The June sell-off did a job on them.

By Wolf Richter for WOLF STREET.

Manhattan luxury real estate vs. stock market downward spiral in June: In the week through June 19, only 12 sales contracts were signed for condos, co-ops, and townhouses with asking prices of $4 million and above, the worst week since the week of December 28, 2020 (with 10 contracts), according to today’s weekly report by Olshan Realty.

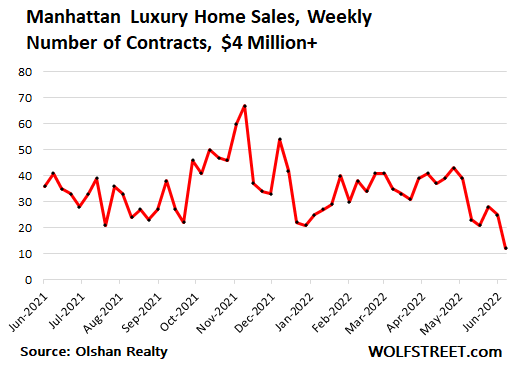

The number of contracts was about one-third of the average number of contracts signed in the prior 52 weeks, and down 70% from the same week in June last year (41 sales).

“This anemic performance coincided with the S&P 500 Index dropping 5.8%, its worst week since March 2020. The S&P has fallen 11 of the last 12 weeks,” Olshan’s report said.

There have been other reports on this phenomenon – though not quite as real-time-ish and as brutal: What is pulling the rug out from under luxury real estate isn’t necessarily the spike in mortgage rates – though that can play a role too by massively boosting the carrying costs of luxury real estate – but the plunge in stock prices that is throwing all kinds of previously taken-for-granted equations and feelings of wealth into uncertainty.

An analysis by Redfin, released earlier in June, found that sales of luxury homes – priced in the top 5% of the local market – during the three-month period through April across the US plunged by about 18% year over year — a much smaller drop than what is now occurring in Manhattan. But the Redfin report was for data only through April, and stocks have dropped quite a big further since then.

“There are only two instances in the past decade when there were steeper declines: the three months ending June 30, 2020 (-23.6%) and the three months ending May 31, 2020 (-21.6%),” the Redfin report said.

The Redfin report blamed the “cooling” of the luxury housing market on “soaring interest rates, a tepid stock market, inflation, and economic certainty.”

The expression, “tepid stock market,” to describe the situation the stock market has been in since January should earn Redfin the understatement-of-the-year award.

And yet, luxury sales in these three months through April cited in the Redfin report hadn’t yet been impacted by the recent sell-off in stocks, including the brutal drop last week.

“The year-over-year cooldown is also a reflection of the market for high-end homes coming back to earth following a nearly 80% surge in sales a year ago,” Redfin said.

Sales of non-luxury homes had dropped only 5.4% over the same three-month period through April, the Redfin report found.

But this was before the recent spike in mortgage rates to 6%. In the three months through April covered by the Redfin report, the average 30-year fixed mortgage rate went from about 3.7% to just over 5%. But in June, the 30-year fixed mortgage rate went over 6%, adding another layer of complications for potential home buyers.

But unlike the Redfin report, Olshan’s data today – the 70% year-over-year plunge in the number of sales contracts of homes priced at $4 million and above in Manhattan – was impacted by at least part of the 11% stock market swoon in June so far.

Stock market sell-offs, if sustained, get a little unnerving for people who have a lot at stake in the stock market, especially if the dynamics point at further repricing of assets as a result of a long and hard tightening cycle by the Fed, which is now belatedly cracking down on raging inflation.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I bet this time around we will break all kinds of records. This one will go to history books. 1929+Japan+2000+2008.

It’s going to be a difficult situation to navigate most likely. A lot of political and geopolitical things coming our way most likely to make it even tougher.

Governments are going to fund themselves even if it takes pretty high real negative rates. My goal is to financially survive whatever comes even if returns are modest.

“My goal is to financially survive whatever comes even if returns are modest.”

Same here..I’m too old (late 70’s) to make it all back again. Almost out of stocks and replacing the stash with fixed income, and the house is free and clear.

Yep. I am spending my retirement savings on a new cherry orchard hoping to be earning inflated dollars down the road. I can’t find any rentals that are reasonable $ anymore. (For farmers, this is like constructing a building for rent, BTW.)

The eyes on the ground in San Diego can confirm this is happening here. Generally speaking, though, anything starting at a little over a million is sitting for much longer and has been forced to reduce asking prices a few times. There is a pretty high end community in the 92115 that sells for big dollars and the one that’s at around 6 mil has been lowered and lowered again for several months now, and sits and sits. This is gonna be the pop heard round the world.

San Diego is toast. People asking a million for 50 year old dumps east of downtown that are in a no go zone when the sun goes down.

Look at pictures of mount Soledad from the 50s. No homes and just barren, like camp Pendleton. Without lots of water that isn’t available that’s what it will look like again. Overpopulated for it’s resource base. I moved away years ago but remember when it was truly a great city.

A college friend moved last year from Tucson to SD… she said the heat was intolerable in the former. But based on the current weather reports SD is only a bit better… and of course she now has the CA taxes to pay. She must be one of the few who went in that direction!

I have very happy memories of a childhood summer spent in La Jolla and then more recent family reunions at the magnificent Valencia Hotel there. I also worked in SD itself briefly around 1999 and enjoyed it. But with the climate change and the water problems (as Iona notes above) I just don’t see it as a place to live any more… perhaps a brief visit for the fish tacos and some tequila :-)

[LOL as I type this I realise I am wearing a T shirt from José’s taco bar in La Jolla!]

LOL the weather within 5 miles of the coast in SD is 20 degrees cooler than Tucson during the summer, that little band where there is just enough fog and ocean breeze to keep cool, but not so foggy you freeze all summer. Inland SD County you might as well be in Tucson.

Problem with living in CA is you hit high state income tax brackets beginning around 100K, and if you are buying a home now, your property taxes will be 10K + per year. Works for very high income I guess. I don’t see how it makes sense for upper middle class to stay there. Retirees with a large portfolio make it work with flexible income from different tax buckets but a working schlub there is working 5 more years than people in some other very nice places to make the same but, unless cashing out and moving cheap to retire.

> SD is only a bit better

Tucson 100+ degrees lately (Phoenix consistently reaches 105-110 and rarely below 90 for hundreds of days yearly) and San Diego in the 70s. That is absurd to claim any comparison. I have lived in SD and Tucson.

Only at 15+ miles from the coast, San Diego is 10 degrees hotter, but not 30 degrees+. That why everyone from AZ who can afford it summers here in SD. Come off it!

In SD I have daily breeze off the ocean a few miles away, no need for AC. Energy bill this month about $20. I can’t imagine what the most minimal bill is in AZ.

Happy1,

Good analysis and I concur.

I lived in SD for a little over a year and while the economic craziness isn’t at a SF/SJ or LA level, like almost all CA “magnet” regions its attractions are badly overstated for many and its downsides badly under discussed.

And they all live much more on an economic razor’s edge than is commonly admitted.

A regression to the economic mean and blow dry Newsom ain’t going to be saving anybody from his reserved table at the French Laundry upstate.

Living in East Count kind of defeats the purpose of living in San Diego. Some parts average 90’s for a month or two in the summer but that’s still gotta be 20 degrees cooler than Tuscon. And if they were in “real” San Diego, they’d be enjoying 70’s and 80’s. Maybe they thought El Centro was San Diego?

There are 99 reasons to dislike SoCal but weather ain’t one of ’em.

I think most of the folks who live in San Diego commenting here seem to concur that our weather is decidedly better than Tucson. The weather patterns remain relatively unchanged year to year and as such, expressions like June gloom, may gray, etc have formed. This spring was remarkably cool and our weather didn’t even start to warm up until a few days ago . Inland will be hotter than the coast but nothing like the heat of Tucson. Unfortunately, the weather is about all we have left here that makes it worthwhile to be here.

Thanks, everyone, for the corrections regarding the SD vs Tucson climate. For some reason I thought that part of So Cal was undergoing a real heat wave right now; but in any case you all are correct that Tucson would be much worse on a regular basis.

My grandma used to tell how there were dairy cows grazing in Mission Valley. I guess the San Diego river used to actually have water in it?

In 1861/62 the entire Sacramento and San Joaquin valleys flooded. After a 20yr drought, it rained about 40 days straight. An inland sea stretched from well north of Sacramento to south of Fresno west of the Sierra Nevada. Much of Orange Co was under water, and Sacramento looked like Venice with people using boats along the streets to get from place to place. San Diego river flowed bank to bank.

One day, that will happen again.

Turtle-only during ‘100-year’ Chubasco floods (which is always an approximation with a wide statistical variance). Born in SD in ’52 and grew up there. According to my own observation, as well as parents/grandparents/great-grandparents, SD River always a trickle (not surprising as annual rainfall was lucky to average 10″/year with no longterm snowpack in the Lagunas to boost flows offseason, not that explosive SoCal development wouldn’t have taken that sort of water, anyway…).

Left for good in ’77, primarily for longterm water concerns. As Wolfe (Thos., not our good host) said: ‘…you can’t go home again…’. All attractive places eventually seem to get ‘loved to death’ by overpopulation, wherever they are…

may we all find a better day.

Question is, when will South OC/West LA be toast? Or will it ever? The superiority complex about pricing in these areas are out of this world. Although I have to give it to SD as well, friend of mine bought over asking just about 6 months ago…wondering how he feels about his market will just flatten out view looks like now..

San Diego is not immunized from a big decline in values despite many locals’ mistaken belief that “everyone wants to live here.” The RE bubble is not localized in SD, it is a national and international bubble. And it’s an everything bubble.

It hasn’t been that long since we’ve had spectacular crashes in RE and stock markets here and around the world. It can be that bad again, maybe it will be this time. Crushing inflation, soaring mortgage rates, sinking stock market, crypto vaporization, all bad signs. RE values continue to levitate but signs of decline are appearing. Jobs/income are the only positive indicator, admittedly a big one, but if jobs/income get shaky and people get spooked, look out below.

Do you have eyes on the blocks from the beach stuff? I’m wondering (hoping) if the $900/sf condos a block or two from the beach will be disproportionately impacted one way or another.

North County SD seems to be doing ok. It’s not as crazy as it has been but properties are still going pending. Coastal market has the Airbnb/Vrbo backstop. So unless something changes with short term rental laws, I wouldnt expect a significant deterioration.

I agree: We are special and this time is different. Come what may, so cal coastal properties would hold its value.

“anything starting at a little over a million”

Which is basically every middle class home worth living in at this point.

Not even that, if you look even in nicer part of Long Beach or LA. $1M is the minimum entry fees and at that even with 50% off some of these places will still be slight overvalue based on sqft and what you get.

It’s funny to look at SoCal market, as if everyone got lazy and just price their home starting at $1M regardless of condition.

Except the well off are still doing exceptionally well since the everything bubble would need to drop, what, another 30% to go back to where it should be? Maybe the stratosphere knows more about what’s coming than the sorta well off. A $475,000 priced house on my street, which used to be a $225,000 house just a few short years ago went under agreement in 3 days. Panic buying or not getting the message? I don’t know.

Still seeing pending sales regularly in my neck of the woods too, but don’t know why. Maybe the last of loan locks? I’m not in a “hot” market, but prices and sales have been eye-popping for a while. Can’t see it lasting much longer.

And yep (had to check it)… My Zestimate is up yet again. Of course it is. Uh huh.

Yep and also just lingering FOMO in many “hot” real estate markets that got played up and still being played up in social media. The worst IMHO is down in Phoenix and Maricopa generally where I have a lot of friends and family. The region and Arizona in general is running out of water even faster than other drought-stricken regions, the Salt River being depleted and polluted from prior poor management and Lake Mead is drying up, with few other reserves. Incomes way below the more familiar housing bubbles like Seattle or Bay Area, and yet grimy, run-down, poorly-built 1BR homes in Scottsdale, Mesa and Tempe with ugly artificial lawns still sell for $1 to $1.5 million. Outrageous. There, maybe Austin, Ft. Worth, and Miami and Tampa for their own reasons still have FOMO mania, heading for an even worse collapse than 2008.

That should read 2BR, as crazy as Maricopa real estate has gotten the 1BR’s aren’t going for quite that high but it’s not unusual for 2BR or 3BR to break into that range. Though then again, I haven’t been back in a couple months and given the lunatic level of Phoenix’s FOMO and the crazy stunts the flippers and realtors are pulling there, who knows, maybe there are 1BR’s going for that much.

Quick note on Austin…

For some insane reason, too many CA economic refugees eagerly seek to recreate the unnecessarily bad economic choices that caused them to leave a mismanaged CA.

Given thousands of square miles of largely empty land around Austin to move to/build on, the CA expats seem to insist upon huddling in a limited number of existing enclaves, immediately driving those enclaves’ valuations to CA like excess.

Move 10-15 miles N/S/E of Austin downtown and housing costs resemble rationality.

Or, gasp, give San Antonio a shot (90 miles south) or Temple (maybe 90 miles north).

Texas is a big state, use it.

There aren’t beaches with humidity under 7546% and that don’t have mosquitos that can carry off small children, so don’t pay some insane premium for coastal property, either.

It is like a Three Stooges movie, where the knuckleheads have to be told to “spread out, spread out!”

It’s difficult. Were are in the UK and the feeling I get is that price doesn’t really matter – all that matters is the level of your belief that govt can/will ensure house prices don’t fall too much. Beyond that you basically just bid the maximum that the bank will lend you, and that sets the price.

This is dangerous stuff, and I don’t think we have been here to such an extent before. But it is what it is, and if I’m being truly honest, I do believe they will find a way to keep prices up.

For example, yesterday the Bank of England removed affordability tests requirements from mortgages. They said they weren’t needed anymore, but you have to wonder about the precision of their timing.

Ironically, it’s only the most delusional specuvestors – who believe their gains are due to their personal genius – that don’t see the market is rigged by the banks and govt. On the street everyone from my in-laws to grads straight out of university see it as a given that the market is rigged, and the only concern is whether the govt might lose control of the situation and be unable to support prices.

I’m getting tired of hearing that this housing market is not like the ’08 one, so no crash is coming. No recession should be like the last one, since human memories are short and defenses only go up against what burnt us previously. Unfortunately, the backstopping fundamentals that prevented all the recessions post-Depression have all pretty much been wiped out. Which means we could be going back to pre-Depression type recessions where massive speculation, lack of regulation and seemingly minor events trigger downward spirals, which unwind sometimes slowly and end when they naturally need to (without intervention). The crypto crash and unwinding of SPACs and over hyped stocks could just be the tip of the iceberg.

Irving Fisher in 1933, though he had messed up the call on stocks in October ’29, explained how the selloff from a peak of high leverage can become a downdraft that goes far below supposed equilibrium prices, overshooting into a deep trough. We had high leverage which was not merely explicit debt, but was also the printed money spewed atop a debt-riddled system. All this can unwind. And dollars are worth more, in such a downturn but very hard to get. The Fed (it public) will never tolerate another 1933. They will print and pass around funny money and be poor, but not completely technically bankrupt. Maybe the next wave of property buyers will be commodity oligarchs.

If we have a recession, the following is something I think will happen in the future.

Since the GSEs pretty much backstopped all Mortgages since 2009, and this makes them the essentially the biggest landlord in the U.S., they will most likely issue forbearance to low income and possibly middle class people if housing foreclosures get to bad.

Otherwise Wall Street will swoop in and buy even more houses.

Thus I think there will be a floor for houses under $500k.

Nothing to back this up with.

Housing in 2022 is very much different than housing in 2008.

Watch The Big Short, its a good explainer on how things went bad in 2008.

I personally believe that the big difference people dont see is that we are coming off of unnaturally low interest rates and have seen interest rates move up faster than ever before.

The higher interest rates are new, so it will take a period of time before the sellers start to understand that they need to lower prices to sell. The inventory of homes needs to move higher for prices to actually start to drop

But this time, the Fed wont/cant move to lower rates to stem declines. So this is a 4-5 year decline in real estate and a massive reduction in the overall debt bubble, that still needs to implode.

I actually think that the strong position of banks works against homeowners. If the banks dont need to be bailed out, the Fed will sit on the sidelines and allow homeowners to lose all their equity, until finally in 3-4 years from now it starts to hit the bank solvency. But that could see prices at 40% lower.

Once people see real estate declines for more than a year or two the whole psychology of real estate will change.

American central bank macroeconomic control is right up there in the “supremely confident, utterly incompetent” category with Russian military logistics.

These “unassailable” government institutions, made holy by a hireling media, are in fact tin pot gods that fail.

And yet some (hopefully diminishing) number of the G faithful will engage in any level of economic recklessness, completely convinced that the G is some sort of diamond pooping unicorn that “fix anything”.

With that Redfin data remember that folks on the inside can pull up to date data points. Relating this publicly would tank the stock even more so I would expect these reports to run into “issues” over the next year with releases.

Business coming in at my company has tanked double digits over last year in 60ish days. “Everything’s fine” they all say but the numbers tell the truth.

Tough times ahead for the over leveraged.

I have the same conspiracy about realtors local data. Normally they publish after 7-10 days into the month about the previous months data.

Just checked, none of the local data on realtor has been published and it is nearing the end of June. I sure do see an absolute mountain of price cuts in my area. All sectors for low to high end affected.

I think we’d all do well to remember how slow housing is to market factors. We’re still getting occasional articles from the media asking if the stock market is even in a bear market and that the current “dips” are just being able to buy stock “on sale.”

It’s incredibly easy to think emotionally. I’ve fallen prey to it in housing a few times but haven’t put any money in it yet. I don’t see any realistic avenue where housing continues to go up. By Christmas, housing will have to have declined, there is no way it can’t. Fed isn’t going to back down. They’re not going to do enough, but they aren’t going to risk hyperinflation over stonks! they’ve already cashed out of and housing that only stupid people have bought in the past couple years.

I’d like to see the numbers, I wonder what percentage have bought a house and/or did a cash out refi/HELOC in the past 3 years with artificial appraisals. Joe Blow that bought years ago and has seen extrodinary wealth effect but hasn’t done anything can have housing prices bust in half and be okay. Gains aren’t gains until you’ve sold.

> I think we’d all do well to remember how slow housing is to market factors.

This is very true. Nobody likes to take a loss and a deal has to close for comps to get re-priced, so if sales aren’t happening, the comps stay put. I’ve seen 6 houses go on the market in the couple blocks around me in the last 2 weeks, this feels like people running for the exits. But if they don’t have to sell, they might decide to pull the listing. The house across the street from me was listed for a few weeks and then de-listed. Absentee landlord so I don’t know the story but I’d guess he just didn’t get the offer he wanted.

I remember after 08 my neighbor moved out of state and his house sat for 3 months. Eventually his employer said to take whatever offer and they’d make him whole. He cut the price about 50k (more than 10% below what he bought it for 5 years earlier), that wrecked the comps for the neighborhood for a while.

> Joe Blow that bought years ago and has seen extraordinary wealth effect but hasn’t done anything can have housing prices bust in half and be okay. …

Counting my lucky stars I am in that category. But here in CA I think the politicians and their mobs may get predatory and confiscatory. That is my fear. I see a sharper class stratification and conflict forming here between have-homes and have-nots.

Correction;

Have permanent SHELTER and have-not same. I’ve lived all over CA for over 60 years and love it here, and WILL BE HERE until I decide my quality of life is no longer acceptable, or I don’t wake up one morning. I was even a “coastal elite” for 4yrs…any more coastal and I would have been in the damn ocean!

Yeah, that class stratification sure is a bitch. I never owned a home. Built one, though, only took me 16 years and was still unfinished.

Was even better after the first 12, when I moved in full time and started punching my own time clock.

By law or other means class warfare “stratification” WILL be solved. I live in a 500 sq ft apt, generate NO food waste, and am here 7-10 days at a time. I have nothing worth taking except maybe vehicle. (BTW, we have a big loaded 2010? SUV with TX plates here now). As long as I can keep on learning things I’m happy as hell. I pissed most all my youth away having FUN…..no regrets, although when stuck in the 80’s recession I thought very different. I have often wondered what it would be like working in an office, pick up some idea of it here. Guess that’s how one gets more money for more shit.

To old to join that mob now, (would if younger, I was sure WELL trained for it, and wish them luck). I had mostly sheer luck, my whole life, including no “hard earned money” to worry about.

Redfin has been putting out some telling/useful info – the “for sale” inventory numbers explain the madness of 2021, even as they shift the mystery to “why the hell will no one, from Ivan to Invitation Homes, not put some more homes up for sale”.

If memory serves, pandemic period “for sale” inventory fell to like 33% of normal (while demand increased).

Things are getting better in the wake of unZIRP, but still, who are these 72 year old geriatric Baby Boomers who refuse to sell the house in Newark and just move to Boca…

I guess Covid fear still runs very, very high.

Perhaps home showings could be run in decontamination bunny suits.

The FED, boom, bust, boom, recession, boom, bust, boom bust, boom , recession. The have the finesse of a bull in a china shop, death to ALL central banks, for the first 200 years of the USA the average inflation was 2.5%, then came 1913 and Jeckyll Island, and has life improved in the USA?

I guess you didn’t see 1819. Or 1837, 1973, 1893, 1907. No Fed in sight. Crashes and depressions as deep and long as anything we’ve seen since. That’s what books are for. Not to excuse what just happened.

1830s, unregulated banks issued private paper money, rather grossly and corruptly over-issued, followed by property boom, bubble, collapse, multi-year depression. States over-borrowed, overbuilt, not federal government, many states defaulted on their debts (we would call emerging market debts today). Investors were shy for a long time after that.

Agree, to a limited extent.

But the last 20 years are the premier example of how the Fed’s supposed “independent”, “stabilizing” function can be perverted to political ends, used instead to (temporarily) paper over very real, very dangerous trends (America’s lack of international productive competitiveness – leading to perpetual deficits and enduring low employment).

It is a lot easier for DC to hit the “print” button (despite its cancerous implications) than it is to cope with hard realities and difficult solutions.

You average sociopathic used-car-salesman-turned-Congressperson isn’t “inclined” to do “difficult” – not when it is so much easier to lie and there is an entire industry dedicated to disseminating propaganda (MSM).

(The MSM…if you want to know what America’s real problems are…think about what the MSM almost never talks about…).

The distortions in place now dwarf any of those examples you provided, not even close.

If you think those were bad, just wait and see what happens from this bust. The one coming up will be viewed by most as over when it’s just getting started, as it’s going to be one of many while really the same one, just as the dot.com bust and GFC are part of the current mania.

We can also count on the government to try its worst (seen as best by the majority) in a futile effort to prevent the inevitable.

2BFrank, it has, but I would say because of medical advances and medicines I’m general. The Fed doesn’t have much to do w that.

Life expectancy 1913 in US – 50.2

Life expectancy 2021 in US – 76.6

Now here’s where the 90% without stocks swoop in and buy up the luxury homes. Oh boy!

That’s why UK is a nation of RE brokers, nannies, accountants. To who? Those with assets: oligarchs. Flight capital.

You forgot hairdressers and public telephone disinfection officials.

(Hat tip, late Douglas Adams).

Remember stock market crashes don’t effect the Chinese with money. Absolutely none of them own stocks all their wealth is in real estate.

“a much small drop” Should be “smaller”.

5th paragraph.

Thanks!

Gram R. Slave. I see what you did there.

Remember the house always wins

This is unrelated but I’m interested if you think that the Fed raising interest rates could lead to problems in countries (especially developing countries) that have to service external debts in order to import oil. I remember reading an IMF report stating the “Volcker shock” as one of the causes of hyperinflation in South America in the 80s.

I know this goes against literally the number one comment guideline so I’ll try not to do this in the future.

There is a lot of discussion going around about that. Also about food shortages, ‘political instability.

A first shot across the bow, I speculate, though not directly what you pointed out, is a big segment of the French public going in parliamentary elections this week against Macron and balking its perception of discomforts for Ukraine’s/NATO’s sake.

I think the US is pivoting toward a war economy although I don’t know how that will manifest itself. When open markets and free trade are reduced it would most likely impact corporate earning, housing prices, etc.

I’m a year into my home purchase and I am very happy. I locked a 3.125% Rate, which landed me not far from what I would be paying monthly if I were to rent.

However, I was speaking with a friend, and houses we were looking at a year ago are closing 100’s of thousands more than they were a year ago at rates above 5% … not sure what is going to happen.

Given the fact that a person who qualified for a million dollar house a year ago only qualifies for 1/2 a million today, I’m not sure what could be going on either, other than MUCH LOWER PRICES.

People buying down market.

The 30 yr fixed mortgage rate surged to 6%. A SW Florida vacant lot that listed for $15k in 2019 may list for about $50k. Unsold home inventory increased, but they usually list more homes in June after school is out and they want to move. There are some price reductions, but some of those were listed unrealistically high to begin with. Another price reduction home might have water damage and toxic mold. Someone I know bought a home on the Internet. The home inspector did not report low flying planes all day long. The home was close to an airport jet traffic lane.

I’m in the Bay Area and many of the houses are now listed below the Zestimate. I see way more price reductions after even just 1 or 2 weeks. However, a house whose Zestimate was $2M in May 2021 is not shockingly $3.3 just a year later. So even with the reductions, they are still asking for $700k+ more than just 1 year ago. I’m actually ok buying at the 2021 prices and I don’t understand the crazy increases in the last year.

Trickle down economics in reverse.

In the past decade, the Fed lifted asset prices in the hope that some wealth would trickle down and raise CPI inflation. It’s quite a blunt tool that never really worked, so the Fed needed a LOT of it!

Now they are trying the reverse: crush asset prices in the hope that some of the “wealth” destruction trickles down and lowers the CPI inflation.

Like the Fed policies worked wonders to create phantom “wealth” for the rich, the “wealth” destruction at the top now also works quite well! But it’s a very blunt tool so the Fed needs a lot more of it before it works into CPI disinflation. They should keep this going for many years.

CPI inflation is still red-hot, but don’t give up now Fed, you’ll get there in the end! Be as persistent as you were on the way up!

The FED is trying to crush the wealth out of the vast majority of United States citizens, period. That’s been their job since the beginning. It is their true mandate. And here, in the last few years of their long journey, they are racing toward the finish line. The FED is a private corporation that will not reveal it’s true ownership – yet they are in command of the US economy. They are not trying to help people, but destroy them through monetary policy.

Let’s be clearer, or at least as much more clear as possible these days Brian:

Federal Reserve Bank is NOT trying to ”destroy” WE the PEONs,,, but, rather, just trying to put US back in ”our place” as slaves:

Whether or not one wants to call it ”wage slaves”,,, etc., for many such terminologies, it is just about equal to how it has been the last couple thousand years.

How to get out of slavery these days is the ”real” sub headline/topic of not only Wolf’s articles, but the many, likely majority of the comments on WolfStreet.com,,,

I, for one, thank all of you for your contributions, and intend to keep MY contributions to the Wolfster going on as long as I do…

I agree YuShan that the Fed is attempting to “crush inflation” with the reverse wealth effect. I also agree that they need to do it for a prolonged period of time, probably at least a couple few years.

But is that politically feasible? Do we really have a Fed that is committed to the reverse wealth effect and forcing austerity upon the entire nation for 2-3+ years? Or will someone somewhere capitulate and bring back easy money?

The US of today has no clue what real austerity looks like.

Lack of access to artificially cheap credit and not being able to borrow under the lowest aggregate credit standards ever to live above someone’s means does not = austerity.

Besides, now that the inflation genie is out of the bottle, hardly any guarantee that the FRB doing more of what’s failed spectacularly (what most view as “success”) will result in a better outcome.

A continuation of shortages with high and increasing price inflation still = most Americans becoming poorer.

There are lots of ways to know that the US is far from austerity. For me austerity is when people no longer drive up to a food bank in an Escalade and have food handed to them through the window.

1)

2) If SPX is back to 4,800 NYC turnover will not rise to 50 /m

3) Raising mortgage rates to normal level of 5%-6% smacked the ultra RE.

4) King Coal is back in Austria and Germany, a civil war between natgas and coal.

5) Oil producers, speculators who accumulated the rights to extract energy from hundreds of thousands acres and wall street gangs who financed this type of energy RE ==> declared a war coal, their arch enemy. Their slogan was : coal is dirty. Dr. Angela was fooled.

6) In the 1970’s there were oil embargo, ARAMCO was confiscated,

the Suez canal was blocked, Petro dollars, Vietnam, Nixon, King Faisal assassination, Jimmy… The mood was down when Paul Volcker raise the FedRate to 21%, causing two severe recessions.

7) But there was still hope : new oilfields were discovered in Alaska, the Gulf of Mexico, the N.Sea, Siberia. After Iran/ Iraq there was an oil glut.

The dreaded G-Word became reality. Oil was down to 10.35 in Dec 1998 testing Apr 1986 low of 9.75, on the way to 147 in June 2008, when the glut was over..

8) Paul Volcker didn’t win the war against inflation. The glut did it. The dreaded G-Word won.

9) There is no glut in 2022. But King Coal is good to go, cheap,

with available coal plants.

10) We cannot win the war against inflation by raising rates by 0.25% or 0.75%. We must use what we got. Let them fight in the cage,

Where I live in suburban Denver it feels like price discovery is just starting to lead to cuts in asking prices, it’s not clear yet, but I think our neighborhood peak will have been April. There is still not much for sale, but houses are now lasting a couple of weeks if not priced right. Zillow still shows an up trend but I think we have peaked. My neighborhood is upper middle class, priced from 600K to about 1.5 million right now. There are still many people moving here from more expensive locales but not like the last 3 decades.

Sounds like my neighborhood in NE Denver. An old neighbor has his place under contract at an even million which is a bit over double what they paid just before GFC. I mentioned it above but a lot of places hit the market in the last few weeks and I’ve seen a couple pulled off the market. I’m still getting snail mail from OpenDoor, I don’t really want to move but I’m very tempted to see what their offer is. Zillow thinks I could walk away with the purchase price of my house in hand.

Best spin I heard from a realtor on YouTube : “Real estate is not crashing-

it’s just entering a short hibernation” .

Just a little hibernation, folks – a temporary bear thingy.

And bears come out of hibernation a lot leaner than before they went in.

Yeah, the analogy might work!

“Destroy”? No. Most people will find the massive upwards wealth transfer survivable. “Destroy” is a bit of an exaggeration.

Now is not the time to panic. That’s still optional at this point, and you’ll have plenty of opportunity later.

Demand seems to be softening pretty much everywhere except food banks, but those are salvage operations and not investment opportunities.

Whenever we head in to an obvious real estate collapse there is always a crew of deniers in the peanut gallery who crow about how some slice of the market is immune from decline. But when you go back and look at the historical data for any prior big slump it always hits across the board. No magic city is immune, not beach houses, not mansions, not hillbilly shacks. Some got blasted worse than others, but you have to face the music and accept that everyone will lose money on real estate for a while, possibly a very long while.

That’s not true at all. 2008 was the first time real estate values across the entire country declined.

That was the premise behind Wall Street’s can’t lose investment strategy. Prior to that declines were region specific and attuned to business cycles.

Laughably and totally false. I’d suggest you look back at 1926 and the huge real estate crashes around the US starting in Florida.

The only reason anyone would make the comment above yours is under the assumption that history prior to WWII is irrelevant since the government and FRB learned to “manage” the economy at that time.

Not much of a slowdown here in the luxury segment in Northern Michigan, although recently there are many more listings. So we’ll see. Many million dollar+ waterfront homes still sell. A lot of retirees from Arizona and Florida are buying up summer lakefront cottages in Traverse City and Charlevoix, etc., to escape the heat!

Adding a little more.

But Wall Street Lobbyist have a lot of power. So another recession may be something they are looking forward too to buy more housing inventory.

Real Estate, with its tax breaks, have become a pretty good long term investment and a hedge against inflation.

Looking at how Central Bank react to each crisis, which is many time caused by them providing too much liquidity, indicates to me, more inflation (currency devaluation) over the long term.

As the wealth gap widens, I am guessing there will be more programs instituted to provide affordable housing to low income. Affordable housing usually just means free money for down payments, or payment assistance, etc. Which over the long term causes house prices to rise.

Of course this is always regional depending upon jobs and the regional economy.

Anyone see the TV clip of all the long line of low income people lining up in Chicago when they thought there were going to be housing vouchers. Politicians will cater to this group to get votes and try to provide affordable housing but the affordable housing rules will be written by wall street so that wall street will profit from any new program.

IMHO

I wouldn’t discount the pandering to the poor, but Realtors are a pretty powerful lobby, as are developers. It also seems like a high number of recent candidates in local elections near me are either Realtors or RE investors. There are also a LOT of amateur RE investors who started up in the last 10 years and they all think they’re geniuses and really don’t want to give up their “4 hour work week”. A few of these stories about poor small business owners go a long way to influencing public opinion. Democrats are expected to lose massively in the midterms and I expect that’ll put pressure on the Biden admin to do something to damage control. To me, that’s the danger – right now the Fed is finally doing what it needed to do, but if they decide to back off, take cover.

The government isn’t that far away from having to choose what to subsidize. The presumed end of the credit cycle means the government won’t be able to subsidize anything and everything simultaneously. The USD will not be trashed to save home equity and anyone who believes it is fooling themself.

The real estate lobby is influential but hardly at or near the top of my list. Tax policy is one, as it’s of limited value to most homeowners since the 2017 reform. The $250K/$500K is a big potential windfall but doesn’t do anything to improve affordability by reducing the monthly carrying cost.

Per an above post, I expect mortgage forbearance of some sort, but no guarantee it will prevent a housing decline or price crash. If it gets to that, the economy will totally suck meaning a lot of people will lose their job and have to move to find another one. A moratorium will also not apply to corporate owned housing or even if it does, will do nothing to prevent these owners from rushing to the exit to beat everyone else since they have no emotional attachment to it.

Not even that, if you look even in nicer part of Long Beach or LA. $1M is the minimum entry fees and at that even with 50% off some of these places will still be slight overvalue based on sqft and what you get.

It’s funny to look at SoCal market, as if everyone got lazy and just price their home starting at $1M regardless of condition.

$1,000,000 here in SoCal is a very cheap price for any house regardless of its condition, as SoCal is the most perfect and wonderful paradise in the world to live.

You are being sarcastic, right?

Given his name and that he is from SoCal, I give it 50/50 that he is being sarcastic. If he is from South OC, then I give 70 no and 30 yes

So looks like the higher end market is moving much faster just like the stock market. Unfortunately the middle and lower end market is still moving like Titanic with lots of last min FOMO buyers and probably more people taking out ARM loans..etc. I think at this point, for the middle and lower end market to really crash or adjust, it will have to be pretty decent size job losses across the board. The middle to lower end market seems to be flooded by people that are stubborn to the last drop and only way these people won’t buy is if they simply don’t have a job or can’t borrow period. Feel like we are still far off from that..

Speaking of tepid stock market and for that matter Crypto market, just read this headline today….just really funny seeing these chalatans now crying to anyone willing to listen of not playing fair. You have Saynor crying about lack of regulation in Crypto and then you have Woodshed now complaining about the FED…I might be mistaken but where’s her whining when Daddy Powell was force feeding them with cheap money?

“Cathie Wood warns the Fed are ignoring dangerous signals as it plows ahead with draconian rate hikes”

Its because the buyers are all buying down here in South Florida, where their millions go a lot further. They’re making our crazy real estate market even crazier. It’s great for brokers and agents though.

Interesting article in the WSJ pointing out that historically, stock markets don’t turn back up until after the fed stops tightening. So if NYC luxury real estate prices really are tied to the stock markets, there’s a lot more downside left, even with today’s dead cat bounce.

So far Boca and Delray Beach haven’t been hit

Gold continues to drop as people realize it has lost much of prior demand in the jewelry industry which was its largest use historically, and that stuff is now down another $5 per ounce to $1835 and headed much lower.

I doubt if gold drops too far. It’s up against just about every currency except the dollar. Central banks doing too much crazy stuff with fiat for gold to not be held by many as insurance.

In practical terms, pun intended, I believe most first-position mortgages in place prior to the recent rate hikes are fixed rate, fully amortizing, and under 4 or 3 percent. So unlike the subprime meltdown years where so many of the first-position mortgage products were adjustable rate loans, many negatively amortizing, many mortgage holders may choose to ride it out if they can. Many many many. “The Big Short” is an excellent movie for seeing a slice of what it was like then as well as the difference in underwriting standards between then and now. These differences are relevant.

True… many people with 2.xx to 3.xx fixed interest rates are going to sit tight, knowing that they won’t likely get those rates again. They are more likely than 2008 to ride out the storm if they can. And I don’t see the huge collapse in prices such as occurred after 2008, so they won’t be as upside down.

Holdouts won’t keep the real estate market from falling because prices are always set at the margin and people always need to move whether the market is good or bad. It’s one thing to leave a house empty for speculation in a rising one. It’s another in a weak one with the interest rate cycle turning and mortgage rates ultimately destined to “blow out” later.

Differences in mortgage standards since GFC doesn’t = sound underwriting because historically versus actually normal underwriting, standards are still pathetic. 80/20 mortgage written against historically overpriced bubble collateral = garbage quality loan. This aside from actual borrower credit quality who is destined to have their net worth crash in the upcoming bear market with millions losing their jobs too.

Another reason they won’t is because enough of them with hugely inflated fake “wealth” equity will attempt to monetize it by selling first before enough others do later.

The windfalls many have from the current housing bubble dwarf any difference in the monthly payment from the change in mortgage rates to this point.

It’s not like everyone or most are going to agree to hold, a form of market collusion.

If anyone is thinking it’s totally pathetic that this casino of an economy and financial system incentivizes millions to gamble with home ownership, I agree but that’s where we are now.

Investors Bought 33% of US Homes in January, Highest Share in a Decade, according to Business Insider.

Presumably that means corporatists were responsible for 33% of January purchases, and don’t own a third of the homes in the country, at least not yet. Headlines aren’t good for making those kinds of distinctions.

This trends means that even members of the rentier class can become rent slaves. Now if they had stocked up on McMansions before the housing bubble they would have this problem.

It’s become so expensive to buy a home any more that only the top 10% can really afford them. Expect the river to be lined with vans, and those who can’t afford a van down by the river can live out of their tents.

Living under bridges is apparently still prohibited:

“In its majestic equality, the law forbids rich and poor alike to sleep under bridges, beg in the streets and steal loaves of bread.”

– Anatole France, ‘Le Lys Rouge’.

Wouldn’t have this problem. Dang fingers anyway.

Unamused,

Sales to investors have been in the same range for a long time, at around 22% to 27%, with May sales to investors dipping to 25% of total sales – see article bottom section.

Before you get too tangled up in your January number — I have no idea where BI got that and how good it is, and why you even brought it up, given that we’re in June now and are looking at May sales — you need to use a little math:

In January, always, home sales to individual buyers plunge to the low of the year. It’s seasonal. And if investors buy less than normal but the drop-off isn’t as big as the drop-off by individual buyers, then investor’s share rises.

“I have no idea where BI got that and how good it is . . . ”

John Burns Real Estate Consulting.

” . . . and why you even brought it up, given that we’re in June now and are looking at May sales”

It’s a particularly interesting number, insofar as it’s large share of purchases, and can be expected to be followed by additional similarly interesting numbers. I carry the past with me as a guide to the future.

Prior to 2010, the single-family rental market was largely ignored by big institutional investors, which preferred easy-to-scale multifamily properties. But since the GFC, and particularly since 2019, that’s changed. Financial heavyweights like J.P. Morgan Asset Management, Blackstone, and Goldman Sachs Asset Management have helped bankroll an industry of more than two dozen single-family home rental companies that are snapping up existing properties.

It’s a thing. Nearly three-quarters of residential purchases by investors were single-family homes, while multifamily homes—a market in which investors have been significant players for decades—accounted for just a quarter of sales.

The influx of this institutional capital is one element driving the surge in single-family housing prices and rents across the US today.

I think that’s important. But that’s just me.

Today, real estate investment trusts, private equity firms, insurance companies, and pension funds view rentals as a relatively high-yielding hedge against inflation. Therefore the trend is likely to continue, it’s likely to keep housing prices high, and it’s likely to squeeze actual persons out of the housing market.

I happen to think that the increasing corporate zombification of America is a bad thing. I myself don’t live in the Metaverse, or The Matrix, or on The Thirteenth Floor, or the political geographies of 1984.

You’re talking about built-to-rent (John Burns does), and that’s the hottest trend in RE. Whole subdivisions are specialty built by developers to be rented out and then sold as a yield-producing package to pension funds and other funds. It’s ideal, because there will be an on-site leasing and management office. These houses are much easier to take care of because they’re all together in one place. And they’re cheaper to build because they’re not as fancy as regular homes. That’s not the same as buying individual houses here and there, which is a nightmare for big institutional investors, and they’re not doing it.

I’ve covered built-to-rent, including here:

https://wolfstreet.com/2021/06/22/no-blackstone-didnt-buy-17000-houses-out-from-under-desperate-homebuyers-and-blackrock-didnt-buy-a-whole-neighborhood-but-built-to-rent-is-a-h/

Meanwhile in Central Ohio, where according to Redfin investors are buying 1 out of every 5 homes, the luxury houses are in contract with a max life of 14 days on the market. Open Door still advertises during local 6PM news. With much of IT moving here – I guess it really is not a surprise prices are outrageous.

1 out 5 homes = 20%. That’s a smaller share than the NAR says investors are buying (in the above article).

I think expectations play a role too. Why buy now if I can negotiate a better deal later. Plus there is a general sense of caution all over. When some of the big name econ people start say recession people react. Plus the Fed Chairman said recession is a possiblity. Plus we haven’t really had a genuine recession in a long time. I think most of us expect the markets to go down including housing. Seems that housing moves much slower than equities for lots of reasons. Looking back this will all seem normal one day.