“The macroeconomic environment has deteriorated further and faster than anticipated.” Kathoomph. And Zoom gives up most of its knee-jerk mini-jump afterhours.

By Wolf Richter for WOLF STREET.

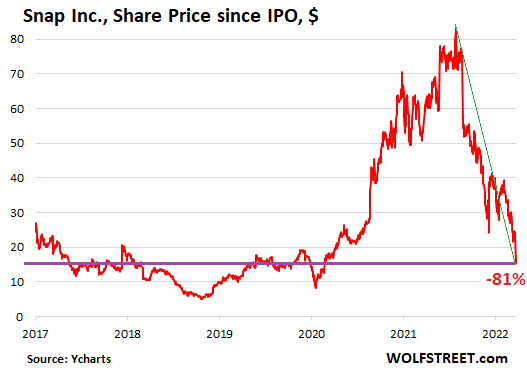

Shares of Snap fell through a trapdoor in afterhours trading today, WHOOSH, gone, after the company said in a filing with the SEC that “the macroeconomic environment has deteriorated further and faster than anticipated,” and that it therefore expects to “report revenue and adjusted EBITDA below the low end of our Q2 2022 guidance range,” without giving specifics.

It had issued this guidance just a month ago, on April 21. And now it walked it back. That didn’t last long.

In afterhours trading today, Snap shares kathoomphed 31%, to $15.51, below its IPO price of $17 back in March, 2017, and are now down 81% from the intraday high of September 24, 2021 (data via YCharts):

Back on February 2, Meta blew up the social media stocks, including Snap, when it said that Apple’s new privacy policy was hurting Meta’s spying business. Snap shares plunged 23%.

The next day, Snap counter-punches with its Q4 earnings and said everything is hunky-dory, and it hadn’t been hurt by Apple’s new privacy policies, and it reported its first-ever net profit, and it raised its guidance for revenues and active users.

In response, the stock [SNAP], which had been brutalized, knee-jerk-spiked as much as 62%! Dip buyers, if they dumped those shares right then and there, had a field day. Markets ate it up because Meta’s warning had just been a head-fake, and the good times were back. True believers that thought this was just another step toward infinity got re-crushed in what came next.

On April 21, Snap reported its Q1 earnings, namely a net loss that was 25% bigger than a year earlier, in what CEO Evan Spiegel infamously called a “challenging operating environment.” Some of the other metrics also missed analysts’ expectations.

It expected Q2 revenue to rise between 20% and 25%, below analysts’ estimate of 28%. But it forecasts daily users of about 344 million, above expectations of 341 million. And it said its profit measure of “adjusted EBITDA” would fall between breakeven and $50 million.

That was the guidance that Snap walked back today, with such spectacular effect.

During regular trading today, Snap shares had already dropped 3.4%, amid a huge rally for the rest of the world, which makes you wonder who knew what and when about this propitious announcement.

Snap thereby joined an ever-larger group of companies that have cut their earnings, often citing a laundry list of reasons, including surging costs of labor, materials, components, and transportation, shortages of all kinds, and waning consumer or corporate interest in their products. And so my column of Imploded Stocks gets more supply.

Earnings revisions are “deteriorating quickly,” said Morgan Stanley Wealth Management chief investment officer Lisa Shalett in a note today, cited by MarketWatch. “Negative earnings revisions and negative economic surprises could produce another 5% to 10% decline in the S&P 500,” she said.

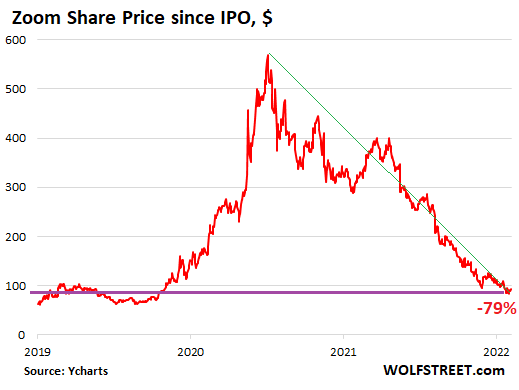

Even the shares of Zoom Video [ZM] gave up much of their knee-jerk 20% spike afterhours, and are now up just 4.8%, to $93.65, after the company reported that its net income plunged by only 50%, which was less bad than expected, and that its revenues rose 12%. And it raised its guidance for the full year.

That’s one of the few companies of that ilk that are profitable, even if less profitable than before, and that are now having to deal with the reality of investors no longer blindly buying all the hype and hoopla, but seeing revenue growth of 12% when inflation is 8%, and they’re seeing a P/E ratio that is still 20, and they’re suddenly seeing the uncertainties that were there all along, and they’re seeing that everyone and their dog among big tech has had a competing video conferencing services for years and decades, and it’s hard to get blindly excited.

Zoom’s 4.7% gain afterhours isn’t even visible on the chart. The shares are down 79% from their intraday high on February 16, 2021, yes, that infamous February when a bunch of these stocks now enshrined in my Imploded Stocks started coming apart. But at least, it’s still above its IPO price of $36 (data via YCharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

haha good show for sure, last couple of months, I have been enjoying the firework drop out of them and Beyond meat. I am sure there are plenty of other overhype IPO from before 2019 but these two was fascinating to say the least.

I know couple of old co-workers of mine left and went to work at SNAP, quick check on Linkedin shows they are no longer there. I know some of them were counting on options going big…hopefully they got a chance to cash out before this crash

Gone in a SNAP

It definitely rhymes with the 99 dot.com implosion.

The massive drops in a short amount of time of companies that were never going to make a profit but…but…high sexy tech.

Next:

Delisting and bankruptcy

Job losses

Housing implosion in certain areas as those stock options go poof

Folks asking for their jobs in boring companies back

2banana,

Some of these tech companies might have a viable business (based off internet advertising, etc.) but not at 30+ PEs, if they are already generating billions in revenues (ad buyers are finite, there are a zillion ad suppliers now, and large revenue companies grow slower because of finite mkts/more competition, etc).

Somewhere buried in the piles of dung there may be real, viable businesses – but they are much smaller and many fewer in number than the delusional public mkts have been projecting for the last year (or 8).

Internet technologies are a real boon (much less costly propagation of info is a big plus for society) but the value focus/revenue models have lagged far behind.

(South Park had this nailed *20 years ago” with the Underpants Gnomes, just like it did in the political realm with the election battle between Douche Bag and Turd Sandwich…evidence for all time that satire may be wholly impotent to effect societal change…).

“and it’s gone…..”

love investing in markets

Wonder if Evan sold any after their Q4 “surprise” and knowing what was announce today will come soon enough. If so, that would definitely be insider trading right? Not that I would expect SEC to be that on top of it..

“In response, the stock [SNAP], which had been brutalized, knee-jerk-spiked as much as 62%! Dip buyers, if they dumped those shares right then and there, had a field day”

Hope Elon can buy Twitter, Snap, and Meta all in one package, and merge it with his solar-panel-spacelink-tunnel company.

Have you seen the inside of that tunnel? DEATH TRAP.

Thunderf00t on YouTube has so many nice debunk videos on things like Hyperloop, SpaceX and a few others. It starts to become a bit repetitive now but it is always funny :)

I recall an event in Oakland tunnel a few decades back. Trucks burnt down to the chassis.

Caldecott tunnel fire. I lived in the Bay Area when that happened

I doubt he can pull Meta into it… but there is no reason that he can’t scarf up SNAP along with Twitter.

Well, no reason other than the fact that SNAP has a market cap of $25 BILLION even now after its big plunge. Their CEO is hopeful that they will make $50 MILLION this quarter (using “adjusted EBITDA” as his profitability measurement) and even with that very generous measuring stick this stock is still priced at a P/E of 120!!!!

There are some very crazy people out there bidding these stocks up to the moon and beyond.

There is little consumer lock-in. Everybody into that novelty can just yell to pals, let’s head over to the new one. The switch to TikTok for example happened in a blink. Same goes for alt-coins. It is all dumpable at the touch of a screen. “Castles made of sand melt into the sea eventually.”

There is more lock-in than that with Social Media. The “network externalities” of social media means that people will only go to the platform that most of their friends are on.

That said, both Twitter AND Snapchat have fewer than 400 million monthly users… and NEITHER is reliably profitable.

Gone in a SNAP[

Oh snap!!!

Snap back to reality?

SNAP! goes the weasel.

Snap, crackle, and flop?

I know Snapchat is a thing, but it ain’t a thing I do. So, I checked out the website. Still don’t know what it is, so I guess it’s not something I’m supposed to do. But, it’s very yellow. I think that’s borderline angry on the color psychology scale.

It should tell me (ABOVE THE FOLD) what the heck it is, but it doesn’t. Or, maybe the yellowness blinded me into missing it. I dunno.

If you just spit it out… For example, “the stories behind business, finance and money”, I can assemble some sort of idea regarding the intended purpose.

Yeah, sounds like it’s the K-Mart of social media. Oh and they made (or make) smart glasses.

SNAP also spent over 100 million to buy Bitmoji in 2016

(“Bitmoji is your own personal emoji. Create an expressive cartoon avatar, choose from a growing library of moods and stickers…”)

I’ll check it out when I feel the need for an avatar to get some online mojo happening.

Sheep do not question where they are bid to go, to be sheered.

phleep-think you’ve hit on an issue of our age-the sheep are being ‘sheered’ (decapitated) rather than being husbanded and expanded to be repetitively, and reliably, ‘sheared’…

may we all find a better day.

I think you like take pictures and stuff and put it on the internet for likes when you are like feeling like female or teenage or something.

You mean I can be a female by using that site? I knew there was a way to make that happen! Then I can go into female bathrooms? Love it!

My roomate is a zoomer goldfish who says snapchat is for texting self destructing naked pictures of your junk. I don’t know why my goldfish is texting photos of my junk. I need to have a discussion with Jerry.

It had only one intended purpose which was to scam speculators.

I guess the problem is, who is carrying all these big losses…. If there is a big institution involved in any of the many big losers, then there may be another Lehman Brothers in the near future ????????

I’m sure Cathie Woodshed is neck deep.

Maybe Cathie Woodshed will start a new fund with a collection of all the New Big Losers and say in a few years it will Zoom to the sky and, Oh Snap, if you weren’t on board you missed the upside.

I know a few top 0.1%ers heavily into ARK, none cashed out.

“It happens” and “cash is trash” (very Ray Dalio) were the comments about it. Lol

Retail investors are probably a good percentage of those getting destroyed right now

I think it was JPM / Chase that had some data that basically said retail investors have taken a full round trip up/down and lost all of their gains in the past couple of years

I am almost afraid to ask… what exactly is “adjusted EBITDA”???

I thought the I, T, D, and A are more than enough adjustments to earnings.

I don’t think most of the “to the moon” crowd read footnotes. They are too busy aspiring to be “influencers” for that Lambo mambo.

A non-GAAP number but in this case, management defines it as they please so that everyone can pretend performance is what they claim.

And…the irony is that GAAP “(e)arnings” themselves are fairly easily manipulated (at least in the near to medium term) under the “rules” of GAAP.

So if these companies can’t even show good results under GAAP…watch out.

It’s basically accounting fraud but in an easily digestible form for the vast masses who failed accounting class in community college.

It’s a measure of what cash flow would be in theory without all the big and bad stuff the company had to pay for. Anytime I see “adjusted EBITDA” it’s, like, ok, whatever. That’s why I always put it in quotation marks. Companies that tout “adjusted EBITDA” are uninvestible.

Glad, very glad to see you understanding what certainly ”appeared” to be the same kind of ”reporting or not” back in the mid 1980s Wolf…

As I have commented, on your wonderful site at least a couple of times if not many more…

I got OUT of the SMs in the mid ’80s because it seemed SO clear then, and since, that it was just another

”rigged” market then,,,

And, to be clear as I can do these days, I had been making some good money in SM before that.

GOOD Luck and GOD Bless each and every one choosing to ”gamble” in every market in 2022…

Shoot, I know investors who won’t buy into a company based on EBITDA… why shouldn’t expenses like taxes be counted against a company?

I get that EBITDA allows analysts to back out the company specific financial variables and compare companies based on their operations alone. So there is some utility to that. But “adjusted EBITDA” doesn’t allow anyone to compare anything.

Sounds a lot like the “Pro Forma” accounting used the Dot.com era.

Or, more precisely:

“Here’s our EBITDA if we, for a moment, ignore this sequence of events that profoundly and adversely impacted our company”

If it were me doing an “adjustment,” I’d discount onetime items or outliers like (maybe) a balloon interest payment that Doug in accounting forgot to include on a spreadsheet, because he’s bad at his job.

Snapchat is just like MSN messenger from 20+ years ago, but on a phone.

Or WhatsApp. Or telegram maybe. Or signal. Or Facebook messenger.

Zoom was just like MSN messenger from 20+ years ago with your webcam plugged in, but on a phone.

Just like teams, WhatsApp, native phone, etc etc.

PE ratios over 10:1 for all this kinda saturated market, fickle user base market, revenue just from advertising market, is lunacy.

But this just shows why valuations are never based in reality or anything, just in the mood of the day based on the hype of the day.

I watch five value stocks that I feel like I understand and can put a price on based on cash flows or dividends. Two of them have tripped my buy price. They aren’t cheap, but offer a reasonable long term return.

My favorite is a no growth, no debt small cap and it recently tripped my threshold of 3% over 10 year treasury or in this case a 6% dividend.

My second favorite is a REIT that tripped my threshold of 10 X cash flow and has a 5% dividend.

I expect stocks to go lower and am at only about 9% stock exposure up from 2%, but you have to determine relative value of things and try to make a reasonable risk reward for your situation.

I never liked high growth stocks, because it is beyond my ability to determine the growth rate and once growth rate disappoints there is an air pocket below.

and the stocks are? tickers?

The five stocks I watch daily are DUK, SKT, PETS, BRK-B, GOLD. My rationale is that you are better off trying to know as much as you can about a limited number of stocks to have any hope of an advantage.

All but BRK-B are in a specific limited business I can understand.

Intel (INTC) trades at less than 7x earnings and 4x cash flow and the dividend yield is roughly 3.5%. It has a solid balance sheet as well.

Hard to imagine it can get much cheaper than this. I don’t think that the stock is a “value trap”.

Intel is losing a big customer, namely Apple, which is now designing its own chips. And it might lose more. It might have to cut its huge margin to compete.

Yes, those are valid points, Wolf.

IMHO, mostly already “priced in”, as the stock is down almost 30% YTD and 40% in the last 14 months. Of course it could get even cheaper, but this is not a bad point to begin building a position.

There was no logical explanation of the crazy up move. You try to apply logic on the way down, when the pain is barely beginning. Don’t you think overshoot on the way down is much more probable?

I read recently that Intel is investing heavily in new production facilities that will hurt the bottom line in the near term. But, long term, I think they will do OK with or without Apple.

At least they’re burning through billions for a productive reason.

Intel is priced below the dot.com peak and was at the recent NADAQ high. Over 20 years with a cumulative negligible return and this is with a mania.

When the major bear market really gets underway, it’s going to be even worse.

It’s a solid company but so is CSCO which has performed equally poorly.

Bam_Mam,

Do your own analysis, very easy. Lower earnings, then multiply by 7x to get a new target price. See how it looks then.

On the balance sheet, they have announce new “investments” overseas and in the US. Translation: higher debt to capital ratio whether it be by getting into debt or burning cash.

On the “hard to imagine” statement…see Enron/LTCM/WolrdCom/AIG/Bernie Madoff/…should I keep going??

Also, if you are looking for different perspective onn the “hard to imagine it can get much cheaper than this”, lookup the Peter Lynch clip on YouTube about “It Can’t go Any Lower” This is from a very successful fund manager.

Since the 90s at least valuations have been strictly based on monetary policy and government spending. In other words, the stock market was subsidized. Wall Street owns the government, which is technically Fascism.

PE over 5 are lunacy for any stock!!!!!

WhatsApp is great actually for those of us with a broad international social network

These charts are so nice! Classic bubbles.

Not sure about the business models of all these companies, but many “tech” companies are simply advertisement sellers. I guess that will suffer a lot during a downturn when corners need to be cut. Even worse: a lot of the advertising is advertisements for other bubble companies, so part of the revenue collapse is self-enforcing.

Another thing that people often overlook: companies that rely on advertisement income (Meta, Alphabet, Twitter etc) are all fishing in the same pool. There is only so much you can spend on advertising and that pool may shrink when people are struggling to even pay for rent, fuel/ energy and food.

That was always David Stockman’s argument. The size of the advertising pie is not that big of a number, so how can you have these incredible market caps all based on eating up the limited pie. Maybe they can figure out how to eat other industries like the financial sector.

Like 1929, all these self-referential structures grow up around cheap debt (underpriced risk). Tiered debt, mutual ad revenues, and then add in some 2000 era games like round trip wash contracts where everybody is buying in a circle. This creates an incredibly weak lattice that can collapse in unexpected ways and places, in far-reaching ways. (That recalls 2008 too, when sudden eruptions appeared in firms thought to have no direct connection to the losses.) And of course, employment numbers and general spending floated on all that.

Phleep-

“Weak lattice” is nice imagery.

Like when the green code in that scene in The Matrix resolves to rain falling off your TV screen.

Also reminds me of Machior Palyi’s concept of the “shiftability” of short-term debt-reliant parts of the lattice. Lose shiftability, the ability to pass debt on when your business demands liquidity, and troubles multiply. The lattice work crumbles in painful and unexpected ways.

Then the question of macro-prudential response determines whether the pain is sharp/violent/cleansing, or protracted/deferred/self-reinforcing. Yuck.

Guaranteed to shrink. There is definitely a massive advertising bubble now.

Another primary beneficiary for decades has been professional sports franchise values, mainly through hyper-inflated media rights contracts.

It seems “impossible”, but these nose bleed valuations are destined to decline a lot.

Facebook has reported more users in some markets than actually exist. This was briefly in the news and then unmentioned and disinformationed.

Foe a real hoot look up what the CEO of Restoration Hardware said about Adwords.

or just read this:

wolfstreet.com/2017/09/11/most-online-ad-spending-wasted-ceo-restoration-hardware/

When I use google to navigate by typing “Home Depot” or “united airlines” I always click on the second NON Ad link. My little contribution …

Same here. Any link with an “AD:” in front of it gets bypassed by me.

We were buying a google adwords campaign targeting competitive products for about $1500-2000 per month. Eventually I just got tired of it. Our competitors started outbidding us on the same words, and in the end the only party benefitting from the spending was google. Clicks were mostly traffic that was coming our way anyway, and then a bunch of bounces after people realized we were a manufacturer and not a reseller. Very little, or no ROI in it. I’d love to see some widespread pushback on online ad spending. The process of setting up the google campaign just felt like a ripoff from beginning to end.

When’s the last time you clicked on a link off of facebook or youtube and bought something. Everytime I see these ads it makes me think of Billy Mays or Vince the shamwow guy.

I don’t use facebook and I watch all YouTube videos using a browser with adblocker, so I never see ads there either.

YouTube is a selling machine, not from the ads, but from content providers directly pushing products to the sheep/audience

Read this morning by an “analyst” over at Martketwatch that he can’t imagine the S&P500 falling below 3,000. Sounds like a Real Estate analyst. We’ve got a long way to go, dude! Go read up on your inflation history, bro!

Inflation started to spike in 1973 and wasn’t tamed until 10 years later. The convergence of anti-fossil fuel sentiment along with the push to renewable, labor issues like unionization, commodities, climate change, military threats, etc are all going to conspire to keep inflation high for WAY longer than “analyst” think is possible.

The Fed is SO FAR BEHIND THE CURVE it’s unbelievable. And the current political climate is not doing inflation taming any favors.

What’s going to drive high inflation for 10 years?

We had this same inflation/stagflation nonsense in 2007/2008 and then suddenly oil was cheap again and everyone wanted a job.

If it happens:

Changing sentiment; the “money printing” was always there.

Ending the asset mania will remove artificial demand but deglobalization matters too.

It’s also possible to have high unemployment and rising/high inflation.

Since “growth” after 2008 has been mostly or entirely fake, in the upcoming major bear market, I expect a lot of people to re-enter the labor force, whether they prefer it or not. Their age and circumstances will be irrelevant.

Someone I know just met this guy who purportedly makes a living by renting spare rooms in his house, with a dog sitting/walking business, and crypto. If this is true, in other words, he doesn’t have a real job, career, or a profession. Late 20’s to early 30’s.

I suspect there are a lot of these people in this bubble economy, maybe making good money too, for now.

To list them again in more detail:

Anti-fossil fuel, pro climate change policies that keep oil & natural gas prices higher than on average.

The huge push to renewables that increases cost of electricity higher than on average due to prematurely shutting down coal & nuclear power plants.

Over regulation, for example recycling old car batteries which is a good thing but will keep the costs from dropping as much.

Higher commodity prices that push up the cost of most products, especially those that support the switch over from fossil fuels to renewables like solar & wind.

Labor issues such as unionization &

Increased competition for rental housing due to current immigration policies.

The current Ukrainian crisis or something even bigger like Taiwan.

And these are just the obvious things.

The two things that will materially affect inflation are:

Who controls the WH & Congress.

When & how deep the next recession is.

In case you didn’t notice, the great recession occurred from 2008 – 2009, thus creating cheaper oil.

All that has yet to happen though.

When no one has any money because of inflation, and there is a recession, because no one buys anything except housing, food and energy, and there is a deep recession, and no pay rises because people are losing jobs, because recession, then everything will get cheaper, by definition demand will be heavily subdued.

Unless, we get pay rises, and then inflation isn’t bad because even 1000% inflation isn’t bad at all.

Moving a decimal place one place to the right for every monetary value, no problem.

Debts are dissolved to nothing. Great.

All the money pumped into the markets since 2008 is burning away as we speak.

All that misallocated and wasted capital that didn’t build viable businesses or buy quality durable goods, is now evaporating.

Now everyone is valuing their stocks and bonds and other assets at lower prices, all the people who will sell at a loss or bought at a higher price have lost value.

Deglobalisation will increase costs yes, but likely people will buy a single item of 10x better quality for 10x more money made domestically, rather than cheap rubbish from China. And they’ll buy 10x less stuff.

The net effect is no inflation, but a hell of a lot less jobs available.

I just can’t subscribe to the idea our economy can keep going with huge inflation but no pay rises.

It’ll fall into recession and deflation.

Unless there are pay rises, in which case fine.

Or UBI/bailouts/whatever, and a new cycle of easy money begins.

Stagflation has happened before but this seems to me more like the prelude to deflation.

Anyone else thinking how the heck they’ll keep buying stuff at high prices, to “suffer” from inflation?

No more credit card, no house price rises to borrow against.

No salary rises.

Everyone is just going to stop consuming and cause a global deflationary shock *if* energy/food/housing keep going up so hot.

Kenny Logouts said: “Unless, we get pay rises, and then inflation isn’t bad because even 1000% inflation isn’t bad at all.”

—————————————-

inflation rewards debtors and punishes savers.

seems bad to me ………………….

The same thing that has driven it for decades. The dollar creation that makes existing dollars worth less.

If price to sales returns to 2009 low of 0.8 then we will be at 1250 on SP500. Might not happen, but you got to know that could happen. Real economy improved that much since GFC?

Good comments.

Cathie Woodshed is one of my favorite names.Thank you DC.

As a guy who uses Textra on my MotoG phone I’ll never be part of the target audience of these “amazing tech companies”.

There’s really dark days ahead for the stonk holders of these fine companies. Must be some interesting conversation going on at churn shops like Fisher Investments 🤑🤡🤑🤡

SNAP is another company that should be worth exactly zero. A perpetual cash burning machine incinerating its “investor” funding.

Like all these companies when I check, the loss is always due to “Selling, General, and Administrative” expenses which = future layoffs, in mass.

As a company it is worth far less than zero if liquidated, but fortunately the nature of equities (stocks) limits the exposure of speculators to only zero!

The founders and bankers of $SNAP have successfully blown through over $8.6 billion of real cash equity over the past 10 years. Yet, they still report almost no real earnings. They also have floated over $2 billion in debt. Good luck to those debt holders in times of the Fed pulling back the punch bowl.

Spent the weekend shopping in the Austin, TX area, Silicon Valley 2.0 for those that don’t know. I have never seen so much money being spent anywhere and I lived in NYC through the Wall Street boom of the 1980’s. Even the Whole Paycheck had a time limit on how long you could park there.

Tech Crash? Crypto Crash? Layoffs? Not obvious there at all.

Austin is Portland with Freedom Fries.

Same thing here in San Francisco. People talking up a “recession” are going to have to be patient.

Its come to Phoenix… restaurants are not that packed, you can walk in shopping centers without jostling each other. Be patient, valve might be turned off but there still some water left in the pipes.

I don’t find that surprising. The spending bubble is driven by housing prices and jobs availability. There has been no evidence of housing price declines or significant layoffs yet.

There have been some recent moderate stock price drops, but that impacts only the 10% of the population who own 90% of the stocks.

I think housing price growth has probably stalled at this point, but there is no strong evidence of price declines.

Same going on at the North side of Houston. Malls packed, restaurants full on Sunday and Monday nights, which they were never on those nights, etc, etc. Maybe it’s oil money along with some high tech successes.

We should expect some lag time between tech stock losses and dampened economic activity driven by tech workers. A lot of these cash burning companies are not going to be able to stay in business, and the few that are actually borderline-profitable are going to have to cut perks, wages, and even jobs to survive. Most of these companies exist purely by burning investor cash and rolling cheap debt over into more cheap debt. As investors (gamblers) dry up and debt begins to incur real carrying costs while we move away from ZIRP and into QT, the picture is going to change profoundly. Many work-from-home tech and quasi-tech leeches are going to be losing their jobs soon… We’re already seeing the very tip of this iceberg with companies like Zillow , Carvana, and Peloton. Not to mention clear weakness in mortgage industry employers. Even heavy hitters like Wells Fargo are looking at cuts, and FB has apparently frozen hiring across several of its products.

At the end of the day, the most effective way to cool inflation is to choke wage growth and chill our overheated labor market. As long as people are bringing in piles of cash without really producing anything, inflation will persist. The folks at the Fed probably understand this. Their messaging and their actions have changed accordingly. Tech workers will drop their extravagant shopping habits pretty quickly once they’ve lost their jobs.

The start of a recession is always – by definition! – a time when everything is going really well, and has been for a while.

But then instead of things getting better, they start rolling over and getting just a little bit worse. The process starts in some places before others. It’s barely noticeable to most people.

Toss inflation into the mix and it’s even harder to spot the turn.

as long as the credit cards work everything is fine. I wonder and worry about a true credit contraction and not just rising rates.

There is a big difference between just rising rates and tightening credit conditions. Rising rates are an outcome but not remotely the same thing.

FFR at 0% (or near it) doesn’t automatically mean widespread credit availability. It doesn’t matter how low rates are if no one will lend to you when you really need it. Rates might as well be infinite.

That’s what is already starting now, though it’s not widely evident. In this initial phase of the bond bear market, probably only the worst consumer credits will be cut-off which isn’t enough to make much difference to aggregate economic data.

But tightening credit is already evident in junk bond rates and crashing stock prices for these companies. Both are symptoms of tightening credit which in turn is a function of changing sentiment, otherwise known as bearish psychology.

This is the real change, as the companies were always ridiculously overpriced bags of hot air and the “business plans” weren’t ever worth funding either.

1) It’s Malthus vs wall street and Meta. Real Earth resources vs silicon valley and wall street bankers.

2) There isn’t enough food to feed eight billion people on this planet.

3) Thanks to Fritz Haber the global population increased enormously in the last 100 years, but that’s is not good enough.

4) Don’t blame the Fed for not producing oil and wheat.

5) Socialism isn’t a substitute for limited resources.

6) Most people earn barely enough to pay for rent and food. They have little left for the rest of the month.

7) The more we live on the poverty line, the richer are wall street bankers. But without their profit there will be starvation.

8) In the late 1880’s 300 people owned 2/3 of the land in Scotland. Today

Pareto top own the most in US.

9) Ukraine is a warning shot : Malthus is back.

10 ) Petunia welcome back.

Some good points, Michael Engel

Re: 1, 2, 4, 7, 9

Can’t remember who said it:

When food ceases to cross borders, military boots do. (Or something like that.)

But but, elon said we could double the population and it will just merrily keep on spinning.

Don’t worry too much about Elon. The Matrix he has planned is probably survivable.

There are certain levels of survival people are prepared to accept.

Michael Engle said: “7) The more we live on the poverty line, the richer are wall street bankers. But without their profit there will be starvation.”

———————————————

Support for the second sentence?

Snap just another techno-psycho-corporate garbage synonym, and all the fake jobs that come with it. These were forced into the market by the bucketful in the lead up to ‘emergency’. Technological, social cancer for the ‘grand-baby’ masses is shady investments exemplified to the fullest. Socialized destruction of your time, electricity energy in a ‘green’ society and social health for the benefit of monetary destruction in plain sight. Value extracting parasites (mostly institutions and pensions) captured by the techno hive while the gov dumps D2 sized buckets of money in the burn barrel on their behalf. Business desperation exemplified throughout the markets. All sold and based on internet account numbers who could be anyone or anything, fraud of pure nonsense in broad daylight all throughout the ‘markets’.

Snap has snapped.

Here is a thought. See if Snap can re-direct it’s incredible brain power skills to supplying butt wipe to Americans at a dependable and low cost basis and innovate with a guaranteed no finger blow-out product en-hancement. We got Big Oil, Big Banks and Big Trucks. It’s time for Big Butt Wipe to bust a move. We need it,and we deserve it.

Those not associated with the Field of Educay-shun will miss the deep irony…

Software packages:

SNAP-B

SNAP-SpLD

are selling on Amazon among other places.

They are used to assess and diagnose deviant investing behavior and obsessive-compulsive crypto & meme stock buying.

“They are used to assess and diagnose deviant investing behavior and obsessive-compulsive crypto & meme stock buying.”

All very useful information if one is in the business of promoting self-imploding vaporcorps for Fun and Profit. One imagines the investment banks subscribe to the premium versions, although it’s more likely they hire boutique staff for that.

How Wall Street banks made a killing on SPAC craze

SNAP-B & SNAP-SpLD software interface used to assess learning disabilities is eerily similar to Coindesk20 charts, logos and avatars. You may look it up at Google Images. Ultra-simple moronic charts like in USA Today (always copyrighted !), cartoonish houses and farm animals…

Meet YearnFinance token.Last year reached ATH of $78K. Last week plummeted to $10K and fell off the turnip truck…

“Do you yearn, Kramer ?” – phrase from Seinfeld’ episode.

I shudder to think that the whole f… world watches this Investing by the Persons of Special Needs (i.e. retards) and recoils in horror.

Brent-suggest a C.M Kornbluth SF short story from the ’50’s entitled: ‘The Marching Morons’.

The horror has always been with us, only now is on mass-communications/media/entertainment steroids. (Never underestimate the power of the statement: ‘…as seen on TV!…’).

may we all find a better day.

Looks like Mr Kornbluth wrote Cliffs notes for Madison Grant & Lothrop Stoddard prescient works, without me being aware of this fact 😀

Thanks for the suggestion

1) Yesterday JPM failed to breach big white May 4 high. Today high breached yesterday high and May 4 high. At 11: 50 AM JPM is an upthrust above May 4 high, with a long selling tail, under Apr 14 low. Apr 14 low is a stopping action. May 2 is a selling climax/ May 4 high was the auto response.

2) Yesterday was a setup bar, today, a trigger.

3) Yesterday JPM Snapped above two years Anti backbone (BB) : Feb 28 lo/ Mar 3 hi 2020. JPM weekly is hovering > ma200 for support.

4) Yesterday QQQ failed to close > Fri high. Today QQQ gap lower into

May 20 fractal zone. May 2 is a stopping action. May 12/17 : a selling climax/ auto response.

5) Same for SPX. SPX is up and down around May 11 close and May 12 close, a dividing zone.

6) For entertainment only.

When the tide goes out, not only does one get to see who’s been swimming naked, but one also gets to see who is standing hip-deep in toxic sludge.

The Fed has trillions of that on their books, the product of unregulated crony capitalism. They’re very good at externalized the mass production of financial waste, and more is better.

The good news is that they’re running out of raw material.

The bad news is that they’re running out of raw material.

They’re laying waste to the planet, and have weaseled most the population into helping them. The rest are merely coerced.

Why, when the situation is so clear and alarming, does it remain so stubbornly intractable to change? It is because those who have power in the world want it to be this way.

All the crazy evaluations, buyouts and buyback happening in the market are the ‘Arizona, ocean, crossing bridge’ sold to the public so we could get to our inflation destination.

Snap -2.4 billion in debt booked in the last 4 years. Multi Billion dollar value for the market glorified picture display. Its worth -2.4 billion plus all the connected waste in the real world.

Yet connected agencies lap it up like a dog in the desert facing heat exhaustion. The mirage is charted, look at all the 2 year ‘dorsal fin’ shaped evaluations, created from a shutdown. And now they are sure to rotate it directly into your basic needs, direct theft in clown world.

Wolf,

Your list of “kathoomphed” stock is fun and most, if not all, are on the escalator to worthless.

But underlying every concept/fad stock (Carvana?), there are long established, profitable, and serious technology businesses getting crushed as well. A sampling:

TICKER 52 WK HI TODAY LOSS %

SQ 289 75 214 74%

SNOW 707 418 289 41%

EBAY 81 44 37 46%

PYPL 310 78 232 75%

ADBE 699 395 304 43%

ADSK 344 177 167 49%

Large cap, serious tech companies down 40 – 75% – most of that in the last 6 months. It’s uglier than we think.

SQ, and Paypal aren’t technology companies, but payments. Ebay isn’t a “tech” company either, but a fading marketplace and auction site. Three of hundreds (at minimum) marketed as “tech” which is just more BS.

Second, though profitable established companies, Paypal and Adobe were stupidly overpriced at peak prices and still overpriced now. At peak, market cap was about $300B and $400B which is totally nuts.

The results in your post are an example of fantasy colliding with reality.

Some of your line items were featured in my Imploded Stocks column. In addition, not on your list, were others such as Netflix. My fingers are getting itchy to put Tesla on it. Gotta wait till -70%. Now at -50%. So some ways to go.