An ugly CPI print of inflation that’s entrenched and getting worse in vast parts of the economy. The Fed will have a heck of a time cracking down on it.

By Wolf Richter for WOLF STREET.

Gasoline prices plunged, but food prices jumped, prices of durable goods rose again, “core CPI,” which excludes food and energy, jumped, and prices of services spiked relentlessly as inflation has shifted from supply-chain issues and commodities to services. This process of inflation muscling into services started a year ago and has been getting worse every month for the 12th month in a row, a clear sign that inflation has gotten solidly entrenched, and is getting worse in vast parts of the economy, and that the Fed will have a hard time dislodging it.

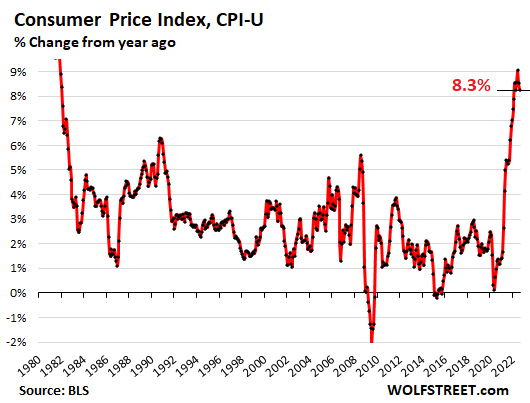

Overall inflation as measured by the year-over-year Consumer Price Index (CPI-U), released today by the Bureau of Labor Statistics, backed off a wee bit, but not nearly as much as expected, to 8.3% in August, from 8.5% in July, and remained in the ugly zone. On a month-to-month basis, CPI rose 0.1%, up from a 0% rise in July.

Social Security COLA for 2023 will be near 8.9%, one more reading to go.

The Consumer Price Index for “all urban wage earners & clerical workers” (CPI-W) backed off to 8.7%, from July’s 9.1%. The average year-over-year rates in July (9.1%), August (8.7%), and September (x%) will determine the COLAs for Social Security benefits in 2023. The two-month average is 8.9%. September’s CPI is going to be roughly in the same range, and the COLA for 2023 will be in the 8.9% range, up or down a little.

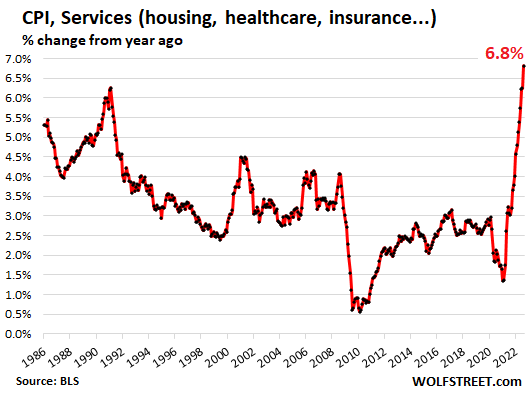

Services Inflation spikes straight up.

The CPI for services spiked relentlessly, jumping by 0.6% in August from July and by 6.8% year-over-year, the worst increase since October 1982. This is now the driver of inflation, it’s a huge part of the economy, and it includes the housing components of CPI, and it’s a nightmare.

Many services have little or no contact with commodities: Insurance, rent-based factors, education, healthcare, etc. Only a few services are impacted by commodities, especially fuel costs: airfares, other transportation services, utility services, etc. And that’s why a decline in commodities prices has little impact on services. Services inflation is the worst kind of inflation.

Service categories where CPI rose year-to-year.

These are the categories with year-over-year increases. Within them are some categories with month-to-month declines, such as delivery services and airline fares, which may indicate that inflation is shifting to categories that now have big month-to-month increases, such as health insurance, vehicle insurance, and vehicle maintenance. More on housing inflation in a moment:

| Services where prices rose YoY | MoM | YoY |

| Health insurance | 2.4% | 24.3% |

| Rent of primary residence | 0.7% | 6.7% |

| Owner’s equivalent of rent | 0.7% | 6.3% |

| Motor vehicle insurance | 1.3% | 8.7% |

| Motor vehicle maintenance & repair | 1.7% | 9.1% |

| Medical care services | 0.8% | 5.6% |

| Delivery services | -0.7% | 11.5% |

| Pet services, including veterinary | 0.6% | 9.6% |

| Airline fares | -4.6% | 33.4% |

| Hotels & motels | 0.0% | 4.5% |

| Other personal services, such as dry-cleaning, haircuts, legal services | 0.3% | 5.8% |

| Admission to movies, theaters, concerts | -0.6% | 6.2% |

| Video and audio services, cable | -0.3% | 3.2% |

| Water, sewer, trash collection services | 0.6% | 4.6% |

Service categories where CPI fell year-over-year:

| Services where prices fell YoY | MoM | YoY |

| Telephone services | 0.0% | -0.1% |

| Car and truck rental | -0.5% | -6.2% |

| Admission to sporting events | -2.8% | -6.7% |

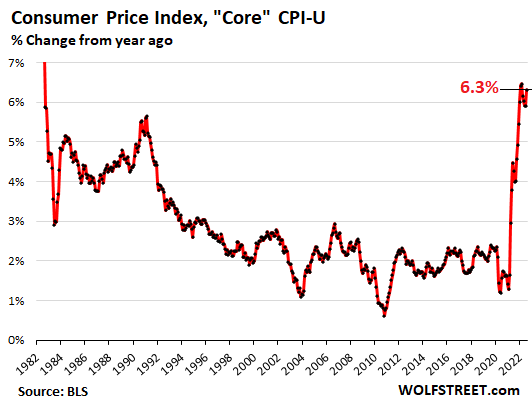

“Core” CPI.

The “core” CPI, which excludes the volatile commodities-dependent food and energy components, jumped to 6.3% on a year-over-year basis, and to 0.6% on a monthly basis. This index is design to measure inflation in the broader economy, and it will give the Fed the willies:

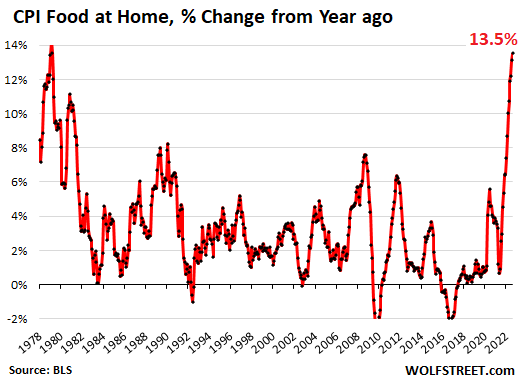

Food inflation worst since 1979, moving from category to category.

The CPI for “food at home” – food bought in stores and at markets – spiked by 13.5% year-over-year, the worst since February 1979. On a month-to-month basis, prices jumped by 0.7%.

Food inflation hits lower-income consumers the most because they spend a bigger part of their budget on food. Food inflation, along with housing cost inflation, are brutal for them.

Inflation cycles from category to category, letting up in some categories, and heating up in others, and you can see the shifting dynamics in the table below:

| Food at home | MoM | YoY |

| Cereals and cereal products | 1.2% | 16.4% |

| Beef and veal | 0.8% | 2.5% |

| Pork | 0.3% | 6.8% |

| Poultry | 0.8% | 15.9% |

| Fish and seafood | -0.2% | 8.7% |

| Eggs | 2.9% | 39.8% |

| Dairy and related products | 0.3% | 16.2% |

| Fresh fruits | -0.7% | 8.3% |

| Fresh vegetables | 1.2% | 7.6% |

| Juices and nonalcoholic drinks | 1.1% | 13.1% |

| Coffee | -1.0% | 17.6% |

| Fats and oils | 1.9% | 21.5% |

| Baby food | -2.0% | 12.6% |

| Alcoholic beverages at home | 0.5% | 3.2% |

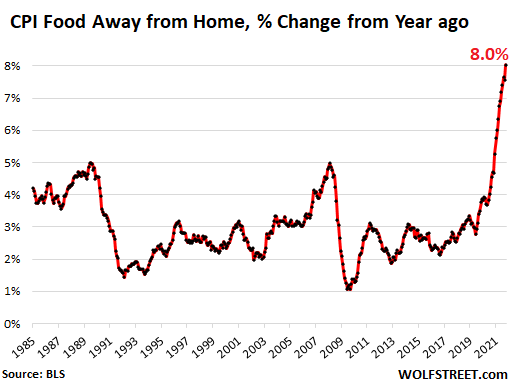

“Food away from home” CPI – restaurants, vending machines, cafeterias, sandwich shops, etc. – jumped by 8.0% year-over-year, the worst since 1981, and by 0.9% in August from July.

Within this category: Food at employee sites and schools spiked by 19.7% in August from July, which brought the year-over-year spike to 23.7%.

Energy plunged from July, but still up hugely year-over-year.

The Energy CPI plunged by 5.0% in August from July, on plunging gasoline prices. But natural gas prices have resumed their rise, and electricity prices have never slowed their rise:

| Energy | MoM | YoY |

| Overall Energy CPI | -5.0% | 23.8% |

| Gasoline | -10.6% | 25.6% |

| Utility natural gas to home | 3.5% | 33.0% |

| Electricity service | 1.5% | 15.8% |

| Heating oil, propane, kerosene, firewood | -2.4% | 48.8% |

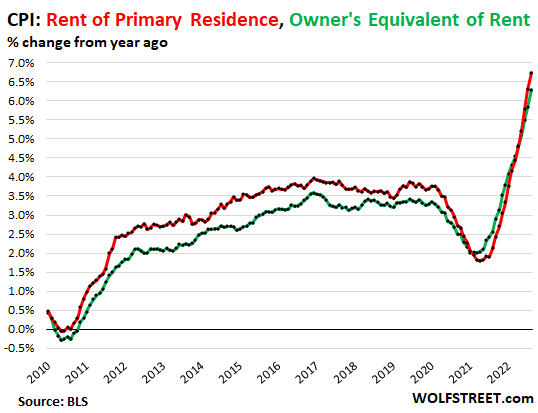

Housing costs surge: part of services CPI.

The CPI for “rent of shelter” accounts for 31.9% of total CPI. It measures housing costs as a service – “shelter” – not as an investment asset to be purchased. Its major components:

“Rent of primary residence” (accounts for 7.2% of total CPI) jumped by 0.7% in August from July, and by 6.7% year-over-year (red in the chart below). It’s based on actual rents paid by a large panel of tenants, including in rent-controlled apartments.

“Owner’s equivalent rent of residences” (accounts for 23.7% of total CPI) jumped by 0.7% for the month and by 6.3% year-over-year (green line). It measures the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for.

Both measures are still below overall CPI and are therefore still holding down overall CPI, but are holding it down less each month. And this is where a big part of the action is, going forward:

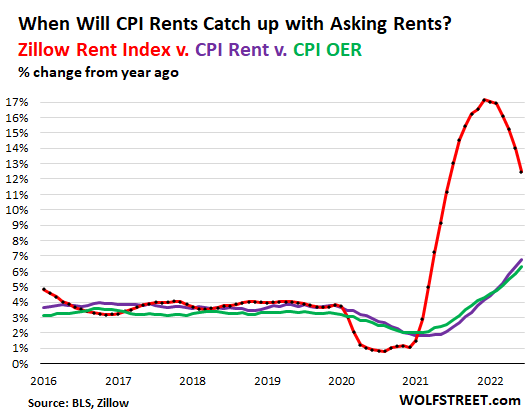

The “Zillow Observed Rent Index” (ZORI) reflects “asking rents” (advertised rents of apartments and houses listed for rent).

In August, the ZORI jumped by 0.6% from July, and by 12.5% year-over-year, to a record of $2,090. But those jumps were smaller than the prior month-to-month and year-over-year spikes, showing that rental inflation is somewhat less brutal than before, but still brutal.

Asking rents (red line) feed only gradually into actual “rents” paid and reported by tenants (purple line) and into “owner’s equivalent rent” as estimated by homeowners (green).

I discussed this lag and what it means for CPI in 2023 here. It’s pretty clear from the chart what this will mean for CPI in 2023, regardless of what asking rents will be doing by then:

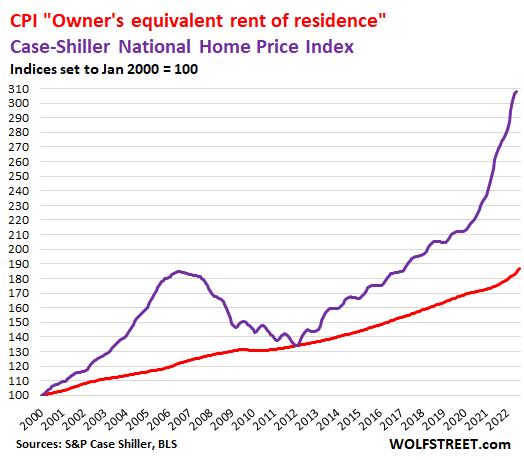

Home prices spiked by 18.0% year-over-year, according to the Case-Shiller Home Price Index (purple line below). The index lags reality on the ground by four to six months, but the first declines are just now cropping up in some markets, as documented in The Most Splendid Housing Bubbles in America:

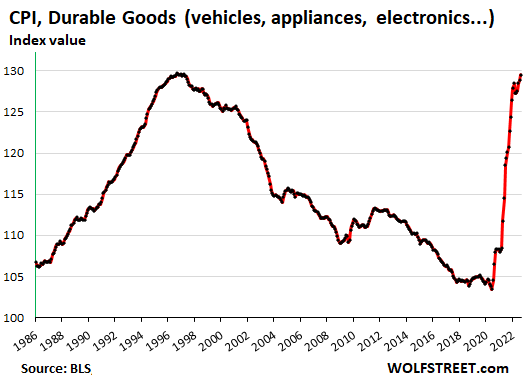

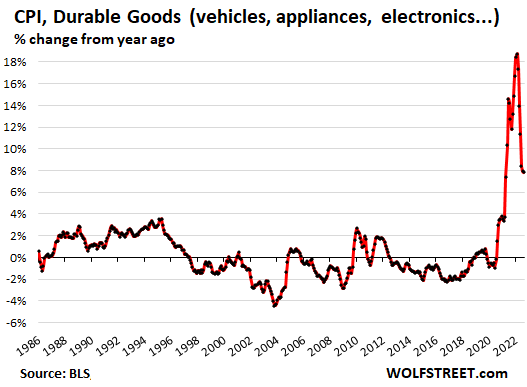

Durable goods CPI.

Surprisingly, the CPI for durable goods keeps rising, and rose 0.5% in August from July, the fifth month in a row of month-to-month increases, when durable goods prices had been expected to come down from the mega-demand-meets-supply-chain-chaos spike during the pandemic. But they’re not coming down; they’re still increasing but at a slower rate.

Durable goods include motor vehicles, appliances, furniture, consumer electronics, sporting goods, etc.

Inflation is supposed to measure how many dollars you have to pay for the same thing over time. But if the product is improved – more powerful, faster, more features, better safety, better fuel economy, more memory, faster processors, etc., “hedonic quality adjustments” remove the costs of those added improvements, with the result that many durable goods have negative CPI rates over the years.

Consumer electronics almost always have a large negative CPI. This makes sense as manufacturing constantly gets more efficient, lowering the costs of products, and only the added improvements cause prices to rise or, in many cases, drop more slowly, such as with laptops. This is a type of “deflation” that is natural and beneficial and should not worry anyone.

But these are not normal times, and the price spikes in new and used vehicles have by far out-powered any hedonic quality adjustments.

As index value: This chart of durable goods CPI as index values shows the long-term decline caused by hedonic quality adjustments and actual price declines (i.e. of laptops), and the current spike, and how prices are still rising but at a slower pace than 10 months ago:

Year-over-year, the CPI for durable goods increased by 7.8%, which is down a lot from the 18% range where it had been late last year and early this year, but still a huge increase.

Note the decline in information technology products, which is typical and has been similar before the pandemic:

| Major durable goods, August | MoM | YoY |

| New vehicles | 0.8% | 10.1% |

| Used vehicles | -0.1% | 7.8% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 1.1% | 10.6% |

| Sporting goods (bicycles, equipment, etc.) | 0.9% | 3.8% |

| Information technology (computers, smartphones, etc.) | -0.9% | -8.8% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

At Kroger store today, one can of Crisco shortening now $10.89. Over twice the price from 18 months ago.

Looking around the store, much the same on most items. There is no way inflation is as little as 8%.

I have a hard time finding any product that has only increased less than 20% year over year.

You saying the Inflation Reduction Act didn’t work?

Or BLS stands for something else.

let me correct name

Inflation PRODUCTION act

more appropriate

had usual at restaurant(hadn’t been there since June)

was $44 now $54

gonna have to cut down on SPLURGING

It worries me that we are 2 months from election and the inflation is so bad.

I wonder what will happen after election when politicians can again forget about us 99% and blow another bubble for the 1%?

Are we now living in an Era od not accountability?

That’s not how 10 year legislative acts work.

Mentioned how bad food and energy inflation was in a deli yesterday. The owner, an older fellow from the Caribbean who barely spoke English agreed. I was amazed at his indictment of the Fed.

Tentatively, I asked, where did you learn about that? “Woofstreet” Congratulations Mr. Richter, the word is getting out.

Then some old lady chimed in, “it’s Putin’s price increase!” The old guy said, “Remember madam, it was Biden who imposed sanctions on the cheap energy, food and fertilizer, not Putin.”

Going to be REAL interesting in 54 days.

Kim,

Thanks for the kind info on who’s reading my site. Love to hear that.

Let’s remember that it was Putin who invaded a European country and who is waging a brutal war on it to take the part of Ukraine that he hadn’t already taken in 2014. So should we just hand him Poland next? Offer him the former East Germany? Look at a map… this is pretty scary stuff.

There are big costs to a war. And this is a war. Thankfully, the Ukrainian military, with support from the US and Europe, plus the sanctions, and the incompetence of the Russian military have done a pretty good job at halting and perhaps reversing Putin’s territorial ambitions.

Also oil prices started surging in mid-2020. By Feb 1, 2022, before any sanctions, WTI was at $88, about where it is today. The charts are quite revealing.

Same here. Kroger’s been a longtime favorite and of course Piggly Wiggly and Food Lion for us folks down south, but the price jumps in the past year have been nuts. We’re trying to do without butter more and more, partially health related but dairy inflation has been even crazier than other things and esp. for butter sticks. Forget about TV dinners, instant oatmeal or anything prepared. We tried shopping around and we’ve done the Sam’s Club thing a lot but even they’re getting pricey.

Resorting to scavenging a few things here and there at the dollar stores, or of course Aldi and Lidl if we can find one wherever we’re traveling. The best kept secret may be the ethnic supermarkets tho, esp the Spanish supermercados that are all over Texas and Arizona (and SC, NC and Florida when we’re going through there). If you can find a good El Rancho, Super, Fiesta Mart or the other places the Latino neighborhoods shop at esp if it sources locally, you can often get a lot of the fresh produce and basics dirt cheap, even some of the prepared items esp if they come with a tortilla.

Unpossible.

The government leader told me inflation was at 0% just last month.

The numbers don’t lie!

When did the Pres say that?

On or about 10 August. A simple Google search will provide many results telling you about the president stating.

It is the typical political spin that is easily cut into sound-bites, but is ultimately untrue.

The problem is, as usual, that the politicians will pretend to care until November, and then continue enriching themselves or doing whatever they need to do in order to maintain their office.

I’ve noticed that Walmart is often 1/2 the price or less for the same item at the Kroger by my house. I think Kroger is just being greedy. As Smokey Robinson said, you gotta shop around.

Buy nearly everything at Costco. They try to hammer down the prices as much as possible.

Agree that there are some businesses that are just being greedy. I hope their customers develop new habits and it hurts them in the long run.

don’t forget SHRINKFLATION at wally mart

Coupons/Preferred shopper at Kroger are better than Walmart.

ie 3 12 packpacks of Pepsi for $11 at Kroger (With Card).

Pepsi is over $6/12 pack at Walmart (3 for $18).

Costco was doing a great job with whole bean coffee until last month. For the last 3 years, the cost of a 2.5 lb bag was $12 with the deal. Last month it increased to $14 with the deal.

I know, I should give up on caffeine.

Same as with Sam’s Club. And no, you should not. 😵💫

I would stop shopping at Kroger.

I already did except for loyalty coupons

Do what Tyler did in Fight Club, dumpster dive surgery clinics for lipo’d fat

Per this article, “Food at Home” inflation is 13.5%, which is substantially higher than 8%. I do all of our grocery shopping and I’m not sure if I fully believe even 13.5%, but as a national average it’s probably pretty close. I’ve certainly shifted the stores I shop at as a result of the price increases.

Bananas 31 cents ar wal mart ,really starting to like them

Still 19 cents at Trader Joe’s. Loss leader at this point I think.

Amen. Keep in mind that the “Federal” Reserve started creating more money than ever created in late 2019 and has continued creating dollars more until now, so that more and more dollars are chasing the fewer goods being produced now due to the covid lock downs in China, supply chain disruptions, etc. Inflation is great for the banksters and their cronies, so expect inflation to continue so the “Fed” can benefit them even more: salaries are effectively reduced at about 10% to 15% per year by inflation; same for their liabilities like bonds, accounts payable, defined pension contributions, tax payments, etc. Its steps to allegedly decrease inflation are puny and half-hearted as a result.

Also, there is no way, in my humble opinion, that inflation has been as low as reported for years: the GPI of the US and other countries has shown increases for years, which may be substantially lower if inflation were “properly” computed. (That has been part of the big con.)

I say “properly” computed, because computing inflation admittedly arbitrary depending on what goods and what percentage of those goods you count: e.g., food v. energy v. housing, etc. Going back years to the early 2000s, the “Fed” kept interest rates low and the computation of inflation has been dubious for many years: they altered the CPI, so Americans and other holders of dollars would not notice that the inflation was inflating away the banksters’ and their cronies’ debts, wages, etc.– because inflation has often been higher than the tiny returns that pensions and other investors can get from their bonds, treasuries, etc. Those low rates led to the 2008 subprime crisis: see CBSnews “Greenspan defends low interest rates”

You are obviously a bad shopper. I bought 2 slabs of ribs for $17. That is a deal even better than pre-covid. Potatoes are also dirt cheap…no pun intended. haha. Deals are out there. You just have to look. Don’t act as if prices weren’t high even before covid. You are just exacerbating the inflation with sticker shock.

I agree. I’ve used Walmart’s delivery service since it was rolled out in 2020. I have data and I actually went back and looked because I don’t believe these numbers.

For example, a 42oz container of quick oats went from $2 to $4 over that period. Same with instant pancake mix. $1 to $2. 100% inflation. Drinks, canned goods, snacks & chips are all up at least 20% across the board.

I think the “outside ring” of the store prices will ride the commodity market. But no one makes money in the middle of the store, from what I understand. I suspect those increases are forced on the stores and are sticky. A new world.

Fortunately, none of this affect us. We are cheap and buy all off-brand, but our finances are rock solid. How someone barely hanging on can cope is beyond me.

Those health care increases are insane. As someone who pays family coverage, these are brutal.

Concur. +24.3%! Ouch.

Where do you cut the budget to accomodate that size of increase, on a line item that is already excessive in cost?

Need to shop for car insurance again for cheater rates.

Djreef,

I want those cheater rates too 🤣❤

We tell the insurance company our annual mileage, rather than have them quote us *their* rate. My wife has an Acura RDX and I have a manual transmission Toyota Corolla. Total cost including both of us in California with $50K bodily injury, $30K uninsured motorist, Comprehensive with $100 deductible and Collision with a $500 deductible is $435 for 6 months, and I sent them the check 3 weeks ago, so that is up to date.

Jeez…

What about “underinsured motorist”? Because if you ran me over with that policy my medical bills would wipe you out. At that point you don’t actually have insurance since your policy fails to “insure” you against catastrophic loss (ie the thing that insurance is supposed to do).

Insurance is a rip-off industry, but on the other hand, buying the cheapest seldom seems like a terrific idea either..

Unless you have no assets to speak of those limits are dangerously low.

It seems to me that unless your bodily injury is $2M you are underinsured. So what’s the point?

I would be better off buying a separate $1 million umbrella insurance policy for $150/yr to pay for expenses if I get sued for the car, or anything else that may pop up in life.

They just need to put some health insurancee and hospital executives in jail for fraud, which is what the current billing system is.

Where are all the politicians when it comes to talking about this? Throw a couple crooks in jail and you get some pretty fast changes.

Umm, Obamacare is calling the shots now. Had to give everything to the Hospitals and Insurance companies to get it to pass.

The only entity committing fraud is the USG. Medicare and Medicaid essentially steal from the private healthcare system to give themselves the appearance of being cost-effective.

anon,

It’s funny, my parents divorced over 40 years ago. It’s hard to find two more diametrically opposed people when it comes to politics. My wife has said she can’t picture them together as she did not know them prior to the divorce. However, both have told me, as you said: “Don’t you dare touch my medicare or social security.”

I think it’s hopeful. Proof we can still find common ground.

Cytotoxic – yes the people that pay are paying for the people that dont pay, but i have to say that it is the cost structure that is insane.

Do you really think a 4 night hospital bill should total $180,000?

The hospitals dont even try to keep costs down. $500 for a doctor to come in for 5 minutes? sure that seems right to them, but not to anyone else.

Maybe if we paid doctors for cures and results we would get better healthcare. i dont pay the mechanic unless he fixes my car, right? Why do we pay doctors for “practicing” medicine?

I know! And what is the justification for this? I know I am going to get slammed for saying this but there should be a government insurance program that people can buy into – at least for major medical – and “doc in the box” clinics that are subsidised by the government where people can walk in and pay a reasonable fee (like $50) to see a doctor for 15 minutes.

In former Yugoslavia there was “free” healthcare too — that is why does not exist any more and we end up in Australia as immigrants.

There is no free lunch, that is socialist nonsense. If you do not pay cash — does not mean that you do not pay at all,

We have “free” healthcare in NZ, but good luck trying to get any of it. Average wait of 3 weeks to see a doctor, radiography appointments take months, and surgical waiting lists are now out to years. If you don’t have private insurance, you’ll probably be dead by the time you get treatment in the public health system.

lol at attributing Yugoslavia’s fall to its healthcare system, you think maybe there might have been other factors at work there? And as far as healthcare systems most of the rest of the world has some form of universal healthcare, in Europe, Asia and most other places, they get better health outcomes than the US in life expectancy, medical errors and everything else. (We actually spend more in the USA than any other country but get worse results) Now the issue I have is slapping that label of “socialist” and “free lunch” on there, it’s just a weasel-ish word that gets contorted to mean whatever the critic wants it to mean. I’ve worked in Europe and Asia and their healthcare systems work, some things are socialist and some things are capitalist, but their hospitals and treatments make sure everyone is covered, no one goes bankrupt from medical bills and they get good results much cheaper than the US. A lot of US healthcare is socialist too, but our healthcare system seems to combine the very worst parts of socialism and capitalism (we’re forced to pay in for it but can’t negotiate prices, and you can go bankrupt for exorbitant medical fees). There’s very little in the US healthcare system to imitate, we get the worst of the all worlds, can’t cover our people, threaten Americans with medical bankruptcy and make it harder to leave a job and start businesses, yet still wind up with the most expensive healthcare (both private and government spending costs) with the lousiest results.

Miller you can find this on wikipedia:

Following the death of Tito on 4 May 1980, the Yugoslav economy started to collapse, which increased unemployment and inflation. The economic crisis led to rising ethnic nationalism and political dissidence in the late 1980s and early 1990s.

the foreign debt grew at an annual rate of 20%, and by the early 1980s it reached more than US$20 billion.

In the 1980s the Yugoslav economy entered a period of continuous crisis. Between 1979 and 1985 the Yugoslav dinar plunged from 15 to 1,370 to the U.S. dollar, half of the income from exports was used to service the debt, while real net personal income declined by 19.5%. Unemployment rose to 1.3 million job-seekers, and internal debt was estimated at $40 billion.

In 1980 the unemployment rate was at 13.8%, not counting around 1 million workers employed abroad.

During the 1960s and 1970s the country’s social security expenditures increased 600%,

The government introduced extensive subsidies for public health care, temporary disability and illness, old age pensions and assistance to mothers. There were, in particular, a great number of social security benefits intended to take the pressure of child raising off women, making it easier for them to focus on studying and gaining employment. Women received 90 days of paid maternity leave after having a baby, a range of other subsidies to help pay for food, clothing and other necessities. There were also subsidised public childcare services that low-income families could use for free.

https://en.wikipedia.org/wiki/Economy_of_the_Socialist_Federal_Republic_of_Yugoslavia

+++ @Miller – that’s a ‘keeper’!

No no no no. The Free Market is working as advertised.

It would if we let it. US had mostly fine healthcare before 1965, then Meidicare/aid came and ruined everything.

The “free market” has been horribly infected with increasing corruption, manipulation and dishonesty. Unless we are able to tame these ugly human traits there will not be a free market. Trust is increasingly being lost.

Yep, there’s no real free market in healthcare when someone’s in a car accident or gets sick with covid and needs care right away, a customer isn’t in a position to negotiate prices there. Besides like you say, the problem with so many US free markets right now (not just in healthcare) is that they’re not even real capitalism or free markets anymore, it’s crony capitalism. I used to be libertarian and quote Ayn Rand myself but this is what moved me away–the ideal free market capitalist utopia always falls apart because soon the oligarchs take over and use their size and power to set up barriers to entry and make utopias that force exorbitant prices on the public. US healthcare, US universities (the student loan disaster) are among many examples, but the most obvious right now is the Federal Reserve at least until recently. Fed policy for 4 decades has been to do everything it can to make sure there isn’t a free market and price discovery for assets, thus the housing bubble and other asset bubbles we’re stuck in. Great example of rentiers and crony capitalists crying out against regulation and “for the free market” all the while they’re using their insider connections and political buddies to skew the market in their favor.

Come to Oregon and have no assets. Get on the Oregon health plan. You could pay almost nothing for decent health care. Much Harder to get housing and money.

It’s gonna be herbal medicine and chiropractors from here on out.

Second 1000-point down day in under one month. Yay!

And so begins the highly efficient process of selling crypto to buy electricity.

Ha! The circle of energy.

Yep, we need a reset, and it will come because it must.

What will happen when the administration slams shut the SPR valve after squandering most of it on political theater? Hope there is no natural or military emergency requiring the SPR!

Any bet that by June 2023, we will think about the ‘good old days’ of 2022 when gas was only $5.50 per gallon?

“Any bet that by June 2023, we will think about the ‘good old days’ of 2022 when gas was only $5.50 per gallon?”

Where I live gas is about $4.15 a gallon. But we’ve been conditioned now to see that as cheap!

Ours is under 3$ now. Paid $2.89 the other day.

You need to move.

For the first time in this last year, I began doubting my strong conviction of recurring high inflationary #’s. I made a bunch of $’s w/ calls on SQQQ these last months, but… yesterday while I still had a bunch of the SQQQ, I saw the risk-on trade happening these last few days… and w/ futures up a good bit this morning, I decided to hedge my bets by going a bit long TQQQ and shorting some SARK. The markets give out maximum pain and even though I covered right after the CPI was announced, I learned yet another expensive lesson.

I talked myself out of my core belief on inflation by starting to look at the day to day market action. Oh well, at least my SQQQ’s made up for the loss. ;-)

All this and Fed is still suppressing rates, and keeping it well in the negative territory. They will never raise rates enough to kill inflation because their real mandate is to inflate Stock, RE and Assets. Even if assets fall a bit in short term, over long time, asset prices will catch up simply with inflation.

Japanese stocks are low now than in 1989, about 30% lower. That’s 32+ years with QE much of the time. I don’t know about real estate but suspect it has risen that much.

QE will result in asset inflation somewhere, but where it goes isn’t controlled by the central bank.

As for the mandate, it’s to support the Empire, not inflate the value of fake paper wealth. It’s a bonus, not the primary goal.

Why isn’t US treasuries downgraded to junk as real returns for bonds is at least -5%. Oh yeah, they keep their investment grade rating under the threat of dismemberment! Obama admin decapitated the ceo of the bond rating agency that dropped America’s debt to AA and that was when the inflation and finances, though very dismal, were much better than today!

lol no, the value of all equities, real estate and assets goes to zero if rampant inflation takes over, the US dollar becomes even more worthless and blood starts to flow in the streets when Americans can’t afford a roof over their heads or food at the grocery store. The Fed knows this and it’s why no, it cannot afford to let inflation get uncontrolled–of all the threats to a country’s economy it is by far the most dangerous, the value of assets is a very, very distant lower priority. The Fed’s policy hasn’t been enough yet but JPow at least is a student of history, and he knows that inflation has utterly dismantled far more great powers and major empires than any war ever has. It’s jack up interest rates even higher and make QT even tougher, or watch the US dissolve in social unrest. The Fed either brings inflation under control like Paul Volcker did or the United States collapses as a viable nation, and with 400 million firearms out there in the US…

Wolf, as I have mentioned before, I have only been around here for about 4 months or so, SO I REALLY appreciated the link you posted here to a previous article you wrote in Feb’ 22. I found it incredibly informative.

https://wolfstreet.com/2022/02/15/when-will-the-brutal-spike-in-rents-drive-up-cpi-inflation-how-much-will-it-add-to-cpi/

…. It’s pretty clear from the chart what this will mean for CPI in 2023, regardless of what asking rents will be doing by then:

So for the recent additions to your fine site, please keep posting relevant links to previous pieces!

Thanks!

To find literally any topic you want in past wolfstreet.com try this in Google search box –

wolfstreet.com cpi

The search result came up with 60,000 instances. While that might make it worse finding something, you can further refine your search with additional word and date ranges. Other search engines work similar. The more you refine the more “on target” the results.

Excellent summation.

High inflation has also doubled the number of strikes and unionizing in the past year which feeds directly into the cost of labor generating more inflation, hence the inflationary feedback loop. Strikes that cause supply chain disruptions generate supply-side inflation of good and services.

Higher interest rates also increase the cost of living and in return higher wages are demanded.

If we’re lucky 1% monthly inflation is the new norm, not to mention our strategic petroleum reserves are being depleted to record lows.

I agree with most of your post, except that higher interest rates increase the cost of living. Wall Street and Corporate America peddles this idea, as they want perpetually cheap money, but I’ve seen little evidence that consumer borrowing rates (outside of mortgages) are impacted by the fed funds rate.

Higher debt increases the cost of living for most people. All except those who are on the receiving end of the interest payments.

It’s never free.

Right, but that doesn’t mean that higher interest rates increase the cost of living.

Higher interest rates keep costs down. Things like subsidies and insurance drive costs up for the underlying product or service. Anyyone who says differnently thinks of the world in terms of payments rather than price, which grossly distorts the market. People who think in terms of payments rather than price are the *real* problem driving America’s hyper-financialized economy.

PS People who insist on using log plots rather than linear plots — same mindset.

I’m observing the effect of higher interest rates from both a business and personal perspective. We haven’t the history to compare to our global modern digital economy that has evolved to be dominated by monopolies and tight markets with the ability to fix prices and governments that implement capital controls to protect the interests of the bankers.

I believe we are entering a new economic age where the opportunities to reduce costs through productive innovations is severely diminished.

The Feds fund rate is trailing behind the real cost of risk to lenders in this global debt trap and geopolitical conflict. The real rate and liquidity available to consumers is driven by the commercial banks assessment of risk.

When businesses and governments have to pay higher interest rates, they are passing on this cost to the consumer in the price of goods and services they provide and through the financing they provide for the monthly club. Aside from massive defaults forcing a liquidation of assets, I don’t see any other significant deflationary mechanics to offset the cost of higher rates since globalization has hit the wall.

When I study my balance sheets, I’m hard pressed to see how rising interest rates will stop inflating the costs of almost everything I consume in my manufacturing plant and personal life. What I do see is demand destruction that converts into less product and quality for the same money, or rising prices, or a mixture of both. I don’t think we have even come close to realizing the actual cost domestic production needs to be in order to balance our consumption with the resources we have.

“productive innovations”

I prefer the pet name, “smoke and mirrors”.

With all the leverage in our system, I have no doubt that The fed increasing rates will lead to demand destruction, and eventually a reduction in the inflation rate.

I agree with your point on domestic production costs — interest rates are only a part of the total costs. We also are on a De globalization trend, which is inflationary. Tariffs, re shoring, sanctions, and reduced domestic oil production are a few of the tailwinds behind the de globalization trend. If we see a weaker dollar how is that going to impact our domestic production costs?

Einhal,

You make a good point because its really more about the liquidity then the rate and this I should be more clear. My understanding is that the massive amount of loans denominated in US dollars will increase the cost of living as these loans reset with higher rates and bailing out insolvent companies and governments only worsens inflation and the consequences of a correction.

Great overview Wolf, as always! Services inflation is surely not ‘transient’!

Utilities is going to take a bit out of the economy as we get into the winter, no doubt!

I had a feeling that the CPI would be higher than expected. Inflation has moved into services sector and the lower gasoline prices narrative was a ploy by Wall Street crooks to spark another suckers rally.

Commodities may fall further but services will continue to surge due to massive increases in housing, healthcare, insurance of various kinds, and other costs.

Have you eaten at a restaurant lately? Have you had your car fixed? Have you had your house fixed? Separate the material costs from labor on your bills and you will see what I mean.

The situation has moved beyond the Fed’s control and Powell knows it, especially with Petrodollar under attack with China officially paying for Russian energy in Rubles.

My business insurance policy runs from September to September so I recently had a new policy proposal from my broker. A mere 25% increase YoY. Never had a claim and always pay upfront at the beginning of the year. I ended up going to a different company at almost half the price but I am no longer covered for some jobs that I normally would consider doing, oh well.

10-year yield at over 3.4% today. Looks like unhinged market optimism over a looming fed pivot has evaporated for the time being. Low unemployment and low credit card balances suggest there’s still some breathing room in face of entrenched inflation, however. Just enough spending power left for a booming holiday season then a collapse afterwards?

I’m figuring 80% chance of 75bp hike and 20% chance of 100bp at this month’s Fed meeting.

So you’re parroting what everybody else is saying. Got it.

Depth Charge: I am figuring only what J-Pow and company will likely think is appropriate to do. This doesn’t say what *I* think is appropriate to do here if I was Fed chair.

You Toucan do it! 🦜

I’m sorry to inform you, phlegm, that I don’t take orders or listen to narcissists. Now go order somebody else around, boy.

Phleep

DC is just insanely angry at everything.

Can you imagine what it would be like to hire him as a contract carpenter? Ranting and raving as nails and lumber fly in all directions.

And what will that kind of interest rate hike do in the face of this inflation? My guess is probably not much.

And once again, another speculators’ bullshit narrative blows up in their faces. “Inflation has peaked.” “FED pivot.” “FED pause.” This inflation is out of control. Completely.

When is Jerome Powell going to grow a pair and start shocking this market back to reality? How about a 150 basis point rate hike along with language like “we’re considering an emergency hike between meetings?” Because the markets were taking off like wildfire again the past few weeks.

There is so much money sloshing around out there that it’s sickening. We see them right here on Wolf’s site, talking about all of their gambling. Once these people disappear from the comments section, we’ll know we’re getting somewhere.

Amen!

150? He needs to nuke them with a 500 point increase. Literally annihilate them once and for all. The carnage would be fantastic to see.

DC, with what I foresee for the behavior of our Monetary Elites going forward, it will be very akin to Japanese Kabuki Theater. A bunch of high pitched screeching chickens sans heads that are going to be increasing telling the American public that they know their Anti-Liquidity Pumping Medicine (to counter excess liquidity and inflation similar to excess gas, gastrointestinal version) tastes terrible, but it is for our own good. Try it, you’ll like it, just hold your nose when you swallow, won’t taste so bad!

Some Whack A Mole inflation spurts to look forward to are, of course, the housing components that ooze through the calculations like an embezzler admits to guilt, the results of shortages of rain and fertilizer in the Fall farm harvest, not to mention forest fires, the costs of operating farms when some jurisdictions piled on with Go Green statues to keep the cows from farting methane, and whatever happens with the railroad workers (and I think they will go on strike in some fashion to grind things to slow-mo) even if Joe Biden points fixed bayonets at them.

Now here’s one for the evening cocktail crowd: What effect on the Inflationary Field of Misery do higher taxes have on the purchasing power of Americans that are looking at one heck of a hard winter coming. Physically and metaphysically speaking! I say taxes, whatever level of government levies them and for whatever God knows whatfor reason, should be taken into account as to what Joe and Josephine Six-Pak have left in their checking accounts at the end of a month or at the end of a quarter. Unfortunately, as Mark Twain opined, they are a cost of living in this once-great country. Ancient Rome comes to mind.

We all need to study the waning days of the collapsing Roman Empire. History is about to repeat itself, but on a much grander and sadder level.

I’m not sure I would imply that the US is “grander” than the Roman Empire.

I should have said, “more severe”. We ain’t grand except in the debt accumulation and denial categories.

1.5% is what the Fed *should* do, but since when have they done anything to reward financially responsible Americans? If you’re waiting for a 1.5% increase this month, you might as well get a nice warm jacket ready for when hell freezes over, because that’s what will have to happen before JPow grows a pair and raises rates by that much.

It’ll be another 0.75% increase at most. A pause will come somewhere in the 3.5% to 4% range to allow “some time” for monetary policy to settle in. The Fed will keep a deeply negative real FFR in place. If there’s anything Powell has been adamant about throughout his tenure, it’s been that he doesn’t want to shock or spook the markets. Today’s 4-5% one-day drop in major stock indices could certainly serve as a sufficient shock to hop on the next leg down.

Deflation is painful and brings about many changes.

The crystal ball window you were looking through, becomes a broken window sill that your barely hanging onto.

If there was really any will, the president could stanch the bleeding by executive order. READ: Executive Order 11615 ordered by Nixon in ‘70 — pursuant to the Economic Stabilization Act. He imposed a 90-day freeze on wages and prices in order to counter inflation. If you raised prices or wages, he threw your ass in jail. Done.

Next calamity?

Liquor at home up 50% MoM ????

Misprint?

Hahaha, they saw me coming as I was trying to stock up on beer to soothe the pain from this CPI report, and they said, hey, there’s ol’ Wolf, he’ll pay whatever for beer, so lets jack up the price, and sure enough the BLS picked up on it…

Thanks. Excel changed a “.5” input to 50% (I know it does that but I get caught by it anyway from time to time). I should have typed “0.5”

Crap beer has gone up a much higher percentage than good beer, as transportation and materials costs are a much higher percentage of the total.

So the 24 pack of Coors Light is up by 40-50% in my anecdotal experience, but the IPAs I drink are only up about 10-15%

Here is what my Safeway did. For the past year, all my favorite IPAs were listed at $19.99 per 12-pack, and then one of them would usually have a big discount, like down to $18.99 and sometimes $17.99 and sometimes cutting the price to $12.99 (which is when I load up). But two months ago, they raised their sticker price to $21.99 per 12-pack, and they’re now discounting to $18.99 or $19.99 across the board. They want people to get used to the idea of paying over $20 for a 12-pack. And eventually people will accept it.

Costco is still below $30 per case (24 bottles) of my favorite IPA. Or at last WAS last time I went there, which was a while ago. So when I go there, I buy a trunk full of beer. You gotta fight this every way you can.

Interesting. I’ve only seen at my Costco the Kirkland brand IPAs, which are decent, but not amazing.

I’ve become a big fan of Voodoo Ranger, and my liquor store still has it for $15.99 for a 12 pack. We’ll see how long that lasts!

My Costco has several local IPAs. I have an author friend who got in with his local Costco in Portland, and he’s selling his books there, including with book-signings on Saturdays. He told me that Costco has a special manager in each store/city to buy local stuff.

Yeah, I’ve noticed this too. The crafty beers are inflating in lock step with most other stuff, but a 12 of Yuengling is only a buck or two more than Miller or Bud.

Funny thing that. While I also enjoy IPA’s, historically my regular brew of choice has been 30 packs of Coors Light and “Old Yeller” (Coors regular). Here in Aridzona, our local Smith’s (Kroger) had both on sale again at $17.76 just before Labor Day. Stocked up. Everything else is stupid expensive, e.g. eggs…BTW, no extra 10 cents/can recycling fee either this side of the River…

Time to build your own still ?

Keep on fighting Wolf!

What beer are you drinking?

It’s same for food I use to never shop at whole foods because it was so much more expensive but if I’m going to pay $8 a pound for chicken breast then I might as well get it from whole foods where it’s allegedly better for you.

Jeff Bezos appreciates your business Aaron.

Just start making homemade beer. At this point, I do everything myself as far as fixing that I am capable of. My wife always makes a joke about that, I always tell her when we are at the store “you want spaghetti sauce, let’s grow a tomato plant and make it homemade” lol.

What’s sad is that I finally get over being an addict (after 10 plus years) start a decent job, work my way up into a supervisor position, making the most money I’ve ever made and then all this inflation occurs and now it’s like I’m making what I made when I first started the job smh. Thank you mister Pandemic for causing all this, although it seems from your site Wolf that this has been years in the making.

I really enjoy reading your articles and all the comments people put. Keep it up Wolf!

Y’all need to quit complaining as y’all been getting a free lunch with the Reserve Currency. When reserve Currency status is finished, and with the monster 30 plus trillion plus of debt and heading to 40 trillion and monster deficits of trade and annual debt, US$ will be worth less than a peso. Then y’all will have something to cry about when everything is going crasharoo and the inflation Turkey is experiencing will be considered mild. Say it can’t happen, well, history says it will and current events says it will happen sooner than later!

Just saying…

Your currency first, USD last :-]

It’s all relative.

Your currency first, USD last :-]

It’s all relative.

Incorrect! The collapse of America will be fire and brimstone!

GringoGreg will collapse first, America 2179th, for sure. Lots of other collapsing entities in between.

10-4, buying the teq and wine by the case or other, ”special” is the only way to go for those with the indigenousity AND the ice peoples genes.

Other than that, Wolf, PLEASE do something about the PPT!

OTJ late at 1100 today, and then, quite obviously, took off for the usual two martoonie lunch at 1330 and only made it back OTJ at the very last minute — probably because it became 5 stingers after, or something,,,

Lazy folks don’t get their act together, we are going to end up at the 15-18000 dow, etc.., some on here estimated in early 2020.

BREAKING: PTT update

Powel and Yellen had an emergency Zoom conference at around 4:30 PM today during which they lamented that the Plunge Protection Team (PPT) had absconded from their posts as soon as the CPI number came out, worried that price increases would be implemented at the bar around the corner from their office, according to people familiar with the matter. Various aides and officials were also in on the Zoom call. Powell and Yellen then were briefed on how the PPT, which is a fairly large group, ended up drinking the entire contents of the bar at the old prices, according to the people who don’t want to be named due to the confidentiality of the matter. By 3:30 PM, with stocks totally losing it, the PPT was still in the bar, and some tried to throw a several hundred billion dollars at the stock market, but were too drunk to even log into their trading software.

Powell and Yellen concluded the Zoom meeting with the decision that they would personally block the exit of the PPT office tomorrow to force the traders to stay inside and to do their job and throw several hundred billion at the market to halt this mess.

Wouldn’t it be loverly!!!

WE, in this case the WE THE PEONs WE, really must insist that you take over the FRB sooner rather than later!!!

Only good news seems to be the 8.9% SS increase, as my dad is retired and that size increase helps. I placed an order to fill up his fuel storage tanks today as I think we might have hit the lows on energy for the next 3-6 months…

Roughly about 1/3 of this high inflation is due to shortages of labor and product from the pandemic, about 1/3 is due to Federal Reserve negligence, and about 1/3 is due to financial “vote buying” scheme stimmies…so 2/3 of today’s inflation resulted from bad decisions by our “leaders”. Perhaps their should be IQ tests for those who have the ability to heavily influence the livelihoods of billions of people…

Our current high inflation was beyond a reasonable doubt predictable, yet sad those who could see this coming 1-2 years in advance did not have the position/power to stop it…

“There should be IQ tests”…not “Perhaps their should be IQ tests”. Excuse my “grammur”…ha

Great analysis Wolf! All I can say is WOW to the numbers! It’s like a 1970’s / 1980’s reduct without the benefit of great music from the time.

It reflects exactly what I’m seeing in the real world groceries/food up, restaurant meals up, electric and gas bill up.

I’m now back to doing my own oil changes, lawn care etc. Going to be a dark cold winter.

All people can do home repairs easily,saving tons of money ,always did my own repairs .Just get off your ass and do it

Yeah Sam’s Club until recently has been resisting the major price bumps too. Plus the usual discounter suspects like Aldi and Lidl, tho with much lower selection of course. I’m with Wolf on this one still, do whatever you can to counter the inflationary pressures. We’ve also been doing our home repairing. Except electrical and HVAC–too afraid to mess with the wiring doesn’t matter how many manuals we read.

Gasoline prices fell because Biden is busy selling the strategic petroleum reserve as part of his pre-election vote purchase regime – otherwise CPI would be much worse.

— Dear Leader, Dear Leader – the people don’t have money to buy gas….

“Well, let them buy Teslas!”

Yup. And the current withdrawal plan is scheduled to end at the end of October. Just before the midterm election.

And then Biden announced,he would refill at 80$ a barrel. Total corruption,where is the free market .We Americans are nothing more than ball less plebes .Rome is crumbling

For those of us over age 50, we should be thankful that social security is indexed to inflation. I have a company defined benefit pension that, like most company pensions, is not indexed to inflation. The value of this pension lost about 15% the past couple years because of the high inflation.

It makes me wonder if teachers, fire fighter, police, and company-provided defined benefit pensions are commonly indexed to inflation. I don’t think so. If that’s true, people anywhere close to retirement better pay close attention to the financial challenges and risks involved. For example, if your pension is going to be worth 50% less in 15-20 years, do you want to have all your eggs in high p/e stocks? Do you really need that new $40,000 car? If you don’t plan accordingly, you’ll be eating cat food in retirement.

It seems likely there will be a massive retirement crisis that pops up, sooner rather than later. It may already be too late to do anything about it. Money printing, interest rate repression, and quantitative easing have consequences.

Also, don’t plan on getting anything more than 70% of your projected social security benefit. They likely will be cutting social security benefits way back with legislation at some point. You won’t get what they currently are promising. It’s nearly impossible.

Bobber,

George Carlin said something about social security. He was prescient that way.

I am one of those rare birds with a pension that is indexed for inflation. With that and social security indexed but with almost no expenses, I can wait this out.

Now we already can end up paying tax on our Social Security benefits each year, Bobber, what I call a Tax Upon A Tax since the money is now taxed twice. We are going to see a campaign to tax this retirement income more and more via an asset-based benefit reduction program: You got too much in accumulated assets that the I.R.S. can find because you were thrifty like Wolf in his Beer Acquisition Program (BAP), skipped expensive vacations each year, drove the family clunker until the wheels wobbled, and you are going to get rewarded, lucky you, by seeing less and less of the tax dollars that were originally taken out of your pay after the Taxman Cometh. Self-employed mugs like me paid into the system at twice the company employee rate! A sort of inverse wealth effect.

I will take all of those upcoming 87,000 I.R.S. field agents some 20 years to find just some of the loot that Americans have buried out in the backyard! But saving for 50 or so years while working is about to be determined to be detrimental to your net worth.

Most DB pensions are based on you final years’ salary, or some average of your final X years’ salary. To the extent your salary rises with inflation, so does your pension.

But once you leave the employer, the pension payment stays fixed. For example, I have a small pension from a place where I worked until 1999. Inflation has and will continue to erode that defined benefit payment to nothing. When I’m 75, it might be worth a pack of golf balls each month.

You can buy a new card for $40k?? Better get two and flip the second.

Most people are financial illiterates. They don’t comprehend your points. A large proportion of the population lacks financial discipline. Or both

As for your question on pensions, it’s my assumption that indexing is primarily with government employment.

Yes, a lack of financial illiteracy is real, I am a case in point: I’ve been woefully ill-educated in the area of finance and have only recently been trying to play catch-up, teaching myself and using this really useful site.

But it’s getting harder to say that people are 100% “illiterate” when they can actually read daily gaslighting claims from their media and their “leaders” like: “We had zero percent inflation last month, folks!” or that deficit spending almost a trillion dollars more in DC is an “act of inflation reduction”. That’s Double-speak of the highest variety, and its purpose is to make innocents think that, contrary to everything their eyes can see and they can feel in their pocketbooks, everything is “just fine”.

As an aside, I came across a recent Economist/YouGov poll of 1500 Americans, Sept. 3-5. When asked, 45% of U.S. adults think the “best indicator” of an economic recession is the prices of goods and services that they buy. Only 20% say the best indicator of a recession is whether the economy is shrinking or growing, and 11% (or 165 people) claim “I don’t know”. Sigh…thanks for reading.

Meant to say, “A lack of financial literacy is real…”

Blew it on the first sentence, sorry…

Bobber, just wait until Net S.S. Benefits are taxed at rates determined based upon taxpayer assets, not income. Hopefully, this mild comment doesn’t get moderated out. Two out of four making it I guess is a good day.

In Canada old age security gets cut to zero or you have to pay everything back at $130,000 net income.

Wolf maybe could shed some light on this but with the COLA increases, and to my understanding, an already unsustainable social security program how quickly could this money run out?

I’m 31 and have known since the first job I had that I’ll never see any the social security tax money I’ve been paying in (wish I could opt out) but a lot of people count on this. What’s the end game here?

This is why the FED needs to end this inflation NOW. Governments buy goods and services also and have obligations to meet. They simply cannot afford this inflation.

Aaron Fairchild,

Your last line is verbatim what the dad of my high school sweetheart told me in ca. 1974. He was in his mid-30s at the time. He was never going to get a dime out of SS, he said. Turns out, he retired about 20 years ago and got his SS benefits just fine, and he passed away about 5 years ago, and then his wife got SS survivor benefits just fine, and she’s still getting them.

So, don’t let some fearmonger morons persuade you that the money is going to “run out.”

SS is insurance. Meaning people pay into it, and then people draw out of it, like all insurance. Periodically, it’s adjusted one or two ways: how much people pay into it (usually by raising the income caps), and how much they can draw out of it (usually by raising the full retirement age threshold).

SS has run a surplus for about 20 years, and this surplus has accumulated into the “Trust Fund.” The Trust Fund is a buffer. Even if it runs out, people still pay into it, and it pays for people drawing out of it. But it won’t run out; Congress will make some minor tweaks to the income caps and the retirement age threshold, and that’ll fix the problem.

The problem with SS is not that it will “run out of money” – it won’t. The problem is that the COLAs don’t compensate you for the actual increases in costs (see the part about the hedonic quality adjustments), and as you draw benefits year after year, you can afford a little less each year, and have to tighten your belt a little more. That’s why you need to have some assets before you retire, so you can supplement your SS benefits every year for decades.

Better yet, just keep doing something that you have fun doing while making some money, and don’t retire for as long as possible, and save your SS benefits for later when you can longer work. That’s the best retirement plan.

I cover SS and the Trust Fund once a year after the end of the fiscal year, so in early October, and it’s coming up, so stay tuned.

Thanks for the master class! I’ll keep an eye out in October 🤙

With the birthrate going to zero watch your deductions on your paycheck for social security to increase way above the inflation rate and if you end up with anything at retirement it will be a miracle.

The birth rate will never go to zero. There are too many people that like sex and make mistakes.

If the COLA covered the period of inflation used in it’s calculation, instead of for THE FOLLOWING YEAR, then that would be a good thing. It’s always a year late, and a dollar (sic) short!

“It’s nearly impossible.” Says you.

This works to the beneficiaries’ advantage when inflation rates are coming down. When the COLA might be 9% for year x, CPI in year x might drop to 5%, and the year after that, the COLA might be 5% and CPI might only be 3%. It’s symmetrical, up and down.

Good to know!

Your SS earnings are also indexed to inflation, until you turn age 60. Earnings from then until you retire are no.

Anyone in their 60’s thats still working is getting the short end of the stick this year.

This just hit the Bloomberg news wire a few minutes ago….

———————————–

“The US may begin refilling its emergency oil reserve when crude prices dip below $80 a barrel, according to people familiar with the matter.

Biden administration officials are weighing the timing of such a move, with an eye toward protecting US oil-production growth and preventing crude prices from plummeting, said the people, who asked not to be named sharing internal deliberations.””

————————

Take a moment to just think about this and all the ramifications…. …it’s put a floor under the futures price of oil… I can’t wait until oil prices start going up again….

No, that does not put a floor under the price of oil. There’s an entire world of supply and demand out there beyond America.

A cup of coffee at my nearby cafe increased 57% in price a couple weeks ago. I am presuming they are seeing supply, wage, and rent inflation up the wazoo.

This is on top of a 33% rent increase for me.

Obviously I have started cutting expenses, and will continue to do so. Which means a lot less coffee outside home in addition to cuts already made.

There was a music festival over the weekend and I attributed the light turnout to the weather, but perhaps there was another reason.

“Surprisingly, the CPI for durable goods keeps rising, and rose 0.5% in August from July, the fifth month in a row of month-to-month increases, when durable goods prices had been expected to come down from the mega-demand-meets-supply-chain-chaos spike during the pandemic. But they’re not coming down; they’re still increasing but at a slower rate.”

Who “expected” prices to come down? Because that runs antithetical to everything I see and experience over the course of life due to the outrageous money-printing orgy the FED engaged in.

I wish you’d post the historic CPI rate next to the FED funds rate to show just how laughably behind the curve they are. How can inflation come down when the FED funds rate is almost 7% BELOW CPI? It can’t. Never in history has the FED funds rate been so divorced from CPI. Jerome Powell should have been FIRED long ago!

“I wish you’d post the historic CPI rate next to the FED funds rate to show just how laughably behind the curve they are. How can inflation come down when the FED funds rate is almost 7% BELOW CPI? It can’t. Never in history has the FED funds rate been so divorced from CPI.”

—- I’ll say this again because almost no one seems to get it (though I know you do). CPI is not the current rate of inflation, and not even a really relevant measure other than to torture ourselves in anger. Useless for management. It’s the inflation we’ve already booked, today’s prices vs last year’s prices.

From Wolf, “The “core” CPI, which excludes the volatile commodities-dependent food and energy components, jumped to 6.3% on a year-over-year basis, and to 0.6% on a monthly basis. This index is design to measure inflation in the broader economy, and it will give the Fed the willies…”

—- So 0.6 = 7.2 annualized. A disaster. Since some (maybe Augustus Frost last time? I forget) point out that a short term measure of just one month is not very useful, too volatile. OK, take it to 2 months, which would be 0.7, so 4.2 annualized. I hate it, a lot, but it’s not 8%+ headline that brings out the bitching that the red funds rate is negative 6%. No, it’s “only” about negative 1.5%. ;-)

“Jerome Powell should have been FIRED long ago!”

– Now this part I fully agree with! And I’m pretty sure any Japanese leader would know how to respond to such shame that he had brought onto himself and his family…..

“Who “expected” prices to come down?”

I did — because prices of durable goods had spiked so much. Used vehicle prices have come down some, and the yoy spike of 40% in late 2021 has been whittled down to about 8%. And electronics prices have come down. Everything else still seems to be going up, which is just stunning to me, given how much prices of durable goods have already spiked. How high can this shit go? When will people finally stop buying at those prices???

But enough Americans are still throwing money around like crazy, and it just doesn’t seem to slow down, and they’re still paying whatever.

It’s the liquidity Wolf, not so much the rate right now. It will probably take another 4-6 months to mop up the extra money sloshing around from the biggest bailout in history before people are forced to be frugal.

Yes, agreed on the liquidity part. Huge amounts still out there, and it might take longer to “mop it up.”

My observations see that we are now firmly in stagflation, and I don’t see that changing. Most of my businesses now have little work. We are now just waiting on layoffs. But my take is inflation from money printing and stimulus has peaked. This excess money at the rich is peaking but imho it’s passed even with today’s print because it takes time to show both ways. Think gas. Now inflation continues from the pandemic and global conflicts sources. We have global decoupling which is highly inflationary and pandemic supply damage. I don’t see wages coming down, rather bankruptcies as no one feels they can operate here on less. In the big picture, I think 50 years of living beyond our means through Fed debt expansion theory(inflation) has finally met it’s match. The Fed can not return the good old days now. The pandemic created imbalances and global isolationism now will unwind debts to a equilibrium and we folks are out of tools for this current monetary system. I see unrest and slow transitions to 3rd world living standards city by city starting where the poor are most concentrated. Now that inflation is high, the Fed game is over. It’s either depression or hyper stagflation which equal the same. The last gasp imho will be their new CBDC which will be a world changer. Nothing good comes out of this. And if climate risks, wars, political divisions etc add on then it’s expedited. This country had it good. If there was a way to simply reinvent itself maybe something could work. I don’t see it happening myself, but I see the Fed trying. MMT and crazy stuff already in the rear view. Time to cherish what matters most, as nothing is certain anymore.

Stagflation in Germany and much of Europe is coming but unemployment here in the US is too low right now with labor shortages and global capital is flowing into the dollar. At least the Fed has the ability to engineer a stronger dollar by tightening money supply against global demand, this is the benefit of the reserve currency. Hopefully we use this to our advantage to reshore domestic production and eliminate waste that is more in line with the human scale. There will be winners and losers in this new economic age. . . .

“Everything else still seems to be going up, which is just stunning to me, given how much prices of durable goods have already spiked. How high can this shit go? When will people finally stop buying at those prices???”

My anecdotal evidence says “much higher,” Wolf. Why? Because I have never seen so many “wealthy” people as I do right now, spending as if there is no tomorrow. This makes 2006 look like a warm-up act.

Over the course of the past couple years, I have run into numerous middle-aged men who are seemingly “retired.”I do not ask personal questions, but I know for a fact they are not working and so that means they have plenty of fat to live off of. They are driving the latest $100k trucks, have houses, toys, etc., but they don’t work at all anymore. Very weird, right?

I have a hunch – CASH OUT REFIS. When you blow a housing bubble as big as the FED just did – an embarrassingly shameful size and scope – and hammer rates to zero, you create a bunch of faux rich people who suddenly suck $400k out of their shanty and refi into a loan at a rate they never dreamed of. Suddenly they “pay cash” for a brand new truck, buy a few other toys, and still have $200k of play money to burn through over a few years.

This is one sick puppy the FED has created. The entire institution should be severely neutered and never again have the carte blanche that they just enjoyed. These people are financial terrorists, nothing more.

The globalists cartel lost control of the FED bank.

Powell is a patriot and his father was a very interesting man.

He was most likely covertly installed by vectors of power within the IC to defend the dollar at all cost.

Wolf, where are these people getting all this money to buy at these prices? Or are they so far detracted from reality that they just don’t see it? When will the madness finally end and reality finally hit people.

I found your site while looking up recessions, housing crash because I have a wife and 5 kids and I really want to buy. Something to call my own and work on and build. Not have to worry about if my landlord is going to kick me out or if my price of rent will go up. Problem is there’s no way I’m buying a house at these prices. Which is why I continue to read your articles and love your site because you don’t roll crap in powered sugar and call it a donut.

Should I keep waiting out to buy (I believe I should)? If so, how long do you think before the donut (the crap I just spoke of lol) hits the fan and I can finally buy or start looking to buy? I appreciate any thoughts.

And these comments and reply’s from everyone (including yours Wolf) have me cracking up!

There was a decade of deflation after 1929. Looking forward to it. History may not repeat, but it sure does rhyme.

The opposite should happen inflation will become runaway inflation.

Do you even have a clue what a depression was like,my aunt wore flour bag dresses to school ,holes in shoes,ate lard sandwiches.My grandmother hab 15 relatives move in at farm butchered a hog every week ,they were lucky at least they had decent food.BE CAREFUL WHAT YOU WISH FOR

I’d love to see Janet Yellen wearing a Hefty bag as a muumuu, pushing a shopping cart around while looking for a dead rat to roast over a trash can fire. Bring it on.

People who constructed their life around living below their means will do just fine, Depression or not.

Just happened to be looking at price change on two of the most popular truck products we manufacture today. Today’s production cost is 48% higher than the cost at mid-year 2018! That is a fully-burdened number so it factors in pretty everything except SG&A – cost to buy all the materials, labor and outside service to process it, and an accounting figure to approximate the factory overhead to be allocated to that work.

I was originally expecting about half of this increase to disappear as steel and aluminum costs fall, but I am becoming less certain of that as the year passes. A bunch of other increases have continued to trickle in and eat up the extra margin that might have come to fruition with dropping commodities.

These crazy high prices just might stick around unless things get really slow and we start fighting with competitors for scraps.

We are starting to see orders drop like a rock. One big customer on the West Coast noted today that it’s “like someone put out a red light and business stopped this month.”

Our healthcare renewal “negotiations” just started, and Blue Cross opened with +9%… ugh.

I think the goal of the FED is to deaccelerat inflation down to 2%.

2% still mean prices go up. I would not count on prices going down? Maybe a few of the bubblish assets will like stocks and housing.

But rent, food, services are sometimes sticky.

Agree but rather Disagree. Think great recession. Rents went down almost 50% I rented near the beach 40% less than what it was from the top. Think $5 foot longs and BOGO free. And $1 menus. Prices reflect supply demand. If there is no demand because no one has money, prices will come down to where a sale is. Most people won’t work for less so wages are sticky but this results in bankruptcies and homelessness which expedites recessions. One by one if Powell keeps rates high, inflation metrics will fall as poverty spreads. But will he really kill it? He knows he must but does he survive? This housing ponzi will take years to unwind, but my take is it will be 2-3x more destructive than the last.

My only comment is why is the S&P down just 4% Today. This is now out of control Inflation.

Some people view stocks as an inflation hedge.

Maybe in Russia where the P/E ratio was about 5 before the war broke out. In America the real P/E ratio must be well above 50 not the stated thirty to thirty five or so. At some point in time U.S. stocks have to implode unless the U.S. dollar implodes first.

P/e is mostly in 17/19 range depends which sector your in

Everyone has jobs and the top 20% are richer than ever. People are still spending money like no tomorrow. Basically, inflation kills the poor but it’s a mere flesh wound for the rich who will keep spending with abandon.

Until that changes expect more of the same.

Thinking of some factors: some relief on Ukraine and the overall energy supply picture for winter?

… and I think USA markets are a haven for global capital.Maybe Mrs. Watanabe is buying our securities?

A funny headline I just saw:

“Options bets blamed for amplifying U.S. stock-market plunge after hot August CPI reading”

That’s weird, because I blame the FED’s money printing orgy.

DC, I think it meant to say, “A highly leveraged investing cadre that has never seen high inflation or a persistent Fed tightening cycle all tried to get out of the theater today, but many were trampled, financially speaking, at the exit doors”. There are so many derivatives hanging over the stock market today that it makes your head swim, options would be just a small part of it. The bond market is a much greater accident waiting to happen with probably 10 times the leveraged bets hanging overhead, say, Credit Default Swaps come to mind. They never went away after 2008.

The problem is the algorithms that amplify everything in both directions. The drop in the S&P seems bad until you realize it’s just giving back the unjustified gains from the past week.

> “… I blame the FED’s money printing orgy” for absolutely every woe on earth. That’s your refrain for what, 750 posts in a row now? FIFY.

You are moderating now?

Phlegm is a speculator who likely just got annihilated today. Just look at the DOW. Phlegm is seething. Note that he’s one of the braggarts always talking up his “investments,” his house, etc. We don’t see him gloating today.

So goes inflation, so goes the fed. Lotta stock volatility up and down between these reports that seems overdone.

Not a great sign for us markets because I don’t think we’ve seen the capitulation one would have expected – a lot of people saw the COVID V and still on hair triggers to buy, so a lot of traps for speculators. P/e and especially cape still too high to attract the long term bargain hunters, they are waiting for the likely recession.

Saw a Yahoo Finance headline this morning: “Inflation is Getting Sneakier.” I thought not if you read Wolf Street which has laid out the process of how inflation infects the economy for a long time. I was expecting a lower inflation print today, but I’m not surprised I was wrong given what you’ve written about inflation seeping into services. Thanks for another excellent report.

Rojo – Your Yahoo Finance headline “Inflation is getting sneakier” was written by none other than Ricki Newman. I can almost predict who writes this crap when I see the headline, and yes, usually the same WH cheerleader.

I hit it on the nose.

Charlie, I can usually do the same thing with Business Insider articles.

Tony, there was money to be made for getting it right.

The Fed’s attempt at fixing inflation is equivalent to the driver having run over the pedestrian shifting into reverse.

Jim Cramer was totally unhinged on CNBC this morning. He was literally sh$tting in his pants. Total Diharea. The hosts had to cut him off. He said could not understand why the big Tech stocks crashed. He was on record of recommended his charitable trust purchase them.

I can’t understand how anybody would watch Cramer. Complete nutcase. Remember when he said that Bear Stearns was “fine” back in 2008 and not to take your money out? Five days later it collapsed to almost nothing. That dude is a total clown.

Swamp — I found Cramer that video on MSNBC’s site. It’s hilarious. Dude just does not get it.

Dude gets it. It’s his job. He is playing his part in the well oiled propaganda machine.

Everytime he says ‘charitable trust’ it comes out of his mouth sounding like a bunch of slobbering marbles. I want to punch him in the face everytime he says it LOL

Jim Cramer just said yesterday that the market lows had been reached in June.

He may have to retract that.

However, can I say “It ain’t over until the fat lady sings”?

Bear market rallies and plunges are notorious.

My bed mattress is lumpy with cash. I am not sleeping well.

Use it as a box spring, and get a new mattress!

> Jim Cramer was totally unhinged on CNBC this morning.

In other news: the sky is blue today and water is wet.

So what’s the solution other than pushing us into a major recession that forces the prices of goods and services to all tank??? I dont see any beautiful soft landings in our future.

It think you misspelled recession= DEPRESSION or in wef speak great reset

The government can regulate the profits of the corporations. Where I live the car insurance companies are the biggest crooks in the entire world. All of them should be regulated by the government. This would bring down the inflation rate but would be somewhat communist.

Inflation is not enough supply for the demand. Part of this is truly money printing.

The fix is to create more Supply. Grow our own food, drill for more oil and gas, and stop funding, spending money on climate change, ecg propoganda to the IMF.