Raging inflation is a tough nut to crack for income.

By Wolf Richter for WOLF STREET.

Consumer spending, adjusted for inflation, is now impacted by sharp price drops for fuel and durable goods, and sharp price increases for services. Inflation continues to rage in services, even as goods prices have dropped. I discussed these PCE price indices here a minute ago. So consumers are paying less for many goods than they had to pay a few months ago, but they’re paying a lot more for services. About 62% of what consumers spend goes to services.

Spending on services, not adjusted for inflation, jumped 0.5% in December from November, and by 8.7% year-over-year, according to the Personal Consumption Expenditure (PCE) data released today by the Bureau of Economic Analysis.

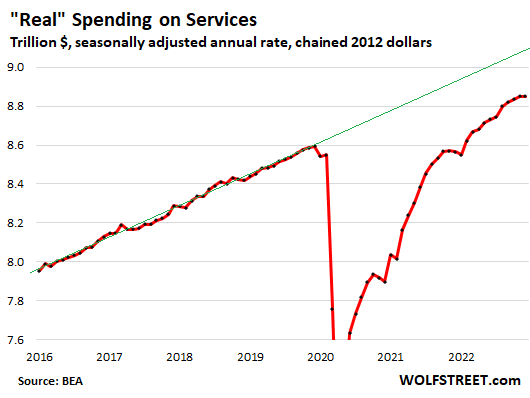

But adjusted for inflation by the PCE price index for services, “real” spending on services remained flat for the month and was up 3.3% from a year ago – 3.3% is decent growth in real spending. Services include housing, utilities, insurance, healthcare, travel bookings, streaming, subscriptions of all kinds, entertainment, repairs, cleaning services, haircuts, etc. On this inflation-adjusted basis, spending on services is still well below pre-pandemic trend:

Goods: prices drop, demand fizzles after pandemic binge.

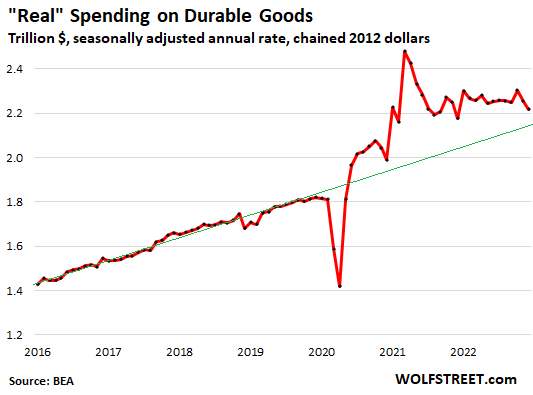

Spending on durable goods, not adjusted for inflation, fell 1.9% in December from November, and was up only 3.2% year-over-year. Durable goods include new and used vehicles of all kinds, appliances, electronics, furniture, etc.

Adjusted for inflation with the PCE price index for durable goods, “real” spending on durable goods fell 1.6% in December from November. Spending fell less than when not-adjusted for inflation because prices have dropped, including prices for used vehicles.

Year-over-year, adjusted for inflation, spending was up only 1.8%, coming off the pandemic binge and is reverting to trend. This was truly a massively overstimulated boom in buying stuff:

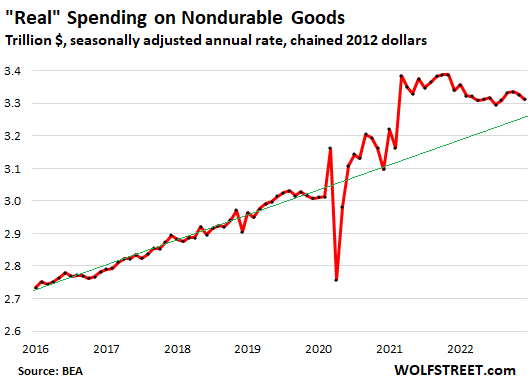

Spending on nondurable goods, not adjusted for inflation, fell 1.4% for the month, on a mix of price drops (gasoline prices plunged, but food prices rose) and dipping demand. Year-over-year, spending was up 5.6%.

Adjusted for inflation, nondurable goods spending fell by 0.4% for the month, and is now negative year-over-year (-0.8%).

Nondurable goods are dominated by food, fuel, and household supplies. Spending, after the pandemic stimulus-fueled binge, is still above pre-pandemic trend, but is reverting to it:

Overall “real” spending growth: slowing.

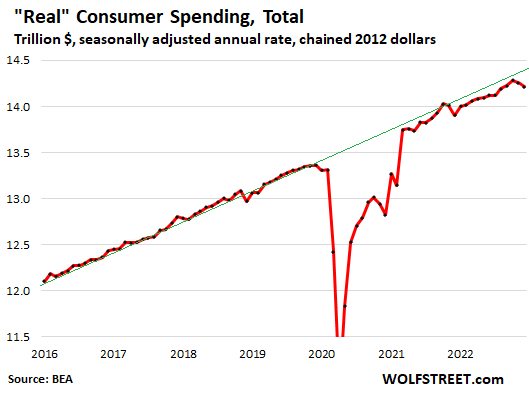

Overall consumer spending on goods and services, not adjusted for inflation, dipped a hair for the second month in a row, but was still up by 7.4% year-over-year.

Adjusted for PCE inflation, total consumer spending on goods and services dipped 0.3%, the second month in a row of declines, and was up 2.2% year-over-year:

“Real” income without government transfer payments: after inflation-caused cliff-dive, not much recovery.

Adjusted for PCE inflation, income from all sources except government transfer payments (Social Security benefits, unemployment insurance, stimulus payments, welfare, etc.) out-edged PCE inflation for the sixth month in a row, gaining 0.2% for the month.

But this measure of income fell off a cliff in the first half of 2022, when inflation tore into it. Raging inflation is a tough nut to crack for income. You can see the cliff dive here in the first half of 2022, which pushed it far below pre-pandemic trend. Over the past six months, real personal income except transfer payments improved a little, but compared to pre-pandemic trend actually fell further behind. Someone is paying for this inflation, it seems:

![]()

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Soft landing in sight. Services inflation will cool.

Better yet, make that no landing like the Malaysian flight MH370…just disappeared into the thin air..Pow Pow got plenty of magic tricks up his sleeves, at least that’s what the market is looking for.

No landing = To the moon

A 40 year old business, one of my favorites is closing the end of the month, adding to the list of my liked businesses that closed in last 2 years.

Reasons: The building owner refused to decrease rent after crazy pandemic increase! Also employee costs soared making the business non-profitable.

Apparently, the current building owner is a big pivot fan and refuses to see that here office building occupancy remains below 25% due to WFH, and most malls here now have 50% vacant space.

Hence I would respectfully disagree with Wolf, that Fed has done enough QT, or is doing enough QT to save the real economy.

that building owner is a perfect example of someone who rather prefers to be right than making money

No it won’t. Fuel prices going back up as well. Inflation is here to stay, and corrupt Wallstreet can pound sand.

Keep those rates up!!! I’m retired and do not like inflation

Time lag of the Fed hikes last year will start to slam the economy!

I dunno about goods prices lowering, my wife and I get more and more selective in the goods we buy especially grocery store goods, but the weekly spend is a lot more than it was last summer. Sorry, no data per se’ but the cart is less full and the check out bill is larger.

Yeah, I’m in queue right behind you. Grocery bill is where it’s most readily perceptible, but I see it elsewhere, including art supplies (paper, ink, paint, etc.). And of course, seeing datum which purport a correction when you still feel the bite at checkout just makes it extra-vexing to the psyche.

The magic of government data when it comes to inflation: We all see it but it dis-appears in govt data.

Harold, sounds like the people you are talking to are too wealthy to notice the inflation and too uninformed about the crisis in the economy that’s currently existing.

Good luck to you

Harrold — not my reading; what I read are simply street level observations by lay persons. What’s more, it just seems like a transparent attempt at passive aggression to cite people as pessimistic when they submit vantages which run askew of the Pollyannas.

Typically, prices bob & plunge from quarter to quarter and I don’t wring my hands or even take note. I don’t even notice when the hothouse cucumber’s go up 60 cents from one grocery store trip to the next, like my wife does. What galls are the manias and the dramatic spikes caused by speculation and manipulation. Meanwhile, I think it’s terrific news that a new toilet seat or a can opener can be found cheaper today than it was in previous quarters.

“The magic of government data” ( or the fraud of USA “Chinese”statistics ….. )

If I was younger, I’d learn to speak Mandarin.

CreditGB, bulfinch, jon:

Food prices are not going down; they’re still going up. Read what I post, for crying out loud.

Gasoline prices plunged in December, and durable goods prices dropped (cars, etc.), for crying out loud.

“Groceries” and “art supplies” are NOT durable goods, for crying out loud.

You’re making up BS theories based on your not-reading the articles about this here.

Sheeesh!!!!!!!!

Earlier today:

https://wolfstreet.com/2023/01/27/services-pce-price-index-spikes-but-goods-pce-price-index-falls-as-energy-prices-plunge-core-pce-re-accelerates/

A sociologist needs to study this. For some reason, people commenting on the internet are extremely pessimistic. The sky is always falling, tomorrow is hyperinflation or the great depression where we all die, etc…

In real life the people I talk to are mostly optimistic. They shrug off higher prices, or pretend not to notice. They never talk about macro economics, and probably can’t define “recession”. The charts you show every few weeks proves the optimistic types are representing the economy.

Harrold,

In terms of your 2nd paragraph: everyone I know bitches about the higher prices. Most of them have enough money to be fine.

Harrold, I suspect the people you socialize with are not representative of America as a whole. The upper middle class and above has not very well from the last 13 years of printing/borrowing.

Hey! I do read these articles, (and I dig your work); I was simply echoing a sentiment. And some art supplies do qualify as durable goods, dammit — at least pens and some other supporting components (my examples of b my original comment were poor).

In the final analysis — the overall cost of living on my side of the street has gone UP, demonstrably, from my electric/natural gas bill to my insurance to my groceries to my gym socks and sundry other items I’ve had to purchase. I have the receipts!

The days of cheap food and energy that drove western wealth is forever in the rear view mirror. All the cheap, easy oil to extract is in terminal decline(witness ghawar once producing 8 million barrels per day now producing 3 million and only after copious amounts of seawater is pumped into it) and all that’s left is the expensive dregs. Now even the sweet spots of the expensive tight oil dregs are in terminal decline.

According to you people, oil production was starting to be in terminal decline year aver year since 1971. Meanwhile, the rest of the world just ignored that stuff and went on and pushed oil production to new highs in the US. The frackers are making a ton of money at $82 a barrel of WTI. And if they want to, they can produce so much oil so quickly that the price of oil will collapse all over again.

Look at plant prices at HD, LOWES, local garden center, way way up.

Eating less red meat (and processed meat like bacon) not only saves you money, but also your health decades into the future.

The ”Close your eyes and think of England” argument! It might not be what you want, and you might not like it, but it’s good for the collective. And if you knew what was good for you then you would like it.

Justification for inflicting your will on an unwilling partner now, just like in the past! We’ll played, Old Chap. Brilliant!

You can have all my bugs and everyone else’s too. I’ll stick to my red meat.

Adjusting spending for inflation as measured by CPI do not really make sense as the base for assembling the CPI is many of these goods and services!

In short, the adjustment factor should be adjusted itself as it is applied. To those knowing signal processing, adjusting by CPI should be implemened as an infinite response filter.

Sams,

That’s not how this is adjusted at all.

None of this has ANYTHING to do with CPI which is an entirely different thing, released by the BLS two weeks ago.

Spending here is based on the personal consumption expenditure (PCE) data released by the BEA today.

Inflation adjustments are based on the PCE price index for each category of PCE spending, also released by the BEA today. I discussed these PCE Price indices by category earlier today here:

https://wolfstreet.com/2023/01/27/services-pce-price-index-spikes-but-goods-pce-price-index-falls-as-energy-prices-plunge-core-pce-re-accelerates/

The BEA makes those inflation adjustments (not me): it produces not-inflation adjusted income and spending data and inflation-adjusted income and spending data, all based on its PCE data. I used the BEA’s inflation-adjusted data.

Each PCE product category of spending is adjusted with the PCE price index for that category. I said this in this article.

From what I can see, both PCE and CPI inflation rates are declining.

“From what I can see,..”

OK, then look over here: yes, gasoline prices plunged in December (they’ve surged since December though), and durable goods prices dropped. But all heck is breaking loose in services, which are the biggest part of consumer spending:

https://wolfstreet.com/2023/01/27/services-pce-price-index-spikes-but-goods-pce-price-index-falls-as-energy-prices-plunge-core-pce-re-accelerates/

Month-to-month PCE for services:

Year-over-year PCE for services:

Month-to-month core PCE:

CPI: https://wolfstreet.com/2023/01/12/services-inflation-spikes-to-4-decade-high-cpi-for-gasoline-durable-goods-plunge/

Year-over-year CPI services:

Month-to-month core CPI:

Definitely seeing these service prices getting out of control…I must be old but I remember paying $40 for a concert ticket. One look at recent ticket price for upcoming Metallica show…holy crap, guess my kids don’t need to eat for a while for me to afford one of those ticket and yet tickets are selling fast, goes to show you these service inflation got legs..

If you want to compare it to a concert from decades ago, it would need to be some band whose fan base had by that time grown up and started working real jobs making real money. Just like apples to oranges, don’t compare angsty college kids to working professionals near the height of their lifetime earning power trying to relive their youth for a couple hours.

Sorry dude. 10 years ago that’s still Metalica. 1984 was 38 years ago.

Most thier fans have not been in college for quite a while.

I paid $9.60 to see RUSH in 1982. Still have the ticket.

Anecdotal experience living in Canada.

Grocery prices are slowly creeping up, even now.

Food inflation is still an issue.

Have you tried bugs? I heard they’re the next great thing.

If you eat shrimp, you can eat bugs. If you eat crawdads, you can eat bugs. If you can eat crabs, you can eat bugs.

Has anybody ever tried filet of central banker?

Roach scampi? Yum.

They used to feed lobster to prisoners….

My dad was at a USAF base in SE Asia during the 1960’s. He said the locals used to collect edible bugs from the runway lights at night.

Lentils and split peas are cheap protein.

Would it follow that if you eat hamburger, you can eat grass. Actually, I have eaten ” bugs”, lots of them. Lived in the Congo for three years. Caterpillars were a mainstay of most diets. Malnutrition was common. Besides, it’s not about whether bugs can be a part of the diet is it?

Kudos to your time in Africa and your dietary choices there.

“Would it follow that if you eat hamburger, you can eat grass.”

Absolutely. I eat grass. Very good too. Just not off your lawn. “Wild rice” is a grass, for example. Not cheap (we get it at Trader Joe’s). Absolutely delicious, nutritious, and healthy (the seeds, not the stems).

In terms of what grows in grasslands: dandelion leaves make great salads (though kind of low-cal, and as you pointed out, if you’re starving, it’s not much help). Lots of other things like that.

I eat pretty much anything, including bugs. My wife has bug-o-phobia (entomophobia), so WE are not eating bugs for sure for sure. But she loves the dried mini-shrimp she gets from Japan that go into everything. They look exactly like bugs. They’re crunchy like bugs, too. I don’t quite get the distinction. It’s the same to me.

Sorry mate, shrimps and crabs give me a swollen face and an itchy throat.

Had to go to the emergency as a teenager because I wolfed down on lobster and got an allergic reaction.

One day the doctor tells you that you’re allergic to shrimp, then crabs, and then lobster with a warning that squid, oysters and clams might give the same allergic reaction.

Sometimes smaller fish give me a slight itchy throat, but that could be contamination with shrimp and other shellfish.

Yes. Food is not durable goods.

https://wolfstreet.com/2023/01/27/services-pce-price-index-spikes-but-goods-pce-price-index-falls-as-energy-prices-plunge-core-pce-re-accelerates/#comment-493951

“The PCE price for food prices slowed to an increase of 0.2% for the month, but it still up 10.6% year-over-year.”

Some consumers are not “keeping up” with raging inflation as Bloomberg ran an article today, “Americans Fall Behind on Car Payments at Higher Rate than in 2009”.

Usually financially destressed consumers continue auto payments above all else as they need to be mobile to drive to a job, etc.

I’m guessing all those free stimmy checks and handout goodies got consumers to buy things that they can’t pay off after the free money ran out??? Hard to buy durables and services when you have to start paying your deferred mortgage/rent and student loan payments, get $90/month less on SNAP, get $1,000-$1,600 less per kid, etc, etc, etc as it is all running out, even on a state level, by March of 2023.

The top 10% can “keep up” easily with 3-5% inflation over the next few years as long as the stock market keeps going up 10-20% per year. The bottom 90%, not so much…

Yort,

SHEEESH. Instead of dragging Bloomberg headline BS into here, you should have read my article about this topic FOUR days ago:

https://wolfstreet.com/2023/01/23/subprime-auto-loan-delinquencies-rise-to-2019-levels-a-dive-into-subprime-lending-and-securitizations/

This delinquency rate is the result of subprime lenders and investors taking big risks to get big returns from the 20% interest loans.

It includes this chart, which shows that delinquency rates are back to 2019 levels, during the GOOD TIMES, when they were much higher than during the Financial Crisis!!!! Like I said, read the article. Your/Bloomberg’s conclusion is off.

My main point was not so much that consumers are “starting” to have a lot of difficulty paying their auto loans, and the fact that will likely get much worse in the next few years. My main point is confirmed by your chart posted above showing the “stimulus payments” are depleted (and not reenacted via Congress), and it doesn’t look good for a huge percentage of Americans over the next few years in regards to “keeping up with raging inflation” through the use of stimulus and other financial goodies…as those are one and done for the moment. And with split Congress, done until at least 2024/2026.

I agree that Bloomberg has some “National Enquirer” level articles at times that are absolute bull shit, like the wet suit article that caught your attention recently (which I assume you have a subscription to access). Yet I have made really good returns digging through their research online. Dig up my one and only MUST BUY stock recommendation for this forum back in 2020 for XOM at $30-$33…my research came from Goldman and Bloomberg Terminal data dug up and heavily filtered from sites full of “BS”.

Data scavenger hunts are fun, don’t you agree??? The profits are just icing on the cake…

Subprime 60+ : there is an uptrend line coming from 2017 to

2019 three peaks. This line might be breached. // 2021 low minus

2011 low is about 1%. Add 1% to the top and u have a min of 7%.

I didn’t know 2019 was considered good times? I was starting to see a lot of cracks in the QE fueled economy back then. It was papered over for years due to the massive printing and spending, but now it seems the cracks are appearing again.

Bloomberg seems to trot out that headline every six months, along with the “Americans can’t cover a $400 emergency expense.” Despite all the doom and gloom, the economy keeps chugging along.

30% of people don’t have a dollar to their name, 60% are living paycheque to paycheque, top 15%-20% are doing fine. Maybe that’s enough….

30+60+15 to 20 = 105 to 110%. That extra 5-10% is holding it together! /s

Math is hard.

Well said. The casual disregard for the lived experience of the overwhelming majority of working people in America is a sign of an unhealthy society.

Another shoe to drop soon on everyone, whether they own or rent, is the coming widespread property tax reassessment of all those homes that “increased in value” over the last decade (SEE: Fed manufactured “wealh effect” illusion).

Those doing the reassessment will no doubt look at the Fed stats for the Median Sales Price of New Homes over the last decade (or whatever the reassessment time trigger for their town, county or state is) with greedy glee…

Median Sales Price for New Houses Sold in the United States

December 2012: $258,300

December 2017 $343,300 (33% increase from 2012)

December 2022: $442,100 (71% INCREASE from 2012)

SOURCE: https://fred.stlouisfed.org/series/MSPNHSUS

I think the official definition of Property Tax (i.e. “Property tax is an ad valorem tax assessed on real estate by a local government and paid by the property owner.”) needs to be adjusted for inflation.

Anyone that claims, based on actual sales prices, that homes ACTUALLY “ad valoremed” 71% in 10 years is a liar. I will leave it to readers here to determine what part of that 71% is due to Fed caused “wealth effect” inflation and what part is ad valorem. IMHO, I over 90% of that 71% increase is due to “wealth effect” inflation.

I live in Vermont. Here is what we are expecting, this year:

Jan 15 2023: With property values soaring, Vermont towns need reappraisals. But experts are in short supply.

SNIPPET:

Two-thirds of Vermont’s 254 municipalities can expect a reappraisal order this year, according to the state’s Department of Taxes.

SOURCE: https://vtdigger.org/2023/01/15/with-property-values-soaring-vermont-towns-need-reappraisals-but-experts-are-in-short-supply/

January 13, 2023 SNIPPET:

“This is a hot topic this year as the Legislature looks for ways to fine-tune the property tax rates and relieve tax pressure on certain taxpayers,” Jake Feldman, a senior fiscal analyst at the Vermont Department of Taxes, told VTDigger.

SOURCE: https://vtdigger.org/2023/01/13/many-second-home-owners-pay-a-lower-tax-rate-than-residents-will-the-legislature-change-that/

The property next door to me: “The RENTAL HOME FROM HELL” just found a tenant after 6 months on the market. A single mom moved in. She must have been so broke that she had to have a roommate move in to share expenses. The dude put his giant Ford F150 on the driveway blocking her from parking there and now has turned into second hand squatter. He’s not even there most of the time, probably lives 90 miles away in West VA, and uses the house just for a place to park his truck. The front yard is full of trash and tree debris and no one cares. This is the state of the typical American family today.

Keeping debt to near zero on non essentials has been my answer to inflation for the past 40 years. Planning (looking past tomorrow) and due diligence has always been the key, no matter at what phase of life. The Fed really has only one tool to keep this game going, inflation. The rest are just window dressing (game management). Keeping debt low will minimize the effects of inflation. During MY good times and bad, there was fair share of each, I never had any doubt of the outcome. Trust in yourself, not the Fed or the government. FOMO and FODD (fear of due diligence) will never set you free. May we all find/have a better day (thanks 1stCav).

DEL – triple check and thanks.

indeed, may we all find a better day.

Wti oil at 82.60 earlier today is at a major long term resistance.

I feel if it breaks out even up to $90 inflation has no hope of coming down unless it drops back into the $70s again and stays there or under.

Producing countries need a solid oil price to feed their populations. Unless the FED raises at least .50 next time and stays firm with their language, perhaps we have a chance to bring down inflation for a while.

I’m not counting on anything…

Key point:

– goods prices can and do sometimes go down.

– services prices rarely if ever go down.

Inflation is not going away any time soon based on what we are seeing with services.

Personal note: Out three times this week to restaurants (I never usually go to restaurants). Shocked at the price increases and shocked at how crowded the places were. Not sure where the money is coming from.

It is coming from savings. The middle class is reducing their savings

rate. Credit card delinquencies are the canary in the coal mine.

Credit card delinquency rates are ticking up from historic lows:

“Ticking up” ha ha looks to me like it’s accelerating the fastest since 2007.

Tony,

That’s silly. Just as silly as predicting back in 2021 that delinquencies would go to zero and then below zero and turn negative or whatever, which is absurd.

Straight-line extrapolations of “trends” during crazy times (stimulus era) are just silly.

Delinquencies are now normalizing from stimulus-fueled lows. There are always people who are behind, even during the best of times, and that number was artificially pushed down by stimulus, and stimulus is now gone, and so now we’re seeing the normal number of people being behind. Everyone knew that would happen. Stuff like this always normalizes.

Delinquencies will rise to normal good-times levels, as in 2019, and then you will see the curve flatten out.

Q: Does food consumed out of home fall under ‘entertainment’? The restaurants seem mobbed, although it’s high season here, and prices are through the roof – which kinda ties to CC debt.

The child tax credit expiring last year will drop the extra cash in American families pockets by $1,000 to $1,600 per kid, so say $2,400 per family of four, around $200 per month.

LendingTree states the national average credit card balance is $6,569. Using bankrate’s minimum payment calculator for that balance, at an 18% rate, one would need to pay at least $164.23 per month not to be delinquent.

$164.23 per month is not a lot of money for many reading this forum, but it is a lot of money for at least 50-60% of society. And losing $200 per month means either you buy less food (note SNAP decreasing $90/month this year), you pay less rent (rent deferral gone), you stop paying your auto payments (hard to do if you drive to work), or you stop paying your credit card debt (easy button).

In general capitalism is very cruel to those without the financial education to understand their situation enough to not be enslaved by perpetual debt. We are all the problem, including myself, as we buy into index ETFs that hold credit card companies and other financially enslaving companies that scam us all, but especially less educated and/or poor families into paying $164.93/month on their $6,569 average debt, which would take 25 YEARS and cost $9,276.69 in interest to fully pay off the average debt serf balance over 300 long months. So get to work debts serfs, else society will call you “lazy”?!? Yet a simple stroke of the pen in five short seconds by either party’s Presidents could fixed the scheme immediately via a national financial crisis executive order, yet nothing but crickets…as the system works great for those at the top of the economic pyramid scheme…not so much for everyone else.

Well said.

“Personal note: Out three times this week to restaurants (I never usually go to restaurants). Shocked at the price increases and shocked at how crowded the places were. Not sure where the money is coming from.”

Well, I can only speak for the places I visit and where I live so it’s anecdotal like your observation but my company raised living out allowances 10% across the board. We also get another 15% on top of that if we have no option to cook and have to eat out(I work out of town a lot) which wasn’t a thing for us pre pandemic.

At the same time, every single town I travel to for work has some establishments which have been shuttered, near my residence it’s the same story, it isn’t a huge amount at all but enough to funnel a few people to other remaining places.

I probably represent a small part of the working pop. but others who simply saw raises (we got those too) will be in a similar situation, inflation is noticeable but manageable for us at this time and we have a little bit fewer spots to continue spending as per usual.

I mean inflation is obviously eating into people’s budgets whether they realize or not, but if I was in the same financial situation as 10yrs ago I’d definately be taking more drastic measures right now, this situation is not affecting every group equally for sure.

Another thing worth mentioning, this extra money I and others are getting, it’s not charity, company is charging clients more, their budgets get hit and that affects their spending elsewhere, lots of knock on effects. But the economy is huge, it takes time, sooner or later it will all come around to affect those of us who don’t feel it quite as much as others right now.

Powell in November 2022

Finally, we come to core services other than housing. This spending category covers a wide range of services from health care and education to haircuts and hospitality. This is the largest of our three categories, constituting more than half of the core PCE index. Thus, this may be the most important category for understanding the future evolution of core inflation. Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation ….

LMCI momentum was 0.62 in September 2021, which is well above zero and high by historical standards: momentum has been below this value for 80 percent of the LMCI’s existence.

January 10, 2023

The Kansas City Fed Labor Market Conditions Indicators (LMCI) suggest the level of activity increased slightly while momentum was little changed in December. The level of activity indicator increased by 0.04, from 1.17 to 1.21 in December.

I can hear Wolf growling…

1) Services : the last 2 dots stalled. The last 5 are glued together, hardly moved.

2) Durable Goods : the last 2 dots before the peak, on the bubble’s left,

are the backbone. After two years of congestion above the BB, Durable

Goods might breach the long term line, the green line.

3) Nondurable Goods : XLE, XOM, CVX are possibly in distribution.

4) Personal Income : the last dot breached 2021 peak, but the last 6 dots

are glued together : no breadth, turtle speed and still below 1970’s high…

5) Since the 60’s entitlements took over.

Wolf,

I am thinking if spending on durable goods is falling, then that means people are being stretched thin by inflation so they need to delay the purchase of appliances, cars, computers, etc. As such Tesla has to drop the price on cars, or others can’t pass appliance costs to consumers like they could during the pandemic. This is bad news for manufacturers since consumers need to divert money to services.

But in many cases consumers are stuck with paying for services. If plumbing breaks or the circuit breaker trips, you need to call the plumber or the electrician and pay up the wazoo.

It is like the old Ford commercial: “Have you been charged by an electrician lately?”

In terms of your first statement: People overbought durable goods during the pandemic, as you can see from the chart. They bought a huge amount of durable goods, and now they’re still buying a huge amount of durable goods, above long-term trend, but purchases are reverting to trend — all adjusted for inflation. This country has never seen an explosion of purchases of durable goods like we saw in 2020 and 2021. This was just gigantic, causing all kinds of issues.

Durable goods last for years: so people who bought stationary bikes, rowing machines, appliances, patio furniture, etc. during the pandemic won’t buy these kinds of things again for years. That reversion to trend had long been expected. It just didn’t get here as quickly as expected because there is still a lot of money out there that is getting spent.

The explosion of durable goods purchases in 2020 and 2021 was expected to be followed by a big undershoot on the principle of reversion to the mean. We haven’t seen any of that yet. But that would be normal, and not a sign of “stretched” consumers.

“This country has never seen an explosion of purchases of durable goods like we saw in 2020 and 2021. This was just gigantic, causing all kinds of issues.

Durable goods last for years: so people who bought stationary bikes, rowing machines, appliances, patio furniture, etc. during the pandemic won’t buy these kinds of things again for years.”

Good points, so as always the Fed pulled demand forward and caused a boom and bust cycle once again. I wonder if Powell is aware of this fact and realizes low interest rates won’t pull demand forward any more, so it is time to raise the rates and keep them there “higher and longer” otherwise inflation will destroy the economy.

Got my auto insurance renewal price. It is up 23 percent and its semi annual raise.

Six months back the hike was 15 percent

So annual increase is more than 40 percent or so.

Mine too. Went up from $40/mo to $100. Statewide increase they said.

Loyalty tax.

Shop around.

I am about to.

I shopped around. In my state AZ I was told that everyone’s auto ins (prog) went up 20-30%. Went to the “costco” insurance and ended up with a rate that beat my old pre-increase premium. Maybe they raise it in a year, who knows, but with insurance I’ve always had good luck shopping around when the rates spike.

Tesla stock up 60% this week. Everything’s fine.

Long term trend is still hard downward for that stock. Sucker’s bounce as oil rises in price. Competition will bury Tesla.

Tesla as a company might continue to grow, but the stock price is way overvalued. If you want a growth company in the EV space BYD is the best company to invest in and at 1/4 the value of Tesla. BYD moving into Europe this year and Tesla having problems selling vehicles in China means Tesla will have big problems in selling all the cars they are going to produce with expanded factories. Only way to do that is with lower price points and that will decimate the high margins at Tesla.

Tesla has under-invested in new product development and in infrastructure, which provides short term profits, but long-term will kill the growth. You simply cant dominate a market with two vehicles, unless there are no competitors (which was the case in the past, but is quickly changing). North American investors mistakenly think that the Tesla dominance in NA is true around the world. It isnt. Market share of Tesla in Chinese BEV market is under 10% and falling every year.

Tesla has more than two models….. S, X, Y, Model 3

Bitcoin up 30%, NASDAQ ascending, stale house listings suddenly going pending en masse despite still being priced 30% or more over pre-pandemic comps, bidding wars returning . And every day we see finance and macro pundits shrieking that the Fed has OVERtightened.

Tight labor environment isn’t likely to dissipate and become catalyst for economic booming recovery, but who can say…

Bart Hobijn of the Federal Reserve Bank of Chicago and Ayşegül Şahin from the University of Texas at Austin argue that most of those jobs are not actually missing, but instead the result of a counterfactual that assumes short-run upward pressure on labor force participation and payroll employment in 2019 would continue through 2022. The authors note that this would have brought the unemployment rate down to 2.3%, which they argue is “unreasonable” and contradicts professional forecasts of the unemployment rate from the months before the pandemic.

Wolf, with respect to this statement!

“Harrold,

In terms of your 2nd paragraph: everyone I know bitches about the higher prices. Most of them have enough money to be fine”.

While it may be true higher prices place less ‘pain’ upon upper class individuals, I feel it is morally wrong to debase the currency. Continual debasement, creating massive unfunded labilities and supporting a debt level which can never be paid back will eventually hurt people within all economic levels.

The falling value of the U.S. dollar will eventually translate into higher inflation in America.

Demand for mid-curve UST notes has surged! Near Term Forward Spread is underwater. Sales didn’t materialize in Q4/Christmas, leaving companies to build inventories they absolutely did not want. Huge foreign (indirect) demand in 5y UST sales is yet another sign the market has no fear over Fed rate policies. “Demand weakens. Microsoft, 3M, Intel, Google…” More layoffs. Soft landing? We’ll see within the next 6/8 months. It will be interesting.

What people are not yet factoring in is the impact of housing market. My assumption is that interest rates stay high for all of 2023 and that will mean property prices fall all year long. Once the real estate market gets seriously underwater and foreclosures rise, it will hit the economy in many ways.

I do think the central bankers will not want to increase balance sheets and will be willing to let the economy suffer a bit more than previously.

And the price of chicken, copper plumbing fittings and romex are staying up by 50 to 100% over pre-pandemic. I paid $16 for a 1 inch copper T fitting that has always cost 5 or 6 bucks. I felt violated over that purchase. 14 gauge romex used to cost 49 bucks. Now it is 140. Better than the 200 a year earlier but I would not say costs are coming down. Our cost for electric went from 9 cents to 14 cents per ???watt. These are just the items that stung me so far. There will be more. So just because the cost of goods is going up at a slower rate, we can’t just ignore that so many goods are way over pre-pandemic. It will ripple through everything. People are just now starting to feel it deeply.

I suspect if you were to poll the-man-on-street about housing, they’d say things will pick back up this summer. People are weirdly out of touch.

Never let them see you sweat. Housing market rants are now a dead horse. Folks treat this debt like it’s actively trading on Wall Street daily. Over priced assets and QE got everyone pumped in their brain that they are house rich. As the price of Home continue to drop folks are trying to hold on to the overpriced past, even though they are not sellers. Who is going to pull equity out in this climates? Market will dictate home value as always buyers and sellers must come to a agreement

As a mature small chemical manufacturer that historically sees sales slow a bit in the winter, we just had a January that looks like April or May revenue. November and December were the same way. This is partly due to our global competitors having shortage issues with certain raw materials.

The icing on the cake is a rep for two of our key components said yesterday we will see price drops on these products. The irony is one of the products is the type of product are competitors can’t get in the quantities they desire.

I’m doing my part to prop the numbers up on consumer spending. I’m finishing up a garage with an apartment upstairs that will house us until our home on the lake can be built. I’m going to spend about $15K on my current home in the next few weeks getting it ready to sell, and probably $15K on the apartment between appliances, alarm install, blinds, patio furniture, and whatever else the wife has up her sleeve.

Regarding building here, my rural county has one equipment rental store, and I pass by it daily to and from work. The skid steers and mini-excavators are stacked 5-wide and 5-deep in the lot. I’ve never seen this before, and it’s eye-opening. The homebuilding here is 98% owner-paid custom home builds.