Stocks of homebuilders swoon amid worst inflation in construction costs, shortages, and spiking mortgage rates that take buyers out of the market.

By Wolf Richter for WOLF STREET.

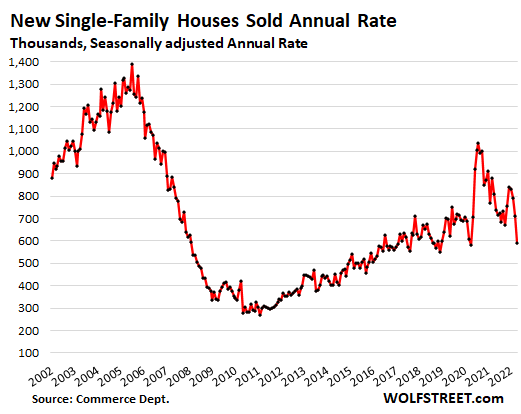

Sales of new single-family houses in April plunged by 16.6% from March and by 26.9% from a year ago, to a seasonally adjusted annual rate of 591,000 houses, the lowest since lockdown April 2020, according to the Census Bureau today. Sales of new houses are registered when contracts are signed, not when deals close, and can serve as an early indicator of the overall housing market.

By region, sales plunged the most in the South:

- South: -19.8% for the month, -36.6% year-over-year.

- Midwest: -15.1% for the month, -25.5% year-over-year

- West: -13.8% for the month, -12.4% year-over-year.

- Northeast: -5.9% for the month, +17.1% year-over-year

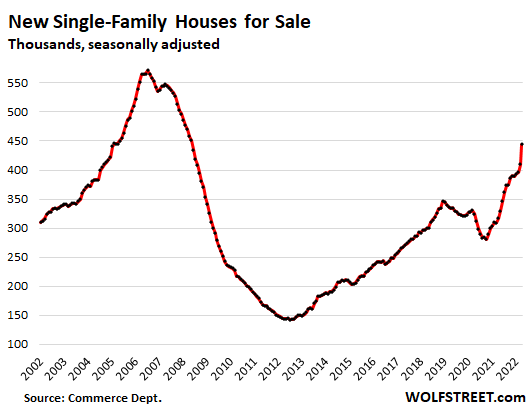

Unsold inventory of new houses spiked in a historic month-to-month leap of 34,000 houses, and by 127,000 houses from April last year, to 444,000 unsold houses, seasonally adjusted, the highest since May 2008.

Both, the month-to-month leap and the year-over-year leap were the largest leaps ever recorded, both in numbers of unsold houses and in percentages.

By region, unsold inventory spiked the most in the South, and dipped in the Northeast. Percent increase year-over-year:

- South: +53%

- Midwest: +39%

- West: +8.4%

- Northeast: -4%

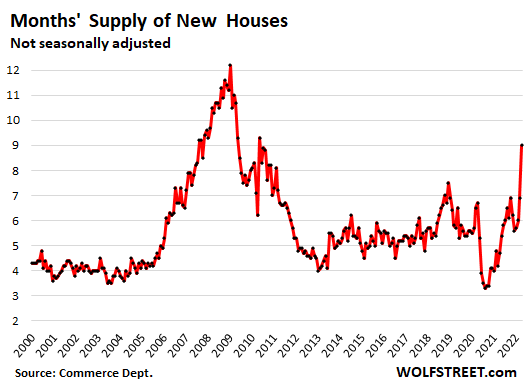

Supply of unsold new houses spiked in a historic month-to-month leap from an already high 6.9 months’ supply in March to a dizzying 9.0 months’ supply in April, having nearly doubled from a year ago:

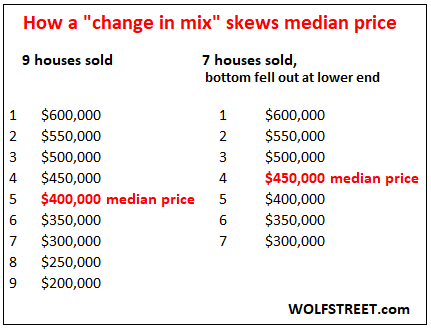

The bottom fell out under $400,000. At the top end, things weren’t so bad: sales were flat year-over-year in the $400,000 to $750,000 range, though they fell on a month-to-month basis. But you cannot maintain a housing market by just selling to the wealthy.

In the price categories below $400,000, the bottom fell out. The drop in sales year-over-year:

- $300k to $400k: -42%

- $200k to $300k: -71%

- $200: dead.

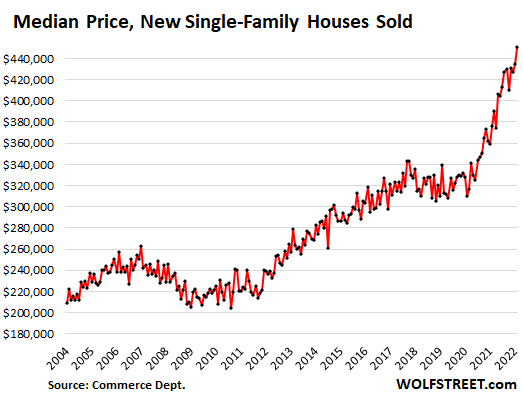

Collapse in sales below $400K changed the mix, skewing the median price.

The median price is the price in the middle. My favorite example: To get the median price in a market where 9 homes sold, you list them by price from the highest to the lowest, and the price of the fifth house from the top or the fifth from the bottom (same house) is the price in the middle, which forms the median price.

Now imagine, two buyers that would have bought the cheapest two houses can’t afford to buy them, and the sales don’t happen. But the remaining seven homes sell. The middle is now the fourth house down, or the fourth house up. This change in mix skews the metric of the median price simply by the way the median price is determined, though the prices of the homes haven’t changed:

And this change in mix is what happened in reality too. The mix changed dramatically, with the bottom falling out below $400k in terms of sales, but sales above $400k were able to hang in there. And this change in mix pushed up the median price to a new record of $450,600, up by 19.6% from a year ago:

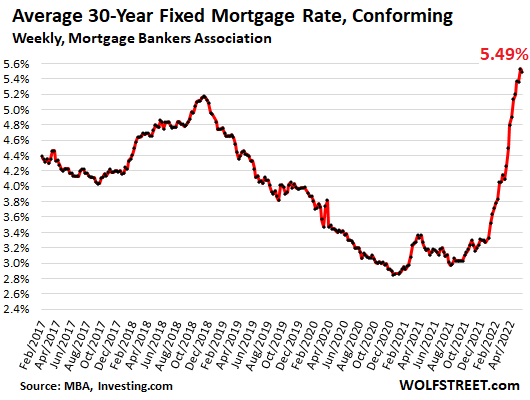

Homebuyers struggle with spiking mortgage rates which make the high home prices that much more difficult to deal with. And with each increase in mortgage rates, and with each increase in home prices, entire layers of potential buyers abandon the market, and sales volume plunges:

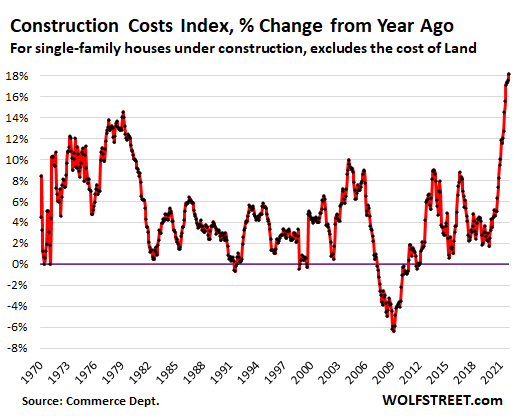

Homebuilders struggle with the worst inflation ever in construction costs, amid shortages of materials, supplies, and labor that tangle up construction projects, cause huge delays and cost-overruns, stall deliveries of completed houses, and cause immense frustration all around.

Construction costs of single-family houses – excluding the cost of land and other non-construction costs – spiked by 18.2% year-over-year, the worst spike ever in the data going back to 1964, and the fifth month in a row with year-over-year spikes of over 17%, according to separate data from the Census Bureau today. April was the 12th month in a row with double-digit cost spikes – which explains in part why the bottom is falling out at homes below $400,000:

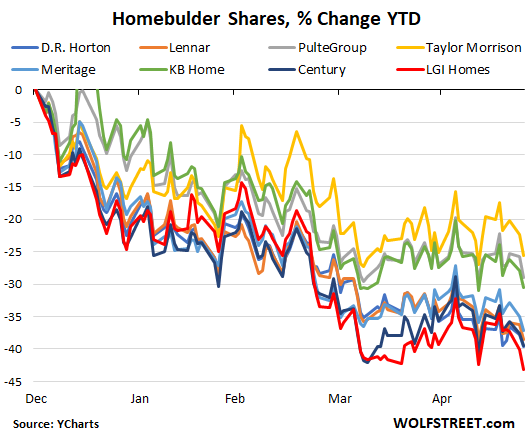

Homebuilder stocks have gotten crushed for months, and swooned again today upon the news. This list and chart of the major homebuilders show the year-to-date declines in percent as of early afternoon today (data via YCharts):

- R. Horton: -39.6%

- Lennar: -38.5%

- PulteGroup: -29.0%

- Taylor Morrison: -25.5%

- Meritage: -37.2%

- NVR: -31.2

- KB Home: -30.6%

- Century: -39.5%

- LGI Homes: -43.1%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s amazing how naive people are when they say things like there aren’t enough houses or this or that. Everything is available for a price. Its the price that matters. The Super Bowl is sold out every year. They aren’t making enough tickets I guess. Yet you can always get one. Just pay up. Magically you can get as many tickets as you want. Well guess what happens when money is no longer free. This isn’t that hard.

If the Fed is lucky they will be able to return all asset prices back to about where they were before the pandemic. A lot of people might have got sucked in by the huge money dump and eat a loss. You can’t print real prosperity.

If the Fed is able to return all asset prices back to about where they were before the pandemic, there will be few who will consider themselves or the Fed to be lucky. It will take a very deep recession, maybe a depression, to wring out the widespread inflationary expectations of the public and drive prices back to 2019 levels. I don’t think the Fed has the guts to go that far.

It happens slowly, then all at once.

At 2019 levels, the stock market is still in deep “nose blee” territory.

The majority of Americans are destined to become poorer or a lot poorer, no matter what the FRB and government does or doesn’t do.

Attempts to prolong the asset mania and fake “growth” that goes with it doesn’t change the outcome.

I dunno building materials are already dropping. Lumber has dropped a lot with copper not far behind. I think labor will be the last shoe to drop.

Fed is gonna fight inflation. They have no choice. If the fight causes big corrections, then there will be big corrections. I think we could have the corrections without the fight, but the fight could cause them to occur sooner.

Shake and shake the ketchup bottle. None’ll come and then a lot’ll.

YOU SIMPLY CANNOT get back to 2019 fiat $dollar level

the fiat $dollar is being massively(has to) devalued

so even depression means FOOD PRICES continue up up and away

and I’ll put $trillion bet on UTILITIES only going UP

and don’t forget our ILLEGAL PROPERTY TAXES – only one way sign on them

Let’s hope they fall back to 2009 prices. Too bad, so sad.

Porcelain Economist

“It happens slowly, then all at once.”

But,

“Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, one by one.”

― Charles MacKay, Extraordinary Popular Delusions and the Madness of Crowds

“f the Fed is lucky” . . . like winning the lottery lucky?

These booms and busts simply cannot be engineered by a government (and a lapdog Fed) that really cares for the majority of the populace. The conclusion is obvious.

think you have your analogy backwards … today the government is the lapdog

in the NEW FINANCIALIZED country – the social engineering will always result in road kill

as in 99%

and yes the fed ALWAYS picks the winners and losers

—

I would put big $$$ on it that jerry informed the 1% to bail back in december – I noticed tremors

“If the Fed is lucky they will be able to return all asset prices back to about where they were before the pandemic.:

———————————————–

High asset prices are most unlucky for the consumer and investor. Prices need to continue to fall.

Most would be better off if prices fell by 50% …………… or more.

I haven’t heard anything from the fed saying the want to return asset prices back to any previous point in time. I would assume that would take deflation. Everything I’ve heard from the fed is that they want to cub the extreme inflation rate to a more sustainable inflation rate. ie asset prices will continue to go up. Not saying there won’t be a correction in asset prices as people start realizing the real values of what they purchase. There is no undoing what has already happened.

Asset price inflation is NOT like consumer price inflation. Asset prices go up hard, and the come down hard, as we’re seeing. That’s not a biggie. Happens all the time after big bouts of asset price inflation.

The Fed is not lucky, its corrupt.

French central bank governor said Euro long term real neutral rate is most likely between negative 1 and zero. I believe he said they want to get rates to the neutral rate within two years. To me it’s very simple. When you can create fiat money out of thin air then real savings in fiat is worthless to a central banker.

You noted that home sales in the upper price ranges had not declined. I think this is simply because the massive price increases have pulled more homes up into that category. Another factor is that those higher priced homes are more likely to be investments and sellers get more attached to the idea of making a killing on a high priced home than a cheap home. Those high priced homes just need to sit there a while. Inventories are still low in some markets and need to build.

The housing market is a couple months away from spiraling into a massive hole.

One of the other issues is the lag in home price discovery. The most recent comps are all from homes sold in a lower interest rate environment. There is a lag on interest rates as they are locked for a period of time, then the lag on comps, so home sellers, buyers and real estate agents are basing pricing off of old information. So sellers are asking too much for their homes. Give it another 4 months and we will see home prices falling rapidly back down. First demand collapses, then inventory shoots higher, then prices fall, then even more inventory gets put on the market, then demand falls even farther as people realize they can wait and get it cheaper, then foreclosures begin to happen again and finally, 3 years later, we hit a new bottom.

My guess is that the Fed will be very wary of ever dropping interest rates this low ever again. As a result, we will not have them put a net under the declines in home prices. Look for 50% price declines in many areas (from the peak).

Yes, that is how things will likely play out. The jury is still out on how the Fed will respond to falling asset prices. If interest rates tame inflation and a recession follows, will the Fed slam on the brakes again? Or, will it consider it over-acted in 2020 and temper that inclination? The economy probably didn’t need both fiscal and monetary stimulus. We deliberately closed the economies. It wasn’t cylical.

I guess I’m old school. When I’m considering buying or trading anything, I care about p/e ratios & dividends and price to income or price to rent ratios.

Buying because of short term price fluctuations or signing up for a 30-year mortgage in an amount the bank assumes you will be able to carry assuming no income volatility with an at-will employer relationship seems absolutely insane. Then throw in the variables of no one knows whether the WFH’ers will be the first to be laid off and whether WFH has staying power…seems like a lot of folks leveraged themselves with a very uncertain future.

you forgot they ‘engineered’ new 40 year mortgage for those who couldn’t pay

“To get a loan, you must first prove you don’t need one” – old school

Surprised I have never heard that! I like it.

The version I remember is, “You only get a loan if you don’t need one.”

A banker is a person who lends you an umbrella on a sunny day, and snatches it back as the rain starts.

I agree. Solid/decent balance sheet, low PE, excellent EPS, high dividend yield (above 4%) have generated strong appreciation YTD. Tickers in my portfolio include DOW, PM, XOM, CVX, GILD. then my hedge TWM. Been my portfolio for about a year. Might be a temp top. But not mad that’s for sure.

I think WFH’ers will maybe be the last to be laid off. Rent is expensive. Getting rid of office workers first allows a company to downsize its footprint and save more money.

How about WFHers that are working for a dog shit startup company that is relying on cheap money? The writing is in the sand. We have too many companies that provide little to no value in our economy. They are zombie corps with employees that provide nothing of value.

No so.

No site?

No WARN Act protection.

That’s the difference between a 60-day severance and a 14-day severance.

WARN act doesn’t specify any severance.

Yes, agree. The other important thing is that WFHers will be able to accept bigger pay cuts in a downturn. This is something we haven’t seen yet, with WFHers currently standing their ground on getting the same salary while the job market is on rocket fuel. But throw in a downturn and we’ll quickly see where their new bid price is at, and my guess is that it will be well below their commuter drone buddies.

If I was the CEO of a business now, I would be rapidly preparing for the day when WFH is a huge cost savings to my company. Because when the crunch hits and line-by-line costs savings get rolled out, the competitor who has figured WFH out is going to clean up.

Got another Nate around – cool :) Good comments too.

Running money professionally means that your time horizon is usually 18 months or less. I saw a study once that said buying on fundamentals was negatively correlated to performance until you pass five year horizon and from that point on it is positive.

In my mind the retail investor has two advantages:

1. Not having short term reward system.

2. Working with small sums of money.

Those two are the biggest advantages (and #2 has a lot of corollaries), but one might extend the list:

3. Not having to convince a committee to support your idea.

4. Not worrying about investor redemptions … at the worst possible moments.

5. Not being constrained by “our fund only does X, Y, Z” prospectus limits.

That’s a very good list.

The incredibly fast/deep year over year collapse in sales volumes indicates just how utterly dependent housing affordability has become on ZIRP.

(Even if there still were lunatic buyers out there at super ZIRP’ed prices, no banks are going to qualify them).

Pull that Fed interest rate figleaf/curtain/shroud back even a bit (5% mortgage rates when 8%+ were normal in 90’s and earlier) and the House of Lies collapses – fast and hard.

Any time over the last 20 years, the Fed could have at *least* made an announcement that ZIRP would not improve employment levels very much (presumably the Fed’s goal – very poorly achieved in practice) so long as grossly inflated home construction prices took precedence over home price affordability (builders have a lot of control over the types/pricing/numbers of homes they bring to the mkt).

But instead of builders targeting more affordable/numerous homes utilizing ZIRP, they simply built fewer, larger, more expense homes and let ZIRP keep affordability constant (despite a very poorly performing economy).

The Fed had over 240 months in which to course correct, cajole, pronounce, etc.

But for the overwhelming part, it just stood there, ZIRP’d, brain dead, paralyzed.

And now when the reckoning comes, inevitable inflation (read diluted-currency deflation) forcing the Fed’s hand, entire mkts unwind with a sudden crash.

So much for stability objectives.

(And this ain’t *nothing” compared to what will happen when money printing/dollar dilution (DC’s only “fix” for its grotesquely unbalanced books) hits the intl value of the USD. Try importing – America’s only skill – when nobody really wants your currency)

Aren’t these ways they can keep global demand for the dollar in the near future?:

1. Being the most stable central bank system and the power/profits that come with dominant world reserve currency.

2. Increasing demand by raising Treasury interest rates.

3. Maintaining the world’s largest and most powerful military.

(not a war hawk here, just pointing out a fact)

Degobah,

The Taliban (Afghanistan *tribesmen*) just made the US military “leadership” (“World’s Most Powerful” TM) look like incompetent and corrupt fools for 20 *years*.

At least the grotesquely corrupt Russian military has the long latent will to compel its high brass to die on a battlefield, accounting for their sins.

US military high brass f*ck around in a private Jet fleet (look up US military equipment rosters – there are dozens of private luxury jets) and do their best to ignore/evade 20 years of humiliation.

And the only officer held accountable for this two decade farce in the Middle East (Iraq was almost lost too – had to be refought starting in 2014) was the only poor bastard to call the Generals out.

And those same Lear Jet jackasses sh*canned him in less than a week – after they themselves miserably failed for *20 years*.

So I don’t think too many in the world still quake at the awe and majesty of the US military – a fish rotting from the head down.

actually for cas:

AGREE totally,,, in spite of my regard for any of the folks willing and able to put up with the bull pucky that MUST be put up with,, and more???

How some ever,,, the most real and challenging part of all this is that these same folks in control of our WAR department(s) are still ”fighting the last war” as has been very very clear for many decades now, and was has been at least somewhat equally clear since Waterloo (1815 or so )…

Not sure IF WE the PEONs have any recourse since ALL or almost all of our elected folks really have NO clue what so ever re the control of the ”war mongers.”

Like any bad plan, the war in Afghanistan had no objectives and had no success criteria. It was a failed mission from the moment the first troops arrived.

The military did not decide to invade Afghanistan, politicians did. The politicians were responsible for the disaster, not the military.

Drifter,

1) Soaring inflation does not bespeak “stability” – it bespeaks corrupt money printing

2) Reserve currencies that abuse their status, lose it. An anchor that drowns you has little utility – and everybody starts hunting for a more trustworthy anchor.

3) Paying out more phoney baloney monopoly money in interest to cover for the fact that it *is* phoney baloney monopoly money only works up to a point.

Otherwise every Latin American nation in history could have printed its way to magnificence rather than capital flight and penury. If people don’t trust your currency to hold its value, promising them more of it in interest stops working after a while.

Cas127 – I totally agree with you but seems like it might be a least-dirty-shirt-in-the-closet situation.

Even a brief study of financial history shows that asset bubbles should be avoided if at all possible. You might could say in theory a central bank’s job is to be counter cyclical to prevent bubbles from forming.

The problem has been that the Fed refused to acknowledge—at least publicly—the effect of monetary policy on asset prices. Bernanke is largely to blame. He openly suggested asset prices were not in the Fed’s remit. While true, the effects were clear. Greenspan was more honest, but his warnings were met with derision. Powell wanted to normalise rates, but presumably came under the same pressure from market makers. The ‘Fed put’ has even become a topic of academic research. The Bank for International Settlements (the central bank for all central banks) has written a paper on it. It looks very much like a very un-independent institution.

The median price of a house doubled! in ten years. And then mortgage rates go up, making them even less affordable. The distortions are immense.

The housing market isn’t just going to pop. It’s going to detonate, and take a lot of the US economy with it when it goes.

It’s just one house but I just saw a $500k reduction on a house in the Bay Area that is now listed $1M below the Zestimate. Still over $2M but I’m hoping this is the start of a new trend. Btw there is nothing wrong with the house and it was recently updated.

Probably someone with margin calls or the initial price was wrong.

My pick is the housing market for those not needing a mortgage or those that can handle a mortgage with a rate that is still way lower than inflation will continue to do OK; people are diversifying away from the tech stock market for obvious reasons

Your pointing to a small fraction of buyers. Sure, they’ll be ok, but the market needs waaay more than them. If they are the only ones buying, the market is in big trouble.

Moosy…

I agree. The impact of this sudden 25% drop in stocks has yet to manifest itself….but it will, and it will display some over leveraging, some pyramiding, and will lead to some selling.

I believe I read house prices are at record 8 X household income in USA or maybe it’s just in certain areas. But the norm today is household income is 2 people working with less than two children.

When I was growing up my mother didn’t work until I got in school and then she only did a little part time work. My parent’s house was paid off in 10 years basically on one “auto mechanics” salary. Sure it was modest, but it was sufficient. My parents had zero debt after age 35.

Old School,

Pretty much the same as my folks. Dad was a Chemical Engineer. Mom stayed at home.

She volunteered at Church after the youngest went to school full time. They were debt free at about 45 or so. (Dad claimed they bought the house using the ‘Slavic Easy Payment Plan’ … 100% down payment. :-} )

We’re retired and looking to downsize. When our friends say … “you might have rpto carry two mortgages at the same time” … we say our home HAS no mortgage. Their blank stares are telling.

Old School,

My parents were similar. Dad worked full-time and mom stayed home to watch the kids. When the kids were all in school, mom became our lunch lady at school so she could be home when we all got home.

They were always debt-free except for a mortgage. They could have been mortgage-free at age 40 but their 30 year mortgage rate was around 5% and their long-term insured bank accounts were paying 8+%. It didn’t make sense to be mortgage-free at that time. The Silent Generation homeowners benefited from high inflation at that time. Will late Boomers and Gen-X benefit the same way now?

The mentality of the silent generation was different on debt also.

I never heard of my parent’s friends having HELOCs or cash-out refi’ing their home equity. Did they not exist in the 70’s and 80’s?

Now, it seems pulling available equity out of a home is more common.

On one hand, having a 3% maxed out mortgage if insured accounts in banks are paying >5% would seem like a good idea.

Investing in SNOW, Netflix, or Bitcoin would IMHO be a bad idea. Insured bank accounts are not at 5%, yet….. Speculative investing has been shown by Wolf to be a VERY bad idea this year.

I know people with 200K mortgages at 3% on a million dollar house. They could theoretically pull out 600K in equity now.

Monthly payments- 30 year mortgage:

3% on 200K – 843/month

5.5% on 600K Second mortgage – 3400/month

Total: 4200/month.

You had better have investments paying better than $4200/month on the 800K just to pay the mortgage monthly and not lose the house. (I’m throwing in principal payments in the total monthly also. )

I don’t think I’d trade an 843/month payment for a 4200/month payment. I’m too conservative.

Dang! Just looked at prices and they have not budged from highs around Ohio. Builders are very slow to react I guess.

No surprise there with the level of entrenched inflation and low unemployment. It may take as much as 6 months for listing prices to continue to fall, depending on how 30YFRM react to June’s start Fed QT in MBS. The problem as housing fights to hang onto low prices, this will force the Fed to continue raising the FFR and possibly accelerating QT.

The guys who determine the short term price are relatively small in number. I think the guys to watch this time are the investor companies and bigger SFH landlords.

The Fed is even more late at the party than they were in the 70s. It took then 10 years, 2 recessions, and massive offshoring to China to stop inflation. Nothing’s gonna stop it now, with inequality through the roof, real economy on monetary and fiscal life support, asset bubbles everywhere. It’s gonna get ugly before it gets worse.

Home prices are not defined by price/inflation but by affordability/demand, especially those offered by builders. Builders may build a home for 500K but may sell it for 400K.

Sell it for less than the cost? Explain how they do that and stay afloat.

Classic observation/reality: Real Estate is local.

Just like inflation is personal for each individual.

The centralist policy of interest rates being dictated nationally instead of guided locally is another aberration that should be abandoned – every region has its own demand profile. Perhaps that was the original objective of the Fed having 12 regional divisions.

You have it half right.

Why would you believe that any attempt to price fix the cost of borrowing (interest rates) will be more successful regionally?

No one knows the “correct” interest rate because there isn’t one, any more than there is for the price of anything else.

Something just costs what it costs based upon supply and demand.

AF-agree, but careful saying that around folks when referring to gasoline or diesel…(controlling how much is being refined to availabilty is a different question…).

may we all find a better day.

“Guided” locally, i.e. based on local demand was meant to be more subtle, rather than ‘fixed’, and I mean right down to individual banks. Anything fixed in price the price immediately becomes obsolete, distorting the market.

Real estate is local but cheap money was universally available irrespective of location.

Robert is mostly right. RE was moving toward a national market but climate change and political demographics changed it back. Ellen Brown supports the notion of regional ‘central’ banks. Of course running different regional interest rates suggests all sorts of arbitrage gambits or carry trade scenarios.

This is all good news. Supply is strong, prices are rising. Wages are on the rise for the first time in decades. Home builders are off because the day of the large development is over. The more stonks go down the more investors want to put their money in hard assets. Home prices could probably double from here in five years, though it might be on lower volume. A players market..

Then go buy that house to flip.

Investor best bet despite 8% inflation is in cash for now, just look at the 2T reverse repos and you realize that many waiting for a dipper correction in sucks and even housing.

The $2T in reverses repo monies will be the first spent on repurchasing all of the assets on the Fed’s balance sheet.

i see your name here often and i’m reading what you’ve posted and think to myself… do you read the articles?

posting to get hits on the link in the name? :)

Sarcasm, correct?

No, read his prior posts.

He’s writing about an alternate universe.

Exactly. This guy reads like his cheese slid off the cracker.

Depth Charge,

Just spit my beer all over the keyboard. Your fault.

SocalJohn,

That’s how I read it.

Yeah like building castles on sand! Go and buy and flip ! Come and buy mine !

I have noticed almost zero multi family housing for sale in my investment area – Bellingham, WA.

I wonder if more investors are switching from S&B ‘s to income producing real estate?

In areas where there is strong demand and no rent control and no income tax, at least.

A perfect example of you have the power to convince yourself of any version of truth..

To paraphrase someone despicable that just came out with a book this week..”You are entitled to your alternate facts”

Phoenix,

I don’t quite understand this? Are you saying all that money I am collecting in rents is not real? Could you please convince the IRS of that for me?

All I am doing is reporting what I see around me.

For example, where I live in Redmond I have seen two houses sell in the last week, one for $600,000 over listing and the other for $700,000 over listing. I don’t see how it can last but it hasn’t stopped yet.

I have also seen some price drops.

In Bellingham, even though there has been a lot of new construction none of these buildings have come up for sale-the developers are hanging on to them.

The only multi family I see for sale are smaller, older [some over a 100 years old] buildings that are going for 3.5% cap rates. And they sell.

Someone has to be buying this junk. Possibly stock investors bailing out of the S&P?

Maybe the real estate fall is going to trail the stock market crash by a couple of years. Maybe not.

I will keep you posted.

Urgh…what are you talking about? My reply was to Ambrose, look at the thread link

Could be, never underestimate what people can do. You’d think people would start to understand it is cheaper to rent than to buy throughout most of the country and investors would start to realize the 5-10 year IRR of buying a house is low single digit optimistically but you never know, they owned a lot of stocks priced to earn 0% IRR or worse last year.

Funny Ambrose, I like sarcasm

Quoting the Big short with

“This is all good news. Supply is strong, prices are rising.”One of my favourite lines………

You forgot the line….”they are in a bit of a gully at the moment”

An Occurrence at Owl Creek Bridge Realty.

In April 2013, 30YFRM were ~ 3.6%. By March 2020, they were the exact same rate. Over 7 years, the rate fluctuated in a band of 3.6% to about 5.10% four months before COVID, when Trump forced JPowell to start lowering rates. And boy did those rates fall.

As Wolf points out, the median home price has doubled since April 2013 with a significant portion of that jump coming in just the last two years. While this is not unprecedented, the forces at play pushing up inflation will ensure there’s no way the Fed can engineer a soft landing. The questions are when and how hard.

I’m keeping an eye on a gated community in ventura county. I’ve seen 400K-500K price reductions on three different listings. Still, even with these reductions, the homes are listed at a significant premium to their pre-COVID market values. However, it’s still early, so we could see further price reductions in the months ahead.

Are insurance companies still offering fire insurance in Ventura? Ballsy if so!

RemoteWorks,

I had to look up where Ventua county is. I could never work out why there were fires near so many expensive houses in California and then I looked at how far south LA actually is. Being a Brit I didn’t realise Los Angeles is at the same latitude as Algeria/Tunisia/Syria and Iran…..

If you said to me that sometimes Algeria in North Africa has a drought I would probably say…so what….

I was even more surprised to see that Houston Texas is further south than Cairo in Egypt, which explains why they need air conditioning lol

ps my cousins live in Thousand Oaks which looks to be around there….

Yes it is interesting. Paris is way north of New York city but but it rarely snows there. The Jet Stream makes a lot of northern Europe have relatively mild weather. The day the Jet Stream weakens or moves south is the day a lot of countries are in trouble.

I lived in Thousand Oaks from 12 years. Nice town in Ventura County.

Being an American, I of course did not realize how far south (globally) LA and Houston are either!

Josh

I’m English and my city had no snow last winter at all and we are 53 degrees north, roughly the same as Hamilton in Canada and Minsk in Belarus…….

Well, 1 house is sold, 99 house owners located nearby have their property taxes reassessed upwards (except those blessed with Prop 13 which will be abolished soon).

FRED:

National Totals of State and Local Tax Revenue: T01 Property Taxes for the United States QTAXT01QTAXCAT1USNO

From $120B to $240B in just one f… year – see the red/blue bar chart.That’s what I call REAL skyrocketing.

Our Sacred Cows – cops, teachers, firefighters – should not worry about their $100K-$200K pensions not being adequately funded.Good job Uncle Jerome !!!

Do you actually know any retired teachers? A retired teacher in Texas after working 30 years gets a pension of about 24k a year.

At least Texas seems sensible – it actually seems to be a funded plan. The North, West, and East? No.

Texas teacher’s pension is only under funded by $50 billion, so as long as they get returns of 7.5%, they should be good.

Much like the electrical grid, Texas teachers are on their own as they don’t pay into SS or Medicare.

I’ve never once met an underpaid public school teacher.

Teachers in Uvalde, TX were underpaid today.

Then you know no teachers

I’m from Chica-Go-Go, Illinoise.

2 years ago fatso Pritzker (IL Governor) uttered piercing cries ” WE NEED $39B RIGHT NOW, ASAP, TO FIX THE BUDGET”. This year everything is copacetic. I wonder why.

God bless TX – my favorite State. I travel a lot, I can compare.And God bless Junior Brown who cheers me up when I drive there 😀

Hey now! Don’t pick on Pritzker. He’s the best thing that ever happened to neighboring states.

I have lived in Texas for over thirty years. It has gotten worse and worse every year. Finally we are calling it quits and moving back to civilization.

Escierto,

Well, regarding your imminent departure…

…to quote the movie, Tombstone,

“Well…bye”

My best friend’s wife is a retired teacher in The Woodlands, Texas. 30 years of teaching gets her about $2,400/month. After taxes, its about $2,000/month

Assuming your stats are correct (but see below), what is the present value of 20 to 40 years of $30k per yr payments?

That present value is the amount that taxpayers have to “save” in the pension fund in order to cover each such teacher pension.

How many current/future payees are in the pension fund? (In many states, non-teacher admin personnel are included in the fund – and make up a disturbingly high percentage of public section “educational” employment).

Another question…is there a parallel 401k type teacher pension fund that taxpayers also contribute to and that operates in parallel to the better known defined benefit ones? Such things exist in some places.

Not sure if TX pays teachers based on education level, but here in GA, it’s pretty sweet deal. We get 2% for every year we work up to 30 years, and I think that can go as high as ~33 years.

So a T6 (Education Specialist – above masters but below Dr) in my school district will retire making at least 60% of their highest two years salary which tops out at about $86,600 or about $52,000 a year. And, we pay into SS, so that benefit if you wait until 65 would be at least $2,400.

The last I checked I think the GA TRS is upwards of 90% funded. I know T6 teachers who’s spouse are T6 as well, and they’ll be making upwards of $160,000 in retirement with TSR & SS.

Escierto,

Link to your data on Teacher pension amounts, salary replacement ratios, etc., please.

In many, many public pensions replacement ratios are applied against “x last years’ salary” and the ratios are often significant (US military after 20 years = 50%).

Also, it is well to keep in mind that teachers likely work 75% or less of the annual work hours of non-governmental workers (due to public union negotiations against…politicians)

There are many other questions that can be asked and factors weighed when it comes to mass lifetime public sector pensions.

Absolutely, man! I only work 190 days a year, so I get 3 months off. It’s a sweet deal. You just have to get up to a T6 Specialist as quickly as possible.

If you look up “average teacher pensions” by state you’ll see that most states in the country have low pensions for teachers, unlike the few examples here of outliers like Illinois, California, etc.

Taught in the wrong state. LOL

I just read that the average Chicago teacher with 30 years retiring at 55 would get an annual benefit of 76k, lifetime contributions were 98k and will recoup their contribution in 4.4 months.

Chicago Public Schools teachers can retire as young as 55, receive up to 75% of their final average salary in pension benefits and receive 3% compounded annual post-retirement increases regardless of inflation. That 3% permanent annual raise doubles the size of the first-year pension benefit after 25 years.

But…On average, to earn a full pension, a teacher must remain in the same state or district for 25 years — a condition that less than half of teachers nationally will meet. In Illinois, where the vesting period for the pension system is 10 years of employment, only half of new teachers will ever vest in the system. And only 1 out of 5 teachers in Illinois will ever break even from their pension plan.

But if you are willing to stick it out, the pension is very good. I have a relative who retired 4 years ago in their mid 502 with a $92k pension as a teacher.

25 or 30 years as a public school teacher….anywhere….like a prison sentence. They deserve every penny.

It doesn’t take a genius to read the writing on the wall, home prices are going to plummet once interest rates continue to rise. Most of you have no idea what happened to real estate in the early 1980’s. Everyone was a developer or builder because banks extended credit to anyone with a pulse. Developers rode the roller coaster of variable interest rates reaching 20% on construction loans. Overnight their loan payments tripled. Mortgage lenders tightened the reins on home loans which in turn stopped new home sales completely. No sales meant no money for developers to pay the banks. In turn, the banks went bankrupt. FDIC owned it all by mid 1980’s. Home prices weren’t even a topic of discussion. History is repeating itself again. How do I know, I was one of those developers.

Same thing in 2007-2011.

You forgot to include farm land ,they got slaughtered

I know a retired CA High school teacher getting a pension of ~$100K.

family member in PA after 36 years with masters degree retired in 2014- runs about 4K a month w/ guaranteed COLA’s ….note…FOREVER. Retire at 61 live until US female nonsmoking average of 87, thats 26y x 48K = total of $1.25 million not including future COLA’s. nothing to sneeze at, add social security and assume home paid for. good to go and can enjoy retirement with no worries. Fair / not fair? not judging but seems a little higher than it should be.

The City I work for requires me to pay 10% of my salary every month towards the fund. Over 30 years that can be a quarter of a million dollars paid out of the monthly salary that one may or may not live to see paid back in retirement. But I’m not a teacher, I work year round and will get ss also.

More recent hires to my PA school district were put on an alternate pension plan years before I was hired in 2014; there is no routine COLA component on this newer plan except by special decree.

Will…..there are no COLAs with PA teacher pensions. I have been retired for 11 years after spending 33 years in the classroom……pension is exactly the same as when I walked out the door.

TX has very sensible public pension plans, as do many other states. IL, NY, CA, outrageous taxpayer rip off pensions prior to some very minimal recent reforms, in CA, there are 40,000 retired employees with pensions of more than 100K, with the average full career retiree earning 75K, a totally unsustainable situation that will collapse into a steaming ruin at the next stock decline as CA depends on volatile high earners for about half of its revenue.

Prop 13’s not going anywhere. Where do you get your info??

In 2020 there were numerous articles in WS & NYT about Prop 15 and Prop 19 intended to dismantle Prop 13.

In 2022 “Happy days are here again, Boss”, Cali is sitting on $56B state budget surplus, looking for noble causes to spend it on …

Mark my words, Prop 15 and Prop 19 will re-emerge.Like herpes virus traveling from one’s spine and blossoming on one’s lips at the most inappropriate time.

“From $120B to $240B in just one f… year – see the red/blue bar chart.That’s what I call REAL skyrocketing“

I knew that couldn’t be true so I looked it up. Just a seasonal trough to peak. Comparing each year’s peak (or trough) shows the usual gradual increases. Your lucky Wolf didn’t call you on it.

Sorry guys, there is no housing bubble, and house price appreciation is only getting started. People will look for a safe place to park money, and homes are that right now. Home prices did just fine during the last rate cycle (2018). Buy now or forever be priced out.

(Per my RE agent friend last night, when I mentioned the prospect that house prices could in theory go down.)

Because as soon as mortgage rates crossed 5% in 2018 JPowell reversed course. That saved the housing market….then COVID happened which temporarily put housing in a recession for two months. This time they will need to double their balance sheet to save it. But I am not sure they are willing for that much of an inflation shock that would cause.

Housing and stock market don’t count, now they are trying to restore business.After nafta gave our country away .Most commodities are way up because China stockpiled food and metals .There always 2steps ahead of USA. Because we have to many silver spoon CEO

“People will look for a safe place to park money”

That’s not true, investors purchase activities already down according to multiple sources. It just dose not make sense to investor or even non investor to buy when prices are flattening at best or even falling soon… Plus look at 2T reverse repos to see where ppl actually parking their money.

I might have had the same real estate agent in 2007.

Isn’t it amazing the way that the agents lie through their teeth. Appreciate the sarcastic humor.

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.” – Upton Sinclair

Even worse, some of the agents do understand it and come up with ongoing BS regardless of the market conditions. Their final conclusion is always the same: now is the time to buy. Right this minute. I’ve yet to meet an agent who stated “the best thing to do now is wait.”

LOL you’re RE friend is scared for his meal ticket. of course that’s what he says.

2018 wasn’t given a chance to mature, and even then, prices were falling and demand waning.

flight to housing in such a rate sensitive environment for… investment purposes? BS. you’d buy treasuries and newly issued AAA debt. wait til mort. rates hit 7%. 8%.

i think i sense however there are a LOT of 401k cash out’ers and A LOT of FOMO buyers doing what EVER they can to get themselves a home.

At this point, it is less what they’re doing vs. what they did.

Soon it will be what they’re doing, to not lose the home.

Must be hard to be “friends” with someone like that. Either this person is incredibly dense or straight selling you heap of BS. Neither a good quality for a real friend IMHO

With friends like that, who needs enemies?

I keep hearing the battle cry, “But mortgage debt quality is so much better than before and homeowners are safe because they have so much equity!”

Nevermind that a huge number of mortgages have been issued to buyers who don’t have the “quality” to scrape up a decent down payment. Furthermore, equity is not the same as an actual dollar printed and put into circulation. Sorry, but if you can’t come up with 20% down, you probably can’t realistically afford the house with any reasonable margin of safety. And equity is only based a theoretical number that some buyer would be willing to pay. If that buyer’s willingness to pay evaporates, so does your equity. Guess what happens to a buyer’s willingness to pay as they watch interest rates and supply both go parabolic as shown in the charts above? That’s right, sales fall off a cliff, also as shown in the charts above. Prices are next on the chopping block once the usual lag time is figured in.

The Reddit bubble story is a lot of people invested in short term rentals (STRs) and are banking on lots of rental stays via AirBNB, VRBO and the like. With consumer wallets tightening from inflation, vacations might get cancelled or scaled back. Some are reportedly trying to convert to normal rentals, but if they bought recently they are likely to have less flexibility to reduce price a bunch. Plus it was popular to leverage up pretty good.

I talked to someone with one (who is now rehabbing a second one) and he said his is still booked all through the summer and was very highly profitable. His is less of a vacation thing and sounded like it was being used for temporary housing and short term work stays, so I dunno.

Vacations are early on the list of discretionary spending items to be cut in an economic downturn. Seems like a shaky foundation to support a mortgage. We won’t see these more extravagant types of expenditures meaningfully fall off right away though. There’s still a whole lot of newly minted monetized debt sloshing around in the economy. We’ve only just started to hear about layoffs in specific industries and cash-burning tech companies. Not if, but when those layoffs accelerate, the folks who lose a job as well as those afraid of losing their job next will scratch their vacation plans off of their calendar in a heartbeat.

This article focuses on sales of new homes, which could be a real leading indicator showing us where the market is headed, but new homes probably aren’t that popular among AirBNB/VRBO buyers. Vacation rentals may be a very big thing in specific tourist spots (along the coasts or in popular mountain towns), but I can’t imagine they’re a huge chunk of the overall market.

Not sure where one can track the percentages, but I know quite a few “new” investors getting into ABB at these prices. I try to warn them they are way over leveraging themselves at current prices and vacancy assumptions, but they don’t listen. I suspect ABB has contributed to some of the SFH shortages.

I further suspect I will be picking up more properties for pennies on the dollar in oh, about 18-24 months….

Pilot Doc, it’s possible that I’m underestimating the size of the vacation rental market. There are tourist traps that are rotten with vacation rentals for sure. Here in southern CA, the ski town of Big Bear and various beach cities come to mind. Just not sure how much weight ABB is pulling in most of the interior U.S. and thus I question its impact on overall housing volume. That being said, I’ll be delighted to see the ABB crowd crushed alongside my most hated group of human beings… House flippers. I can’t wait to see those greedy insects writhing in financial misery.

I waited patiently last time around and was rewarded for my patience. I’ve sold and, much like you, I’m waiting patiently again for the next inevitable downturn. Maybe it’ll be a great opportunity to get out of CA.

Agreed but this category of homes could become somewhat of an X-factor once the RE markets moves past a 10% downturn in the next 12-18 months. The only questions are:

Does the Fed put arrive to save housing?

And does the Congress Put (rent & mortgage forbearance) arrive again?

The short term rental segment is very large in ski towns in the West. Probably not a factor for most places people live.

Lending standards are still in the basement, just not in the sub-basement from housing bubble 1.0.

On your equity comment, 80% loan with a 20% down payment in the most overpriced US housing market ever is hardly conservative lending.

There is the perception of safety primarily due to government distortions: mortgage guarantees, the FRB “put”, QE, and fake “growth” from unprecedented deficits which creates the appearance of a more robust economy and the inflated incomes that go with it.

Like the economy and financial system on which it depends, the real estate market is built on a foundation of sand.

AF, I always read your comments with great interest. But you describe the general economy as though there’s some bedrock that it’s all built upon. I think that’s an illusion. If only the “foundational” parts of the economy were to exist, a good 90% of employment would disappear. Further, the nation-states would be erased in the same process. There’s no “there there”. It’s all a house of cards, but it’s a house of cards that has given one hell of a lot of people a good standard of living, longevity, a degree of civility (which is now being dismantled by the right wing and oligarchs) and the time and resources to contemplate economic ideas like yours.

There is no absolute or permanent stability. I’m aware of that.

But to the extent stability exists, internally within a society, it’s substantially the culture and social fabric. This is one of the primary differentiators, not (as an example only) whether a country has a lot of natural resources.

This is falling apart at the seams in the United States and the western world generally, but it just isn’t fully evident yet because it’s papered over by manic psychology and borrowing from the future.

As for the “foundational” parts of the economy, I don’t disagree.

Concurrently, there is a big difference between luxuries an affluent society can afford and enough members want versus the economic waste which passes for “growth” and consumption funded by unsustainable debt.

Juvinal: “Prosperity is more brutal than war.”

Mortgage quality very bad (2008): Bank is the bag holder. Mortgage quality very good: People are the bag holders. It may change the dynamic a bit because regular people may not have the grit to hold through a downturn like banks can do…. Watching how this turns out

Regular people who have bought home to live in and can afford to pay mortgage would be able to hold homes with no issues.

The problem would be investors/mon-n-pop landlords who have multiple homes and they may decide to sell if they get a sense that the market is going to go down.

I have many friends with many homes and they firmly believe come what may, home prices won’t go down at least in san diego.

Your friend’s mentality is the defining characteristic of a bubble. It was the same way in SD during hb1. I knew many in SD who lost their shirt.

“I have many friends with many homes and they firmly believe come what may, home prices won’t go down at least in san diego.”

Your friends are definitely right.

Love,

2007-2010

Tried to warn my old coworker about SD, but like many, just won’t listen and convince himself that the market will just level off..guess we will see how this show ends..

California recently passed a proposition, those inheriting a house must mostly do a forced sale in a short time window, to get a (now) hacked-off capital gains break. Not going to be a good time window, coming up. This is new arrivals voting themselves a tax share of others’ capital gains. that is so they can ruin the place worse than it already is.

They will when the Congress Put / rent & mortgage forbearance makes a return. Don’t worry. It’s coming.

Banks are not bag holders,mbs are and FED bought them ,means TAXPAYERS again . I’m tired of this shitshow. Hear Portugal is nice

I heard Uruguay, maybe?

Almost no mortgage underwritten against housing bubble 2.0 values is good quality.

Being able to afford it at or near the top of a market cycle is completely different than during or at the bottom of a bear market.

That’s the difference between “weak hands” who think they are “strong hands” but aren’t.

We have a home in Punta Gorda, FL we built 3 years ago before construction prices skyrocketed. Home construction here is insane and prices are going through the roof. Don’t know how this can be sustained because where are all these buyers coming from?

Former renters. Rents are skyrocketing.

Nope. Most of them are people speculating on the housing market just like they do on the stock market. There are some former renters and new household formations, of course but the majority I would wager are people buying second, third, and nth homes…

Correct. Home buyers for the purpose of shelter are sidelined in many metros. They simply cannot afford it. The market is now more speculative than it was during hb1. Guess how that ends…

Your forgetting work from home. In an apartment, that is pretty much undoable for a couple.

WFH is dying, which is a good thing. I’m encouraged by all the business leaders who are pointing out all its flaws. It will soon be thrown in the trash can of history.

Says the unemployed guy LMFAO!

Or Chinese offshore buying ,because they now China property is in trouble

You make a fat point.

I assume that is a rhetorical question. They are fleeing some other states.

The migration flow has been insane. It’s a demand thing.

KH,

Been here since 06..

The secret is out….

Dammit…

just for amusement cowg:

”There I was” back to work in Chicago in the fall of ’37 after selling everything in ’33, buying a sailboat and sailing ”The South Seas” until my partner cabled to Honolulu to say work was starting up again.

COLD,,, very very COLD!!!

”To heck with it, I’ll move to flower duh!

Looks like those builders in Florida might already be running out of buyers.

New house sales plunged the most in the South, which includes Florida: -19.8% for the month, -36.6% year-over-year.

Unsold inventory also spiked the most in the South, +53% year-over-year.

When you state ‘plunge’, is that in real value or in dollar value?

With all the extra dollars printed, houses have been going up in dollar value but how much in real value?

E.g if you sold your house 40 year ago for an amount X, you could live a number of years of that. If you sell that same house (in same state) now. Can you live longer of the proceeds or less?

If it is longer, then yes, house value has gone up. If it is less, then house value has gone down.

The number of years you can live of the proceed likely will plunge but the value in USD may actually stay around the same

You’re overthinking things. The housing market is turning. June will be the month that starts the downward sales prices in many areas once it’s reported in August.

“ Looks like those builders in Florida might already be running out of buyers.”

Not yet…

The damn things are popping up like mushrooms…

Everything in my hood never goes up for sale… it’s occupied on completion…

Everywhere around here has increased in population by 25-50% in the last ten years…

Part of the exception here is many people have sold in cold country and are plunking their profit into a home in this area…

I don’t think that it’s so much speculation ( but not saying it isn’t either), I think it’s more along the lines of “ we’re done”…

With 15-20 years of life left, I really don’t think they give a damn wether the house is $350k or $450k…

Wolf

Some drop that……..

High tax states in the northeast and upper midwest?

Alaska is the northern most state, and the state with the lowest tax burden (according to Wallethub). But I have never heard of anyone retiring and moving there.

Tennessee, Delaware and Wyoming are the next lowest taxed states. Again, I have never heard of anyone retiring and moving there, either.

I think climate is a better predictor of where people would like to live.

Holy shit man, TN is exploding. RE prices have doubled in 2 years. Infrastructure can’t keep up. People are moving here from all over the country.

The floodgates have been opened.

A once great place to live is being destroyed like everywhere else.

Recently in a previous story Wolf reported on unfinished new houses and various percentages of completeness- and how low NEW inventory numbers were a big deal. Now, in light of this new story I don’t understand how quickly the pendulum could swing this far.

I find myself in a predicament similar to the builders unable to get windows, appliances, and so forth as I started a build 9 months ago and things are trickling in – like the garage door I ordered 6 months ago… The windows ordered 4 months ago just arrived but the crew is long gone to install them and I’m waiting for them to come back. Plumbers don’t show up to finish things. Luckily I have a good electrician, but his rates went up faster than copper. I’ll count myself very lucky if I can finish and get my current residence sold before the whole thing goes down.

Tom H,

Don’t complain about your windows being 4 months late. I still cannot get my beer mugs, and I ordered them on May 31, 2021. Apparently, glass is being prioritized to make your windows instead of my mugs :-]

Booze bottles ,always needed in a recessionary environment

Do not drink that toxic pee.

Stick to cannabis.

When this is over you will still have your liver and brain cells.

Loup, yes even the desert sand hasn’t gotten scarce, sarcasm.

I heard that Canadian Liberal politician Adam Vaughan is trying to buy mortgage backed securities to prop the housing bubble.

Meanwhile, the Minister of Housing who owns rental properties, Ahmed Hussen, assented to increasing the immigration quota to 450,000 this year.

Good for the Chinese investors who own rental apartments in Toronto.

New business model of western democracies: sell out the locals, shelter foreign oligarchs’ funny money. Your kids will make nice nannies and butlers! Just ask England.

This data represents the transfer of wealth by the fed. Folks with assets and have sold those assets may be able to afford the spike in home prices would assume so.

Love the analysis of how the median price of the home is easily skewed.

“Love the analysis of how the median price of the home is easily skewed.”

This, in the extreme, would be a great real world example of “Simpson’s Paradox”.

Simpson’s Paradox example: sales price declines at both high end and low end, yet much greater high end sales (than before) increases overall

sales price.

Another example (my own) …

Team A’s overall shooting percentage is greater

than team Bs. Yet Team B has a higher percentage for both 3 point shooting and

2 point shooting. How is this possible ?

Team A shoots 55% at 2 point land, B shoots

58%.

Team A shoots 26% at 3s, B shoots 30%.

But…. 85% of As shots are from 2 point land where a relatively (to 3s) high percentage is made. By contrast B only shoots 40% from

2 land. The 60% B shoots from 3 land hurts their overall percentage much more so than the 15%

A shoots from 3 land.

Hence Bs overall percentage is less than As.

In essence B is the better shooting team but

A is tactically (strategically?) smarter with theirs

shooting mix. The difference in tactical

percentages is greater than the difference

in actual shooting percentages (both 2 and 3)

and so has the greater effect.

There are plenty of examples on the internet

of Simpson’s Paradox. See Wikipedia for instance. Moore and McCabe Intro to Stats has a nice example using 2 hospitals and patient

results. Hospital A appears better than B.

But when taking into account the overall health status (new factor), simplistically as

good or poor, then we get a reversal of outcomes: Hospital B performs better with

each category of patients but has a much higher ratio of poor health admissions than A.

Hence overall rating of B is worse than A.

Wait, if house sales keep dropping, soon to be followed by prices, what will they do with all those slots on cable TV now devoted to various kinds of house flippers and RE pumpers.

Maybe they can convert the RE pumper shows to something more relevant like, where they have Dog the Bounty hunter track down the house flippers who skip out on their mortgage in one of the recourse states.

There’s no drama in the USA more catchy than the woes of the fallen mighty, in bankruptcy, divorces, etc. TV will do fine. Note all the attention squandered on this Johnny Depp court fiasco.

Strange voyeuristic society that thinks their business is the private lives of people who just happen to work in front of a camera.

Makes the country look like a bunch of pathetic wretches.

IMO at least 2 years before the chicken little bubble pop headliners are right. Too little inventory in most of US. Skyrocketing rents. Unemplyment at 3.6% and wages are increasing. Increasing 30 yr old population with new families. Plus, Fed will most likely capitulate (wrongly IMO) with elections coming up driving rates lower again and stoking the markets. Lets see, I’m betting on a short term lull and then continued home price increases

“Too little inventory in most of US.”

RTGDFA and if you cannot read, at least look at the pictures, particularly the second picture, which is unsold inventory, which spiked by the most ever, to the highest level since May 2008; and then look at the third picture, which is months’ supply, which spiked to 9 months’ supply. Duh.

hey wolf, is this because more housing is returning to supply because of rising rates (e.g. investors are dumping housing for bonds, or people are starting to sell off their 2nd homes or foreclose) or is it because housing is now too expensive to buy?

This article and all the charts are just about *new* homes for sale. However, it could be the case that because people are also selling used homes that buyers have more choices now and part of the purchases are going to used homes instead of new homes. My guess would be that:

1) things have gotten too expensive both due to the higher prices and higher interest rates

2) people have lost down payments when the market/crypto crashed

3) some people are hesitant to buy because they believe a recession is coming and are worried they may get laid off or they believe the prices will come down further

I am one of the person who lost a decent chunk of money in the recent months.

Had some big purchases planned but holding off for now.

Few of my friends made bunch of money in last 2 years.. retired.. lost money and now are back work.

So, Zillow lost their butts in the flip business and I thought they cut their losses and ran. Does anyone know if they’re still unloading?

The reason I ask (you guessed it) — my crazy Zestimate went up again. Today.

Do they still have a *motive* for crazy numbers?

You used to be able to hit “more” on Zillow and filter for “Zillow-owned” properties. I see in the last month or so they have removed that feature. Probably because people were going crazy on Youtube and Reddit finding all their price reduced homes and homes they were going to lose money while flipping.

Nope, Zillow is pretty much a parody in itself now, same with Redfin. Zillow’s still forecasting 13% growth for the housing market next year..people as a collective should tell them to STFU

There is plenty of inventory in Boston area comparing with few months ago or even last year but most over priced even though many priced under zillmate and reducing further.

It is great and valuable to document the carnage, but at the end of the day you should ask why do we have these boom and bust real estate cycles?

What do we have to change?

Obviously it is government policy that is causing it.

How should we change it?

It is not just low interest rates causing it.

I pin the cause on income tax and it’s deductions, along with excessive flipping.

We should abolish the income tax , go to consumption taxes and make flipping not as lucrative.

I wrote a story on how to do that. The link is above. I would post it again next but I think my comment would be deleted.

We should be discussing what needs to be changed.

AJD: I fully agree with what you think we should do.

But I am very sure that everyone in the highest echelons know it too.

I think there are compelling reasons why they don’t want to do it. And those reasons could be that the higher echelons do not benefit from it.

That is, they are making tons of money from the churn, the flip, the higher commissions from home sale prices, the higher mortgage payments, etc. Everyone including the mortgage bankers, the brokers, the title companies – virtually everyone except the poor buyer makes a lot of money out of every transaction.

The market doesn’t work well when 4 out of 5 people in a home sales transaction benefit from higher prices.

Sean, you are right.

The buyers have far less influence on policy than all the people profiting from current policy.

It is a great problem.

Homebuyers have a *ton* more power than they know.

1) If a flaky local candidate in NYC could achieve national fame for “The rent is too damn high!” in eternally rent immiserated NYC during less costly times, a *national* movement baldly stating “home prices are way too f****** high” could start a literal revolution.

2) Two months into non-ZIRP economics, 70% are already saying the economy is doing poorly based off food inflation. What will a year’s worth of rent/mortgage pmt inflation do to public sentiment?

Pitchforks, torches, and tumbrels.

Coming to elections near you. Not that the alternatives will work either.

Consumption taxes are highly regressive.

SiCal,

Regression can be finessed.

Transaction taxes on more expensive house would be more.

More expensive cars could face higher taxes.

And so forth…

Proposals I’ve heard involve a pre-bate (?) Or whatever it’s called. The idea is that everyone gets a check to cover some basic amount of taxes. As such, the lower rungs do not really pay the consumption tax at all. The more stuff you buy, the more tax you pay. No need to single out certain expensive items for an extra tax (which never works anyway). Clinton introduced a big luxury tax on luxury boats (yachts and such). It caused boat builders to lose their jobs and was quickly reversed.

“It is not just low interest rates causing it.”

lol

“I pin the cause on income tax and it’s deductions”

LOL

“How should we change it?”

you don’t get to.

Howdy Ace!

Derision is not an actual argument.

Theory of Proper Taxation strongly supports taxation at the point money is actually spent.

Do you disagree or did you not even look at the link in my name?

But you are right, we do not get to, without significant efforts.

I agree that “Derision is not an actual argument.”

On the other hand, I can’t imagine a laudable thought process behind calling anything the “Theory of Proper “, and acting like that’s that, the name defines reality.

Lack of imagination is also not an argument.

If you want to critique the argument, I posted the link above, just click on my name.

Flipping doesn’t work without bubble/mania psychology.

Income taxation of real estate has changed regularly since I first read about it in the 80’s, but don’t think this is a primary reason for speculation.

The psychology behind housing bubble 1.0 and the current one isn’t caused by income tax laws. Real estate had favorable tax treatment versus renting (sometimes more and sometimes less) long before housing ever reached bubble levels.

Generically, what needs to happen to end the mania mentality is to let people eat all their losses from their bad decisions, rich or poor.

Totally. I’m renting and looking to buy… besides the basics, the first thing I do is see if it’s a flip. I won’t touch them. I don’t care if the countertops are platinum plated. Not only do the flippers put in the Lowes and Depot leftover crap, there’s just something wrong about paying 50k – 200k more for the same pig with lipstick than when it didn’t have lipstick a year or two earlier.

I’ve been seeing this for the last 6 months in AZ and knew trouble was brewing. I have been spending my days talking with lenders, investors, new home builders and clients/prospects. I am a RE Agent and there has to be price drops dramatically or the mortgage applications will continue to slow down. The only people putting in mortgage applications now are rich people, people experiencing FOMO and that’s it. Normal buyers have stopped looking and are gonna sit tight. I sold two homes in last 18 months and am now renting. I saw the writing on the wall. Paying a premium to rent the last house I sold but with 800 credit score, I will jump in when the time is right. New builders are complete morons and are panicking now. Just in the last 10 days, I have seen things like “ now selling to investors” … that is a sign that they are panicking with unsold spec homes. When investors who are mostly smart, wait for drops, then prices will definitely drop big. Always a supply and demand but if job market shifts a little then people won’t feel comfortable buying a new home.

“ Totally. I’m renting and looking to buy… besides the basics, the first thing I do is see if it’s a flip”

Brother,

Nobody says you have to offer what they’re asking…

Most flippers get flipped into cash flow problems at some time or another…

Offer what you think is reasonable (regardless how you got there)… no law says you can’t…

They may need to dump the property to pay some bills and want to move it… especially if they see the market moving against them…

If your offer is rejected, be polite, leave your contact info and tell them if their circumstances change and they’ll sell at your price, give you a call…

Who knows, the guys wife might run off with a better flipper next month and he needs to move some things quick…

Have your ducks in a row and be able to move on something quickly…

Don’t be mad, be aware, smart and patient…

The most stable American housing period was 1945-1972. Look it up. And what is also true is that income tax rates were very much higher than today. The US Government was strong and capable.

So I would say it’s just the opposite. Deregulation, moving off the gold standard and defunding the very organizations established to protect us (like the IRS, SEC, FDA, etc,) are just a few of the factors that have fostered the something for nothing mentality that backs this speculative society.

The consumption tax you propose is just another wealth extraction devise to take money from legitimate production to oligarchic speculation. But they make neat little arguments about “equality” and “freedom” to get people to buy into it.

It’s the exact opposite of what is required.

For most of that period, the US was the lone economic superpower. Europe and Japan were rebuilding post WW2, and China was starving by the 10s of millions in the Great Leap Forward then destroying higher education in the Cultural Revolution. There was no real economic competition. Leaving the gold standard and the Vietnam War were colossal errors, but we could have had almost any tax policy during that time and done very well. And taxes were higher on paper but tax collections as a percentage of GDP were similar. Very few people paid the top rates because there were ample shelters.

Not sure how any of this is relevant to what I posted.

Housing prices were stable during the Bretton Woods period for a few reasons:

One mentioned in the post above mine, US was the only major economy not devasted by WWII which enabled a stable middle class.

Second, moderate but consistent USD debasement which supports collateral values and reduces servicing burden. This applies now too but the difference is there is a second housing bubble which makes the housing market unstable.

Third, low but more accurately priced interest rates. Mortgage rates were low but not distorted like now.

Four, financial system with low leverage. There was no credit or asset mania.

The combination of these factors made government created moral hazard (like mortgage guarantees and deposit insurance) temporarily stable and even to now, appear sustainable.

The reason why housing prices were unstable prior to the 1930’s is because lending long term with short term funding without fake government created stability is a high-risk proposition. MBS now distributes credit risk but the other distortions in the financial system caused mostly by government policy create an inherently unstable environment.

Fake government created stability replaced periodic “panics” with a future “fat tail” catastrophic system failure at an unknown date, aka a supposed “black swan”.

The prior environment cannot be recreated, as there is no such thing as a permanent “equilibrium” state managed by central planning.

The fundamentals supporting it are long gone and there is never something for nothing, ever.

Only going to quibble re, “The prior environment cannot be recreated, as there is no such thing as a permanent “equilibrium” state managed by central planning.”

And only because there is no such thing as a permanent equilibrium. Period

Only ”thing” permanent is change, the opposite in fact of equilibrium.

So far, eh?

The concept of long lending based on short resources is certainly ONE reason for the for ever prior instability of housing prices, but there are equally certainly others, including war, pestilence, famine/drought.

But first and foremost might be GREED, which seems to be one of the most egregious foundations of the financial morass many ( perhaps actually all ) are in these days.

“Obviously it is government policy that is causing it.”

Government policy is written by corporations who profit from them.

“We should abolish the income tax”

As if the billionaire class needs yet another windfall.

“We should be discussing what needs to be changed.”

We should be discussing your pleonexia.

“pleonexia”

sent me scrambling for a definition.

interesting choice of words.

It was new at the time.

Other favorites, like chrematistiki and exsanguination, also come in handy around here.

Aqius-

Don’t encourage him. He captured me weeks ago with “exsanguination,” and I’ve read Una religiously ever since!

It’s the cohort to penophobia….not what you think it is…😉

There are no sub 400k new houses for sale at all where I live. The cheapest is 800k+. So sales of 400k and lower dropped 100% here.

People are spending like there is no tomorrow. Costco might end up

visiting 2018 congestion area : 275 – 325.

Plus there’s talk about raising membership fee ,will opt out and go to sams club ,better prices anyway. Greed will hurt them badly in this environment

Once they change the price of the $1.50 hot dog and Coke, I’m GONE!

Didn’t that used to be a $1 combo?…

Not where I live.

Although our Costco was built about 5 years ago. That combo could have been $1 earlier than I have knowledge of.

Anthony,

I was just making an inflation joke.

“People are spending like there is no tomorrow.”

How prescient of them.

There’s a tomorrow for the free spenders. Sleep on a sidewalk, eat dry dog food. Yell at the sky.

Add hold cardboard signs and ask for money.

Unsold existing home inventory for sale, not pending, has been rapidly rising in my SW Florida town. Some homes in this area were used as winter seasonal residences, not as primary residences.

Some statistics include new home inventory that has not been built and in some cases homes where construction has not started. U.S. home prices have been rising every month reported this year, so far.

Month’s supply, new houses – at 9, at 2010 high, at the 2007 congestion area, on the left side of the bubble – might rise a little, before backing up during the summer months, possibly to 2006 congestion area, to 7 months ==> before moving up again, testing or breaching the previous all time high, until prices adjust.

One year supply is not good enough. Generation Z will ask for more, more months of supply, a different type of supply, because they need modern houses that make sense to them, fit their needs, not the ones from 1950’s to the early 2020’s.

What will gen Z pay with? NFTs? Cancelled student loan bills?

Pay???

What is this “pay” of which you speak…

Great analysis, and agree this market can’t hold if lower tier buyers start dropping out in big numbers. Though the West looks better than other regions, I’m starting to see both an uptick in new listings and some price cuts, which definitely wasn’t happening in Denver a few months back.

Latest Zumper Ntl Rent Rpt – Out of 100 metros followed, *69* saw annual rent hikes of 10% or

greater.

50 of those saw hikes of 15% or higher.

In one yr.

In normal yrs, in normal places, hikes are maybe 2% to 3%.

2010 renter occupied units as a percentage of all housing:

46.8% L.A. – Long Beach – Santa Ana

45.0% New York – New Jersey – Long Island

42.6% San Franciso – Oakland – Fremont

42.6% San Diego – Carlsbad – San Marcos

The 2020 census captures the new numbers.

It’s 65% in the City of San Francisco.

But they don’t pay asking rents unless they’re moving in. Zumper lists asking rents.

Wolf,