Homebuilder sentiment dives 8th month in a row, their stocks are down 19% to 36% YTD despite blistering summer rally.

By Wolf Richter for WOLF STREET.

“Tighter monetary policy from the Federal Reserve and persistently elevated construction costs have brought on a housing recession,” said National Association of Home Builders Chief Economist Robert Dietz.

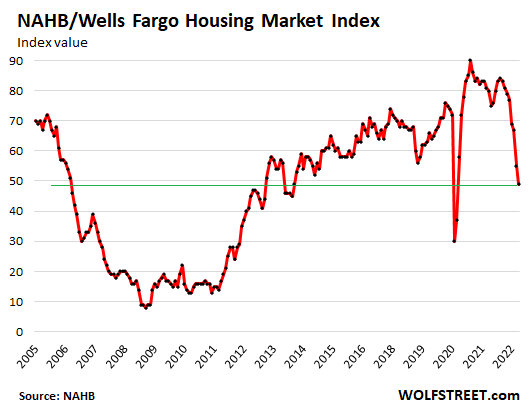

The confidence of builders of single-family houses, after the second-biggest plunge in the data last month, fell again in August, the eighth month in a row of declines, having gone downhill every month this year, “as elevated interest rates, ongoing supply chain problems, and high home prices continue to exacerbate housing affordability challenges,” according to the NAHB.

With today’s index value of 49, the NAHB/Wells Fargo Housing Market Index is now back where it had been in June 2014, and below where it had been in April 2006, at the eve of the Housing Bust.

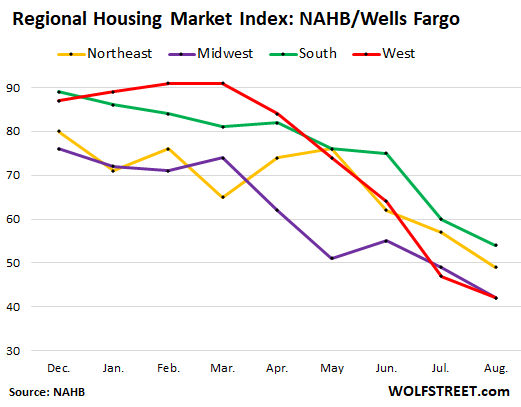

The NAHB/Wells-Fargo Housing Market Index has plunged across all four regions so far this year, but unevenly, with the index hitting the lowest levels in the Midwest and the West, and with only the South still being above 50 if barely. Note that in the West (red line), after still rising early in the year, the index has plunged since March from 91 to 42. Chart shows from December through August:

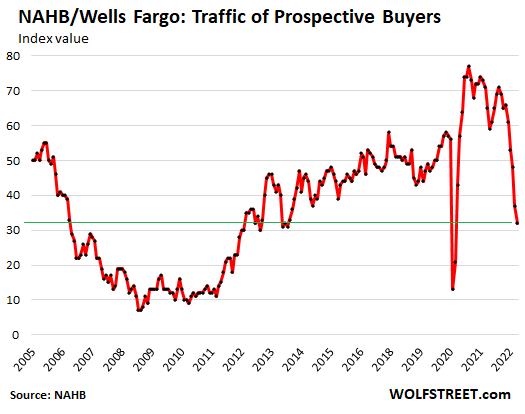

Traffic of prospective buyers plunged.

“And in a troubling sign that consumers are now sitting on the sidelines due to higher housing costs, the August buyer traffic number in our builder survey was 32, the lowest level since April 2014 with the exception of the spring of 2020 when the pandemic first hit,” the NAHB report said.

Traffic is an indication of interest by buyers. And with the headwinds buyers face, including sky-high prices and 5%+ mortgage rates, they’ve lost interest:

Homebuilders cut prices to prop up sales and limit cancellations: 19% of the builders said they cut prices over the past month to “increase sales or limit cancellations,” the NAHB said. This was up from 13% of the builders who’d reported having cut prices in the prior month.

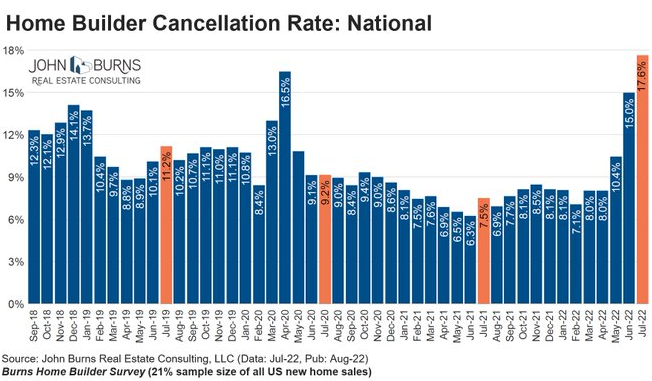

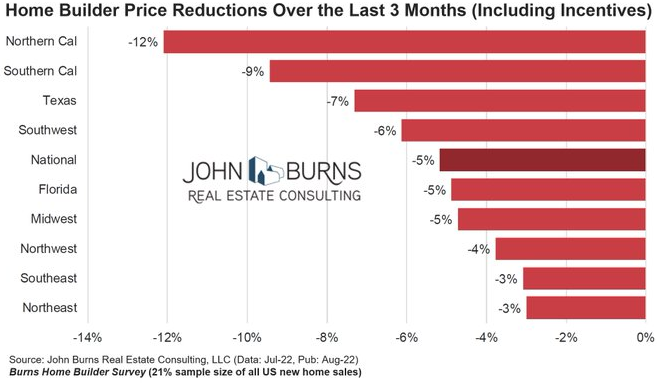

In terms of cancellations: Based on data from John Burns Real Estate Consulting, the cancellation rate homebuilders experienced in July, despite their efforts to limit them by cutting prices, spiked to 17.6%, out-spiking lockdown April 2020 (click on the image to enlarge):

In terms of price reductions: They’ve started sooner and faster in California, Texas, and the Southwest, according to John Burns, for the three months through July. The price reductions include incentives:

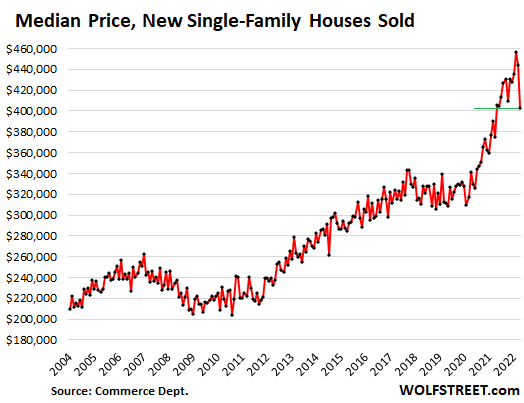

The Census Bureau reported earlier that the median price of new single-family houses sold had plunged by a combined 12% in May and June:

The NAHB index for current sales has dropped every month since February, and in August dropped 7 points, after the 12-point plunge in July, to a value of 57. A value of over 50 means that still more builders rated current sales as “good” rather than “poor,” and price reductions would certainly help.

Future sales look worse: The NAHB index for sales over the next six months fell by 2 points, after having plunged by 11 points in July, to an index value of 47, the second month in a row when more builders rated their future sales as “poor” rather than “good.”

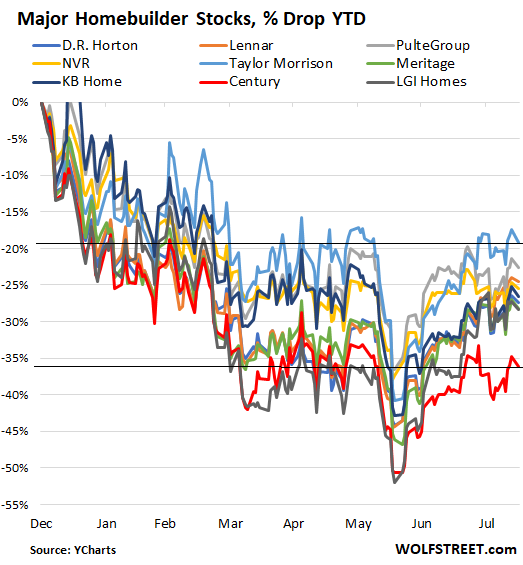

Homebuilder stocks, despite the blistering summer rally, are down between 19% and 36% so far this year, including between 0.8% and 2.1% so far today (data via YCharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Home Construction ETF (ticker: ITB) was down about 42%. Granted it is not like the +80% drop back 2007 to 2009.

Home Depot is down about 25%, and it recently bottomed at 38% below its 52 week high.

Almost everything is overbought. The market needs to pullback some or trade sideways.

ITB down 42% from when to when? At $62 it seems extremely bloated to me, especially since this drop in sales is not factored into Q3 builder earnings. I say ITB will be sub $50 by mid Sept.

All these declines have to be weighed in the context of the moronic run-ups that occurred in 2021 (and in light of the fact that equities were already overvalued by 40% from, say, 2015 thru 2019).

20 years of ZIRP asset price inflation means that things can fall a long, long, looonnng way.

Simple question – at what point does the drought in the West cause real estate prices to collapse in places like Az and Utah?

Is that why we are seeing larger price declines in these areas?

How does that ripple through the economy when millions of people then claim ‘act of god‘ and don’t pay their mortgages because no one will buy a home that may not have access to water?

Massive banking collapse?

Jvp,

It’s not the cities that use up most of the water, in California for sure; it’s agriculture. Probably the same in Arizona, Utah, and maybe Nevada. And that food that is being produced with irrigation gets shipped to other states and other countries. So it’s kind of important.

In CA, cities use about 20% of the water, and there will be plenty of water for cities because we can build desal plants, but it’s going to be EXPENSIVE water for showers, etc. People are going to have a cow when they see the bill for filling up their pool with desal water. There is already a desal plant there. There are other problems with desal plants, not just costs, and cities will have to learn how to deal with them. Recycling of waste water (reclamation) is already being done in cities. So cities can get enough water, it’s just going to be very expensive.

But ag is different; ag in the West needs cheap water. Ag is a HUGE business in California. They grow just about everything, high-value products, not just commodities, that people across the US and the world eat and drink. So the drought is impacting food production a lot more than it impacts housing.

What upsets me about this….we were headed for something like a mini version of this in 2019. The Fed’s action in 2020 and beyond did more than just stave that off, it drove a massive bubble on top of what should have been a declining market. Twice as bad.

Oh, BTW, housing shortage! Crisis!

The analyst at MS is comparing this stock market rally to 2019, after the Fed pause (which is sort of priced in right now). There was a recession looming at the time, and some were criticizing the Fed for loosening policy ahead of a slowdown. We don’t know what happened then, because of the pandemic. The difference now is several trillion more in the money supply, and the precedent of mortgage forbearance, and other Fed tools should the recession prove difficult. I think you’re right about the Fed bubble on top of the market slowdown, call it an inflation bubble. Banks are still sitting on excess reserves. Nothing goes to heck in a straight line, including housing prices. WFH tends to cancel some lower value demographics. With tight labor demand, falling mortgage rates, and home builders cutting prices. Do you really think growth and inflation have peaked? Recessions are traditionally periods when business puts money to work, and this one maybe doubly so.

So what if inflation has peaked at 9.1 percent, currently at 8.5%. Even if it goes down to say 6-7% in next few months, it is still quite above Fed’s target inflation rate of 2%.

I don’t see why Fed would pivot unless something bad happens.

Because they are first and foremost a political institution, not an economic one. They are beholden to the desires of the banks they serve and the government (FOMC), with the state of the economy being a tertiary concern, despite lip service to the contrary. Chances that they hold their ground past next March are slim, and markets know it.

Exactly right Gattopardo, and you’re not alone in your frustration. We were going to be weened off of QE/ZIRP, and markets were correcting like they should. I was getting ready to dust off my house-buying hat as prices were flattening out and even coming down a teeny tiny little bit going into 2019. Between gutless Powell’s U-Turn and the Fed’s pandemic printing-fest, the chance of homeownership here in southern CA quickly faded from being a real possibility to something that only exists in my dreams now that a shack in a rough neighborhood is $500k+ and anything even remotely nice is more like $700k-800K.

A third of all the dollars ever created were created in 2 years, which is bonkers. The Fed hasn’t removed a meaningful amount of those dollars, and we wouldn’t see anything that even resembles sane pricing vs. income in various markets for a long time unless they do. But they won’t. They’ll run a little QT and maintain higher (but still historically low) interest rates until the job market starts to show stress signaling an actual recession, at which point, they’ll back off pretty quickly. Things didn’t become more valuable. The dollar has simply lost value, and that value is never coming back… We’ll see disinflation, but deflation is not an option. Deflation is something far more terrifying for the Fed than inflation.

That I’m not sure about. I think to a large degree the Fed has been exposed. If the $5 million they printed in the past 2.5 years isn’t removed, then they’ll never be able to print money again, as everyone will know it’s permanent.

Part of regaining credibility is removing that money.

Einhal,

I wish we had a central bank that actually cares about credibility, but they don’t seem all that worried about their image. Even if Powell sticks to his guns, the Fed’s plan is to run off $95B/month for perhaps the next couple of years. That would only be half of the $5T that they added to the balance sheet at best, and it will still take a while to get there. My suspicion is that enough cold water will have been thrown on the labor market to kill demand and bring back lower inflation long before they ever come close to reaching a couple trillion worth of QT. Once they have some breathing room and they can claim that inflation is abating, they could taper QT down or stop it altogether. I don’t think this debt-based economy can handle very much QT before the wheels start falling off. It really all hinges on jobs… The Fed will maintain QT until it starts having a noticeable impact on those 10-11 million job openings, a significant factor driving inflation. If job openings turn into layoffs and unemployment blows up, look for a Fed U-turn.

From DC’s perspective, idiotic asset inflation wasn’t a bug, it was a feature (“wealth effect” to kickstart 20 years of essentially moribund employment growth)

Yeah, the problem with that as we’re seeing is that “wealth” is not evenly distributed among the population. A small percentage has nearly all of it. So the “wealth effect” manifests itself in the rich buying tons of toys (RVs, boats, luxury vacations, sports cars, and so on), while everyone else has a hard time paying rent and groceries.

The problem, of course, is that the extremely wealthy are unable to spend (as consumers in the equation C+I+G+NX) as fast as the lower 95%. How many yachts can you own before it starts to become unseemly? So much for the wealth stimulation effect.

Enough to cause inflation for everyone, it seems.

Well, the counter-argument is that people are employed building those toys for the rich.

Of course, the lobotimized Fed has failed to notice (for 20 years) that those workers are in China.

Everything this is still way above Pre-pandemic highs.

Mainstream media keeps repeating narrative: Slightly lower inflation = lower prices!

Is the Math of majority of Americans so week, that they don’t know difference between first and second Derivatives?

Or is it that they can’t compare prices themselves

Prices are getting lower. Gasoline, automobiles, housing are all going down.

Harrold,

Yes, gasoline has been going down. And home “prices” are starting to head down.

“Rents” are NOT going down — and that’s what goes into CPI.

New vehicles are NOT going down in price. Ram offers some discounts, and a few others do. But on average new vehicle prices are sill spiking.

Used vehicle prices have flattened near record high levels.

Just thinking out loud. Used vehicle prices flattened. If we can get rent to flatten and food prices to flatten, goods and services to flatten, will we be at 0% inflation?

We don’t need prices to drop….just flatten and the FED can say they are successful?

Job market is still hot from what I read. That is still inflationary.

I read Mexico and Argentina raised rates but China just cut rates. The whole world is raising rates except China. China is always hard to figure out what is true and not true.

By the time rents flatten, the prices of gasoline, vehicles, food, insurance, etc. will all be spiking all over again. That’s the nature of inflation. It’s a game of Whac A Mole, it jumps from category to category and then circles around again, fueled by higher wages, borrowing, government deficit spending, high asset prices, ongoing interest rate repression, etc. That’s why inflation doesn’t go away on its own. It just keeps circling from product to product.

In the past year, food is up 50-100%, rent up 15-30% depending upon where you live, new cars (if you can find one) at up 15-20% and some people paying $10-15k over MSRP. I don’t know where it is, but there is a pricing or inflation tipping point where everything crashes down hard. I’m sure we’re very close.

JM,

See my comment just above. It explains how inflation behaves when you let it rip. It circles from category to category and then all over again. Inflation backs off in one corner but spikes in another.

diesel isn’t going down much though. And diesel is what moves the economy.

That and bunker c. Have you seen overseas shipping costs lately? OMFG.

The Drewry World Container Index has plunged, but is still 3x where it was before the pandemic. Shanghai to Los Angeles about $6,500, down from about $11,000 last fall, but up from $2,000 before the pandemic, hahahaha, what a deal!

I just sent out the first batch of WOLF STREET mugs. Shipping costs from my door to your door have jumped 23%, FedEx over the past 18 months or so. All my other costs of the mugs have jumped about 25%, except those costs that have jumped by 50%.

Be patient.

It’s happening.

As a former HS teacher of construction tech, I can testify that half of the students, ( program required minimum age 16 and some adults,) did not know basic fractions SS, much less anything to do with ”first and second Derivatives.”

Most of them learned very quickly when the ”problem” became how to lay out ballesters/pickets for a stair or deck, etc., but they told me they had had no interest in ”math” because it was ”not relevant.”

I made the teenagers figure out how they were going to live on the $10/hour wages they could expect, with budgets, etc.

Opened quite a discussion in class, especially when they realized how much $$$ they would actually have to earn to live the lifestyle they wanted…LOL

That’s the result when a noticeable part of an entire generation grows up in a household where they don’t know what it’s like to do without. They have no clue.

Because we’ll be better off when finally all kids are doing without more often?

eg-think AF’s point is that it doesn’t take too-many generations of prosperous living without serious remembrance/reflection for a people to forget/never know how they got to that dance…

may we all find a better day.

There’s always SIRI. Just ask, you’ll always get an answer. People under 30 have been conditioned not to think. And it worked.

‘but they told me they had had no interest in ”math” because it was ”not relevant.”’

—

There was a saying in the 90s I’ve not heard recently: ‘Only in America is it OK to say “I’m bad at math.” ‘

I actually had a student tell me that his financial plan to get wealthy was to win the lottery multiple times.

JJ-my former quasi-stepson (’90’s) was convinced if he followed GQ closely and ‘dressed for success’ that the highway to CEO-ship was wide open. (He, like many of the young (once was, myself as i recall), eventually figured things out…).

may we all find a better day.

seems to be a lot of bad/disconcerting news BUT stock market is flying- !crypto is flying ! adam neumann of wework fraud just got $350,000,000 for a new fraud and a valuation of on his new fraud of $1,000,000,000 – so there is a lot of doom and gloom but a LOT MORE of “to the moon”

“adam neumann of wework fraud just got $350,000,000 for a new fraud”

Kinda makes you wish you could short Andreessen Horowitz, doesn’t it?

It’s called SPACs. You missed it.

“With today’s index value of 49, the NAHB/Wells Fargo Housing Market Index is now back where it had been in June 2014, and below where it had been in April 2006, at the eve of the Housing Bust.“

Nice. Now, if we can just fuel this sentiment into an absolute train-wreck in housing, across all types, that’d be great. At least for me. That way, I could cuss the FED for raising rates still making housing unaffordable for me instead of prices making it unaffordable.

The housing bust took 4-5 years to play out. You gotta be patient. Housing isn’t a crypto chart, it doesn’t give you instant gratification, though Zillow and the like are sure trying.

Wolf,

What do you think about “for sale inventory” as being one of the best quick turnaround metrics for SFH trends?

It goes right to the heart of the supply-demand equation.

And Calculated Risk has been able to report it weekly. Kinda hard to beat that for speed.

“For sale inventory” = “active listings,” and Calculated Risk gets this data from the NAR, which I report on monthly, and if you read my articles, you would see that, and I could report on it weekly, because the NAR releases weekly data, but it doesn’t make sense for me to report on it weekly because the moves are too small and uneven.

Months supply = active listing divided by sales in that month, which I report on monthly as well. All you have to do is read the articles:

What is your take on the collapse of First Guaranty Mortgage on Monday. They shuttered their doors. No restructuring. $10.6 billion in loan origination last year. Is this the canary in the coal mine? No one is talking about their fall.

John,

When 60% of your business (refis) disappear, what are you going to do? These companies just originate the mortgages and sell them, and they make money off the difference and off fees. Refis were a huge part of that business. And now it dried up. No refis, no fees; and no revenues from refis.

Mortgage lenders worth their salt normally see this coming and know how to ride this out via layoffs, cost cuts, etc. before it’s too late.

But Guaranty Mortgage had also other problems. It got stuck with some mortgages whose value dropped while it held them (as mortgage rates suddenly spiked) and when it sold them, it lost money on them. And it didn’t have enough of cushion to absorb the losses.

BTW, this was chap 11 bankruptcy filing = restructuring, if possible.

We have seen mass layoffs in the mortgage industry since late last year when this started. It’s the refi business that collapsed due to higher rates.

Lots of houses around the country for $10,000. Many in beautiful places where you can kayak and ski and hike and hunt and fish and free climb…many many other actual things instead of watching Netflix in some cookie-cutter’ ‘Town-Center-USA. Even better, get a small piece of land which is basically free in many places and a hammer and a saw and some nails and some wood, sitting in dumpsters all over Arlington VA on tear-down infill projects, windows/ doors/trim at recyclers for free and BUILD a small house. Our system of consumption has literally destroyed planet Earth, this whole Ponzi fraud of how our government is operated for the ignorant masses is THE PROBLEM- you just need to learn how to live properly and then you can afford literally Paradise.

“I intend to build me a house which will surpass any on the main street in Concord in grandeur and luxury, as soon as it pleases me as much and will cost me no more than my present one.”

– Walden

Well said!

It will be interesting to see what the median price of new homes will be next year since new home purchases have dropped off a cliff. Builders need to lower costs more.

Builders have taken massive advantage of ZIRP over 20 yrs to double prices beyond their likely true costs.

That certainly was the case before the pandemic dislocations.

As with auto production over the last 20 years, producers simply appropriated all the “affordability empowerment” by doubling prices while ZIRP held monthly pmts constant.

In an alternative history, true product affordability could have been massively increased via ZIRP but consumers were too ignorant to negotiate for it and suppliers too ruthless/collusive/short sighted to offer it.

Generally speaking for Southern California at least, Public Home Builders are in a competetive bid environment to acquire either paper or finished lots. Many don’t take the entitlement / development risk on raw land. Profit Margins are usually in the 10-12% range. This is how they come up with the price they offer on the land. Sure, they have benefited from upward movement in home values over the years but some people get this idea that builders are making obscene profits when it’s a pretty standard margin for most businesses.

Land Developers, on the other hand, do occasionally make huge profits by taking big risks on rezoning a property, securing entitlements, final engineering, assembly of multiple parcels, etc. Much of the hot money from these high prices ends up in the land owners’ pockets.

Also, Cities have continued to increase development impact fees dramatically. I’ve seen some as high as $100k per home in my limited experience.

I’m not saying there isn’t a sickness in housing prices and asset values in general, quite the contrary. It’s just not as simple as it seems.

Now here’s a guy that knows what he’s talking about versus some of the other comments.

GS-and referring to the West, the water to sustain that ‘development’ usually came from somewhere else, delivery systems paid for by someone else (whether $ or sale/loss of local water rights and local water), and even then, @below cost, with no serious longterm view of the effects of so many moving in…

the profits were lovely for some, though.

may we all find a better day.

The same is true in Canada. In two thirds of Canada a new house runs in the 2 to 4 million dollar range and the only buyers are the Chinese. The Chinese only buy into rising markets not falling markets so now there’s no one buying any new housing stock except at the very lowest levels of the condo market.

With only the first five years at a fixed rate on a mortgage, variable after that, I don’t know how anyone can afford to own a home in Canada without an inheritance or by winning the lottery.

Suppliers need to lower costs more. ABC and L & W are making bundles off of mispricing.

No they don’t. And they really can’t anyway. In the end, prices reflect how much fake money central banks have printed to avoid the truth of the 40-year Ponzi scheme. And this is the first cycle where the Fed is no longer in a position to bail out the binge TV Watchers, wasting their lives instead of learning things like battery chemistry and how to participate in the biggest ‘Industrial’ Revolution in history, beginning now and running for the next 50 years. Collectively, people are intellectually weak and lazy. Nowhere near doing the work to understand how to improve their lives from an actual economic reality basis. A previous commenter said it well, teaching the dumbest of the dumb some basic technical skills and hearing that the students don’t think math is relevant is Who We Are as a society born of our system. There needs to be some pain and a big reset and climate is going to cause it starting now.

How unfortunate. I’ve always thought we really need to have more big companies that specialize in building Conestoga wagons ’cause it’s imperative to have ten million more people dragging a freaking pianola across the Oregon Trail. How else are you going to have a functional economy unless you keep doing something the same way into eternity. And there’s no end to the number of potential farmer wannabees. And lots of future lumberjacks ready to follow on their heels. Besides, we need a good reason to get all those pesky natives out of the way…buffalo steaks on the menu, crazy fools! Moar houses, moar roads, moar conjestion, moar debt, yeah! Less solution, less production, less profitable work…it’s the only way to get rud of that insane idea that savings represents profits made. Let’s keep blowing what we don’t have on funding what we don’t need…sh*t shacks aplenty…it’s the only way to have moar. Gotta keep ’em reproducing or there will never be any shortages to drive up prices. That can’t be good.

Hahahaha. EXACTLY.

This data underscores the bad call made by the Fed in assuming inflation was “transitory”. By not increasing the rates last year, home prices got driven up to the point where most people cannot afford a home even at a mere 5% interest rate. The real estate market needs more than a reset, it needs to crash.

It wont crash until the stonks & crypto crash, and there are layoffs. We may never get there.

True, but then we’ll end up with a glut of homes on the market and some builders will go out of business or only be able to build for the wealthy. We need builders like Joseph Eichler of the 1950s, who built great, affordable homes for the masses.

“great, affordable homes for the masses.”

Will not happen. I don’t think today’s governments allow any thing that helps the masses.

Butter — exactly. People used to be able to build their own homes. Now there are a number of regulations in place to virtually guarantee they can’t, to force people to out source work so a bunch of unnecessary parties can take their skim. They call it, “building a strong economy”, Lol! Sounds more like communism to me.

JeffD, My County – the 2nd wealthiest in WA State has an exemption for owner builders that only requires a “life safety” inspection for things like smoke detectors, hand rails, guard rails, etc. there are no structural inspections. This route limits your ability to finance or resell the property. I built my house with a standard permit in full compliance with the 2018 IRC and fully engineered even though I didn’t finance it and don’t plan to sell it.

Jr, unfortunately this is the exception, and not the rule, and as you said, permits are still required. Even rural Alabama requires permits.

Coastal counties and municipalities in Mississippi require permits and inspections and certificate of occupancy for anything bigger than a shed. It’s not who you know anymore.

Quite rightly, as people will build anything you let them get away with. Overhead imagery tracks unauthorized construction and an inspector shows up. Homeowners permits are very limited and electrical/plumbing/HVAC must be licensed/bonded/insured everywhere. Rules are loosened for hurricane repair sometimes to get vital businesses open again. The inland counties have an evil reputation for obstructiveness and I never go there.

Millwork from Brazil isn’t coming down much, I spent over $70 in materials to case a window Sunday. Unaffordable for the average homeowner who can’t do it themselves.

butters

Stonks keep going up on the power of perception and hope of an early pivot.

This will go on until the next rate hike in September. The ultra dovish Fed is very well on record to be very accommodative to the Mkts.

Until this changes in ‘action’ not just rhetoric, Mkts will keep on marching, whether one likes it or NOT.

This is why I don’t really trust Mr Bowell. He’s not serious about taming the inflation. He has to crash stonks/houses/cryptos. If he’s serious why can’t they do even a 25 basis points hike this month? Ofcourse he won’t.

Fed raised rates by 75bps and is on path for balance sheet reduction to the tune of 95 billion dollars/month.

We’d come to know if Fed has been serious about taming inflation in Sep.

Let’s see what does the Fed do when the current inflation is at 8.5% and their target inflation is 2%ish

Till then, it’s all speculation.

The FED’s “soft landing” = take their sweet time with everything they do to allow speculators to continue their despicable gambling. The FED should be abolished for what they’ve done.

Yep. As long as cryptos are being pumped, that means there is still plenty of liquidity sloshing around.

honestly it doesnt look like stocks gonna crash, look at it on friday and today, its unstoppable.

When the last bear throws in the towel, it crashes.

There’s too much liquidity. They printed too much.

👍

A long time ago the US dollar was gold backed. Today the US dollar can be considered real estate backed. At least partly. A real estate market crash can be interesting.

Right on schedule. Believed it would be this fall that we would be headed into recession ( at least on the housing side ).

I remember 08 & the fed telling how long it took for rate increases to have an impact. Thankful to be debt free this time around. Might be able to find some good deals on used/new equipment.

We are nowhere near a recession yet. The amount of money sloshing around is mind-blowing.

I’ll take my 30+ yrs in the industry v.s. any media.

Experiencing it in real time v.s. #’s from a month ago or later.

In 08 we were told housing could not take down the economy.

It was the banks. We will see soon enough if its only the housing industry that tanks.

When “The Great Recession” hit, it was completely obvious. My whole area just shriveled up and died. Leading up to it, traffic was way down and you could tell it was coming.

Right now I have never seen so much traffic. You can’t do anything without fighting crowds. This is not what the beginnings of a recession feel like.

…but wait, the National Realtors said the exact opposite earlier in the year. What’s going on?

Rest assured, Djreef, it’s a GREAT time to buy!

“ Traffic is an indication of interest by buyers. And with the headwinds buyers face, including sky-high prices and 5%+ mortgage rates, they’ve lost interest:”

Can’t make any easy money…

The greater fools have already bought…

Great Wells Fargo I love it I bought a few Repo’s from them “Direct ”

Those Charts tell it all now just sit until they get ancy like 2012 > Now with the Water problem in Las Vegas and southern Ca things are really going to cook

i’ve heard a lot of people say home prices won’t crash, that it’ll take 5 years to bottom out. i think that’s recency bias. if we look at how fast home prices went up compared to other bubbles, it can certainly crash cause they’ve never went up as fast. up to the fed really…

Totally agree. This time if things unravel in housing market, it’d be fast unlike last time.

Jon,

This makes me wonder if this is a record, per the chart above.

“the median price of new single-family houses sold had plunged by a combined 12% in May and June…”

Using Zillow’s Zestimate on a variety of off-market properties in the Austin metro area, prices are already down 9-11% from their peak valuations (May 2022). That’s quite a drop in such a short period of time.

Bet the prices reductions in the SE increase. The buyers of homes in areas we looked at were from CA, Ill, and NE including PA, NYC and Beantown. We visited Reno not long ago. The homes in Spanish Springs north of Sparks and the 2,000 SF homes were near $700k. The median HH income in Sparks is sub-$40,000 a year. Buyers were not locals. Once the exodus stalls when sellers cannot sell in high-priced areas, the tertiary markets will crater. That’s our thinking and I’m sitting on my hands until prices come way down. In our target market, no more multiple overbids and some price reductions but not like I expect in the future.

Every market is different and regional.

This has been such a weird housing market because of covid, low interest rates, low housing inventory.

In my area, housing inventory has been running up all year but fell in July. But so have prices.

The following YOY numbers are July 2021 to July 2022.

1) New home inventory is up 65% YOY

2) Existing home inventory is down 10% YOY

3) New Home Prices are up 22% YOY

4) Existing home prices are up 18%

Anyway, it is really hard to determine how good any sales number are because I equate the current prices this year to a stock with a flow float of outstanding shares. Small demand for a stock with low float can cause prices to shoot up, but also can cause prices to crater quickly. Maybe the spike during the pandemic is partly low float…maybe or maybe not?

Some is certainly inflation. If input cost go up, so does the finished product.

Also, we really never had this type of dynamic range of buyers. The historically mom and pop home buyers, historical mom and pop land lords. Plus now we have short term rentals (AIRBNB), Wall Street Landlords because of the MBS backed by GSEs, foreign landlords because of the internet and just click to buy a house, and foreign investors looking for a safe store of value.

We probably never had this many new entrants competing for real estate before at the same time?

IMO, ” We probably never had this many new entrants competing for real estate before at the same time? ” Is correct ru.

Based on GUV MINT statistics, it appears the flower duh state is GAINING approximately 300,000 ”NET” people per year; 850 PER DAY is the current balance.

Many of them apparently NOT moving from high tax and /or dangerous and/or HCOL places, “Up North” in USA, but from other many countries as mentioned earlier.

How this can continue in a place that is SO free king HOT most of the year without continuing and even more massive destruction of environment and resources is amazing.

Every market is pumped up by cheap money.

No market is left alone as cheap money was omnipresent.

If the cheap money is withdrawn then It’d impact all market

FOMO

I am a residential appraiser and can tell you point of fact…..homes will be down 10-20% in the next 60 days. )Depending on when the Gov finalizes the data) from N Texas. It’s OVER….there are no new loans coming into the pipeline in August and 50% decline in July. Rates may have an impact but the entire PSYCHOLOGY has changed in housing. Lowering rates will NOT correct this issue.

Thanks

Housing is all a game of psychology.

The social media helps form the psychology both ways..

Thanks Brian for sharing the latest from the field!

And you are spot on re psychology

some of us here have been arguing for quite a while this will happen – opposing others saying prices can not come down because of this and that

now it appears we are finally there :)

Some SoCal communities are allowing residential to water 10 minute watering per week (total) for grass. That is down from 15 minutes. That will kill yards quickly in this desert. So the cost of housing just increased to put in artificial turf or equivalent. Two friends just had to get emergency Air Conditioning replacement installed, both were over $15k. Both AC jobs were available same week.

Home ownership has some serious down sides as well

I’ve said it before and I’ll say it again – houses are money pits. I know some people whose well just went dry and they are having to have water trucked in. The cost to hook up to city water is approaching $75,000. That pays a lot of rent.

Why not xeriscape?

c h-‘…because my freedom and sense of aesthetics supersedes any piddlin’ situation the planetary environment lays on me…’ (/s).

(or, ‘…sure! but you, first…’).

may we all find a better day.

“Just thinking out loud. Used vehicle prices flattened. If we can get rent to flatten and food prices to flatten, goods and services to flatten, will we be at 0% inflation?”

No, totally wrong. Inflation is approaching 20%, 45 year high. Prices would have to drop significantly to be at 0%.

The stock markets are now addicted to the same QE fed low rate environment that existed for more than a decade (2008) and so has the housing market. the Fed is saying this time is different but the money has not been removed (qt) yet and will take some time.

Moves in any asset take time to adjust to a new realities and in this case we have QT on top of the weak markets.

So goes housing so goes markets

I know it is a one off but I saw that Sedona, AZ is proposing to pay landlords up to $10k a year not to do short term rentals but instead do long term rentals to residences.

Well, that seems inflationary. How many people are going to try to take advantage of this buy turning a home in to rental.

SEDONA, Ariz. — The city of Sedona is willing to pay thousands of dollars to local homeowners who offer long-term leases to local workers who can’t find a place to live.

A lack of affordable housing in the area has prompted city officials to allocate funds for a pilot program that incentivizes homeowners to stop leasing out their homes to visiting tourists.

On Tuesday, the Sedona City Council approved spending for property owners who currently rent out their homes through short-term rental services like VRBO and Airbnb.

The program would pay homeowners anywhere from $3,000 for a single bedroom all the way up to $10,000 for a 3-bedroom house. In exchange, the homeowner would agree to rent to a local worker for a one-year lease.

“You’d be really hard pressed to find anything for rent under $2,000,” Sedona Housing Director Shannon Boone said. “With gas prices rising, we can’t keep expecting people to live an hour away.”

“With gas prices rising, we can’t keep expecting people to live an hour away.”

SURE THEY CAN,,, just exactly like many of us manual workers did in the 1950s in many areas of FL that did not want ”those people — workers” living near them that I know from personal experience.

It was called car pooling, and sometimes big old cars would have 10 people in them riding an hour or so to work. Driver got ”gas money” from everyone, a dollar or so a day, when $1.25 was minimum wage and what most of us got paid.

Suicide in Sedona. Sounds like a country western song.

Most of the rental market is very happy to have AIRBNB instead of long term traditional rental. Why? Because the tenant pool is destroying the property on purpose. They do not care and they don’t treat the rental unit as their own home. There are exceptions to the rule, but very few. At the end of the day ALL living souls are tenants who rent from either the bank or landlord.

Unfortunately I think the govt precedent of rent moratorium will defer many landlords from going that route.

Long-term rentals became a problem where I live (usually one-year agreements), because many renters are waiting to purchase a home, and the rental agreement becomes a liability.

Hard to time a purchase of the ‘right’ home, for example, when one still has nine months left on the rental agreement.

I guess it’s a two-edged sword.

A 12% price reduction on a $1 million dollar N. Cal home? All this proves is that the price increases were driven more by greed than inflation, despite vehement claims to the contrary. Same thing was/is happening on car dealer lots with fake “fees”.

Builders are deep into houses on the market. Materials and labor have been unbelievably crazy high, these two factors weren’t that much in play during the 2005-2010 housing crises. Builders may not have much margin to play with for long before going into the red.

This is going to be nasty, there is a long way to drop. Proud owners of homes bought in the last two years all stand to be underwater with their mortgage before long.

“price increases were driven more by greed than inflation,”

Warren said the same nonsense. Consumer price inflation = price increases across the economy. The question is why? The answer is at least in part: the inflationary mindset of the buyers.

When the inflationary mindset kicks in, companies get away with these price increases, and their suppliers get away with them too.

Every company always tries to get the maximum price for its products and services, while still obtaining its sales goals. If there is enough demand, it will raise prices, and if demand doesn’t sag after raising prices, it will raise prices again. That’s always how it is. But usually, the company doesn’t get away with it; usually, sales fall when the company tries to raise prices.

But now, as the inflationary mindset kicked in, price resistance has largely gone away. Only when price increases got too huge, price resistance came back, and there was demand destruction (gasoline, used cars, etc.). But there is still no price resistance in other products, and consumers and businesses pay whatever. That’s what is happening now.

Let’s hope The Fed is listening to what you just said.

I guess I wonder who these “pay anything” people are. I have been battening down the hatches, refusing to buy anything other than the bare necessities. I’d rather never buy another vehicle than pay these ridiculous prices. I think what I have could last the rest of my life, so that’s an option.

Yes, if the majority of people were like you, this inflation would be OVER!!!

Yeah same here, don’t know if we should call it a “buyer’s strike” but us and our neighbors have been so annoyed at these stupid price run-ups that we just refuse flat out, to buy anything we don’t absolutely need right now. (And even if we do need it, we still try to make do, barter, find used parts or whatever we can do to stave off purchasing at these nose-bleed prices)

We can handle it OK but it’s a shame for esp the younger people who may want to make key purchases but feel trapped at these inflated prices. Our son and his wife have wanted for a while to buy a home and start a family, and they make good money but cost of living where they are is totally out of control and even with recent drops, home prices are way, way beyond what incomes can support. And they can’t “just move”–his job is very specialized and not many places have it.

They’ve already been seeing some of their Millennial friends who “took the plunge” now underwater with the homes they bought in the past 3 years, and for both strategic reasons and principle they don’t want to jump in and buy a home. It was just stupid beyond belief for the Fed esp to use QE to inflate the housing bubble or in other necessities like healthcare and college. If a country wants to create an asset bubble, at least do it in trivial things like tulips or crypto where only the speculators really get burned. Another reason we’re likely in store for a huge recession early in 2023 as things tighten, but it’s the only realistic way to cleanse away these asset bubbles. Paul Volcker knew well what he was doing and it was the only way to do it.

Last week I stumbled on a Small Business Administration website that enables one to download CSV files of their database of all the PPP (Paycheck Protection Program) loans they made during the pandemic crisis.

Importing them into an SQLite database and running some queries, I find that in the Zip code of the light industrial park in the far Chicago suburb in which I own a “man-cave” office/workshop, the SBA doled out nearly $70 million in loans, and has forgiven about $65 million (Google “PPP loan forgiveness” to learn how that works).

The population of this Zip code is about 17,000. The number of jobs reported was 7,231 (some of the companies clearly employed people outside the Zip code). About $10,000 per reported job.

The number with ForgivenessAmount > $150k was 151.

The total forgiven for those loans was $52 million.

A very large fraction of these loans went to firms doing the kind of home renovation/construction work that, IIRC, was booming during the pandemic, so I find it rather curious nearly all the loans were forgiven. I wonder how much of this money found its way into the stock market, and into conspicuous consumption.

It’s all a shitshow.

The Fed is “raising rates” to “curb inflation” and then they turn around and finance all these “loans” and gubment programs that basically mean free money through debt that will never be repaid and everybody knows it.

It will and has to end in hyper-inflation. There is no other way. While the paper casino for gold and silver is terminally broken with silver being in backwardation now for months, the real stuff is flying off the shelves like hotcakes. When it becomes unobtainium, things will get interesting.

This is good information. Thank you. I’m sure there is a pile of fraud.

Individuals and companies received sooooo much money during the pandemic. PPP (1&2), County CARES Grants, Restaurant Revitalization Grants, Low interest COVID-19 Loans from the SBA…

I own a small business, and we entered the year more flush with cash than we have in any of the prior 8 years in business. For the first time in 8 years, I do not worry about keeping our bills paid, I don’t worry about equipment breaking down…because I have the largest financial buffer ever in the existence of my company. Businesses in the US are flush with cash right now!

I personally think this is where most of the inflation originated. Small mom and pop, sole proprietorships, small businesses of all kinds went on a spending spree…all that money is being passed around and everyone feels rich.

Thanks for posting this, reading about stupidity like this just makes me hopping mad. It was clear fraud, abuse and corruption with PPP just like many of us warned, and there need to be more investigations but these jerks who ripped off the programs and the US taxpayers for, what looks like trillions just get a jubilee walk away tax-free. Truly makes you think the US budget deficit and the dollar itself are just funny money.

If they’re going to forgive the debts of all these PPP fraudsters, then the USA should also be forgiving at least the medical debts of Americans stuck with medical bankruptcies. Not just for moral reasons (healthcare is stupid expensive here), but hey as the PPP debt jubilee itself, the US budget deficit is just a number, no big deal if it goes higher and higher, right? And people stuck with medical debt for ex. car accidents or diseases they had no control over have a far better case for debt forgiveness than these PPP scammers who deliberately ripped off taxpayers. In fact, these revelations about the PPP are even making me more sympathetic to the idea of forgiving US student loans. That’s what happens with moral hazard like this.

I was initially dead-set opposed to the idea, my wife and I had to pay back every penny of our student tuition debt with interest, but again even students with student debt have a much better case for debt forgiveness for their loans than these PPP crooks. (At least for US students, they often have to take on the debt to get a degree since corporate HR departments these days won’t even look at their applications without them going to college, and even public universities are community colleges are stupid expensive) We’re actually encouraging our nieces and nephews to do university in Europe–they don’t have the “everyone should go to college” mentality there and universities are much lower frills which keeps costs down, so if you’re good enough to qualify and get in there and learn the language, your tuition is much lower, even living overseas you can save more than $100,000 compared to the stupid high expenses of the US these days. But I realize big majority of US parents won’t think to do this. And until Congress and the US institutions cut off the gravy train of student loan money that just leads to ballooning institutions, it’s students left holding the tab for getting that diploma that they need more and more to get considered. It’s a totally broken system–what are we at now, $1.6 trillion student loan debt in the US? It should have never gotten that high, but if they’re going to forgive the PPP ripoff artists their loans, might as well forgive the student loans too. It’s just extra budget deficit numbers on a computer screen, not real money, right?

The PPP thing was disgustingly despicable – just a fleecing of taxpayers in a morally bankrupt, reprehensible manner. Never, ever should you just give “free money” away like that, and mostly to people who never needed it. That’s what set houses’, cars’ and all toys’ prices on fire. These people got free 2nd and 3rd houses, vehicles, boats – you name it.

I could have applied and been approved for a lot of this largesse, saying I was impacted by the pandemic – that’s all that was really required – but I chose not to. I feel like a fool and a sucker for being honest. I don’t think honesty pays in this world, I think scammers rule the day.

two constant views-

“…the only way to win is not to play…” – anonymous

“…of course the game is rigged, but if you don’t bet, you CAN’T win…”

-r.a. heinlein

may we all find a better day.

1) US RE is a global piggy bank.

2) NAHB/WFC, 2012 high is support.

3) NAHB built a for years Lazer between 2014 and 2018, aiming at the top.

4) 2019 high was a failed attempt. It led to the 2020 plunge.

5) In 2020 the market was so hot, the initial break, in 2021 low, was

a harbinger of things to come.

6) After three dots at the top in 2021, the plunge.

7) Seven good years between 2013 and 2020 // seven bad years might come. Inflation will add more pain…

Rate rises (FFR) increase for an average of 2.1 years before the PTBs reverse course. This rate rise cycle started March 2022 so expect the FFR to crest around April 2024. Anyone else notice AAPL closed above 173 within 5% of its all time high of 182.94? As Yogi observed: “It’s hard to make predictions, especially about the future”.

I know it seems like forever, but we’re only about 2 years into the Covid Financial Crisis. We’ve only just begun. It will probably be about 8-10 years start to finish. This is going to be fun to watch for us suspense horror movie fans.

Blackstone preparing 50B for purchasing during downturn. The article I just read has this title (paraphrase). Enough is enough. I am so out of patience with waiting. The American dream is dead.

SOL,

You’re looking at this the wrong way. The media is being braindead about this, just hyping the dickens out of the wrong thing.

These institutional investors are trying hard to NOT overpay. The big investors are now leaving the market, or have already left the market, because it doesn’t make sense to them anymore at these prices and interest rates. They’re going to wait until prices make sense again, given whatever the rates will be at the time; higher rates = lower prices. So just watch when they start buying. This may be the bottom then, or it may be just a falling knife they’re catching. And it may be years from now. These investors have long-term horizons.

When you have access to free money, you don’t care about valuations.

Yes, that is one of the primary problems with free money (interest rate repression). And it’s very addictive to the decision-making process, and leads to awful decisions. Now everyone is squealing because mortgage rates have ticked up a little.

SOL the Chinese seem to be edging out of the US housing market as 1. It’s on a downhill trend and 2. some leveraged money was lost in their own RE fiascos. That 50B of Blackstone’s probably doesn’t make up for that. There is Chinese money in US RE both directly and indirectly where a US citizen is the official owner instead of the person who came up with the money.. So- any estimate of how much there is will probably be way way off. In addition maybe Chinese money invested into US property acquiring REIT companies is slowing down. It would make sense.

Also, subtract some unknown amount of sanctioned Russian monies coming in for US RE. Plus some other unknown percentage of other offshore monies caught in the crossfire of that with FINCeNs new regulations and present psychological incentives.

I believe Blackstone also buys RE in other countries, and I’m guessing some of that is commercial RE including multifamily and residential towers. So the total of money invested in buying SFHs would not be 50B.

But yes, it all still makes it difficult for people to afford shelter and it should be illegal for homes to be investments at that larger level. Our homes do not need to be holding and laundering banks for the world’s ultra wealthy.

Vonovia, the biggest landlord in Germany is owned by Blackstone.

The Chinese only buy into rising real estate markets not falling ones. The Chinese with no grasp whatsoever on value home prices can fall to bargain levels and the Chinese still won’t enter the market as long as its still falling.

Except Chinese are buying farmland now,can’t feed there people .There efficient system only produces half as much per acre as American farmers

Saw that Compass which couldn’t generate a positive cash flow during the boom, expects to be cash flow positive in 2023 so maybe this housing downturn will be just a blip /s

Update to previous comment on Australian real estate:

The upper, high price homes it seems are having no problem being sold with two new records hit in Melbourne.

The house I previously stated that was the highest priced house for sale in Toorak at 17 St Georges Road was sold for just under A$75 million. That is about A$5 million MORE than the high price being asked which was $A65 to A$70 million.

And as this article is about new homes, the highest priced house in Melbourne has also been sold in Toorak at 29- 31 St Georges Road in an off market transaction so it was never listed for sale on any real estate site. The price was $80,000,088.

The house last sold for A$5 million in 1991. (So what is the annual rate of return on that??)

This property has a derelict house on it and will be torn down and a new house built.

So two buyers just spent A$150 million on two houses with the transaction tax due to the State of Victoria another A$9 million or so on top of that………….

Did you guys ever pass those laws restricting SFH ownership in Australia to 1 per foreign owner?

We have federal rules about house ownership and numerous state laws regarding taxation of real estate owned by foreigners or non- state residents or multiple property ownership.

It is all quite complicated.

There is only one real estate “project” in Australia that I know of that allows foreigners (non citizens and non permanent residents) to buy existing residential real estate without regard to resident or citizenship status and that is Sanctuary Cove in Queensland.

Other than a few exceptions, purchase of EXISTING residential real estate in Australia by foreigners is prohibited. And in the few circumstances that it is allowed, it can not be rented out and must be sold within three months of the person leaving Australia.

But the most important area where real estate has changed for foreigners in Australia is the area of taxation and fees.

For a foreigner to buy property they have to apply to the FIRB and pay a fee. (For a house in the A$1 million to A$1,999,999 range the fee is A$12,700.)

Then the Federal government also levies an annual fee in the same amount if the property is deemed to be vacant. This is equal to the above FIRB application fee.

And when it comes to state taxation of real estate either owned or purchased by a foreigner, it is a real mine field.

Each state has their own taxes. In Victoria the foreigner must pay an additional 8% on top of the normal land transaction tax when buying a property. This is called the foreign purchaser additional duty.

We also have an “absentee owner tax” that may apply if you are absent from the state on 31 December. That is an amount of 2%.

And if vacant, the property may be subject to additional taxes regardless if owned by a foreigner or legal resident. That is an additional 1%.

So from this aspect, foreigners buying real estate get soaked.

According to the FRED New Privately-Owned Housing Units Completed: Total Units chart, the number of July 2022 housing unit completions is far below its 2006 peak.

Seeing weakness in demand in an area witnessing a declining population is not the same as watching an area with a growing population.

Single family housing starts were weak, -18% yoy. Multifamily were strong, +16% yoy, maintaining the boom. People keep forgetting that. Article coming.