Starts: Single-family houses: -18.8% year-over-year; larger multifamily buildings: +15.9%. Here are the long-term trends.

By Wolf Richter for WOLF STREET.

What became clear (again) in the Census Bureau’s data today on housing starts was the divergence of the multi-year boom in construction of apartment and condo buildings with five or more housing units and the current slump in construction of single-family houses. Builders of single-family houses are now confronting a host of issues that have tangled up their businesses, including dropping traffic and spiking cancellations, to which they respond with price reductions, as sales decline amid surging inventories.

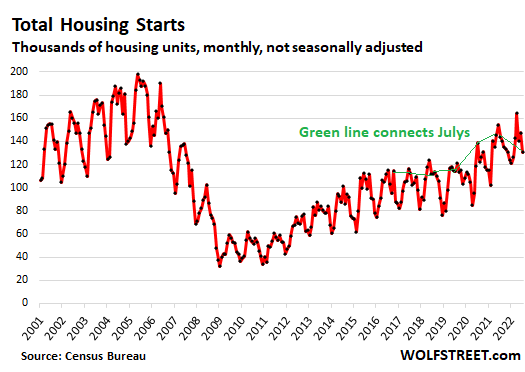

So “Housing Starts” – the number of housing units on which construction started – in July dropped by 9.6% from June and by 8.1% year-over-year to a “seasonally adjusted annual rate” of 1.446 million housing units.

Not seasonally adjusted, and not annual rate, total housing units that were started in July fell by 9.2% year-over-year to 130,600 housing units. But this was composed of a plunge in starts of single-family houses (-18.8% year-over-year) and a surge in starts of units in buildings with 5+ units (+15.9% year-over-year). The green line connects the Julys of the past few years in total housing starts:

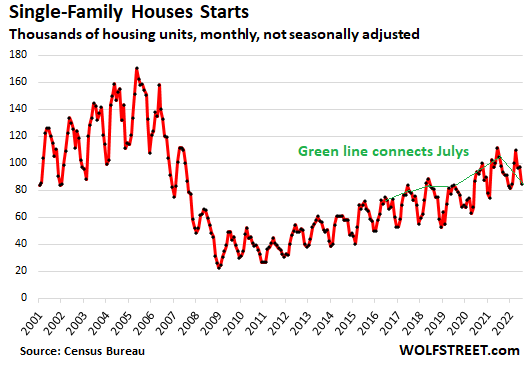

Starts of single-family houses drop to winter level.

The number of single-family houses where construction started in July plunged by 18.8% from July 2021, to 84,900 houses.

This was the second month in a row of declines during the summer, and the lowest since the winter months, when construction starts slow for seasonal reasons.

Note that starts of single-family houses include both – those built for homeowners and those built specifically for rentals.

July starts are usually near the top of the range, and the low points during the year occur in the winter. So the drop in July to the level of last February was quite something. And it shows how homebuilders are reacting to demand that has suddenly fizzled amid 5%+ mortgage rates.

Note also the long-term trends: The peak in 2005, the plunge afterwards during the housing bust, and the gradual recovery that remains far below the peak:

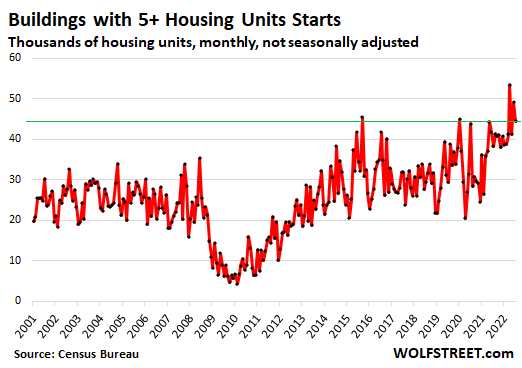

Starts of units in buildings with 5+ units.

In July, the number of units started in buildings with 5+ units jumped by 15.9% year-over-year, to 44,400 units.

In April, starts of buildings with 5+ units had hit 53,500, the highest since 1986. The plunge in starts during the Housing Bust was brutal but relatively short. By 2013, the number of starts were back at pre-Housing-Bust levels and continued to rise to set multi-decade records by 2015, before slowing. But then they took off again in 2019 to hit that new multi-decade record in April.

The category of buildings with 2-4 units that fits between single-family houses and buildings with 5+ units has fallen out of favor, with only about 1,000 starts each month.

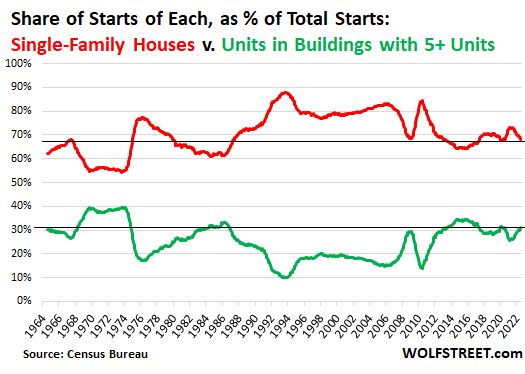

Single-family v. multi-family starts: it comes in waves.

Starts during the 12-month period through July:

- Single-family houses: 1.113 million, -2% year-over-year.

- Units in buildings with 5+ units: 509,100, +27% year-over-year.

Over the decades…

Multifamily peaked in the early 1970s in a huge boom when between 75,000 and 85,000 units were started per month. After this boom came the sudden bust, and by 1974, starts bottomed out at 14,000 units for a few months. By 1983, there was another boom, but with lower highs, that maxed out with just over 60,000 starts a month. Which then fizzled for decades, and bottomed out during the Financial Crisis in the 6,000 range. Then it recovered and returned to the highs of the early 1980s but not the peak of the 1970s.

Single-family housing had a good run in the late 1970s, exceeding 150,000 starts for a few months, then peaked in 2005, maxing out with 170,000 starts in May that year, and then collapsed and never got back to those old highs.

The share of single-family starts of total starts and the share of multi-family starts come in big waves – as a function of the boom-and-bust cycles that single-family and multi-family construction go through.

This chart shows the 12-month moving average of the share of starts of single-family houses as percent of total starts (red line) and the share of starts of units in buildings with 5+ units as percent of total starts (green line).

As the chart shows, since the Housing Bust, the share of multifamily starts has been relatively high, while the share of single-family starts has been low.

In some high-density cities, such as San Francisco, and in parts of New York City, such as Manhattan, practically no single-family housing has been built over the past decade. It has nearly all been multifamily, often large towers. The same has occurred in many city centers, where residential towers have sprouted like mushrooms. Many of these new buildings are relatively higher-end condos and rental apartments, in response to demand from people for whom this is a life-style choice.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Many of these new buildings are relatively higher-end condos and rental apartments, in response to demand from people for whom this is a life-style choice.”

I would love to know if there is a standard definition in the industry for “high-end” or “luxury.”

It’s common to hear developers say “Luxury Apartments for Sale” and to listen to NIMBYists complain that the ultra-luxe apartments being built destroy neighborhood “character.”

But here in NYC, most of those “luxury” apartments are just standard one-to-two bed places with some basic amenities, a washer/dryer and a normal sized bathroom. Hardly luxuries outside this city.

Besides, what developer is going to call their new building “A lovely place with perfectly average apartments to rent.”

“I would love to know if there is a standard definition in the industry for “high-end” or “luxury.””

Relative price.

I am in that segment of the industry and the benchmark I’ve always heard is properties priced 10 times the average home price in a particular market and above.

I think you’re talking about super-luxury. The pain luxury category is generally and variously considered in the top 25% or top 15%, something like that.

“Boom and bust cycles”

The FED and their rich buddies have become fantastically wealthy through these pump and dump scams which hurt most of society. I don’t believe the system is fixable. I believe it so shot through with corruption that a complete failure is the only answer at this point. Burn it all down. I hate that it’s come to that, but it’s the only way something more fair, equitable and sustainable can come to be. What we have now is just a disgusting Davos crowd greedfest.

In a system that boasts of “checks and balances”, who checks the Fed?

The Senate banking committee is focused on racial inclusion, climate change, and gender issues rather than monetary policy.

The Fed has made it near impossible for small businesses and contractors to rely on some type of stability.

If Fed Funds had sat at 2% and 30yr mortgages 5.5% for the past 13 years we would have been better off, IMO. No Fed games.

“You will own nothing and be happy” ….

Housing unaffordable (due to crazy high prices)

Eventually Cars leasing going to become more main stream (Tesla taking the lead) with ownership going down due to affordability.

Cell phone leasing (apple taking the lead) coming up….

I thought that it would take dictatorship to manipulate money and value of assets to such an extend that the majority of productive population is reduced to debt slaves.

Today, I see it in democracies, not just US, but whole of Europe and UK!

We need to keep our conservative and liberal feelings aside and focus on logic and math behind money to come together to uphold the fundamentals behind our constitution.

As Spock said “Logic clearly dictates that the needs of the many outweigh the needs of the few, Or the one.”

The most successful way to run a dictatorship is to masquerade it as a democracy.

“I thought that it would take dictatorship to manipulate money and value of assets…”

What would you call central banking?

Spock was a collectivist. A Borg with pointy ears. And it was in a military setting (Star Fleet Command).

It’s not enough that you’re a wage slave and a debt slave, you must also become a rent slave. Wall Street’s idea is to monetize your life so you can lease it month to month.

Una,

If DC had not been manipulating the hell out of interest rates for 20 years (ZIRP), the housing market would not have turned into a whipsaw casino.

Without interest/savings rates being slashed in half (or more) (most blatantly and profoundly by DC money printing), the doubling (or worse) of housing prices would have been aborted on takeoff circa 2003.

It was only the slashing of mortgage rates that empowered the mass delusion that a moribund employment mkt/economy could “afford” a doubling of housing costs – no ZIRP, no McMansions for McMorons.

No phony booms, inevitable crashes, cratered housing supply, insane housing price inflation.

The housing mkt had functioned semi well for many, many decades before DC/Fed got delusions of grandeur about being inerrant Central Managers of the Economy.

They effed up international trade/employment and in response, they effed up interest rate/macroeconomic policy.

And failed to course correct for 20 years (see Mideast wars also).

I just read (per Forbes) the US now has 735 certified Billionaires and a whole lot more that may or may not be.

How many “voting” members does the CCCP have?

I betcha they have us beat on “decision making efficiency”…..but more citizen input into governance is the idea of a democracy, right?…. so obviously the number of Billionaires will have to increase.

@Concerned_guy…”you will own nothing..” may very well become true for 99% of the population. As far as being happy with that, we will have to wait and see.

In terms of ownership versus leasing…well, the only difference would be that the leasing guys would squeeze every ounce of blood from us instead of the guys who sell us stuff…

IDK my husband is a confirmed ‘why own a depreciating asset’ when it comes to auto leasing. That might be one of the few areas where it makes sense…

Depth Charge is spot on. The whole system is corrupt and evil to the highest degree. The federal reserve and the wall street are making a mockery of the concept of justice and goodness. Trillions of dollars wasted in speculation which could end world poverty. And they can get away with this massive crime because of the ignorance and indifference of the masses brainwashed by media and popular culture.

How right you are! I bought my first house with a personal loan from a banker friend. He couldn’t finance the loan as the house was outside the banks area.

I bought the second house contract for deed as there was no money available. Congress then started the IRAs/401Ks and suddenly money was available.

Later I purchased a tract of land and the yahoo attorney wanted a certified check for payment. Sent him a personal check via return receipt requested. He deposited the check and was happy.

Non of these times were any points, under the table payments, or any of the items now charged that are really bank expenses and fraud.

The banking system is not the only system with greed and fraud. Politicians and government are also in on the take!

Bread & Circuses my friends.

Like an addict, we will need to slam into a rock bottom before serious change will occur.

By then it will be too late.

Where do you get any of that from those charts??

Lol I know. SFH starts down, MFH up means it’s so fucked we should burn it all down?

Plenty of wolf’s posts fit way better. This one is though is the unsurprising finding that apartments building going strong while SFH is going down.

I dare you to provide a shred of proof for any of this.

It’s axiomatic. Look it up.

Easy big, fella. In case you weren’t paying attention (which I know isn’t the case), COVID put the nail in the coffin regarding the Fed / Congress use of MMT to run our economy. There is no “complete failure” looming on the horizon for housing. We WILL see mortgage & rent forbearance again. These are the new tools to ensure housing never has “the big one”.

Totally agree on everything else.

The best multifamily housing to invest in are prisons. We’re going to need a lot more of them the way things are going. Michael Burry (the Big Short guru) has liquidated all his stocks in his portfolio with the exception of prisons, especially the maximum security kind.

Swamp creature

The coming social, financial & political chaos need more prisons, right?

sunny129

Yep, Prisons will be the next growth industry.

Build more prisons for what? The violence today is nowhere near the most violent street era in America,, 1990-1995. There were 2400 murders in NYC in ‘90, lcompare that to 2020. I know how it was, I was a teen in a major city back then. Most of the young guys today who would have robbed the pawn shop or bank yesteryear are trying to be scammers. Swiping credit cards, stealing bank logs, returning stolen goods at Home Depot, etc. A good measure of how bad things are… look at Aggravated Assaults. From 1990-95 aggravated assaults hit 1million every year but that mark has never been reached in the entire 21st century. And in 1990 there were 60million less ppl in the USA. You can’t incarcerate a guy in maximum security if all he does is white collar crime. Sure, there are more accident murderers today than 30yrs ago but the real killer population is less. That maximum security bet is a loser or maybe it will only draw even. These kids are less vicious than back in the day but they are more mobile so they touch more affluent areas than their predecessors

Debth prisons, for those who do not pay.

Maximum security prisons for those that think, speak and others listen to.

It’s easy to talk about incarceration if you’ve never been handcuffed. Just one night in a holding cell will change your tune remarkably. There’s a lot of misplaced pride amongst the fortunate of this world, born on third base and believing that they hit a triple, as someone has said here recently. Nobody’s immune from police abuse if they are perceptibly not powerful. The police make mistakes too. If a drinking man works construction in the South, he’s going to meet the law sooner or later. Once had my entire crew locked up in Sinton, Texas, had to bail them out to finish the job. Bailed my foreman out in belton Missouri. Construction workers do not share holding cells with bankers. Bankers should not be able to take someone’s liberty for a debt. They own too much of our lives as it is. Prison as a concept does seem medieval, especially from the inside. Future incarceration will likely be pharmaceutical.

Been there and agree:

Time and enough for all these so called ” white collar” bad guys to do at least a mandatory minimum in jail, far damn shore S!!

Time and enough to make every crime against people have mandatory minimum time in jail too…

Otherwise, WE, that we being WE the PEONs, will continue to be on the short end of the legal system, also known incorrectly as the ”justice” system in USA,,, where JUSTICE is only available to those who can pay enough, per OJ, et cetera…

Time and enough for some really rational results from every elected person,,, and stop,,, stop,,, stop the ”legislation by bureaucrats.”

Imprisoning people is really expensive. We might not be able to afford it.

It’s not like we incarcerate more than the Russians or Chinese because they are nicer governments.

With 87,000 more IRS agents on the way, they are going to need more prisons to house the tax cheats.

If you overlayed Democratic vs Republican President on that the republican is almost always during single family booms and the democrats during multi family booms.

Maybe a coincidence? Maybe democratic power centers are more urban where multis go and republicans more rural where singles go?

17% of the US population lives in rural areas and 7% lives urban areas, 76% of America lives in the suburban sprawl. What happens in the city or the country is irrelevant.

Whuuuuut?

John Stotes is pulling your leg. Everybody knows that 105% of all Americans live in Antarctica. And the other eleventeen percent live underneath Wolf Richter’s kitchen sink.

“Maybe a coincidence?”

Maybe an invention. You’re trolling.

fyi

A new online survey commissioned by Anytime Estimate and Clever Real Estate has shed light on how much millennials paid for homes during this period[..}

72% Of Millennials Have Regrets About Homes They Overpaid Or Settled For In 2021 And 2022

(zh)

The infrastructure overhead of maintaining SFRs will get progressively more and more expensive. I’m already starting to see huge changes in trash pickup schedules and rates for SFRs. Granted it’s only about $100 extra, but those nickels add up. Pretty soon USPS will move individual boxes to neighborhood mail centers, or Amazon will charge a fee for not using a delivery hub…

Are ADU’s (Accessory Dwelling Units) included in the single family totals?

It doesn’t matter because their number is so minuscule. Not even a rounding error.

Reduced construction of SFH will only lead to an even larger shortage of homes (both affordable and unaffordable) and eventually, to higher prices for the existing stock of homes.

We are currently seeing the consequence of underbuilding from 2008 – 2018, in addition to low interest rates. This leads to more renters, which is why the number of multi family units is increasing at the same time.

I think its more likely that the “underbuilding” of SFHs from 2008-2018 was a consequence of the massive overbuilding of SFHs in the preceding decade.

I dunno. In some cities, demand shifted at the top. People moved back to the cores as traffic got maxed out around 15 years ago. For the ones who get to choose where they live, the lifestyle is usually apt in a fun part of the core post college, suburbs for the kids, then back to apartment/condo after college for the march to retirement.

So, more demand for luxury apts.

The Amerikan Dream to rent a 750 sq ft apartment located close to your high-paying WalMart service job.

Multi family is outpacing SFR’s by huge margins in the city of San Diego. Some zip codes are seeing massive price spikes because of the potential for upzoning.

1) Single family starts had a good run in the fifties and the late seventies.

They peaked in 2005. Constructions co learnt the lessons of the 2009/2011

bust. They became conservative. That’s why prices are still rising.

2) Multi family starts for rent had a bull run in the sixties, peaked in the

early seventies, reached nadir in 2009/2010 and bounced to a lower high

in 2022, while population doubled.

3) It’s all about accumulation. Volume is down, but accumulation of total housing have reached a new all time high.

4) Within a decade the front line of the boomers will reach mid 80’s.

5) When they expire they will leave plenty empty units behind, for rent,

for sale.

6) Wall street executives and high tech millennial making between $400/day and $700/day don’t care about prices, in most cases, but the zoomers do. They will wait until the boomers leave behind houses for half prices.

What effect does the aging baby boomer population have on the demand for multi-family?

Millenials, the largest generation ever, is moving in behind them. Generations are a flow.

7) The front end of the boomers is 76 years old. Single homes and multi

units accumulation reached a new all time high.

I’m assuming there are still vastly more single family homes than multi family units, and that the majority of those are owner-occupied?