Amid shortages, exploding prices, and long lead times, there are now the new realities of a turning housing market.

By Wolf Richter for WOLF STREET.

Shortages of all kinds, exploding prices, and long lead times have waylaid the construction industry since late 2020 and have grown into a crescendo of disruptions in 2021 and in 2022. We’ve been reporting on it, and homebuilders have been complaining about it in their earnings calls, and commercial property developers have been screaming about it and practically wishing for a recession to end the shortages, price spikes, and delays. It has been a mess.

Professional home remodelers.

And there is another aspect to this: Professional home remodelers, and how they’ve have had to adapt to the pricing chaos and shortages – and what risks they might run into under these conditions, as the housing market has begun to turn amid spiking mortgage rates.

In a survey of professional home remodelers – not DIYers – independent research firm John Burns Real Estate Consulting found that they confront the worst shortages and longest lead times with appliances, windows, and cabinets: 64% of the surveyed professional homebuilders said that it takes over 16 weeks to get appliances. Another 12% said it takes 12-16 weeks to get appliances (in total, 74% said it takes 12+ weeks to get appliances):

| Home remodelers said lead times for: | 12-16 weeks | Over 16 weeks | Total over 12 weeks |

| Appliances | 12% | 64% | 76% |

| Windows | 31% | 39% | 70% |

| Cabinets | 33% | 38% | 71% |

| Doors | 28% | 23% | 51% |

| Plumbing | 21% | 11% | 32% |

How they adapt to “the wild housing market conditions.”

John Burns asked the professional home remodelers how they are adapting to “the wild housing market conditions,” and then highlighted the top seven most common responses.

- Remodelers are raising prices in response to rapid material price inflation, a dire labor shortage, and extremely long backlogs of demand.

- Faced with unprecedented product lead times and unpredictable delays, remodelers are ordering materials earlier, long before work begins.

- Remodelers are becoming logistics and supply chain experts, as large projects require extremely close coordination with vendors, subcontractors, and clients.

- Remodelers are pushing project start dates out later, while they wait for products and materials to arrive on-site.

- As remodelers navigate unexpected delays, many are now filling in scheduling gaps with smaller projects to keep cash flowing.

- We see worrying signs that remodelers are stocking up on materials when prices could be peaking and demand could be slowing, setting the stage for potential deflation in building material prices.

- Remodelers are putting homeowners on the hook for unexpected price increases by shortening quote windows, adding strict escalation clauses, and rebidding materials before signing agreements.

In light of the turning housing market, the #6 item is particularly interesting: that professional remodelers are stockpiling materials to deal with the shortages and eternal lead times just when prices of those materials “could be peaking and demand could be slowing.”

Three major risks for pro home remodelers.

Given these strategies to deal with shortages and exploding prices as the housing market is turning, John Burns identified three major risks for pro home remodelers as they head into the second half of 2022.

Customer sticker shock and push-back: “Customers are seeing massive price increases from remodelers, and they are starting to push back. Watch for more projects hitting ‘pause.’”

Vanishing backlogs: “Some remodelers are now taking deposits for 2023 projects. However, if home values soften or decline, some of this future demand could vanish.”

Spiking mortgage rates: “In the short term, rate spikes threaten homeowners’ ability to tap record-high home equity and write large 5- and 6-figure remodeling checks.”

Cash-out refis at holy-moly mortgage rates to pay for remodeling projects?

I call them “holy-moly” mortgage rates because that’s the sound people are making when they try to buy a home at current prices and figure the mortgage payment at current mortgage rates.

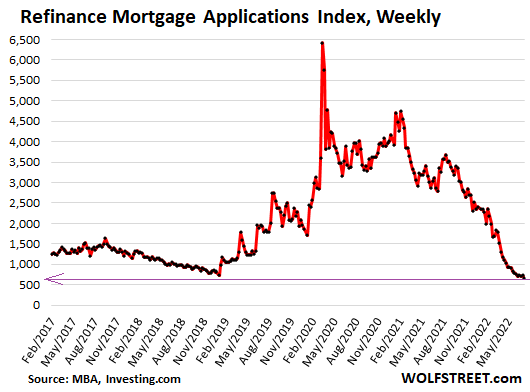

These holy-moly mortgage rates have caused mortgage refi’s in general to collapse – entailing large-scale lay-offs in the mortgage industry because a big part of their business has vanished. Applications for refi mortgages, according to the Mortgage Bankers Association, have collapsed by 76% from a year ago and hit the lowest level since the year 2000 (data via Investing.com):

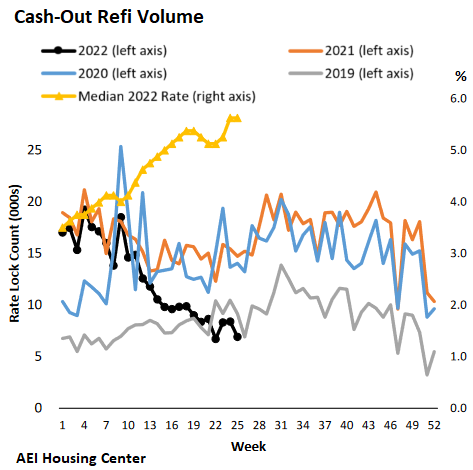

And these holy-moly mortgage rates have also caused applications for cash-out refi’s to plunge by 53%, from a year earlier, according to the AEI Housing Market Indicators for June, because who’d want to refi a 3% mortgage with a 5% mortgage or a 6% mortgage to draw $200,000 out in home equity?

If an existing 30-year mortgage with a balance of $500,000 at 3% is refinanced with a $700,000 cash-out refi mortgage at 6%, the payment is going to nearly double from $2,108 a month to $4,197 a month. And for most people, a doubling of the mortgage payment would be a no-go zone.

So if homeowners have to do a cash-out refi to pay for their remodel project, that remodel project is in serious trouble.

If homeowners can pay for it by drawing on their much-diminished brokerage account balances, maybe OK. Or maybe they’ll take out a margin loan, relying on the next perma-rally, or whatever, so that they might get margin calls in the middle of their remodeling project, which would be an additional marital stress test to overcome.

But if homeowners have the cash sitting around, earning 1% to 3%, or nothing, they might plow it with good conscience into the remodeling project.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I had deck repairs that needed to be done and I could find on one firm ready to bid. The price was about double what I expected. But there was no alternative.

DIY comes with bragging rights.

And a little more money to do some extras to make it nicer….

If you don’t do it yourself you run the risk of forgetting where you live, and then you wander about and somehow land in Macao in a run-down office writing articles for stodgy British journals that nobody reads until you fall in love with a moonfaced Oriental who dumps you for a rude Italian and you end up hanging yourself with your typewriter ribbon.

I must know ten guys this has happened to.

unamused

same ole story /s

@unamused

!

I recently looked at some appliances

EVERYONE SAID – in stock or week to 10 days out their warehouses

only SPECIAL ORDER taking long time

year ago – I had to take what I could on floor

——–

most other items are in huge stock and price increases to match(ie huge)

also hearing AMAZON and HOMELESS DEPOT cutting hours for workers

@Joedidee – I am doing some DIY projects and made multiple trips to HD. I noticed the cash register girls were standing out in front looking for customers to checkout. My buddy is building a house in San Antonio and he said their HD is still really busy.

You can tell things are getting tough by the number of opened packages you see on the shelves. I was at Home Depot the other day and saw several small packets of screws where a “customer” opened the package and pulled one or two out, free of charge.

You know trust and sentiment is really bad when you see the same thing happening at Dollar Tree, and I saw that as well. Somebody couldn’t afford the $1.25 for the complete package, so they opened the package and pulled a few out.

Interesting how this world is turning dog-eat-dog. When scammers and speculators are rewarded at the expense of hard-working folk, many of these hard-working folk wise up and turn into scammers and speculators. Blame central banks for upsetting generations of long-standing trust and civil behavior.

I fortunately found 8 4×4 pressure treated 10 ft posts for $3 each at a garage sale! Pulling out broken cement encrusted fence posts was the hard part. The ‘hard part’ is definitely an understatement!

I find tractor works well for some work

Missing the tractor, I found a high lift jack did the job!

Have you tried using a car jack to pull the posts?

Yes, the high lift jack 😊

Buy a miter saw, a drill, and a hammer, then watch a youtube on deck repair. You got this!

Planning to have floors installed at 50% discount 6-9 months from now.

Sotto voce: I’m considering the same timeline for the replacement of a couple of appliances.

And I’m keeping my voice down because I don’t want my current appliances to get any ideas.

Starting to think the appliances read wolfs articles! But fortunately, most of the faulty parts were easily obtainable.

Parhaps better to get appliances now. Before they placed you on 9 months wait list. You can even get good discounts still.

Andy

I am a Builder and something to consider :

As Example Redwood rots out like most all wood in a very few years.

( about 3 Decks every 15 years becomes costly )

What I suggest is a Concrete Deck not a wood deck build it once and forget it short of a major Earthquake .

Cost is the same I have found you need Galvanized Steel Ventilated Decking Supported about every 10 Feet ( also Galvanized Steel edging )

( I use steel I Beam / on Metal Poles cemented into the ground )

Most Places you don’t need any permit as long as its not attached to the Building /House ( just leave a 1 inch gap between or so) Is called a Raised Platform most often less then 36 inches in Height .

I Use Mixed on sight poured right from a Cement truck and use 12 inch Lag bolts every 3 ‘ along the sides to add on 4X4’s later to support a railing afterward .

You can finish the deck in many way’s Like a Cement Dye , Slate or other Tile, and so on . Don’t forget to have a 1″ or 1.5 “drop off to the edge for every 12 feet or away from any building

on the sides to attach

I was on a condo board of directors. We had a problem with our concrete balcony steel hand rails and rebar in the concrete rotting. Even though most of the balconies were in good condition, there was risk of us getting sued if the bad ones failed and someone fell. Our management company could not find matching steel handrails. We got an architect to design new balconies with trex decking and rails over the existing steel I-beams. The cost was less than half the price of new concrete balconies. Trex deck boards are like dense plastic, it does not rot, or need painting.

“Trex deck boards are like dense plastic, it does not rot, or need painting.”

David,

Sunlight kills Trex…they will eventually split and swell.

My parents put in trex and within 1 year it was discolored. They did not stand by the product. 50k wasted. Parents too old to fight them. F trex!

Installer was shocked they didn’t warranty the product.

I looked up trex composite decks. The newer trex does not fade as much. They claim it will last 25-30 years. Painted or stained wood needs repainting in less than ten years and it fades. The wood splits, cracks and rots.

Check carefully if a product is made from UV stabilized plastic.

Curiously, Home Depot claims Trex is UV-Protected but nothing shows up on the Trex website anywhere in a simple search.

It’s an important feature!

Sounds like if you are a professional remodeler it is time to finish out the jobs you have on the books with a skeleton crew, sell everything you can ( especially the big trucks, trailers etc) and head for the bug-out cabin in the hills.

Do you think it’s going to be that bad?

Yes.

We did a first floor bath remodel last year and it took the contractor 5-6 months to get to us. Been wanting to remodel another bathroom but plan on waiting it out as contractors are far and few to come by and prices have gone up.

You are best served by picking a reliable honest contractor, paying him a fair price (what you consider outrageous), and giving him the time to do the job. Consider a substantial performance bonus – ~20%, but there may be a lot of arguing later over that. Be specific. What you think would take a few weeks turns into 3-9 months after permits, worker scheduling, supply deliveries, etc.

I usually buy the main supplies myself and have them ready on site Contractors don’t like that (they lose markup) but you give them veto on purchases – no problem if you buy the best ($1000 faucets, I hate petty maintenance).

If you don’t give the contractor the time, he will be forced to put whoever shows up for work on your job. You want the good guys who you watch doing professional work. And then you must accommodate their schedule. The guy doing the marble work in my bathroom had an expecting wife. I had to work around his health care activities which delayed things weeks but he was worth it. Then he was sent to a priority job in another state for 2 weeks. The contractor, trying to speed up the job sent over some replacements. They were bozos – walled over the cutoffs, overlaid the cementboard wrong, I insisted it be torn out and redone – more delay.

It is true. You want fast, cheap, and quality. Pick one.

Or learn to do it yourself. There are so many ways to educate yourself now. All I had were do-it-yourself books. Go slowly, practice stuff like soldering plumbing, buy quality supplies. Measure 3X cut 1X. You will be surprised how many tools you accumulate. But learn while you are young. It gets hard if you are old.

My contractor ordered our SubZero frig and freezer in May 2021. It is just getting installed today – July 2022!! And SubZero is made in USA too

Yikes. Which model did you get?

dont remember the model… 24 inch fridge with 18 in freezer – side by side

Probably 42″ classic. Nice.

I’m in planning stage for kitchen redo and thinking about similar (42 or 48 classic depending on measurements). Thanks for heads up on the wait… I put Subzero in a kitchen I did years ago in another house and loved them. Back then, it was like “when do want them?”.

Contracted for a Tiki Bar July 2021. Received the SubZero undercounter beverage center and sink in September. Still waiting on the Tiki Bar.

I did a full remodel of my rental in 2009 for about half of what it would have cost me a few years prior. People in the industry were really hurting and materials were dirt cheap.

Also had friends selling RE and mortgages and man were they hurting. A few left the state (Ca).

Predicting a similar outcome this go round.

I sure hope so! It all needs to crash down so bad that there’s a Congressional inquiry / post-mortem:

1) $11T in Fed & Treasury debt in 24 months is gonzo crazy!

2) Rent & Mortgage forbearance is gonzo crazy!

3) 2.66% 30YFRM is gonzo crazy!

4) Houses doubling in value in 3-4 years is gonzo crazy!

5) Lumber prices at $1700+ 1000 bf is gonzo crazy!

6) 6/3 romex wire at $6.50 per foot is gonzo crazy!

7) Lead times on windows 3-4 months is gonzo crazy!

8) A slow-poke Fed being a year behind schedule taking action is gonzo crazy!

9) Median price of houses sold at $428K is gonzo crazy!

10) Average price of a new car over $45K is gonzo crazy!

What’s not gonzo crazy is 9% inflation and watching 30YFRM jump 2x in four months as a reaction to all this chaos.

History lesson: Inflation was 9% when Volcker took over in Aug 1979 and the FFR was already at 10.5%. So, JPowell is upwards of 8% behind the curve as of Wednesday. Would love to see CPI push past 9%.

It’s a clown show.

We will soon find out if the inflation was caused by money printing or supply chain etc. If prices crash at 2% FFR way below inflation, then the culprits are the Fed and the stimmys. Otherwise, it’s structural and we’re screwed.

We’ve already found out that the crypto and stock market wealth was fake.

You understand how big $11T is right? That’s more than two years of federal spending on top of the usual $4.8T that would have otherwise been spent without the pandemic. And all of it hasn’t been spent yet. There are parts of the pandemic spending that will take until 2028 to be spent. In addition, Congress just past another $1T in infrastructure.

This was a global situation, so there’s going to be global pressures on higher inflation and central bank yields. All of this was created by the Fed pushing down yields. Now, counties across the US are flush with cash from sky high property taxes. And we all know how slow property taxes are to fall. This is baked in inflation for at least 3-4 years.

Janus

Its the Fed.

The inflation “pull” caused any bottlenecks IMO

Ports moving more than pre pandemic according to a Phil Gramm WSJ article

The Congressional inquiry will find that it was all the fault of black people buying homes. Like they concluded the last time. Can’t be wall Street or the Fed, no sirree! Not my current donors!

Questions will be asked. Lies will be told. Millions will be pocketed. Pitchforks and torches will be raised. Nothing will happen. Life, such as it is, will go on.

I hate doing all construction / maintenance related work – and I can (reluctantly) afford what is being charged nowadays, but I’ve become a DIYer in 2021 and 2022 – man’s got his limits !!

My WTF moment was when a friend of mine PMed me out of the blue in the middle of 2021 asking if she should get a compound miter saw or if a cheaper one would suffice for her DIY home projects. Given that both her and her husband are white collar finance/IT folks and, based on her own words a few years prior, never held a hammer in their hands before, it was quite … alarming to see it.

I am postponing all home repair and remodel projects as long as I can.

1) US10Y futures price weekly backbone : Jan 1 2001 hi/ Jan 22 lo //

106.16/103.20.

2) Price osc around 2018 low at 118.09. It peaked at 140.24 on Mar 9 2020. Options :

3) Drop to the BB.

4) Breach the BB, form a setup bar and a trigger < June 2007 low,

at around 100.

5) If correct, inflation cont.

6) For entertainment only.

It’s a horrible time to get work done on a house. If the work is not urgent, then wait until things cool down and probably you’ll get a bargain. We had to do three items in the past two years and got high prices on all of them. Additionally, one contractor was really bad, but he was the only one who responded. That project got done, but it was unpleasant if I could have waited I would have.

It would be highly disappointing if the one project completed wasn’t a surly Scottsman banging a CAUTION: WELL sign into the ground with the back of a shovel.

What’s going to happen to HGTV and the Discovery Channel? I guess they can always fall back on CNN until its ratings hit zero!!!

They’ll go back to the “Design on a Dime” formats.

People do projects on their homes, even when the economy is in the sh!tter. They just might not be as grand. I did have a home interior painted during a horrible market (think a steel town in the early 1980’s). The contractor was an artisan house (did concert halls, museums, faux finishes, etc.) but had no work…. so he bid the job for cost just to keep his guys working. And I have to tell you… these were the best painters you could imagine. The older guys were impressed that a young guy (me) was interested in their craft, so they showed me the tricks of the trade. Was a valuable lesson.

Cool!

If they keep pushing shiplap and barn doors, I’m gonna go postal.

You have to belong to the union.

In the example, a $500k mortgage at 3% was traded for a $700k mortgage at 6%, so the mortgage payment doubles. However, that assumes the original mortgage was extinguished.

I wonder if there is a way for people to keep the $500k mortgage at 3%, then get a home equity loan for the additional $200k. That way, borrowers retain the benefits of the original low-rate mortgage.

HELOCs died out in recent years, and some lenders stopped writing them because there was no demand. But this situation may revive them.

HELOCs, like refis, are more difficult to get when home prices fall and home equity declines and becomes uncertain or vanishes.

We’re going to get q2 HELOC data pretty soon, and it will be part of my consumer credit update. I expect HELOCs to rise from the ashes, but maybe not. We’ll see.

I just got a HELOC from BECU [Boeing Employees Credit Union] for 500k, in case of any emergencies.

Also was the offered same deal from WAFD.

So they are out there. The banks have to loan out money somewhere and as was mentioned first mortgages are dead.

Yes, they’re out there, but demand for them has died, This is through Q1:

Banks are gearing up to offer HELOCs again—precisely because cash-out refis no longer make sense for remodeling/repair projects at the higher rates. Not sure if the new activity will show up in 2Q reports though.

Struggling loanDepot to cut nearly 5,000 jobs in 2022.

More ignition!

Collapse of the refi mortgage business is tough for specialized mortgage companies. 60% of their business just vanished. We already had one of them file for bankruptcy (in Texas I believe) in that space.

If you’re taking on debt to do a six-figure remodel, all I got to say is best of luck!

After my last car purchase in 2014, I’ve tried to stay away from debt. Just credit cards paid off at the end of the month for points and apartment leases, usually with caps in case I need to cancel. Steadily paying off student loans to zero, would have paid them off sooner but interest rate too low.

Taking on debt for consumption during good times is dangerous. The hedonic treadmill means it’s never enough.

The Fed has everyone trained to make decisions based on easy money. My parents did expensive upgrades to their home, but only after they paid off the mortgage.

It’s flipped around as the winners have been those that went all in on leveraging up their house and installing the latest kitchen and bath upgrades.

The pandemic economic shutdown led to the money drop that led to inflation that is leading to a hard landing and shouldn’t have anyone with taking on debt for consumption right now.

Paid off my mortgage twenty years ago. Never borrowed for anything since then, never will.

I finally got a contractor (through a personal friend). Took out a revmo, got a generous appraisal, and I put the remodel money into a brokerage account, where it gets 1 1/2% overnight rates. The remodel costs should follow housing prices. If need be I can pay down the revmo with a portfolio loan, while both assets are working for me.

Math sounds very fuzzy…wishful…

All these houses that people bought sight unseen and uninspected for more than they’re worth are going to need work. Either to sell or to change to suit the buyer’s dreams, and then they get sold anyway. Because nowadays they’re also a piggy bank. Nobody buys a house and just lives in it as it is anymore. This article is mostly about remodeling on a scale so as to possibly require a cash-out refi to pay for an individual job. That implies remodeling companies that are big enough to make strategic purchases of their bread-and-butter construction materials to ensure future availability for smooth continuity of work completion and incidentally hedging against inflation. Like the airlines that guessed wrong on jet fuel futures, they are buying at the putative top and are likely going to eat the spread if they can’t shove it off onto their customers. These big remodelers are going to see their work load diminish as homeowners can’t afford them at these monthly mortgage payment levels and go back to small cosmetic projects they can diy from YouTube, goof those up, and call someone like me to bail them out. Or the remodelers will concentrate on a lucrative niche. Or stop doing finish work that opinionated customers and rework make unprofitable. But they’ll lay off the guys they can get along without and those are a mixed bag when it comes to unsupervised work. That won’t stop them from undercutting each other and the company that just canned them. Big contractors always pull in their horns, do smaller faster jobs, get paid and hide it, let the deer lease and the fishing camp go, and wait for conditions to improve. At some point frustrated homeowners may cut their losses if they can afford it and presumably some will lose their butts if they can’t. The assumptions buyers made about maintaining and improving real estate for appreciation in the market are all out the window now. But there’s never been much certainty in real estate unless you’re just living in it, and Nature doesn’t pick you to bone on any given day. I restored Victorian and prairie style houses in Dallas for a while, they were well designed and comfortable dwellings as built. Modern houses are often boring architectural dungeons, there’s a sameness about them that makes me wonder why they cost so much. Traditionally you only got your money back out of certain specific remodel jobs when you sold your house, others wouldn’t contribute to the value. Now, who knows? If remodeling pays it’s way at closing, those companies will keep getting called, even at highwayman prices.

yep, buyer bought next door to me sight unseen, paid top dollar (850k) and has since had to get a bunch of work done, including adding a deck which cost 20K per the permit and took quite a while. And there aint any good paying jobs where I am either – I rent my house for 1100/mo!

What size was the deck?

It’s not the size of the deck that matters, or so I’ve been told…

Permit for deck?

Schedule job for public employees holidays.

Until they come, red tag it, and force you to tear it down.

I did a similar thing years ago in suburban Philadelphia. Built a deck in the yard without a permit. The township came by and tagged it. I called them and set up an appointment. I removed two boards and showed them it was not connected to the structure. I had photos of the footings (freeze thaw).

They thanked me and left. The saving grace was that it was not connected to the structure (which I did for water control / siding integrity) which was then a “raised platform”.

I did have to pay for the permit, however. I think it was $35 as there was only materials involved…. no labor.

@rick m:

Your post would have been much more readable had you broken it up into multiple paragraphs.

This iss a point I have made before

This time the housing bubble IS different

replacement costs are skyrocketing

but copper and lumber suggest that may change

the trades is where the money will be

and schools that train electricians carpenters and AC and Furnance

Who is fixing all the Blackrock and Blackstone properties?

I agree but it does not matter things have skyrocketed in price. what matter most is mortgage rates and affordability.

Once the cheap money is gone, things would come back to earth.

Only if Fed does not pivot!!!!

Decent pay,decent work

Why do you keep saying holy moly? Rates aren’t that high at all.

RDGDFA

“I call them “holy-moly” mortgage rates because that’s the sound people are making when they try to buy a home at current prices and figure the mortgage payment at current mortgage rates.”

What’s RDGDFA?

I seek only information.

“Read da got dam friggin’ article”

Oh. Okay. Thanks.

It’s like RTFM, except with more emphasis.

My ignorance is reduced infinitesimally. No shortages here.

Sometimes you have to study them. Well, not you personally.

We’ll have to watch reruns of “Flip this House”.

I dated a super re-model, she had a lot of work done.

Good bones tho.

In my humble hometown…

Lead times are still huge – spec type/quality:

trusses – 10 weeks

doors – 8 weeks

trim – 6 weeks for hardwood

windows – 14 weeks (just for white vinyl single hung)

garage doors – 10 weeks

Fixtures, pipe, wire, equipment, siding, shingles and appliances are much better, almost normal.

Builders have warehouses of supplies – can’t board up a new house.

Custom home completions remain below demand due to these scheduling concerns. A wet spring shortened the season too. People are giving up and pushing out to 23′. Absent a major shock causing cancelations, the quality builders are going to be slammed next summer too.

However, there’s much less spec going up and some early spring completions sitting at 2021 prices.

I’m pushing ahead with about 50% of the projects we’d like to tackle. It’s gonna slow down, but not soon enough to put off everything.

thanks for the input

what region of the country?

I bought an older house in 2018 that needed lots of projects, and I had no problem getting contractors 2018 through Covid in 2020. I was down to a few more projects mid-2021 but by then could not get anyone to do anything if it was less than a $50k (I had two $10k projects, and was willing to do no-bids and pay above rates but no takers).

I figured things would change within two years, so went to DIY for 2021-2022. I have one last project that needs a pro, and I’m figuring that I can get that done easy and cheap by late this year.

Then the old tired house I bought will be totally updated and done, which will mean time to move again.

Was at the lumberyard today (not big box) talking to my salesman.

Lumber has come down from last year. A 2×4 is about $5. but in 2019 that same 2×4 was $2 to $2.50, so still double what it was.

They did a truss package bid for a dead copy of a house built in 2016. In 2016 that roof truss package was $9500. today’s bid: $34,000

that same house had $360,000 in total materials in it in 2016. Today’s bid : $775,000.

I guess it is time to move to Metaverse as the next big thing to do nothing and make $$$. I am going to go buy a bunch of N. Dakota Farmland before Bill Gates does.

I just saw this pop-up in an advertisement

—————————————————–

Upland

Buy, Build, Sell in the Metaverse

Virtual Properties, Sports, and Cars

Become a Virtual Real Estate Tycoon

Earn $$$

6000 UPX Sign-Up Bonus

When a person buys a home they are buying materials and labor from a different pricing era

Yes. Bought a 60 year old house last year. All of the double hung wood windows are fine, but the glazing on the outside of the panes is shot/gone. Last person I saw do that job was my Dad, b. 1921.

Easy putty knife

Shi:

Get some glazing putty and a glazing knife (it has a “v” on one end for shaping the new putty). Clean out the old putty thoroughly. You can use a heat gun to soften the old putty. Have some glazing points handy. Pack the putty with the flat end, moisten the putty slightly, and use the “v” part of the putty knife to smooth it. Let it dry, use a high quality primer painted slightly onto the glass, and then finish coat. The paint on the glass keeps the water from getting between the putty and the glazing. The mistake most folks make is to scrape all the paint from the glass.

It ain’t rocket surgery and an old window, properly maintained, is nearly as efficient as a new one. Key operating word – properly maintained.

A margin loan .. towards a residence. Wow! .. who’d a thunk it.

Didn’t realize he monied desperati did such glib WheelDeal. I know .. timing is Everything, right?

Phools.

Would-be new home buyers are utterly frustrated with rates at their current levels. They are requesting a family member of mine who works in the industry to unilaterally lower their rate because they are certain he has the power to set interest rates. It is now routine for would-be buyers to move through the application process and flake at the last minute rather than finalize their contract – the reason cited is the rate in relation to the monthly payment. Often it escalates to invoking a hail mary and having their real estate agent call on their behalf to plead desperately for a lower rate. Repeatedly headbutting an unyielding brick wall. And that’s the trend coming from those that meet prequalification. An ever-growing number simply do not prequalify. Not that it portends the future, but this is the reality while rates have yet to retread to historical average.

Home sale cancellations are up to 15% and climbing. Not as high as during GFC, but it’ll probably climb more.

Deflation 2023 here we come!

Who has ever seen deflation?

https://wolfstreet.com/wp-content/uploads/2020/08/US-CPI-2020-08-12-purchasing-power.png

Telephone calls are cheaper. I’ve got the handwritten long distance call booking tickets (no direct dial off-continent then) that the post office would send with the phone bill and the payment transfer card each month. In June of 1972 it cost fifty six cents US a minute to call Glasgow from Starnberg in southern Bavaria, Santa Clara CA was $2.28 a minute and Mexico City was $6.57 a minute(FX

rate as of 3/31/72, DM 3.19/USD, 1972 dollars). It’s cheaper now. But I’m not sure if the deflationary effect of technology on communication is the same thing as Deflation as a widespread phenomenon. We had TWX and Telex machines back then too, and they cost so much to operate internationally that you typed your messages in advance producing punched paper tape that could be transmitted through a tape reader over telephone lines to another machine that would type it out on paper at sixty words per minute (Telex) or up to 110wpm on TWX to TWX. All of this to minimize long distance per minute charges. Expensive equipment that had to be leased just like telephones were back in the day and that took up a lot of room and was noisy at night in a quiet house. Seems byzantine now, but we were pretty proud of ourselves for having thought it up, I guess. And then there’s email and landfills are full of Telex machines, IBM mainframe tape drives, dial phones and answering machines. Information and communication are just so much handier now. Possibly too much so for some. Big difference between being smarter and being better informed, or so I’m told by the smarter and better informed.

The reality is that any loans made under current US law are ponzi finance. The bigger the loans you take out, the more that gets inflated away. You can live a lifetime snowballing loans — just look at the very rich, because that’s exactly what they do. Any modicum of responsibility is impossible, since the irresponsible rich would simply never let it happen through legislation. Legislation pushing us further and further into ponzi territory has been increasing for at least the ladt 40 years.

Europe has passed the event horizon, meaning below 0% interest rates on issued debt, so a breaking point is *inevitable* within the next 10 years as the gravity of the black hole starts exponentially crushing them.

Kenny Logins,

People have been saying this deflation BS my entire life. And they’ll never stop. BS is just too much fun. Reality is not. In reality, my entire life, we’ve had everything between inflation and raging inflation. With only a few quarters of mild deflation in between to let us know how good it would feel when the purchasing power of our income finally rises just a tad. I’m just stunned that people can keep up this deflation-mongering BS decade after decade. Don’t you people get tired of regurgitating the same BS and ignore the bitter reality of inflation? Does it make you feel better to daydream about deflation?

Cash out refis and HELOC loans sound suspiciously like ponzi schemes at today’s real estate valuations.

If the government were wise rather than scamy, rates for those loans would be prime + 2%.

I keep seeing the commercials for 100% cash out refinance for veterans by New Day. I assume taxpayer is on the hook if loan goes bad.

If US elected government was really concerned about inflation, they could have reinstituted student loan payments at first of the year to kill some demand. Soon they are going to have the excuse, we can’t restart student loans because we are in recession.

Well, they’re obviously not concerned about inflation because they gave away close to 1 T to small business owners and the wealthy with PPP. How about clawing that back first?

A local remodeling construction company is booked six weeks in advance and is selective in accepting new contracts.

Canadians with ARM loans are worried they might lose their homes. Canada is in an interest rate hiking cycle.

Guys I know personally are telling me:

3 to 6 months in Tpa Bay area DH, the closest to you that I have heard from recently;;;

6 to 15 months in the Tahoe area;;;

6 to 12 months in HI for ”minor” work by well qualified folks,,, and 2 to 3 YEARS for ”major” work including new builds in Kauai…

And you (and I far damn shore) don’t even want do hear about the labor rates now apparently routine.

Gonna bee a very very bad ”crash” this time IMHO…

Will there be a spate of Refi Mortgage defaults in the near future IF and when real estate values tank, and these lenders or their down stream MBS holders are left with negative collateral value and defaulted payments?

Nah, never happen, it will all work out OK.

Most of the MBS are guaranteed by taxpayers. That’s who’s going to take the biggest loss.

But if these are full recourse loans, in theory no one can get out of the debt. Creditors will hound these people daily, and they won’t be able to get credit again, right?

Or is the reality, like always in the US, that the most irresponsible are the most rewarded by forgiveness of debt?

I just purchased 12 x22 Blue Tarps, just to have them on hand if

needed and while still available. I still remember the Tom Ridge scare

from Homeland Security to always have duct tape and plastic sheeting.

Sure as hell people were lined up purchasing these items the next day.

You can make a nice hut in the woods with a chain saw and a tarp.

Remodeling is like any other big purchase, it is all about financing cost and availability and not demand for the underlying service. Back in 2006 I did a lot of business with the motor coach industry ( high end RV’s). The bubble nature of the housing market and interest rates were making me nervous so I slowly shifted out of that market in to medical over the next year and a half. My welding salesman scoffed at me ( motorcoach builders were his biggest customers) because he said that the size of the boomer population the right age to buy motor coaches was growing rapidly ( in 2006 he was right) and demand would continue to boom. But he forgot that people only bought fancy class A motor coaches if they could sell their house for a big profit and/or get a good deal on a loan. A few months later in 2007-2008 our mutual biggest customer in the industry when bankrupt. The owed me $78 at the time and they owed his employer $1,000,000. Large scale ( not DIY) remodeling is the same.

I did quite a bit of building new construction and remodel/additions back in the 1980s and 90’s…. but I worked mostly on a summer resort island. At the time, the north side of that island (north of the Causeway Bridge) was inhabited by mostly seasonal and wealthy folks. The south side of the island was inhabited by quite a few wealthy people, but with a mix of middle class too. In any event, I built and remodeled a lot of homes during those years, but only once did I deal with “financing”. Every job (except for one) was paid for by the homeowners… no banks or finance companies involved.

Today, that entire island is loaded with wealthy people, from the north end to the south end and homes sell for in the millions… even the tens of millions. And the builders are busy… one told me, “The customers are not even looking for bids… they just want to know if and when we can begin and complete the job”.

My point is this: There are more wealthy people in America than ever before and for them, financing or interest costs are NOT a problem. You need to find the market. They are all over America.

However, the fact that cash is no longer “trash” may put the brakes on some of the spending by the wealthy… they do hate to dip into the principal and prefer to spend some of the earnings instead.

Suggest YOU and any similar ”legitimate contractor” become well or very well acquainted with the concept of ”Builder’s Control” as was the very best way to get paid back in the days when money was more or much more costly and hard to get than it has been the last few decades.

Builder Control IIRC was a very clear system where ALL the money for a project was deposited into ”Escrow”,,, and the bank loaning the money for the project had a ”professional” who would come to the project, see the progress as noted on the contractors pay request, and sign off…

Was a really great thing for contractors whose clients might not have had the best credit when their projects ”penciled out”…

SoGen analyst said that the speed of all the price drops (Stock Market and Bond Market drops), Soft Commodities (Wheat, Corn), and energy (Oil and Nat Gas), metals (copper and silver), inflation will drop but now there is fear that we are at the beginning of a recession. They see the FEDs interest rates back at 1% early next year.

The drop in stocks is the worst from the beginning of the year since 1932. It was the worst until last weeks gains in the SPY. Also the bond rout is the worst drop since 1880.

Fed is doing a pretty good job at knocking inflation down fast.

Sounds like there are a few concerns in this big drop in everything. –

“Faster than expected changes to the federal funds rate could stress the economy and financial markets, with steady and well-communicated increases preferable in the current uncertain environment, Kansas City Fed president Esther George said on Monday.”

“This is already a historically swift pace of rate increases for households and businesses to adapt to, and more abrupt changes in interest rates could create strains, either in the economy or financial markets,” said George, who dissented against the Fed’s larger than anticipated three-quarter point rate increase in June.

rue82,

“The drop in stocks is the worst from the beginning of the year since 1932. It was the worst until last weeks gains in the SPY. Also the bond rout is the worst drop since 1880.”

I already explained that this was just a coincidence of the calendar because the S&P 500 started dropping on Jan 4. During the dotcom bust, it started dropping in March, and by July it was only three months into the decline. Now we’re 7 months into the decline. There were a LOT OF declines where the S&P 500 dropped 20% a LOT FASTER than in 6.5 months, including in March 2020, when it dropped that much in just a few days.

Hoping the the next stock market drop to send the SP500 to 3400 and pre-covid price. That would wipe out another $5 to $6 trillion of wealth in the stock market and total stock market value would be around $33 trillion. 33 Trillion is still almost 20 trillion higher in value than the 12 trillion stock market valuation in 2010. But $14 trillion of stock market wealth has disappeared from the peak of $53 trillion a few months ago.

The it will be interesting what the next steps will be for the FED if we get to that value.

The U.S. stock market after losing $14 Trillion in 8 months, and the Cryptos losing about 1 trillion, I thought we would see a few more Hedge funds in trouble but they must have set up good hedges. LOL

If that happens, the Federal Reserve FOMC will be quite encouraged and satisfied that their jawboning has been so superbly effective.

I am skeptical of this one “We see worrying signs that remodelers are stocking up on materials when prices could be peaking and demand could be slowing, setting the stage for potential deflation in building material prices.” What remodeler has a warehouse to be storing bulky building products, even home depot uses outside distributors to story their lumber. Or the balance sheet to carry the working capital.

I’ve worked for contractors for a long time. In the US only in metropolitan New York and on government jobs has materials storage been a real issue for anybody I’ve known, and doing service work in Manhattan is such a pain that you have to charge exorbitant rates to ameliorate the hurt, and that solves the problems that can be readily solved anyway. Everywhere else in my experience builders have always found room for their stash of leftovers, which are usually valuable enough to be worth holding onto, but at a point it stops. Few keep big piles of sheetrock, because it’s awkward and bulky and has to be dry-stored. Or concrete. Or generic tile. Or hundreds of lengths of PVC electrical conduit or plumbing pipe. Roofing stuff. These kind of materials are best left at the supply house until needed. But relatively expensive things like hardware, trim, plumbing and electrical fittings, prehung doors and windows, and the fasteners that any contractor will need on any job are going to be kept, and room will be found for them. Especially these days, if you have to go to the supply house for every little thing as you need it, half of which they’re not going to have, you’re not going to be in business long. And tools and scaffolding and ladders and the rest have to be stored somewhere, and for just a slightly larger storage area a contracting outfit can position itself to respond quicker and cheaper and with greater profitability.