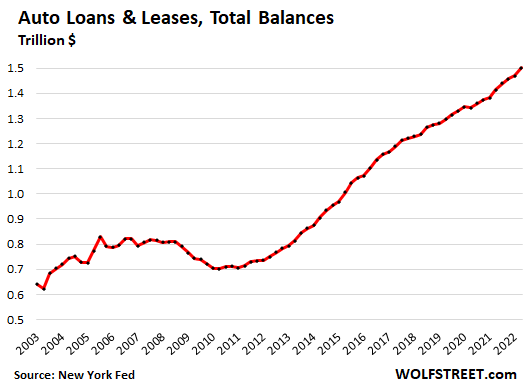

The balance of loans & leases outstanding rose on much higher vehicle prices but much lower sales volume.

By Wolf Richter for WOLF STREET.

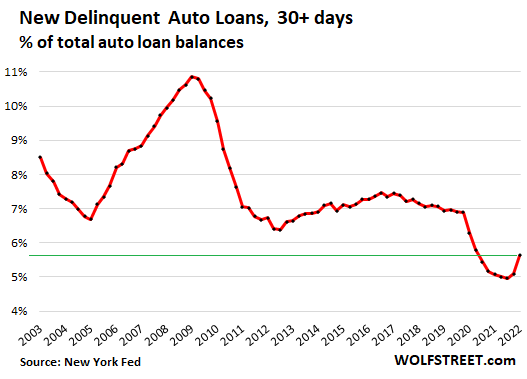

In 2020 and 2021, consumers used their stimulus money and extra unemployment benefits and their PPP loans and the cash left over from not having to make rent or mortgage payments, or whatever, to get caught up on their auto loans. And the rate of auto loans that were delinquent 30 days or more dropped from one historic low to the next and finally bottomed out in Q4 2021 at 5.0%.

Since then, this delinquency rate has started to rise from the historic low. In Q2 2022, the delinquency rate rose to 5.6% of total auto loan balances, according to data today from the New York Fed’s Household Debt and Credit Report. It remains below the pre-pandemic low of 6.4%.

The delinquency rate is now normalizing, heading back toward the old normal, which hovered at around 7% during the Good Times:

Note how the delinquency rate began rising back in late 2005, in parallel with the Housing Bust, more than two years before the recession, because people under mortgage stress also fell behind on their auto loans. The delinquency rate continued rising as the mortgage crisis triggered the Financial Crisis when Bear Stearns, Lehman, AIG, Fannie Mae, Freddie Mac, and other financial firms collapsed (some got bailed out, others didn’t). Delinquency rates peaked in 2009 at nearly 11%, and then backed off.

The delinquency rates during the Great Recession show what can happen when 10 million people end up unemployed at the peak.

Auto loan balances: spiking prices, falling sales.

Balances of auto loans and leases rose 6.1% in Q2 year-over-year to $1.50 trillion in Q1, on much higher vehicle prices and much lower sales volume – meaning fewer loans, but with higher balances.

The used vehicles CPI was up 6.1% year-over-year in June, and the new vehicles CPI was up 11.4%, according to the Bureau of Labor Statistics.

The average transaction price of new vehicles, which accounts for the shifting mix of vehicles, in addition to price increases, spiked by 14% year over year in June, to nearly $46,000, according to J.D. Power data. And these more expensive vehicles needed to get financed, and so the loans got bigger.

![]()

But new vehicle sales, in terms on the number of vehicles sold, in Q2 were down by 21% year-over-year. And used-vehicle retail sales were down by about 10% year-over-year.

So auto loan balances increased by 6.1% in Q2 to $1.5 trillion, on this mix of surging prices and falling sales, leading to fewer but bigger loans:

“Car Repos Are Exploding” Not.

A few weeks ago, an article on a major financial news site proclaimed in the headline that “Car Repos Are Exploding.” The article was circulated everywhere, and yet it was devoid of actual data on repos, it had no chart of repos, and was really just clickbait. Most people who spread this thing around the internet never read the article; they just read the clickbait headline, and that was good enough. The internet is a strange place.

But the entire auto industry and auto finance industry got a good chuckle out of it. Before there is a repo, the borrower must be delinquent on the loan. If the borrower falls behind on payments and cannot catch up and thereby cannot cure the delinquency, the lender will repossess the vehicle and sell it at auction.

So before the number of repos can spike, the rate of delinquencies of 30+ days must spike, because it comes first.

As we’ve seen with data from the New York Fed today, there is no “explosion” of delinquencies, and therefore no explosion of repos. Repos remain low compared to historic levels. They ticked up from the record lows last year and are in the process of increasing to more normal levels.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

No they never spent a cent more then or if required to keep the loan above water.

It’s just a plastic fantastic personal degrading self propelled cart with no next to zero style.

Geeeeze.

It’s interesting the change in American psychology for paying loans.

Pre 2008 – the mortgage came first before any other loans then. Period. The end. Then that changed overnight.

2008-2018 – the car loan came first because you had to get to work and you could always live in your car.

2019-2022 – WFH. Who needs a car. I got internet.

2022. – ATT took a yuge hit because folks are not paying for their internet or cell phone plans anymore. Quite the surprise.

So….what debt takes priority today? I don’t know.

Not paying for Internet and cellular…how do es that work for very long🤔🤔

Poor people that can manage their money go to free tv or radio for entertainment and news when they have to cut deeply. Plus pay based on usage flip phone mame $10 – $20 / month.

many subsidies out there for anyone who cares to claim help these days IT,,, AS it damn shore “SHOULD BEE”” for every USA citizen who has PAID INTO the ”system” for the last 40 or 50 +++ years///…

SO many that it becomes attractive for those of us ”retired” etc. with NO debt…, to at least consider..

poor??? maybe by some metrics,,, but actually living a very very ”rich” live with no debt, couple of very loving ”girlfriends” albeit of the 4 legged kind in my bed along with my loving spouse…

BEST time of my life, so far…

Really and truly HOPING for all folks to have a similarly WONDERFUL experience while ”giving away” everything YOU are com fort able giving..

>Poor people that can manage their money go to free tv or radio for entertainment and news when they have to cut deeply

Darn, now I realize I have been poor for so many years with my $30/mo internet only home plan + $15/mo prepaid mobile on an old cheap Android phone. When I see people making (roughly) less than a half of what I make using fully-financed latest iPhones with unlimited everything plans PLUS all-in TV entertainment packages from their provider for another $140/mo, I just can’t comprehend it. Whatever…

Ignoring the debt for you Masters in gender studies.

This is the same argument as the increase in the use of credit cards Wolf covered a few weeks ago. Wolf argues in both cases that both ‘increases’ simply amount to the return to the previous normal. Yet if people got all caught up on bills during all the stimulus days, the trend is still going up (just from a lower starting point). In theory the trend line should just continue at 5% through 2022 if things were continuing as before the pandemic. We still have to ask ourselves why is it rising again so quickly? From these graphs there is still something seriously messed up going on. As far as I have heard, the credit card balances this month are still continuing to go up also. I think something stinks, and yes delinquencies are exploding in context with the new starting point of 5% post pandemic rate.

Btw, I did RTGDFA!

Gooberville Smack,

I will cover credit card data tomorrow: balances, delinquencies, third-party collections, bankruptcies, and other goodies. You will be disappointed :-]

I understand that it’s a lot more fun to say that everything is collapsing and that consumer debt is exploding and that no one has any money, etc. etc. It makes great clickbait. But that’s just not the case.

Yet they are talking about extending the student loan pause once again. Why would they do this if we are all flush with cash? Click bait? Anyways, I always look forward to your work.

IMO student loan pause is simply a vote buying scheme. If they ever terminated the loans the truck drivers (Teamsters), plumbers (pipe fitters union), electricians(IBEW), and alll other trades would take it out of the Democratic parties hide at next opportunity. No amount of union arm twisting would help.

Gooberville Smack,

What is this BS???? Student loan forbearance is a POLITICAL decision. Student loan forgiveness is a POLITICAL decisions. Buying votes with taxpayer money. Why is that so hard to understand?

As a retired person my credit card usage is way up ,pay everything on card pay one bill . Simple really

Yes, us too, and get 2% cash back which we use to cover Xmas costs annually.

Plus: Using a credit card makes one less of a target for an enterprising entrepreneurial individual to rob you. I used to carry a lump of cash because I traveled for a living and needed tip cash as well as there were times in parts of rural America that they weren’t interested in no stinkin’ credit card. Cash or start walking (a two pump gas station in South Dakota). Since retirement, I just use one card. Everything goes on there and, if someone steals it, cancellation is a phone call away. In fact, the wad that I retired with 5 years ago is still mostly intact (same bills).

AA and EK:

Yep, loving it w the one thin card doing all the ”heavy lifting and carrying” to the mouse click on the ”pay it all” tab once a month…

Also used to carry a couple thousand cash for all the uh , discounts,,, (cash loose in a pocket to be able to throw away without the wallet getting lost.)

BUT, a huge but: I could run really really fast in those days, and still bench twice my weight many reps, etc…… LOL

And love the interest far damn shore,,, somewhat makes up for the lack on the bank accounts.

You should use a debit card instead and put enough money in your linked, checking account to cover your budget. Then, you can avoid the credit card fees and interest if you are late in paying.

Checking accounts can be linked to savings accounts, if you are one of those people whom the banksters’ “Federal” Reserve is stealing the value of their dollars from with their created inflation, like my parents. Credit cards that charge high interest rates should be outlawed or else taxed into oblivion, as should advance loans on paychecks-salaries, unless their fees are made reasonable.

Those are ways by which the banksters and their cronies rob Americans of even more money. Those are ways in which the blood-sucking, parasitic banksters and financiers regularly drain the vast majority of hard, working Americans of their puny earnings with little effort. Usury laws should be reinstated and enforced again. The effective repeal of usury has allowed the banksters and financiers to use the effective guarantees of their own credit from their “Federal” Reserve to get money at ultra-low interest rates then to charge Americans usurious, high interest rates on credit cards and paycheck-advance loans.

Your last 2 articles are great and completely contradict the idea the the economy is not doing well and the market is going to crash. The fed may continue to raise rates but there is plenty of cash flow to support the higher prices. Inflation is not going to stop nor is the fed going to force a crash. It’s going to suck for the bottom 80% but nobody cares about them anymore.

Not sure what you’re talking about. Wolf has been steadfast in his statements that there is “plenty of fuel for inflation” and that inflation will not go away on its own. The place where you are differing is that you are maintaining that the Fed will allow inflation to continue unabated. Wolf is saying that they won’t.

One thing everyone glosses over is that total debt to GDP growth trajectory is unsustainable in the long run unless real interest rates are managed to around zero.

You can always amp up the economy with easy money, but the economy gets addicted to it. If I am not mistaken it was Lee Iocca that started 3 year car loans in the 1960’s.

Average GM car sold just topped $50,000. You will soon be paying $7500 to GM stockholders for your neighbor to finance an even more expensive GM EV.

No one glosses over that. It may be true that total debt to GDP growth is unsustainable unless rates are kept at zero, but the value of the dollar, and thus, the empire, is also unsustainable if rates ARE kept at zero.

There is no easy way out.

Not a delinquency question, but no surge of gramps owner die-offs leading to more used Buicks and Grand Marquis inventory?

Grandchildren have a constitutional right to granma’s car until they can buy a new one. So it will be a while to show up…

Darn.

I want to buy a cheap repo like the old days.

>Before there is a repo, the borrower must be delinquent on the loan. If the borrower falls behind on payments and cannot catch up and thereby cannot cure the delinquency, the lender will repossess the vehicle and sell it at auction.

I recently wondered if in the current market conditions there is an elevated incentive for a lender to strike a borrower with a repo instantly as soon as there is an excuse to do so? (not sure at all how this industry works, just thinking out loud).

I am currently in a process of buying my Toyota lease out and my payoff amount is almost 20% less than what Carvana, Vroom or Carmax are ready to offer me for the car right away. That said, if the market does not take a very drastic turn, I will end up with a car loan with a principal that will be substantially less than the “real” value of this car at some given moment. Now if I was a lender, I would’ve probably waited like a hawk for a consumer to make the very first mistake (e.g. delay a payment for 1 day) and repo the car immediately knowing well I can sell it at a profit or extort any amount of fees from a forgetful borrower.

Again, not sure if it’s a thing at all (hopefully not), but I’m certainly going to put this (and only this one!) loan on auto-pay for the time being…

Yes, with used-vehicle prices still high (except for guzzlers), you’d think a lot of people have “car equity” and can escape repo hell by cash-out refinancing, or selling the vehicle, maybe even for a profit.

Despite that, I bet newly-delinquent 30+ loans will hit 7% again sometime. What’s the WolfPack (commentariat) estimated date when that happens? If it goes to heck in a straight line at the same pace as 2006-2008, might take a year??

Although I know we don’t have it, the metric I would like to see is the length of the the delinquent loans…

If the length of the delinquent loans were fairly short term, then I would say the bottom is running out of money..

With the run up in prices, it wouldn’t be difficult to buy, have no payments for a couple of months, make a payment or two, and then trade in to start it all over again…

Easy to do when you have moratoriums on your other obligations and are/were getting showered with money…

For the bottom 20%, the last two years are the good times…

The normal range in the Good Times of a 7% delinquency rate is nothing to worry about. Lenders get paid interest to take those risks, and they’re taking them. And that 7% will reappear eventually. Maybe next year.

But if we get a big spike in unemployment due to a big-fat recession, you’re looking at higher delinquency rates. I don’t see that type of recession right now, but it could happen.

Spend our time more accordingly

Came across one of those shell companies stock symbol VII. I found it because a stock screener caught it. Anyway, one of the companies they purchased/invested in is called Roofstock. It is a company that allows mom and pop global investors to buy SFH rentals and has a global reach.

Guess what, they also offer a service to purchase newly built homes for rental from Lennar.

“Roofstock and Lennar have forged a partnership to make buying new homes in the U.S easier, for both international and domestic owners. Purchase Lennar new construction properties as a primary residence, as secondary homes, or as investment properties from anywhere in the world.”

Just another example of what was fueling housing. Here is one of their comments from a customer.

“I ve never been to Memphis, we’ve never seen the property we bought on Roofstock. It appraised for $30k more thatn we bought if for before it even closed. Our renters are great and we are cash flowing every month.”

FYI – the little mom and pop Roofstock dids $5 billion in total transactions. When you go to get a loan, they use a company called Beeline. Beeline is offering a 5% 30 year with only a $375 processing fee.

The sitedoes all the hard work for you. They calculate the Annual Return, the Cap Rate, Neighborhood rating. If the house is vacant when you buy it they will pay up to 6 months of rent until it is rented.

There you go. Here is the future. VII really only focus on SFH or duplex/triplex. They currently have 1330 homes for sale as rentals for global investors to buy. That is part of their marketing for sellers. They look to buy houses with tenants in place. I am amazed at home many have returns of 15% to 25% annum

Totally legit business.

Not a ponzi or business that only works in an exploding housing price and low interest rate economy.

I could find no flaws in this business model.

rue82,

These are built-to-rent homes. All home builders are specifically building entire subdivision for rental purposes. It’s the hottest trend in home building. Builders fill them up with tenants and then sell the subdivision as an income producing asset to some fund. This does NOT take homes for sale off the market.

It’s no different than building an apartment tower, but it’s just in a suburb and spread out, rather than going up.

Wolf,

As a descriptive matter, your observation is correct. However, to the extent that homebuilders are building rental houses, they are utilizing land that could otherwise be used for owner-occupied houses, which drives up the cost of land available to builders of owner-occupied houses. I think this “hottest trend in home building” will eventually lead a bunch of Pottervilles in this country.

Nah. Just look at the data. Homebuilders have a problem:

https://wolfstreet.com/2022/07/26/prices-of-new-houses-plunge-sales-crater-to-lockdown-level-inventories-pile-up-to-highest-since-2008/

Inventory of unsold houses in the US:

It takes future homes off the market indirectly, unless builder resources, construction workers, and construction materials are unlimited. These are being built instead of owner homes because they are more profitable in the current/future rate environment.

That takes an assumption that everybody wants to buy…

Many people would prefer to rent and don’t want to live in a high density building…

Especially if the rental has amenities included/available …

Somewhat unrelated, but I don’t think the owners of rental communities are going to like the long-term consequences. What happens if a suburban city of 20,000 is all renters? Renters vote, and the owners can’t. That’s when you start to see rent controls, higher property taxes to provide more services, higher taxes on non-owner occupied buildings, and other things that are painful for owners for great for residents.

During the post GFC selloff we looked at condos on Florida Gulf Coast as rentals and realized that the only one making money long term were the management companies. The cash flow is great for the first 8-10 years but then maintenance kicks in, first appliances, then minor plumbing and electric, followed by HVAC system, flooring,kitchen cabinets and then roof.

If you buy new, rent and depreciate for no more than 10 years and sell you might come out ahead. After that you are up the creek and probably sold your paddle because the first 6 years were so great.

It also only works well if you either are large enough to have your own full time handyman on stuff or if you can do a lot of things yourself.

If you have to call a plumber for every leaking faucet or an electrician to replace every bad receptacle, you’ll see repair costs eating away all of your profits very fast.

I think it will become more and more difficult for Wolf to get accurate data on repos. After all, cars are getting more and more “intelligent” by the day.

Soon, new cars can be switched off remotely if the borrower gets behind on payments, and its built-in GPS will show where to pick it up. No repo man required, just a driver. But that is only the beginning.

In the near future, if you get behind on payments, your car will simply eject you and drive itself back to the lender’s premises. It will also report you

to the authorities and kill your credit score while it’s at it. Alternatively, the car’s central locking will engage and drive you directly to a debtor’s prison. While this is happening the onboard camera’s will film you and the footage will be sold to reality TV programs, with the proceeds going to the lender.

At that point it will become very difficult if not impossible to distill the real repo data from all the other reasons that cause cars to grass on their drivers and getting them locked up, like speeding, running red lights, smoking or drinking while driving, visiting questionable locations or leaving your fly unzipped.

Progress. Where would we be without it?

Have you heard of on star been around 20 years,they knew where you were and could shut car off then

There’s been dealers who installed a kill switch on vehicles they sold to credit criminals. From Chicago, July 14, 2022:

“They’ve used the kill switch to try to induce my clients to pay, without telling them that they would [shut their cars off permanently],” Schneider said. “And they’ve disabled the vehicle, which has hurt their ability to repay the amount or even to sell it to get the money to pay what they owe.”

The cars have remained parked in front of the owners’ respective homes for more than two years while Overland continues to pursue thousands of dollars through collections lawsuits

Schneider is seeking class-action certification for all borrowers in the same bind as his clients, a group that likely numbers in the thousands, based on the number of collections actions Overland has filed in Cook County during the pandemic. Overland did not respond to questions from the Chicago Sun-Times.”

Could get a bit ‘spensive.

“Before there is a repo, the borrower must be delinquent on the loan. If the borrower falls behind on payments and cannot catch up and thereby cannot cure the delinquency, the lender will repossess the vehicle and sell it at auction”

What if you cannot answer the question, who “the lender” actually is ?

“You can ignore reality but you cannot ignore the consequences of ignoring reality”

Ayn Rand

Auto loans are not home mortgages. Auto lenders don’t need to go through a foreclosure procedure to repossess a vehicle. The lender can just hire a repo company, and they go out and get the vehicle with a tow truck, clean it up, and run it through the auction. This is a very liquid business.

The finance company has a lien on the title. It’s not rocket surgery to figure out who owns what. The finance company (at least a captive) floats an issue of bonds for a set amount of dollars – not VIN specific. Those bonds are sold and paid at maturity. The investors have no claim against the chattel.

To be fair, the article said there’s potential for exploding car delinquencies. There was a bunch of data on why the author theorized now was the worse time to buy a car. Yes title was clickbait but if you read the article it was more nuanced, and just said all signs point to a crash in used car prices.

Alex,

The title is all people read, and they tried to spread the link and the title a million times in the comments here and in my inbox. Without that title, no one would have read that article. That’s the definition of clickbait. They had essentially NO DATA on repos, and yet they came up with this clickbait title that provided people with FALSE information. That is unforgivable for a publication of that type.

This is why we read your excellent posts, Wolf.

I admit that I am overwhelmed with clickbait titles.

I’m sure the clickbait authors hope that something sticks in people’s brains.

I expect clickbait to increase closer to election time. Paid for by whichever PAC will benefit. Sad.

Excellent data and yes the economy does look strong yet the narrative from wallstreet is just the opposite. Unemployment low, repo low, jobs availability high, and people leaving the workforce voluntarily high (maybe wage increase) auto prices higher….

All point to higher inflation and the fed not backing off.

At the same time the 10 year did drop significantly which the fed was surprised at and was not driven by fed action . QT accelerates in Sept .

This process is slow which does correlate to 2005 -2009. Startups are running out of cash if their model is broken but they are not the major employers. I think this will take a few years to play out and people are addicted to information overload and very quick response times to data.

Wall Street is peddling that narrative because they are addicted to cheap money from the Fed. They want the average person to think things are going badly such that the Fed will be politically pressured into backing off.

Total employment is about the same number as just before the pandemic. There are a few million missing workers as population has increased about 10 million people. Economy is still finding it’s new footing. You have to be careful investing as excessive money is still in the system, but fiscal and monetary policy is changing rapidly.

Real wages going down and real interest rates highly negative tells you what current reality is for average worker and average retiree.

if the fed always hikes until something breaks then it seems to have a long way to go in raising interest rates. All you hear on Wall Street is about the coming fed pivot. Talk about addicted junkies! Wolfs site is one of the few that sticks to the data. now the data can be behind and it does seem that some parts of the economy are slowing. People still seem to be spending.

(1) Inflation is outpacing wage increases, but consumption continues to increase so the economy is strong.

(2) Consumer debt rises to an all-time high, including a big increase in credit card debt (see yesterday’s CNBC article), but as share of GDP, etc., it’s not that bad.

(3) Even with the high debt, home equity and savings are strong, so bankruptcies, repos, etc. are low.

(4) Summary: everything is fine, unless the above trends continue (high inflation continues, debt rises) and home/car prices come under pressure. But surely that won’t happen. The Fed and Congress are on the job!

Truflation up to 10.25% today… increase from 9.68% on July 25th! So #4 is in play… go Fed go!

I expect spending will be strong for the next 6 months or so as the pandemic led savings is used up. Next year will be the real test to see if rising interests rates can address the structural problems driving inflation. I think interest rates have completed a 40-year cycle of decline and are now in a secular cycle higher. The longer the market takes to sober up, tighten up and invest capital wisely, the harder the adjustment will be on us all. The developing conditions of deglobalization, economic alliances and the end of subsidized energy will prove inflation has a long term structural problem to work out.

I said it before and I’ll say it again. Much of the inflation is coming from the top 20% who feel emboldened by the paper gains in their assets.

The Fed will NOT get inflation under control unless it crashes asset prices back to something more reasonable. It’s that simple.

Of the multiple geezers that I know that have paper gains in their assets, they have cashed some of it out already (so the fear of loss is reduced) and are spending the money on Viking river cruises (for as long as the water is deep enough for the barges to draft) and other luxury travel. They’ve set up college funds for their grandkids… things like that.

The fact they have money doesn’t mean they don’t squawk at food costs (witnessed this morning at Safeway during “geezer day” 10% off). However, we’ll still buy prime cuts of beef rather than choice or select because we can.

Many geezers are also wising up to the fact that their fancy cars make them targets for “parking lot entrepreneurs” that wish to improve their lot at your expense. On our little block of paradise, there’s more Toyota’s and Honda’s than there are Porsche’s and Benz’s (which were dominant when we arrived here). I have the only remaining Kraut cans on the street and the newest one is nearly 20 years old (garage queen).

As in our case, we don’t need anymore “stuff”. We only replace what breaks, wears out, we drink, or my bride leaves scattered all over an intersection.

Buddy returned his Kia forte and they paid him $7000 OVER the lease residual value which he put towards a new lease on a new Sportage which was the ONLY new car they had in stock and the only reason this one was still there was because it was the front wheel drive model which nobody wanted.

We are a long way from normalcy

Kia/Hyundai only sell front wheel drive cars. What line of BS were you fed from Buddy?

Kia Sportage also exists in 4WD.

You must have missed the AWD K5, Stinger, and all the AWD SUVs they sell to think they only sell FWD.

I always love a good slap down. Best reason for a comment section lol.

Arya: They didn’t “pay him” over residual for his car…. he had to purchase the car for the residual value, pay sales tax and registration, then sell the car back to the dealer. The lease contract stipulates what the residual value is at maturity of the lease and the customer has the option of buying the car at that price…. but the dealer/finance company won’t pay a premium to the customer without his performing the purchase because they’re not obligated to do so. That would be absolutely stupid on the finance company / dealer’s part.

A friend of mine bought his Range Rover at lease maturity last May. Don’t remember the exact numbers, but he bought it in the mid $80K range… paid CA sales tax and registration, and sold it for $110,000 off his driveway – pocketing about $18,000 for doing basically nothing.

So, from the shills at CNBC, it sounds like people are switching from leasing to purchasing. With the cost of cars going out the wazzoo, I suspect that a couple years down the road, this may come back to bite some people… if unemployment starts to tick up.

As for the moment… party on Garth!

“The share of automobile transactions that involve leases fell in July to 18%, down from 27.2% a year ago, according to Edmunds.com.

Deals on leasing are minimal, pushing up the average monthly payment to $595 last month, an increase from $575 in June and the highest in Edmunds’ database.”

It will be interesting to see how the new auto market will play out as supply issues drag on. They seem to be easing, but it could take a while.

If I were a manufacturer, I’d be looking at how to exploit holes in the market with the resources at hand. Technically, this would be a mid size SUV or wagon with a low chip burden, which also means low options/content. They were known as a strippo back in the day.

But the big question is whether U.S. buyers are sufficiently frustrated in the expensive used market to accept a low content new car as a substitute. I seriously doubt it.

This situation reminds me of the switch to small trucks in the mid to late 1980s when a pair of crushing recessions and inflation (yes, we’ve been here before) raised car prices to nosebleed levels (the word sticker shock was coined at the time). People responded by buying trucks because it was socially acceptable to be seen as a practical person who bought for the home projects and gardening, rather than because it was all they could afford.

There has to be some sort of low-content model that could be configured in such a way that gives buyers a social fig leaf. If an automaker could crack that nut, they might be able to utilize excess manufacturing capacity (assuming they could find sufficient labor).

Another problem is if an automaker is too successful at this, they could go the way of American Motors. Tight margins don’t support new R&D which ultimately results in a stale lineup with a reputation for mediocre quality.

You can’t build a “strippo” in this day and age due to government mandated “safety” equipment. Rear cameras, ABS, airbags, stability control, blah blah blah. It would likely cost more to build a car with crank windows than one with the power windows as deleting the power windows would require different window regulators, different wiring harnesses, CANbus modifications, add assembly line complexity, and bunch of other stuff.

It ain’t the 80’s anymore.

PS: The switch to small trucks was started by Nissan (aka Datsun) and Toyota and began to impact the domestic small truck business – which is how we ended up with the “Chicken Tax” and import quotas.

El Katz: note I said low chip burden, not sans chips. The items you listed are standard on a base Corolla. Base MSRP is $22k. The engine and transmission has a chip controller and the stability/ABS/traction control share another one.

It’s quite technically feasible to configure the base model to look more like the rest of the world with manually operated climate control, manual steering, etc. Note also that most of the world now enjoys power windows because manual risers no longer save much money (they also don’t require chips).

It would be nice if you paid attention to the actual thought experiment rather than condescendingly assuming that I am advocating to a return to the 80’s. It is a directly relevant example of socially acceptable downgrading and begs the question of how car buyers will tackle the same problem this time around.