about everything headed toward bust. I’ll let Wolf claim the copyright on that name.

Very clever!

Now at $79 and still going….

Trash Crash.

BKX monthly made a rd trip to July 1998 buying climax.

BKX is the banks index.

I think we should lay the blame where it lies – at the foot of the Fed Reserve with its hallucination-inducing ZIRP and easy money policies.

It should really be called FedBust.

How about: HoE Down (Hallucination of Everything Downfall).

pivotaloosa. Cause you know it’s coming

How about “East Bound and Down” (or the “EBAD Era”)? Hope that brought a grin to your face.

or southbound! lol

1) WFC monthly Lazer : Mar 1998 buying climax to Aug 2006 highs // parallel from : Sept 1998.

2) In Sept 2008 WFC popped > the Lazer but closed inside. That failure led to the Mar 2009 plunge.

3) WFC misbehavior infect BRK/B.

4) Since Dec 2018 WFC struggled to stay inside, but in Jan 2020 WFC lost

it’s grip and plunged to Oct 2005 backbone.

5) In Feb 2022 WFC reached/ breached the Lazer, but it’s first attempt

failed.

6) WFC might try it again in a sling shot when consumers will get used to

higher rates.

7) WFC pays 2.80% dividends, but charge between : 20% and 30% c/c

rates.

8) WFC passed the Fed banking test.

But, i noticed WFC was offering amongst the highest CD rates starting back in May/June. It seemed they were trolling for cash with the high CD rates, which made me wonder how bad it is…

It will be called something like “The Great Banking Collapse.” It was clear when last year Central Banks (including our Fed) sent billions to the Swiss National Bank, in what I see as an effort to bail out Credit Suisse. It was just the start. Now we see SVB teetering. Deutsche Bank and Wells Fargo look shaky and may be next. Maybe they are too big to fail, but Credit Suisse ($1.6 trillion) and Lehman ($600 billion in 2008 dollars) were not small.

Great Recession Part2

Great Recession II

Great Recession II – Electric Boogaloo

The “Disruptive” bust

Tech Trash Tumble…

“Welcome to the Grand illusion

Come on in and see what’s happening

Pay the price (no Bitcoin please), get your tickets for the show!”

Forty-six years later and I still love that song. The illusion is orders of magnitudes greater than it was then.

“A public stock offering of $1.25 billion of common shares”

LOL, do I smell some good opportunity for those FOMO retail dip buyers to jump right in? At this stage if you’re stupid enough to buy, perhaps you enjoy getting shot in the eyes…

So long sweetheart. It’s time to go.

We stole all your resources a longtime ago.

HTGC down 9%.

The Great Inversion.

SVB is doing what it can to remain solvent – “relevancy” is a luxury it cannot afford.

Would not be surprised if there is more bad news to come….

Why not something simple. The Central (Bank) Ponzi Bubble. or maybe we turn it around as Ponzi Central.

Can we start using Powell as a verb. Like, “you really Powell’d that up, didnt you”?

Or we put together Powell and Ponzi and make it Powzi.

A badly missed play in any sporting contest can become a Powell-up.

Wasnt everyone asking for their next Stimmie payment, like junkies?

The Stim Gimme Bubble.

Zombie Apocalypse

Boomer Bust

Free Money Meltdown

Everything Bubble

The Greater Depression.*

*We’ll do worse sometime in the future.

In after hours trading SVB is down to $78 a share after closing at $106.

“The Big Dump”

Trust Bust

Easy Money Massacre

The Great Pump ‘N Dump

Tech Wreck

Housing Hullabaloo Pt 2

QE Jamboree

Moneybomb

Interested to hear from the community and Wolf about the potential risk for a contagion of this SVB bust (potentially a Chapter 11 here), to the rest of the financial sector and/or economy?

Feducini Albusto

MMB

BitCON and all craptocurrencies have decided to start swan-diving. BitCON has now breached the $20k psychological barrier on its way to zero.

Modern Monetary Terror.

We should stop trying to use words to describe the coming economapocalypse. Since we now live in a world that’s a hybrid of “Idiocracy” and “Dumb and Dumber” the label for this crash should be a string of sad face, vomit, poop emojis.

Taken from another blog:

The dildo of consequences

some hedge fund(s) got their face(s) ripped off today … the price of money just got real expensive. rolling over low cost debt to higher cost debt is never fun.

thank you Wolf! love the term ‘mass extinction event’.

Wolf you should have a contest. Everyone gets two entrees for naming this thing. Number them and have people post their vote in replies by number and Winner gets a free mug.

Blood bath bust

Crypto spacs and beyond bust

Everything and the kitchen sink bust

High as a kite bust

It’s different this time bust

Hallucination inflation bust

Powell pow bust

What goes up must come down bust

The SPAC Splat

The Great DeFaanging?

“we still have to come up with an appropriate name”

Given the excesses and mark-to-fantasy rules in place since Mar 2009 (that the banks may well need soon), here we go

“The greatest bust since the great depression”

“The greatest bust of the century”

“The magnificent bust”

“The stock market train wreck of the century”

Pick your poison. Can we poison the Nobel Laureate without getting jail term?

with a hat tip to Mardok:

CryptoTrash Crash

I posted the following snip Feb 17 in a comment section here. There’s a tsunami of problems ahead with banks and every leveraged entity around the globe. As I’ve said for many months, cash is going to become very scarce and precious. Let the buyers beware!!!!!

FEDERAL RESERVE BANK OF KANSAS CITY

September 08, 2022

“The rising interest rate environment has led to unrealized loss positions in community bank* available-for-sale securities portfolios and declining tangible equity capital ratios

At year-end 2021, only 4 community banks had tangible equity capital ratios below 5 percent; that number increased to 333 at June 30, 2022, indicating less ability to sustain economic shocks“

“$21 billion in available-for-sale securities” out of $210 billion of assets. What is the remaining $189 billion?

Cash, cash on deposit at the Fed, loans (mortgages, etc.), probably some real estate and other assets, plus a lot of securities that are “held-to-maturity bonds” and are not held for sale, meaning it has no intention of selling them. And these not-for-sale securities have not been marked to market at all, thus involving bigger losses if it has to sell them.

Thanks. It seems really strange, how come that a small bank with only 6 offices can control $210B? Even worst being the “16th largest bank in the US” Either something is wrong with this picture or something is wrong with our country. Is this bank being used as what charity companies call “black holes” meaning “charity” money goes in from the upper 0.01% of our society as tax deductible contribution but none ever saw money coming out and given to those who are in need?

There is no mystery and no secret. Silicon Valley Bank got a huge amount of cash from the startups that were being funded with huge amounts of cash everywhere during the Free Money era. About half of all startups in the US have accounts at Silicon Valley Bank (they have offices in the startup hot spots around the country). If a startup gets $300 million in funding, that cash goes straight to accounts at the bank – these are the “deposits.” And the bank had to do something with that cash from those deposits, so it bought securities and it put some of it on deposit at the Fed and extended loans, including to startups, etc. That’s how a bank grows. The Free-Money startup bubble just inflated the deposits at the bank into the stratosphere, and the bank bought securities with that cash, and now those securities have dropped in value, and the startups are withdrawing their cash because they’re burning it, and to come up with the cash for those withdrawals, the bank has to sell its securities, but is losing money on them.

All this was predictable to some extent. Free-money bubble mentality does this. To me it shows reckless bubble-minded bank management. Free money turns brains to mush, even the brains of bankers.

Well cry me an atmospheric river, it’s the crypto crackup coming to roost.

I’m confident, with this mass extinction cascading collapse, that every rating agency will once again be guilty of malfeasance and corruption, in a very long chain of exuberance to upgrade every entity they worked for.

The rating agencies are the gatekeepers for authorizing fraudulent accounting that overlooks leveraged portfolios that are filled with excessive exposure to risk.

Those agencies also will now be at the epicenter of cascading defaults which will be linked to a global inability to analyze risk exposure and this find realistic valuation.

That process was what made the CDS implosion so fun in the GFC — and once again, corrupt rating agencies will blame corruption at corporations who willing provided fraudulent earnings reports, covering up impairments.

Every idiot clown in this casino deserves exactly what’s happening to ftx, silvergate and all these ponzi companies, from alphabet to zoom, and definitely all the real estate investors in the Airbnb bubble.

Hopefully a shocking reset is underway…

Wolf: How many $$ in their held to maturity investment portfolio? How much unrealized loss there? If they had to sell those bonds, would the loss take the tangible book value of equity below zero?

If they have to sell part of their held-to-maturity bonds, that would not be good.

Losses on held to maturity bonds marked to par – from my reading, run at 800b+ system wide. If more banks have to liquidate them to raise capital, well, here we go again.

And the next shoe will be PE and their beanstalk in the sky valuations (of course we should all trust a thirty something with ten years of education and never experiencing a down market will know what to do?)

Mark to market can be brutal, but when it is suspended the fall can be a lot worse.

If Cramer says SBV has “a bullet proof balance sheet” I’m going to short the whole market.

Silvergate had a bullet-poof balance sheet too, mostly Treasury securities. The problem isn’t the type of securities, it’s that yields that have surged, causing all yield-assets to drop in price.

“The 84% plunge from the high already exceeds SVB’s Dotcom Bust plunge of 77% from September 2000 through October 2022”

I think the latter year should be 2002.

I can’t come up with any better names for this crash than posted above.

But I would suggest abandoning the Orwellian attempt to instill the use of “The Great Moderation”, as this period has very clearly had nothing to do with moderation. In its place, I humbly submit: “The long, strange trip”.

Chairman Powell’s Rate Leap Forward gives us this era of Quantitative Wheezing, culminating in The Omnibust and Great Disgorgement

Very funny and subversive, SnotFroth, you commie, you :-).

I love this creativity from the commentariat here.

But I’m going early on the next crash, circa 2032, driven by AI hype and hoopla:

The Bot Bom

The everything bubble is popping. But I don’t think the future will call this collapse something that ends in “bust”. I believe the Fed, being controlled by their master(s), knows exactly what they want to accomplish – the final reset. They know they have destroyed their fiat monetary system by their debt expansion theory reaching it’s end . Inflation without remedy now says so. I believe history will describe this event as the “great wealth transfer” as the world enters into a state of extreme hardship.

I’m not sure the whole world will share equally in the hardship….producer based economies with commodity backed currencies will fare better while “we” languish like Albania in the 50s (never been there, but it sounds good.)

This is America after all.

“The Super Bust”

we can even start numbering them with roman numerals.

Maybe this is

“Super Bust II”

I like this suggestion…

“Super Bust”

“Super Bust I”

“Super Bust II”

DotCon Bust.

California AND Bust

Mama’s and Papa’s sequel

(thought of this years ago):

“California Leavin”

Journey remake:

“Dont Stop Bleeding”

Blue Oyster Cult … such prescience:

“Burnin for You”

RagingVentures on twitter posted that SIVB has a huge mortgage bond problem:

“The bank basically increased its security portfolio by 700% at a generational TOP in the bond market, buying $88 b of mostly 10+ year mortgages with an average yield of just 1.63% at Sept 30th. Oops! 4/10”

Everyone holding bonds has the same problem. But the problem is smaller for 30-year MBS with 1.6% yield than for 30-year Treasuries with a 1.6% yield. Here is why:

ALL bonds that were issued during the low-yield era that still have long remaining maturities are under water. Government guaranteed MBS might be less under water than Treasuries with similar maturities because holders get the flow of pass-through principal payments at face value that reduces the amount of the MBS every month with no loss. So you get your money back in a monthly flow without having to sell the MBS. The average life of a 30-year mortgage in the US is about 7 years, which is when they get paid off via sale of the home or a refi! The principal is forwarded to the holder, which reduces the amount of the MBS. At some point, when the MBS has been whittled down far enough – maybe 7 years or so into the life of a 30-year MBS – the issuer will call the MBS at the remaining face value, at no loss to the holder. No one can ever hold 30-year MBS for 30 years because most of the mortgages in the pool will be paid off long before then, and there’s nearly nothing left in the pool, and the MBS will be called long before then. This is a big advantage of MBS during times of rising rates.

” The average life of a 30-year mortgage in the US is about 7 years”. Is that average calculated before most homeowners in the USA refi-ed, or got a purchase money mortgages, at or near 3%? I keep reading articles about how homeowners are not selling or refinancing because they have such a great rate on their current mortgage. Also, very little principal gets amortized away in the first seven years of a thirty year mortgage. These banks could be in a lot more trouble than is apparent on the surface.

This is the long-term average.

RagingVentures on twitter posted that SIVB has a huge mortgage bond problem:

“The bank basically increased its security portfolio by 700% at a generational TOP in the bond market, buying $88 b of mostly 10+ year mortgages with an average yield of just 1.63% at Sept 30th. Oops! 4/10”

Snippet from the Wall Street Journal opinion section called Nothing Redeems Crypto.

Do the benefits of crypto markets outweigh the cost of regulating them? No. But letting crypto burn wouldn’t be costless, either. The financial pretensions of crypto need to be actively dismantled. Contrary to what its marketing wizards tell us, crypto is neither money nor a vehicle for finance. It’s an elaborate simulation of finance that produces gains and losses.

Yet letting crypto burn would allow the most shameless actors to gamble on a quest for resurrection. The ease of spinning out new tokens makes an attempt to return to the tables irresistible. The disgraced author of the Terra/Luna debacle, which vaporized billions of dollars overnight in May 2022, immediately returned to the market with Terra 2.0. The disgraced founders of Three Arrows Capital, bankrupted in July 2022, now want to buy up crypto users’ bankruptcy claims, funded by—you guessed it—the proceeds of a new crypto token.

Hmmm.

Try re-reading the WSJ snippet, but this time substitute for the word “crypto.” Insert either “dollar” or “dollars” or “debt” instead.

Is not the dollar also a token?

You really cannot compare cryptos to Dollars.

There is transparency in the dollar. At least you know when and where the U.S. government is going to print dollars or take on debt.

Cryptos are not regulated. It is like investing in Bernie Madoffs old fund. Everything happens on the 17th floor which is run by a wizard behind a curtain and they can do whatever they want and they do not have to tell anybody what they are doing.

Was it Nixon who opened China to trade leading to the de-industrialization and financialization of the US?

Was it Nixon who took us off the gold standard leading to the current widespread abuse of fiat “currency”?

Might this be called the end of a long (and not always unpleasant) “Dicking”?

The FED’s GOAT Bust –

which followed the FED’s GOAT Bubble.

Crypto Inferno

How about Crypto Crash or Crypto Collapse?

Cute! I can hear the song in my mind!

How about the “Liquidity Plunge” as a name for this crash?

When monetary Viagra ran out.

Financial softening?

Noticed the SIVB provisions for credit losses went from $123k to $420k between 2021 and 2022. About 241% increase.

“……and elevated cash burn levels from our clients as they invest in their businesses,”

As you point out, their client’s cash burn now with little or free money in the cash pipe line, will see their clients winking out, one by one, like dying embers in the camp fire. Can’t see much up side in 2023 when it comes to reserves for credit losses. Reserves reserves and more reserves….ugh.

I might be late to the party, but I’m betting on “Free Money Bust” or something along those lines. Hopefully whatever sticks has “free money” included, so that future generations get a hint that it’s a terrible idea.

SVB is now a dead duck…oh well!

It’s FDIC FRYDAY once again, as fond memories of 2009 return!!!

Who to blame for the failure to require banks to engage in realistic mark to market of their assets daily? SEC and FDIC in 2009, it seems. Now we get the threat of an even larger “mass extinction event.”

The Free Candy Sugar Crash

In startups I have seen personally that got infusions of cash from finance backers, initially there were a LOT of parties with exotic food and booze, new cars and houses and furniture, bursts of newspaper articles touting how wonderful they were, then employees laid off, then I quit watching.

Great/spectacular work as always Wolf – thank you! :)

The name for this bust is obvious to me, and I’m very surprised nobody else has already suggested it (that I can see?)…

Perhaps you can take a lot of the credit for the name (?)…

A little bit irreverent – but perhaps that is appropriate: WTF Bust

LOL.

“Moody’s downgraded SVB Financial and Silicon Valley Bank by one notch.”

—————————————–

too little, too late

says something about Moody’s

Yes funny, isn’t it. Still investment-grade too, on the day of collapse, LOL.

But this went very fast.

It didn’t quite go to heck in a straight line, but it was pretty close there at the end…

The Scumbag FED Bust

That is the cause

not to worry, the bust will be blamed it on covid

Aaaand SVB is gone. FDIC seized it this morning.

Death Valley Bust or

Death Valley Disintermediation.

Silicon Implode

Silicon Faceplant

Honestly, this doesn’t worry me at all for the economy at large.

BEFORE COVID, available jobs had climbed to ridiculous heights. This (IMO), is about demographics. The ratio of new workers to retiring workers has been moving toward 1:1 for long, long time. But, 2010 is actually when we would’ve seen the impact of the Great Boomer Migration (out of the workforce) — except all that data was hidden under the Housing Bust Rubble.

So, we maintained the illusion of a decent new:leaving ratio for another decade, because it took so long to rehire the millions who get canned in 2009.

Go look at the monthly NFP numbers from 2019 to get a feel for what’s coming. The COVID recovery phase is all but over – (and we lost 2 full years of legal immigrant workers in there, too).

Nobody has a model for a recession where there are 2 jobs for everyone looking. Heck, we don’t have any models for that in a good economy, because it never happened, (far as we know).

Yeah, the tech sector will take a hit. But, it’s not like the need for tech will vanish. This is trimming at the margins of a much, much larger workforce. And, (so far), the big name layoffs haven’t touched the U3, because nobody has an easier job finding work in the modern age than college educated tech workers. (And remote work means moving is no longer mandatory). How many Silicon Valley workers will be working in Durham without having to move?

The fact Openings was 10 million BEFORE COVID tells me the Openings numbers are not a post-COVID spasm (like some of the other stuff). My view — until Openings drops to about 7 million, recession is nearly impossible, (as is getting inflation down to 2%). I think it may drop to 4% before it stalls, but we are not heading for the 70s again, nor the 2000s. It’s a whole new ballgame, and NOBODY knows the rules …. yet.

The aftermath will be the true Great Reset: gold-backed money, small, responsive government, death of Empire, etc.

Was SVB’s business model unique? Are there other banks as massively exposed to the private equity space as SVB?

I thought that post GFC regulations shored up bank balance sheets and prevented this kind of thing?

SVB had about half of all startups in the US. The other half was spread over all the other banks.