The ridiculous price spikes now face Bank of Canada’s monster rate hikes, QT, and spiking mortgage rates.

By Wolf Richter for WOLF STREET.

In Hamilton, Ontario, after a ridiculous mind-bending spike, prices plunged 5.8% in August from July, and are down 10.5% in three months. In Toronto, prices plunged 4.0% in August from July, and are down 8.3% in three months. In Vancouver, prices dropped by 2.0% in August from July; in Ottawa by 3.1% in August; in Halifax by 3.6%. But in the two oil towns, Calgary and Edmonton, prices still jumped. We’ll get to each of them in a moment.

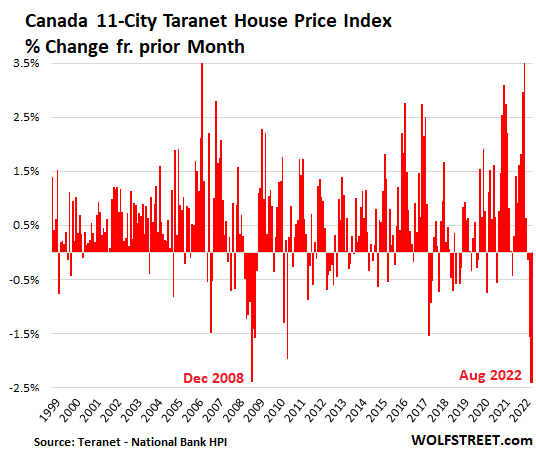

The overall 11-City Teranet-National Bank House Price Index plunged by 2.4% in August from July, the largest drop ever, together with the December 2008 Lehman-bankruptcy plunge. Over the past three months, the overall index is down 4.1%. This whittled down the year-over-year spike from the 19% range in March and April to 8.9%:

Canada’s most splendid housing bubbles are often ranked among the top of all global housing bubbles. But consumer price inflation has spiked and is spreading into the core of the economy, and the Bank of Canada has been cracking down with a series of rate hikes and QT.

These rate hikes included 75 basis points at its September meeting, when it specifically brushed off the pullback in the housing market, and by a monster 100 basis points at its July meeting, which BoC Governor Tiff Macklem explained to Canadians this way: “Things are not normal right now. After 30 years of low, stable inflation, many Canadians are experiencing the pain of high inflation – and the uncertainty that comes with it – for the first time.”

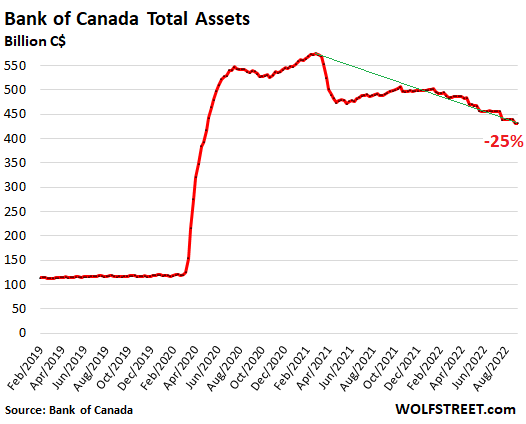

The BoC has also been unloading its balance sheet. Quantitative tightening is the opposite of quantitative easing, or “money printing,” and has the opposite effects on asset prices. Its total assets have fallen by 25% from the peak:

Higher rates & QT prick the most splendid housing bubbles.

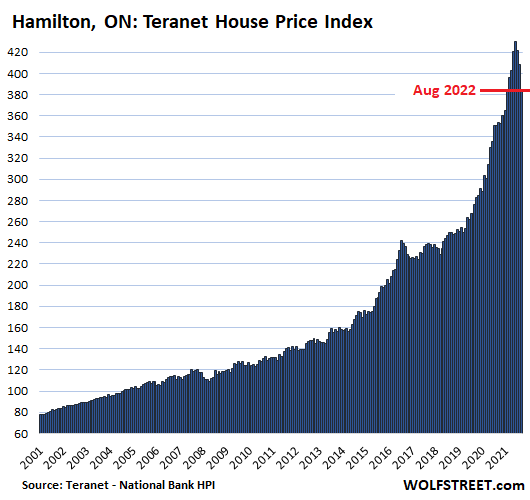

Hamilton, Ontario, had become the #1 All Time Ever Most Splendid Housing Bubble in Canada, with ridiculous year-over-year price gains of around 30%, blowing past Vancouver and Toronto.

But now there are the distinctive sounds of hot air hissing out of this most splendid housing bubble. In August, prices plunged by 5.8% from July, according to the Teranet-National Bank House Price Index. In the three months since the peak in May, they have plunged by 10.5%, which slashed the year-over-year price increase to 8.7%.

Blame the three-month plunge on seasonality? Nah. Look at the chart and see if there is anything seasonal about this plunge.

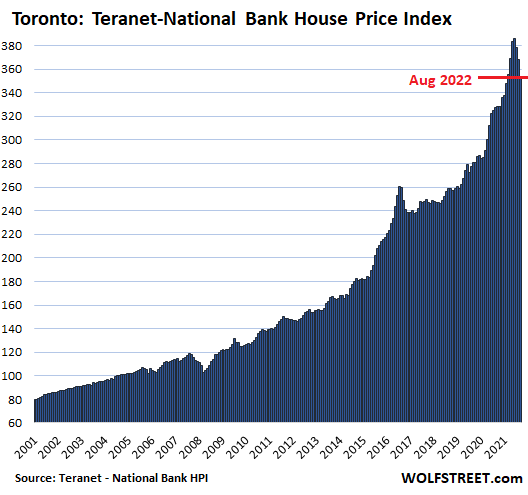

In the Greater Toronto Area, after the majestically ridiculous spike that peaked in May, home prices plunged 4.0% in August from July. Over the three months since, the index has plunged by 8.3%, slashing the year-over-year gain to 7.8%:

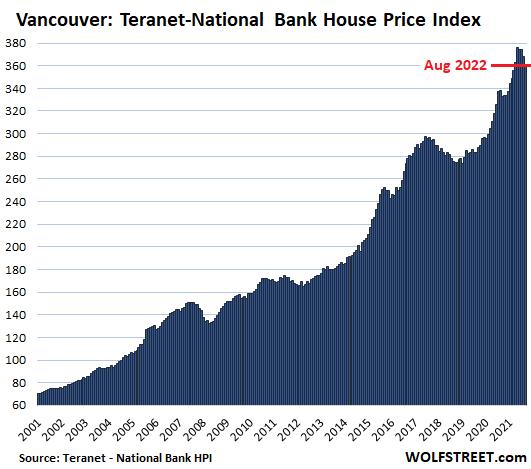

In Greater Vancouver, house prices dropped 2.0% for the month, and are down 4.1% from the peak in April. This whittled down the year-over-year increase to 8.4%:

The Teranet-National Bank House Price Index is based on closed sales in August. This data set here is not seasonally adjusted and is not a three-month moving average. For the purpose of watching the housing market go from ridiculous spike into cliff-dive, the three-month moving average – which I used in all my prior reporting – is too slow in reacting.

The methodology of the Index is based on “repeat sales” that tracks the price of the same home each time it is sold over time. Unlike median prices, the “repeat sales” method is not impacted by a shift in mix of the homes that sold.

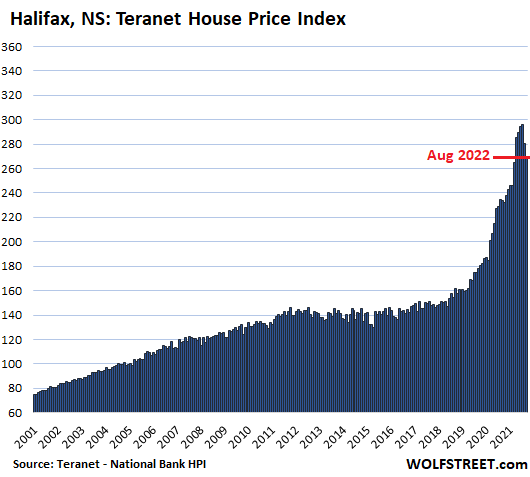

Halifax is not a huge city by any means, but it had a hugely splendid housing bubble with year-over-year price spikes in the 35% range. And the show peaked in June and over the two months since then, prices have plunged by a combined 8.7%, including by 3.6% in August from July. This has slashed the year-over-year gain in half, to 15%:

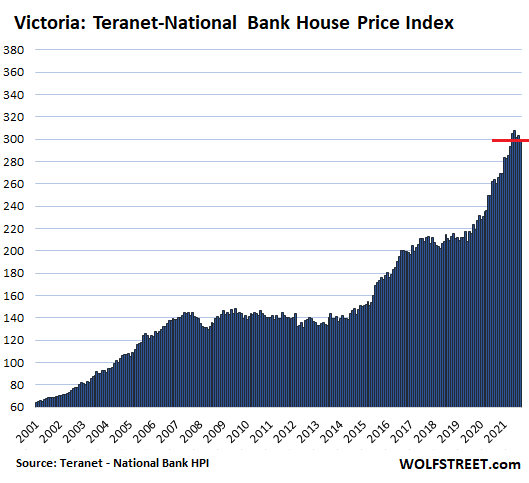

In Victoria, house prices fell by 1.2% for the month, and by 2.7% from the peak in May. This whittled down the year-over-year gain to 15%:

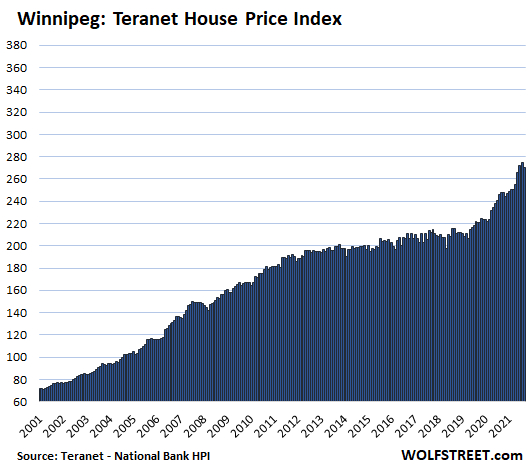

In Winnipeg, house prices fell 1.4% in August from July, which had been the peak, whittling down the year-over-year gain to 9%:

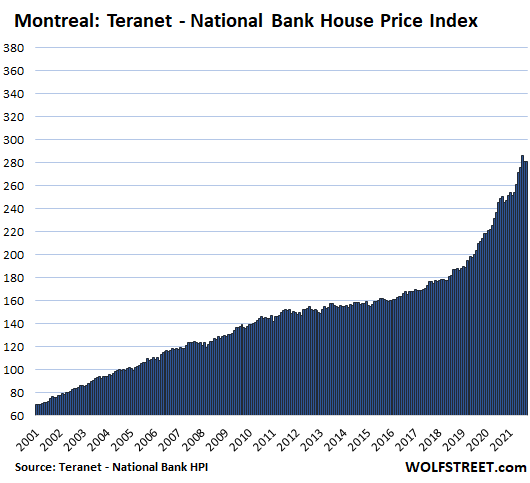

In Montreal, house prices, after falling 1.9% in July from the peak in June, edged down a hair in August. This left them down 1.7% from the peak in June and whittled down the year-over-year gain to 12.1%:

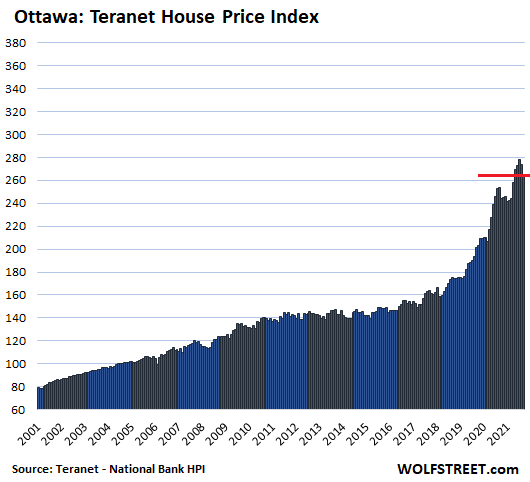

In Ottawa, house prices plunged 3.1% in August from July and by 4.6% over the two months from the peak in June. This slashed the year-over-year gain to 4.5%. Note the majestic late-to-the-party price spikes in March through May:

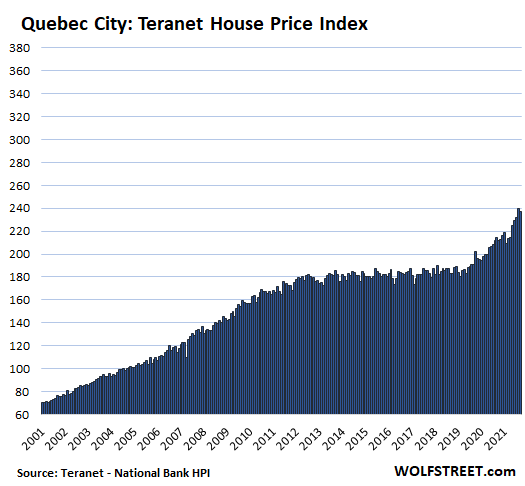

In Quebec City, house prices fell 1.1% in August from July, which had been the peak. This whittled down the year-over-year gain to 10.5%.

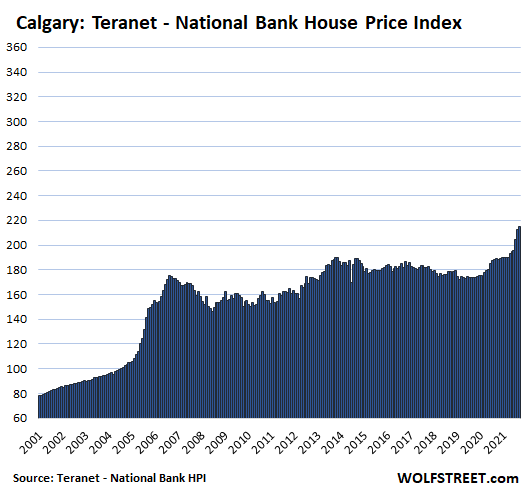

In Calgary, house prices had been roughly flat from mid-2007 until the Bank of Canada’s money-printing orgy started reaching this housing market in mid-2020. Calgary being the oil capital of Canada, and the oil business being in a boom right now, money is still flowing into the housing market.

In August, the index rose 1.3% from July, to a new record, bringing the year-over-year gain to 13.6%:

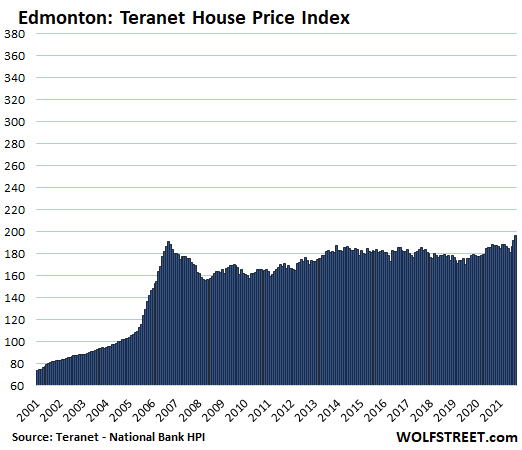

In Edmonton, also in Canada’s oil patch, house prices jumped by 2.7% for the month, bringing the year-over-year gain to 4.6%. Note how the oil-boom housing bubble that ended in 2007 turned into 15 years of essentially no price increases. Not much of a housing bubble here:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So QT in Canada a neighbor to USA this QT should also trickle into the USA QT party.

I also received a txt from my son in law about a record RRP from Feds

2.36 trillion in reverse repo today. Record setting.

From previous Wolf Fed tracking I would expect this quarter end from the banks not mid month.

Can Wolf confirm or provide a theory for this event? And could be the report is just wrong.

If there is a quarter-end spike in RRPs, it tends to be in the last couple of days of the quarter. And we’re not there yet.

Treasury money market funds are attracting a lot of funds that used to be in bank accounts (deposits). People are taking their money out of 0% bank accounts and put them into 2% Treasury money market accounts, and so these MM funds have a huge amount of cash to invest. Meanwhile the cash they hold goes to RRPs, where it earns 3.05% now, instead of their bank accounts where it earns 0%. Eventually, they’ll buy Treasury securities with it at auctions, but that takes time. This shift of cash to RRPs from bank accounts will continue until banks raise the interest they’re paying on deposits – and some have started to.

Ahhhhh! Ding, ding, ding. My RRP bulb is finally starting to light up.

Time to support the WStreet cause!

30 year Vanguard ETF fell 2.51% today, and Marcus bank (Goldman) increased savings accounts from 1.9% to 2.15% today also. Banks and investors woke up from the “Pivot Dream”. I think lack of a “House ATM” is going to hurt consumers and the global economy more than people realize…

There could be a window for 4-5% CDs in the next 6-12 months, which takes us back 14 years to 2008 as that was the last time I had we had 4.5% CDs in America.

Financial repression for savers is reversing, but I don’t think it will last very long as the global financial house of card is built upon a foundation of debit quicksand. Will need a lot of luck to time “the pivot”…

I have US T-Bills expiring 12/31. Also bought the max I-bonds this year.

Looking at maturities up to five years when T-Bills mature, but not about to go longer than that any time soon. 5YR would be more of an interest rate speculation if I think this initial phase of the interest cycle has peaked.

Can’t buy a house now even if I wanted one which I do not. Stocks would have to fall to at least the March 2020 low before I would take any meaningful position on the market as a whole. Maybe I’d buy individual stocks if the div yield is good enough and the balance sheet is sound which it usually isn’t now. Most corporate balance sheets are garbage.

Excellent info., Wolf.

On the subject of banking raising interest rates on deposits…

Many large banks are now offering so-called “Special CDs” alongside “Regular CDs”. A typical APR comparison for a 1 year CD would be 0.4% (thereabouts) for the Regular and 2.0% (or a shade better) for the Special CD.

However, there are remarkably few takers for Special CDs at this point in time because of two….special…characteristics of the Special CDs:

a) Much higher minimum initial deposit amounts (typically, $2,500 and sometimes in excess of $10,000)

and *more* significantly..

b) Breathtakingly-large early withdrawal penalties. Whereas the Regular CD would typically carry an EWP of 3 months of interest (peanuts, really) – the Special CDs are imposing EWPs of between 3-6% of the account balance!

I don’t understand this. House prices have risen 10 times in the last 10 years but the income has only risen 10% and inflation had risen 10% along with the mortgage interest rates. The people who bought houses when it was cheap have either remortgaged it to buy another house or upgraded their houses.

Now what? You all believe that the prices would stagnate or fall a small percentage only? Don’t you see the problem here? We either need to increase our income potential to match the house prices or bring down the house prices to match the affordability index of families in Canada. Can you guess which one is more likely to happen?

If you think neither is going to happen and everything will be alright, then you are ignorant as hell. The housing market is a bubble long waiting to burst. When it bursts it’s going to explode. Housing prices in Canada is going to literally HALVE or even further down. When that happens it will collapse the entire economy. What goes up comes down…

Wait and watch the fun!!

Suggesting house prices in Canada need to fall by 50%+++ is a bold statement and would probably be mocked in men’s stream media. But it’s not without precedent. Back in 2007, North and Ireland experienced a phenomenal housing bubble, house prices quadrupling in under 10 years following the peace process. When the crash came around 2008, prices fell 50 to an astonishing 80%. It sure stopped the smug and irritating dinner table chat among the middle classes boating about their equity

Maybe…but I’ve got a hunch you may be overestimating the potential for a large drop.

My “hunch” is based on the following couple items…

All housing markets are local – as I’m frequently reminded – and my local market (Metro Boston) has gone from merely “white hot” to “plasma hot” in the past couple months.

The explanation?

We’re seeing a large influx of affluent buyers from Western Europe who seem – shall we say? – “to be proceeding to make their purchases with a real sense of urgency”. Nobody wins any prizes for correctly guessing why this particular, new demographic has recently materialized.

And then there’s another thing…

Most USA cities and towns are more dependent on receipts from property taxes than at any point in their history due to the loss of many small/medium-sized business during COVID. With the state aid (courtesy of the fed government) having more or less ended – they will be facing serious revenue shortfalls if appraisals drop and they cannot raise their tax rates. This would fuel a very serious problem for municipal bonds and that *MIGHT* be enough to force a pivot from the Fed.

And nobody, IMO, should be discounting the possibility of another 2019-esque pileup in the Fed Funds Market – even if the cause and manifestation are different. The Fed’s messaging has been clear about its (apparent) willingness to tolerate an economic slowdon in the interest of getting inflation under control – but they have also indicated that they have to remain vigilant for credit market “events”.

However, real estate should never be measured on a month over month basis. It should always be looked at on a yearly basis, and to that, although gains have eroded, there still is a year over year increase which falls in line with what typically we see. So bottom line, unless you bought last year and are selling this year, the drop in pricing is meaningless.

What was the cause of the Canadian housing bubble? Lack of supply like the US? High immigration? No shortage of land.

Everyone wants to live there.

Not really too cold

Agreed. . .

I have to laugh when I hear people wine about prices in Cali

Has to be some of the best weather in NA and yet cheaper than Toronto and Hamilton.

My friend owns a precast factory in San Juan Bautista and he can do a large part of his production outside. The reduces the cost for building space, heat, anti-depressants (vitamin D), etc.

Since when? All the Canadians I keep in contract with have moved to Central America or are counting down the days to their escape.

When they told me how their voting systems works, my stomach sank.

lol. I am CDN, Brain Drain to the USA in large numbers has been going on since WWII in large numbers.. Canada’s recent growth since 1968 has been a result of political ideologies driven by Big money interests designed to further dumb down the population with docile uneducated lower paid workers which are ‘profitably perfect’ to pull the resources out of this place, while concentrating population in large centres in shitty row housing London style circa 1800s makes them easy to manage. Moo, baaahh , neyyyyeh, take your pick. Add in double taxation everywhere and you get the picture.

But OTOH,

Abudnant natural resources, and energy relativley little objection to developing them, etc…

My guess is that you will be seeing planeloads of Europeans touching down on Canadian soil in the not-terribly distant future.

@frank Standard bubble causes, really. Speculation. Overconfidence. Cheap credit. FOMO. Herd mentality. Cult of Homeownership. High rent. Pandemic upsizing, ie ‘get divorced or get a bigger house’. Weak oversight of who owns resulting in ‘parked money’ though not as much as Canadians whine about. I’m a mortgage agent and many buyers are on their third or fourth property. They do not have exotic surnames.

There’s a lack of supply driven by poor zoning and nimbyism, especially mid-density zoning. Most Canadians live in major cities.

Trevor,

I never heard that before, “get divorced or get a bigger house.” Now I know why my neighbors have such huge houses. Thanks for the explanation.

All it takes is a handful when the foreigners are bidding against each other not against the local Canadians. People for some strange reason just don’t seem to understand this.

Exactly. Go to a place like Oakville and look how many locals can even bid on a property.

A few extra foreign buyers at the margin, with the ability to pay more, can move the market quite quickly, especially if there is not much supply.

Someone coming from Beijing or Shanghai can sell an ok apartment there and buy a very nice house here for less money.

Lack of supply now has much bigger causes than (merely) poor zoning…

To be specific: shortages of building materials, fixtures, applicances, fasteners, etc. Shortage of skilled trages people, etc.

While there’s been some recent loosening of Zoning Restrictions…*nobody* is going to want to increase the supply of houses against an overall economic backgroup supportive of lower housing prices. Thus, any sort of YIMBYism reforms will be hastily walked-back.

A think that mainland Chinese buyers helped to fan the flames.

Frank,

None of the above. Or else prices wouldn’t be plunging now, because none of those conditions have changed over the past three months.

What changed over the past few months were mortgages rates, which spiked; and the BoC’s QT, which is deflating all asset prices.

What caused it? As a sometimes-1%er, living in a crappy town with literally nothing to recommend about it, but being unable to afford* a house here nonetheless, I can only comment from the sidelines that a combination of madness, delusion, FOMO, and the rocket fuel of cheap money is to blame. A little special sauce in the form of money laundering and foreigners stashing away something extra here is some added flavour. But it’s all basically insanity. Every day I find myself saying some variation on “WTF?” when I look at what is going on all around me.

*I can buy a house, but I cannot afford a house, if that makes sense.

“But it’s all basically insanity.” Exactly right. Like the tulip mania, how can it be explained that everyone lost their minds. Even now Canadian real estate prices are a bad joke. A million dollar house is a 2 bedroom 1 bath dump in a bad neighborhood.

The Chinese buy with zero regard for value. A lot of other Canadians caught the same disease.

Tulip mania is exactly the analogy for the Everything Bubble esp in the US and Canada, that and maybe the South sea bubble. Just completely unhinged and detached from economic reality or any even common-sense valuation, the argument made for continued investment in this ridiculous housing bubble across North America is the same one made for the tulips. Nothing related to intrinsic value, but just “housing values will keep going up! buy now or you’ll be always priced out!” At least with tulips and even crypto, the bubbles are in something frivolous and dumb that speculators can lose their shirt in. With housing though, the asset bubble is in a basic component of society–shelter–that everyone absolutely needs, like healthcare and education. Bubbles in areas like that are far worse because they cause permanent damage to society. Encouraging asset bubbles in housing was dumb and tbh criminal, made possible esp by the Fed’s foolish QE policies and MBS purchases only now unwinding.

“I can buy a house, but I cannot afford a house, if that makes sense.”

It makes perfect sense, to those who understand prudent financial management.

Being able to qualify for a loan and make the mortgage payment does not equal “affordable”.

This x100. My broker says the bank will qualify me for a 5-600k loan no issues, but we certainly can’t afford that monthly payment. I for the life of me cannot understand that break in logic.

A very tight supply of residential zoning for raw land regulated via provincial government policy.

It’s also very difficult to finance raw land without at least 50% down.

40% of the market is mortgage free.

People don’t realize how conservative the Canadian banks really are in comparison to US banks.

I have a rural acreage in Hamilton, it nearly doubled in value during Covid and I had no interest in selling because land is hard to find.

Same thing with lake front north of Toronto.

so according to you, no crash in home prices in CA ?

We think the same in California :-) and we have our own reasons.

In our neighborhood the real estate people say that there are at least 20 cash customers waiting to buy and they’re all want at least a million dollar home or more and they are all Chinese or Koreans

Replying to “Dl cu ni gham” ==> real estate people :-).

Replying to “Dl cu ni gham”: pretty soon your street signs will be changed to another language instead of English!

“People don’t realize how conservative the Canadian banks really are in comparison to US banks.”

AFAIK Canadian banks force new home buyers to purchase mortgage insurance from the government. Consequently banks offload their risks to government, and therefore have incentives to issue mortgages to a maximum amount allowed by this insurance scheme. I don’t see how this makes banks conservative. The 50% down for plot of land is certainly conservative, but regular mortgage lending doesn’t seem to be. These banks issue million-dollar mortgages left and right; you can’t find any property in Toronto below $1M.

AK,

Fascist is probably a better word since they pretty much run gov policy up here.

When I mortgaged my first property in 1994, the loan sharks would only finance my wife and I if we paid $15K in mtg ins. on a $147K mtg. and we had to lock in for a 5 year fixed rate at 9.875%. I renewed for 3 years a bit lower and then paid it out in full with the cash I saved because I was pissed off watching rates collapse from the Greenspan effect. After that I only paid cash for properties.

I say conservative in the context of comparing to the boom/bust schemes of US banks, especially during the lending spree leading up to the 2008 mortgage crisis. The Canadian market barely burped, our boomers were going on bus tours buying up Florida real estate.

I believe the requirement for mortgage insurance is based on the size of the downpayment; anything above 20% does not require mortgage insurance.

With most modern L/V ratios, loans secured by bubble or mania priced collateral aren’t conservative.

Good luck but the rule of thumb has always been land falls first in price and the hardest. It’s also very illiquid when it falls in price. I’ve bought and sold a lot of land right across the country dating back to the 1970’s.

Unless it’s prime farmland or timberland, or comes with mineral rights and there’s proven oil or gold or something under the ground, land is almost a worthless money suck. That’s why I laugh my ass off when I see postage stamp lots in the desert selling for 3/4 million. The only kind of person who pays that is the biggest sucker alive.

Actually, the emigration (not immigration) numbers spiked during Covid to 1970 highs – go figure?

Yeah this is a great point easy to miss, one of the ironies of the blind mass immigration policies in Canada and the US in recent years to solve “labor shortages” (read: reduce wages while driving up housing prices and inflation for real estate investors corporate purchasers) is that they’re ultimately self defeating. In fact they’re ironically turning out not to “solve” labor shortages, low birth rates or low regional populations (closing schools) at all. They’ve been finding in Canada for ex. that the short sighted high immigration policies of all the major parties are countered by ever faster falling birth rates for the population of Canadians born in Canada (Canada may well drop below Japan, at least in Anglo Canada outside of Quebec and the indigenous provinces).

Not only that but hordes of well-educated Canadians and Americans even leave the country and become expats themselves as mass immigration depresses their wages and makes it harder to afford a home. (On our work trips to Europe we’ve been running into many many more American and Canadian expats raising their families there–it’s getting easier to do if you can dig up ancestry documents, you can just go to the consulate and get citizenship right away if you have a great-great-grandfather in many countries, and even with issues over there most of the EU still sticks to the old idea of a home as shelter instead of investment, and even the rental properties are strictly controlled so rent stays stable and you can comfortably raise a family without worrying about the rent rising up out of nowhere with the next lease) So the extra immigration to Canada and the USA is offset by plunging birth rates and emigration of their most qualified young people, and what’s more the best educated and skilled people who leave are generally replaced with a population that doesn’t have the same skill levels or connection to the country. It’s yet another dumb neoliberal short term obsession that leads to total disaster for the country in the medium term.

You extol the virtues of rent control but it can backfire. We, Mom & Pop landlords, have just sold two rent-controlled suites on Vancouver Island. It is becoming unprofitable. The cost of municipal taxes, insurance, appliances, garden maintenance etc far outstrip allowable rent increases. We were not prepared to let it become a slum. We sold to a Chinese buyer who will live in one suite and put extended family in the other. The two existing, longstanding, tenants were given notice to vacate and must find elsewhere to live.

I would say the cheap borrowing costs are the major driver. When it comes to things like supply, people have made that case for years, by people I mean investors and especially RE agents because many are in that game too. The reality is, if you have around 20% multihome ownership rate that means a massive chunk of your demand is speculative and yeah cities have failed to meet that demand. It is up to each person to decide whether the problem is on supply side or demand side. Me personally I say more on demand side. If a city like TO can have multiple years leading every city on the planet in new Condo projects being constructed at any given time then how much faster would they have to build to “fix” the supply side? IMO that’s ridiculous and mostly scapegoating, it was the same the previous run up when everyone was blaming “foreign investors” while domestic investors accumulated 10-20 properties. BTW there’s firm out of TO, can’t remember the name but it can be Googled, that a year or so ago invested $1B into RE, it isn’t a Chinese company.

Yeah totally this. The central banks and Fed in particular knew what they were doing with ZIRP and QE, they wanted a housing bubble and they got one, not realizing the scale of the societal damage it would cause. The fact that QE involved explicit purchases of MBS like Wolf has talked about is proof positive of it.

The rich Chinese came to Canada in 2015 and 2016. If you look at the charts of home prices in America and in Canada you’ll see the affect the Chinese had on prices from 2015 onward. It certainly wasn’t wages or disposable income. In fact price rose last month in Markham. The Teranet index is backward looking in time. Home prices peaked in February in Canada. In one third of Canada population wise you can’t find a studio apartment for under $450,000 Canadian. In Edmonton resale apartments were selling for less than most used cars last year in the $35,000 range Canadian. Over 3 dozen of them sold right around $35,000. None were leaseholds. The same apartment in Toronto would be about 20 times that in 2021.

It was certainly true then, though right after that, China introduced some of the toughest capital controls in modern history that have made it much much tougher to do that, and since then it’s been mostly domestic purchases. Even the Chinese who went earlier have more and more had to return home when they haven’t been able to secure ongoing funds (or moved their money to other real estate destinations like Brazil, Malta or even South Africa). What’s interesting is that the Chinese capital controls in this case were helped by policies in British Columbia province esp that began to more harshly target and penalize the foreign investors trying to park assets there, with the rest of Canada gradually starting to follow. This is one of the few cases when whatever their differences elsewhere, the Chinese government and Vancouver began to see eye to eye and in agreement with the people living there. Just about everyone hates the money-launderers and foreign real estate “investors” who buy up mass housing only to leave it unoccupied and drive up home prices further making it impossible for even high earning locals to rent or buy, other than the money-launderers themselves and a few corrupt local officials who were on the take. So there was a rare case of almost full agreement on all sides on policies to make it tougher for money to leave China, and tougher to invest in real estate too.

Yes, the Yuan dropped somewhat beginning in the summer of 2015 and the CCP immediately began impossing capital controls.

Since about the summer of 2017, Chinese buyers have disappeared from the Metro Boston housing market and – as far as I can tell – they have not returned.

Foreign investment for one – Chinese buying safety deposit boxes in the form of canadian housing.

Also, locally, near zero interest rates combined with a 2k/month stimulus to every man, woman, and child in the country for 2 friggen years straight because of covid.

The media will tell you every reason under the sun except the Chinese had anything to do with it. They don’t want to offend the money launderers in case they lose them by insulting them.

Ironically at least in an up market the more supply that comes to market the higher prices go and I mean exponentially higher not just higher. All of it is new stock which would be snapped up and even flipped all in the same span of a couple of hours of the sales office opening.

The more supply the higher prices go and I mean much, much higher. It’s not anything like in America.

The global Feds are helping extend the “housing shortage” due to the unintended interest rate manipulation consequence called the “Golden Handcuffs”, explained by WSJ below:

Homeowners with low mortgage rates are balking at the prospect of selling their homes to borrow at much higher rates for their next homes, a development that could limit the supply of houses for sale for years to come.

Housing inventory has risen from record lows earlier this year as more homes sit on the market longer. But the number of newly listed homes in the four weeks ended Sept. 18 fell 20% year-over-year, according to real-estate brokerage Redfin Corp. That is an indication that sellers who don’t need to sell are staying on the sidelines, economists say.

Millions of Americans locked in historically low borrowing rates in recent years when the Federal Reserve kept short-term interest rates low. As of July 31, nearly nine of every 10 first-lien mortgages had an interest rate below 5% and more than two-thirds had a rate below 4%, according to mortgage-data firm Black Knight Inc. About 83% of those mortgages are 30-year fixed rates, Black Knight said.

My take from Toronto:

1) Chinese and Iranian exiled money parking

2) Low borrowing costs and unrealistic bank-approved mtg. amounts

3) Gov. propaganda to Millennials: you must own a house if you want a family. Lie, borrow, and steal, get downpayment from parents, buy, buy, buy.

4) RE & investment industry propaganda: RE prices only go up. Look at the past 30 years. Wise investment, young lady/gentleman. Pat yourself on the back. You are a “have” now.

5) Historical norm for 80% of Canadians is to own a house. Habits are hard to shake off.

6) Young people don’t know the art of critical thinking.

My wife is a Millennial, and most of her friends are $million in mtg. debt, living like dogs, no car or driving ’02 Civic, no juice for kids/water only… One professional pair bought a shack in TO, tore it down, start building the new one, now live in the partially built house, parents help, but it’s been years, and they are $100’s K underwater, with things getting worse every day. “Too much television got me chasing dreams”. Everybody’s builder now.

Hamilton is a heavy industry city, which stinks to high heavens, like something ripped straight from the ’70s. All it has is a decent train connection to Toronto, so it’s only 3 hours to get to work and back.

I work with IT contractors from the Ancaster/Dundas areas.

They’ve told me there’s been no Chinese buyers in the market up there for at least the last five years. I have never asked them about Iranians.

However, they did say that there has been an *immense* surge of investment buying from India starting from about the time of the 2016 demonetization experiment up until the present time. India’s currency has been sinking for years and that’s motivated a lot of wealthy folks to invest money overseas. India dispensed with most of its capital controls in the late 1990s – so there are few restrictions on moving money overseas from there.

The direction is promising but those indexes are still insanely high. There is a looooong way to go before even the pandemic premium is removed.

Agreed. Probably at least 50 percent and more like 60 to 70 percent drops in the values for the bubbliest markets in Canada and the US housing bubble. A long way to go, and just like in 2007 and 2008, it’ll probably be another 4 to 5 years before we really see a bottom. Until then, any “value-purchasers” will only be trying to catch a falling knife.

I thought the Canada had a system of Mtg rates that are adjustable maybe 1-5 year reset. So if folks can sell at the higher price they can then not be paying a much higher interest rate on a house worth less in a couple of years and the real inventory of homes for sale comes alive

So far this year, over 50% of new mortgage originations have been variable, a historically high figure. Other mortgages are fixed rate, typically for 2 to 5 years, after which they adjust and 25% of mortgages will reset this year.

Variable rate mortgages are stress tested plus 2.25%, and fixed rates are stressed plus 2%.

The front end loading were seeing could come back to bite!

I forgot about the short mortgage durations. That is going to kill the market. Better to sell out quickly than to get hit with a large interest rate reset. That will given an incentive for sellers to lower those prices.

I was sorry to hear about your passing. Have a good day!

I swear there was a comment posted by a “gorbachev”.

Must be losing my mind. Wolf?

Toronto person here. A friend sold a townhouse previously priced at 1 million in December – matching two recent sales of similar homes – for $1.4 million in March. Point is the spike in March/April was crazy. The recent drops mean nothing if they are compared to the spike. When the prices drop 10 or 20 percent below December’s price only then would I feel sanity has begun to return.

Prices peaked in February in the greater Toronto area. They did peak slightly later in Toronto.

I noticed a huge spike in prices in many high-demand areas in the early Spring (Mar/April/May 2022). It’s hard to identify where that demand suddenly come from. The stock market was dropping around that time, so maybe people were pulling money out of stocks and throwing it at RE.

Or, maybe the price spike triggered peak FOMO, thereby feeding on itself.

In any case, the early Spring period was completely nuts. I hope economic justice is handed to these ridiculous speculators.

The Bank of Canada has to hike some more. The home prices are still waaayy unaffordable.

Canadian real estate has to crash in order to correct unfortunately.

The inverted yield curve on our 3 year/1- year (3.747 / 3.114) is spread 63 bp.

The BOC rate is 3.25% (same as the Fed)

The ECB is only 1.25%

I’m surprised our yields are this low with recent QT !

Seems like manipulation. The mortgage industry relies on the 5 year bond which is criminally low compared to the 3 month, 6 month and 1 year. Something is not right.

Looks like bond traders don’t believe that inflation will stay high for longer than a year or perhaps two. Seems like they continue sticking with the “inflation transitory” or “central bank pivot” narratives. My general impression is that apart from Wolf and central banks, nobody takes inflation seriously.

Inflation is eating healthy away my savings. It’s also criminal that property-owning rentiers are apathetic to the plight of the middle and working classes. They are bearing the brunt of the food prices, insane rents and skyrocketing insurance costs.

Good thing that Toronto Police are paid a billion dollar budget to kick down homeless people in their destroyed tents. That will solve the homeless problem due to inflation /s

I hear you, and I am fully sympathetic to your plight, but I suspect that things will remain this way until Canadian housing market totally collapses, and brings decades of deflation (like Japan).

The working class wishes for the housing market to collapse because the gains in real estate are seldom taxed, yet working an extra job to pay the rent for the REITs result in higher taxes.

Canadian real estate has to collapse to stave off potential civil unrest

Too many Canadians boast that their home prices tripled when they bought it in the 1970s while the working class pay rent or live in a tent. Oh wait, the police would kick people on the ground. Not even dogs get kicked like that in Canada.

Lived in Toronto ALL my 69 years and counting. Torontonians think everyone wants to live here. They think Toronto is like New York, London, Paris, all of which are more expensive. So, if we’re as good as they are, we should be just as expensive.

The problem with this thesis is that Toronto is not, and never will be, London, New York, or Paris. The last 15 years have been insane, and notwithstanding Canada’s homegrown reckless fiscal and monetary policies, massive immigration has been a factor. Toronto is growing massively in population. People like living here, and I get that. I support that.

But there’s going to be hell-to-pay, obviously. Pure speculation (no pun intended) on my part, but I believe the “root” of the problem goes back to the madness that started with the Fed’s answer to the meltdown of 2009. Endless QE and fiscal madness, which did very little for the average American (or Canadian), has brought us to where we are. Bubbles everywhere.

Only NOW, at this critical juncture, is the Fed acknowledging that they didn’t know what the outcome of kicking the can down the road would be. They didn’t expect that weird economic phenomenon called “inflation.” And they actually don’t know whether they have the tools to deal with it. But we have historical precedents, don’t we? By all rights the painful cleansing of the system that OUGHT to have been managed back in 2009 was postponed. Now the problem is MUCH worse. Much, much higher US debt now PLUS uncontrollable inflation. Not good.

“Endless QE and fiscal madness, which did very little for the average American (or Canadian)..”

I beg to differ. About 70% of Toronto residents are home owners, and every homeowner benefited tremendously from all these years of ultra-easy money. Buying $500,000 CAD home in Toronto suburb and then watching it appreciate to $1,500,000 over 10 year period, without any effort on your part whatsoever – who wouldn’t like that !

So this long era of easy money had a lot of support in the population, in all age groups. Perhaps a majority of population loved and fully supported this.

But will they love it when it plunges back down to 750K?

The problem with bubbles is that they break and cause alot more carnage than if they were never blown in the first place.

25% of these happy home owners may end up very unhappy:

https://www.manulife.com/en/news/buyers-remorse-manulife-bank-debt-survey-2022.html

…“every homeowner benefited tremendously from all these years of ultra-easy money”.

Important to note that easy money did not contribute to increased Canadian home ownership. That percentage has remained constant for some time.

WR’s graphs show that you would have “benefited” IF you purchased in the right city and AT THE RIGHT TIME, ie BEFORE the meltup.

Much will depend also on whether we’re in for a Japanese-style real estate meltdown, or whether the “readjustment” we’re now witnessing is limited in scope and the bubble remains permanently inflated.

In other words are the gains on paper only?

Last but not least, with increases in income not being commensurate increases in RE values, many new homeowners will be burdened with outsized mortgage payments for years. Not sure that’s a benefit. Again, much depends whether RE values hold up. Still, many homeowners may realize that they got ripped off, paying far more than they should have.

The US credit cycle from 1981 appears to have ended in 2020. I’m not sure about Canada’s but it can’t be much different.

If the cycle ended in 2020, rates are destined to “blow out”. The actual fundamentals are far worse now than 1981 at the peak even though rates are much lower now, it just isn’t visible yet but will be obvious years from now.

If the rate cycle turned in 2020, then the real estate bubble is done with it. I can anticipate that the government (both in Canada and the US) will attempt to prevent a hard crash landing and one or both may succeed temporarily.

The long-term outcome won’t be any different.

Most of the population probably did support it because they are economic illiterates and gain psychological comfort from increased paper wealth.

Most of this wealth is destined to ultimately evaporate.

Like your comment.

RE in Pac NW US has been going up rapidly last 5 to 10 years. Rents too… hence more economic related rent evictions. Portland, Oregon got pretty nasty a few years ago (Portland Tenants United). Enough conflict that the Oregon state government passed a limited gorm of rent control. It joined California and perhaps one New England state (Vermont ?) in doing so.

PBS, supposedly a liberal TV network, almost never covers this in their Newshour. Democrats had next to nothing to say about housing affordability in their 2019-2020 debates.

Why ? My guess is they didn’t want to offend homeowners. To heck with the poor, let them go homeless, all I care about as a politician is middle class votes.

Caveat: yes in the Midwest and parts of the South it has only been the last 2 to 4 years that RE appreciated a fair amount.

But in the Rockies and to the West the large RE appreciation has been going on for at least 7 years.

Some Democrats addressed affordable housing in their websites but as I stated I never heard them speak publicly about it.

This REALLY bothered me.

I searched the transcripts of the 11 Democratic debates for Affordable Housing discussions. In the Atlanta debate a question was raised about AH. Three candidates put in their two cents.

Beyond that there were only brief sound bites here and there in the other 10 or so debates.

This omission from the Democrats not the Republicans !

If Democrats could be so terribly interested in Medicare for all… why not more concern for affordable housing ? For the homeless ?

For investors buying up 18% of residential RE in the US in 2021 (33% in Atlanta) ?

I no longer consider myself a Democrat, Independent instead.

We have Camp Hope in Spokane, WA. About 600 to 700 homeless folks. I genuinely believe the city council members are trying to come up with a solution of sorts to this situation.

But its not going that well.

If builders had provided some homes in the lower to mid price range maybe there would be fewer homeless.

Nikie Johnson had an excellent article (Pasadena Star, don’t believe she is there now) in late November 2021.

It aptly demonstrated how builders were heavily focused on the high end market

in California with very little built for the low and mid segments. Oakland area may have been a rare exception to this.

Randy, I admire your compassion. Nothing raises my ire more quickly than a politician claiming to care about affordable housing. I have restored 8 homes in a fairly poor section of tidewater Virginia, USA. Every year, the friction and cost goes up. The state comes up with new and expensive code additions, transfer taxes, and regulatory issues. These become mandates that trickle down to the county level and the threat of witholding funding compels county permitting agents and inspectors to become the spearpoint to force compliance. The political class could care lsss about affordable housing.

I’d say the *real* madness started with the LTCM bailout in 1998.

As for “reckless fiscal” policies and the like…

a) Canada’s Debt-GDP is about 54.6% – which is not very big.

b) Even if the SHTF, Canada has lots of stuff (read: energy, natural resources) that it can trade with the rest of the world to get by.

The Hamilton chart is crazy. How did the bubble ever get pumped up that high?

I can understand Toronto, Montreal, and Vancouver to some extent, but Hamilton is traditionally a steel town. Sure, it has managed to diversify into healthcare and education (not unlike Pittsburgh), but I’m not understanding what is driving people to spend crazy amounts of money to live there.

They don’t view buying home as “spending” money, they view it as a sure-fire way to earn fat returns, and quickly. It doesn’t matter where these expected returns come from – Toronto or Hamilton or Whats-its-name, as far as “investors” are certain they will get into the money. Could have been tulips or anything in Wolf’s stock column, same mindset.

It certainly isn’t the weather….

Could be worse: Buffalo (unless you like massive snowfalls).

John, look at a map! Hamilton, Ont is only 50 miles from Buffalo. The heavy lake effect snow is mainly south of Buffalo, northern suburbs and Niagara Falls have about the same snowfall as Hamilton. Bonus, the housing prices are much cheaper in Western New York than they are in Canada.

It’s about the furthest town west where you can actually drive to Toronto and back. Barrie to the north and Bowmanville to the east are the same. Burlington also had a huge runup. Hamilton *was* one of the last places where first time buyers could actually buy and commute to Toronto to work.

Paul, Hamilton is almost at the Western end of the GO Train line (called Lakeshore West) that runs to Toronto — there’s some partial service out into Niagara, but Hamilton is probably the furthest stop on the western line that is practical for commuters. Lakeshore West used to terminate in Burlington, and the recent extension is a huge factor in the Hamilton real estate run-up.

I lived in Hamilton.

Economically depressed region, with homes going for half what they would in the rest of the Greater Toronto area. There was always room for a significant price hike in the housing stock there. The problem was, no one wanted to live in Hamilton. They’d rather pay an inflated price for a Barrie or a Milton, Ontario, house than move to “Crackilton.”

Still, when you start from a low price base, double digit gains look impressive. The houses in Hamilton started very low in value and now have achieved modestly priced status. It should remain that way for a while longer.

Yep. Everyone has a choice where to live. If they choose to buy a house in Toronto then they know the house will be expensive so they should not complain. There are affordable areas to live. Maybe a big company should just create their own company town in a cheap area. I think I read some companies in Texas where building their own subdivision that only their employees could rent or rent to own.

Anyway, all those charts housing charts in this post look just like M2 Money. Why is everyone so surprised at these prices. This is what happens when you print a lot of money. Inflation of assets.

Things that are finite have the same charts such as stocks, houses, land, rare baseball cards, rare comic books, rare cars, rare art, superstar football player salaries, etc. All these charts have the same parabolic pattern.

“Things that are finite have the same charts such as stocks, houses, land, rare baseball cards, rare comic books, rare cars, rare art, superstar football player salaries, etc. All these charts have the same parabolic pattern.”

Except that everything that you listed is inflated by a bubble or a mania.

There is a huge sports bubble and has been for years. It starts with inflated media rights contracts which is only possible because of the fake economy where mostly public corporations waste money on inflated advertising rates.

Inflated media rights contracts along with inflated ticket prices inflate franchise values and player salaries. When the mania ends, most of these inflated values and prices will collapse.

Of the objects you listed, only art is or may be actually rare. The others only on occasion, being usually mass produced. Any supposed “rarity” is usually just more financialization and marketing hype. These values are also destined to collapse when the asset mania ends.

How do newcomers to Canada feel that they are being used to create artificial demand for Canadian housing?

Canada has a dismal birth rate because the cost of housing is so high, but the oligarchs depend on newcomers to work the dead-end factory jobs to make the rich richer.

Who in their right mind wants to work for $15 per hour while rent for a studio apartment is over $1500 a month? That is modern day serfdom.

The world is wealthier than ever. According to McKinsey’s report, global assets grew from $440 trillion (approximately 13 times GDP) in 2000 to $1,540 trillion in 2020, while net worth increased from $160 trillion to over $510 trillion.

As of March 31, 2021, there was nearly US $2.1 trillion in circulation, including Federal Reserve notes, coins, and currency no longer issued.

If you are looking for all the physical money (notes and coins) and the money deposited in savings and checking accounts, you could expect to find approximately $40 trillion. This figure represents only ‘narrow money.’

However, if you add the ‘broad money,’ the amount rises to over $90.4 trillion. This amount further increases when bitcoins and other cryptocurrencies are included.

Money in the form of investments, derivatives, and cryptocurrencies exceeds $1.3 quadrillion. This is what it looks like written out: $1,300,000,000,000,000.

Derivatives aren’t money where the notional value of a contract can be compared to other debt instruments or shares. That’s your $1.3Q. Besides, it’s just someone else’s debt subject to default.

Same principle with most of this “wealth” McKinsey quantified. It’s mostly someone else’s debt and where it isn’t, substantially (absurdly) overpriced stocks and bubble priced real estate.

The wealth you describe applies to individuals but not collectively to a society or the planet. Rising asset values or increasing debt doesn’t make any society wealthier as it has nothing to do with actually producing anything.

Most of this wealth is ephemeral, as all financial values are abstract with no tangible connection to the physical world at all. That’s how it’s possible to have these absurdly inflated asset markets.

You or I can convert it to tangible wealth as individuals, but more than a tiny fraction can’t be converted at anything close to current value collectively in close proximity, as the actual production doesn’t exist to accommodate it.

Dividing $1.3Q USD by 7B (population of this planet) gives $185K to every human being living on this planet. There are 100M people in Ethopia, and each one of them has $185K, per McKinsey. How absurd is this ?

Well, part of the article I did not paste said the combined wealth of the top 26 wealthiest people is more that the combined wealth of the poorest 3.8 Billion people on earth. Hard to imagine they hold more wealth than 1/2 the people on earth. That is why this class push Governments to give out food stamps, etc. 40% of Wallmart workers receive some type of Government entitlement. Without those government entitlements, you would have a bunch of workers working for one of the riches companies in the world that would be hungry and homeless and angry. As Mark Blythe has been quoted, the Hamptons are not defendable.

I think any Billion dollar company employee should not receive any entitlements. That would make the company pay a living wage.

It is hard to imagine but Kings and Queens used to think they were wealthy but they cannot hold a candle to todays richest people. Kings and Queens used to have to build forts and castles and hire armies to protect their wealth.

Eliminating or reducing social entitlements wouldn’t make any large company pay a living wage. That’s not how economics works. It would dramatically increase the labor participation rate though and make wages even lower.

Now, sealing the border and banning people from working who aren’t here legally from being hired, that would go a long way toward accomplishing what you describe because it would end the intentional dilution of low-cost labor’s bargaining power.

Wealth defined by me:

Tangibles in your possession which have a use or intrinsic, extrinsic value.

Nova Scotia is bonkers!

Is it possible that is due to New Englander’s finding a – not too far away – spot with an affordable RE market (3 years ago) to dump some cash into? Especially the way New England prices are?

Pure speculation.

I’m not knowledgeable on how Canada treats non-resident RE buyers. I’d imagine the door is open if you have money to spend?

Also, if secondary and investment housing is allowed, that may have contributed to these housing chart “ramps” and might result in a minor “walk-away” scenario like the US if the knife keeps falling?

Does the secondary mortgage market work similarly to the United States? Bank package the mortgages and sells them to BoC? Or are their other a variety of buyers there?

More to research.

Sorry. …are their a variety of….

Wolf, I don’t know if the equivalent data exists for the same type of charts you show above, but a comparison with the late 80s boom and 91-93 housing crash in Canada will probably give a good indication of what’s coming in the next couple of years here.

A non-economic factor that hasn’t been mentioned is the increasing attraction of Canada as a place to move to and invest in property vs. the United States. Correct or not, the U.S. is now viewed by many in the world as a ghastly place. (Gun violence, unlivable big cities, social strife, and even now questionable political stability, etc). Educated Asians, Europeans, etc are increasingly choosing Canada and Australia over the U.S., which will continue to be a positive catalyst to some degree.

Agree Neil, to many from Asia and Europe, the U.S. looks like a dangerous place to live, btw, to me too, so Canada becomes their first choice.

Fwiw, my realtor says prices in burbs declining much more that city center, talking Toronto here.

In small community I now live in, the fees paid to town before the first shovel goes in, keep mounting, pushing house prices up; used to be approx 35k, now, can’t verify, approx 100k, incl water/sewer hook ups etc.

As to inflation, disagree Wolf, think we will arrive at new cost plateau, sooner rather than later, and inflation will drop to 2 -3.5%, because of recession…thus lower demand, more people available for work ( need to supplement retirement) and more unemployment, cheaper imported goods, export decrease, fuel price decreases etc etc….all result of higher interest rates….and the speed of the interest increases and of QT are an economic ‘shock and awe’, intended to get it all happening at double quick speed….I’m guessing 12 months from now.

However, because inflation slows to near ‘normal’, does not mean that base input prices ( save fuel ), will go down…so building a house, apt, will be more expensive than in 2018 by a margin, and thus house prices will not ‘collapse’ as some here hope, they will decline, but hold at levels still somewhat above 2018 levels.

All just imho.

The number of Europeans coming to Canada are like one drop of water in a 10 gallon drum of water. The word on Canada has been out for a long, long time.

Wow – just wow.

4% in 1 month is HUGE. More than 38% drop annualized for GTA.

5.8% in 1 month is catastrophic – 51% annualized drop for Hamilton.

If sustained for a full year, these drops would wipe out the pandemic era gains and then some.

I know “nothing goes to heck in a straight line” but price declines as are as likely to accelerate from here as they are to moderate.

4 percent sounds huge but when you consider how much everything spiked in January to March it’s not huge. It’s just wiping out the insane spike. Are we even back to December 2022 prices? I’d like to see about 6 more sinking months like that.

I live in Calgary and a house comes up for sale, it is gone in a few days. It’s oil money, and we don’t see the foreign buyers like we used to. As for the rest of the country, in a lot of areas where outsiders were moving in to buy what they saw as cheap properties, like Halifax, locals are happy to see the fall in prices. A big thing up here are adjustable rate mortgages which have so far sheltered/deferred interest rate hikes. We are heavily dependent on the housing sector here, so if this falls significantly watch out. Also, the longer these rates hold or go up the bigger the problem….

I find it to be a nice turn of events, just one step towards normality in financial literacy. For the last 10 years I have been told “if someone pays the price for something, then that is the correct value.” It was insane because they only used that logic to make prices climb, once you told one of these FOMO types the value isn’t going up anymore they would scoff and hold their ground because interest rates were near negative so they could afford to sit on it. Those folks have gone real quiet, if these interest rates hold for decades instead of years we will see a proper correction in the insane markets.