But inflation is eating everyone’s lunch.

By Wolf Richter for WOLF STREET.

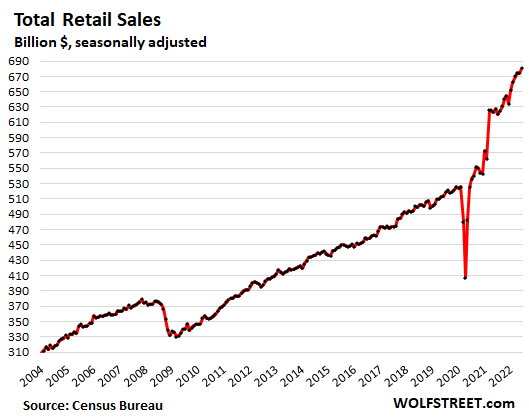

Retail sales in June jumped by 1.0% from May, and by 8.4% from a year ago, and by 32.5% from June 2019, to $681 billion, seasonally adjusted, the Census Bureau reported today.

Retail sales are sales of goods. Sales of services, such as insurance, healthcare, airline tickets, etc., are not included in retail sales. Ticket sales at the multiplex in the mall are not included in retail sales, but are services, and consumers have been shifting some spending back to services. And yet, consumers still splurged on goods. These folks are tough, when it comes to shopping. Nothing appears to be able to knock them down – not even the raging inflation.

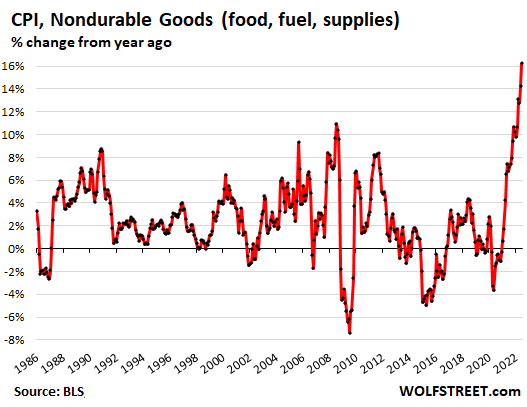

Inflation rages in services, food, gasoline; recedes in durable goods.

Inflation is ricocheting around the economy. Where prices are now spiking are in services – but they’re not included in retail sales.

And prices are spiking in nondurable goods, dominated by food, gasoline, and supplies. These nondurable goods are sold at various categories of retailers, such as grocery stores, gas stations, general merchandise stores that sell food, supplies, and gasoline, at some “miscellaneous stores,” such as cannabis stores. But wait… cannabis products are not in the CPI basket.

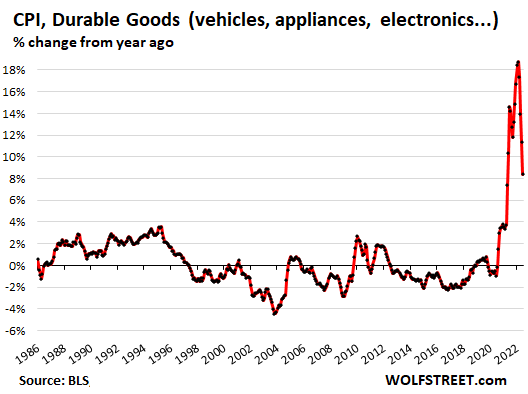

But in durable goods, crazy-raging inflation of nearly 19% early this year has been abating and in June down to 8.4%. Retailers in that categories are stores that sell motor vehicles, auto parts, appliances, tools, electronics, furniture, etc.

Sales by category of retailer, not adjusted for inflation.

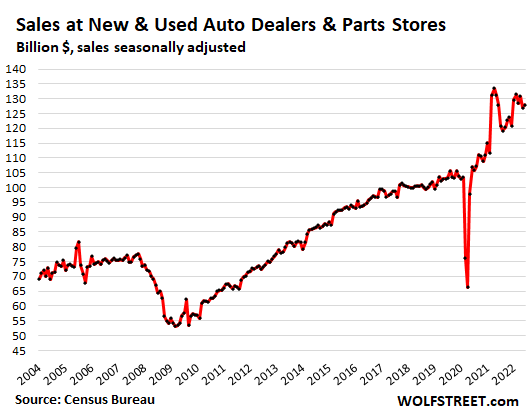

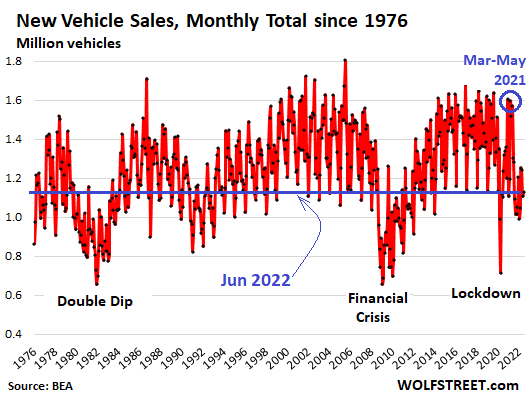

Sales at New and Used Vehicle and Parts Dealers, the largest category of retail sales, rose by 0.8% in June from May, to $128 billion, seasonally adjusted, and were unchanged from a year ago, but up 24% from June 2019, amid huge price increases in 2021 that are now flattening out. There was plenty of supply in used vehicles. But many new vehicle dealers were still woefully short on inventory, and consumers who want to purchase a vehicle are having to order it and wait for months.

But unit sales are way down from a year ago for both new and used vehicles. The number of new vehicles delivered to end users in June plunged by 13.5% from the beaten-down June 2021, to 1.13 million vehicles, and by 25% from June 2019.

The number of used vehicles delivered to retail customers in June fell by 13% year-over-year, according to Cox Automotive, as consumers are starting to rebel against the ridiculous price spike last year, and those price spikes have hit buyers’ resistance.

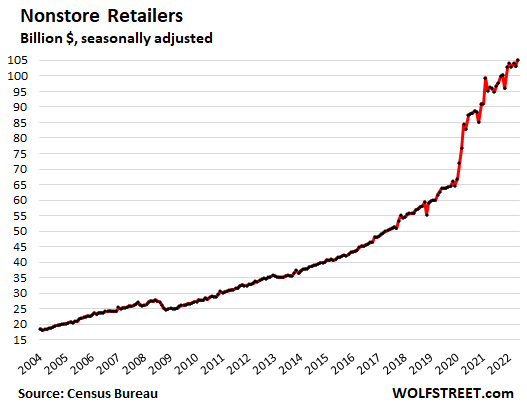

Sales at ecommerce and other “nonstore retailers,” the second largest category of retail sales, jumped by 2.2% in June from May, to a record $105 billion, and were up 9.6% year-over-year and up by 68% from June 2019. This includes the ecommerce operations of brick-and-mortar retailers, along with sales at stalls and markets. The ecommerce boom continues:

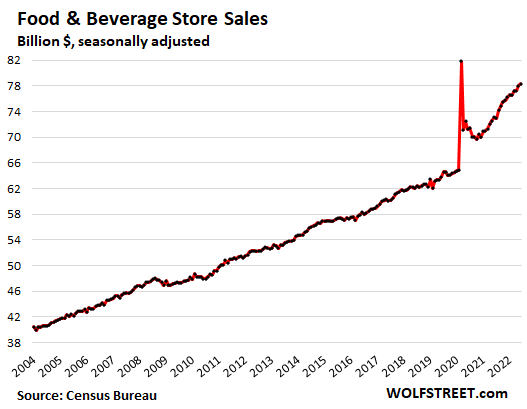

Food and Beverage Stores: Sales rose by 0.4% for the month, and by 7.1% year-over-year, to $78 billion. Compared to June 2019, sales were up by 23%:

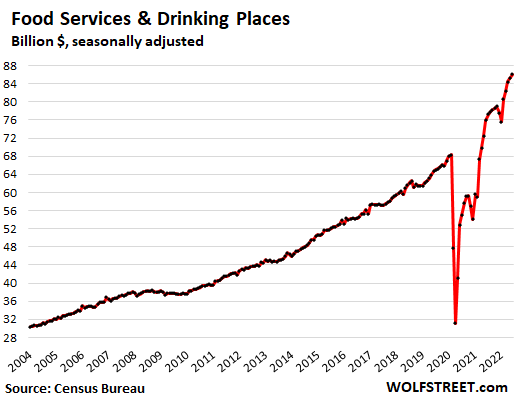

Food services and drinking places: Sales at bars, restaurants, cafes, cafeterias, etc. jumped by 1.0% for the month, and by 13.4% year-over-year, to a record $86 billion. They’re in a boom, with sales up 33% from June 2019. Note that the year-over-year sales increase of 13.4% far outran the CPI for “food away from home” (7.7%). Americans are going out with a vengeance and are flocking to restaurants.

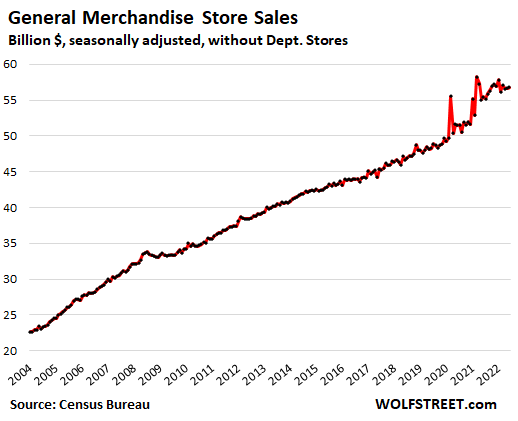

General merchandise stores: Sales ticked up 0.3% for the month, and by 2.4% from the stimulus-miracle last year, to $57 billion. Walmart and Costco are in this category, but not department stores. Compared to June 2019, sales are up by 18%:

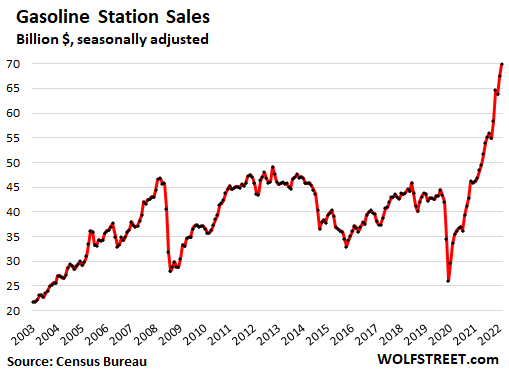

Gas stations: Sales jumped by 3.6% for the month, and by 49% year-over-year, to $70 billion, on spiking gasoline prices, even while actual consumption, measured in volume, has dropped, as consumers are responding with changes in their driving patterns to cut fuel consumption and put a lid on their gasoline expenditures.

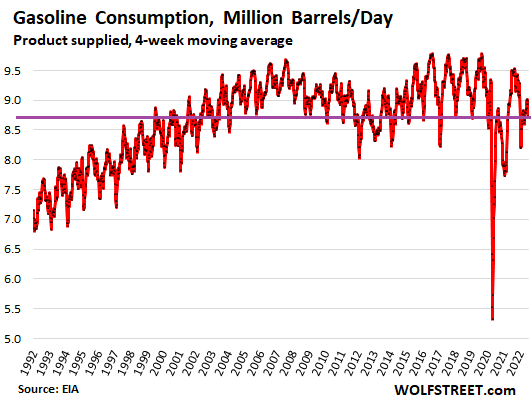

Actual gasoline consumption, in barrels per day, hadn’t gone anywhere since 2007. And now the price spikes have triggered a buyers’ strike. In the week through July 8, gasoline consumption plunged to 8.73 million barrels per day (four-week moving average), according to EIA data, a level first seen in July 1999

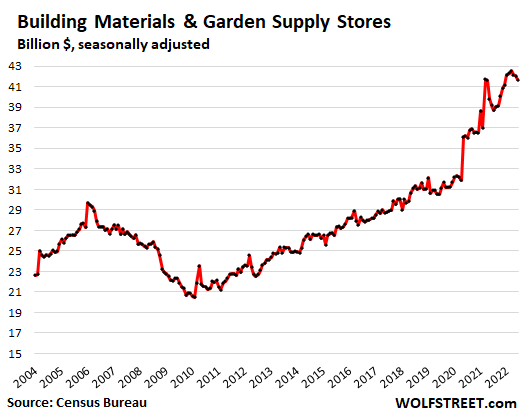

Building materials, garden supply and equipment stores: Sales fell by 0.9% for the month to $42 billion, but were still up by 6.4% from the stimulus miracle last year:

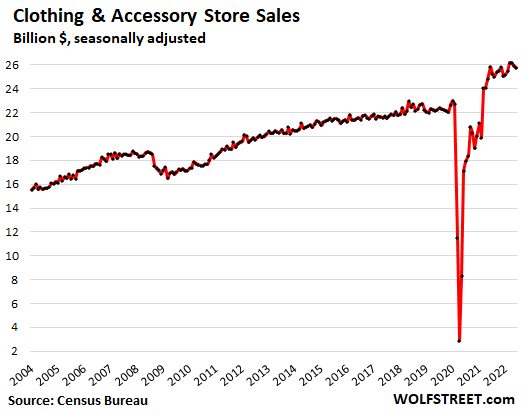

Clothing and accessory stores: Sales dipped 0.4% for the month and were flat year-over-year. At $26 billion, they were still up by 16% from June 2019:

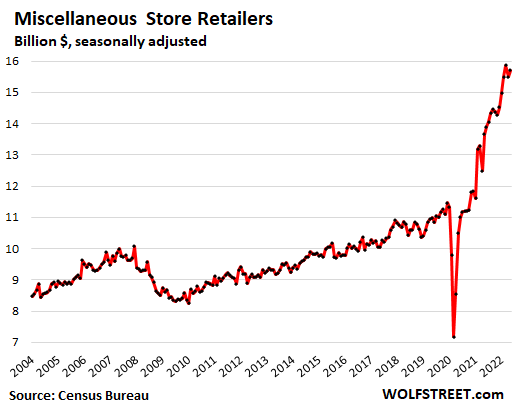

Miscellaneous store retailers (includes cannabis stores): Sales jumped by 1.4% for the month, and by 15.1% year-over-year, to $15.7 billion. Compared to June 2019, sales were up 43%! This category tracks specialty stores, such as arts supplies stores, brewing supplies stores, and cannabis stores – now the hottest category in brick-and-mortar retail:

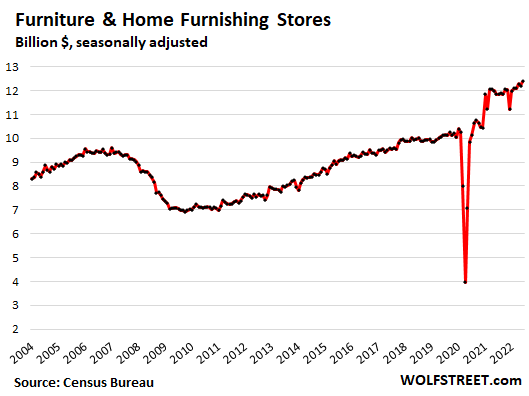

Furniture and home furnishing stores: Sales rose 1.4% for the month, and by 4.6% year-over-year, to $12 billion, and were up 22% from June 2019:

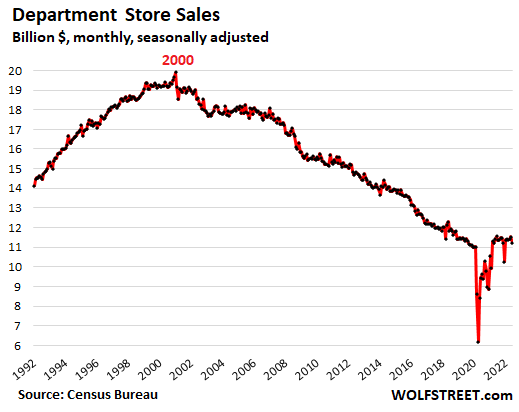

Department stores: sales fell 2.6% for the month, and by 2.9% year-over-year, to $11 billion. Compared to the peak in the year 2000, sales were down 44%, after numerous department store chains were liquidated in bankruptcy courts, and thousands of stores closed, and the surviving department store chains are still closing stores.

This chart, which goes back to 1992, shows the slow and methodical demise of what once was the quintessential way of shopping for Americans:

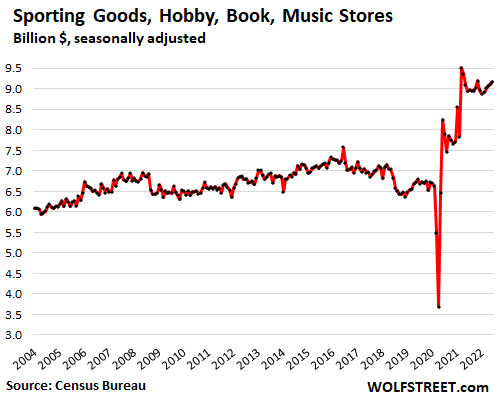

Sporting goods, hobby, book and music stores: Sales rose 0.8% for the month, and 2.7% year-over-year, to $9.2 billion, up 35% from June 2019:

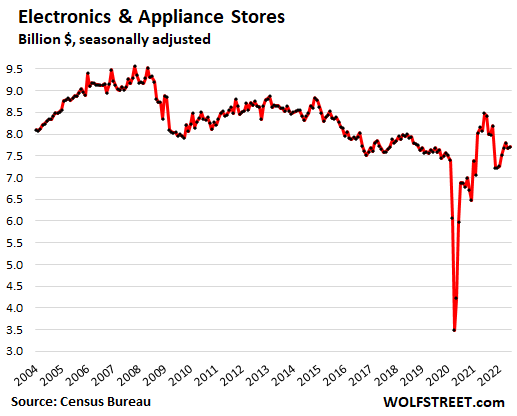

Electronics and appliance stores: Sales ticked up 0.4% for the month, but were down 9.1% from the stimulus miracle a year ago. At $7.7 billion, sales were up just a tad from June 2019.

This segment covers only specialty electronics and appliance stores, such as Best Buy or Apple stores, not any of the other stores, such has Walmart, and ecommerce sites, where the vast majority of these goods are sold.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I still don’t understand where all this money is coming from. Wages aren’t up enough to account for a 35% increase from 3 years ago.

Lots of Americans HAVE lots of money. Lots of Americans EARN lots of money. Lots of Americans MADE a HUGE amount in stocks, cryptos, real estate, etc. — they made trillions of dollars, though they gave up some of it recently. And lots of Americans have little and make little. Those that can buy stuff, buy lots of stuff. That’s the American way.

If that’s true, and these numbers are being driven by asset gains among the top 20% or so, there is no way to get inflation under control without causing a massive drop in asset prices.

Anyone who thinks the Fed can do the former without also doing the latter is deluding himself.

These are sales figure in Dollars. Can we get real sales figures in units?

SS,

Yes, on the big ticket items. RTGDFA

But dollars are a “unit of account,” which is one of the three functions of a currency, and a huge convenience so you don’t have to count units and say that online retailer sold “16.578 trillion units” last month, ranging from USB connectors for $1.99 to Samsung Side-by-Side Refrigerators for $2,099. Counting diverse units for retail sales is idiotic. It makes sense on big ticket items of motor vehicles. But not across the board. That’s just stupid.

I’d call the 81st to 90th percentiles in the wealth distribution part of the “mass affluent”. Much of their wealth is tied up in home equity or retirement accounts where it’s not readily accessible or expensive to access due to tax law.

The number and proportion with a lot of readily available spending cash isn’t that substantial from this group, relative to their net worth.

A high proportion of this group also live in high cost locations and can’t or aren’t in a position to save a lot of money.

Also depends upon which top 20%, income or wealth, as not everyone is in both.

Also depends upon household size. Two wage earners with a household income in the top 20% with dependents have a lot less discretionary income than a single person with none.

Cmon guys, this isn’t so hard. The top 10-20% have a lot of money. They buy what ever they want, when ever they want it.

The middle 80% have credit cards, student loans and all other kinds of debt. They spend a lot on restaurants/bars, movies and gas because it’s cheap ish entertainment. They may have to cut back but they still spend on those services for as long as they can maintain a “fun” lifestyle.

The bottom 20% or more live a free life of welfare, subsidized housing, etc… They still spend on restaurants/bars because they don’t need much for housing.

Sorry, I thought this Retail Sales figure is not adjusted for inflation? Meaning that people just spent more, not that they bought more things. And if adjusted for inflation, isn’t Retail Sales actually lower?

Kyrtsyn Podgajski,

No.

RTGDFA and not just the headline before commenting.

It’s conceptually wrong to apply the overall CPI inflation rate (9.1%) to overall retail sales, and people who do that don’t know what they’re talking about.

CPI inflation covers all categories or goods and services that consumers spend money on, including housing (spiking inflation), insurance (spiking inflation), healthcare (spiking inflation), etc.

Retail sales covers retailers (businesses!), not products, and consumers spend only about 25% of their total spend at retailers. They spend the rest on services and at institutions that are not retailers.

I discussed the inflation factors IN THE ARTICLE. I also have unit sales v. dollar sales for auto dealers and gas stations. RTGDFA

For example, electronics retailers here sell consumer electronics. But consumer electronics had negative CPI, meaning prices fell. So you want to apply the overall CPI to electronics dealers? See what I’m saying.

You cannot apply the overall CPI to sales at retailers.

Well, depending on how you look at it, the concept of CPI itself might be wrong;)

Wrong use of CPI is then just a follow on error.

Yup and high paying jobs are still plentiful. And based upon the Fed’s comments today they are gonna let it run hot. I’m expecting another big run up.

Wolf, my real estate agent was saying that market will heat up aging in 3 months simply because inflation will keep increasing and house price will inflate more than everything else like last year.

What do you feel?

Fire that real estate agent if you want to use them to BUY a property. But if you hired them to SELL your property, they’re doing a good job by spreading RE hype. But then, they might be unrealistic about the price, and you might not be able to sell your property, and then you will have to fire them anyway. So, I guess, just get it over with and fire them right now.

@SS: I called a real estate agent asking him: I have a house and I want to sell, is it a good time to sell ? He said yes because home prices are still hot and it can’t go up but down only, so best time to sell now.

My friend called the same agent asking him if it is a good time to buy: The agent said, interest rates are still quite low historically and home prices won’t go down, may remain stagnant or go up, rates may go up and if it goes down, one can always refi. So best time to buy :-)

Haha replying to Jon’s comments since I can’t reply directly. I never knew RE agents are so good at playing both sides. I think we need more of them switch over to working for the CIA or become double agent.

Arya Stark,

The Fed said no such thing. They said they will raise by 75 basis points at the end of July. And they said they’re going to raise more afterwards.

And the S&P 500 rose today, finally, after having dropped five days in a row. What else is new?

The 1% rise in June retail sales is in synch with the 1.3% seasonally adjusted month to month rise in the June CPI. That seems like 15% inflation after annualization. They are spending more to get nearly the same amount of goods, not increasing consumption of goods.

From the 7/13 BLS CPI report:

“The Consumer Price Index for All Urban Consumers (CPI-U) increased 1.3 percent in June on a seasonally adjusted basis after rising 1.0 percent in May, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 9.1 percent before seasonal adjustment.”

David Hall,

People who try to compare total retail sales to headline CPI don’t know what they’re talking about.

Retail sales are by retailer (businesses). CPI inflation is by product category.

Retail sales cover only about 25% of consumer spending. The rest of what consumers spend is on services, including housing (spiking inflation), insurance (spiking inflation), healthcare (spiking inflation), etc., and spending at other institutions that are NOT retailers (prescriptions drugs at hospitals, etc.)

It’s conceptually wrong to apply the overall CPI inflation rate to retail sales, and people who do that don’t know what they’re talking about.

I discussed the inflation factors IN THE ARTICLE. I also have unit sales v. dollar sales for auto dealers and gas stations.

For example, electronics retailers here sell consumer electronics. But consumer electronics had negative CPI, meaning prices fell. So you want to apply the overall CPI to electronics dealers? See what I’m saying.

You cannot apply the overall CPI to sales at retailers.

“based upon the Fed’s comments today they are gonna let it run hot.”

The Fed didn’t imply that at all. Esp after the alarm bells sounded from the last CPI report the Fed made it clear it’s set to move even more aggressively than before to bring this inflation under control, Volcker style–runaway inflation wrecks economies and nations and it’s getting dangerously close to getting uncontrollable, crippling the dollar’s buying power. JPow and the team have no choice but to move in aggressively now. The Bank of Canada raised rates by 100 bp and this also flags a much more aggressive Fed move.

“high paying jobs are still plentiful”

In some sectors yes, others no. Silicon Valley and other smaller tech centers are moving to more-and-more hiring freezes as the latest tech bubble unwinds, even the FAANG’s. And part of the availability of such jobs to begin with is due to worsening labor shortages, partially due to labor force gaps from things like Americans getting sick with COVID or long COVID. Some sectors have plentiful such jobs simply due to them not being filled.

“The Fed said no such thing. They said they will raise by 75 basis points at the end of July.”

Which just goes to show that Jerome Powell and Co. have absolutely no business still having jobs. They are completely incapable of doing the right thing, which would be to front load interest rate hikes massively to get ahead of inflation. I don’t think they have any intention of ever actually getting ahead of inflation. Jerome Powell is a traitor and a coward.

Arya Stark

“The important number is Real Final Sales (RFS). It’s the true bottom line number for the economy. etail Sales Look Strong But Fail to Keep Up With Soaring Inflation

A week ago, the GDPNow RFS estimate bounce to +1.3 percent from +0.3 percent. Today RFS settled lower at 1.0 percent.

If RFS comes in negative for the quarter, the recession may have started in the first quarter.

The July 15 update to the Atlanta Fed GDPNow Forecast shows a slight dip to -1.5 percent”

(h/t Mishtalk)

yesterday’s zoom of indexes could very well a ‘BEAR’ trap bounce!? Let’s wait n See

Exxxactly. We have become a country of 2 classes of people. It doesn’t look like it has slowed down one bit in my neighborhood in Capital Hill in Seattle, or in Queen Anne, or any other uppity neighborhood. The techno-successful 20/30-somethings are out in droves on Pike and Pine St spending $25 per tapas item EXCLUDING the 20% tip AUTOMATICALLY added and EXCLUDING the 10.25% sales tax. Compare that to what is going on in some other areas, it’s night and day.

Great for the State of Washington and supports the local service economy.

Probably different distribution now that many high earners work remotely.

Anecdotal, but I’ve heard from multiple successful 20/30 somethings that they don’t see our economy as sustainable, so they’d rather enjoy life while they can.

That’s not a sign of confidence, but resignation as to a dark future.

“That’s not a sign of confidence, but resignation as to a dark future.”

They’re spending like there’s no tomorrow, expecting that someday soon there won’t be one.

Plus they’ll never be able to afford a home, unless it’s retirement home after they’re done repaying their student loans, so there’s no point in saving up for one.

Tried to make a reservation for a BDay party at three steakhouses this last weekend and no seating available both Friday and Saturday nights (eventually had to go with Sunday and was max packed) – busier than 2019 from what I can recall.

Good to hear about Capitol Hill and Queen Anne. This southern boy made some good money in the early 2000s doing remodeling in Seattle. It was the first housing boom and you could name your price. Only thing was that with my southern accent, some people asked what country I was from.

This country has always been a 2 class system,first you immigrate ,then work your way up ladder. Then depending on choices ,spend money on wine women and song ,or you invest to get a better lifestyle.I did both and it’s turned out great

@unamused:

“Plus they’ll never be able to afford a home, unless it’s retirement home after they’re done repaying their student loans, so there’s no point in saving up for one.”

There may be a lot of truth to this. Been seeing more Millennials and Zoomers in tech be less willing to build up savings and more wiling to sink into credit card debt, even higher earners living way beyond their means. Been talking to some STEM grads who otherwise have good prospects but many bring this up, the cost of homes is so ridiculous now while inflation removes their buying power, they see little value in patiently building up savings that won’t afford critical goods anyway. So why not spend and fall into debt anyway? Another example of the societal damage caused by this Everything Bubble (and housing bubble esp) from reckless Fed policy over the past decade and half.

@Brant Lee

I know some contractors on the SW side of Chicago/burbs who have affected an Irish brogue even though their grandparents/great grandparents came over here over 100 years ago. Marketing!

In terms of this just being the spending the cash from sales of inflated assets, this happens every cycle, but much more magnified now than ever before, and the smart money always seems to find a new venue, leaving a larger pool behind.

That makes sense. All the gamblers that have now cashed out are sitting on a nice stash to enjoy as they please. People that were depending on wages and refi’s not so much.

If you were gambling in anything these past few years, either crypto, real estate, stocks, sports memorabilia, you could not lose. The only question is did you get out in time?

Buying and selling in financial markets doesn’t increase the aggregate amount of cash in the economy. It only changes ownership.

Rising asset prices incentivize those with appreciated assets to spend the cash they have, the psychological wealth effect.

Augustus, have you heard of the fed?

Cyrus,

What does the FRB have to do with my post?

Nothing to do with the Americans trading the same assets back and forth at higher prices while pretending it increases wealth.

We are way overdue for an asset recession (deflation). Labor and consumer price inflation can stay high. Demographics support it.

I read a Salon article today SCREAMING for the Fed to stop raising rates or we risk tanking the entire economy into a massive jobs loss meltdown. The top 50% are going to fight this recession with everything they’ve got, and the bottom 50% are going to pay the price.

Oh my goodness, the comedy of it all.

Seems to me, from this article, folks with money are spending it, in ways that are trickling down to less fortunate workers. So it seems a comedy in maybe the old-fashioned sense of, a happy interval possible for awhile? I applaud those folks for spending so patriotically. I’m a contrarian. I like to have cash when times look bad. So, I play it cool when things look hot. This has worked, so far.

I agree Wolf. I know this guy whose daughter is a dentist, her husband an engineer. We were chatting on the ski lift and he talked about the great money they make together. Younger couple, I believe still under 30. If you got two people making good money, you can weather whatever storm.

Unless divorce breaks up that high earning couple and one winds up paying crippling alimony and child support to the other, at least the way the US family law system is currently designed. Seen it happen countless times in state after state, even one of my best friends (a surgeon) got financially crushed by his divorce settlement. A skiing connoisseur himself Fwiw too, at least until the marriage fell apart.

Yup, Miller — divorce is for rich people.

Recession is definetly here. I only received four out of my six packages.

I am one of those conspiracy theorists that thinks inflation is being miscalculated. So, adjusted for “conspiracy inflation,” these figures would be back at pre-pandemic levels, and real GDP would look like Venezuela in 2014. As hyperinflation unfolds, the real figures will portray total economic collapse, meanwhile these “nominal” headline numbers may portray growth. Having “LOTS” of money is meaningless when it has no purchasing power.

First, inflation used to be defined as monetary inflation. The inflation number did then track inflation of money, in other words how much money that was created in a given timeframe.

Then CPI, Consumer Price Index, came along. Note, index, not inflation in the name. Some, you could say the ruling class of econonomics, did chose to use the CPI as a measure of the inflation.

The use of CPI as a measure of inflation do require that there is a strong coupling between inflation and CPI, that may or may not exist.

If the coupling between inflation and CPI is weak, non existent or the CPI is strongly affected by other variables much of the economy theory as presented by central banks are wrong.

Also numbers like the GDP make little sense then as the calculatios are «corrected» for «inflation».

WR

In short, the rich are doing fine. The middle and lower middle classes are getting hammered. The lower the income the worse it gets as inflation eats up all of their disposable income. The poor are now living out of their cars or in the streets. The US has turned into a third world s$ithole almost overnight. Just drive into the DC Swamp and you will see all of this right before your eyes.

Nonsense! Only 6% of Americans make over $100k a year and a large % of then earn about $145k last time I googled it. The top 10% of the country is spending as you describe. Look at the average city or town. Look at the workers. For every doctor, lawyer, business owner, franchisee, upper manager etc. there are a hundred peons earning less than $20 an hour. The American way you talk of is when America had a burgeoning middle class.

If my stats above are wrong then please argue otherwise. America is becoming a third world country. The hyper consumptive middle class is dying off and those surviving are living off the disastrous debt and credit system.

You need to look at “household income” — not at individual wages and salary.

So in 2020, income dropped because of the spike in unemployment. Incomes have surged in 2021 due to surging wages. But we don’t have the annual income figures yet for 2021.

For example, in San Francisco the median “household income” in 2020 was $119,100 (Census). This means that 50% of the households had an income above $119,000.

For Boston, in 2020, this figure was $76,000. For New York City, in 2020, this was $67,000. In Dallas, this was $54,700. In Miami, in 2020, this was $44,000.

A big flaw in your analysis…..retail sales are up, but so are retail unit costs. Consumers are spending more, but are buying a lot less product!

You see the economy through an empirically distorted lens of the 10% wealthiest Americans. Inflation has hit the majority of American families who are living paycheck to paycheck

There’s a reason why Walmart and Target has had ugly earnings misses recently. Shoppers are buying more necessity items like low margin groceries and less on store shelve products because of strained levels of discretionary income.

RTGDFA

The credit cards still work!

Yep, also been seeing a lot of credit card maxing even by some old friends who I used to associate with frugalness. Big part of what’s fueling this.

Miller

Exactly!

There is significant increase in Consumers revolving (CCards) credit/debt. As purchasing any thing ‘Money and Credit’ are synonymous except for credit demands pays back along with interest and penalties!

Bottom 50-60% (may be even more) look at life as YOLO and want to live it up. Bankruptcy is always, right?

I’m with those saying the incentives today are skewed towards a “party-now, save-later” approach to life, at least for those who aren’t budget-stripped by inflation (yet).

There’s no point in saving when inflation is killing the value of any savings, and the Fed’s not serious about stopping the inflation.

And anyway there’s no point in investing those savings while the markets are all going down, banks pay very little interest, etc.

Might as well party!

Weimar Germany? Roaring 2020s?

Amen.

> There’s no point in saving when inflation is killing the value of any savings

I have to differ. the point is, survival. Survival is very underrated, apparently,if people are tossing cash to the wind.

To survive cash flow is essential. In a debt based society survival is to keep the cash flow going as long as possible. Preferably to leaving this world. Leaving the world with a huge debt is rational, no repo man will come after you then;)

If you’re a homeowner you basically won the lottery over the past 2 years. I have no idea what the average home equity gains were, but I’m guessing there were millions of people who had hundreds of thousands in gains.

Just imagine if that many people were handed winning lottery tickets.

Then there are those of us who were priced out of the market already and are now forever renters, and no winning lottery ticket.

Move to flyover plenty of houses at 100 k

Yeah that’s true. Talked with a manager at Jimmy Johns who is leaving Tacoma for Arkansas soon, due to high cost of living here. Said their new house on an acre cost $90k. I had no idea still that cheap in places. Sorry flyover, people are heading your way. Better buy more guns.

That is true. It might all turn around quickly though. It’s kind of standard for leverage and foolish spending to be excessive right at the peak. Buying a house or a stock a year before the blowoff top can look very smart in one year and very foolish the next. Fed juicing assets looks like it went on at least a year too long.

It’s not over yet – wait and see what happens next.

If the housing bubble deflates and prices return to pre-pandemic levels homeowners would just have been paying excessive property taxes for a few years.

If they did a cash out refi they might be in a negative equity situation.

Too soon to tell right now.

SOL,

“If you’re a homeowner you basically won the lottery over the past 2 years.”

Not sure. If the price of your house that you bought in early 2022 tumbles 40% over the next few years, you sit on a big loss, and you cannot sell the house, but you’re financing that big loss with a cheap mortgage. But if you bought your house 10 years ago and refinanced the mortgage at 3% last year, then you won the lottery.

“But if you bought your house 10 years ago and refinanced the mortgage at 3% last year, then you won the lottery.”

According to Freddie Mac, exactly 10 years ago in July 2012, the mortgage rate was 3.55% so if you refinanced it down to 3% then it’s a small saving that has likely been eaten up your increased property taxes and insurance.

Bit of a stretch to call it “winning the lottery”

> Then there are those of us who were priced out of the market already and are now forever renters, and no winning lottery ticket.

Remote work + move to the midwest, buy a home with a lot where you can do permaculture => you turn the NIMBYs into your slaves instead of the other way around :-)

You HAVE to make the NIMBYs work for you or your quality of life would decline.

The top 10% have over 90% of Wall St wealth and the bottom 90% less than 7%.

35% of the Consumer based (70%) consumption is by the top 10%-20%

No wonder they can spurge without any restriction.

Story on the bottom 80-90% is different. Majority don’t have $1000 in savings or $400 for an emergency! But, there is always the credit (CCards) right?

The US personal savings rate is near a five-year low as pandemic fiscal stimulus savings run dry. The spending is supported by Consumer revolving credit (CCards) is highest level in decades.

Biforked economy – Prieto rule 20% haves vs 80% have-nots. Just like in many developing Countries, more or less.

One source: consumer debt load has been rising steadily in 2022.

Anecdotally: I visited a major mall in the Jacksonville, FL area yesterday. This place has been busy for mos. For the first time it was way short on foot traffic based on previous visits. I asked several of the shopkeepers ‘wazzup with dat” and each passed the same: slow down started a couple weeks ago.

Could be Summer heat. Or not.

Similar situation in the saintly part of tpa bay area pj.

BRUTUL Heat far damn shore.

Bottom priced, etc., still fairly busy, but definitely

”the season”

to be somewhere else if you can

Savings. Re restaurants and “They’re in a boom, with sales up 33% from June 2019” people can sense that the end is near given Climate Change, so they are spending savings now, giving up on ever having a retirement in 2-3 decades as the planet will not be livable by then.

Everywhere you look you see signs of this collapse.

Ha ha, like any of this remotely applies climate change.

So true…. I saw a TRex running down 101 yesterday, end is near, piss away all your money and wait for it!! /s

Einhal wrote: “… these numbers are being driven by asset gains among the top 20% or so, there is no way to get inflation under control without causing a massive drop in asset prices.”

Or they could tax the top 20%. But that might inconvenience some of the wrong people.

I wonder how the BLET railroad strike scheduled for Monday affect some of these businesses?

You can’t tax this “wealth” because it’s not real wealth. It’s all a bubble.

You can tax bubbles. Capital gains tax catches a lot.

Yes, if people sell. But much of the “wealth” is tied up in fantasy valuations of assets.

Property tax have to be paid each year and market value is the taxable property in some countries. That is the wealt in financial papers are taxed as property belonging to owners. Tax value is equal to market value.

Einhal

It is NOT bubble if you had ‘cashed out’ 90% or more or cash out 50% and stay invested with uncorrelated including going against the mkts with puts and or inverse leveraged ETFs( always paired with their long counter part!

I made a huge profit during GFC but lost most of it b/c I was dumb enough NOT to realize the powerful effect of ZRP+ 4 QEs+ Stimuli with Trillions thrown at the mkt by Fed by printing out of thin air. The debts now at record levels, unlike any time in human history.

Reversion to the mean, in progress, with expected strong ‘re-bounces’ aka bear traps along the way. Gone thru more 1 bear since ’82. The coming one will be a lot worse b/c humongous debt levels here and all over the world.

Nimble option traders don’t have to worry. Smart ‘swing’ trades can also cushion the effect of the bear. Made more during Bear mkts than during Bull ones!

I have bought PUTs for the short/intermediate term and long leap calls, for the long term, adjusted periodically and under review. It is working fine.

Most retail investors don’t know option trading or psychologically prepared or trained to against the mkt. They have been ‘pavloved’ by Fed’s put and siren song from the Wall ST that STOCKS always go up in the long term. If one analyses the recent mkt history by rolling 10 and or 20 yr performance, one has to be lucky enough to ride the bull and stay out during bear, which is virtually impossible.

So most retail investors will end up holding the bags just like after dot com bust and GFC. The comfortable ‘group’ thinking also clouds and impacts the performance of most of Money managers, MFunds, investment banks and of course pension funds.

We are in uncharted waters!

Most of the top 20% aren’t wealthy. Most of them are already tax donkeys, unlike the .01%.

I have a better idea. Why don’t you volunteer to pay a lot more tax since you think taxes aren’t high enough?

There is nothing stopping anyone who agrees with your view from writing an extra check to the IRS at any time, over and over.

“Most of the top 20% aren’t wealthy” yeh, right, sure.

And Powell doesn’t have 85 million dollars stashed, right?

Thanks for enlightening us.

The median net worth of the top 20% is $600,000, most of that in home equity or retirement accounts. Nowhere $85 million.

You should get your facts straight next time before you display your ignorance.

It’s maybe the top 5% that are “wealthy”. The rest of the top 20% are better described as the “mass affluent”.

“The rest of the top 20% are better described as the “mass affluent”.

Agustus,

Spelling error…it’s spelled “effluent”….

Not true. There is a large contingent of what some people call “HENRY”, high earnings, not rich yet. Most of the truly wealthy in the US are older, in their 60s and 70s. Lots of high earners in their 20s to 40s have far less than a million in net worth but still spend like a drunken sailor. And there is a massive difference between the 0.1% and even the 1%, generational wealth vs people with 5-10 million net worth.

”GET REAL” folks!!!

”OLD ” money folks do NOT care about any of this kind of ”market” BS/propaganda, and never have.

Kinda sorta a challenge for those of us NOT part of that party…

but kinda sorta need to ”get over it” for most of ”WE The PEOPLE”

Unfortunately, similar to ”the poor”,,, ”the rich” are likely to be always with us and do SO much to ”challenge” WE the People that I would not doubt at all to see una make once again his very good ”rants” or better!!!

Those who promulgate class warfare love to talk about “raising taxes on the wealthy” and “taxing billionaires”, but when push comes to shove, they actually tax the everyday people that most people see as the “rich”, the dentist or lawyer or business owner in the neighborhood who is a wage earner making 200-500K, these people pay the 30%+ rates while billionaires pay capital gain taxes or borrow against their wealth and pay nothing, or give money to foundations and pay nothing. The upper middle class gets the shaft. The truly rich skate free.

They create foundations,which shelter income

AF, by definition a donation is not the same as taxation, and the latter is necessary for a host of priorities unrelated to revenue.

Whaddaya mean the bar’s closing?!? Where’s the after party???

The afterparty is on the Titanic.

We ain’t scared of no iceberg

Cool, looks like party on then Garth. Since recession is not happening anytime soon. Guess the hope for a housing crash can down to the drain as well. Wealth effect is still alive and kicking.

Viva, wealth effect. We are all dancing above the abyss. Every balance sheet in the universe has a bottom somewhere.

I’d say there’s a good chance for a recession in 1st half of 2023, just not as soon as some were predicting (for this year). The Fed has to move aggressively or inflation flies out of control, and that historically has crippled empires, great powers and nations more than any other economic disruption–a recession is just a speed bump by comparison, and the right “kind” of recession can be healthy longer term, by deflating asset bubbles and normalize prices closer to incomes. But no nation can survive its currency becoming more worthless to buy real goods and services without a huge civil collapse. Esp the US dollar, with the US having such a large trade deficit. Short sighted QT and ZIRP are the cause of the Everything Bubble in the first place, and the effects of their unwinding can only be resisted for so long. The housing bubble is already starting to pop in some US markets, though not nearly enough yet. Still, laws of basic economics dictate that they have to fall for the economy to be sustainable–in many markets, US real estate has gotten so stupid expensive that even top earning professionals and software engineers can’t afford decent homes, and so can’t afford to start families either. That’s not sustainable. Prices have to have some sane connection to incomes, otherwise it’s a bubble by definition, and some of the housing markets would have to fall more than 50 percent to be in line with incomes.

It’s pretty clear from the data I have seen that people tend to spend and save at the wrong part of the cycle. People tend to leverage up late in the cycle in the gogo years and then stop spending and try to increase savings during recessions.

It is understandable, but you probably end up with more money if you borrow and spend in a recession and build cash in go go times.

When inflation is raging (like ummm now), it’s better to buy stuff today than tomorrow. Because it will only be more expensive tomorrow. I think this is quite a bit of the goods upswing

I always believed that Americans would binge-spend after the worst effects and restrictions from covid passed. I bought two new mountain bikes last month for my spouse and I, at least in part because it feels great to be out and about again. I rejoined my gym last month to lap swim under the sun and I’m hearing that members like me are coming back.

There is such a thing as a new season, and a springtime, and another chapter, and we don’t have to wait for some statistician to sign off on it.

I bought really good stationary mountain bike.

Aren’t mountains always stationary?

Given the extremely strong data of the past few weeks (for June M/M: +372K NFP, +1.3/+0.7 CPI, +1.0% retail sales), why do Wall Street, the financial media, and the bond market continue to hammer this recession narrative day & night? The 10 year treasury yield can’t seem to hold above 3%.

It’s clear the economy can withstand much higher rates. The markets just want to throw a tantrum.

I agree. We’re going to get Q2 GDP soon, and it’s going to be a positive number. You cannot have a recession with this kind of spending, and a red-hot labor market. There may eventually be a recession, but not now.

How will the final Q2 GDP numbers differ from the Atlanta Fed’s GDP Now tracker?

What I mean is, does GDP Now’s current -1.2% Q2 move upward as it lags data over the next two weeks, or are there revisions in the works that will be applied retroactively to turn this -1.2% into a positive number? Both?

GDPNow is a “nowcast” not a forecast and it’s not GDP. The GDPNow has nothing to do with actual GDP.

The folks at the Atlanta Fed take the data as it shows up and put it into their model, and out comes GDPNow. The final version, which is released just a day or two before GDP, rarely matches GDP. In the past, it was way off, so often that I stopped paying attention to it. Sometimes it was way high, sometimes it was way low. Just random.

So we can get actual GDP of +1.5% annualized and the final GDPNow of -1.2% the day before. No problem. This kind of stuff has happened many times.

If there is a big disconnect, maybe it’s time for an article about it since this keeps coming up.

Wolf, just thinking about 2q being positive because of the red hot consumer spending. My first thought is how much of tbat spending is debt based. My second thought is to wonder what relevance a GDP print really is if it is so based on consumption as opposed to production? What is it really saying other than we spend alot ( in many cases money that we don’t have)

Jackson – “why do Wall Street, the financial media, and the bond market continue to hammer this recession narrative day & night?”

Because for people spinning that narrative would have you believe that up is down and down is up. The narrative right now is that if we have a recession that means the Fed will stop hiking rates and restart QE, thus good for stocks. AKA recession = restart QE = stocks go up. Crazy right?

This narrative is meant to dupe suckers into going long so the ones behind the narrative can cash out.

Peachy

Spot on.

Couldn’t have said it better!

“It’s clear the economy can withstand much higher rates. The markets just want to throw a tantrum.”

Yep, this totally. The squawkers and Wall Street welfare beneficiaries are indeed throwing a tantrum and just like any toddler, they’re doing it to try to force their rich Daddy (the Fed) to give them even more candy that’s rotting their teeth and ruining their health for the next sugar high. Daddy Fed has stupidly given in to such tantrums constantly over the past 2 decades (last 40 years really), but that option is now over with inflation this high, and the whining Wall Street toddlers will have to deal with it. There likely is eventually a recession in the works from the necessary tightening (both with the interest rate hikes and esp QT) to break the back of this inflation, but it’s unlikely to happen this soon. Early in 2023 is much more likely, and it would be a cleansing recession to finally bring outrageous asset and goods prices closer in line with incomes, setting the stage for a strong recovery later in 2023.

Can the economy withstand higher interest rates if that make rentier activity tax the economy even more?

Note that with higher interest rates more money go to rentiers.

Too much of our economy like many other things in this country is influenced and driven by the news media. If you tell people the same thing time and time again they will soon accept and believe it. Sad but true.

Retail sales blew right threw the Fed’s pissy little rate increases. This retail gobbling bunch will eat the Fed’s slow rolling QT scheme as a snack. These well heeled retail warrior’s with also gave the Fed the bird to boot. 30% inflation will not stop these retail battle hardened veterans. If you can’t run with the big dogs stay under the porch. By the way, I am under the porch,woof …woof.

Damn, I felt like ‘suiting up’ for the moment!

It’s kind of like handling cattle. First, you have to gather them, then you get them to move in the right direction. But eventually they will test you, and the fun begins. Too little control and you lose them. Too much control can end up the same way. Raising rates to control inflation amounts to the same thing. The second time around, it gets serious. Best to do it right the first time. I doubt they’re up to it.

I’s like pivoting an aircraft carrier, except one ten thousandtimes the size of any carrier, ever.

Yep …. 12 cowboys can run a cattle drive of thousands of cattle.

BTW, ‘How many members of the FOMC?”

Interesting headline, as I was just at my local family diner and it was practically dead, during the lunch hour. Only 2-3 tables occupied.

Listening to the waitresses talking to others, it had been slow all day.

I explained I hadn’t been in for a while because my once a week treat has been reduced to once a month.

Not a lot of foot traffic in touristy old town either.

Go to a restaurant that is thriving, not one that is dying. Restaurants have life cycles, and they die, even the successful ones.

It had been slow during COVID but was picking up earlier this year.

One Sunday morning about six weeks ago I had to pitch-hit as a bus boy, as every table was full and only one waitress had showed up to work. Two more wait staff eventually showed up and I left once the backlog was gone.

Recently they have been busy on Friday’s at lunch time.

But this is also the place where people get sticker shock when they get their bill. We have one of the highest minimum wages in the nation.

Nobody goes to that restaurant anymore. It’s too crowded.

Sounds like an interesting topic to write about, if you haven’t already.

Tell me about it…. One of the best pizza places I have ever eaten at is Giordanos in Chicago. When we moved to Phoenix, we found a Giordanos in the suburbs, just as good as the Chicago restaurant!! They closed permanently this February. We ordered regularly throughout the pandemic and not once did they mess up an order. Why they would close is a mystery, now I will have to go to Chicago to get that pizza. Given the state of Chicago, looks like I am not going to eat at Giordanos ever again.

Stick to the SW side of Chicago for Pizza. Palermo’s, Home Run Inn, Vito & Nicks.

Send them a e- mail selling half baked pizza can ship to you

Let’s see how long this will last if the stock markets & cryptos implode along with massive layoffs. The hungry, who will also be very angry and resentful will be waiting for the restaurant goers and shoppers leaving to go home.

I think Americans can’t admit being broke, just like their Gov 31 trillion in debt, the fake image has to be maintained, so load up on debt, the guard rails (the banks) are just non existent to curb dangerous debt. Deja vue.

I think ya correct & will add, most people in restaurants today will be jobless, homeless & hungry themselves.

I don’t think the markets matter that much to the real economy, to be quite honest. 2000-2002 was a textbook example of a market meltdown that didn’t bring down the economy. While the NASDAQ tanked by 90%, full-year GDP growth was positive for all 3 years, and unemployment peaked around 6%.

It’s hard for people to conceptualize a recession that has no job losses. But I think that is what is occurring right now.

Except it won’t be called a “recession.” The NBER calls out recessions, and it uses a variety of metrics in its decision, including several labor market metrics. GDP itself is a pretty lousy metric for the economy, everyone agrees on that. So that’s why a recession needs to come with weakness beyond GDP, such as declines in employment, major increases in unemployment claims, etc.

just to be clear JY,,,

that crash when ronnyrat came into POTUS was a very devastating ”crash” for some of us…

back in those days,, going at least back to FDR,,, every, repeat EVERY ”administration” wanted to make sure, as in damn sure,,,

that everyone in USA knew very well where, as in what political party, the money came from.

So, while modern folks want to make something bad or worse about ”the other party”,,,, fact IS that both ”parties” are in the biz of screwing the workers.

Other wise,,, both ”parties” would start voting in our Congress for laws and regulations that would help the folks who actually produce our wealth, rather than those who ”financialize” our wealth to rob us.

Pretty clear at this point in time,,, only question is IF this clear robbery of ”workers” will stop.

the stock market is not going to implode….

Agree…100%

The market will slowly deflate…slow enough, with enough rallies, to keep people from panicking.

Hold on… The Fed has only started dipping its tows into QT. Combine that with seasonal factors associated with tax collections and the impact of QT on the economy has been very muted so far. Let’s wait and see what Sept./Oct. brings.

This will end in a depression, the banks are giving anyone with a pulse massive credit & people are having one last splurge in total denial.

I don’t think for one second it’s spending from gains, no chance. This is massive debt creation, zero standards, defaults will explode, will make 2007 look small.

People living in fantasy land, the US is already in recession & soon a depression.

that is bs. I work for a CRA, people are getting denied with bad credit, underwriting has tightened. DTI and PTI are now focused numbers

It’s not bs, 8 yr car loans, defaults skyrocketing, millions unable to pay mortgage or rent, the credit ratings ain’t worth anything after the last two years, everyone had a massive bump higher in ratings due to payment holidays & no missed payments.

So everyone has a fake credit rating & all this crazy crazy spending is proof, they can’t pay that back, ya can’t get this amount of spending unless something fundamental changed & I know it’s lending standards being non existent, knew it in 2007 & know it now.

I try to balance my natural pessimism with other views but my small little slice of flyover and our business are my primary window to the world. And I’m with you.

Our business tends to follow pretty closely the economic sentiment of the country at large. The story of 2021 was of massive demand, but with high costs. The story of 2022 is of cooling costs, and rapidly cooling demand.

Our order rates are abysmal for July so far, and things are usually pretty steady. If the second half mirrors the first, it will be the lowest order month in over a decade. Only worse ones in ‘09/10. Backlog is still strong enough to take about 2 months of that, but not more.

Raw material prices spiked just before the Great Recession, only to be followed immediately by dropping through the floor with the crash. We are seeing that commodity movement rhyme right now.

Our scrap buyer is a pretty big operation, and they said no one even wants their metals right now. No buyers. Price is low. This is good because the high metal prices killed us in 2021, but if orders for durables drop, it’s just as big of a big mess too.

We have a deep layoff list ready. If orders stay at this level for another 6 weeks, layoffs will hit our place hard and fast. Hoping it doesn’t come to that.

Just spoke with a lawyer and banker at a property closing two weeks ago. Both said real estate activity has completely vanished in our little patch. Lawyer was doing 10-12 closings per week. He said it’s barely 1-2 now.

Our story isn’t necessarily the story of everywhere. Who knows.

Just because you’re depressive doesn’t mean the rest of America is. The economy has cycles of boom and bust, but right now we have the strongest currency in the world and people are spending it. Employment is at record highs and people are happy to be out and about after two years of pandemic malaise. There’s always doomers and they’re rarely right.

Never underestimate the resilience of the American consumer. I think of all the financial suffering coming, the USA will end up suffering the least of the world, collectively speaking.

From where does the American consumer get its “resilience?” Certainly not from collective production!

Strongest currency in the world doesn’t hurt, not does the largest economy.

I was in a Home Goods store this Friday morning, it looked like Christmas. The women seemed to be panic buying doo-dads and knick-knacks.

Wow, up 32% from 2019? That’s bonkers. You have commented specifically in the past regarding the extremes occurring in the auto market. Combined with the historically hot labor market, crazy housing market, etc, and the much-feared “recession”, if it occurs, may just be the economy reverting to historical means…

Lenin believed Britain would colonize itself out of existence, Germany would militarize itself out of existence, and the US would spend itself out of existence.

His grave is a communist plot.

The war is over (for now). People are happy to be able to be out and about.

Yep don’t see a recession soon as mentioned by Wolf months ago. Employment too strong.

Plenty of cash from the previous reduction in interest rates.

Lots of cash ready to go back into stocks i think as well.

you bet because its mid terms and a distinct pattern is rolling now into bullish time frames

all the hype on recession and doom probably scared a lot of new money players out, old school folks just bought the dip and are now about to get richer….

their is no slow down in lower middle class thru the rich…

Cash cannot “go back into stocks.” That’s impossible. For each buyer that must be a seller. Someone puts cash into the market (the buyer), then someone else is taking cash out of the market (the seller).

All they can do is change the buying pressure or the selling pressure.

So the European Union is starting unlimited bond buying next week per Bloomberg. Isn’t that QE 2.0 again?

It is but you are not aloud to call it that

John,

You misread this completely.

If yields diverge too much, for example between Germany and Italy, the ECB may shed German bonds to raise German yields, and buy Italian bonds to lower Italian yields. Or they may shed German bonds faster than they shed Italian bonds. The goal is to keep the spread between them somewhere in the acceptable range.

The ECB can do QT on this basis just fine, and they will do QT, but unevenly to keep the yield spread within bounds.

A headline from two days ago:

“ Chinese Lehman moment as “jingle mail” arrives”

They built too many half finished towers.

This is an interesting story to watch. Second largest economy in the world.

1) Total retail sales made a new all time high, but the spread between the

last three dots is a thud, to be confirmed. // For entertainment only :

2) SPX weekly failed to close above June 20 despite the higher efforts.

3) NDX weekly : a hammer, an inside bar, on higher volume. Last week had only 4TD.

4) NDX weekly : June 13 was a spring. The spring job is to send NDX above the previous high. After four weeks NDX failed to breach May 31 high. // June 21 white bar closed > June 13 high. June 21, a setup bar. June 27 higher high, a trigger. There is no close above the trigger high. There is no close under the trigger low.

5) NDX daily : since June 16 low most of the activity was in the upper half. It reached about 50% of the move from Jun 2 high to the bottom.

6) NDX daily : today bar was the smallest bar in the last two weeks, on a higher volume, under dma50, under a downtrend line coming from

June 2 to July 8 highs, under the red cloud, but above T&K of the cloud. NDX weekly entered T&K.

7) NDX might be tempted to penetrate the sexy groove above.

Why do you keep doing these postings? The era of financialization is over, nobody cares about this stuff anymore. Markets are dead.

People were doing charts long before “the era of financialization.” (Not that I do it.) But I reckon, picking a figure as arbitrary as any other, that “era” started with the commencement of the USA. That’s why (real) history books are never “over.”

It does matter what stocks do, versus dollars, versus real estate, versus commodities. “Era of financialization” or none. People still steer value through time: definition of finance.

Historically, market data reflected actual transacted values. Now they make this shit up, and not just in a few areas, it’s everywhere, all manipulated crap. Dark pools, HFT, buybacks, repos, sdr’s, cpi, ppi, all made up crap to siphon off your money.

Nobody cares.

Could not agree more Pet.

Somehow and some when, WE, as in the entire population of earth WE, will/must ”take back”

OUR world from the folks who appear to be ONLY at and IN the ”financialization” of OUR productions of value.

There is nothing ‘dead’ about markets whatsoever, and they are more alive than ever and now effectively doing price discovery with a lot of volatility and divergence among opinions as to the future of the US and global economies.

Agree with your comment vis manipulation. The data is not trustworthy. Better expressed, the components of the metrics and the metrics that are chosen change to meet political objectives. As do many accounting standards.

I really think you are wrong on your take on this number Wolf…

Are you saying the WSJ is wrong here? Look, they have a chart that shows the retail sales number adjusted for inflation.

https://www.wsj.com/articles/retail-sales-june-rose-consumers-inflation-11657833254?mod=hp_lead_pos3

“Are you saying the WSJ is wrong here?”

YES. The author is a young reporter, a few years out of college, with a BA in journalism (2016), and knows nothing about how any of this stuff works. I have called out the BS written by young reporters in the WSJ a bunch of times. They got rid of all their grizzled editors that would have caught this, and these young clueless reporters write whatever.

So give it up. READ my comment. RTGDFA, because it explains ALL THIS. You clearly cannot make yourself read my stuff. So be it.

Well here is a bet then. You said that GDP will come in positive because of this “strong spending”. I do not think it is strong because I think it is all inflation, so I say GDP will be zero or negative. If GDP is positive I will donate you your website. If it is zero or negative you acknowledge I was right on a post. Deal?

And if it’s positive? What are YOU going to do, anonymous commenter?

I’m going to discuss GDP anyway, no matter how it comes out. So what are you going to do?

RTGDFC! ;)

“If GDP is positive I will donate you your website.”

🤣 You got me.

Yeah, the WSJ can make pretty egregious errors. Case in point… a few weeks ago their main editorial article was a piece praising the recently-elected Republican governor for allowing the creation of university-sponsored charter schools, to supplement (and supposedly compete against) existing school district sponsored charter schools).

The main thrust of the editorial was that the governor did this as a way of getting around existing collective-bargaining restrictions associated with the state’s ‘evil’ teacher unions.

The only problem is that Virginia has neither public-sector collective bargaining, nor teacher unions. These have been outlawed in the commonwealth for a long time. Although the outgoing Democrat governor did sign a bill that authorized the optional formation of separate teacher unions in the 100+ districts in the state, this happened very recently and it will take many years for such unions to actually organize and begin to collectively bargain – if that even happens at all (I’d say there’s a high likelihood that it won’t).

The WSJ has a few really good reporters (which yes, do tend to be older and more experienced) but also a bunch of really crappy ones.

Good thing there is not a Virginia Professional Educators or a Fairfax Education Association then…eh?

@ phillip jeffreys, the organizations you list are voluntary and to which only a fraction of teachers belong to. They do not perform collective bargaining. Maybe they will someday, but they currently do not. The WSJ article was clear that the main reason for the establishment of the new type of charter schools was to circumvent restrictions in the existing collective bargaining agreements which is not true.

GDP for the second quarter 2022 appears that it will be NEGATIVE BY AROUND 1.5% YET AGAIN according to GDPNOW and here in Southern California stores are NEARLY EMPTY including restaurants, grocery stores, big box stores, discount stores and everything else.

San Francisco is packed with tourists, and it’s hard to get into restaurants. So maybe everyone went north?

I was just in the west Palm Beach, and Miami area, and the crowds were incredible. Hard to believe does are empty elsewhere.

Thousand Oaks seems to be doing fine. I haven’t noticed any drop off in traffic when I shop or go out to eat. Grocery stores tend to retain traffic in any economic conditions, though the buying patterns may shift. Maybe it’s just where you live.

I went to our Costco earlier today.MAYHEM!! People buying no matter what. Prices up like crazy, and people are still buying like there’s no tomorrow.

Many WSJ writers (and A.M Best, S&P) were just fine with AIG right until it collapsed in 2008. Likewise with Reliance Insurance Co. around 2000. Hack WSJ insurance expert Leslie Scism will give the roadkill play-by-play as it appears in the rear view mirror.

I’m spending because after years of austerity everything needs replacing. So far, I’m replacing clothing, phone, sheets, towels, pillows, kitchenware, tires, etc. All the everyday items are just plain worn out. Whatever it costs to replace what I need is what I have to spend. My spending is way up for the year.

I would suggest you LOOK FOR QUALITY on things you buy in the future as they are much cheaper over the long run that buying the cheapest stuff.

I’ve been trying to wrap my head around just how much money was created (not earned) in the last couple years, and I don’t think the human brain is really capable of actually understanding what a trillion of something is, much less several trillion.

Our money supply increased from ~$15 trillion to ~$22 trillion in 2 years. Nearly a third of dollars were created in 2 years! As much as were created during the entire already crazy previous decade of QE. That’s just nuts, a truly mind-boggling mountain of dollars. Some gets tied up in reverse repos, a lot is yet to be spent by the government, some went right into circulation, some is still getting lent out at historically low rates. Anyway around it, there is still just a huge amount of money sloshing around in this economy looking for something to buy. Clearly, those dollars are still chasing goods and services as evidenced by this article. I just don’t see this relenting while the job market is still red hot and the Fed is still taking their time with incremental adjustments. Markets may creak and groan, but how would we get a recession with so many millions of job openings and so many trillions of new dollars still looking for a purpose? The fed is so woefully behind the curve, I have to question if they have any real control over the situation at all.

and its why scared money is not going to make money….

their are trillions of dollars floating around waiting to be spent, it makes 2008-12 QE look like pre school lesson

Where do you come up with that notion?

And demand for USD has never been higher. DXY is a wrecking ball right now.

Despite insane amounts of DXY printed, the global economy is dying for more.

I don’t really know what to make of it. I mean the Euro is falling apart and the JCB is hari-kari with the Yen right now!

Flight to quality sounds ludicrous if it is to the USA, until one ponders what a hash the other economies have made of their situations. And they keep up a PR front. I don’t see how some countries are holding together at all.

But the US dollar definitely has its risks. An open system, no capital controls, well, the Brits had that. Their attempts to cling to that (in a gold standard) finally became a series of failures with big impact on their people. Luckily we did not hang ourselves too long on a cross of gold. Now the dollar can float and flex and not crack.

An open system is what insures the survival of network effects. It takes an awful lot of dollars. It buys everything on the planet every day. It has been hard to print ourselves into enough trouble, yet.

Our openness is being studied by every starving “student” worldwide to find hacking vectors.

Try buying Russian natural gas from the pipeline in Europe with US dollars;)

The risk is that those exporting natural resources want controll over payment exchange rate.

YouTube the dollar milkshake theory.

When a borrower takes a USD loan or issues a USD bond, it is effectively shorting the USD. When that USD debt can’t be rolled over (when interest rates increase), borrowers need to raise dollars to service existing, usually by selling USD assets (stocks, bonds) or forex intervention, and creating a squeeze on USD. And since global trade is settled in USD… see Sri Lanka fuel crisis.

Fun times.

Good post NS. Waaaaay too much fiat sloshing around.

Why the low LFPR?

Your concerns about money printing/ZIRP are entirely on point. It has been in play for quite a while. Basically turned one asset class after another into speculative casinos divorced from market forces.

And what’s not to love about Modern Monetary Theory! It’s practical application has worked in Japan!

Central banks abandoned tying their rates to monetary aggregates decades ago for a reason.

And the aggregate without any consideration of the differential propensity to save/consume across the income/wealth distribution isn’t very useful.

Not Sure said: “Our money supply increased from ~$15 trillion to ~$22 trillion in 2 years. ”

————————————–

I have seen $5 Trillion, even $10 Trillion, but I have not seen numbers as large as you are claiming. Where or how did you come up with 15 to 20 Trillion? which is quite a large range by the way.

What do you think Wolf?

This is astonishing. I mean everyone has their anecdotal experiences, but $$$ is just flying around all over. With as much as was dumped into the economy from 2020-2022, I bet this inflation could keep rolling another 2 years.

The argument has been made by so-called “monetary experts” that when a currency is experiencing raging inflation (i.e. debasement), then there is no point in holding it anymore. So, you spend it out of existence. After all, what is the point of saving dollars if $100 in 2000 is now worth $50 in 2022? This is how hyperinflation sets in. So, Wolf’s comment about people spending a lot of money despite raging inflation could be amended to read people are spending a lot of money BECAUSE of raging inflation.

Personally, I don’t believe the U.S. will experience hyper-inflation, but holding cash is getting more painful these days. That being said, as I have stated many times, if you don’t keep some powder dry in the form of cash or near-cash, then you will miss some “once in a generation” buying opportunities, whether it be in the stock market, the housing market, etc.

Agree.

Does CBDC throw a monkey wrench in this thought process?

Inflation is the economy’s way of saying your money supply is greater than the quantity of products and services available for consumption, and is a function of income inequality. The bottom 80% are not driving inflation. They’re following it.

We’re testing our hypotheses against those historical inflationary periods for which we have adequate data, however marginal, and so few it’s unlikely we could ever raise it to the status of a theory. That paucity is the likely result of economics having been relegated to the role of public relations service for the Financial Industrial Complex post-WWII. Our modeling confirms our earlier supposition that interest rate and QT policies will be quite unable to either reduce inflation to moderate levels, say, 2%/year, or to prevent severe recession.

To say that economics is a soft science is an understatement. It’s positively squishy because there’s so many variables and non-linear relationships.

World population is expected to exceed eight billion next year, mostly people who need too much and aren’t going to get it but also including a couple of billion who want too much and aren’t going to get it. Crop failures are projected to double two or three times in the next few years with no prospect of eventual recovery. My selection of Dirges commemorating the Coming Population Crash includes ‘Would’ by Alice in Chains and ‘Whipping Post’ by the Allman Brothers.

People would be well-advised to focus their purchasing on productive items conducive to collective survival in isolated cooperatives, but hey, I’m not going to tell you what to do.

Sometimes I feel like I’m dying…

Una: ”To say that economics is a soft science is an understatement. It’s positively squishy because there’s so many variables and non-linear relationships.”

Is very polite, but the stone cold hard fact is that economics is exactly the same as other ”social sciences” are not science at all, same as it was when I got my degree in such stuff 50 years ago, mostly just listening in class and parroting back the same stuff on tests/papers, etc.

All of them are simply aggregated opinions that have received the blessing of whatever/whoever is the current pope and similar.

The very clear and equally abject recent failures of reality results of actions of FRB and it’s plethora of PhD. type folks is a stirling example.

The equally dismal results of ”criminology” ( as opposed to criminalistics) is another glaring example.

”Psychology?” HAH!

‘”Psychology?” HAH!’

The disciples of Edward Bernays have you exactly where they want you, in line for your exsanguination. And just because that science-y stuff confuses you doesn’t mean it’s wrong.

This post, and in my opinion, often Wolf’s thesis, overlooks the supply shock caused by covid 19. I still think that this blog understates the effect of the supply side of the equation, and I still expect the supply shocks to be transitory, to resurrect a much maligned term from 2021. When I can walk onto a Honda lot and look at current models, and buy one that day and drive off with it, I’ll be more interested in what the inflationary mindset is responsible for. At this point I still believe that the pandemic, and the supply disruptions caused by it, as well as the pent up emotional YOLO mindset as a result, are all far more interesting than the inflationary mindset.

Agree P:

Some ”stuff” temporarily high and higher and higher, far damn shore…

Other stuff may actually seek and find new lows, low prices and low availability, as we are seeing, ”sometimes” and with some goods.

Later, as we saw very clearly in the after effects of the gas/oil shocks 50 or so years ago,,, some products were no longer available at any price.

If retail sales are up 1 plus 8.4 equals 9.4% then we are just keeping up with inflation. Kinda like we are in denial and just buying like always. At some point the credit users will hit the limit and then we slide toward less buying. I have a barometer. 2 relatives did a major kitchen upgrade last year at 50k and 70k. They rationalize that home prices will always go up and home equity loans are cheap. Ironically they can’t cook much differently than before, but they are keeping up with trends – black cabinets yuck. Bottom line, people like to spend, it makes them happy. At some point it won’t be so easy. Then I shall buy good stocks at low prices. I think it will be October.

Uh oh, I should have read Wolf’s replies first.

.

.

.

Red hot iron takes a while to cool.

Expect the chill to be noticeable in October, as rate increases and QT start to bite.

.

.

.

1/3rd of all dollars were created from the founding of the currency until the GFC. The next 3rd were created from the GFC until 2020. The last 3rd were created in the last 2 years… Again, 1/3rd of all dollars were created in just 2 years!

It’s going to take more than a few months to burn through enough cash to see a cooling of inflation, a meaningful reduction in job openings, and thus a chill in the economy. At the end of the day, the money supply has to be suited to the size of the economy. Rate hikes and QT will continue to make markets wobbly, but to see fast results in consumer spending, the Fed would have to deploy their balance sheet’s anti-dollars much faster than they’re planning to.

“Again, 1/3rd of all dollars were created in just 2 years!”

No wonder you have raging inflation. And still the dollar is so strong it’s crushing everybody else.

Why would they do that?

Perhaps Our Illustrious Blogger can explain.

You wouldn’t like my explanation because it’s going to come off like another doomsday scenario.

Hoping BRICS+ changes that!

I would remind you of the asian financial crisis in the nineties and its’ relavance to today’s situation. Then ask yourself if the FED sees this as a feature or bug.

Unamused said: “Perhaps Our Illustrious Blogger can explain.”

———————————–

Yes Wolf, we really do need a primer on money supply. In these comments, “Not Sure” is claiming 15 to 20 trillion created in the last couple of years and 45 to 60 trillion existing. Much larger than other estimates.

The good news is that with retail sales being so strong, with inflation at 9.1%, with so many jobs being available, that interest rates will at last start to go up at a decent rate. I would like to see it up to 6% as soon as possible and up to 9% by Christmas. Only then will sanity arrive.

Speaking of sanity, food prices. I was speaking to a member of the staff at my local Lidl and on average they have put stuff up around the 25% mark for the last year. Most of the food I buy has gone up at least 25% and sometimes more and that is before the effects on this years food supply. I know, as I’ve lived through it before, that inflation is a beast that is very hard to control and has to be beaten down very hard.

As inflation is so high around the world, it has to be stopped, I can see the same thing happening as of the 1970’s and that is assets stop rising. They will stay flat for long periods, maybe ten years at least. So, the wealth created by the stock market boom will have to stay flat for the same ten years. Get used to it. It’s coming to a country near you.

Just to point a small thing out… Retail sales are up, the stock market, Crypto and house prices are down.

Oh, I don’t know if it means much but many of the farmers in the USA are very twitchy this year, in many ways similar to the 1930s.( a period, as well, where the Germans and the Russians hated each other…go figure) Hopefully not like the 1930s…but life is often ruined and run over by cycles. lol

Anthony wrote:

“Retail sales are up, the stock market, Crypto and house prices are down”

House prices are not down yet – at least not in the USA.

Wolf,

If the yield curve gets inverted, does that mean that FED does not roll over the long term bonds/mortgages fast enough? Could it be that after the QT goes full speed we would still see inverted yield curve?

Inflation doesn’t reduce spending in fact it increases it.

If your ice cream is melting you eat it ASAP, you don’t wait until it’s completely melt.

This is a very American attitude. Also why can’t you put the ice cream in the freezer so you can have it next time?

Muppets.

Cuz you can’t freeze inflation?

Well you can do one better. You can stop buying!!! And then there will be demand destruction. And then prices would come down.

Brilliantly put, even if SocalJimObjects won’t accept ti.

Wolf: I RTGDFA twice. You did not address the issue of nominal vs real retail sales. Even Robert Hughes at AIER (MA in Economics among other qualifications) clearly stated today that real retail sales has decreased, although he did deflate by CPI. You have a very compelling point that nominal retail sales cannot be appropriately deflated by CPI, but there has not been a compelling argument presented that nominal retail sales should not be deflated to determine if there has been a decrease.

I think Wolf’s point is that once you break out sales to individual components and you wanted to show deflated and undeflated figures then you’d need to show deflated figures deflated with that specific component’s price index, rather than comparing to overall CPI which is what so many commenters are suggesting.

“you’d need to show deflated figures deflated with that specific component’s price index”

And where do we find these inflation figures for specific components?

Inquiring minds want to know!

Ben,

There is NO DATA to show if inflation in the specific goods that make up retail sales was higher or lower overall than sales growth. People who try to show that are making stuff up.

So we cannot say whether in real terms retail sales rose or fell — and that’s not even the job of this data. The job of this data is to look at retailers, not consumers.

We’re going to get consumer spending data that is adjusted for CPI. We just have to wait for that.

We do know from this data here that consumers spent a shitload of money.

All this demonstrates just how far behind the curve the Fed is…..

and the foot dragging suggests they foster this condition.

Quite a recession with restaurants packed, hotels and resort areas packed, warm weather destinations for the coming winter full. In the areas I would entertain moving to, little inventory and still fully priced.

House replacement costs still extremely high.

As for the Fed…..

“Procrastination is irresponsible and likely deceit.” D Bonhoeffer

“It is absurd to put important decision making into the hands of those who pay no price for being wrong.” T Sowell

“In a system that boasts of “checks and balances”, who checks the Fed.” Me

historicus wrote:

“House replacement costs still extremely high”