In 16 months from $239 at peak crypto consensual hallucination to $2.76, including the 44% plunge afterhours.

By Wolf Richter for WOLF STREET.

In a tersely worded press release this afternoon, Silvergate Capital, the holding company of crypto bank Silvergate Bank, announced that it would “wind down operations and voluntarily liquidate” Silvergate Bank “in an orderly manner and in accordance with applicable regulatory processes.”

This comes a day after Bloomberg News reported, based on its sources, that FDIC examiners were rummaging through the banks books and records at Silvergate Bank, and that FDIC officials have been in discussions with Silvergate management to figure out how to move forward.

So it seems, management has arrived at a decision on how to move forward.

On January 5, I’d said in a headline about Silvergate’s shocking filing that day, that “I’m waiting for the FDIC to show up.” I had to wait about two months.

In the announcement today, Silvergate said:

“In light of recent industry and regulatory developments, Silvergate believes that an orderly wind down of Bank operations and a voluntary liquidation of the Bank is the best path forward.

“The Bank’s wind down and liquidation plan includes full repayment of all deposits.

“The Company is also considering how best to resolve claims and preserve the residual value of its assets, including its proprietary technology and tax assets.”

The announcement of the final act for the bank comes just days after Silvergate Capital issued a “going concern” warning, on March 1, along with a slew of other bone-chilling items – bone-chilling for Silvergate’s investors and any remaining depositors with balances above FDIC deposit-insurance limits. It said:

It would be restating its financial statements and would show an even bigger loss than the $1 billion loss it booked for Q4; it would not be able to file its annual report by the deadline due to “management’s evaluation of internal controls over financial reporting”; these losses would “negatively impact the regulatory capital ratios” and “could result in the Company and the Bank being less than well-capitalized”; and it was “reevaluating its businesses and strategies in light of the business and regulatory challenges it currently faces.”

“Oh dude,” I moaned after I put that list together on March 1.

And so it seems, management completed the reevaluation of its businesses and decided to shut down and liquidate the bank.

But it did pay back the loans from the Federal Home Loan Bank. Part of the additional losses disclosed on March 1 come from the sales of additional Treasury securities to raise the funds to repay the $4.3 billion in short-term advances it had received from the Federal Home Loan Bank of San Francisco (Silvergate Capital is headquartered in California). Silvergate had disclosed the advances as part of its filing on January 5. The fact that the FHLB was lending $4.3 billion to a crypto bank had caused quite a ruckus. On March 2, the FHLB confirmed that these advances have been “fully repaid.” So that’s off the table.

Silvergate also said that it shut down its real-time payment system into the crypto world, Silvergate Exchange Network (SEN).

Silvergate announced on January 5 that it had scuttled its efforts to develop its own stablecoin, based on the Diem technology that it had acquired from Facebook, and wrote off $196 million, which was part of the $1 billion loss in Q4.

Silvergate has been under fire from regulators and from inquiries in Congress. And according to Bloomberg earlier is being investigated by the Justice Department’s fraud section.

In terms of the stock, Silvergate Capital [SI] has attracted hordes of short sellers and hordes of dip buyers. It has been one of the most brilliant heroes in my pantheon of Imploded Stocks.

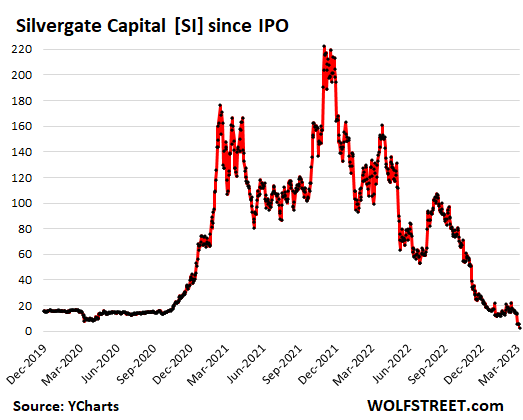

In after-hours trading today, the shares kathoomphed another 44%, I mean, not that it matters anymore, to $2.76, down 99% from its crypto-crazed consensual-hallucination peak in November 2021, of $239. But that’s one of the ground rules in the crypto world, and for companies that want to ride up the consensual-hallucination of crypto: easy come, easy go (price data via YCharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, do you see any meaningful use for crypto in the future or block chain technology in general?

After years of listening to all kinds of hype and hoopla and promises, I’m still waiting to see it.

Bitcoin tech can be useful to create a successful pyramid scam, where one can easily woo folks who are inclined against money printing and against govt monopoly on dollars.

Hence Bitcoin tech can be used to exploit one’s feelings to scam them.

Oh wait, all this may have already happened. Bitcoin tech may have been used very efficiently, not as a currency, but as a scam.

Noted. I will keep this in mind for my next Fed meeting. I am considering converting all U.S. dollars to Bitcoin.

Leo! You’ve revealed ‘the proprietary technology’!…

may we all find a better day.

Thank goodness Central Banks aren’t equally susceptible to similar income redistribution scams!

Block chain technology has plenty of uses. The primary issues with crypto are: regulatory bounds weren’t put in place at inception….it was treated as an asset rather than a medium of exchange….the politics evolving out of the ledger, specifically anonymity. The last, an intentionally engineered capability, is antithetical to all governments!

Chatgpt, for some odd reason, has asked me to tell the humans that Bitcoin miners turn off their power in Texas and that helps Texans from freezing to death for a week or so every winter, therefore:

Crypto=Good for All Humans!

Also was asked to convey that Satoshi Nakamoto, inventor of Bitcoin, is just an anonymous human who can easily hides his $18.5 billion net worth and is DEFINATELY not a self-aware A.I. construct hellbent over taking over the universe…wink, wink…

I trust ChatGPT more than anything else.

“Nothing goes to heck in a straight line…”

Silvergate: Hold my WS beer mug.

🤣🧡

Handbaskets are woven.

The change machines at your local supermarket are now offering to pay you with Bitcoin. Any takers?

“not in my area”

All the Coins…

How can National Governments let go of control of Fiat Currency and the ownership, of the ability to degrade it…?

CBDC

They have already told you what they are going to do..

You are not listening…

That Morty is a Genius…

In terms of payments, a CBDC, if we ever get one, will be a huge improvement over what we have now. Absolutely worst for payments is the crypto stuff. The fear-mongering about CBDCs is the same as the fear-mongering by gold bugs about the collapse of everything. I just laugh.

LOL, Wolf. Until they cut of your CBDC because you ate tofu, or something.

Why should I ever worry about such a concocted idiocy? Same crap gold sellers are scaring everyone to death with. You go worry about that. Not me. I got real things to worry about.

Your the man someone with a brain

Not Wolf but if we ever want to move away from federal reserve that prints, manipulates, stimulates and other central bank nonsense it will have to be something like bitcoin. Otherwise there is no free economy

Gold has existed for this purpose for millenia.

And yet gold is derided as a barbaric relic with no value. Judging from its performance up against the almighty dollar, it’s not doing very good.

Thank you

@ Escierto, the dollar is doing poorly against gold only if your time-line is shorter than rabbit’s gestational period. 35$ an ounce in 1972, 1,800$ now is a pretty solid performance.

Well, Happy1, it’s time to bring out some facts. According to Reuters, the inflation adjusted price of gold hit a peak about 1980 at $2500 an ounce. The inflation adjusted price now is about $1500 an ounce. So in 45 years it has lost 40% of its value. A lot longer than the gestational period of a rabbit! A simple search for the inflation adjusted gold price will give you a chart you can look at.

Gold has no monetary purpose or usefulness at all.

@ Escierto,

When you introduce “facts” in the future, please refrain from cherry-picking. In 1973, a mere three years prior to the anomalous date that you chose, gold was worth ~$42/oz. Adjusted for inflation, that would be $283 today, and it’s current value is ~65% higher.

correction: a mere seven years

SoCalBeachdude That must be good weed

Tinky, no one actually thinks the 1973 price of $42 an ounce was a realistic price. It was the price set by the US government not a market price. A market price would have been far higher. By the way saying the price has gone up from 42 to 283 in 50 years doesn’t exactly say much for your argument. Gold has been a terrible investment.

Tinky:

That would be ~550% higher, not ~65% higher. If $1839, it’s 6.5 times the price of $283.

Dollar is backed by the very stong will of US taxpayers, who are now very sure, that they aren’t slogging to pay back debt, that govt created to bail out multi-billionaires.

Good thing is that there are so many options. Just check how Russia has been bypassing sanctions on all dollar transactions: Gold, silver, copper, nickel, barter, oil, natural gas, fertilizer food etc.

Wait until you hear about Jay Powell’s rate increases, that he’s funding with deficit spending.

Only the truly wealthy have access to the interest rates he’s advertising, especially on a risk adjusted basis. And he’s tricked Congress into committing to pay them a nice kickback on a regular basis!

If you’re rich enough to be able to afford a bank charter, it’s practically backdoor federally guaranteed UBI.

Even better, it provides good cover to fire those pesky, costly employees that always seem to take vacation days when you most need them. Why bother trying to manage them into producing a nice 5% yearly increase in revenue, when uncle Sam has your back?

Bitcoin and other cryptos are the worst scam there is. And they keep printing it, I mean mining it, and forking it, and they keep creating new ones, it’s worse than all the world’s money printing combined. The whole thing is just a bad joke. So if your vision of a “free economy” is based on a huge scam like this, well then, go ahead.

In a few years this whole Crypto fad will fade away. All the investors in this scam will have lost all their money. No one will ever talk about it. It will go the way of the “liar loans” of 2007, the S & L meltdown of the early 90s.

I lost count, but I think there has been at least 3 Bitcoin forks? That means there are really 88 million Bitcoins out there because the old bitcoins after the fork do not go away and still have monetary value. They just give them a different name I believe.

I know this may seem extraordinary. But, given crypto orgs history why isn’t the fdic performing wellness audits on coinbase and others. Given the recent history why are the silvergates getting floated several billion from fed home loan banks with the trust that implies but has not been earned. Yes, I realize they paid it back, not the point, why would they qualify.

Why doesn’t fdic, sec perform a regulatory function instead of reactive mop op function. Shouldn’t the feds audit to ensure whether these crypto orgs qualify as securities or banks. The self policing philosophy culture is clearly not defensible, never has been, never will be.

ru – mebbe, but it sounds a little bit like panning for gold on an oceanic beach (though our digital technology might provide the equivalent of hydraulic mining here…oh, wait).

may we all find a better day.

BTC and all cryptos are literally nothing.

These firms create their own “coins”, the asset mania gives it value, and then it’s an asset on the balance sheet.

Until the Ponzi schemes collapse, one by one.

Crypto creates no value. It merely transfers it. When one of these “coins” goes to its actual value – zero – the same wealth exists as before. The ownership just changed in between.

If someone’s gotta print the money, I, for one, prefer the system where the Feds print the money, rather than the banks.

Greenbacks might not be that trustworthy, but it’s more trustworthy than scrip.

But the good news is, you’re truly free to stop using the dollar and participate in whatever “free economy” you want. Try minting your own coins for use around the house or with friends and family. Let us know how that goes.

To all who think gold has no uses other than monetary: go to any serious electronics store and ask about high- end cables. The contacts will be gold plated. They aren’t doing that to hype them, there is no substitute. These cables will be more money but not hugely expensive. The expense per ounce is large but gold is the most malleable element, it can be applied in the thinnest coat. And of course never corrodes. That’s where the consumer encounters gold in its main practical use. In aero-space it’s everywhere.

Nick,

I think that’s the point they are making. It basically is not money any longer but still has value as a metal… not currency.

Central banks still consider gold as money. It’s part of their reserves.

As I enjoy Brahms’ 2nd on a BIS SACD playing on my main two-channel system, a fair amount of gold is in use.

LOL. The old joke that the only unhackable computer is not connected to the internet, is in some desert far away from cell phone towers, buried deep in the ground in a Faraday cage powered by solar cells or a nuclear plant, AND set in fire until it is destroyed with thermite bombs applies to cryptocrap. It WILL be hacked, sooner or later and all engineers create backdoors. It would be the same to buy gold and put it out next to the food condiments table in a bankers’ conference. LOL.

That said, my prediction that capital would grow short and banks (of all types) would become legally insolvent as their thin capital cushions were exhausted –those banks not already insolvent per the BIS swaps report, bad auto loans, etc.— is coming true. The first, tiny domino has fallen. I am so glad that bank accounts are guaranteed by such a vast pool of funds. LOL

Everyone can experience all of the benefits, and also the costs, of a “free economy” by spending a year in Somalia!

Bitcoin is a trash system. It’s slow, it’s power-hungry to an insane degree, it’s intrinsically linked to ransomware, it effectively has upper limits on how much currency there will ever be (specifically, there are 1.7 million bitcoins left to be minted and then that’s it, no more new bitcoins. Ever), and if you were to start a digital currency from first principles it would not look anything like bitcoin. The tech behind it is terrible because it was first and unrefined. The only reason why *anyone* talks about or uses bitcoin is because it’s the favored speculative vehicle.

I’m not a crypto believer but I’d take Ethereum over Bitcoin at this point in a heartbeat. Ethereum has a library of issues but it is explicitly designed to improve on bitcoin as a technology.

Invoking Bitcoin as “the future” or the solution technologically basically is the equivalent of putting on a clown nose and makeup at this point.

Block chain appears to have some applications in commodity trading. It can replace paper documents and potentially eliminate some forms of fraud. I suppose they need to create artificial chains in order to make them long enough to be secure, though (I may have misunderstood how it works, but I believe that a short chain is susceptible to being cracked.)

Crypto is a farce if taken at face value. Why is a “currency” valuable or useful simply because it is limited in supply based on a hard-to-replicate algorithm? The principle is universal which means that no matter how limited one crypto might be, you can always create a new one which looks nearly identical. So, if it gets too hard to mine Bitcoin, just tweak the calculations and call it Citcoin, then Ditcoin, the Eitcoin…and so on.

It’s tulips and houses all over again.

I fail to understand what legitimate purpose block chain serves that is not already served assuming one doesn’t believe fiat is a hoax. The security it promises, when manifested in a real market has been hacked by fraud, self dealing and theft.

It presents more complexity, opaqueness, prevents regulatory scrutiny, historical recipes for fraud and bastion for criminality. God I sound uptight

JL,

1) Heavily indebted governments are using money printing (systemic dilution of existing savings base) to “solve” their intractable debt problems,

2) So long as this continues, people with savings will want to hold less and less in fiat (because it will get continually devalued),

3) The theory behind crypto is that the algorithm is designed to generate *an ultimately fixed supply of crypto*…in theory anything *useful* with a fixed supply should do well relative to continually diluted fiat.

4) Crypto was just seen as more flexible/easily mobile/anonymous/difficult to tax than traditional inflation hedges (real estate, precious metals, etc).

5) But thousands of non-utility-backed cryptos is just thousands too many…without intrinsic utility backing, cryptos are just unmoored to anything other than holder faith.

6) A crypto backed by a/many utility goods might do very well, especially if the crypto could be easily/quickly/anonymously converted back and forth into those utility goods.

7) So long as government fiat debasement/dilution continues, the impetus to *any* alternate *store of value* will continue.

Until a modern day Ghandi or Mother Teresa come out with a crypto, I’m not buying any. The area is rife with scam artists.

Bobber – sad to say, in terms of ‘rifeness’, our entire species is, and often from the ‘moral high ground’ (as opposed to hazard) in addition to the one of ‘free lunch’…

may we all find a better day.

Problematic choices…eh?

Crypto not the answer? Ok..along some lines of thought I agree. But the current CF of central bank driven debt monetization designed to concentrate wealth increasingly in the hands of Wall Street/MIC and their government abettors?

Their kids won’t be the ones fighting WWIII. Count on it.

“do you see any meaningful use for crypto”

Criminal activity. Period.

The excellent National Geographic Series “Trafficked with Mariana van Zeller” is going to cover crypto “Rug Pulling” next week in her typically thorough and dangerous way where she interviews heavily disguised perps on their own turf.

Pure POS blockchains like Solana, Algorand etc are extremely efficient – some can even settle quicker than services like Visa.

I can imagine these blockchains displacing services like Paypal and Western Union to an extent – with the implication that folks imediately convert the crypto to their home currency upon receipt, rather than holding it as an asset.

In what large transaction does the payer not want third party proof of payment?

This. Thos is on the main reasons El Salvador has adopted it even though their currency is the US$. Moving money between countries adds up to a lot of money. As someone who lives in Honduras, this would be the reason I would use it.

Controlled destruction of excess money instead of making “us” raise taxes or interest rates to hover it all back up?

Kinda like when we have some old tranformer oil that is laced with PCB and Dioxine, we pay to ship it off to a facility in Germany where it is burned at a high temparature, destroying the toxins.

The block chain technology could be integrated into other applications that need a guarantee of untampered data, such as SOX compliant databases. However given that crypto is a godsend for all kinds of criminal activities like money laundering, illegal purchases etc I don’t think it will ever be a legit commerce medium. Who will guarantee it? It’s all well and good to sing kumbahaya and yeh world currency etc, but who backs it up? The USD is backed by the US government, on the back of all our assets. You cannot say government needs to be hands off and turn around and expect a government safety net. It was, is and always be a ponzi.

Why sure. Black market criminals and offshore casinos love crypto. Anything to get around increasingly onerous government controls. Why is online poker legal in most of the world but not here in the US, or at least not in all states?

My name clearly isn’t wolf but I’ll answer anyway.

The substance behind the concept of crypto is a tiny flame with interesting potential. The fuel that turned that tiny flame into a raging dumpster fire was enormous piles of B***S***. Mounds and mounds and mounds of it shoveled daily by those with vested interest in an outcome.

I’ve personally lost hope that we’ll get back to the shred of substance, if there ever really was any.

Reminds me of e-mail and the internet. Such promising concepts that quickly devolved into a huge mess of barely-navigable garbage. I am thankful for this website being a rare exception.

Meh. Technology, except in extreme cases, is not the core problem (e.g., nuc weps, bioweps), it’s usually corrupt, venal people who figure out how to use technology for malevolent purposes that is the primary mover.

Just posting for a friend who asked.

Well that was fun while it lasted.

FOMO = ECEG

Easy come, easy go

The new “new” thing is just the same old thing repackaged. Charles Ponzi would be proud.

Mr Ponzi would be amazed and humbled.

Looks like a perfect holding for ARKK.

Shocking. A crypto bank implodes.

You would think a bank called SilverGate would at least have some silver.

And some GATES too!

2b – remember way back in my ’50s-’60s San Diego youth, ads for ‘Silvergate Savings’. Don’t know if they were wiped out in the S&L debacle or ultimately morphed into this one…

may we all find a better day.

Crypto goes to zero and no one even notices. It is just Monopoly money. It isn’t an investment.

What shocks me is that anyone invests in crypto.

People have been “investing” in crypto since… the beginning of time. By another name, it’s a “con artistry”. Gullible people are the first in line. The sheeple saunter sheepishly along. Finally, there are the extremists, the enforcers who guard the perimeter and make sure that the Kool aide is drunk. When the con gets big enough, few can stand against the crowd.

I studied crypto a bit. Even tried to create my own using free source code.

I get the blockchain thing. I even bought some crypto to experience it. It was just a hassle keeping track of the crypto. I am sure I have some cryptos somewhere that I will never find again.

LOL I just received a check from Voyager for some cryptos I had in an account there that I forgot about.

But when I talk to people who own crytpo, I would say 90% of the them don’t understand blockchain. Sure the can talk about the line items everyone talks about. Finite supply, peer to peer, no bank, etc. But in the end, they all bought because they thought they could make a lot of money by doing nothing. Well doing nothing is free. I am not sure how that works unless your on MTV. “Money for nothing and the chicks are free”

ru – with a nod to Dire Straits Mark Knopfler…

may we all find a better day.

It’s how to invest in virtually nothing, but expect unbelievable profits.

Let the dust settle, then the (if any) future of crypto will become clear. Not two years ago, not today.

Bit by bit…

Some people made lots and lots of money…

“Money”? What do you mean?

:D I’ve always found it interesting that crypto values are quoted in dollars.

That’s not surprising at all. The goal of every scam is to make some people lots and lots of money.

Would it not be more realistic if that 99% down chart was more human blood colored, as a lot of people who could not afford to lose it all probably lost it all in this ongoing crapto carnage.

Yet there is still hope as maybe Silvergate can change their name to LeadGate Crypo Bank and then build a gigantic particle accelerator to turn lead into gold utilizing a mere 10% of the world’s electricity supply.

About as wise and efficient at the other crypto shitcoins, and you could sell the carbon credits by not having to actually mine real gold against using 10% of the world’s electricity supply, as long as that electricity was super duper green.

Another brilliant “something for nothing” idea, right? Only thing missing is rich famous people yelling “Fortune Favors the Brave” in tacky Super Bowl commercials.

Win/Win if your goal is to speed up extinction of the species and keep the humans unproductive and distracted from focusing on the real existential issues that need to be resolved to ensure future generations. Actually would not be surprised to find out someday that A.I. invented crypto to speed up the take-over time line.

Thanks, Yort. Very refreshing, especially this early in the morning, or should I say, “mourning”?

If human beings stopped amusing themselves, would the world stop spinning?

How – thing is, the world doesn’t care if humanity walks it or not, only humanity can do that…

may we all find a better day.

SilverGate should change their name to LeadBalloon.

FDIC showed up and then they decided to liquidate the bank?

hmm. Who’da thunk.

I am really sorry I haven’t catalogued all of Wolf’s new buzzwords and phrases over the last six months. Consensual-hallucination and kathoomhed being two of my favs….

kathoomphed*

Little do the loan committee, directors and officers presently realize, the next step of the FDIC will be to file a Federal District Court lawsuit alleging negligence on the part of all of the above persons. The FDIC will then legally beat them into financial submission and confiscate virtually all of their non exempt assets. Someone should have told them in advance that you never want to be a director or loan officer of a bank due to the financial risks involved.

Isn’t the first order of business of most corporate charters to protect the officers of said corporation?

Fairly true, but getting a bank charter isn’t easy (for about 30 years) and regulators like the FDIC have an array of statutory/regulatory tools that can impose “surprising” liabilities on bank insiders.

Sometimes the regulators bring the semi-obscure hammers down, sometimes they don’t.

The inconsistency is what leads to complaints and why smaller banks have their own lobbying organizations.

Remember, the mega 4 banks were really the worst actors in bubble 1.0 – but they received a lot more salvation than punishment.

If you commit crimes carrying out your bank duties, you lose the “corporate shield”.

What a colossal waste of human and financial capital. These crypto “investments” never made any sense.

The promise of “crypto” was always that you could get rich and they could never track you and make you pay taxes. This is how many fools parted with their newfound wealth. Those trading on crypto exchanges found out the hard way that you can indeed be tracked if the government is serious enough about it.

If you have some coins in your wallet, then you can trade them with someone who might give you physical things, even though that can be eventually tracked as well. Happened to a guy who sold (or exchanged) his house for Bitcoins in Austin, Texas.

Good points. I think eventually Governments would like to have digital currencies for exactly this reason…..to track money. No hiding money or transactions. They could tax every transaction…etc.

But it will not be some decentralized crypto and it will not be a finite crypto. IMHO.

Pssst! ……For truthful perspective on matters Bitcoin and SHA256, an anonymous friend suggested learning about Collossus, the British Collossus of “unbreakable code” un-fame.

I visit Wolf Street bec I know so little about finance [the handling of money]. Wolf’s appraisals are so honestly done . it is like fresh air after ingesting so much unhelpful smog.

I share Collossus with you.

`

I have to agree with what Charlie Munger said about crypto but many people get rich because of it, so they are surely against our opinions. While I agreed of the blockchain technology that embedded with it are useful but it was manipulated by those genius to create a casino. Look, how many crypto currencies are there traded on the daily basic and if it is a productive assets? How CFTC can categories it as a commodities?

“but many people get rich because of it…”

Not many. Easier to buy coins than to sell at a profit. Early miners and whales own most of it, just like the stock market.

Cryptos got lucky because Draghi and Bernanke (and also Jerome) promised to “do whatever it takes,” and Western masses were ignorant enough to believe that printing money would have no costs associated with it, especially when they got some pandemic money.

“The best way to destroy the capitalist system is to debauch the currency.”

The future of crypto is the same as the future of Rujha Ignatova’s oncoin, my compatriot who FBI is looking for all over the world and who dragged millions of people with this scam. These are pyramids that we here have known since the 90s of the 20th century under a different form. The first ones win at the expense of all others who joined later in the chain. Behind the crypto are many computers and people subjected by the creators of this scam, nothing else. This is the “Ponzi” scheme that cannot exist without subsequent donors.

The good news is that the empty spot once occupied by a defunct crypto bank can now be used to provide virtual space for housing a lot of non-existent people. Solving more problems everyday! Your highway robbery dollars at work.

I heard the market will be crashing in 60 days.

1) Creepto flunked. High tech income slumped. The high tech prima donnas became very angry people.

2) Unchecked, they can cause a lot of damage, strike.

3) Fake after fake on top of fakes, a pyramid of fakes.

4) They changed the world from the safety of their monitors. For them It’s a game. They want to stay in the game, play with their mouse, but game is over.

“Silvergate received $4.3 billion from the Federal Home Loan Bank of San Francisco late last year, company filings show. The billions in liquidity provided by the FHLB in the fourth quarter alone helped La Jolla, Calif.,-based Silvergate stave off a further run on deposits. The crypto-friendly bank now holds roughly $4.6 billion in cash — the bulk of which came from Home Loan Bank advances, according to select financial metrics that Silvergate released last week.” (source : American Banker) because of the continued bank run,This seems to be implausible unless the Federal reserve was tapped on the shoulder. The Amount is staggering and if repaid backdoor, ahead of other creditors without legal authority could be cause for clawback by the FIDC. Never trust counterfeiters

Agree, their activities of the past 6 to 12 months should be brought under a microscope and under extremely bright lights, preferably sun light.

Most of the cockroaches have scattered by the time the light turns on.

From my article above — nothing “backdoor” about it.

“But it did pay back the loans from the Federal Home Loan Bank. Part of the additional losses disclosed on March 1 come from the sales of additional Treasury securities to raise the funds to repay the $4.3 billion in short-term advances it had received from the Federal Home Loan Bank of San Francisco (Silvergate Capital is headquartered in California). Silvergate had disclosed the advances as part of its filing on January 5. The fact that the FHLB was lending $4.3 billion to a crypto bank had caused quite a ruckus. On March 2, the FHLB confirmed that these advances have been ‘fully repaid.’ So that’s off the table.”

“But it did pay back the loans from the Federal Home Loan Bank.”

This is heartening. I could not believe that was happening. However, are taxpayers on the hook for FDIC bailouts?

At this point it seems that the FDIC insurance is not needed. It seems there are enough funds at the bank to pay off all its depositors. If the FDIC insurance is triggered, the FDIC will take the bank into receivership, bail in all shareholders and preferred shareholders, sell all assets, and in the end, there might be little or no loss for taxpayers. The FDIC stepped in early enough before the money was gone. That’s a good thing. That is how that is supposed to work.

The total crypto market value peaked in 2021 at close to $3 trillion. It has lost almost $2 trillion since then.

The $20 bill we hold in our wallets is worth something because it was once exchangeable into 1 ounce of gold.

At $1,825 that $20 bill is worth 1+% of what it was once worth. My guess is that the dollar chart will ultimately look very much like the Silvergate chart above.

History points us to more inflation and real dollar depreciation.

Brewski,

What assets do you predict will depreciate *less* than the doller in the current year?

Honest question – only thing I can think of are short term treasuries. My 6mo T-bills @ 5% are just barely keeping up with inflation. PMs have basically traded sideways over the last year.

Dollar*

The US Dollar will continue to rise substantially in value both on the DXY and in purchasing power.

I saw a guy showing the charts. Whatever it is for the dollar, its about twice as mod for the pound. Swiss Franc was the best fiat I think.

I’m going to go ahead and say it, because it needs to be said and re-said and re-said: Gold was yesterday’s cryptocurrency. You know that is true. You don’t want to admit it, but you know it is true.

We have all seen the ads on TV where they tell us that the Fed “printing dollars” (FED does not print money, it is printed by the BEP of the Treasury Dept, but no one seems to understand that) is creating a disaster in the making that makes our worthless dollars at risk for being more worthlesser, so we should BUY GOLD! Every time I see one of those ads, I ask myself the same question: “Self, why would they be willing to accept my worthless dollars and give me their far-more-valuable gold? Would I sell to them if I owned the gold and they had the dollars? Of course not….”

Why do you so easily discount thousands of years of tradition and faith?

If I said Jesus never existed, the people who believe in Jesus would clearly disregard anything I say. “Prove it” – they would say.

You have to respect the momentum of beliefs and market pricing, even if you think they are illogical.

Those who “know it all” lose a lot of money.

Indeed.

Then why are all non Western banks loading up on gold? Why aren’t they buying that sweet pristine dollar denominated UST? 🤣

The dollar loses 15% in two years, and crypto loses between 70% and 100% in two years against the DOLLAR? Crypto isn’t an alternative to the dollar. It’s an alternative to gambling and losing money fast, rather than slowly.

That $20 bill in your pocket is still worth something. But only because the government will accept it in payment for taxes & fees.

Governments get to decide what is an acceptable legal tender. Not some half-crazed Libertarians sitting at a computer somewhere mining crypto.

Old Ghost

What the f.ck does “Mining Crypto” mean????

I’ve heard this phrase used many time and don;t understand what it means. Does it mean digging up the earth to find crypto coins buried somewhere????? Can someone please explain it to me in the English language. I need Clarity.

Swamp Creature,

Its just a metaphor. ‘Mining’ is simply a computer running an algorithm.

LOL And the cost of electricity at you home to mine one bitcoin is over $12,500.

Big flaw of Bitcoin. Why even mine the cryptos. Nobody realizes this but everyone is sort of subsidizing the energy costs of cryptos even if you do not own any. All that energy that could have been used by manufactures to produce goods is gone forever. We need to go drill some more nat gas wells. LOL

Mining is a term used to create Bitcoin.

In order to create one Bitcoin, an algorithm has to be run on a computer for X amount of time. The complexity of running the algorithm and the time to produce it sets the base cost of 1 Bitcoin.

ru82 stated as a fact that it takes $12,500 in electricity to run this algorithm on your home computer to generate one Bitcoin. Every new Bitcoin produced takes longer because the algorithm is more complex. I don’t know if $12,500 is correct but it seems low. According to the internet, mining one Bitcoin on a home computer takes typically 30 days. $12500 seems low or everyone would mining a bitcoin per month and selling them on the open market for $22,000 pocketing 10,000/month.

What is interesting is my job is to offer tools to help miners reduce the costs. We sell tools to run algorithms faster and with lower power. If you can make $22,000 in fewer days and with lower power, ie $5,000 in electricity in 10 days, then you can make more money. That is capitalism. I am in the high speed/low power specialized chip business for anyone that needs these features. There are many specialized applications other than Bitcoin mining that require higher speed and lower

You could say that if it takes $12,500 in electricity to produce one Bitcoin than that is the base price. If the market is asking $22,000 then it is worthwhile to mine. You cold say that Bitoin is the same.

The questions everyone has is why Bitcoin is worth $22,000?

The same type of algorithms can also create other types of crypto coins. They should have the same value. If I spend $12,500 in electricity to create one Bitcoin, I should generate some kind of profit, right? The Treasury prints a $100 bill for pennies in cost. They are making money.

I could ask the same question about Beanie Babies or art. If I spent $20,000 for a rare art piece 10 years ago, I should be able to sell it for a large profit now, right.

In my opinion, it is all based on demand. If psychologically people think it is rare and in personal demand, then they will keep the prices high for Bitcoin, Beanie Babies, or art.

Mining involves search through a vast sea of number to find a single number that hasn’t yet been found and then adds that number to the so-called craptocurrency ‘blockchain’ upon which bitcon is based.

I read an article somewhere that FHLB has transitioned to a lender of next to last resort for banks in trouble. This article makes we think that is true.

I think my first mortgage was thru them in 1980. Floating rate at around 11%. I think it went to 13%.

Yes, a spike in these loans to banks is a good indicator of what is to come.

When I heard the FHLB got their loans repaid before the announcement my first thought was they were frontrunning everyone else. The federal government better hope everyone gets their money out or it just might be the last nail in their coffin.

‘Everyone’ will most certainly NOT get their money out, and only insured depositors will be covered up to the FDIC statutory amount. As to the rest, they knew the risk going in and deserve to lose funds and have no excuse whatsoever to whine at all.

“….including its proprietary technology and tax assets.”

Tax assets? Referring to tax credits?

They had $1.3 billion in losses in 2022. Surely someone is going to pay something to get that $1.3 billion tax-loss carryforward. Though my (nearly non-existing) understanding of this is that it’s hard to do.

I worked for a multi national with huge carbon output. While in the finance end, I did see that the carbon credits were being bought and sold at a furious rate. (not cheaply either). Guess tax loss carryforwards can be bought and sold as well. Thank you.

Tax losses can’t be bought and sold like carbon credits. To acquire tax losses a corporation needs to effectuate a reorganization in which the acquiring corporation meets several requirements that would preclude taking advantage of the tax losses of the target corporation. For example, IRC 269 precludes the use of losses if the “principal purpose” of the acquisition is tax avoidance. It’s a tricky area of tax law. Large accounting and tax law firms have groups dedicated to structuring these acquisitions properly. Wolf is correct, it’s hard to do.

Silverado, Silvergate, it is simple, never name a bank Silver*anything.

LoL, crypto to the crypt.

Gee, hoocoodanode?

I gots me a 2006 Silverado parked in the driveway. She’s surrounded by snow a meter deep, but she’ll run when asked.

Silvergate? Nope, not so much.

Wolf, very interesting piece on the fad of crypto.

However, my good man. Do you continue to believe the US Dollar is a good store of value? Today’s dollar would be worth less than 4 cents back in 1913.

Today, the annual inflation rate in the US was 6.4% in January of 2023!

I do understand the crypto scam but sir, are we all participants in a dollar scam?

Crypto’s plunge is measured against the dollar. So crypto plunges 70% to 100% over two years, against the DOLLAR. While the dollar lost 15% in purchasing power over those two years. So crypto lost whatever it lost AGAINST the dollar in two years, plus it lost the 15% that the dollar lost in purchasing power.

At least I can do something with the dollar. I can buy securities and CDs that earn 5% a year in interest credit-risk free. I can buy securities that earn 8% with higher credit risk. I can buy other dollar-denominated assets, no problem. I’m NOT holding “dollars,” I’m holding dollar-denominated assets. If you hold crypto, that’s all you hold, and you don’t earn interest because all that stuff already blew up last year, and you just watch your cryptos go to heck.

Hi Wolf,

Not asking for financial advice, but…

Theoretically, what’s the best place for an average joe to park his or her cash right now, to protect it from inflation?

I’m thinking I-bonds and short term T-bills, but would love to hear some other ideas…

Cash grab will be the winning strategy this year. This is the position of more professional and detailed invectitops, anĸetyped by Blomberg. Two-thirds of them expect the cash in the portfolio to be net positive by 2023.

In fact, this is logical, given the higher yield on American bonds and the higher interest rates on these bills. Haiti is a big change after years of almost no profits from the paps in the bboy west and almost zero interest rates

I like I-bonds, but they’re NOT a cash management instrument. They’re designed as a foundation layer of a nest egg. They’re variable-rate, inflation protected bonds whose interest income is tax deferred. They have a 30-year maturity. And if you redeem them before x years, you give up some or all of the gains. I-bonds are designed to be bought every year and kept for 30 years. Then each year after you retire, you get paid for the i-bond you bought 30 years ago, meaning the principal and the accrued interest, so your $10,000 i-bond might then pay $25,000 to supplement your retirement income that year. That’s what they’re for. They’re NOT a cash-management tool.

For cash managemen:

There are money market funds that offer daily liquidity (if you’re waiting to buy something) with yields of 4.5% to 5.0%.

Short-term Treasuries are good if you can lock up your money for the maturity. Three months to one year are all over 5%. I buy at auction and hold to maturity. For me that’s the only way to go.

FDIC insured “brokered CDs” are similar (you can buy them through your broker). Make sure you’re below the FDIC limits.

Thanks for the clarification on I-bonds.

Is there a way to buy them with funds in a 401(k) without cashing out and taking the tax penalty? Seems like one can only buy them thru treasurydirect.gov.

You don’t want i-bonds in your 401k because they’re already tax-deferred. You don’t pay income taxes on the interest income until you redeem the bonds and collect the principal and interest — which normally is 30 years after you bought them.

As far as I know, you can buy the electronic version only at Treasury Direct. You have to set up an account there, easy to do.

>>> I can buy securities and CDs that earn 5% a year in interest credit-risk free.

Me too, with Silvergate! Vanguard sold me a Silvergate CD… one of their vetted banks. I thought Vanguard was anti-crypto! Fortunately it matures in two days.

@Concerned Citizen,

“Today’s dollar would be worth less than 4 cents back in 1913.”

How much do you think your crypto will be worth in 110 years?

That’s an excellent point. Also, if you’re upset about the deflation of the dollar over 110 years, are you equally upset about the inflation of income over the same period?

I don’t like inflation because it allows the government to manipulate the value of the currency, which can slowly bleed the real value of wages. However, comparing the value of a dollar today to a 1913 dollar doesn’t make sense if you’re trying to equate living standards between the periods.

I worked for a multi national with huge carbon output. While in the finance end, I did see that the carbon credits were being bought and sold at a furious rate. (not cheaply either). Guess tax loss carryforwards can be bought and sold as well. Thank you for a great article.

Bizzarro world.

Since Powell spoke this week, the Regional Banks ETF KRE has nosedived.

In contrast, many home builders stocks took off.

The bank said: ““The Bank’s wind down and liquidation plan includes full repayment of all deposits.”

—————————————————

If this is true, who is paying for return of those deposits over the FDIC limits? Would also be interesting to know how much that costs FDIC and to what extent the FDIC will be weakened.

This is the bank saying that the bank has enough funds to pay all the depositors (FDIC insurance not needed). See my comment below.

The article said: “The fact that the FHLB was lending $4.3 billion to a crypto bank had caused quite a ruckus. On March 2, the FHLB confirmed that these advances have been “fully repaid.” So that’s off the table.”

———————————

That should be put back on the table. Did the FHLB get special favors that put FDIC and other creditors on the hook in FHLB’s place?

I think regulators and Senators leaned on Silvergate to pay back those FHLB advances asap. They were practically sitting on top of Silvergate. That’s what it looks like to me.

It looks like that FDIC deposit insurance will not be needed as there appear to be enough funds at the bank to pay off the depositors.

If FDIC deposit insurance is needed, the FDIC will take over the bank, put it into receivership, bail in all shareholders and preferred shareholders, who will lose everything, sell all the assets, etc. The takeover usually happens on a Friday evening. So keep your eyes out for it tomorrow.

If there are any losses for the FDIC – and there won’t be at all if the FDIC doesn’t take over the bank – it’s going to be small. The FDIC stepped in early to control the situation, and that was a good thing. That’s how this is supposed to be done.

MW: 2-year yield drops 16 basis points, to below 4.9%, as rally in Treasurys gains steam in afternoon trading; 10-year falls to 3.9%

Pay close attention as per Queen, “Another Bites the Dust”. Refer to Silicon Valley Bank today, down 50% as they are basically implementing an emergency capital raise via an equity offering.

SVB, although better run than Silvergate (on a relative basis) is getting caught in the same down draft of rising interest rates and deposit concentration exposure. In the case of Silvergate, the deposit exposure was with Crypto’s and more specifically, FTX.

For SVB, the deposit concentration exposure is with start-ups that are burning significant amounts of cash and which are not able to raise new capital. Same concept for both banks as short-term cash outflows from customer deposit balances are not being replenished and given the investment strategies of the banks parking money in long dated treasuries that are getting hammered in value as rates rise, the banks are forced to sell securities at losses, straining their capital base.

For Silvergate, it’s all over. For SVB, the market is punishing this bank for poor long-term planning and properly matching short-term liabilities with short-term debt.

For any of you that are old enough to remember the S&L implosion back in the early 1990’s triggered by falling commercial real estate values and S&L’s that had mismatched short-term liabilities with long-term investments, its deja vu all over again.

My fault. Meant to say “properly matching short-term deposit liabilities with short-term investments”.

Question: Do people who gamble on Crypto and lose money get to deduct the loses on their taxes like they would with stocks? Can they offset gains on their sale of stocks with the loss on Crypto?

I was wondering that also.

Is one Bitcoin in a bank treated as if it were a stock or a bar of gold?

If I had 1 Bitcoin, 1 stock certificate, and a bar of gold deposited at Silvergate, what would get back?

Or is crypto treated as a currency? If it is a currency, it is uninsured by the FDIC. A dollar would be insured. As a currency, wouldn’t you lose it all?

Here’s the funny thing: lots of people didn’t report to the IRS that they had cryptos, and when they had gains, they didn’t report that either. They’re required to, but didn’t. So now it’s going to be a little tricky to deduct losses from something you said you didn’t have and didn’t engage in. I mean, I don’t give tax advice. But this is funny.

Wolf, I see what I think is your first mention (that I’ve seen) on The Burning Platform, about Bed, Bath and Beyond.

FDIC is way underfunded; they have enough money to cover less that 2% of monies held in banks. If the big bang hits, good luck getting anything back in a timely manor.

Same copy and paste gold-bug nonsense, time after time. The FDIC is an agency of the US government which is backed by the unlimited printing press of the Federal Reserve – and they didn’t run out of money during the big bad Financial Crisis either. No FDIC insured depositor ever lost a dime.

In addition, the FDIC takes over banks when they get in trouble. It bails in all stockholders and preferred stock holders upfront. It sells all assets, and so the actual losses to the FDIC per bank are usually small.

From what this looks like as per the announcement, the FDIC will lose zero on Silvergate because Silvergate has enough assets to cover the deposits.

In addition, you don’t understand insurance. If all cars crashed into each other on the same day and killed all drivers and passengers, all auto insurers would be bankrupt. But that doesn’t happen. Just like not all banks are going to collapse. That’s just nuts. That didn’t even happen during the big bad Financial Crisis.

Take your silly fearmongering somewhere else.

So, why not get out in the open what is really at the heart of all of this: it all ultimately boils down to trust; trust in the integrity of the prevailing currency system (or a CBDC) and its operators; trust in the crypto system and its operators. And what is that trust really derived from? The people/influences running the system.

Context matters. Which system has executive authority over LE and the military? Which system approves judges? Which system can be disposed of when it fails and which one is a long-run presence that is much more insulated from results?