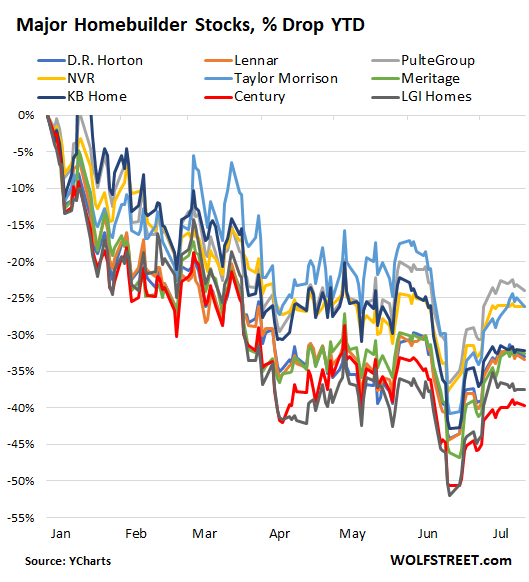

Homebuilder stocks have been wobbling lower all year, now down between 24% and 40%.

By Wolf Richter for WOLF STREET.

Homebuilders have struggled for well over a year with supply and labor shortages and ridiculously spiking costs. In addition, this year, the new holy-moly mortgage rates added to the woes, and unsold inventories surged to levels not seen since 2008, as sales fell. And homebuilder stocks have gotten hammered across the board, down year-to-date between 24% and 40%.

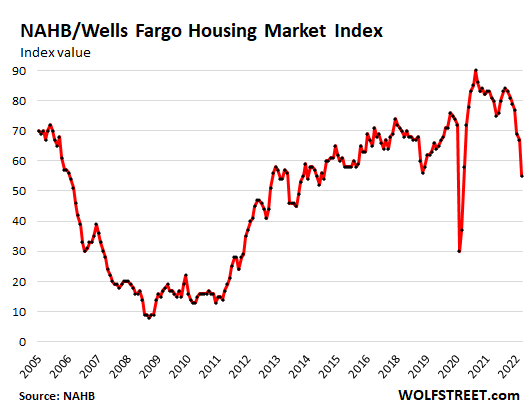

So, not all that surprisingly, the confidence of builders of single-family houses, as depicted by the NAHB/Wells Fargo Housing Market Index for July, released today, plunged by 12 points, the second biggest drop in the data going back 35 years, behind only the April 2020 lockdown cliff-dive, as “high inflation and increased interest rates stalled the housing market by dramatically slowing sales and buyer traffic,” the NAHB said.

It was the seventh month-to-month drop in a row. In other words, it’s been all downhill so far this year. With today’s index value of 55, it is now back where it had been in May 2015. And it’s right back where it had been in February 2006, though it was dropping a lot more slowly back then.

“Production bottlenecks, rising home building costs, and high inflation are causing many builders to halt construction because the cost of land, construction, and financing exceeds the market value of the home,” said the NAHB.

And builders are cutting prices: 13% of the builders have reacted to those conditions by reducing home prices in the past month to boost sales “and/or limit cancellations,” the report said.

Regionally, the Housing Market Index plunged by the most in the West (-16 points) and the South (-15 points), with the West and the Midwest showing the worst HMI levels of 48 and 49 respectively.

| Region | HMI, July | Point Change fr. prior month |

| Northeast | 57 | -5 |

| Midwest | 49 | -6 |

| South | 60 | -15 |

| West | 48 | -16 |

The future looks worse, homebuilders said.

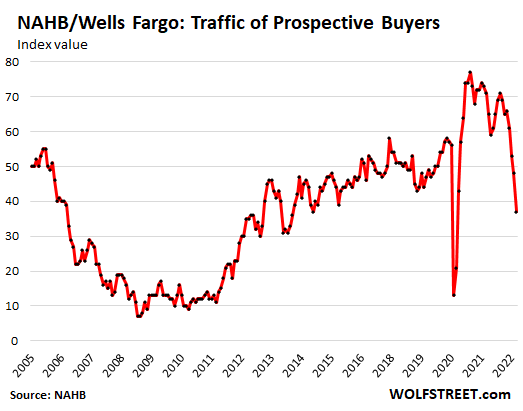

There are three components in the MHI: Current sales, sales outlook for the next six months, and traffic of prospective buyers. Only the current sales component was still at a positive level.

The index for current sales plunged 12 points in July, to a value of 64, which means that still more builders rated current sales as “good” rather than “poor” (an index value of 50 would be neutral).

The index for sales over the next six months plunged by 11 points to an index value of 50, which means that builders were evenly split between those who rated their future sales as “good” and those who rated them as “poor.”

And the index for Traffic of prospective buyers plunged by 11 points, to an index value of 37, after having already dropped below 50 in June. Traffic is an indication of interest by buyers, and buyers have lost interest. That’s a real problem going forward.

For this component, builders were asked to rate traffic of prospective buyers as “high to very high,” “average,” or “low to very low.” Today’s index value of 37 means that more builders rated the market “low to very low” rather than “high to very high,” the second month in a row with below-50 reading:

Homebuilder stocks have been wobbling lower all year, interrupted by sharp bear-market rallies when dip buyers piled in, only to get run over shortly thereafter by more selling. The last rally that had started in mid-June seems to have run its course now (data via Ycharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Long, long, long time coming.

Concur. What goes up, must come down….at least hopefully.

I’m just glad to seeing an ebbing in the madness. I have a severe case of NIMBY and this downturn is comforting.

While all else has corrected >20%, e.g. Bonds, Stocks, Home builder stocks, cryptos etc, still home prices from case shiller are still at all time high.

Is there any other dynamics in play for home pricing? Is it the result of negative real interest rate? Is it that money is moving from all other asset classes to housing? Or is it that housing is now expected to be “Too big to fail”? Or is it that high inflation implies housing inflation also?

“still home prices from case shiller are still at all time high.”

The Case-Shiller is great, but it lags six months actual market conditions, as explained below somewhere.

SS

House prices tend to drip down, sometimes for years….

It’s simple supply and means economics. Prices will continue to creep upwards until we see a dramatic increase in inventory, which I don’t see happening because we have record equity in homes, people have crazy low rates/payments, and the job market is stable, or a massive (and I mean massive) drop in demand. The fed is trying to slow demand down with The high interest rates and it should continue to stabilize the market. That’s a good thing.

However, this isn’t 2008/9. Prices will continue to be stable in my opinion regardless of all this fancy math because supply/demand economics is undefeated. That’s basically all we need to look at. Until absorption rates get to 7/8/9 months, prices won’t budge.

Houses will take longer to sell and there will be less sales overall, but those prices will stay. They just won’t go up as fast as before.

@Billy Howard

It’s wishful thinking to think that home prices won’t drop or that “this time is different” than 2008-2009, if anything all signs are pointing to the opposite, an even more drastic drop considering the unrealistic home price inflation and the even worse housing bubble we’re in. The simple fact is that the real estate market ultimately has to be in line with American’s incomes and what they can actually afford–this is true of any commodity but especially of an essential like housing that represents such a significant purchase. And if the prices are too high, they will come down one way or another.

You cite lack of supply as an apparent argument against a major home price drop, but the reality is that Americans will find a way to increase the “supply” of housing in any way they can, unfortunately often in ways that drastically drop the already plummeting quality of life in the USA. I’ve been seeing this all over even with some of my own distant relatives, people moving back home with close or extended family and more room-mates moving in and bunking together (includes even the highly paid professional class in the Bay Area). Or people moving out into tent-cities, or into RV camps. Or just leaving the country (ex. tons of Boomers getting cheap retirement homes down in Mexico or Panama). The cost of homes like other key goods has gone way up past what Americans can actually pay with their incomes and savings, and the massive increases in US household debt and leverage to cover it is just leading to yet another American financial crisis. Those costs have no choice but to come down, and not just by a mild 25 or 30 percent. They have to fall by half, in some cases 60, 70, even 80 percent in some markets to line up with US incomes. Maybe a tiny few markets esp in areas like southern California or Manhattan will stay bloated due to investor purchases and speculation, but the ridiculous prices and rents in markets like Phoenix, Austin and Tampa are already headed sharply down, and are only beginning a long and sharp drop down to much lower levels.

Loan officer here, Washington state still going strong for now with home buyers and new home buyers. Homes have dropped $60,000 – $120,000 in price from what I’ve seen and it’s giving other people a chance. New cars on the street. Home inventory strong. How other states are fairing I have no idea.

Same here Howell Michigan, rural small farms premium, everyone here driving new Jeeps, Rams, F150, Telluride, no drop, money flows like usual.

Most people at work marvel at the gains they have made on their houses. I now have a canned response. I tell them I would rather make a $1 profit on my home I have paid off if it would mean my children could afford to buy a home today.

I bought my home as shelter and it has served its purpose wonderfully. I want my children to be able to buy a home and enjoy it as a home, not a commodity.

or rent it from Blackrock

Oh the American Dream… I for one welcome our corporate overlords.

*BlackStone

I absolutely agree. I said pretty much the same thing to a colleague who was lamenting the falling price of her home in 2010. In my view, inflating home prices are a sign of poverty, not wealth. If it takes a million dollars (and roughly $300,000 in household income) to buy a 1970s era 3/2 with 1,500 square feet, then that’s awful for all the middle class people who can’t afford it. However, it’s really not much better that that’s all a relatively high income family can afford. I purchased my house to live in and it looks like I’ll ride two bubbles up and down in the last 20 years.

Agreed on everything here, we’ve all found it just infuriating the way the media so plays up rising home prices and the housing bubble like it’s some kind of indicator of wealth, talking about how “the housing market is hot” like it’s something to celebrate. There’s nothing that magically happened to add so much value to that home–it’s a classic example of a dangerous asset bubble. It isn’t even good for the homeowners, for us it’s just meant even higher costs for things like insurance, property taxes and repairs on an asset that isn’t really all that liquid, as one of our financial advisors put it. And due to these asset bubbles, the US has suffered possibly permanent damage to its middle class and professional class–even many in the upper class (ex. successful small business owners) who don’t have quite enough money to “purchase” policy from a Senator. And it’s made it difficult if not impossible for even the most successful young graduates in the United States, in in-demand fields, to settle down and start families. The overzealous QE and ZIRP of the Fed (and not just since the pandemic, more like going back a decade or even 4 decades) has been a wrecking-ball for American society.

That’s an excellent response.

“I bought my home as shelter and it has served its purpose wonderfully. I want my children to be able to buy a home and enjoy it as a home, not a commodity.”

Well spoken. If this attitude was more widespread, even with the Fed’s stupid ZIRP and QE excesses over the past 40 years, this housing bubble could have been avoided.

Market action this year has hurt A LOT of people. Cryptos. Meme stocks. Tech stocks. Some huge percentage declines. Against a backdrop of historic leaps in interest rates and inflation.

Lifestyles irrevocably changed, not for the better.

Economists missed it. The Fed missed it. Politicians missed it.

A few folks got it right.

Totally agree about massive changes.

But…”Economists missed it. The Fed missed it. Politicians missed it”. We can’t give excuses for not understanding what is happening. We’re in this position because the Fed, politicians, and economists, all have ulterior motives. While there are outliers, the bulk of people in these groups are not idiots, they’re either manipulators or mouth pieces. Thankfully bastions of reason like this site exist for those that want to attempt to understand what’s really happening.

Reminds me of a quote that goes like, “Once you’ve tasted fruit from the tree of knowledge, paradise is lost”. Meh, paradise sounds a little boring anyway. Might as well get out there and have a little fun amidst the chaos.

I like the attitude. Why not wade into the current. Life is meant to be lived, not by sitting on a a shore watching the water pass. Water of life is as much metaphysical as it is physical.

“If you wait by the river long enough, the bodies of your enemies will float by.” Sun Tzu

It depends on why you’re watching the water pass by.

“”Economists missed it. The Fed missed it. Politicians missed it”. ”

The man who started the Weather Channel made an observation that applies to those mentioned above…

to paraphrase, he said…..If your research does not fit the narrative promoted, you will lose your government grant money.

So, did these people “miss it” or were they “dancing to the music”?

Did all the Fed people really “miss it”, or was there a blind eye effect?

I suspect that the big money (Corporate, Banks, Billionaire family trusts) could not be prepared for the COVID-19 downturn due to that being a quickly evolving natural disaster.

Because they were not prepared, they stood to loose massive sums of money quickly. So the Fed steps in and averts disaster (for big money). Huge heavily indebted companies would have gone out of business. The travel industry would have been gutted, housing downturn, etc. Those things had been building for many years and would have seen a natural recession as had started happening in Fall of 2018 as interest rates rose back then until Trump yelled at Powell to lower rates again.

So averting the rapid and compounding COVID-19 downturn was great for big money. But the cost of allowing them time to prepare for the downturn will be a much harder downturn in a much more drawn out pattern that is harder for us to predict and plan around. I think a sharper and harder recession might have been the better outcome instead of pumping an already unstable economy with unprecedented money printing. I personally benefitted from this policy of the Fed as I owned a house during this time and sold it. I still do not like their tactic here as it seems self-serving. Also it seems this Fed tactic of money printing is now a political apocalypse for the democrats even though it started during Trump times.

Because the pain for the average American is inflation now. Not unemployment that would have spiked from COVID-19 if that recession had been allowed to happen, but inflation that is threatening the working class on all fronts and now threatens the integrity of the economy into the coming years. The value of the dollar globally may not stand up to this.

The issue reminds me of the Chinese billionaire that got stuck with a massive short position in Nickel this year. Fully bailed out by the Metals Exchange in London because he was too big to mess with and try to collect from.

“Nothing goes to hell in a straight line” eh? Draw out the pain for years and shift the pain to the working people from the elites.

As long as you can before the big machinery grinds you up.

with unjust rewards come the danger of pullbacks ………………

some of my friends got retired, had plans as they were making good money in stocks. Now plans canceled, had to come back to work :-(

I’ve been looking for camper van for a few years but tapped out in the last two as $20k vans became 40k vans and the high end of the market moved from $100k+ to $200k+. I’ve seen quite a few ads of the high end lately that begin “selling because our circumstances have changed,” which I keep interpreting as meaning “my crypto has crashed.” But asking prices are barely moving down so far, maybe 10-20%.

There’s still too many limited variables out there so this situation may just slowly unwind. There’s tons of people still making stupid money.. There’s tons of inflated wealth in the RE markets. Still highly favorable tax rates for speculation. And that pesky inflationary mindset where people will irrationally refuse to sell an asset at 50% of its bloated bubble value, even if the market goes there, because they can’t let go of that perceived value.

“ And that pesky inflationary mindset where people will irrationally refuse to sell an asset at 50% of its bloated bubble value, even if the market goes there, because they can’t let go of that perceived value.”

DD,

Why you have a “mindset” of worrying about what the asking price is for what you want to buy….

No matter what it is, houses, vans, or anything else, make an offer based on the valuation you determine and are comfortable with… if accepted, great… if not, move on… eventually, you will find what you’re looking for at a price you’re willing to pay…

I try not to pollute my mind with useless thoughts of what loss they’re taking…

Basically, I don’t give a damn what they’re asking…. I do give a damn about what I’m paying…

I lucked out and bought a 2001 Dodge Minivan for $2800 about three years ago. I have been living in it ever since.

$20K for a camper van is totally unnecessary.

$20K for a van to live in?

Bought my first house for $22.5K back in 76. Small owner built camp on a tenth acre with 52+- feet of frontage on a clean lake. Low taxes and minimal maintenance with great neighbors. Sold it in 84 for $73K and thought I had done real good. My son told me it recently sold for $850K! Taxes now more than my initial purchase price! Totally insanity thanks to our central bankers.

And the “safety” of bonds. No where to hide in this bear market, except cash!

There are a few places. The dollar for example. Check out symbol uup. It ‘s up 11.98% YTD and 15% in the past year.

If the Fed persists with raising interest rates the way they have been in my opinion there’s good odds the dollar will go higher. if you’re not familiar with “charting“ then it’s likely better to stay in cash. At some point, every asset class reverses and if you don’t know how to see when when you’re better off staying in cash or short term T-bills. 90 day to 1 yr. No longer until Fed backs off raising interest rates and “qualitative tightening“. Talk about an odd situation, the one year T bill is paying more than the 30 year treasury bond. This is not meant to be investment advice or a recommendation to buy or sell any investment. The above is based solely on my observations and can change at any time. You should seek The opinion of an investment expert, especially one who is experienced with a long-term verifiable track record.

There are thousand of places where you could beat cash, obviously. If you take risk. You could throw a dart at any short ETF and do better than your UUP, in the same time frame.

I never use “charting” , I prefer to read tea leaves.

Isn’t the Rouble up too?

“There are a few places.”

Name another. Few suggests more than two. Everything has been crushed outside of the soaring dollar. Shorting something doesn’t count as there is too much risk of big boys coming along and squeezing something that has been shorted too much.

I’d like to hear two more examples please. A case could be made for uranium miners depending on the time frame.

// Economists missed it. //

I have zero respect to those so-call “Economists”. Economists should tell us what IS happening in our economy, and explain why. As ROYCE said, many economists are either mouthpieces or manipulators.

And thus, I appreciate you, Wolf, for telling us what mainstream media won’t tell us.

The only people who missed what was going on were those blinded by their own greed. You don’t need an PHD in economics to be able to figure out that asset prices going up by 50% while revenues remained stagnant (or worse), and large parts of the workforce were being paid to stay at home, was not sustainable.

The Fed made a joke out of those of us who work for our dollars. Fair enough, during the pandemic I accept this was a necessary evil, but they let it run on way too long. Now it’s blown up in their face and it looks like they might, with much regret, actually do something about making sure the economy favours those who go out and do stuff over those who sit at home attached to the QE fountain.

Im still not completely convinced, but it really looks like enough of the ‘losers’ who go out to work each day are getting sick and tired of being beaten down by stagnant wages and ever rising demands on their incomes, that they are going to have to do something to prevent a wider breakdown of the labour market (aka wage-price spiral taking off).

Inflation is theft

And those who promote ANY inflation are thus thieves

And those who are charged with preventing inflation (stable/fixed prices) are shirking their fiduciary responsibilities

Yep, economists have been missing these calls on a regular basis and now even the Ivy-League and U. Chicago deans are admitting it. Too much focus on pretty and elaborate mathematical models, too little actually talking to the middle class and working grunts who deal with the economy in the real world.

I read the CNCBC article. It also made the comment that homebuilders are offering options to improve affordability which I interpreted as more than just price cuts. Probably rebates to make it easier for their broke potential customers to scrape up enough of a down payment.

I interpret that as “anything but actual price cuts.” Or “stealth price cuts” if you prefer.

I hear you the most. Now we will go back to stick homes. Just plywood at all the corners for square. Same as 1978 when my home was built by previous owners. I have since finished adding all the proper materials. But cost cutting is real. Back then, bonds paid a respectable 8% but mortgage rates were high.

We have to build for the big earthquake, half the walls in my house have plywood on both sides, not to mention the 14 HDU hold-downs.

Homes are built to the current codes. They’ve always been quite adequate Let-in bracing is still permitted under the IRC in non earthquake/hurricane areas and is perfectly acceptable.

OSB sheathing can be a nightmare when it rots.

This for IC:

”Let in bracing”, that I installed for many years/decades as a framing carpenter is not worth much, if anything beyond squaring and plumbing walls.

Please add some of the now widely available steel ”strapping” for ANY application…

ANY of these can be scoped and analyzed and ”computed” these days, as opposed to when we, in this case the ”framing carpenter” we, used it extensively in CA, OR, WA, and the entire SE USA.

Because it was CHEEP/cheepest way to go.

Yes, but as in 2008, the prices of too many houses have risen to levels that are not affordable to ordinary Americans, particularly since inflation is making their wages worthless. That RE inflation may decline, while other inflation rises and rises, because it is desirable to some.

What people forget is that there is a large, parasitic group of crooks that own all of the “Fed” by owning its district banks indirectly, called banksters and financiers, who profit immensely from inflation: this year, if the real inflation rate per year was merely running at 6% over what they pay their depositors (0% to 3%), who deposited $15 to $20 trillion with them, those banksters and financiers are making windfall profits of over one trillion US dollars, because inflation is reducing their liabilities in real terms.

Events such as the economic collapse of China will reduce demand and thereby, inflation (albeit some of the tactics of the crooks in charge there also reduce supply, like the lockdowns), but ultimately, unless they could take away the trillions of dollars that they have given the parasitic groups (which is practically impossible), inflation has merely been delayed.

When the parasitic banksters and financiers start enjoying their windfalls, by buying yachts, cocaine, prostitutes, etc., inflation will climb and climb. The measly aid given to ordinary Americans (who could not afford a $400 emergency even before the pandemic) will only enable them to pay down their enormous debts or their rent. It did not cause more than a tiny fraction of the oncoming inflation.

The American dream of beeing a rentieer. No need to work, let the money work and live of the rent. The trouble is that an economy can only be taxed with a finite level of rent.

After the limit have been reached, more rentieers only consumes what later should pay rent and the economy contracts.

High interest rates do not help, it just shift how the rent is extracted. High interest rates may bring about demand destruction. It may as well bring supply destruction.

A lot of US oil production vas viable due to cheap finance and the possibility to use the oil production as a base for financial income. With high interest rates there will be expensive or little oil.

We may see the same happen with other industries.

Good description. This was something they taught us in Econ101, even the most productive economies can be distorted and lose their foundation when rent seeking and rentiers become the heart of the economy, and what the policy-makers eventually cater to (just like the Federal Reserve over the past 40 years). Rent seeking is always a part of any modern economy, but it has to be reigned in if it starts to intrude on actual productive activities, or to make it hard for workers and producers to get basic needs like housing, healthcare and education. All 3 areas where the US now has some of the worst cost extremes and asset bubbles.

Let us not rule out 40 year mortgages. Got to keep the monthly payment manageble. It’s ALLLLLL about the monthly payment.

I doubt prices will drop by a meaningful. Drops by half a percentage point do not count. Many experts have been predicting housing crash for last 10 years. Most have been predicting over last 3-4 months. They are tireless. But home prices refuse to drop, it only goes in one direction.

I suspect if home prices will fall by 10% or even 5% Fed will panic and start talking about lowering rates and investors will jump back on the Titanic. The party will go on. Fed has created a new mindset among US citizens and investors, that Fed will always save assets from crashing and investors from losing in US markets, therefore asset prices will never fall.

Bond market is already predicting Fed U turn in spite of record inflation month after month.

RE price drop is a wishful thinking at best and really bad financial advice at worst.

Kunal, you’d be correct if you had two lives for 60-year morgage.

“RE price drop is a wishful thinking at best and really bad financial advice at worst.”

Whistling past the graveyard, I see. How…..deluded….

Well, RE assets can drop in prices more than one way. The nominal value can crash and the sticker prise get lower.

The purchasing power of fiat money can drop and the value of RE relative other goods and services realign. The sticker price may the even rise, but still the price drop.

Think almost no RE price rise and a tenfold rise in vages comming up. Not likely, but the effect on RE price would be the same as a price drop.

The bond market and stock market is so accustomed to a Fed u-turn, simply because the past 13 years have made it look like printing money is free, with no deleterious consequences. Now that that fantasy has been exposed, the Fed is starting to realize it can either save the markets or it can save the dollar. It can’t do both. The dollar has gotten stronger against the Euro and Yen solely because the Fed is acting hawkish. If the Fed u-turns, all of those gains go away.

The money to bail out housing doesn’t exist in the real economy. It would have to be printed. There’s never something for nothing.

May 17 2022

“Federal Reserve Chair Jerome Powell emphasized his resolve to get inflation down, saying Tuesday he will back interest rate increases until prices start falling back toward a healthy level.

“If that involves moving past broadly understood levels of neutral we won’t hesitate to do that,””

I think they have right now finally come to a place where they are under a lot of public pressure to put their money where their mouth is. Even people who had no idea what they were several years ago have been blaming them for what they’ve been doing.. It looks like the party is over and they are slowly boiling frogs’ asset prices.

I will be the biggest cheerleader of this bust you ever know if price can bottom out faster this time around than 3+ yrs it took last time. Call me shallow, but to see the smug faces of friends and relatives that have beaten me over the head with their RE will only up disapproval look when I try to explain why I don’t want to overpay for a crap shack turn into a “Oh crap” look will be priceless to me and I will enjoy every moment of it.

The sad reality of it, in majority of SoCal and NorCal markets, even a 50% drop is frankly still not all that cheap and maybe come closer to income fundamentals. As much as I would love to see it happen, I am just a bit doubtful this market will have a 50% downturn in desirable metro area. Even then Culver City houses now at $2M, 50% is still no where near affordable for most people. Would love to be prove wrong on this as I have said time and time before.

50% drop is a sweet dream that will never realize. I bet even a 5-10% drop will wake up a deluge of investors and buyers, and music will begin again at the highest volume. You do not know how much hard money is parked at the sidelines, waiting for any meaningful drop, its in hundreds of Billions if not Trillions. Every RE investor in Bay Area I know of is waiting for a drop in prices. All this hard money will be invested with heavy leverage so its unimaginable amounts of dry powder waiting to be plowed back in RE. Not an environment for any sustained price drops, trust me.

I feel sorry for hard working folks who are waiting for a huge drop in RE prices so they can afford to buy, because that moment will never come.

That “dry powder” is evaporating under rising interest rates, QT, and market losses. When markets sink, liquidity disappears.

Yes, I agree, Wolf. This will drive prices down significantly in the short term, but will we have a retread of what happened in March 2020 with the stock market. Big plunges in any sizable asset class have, it appears, ALWAYS (in late crony capitalism) caused a legislative and executive rescue plan that artificially reflates the market. Are you saying that then fundamentals have finally reached a point of such stark contradiction that no matter what the artificial interventions are, they will NOT be able to kick the can down the road and load a few more trillion dollars of debt on to future generations? Peter Zeihan is likely to agree with you. My own thoughts are that the ATTEMPTS at the old legerdemain will be made and that the will be at least semi-successful in stemming deep dives, but they won’t be enough to stop the OVERALL decrease in asset classes, because there really is a limit to fake liquidity, especially when the Boomer generation is retiring and USING that liquidity to fund their (somewhat lavish by historical standards) expectations and retirement. That takes more money out of the system. I think we might see a retrace of the Great Depression where the initial crash (as traumatic as that was), did not signal the bottom at all, but rather signaled a struggle to keep things afloat for years before the real bottom was reached, Stocks went from 400 to 200 and then upward, until descending to nearly 50 almost three years later and stayed down another year. Could you do an article on liquidity and generational pressures (low population, spiking debt, reduced [material] standard of living, huge entitlement shortfalls, etc.) as making an excessive demand on the liquidity already out there, making money even more scarce and, therefore, desirable. What effect will this have on the price of gold and silver do you think?

Kunal is this a re-post from 2006?

Are you a RE investor holding many properties or landlord or a realtor ?

Everyone is looking at this data with tinted glasses.

Kunal is correct. The price drop will be 49%.

All that money parked on the sidelines will stay on the sidelines for a long time. This is a process. Inventories need to rise further. Then the first batch of lower comps will hit the markets. That gets buyers to pull back and wait for more declines and sellers to cut their prices. We will need to go through wave after wave of lower prices hitting the comps and resetting the “baseline” that is used in every negotiation for a new home, until the fundamentals of montly payments gets rationalized and real demand starts.

Markets that get this out of whack are all based on psychology. When people think they can put down 100K as a down payment and make 400K in profits, they tend to neglect to ask whether the price is rational.

5-10 is already happening. Today! This party is just getting started.

There is no such thing as “cash on the sidelines”. It’s a myth.

Practically all “cash” is actually someone else’s DEBT which must first be sold to obtain actual cash.

An example is MMMF which accounts for trillions of so-called “cash”. It’s all debt. When the fund sells holdings to give someone actual cash, there has to be another buyer who uses cash to buy it.

Any other rationalizations?

Not exactly true.

In 2010, there was 960 Billion of U.S. currency in circulation. This is paper dollars, coins etc.

Now there is over 2 trillion currency in circulation.

It took over 200 years to get to 1 trillion and 10 years to get to 2 trillion.

The U.S. treasury printing press is cash on the sidelines. When they have me and many other people $2000 in 2020, we all suddenly had cash on the sidelines.

But I get your point of no cash on the sideline if we had a closed system where governments never printed more currency YOY.

I recently transferred an IRA from Equity Institutional to Fidelity. It took two months! I started to get a little nervous.

Debt centric financial systems create the ‘boom and bust’ cycles. It’s baked in the cake. GDP cannot grow as fast as compound interest, which pushes risk taking upwards, along with asset prices. That’s all that is going on. Sooner or later the bubble pops for whatever reason, and the prices collapse. The wealthy get stung but they have enough to make it all back, and more, picking up truly valued assets.

Exactly, those who keep screaming about ‘ cash buyers ‘ act like there is literally a bunch of bags of money with billions upon billions of dollars lying around on the sidelines, waiting to be deployed. Yet, most of the cash buyers during this irrational binge buying craze of the past two years were from cashed out assets… assets that have taken a beating so far this year, and no one has yet seen the end to the downdard spiral. It was all built upon cheap and easy fake money that the tides of inflation ,QT, and interest rate hikes are washing away.

Very true. It’s funny how the “cash buyers” have been among the groups disappearing the fastest as interest rates go up. You’d think they’d be unaffected if going in with all cash, but they’re the hardest hit. Because as you point out, the mythical cash buyer was always a myth. It just debt in a different form, often fueled by things like HELOC’s and other questionable “sources” of cash based on nothing more than excess leverage.

“hard money” is gold.

Dollars are hardly “hard money”. They can be created by the click of a Mouse and disappear just as fast. They never really exist anyway. To call that “hatd money” is just the Kind of insanity that lead to this mess.

Gold is down 7% this past month. More than housing, but less than gasoline.

Ukraine central bank is selling large amounts of gold to keep economic afloat. Soner or later they will run out of gold to sell.

”Last Crash” K, we were looking at a couple of 1800SF ranch type places on a canal with sailboat water and no bridges to the GOM for $800K or so in 2006.

They went to auction in 2009 for $225K.

Keep your powder dry folks, this crash is just in the very beginning innings.

I also live in SWFL and saw similar stuff back then.

My only concern for your statement is that “this time” may not be exactly like “last time”.

The future is unknown. So we shall see….

I think “heavy leverage” means that money is not dry, but “wet power” by definition.

powder

I’m with you, Phoenix. I wish it would, but a 50% drop is not going to happen. There are just too many fresh dollars out there. Anybody waiting for a 50% price drop in an asset of necessity shortly after the money supply grew 50% in 2 years should expect to keep waiting indefinitely. The value of housing didn’t go up, it’s the purchasing power of middle class buyers that went down.

And the purchasing power of the working class went below zero.

There is no such things as cash sitting in the sidelines.

Also, bunch of my friends wanting to buy home sin san diego postponed their plan as their portfolio took big hits.

Couple of them retired 2 years back, rejoined work force because of these hits.

If money supply can grow fast, it can vanish faster. Let’s wait and watch.

I though the same in 2008, that home prices in socal can never go down and if it goes down , it wont go down by 30-40%. the rest is history as they say.

I personally think the market has turn big time for all asset classes. Gone are the days of cheap money. Let’s see if and when the FED pivots.

Yep. The “cash on the sidelines” myth is largely just debt showing up in another form. It never was cash in the form of actual savings and earnings in liquid form, which is why the “cash buyers” have been heavily drying up as quantitative tightening enters in the picture and interest rates are rapidly increased.

Wrong, people will be able to buy for 50% off but those will be “real” all cash deals – just like last time when no one wanted to buy. Wont be every property, but a subset of whats for sale thats on the banks books for whatever reason.

In fact, I know of condos a stones throw from the ocean that went for 10% of the price they were bought at in 2008. Crazy things can happen.

Why would anyone buy a condo? Trust the future of your asset to a group of other owners who have no training and a random level of common sense?

10%? Love to see the data, some examples.

There were couple of resort towns in Florida that went down 90%-ish the last time. Fort Mayers and Cape Coral I think. Im sure there were others. A guy I knew was buying town houses in his division for $40-45K (also Florida). I think he bought nine.

Wait until after the next Florida hurricane to pick up houses at huge discounts.

Even a 30% downturn would only move SoCal home prices back to the outrageous prices they were at two years ago.

I live in SoCal and most of the nice neighborhoods in SoCal looks like slums.

Many families living in 3 bedroom homes, streets are packed with cars. Downtown streets filled with homeless people.

Those are not nice areas in Southern California at all, but there are many beautiful areas like the Pacific Palisades, Palos Verdes Peninsula, Brentwood, and of course, Beverly Hills among many others that have no such issues at all.

SCBD, please go live with Michael Synder in Idaho.

There are neighborhoodsd in Torrance that look like slums and are priced at a million dollars. Same thing in West LA.

What happens all depends upon interest rates and inflation. If inflation abates and the Fed can lower interest rates in another year, then prices will adjust down, but not get cut in half. But if the interest rates must stay high and even go higher, then the prices of properties will get cut by upwards of 35%, maybe 50%.

Yeah I know what you’re talking about. Just honest about it but a lot of Torrance looks like a dump, but with home prices that would rival the richest districts in many big cities in a saner less bubbly period. The truest sign of the extremes of the everything bubble America has been stuck in.

My neighbor just shared with me that while I was away in Georgia and renting out my SoCal unit via a management company six people had moved into my two bedroom condo. Wow. I thought the mail I was receiving must have been a mistake. An error. But her comment lined up with the number of mail recipients I had saved.

You’re handling it rather well. I wouldn’t even want to be associated with such a depreciating debt anchor. I can only imagine the wear and tear.

Any former chemistry teachers?

Went to LA recently. Downtown is full of zombies. Right next to $400/night hotel. They literally all start stumbling towards you like in a horror movie. Never seen anything like it.

Santa Cruz and east side Santa Barbara fit that description to a T. Million dollar properties that are 50-70 year old dumps with 5+ cars in the driveway and on the lawn (beer cans too). Ugly pit bull barking 24/7.

Al Jazzera did give a Zillow representative a soap box to speak from today. He did paint a different picture;)

Well, will RJ Reynolds ever admit that the product might have harmful/deadly effect on their customers? Same logic goes for Zillow.

Apply George Costanza logic to them, they say one thing, do the opposite, then you can’t really go wrong

Aren’t Zillow’s shares down like about 85% :-]

This time is different he said.

Could be he is right, but I bet not the way he says. The difference can come in a different shape with a different oucome.

And builders also do everything they can NOT to cut prices. It is the last concession they give.

They would rather do the “free” upgrades like hardwoods, granite and stainless appliances, credits for closing costs, etc.

“And builders are cutting prices: 13% of the builders have reacted to those conditions by reducing home prices in the past month to boost sales “and/or limit cancellations,” the report said.”

“cut prices. It is the last concession they give.”

They’re going to have to. The Fed has barely gotten started with interest rate hikes, so it may be easy to surmise that residential real estate is going to get smushed as a Serious side-effect of getting cpi under control, which they can’t but are going to try anyway.

The American Dream of home ownership is dead but could come back as a zombie.

You might expect institutional investors to gather up the low-hanging fruit and convert vulnerable demographics into rent slaves, so as to avoid the inevitable losses in the equity markets.

Well, the rent slaves may not have the economy to have many children. Slowly that demographics will feed back to the housing market. Note that a shrinking population is poison to an economic system founded on ethernal growt.

Very true to point this out. This has already been happening across lots of regions of the US, the cost of living has gotten so high that couples simply can’t afford to start families, leads to a downgoing spiral of fewer kids, schools collapsing, the few remaining families moving out and fewer still moving in. The usual response by some of the more clueless idiots in the punditry, especially many of the neoliberal economists who think they can just paper over the mess, is that the United States could solve the problem just with more immigration. But they forget that policies like a housing bubble, uncontrolled inflation and massively increasing rent and cost of living also make the USA much less attractive as an immigrant destination, especially for the skilled immigrants who start businesses and actually add to the country more than they take in benefits.

In fact, these policies are even leading more Americans to leave and become expats. One of our seminars had a stat that for the time in US history, over the past decade more Americans moved to Europe than Europeans came here, and by a huge margin. Same even with some parts of Asia. You can’t paper over failing policies and asset bubbles by just opening the door to mass immigration, because people simply won’t come, and your own people will leave. Bubbles especially in essentials like housing, healthcare and education are the doom of a productive society.

I would love, love, love, to see this housing market brutalized. I would potentially have a lot to gain from it, but I’m starting to seriously question how big this crash will be, or if there will even be a crash. I can’t stress this enough… About a 3rd of all U.S. Dollars ever created (printed, digitally conjured, monetized debt, etc.) were created in the last 2 years. 2 flippin’ years! So one must ask the question, has housing really gotten more expensive in real terms? Or did the little guy just get priced out by having his currency devalued far faster than his income is being revalued? I’m starting to think that maybe, just maybe, the 30% increase in U.S. median house price (price, not value) over 2 years might just be driven primarily by the 50% growth in the money supply over those same 2 years.

This article focuses on builders of new houses. Of course their sentiment is in the dumpster. The average homebuyer’s income growth has not held up to the price growth of land, lumber, windows, wiring, appliances, construction labor, and everything else required to build a house. So homebuilders are going to have trouble making a profit selling to the average home buyer, especially as we enter a period of time where the value of the dollar is decreasing while borrowing costs are increasing. But if new construction is falling off a cliff while the job market is still raging, and trillions of extra dollars are still floating around trying to find goods, services, or assets to chase… I’d say that doesn’t bode well at all for the little guy like me just trying to find a reasonable used home to own. And if demand destruction is the only way to cool this rig off, guess who’s in the Fed’s crosshairs… It ain’t institutional investors with hoards of cash to continue buying safety in assets, it’s me and others like me in the dwindling middle class. Until we see weakness in the job market, and as long as a vast ocean of cash is still waiting to be burned through, I don’t see any major drops in home prices. I desperately want to see a major drop, but it’s just not there.

Today’s WSJ has an interesting article talking about divergence in the job market. Couldn’t read all of it cause I’m too cheap to pay the subscription. Plus, we have Wolf and I think we’re all better off with his research and analysis anyway. I’m one of those little guys myself.

Prices are already dropping. It is happening.

I won’t believe that until Socaljim says so.

You want prices to drop. Need them to drop? So, you hedge emotionally by saying “It will never happen.”

It is going to happen. Be patient and persevere a little longer. The herd ran it up, they will trample it down.

Your premise is a fallacy. There is never a direct correlation between some arbitrary measure of “money supply” and prices.

There was a lot more “money” when the bottom fell out of the housing market during and after the GFC versus before it. Prices still fell anyway.

The cause of any housing crash is going to be tightening credit conditions. This is reflected in higher rates now.

I assume government will at least attempt some idiotic counterproductive policy (like another mortgage moratorium) to keep housing unaffordable. In isolation, it may partly succeed in supporting prices, but the government is going to have a lot more to deal with than just the housing market, again.

Housing prices aren’t going to decline in a vacuum. It’s not possible to support the housing market in full while concurrently artificially supporting everything else. The housing lobby will be competing against many other special interests, many of which are a lot more powerful.

Augustus, Wolf maintains and regularly shares a chart showing the purchase power of $100 since Jan 1, 2000. Compare it to a chart of M2. Where M2 grows, the dollar drops in value. Where M2 grows fast, the dollar drops fast. Where M2 flattens out, so too does the value of the dollar. One chart looks uncannily like an inversion of the other. The effects of the last 2 years of printing are still playing out, so let’s look at the 20 years from Jan 2000 to Jan 2020 right before COVID liftoff. M2 tripled in that period. The S&P500 doubled in size from its tech boom peak, or tripled from its 2002 bottom which sits along its long term trend line. Median house price doubled by 2020, and it had tripled by 2022. Add a year or two of lag time from printing presses to price tags, and you’ll find the money supply growth and price growth share one of the most direct correlations in economics. Inflation is always an effect of monetary policy over the long haul.

I think we agree on where the American standard of living is headed, but differ on the method that we will use to get there. Sure money was lost on housing during the GFC, but median house price peaked in 2007 and it only took 6 years to regain that peak in nominal terms. We can absolutely expect forbearance again and maybe even some type of forgiveness, tax breaks, or credit toward mortgage debt in the next downturn. Who knows what politicians will cook up next in search of votes? Eventually most Americans will be millionaires, but multigenerational/multifamily homes will be the standard and $1m won’t feel like a lot when a loaf of bread is $100 and an entry level cheap new car is $500,000. Americans will be poor in real terms.

Good post. I have the same thoughts.

The M1 money supply was 3.9 Trillion in 2020 and now it is $20.5 trillion.

It is sloshing around out there. I am not an Money supply expert. How do they reduce the M1. When I look at the historical chart that goes back to 1960, they never have reduced the M1.

From the FRED: M1 consists of (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) demand deposits at commercial banks (excluding those amounts held by depository institutions, the U.S. government, and foreign banks and official institutions) less cash items in the process of collection and Federal Reserve float; and (3) other liquid deposits, consisting of OCDs and savings deposits (including money market deposit accounts

How is your money supply? Quadrupled since 2020?

ru82, the Fed changed their methodology for M1 significantly in May 2020 (look at the notes below the FRED chart), which is why it shows such a huge spike in 2020. I’m looking at M2 which has stayed more consistent. M2 increased by about 40% in 2 years from about $15.5t peaking around $22t.

If there’s so much cash out there burning holes in pockets, why are so many buyers putting 5% or less down? Something doesn’t add up.

Exactly!

A huge account of that cash is borrowed from non-mortgage lenders.

Because they are leveraging their money to the max expecting to make money via inflation. It has often worked.

Because the cash isn’t in the pockets of the people who need the low down payment mortgages. We’re out here watching our savings get eaten just sitting there in the bank.

Some of us aren’t flush nor well-heeled, and never will be so long as we’re stuck paying the bananas rents. 5% down, 20%, whatever. Its not a financial morality lapse to try to break the renting cycle and get a foot in the door, so long as you can afford to do so with stable income and can understand the long term math.

FHAs are for first time home buyers only, as are many other (not all) low down payment programs. Those buyers tend to have less to put down for numerous reasons. These loans aren’t just passed out like candy, there are employment requirements, income limits, DTI ratios, and restrictions how you can raise the down payment funds and who can gift it to you/how much of the down payment can be gifted, plus documentation of the closing fees and at least 3 months’ reserves. Plus the PMI, which is a brutal throwaway of money. Yes I know what PMI is and why its so high on FHAs, etc, but naw.. at its current requirements its a scam and another tax on the lower income folks.

Its not a perfect system but the low DP mortgages are not necessarily the irresponsible windfall some seem to make them be. And even after all those hoops to secure the pre-approval, good luck getting an FHA offer accepted in a Cash is King market.

Almost forgot… those 3.5% down FHA mortgages also have restrictive conditions the property must meet, you have to pay for an FHA inspection, any issues identified (anywhere from peeling deck paint to roof condition) must be remedied in a specific timeframe, if major repair is needed then that goes into the Rehab loans which are another tangle of restrictions and red tape.

Oh, you’re also a tradesman and can do the rehab work yourself for cheaper? Yeah no, you can’t, has to be an unaffiliated approved contractor. And then you get to pay the FHA inspectors to come out again to sign off on the finished work (6 months time if memory serves me–good luck getting any rehab done inside of 6 months these days much less a willing seller) and if the inspector finds flaws, you get to pay them to re-inspect again.

Its not completely prohibitive but HUD/FHA don’t make it easy (for reasons, certainly) and most sellers don’t want to deal with the headache of an FHA offer even in a buyers market. Not the only low down payment program of course but certainly one of the most popular.

Lily Von Schtupp, Yes, absolutely, I agree, have looked into those. These are virtually unicorn loans. There are some who get them but they are few and far between. The USDA loans- same thing, even worse as the funding tends to be depleted long before the year is up going to developers with connections rather than individual families, at least on the coasts.

On a real estate investors forum I lurked on there were sharks discussing how to access those loans and funds, even though they are not supposed to be the persons benefiting from them.

Lynn, that doesn’t surprise me in the slightest, especially on the Coasts where so few properties meet the eligibility requirements even if the borrowers do.

Even the more traditional mortgage/non-FHA/USDA LDP loans have strict guidelines and limits. I see them talked about like the woman who sued McDonalds for hot coffee–frivilous on the surface, but there is far more to the actual story.

I’m curious how much longer USDA and FHA loans will be viable on the East Coast given how raggedly aged and poorly qualified, if at all, the more ‘affordable’ houses are here. Even the 203k loans aren’t cutting the mustard.

Sure, you can try to find a fixer upper in Bumpkinville Upstate NY, where the economy is nice and dead dead, but 1) mind the many flood zones, 2) good luck finding work unless you’re in healthcare/don’t mind driving an hour+ into Albany (even remote work, given the poor internet connection and frequent weather related power outages), and 3) the house likely hasn’t had a lick of maintenance since the farm failed or GE/Sylvania/RCA/Beechnut/whoever closed shop, so you might as well bulldoze it and start a whole new house. Failing that, with a little luck it might get hit by lightning or a microburst/F1.

Something like a 1/4 of buyers are putting down 100% cash. Lots of others have taken the proceeds from a previous sale and are putting down 20% or more toward the next purchase. Entry level or first time buyers might be stuck down at the bottom of the FHA loan distribution for a down-payment, and the working poor are starting to live out of their cars if they can’t pile into a rental with other families to spread the cost. This is the outcome of financializing the housing market, turning houses into stores of wealth rather than places to live.

Most of those “100% cash buyers” should have a footnote. It might appear that debt wasn’t used to make the purchase, but in reality a loan was taken against another property and the proceeds used to make that purchase. And if it’s really 1/4, woo boy, speculation is running wild. I doubt it’s all just boomers trading one house for another.

Not Sure I think it is (was?) actually around 20% according to a 2022 article I read. That number is going down, possibly quickly. Still a very high number. A good percentage of that I suspect is ultimately offshore money, some funneled through US citizens or legal resident aliens.

To yout point.. Have your cash reserve go up 1/3 in the last 2 years? Same for every other joe six pack signing their life away for a morgage. I dont think those getting that printed cash compete with you for housing.

Didn’t this happen in ’08?

Same old, same old.

Bubble #3 in what? 2024-5.

Yes, but in a few years prices were back and higher than ever.

And with 0% 40-year morgage prices may still double from here.

No more bubbles. We’re all going to be, collectively, too poor.

Can someone explain in layman’s terms what the difference is between currency devaluation and inflation? To me; devaluation would mean if country A’s currency is devalued, then country A’s currency is now less worth than country B’s currency. Is that not the case. Right now the exchange rate of USD to any other major currency is going up, so doesn’t that mean the USD is becoming more valuable?

People keep talking about currency devaluation, but to me all the side effects they quote of currency devaluation look like our good old friend inflation.

You’re confusing devaluation with depreciation.

Only pegged currencies can be devalued. Floating currencies appreciate or depreciate versus other currencies, but this doesn’t consider local inflation which determines the purchasing power for those who use it as their currency of reference.

Good explanation.

“Right now the exchange rate of USD to any other major currency is going up”

It’s not. The DXY is going up. But the DXY is a scam. Look at the dollar vs russian rubles, saudi currency, look at the dollar vs gold. The “strong dollar” is an illusion. It’s only strong vs the zombies euro and yen.

Dollar is appreciating with regards to gold. Takes 7% less dollars to buy an ounce of gold then it did 1 month ago.

Ukraine central bank is selling large amounts of gold to keep the economy afloat. That may be part of the lower gold price.

Soner or later they will run out of gold to sell.

Right now we have a short “risk-on” move imo. So it’s sell gold, buy stocks. This move should run out of steam. The longer trend is bearish for stocks. I could be wrong of course.

We don’t have a market. Powell moves the market. How long will he stay the course? How long will people feel the need to buy stocks?

Looking at the chart above the home builders coming down doesn’t that just sort of follow the macro market in that there was a sell-off all across the entire enchilada?

Also if home builders are going to stop building doesn’t that make supply less and not alleviate the demand?

Who is going to be selling a house if they secured a 3% or less 30-year fixed mortgage?

The S&P 500 is down 20% YTD.

The homebuilders in the chart are down between 24% and 40% YTD.

“Who is going to be selling a house if they secured a 3% or less 30-year fixed mortgage?”

Someone who owns multiple houses where one is now empty who wants to get rid of it before prices start falling.

Someone who has big bubble gains and wants to “cash out” before others do.

Someone who later loses their job when the recession begins and can’t pay their mortgage.

I’m sure someone else can come up with additional reasons.

Prices are set at the margin. It doesn’t take a significant shift to noticeably change market dynamics. It’s happening now.

Infidelity is another one…just for S$$$ & giggles, wonder how much of that in terms of % force people to sell every year..

Someone who loses their job, or loses a ton on stocks and needs to sell their “good” high-priced asset to cover other losses and raise cash.

I will add to the list people who will panic because they think the sky is falling. I have a friend who is a relator. He was part of HB1 and had bought 3 rental houses. The recession hit in 2009, 2 or his rentors e lost their jobs and he sold all 3 for what ever he could get in 2010.

LOL He regrets selling to this day.

Same thing will happen in stocks. That is when you buy.

People also die, especially in a pandemic. The estates have to sell.

I have a 30 year fixed at 2.75. No plans to move, and mortgage is smallish.

If mortgage rates get over 8%, I would be very surprised. I see the Fed choking before 2024, and reversing course, and eventually going negative. There is no way on this planet that the US can handle much higher interest payments on all the debt it has. Look at all the countries defaulting, and we are early innings in that respect.

So Powell, is going to be forced to turn tail on rates. It’s inevitable. Congress nor anyone else has the guts to cut way back on their profligate spending.

Fed can’t go low until inflation also goes low. Inflation is 9ne thing that is more powerful than the Fed.

Inflation forcing the hands of AirB&B owners when travel dries up; second home owners cutting losses in a down market; investors who can 6-7% on Treasuries.

Travel is up in case you haven’t been following the trend.

Yeah, like when travel was collapsed at the start of the pandemic in April 2020. I was sure then that Airbnb forced sales would get me a cheap beach house.

Instead, much to my surprise, the opposite happened. I have given up thinking this will happen, although it is possible it will start slowly, and the Airbnb owners will go broke all at once if things get really bad on the stagflation front.

Meanwhile, if you study the Weimar Republic hyper- inflation, you will note holding real estate was one of a few places to be. Ultimately, real estate is one of the ways common folk have to protect themselves in an inflationary world.

When homeowners start going underwater they tend to panic. A friend of mine bought a short sale in Henderson, NV in 2010. The PO was not distressed in any way other than the fact that the house he paid $450k for was now worth $160. He just wanted to cut his losses and his $395k mortgage…….

Average divorce rate will remain 50% even with 3% morgage. Same with all other human statistics.

I live in an extreme bubble market — maybe not quite Boise, but not far off either. I sold my house last August. I check the list of sold homes in my zip code and an adjacent zip code, and the price never really went up for a house with my square footage, age, lot size, etc. since August. My wife and I are renting while we wait to see what happens with the market.

If you look at Boise and Utah, prices have already started coming down a bit from the peak hit back in February, March or April. I would say where I live, any gains that may have occurred at the beginning this year are now gone and probably a bit in decline.

I feel discussion about the Fed printing x # of dollars and how that means real estate won’t go down substantially is not accurate. The most fundamental issue regarding housing is affordability. If affordability is not there, it destroys demand, period. If the inflation adjusted principal and interest payment should be around $1,500 for a new/existing home purchaser with 20% down and we’re at close to $2,100 then there’s a huge problem. That is a massive gap, not 10 or 20% which could be covered up by a couple bad years of inflation — but 40%.

The Fed with its recent actions and discussion have made it clear that they WANT housing costs to go down. It’s not a bug of what they’re doing, but a feature. To a certain extent, I don’t think the 10 yr yield matters over the next while because the Fed is just going reduce its balance sheet creating a spread between USTs and MBS that will keep mortgage rates above 5%. A perpetually high housing cost — 40% above what it should be normally– represents an enormous drag on the economy. Additionally, it economically disenfranchises young people.

In real terms, the median home price actually declined around 10%between Q4 2017 and Q4 2019. Why? Because mortgage rates went above 4.5% for much of 2018. Home prices stagnated in 2018 and even stayed there in 2019. Consider that the starting point for prices in Q4 2017 don’t even approach the insane prices of Q2 2022. Additionally, mortgage rates were past 4.5% and into the 5s by March and were in the 6s during the 2nd or 3rd most important buying month of the year.

Investors have hopefully gotten the message, and in some markets they’re running for the exits. AirBNB insanity drove much of this increase and a glut of these short term rentals will play no small part in the decline.

“If you look at Boise and Utah, prices have already started coming down a bit from the peak hit back in February, March or April.”

Trich, I live in the Panhandle region and I saw my first ‘price reduced’ placards on the ‘house for sale’ signs in May. So sales surely began to soften then.

Sales have now just about stopped. But there is an older double-wide down the road from me on 1.5+ acres still asking $499k!

Madness.

MiTurn….context, my friend. Is $499k a lot? Anywhere on the CA coast, that’s a fraction of what a 1/8th acre costs. If you’re telling me you can get 1.5 acres of ocean (ok, gulf) view, and it’s a good idea, for $499k, I’m moving!!! I’ll even give ’em $510k for it if they take the 2x wide with them!

(good AREA, not idea)

Mi/Gatto-think Mi meant ID panhandle, which might have a view of Lakes Cd’A or Pend’ Oreille, but maybe not, and certainly not the Pacific. TX/OK is a very long view to the Gulf of Mexico. (as always, willing to stand corrected…).

may we all find a better day.

Lots are $50k all day long on the Texas gulf coast.

I am in San Diego and am seeing multiple price reductions. 1 year back, it was all bidding war and every home was a hot home.

I don’t think prices have really come down but prices are being reduced from aspirational asking price. The sellers are becoming smarter now a days because they now know the trend due to easy access to all kinds of media.

“The sellers are becoming smarter”

I concur with this in So Cal. Reductions, when they happen, happen FAST now. I’ve seen several within weeks of listing.

No supply this time around is a variable that has to be considered. Panic at the fed is another variable.

Also goofy city policy driving up land costs keeps it interesting. There is a correction in the city of San Diego underway but strange things are fueling this market, very strange things.

Good comment j, especially your last sentence.

My hopium is for everyone who wants to take on the challenges of SFR and other residential properties WILL get their wish.

Especially in places, many many places to what SHOULD BE the SHAME of our oligarchy, that are STILL marginalizing and driving out the very folks needed to do the works needed for a viable municipality.

Re supply.

I am hearing a lot of argument that supply will be tight and everyone will hold. I am skeptical of this argument.

Builders can’t hold forever. Life events create supply in the resale market. COVID and government policy caused supply to be temporarily low. There were incentives to not moving (limiting exposure) and government took away rights to foreclose/evict. Otoh, you had tons of demand from WFH arbitragers and desire for more private space during a pandemic.

The mortgage rate increases clearly reduced demand. If layoffs happen during a recession, expect further decreases in demand. Otoh, divided government almost a certainty in the next election cycle. So government intervention seems to not be guaranteed. Price is always a function of supply and demand.

Whether we see nominal prices get crushed like the last time, or it limited to real prices covered up by inflation is unclear. All we do know was housing market was weird and now some of those variables are moving in the opposite direction.

“Additionally, it economically disenfranchises young people.”

Not just young people but other groups which the “newly improved” social engineering FRB is claiming to help.

One of the reasons given for continuing ultra-loose monetary policy was to reduce unemployment and improve the market for low wage labor. I’ve heard that many times.

They assumed they could continue to “print” and keep money artificially super-cheap with low price inflation because during the GFC, this “printing” went into asset markets.

The boatload of modern day “bread and circus” approved by Congress (subsidized by monetary policy) as documented here summarizes how that went.

So, now that the least affluent are getting crucified by monetary policy, can’t use that as an excuse anymore. It doesn’t matter whether they meant it or not, they look bad.

Amy’s new San Jose Frozen Pizza factory, only a couple years old, has closed because of supply issues and the sanctioned price of oils, grains and other ingredients.

We’re still better off than Iran or Venezuela however, but with sanctions now aimed inward, rather than externally we’re getting a taste of what other countries went through. My oil, ADM and defense stocks are skyrocketing. Thank you President Biden, or whomever makes the decisions.

Paolo,

You whole entire comment, every part of it, is BS. You probably don’t even own the stocks you said you own because they aren’t “skyrocketing.” Oil stocks and ADM have plunged in recent weeks. ADM has plunged 25% since April high; and Exxon, to use an example for “oil stocks,” has plunged 16% since June 7.

In terms of Amy’s Kitchen, there is the story:

“It has been a very bad year for Santa Rosa-based vegetarian frozen food company Amy’s Kitchen. Earlier this year workers filed a complaint alleging unsafe working conditions at the company’s Santa Rosa factory, leading to calls for boycotts and at least three Bay Area grocery stores pulling the company’s products from shelves.

“Now the company announced Monday it will close its San Jose production center sometime in September. The Mercury News reports “inflation, skyrocketing materials costs, labor shortages and disruptions in the worldwide supply chain” are to blame for the closure. The 1885 Las Plumas Avenue facility began producing food for the company in March 2021.

“Fred Scarpulla, acting chief operating officer and chief culinary officer, told the Mercury News the company suffered from staff turnover and labor shortages, and he estimated the facility has lost about $1 million a month over the last six to eight months. Interestingly, the interview with Scarpulla and the report, in general, glosses over any of the company’s labor disputes this year.”

“Investors have hopefully gotten the message, and in some markets they’re running for the exits. AirBNB insanity drove much of this increase and a glut of these short term rentals will play no small part in the decline.”

Don’t forget those A$$hat Chinese or foreign “investors” parking their sometimes ill gotten fortune over here. This was especially rampant since 2012 and up until a year or two before COVID. It’s not uncommon to hear stories about these people paying cash, outbidding local buyers with real needs (rather than park their money and leave the property empty). This is all too common in SoCal and NorCal, in SoCal this is the rule in San Gabriel Valley or Irvine.

For this group, they probably haven’t pull their money out yet but with all the S hitting the fan in China, who knows if that will change soon. One thing for sure, I sure have plenty of contempt for them, maybe more so than mom and pop investors that jumped in during this pandemic boom

The Chinese government is putting the brakes on money laundering and capital flight in recent years. I have no illusions they can stop it altogether but there seems to be less flow now.

My anecdotal indicator is the number of exotic cars driven by Chinese students at the college where I work, the number of high-dollar European cars in the lot is way down from pre-pandemic times.

Thank you! Your anecdotal indicator is probably a much more reliable source than any I’ve been able to find. With all other attempts by the Chinese government to thwart capital flight it just seemed to increase after a short pause. That info is very encouraging! Probably has more to do with fear of future sanctions and money lost in China and offshore in bit-coins than anything else is my guess.

“prices have already started coming down a bit from the peak ” -> This article is about new houses which I am not monitoring but I am certainly seeing a ton of price reductions in the Bay Area. In the last week I also noticed:

1. house listed for $2.9M in Jan 2022, sold for $3.3M and that same house is now back on the market for… $2.9M. I don’t think anyone is going to bid that up to $3.3M this time and I doubt it gets the $2.9.

2. house listed for $1.8M in Feb 2022, sold for $2.55 in April and is now back on the market for $2M. I don’t think it is going to get that (it’s a 2 bedroom).

Those are the extremes. Most other houses listed have been owned for 10+ years and often longer. But it does show that some times people need to sell earlier than they probably expected and those people are going to get crushed.

In OC there is a house around the corner that sold for 1.66million in early April (asking was 1.4) and sold in a bidding war.

It came back on the market in early June for 1.75m. After 2 weeks, drop to 1.66. Another 2 weeks down to 1.5!

It’s still sitting. A “fair price” for this home (read still overpaying) would be 1 million.

Unfortunately, for most working families the price reductions as a product of higher interest rates does not make buying housing more feasible unless the reductions far out-range the interest increases.. I mean, it would help me personally to buy a home, but not most people.

We also need something to drastically reduce large time investment companies- both domestic and foreign and pension funds from investing in residential housing if we want workers to be able to afford shelter and homes.

Also all the money going towards housing can not be spent on other stuff. We can’t have a healthy economy when housing costs are so high.

Maybe some of this money subsidizing shelter costs for families should instead be spent on building more low income and worker affordable homes.

A sadistic way to lower the price of houses is to raise interest rates to destroy the demand.

A beautiful and elegant way to lower the price of houses is to build many more houses.

Current difficulties suggest that the era of the stick built house with a thin veneer is over.

We need to re-engineer the house building model, both in terms of architecture as well as the process.

Surprised nobody has stepped up yet.

AJD,

The elegant way would be costs > price. Problem there.

No one has stepped up yet, but some have tried. Lots of hurdles to overcome, and huge momentum with the current way. I do know manufactured housing doesn’t carry quite the stigma it used to, and there is at least some customization possible. But I think the bottom line is that if there’s some “there there” then it would be happening. Hell, if some of these ridiculous “disruptive” companies got funding for whatever (see Wolf’s list of imploded junk), then surely disruptive housing would have.

Well over 100 years ago, folks used to be able to buy complete ready-to-assemble houses shipped to them through the Sears catalog, and Sears might want to consider bringing that excellent idea back.

These are still available, just look up kit homes, or prefab ready to assemble (among other terms).

SCBD-might want to convince Fast Eddie to bring Sears back, first…

may we all find a better day.

Sears is long gone.

Menards has them.

Also a good movie rarely shown is The Phantom Of The Open Hearth by Jean Shepherd. Has a kit house-by-Sears scene.

My grandpa bought one of those sears kit houses in the 50’s and still lives in it. Frankly, it is a cheap piece of crap. 2×2” wall studs. Barely insulated. Tiny. Poor workmanship with skewed walls sitting on a lumpy concrete slab. The whole neighborhood was built like this, and all their sewage went into an empty mine shaft. He hand-built an addition in the 70’s which makes the house far more livable.

My only experience with those old sears houses is helping him on some projects, and observing the neighboring houses, so the sample size is small…But if that is emblematic of the whole Sears approach, there is little to admire other than a low price.

RG62—

That doesn’t sound right to me. The Sears kit homes were sold earlier in the century and the quality was actually quite good.

Most are still standing and quite solid today.

My great grand parents homesteaded 160 acres in South Dakota (at the time it was called the Dakota Territory). They lived in a sod house for many years. After some years my grandparents bought a kit home farmhouse, think it was around 1910. I used to spend summers there in the 1970s, driving tractors on the farm. In the 1990s my cousin finally got married. His wife wanted a new modern house. So the new house was built about 50 feet from the old farm house. So what became of the old farm house? My cousin sold it for $5,000. A company came and moved it to another location about 5 miles away. Now somebody else is living it!

1,040 square feet; two bedrooms; one bath; solid basement foundation; nine foot tall ceilings; Craftsman style with beautiful woodwork inside. An 18 foot long, dark oak & glass french door set, with a brick fireplace in the middle, and a three inch thick oak mantle running along the length of it. Galley kitchen with a large farm sink that was set to wash clothes also.

A Sears, Roebuck and Co. bungalow kit house which was finished in 1921. Mine since 1995. Cost was $71.25 per sq/ft.

“Life is good in Minneapolis.” -DanBob

@SC My parents still live in the 1924 Sears house they bought in 1970. We did some research over the years. They shipped by rail, so most were built in proximity to lines. Even their model had all sorts of customizations available from the factory. Well built house. There are probably a dozen within a half mile of it.

first, you might want to bring back Sears. then the houses.

There isn’t a shortage of houses. Look at the ratio of housing units to population over time.

It’s entirely driven by monetary distortion.